Exhibit 99.1

Condensed Interim Consolidated

Financial Statements

For the three and nine months ended July 31, 2022 and 2021

(Stated in thousands of Canadian dollars, except share and per share amounts)

(Unaudited)

|

| High Tide Inc. |

Condensed Interim Consolidated Financial Statement | |

For the three and nine months ended July 31, 2022 and 2021 |

Condensed Interim Consolidated Financial Statements for the three and nine months ended July 31, 2022 and 2021.

The accompanying unaudited condensed interim consolidated financial statements of High Tide Inc. (“High Tide” or the “Company”) have been prepared by and are the responsibility of the Company’s management and have been approved by the Audit Committee and Board of Directors of the Corporation.

Approved on behalf of the Board:

(Signed) “Harkirat (Raj) Grover” | (Signed) “Nitin Kaushal” |

President and Chair of the Board | Director and Chair of the Audit Committee |

|

| High Tide Inc. |

Condensed Interim Consolidated Statements of Financial Position | |

As at July 31, 2022 and October 31, 2021 (Unaudited – In thousands of Canadian dollars) |

| | | | | | |

|

| Notes |

| 2022 |

| 2021 |

| | | | $ | | $ |

| | | | | | |

Assets | | | | | | |

Current assets | | | | | | |

Cash and Cash Equivalents | | | | 18,321 | | 14,014 |

Marketable securities | | 18 | | 419 | | 860 |

Trade and other receivables | | 9 | | 13,542 | | 7,175 |

Inventory | | | | 23,539 | | 17,042 |

Prepaid expenses and deposits | | 7 | | 7,753 | | 6,919 |

Current portion of loans receivable | | 8 | | 568 | | 277 |

Total current assets | | | | 64,142 | | 46,287 |

Non-current assets | | | | | | |

Loans receivable | | 8 | | - | | 2,720 |

Property and equipment | | 5 | | 28,841 | | 24,756 |

Net investment - lease | | 21 | | 203 | | 506 |

Right-of-use assets, net | | 21 | | 31,061 | | 27,985 |

Long term prepaid expenses and deposits | | 7 | | 3,346 | | 1,681 |

Intangible assets and goodwill | | 3,6 | | 182,066 | | 142,280 |

Total non-current assets | | | | 245,517 | | 199,928 |

Total assets | | | | 309,659 | | 246,215 |

Liabilities | | | | | | |

Current liabilities | | | | | | |

Accounts payable and accrued liabilities | | | | 22,813 | | 18,532 |

Notes payable current | | 11 | | 11,231 | | 5,600 |

Current portion of convertible debentures | | 12 | | - | | 946 |

Current portion of lease liabilities | | 21 | | 7,405 | | 5,729 |

Current portion of derivative liability | | 3,10 | | 10,763 | | 9,980 |

Total current liabilities | | | | 52,212 | | 40,787 |

Non-current liabilities | | | | | | |

Notes payable | | 11 | | 12,049 | | 11,893 |

Convertible debentures | | 12 | | 7,022 | | 7,217 |

Lease liabilities | | 21 | | 25,482 | | 24,044 |

Derivative liability | | 3,10 | | - | | 1,693 |

Deferred tax liability | | | | 10,393 | | 8,577 |

Total non-current liabilities | | | | 54,946 | | 53,424 |

Total liabilities | | | | 107,158 | | 94,211 |

Shareholders’ equity | | | | | | |

Share capital | | 14 | | 272,805 | | 208,904 |

Warrants | | 16 | | 16,501 | | 10,724 |

Contributed surplus | | | | 21,044 | | 15,162 |

Convertible debentures – equity | | | | 647 | | 859 |

Accumulated other comprehensive loss | | | | (25) | | (648) |

Accumulated deficit | | | | (115,408) | | (87,792) |

Equity attributable to owners of the Company | | | | 195,564 | | 147,209 |

Non-controlling interest | | 23 | | 6,937 | | 4,795 |

Total shareholders’ equity | | | | 202,501 | | 152,004 |

Total liabilities and shareholders’ equity | | | | 309,659 | | 246,215 |

3 |

| High Tide Inc. |

Condensed Interim Consolidated Statements of Loss and Comprehensive Loss | |

For the three and nine months ended July 31, 2022 and 2021 (Unaudited – In thousands of Canadian dollars) |

|

| |

| Three months ended |

| Nine months ended | | ||||

| | | | | | | | | | | |

| | Notes | | 2022 |

| 2021 |

| 2022 |

| 2021 | |

| | | | $ | | $ | | $ | | $ | |

| |

| |

| |

| |

| |

| |

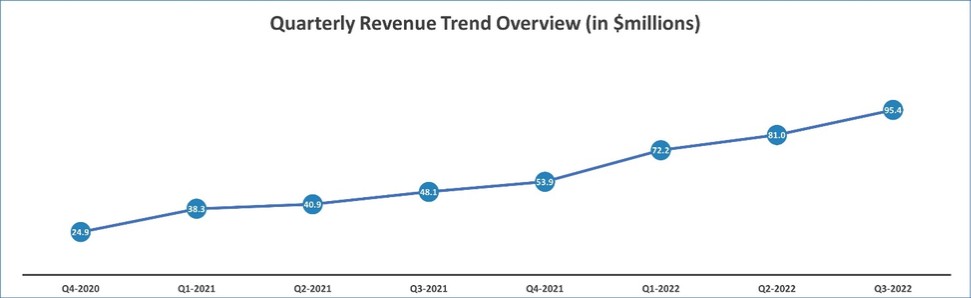

Revenue |

| 4 |

| 95,354 |

| 48,069 |

| 248,604 | | 127,256 | |

Cost of sales |

| | | (69,599) |

| (31,390) |

| (177,170) |

| (80,811) | |

Gross profit |

| | | 25,755 |

| 16,679 |

| 71,434 |

| 46,445 | |

Expenses |

|

|

| | | |

|

|

|

| |

Salaries, wages and benefits |

| | | (11,453) |

| (7,318) |

| (30,933) |

| (19,373) | |

Share-based compensation |

| 15 |

| (1,734) |

| (508) |

| (5,988) |

| (2,578) | |

General and administration |

| | | (6,267) |

| (5,316) |

| (18,798) |

| (11,259) | |

Professional fees |

| | | (1,170) |

| (721) |

| (3,249) |

| (2,391) | |

Advertising and promotion |

| | | (1,871) |

| (1,364) |

| (6,368) |

| (1,679) | |

Depreciation and amortization |

| 5,6,21 |

| (7,182) |

| (8,299) |

| (21,920) |

| (22,107) | |

Interest and bank charges |

| | | (748) |

| (420) |

| (2,483) |

| (881) | |

Total expenses |

| | | (30,425) |

| (23,946) |

| (89,739) |

| (60,268) | |

Loss from operations |

| | | (4,670) |

| (7,267) |

| (18,305) |

| (13,823) | |

Other income (expenses) |

| |

|

|

|

|

|

|

|

| |

Gain on disposal of assets | | | | - | | 2,997 | | - | | 2,997 | |

Gain on financial liability |

| |

| (784) |

| - |

| (784) |

| - | |

Debt restructuring gain |

| |

| - |

| - |

| - |

| 1,145 | |

Impairment loss | | | | - | | (57) | | (89) | | (57) | |

Gain (loss) on extinguishment of debenture | | | | 140 | | - | | 255 | | (516) | |

Loss on revaluation of marketable securities | | | | (146) | | (112) | | (409) | | (256) | |

Finance and other costs |

| 13 | | (2,484) |

| (3,034) |

| (7,154) |

| (11,044) | |

Gain (loss) on revaluation of derivative liability |

| |

| 6,078 |

| 5,919 |

| 7,331 |

| (8,553) | |

Foreign exchange loss (gain) |

| | | (120) |

| 28 |

| (324) |

| (66) | |

Total other income (expenses) |

| | | 2,684 |

| 5,741 |

| (1,174) |

| (16,350) | |

Loss before taxes |

| | | (1,986) |

| (1,526) |

| (19,479) |

| (30,173) | |

Income tax (expense) recovery |

| | | (731) |

| (224) |

| 1,133 |

| (688) | |

Net loss |

| | | (2,717) |

| (1,750) |

| (18,346) |

| (30,861) | |

Other comprehensive loss |

| | |

|

|

|

|

|

|

| |

Translation difference on foreign subsidiary |

| | | 1,095 |

| 4 |

| 623 |

| 86 | |

Total comprehensive loss |

| | | (1,622) |

| (1,746) |

| (17,723) |

| (30,775) | |

Comprehensive (loss) income attributable to: |

| | |

|

|

|

|

|

|

| |

Owners of the Company |

| | | (1,920) |

| (1,677) |

| (18,667) |

| (30,797) | |

Non-controlling interest |

| | | 298 |

| (69) |

| 944 |

| 22 | |

|

| | | (1,622) |

| (1,746) |

| (17,723) |

| (30,775) | |

Loss per share |

|

|

|

|

|

|

|

|

|

| |

Basic and diluted |

| 17 |

| (0.04) |

| (0.03) |

| (0.31) |

| (0.79) | |

Subsequent events (Note 24)

4 |

| High Tide Inc. |

Condensed Interim Consolidated Statements of Changes in Equity | |

For the nine months ended July 31, 2022 and 2021 (Unaudited – In thousands of Canadian dollars) |

|

| |

| |

| |

| |

| Equity |

| Accumulated | | |

|

|

|

|

|

|

| | | | | | | | | | portion of | | other | | | | Attributable | | | | |

| | | | | | | | Contributed | | convertible | | comprehensive | | Accumulated | | to owners of | |

| |

|

| | Note | | Share capital | | Warrants | | surplus | | debt | | income (loss) | | deficit | | the Company | | NCI | | Total |

|

| |

| $ |

| $ |

| $ |

| $ |

| $ | | $ |

| $ |

| $ |

| $ |

Opening balance, November 1, 2020 |

| |

| 32,552 |

| 5,796 |

| 4,704 |

| 1,965 |

| (487) | | (34,359) |

| 10,171 |

| 1,552 |

| 11,723 |

Acquisition - Meta Growth |

| 3 |

| 35,290 |

| 2,739 |

| 240 |

| 9,008 |

| - | | - |

| 47,277 |

| 1,821 |

| 49,098 |

Acquisition - Smoke Cartel, Inc. |

| 3 |

| 8,396 |

| - |

| - |

| - |

| - | | - |

| 8,396 |

| - |

| 8,396 |

Acquisition - Fab Nutrition, LLC. |

| 3 |

| 9,243 |

| - |

| - |

| - |

| - | | (4,535) |

| 4,708 |

| 988 |

| 5,696 |

Acquisition - DHC Supply LLC |

| 3 |

| 7,751 |

| - |

| - |

| - |

| - | | - |

| 7,751 |

| - |

| 7,751 |

Sale of controlling interest |

| 6 |

| - |

| - |

| - |

| - |

| - | | - |

| - |

| (892) |

| (892) |

Prepaid Interest paid in shares | | | | 1,458 |

| - |

| - |

| - |

| - | | - |

| 1,458 |

| - |

| 1,458 |

Share-based compensation | | 15 | | - |

| - |

| 2,578 |

| - |

| - | | - |

| 2,578 |

| - |

| 2,578 |

Equity portion of convertible debentures | | | | - |

| - |

| - |

| 157 |

| - | | - |

| 157 |

| - |

| 157 |

Exercise options |

| 15 |

| 1,005 |

| - |

| (179) |

| - |

| - | | - |

| 826 |

| - |

| 826 |

Warrants expired |

| 16 |

| - |

| (5,394) |

| 5,394 |

| - |

| - | | - |

| - |

| - |

| - |

Issued to pay fees in shares |

| |

| 468 |

| - |

| - |

| - |

| - | | - |

| 468 |

| - |

| 468 |

Extension of convertible debenture |

| |

| - |

| - |

| 340 |

| - |

| - | | - |

| 340 |

| - |

| 340 |

Conversion of convertible debentures |

| |

| 43,317 |

| - |

| - |

| (9,661) |

| - | | - |

| 33,656 |

| - |

| 33,656 |

Warrants exercised | | 16 | | 15,045 |

| (1,676) |

| 28 |

| - |

| - | | - |

| 13,397 |

| - |

| 13,397 |

Cumulative translation adjustment | | | | - |

| - |

| - |

| - |

| 86 | | - |

| 86 |

| - |

| 86 |

Shares and warrants issued through equity financing | | | | 38,447 |

| 10,022 |

| - |

| - |

| - | | - |

| 48,469 |

| - |

| 48,469 |

Share issuance costs | | | | (5,535) |

| - |

| - |

| - |

| - | | - |

| (5,535) |

| - |

| (5,535) |

Vesting of RSUs (Note 14) | | 15 | | 743 |

| - |

| (743) |

| - |

| - | | - |

| - |

| - |

| - |

Comprehensive loss for the period |

| |

| - |

| - |

| - |

| - |

| - | | (30,883) |

| (30,883) |

| 22 |

| (30,861) |

Balance, July 31, 2021 |

| |

| 188,180 |

| 11,487 |

| 12,362 |

| 1,469 |

| (401) | | (69,777) |

| 143,320 |

| 3,491 |

| 146,811 |

Opening balance, November 1, 2021 |

| |

| 208,904 |

| 10,724 |

| 15,162 |

| 859 |

| (648) | | (87,792) |

| 147,209 |

| 4,795 |

| 152,004 |

Acquisition - FABCBD | | | | 313 | | - | | - | | - | | - | | - | | 313 | | - | | 313 |

Acquisition - NuLeaf |

| 3 |

| 35,527 | | - | | - | | - | | - | | (8,326) | | 27,201 | | 2,700 | | 29,901 |

Acquisition - Budroom | | 3 | | 3,738 | | - | | - | | - | | - | | - | | 3,738 | | - | | 3,738 |

Acquisition - Boreal Cannabis | | 3 | | 2,203 | | - | | - | | - | | - | | - | | 2,203 | | - | | 2,203 |

Acquisition - Crossroads Cannabis | | 3 | | 2,189 | | - | | - | | - | | - | | - | | 2,189 | | - | | 2,189 |

Issuance of shares through ATM | | | | 8,307 | | - | | - | | - | | - | | - | | 8,307 | | - | | 8,307 |

Issued to pay fees in shares | | | | 100 | | - | | - | | - | | - | | - | | 100 | | - | | 100 |

Share-based compensation | | 15 | | - | | - | | 5,988 | | - | | - | | - | | 5,988 | | - | | 5,988 |

Equity portion of convertible debentures | | | | - | | - | | - | | (212) | | - | | - | | (212) | | - | | (212) |

Exercise options | | 14 | | 571 | | - | | (261) | | - | | - | | - | | 310 | | - | | 310 |

Warrants expired | | 16 | | - | | (273) | | 273 | | - | | - | | - | | - | | - | | - |

Warrants exercised | | 16 | | 4,052 | | (6) | | - | | - | | - | | - | | 4,046 | | - | | 4,046 |

Share issuance costs | | | | (966) | | - | | - | | - | | - | | - | | (966) | | - | | (966) |

Vesting of RSUs | | | | 118 | | - | | (118) | | - | | - | | - | | - | | - | | - |

Issued warrants |

| |

| - | | 6,056 | | | | - | | - | | - | | 6,056 | | - | | 6,056 |

Acquisition - Budheaven |

| 3 |

| 1,985 | | - | | - | | - | | - | | - | | 1,985 | | - | | 1,985 |

Shares issued through equity financing |

| |

| 5,764 | | - | | - | | - | | - | | - | | 5,764 | | - | | 5,764 |

Partner distributions |

| |

| - | | - | | - | | - | | - | | - | | - | | (1,502) | | (1,502) |

Cumulative translation adjustment |

| |

| - | | - | | - | | - | | 623 | | - | | 623 | | - | | 623 |

Comprehensive (loss) gain for the period |

| |

| - | | - | | - | | - | | - | | (19,290) | | (19,290) | | 944 | | (18,346) |

Balance, July 31, 2022 |

| |

| 272,805 |

| 16,501 |

| 21,044 |

| 647 |

| (25) | | (115,408) |

| 195,564 |

| 6,937 |

| 202,501 |

5 |

| High Tide Inc. |

Condensed Interim Consolidated Statements of Cash Flows | |

For the nine months ended July 31, 2022 and 2021 (Unaudited – In thousands of Canadian dollars, except share and per share amounts) |

| | | | | | |

|

| Notes |

| 2022 |

| 2021 |

| | | | $ | | $ |

Operating activities | |

| |

| |

|

Net loss |

| |

| (18,346) |

| (30,861) |

Adjustments for items not effecting cash and cash equivalents |

| |

| | | |

Income tax (recovery) expense |

| |

| (1,133) |

| 688 |

Accretion expense |

| 13 |

| 3,951 |

| 4,575 |

Fee for services and interest paid in shares and warrants |

| 16 |

| - |

| 1,926 |

Depreciation and amortization |

| 5,6,21 |

| 21,920 |

| 22,107 |

Revaluation of derivative liability |

| 3, 12, 16 |

| (7,331) |

| 8,553 |

Gain (loss) on extinguishment of debenture | | | | (255) |

| 516 |

Debt restructuring gain |

| |

| - |

| (1,145) |

Impairment loss |

| |

| 89 |

| 57 |

Foreign exchange loss |

| |

| 324 |

| 66 |

Share-based compensation |

| 15 |

| 5,988 |

| 2,578 |

Gain on sale of marketable securities |

| |

| - |

| (2,997) |

Revaluation of marketable securities |

| |

| 408 |

| 256 |

|

| |

| 5,615 |

| 6,319 |

Changes in non-cash working capital |

| |

|

|

|

|

Trade and other receivables |

| |

| (6,130) |

| (944) |

Inventory |

| |

| (4,156) |

| (3,973) |

Loans receivable | | | | (2,429) |

| (161) |

Prepaid expenses and deposits |

| |

| (2,194) |

| (390) |

Accounts payable and accrued liabilities |

| |

| 5,518 |

| (8,687) |

Net cash used in operating activities |

| |

| (3,776) |

| (7,836) |

|

| | | | | |

Investing activities |

| |

|

|

|

|

Net additions of property and equipment |

| 5 |

| (6,880) |

| (6,206) |

Net additions of intangible assets |

| 6 |

| (1,060) |

| (124) |

Purchase of marketable securities | | | | - | | 2,300 |

Cash acquired through business combinations, net |

| 3 |

| 616 |

| (14,172) |

Net cash used in investing activities |

| |

| (7,324) |

| (18,202) |

|

| | | | | |

Financing activities |

| |

|

|

|

|

Repayment of finance lease obligations |

| |

| - |

| (11) |

Proceeds from convertible debentures net of issue costs |

| 12 |

| - |

| 1,273 |

Proceeds from notes payable net of issue costs and repayment | | 11 | | 9,500 |

| - |

Repayment of notes payable | | | | (4,040) | | - |

Repayment of convertible debentures |

| |

| (2,325) |

| (3,813) |

Proceeds from equity financing | | | | 10,645 |

| 43,250 |

Interest paid on debentures and loans |

| |

| (932) |

| (985) |

Lease liability payments |

| 21 |

| (7,232) |

| (5,270) |

Share issuance costs | | | | (966) |

| - |

Proceeds from equity financing through ATM | | | | 8,307 |

| - |

Warrants exercised |

| 16 |

| 2,141 |

| 9,885 |

Options exercised |

| |

| 309 |

| 825 |

Net cash provided by financing activities |

| |

| 15,407 |

| 45,154 |

|

| | | | | |

Net increase in cash |

| |

| 4,307 |

| 19,116 |

Cash, beginning of period |

| |

| 14,014 |

| 7,524 |

Cash, end of period |

| |

| 18,321 |

| 26,640 |

6 |

| High Tide Inc. |

Notes to the Condensed Interim Consolidated Financial Statements | |

For the three and nine months ended July 31, 2022 and 2021 (Unaudited – In thousands of Canadian dollars, except share and per share amounts) |

1. | Nature of Operations |

High Tide Inc. (the “Company” or “High Tide”) is a retail-focused cannabis company with bricks-and-mortar as well as global e-commerce assets. The Company’s shares are listed on the Nasdaq Capital Market (“Nasdaq”) under the symbol “HITI”(listed as of June 2, 2021), the TSX Venture Exchange (“TSXV”) under the symbol “HITI”, and on the Frankfurt Stock Exchange (“FSE”) under the securities identification code ‘WKN: A2PBPS’ and the ticker symbol “2LYA”. The address of the Company’s corporate and registered office is # 120 – 4954 Richard Road SW, Calgary, Alberta T3E 6L1.

High Tide does not engage in any U.S. cannabis-related activities as defined by the Canadian Securities Administrators Staff Notice 51-352.

COVID-19

The Company’s business could be adversely affected by the effects of the outbreak of novel coronavirus (“COVID-19”). Several significant measures have been implemented in Canada and the rest of the world in response to the increased impact from COVID-19. The Company cannot accurately predict the impact COVID-19 will have on third parties’ ability to meet their obligations with the Company, including due to uncertainties relating to the ultimate geographic spread of the virus, the severity of the disease, the duration of the outbreak, and the length of travel and quarantine restrictions imposed by governments of affected countries. In particular, the continued spread of COVID-19 globally could materially and adversely impact the Company’s business including without limitation, employee health, workplace productivity, and other factors that will depend on future developments beyond the Company’s control. In addition, a significant outbreak of contagious diseases in the human population could result in a widespread health crisis that could adversely affect the economies and financial markets of many countries resulting in an economic downturn that could negatively impact the Company’s financial position, financial performance, cash flows, and its ability to raise capital. Since the initial outset of the pandemic, the Company did not experience a significant decline in sales for most of the operating businesses.

2. | Accounting Policies |

A. | Basis of Preparation |

These condensed interim consolidated financial statements (“Financial Statements”) have been prepared in accordance with International Accounting Standard (“IAS”) 34 Interim Financial Reporting as issued by the International Accounting Standards Board (“IASB”). They are condensed as they do not include all of the information required for full annual financial statements, and they should be read in conjunction with the audited consolidated financial statements of the Company for the year ended October 31, 2021 which are available on SEDAR at www.sedar.com.

For comparative purposes, the Company has reclassified certain immaterial items on the comparative condensed interim consolidated statements of financial position and the condensed interim consolidated statements of loss and comprehensive loss to conform with current period’s presentation.

On May 13, 2021, the Company completed a one-for-fifteen (1:15) reverse share split of all of its issued and outstanding common shares (“Share Consolidation”), resulting in a reduction in the issued and outstanding shares from 690,834,719 to 46,055,653. Shares reserved under the Company’s equity and incentive plans were adjusted to reflect the Share Consolidation.

These condensed interim consolidated financial statements were approved and authorized for issue by the Board of Directors on September 14, 2022.

7 |

| High Tide Inc. |

Notes to the Condensed Interim Consolidated Financial Statements | |

For the three and nine months ended July 31, 2022 and 2021 (Unaudited – In thousands of Canadian dollars, except share and per share amounts) |

B. | Use of estimates |

The estimates and assumptions are reviewed on an ongoing basis. Revisions in accounting estimates are recognized in the year in which the estimate is revised if the revision affects only that year, or in the year of the revision and future years if the revision affects both current and future years. Significant judgements, estimates, and assumptions within these condensed interim consolidated financial statements remain the same as those applied to the consolidated financial statements for the year ended October 31, 2021.

C. | Accounting Policies |

The significant accounting policies applied in the preparation of the unaudited condensed interim consolidated financial statements for the three and nine months ended July 31, 2022, and 2021 are consistent with those applied and disclosed in Note 3 and 4 of the Company’s Consolidated Financial Statements for the years ended October 31, 2021 and 2020.

As a result of activities during the nine month period ended July 31, 2022, the following policies have been updated:

Inventory

Inventories are measured at the lower of cost and net realizable value. The cost of inventories is accounted for as follows:

Raw materials, work in progress and finished goods that arise from the extraction process under NuLeaf include raw materials and manufacturing overheads. Raw materials are calculated on a weighted average cost basis and include expenditures incurred in acquiring the inventories and other costs incurred in bringing them to their existing location and condition. Manufacturing overheads such as labour and other manufacturing expenditures are overheads based on the normal operating capacity.

Finished goods purchased from third parties are measured at the lower of cost and net realizable value. The cost of inventories is calculated on a weighted average cost basis and include expenditures incurred in acquiring the inventories and other costs incurred in bringing them to their existing location and condition.

Net realizable value is the estimated selling price in the ordinary course of business, less the estimated costs of completion and costs necessary to make the sale. The Company reviews inventory for obsolete, redundant, and slow-moving inventory items and any such items are written down to net realizable value. Any write-downs of inventory to net realizable value are recorded in consolidated statement of loss and other comprehensive loss of the related year.

8 |

| High Tide Inc. |

Notes to the Condensed Interim Consolidated Financial Statements | |

For the three and nine months ended July 31, 2022 and 2021 (Unaudited – In thousands of Canadian dollars, except share and per share amounts) |

3. | Business Combinations |

In accordance with IFRS 3, Business Combinations, these transactions meet the definition of a business combination and, accordingly, the assets acquired, and the liabilities assumed have been recorded at their respective estimated fair values as of the acquisition date.

A. NuLeaf Naturals, LLC Acquisition

Total consideration |

| $ |

Common shares | | 35,527 |

|

| 35,527 |

Purchase price allocation |

|

|

Cash and cash equivalents |

| 565 |

Accounts receivable | | 216 |

Other receivables | | 21 |

Inventory | | 2,341 |

Prepaid expenses | | 305 |

Property, plant and equipment | | 4,190 |

Right of use asset | | 3,144 |

Intangible assets - software | | 211 |

Intangible assets - brand |

| 10,168 |

Goodwill |

| 24,728 |

Accounts payable and accrued liabilities |

| (1,450) |

Other liabilities |

| (105) |

Lease liabilities |

| (2,984) |

Deferred tax liability | | (3,123) |

Non-controlling interest |

| (2,700) |

|

| 35,527 |

On November 29, 2021, the Company closed the acquisition of 80% of the outstanding common shares of NuLeaf Naturals LLC. (“NuLeaf”). Pursuant to the terms of the Arrangement, the consideration was comprised of 4,429,809 common shares of High Tide, having an aggregate value of $35,527.

The acquisition agreement also includes a call and put option that could result in the Company acquiring the remaining 20% of common shares in NuLeaf not acquired upon initial acquisition. The Company analyzed the value in the call option and considers it to be at fair value, and therefore has no value related to the acquisition. As the put option is a contractual obligation, it gives rise to a financial liability calculated with reference to the agreement and is discounted to its present value at each reporting date using the discounted cash flow model. The initial obligation under the put option was recorded as a liability with the offset recorded as equity on the Condensed Interim Consolidated Statements of Financial Position, at its fair value at acquisition of $8,326 with an exercise date of May 29, 2023. For the three and nine months ended July 31, 2022, the Company recognized $2,928 and $2,476 as a gain on revaluation of derivative liability in the statement of net loss and comprehensive loss.

In accordance with IFRS 3, Business Combinations (“IFRS 3”), the substance of this transaction constituted a business combination. Management is in the process of gathering the relevant information that existed at the acquisition date to determine the fair value of the net identifiable assets acquired. As such, the initial purchase price was provisionally allocated based on the Company’s estimated fair value of the identifiable assets acquired on the acquisition date. The values assigned are, therefore, preliminary, and subject to change. Management continues to refine and finalize its purchase price allocation for the fair value of working capital, right of use assets, lease liabilities, identifiable intangible assets, income taxes, the allocation of goodwill and the non-controlling interest. The goodwill is primarily related to the opportunities to grow the business, expanded access to capital and greater financial flexibility. For the nine months ended July 31, 2022, NuLeaf accounted for $12,292 in revenues and $132 in net income. If the acquisition had been completed on November 1, 2021, the Company estimates it would have recorded an increase of $1,440 in revenues and a decrease of $722 in net loss for the nine months ended July 31, 2022. The Company also incurred $71 in transaction costs for the nine months ended July 31, 2022, which have been expensed to finance and other costs during the period.

9 |

| High Tide Inc. |

Notes to the Condensed Interim Consolidated Financial Statements | |

For the three and nine months ended July 31, 2022 and 2021 (Unaudited – In thousands of Canadian dollars, except share and per share amounts) |

B. Bud Room Inc.

Total consideration |

| $ |

Common shares | | 3,738 |

|

| 3,738 |

Purchase price allocation |

|

|

Cash and cash equivalents |

| 63 |

Trade and other receivables | | 31 |

Inventory |

| 40 |

Prepaid expenses | | 31 |

Property and equipment |

| 41 |

Leasehold improvements | | 79 |

Goodwill |

| 3,499 |

Right of use asset | | 365 |

Lease liability | | (365) |

Accounts payable and accrued liabilities |

| (46) |

|

| 3,738 |

On February 9, 2022, the Company closed the acquisition of 100% of the outstanding common shares of Bud Room Inc. (“Bud Room”). Pursuant to the terms of the Arrangement, the consideration was comprised of 674,650 common shares of High Tide, having an aggregate value of $3,738 and acquired all rights to the customized Fastendr™ retail kiosk and smart locker technology and Bud Room’s retail cannabis store located at 1910 St. Laurent Blvd in Ottawa, Ontario.

In accordance with IFRS 3, Business Combinations (“IFRS 3”), the substance of this transaction constituted a business combination. Management is in the process of gathering the relevant information that existed at the acquisition date to determine the fair value of the net identifiable assets acquired. As such, the initial purchase price was provisionally allocated based on the Company’s estimated fair value of the identifiable assets acquired on the acquisition date. The values assigned are, therefore, preliminary, and subject to change. Management continues to refine and finalize its purchase price allocation for the fair value of working capital, right of use asset, lease liability, identifiable intangible assets, income tax, the allocation of goodwill. The goodwill is primarily related to the opportunities to grow the business, expanded access to capital and greater financial flexibility. For the nine months ended July 31, 2022, Bud Room accounted for $1,284 in revenues and $93 in net income. If the acquisition had been completed on November 1, 2021, the Company estimates it would have recorded an increase of $613 in revenues and a decrease of $14 in net loss for the nine months ended July 31, 2022.

10 |

| High Tide Inc. |

Notes to the Condensed Interim Consolidated Financial Statements | |

For the three and nine months ended July 31, 2022 and 2021 (Unaudited – In thousands of Canadian dollars, except share and per share amounts) |

C. 2080791 Alberta Ltd.

Total consideration |

| $ |

Cash |

| 200 |

Common shares | | 2,203 |

|

| 2,403 |

Purchase price allocation |

|

|

Cash and cash equivalents |

| 251 |

Inventory |

| 182 |

Prepaid expenses | | 8 |

Property and equipment |

| 161 |

Goodwill |

| 1,829 |

Right of use asset | | 160 |

Lease liability | | (160) |

Accounts payable and accrued liabilities |

| (28) |

|

| 2,403 |

On April 21, 2022, the Company closed the acquisition of 100% of the outstanding common shares of 2080791 Alberta Ltd. operating as Boreal Cannabis Company (“Boreal”) which operates two retail cannabis stores in Alberta. Pursuant to the terms of the Arrangement, the consideration was comprised of $200 in cash and 443,301 common shares of High Tide, having an aggregate value of $2,203.

In accordance with IFRS 3, Business Combinations (“IFRS 3”), the substance of this transaction constituted a business combination. Management is in the process of gathering the relevant information that existed at the acquisition date to determine the fair value of the net identifiable assets acquired. As such, the initial purchase price was provisionally allocated based on the Company’s estimated fair value of the identifiable assets acquired on the acquisition date. The values assigned are, therefore, preliminary, and subject to change. Management continues to refine and finalize its purchase price allocation for the fair value of working capital, right of use assets, lease liabilities, identifiable intangible assets, income taxes, the allocation of goodwill. The goodwill is primarily related to the opportunities to grow the business, expanded access to capital and greater financial flexibility. For the nine months ended July 31, 2022, Boreal accounted for $984 in revenues and $123 in net income. If the acquisition had been completed on November 1, 2021, the Company estimates it would have recorded an increase of $1,861 in revenues and a decrease of $132 in net loss for the nine months ended July 31, 2022. The Company also incurred $5 in transaction costs for the nine months ended July 31, 2022, which have been expensed to finance and other costs during the period.

11 |

| High Tide Inc. |

Notes to the Condensed Interim Consolidated Financial Statements | |

For the three and nine months ended July 31, 2022 and 2021 (Unaudited – In thousands of Canadian dollars, except share and per share amounts) |

D. Crossroads Cannabis

Total consideration |

| $ |

Common shares | | 2,189 |

|

| 2,189 |

Purchase price allocation |

|

|

Cash and cash equivalents |

| 3 |

Inventory |

| 284 |

Property and equipment |

| 233 |

Goodwill |

| 1,296 |

Leasehold Improvements |

| 373 |

Lease liabilities | | (751) |

Right of use assets |

| 751 |

|

| 2,189 |

On April 26, 2022, the Company closed the acquisition of three retail cannabis stores in Ontario operating as Crossroads Cannabis (“Crossroads”). Pursuant to the terms of the Arrangement, the consideration was comprised of 378,079 common shares of High Tide, having an aggregate value of $1,777. On May 17, the Company closed the acquisition of an additional retail cannabis store operating as Crossroads Cannabis, the consideration was comprised of 138,656 common shares of High Tide having an aggregate value of $412.

In accordance with IFRS 3, Business Combinations (“IFRS 3”), the substance of this transaction constituted a business combination. Management is in the process of gathering the relevant information that existed at the acquisition date to determine the fair value of the net identifiable assets acquired. As such, the initial purchase price was provisionally allocated based on the Company’s estimated fair value of the identifiable assets acquired on the acquisition date. The values assigned are, therefore, preliminary, and subject to change. Management continues to refine and finalize its purchase price allocation for the fair value of working capital, right of use assets, lease liabilities, identifiable intangible assets, income taxes, the allocation of goodwill. The goodwill is primarily related to the opportunities to grow the business, expanded access to capital and greater financial flexibility. For the nine months ended July 31, 2022, Crossroads accounted for $1,612 in revenues and $82 in net income. If the acquisition had been completed on November 1, 2021, the Company estimates it would have recorded an increase of $2,569 in revenues and a decrease of $238 in net loss for the nine months ended July 31, 2022. The Company also incurred $30 in transaction costs for the nine months ended July 31, 2022, which have been expensed to finance and other costs during the period.

12 |

| High Tide Inc. |

Notes to the Condensed Interim Consolidated Financial Statements | |

For the three and nine months ended July 31, 2022 and 2021 (Unaudited – In thousands of Canadian dollars, except share and per share amounts) |

E. Ontario Lottery Winner

Total consideration |

| $ |

Cash |

| 116 |

Loan Receivable - Settlement | | 1,383 |

|

| 1,499 |

Purchase price allocation |

|

|

Cash and cash equivalents |

| 7 |

Inventory |

| 221 |

Prepaid Expenses |

| 2 |

Property and equipment |

| 313 |

Goodwill |

| 956 |

|

| 1,499 |

On May 10, 2022, the Company closed the acquisition of two Ontario Lottery Winner retail cannabis locations. Pursuant to the terms of the Arrangement, the consideration was comprised of $116 in cash and settlement of a $1,383 Loan Receivable.

In accordance with IFRS 3, Business Combinations (“IFRS 3”), the substance of this transaction constituted a business combination. Management is in the process of gathering the relevant information that existed at the acquisition date to determine the fair value of the net identifiable assets acquired. As such, the initial purchase price was provisionally allocated based on the Company’s estimated fair value of the identifiable assets acquired on the acquisition date. The values assigned are, therefore, preliminary, and subject to change. Management continues to refine and finalize its purchase price allocation for the fair value of working capital, and the allocation of goodwill. The goodwill is primarily related to the opportunities to grow the business, expanded access to capital and greater financial flexibility. For the nine months ended July 31, 2022, the two locations accounted for $6,093 in revenues and $911 in net loss. If the acquisition had been completed on November 1, 2021, the Company estimates it would have recorded an increase of $2,760 in revenues and a decrease of $176 in net loss for the nine months ended July 31, 2022.

13 |

| High Tide Inc. |

Notes to the Condensed Interim Consolidated Financial Statements | |

For the three and nine months ended July 31, 2022 and 2021 (Unaudited – In thousands of Canadian dollars, except share and per share amounts) |

F. Bud Heaven

Total consideration |

| $ |

Common Shares | | 1,986 |

Cash True-up Payable | | 992 |

|

| 2,978 |

Purchase price allocation |

|

|

Cash and cash equivalents |

| 41 |

Inventory |

| 102 |

Trade and other receivables |

| 13 |

Prepaid Expenses |

| 37 |

Property and equipment | | 240 |

Goodwill | | 2,657 |

Right-of-use-assets |

| 250 |

Lease Liabilities |

| (250) |

Accounts payable and accrued liabilities |

| (112) |

|

| 2,978 |

On June 1, 2022, the Company acquired all of the issued and outstanding shares of Livonit Foods Inc. operating as Bud Heaven (“Bud Heaven”) which operates two retail cannabis stores in Ontario. The consideration was comprised of 564,092 Common Shares, having an aggregate value of $1,986 and a cash true-up payable of $992, due upon settlement of the post-closing working capital adjustment.

In accordance with IFRS 3, Business Combinations (“IFRS 3”), the substance of this transaction constituted a business combination. Management is in the process of gathering the relevant information that existed at the acquisition date to determine the fair value of the net identifiable assets acquired. As such, the initial purchase price was provisionally allocated based on the Company’s estimated fair value of the identifiable assets acquired on the acquisition date. The values assigned are, therefore, preliminary, and subject to change. Management continues to refine and finalize its purchase price allocation for the fair value of working capital, right of use asset, lease liability, identifiable intangible assets, income tax, the allocation of goodwill. The goodwill is primarily related to the opportunities to grow the business, expanded access to capital and greater financial flexibility. For the nine months ended July 31, 2022, Bud Heaven accounted for $790 in revenues and $75 in net loss. If the acquisition had been completed on November 1, 2021, the Company estimates it would have recorded an increase of $2,728 in revenues and a decrease of $676 in net loss for the nine months ended July 31, 2022. The Company also incurred $4 in transaction costs for the nine months ended July 31, 2022, which have been expensed to finance and other costs during the period.

14 |

| High Tide Inc. |

Notes to the Condensed Interim Consolidated Financial Statements | |

For the three and nine months ended July 31, 2022 and 2021 (Unaudited – In thousands of Canadian dollars, except share and per share amounts) |

G. Kensington

Total consideration |

| $ |

Cash |

| 160 |

Loan Receivable - Settlement | | 523 |

|

| 683 |

Purchase price allocation |

|

|

Cash and cash equivalents |

| 2 |

Inventory |

| 21 |

Right-of-use assets | | 199 |

Lease liabilities - non-current | | (199) |

Property and equipment |

| 185 |

Goodwill |

| 475 |

|

| 683 |

On June 4th, 2022, High Tide Inc. (“the Company” or “High Tide”) purchased a licensed cannabis retail store location in Alberta. The consideration was comprised of $160 in cash and settlement of a $523 Loan Receivable.

In accordance with IFRS 3, Business Combinations (“IFRS 3”), the substance of this transaction constituted a business combination. Management is in the process of gathering the relevant information that existed at the acquisition date to determine the fair value of the net identifiable assets acquired. As such, the initial purchase price was provisionally allocated based on the Company’s estimated fair value of the identifiable assets acquired on the acquisition date. The values assigned are, therefore, preliminary, and subject to change. Management continues to refine and finalize its purchase price allocation for the fair value of working capital, right of use asset, lease liability, identifiable intangible assets, income tax, the allocation of goodwill. The goodwill is primarily related to the opportunities to grow the business, expanded access to capital and greater financial flexibility. For the nine months ended July 31, 2022, Kensington accounted for $173 in revenues and $16 in net loss. If the acquisition had been completed on November 1, 2021, the Company estimates it would have recorded an increase of $447 in revenues and a decrease of $156 in net loss for the nine months ended July 31, 2022. The Company also incurred $11 in transaction costs for the nine months ended July 31, 2022, which have been expensed to finance and other costs during the period.

15 |

| High Tide Inc. |

Notes to the Condensed Interim Consolidated Financial Statements | |

For the three and nine months ended July 31, 2022 and 2021 (Unaudited – In thousands of Canadian dollars, except share and per share amounts) |

H. Halo Kushbar

Total consideration |

| $ |

Note Receivable - Settled | | 811 |

|

| 811 |

Purchase price allocation |

|

|

Cash and cash equivalents |

| 160 |

Trade and other receivables |

| 341 |

Inventory |

| 190 |

Prepaid Expenses |

| 14 |

Right-of-use assets | | 718 |

Lease liabilities - non-current | | (718) |

Accounts payable and accrued liabilities |

| (418) |

Property and equipment | | 524 |

|

| 811 |

On July 15, 2022, High Tide took control of the shares of Halo Kushbar Retail Inc (“Halo”), which owns three operating cannabis retail stores in Alberta. The consideration received was a settlement of a convertible promissory note that was revalued to a principal amount of $0.8 million (the “Note”).

In accordance with IFRS 3, Business Combinations (“IFRS 3”), the substance of this transaction constituted a business combination. Management is in the process of gathering the relevant information that existed at the acquisition date to determine the fair value of the net identifiable assets acquired. As such, the initial purchase price was provisionally allocated based on the Company’s estimated fair value of the identifiable assets acquired on the acquisition date. The values assigned are, therefore, preliminary, and subject to change. Management continues to refine and finalize its purchase price allocation for the fair value of working capital, right of use asset, and lease liability. For the half month ended July 31, 2022, Halo accounted for $154 in revenues and $5 in net income. If the acquisition had been completed on November 1, 2021, the Company estimates it would have recorded an increase of $2,524 in revenues and a decrease of $33 in net loss for the nine months ended July 31, 2022.

16 |

| High Tide Inc. |

Notes to the Condensed Interim Consolidated Financial Statements | |

For the three and nine months ended July 31, 2022 and 2021 (Unaudited – In thousands of Canadian dollars, except share and per share amounts) |

I. Meta Growth Corp. Acquisition (Prior year)

Total consideration |

| $ |

Common shares |

| 35,290 |

Conversion feature of convertible debt |

| 9,008 |

Warrants |

| 2,739 |

Options |

| 86 |

Restricted stock units |

| 154 |

|

| 47,277 |

Purchase price allocation |

|

|

Cash and cash equivalents |

| 10,209 |

Trade and other receivables |

| 2,015 |

Inventory |

| 3,547 |

Prepaid expenses |

| 2,479 |

Marketable securities |

| 635 |

Notes receivable |

| 262 |

Property and equipment |

| 6,849 |

Loan receivable |

| 756 |

Intangible assets - license |

| 30,900 |

Right of use asset |

| 12,490 |

Goodwill |

| 32,247 |

Non-controlling interest |

| (1,821) |

Accounts payable and accrued liabilities |

| (6,336) |

Deferred tax liability |

| (1,933) |

Lease liability |

| (12,887) |

Convertible debenture |

| (18,809) |

Notes payable |

| (13,326) |

|

| 47,277 |

On November 18, 2020, the Company closed the acquisition of 100% of the outstanding common shares of Meta Growth Corp (“Meta Growth” or “META”). Pursuant to the terms of the Arrangement, holders of common shares of META (“META Shares“) received 0.824 (the “Exchange Ratio“) High Tide Shares for each META Share held. In total, High Tide acquired 237,941,274 META Shares in exchange for 196,063,610 High Tide Shares pre-consolidation (13,070,907 post-consolidation shares), resulting in former META shareholders holding approximately 45.0% of the total number of issued and outstanding High Tide Shares.

In accordance with IFRS 3, Business Combinations (“IFRS 3”), the substance of this transaction constituted a business combination. Management gathered the relevant information that existed at the acquisition date to determine the fair value of the net identifiable assets acquired. As such, the initial purchase price was allocated based on the Company’s estimated fair value of the identifiable assets acquired on the acquisition date. Management finalized its purchase price allocation for the fair value of identifiable intangible assets, property plant and equipment, right of use asset, non-controlling interest, income taxes and the allocation of goodwill. The goodwill is primarily related to the opportunities to grow the retail cannabis business, expanded access to capital and greater financial flexibility. Goodwill is not deductible for tax purposes. For the year ended October 31, 2021, Meta Growth accounted for $63,016 in revenues and $11,451 in net loss. If the acquisition had been completed on November 1, 2020, the Company estimates it would have recorded an increase of $3,422 in revenues and an increase of $401 in net loss for the year ended October 31, 2021. The Company also incurred $1,359 in transaction costs for the year ended October 31, 2021, which were expensed to finance and other costs during that period.

17 |

| High Tide Inc. |

Notes to the Condensed Interim Consolidated Financial Statements | |

For the three and nine months ended July 31, 2022 and 2021 (Unaudited – In thousands of Canadian dollars, except share and per share amounts) |

J. | Smoke Cartel, Inc. Acquisition (Prior year) |

Total consideration |

| $ |

Cash |

| 2,512 |

Common shares |

| 8,396 |

Contingent consideration |

| 1,319 |

|

| 12,227 |

Purchase price allocation |

|

|

Cash and cash equivalents |

| 1,680 |

Intangible assets - Brand |

| 3,820 |

Intangible assets - Software |

| 7,217 |

Goodwill |

| 2,594 |

Accounts payable and accrued liabilities |

| (1,093) |

Deferred tax liability |

| (1,991) |

|

| 12,227 |

On March 24, 2021, the Company closed the acquisition of 100% of the outstanding common shares of Smoke Cartel Inc. (“Smoke Cartel”). Pursuant to the terms of the Arrangement, the consideration was comprised of: (i) 9,540,754 common shares of High Tide pre-consolidation (636,050 post-consolidation shares), having an aggregate value of $8,396; (ii) $2,512 in cash; and (iii) a contingent consideration depending on certain revenue targets being achieved by December 31, 2021. Contingent consideration of $1,319 was calculated using Monte Carlo simulation due to the uncertain nature of the potential future revenues of the Company. During the year ended October 31, 2021, the Company finalized the future obligation owed and recorded a loss on the contingent consideration of $1,671 through profits and loss.

In accordance with IFRS 3, Business Combinations (“IFRS 3”), the substance of this transaction constituted a business combination. Management finalized its purchase price allocation for the fair value of identifiable intangible assets, income taxes and the allocation of goodwill. The goodwill acquired is primarily related to the opportunities to grow the business, expanded access to capital and greater financial flexibility. Goodwill is not deductible for tax purposes. For the year ended October 31, 2021, Smoke Cartel accounted for $7,535 in revenues and $52 in net loss. If the acquisition had been completed on November 1, 2020, the Company estimates it would have recorded an increase of $5,846 in revenues and a decrease of $743 in net loss for the year ended October 31, 2021. The Company also incurred $97 in transaction costs for the year ended October 31, 2021, which were expensed to finance and other costs during that period.

18 |

| High Tide Inc. |

Notes to the Condensed Interim Consolidated Financial Statements | |

For the three and nine months ended July 31, 2022 and 2021 (Unaudited – In thousands of Canadian dollars, except share and per share amounts) |

K. | 2686068 Ontario Inc. Acquisition (Prior year) |

Total consideration |

| $ |

Cash |

| 5,980 |

|

| 5,980 |

Purchase price allocation |

|

|

Cash and cash equivalents |

| 3 |

Inventory |

| 120 |

Property and equipment |

| 274 |

Intangible assets - license |

| 5,627 |

Right of use asset |

| 1,148 |

Goodwill |

| 1,611 |

Lease liability |

| (1,148) |

Accounts payable and accrued liabilities |

| (164) |

Deferred tax liability |

| (1,491) |

|

| 5,980 |

On April 28, 2021, the Company closed the acquisition of 100% of the outstanding common shares of 2686068 Ontario Inc. (“2686068”). Pursuant to the terms of the Arrangement, the consideration was comprised of $5,980 in cash.

In accordance with IFRS 3, Business Combinations (“IFRS 3”), the substance of this transaction constituted a business combination. Management gathered the relevant information that existed at the acquisition date to determine the fair value of the net identifiable assets acquired. As such, the initial purchase price was allocated based on the Company’s estimated fair value of the identifiable assets acquired on the acquisition date. Management finalized its purchase price allocation for the fair value of identifiable intangible assets, income taxes and the allocation of goodwill. The goodwill is primarily related to the opportunities to grow the retail cannabis business. For the year ended October 31, 2021, 2686068 accounted for $1,117 in revenues and $1,407 in net loss. If the acquisition had been completed on November 1, 2020, the Company estimates it would have recorded an increase of $1,107 in revenues and an increase of $123 in net loss for the year ended October 31, 2021.

19 |

| High Tide Inc. |

Notes to the Condensed Interim Consolidated Financial Statements | |

For the three and nine months ended July 31, 2022 and 2021 (Unaudited – In thousands of Canadian dollars, except share and per share amounts) |

L. | Fab Nutrition, LLC. Acquisition (Prior year) |

Total consideration |

| $ |

Cash |

| 15,193 |

Common Shares | | 3,752 |

|

| 18,945 |

Purchase price allocation |

|

|

Cash and cash equivalents |

| 642 |

Accounts receivable | | 125 |

Inventory |

| 403 |

Property and equipment |

| 22 |

Intangible assets - brand |

| 7,801 |

Goodwill |

| 13,897 |

Accounts payable and accrued liabilities |

| (552) |

Deferred tax liability | | (2,131) |

Non-controlling interest |

| (1,262) |

|

| 18,945 |

On May 10, 2021, the Company closed the acquisition of 80% of the outstanding common shares of Fab Nutrition, LLC. (“FABCBD”). Pursuant to the terms of the Arrangement, the consideration was comprised of: (i) $15,193 in cash; and (ii) 6,151,915 pre-consolidation common shares of High Tide (410,128 post-consolidation), having an aggregate value of $3,752.

In connection with the acquisition agreement, 9,679,778 pre-consolidation common shares of the Company (645,319 post-consolidation) were placed in escrow for a period of 24 months. Every 6 months 25% of escrow shares are released to the minority shareholder of FABCBD. Over the 24-month period, as the shares are earned by passage of time, the Company recognizes share-based compensation expense through profit and loss.

The acquisition agreement also includes a call and put option that could result in the Company acquiring the remaining 20% of common shares in FABCBD not acquired upon initial acquisition. The Company analyzed the value in the call option and considers it to be at fair value, and therefore has no value related to the acquisition. As the put option is a contractual obligation, it gives rise to a financial liability calculated with reference to the agreement and is discounted to its present value at each reporting date using the discounted cash flow model. The initial obligation under the put option was recorded as a current liability with the offset recorded as equity on the Consolidated Statements of Financial Position, at its fair value at acquisition of $3,722. For the three and nine months ended July 31, 2022, the Company recognized $530 and $1,4641 as a gain on revaluation of derivative liability in the statement of net loss and comprehensive loss.

In accordance with IFRS 3, Business Combinations (“IFRS 3”), the substance of this transaction constituted a business combination.

Management gathered the relevant information that existed at the acquisition date to determine the fair value of the net identifiable assets acquired. As such, the initial purchase price was allocated based on the Company’s estimated fair value of the identifiable assets acquired on the acquisition date. Management finalized its purchase price allocation for the fair value of identifiable assets, income taxes and the allocation of goodwill. The goodwill acquired is primarily related to the opportunities to grow the business, expanded access to capital and greater financial flexibility. Goodwill is not deductible for tax purposes. For the year ended October 31, 2021, FABCBD accounted for $4,746 in revenues and $640 in net income. If the acquisition had been completed on November 1, 2020, the Company estimates it would have recorded an increase of $7,790 in revenues and a decrease of $306 in net loss for the year ended October 31, 2021. The Company also incurred $872 in transaction costs for the year ended October 31, 2021, which were expensed to finance and other costs during that period.

20 |

| High Tide Inc. |

Notes to the Condensed Interim Consolidated Financial Statements | |

For the three and nine months ended July 31, 2022 and 2021 (Unaudited – In thousands of Canadian dollars, except share and per share amounts) |

M. | DHC Supply LLC. Acquisition (Prior year) |

Total consideration |

| $ |

Cash |

| 4,045 |

Common Shares | | 7,767 |

|

| 11,812 |

Purchase price allocation |

|

|

Cash and cash equivalents |

| 1,054 |

Trade and other receivables | | 66 |

Inventory |

| 1,270 |

Prepaid expenses | | 18 |

Property and equipment |

| 10 |

Intangible assets - brand |

| 2,671 |

Goodwill | | 8,201 |

Right of use asset |

| 592 |

Lease liability |

| (592) |

Accounts payable and accrued liabilities |

| (1,478) |

|

| 11,812 |

On July 6, 2021, the Company closed the acquisition of 100% of the outstanding common shares of DHC Supply LLC. (“DHC”). Pursuant to the terms of the Arrangement, the consideration was comprised of: (i) 839,820 post-consolidation commons shares of High Tide (12,597,300 pre-consolidation), having an aggregate value of $7,767; (ii) $4,045 in cash.

In accordance with IFRS 3, Business Combinations (“IFRS 3”), the substance of this transaction constituted a business combination.

Management gathered the relevant information that existed at the acquisition date to determine the fair value of the net identifiable assets acquired. As such, the initial purchase price was allocated based on the Company’s estimated fair value of the identifiable assets acquired on the acquisition date. Management finalized its purchase price allocation for the fair value of identifiable assets, income taxes and the allocation of goodwill. The goodwill acquired is primarily related to the opportunities to grow the business, expanded access to capital and greater financial flexibility. Goodwill is not deductible for tax purposes. For the year ended October 31, 2021, DHC accounted for $3,399 in revenues and $14 in net income. If the acquisition had been completed on November 1, 2020, the Company estimates it would have recorded an increase of $7,513 in revenues and an increase of $301 in net loss for the year ended October 31, 2021.

21 |

| High Tide Inc. |

Notes to the Condensed Interim Consolidated Financial Statements | |

For the three and nine months ended July 31, 2022 and 2021 (Unaudited – In thousands of Canadian dollars, except share and per share amounts) |

N. | 102105699 Saskatchewan Ltd. Acquisition (Prior year) |

Total consideration |

| $ |

Cash |

| 698 |

Common Shares | | 2,018 |

|

| 2,716 |

Purchase price allocation |

|

|

Cash and cash equivalents |

| 7 |

Trade and other receivables | | 7 |

Inventory | | 46 |

Prepaid expenses | | 55 |

Property and equipment |

| 136 |

Intangible assets - license |

| 879 |

Goodwill |

| 1,966 |

Right of use asset |

| 691 |

Lease liability |

| (691) |

Accounts payable and accrued liabilities |

| (143) |

Deferred tax liability |

| (237) |

|

| 2,716 |

On August 6, 2021 the Company closed the acquisition of 100% of the issued and outstanding common shares of 10210569 Saskatchewan Ltd. (“OneLeaf”). Pursuant to the terms of the Arrangement, the consideration was comprised of: (i) 254,518 post-consolidation common shares of High Tide, having an aggregate value of $2,018; and (ii) $698 in cash.

In accordance with IFRS 3, Business Combinations (“IFRS 3”), the substance of this transaction constituted a business combination. Management is in the process of gathering the relevant information that existed at the acquisition date to determine the fair value of the net identifiable assets acquired. As such, the initial purchase price was provisionally allocated based on the Company’s estimated fair value of the identifiable assets acquired on the acquisition date. The values assigned are, therefore, preliminary, and subject to change. Management continues to refine and finalize its purchase price allocation for the fair value of identifiable intangible assets, income taxes and the allocation of goodwill. Goodwill is not deductible for tax purposes. For the year ended October 31, 2021, OneLeaf accounted for $90 in revenues and $83 in net loss. If the acquisition had been completed on November 1, 2020, the Company estimates it would have recorded an increase of $254 in revenues and an increase of $72 in net loss for the year ended October 31, 2021.

22 |

| High Tide Inc. |

Notes to the Condensed Interim Consolidated Financial Statements | |

For the three and nine months ended July 31, 2022 and 2021 (Unaudited – In thousands of Canadian dollars, except share and per share amounts) |

O. | DS Distribution Acquisition (Prior year) |

Total consideration |

| $ |

Cash |

| 5,013 |

|

| 5,013 |

Purchase price allocation |

|

|

Cash and cash equivalents |

| 115 |

Inventory |

| 160 |

Prepaid expenses |

| 158 |

Property and equipment |

| 69 |

Intangible assets - brand |

| 1,375 |

Goodwill |

| 4,384 |

Right of use asset |

| 299 |

Lease liability |

| (299) |

Accounts payable and accrued liabilities | | (863) |

Deferred tax liability | | (385) |

|

| 5,013 |

On August 12, 2021 the Company closed the acquisition of 100% of all the issued and outstanding common shares of DS Distribution Inc. (“DankStop”). Pursuant to the terms of the Arrangement, the consideration was comprised of 612,087 post-consolidation shares of High Tide, having an aggregate value of $5,013.

In accordance with IFRS 3, Business Combinations (“IFRS 3”), the substance of this transaction constituted a business combination. Management is in the process of gathering the relevant information that existed at the acquisition date to determine the fair value of the net identifiable assets acquired. As such, the initial purchase price is provisionally allocated based on the Company’s estimated fair value of the identifiable assets acquired on the acquisition date. The values assigned are, therefore, preliminary, and subject to change. Management continues to refine and finalize its purchase price allocation for the fair value of identifiable intangible assets, income taxes and the allocation of goodwill. Goodwill is not deductible for tax purposes. For the year ended October 31, 2021, DankStop accounted for $380 in revenues and $117 in net loss. If the acquisition had been completed on November 1, 2020, the Company estimates it would have recorded an increase of $6,473 in revenues and an decrease of $311 in net loss for the year ended October 31, 2021.

23 |

| High Tide Inc. |

Notes to the Condensed Interim Consolidated Financial Statements | |

For the three and nine months ended July 31, 2022 and 2021 (Unaudited – In thousands of Canadian dollars, except share and per share amounts) |

P. | Blessed CBD Acquisition (Prior year) |

Total consideration |

| $ |

Cash |

| 7,165 |

Common Shares | | 4,432 |

Working capital adjustment | | 1,086 |

|

| 12,683 |

Purchase price allocation |

|

|

Cash and cash equivalents |

| 2,155 |

Trade and other receivables |

| 472 |

Inventory |

| 293 |

Property and equipment |

| 19 |

Intangible asset - brand |

| 4,220 |

Goodwill |

| 8,889 |

Accounts payable and accrued liabilities |

| (1,530) |

Deferred tax liability |

| (971) |

Non-controlling interest | | (864) |

|

| 12,683 |

On October 19, 2021, the Company closed the acquisition of 80% of the issued and outstanding common shares of Enigmaa Ltd. (“Blessed CBD”). Pursuant to the terms of the Arrangement, the consideration was comprised of: (i) 607,064 post-consolidation shares of High Tide, having an aggregate value of $4,432; (ii) $7,165 in cash, and (iii) and working capital adjustment of $1,086.

In connection with the acquisition agreement, 529,487 post-consolidation common shares of the Company were placed in escrow for a period of 24 months. Every 12 months 50% of escrow shares are released to the minority shareholder of Blessed CBD. This share issuance was initially recorded through equity. Over the 24 month period, as the shares are earned by passage of time, the Company recognizes share-based compensation expense through profit and loss.

The acquisition agreement also includes a call and put option that could result in the Company acquiring the remaining 20% of common shares in Blessed CBD not acquired upon initial acquisition. The Company analyzed the value in the call option and considers it to be at fair value, and therefore has no value related to the acquisition. As the put option is a contractual obligation, it gives rise to a financial liability calculated with reference to the agreement and is discounted to its present value at each reporting date using the discounted cash flow model. The initial obligation under the put option was recorded as a current liability with the offset recorded as equity on the Consolidated Statements of Financial Position, at its fair value at acquisition of $4,323 with an exercise date of October 19, 2022. For the three and nine months ended July 31, 2022, the Company recognized $1,229 and $1,301 gain on revaluation of derivative liability in the statement of net loss and comprehensive loss.

In accordance with IFRS 3, Business Combinations (“IFRS 3”), the substance of this transaction constituted a business combination. Management is in the process of gathering the relevant information that existed at the acquisition date to determine the fair value of the net identifiable assets acquired. As such, the initial purchase price is provisionally allocated based on the Company’s estimated fair value of the identifiable assets acquired on the acquisition date. The values assigned are, therefore, preliminary, and subject to change. Management continues to refine and finalize its purchase price allocation for the fair value of identifiable intangible assets, income taxes, the allocation of goodwill and the non-controlling interest. The goodwill is primarily related to the opportunities to grow the business, expanded access to capital and greater financial flexibility. Goodwill is not deductible for tax purposes. For the year ended October 31, 2021, Blessed CBD accounted for $296 in revenues and $130 in net income. If the acquisition had been completed on November 1, 2020, the Company estimates it would have recorded an increase of $10,083 in revenues and a decrease of $2,382 in net loss for the year ended October 31, 2021. The Company also incurred $360 in transaction costs for the year ended October 31, 2021, which were expensed to finance and other costs during that period.

24 |

| High Tide Inc. |

Notes to the Condensed Interim Consolidated Financial Statements | |

For the three and nine months ended July 31, 2022 and 2021 (Unaudited – In thousands of Canadian dollars, except share and per share amounts) |

4. | Revenue from Contracts with Customers |

For the three months ended July 31 |

| 2022 |

| 2021 |

| 2022 |

| 2021 |

| 2022 |

| 2021 |

| 2022 |

| 2021 |

| | Retail | | Retail | | Wholesale | | Wholesale | | Corporate | | Corporate | | Total | | Total |

| | $ | | $ | | $ | | $ | | $ | | $ | | $ | | $ |

Primary geographical markets (i) | | | | | | | | | | | | | | | | |

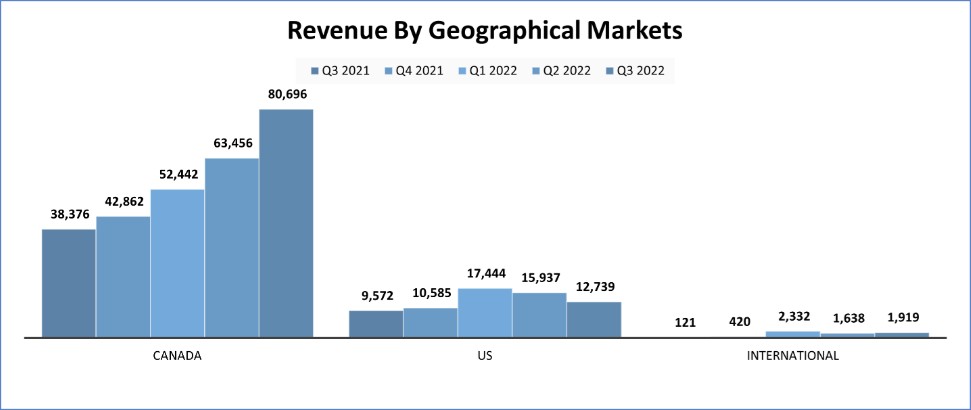

Canada | | 80,436 | | 37,695 | | 215 | | 676 | | 45 | | 5 | | 80,696 | | 38,376 |

USA | | 12,012 | | 8,467 | | 727 | | 1,105 | | - | | - | | 12,739 | | 9,572 |

International | | 1,919 | | 121 | | - | | - | | - | | - | | 1,919 | | 121 |

Total revenue | | 94,367 | | 46,283 | | 942 | | 1,781 | | 45 | | 5 | | 95,354 | | 48,069 |

| | | | | | | | | | | | | | | | |

Major products and services | | | | | | | | | | | | | |

| |

|

Cannabis | | 79,140 | | 32,031 | | - | | - | | - | | - | | 79,140 | | 32,031 |

Consumption accessories |

| 9,427 | | 9,962 | | 941 | | 1,773 | | - | | - |

| 10,368 |

| 11,735 |

Data analytics services |

| 5,475 | | 3,839 | | - | | - | | - | | - |

| 5,475 |

| 3,839 |

Other revenue |

| 325 | | 451 | | 1 | | 8 | | 45 | | 5 |

| 371 |

| 464 |

Total revenue |

| 94,367 | | 46,283 | | 942 | | 1,781 | | 45 | | 5 |

| 95,354 |

| 48,069 |

| | | | | | | | | | | | | | | | |

Timing of revenue recognition |

| | | | | | | | | | | |

|

|

|

|

Transferred at a point in time |

| 94,367 | | 46,283 | | 942 | | 1,781 | | 45 | | 5 |

| 95,354 | | 48,069 |

Total revenue |

| 94,367 | | 46,283 | | 942 | | 1,781 | | 45 | | 5 |

| 95,354 |

| 48,069 |

For the nine months ended July 31 |

| 2022 |

| 2021 |

| 2022 |

| 2021 |

| 2022 |

| 2021 |

| 2022 |

| 2021 |

| | Retail | | Retail | | Wholesale | | Wholesale | | Corporate | | Corporate | | Total | | Total |

| | $ | | $ | | $ | | $ | | $ | | $ | | $ | | $ |

Primary geographical markets (i) | | | | | | | | | | | | | | | | |

Canada | | 195,007 | | 104,804 | | 1,492 | | 2,768 | | 97 | | 35 | | 196,596 | | 107,607 |

USA | | 44,484 | | 16,098 | | 1,636 | | 3,051 | | - | | - | | 46,120 | | 19,149 |

International | | 5,888 | | 500 | | - | | - | | - | | - | | 5,888 | | 500 |

Total revenue | | 245,379 | | 121,402 | | 3,128 | | 5,819 | | 97 | | 35 | | 248,604 | | 127,256 |

| | | | | | | | | | | | | | | | |

Major products and services | | | | | | | | | | | | | |

| |

|

Cannabis | | 197,581 | | 91,978 | | - | | - | | - | | - | | 197,581 | | 91,978 |

Consumption accessories |

| 30,991 | | 19,915 | | 3,112 | | 5,779 | | - | | - | | 34,103 | | 25,694 |

Data analytics services |

| 15,275 | | 8,201 | | - | | - | | - | | - | | 15,275 | | 8,201 |

Other revenue |

| 1,532 | | 1,308 | | 16 | | 40 | | 97 | | 35 | | 1,645 | | 1,383 |

Total revenue |

| 245,379 | | 121,402 | | 3,128 | | 5,819 | | 97 | | 35 |

| 248,604 |

| 127,256 |

| | | | | | | | | | | | | | | | |

Timing of revenue recognition |

| | | | | | | | | | | |

| |

| |

Transferred at a point in time |

| 245,379 | | 121,402 | | 3,128 | | 5,819 | | 97 | | 35 |

| 248,604 | | 127,256 |

Total revenue |

| 245,379 | | 121,402 | | 3,128 | | 5,819 | | 97 | | 35 |

| 248,604 |

| 127,256 |

(i) | Represents revenue based on geographical locations of the customers who have contributed to the revenue generated in the applicable segment. |

25 |

| High Tide Inc. |

Notes to the Condensed Interim Consolidated Financial Statements | |

For the three and nine months ended July 31, 2022 and 2021 (Unaudited – In thousands of Canadian dollars, except share and per share amounts) |

5. | Property and Equipment |

|

| Office equipment | | Production |

| Leasehold |

| |

| |

| |

| | and computers | | equipment | | improvements (iv) | | Vehicles | | Buildings | | Total |

Cost | | $ | | $ | | $ | | $ | | $ | | $ |

Balance, October 31, 2020 | | 778 | | - | | 12,980 | | 167 | | 2,800 | | 16,725 |

Additions | | 626 | | - | | 9,923 | | 14 | | - | | 10,563 |

Additions from business combinations (Note 3) | | 1,857 | | - | | 5,516 | | 5 | | - | | 7,378 |

Disposal (i) (ii) | | (146) | | - | | (1,061) | | (170) | | - | | (1,377) |

Impairment loss (iii) | | (4) | | - | | (129) | | - | | - | | (133) |

Foreign currency translation | | (11) | | - | | (5) | | - | | - | | (16) |

Balance, October 31, 2021 |

| 3,100 | | - |

| 27,224 |

| 16 |

| 2,800 |

| 33,140 |

Additions and reclasses |

| 579 | | |

| 6,301 |

| - |

| - |

| 6,880 |

Additions from business combinations (Note 3) |

| 735 | | 3,532 |

| 1,620 |

| - |

| - |

| 5,887 |

Foreign currency translation | | (22) | | 1 | | (32) |

| - |

| - | | (53) |

Balance, July 31, 2022 |

| 4,392 | | 3,533 |

| 35,113 |

| 16 |

| 2,800 |

| 45,854 |

| | | | | | | | | | | | |

Accumulated depreciation | | | | | | | | | | | | |

Balance, October 31, 2020 |

| 252 | | - |

| 3,218 |

| 158 |

| 12 |

| 3,640 |

Depreciation |

| 1,044 | | - |

| 4,192 |

| 9 |

| 44 |

| 5,289 |

Disposal (i) (ii) | | (89) | | - |

| (291) |

| (158) |

| - | | (538) |

Foreign currency translation | | (2) | | - |

| (5) |

| - |

| - | | (7) |

Balance, October 31, 2021 |

| 1,205 | | - |

| 7,114 |

| 9 |

| 56 |

| 8,384 |

Depreciation |

| 1,038 | | 366 |

| 7,198 |

| 3 |

| 42 |

| 8,647 |

Foreign currency translation | | 7 | | (13) |

| (12) |

| - |

| - | | (18) |

Balance, July 31, 2022 |

| 2,250 | | 353 |

| 14,300 |

| 12 |

| 98 |

| 17,013 |

| | | | | | | | | | | | |

Balance, October 31, 2021 | | 1,895 | | - | | 20,110 | | 7 | | 2,744 | | 24,756 |

Balance, July 31, 2022 | | 2,142 | | 3,180 | | 20,813 | | 4 | | 2,702 | | 28,841 |

| (i) | During the year ended October 31, 2021, the Company sold it’s 49% interest in two of the joint ventures under META that operated as retail cannabis stores in Manitoba. The Company recognized $647 as a gain on the sale at October 31, 2021. |

| (ii) | On July 15, 2021, the Company completed the sale of three of its KushBar retail cannabis stores to Halo Collective Inc. (“Halo” formerly Halo Labs Inc.) for total gross proceeds of $5,700. In 2020, the Company was paid a deposit of $3,500 by way of issuance of 13,461,538 common shares of Halo at a deemed price of $0.26 per common share. During the fiscal year 2020, the Company had sold those shares and received a net amount of $1,700. On the date of close, July 15, 2021, the Company received a convertible promissory note (Note 8) issued by Halo Collective Inc. in the principal amount of $1,800 with a conversion rate of $0.16 per Halo common share. The promissory note was recorded at a fair value through profit and loss of $1,522 based on risk adjusted discount rate of 15%. For the year ended October 31, 2021, the Company recognized $2,654 as a gain on the sale of assets. On July 15, 2022, High Tide took control of the shares of Halo Kushbar Retail Inc. which served as the security for the convertible promissory note. High Tide accounted for this seizure as a business combination (Note 3). The consideration received was settlement of the convertible promissory note, which was revalued to a principal amount of $0.8 million. |

| (iii) | During the year-ended October 31, 2021, the Company identified two locations from the Meta acquisition that would not be operated due to market pressures and increased competition, which resulted in impairment of $133. |

| (iv) | During the nine months ended July 31, 2022, there were additions of $1,627 (July 31, 2021, $1,020) in assets under construction, largely related to cannabis retail locations not yet in operation. |

26 |

| High Tide Inc. |

Notes to the Condensed Interim Consolidated Financial Statements | |

For the three and nine months ended July 31, 2022 and 2021 (Unaudited – In thousands of Canadian dollars, except share and per share amounts) |

6. | Intangible Assets and Goodwill |

|

| Software |