UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington D.C. 20549

FORM

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For

the fiscal year ended

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ______ to _____

Commission

File Number

(Exact Name of Registrant as Specified in its Charter)

(State or Other Jurisdiction of Incorporation or Organization) |

(I.R.S. Employer Identification No.) | |

| (Address of Principal Executive Offices) | (Zip Code) |

(Registrant’s Telephone Number, Including Area Code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

| The Stock Market LLC | ||||

| The Stock Market LLC |

Securities registered pursuant to Section 12(g) of the Act:

| Title of each class |

| N/A |

Indicate

by check mark if the registrant is a well-known seasoned issuer as defined in Rule 405 of the Securities Act. Yes ☐

Indicate

by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐

Indicate

by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange

Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2)

has been subject to such filing requirements for the past 90 days.

Indicate

by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule

405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant

was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| ☒ | Smaller reporting company | ||

| Emerging growth company | |||

If

an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying

with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

Indicate

by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness

of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered

public accounting firm that prepared or issued its audit report.

If

securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant

included in the filing reflect the correction of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate

by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No

The

aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which

the common equity was last sold was approximately $

There were shares of the registrant’s common stock, $0.000001 par value per share, outstanding as of April 15, 2024.

TABLE OF CONTENTS

| 2 |

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K and the documents incorporated herein by reference contain forward-looking statements. Such forward-looking statements are based on current expectations, estimates and projections about AERWINS Technologies Inc.’s industry, management beliefs, and assumptions made by management. Words such as “anticipates,” “expects,” “intends,” “plans,” “believes,” “seeks,” “estimates,” variations of such words and similar expressions are intended to identify such forward-looking statements. These statements are not guarantees of future performance and are subject to certain risks, uncertainties and assumptions that are difficult to predict; therefore, actual results and outcomes may differ materially from what is expressed or forecasted in any such forward-looking statements. Although we believe the expectations reflected in our forward-looking statements are based upon reasonable assumptions, it is not possible to foresee or identify all factors that could have a material effect on the future financial performance of the Company. The forward-looking statements in this Annual Report on Form 10-K are made on the basis of management’s assumptions and analyses, as of the time the statements are made, in light of their experience and perception of historical conditions, expected future developments and other factors believed to be appropriate under the circumstances. Except as otherwise required by the federal securities laws, we disclaim any obligation or undertaking to publicly release any updates or revisions to any forward-looking statement contained in this Annual Report on Form 10-K and the information incorporated by reference in this Annual Report on Form 10-K to reflect any change in our expectations with regard thereto or any change in events, conditions or circumstances on which any statement is based.

SUMMARY RISK FACTORS

Our business is subject to numerous risks and uncertainties, including those described in the “Risk Factors” section beginning on page 23 and elsewhere in this Form 10-K. These risks represent challenges to the successful implementation of our strategy and to the growth and future profitability of our business. Below is a summary of material risks, uncertainties and other factors that could have a material effect on the Company and its operations:

Risks Related to the Lind Global Financing

| ● | It is not possible to predict the actual number of shares of common stock, if any, we will issue upon conversion of the Convertible Notes or sell upon exercise of the Warrants by Lind Global, or the actual gross proceeds resulting from exercise of those warrants; |

| ● | Investors who buy shares of common stock from Lind Global at different times will likely pay different prices; and |

| ● | We may use proceeds from issuance of the Convertible Notes sales of shares of our common stock upon exercise of the Warrants in ways with which you may not agree or in ways which may not yield a significant return. |

Risks Related to our Business

| ● | We have incurred, and in the future may continue to incur, net losses; |

| ● | We are a holding company and will depend upon our subsidiary Aerwin Development CA LLC for our cash flows; |

| ● | We will need additional capital, and we cannot be sure that additional financing will be available; |

| ● | Our business performance may be adversely affected if the growth of the Air Mobility Vehicle industry slows down; |

| ● | Our future growth depends on the demand for, and customers’ willingness to adopt, our planned Manned Air Vehicle; |

| ● | We may be unable to make product deliveries as we have not completed the design of our planned MAV and due to limited production capacity; |

| ● | We may not be able to engage customers successfully and to obtain meaningful orders in the future. |

| ● | We may become subject to product liability claims or warranty claims, which could harm our financial condition and liquidity if we are not able to successfully defend or insure against such claims; |

| ● | If we fail to successfully develop and commercialize new products, services and technologies that are well received by customers, our operating results may be materially and adversely affected; |

| ● | The execution of our business plans requires a significant amount of capital. In addition, our future capital needs will require us to sell additional equity or debt securities that may dilute the equity interests of our shareholders or introduce covenants that may restrict our operations or our ability to pay dividends; |

| ● | The failure to attract and retain additional qualified personnel could prevent us from executing our business strategy; |

| ● | We and our subsidiaries may need to defend ourselves against claims of intellectual property infringement, which may be time-consuming and costly; |

| ● | Our or our subsidiaries’ intellectual property rights may not protect us effectively; |

| ● | Failure to comply with laws and regulations could harm our business; |

| ● | We are exposed to fluctuations in currency exchange rates; |

| ● | Nasdaq may delist the Company’s securities from trading on its exchange, which could limit investors’ ability to make transactions in our securities and subject the Company to additional trading restrictions; |

| ● | The market price of our common stock may be volatile, and you could lose all or part of your investment; and |

| ● | As an “emerging growth company” under the JOBS Act, we are permitted to rely on exemptions from certain disclosure requirements. |

| 3 |

PART I

ITEM 1. BUSINESS

AERWINS Technologies Inc., a Delaware corporation (the “Company,” “we,” “us,” or “AERWINS”) together with its wholly owned subsidiary Aerwin Development CA LLC, a California limited liability company (“Aerwin Development”), is redesigning its single-seat optionally Manned Air Vehicle (“MAV” or “Manned Air Vehicle”). All refences in this Form 10-K to the “Company,” “we,” “us,” or “AERWINS” include both AERWINS and Aerwin Development.

We were originally incorporated in Delaware on February 12, 2021 under the name “Pono Capital Corp” as a special purpose acquisition company, formed for the purpose of effecting a merger, capital stock exchange, asset acquisition, stock purchase, reorganization or similar business combination with one or more businesses. On August 13, 2021, we consummated an initial public offering. On February 3, 2023, we consummated a merger (the “Merger”) with Pono Merger Sub, Inc., a Delaware corporation (“Merger Sub”) and a wholly-owned subsidiary of the Company, then called Pono Capital Corp., a Delaware corporation (“Pono”) with and into AERWINS, Inc. (formerly named AERWINS Technologies Inc.), a Delaware corporation pursuant to an agreement and plan of merger, dated as of September 7, 2022 (as amended on January 19, 2023, the “Merger Agreement”), by and among Pono, Merger Sub, AERWINS, Mehana Equity LLC, a Delaware limited liability company (“Sponsor” or “Purchaser Representative”) in its capacity as the representative of the stockholders of Pono, and Shuhei Komatsu in his capacity as the representative of the stockholders of AERWINS, Inc. (“Seller Representative”). The Merger and other transactions contemplated thereby (collectively, the “Business Combination”) closed on February 3, 2023 when pursuant to the Merger Agreement, Merger Sub merged with and into AERWINS, Inc. with AERWINS, Inc. surviving the Merger as a wholly-owned subsidiary of Pono, and Pono changed its name to “AERWINS Technologies Inc.” and the business of the Company became the business of AERWINS, Inc., and this business section primarily includes information regarding the AERWINS’, Inc. business. We formed Aerwin Development on October 18, 2023.

On April 2, 2024, the Company consolidated its issued and outstanding share on the basis of one post-consolidation share for each 100 pre-consolidation common shares. All share figures and reference have been retrospectively adjusted.

For additional information on the corporate history of our Company please see the section titled “Corporate History” on page 20 of this Form 10-K.

Mission

With the mission of “Transforming society from the sky down,” we aim to realize an “Air Mobility Society” in which cars, specialized crafts, and drones can fly freely. To this end, are redesigning our single-seat optionally Manned Air Vehicle. We aim to align this vehicle with the stringent requirements of the Federal Aviation Administration’s (“FAA”) Powered Ultra-Light Air Vehicle Category, setting a new standard for safe low-altitude manned flight.

To achieve this goal, we have established AERWIN Development Company LLC, a California subsidiary with offices in Los Angeles, California, and entered into the Letter of Intent with Helicopter Technology discussed below. Helicopter Technology is a designer, developer, and manufacturer of over 20 FAA-approved helicopters and turbine systems with over 20,000 square feet of facilities located five miles from the Company’s Los Angeles office. Its primary focus is helicopter rotor blades with capabilities that include tool design and fabrication, structural design and assembly, and fatigue testing. They are an FAA-approved repair station, certified ISO 9001:2015 + AS9100D, ISO 9001:2015 + AS9110C, hold various EU approvals, and have U.S. Department of Defense (“DOD”) clearance.

The specifications for our MAV has a target price of $200,000 and is designed to be used for sightseeing, sports, agriculture, surveillance, field delivery and numerous military applications. Training time for flying the MAV is expected to last three to five days, with a payload of up to 250 pounds to carry a single-seat occupant, cargo, or weaponry. The MAV is expected to be designed to be manually or entirely remotely controlled with an innovative and proprietary three-rotor configuration to reduce sound and increase stability at a cruise speed of up to 40 miles per hour at a height ranging from 20 to 50 feet.

The timeline for the planned development and launch of our redesigned MAV is as follows:

| ● | End of 2024 – Schematic design and detailed specifications; |

| 4 |

| ● | End of 2025 – Prototype parts design, fabrication, and systems finalization; | |

| ● | End of 2026 – Commencement of assembly, test planning, then testing, and DOD review; and | |

| ● | End of 2027 – Begin sales of the MAV. |

Our Chief Executive Officer, Kiran Sidhu, will lead the MAV development initiative. He plans to lead a dedicated U.S.-based team working with and within Helicopter Technology to design, build, and commercialize the MAV within the Federal Aviation Regulation Part 103 requirements for ultralight aircraft.

Data from the U.S. Bureau of Labor Statistics and Indeed.com reveal that the Los Angeles metropolitan area is home to the highest number of aerospace engineers in the U.S., with over 4,000 aerospace engineers. The region potentially employs over 50,000 professionals in the aerospace and defense sector. Prominent aerospace entities like Jet Propulsion Laboratory in Pasadena, SpaceX in Hawthorne, and NASA Armstrong Flight Research Center in Palmdale are nearby, and major aerospace corporations, including Boeing, Lockheed Martin, and Raytheon, have a local presence.

Manned Air Vehicle Development Letter of Intent

Effective as of December 19, 2023 (the “Effective Date”), we entered into a letter of intent (the “Letter of Intent”) with Helicopter Technology Company (“Helicopter Technology”) regarding the design, development, manufacturing, sales, and marketing (collectively, the “Project”) of the MAV (the “MAV”). Under the Letter of Intent, we and Helicopter Technology will form an entity (the “Operating Company”) that will be owned 70% by us and 30% by Helicopter Technology. The Operating Company agreed to enter into an agreement with Helicopter Technology to design, build, assemble, and test the MAV planned to meet the FAA Powered Ultra-Light Category (the “Development Services Agreement”). In addition, according to the Development Services Agreement, Helicopter Technology will determine and obtain all required regulatory approvals for the MAV, providing all the necessary labor, materials, and customized equipment. The Letter of Intent contemplates that we and Helicopter Technology will enter into a manufacturing supply agreement on terms to be mutually agreed on. In addition, the parties will work together to secure the funding required to start production of the MAV. Helicopter Technology already has a working capital arrangement with its bank. The Operating Company will pay Helicopter Technology its costs plus 15% of such amount to provide the services it provides pursuant to the Development Services Agreement in addition to equity compensation in our company no less favorable than comparable compensation to our executive management.

The Operating Company will enter into a marketing and support agreement with us whereby we plan to provide certain engineering oversight, accounting, marketing, sales, advertising, development of a dealer distribution network, online marketplace, and other distribution channels, and financial management, budgeting, accounting, legal, and other administrative services as may be required by the Operating Company. The Operating Company will pay us our costs plus 15% of such amount to provide these services. Payments will be subject to the available cash flow of the Operating Company. In addition, we have agreed to provide working capital to the Operating Company of up to a maximum of $1,700,000 for its operations over the first 12 months.

Pursuant to the Letter of Intent, the parties intend to use their best efforts to negotiate and enter into an operating agreement for the Operating Company (the “Operating Agreement”) within 45 days of executing the Letter of Intent. The Letter of Intent also contains additional customary conditions for entering into the Operating Agreement. The Company and Helicopter Technology are in ongoing discussions in an effort to finalize each of the agreements contemplated by the Letter of Intent.

Discontinued Operations

On December 27, 2023, we discontinued the operations of A.L.I. Technologies Inc., a Japanese corporation (“A.L.I.”) which is our wholly-owned indirect subsidiary, as part of our operations, moved to Los Angeles, California, and continued the development of a line of FAA-compliant manned and unmanned crafts for low-altitude flight. Among the reasons for discontinuing the business of A.L.I., was the desire to develop an MAV that would comply with the Federal Aviation Regulation Part 103 requirements for ultralight aircraft and the difficulties that we believed the XTURISMO limited edition hoverbike being developed by A.L.I. would encounter. Following the discontinuation, on December 27, 2023, A.L.I. filed a voluntary bankruptcy petition with the Tokyo District Court, Civil Division 20, “Tokutei Kanzai Kakari” [Special Trusteeship Section], Case ID: No. 8234 of 2023 (Fu). A bankruptcy trustee was appointed on January 10, 2024, and proceedings have commenced. See “Item 3 – Legal Proceedings” and the discussion regarding the A.L.I. Bankruptcy.

| 5 |

ALI’s discontinued operations include the manned air mobility business, including the further development of the XTURISMO limited edition hoverbike, the air mobility platform COSMOS (Centralized Operating System for Managing Open Sky), the computing power-sharing business, drone photography business and drone and artificial intelligence research and development business.

Significant Market Opportunities

In today’s increasingly populated and interconnected world, traditional modes of urban transportation continue to contribute to congestion and pollution, and they are primarily confined to land-based infrastructure. Mobility for the future requires a revolutionary solution.

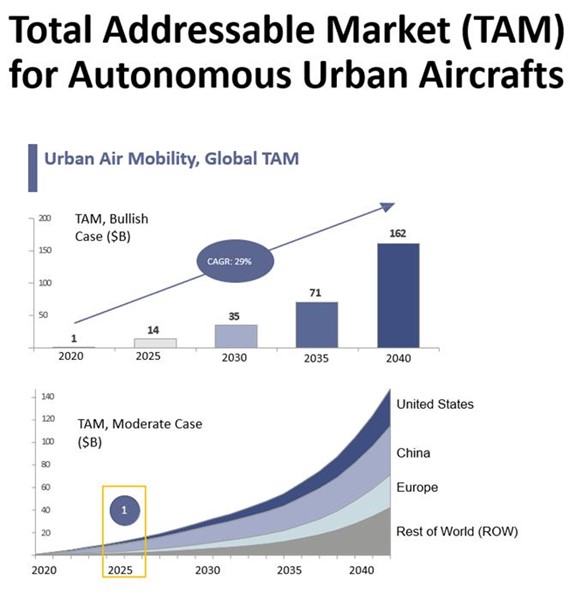

The Total Addressable Market (TAM) for Autonomous Urban aircraft is expected to increase at a cumulative annual growth rate of 29% from 2020 to 2040, reaching $162 billion. 2

2 See UBS report/Japan Ministry of Economy, Trade and Industry.

| 6 |

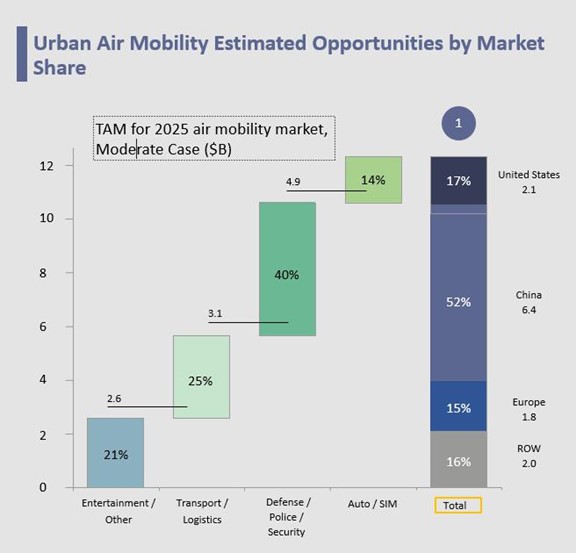

Estimated urban air mobility opportunities by market share are as follows:

See: Urban Air Mobility eVTOL/Urban Air Mobility TAM Update: A Slow Take-Off, But Sky’s the Limit, Morgan Stanley May 6, 2021 .

| 3) | Manned Air Mobility |

The manned air mobility industry has been the focus of much attention, with demonstration tests being conducted in many countries and a roadmap published in Japan under the leadership of the Ministry of Economy, Trade, and Industry.

According to data published by Morgan Stanley Research in 2019, the global market for manned air mobility, including hoverbikes, is expected to grow to over 150 trillion yen (approximately $1,036 billion USD) by 2040 according to long-term global forecasts. Data published by PWC in 2020 indicates that the air mobility market in Japan will grow to approximately 2.5 trillion yen (approximately $17 billion USD) by 2040. According to “Flying Cars Global Market Report 2021” published by The Business Research Company in 2021, the global market is expected to grow at a CAGR of 58.7% to 35 billion yen (approximately $241 million USD) by 2025. The report says that the key to growth will be the development of infrastructure system requirements, aircraft development, and institutional response, particularly in passenger transportation.

| 7 |

The manned air mobility field in the air mobility industry, to which we belong, is expected to contribute to solving various social issues such as eliminating traffic congestion and improving productivity in cities, reducing land infrastructure costs for the approximately 20,000 marginalized villages in rural areas (remote islands and mountainous regions) in Japan, transporting people between inhabited islands, replacing helicopters, and diversifying entertainment and sightseeing, as advanced mobility that can go “wherever they want” and “whenever they want.”

Marketing, Sales and Distribution

We plan to develop a marketing, sales and advertising programs following completion of the schematic design and detailed specification phase of our redesigned MAV during 2025 and 2026 as well as begin seeking indications of interest by prospective dealers as part of a dealer distribution network and other distribution channels including online sales.

Competition

We recognize that there are no new alternatives at this time, as hoverbikes and drones themselves are substitutes for existing solutions at this time. Most of the industry’s production experience in the manned air mobility business is still in the demonstration stage, although eHang in China has produced and delivered products. Many companies are still in the research and development stage and are not disclosing their sales prices. The low-altitude manned flight market is, however, evolving and is expected to be highly competitive with a variety of aircraft manufactured in the United States and abroad. With the introduction of new technologies and the potential entry of new competitors into the market that may offer alternatives to our planned MAV, we expect competition to increase in the future, which could harm our business, results of operations, or financial condition once we complete development and commence production and sales. We expect to face significant competition from other manufacturers of low-altitude manned flight vehicles, which may have an adverse effect on expected revenues.

We believe our ability to compete successfully with other manufactures will also depend on a number of factors including purchase price, safety, after-sales support and product warranties, and on factors such as brand, established customer relationships and financial and manufacturing resources. Many of the incumbents have, and future entrants may have, greater resources than we have and may also be able to devote greater resources to the development of their current and future vehicles. They may also have greater access to larger potential customer bases and have and may continue to establish cooperative or strategic relationships amongst themselves or with third parties (including OEMs) that may further enhance their resources and offerings.

Intellectual Property

In connection with our redesign of the MAV, we are evaluating the utility of the proprietary systems, technologies and other intellectual property developed or owned by A.L.I. given that we elected to discontinue all of its operations, shift development, production and potentially initial sales efforts to the United States. Our success depends in part on our ability to protect our technology and intellectual property we may develop or license as part of our efforts to develop the MAV. We expect to rely on a combination of patents, patent applications, trade secrets, know-how, copyrights, trademarks, intellectual property licenses and other contractual rights to establish and protect proprietary rights in technology we utilize in connection with the development and ultimate sale of the MAV. In addition, we plan to enter into confidentiality and non-disclosure agreements with our employees and business partners. The agreements we plan to enter into with our employees will provide that all software, inventions, developments, works of authorship and trade secrets created by them during the course of their employment are our property or that of the Operating Company.

COVID-19

On March 11, 2020, the World Health Organization declared the COVID-19 outbreak a pandemic. The pandemic has resulted in the implementation of significant governmental measures, including lockdowns, closures, quarantines, and travel bans, intended to control the spread of the virus. Companies are also taking precautions, such as requiring employees to work remotely, imposing travel restrictions, and temporarily closing businesses. While the duration and extent of the COVID-19 pandemic depends on future developments that cannot be accurately predicted at this time, such as the extent and effectiveness of containment actions, it has already had an adverse effect on the global economy and the lasting effects of the pandemic continue to be unknown. As of the date of this Form 10-K, the extent of the future impact of COVID-19 is still highly uncertain and cannot be predicted.

| 8 |

Recent Developments

Closing of Business Combination

We were originally incorporated in Delaware on February 12, 2021 under the name “Pono Capital Corp” as a special purpose acquisition company, formed for the purpose of effecting a merger, capital stock exchange, asset acquisition, stock purchase, reorganization or similar business combination with one or more businesses. On August 13, 2021, we consummated an initial public offering. On February 3, 2023, we consummated a merger (the “Merger”) with Pono Merger Sub, Inc., a Delaware corporation (“Merger Sub”) and a wholly-owned subsidiary of the Company, then called Pono Capital Corp., a Delaware corporation (“Pono”) with and into AERWINS, Inc. (formerly named AERWINS Technologies Inc.), a Delaware corporation pursuant to an agreement and plan of merger, dated as of September 7, 2022 (as amended on January 19, 2023, the “Merger Agreement”), by and among Pono, Merger Sub, AERWINS, Mehana Equity LLC, a Delaware limited liability company (“Sponsor” or “Purchaser Representative”) in its capacity as the representative of the stockholders of Pono, and Shuhei Komatsu in his capacity as the representative of the stockholders of AERWINS, Inc. (“Seller Representative”). The Merger and other transactions contemplated thereby (collectively, the “Business Combination”) closed on February 3, 2023 when pursuant to the Merger Agreement, Merger Sub merged with and into AERWINS, Inc. with AERWINS, Inc. surviving the Merger as a wholly-owned subsidiary of Pono, and Pono changed its name to “AERWINS Technologies Inc.” and the business of the Company became the business of AERWINS, Inc. (the “Company,” “we,” “us, “our” “AERWINS,” or “AERWINS Technologies”).

Pursuant to the terms of the Merger Agreement, the total consideration for the Business Combination and related transactions (the “Merger Consideration”) was approximately $600 million. In connection with the Special Meeting, holders of 11,328,988 pre-consolidated shares of Pono common stock sold in its initial public offering exercised their right to redeem those shares for cash prior to the redemption deadline of January 25, 2023, at a price of $10.50 per share, for an aggregate payment from Pono’s trust account of approximately $118.9 million. Effective February 3, 2023, Pono’s units ceased trading, and effective February 6, 2023, AERWINS Technologies’ common stock began trading on the Nasdaq Global Market under the symbol “AWIN” and the warrants began trading on the Nasdaq Capital Market under the symbol “AWINW.”

After taking into account the aggregate payment in respect of the redemption, Pono’s trust account had a balance immediately prior to the Closing of $1,795,997. Such balance in the trust account was used to pay transaction expenses and other liabilities of Pono, pay certain transaction expenses of AERWINS, Inc., with the remaining being deposited in AERWINS, Inc. cash account. In connection with the Business Combination, a warrant holder of AERWINS, Inc. received a warrant to purchase 4,693 shares of AERWINS Technologies’ common stock as Merger Consideration as set forth in the Merger Agreement. The Merger Consideration was subject to a post-Closing true up 90 days after the Closing. The post-Closing true up period expired on May 5, 2023 without any claims having been made.

As a result of the Merger and the Business Combination, holders of Pono common stock automatically received common stock of AERWINS Technologies, and holders of Pono warrants automatically received warrants of AERWINS Technologies with substantively identical terms. At the Closing of the Business Combination, all shares of Pono owned by the Sponsor (consisting of shares of Class A common stock and shares of Class B common stock), which we refer to as the founder shares, automatically converted into an equal number of shares of AERWINS Technologies’ common stock, and Private Placement Warrants held by the Sponsor, automatically converted into warrants to purchase one share of AERWINS Technologies common stock with substantively identical terms. As of the Closing: public stockholders owned approximately 0.3% of the outstanding shares of AERWINS Technologies common stock; the Sponsor and its affiliates owned approximately 6.7% of the outstanding shares of AERWINS Technologies common stock and AERWINS, Inc.’s former security holders collectively owned approximately 93.0% of the outstanding shares of AERWINS Technologies common stock.

| 9 |

At the closing of the Merger, we issued to the former shareholders of AERWINS, an aggregate of 519,291 shares of common stock, of which 14,079 shares are being held in escrow (the “Escrow Shares”). The Escrow Shares were subject to a post-Closing true up 90 days after the Closing based on confirmed amounts of the Closing Net Indebtedness of AERWINS, the Net Working Capital of AERWINS, and certain Transaction Expenses, each of which are defined in the Merger Agreement. If the adjustment is a negative adjustment in favor of us, the escrow agent shall distribute to us a number of shares of our common stock with a value equal to the adjustment amount. If the adjustment is a positive adjustment in favor of AERWINS, we will issue to the former AERWINS stockholders an additional number of shares of our common stock with a value equal to the adjustment amount. The post-Closing true up period expired on May 5, 2023 without any claims having been made. In addition, at the closing of the Merger, the Company issued an aggregate of 1,500 shares of common stock (the “Compensation Shares”) to Boustead Securities, LLC (“Boustead”), in partial satisfaction of fees due to them in connection with the Merger. In addition, Boustead is entitled to an increase in the number of Compensation Shares on the 180th day following the closing of the Merger (the “Measurement Date”) if the VWAP for the common stock during over the five trading days prior to the Measurement Date is less than $1,000 per share (the “Adjustment”). The number of shares of common stock subject to the Adjustment is equal to (1) $1,500,000 divided by the average VWAP of the common stock over the five trading days prior to the Measurement Date, minus (2) the number of Compensation Shares.

Lock-up Agreements

In connection with the Business Combination, certain stockholders of AERWINS, Inc. and certain of AERWINS’, Inc. officers and directors (such stockholders, the “Company Holders”) entered into a lock-up agreement (the “Lock-up Agreement”) pursuant to which they are contractually restricted, during the Lock-up Period (as defined below), from selling or transferring any of (i) their shares of AERWINS common stock held immediately following the closing and (ii) any of their shares of AERWINS common stock that result from converting securities held immediately following the closing (the “Lock-up Shares”). The “Lock-up Period” means the period commencing at closing and end the earliest of: (a) six months from the closing (or, in the case of Shuhei Komatsu, AERWINS’ Chief Executive Officer, thirty months from the closing), (b) the date the Company consummates a liquidation, merger, share exchange or other similar transaction with an unaffiliated third party that results in all of the Company’s stockholders having the right to exchange their shares of common stock for cash, securities or other property and (c) the date on which the closing sale price of the Company’s common stock equals or exceeds $1,200 per share (as adjusted for stock splits, stock dividends, reorganizations and recapitalizations and the like) for any twenty (20) trading days within any thirty (30) trading day period commencing at least one hundred and fifty (150) days after the closing; provided that 1/3 of such restricted shares shall be released from such restrictions if the closing stock price of the Company’s common stock reaches each of $1,300, $1,500, and $1,700.

The Sponsor is subject to a lock-up pursuant to a letter agreement (the “Sponsor Lock-up Agreement”), entered into at the time of the IPO (as defined below), among Pono, the Sponsor and the other parties thereto, pursuant to which the Sponsor is subject to a lock-up beginning on the Closing and end the earliest of: (a) six months from the Closing, (b) the date the Company consummates a liquidation, merger, share exchange or other similar transaction with an unaffiliated third party that results in all of the Company’s stockholders having the right to exchange their shares of the Company’s common stock for cash, securities or other property and (c) the date on which the closing sale price of the Company’s common stock equals or exceeds $1,200 per share (as adjusted for stock splits, stock dividends, reorganizations and recapitalizations and the like) for any twenty (20) trading days within any thirty (30) trading day period commencing at least one hundred and fifty (150) days after the Closing; provided that 1/3 of such restricted shares shall be released from such restrictions if the closing stock price of the Company’s common stock reaches each of $1,300, $1,500, and $1,700. “IPO” means Pono’s public offering of 10,000,000 pre-consolidation units (the “Units”) at pre-consolidated of $10.00 per Unit, generating gross proceeds of $100,000,000, which was consummated on August 13, 2021.

Indemnification Agreements

On February 7, 2023, AERWINS Technologies entered into indemnification agreements, with each of AERWINS Technologies’ directors containing provisions which are in some respects broader than the specific indemnification provisions contained in the Delaware General Corporation Law. The indemnification agreements will require AERWINS Technologies, among other things, to indemnify its directors against certain liabilities that may arise by reason of their status or service as directors and to advance their expenses incurred as a result of any proceeding against them as to which they could be indemnified.

| 10 |

Non-Competition and Non-Solicitation Agreements

Following execution of the Merger Agreement, certain significant stockholders of AERWINS, Inc. entered into non-competition and non-solicitation agreements (the “Non-Competition and Non-Solicitation Agreements”), pursuant to which they agreed not to compete with Pono, AERWINS, Inc. and their respective subsidiaries during the two-year period following the Closing and, during such two-year restricted period, not to solicit employees or customers or clients of such entities. The Non-Competition and Non-Solicitation Agreements also contain customary non-disparagement and confidentiality provisions.

Registration Rights Agreements

At the closing of the Business Combination, certain significant stockholders of AERWINS, Inc. entered into a registration rights agreement with Pono providing for the right to three demand registrations, piggy-back registrations and shelf registrations with respect to the Merger Consideration shares.

Purchaser Support Agreement

Simultaneously with the execution of the Merger Agreement, Lind Global Representative entered into a support agreement (the “Purchaser Support Agreement”) in favor of Pono and AERWINS, Inc. and their present and future successors and subsidiaries. In the Purchaser Support Agreement, the Purchaser Representative agreed to vote all equity interests in Pono in favor of the Merger Agreement and related transactions and to take certain other actions in support of the Merger Agreement and related transactions. The Purchaser Support Agreement also prevents the Purchaser Representative from transferring its voting rights with respect to equity interests in Pono or otherwise transferring equity interests in Pono prior to the meeting of Pono’s stockholders to approve the Merger Agreement and related transactions, except for certain permitted transfers.

Voting Agreement

Simultaneously with the execution of the Merger Agreement, certain stockholders of AERWINS, Inc. entered into a voting agreement (the “Voting Agreement”) in favor of Pono and AERWINS, Inc. and their present and future successors and subsidiaries. In the Voting Agreement for certain stockholders of AERWINS, they each agreed to vote all of their AERWINS, Inc. stock interests in favor of the Merger Agreement and related transactions and to take certain other actions in support of the Merger Agreement and related transactions. The Voting Agreement also prevents them from transferring their voting rights with respect to their AERWINS, Inc. stock or otherwise transferring their AERWINS stock prior to the AERWINS, Inc. approval of the Merger Agreement and related transactions, except for certain permitted transfers.

Executive Employment Agreements

On February 3, 2023, the Company entered into employment agreements (the “Employment Agreements”) with executive officers: Shuhei Komatsu (former Chief Executive Officer), Taiji Ito (Global Markets Executive Officer), Kazuo Miura (former Chief Product Officer) and Kensuke Okabe (former Chief Financial Officer). The Employment Agreements all provide for at-will employment that may be terminated by the Company for death or disability and with or without cause, by the executive with or without good reason, or mutually terminated by the parties. The Employment Agreements for Mr. Komatsu, Mr. Ito, Mr. Miura, and Mr. Okabe provide for a severance payment equal to the remaining base salary for the remaining period of the respective term of employment (each term is one (1) year) upon termination by the Company without cause or termination by such executive for good reason. The executive agreements provide for a base salary of $200,000, $200,000, $200,000 and $200,000 for Mr. Komatsu, Mr. Ito, Mr. Miura and Mr. Okabe, respectively, as well as possible annual performance bonuses and equity grants under the equity incentive plan if and when determined by the Company’s Compensation Committee. No performance bonuses were paid under these agreements.

| 11 |

Option Award Agreements

On February 3, 2023, the Company entered into Option Award Agreements (the “Option Award Agreements”) with former executive officers: Shuhei Komatsu (former Chief Executive Officer), Taiji Ito (former Global Markets Executive Officer and Chief Executive Officer), Kazuo Miura (former Chief Product Officer) and Kensuke Okabe (former Chief Financial Officer).

The Option Award Agreements grants to each of the following persons options to acquire shares of the Company’s common stock, to vest as set forth in the Option Award Agreements, as follows:

| ● | Shuhei Komatsu–- 15,256 options at an exercise price of $0.015 per share of common stock. These options were forfeited upon Mr. Komatsu’s resignation. |

| ● | Taiji Ito–- 7,039 options at an exercise price of $0.015 per share of common stock |

| ● | Kazuo Miura–- 7,399 options at an exercise price of $0.015 per share of common stock. These options were forfeited upon Mr. Komatsu’s resignation. |

| ● | Kensuke Okabe–- 4,693 options at an exercise price of $0.015 per share of common stock |

Stock Purchase Agreement

On February 2, 2023, the Company entered into a Subscription Agreement (the “Agreement”) with AERWINS, Inc., and certain investors (collectively referred to herein as the “Purchasers”). Pursuant to the Agreement, the Purchasers agreed to purchase an aggregate 31,963 shares of common stock (the “Shares”) of AERWINS, Inc. which was immediately exchanged for 50,000 shares of common stock of the Company (the “Company Shares”) upon the consummation of the Business Combination in exchange for an aggregate sum of $5,000,000 (the “Purchase Price”) with the Purchase Price being paid to AERWINS, Inc. prior to the closing of the Business Combination (the “Closing”). Effective immediately prior to the Closing, AERWINS, Inc. issued the Shares to the Purchasers and thereafter immediately upon the Closing, the Shares were exchanged for the Company Shares, and the Company Shares were issued as a registered issuance of securities under the Securities Act of 1933, as amended (the “Securities Act”), pursuant to an effective registration filed by the Company on Form S-4 (Registration No. 333-268625) which was declared effective by the Securities and Exchange Commission on January 13, 2023.

Standby Equity Purchase Agreement

On January 23, 2023 (the “Effective Date”), Pono entered into a Standby Equity Purchase Agreement (the “SEPA”) with YA II PN, Ltd., (“YA”). The Company and its successors will be able to sell up to one hundred million dollars in aggregate gross purchase price of the Company’s shares of common stock, par value $0.000001 per share (the “Common Shares”) at the Company’s request any time during the 36 months following the date of the SEPA’s entrance into force. The shares would be purchased at 96% or 97% (depending on the type of notice) of the Market Price (as defined below) and would be subject to certain limitations, including that YA could not purchase any shares that would result in it owning more than 4.99% of the Company’s common stock. “Market Price” shall mean the lowest daily VWAP of the Common Shares during the three consecutive trading days commencing on the advance notice date, other than the daily VWAP on any excluded days. “VWAP” means, for any trading day, the daily volume weighted average price of the Common Shares for such trading day on the principal market during regular trading hours as reported by Bloomberg L.P.

Pursuant to the SEPA, the Company is required to register all shares which YA may acquire. The Company agreed to file with the Securities and Exchange Commission (the “SEC”) a Registration Statement (as defined in the SEPA) registering all of the shares of common stock that are to be offered and sold to YA pursuant to the SEPA. The Company is required to have a Registration Statement declared effective by the SEC before it can raise any funds using the SEPA. The Company may not issue more than 19.99% of its shares issued and outstanding as of the Effective Date without first receiving shareholder approval for such issuances, unless such additional shares may be issued consistent with the rules and regulations of the Nasdaq Stock Market. Pursuant to the SEPA, the use of proceeds from the sale of the shares by the Company to YA shall be used by the Company in the manner as will be set forth in the Form 10-K included in the Registration Statement (and any post-effective amendment thereto) and any Form 10-K supplement thereto filed pursuant to the SEPA. There are no other restrictions on future financing transactions. The SEPA does not contain any right of first refusal, participation rights, penalties or liquidated damages. The Company has paid YA Global II SPV, LLC, a subsidiary of YA, a structuring fee in the amount of $15,000, and, on the Effective Date, the Company agreed to issue to YA shares with aggregate value equal to one million dollars, as a commitment fee.

| 12 |

YA has agreed that neither it nor any of its affiliates shall engage in any short-selling or hedging of our common stock during any time prior to the public disclosure of the SEPA. Unless earlier terminated as provided under the SEPA, the SEPA shall terminate automatically on the earliest of (i) the first day of the month next following the 36-month anniversary of the Effective Date or (ii) the date on which YA shall have made payment of Advances (as defined in the SEPA) pursuant to the SEPA for the Common Shares equal to the Commitment Amount (as defined in the SEPA).

Loan Agreement

On February 27, 2023, the wholly owned subsidiary of the Company’s wholly owned subsidiary, A.L.I. Technologies Inc., a Japanese corporation (“A.L.I.”) entered into a Loan Agreement with Shuhei Komatsu, the Company’s former Chief Executive Officer (the “Agreement”). The Agreement was approved by the Company’s Board of Directors on February 26, 2023 and by the Company’s Compensation Committee on February 26, 2023. Pursuant to the Agreement, Mr. Komatsu agreed to lend A.L.I. 200,000,000 yen (approximately $1,469,400 US Dollars based on a conversion rate of $0.007347 US Dollar for each $1 yen as of February 27, 2023) (the “Loan”). The original maturity date of the Loan under the Agreement was April 15, 2023, and was extended to June 30, 2023 (the “Maturity Date”) pursuant to the terms of a memorandum agreement signed on May 15, 2023 (the “Memorandum”). The interest rate under the Agreement is 2.475% per annum (calculated on a pro rata basis for 365 days a year), and the interest period is from February 27, 2023 until April 21, 2023. Pursuant to the terms of the Memorandum, the Company paid Mr. Komatsu 100,000,000 yen (approximately US$753,266), the interest rate was increased to 14.6% per annum as of April 22, 2023 and A.L.I. agreed to delay damages in the amount of 480,000 yen (approximately US$3,616). In addition, A.L.I pledged as collateral for the Loan shares of ASC Tech Agent Co., Ltd. held by A.L.I. and the equity interest in any entity in which A.L.I. may transfer its drone service business in the future. We are in discussions with Mr. Komatsu regarding further extension of the maturity date of the Loan and other alternatives regarding settlement of this debt.

If any of the following events occur while the Loan is outstanding, the Loan will become immediately due and payable together with all interest thereon: (i) if payment is suspended or bankruptcy proceedings are initiated against A.L.I., (ii) if A.L.I. initiates legal proceedings related to debt reorganization involving court intervention or when facts are recognized as having occurred that payment has been suspended, (iii) if provisional seizure, preservation seizure, seizure order, or delinquent disposition is received by A.L.I., (iv) if A.L.I. is delayed in make any payments under the Agreement, (v) if A.L.I. violates any provisions of the Agreement or (vi) upon the occurrence of any equivalent reasons requiring the preservation of the right to claim arise in addition to the foregoing. Pursuant to the Agreement, if A.L.I. does not timely repay the Loan in accordance with the terms of the Agreement, the interest rate on the Loan will increase to 14.6% per annum until the full payment is made. Under the Agreement, for any litigation arising under the Agreement, regardless of the amount or claim, the exclusive court of jurisdiction will be the Tokyo District Court.

Summary of Lind Global Financing

On April 12, 2023, we entered into the Purchase Agreement with Lind Global pursuant to which we agreed to issue to Lind Global up to three secured convertible promissory notes (the “Convertible Notes” and each a “Convertible Note”) in the aggregate principal amount of $6,000,000 for an aggregate purchase price of $5,000,000 and warrants (the “Warrants” and each a “Warrant”) to purchase 56,016 shares of the Company’s common stock (the “Transaction”). On August 25, 2023 (the “Amendment Date”), we entered into an Amendment to Senior Convertible Promissory Note First Closing Note and an Amendment to the Senior Convertible Promissory Note Second Closing Note with Lind Global (collectively, the “Floor Note Amendments”) which amended the Conversion Price (as defined below) to include a floor price of $18.176(the “Floor Price”). In addition to inclusion of a Floor Price, the Note Amendments also provide that at the option of Selling Securityholder, if in connection with a conversion under the Closing Notes, as amended, the Conversion Price is deemed to be the Floor Price, then in addition to issuing the Conversion Shares (as defined in the Closing Notes) at the Floor Price, we agreed to pay to Selling Securityholder a cash amount equal to (i) the number of shares of common stock that would be issued to Selling Securityholder upon a conversion determined by dividing the dollar amount to be converted being paid in shares of common stock by ninety percent (90%) of the lowest single VWAP during the twenty (20) Trading Days prior to the applicable date of conversion (notwithstanding the Floor Price) less (ii) the number of Conversion Shares issued to Selling Securityholder in connection with the conversion; and (iii) multiplying the result thereof by the VWAP on the Conversion Date.

| 13 |

The closings of the Transaction (the “Closings and each a “Closing”) occured in tranches (each a “Tranche”): the Closing of the first Tranche (the “First Closing”) occurred on April 12, 2023 and consisted of the issuance and sale to Lind Global of a Convertible Note with a purchase price of $2,100,000 and a principal amount of $2,520,000 (the “First Closing Note”) and the issuance to Lind Global of a Warrant to acquire 23,527 shares of common stock and the Closing of the second Tranche (the “Second Closing) which occurred on May 23, 2023 and consisted of the issuance and sale to Lind Global of a Convertible Note with a purchase price of $1,400,000 and a principal amount of $1,680,000 (the “Second Closing Note”), and the issuance to Lind Global of a Warrant to acquire 15,685 shares of common stock. The Convertible Notes issued in the First Closing and the Second Closing are hereinafter referred to as the “Closing Notes”. As provided for in the January Note Amendments, neither party to the Purchase Agreement is obligated to complete the previously agreed on third Tranche (the “Third Closing), which would have consisted of the issuance and sale to Lind Global of a Convertible Note with a purchase price of $1,500,000 with a principal amount of $1,800,000, and the issuance to Lind Global a Warrant to acquire 16,805 shares of common stock. The Third Closing would have closed upon the effectiveness of the Registration Statement discussed below, but the Registration Statement was never declared effective by the SEC. Pursuant to the Purchase Agreement, at each Closing, the Company agreed to pay Lind Global a commitment fee in an amount equal to 2.5% of the funding amount being funded by Lind Global at the applicable Closing. Pursuant to the Purchase Agreement, at each Closing, the Company agreed to pay Lind Global a commitment fee in an amount equal to 2.5% of the funding amount being funded by Lind Global at the applicable Closing.

The Convertible Note issued in the First Closing has a maturity date of April 12, 2025 and the Convertible Note issued in the Second Closing has a maturity date of May 23, 2025 (the “Maturity Date”).

Each Convertible Note has a conversion price equal to the lesser of: (i) US$9.00 (“Fixed Price”); or (ii) 90% of the lowest single volume weighted average price during the 20 Trading Days prior to conversion of each Convertible Note (the “Conversion Price”) “), provided that in no event shall the Conversion Price be less than $18.176 (the “Floor Price”), and in the event that the calculation as set forth above would result in a Conversion Price less than the Floor Price, the “Conversion Price” shall be the Floor Price.

In addition to inclusion of a Floor Price, the Note Amendments also provide that at the option of Selling Securityholder, if in connection with a conversion under the Closing Notes, as amended, the Conversion Price is deemed to be the Floor Price, then in addition to issuing the Conversion Shares (as defined in the Closing Notes) at the Floor Price, we agreed to pay to Selling Securityholder a cash amount equal to (i) the number of shares of common stock that would be issued to Selling Securityholder upon a conversion determined by dividing the dollar amount to be converted being paid in shares of common stock by ninety percent (90%) of the lowest single VWAP during the twenty (20) Trading Days prior to the applicable date of conversion (notwithstanding the Floor Price) less (ii) the number of Conversion Shares issued to Selling Securityholder in connection with the conversion; and (iii) multiplying the result thereof by the VWAP on the Conversion Date.

The Convertible Note will not bear interest other than in the event that if certain payments under the Convertible Note as set forth therein are not timely made, the Convertible Note will bear interest at the rate of 2% per month (prorated for partial months) until paid in full. The Company will have the right to prepay the Convertible Note under the terms set forth therein.

The Warrants were issued to Lind Global without payment of any cash consideration. Each Warrant will have an exercise period of 60 months from the date of issuance. The Exercise price of the First Closing Warrant and Second Closing Warrant is $89.26 per share and $73.16 per share, respectively, subject to adjustments as set forth in the Warrant.

In the event that there is no effective registration statement registering the shares underlying the Warrants or upon the occurrence of a Fundamental Transaction as defined in the Purchase Agreement, then the Warrants may be exercised by means of a “cashless exercise” at the holder’s option, such that the holder may use the appreciated value of the Warrants (the difference between the market price of the underlying shares of common stock and the exercise price of the underlying warrants) to exercise the warrants without the payment of any cash.

| 14 |

In accordance with our obligations under the Purchase Agreement, we filed a registration statement on Form S-1 on May 12, 2023 (the “May 2023 Registration Statement”) with the SEC to register under the Securities Act the resale by Lind Global of up to 112,223 shares of common stock issuable by us upon partial conversion of the Convertible Notes and exercise of the Warrants issued by us in connection with the Purchase Agreement. We plan to withdraw the May 2023 Registration Statement as permitted pursuant to the SPA Amendment No. 2 discussed below.

The Purchase Agreement contains customary registration rights, representations, warranties, conditions and indemnification obligations by each party, including our agreement to refrain from engaging in certain “Prohibited Transactions” as defined in the Purchase Agreement, to hold a special meeting of shareholders for the purpose of obtaining shareholder approval of the Transactions, certain events giving rise to a default under the Convertible Notes, obligations to use the proceeds from certain future financings to repay a portion of the principal amount of the Convertible Notes, our pledge to Lind Global of the ownership interests in our subsidiaries, a grant by us and our subsidiaries of a security interest in all of their respective assets and rights as collateral for the obligations due under the Convertible Notes, and a guaranty by our subsidiaries of our obligations under the Convertible Notes.

The A.L.I. Bankruptcy constitutes an event of default pursuant to the Closing Notes in the aggregate principal amount of $4,200,000. Consequently, Lind Global may at any time, at its option, (1) demand payment of an amount equal to 120% of the outstanding principal amount of the Closing Notes and (2) exercise all other rights and remedies available to it under the Closing Notes and other agreements entered into among the Company and Lind in connection with the issuance of the Closing Notes (collectively, the “Transaction Documents”); provided, however, that (x) upon the occurrence of the event of default described above, Lind Global, in its sole and absolute discretion (without the obligation to provide notice of such event of default), may: (a) from time-to-time demand that all or a portion of the outstanding principal amount of the Closing Notes be converted into shares of the Company’s common stock at the lower of (i) the then-current Conversion Price (that price being $18.176 per share (the “Floor Price”)) and (ii) eighty-percent (80%) of the average of the three (3) lowest daily volume weighted average prices (“VWAPs”) during the 20 trading days prior to the delivery by Lind Global of the applicable notice of conversion or (b) exercise or otherwise enforce any one or more of Lind Global’s rights, powers, privileges, remedies and interests under the Closing Notes, the Transaction Documents or applicable law.

The Closing Notes also provide that at the option of Lind Global, if in connection with a conversion under the Closing Notes, the Conversion Price is deemed to be the Floor Price, then in addition to issuing the Conversion Shares (as defined in the Closing Notes) at the Floor Price, the Company will also pay to Lind Global a cash amount equal to (i) the number of shares of common stock that would be issued to Lind Global upon a conversion determined by dividing the dollar amount to be converted being paid in shares of common stock by ninety percent (90%) of the lowest single VWAP during the twenty (20) trading days prior to the applicable date of conversion (notwithstanding the Floor Price) less (ii) the number of shares of the Company’s common stock issued to Lind Global in connection with the conversion; and (iii) multiplying the result thereof by the VWAP on the date of conversion.

On January 23, 2024, the Company and Lind Global entered into an Amendment No. 2 to Senior Convertible Promissory Note First Closing Note and an Amendment No. 2 to the Senior Convertible Promissory Note Second Closing Note (collectively, the “January Note Amendments”) which amended the Closing Notes to, subject to the conditions discussed below, (i) reduce the aggregate principal amount of the Closing Notes from $4,200,000 to $3,500,000, (ii) require the Company to repay an aggregate of $1,750,000 of the principal amount of the Closing Notes no later than the closing date of a public offering of the Company’s common stock where it receives gross proceeds of at least $13,500,000 (the “Public Offering”) no later than April 15, 2024 and (iii) requires Lind Global to convert no less than an aggregate of $1,750,000 of the Closing Notes no later than 11 months after the closing of the Public Offering, provided that at the time of such conversion Lind Global receives shares of common stock that may be disposed of without restrictive legend at their issuance pursuant to an effective registration statement under the Securities Act of 1933, as amended (the “Securities Act”) or pursuant to an available exemption from or in a transaction not subject to the registration requirements of the Securities Act (the “Mandatory Conversion Amount”).

In addition, on January 23, 2024, the Company and Lind Global entered into Amendment No. 2 to Securities Purchase Agreement (the “SPA Amendment No. 2”) to, subject to the conditions discussed below, (i) eliminate the obligation of the Company and Lind Global to complete the Third Closing discussed above, (ii) delete the clause obligating the Company to register the shares of common stock issuable upon conversion of the Closing Notes and exercise of the Warrants (collectively, the “Closing Securities”) or pay Lind Global any delay payments as a result of the Company’s failure to register the Closing Securities, (iii) eliminate certain restrictions on the Company’s right to issue equity and debt in future transactions and (iv) eliminate Lind Global’s right to participate in future offerings of the Company’s securities, other than its rights to participate in this offering.

| 15 |

The January Note Amendments and the SPA Amendment are subject to the Company completing a public offering of its Common Stock where it receives gross proceeds of at least $13,500,000 (the “Public Offering”) and making the Mandatory Prepayment as discussed above. In as much as the Company failed to complete the Public Offering by April 15, 2024, Lind Global is not obligated to fulfill the terms of the January Note Amendments. The Company plans to enter into discussions with Lind Global to extend the time period in which it is obligated to complete the Public Offering.

Officer and Director Changes

On March 20, 2023, Shuhei Komatsu resigned from his positions as Chief Executive Officer and Director and Chairman of the Board of Directors of the Company (the “Board”). Mr. Komatsu previously served as the Company’s Chief Executive Officer and a Director and Chairman of the Board since February 3, 2023. Mr. Komatsu’s resignation was not the result of any disagreement with the Company on any matter relating to the Company’s operations, policies or practices.

On March 20, 2023, the Company’s Board appointed Taiji Ito to serve as Chief Executive Officer of the Company. Mr. Ito formerly served as the Company’s Global Markets Executive Officer and as a Director of the Company, and has served in such capacities since his appointment to those positions on February 3, 2023 until his resignation as discussed below.

On March 22, 2023, the Board appointed Daisuke Katano to fill the vacancy on its Board created upon Mr. Komatsu’s resignation to serve as a Director of the Company, and on the same date also appointed Mr. Katano to serve as the Company’s Chief Operating Officer.

On March 22, 2023, the Board appointed Marehiko Yamada to serve as the Chairman of the Board. Mr. Yamada was appointed as an independent director of the Company on February 3, 2023. On March 22, 2023, the Company’s Board of Directors also appointed Dr. Sayama to serve as the Vice-Chair of the Board. Dr. Sayama was appointed as an independent director of the Company on February 3, 2023. On March 22, 2023, the Company’s Board also appointed Kensuke Okabe to serve as Secretary of the Company. Mr. Okabe was appointed as the Company’s Chief Financial Officer on February 3, 2023.

On March 22, 2023, the Board also appointed Mr. Yamada as the Chair of the Company’s Compensation Committee and appointed Dr. Sayama as the Chair of the Company’s Nominating and Corporate Governance Committee. Dr. Sayama previously served as the Chair of the Company’s Compensation Committee from February 3, 2023 to March 22, 2023. Mr. Yamada previously served as the Chair of the Company’s Nominating and Corporate Governance Committee from February 3, 2023 to March 22, 2023.

On March 27, 2023, the Board approved the removal of Kazuo Miura as the Company’s Chief Product Officer. Mr. Miura served as the Company’s Chief Product Officer since his appointment to this position on February 3, 2023. Mr. Miura’s removal was not the result of any disagreement with the Company on any matter relating to the Company’s operations, policies or practices.

On May 15, 2023, the Company’s Board appointed Kiran Sidhu as the Chairman of the Board. Following the appointment of Mr. Sidhu, Dr. Sayama and Mr. Yamada resigned as members of the Board, effective May 18, 2023 and May 15, 2023, respectively. Their resignations were not the result of any disagreement with the Company on any matter relating to the Company’s operations, policies or practices.

On May 22, 2023, the Board also appointed Katharyn (Katie) Field and Pavanveer (Pavan) Gill as independent directors to fill the vacancies on the Board created by the resignations of Dr. Sayama and Mr. Yamada. Following the appointment of Ms. Field and Mr. Gill, Mr. Iwamura resigned as a member of the Board. Mr. Iwamura’s resignation was not the result of any disagreement with the Company on any matter relating to the Company’s operations, policies or practices.

| 16 |

On July 17, 2023, Daisuke Katano resigned as a member of our Board of Directors and on July 25, 2023 resigned as our Chief Operating Officer. Mr. Katano’s resignation was not the result of any dispute or disagreement with the Company or the Board on any matter relating to the operations, policies or practices of the Company.

On July 18, 2023, the Board appointed Kiran Sidhu as Executive Chairman of the Board and President of the Company and expanded the size of the Board by one person, to a total of seven persons, appointing Mr. Robert Lim as an independent Director of the Company, filling the vacancy created by Mr. Katano’s resignation. Mr. Lim’s term is to serve in such position until his earlier death, resignation or removal from office.

On July 18, 2023, the Board changed the composition of the Committees of the Board to be comprised of the following persons:

| ● | The Audit Committee shall be comprised of the following persons: Katharyn Field, Committee Chair and Audit Committee Financial Expert; Robert Lim; and, Pavanveer Gill. | |

| ● | The Compensation Committee shall be comprised of the following persons: Pavanveer Gill, Committee Chair; Robert Lim; and, Katharyn Field. | |

| ● | The Nominating and Corporation Governance Committee shall be comprised of the following persons: Robert Lim, Committee Chair; Katharyn Field; and, Pavanveer Gill. |

On July 18, 2023, the Board formed a “Funding Committee of the Board” that is comprised on the following persons: Katharyn Field as Committee Chair; Mr. Lim; and, Mr. Katano. The purpose of the committee is to consider funding alternatives and make recommendations on such alternatives to the Board.

On August 24, 2023, we appointed Yinshun (Sue) He as our Chief Financial Officer following the resignation of Kensuke Okabe.

On December 12, 2023, Kiran Sidhu was appointed as our Chief Executive Officer following the resignation of Taiji Ito as our Chief Executive Officer. Mr. Ito remains as a director of the Company. As part of this change, the Board appointed Ms. Field as the Chairman of the Board to take on the role formerly held by Mr. Sidhu who will remain as a director of the Company in addition to his role as its CEO.

Potential Nasdaq Delisting

As previously disclosed in the Current Report on Form 8-K filed on April 21, 2023 by the Company, on April 20, 2023, Nasdaq Listing Qualifications staff (“Staff”) of The Nasdaq Stock Market LLC (“Nasdaq”) notified the Company that it no longer complied with the minimum bid price requirement under Listing Rule 5450(a)(1). In accordance with Listing Rule 5810(c)(3)(A), the Company was provided 180 calendar days, or until October 17, 2023, to regain compliance with Rule 5450(a)(1) (the “Bid Price Rule”). As previously disclosed on a Form 8-K filed with the SEC on October 23, 2023, on October 18, 2023, Staff notified the Company that it had determined to delist the Company as it did not comply with the requirements for continued listing on the Exchange. As previously disclosed in the Current Report on Form 8-K filed with the SEC on November 28, 2023, the Company appealed Nasdaq’s determination in accordance with the procedures set forth in the Nasdaq Listing Rules and requested a hearing (the “Hearing Request”) before the Nasdaq Hearings Panel (the “Panel”). As previously disclosed on a Form 8-K filed with the SEC on November 28, 2023, on November 21, 2023, Staff issued an additional delist determination letter after the Company failed to file its Form 10-Q for the period ended September 30, 2023 (the “Delinquent Report”), as required by Listing Rule 5250(c)(1) (the “Periodic Filing Rule”). On November 28, 2023, the Company filed its Delinquent Report and, thus, regained compliance with the Periodic Filing Rule. As previously disclosed on a Form 8-K filed with the SEC on December 12, 2023, on December 6, 2023, Staff issued an additional delist determination letter as the Company’s no longer complied with the $50,000,000 minimum market value of listed securities requirement set forth in Listing Rule 5450(b)(2)(A) (the “MVLS Rule”), which served as an additional and separate basis for delisting.

A hearing before the Panel was conducted on January 4, 2024. The Panel conditionally granted the Company’s request to transfer its shares from The Nasdaq Global Market to The Nasdaq Capital Market, effective at the open of trading on January 18, 2024 and the Company’s request for an exception to the Exchange’s listing rules until April 15, 2024, to demonstrate compliance, subject to the satisfaction of the following conditions (the “Panel Decision”):

| 1. | On or before January 23, 2024, the Company shall file a Form S-1 for a public offering of up to $13.5 million contemplated in its presentation to the Panel; | |

| 2. | On or before January 19, 2024, the Company shall file all necessary documentation required to transfer its listing from The Nasdaq Global Market to The Nasdaq Capital Market; |

| 17 |

| 3. | On or before January 31, 2024, the Company will complete the deconsolidation of its Japanese subsidiary A.L.I. Technologies Inc. (“A.L.I. Technologies”); | |

| 4. | On or before March 28, 2024, the Company will implement a reverse stock split in a range of 1-for-10 to 1-for-100 with a target per share price of $7.00 per share; | |

| 5. | On or before April 15, 2024, the Company shall demonstrate compliance with all applicable continued listing requirements for The Nasdaq Capital Market under Rule 5550. |

The Panel Decision indicates that the Company may request that the Nasdaq Listing and Hearing Review Council (the “Council”) review the Panel Decision, in which case a written request for review would need to be received within 15 days from the date of the Panel Decision. The Council may also on its own motion determine to review the Panel Decision.

The Panel Decision has no immediate effect on the listing of the Company’s common stock on the Nasdaq Global Market. The Company plans to fulfil each of the conditions as stated in the Panel Decision. To this end, the Company filed a Registration Statement on Form S-1 which this prospectus is a part on January 23, 2024 and completed the filing of all necessary documentation required to transfer its listing from The Nasdaq Global Market to The Nasdaq Capital Market. In addition, in satisfaction of the A.L.I. Technologies deconsolidation condition of the Panel Decision and as previously disclosed in a Form 8-K filed by the Company with the SEC on January 16, 2024, the Tokyo District Court entered an order on January 10, 2024, (the “January 10 Order”) confirming that bankruptcy proceedings are commenced against the A.L.I. Technologies, that A.L.I. Technologies is found to be insolvent and other administrative matters relating to the A.L.I. Technologies bankruptcy filing. Finally, on November 20, 2023, our stockholders voted to approve an amendment of our Fourth Amended and Restated Certificate of Incorporation (the “Certificate of Incorporation”), to effectuate a reverse stock split of our common stock at a ratio of no less than 1-for-10 and no more than 1-for-100, with such ratio to be determined at the sole discretion of our board of directors and, effective as of April 2, 2024, we effectuated a 1-for-100 reverse stock split of our common stock. No assurance can be given, however, as to the definitive date on which the remaining fifth condition set forth in the Panel Decision will be achieved.

Following a request submitted by the Company on April 12, 2024, the Panel granted a further extension to the exception granted on January 16, 2024, to the Company, as amended on January 17, 2024 (the “Decision”), to extend the Company’s deadline to regain compliance with Listing Rule 5550(b)(1) (the “Equity Requirement”). In granting the extension, the Panel noted that as of April 15, 2024, the Company has regained compliance with Nasdaq Listing Rule 5550(b)(1). Based on the information presented, the Panel determined to grant the Company’s request for an exception extension to regain compliance with the Equity Requirement until May 31, 2024, subject to the Company demonstrating compliance with all applicable continued listing requirements for The Nasdaq Capital Market under Rule 5550.

On April 17, 2024, the Company received an Additional Staff Delisting Determination (the “Additional Staff Determination”) from Nasdaq. The Additional Staff Determination noted that the Company is now delinquent in filing its Form 10-K for the period ended December 31, 2023 (the “Form 10-K”), which additional delinquency may serve as a separate basis for the delisting of the Company’s securities from Nasdaq. The Additional Staff Determination notified the Company that the Nasdaq Hearings Panel (the “Panel”) will consider this matter in their decision regarding the Company’s continued listing on The Nasdaq Capital Market and that it should present its views with respect to this additional deficiency to the Panel in writing no later than April 24, 2024. On April 30, 2024, the Company filed its delinquent Form 10-K for the period ended December 31, 2023.

Submission of Matters to a Vote of Security Holders

On November 20, 2023, the Company held its 2023 virtual special meeting of stockholders to vote on the following matters:

Stockholders voted to approve the amendment of the Company’s Fourth Amended and Restated Certificate of Incorporation (the “Certificate of Incorporation”), to effectuate a reverse stock split of the Company’s outstanding shares of our common stock, at a ratio of no less than 1-for-10 and no more than 1-for-100, with such ratio to be determined at the sole discretion of the Board (the “Reverse Stock Split”).

Stockholders voted to approve, for purposes of complying with NASDAQ Listing Rule 5635(b), the issuance of the shares of the Company’s common stock pursuant to its purchase agreement with Lind Global representing more than 20% of our common stock outstanding, which would result in a “change of control” of the Company under applicable Nasdaq listing rules.

Stockholders voted to approve, for purposes of complying with Nasdaq Listing Rule 5635(d), the issuance of more than 20% of the Company’s issued and outstanding common stock pursuant to its purchase agreement with Lind Global.

| 18 |

Recent Sales of Unregistered Securities

On February 27, 2024 and March 22, 2024, we entered into and completed the sale to two unrelated accredited investors (the “Investors”), of 100,000 shares and 35,500 unregistered shares, respectively, of our Common Stock at a price of $4.00 per share for an aggregate of $542,000 in cash (the “Offerings”). The Offerings were made pursuant to the terms of a Subscription Agreement. In connection with the Offerings, the Company entered into a Piggyback Registration Rights Agreement with each Investor whereby the Company agreed to register the Common Stock acquired by the Investor in the Offering if at any time while the Investor remains the holder of such shares, the Company proposes to file any registration statement under the Securities Act of 1933, as amended (the “Securities Act”) with respect to its Common Stock for its own account or for shareholders of the Company for their account, subject to certain customary exceptions.

Effects of Inflation

We have not been affected by inflationary pressure as we are in the development stage of the MAV and have not commenced production.

Employees

Prior to the closing of the Business Combination, at December 31, 2022, the Company had three executive officers and the Company did not have any full-time employees prior to the completion of the Business Combination.

Following the December 27, 2023 discontinuation of A.L.I., we have two employees as of January 22, 2024. Of these, both are part-time, temporary, or other temporary employees. No labor union has been formed, but labor-management relations are amicable.

Facilities

Prior to the December 27, 2023 discontinuation of A.L.I., our headquarters were located at Shiba Koen Annex 6 f, 1-8, Shiba Koen 3-chome, Minato-ku, Tokyo, Japan 105-0011, where we leased and occupied office space with an aggregate floor area of approximately 340 square meters from unrelated third parties under operating lease agreements. Our manufacturing and shipping facility was located at 1-2-11 Fukamidai, Yamato-shi, Kanagawa. Our testing facilities was located at 72 Misawa, Minobu-cho, Minami Koma-gun, Yamanashi. We no longer occupy any of these offices or facilities and following the discontinuance of ALI’s operations and bankruptcy filing on December 27, 2023, we moved our corporate offices to The Walnut Building, 691 Mill St, Suite 240, Los Angeles, California 90021 where we lease this this office.

We believe that our existing office is generally adequate to meet our current needs, but we expect to seek additional space as needed to accommodate our future growth. There are no major facilities currently inactive.

Insurance