Exhibit 99.4

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS OF AERWINS

The following discussion and analysis of AERWINS’ financial condition and results of operations should be read in conjunction with AERWINS’ financial statements and related notes that appear elsewhere in this proxy statement/prospectus. In addition to historical information, this discussion and analysis contains forward-looking statements that involve risks, uncertainties, assumptions and other factors that could cause actual results to differ materially from those made, projected or implied in the forward-looking statements. Factors that could cause or contribute to these differences include, but are not limited to, those discussed below and elsewhere particularly in the “Risk Factors” and “Cautionary Note Regarding Forward-Looking Statements” sections of this proxy statement/prospectus.

Business Overview

We were incorporated in the State of Delaware on June 9, 2022. We conduct business activities principally through our 100%-owned subsidiary, A. L. I. Technologies Inc., a Japanese corporation (“A. L. I. Technologies”), which was established in Japan in September 2016 and was acquired by us in August, 2022.

The acquisition of A. L. I. Technologies was accounted for as a recapitalization among entities under common control since the same controlling shareholders controlled all these entities before and after the transaction. The consolidation of the Company and its subsidiaries has been accounted for at historical cost and prepared on the basis as if the transaction had become effective as of the beginning of the first period presented in the accompanying consolidated financial statements.

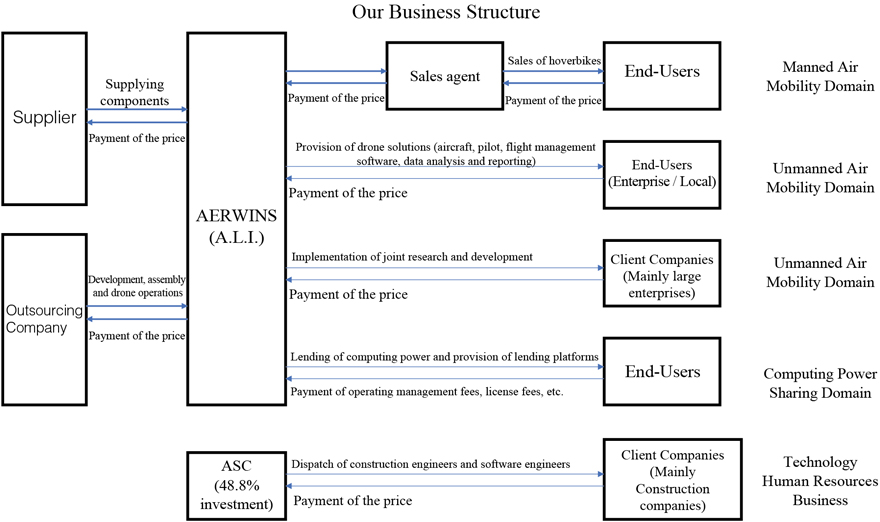

We are developing our air mobility business with the aim of contributing to society as a global company that leads the air mobility society by providing infrastructure that enables anyone to use the airspace safely, securely, and conveniently through the constant challenge of new technologies and their implementation in society.

To realize this vision, we are developing the following business areas:

(1) manned air mobility area, which involves the sale and development of hoverbikes that can float at low altitude through difficult-to-move zones in times of disaster,

(2) unmanned air mobility domain, which provides solutions utilizing industrial drones (integrated provision of R&D, aircraft rental or sales, operators, operation management, and other software); and

(3) the computing power sharing domain, which provides services such as blockchain verification and AI.

1

Significant Market Opportunities

In today’s increasingly populated and interconnected world, traditional modes of urban transportation continue to contribute to congestion and pollution, and they are largely confined to land-based infrastructure. Mobility for the future requires a revolutionary solution.

The market opportunities created by our technology are significant. According to an analysis by Frost & Sullivan, the autonomous vehicle services market is expected to grow from a mere $1.1 billion in 2019 to $202.5 billion in 2030 at a CAGR of 60.1%, facilitated by mutually beneficial business models across the entire mobility value chain. To capture the significant growth potential in the AAV market, we strive to continue to innovate and expand the boundaries for air-based mobility.

The sky above has always held possibilities, and we have already completed our first manned flight test with a test aircraft in 2019, and our business is progressing well since then. We plan to work with business partners, mainly in the Middle East area, for additional development, production and sales to realize products that can be utilized in the Middle East area. In the future, we are also preparing to develop new models that are electrically powered and even more compact, and to provide infrastructure such as airways and air traffic control systems in an air mobility society.

We are one step closer to making safe, cost-effective, and easy-to-use air mobility solutions a reality. Our air mobility enables urban mobility to expand into three-dimensional space. We believe our technology will change the future of transportation, improve lives, and create new industries.

We design, develop, manufacture, market, and operate unmanned aircraft and their supporting systems and infrastructure for a wide range of industries and applications, including passenger transportation, logistics, and smart city management. Our goal is to ensure that both passengers and goods take to the skies safely and conveniently.

Orders, Delivery and Financial Results

We are developing the following business areas:

(1) manned air mobility area, which involves the sale and development of hoverbikes that can float at low altitude through difficult-to-move zones in times of disaster;

2

(2) unmanned air mobility domain, which provides solutions utilizing industrial drones (integrated provision of R&D, aircraft rental or sales, operators, operation management, and other software); and

(3) the computing power sharing domain, which provides services such as blockchain verification and AI.

For the fiscal years ended December 31, 2022 and 2021, we generated revenues of $5,270,490 and $7,830,130, respectively, from continuing operations, and reported net loss of $14,479,819 and net loss of $14,527,021, respectively from continuing operations, and cash flows used in operating activities of $16,865,274 and $10,119,103, respectively. As noted in our consolidated financial statements, as of December 31, 2022, we had an accumulated deficit of $46,472,904.

Key Factors that Affect Our Results of Operations

We believe the following key factors may affect our financial condition and results of operations:

Our Ability to Strength Our Competitive Advantages

Our results of operations rely on our purported product superiority. Both hardware and software technologies are key factors intended to strengthen our competitive advantages. Regarding hardware, we developed air mobility CFRP material for XTURISMO which reduced the weight of the open propeller and its body. CFRP is also easy to process and corresponds to various designs, and has strong resistance to dust and salt air. We also developed an original body and steering wheel which enables a driver to drive manually easier. The original hybrid engine has high power generation with low revolution with electric supply support to control system device. Regarding software, the stability control of XTURISMO assists driving by sensor fusion surrounding the body and links with cloud real time with encrypted driving and control data communication. Also, C.O.S.M.O.S., the air traffic control platform connects with each hoverbike and provides flight and network management. These hardware and software are all made in Japan.

Our Ability to Expand International Market

We are seeking to promote global expansion using partnerships, and our ability to succeed in this endeavor will affect our results of operations. Especially in Gulf Cooperation Council, we have partners for creating the business in the area and will raise fund which we believe enables the Company to establish an office and R&D center in the area and we also intend that the area can be a distribution, manufacturing and marketing hub for the vehicles. After that or at the same time, we plan to expand sales channels to other regions including the United States. Also, in order to facilitate such global expansion, the Company plans to acquire human resources in various countries, and the Company intends that by 2024, over 50% of its employees will be non-Japanese.

Our Ability to Control Costs and Expenses and Improve Our Operating Efficiency

We are aiming to establish a highly profitable structure for a mass production of hoverbikes by using a fabless model which focuses on design and supply chain control. We plan to select subcontractors and suppliers appropriately based on cost, quality, and delivery date, and seek to build an efficient production system. We also hope to sign a partnership agreement with a local government to implement hoverbikes in society. We aim to reduce the cost of developing advanced technologies and implementing our products in society by utilizing subsidies as part of such support.

3

A Severe or Prolonged Slowdown in the Global and Japan Economy Could Materially and Adversely Affect Our Business and Our Financial Condition

In recent years, the economic indicators in Japan have shown mixed signs, and future growth of the Japanese economy is subject to many factors beyond our control. The Japanese economy is gradually recovering due to the effects of various government policies which encourage the transition to the post-covid society. However, it is necessary to note downside risks due to fluctuations in the financial markets, price increase, and supply-chain constraints as global monetary tightening is progressing. Any future deterioration of the Japanese or global economy may result in a decline in consumption that would have a negative impact on demand for our products and their prices.

Results of Operations

Comparison of Results of Operations for the Fiscal Years Ended December 31, 2022 and 2021

The following table summarizes our operating results as reflected in our statements of income during the fiscal years ended December 31, 2022 and 2021, respectively, and provides information regarding the dollar and percentage increase or (decrease) during such periods.

| For the Years ended December 31, | ||||||||||||||||||||||||

| 2022 | 2021 | Variance | ||||||||||||||||||||||

| Amount | % of revenue |

Amount | % of revenue |

Amount | % of | |||||||||||||||||||

| REVENUE |

$ | 5,207,490 | 100.0 | % | $ | 7,830,130 | 100 | % | $ | (2,622,640 | ) | -33.5 | % | |||||||||||

| COST OF REVENUE |

5,070,507 | 97.4 | % | 6,433,913 | 82.2 | % | (1,363,406 | ) | -21.2 | % | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| GROSS PROFIT |

136,983 | 2.6 | % | 1,396,217 | 17.8 | % | (1,259,234 | ) | -90.2 | % | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Operating expenses |

||||||||||||||||||||||||

| Selling expenses |

90,654 | 1.7 | % | 259,799 | 3.3 | % | (169,145 | ) | -65.1 | % | ||||||||||||||

| General and administrative expenses |

7,212,327 | 138.5 | % | 5,839,433 | 74.6 | % | 1,372,894 | 23.5 | % | |||||||||||||||

| Research and development expenses |

8,926,205 | 171.4 | % | 9,335,977 | 119.2 | % | (409,772 | ) | -4.4 | % | ||||||||||||||

| Total operating expenses |

16,229,186 | 311.7 | % | 15,435,209 | 197.1 | % | 793,977 | 5.1 | % | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Loss from operations |

(16,092,203 | ) | -309.0 | % | (14,038,992 | ) | -179.3 | % | (2,053,211 | ) | 14.6 | % | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Other income (expenses) |

1,613,927 | 31.0 | % | (488,029 | ) | -6.2 | % | 2,101,956 | -430.7 | % | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Loss before income tax provision |

(14,478,276 | ) | -278.0 | % | (14,527,021 | ) | -185.5 | % | 48,745 | -0.3 | % | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Income taxes expense |

(1,543 | ) | -0.0 | % | — | — | (1,543 | ) | — | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

4

| For the Years ended December 31, | ||||||||||||||||||||||||

| 2022 | 2021 | Variance | ||||||||||||||||||||||

| Amount | % of revenue |

Amount | % of revenue |

Amount | % of | |||||||||||||||||||

| Net loss from continuing operations |

(14,479,819 | ) | -278.1 | % | (14,527,021 | ) | -185.5 | % | 47,202 | -0.3 | % | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Less: net income (loss) attributable to non-controlling interest |

— | — | % | — | % | % | ||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||

| Net loss from discontinued operations |

— | — | 28,649 | -0.4 | % | 28,649 | -100.0 | % | ||||||||||||||||

| NET INCOME (LOSS) ATTRIBUTABLE TO AERWINS TECHNOLOGIES INC. |

$ | (14,479,819 | ) | -278.1 | % | $ | (14,555,670 | ) | -185.9 | % | $ | 75,851 | -0.5 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

Revenue

Our total revenues decreased by $2,622,640, or 33.5%, to $5,207,490 for the year ended December 31, 2022 from $7,830,130 for the year ended December 31, 2021. The decrease in our revenues was mainly due to the depreciation of JPY and decrease in sales from shared computing business.

Cost of Revenue

Our total costs of revenues decreased by $1,363,406, or 21.2%, to $5,070,507 for the year ended December 31, 2022 from $6,433,913 for the year ended December 31, 2021. The decrease in our costs was attributable to the decrease of the sales described above.

5

Gross Profit

Our total gross profit decreased by $1,259,234, or 90.2%, to $136,983 for the year ended December 31, 2022 from $1,396,217 for the year ended December 31, 2021. For the reasons discussed above, our overall gross profit margin decreased by 15.2% to 2.6% in the fiscal year 2022 from 17.8% in the fiscal year 2021.

Operating Expenses

The following table sets forth the breakdown of our operating expenses for the fiscal years ended December 31, 2022 and 2021:

| For the Years ended December 31, | ||||||||||||||||||||||||

| 2022 | 2021 | Variance | ||||||||||||||||||||||

| % of | % of | |||||||||||||||||||||||

| Amount | revenue | Amount | revenue | Amount | % of | |||||||||||||||||||

| Total revenue |

$ | 5,207,490 | 100 | % | $ | 7,830,130 | 100 | % | $ | (2,622,640 | ) | (33.5 | )% | |||||||||||

| Operating expenses |

||||||||||||||||||||||||

| Selling expenses (advertising expenses) |

90,654 | 1.7 | % | 259,799 | 3.3 | % | (169,145 | ) | (65.1 | )% | ||||||||||||||

| General and administrative expenses |

7,212,327 | 138.5 | % | 5,839,433 | 74.6 | % | 1,372,894 | 23.5 | % | |||||||||||||||

| Research and development expenses |

8,926,205 | 171.4 | % | 9,335,977 | 119.2 | % | (409,772 | ) | (4.4 | )% | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total operating expenses |

$ | 16,229,186 | 311.7 | % | $ | 15,435,209 | 197.1 | % | $ | 793,977 | 5.1 | % | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

General and Administrative Expenses

Our general and administrative expenses primarily consist of employee salaries and welfare, consulting and professional service fees incurred for company reorganization and going public, depreciation and amortization expenses, rental expenses, office, utility and other expenses, bad debt expenses, and travel and entertainment expenses.

| For the Years ended December 31, | ||||||||||||||||||||||||

| 2022 | 2021 | Variance | ||||||||||||||||||||||

| Amount | % of* | Amount | % of | Amount | % of | |||||||||||||||||||

| General and Administrative Expenses |

||||||||||||||||||||||||

| Salaries and welfare |

$ | 2,744,757 | 38.1 | % | $ | 2,800,058 | 48.0 | % | $ | (55,301 | ) | (2.0 | )% | |||||||||||

| Consulting and professional service fees |

2,680,345 | 37.2 | % | 1,527,311 | 26.2 | % | 1,153,034 | 75.5 | % | |||||||||||||||

| Depreciation expense |

141,026 | 2.0 | % | 86,025 | 1.5 | % | 55,001 | 63.9 | % | |||||||||||||||

| Rent expense |

148,474 | 2.1 | % | 243,265 | 4.2 | % | (94,791 | ) | (39.0 | )% | ||||||||||||||

| Office, utility and other expenses |

674,238 | 9.3 | % | 472,868 | 8.1 | % | 201,370 | 42.6 | % | |||||||||||||||

| Travel and entertainment expense |

395,708 | 5.5 | % | 145,598 | 2.5 | % | 250,110 | 171.8 | % | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Commission fees expenses |

46,673 | 0.6 | % | 302,495 | 5.2 | % | (255,822 | ) | (84.6 | )% | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Other expenses |

381,106 | 5.3 | % | 261, | 4.5 | % | 119,2 | 45.6 | % | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total general and administrative expenses |

$ | 7,212,327 | 100 | % | $ | 5,839,433 | 100 | % | $ | 1,372,894 | 23.5 | % | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| * | Refers to the percentage of total general and administrative expenses. |

Our general and administrative expenses increased by $1,372,894 or 23.5%, to $7,212,327 in the fiscal year 2022 from $5,839,433 in the fiscal year 2021, primarily attributable to an increase of consulting and professional service fees, mainly outsourcing fees paid to professionals for the completion of the merger with Pono Capiral Corp.

6

The overall increase in our general and administrative expenses in fiscal year 2022 as compared to fiscal year 2021 reflected the above-mentioned factors combined. As a percentage of revenues, general and administrative expenses were 138.5% and 74.6% of our revenue for the fiscal years ended December 31, 2022 and 2021, respectively.

Research and development expenses

Our research and development expenses primarily consist of employee salaries and welfare, and outsourcing expenses.

| For the Years ended December 31, | ||||||||||||||||||||||||

| 2022 | 2021 | Variance | ||||||||||||||||||||||

| Amount | % of* | Amount | % of | Amount | % of | |||||||||||||||||||

| Research and Development Expenses |

||||||||||||||||||||||||

| Raw materials |

$ | 2,727,178 | 30.6 | % | $ | 2,434,512 | 26.1 | % | $ | 292,666 | 12.0 | % | ||||||||||||

| Labor cost |

1,675,129 | 18.8 | 1,142,652 | 12.2 | 532,478 | 46.6 | ||||||||||||||||||

| Outsourcing expenses |

3,762,590 | 42.2 | 5,062,176 | 54.2 | -1,299,586 | (25.7 | ) | |||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Other expenses |

761,307 | 8.4 | 696,637 | 7.5 | 64,670 | 9.3 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total research and development expenses |

$ | 8,926,205 | 100.0 | % | $ | 9,335,977 | 100.0 | % | $ | -409,772 | (4.4 | )% | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| * | Refers to the percentage of total research and development expenses. |

Our research and development expenses decreased by $409,772, or 4.4%, to $8,926,205 in the year ended December 31, 2022 from $9,335,977 in the year ended December 31, 2021, primarily attributable to the decrease in outsourcing expenses for development of XTURISMO.

As a percentage of revenues, research and development expenses were 171.4% and 119.2% of our revenue for the fiscal years ended December 31, 2022 and 2021, respectively.

Other Income (Expenses), net

Our other income (expenses) primarily includes gain or loss on disposal of fixed assets, impairment on fixed assets and financial related expenses. Total other income in the fiscal year 2022 was $1,613,927, and the total net expenses in the fiscal year 2021 was $422,469.

The Company disposed part of its business of Zeroboard and recognized $580,177 of gain on disposal of the business in the fiscal year 2021.

In the fiscal year 2022, the Company recognized impairment loss of fixed assets of $511,695 and recognized $1,801,660 of gain on sale of investment securities from sale of Zeroboard and Liberaware stocks (See Note 18).

Provision for Income Taxes

Our provision for income taxes was $1,543 and zero in the fiscal year 2022 and 2021 respectively.

7

Net Income (Loss)

As a result of the foregoing, we reported a net loss of $14,479,819 for the fiscal year ended December 31, 2022, representing a $47,202 or 0.3% decrease from a net loss of $14,527,021 for the fiscal year ended December 31, 2021. All net income is attributable to AERWINS Technologies Inc.

Liquidity and Capital Resources

As of December 31, 2022, we had $1,278,026 in cash as compared to $10,020,459 as of December 31, 2021. We also had $980,688 in accounts receivable as of December 31, 2022 as compared to $725,287 as of December 31, 2021. Our accounts receivable primarily include balance due from customers AMVs sold and services provided and accepted by customers.

As of December 31, 2022, our working capital balance was $2,325,029. In assessing our liquidity, management monitors and analyzes our cash, our ability to generate sufficient revenue in the future, and our operating and capital expenditure commitments. We believe that our current cash and cash flows provided by operating activities, borrowings from banks and from our principal shareholders, and other capital raising contracts including the standby equity purchase agreement will be sufficient to meet our working capital needs in the next 12 months from the date the audited financial statements were issued. Even though we face uncertainties with regards to the size and timing of capital-raising, we are confident that we can continue to meet operational needs solely by utilizing cash flows generated from our operating activities and shareholder working capital funding, as necessary.

Cash Flows for the Years Ended December 31, 2022 and 2021

The following table sets forth summary of our cash flows for the periods indicated:

| For the Years Ended December 31, |

||||||||

| 2022 | 2021 | |||||||

| Net cash provided by (used in) operating activities |

$ | (16,865,274 | ) | $ | (10,119,103 | ) | ||

| Net cash provided by (used in) investing activities |

(344,964 | ) | 293,303 | |||||

| Net cash provided by (used in) financing activities |

9,579,119 | 6,380,047 | ||||||

| Effect of exchange rate changes |

(1,111,314 | ) | (1,603,633 | ) | ||||

| Net increase (decrease) in cash and cash equivalents |

(7,631,119 | ) | (3,284,283 | ) | ||||

| Cash and cash equivalents, beginning of the year |

10,020,459 | 14,619,164 | ||||||

|

|

|

|

|

|||||

| Cash and cash equivalents, end of the year |

$ | 1,278,026 | $ | 10,020,459 | ||||

|

|

|

|

|

|||||

Operating Activities

Net cash used in operating activities was $16,865,274 for the year ended December 31, 2022, primarily consisting of the following:

| • | Net loss of $14,479,819 for the fiscal year. |

| • | Depreciation expenses of $327,576. |

| • | An increase in inventory of $2,483,254, as raw materials increased to prepare for manufacturing hoverbikes. |

| • | Gain on sale of investment securities of $1,801,660. |

8

Net cash used in operating activities was $10,119,103 for the year ended December 31, 2021, primarily consisting of the following:

| • | Net loss of $14,527,021 for the fiscal year. |

| • | Depreciation expenses of $193,812. |

| • | A decrease in accounts receivable of $3,289,638, as the relevant sales increased from the prior year |

| • | Gain on disposal of business of $580,177. |

Investing Activities

Net cash used by investing activities amounted to $344,964 for the year ended December 31, 2022, and primarily included purchase of fixed assets of $950,500, purchase of investment securities of $575,000 and proceeds from disposal of investments of $1,189,725.

Net cash provided by investing activities amounted to $293,303 for the year ended December 31, 2021, and primarily included purchase of fixed assets of $866,862, proceeds from disposal of a subsidiary of $473,123 and proceeds from disposal of a business of $819,352.

Financing Activities

Net cash provided by financing activities amounted to $9,579,119 for the fiscal year ended December 31, 2022, primarily consisting of proceeds from capital contribution of $9,834,302 and repayments to loans of $171,384.

Net cash provided by financing activities amounted to $6,380,047 for the fiscal year ended December 31, 2021, primarily consisting of proceeds from issuance of bonds of $7,524,383 and proceeds from loans of $1,165,937 and repayment to loans of $2,262,294.

Contractual obligations

Lease commitment

The Company’s subsidiary, A. L. I. Technologies entered into 13 leases for its office space, multi-function printers and a vehicle, which were classified as operating leases. A. L. I. Technologies also entered into two leases for containers, and these leases were classified as finance leases.

As of December 31, 2022, future minimum lease payments under the non-cancelable lease agreements are as follows:

| Year ending December 31, |

Finance lease |

Operating lease |

||||||

| 2023 |

$ | 105,775 | $ | 298,580 | ||||

| 2024 |

54,888 | 244,125 | ||||||

| 2025 |

11,271 | 157,099 | ||||||

| 2026 |

11,271 | — | ||||||

| Thereafter |

14,088 | — | ||||||

|

|

|

|

|

|||||

| Total lease payments |

197,293 | 699,804 | ||||||

| Less: imputed interest |

(8,123 | ) | (8,374 | ) | ||||

|

|

|

|

|

|||||

| Total lease liabilities |

189,170 | 691,430 | ||||||

| Less: current portion |

102,114 | 293,710 | ||||||

|

|

|

|

|

|||||

| Non-current lease liabilities |

$ | 87,056 | $ | 397,720 | ||||

|

|

|

|

|

|||||

9

Long Term Debt

The Company’s long-term debts included bond payable and loans borrowed from banks and other financial institutions.

As of December 31, 2022, future minimum loan payments are as follows:

| Year ending December 31, | Loan Payment |

|||

| 2023 |

$ | 77,930 | ||

| 2024 |

332,900 | |||

| 2025 |

354,339 | |||

| 2026 |

2,240,117 | |||

| 2027 |

341,942 | |||

| Thereafter |

23,352 | |||

|

|

|

|||

| Total |

3,370,580 | |||

|

|

|

|||

| Less interest |

56,719 | |||

|

|

|

|||

| Balance as of December 31, 2022 |

$ | 3,313,861 | ||

|

|

|

|||

Off-Balance Sheet Arrangements

We did not have any off-balance sheet arrangements as of December 31, 2022 and 2021.

Critical Accounting Policies and Estimates

Our discussion and analysis of our financial condition and results of operations are based upon our consolidated financial statements. These financial statements are prepared in accordance with U.S. GAAP, which requires us to make estimates and assumptions that affect the reported amounts of our assets and liabilities and revenue and expenses, to disclose contingent assets and liabilities on the date of the consolidated financial statements, and to disclose the reported amounts of revenue and expenses incurred during the financial reporting period. The most significant estimates and assumptions include the valuation of accounts receivable, advances to suppliers, useful lives of property and equipment, the recoverability of long-lived assets, provision necessary for contingent liabilities, and revenue recognition. We continue to evaluate these estimates and assumptions that we believe to be reasonable under the circumstances. We rely on these evaluations as the basis for making judgments about the carrying values of assets and liabilities that are not readily apparent from other sources. Since the use of estimates is an integral component of the financial reporting process, actual results could differ from those estimates. Some of our accounting policies require higher degrees of judgment than others in their application. We believe critical accounting policies as disclosed in this prospectus reflect the more significant judgments and estimates used in preparation of our consolidated financial statements.

The following critical accounting policies rely upon assumptions and estimates and were used in the preparation of our consolidated financial statements:

Use of Estimates

In preparing the consolidated financial statements in conformity U.S. GAAP, the management is required to make certain estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. These estimates are based on information available as of the date of the consolidated financial statements. Significant estimates required to be made by management include, but are not limited to, the allowance for doubtful accounts, useful lives of property and equipment, the impairment of long- lived assets, valuation allowance of deferred tax assets, and revenue recognition. Actual results could differ from those estimates.

10

Accounts Receivable

Accounts receivable, net represent the amounts that the Company has an unconditional right to consideration, which are stated at the original amount less an allowance for doubtful receivables. The Company reviews the accounts receivable on a periodic basis and makes general and specific allowances when there is doubt as to the collectability of individual balances. The Company usually determines the adequacy of reserves for doubtful accounts based on individual account analysis and historical collection trends. The Company establishes a provision for doubtful receivables when there is objective evidence that the Company may not be able to collect amounts due. The allowance is based on management’s best estimates of specific losses on individual exposures, as well as a provision on historical trends of collections. The provision is recorded against accounts receivables balances, with a corresponding charge recorded in the consolidated statements of income and comprehensive income. Delinquent account balances are written off against the allowance for doubtful accounts after management has determined that the likelihood of collection is remote. In circumstances in which the Company receives payment for accounts receivable that have previously been written off, the Company reverses the allowance and bad debt.

Lease-Lessee

In accordance with the Accounting Standards Update (“ASU”) 2016-02 Leases (Topic 842), the Company determines whether a contract is or contains a lease at inception of the contract and whether that lease meets the classification criteria of a finance or operating lease. Lease terms of certain operating leases include the non-cancellable period for which the Company has the right to use the underlying asset, together with renewal option periods when the exercise of the renewal option is reasonably certain.

11

The Company leases office facilities, which are classified as operating leases and leases office equipment and furniture, and a vehicle, which are classified as a finance lease in accordance with Topic 842. Under Topic 842, lessees are required to recognize the following for all leases on the commencement date: (i) lease liability, which is a lessee’s obligation to make lease payments arising from a lease, measured on a discounted basis; and (ii) right-of-use asset, which is an asset that represents the lessee’s right to use, or control the use of, a specified asset for the lease term. Operating leases are included in operating lease right-of-use assets, operating lease liabilities, current, and operating lease liabilities, non-current, and finance leases are included in property and equipment, finance lease liabilities, current, and finance lease liabilities, non-current in the consolidated balance sheet.

As most of the Company’s leases do not provide an implicit rate, the Company uses its incremental borrowing rate based on the information available at commencement date in determining the present value of future payments.

The Company has elected the short-term lease exception, and therefore operating lease right-of-use assets and liabilities do not include leases with a lease term of twelve months or less.

Foreign Currency Translation

The Company maintains its books and record in its local currency, Japanese YEN (“JPY”), which is a functional currency as being the primary currency of the economic environment in which its operation is conducted. Transactions denominated in currencies other than the functional currency are translated into the functional currency at the exchange rates prevailing at the dates of the transaction. Monetary assets and liabilities denominated in currencies other than the functional currency are translated into the functional currency using the applicable exchange rates at the balance sheet dates. The resulting exchange differences are recorded in the statements of operations.

The reporting currency of the Company is the United States Dollars (“US$”), and the accompanying consolidated financial statements have been expressed in US$. In accordance with ASC Topic 830-30, “Translation of Financial Statements”, assets and liabilities of the Company whose functional currency is not US$ are translated into US$, using the exchange rate on the balance sheet date. Revenues and expenses are translated at average rates prevailing during the period. The gains and losses resulting from the translation of financial statements are recorded as a separate component of accumulated other comprehensive loss within the statements of changes shareholders’ deficit.

Translation of amounts from the local currency of the Company into US$1 has been made at the following exchange rates:

| December 31, 2022 |

December 31, 2021 |

|||||||

| Current JPY: US$1 exchange rate |

131.81 | 115.17 | ||||||

| Average JPY: US$1 exchange rate |

131.46 | 109.84 | ||||||

Revenue Recognition

The Company recognize revenue under ASC 606, “Revenue from Contracts with customers”.

To determine revenue recognition for contracts with customers, the Company performs the following five steps : (i) identify the contract(s) with the customer, (ii) identify the performance obligations in the contract, (iii) determine the transaction price, including variable consideration to the extent that it is probable that a significant future reversal will not occur, (iv) allocate the transaction price to the respective performance obligations in the contract, and (v) recognize revenue when (or as) the Company satisfies the performance obligation. Revenue amount represents the invoiced value, net of a value-added tax (“Consumption Tax”) and applicable local government levies. The Consumption Tax on sales is calculated at 8% before October 1, 2020, and 10% afterwards of gross sales.

12

The Company currently generates its revenue from the following main sources:

Revenue from Sales of Computing Equipment

Revenues from the sale of equipment are recognized at the point in time when obligations under the terms of a contract with our customer are satisfied and control has been transferred to the customer. For equipment placements that require us to install the product at the customer location, revenue is normally recognized when the equipment has been delivered and installed at the customer location. Sales of customer installable products are recognized upon shipment or receipt by the customer according to the customer’s shipping terms.

Revenue from Computing Power Sharing services with Equipment Installation

The Company provides customers with computing power sharing services with equipment installation, which includes a one-time equipment installation and a certain period of time technology service. The Company recognizes revenue from one-time equipment installation at the point in time when the installation is completed and accepted by the customer. The Company recognizes revenue from technology service over time when the service is rendered and accepted by the customer, normally monthly.

Revenue from Computing Power Sharing services without Equipment Installation

The Company also provides customers with computing power sharing services without equipment installation, which includes a one-time platform set up without equipment installation, and a certain period of time technology service. The Company recognizes revenue from one-time platform set up at the point in time when the platform is set up to function and accepted by the customer. The Company recognizes revenue from technology service over time when the service is rendered and accepted by the customer, normally monthly.

Revenue from Air Mobility Drone Solution

The Company provides customers with air mobility drone solution, which includes UAS (Unmanned Aircraft Systems) main equipment, laser scanner, software package, camera system, etc. The solution includes a one-time system set up and a certain period of time technology service. The Company recognizes revenue from one-time system set up at the point in time when the system is set up to function and accepted by the customer. The Company recognize revenue from technology service over time when the service is rendered and accepted by the customer, normally monthly.

Revenue from Project Management

The Company provides customers with project management, which includes project planning and implement, and providing needed technology human resources, such as construction engineers and software engineers for various projects. The Company recognizes revenue from project management over time when the service is rendered and accepted by the customer, normally monthly.

Revenue from Outsourcing Service

The Company provides customers with outsourcing service of temporary staffing for construction or technology industries. The Company recognizes revenue from outsourcing over time as the service is rendered.

13

Disaggregation of Revenue

The Company disaggregates its revenues from contracts by service types, as the Company believes it best depicts how the nature, amount, timing and uncertainty of the revenue and cash flows are affected by economic factors. The Company’s disaggregation of revenues for the years ended December 31, 2022 and 2021 is as following:

| For the Years Ended | ||||||||

| December 31, | ||||||||

| 2022 | 2021 | |||||||

| Revenue from Sales of Computing Equipment |

$ | 894,736 | $ | 879,164 | ||||

| Revenue from Computing Power Sharing services |

1,092,012 | 2,166,953 | ||||||

| Revenue from Project Management for Computing Share |

595,745 | 2,172,421 | ||||||

| Revenue from Air Mobility Drone Solution |

797,396 | 822,078 | ||||||

| Revenue from Project Management |

1,727,601 | 1,507,409 | ||||||

| Other |

100,000 | 282,105 | ||||||

|

|

|

|

|

|||||

| Total Revenue |

$ | 5,207,490 | $ | 7,830,130 | ||||

|

|

|

|

|

|||||

As of December 31, 2022 and 2021, and for the years then ended, almost all the revenue generated are attributed to the Company’s operation in Japan.

Share-based Compensation

The Company accounts for share-based compensation awards in accordance with ASC 718, “Compensation – Stock Compensation”. The cost of services received from employees and non-employees in exchange for awards of equity instruments is recognized in the consolidated statement of operations based on the estimated fair value of those awards on the grant date and amortized on a straight-line basis over the requisite service period or vesting period. The Company records forfeitures as they occur.

14