UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

(Mark One)

For the fiscal year ended

For the transition period from to

Commission File Number:

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of | (IRS Employer | |

| incorporation or organization) | Identification No.) | |

| (Address of principal executive offices) | (Zip Code) |

(Registrant’s telephone number, including area code)

Not applicable

(Former name, former address and former fiscal year, if changed since last report)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

Securities registered pursuant to Section 12(g) of the Act: None.

Indicate by check mark if the registrant is a

well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

Indicate by check mark if the registrant is not

required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐

Indicate by check mark whether the registrant

(1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12

months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements

for the past 90 days.

Indicate by check mark whether the registrant

has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (Section 232.405

of this chapter) during the preceding 12 months (or such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act:

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| ☒ | Smaller reporting company | ||

| Emerging growth company | |||

If an emerging growth company, indicate by check

mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting

standards provided pursuant to Section 13(a) of the Exchange Act.

Indicate by check mark whether the

registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal

control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public

accounting firm that prepared or issued its audit report.

If securities are registered pursuant to Section

12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction

of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant

is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No

As of June 30, 2023, the last business day of

the registrant’s last completed second quarter, the aggregate market value of the Class A common stock held by non-affiliates of

the registrant was approximately $

As of March 12, 2024, there were

DOCUMENTS INCORPORATED BY REFERENCE

Specified portions of the registrant’s proxy statement with respect to the registrant’s 2024 Annual Meeting of Stockholders, which is to be filed pursuant to Regulation 14A within 120 days after the end of the registrant’s fiscal year ended December 31, 2023, are incorporated by reference into Part III of this Annual Report on Form 10-K.

TABLE OF CONTENTS

i

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

Various statements in this Annual Report on Form 10-K of PSQ Holdings, Inc. are “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements involve substantial risks and uncertainties. All statements, other than statements of historical facts, included in this report, including statements regarding our strategy, future operations, future financial position, future revenues, projected costs, prospects, plans and objectives of management are forward-looking statements. These statements are subject to risks and uncertainties (some of which are beyond our control) and are based on information currently available to our management. Words such as “anticipate,” “believe,” “estimate,” “expect,” “intend,” “may,” “plan,” “contemplates,” “predict,” “project,” “target,” “likely,” “potential,” “continue,” “ongoing,” “will,” “would,” “should,” “could,” or the negative of these terms and similar expressions or words, identify forward-looking statements. The events and circumstances reflected in our forward-looking statements may not occur and actual results could differ materially from those projected in our forward-looking statements. Such forward-looking statements are based on current expectations and involve inherent risks and uncertainties, including risks and uncertainties that could delay, divert or change these expectations, and could cause actual results to differ materially from those projected in these forward-looking statements. These risks and uncertainties include, but are not limited to, those factors described under Part I, Item 1A: “Risk Factors.” Should one or more of these risks or uncertainties materialize, or should any of our assumptions prove incorrect, actual results may vary in material respects from those projected in these forward-looking statements.

This report contains market data and industry forecasts that were obtained from industry publications. These data involve a number of assumptions and limitations, and you are cautioned not to give undue weight to such estimates. We have not independently verified any third-party information. While we believe the market position, market opportunity and market size information included in this report is generally reliable, such information is inherently imprecise and subject to change.

All written and oral forward-looking statements attributable to us or any person acting on our behalf are expressly qualified in their entirety by the cautionary statements contained or referred to in this section. We caution investors not to rely on the forward-looking statements we make or that are made on our behalf as predictions of future events. We undertake no obligation and specifically decline any obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws.

We encourage you to read the management’s discussion and analysis of our financial condition and results of operations and our consolidated financial statements contained in this Annual Report on Form 10-K. There can be no assurance that we will in fact achieve the actual results or developments we anticipate or, even if we do substantially realize them, that they will have the expected consequences to, or effects on, us. Therefore, we can give no assurances that we will achieve the outcomes stated in those forward-looking statements, projections and estimates.

ii

PART I

Item 1. Business

Unless the context otherwise requires, throughout this Annual Report on Form 10-K, the words “PSQ,” “PSQH,” “we,” “us,” “PublicSquare” the “registrant” or the “Company” refer to PSQ Holdings, Inc. and its subsidiaries (as applicable).

On February 23, 2023, PSQ completed a stock-for-stock transaction to purchase 100% of the outstanding shares of EveryLife, Inc. (“EveryLife”), a Delaware corporation, in exchange for 1,071,229 shares of common stock, par value $0.001 per share, of Private PSQ (“Private PSQ Common Stock”).

On July 19, 2023 (the “Closing Date”), we consummated the transactions contemplated by that Agreement and Plan of Merger, dated as of February 27, 2023 (the “Merger Agreement”), each by and among PublicSq. Inc. (f/k/a PSQ Holdings, Inc.), a Delaware corporation (“Private PSQ”), Colombier Acquisition Corp., a Delaware corporation (“Colombier”), Colombier-Liberty Acquisition, Inc., a Delaware corporation and a wholly-owned subsidiary of Colombier (“Merger Sub”), and Colombier Sponsor, LLC (the “Colombier Sponsor”), a Delaware limited liability company, in its capacity as purchaser representative, for the purposes set forth in the Merger Agreement, which, among other things, provided for the merger of Private PSQ into Merger Sub with Private PSQ surviving the merger as a wholly owned subsidiary of Colombier (the “Business Combination”). At the closing of the Business Combination (the “Closing”), Colombier changed its name to “PSQ Holdings, Inc.”.

Our Business

We are a values-aligned platform where users with traditional American values can connect with and patronize business members whose values aligned with their own. Users are able to search for and shop businesses offering products and services both locally and online. The PSQ platform is accessible through the web and mobile devices. Since our nationwide launch in July 2022, we have become the largest values-aligned platform of pro-America businesses and consumers.

Our Values

We are passionate about our mission and that passion guides everything we do. We believe that the Platform is the leading widely accessible repository dedicated to empowering like-minded, patriotic Americans to discover and support companies that share their values. As a company, we strive to connect consumer members with a wide selection of values-aligned and patriotic business members from a wide variety of industries. In order for a new business to join the Platform, a representative of that business must agree that the business will respect the following five core values (the “five core values”) that we strive to uphold and promote within our community:

| ● | We are united in our commitment to freedom and truth — that’s what makes us Americans. |

| ● | We will always protect the family unit and celebrate the sanctity of every life. |

| ● | We believe small business members and the communities who support them are the backbone of our economy. |

| ● | We believe in the greatness of this Nation and will always fight to defend it. |

| ● | Our constitution is non-negotiable — government isn’t the source of our rights, so it can’t take them away. |

These five core values are the foundation of our Company’s vision, which connects the consumer members and business members who use the Platform to promote their voice through their purchasing power, or ‘vote with their wallet’.

The Platform

We are free-to-use for users, who can use the Platform to search for and shop from values-aligned business members both locally and nationally. The types of business members found on the Platform currently include, among others, retailers and other merchants, restaurants, banks and other service providers.

The PSQ platform (the “Platform”) can be accessed through two primary means:

| ● | Mobile application — Our mobile app is available for both iOS and Android-based devices. |

| ● | Web — Users can access the Platform at PublicSquare.com. |

1

Business owners from a wide array of industries, offering a myriad of products and services, can host their business listing on the Platform directory at no cost. Users using the Platform can then identify and patronize these business members. Users are able to review our five core values on the Platform. By accepting the terms and conditions of our application, business members confirm that they have reviewed our five core values and affirm that they will respect these values. We believe that having our business members confirm that they respect our five core values, helps ensure platform mutual trust in order to drive consumer and business satisfaction and retention. We ensure that our business members respect our five core values by having our team routinely review business member profiles and other advertising materials and content on the Platform to ensure that they do not upload any content that we believe does not respect our five core values. Users are encouraged to send reviews and report to our support team if they come across businesses who should be considered noncompliant in relation to our values. When we find noncompliant business members who do not support our five core values, we confirm the validity of the feedback and determine the best course of action with the business member, which may include contacting the business member directly, or removing the business member from the Platform. When joining the Platform, business members upload their respective profiles to be included in the Platform directory at no cost. In addition, they can advertise their services on the application platform, which increases their exposure to the consumer members in our network, for a monthly fee. They can also sync their products in order for users to purchase their product on the app.

For users, our user-friendly app provides different tabs where they can find both local and online business members. The Platform categorizes products and services into industries including but not limited to: coffee & tea, clothing, outdoor recreation, shooting, and vitamins and supplements. Each business profile provides information about the business, such as its location, a description of services and/or products provided by such business, and, in many cases, contact information and a PSQ-specific discount code, if applicable. Users are able to purchase products, bookmark favorite businesses, and share business profiles. A link to each business’ website, when available, is also provided to facilitate ease of shopping by interested consumer members if the business is not set up for e-commerce capabilities.

2

Our Business Model

Digital Advertising — We currently generate revenue from digital advertising fees from both local and national advertisers. Business members advertising on the Platform pay monthly or purchase certain items a la carte to advertise, with a tiered pricing system. By advertising their services on PSQ, business members can increase their exposure to users on the Platform. All advertisers we conduct business with are listed on the Platform and are required to affirm that they respect our five core values.

Business to Business (“B2B”) Revenue —

Through a B2B initiative that we are in the process of further developing, we currently collaborate with multiple business members on the Platform that primarily serve other business members through revenue sharing arrangements pursuant to which we receive referral fees in the form of commissions based on the dollar amounts of transactions between the business members we connect through our B2B referral initiative. The business members with which we have such relationships currently include, but are not limited to telecommunications, recruiting services, and business and marketing services. We vet these members for quality and values-alignment by researching the business members through publicly available data to assess their public reputation. We then refer them to our business network and either receive fees representing a percentage of the revenue earned by our business members through the relationships that we facilitate or place their advertising in an email distributed to PSQ business members.

E-Commerce Transactional Revenue — We launched e-commerce capabilities on the Platform in November 2023, which provide in-app shopping capabilities with discounts for the PSQ community. The Platform allows consumer members to purchase products and services provided by business members directly on our app and further facilitate and ease their experience, from which we realize transaction-based revenue fees.

Direct to Consumer (“D2C”) — We are also in the process of developing networks and relationships to facilitate future direct-to-consumer sales of products which we expect to offer to consumer members through the Platform under our own brands (including our EveryLife brand name). We believe that the level of consumer member demand observed based on utilization of the Platform to date suggests that there is untapped potential to create and sell our own branded products to our customer base, and the success of EveryLife is proof. We believe that our existing (and growing) consumer member base represents an opportunity for us to reach and sell branded products with minimal marketing spend due to our established primary customer acquisition channel on the Platform directory. We launched our first D2C product, disposable diapers and wipes, in July 2023 under our pro-family “EveryLifeTM” brand.

Our Constituents and Engagement

Consumer members/users

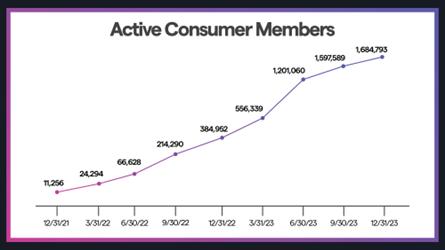

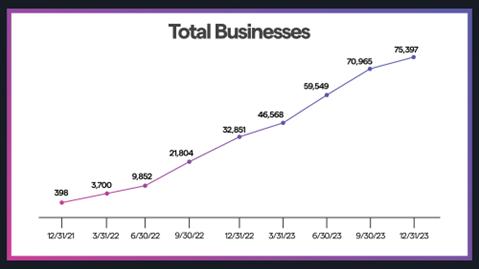

Our consumer members are like-minded Americans who desire to discover and support business members that share their values. As of December 31, 2023, on the Platform we have more than 1.6 million active consumer members (defined as unique consumer membership accounts for which we have received all required contact information and which have not been deactivated or deleted since our reception) and more than 75,000 business members from a wide variety of industries.

3

Business members

The business members that choose to participate on the Platform are required to affirm that they agree to respect our five core values. As of December 31, 2023, over 75,000 business members have joined the Platform and our MoM business growth rate (as measured the number of business members that have joined the Platform as of the last day of each month) was 13% for the period from July 1, 2022, through December 31, 2023. Business members listed on the Platform directory come from a diverse group of industries, including but not limited to retailers and other merchants, restaurants, banks and service providers.

Advertisers

While it is free for a business to sign up for the Platform, during the signup process, business owners are asked if they would like to increase their exposure throughout the Platform by purchasing paid advertising. Our monthly advertising packages are offered at different price points depending on the selected features including but not limited to: category promotion, promoted products, ad placements on the “Shop” tab, push notifications, and email advertising to our consumer members.

Brand Customers

EveryLife’s key demographic comprises mothers in their early thirties, navigating parenthood with multiple children. These moms are fervent about supporting companies that mirror their values, placing a strong emphasis on family priorities. In response to a growing discontent with baby brands supporting abortion and progressive causes, EveryLife emerges as a solution, filling a significant market gap.

D2C Brand

Overview

EveryLife is a direct-to-consumer baby care company founded in 2023 with a mission to provide premium products to every miraculous life. Every baby is considered a gift from God and deserves love, protection, and celebration. EveryLife is committed to its core values, ensuring product quality, and demonstrating generosity by donating diapers and wipes to moms in need. This commitment has quickly set EveryLife apart, elevating both its brand and products. Since its launch in July 2023, EveryLife has been delivering high-performing and price-accessible products that align with the values of our consumers.

Our Products and Services

| ● | Diapers: EveryLife’s diapers use high-performance flow channel technology for faster absorption and 12-hour leak protection. EveryLife diapers are carefully made to limit and eliminate harsh chemicals to help protect baby’s developing brain and body. EveryLife’s diapers are made without fragrances, dyes, lotions, latex, parabens, phthalates, or elemental chlorine. |

| ● | Wipes: EveryLife’s baby wipes are made with 99% purified water and with only five, clean ingredients. EveryLife baby wipes are made without harsh chemicals, alcohol, fragrance, parabens, dyes, lotions, PEG ingredients, or plastics. |

| ● | With EveryLife’s auto-renew service, parents can have their premium products delivered to their doorstep every month. With a simple text, parents can edit, pause, or cancel their orders at any time, providing the ultimate experience of convenience. |

Customers and Markets

EveryLife’s key demographic comprises mothers in their early thirties, navigating parenthood with multiple children. These moms are fervent about supporting companies that mirror their values, placing a strong emphasis on family priorities. In response to a growing discontent with baby brands supporting abortion and progressive causes, EveryLife emerges as a solution, filling a significant market gap.

EveryLife caters to mothers seeking more than just baby care products – they are actively seeking brands that share their values. Positioned as a choice for those making conscious decisions in favor of life-affirming principles, EveryLife contributes to the development of a parallel economy. This concept involves consumers actively supporting businesses that align with their values, and EveryLife, in conjunction with its parent company PSQH, plays a vital role in shaping this distinctive marketplace. By doing so, EveryLife becomes more than just a provider of baby care items; it becomes a symbol of choice for a community of like-minded mothers actively shaping a marketplace aligned with their shared values.

Competition

EveryLife faces competition from a diverse range of players, including both direct-to-consumer companies and retail-exclusive brands. While the quality of EveryLife’s products aligns with that of other well-established diaper brands in households, what sets EveryLife apart is its unique emphasis on pro-life values. Unlike many competitors, EveryLife is singularly dedicated to leading with these values, making it a distinctive choice for consumers who prioritize such principles in their purchasing decisions.

4

While competitors often extend their offerings beyond diapers and wipes, EveryLife recognizes the importance of catering to a broader spectrum of baby essentials. In response to this, EveryLife is committed to consistently introducing new products, ensuring that parents who share their values can find a comprehensive range of baby essentials under the EveryLife brand. This strategic expansion aims not only to satisfy consumer needs but also to position EveryLife as more than just a diaper company – it aspires to become a trusted brand synonymous with comprehensive baby care.

By evolving into a one-stop-shop for various baby care products, EveryLife seeks to redefine its identity from a mere diaper company to a holistic baby brand. This strategic shift not only aligns with the diverse needs of parents but also strengthens EveryLife’s competitive standing within the dynamic landscape of the baby care industry. As a result, the brand aims to resonate more profoundly with consumers who seek not only quality products but also a shared set of values when it comes to caring for their little ones.

Marketing Strategy

EveryLife’s marketing strategy centers around values-aligned messaging and user acquisition, communicating the mission to protect and celebrate life while providing premium products for every baby. This message is disseminated through various channels, including social media, the PublicSquare app and email list, field marketing, influencer marketing, and digital advertising.

The grassroots Ambassador Program has successfully enlisted nearly 700 moms across the United States who are dedicated to spreading EveryLife’s mission in their communities, local churches, and pregnancy centers.

Manufacturers/Supply Chain & Operations/Third Party Logistics

EveryLife manages a North American-based supply chain of highly qualified, third-party manufacturing and logistics partners to produce and distribute EveryLife products. EveryLife partners with manufacturing partners who are committed to quality, Current Good Manufacturing Practices (“cGMPs”), sustainability, and innovation. EveryLife conducts quality audits of third-party manufacturing partners and requires that they follow EveryLife’s quality standards of controlled documentation, cleaning and safety protocols, and laboratory controls. EveryLife’s third-party manufacturing and fulfillment partners are located in various locations including the United States and Mexico. EveryLife’s Operations team manages these third-party relationships and processes.

EveryLife’s distribution network includes multiple warehouses in the United States with direct-to-consumer (“D2C”) fulfillment capabilities and value-added services. The fulfillment centers are operated by third party logistics (“3PL”) service providers. EveryLife manages inventory by forecasting demand, analyzing product sell-through, and analyzing supply chain with manufacturers to ensure sufficient capacity to support demand.

Product Development

EveryLife is embarking on an exciting expansion beyond diapers and wipes to broaden its product offerings. The first addition to our range will include scented and unscented soaps and lotions, meticulously crafted to be gentle, clean, and proudly made in the USA. This extension aims to enhance the overall baby care experience, catering to the diverse needs and preferences of our discerning customers.

In our continuous commitment to providing premium products, EveryLife is set to introduce training pants as the next expansion. This strategic move allows us to further extend our reach and cater to the evolving needs of families. By diversifying our product line, we position ourselves as more than just a diaper company; we are becoming a comprehensive baby brand, dedicated to offering high-quality essentials that parents can trust.

This expansion is not a one-time endeavor but part of a larger strategy to establish EveryLife as a dynamic and growing player in the baby care industry. Our commitment to meeting the needs of our customers drives us to continuously launch new baby essentials. As we identify opportunities and trends in the market, EveryLife is poised to introduce innovative products that align with our values and resonate with the evolving needs of families.

Team

EveryLife is a vibrant team consisting of three co-founders and a dedicated staff of ten individuals. These team members expertly handle key roles across diverse departments, including finance, operations, marketing, creative, customer support, and strategic partnerships. Each department plays a pivotal role in ensuring the seamless operation and growth of EveryLife, working cohesively to bring our mission to fruition.

5

As a wholly owned subsidiary of PSQH, EveryLife operates within a synergistic relationship, strategically collaborating to advance the concept of the parallel economy. This partnership allows us to leverage the strengths and resources of PublicSquare, enhancing our ability to create a meaningful impact within the market.

Our co-founders and employees collectively share a passion for EveryLife’s mission, working tirelessly to provide premium products that align with our values. This collaborative effort not only solidifies our position as a dynamic player in the baby care industry but also underscores our commitment to contributing to the development of a parallel economy alongside our parent company, PSQH. Together, we are focused on building a brand that resonates with consumers who prioritize values-driven choices in their purchasing decisions.

Our Competitive Strengths

We believe that the collective expertise of our team, our vision and the strength of the platform we are building, taken together with the following competitive strengths, will allow us to successfully build our business and capitalize on our large market opportunity. We believe we are the only patriotic marketplace that is operating at scale and launching wholly owned subsidiaries that fill the gaps for our users and business members.

| ● | First Mover Advantage: |

| ● | We view PSQ as the first business, at scale, to address the concerns and needs of our target consumer and business members through an online platform oriented towards patriotic Americans inspired to build a parallel economy. We have observed that many consumers are increasingly disenchanted with large corporations that have embraced non-traditional, progressive ideas and policies and would prefer to re-allocate more of their dollars to business members who do not stand in opposition to their views and values. At the same time, businesses that also share these traditional American values are seeking to attract new customers; our values-aligned platform allows these business members to get exposure to our consumer member base. We are unique in that it is a leading mission-driven platform focused on connecting patriotic Americans with like-minded business members. We believe our differentiated platform allows consumer members to feel confident when shopping on the Platform that they are directing their dollars to business members that share similar values to theirs. We further believe that the growth in the number of business members and consumer members using the Platform that we have experienced since our nationwide launch in July 2022 demonstrates that there is significant demand for a values-aligned platform like us. We “sing a different tune” than many other major e-commerce platforms and businesses in the United States and we believe this differentiation will work to our advantage. |

| ● | Value Proposition for Users: |

| ● | We provide users using the Platform the ability to search for and shop with business members that share their traditional American values. We aim to serve this large unaddressed market with our high-quality Platform of values-aligned products and business members, along with our wholly owned subsidiaries such as EveryLife. |

| ● | Value Proposition for Business Members: |

| ● | By connecting business members with like-minded consumer members, we are able to fill a gap in the market that we believe has been purposefully ignored by our larger competitors. We are uniquely situated to provide this connection and bond that can help support small and medium sized American business members sharing traditional values. |

| ● | Mutually Reinforcing Business Model: |

| ● | The Platform serves as an ecosystem designed to connect patriotic consumer members with values-aligned business members to create trust-driven transactions between consumer members and business members. We, in turn, utilize data from the Platform to identify the needs of our users and businesses which we can fill through launching or acquiring wholly owned subsidiaries that provide solutions. The more we are able to provide high quality products to our users and business members, the more the reach of the Platform can grow. |

6

Our Growth Strategy

We are currently focusing on the following areas to drive our growth:

| ● | Continue to Innovate and Improve the Platform Offering — We are continuously looking to improve the Platform functionality and user experience, and to add new features and technologies to improve the Platform and value proposition. In February 2023, we introduced an improved user interface and user experience that we expect will continue to serve our existing app users, attract new app users to the Platform and grow application engagement with the availability of the e-commerce interface. In November 2023, we rolled out an enhanced e-commerce platform, where our consumer members are able to purchase products from our business members directly through our app and through which we realize transaction-based revenue fees through purchases being made using the Platform. |

| ● | Expand Our Outreach Program — Growth in our consumer member base is an important driver for our business’ growth, and we believe that there is a significant opportunity to expand the number of consumer members and business members using the Platform. Through the PSQ Outreach Program, we are collaborating with over 1,200 highly influential individuals, as of February 29, 2024, who serve as our ambassadors and influencers to raise awareness about and advocate for the Platform and our five core values. We believe that our Outreach Program is key to growing our awareness and presence in the digital world. Participating influencers share their positive interactions with the Platform and the various experiences connecting with patriotic business members that use the Platform. Through media outreach, our ambassadors are able to actively onboard new business and consumer members on the Platform. We actively seek to continue growing this program. |

| ● | Expand Our Branded D2C Product Offerings — We introduced our first branded D2C products, disposable diapers and wipes offered under our pro-family “EveryLifeTM” brand in July 2023 and expect to expand and diversify our branded D2C offerings in areas where we believe there is significant existing market need or opportunity going forward. We believe these brands will enable us to fill gaps within consumer spending through our established primary customer acquisition channel. |

| ● | Increase Monetization on the Platform — We are still in the early stages of monetization on the Platform and believe there are many avenues for sustained revenue growth that may be available to us in the future through the Platform and the network of connections that it allows us to establish and grow. We are currently focused on near-term goals in two main areas — scaling our digital advertising business and developing new revenue streams, such as our e-commerce integration and the development and launch of B2B products and the expansion of our D2C product offerings. |

| ● | Pursue Value-Enhancing Acquisitions — In order to fully capitalize on opportunities within our addressable market, as well as to further expand the Platform and offerings, we intend, over time, to pursue value-enhancing acquisitions as they become available in the future. In so doing, we intend to focus on like-minded business members that respect our five core values, complement our values-aligned platform, and fulfill demand from our consumer members and business partners. |

7

We also expect to further scale the scope and form of our advertising and marketing efforts, as briefly described below. One path we are pursuing to further scale our advertising business involves further improving advertising products and tools, organizing and growing our sales force, and investing in media agency and channel partner relationships. We are continuing to invest in our self-serve advertising platform, which will provide the ability for business owners to purchase an advertising package directly from our website and manage their own advertising content. We believe these additions will improve ad relevance and effectiveness. Business owners will have greater control of their own experience, as well as further success measurement. We intend to gain efficiencies in scaling and will be able to focus our salesforce on attracting and retaining larger enterprise partners, with opportunities to upsell and partner with them in more meaningful ways.

We expect that our ongoing product investments will allow us to enable and capture potential new revenue in small business and e-commerce offering for goods and services.

| ● | Other growth strategies: |

| ● | Increase our marketing, sales, and business development initiatives to attract new customers and create financial partnerships. |

| ● | Continue to hire highly competent, hardworking, ethical executives and personnel based on merit. |

| ● | Exploit our proprietary data and utilize to provide high-quality services to our consumer base. |

| ● | Lower operating costs. We are focused on developing and implementing efficiencies to decrease the acquisition cost of consumer members and business members. Additionally, we expect that, as we scale operations, our staff will become more efficient in various aspects of operations and maintenance such that we can reduce operating costs. |

Acquisition of Credova

Credova Merger Agreement

On March 13, 2024, we entered into an agreement and plan of merger (the “Credova Merger Agreement”) with Cello Merger Sub, Inc., a Delaware corporation and our wholly-owned subsidiary (“Merger Sub” and, together with PSQ, the “Buyer Parties”), Credova Holdings, Inc., a Delaware corporation (“Credova”), and Samuel L. Paul, in the capacity as the Seller Representative in accordance with the terms of the Credova Merger Agreement.

Structure of the Transaction

Pursuant to the Credova Merger Agreement, on March 13, 2024, the transactions which are the subject of the Credova Merger Agreement were consummated (the “Closing”) and Merger Sub merged with and into Credova (the “Merger”), with Credova surviving as a wholly-owned subsidiary of PSQ. In connection with the Merger, each share of Credova was converted into the right to receive newly-issued shares of our Class A common stock (“Class A Common Stock”), delivered to the Credova stockholders at the Closing (“Credova Stockholders”).

Merger Consideration

As consideration for the Merger, Credova stockholders received 2,920,993 newly-issued shares of Class A Common Stock (the “Consideration Shares”). A number of Consideration Shares equal to ten percent (10%) of the Consideration Shares (the “Escrow Shares”) was placed in an escrow account for indemnity claims made under the Credova Merger Agreement. Assuming they are not subject to indemnity claims, the Escrow Shares remaining in escrow upon the 12-month anniversary of the Closing will be released and distributed pro rata to the former stockholders of Credova.

8

Note Exchange

Prior to the execution of the Credova Merger Agreement, Credova, PSQ and certain holders of outstanding subordinated notes (“Subdebt Notes”) issued by Credova (the “Participating Noteholders”) entered into a Note Exchange Agreement (the “Note Exchange Agreement”) pursuant to which, immediately prior to the Closing, the Participating Noteholders delivered their subdebt notes of Credova for cancellation,, in exchange for newly-issued replacement notes issued by PSQ, convertible into shares of Class A Common Stock (the “Replacement Notes”). The Replacement Notes have 9.75% simple interest per annum and ten-year maturity dates.

Pursuant to the terms of the Replacement Notes, at any time after the Closing, Participating Noteholders may elect to convert their Replacement Notes into a number of shares of Class A Common Stock equal to the quotient obtained by dividing (x) the outstanding principal amount of the Replacement Note to be converted plus accrued and unpaid interest by (y) 4.63641, subject to adjustment for stock splits and other similar transactions (the “Conversion Price”). At any time, the Company may call the Replacement Notes for a cash amount equal to accrued interest plus (i) between the Closing and the first anniversary of the Closing, 120% of the then outstanding principal amount, (ii) between the first anniversary and the second anniversary of the Closing, 105% of the then outstanding principal amount and (iii) after the second anniversary of the Closing, the then outstanding principal amount of the Replacement Note. Further, the Replacement Notes permit the Company, in its discretion, to require conversion of the Replacement Notes into shares of Class A Common Stock if the daily volume-weighted average trading price of the Company Class A Common Stock exceeds 140% of the Conversion Price on each of at least ten consecutive trading days during the twenty trading day period prior to notice of such required conversion.

Credova Subdebt Notes not exchanged for Replacement Notes at Closing were cancelled following payment in full in cash.

Lock-Up Agreement

Concurrently with the execution of the Credova Merger Agreement, Credova Stockholders and recipients Replacement Notes entered into lock-up agreements pursuant to which they will be subject to trading restrictions and restrictions against selling short or hedging PSQ securities for a period of 12 months after the Closing.

Employment Agreements

As a condition to the Closing, certain key employees of Credova entered into and delivered employment agreements to become employees of the Company or subsidiaries thereof from and after the Closing.

Non-Competition and Non-Solicitation Agreement

Concurrently with the execution of the Credova Merger Agreement, Credova stockholders and certain key employees of Credova entered into a non-competition and non-solicitation agreement with the Company and Credova (the “Non-Competition and Non-Solicitation Agreements”), pursuant to which they will agree not to compete with Credova during the two-year period following the Closing and not to solicit employees or customers of Credova.

Registration Rights Agreement

Concurrently with the execution of the Credova Merger Agreement, PSQ, Credova Stockholders and recipients of Replacement Notes entered into a registration rights agreement (the “Registration Rights Agreement”), pursuant to which, among other things, the Company will be obligated to file a registration statement to register the resale of the Consideration Shares and the shares issuable upon conversion of the Replacement Notes within a certain period after the Closing, upon demand by holders of a majority of the registrable securities. The Registration Rights Agreement also provides for certain additional demand registration and “piggy-back” registration rights, subject to certain requirements and conditions.

9

Description of Credova’s Business

Overview

Credova assists consumers, lenders, and retailers in offering point-of-sale financing products. Credova has developed and maintains an internet-based proprietary retail finance platform and related application programming interfaces (“APIs”) through which Credova, certain FDIC and NCUA insured financial institutions, and other financial institutions authorized by Credova (each a “Financing Partner”), and merchants can dynamically offer certain financing products (collectively, the “Services”).

Credova’s offerings fall into four main categories: (i) Merchant-originated products; (ii) Bank Partner-originated closed-end installment loans; (iii) Credova-originated loan products; (iv) Zero-interest installment product (“Pay-in-4”).

The Services and products offered by Credova promote convenience in the borrowing community by providing interest bearing and non-interest bearing financial products that cover the majority of the credit spectrum. Credova’s proprietary software and application offers consumers a near frictionless application process with high-quality security to protect the consumer’s information. Financing products are facilitated and signed through Credova’s internet-based platform and closed and funded by Credova or a Financing Partner. Credova relies on a third-party servicer to service its financing products. Credova intends to comply with all applicable state and federal statutes and regulations. Credova has adopted rigorous compliance policies and procedures, engages in regular internal and external audits of its practices, and has implemented a schedule of continuous learning and training for its employees.

Market

Credova’s Services allow merchants to offer point of sale financing options for the purchase of consumer goods online and in store. The intended market includes consumers making purchases from retailers with a focus on those in the outdoor recreation industry and others. The creditworthiness of consumers is largely determined based on credit scores provided by national credit reporting agencies and other proprietary underwriting criteria.

Marketing

Credova operates Credova.com, which provides information to potential retailer partners about the benefits of partnering with Credova. In addition, Credova looks for retail partners by utilizing an in-house sales team, referrals, and online marketing. Credova provides merchants with compliant advertising and other marketing content that will advertise the retailer’s products and the financing solutions facilitated by Credova. These campaigns include email, web banners, and display ads.

Corporate Information

Credova is a Delaware limited liability company organized in 2018 with its principal office location in Bozeman, Montana.

Our Technology

Our investments in technology are currently focused on the following areas: business solutions, cloud infrastructure and development principles.

| ● | Business Solutions — Our proprietary Content Management System (“CMS”) is the core our business toolset, powering our advertising products, content technology stack and reporting capabilities. Built with flexibility in mind, our CMS consists of content targeting and delivery engines. These capabilities serve all of our paying business members. |

| ● | Cloud Infrastructure — We continually invest in the underlying technology platform that powers all of the Platform and services. From its inception, our infrastructure was built to be cloud-native, applying well-tested design patterns with distributed systems that are linearly scalable and highly flexible. We currently utilize a large third-party cloud service provider to support the Platform needs. |

10

| ● | Development Principles — Execution, quality, velocity and autonomy are core pillars of our engineering culture. We employ agile development processes and techniques combined with continuous integration (“CI”) and continuous deployment (“CD”) to empower our teams to rapidly improve our products and the platforms that power them. Leveraging data generated by the usage of our products is a priority in how we develop, test and iterate to continually improve the user experience and build our future product roadmap. Moreover, we build our products to be accessible and functional in both web and mobile app environments. |

Intellectual Property

Our intellectual property includes trademarks, copyrights and trade secrets. In addition, the Platform is powered by proprietary technology and certain open-source software. We rely on, and expect to continue to rely on, a combination of development, assignment, and confidentiality agreements with our employees, consultants, and third parties with whom we have relationships, as well as trademark, trade dress, domain name, copyright, and trade secret laws, to protect our brands, proprietary technology, and other intellectual property rights.

Marketing and Advertising

To date, a majority of our marketing and advertising activity has been conducted by our management team and employees, through our Outreach Program, earned media exposure, social media exposure, word of mouth growth, and guerrilla marketing (creating viral videos to capitalize on current events, engaging with content creators through superchats, press campaigns to support local business members, and culturally relevant merch drops). To a lesser extent, we also have prioritized digital advertising on platforms such as Rumble and Meta, and podcast advertising on shows such as Allie Stuckey’s “Relatable”, The “Charlie Kirk Show”, Steve Bannon’s “War Room”, and others.

Business to Business (“B2B”) Partnerships

As discussed above, we currently operate in partnership with multiple business members on the Platform that primarily serve other business members. These include, but are not limited to, telecommunications, recruiting services, and business and marketing services.

Product Development

Since our inception, we have focused on continuous improvement of the Platform and user experience, with our product and engineering teams working in an environment focused on efficiency and speed combined with end-user value. As we continue to grow, we believe it will be important to maintain and enhance this culture and scale our business as we look to bring new innovations to consumer members and business members.

Our product organization focuses on creating and improving digital products for all of our consumer members and business owners. As of December 31, 2023, we had over 1.6 million active consumer members (defined as unique consumer membership accounts for which we have received all required contact information and which have not been deactivated or deleted since our inception) and over 75,000 business members on the Platform, respectively. Using machine-learning and proprietary technology, we surface relevant business listings, keeping members informed while supporting growth for business members of all sizes.

Employees

As a mission-driven technology company, we believe our employees are our most valuable resource. As of December 31, 2023, we had 82 full-time employees (including employees of wholly-owned subsidiaries), all of whom are based in the United States. We believe we have good relationships with our employees. Our human capital resources objectives include identifying, recruiting, retaining, incentivizing, and integrating our existing and additional employees. The principal purposes of our equity incentive plans are to attract, retain, and motivate key employees and directors through the granting of share-based compensation awards.

11

Competition

We compete with, among other business members, traditional e-commerce platforms, business directories and online retailers, as well as some smaller competitors who also position themselves as values-aligned platforms. The competitive landscape in the app and website platform markets is complex and constantly evolving. There are participants of many different sizes with different operational capabilities, platform reach and financial resources. Some of the companies we compete with include but are not limited to Yelp, Angi, Etsy, and Amazon. Many of these companies are much larger and more well capitalized than we are. Other companies that position themselves as values-aligned platforms include New Founding and Mammoth Nation. We also compete with companies such as The Honest Company, Hello Bello, Huggies and Coterie, among others, with our current D2C offerings of disposable diapers and wipes that are sold under our “EveryLifeTM” brand. We compete with all of these companies to attract, engage, and retain consumer members and business members. We believe that we are a unique platform for value-aligned business members and consumer members who feel increasingly ignored or alienated by many of our competitors and who want to support patriotic, traditional pro-American business members that share their values, and that we can compete effectively on that basis. As we introduce future products, as the Platform evolves, or as other companies introduce new products and services, we may become subject to additional competition.

Government Regulation

We are subject to a number of U.S. federal and state laws and regulations, as well as foreign ones, that involve matters that are important to, or may otherwise impact, our business and that may affect companies conducting business on the internet, including, but not limited to, internet and e-commerce, labor and employment, anti-discrimination, payments, whistleblowing and worker confidentiality obligations, product liability, intellectual property, consumer protection and warnings, import/export, marketing, taxation, privacy, data security, competition, arbitration agreements and class action waiver provisions, terms of service, and mobile application and website accessibility. These regulations are often complex and subject to varying interpretations, in many cases due to their lack of specificity, and as a result, their application in practice may change or develop over time through judicial decisions or as new guidance or interpretations are provided by regulatory and governing bodies in the United States and abroad, such as federal, state, and local administrative agencies. Many of these laws and regulations are subject to change or uncertain interpretation, and could result in claims, changes to our business practices, monetary penalties, increased cost of operations, declines in user growth or engagement, negative publicity, or other harm to our business. See the section titled “Risk Factors — We are or may be subject to numerous risks relating to the need to comply with data and information privacy laws.” Many of these laws and regulations are subject to change or uncertain interpretation, and could result in claims, changes to our business practices, monetary penalties, increased cost of operations, declines in user growth or engagement, negatively publicity, or other harm to our business. As a result, we could be subject to actions based on negligence, various torts and trademark and copyright infringement, among other actions. See the sections titled “Risk Factors — If we infringe on the intellectual property (“IP”) of others, we could be exposed to substantial losses and face restrictions on our operations,” “Risk Factors — Litigation or legal proceedings could expose us to significant liabilities and have a negative impact on our reputation or business.” The varying and rapidly evolving regulatory framework on privacy and data protection across jurisdictions could result in claims, changes to our business practices, monetary penalties, increased cost of operations, or declines in user growth or engagement, or otherwise harm our business. See “Risk Factors — Compliance obligations imposed by new privacy laws, laws regulating social media platforms and online speech in the U.S., or industry practices may adversely affect our business.”

In the ordinary course of our business, we may process a significant volume of personal information and other regulated information from our users, employees and other third parties. Accordingly, we are, or may become, subject to numerous privacy and data protection obligations, including federal, state, local, and foreign laws, regulations, guidance, and industry standards related to privacy and data protection. Such obligations may include, without limitation, the Federal Trade Commission Act, the California Consumer Privacy Act of 2018 (“CCPA”), and the California Privacy Rights Act (“CPRA”).

The Platform facilitates online payments, including subscription fees, and therefore we will be subject to a variety of laws governing online transactions, payment card transactions and the automatic renewal of online agreements. In the U.S., these matters are regulated by, among other things, the federal Restore Online Shoppers Confidence Act (“ROSCA”) and various state laws.

12

Item 1A. Risk Factors

Investing in our Class A common stock involves risk. You should carefully consider the risks described below as well as all the other information in this Annual Report on Form 10-K, including the consolidated financial statements and the related notes included in this report. The risks and uncertainties described below are not the only risks and uncertainties we face. Additional risks and uncertainties not presently known to us or that we currently deem immaterial also may impair our business operations. If any of the following risks actually occur, our business, results of operations and financial condition could suffer. In that event, the trading price of our common stock could decline, and you may lose all or part of your investment. The risks discussed below also include forward-looking statements, and our actual results may differ substantially from those discussed in these forward-looking statements.

Risk Factor Summary

Our business is subject to numerous risks and uncertainties, including those highlighted in this Item 1A, that represent challenges that we face in connection with the successful implementation of our strategy and the growth of our business. In particular, the following considerations, among others, may offset our competitive strengths or have a negative effect on our business strategy, which could cause a decline in the price of shares of our Class A Common Stock or Warrants and result in a loss of all or a portion of your investment:

| ● | We may not continue to grow or maintain our base of consumer and business members or advertisers and may not be able to achieve or maintain profitability. |

| ● | Our recent and rapid growth in platform participants may not be sustainable or indicative of future performance. |

| ● | The market for the Platform and services may not be as large as we believe it to be, presently or in the future. |

| ● | We have limited experience with respect to determining optimal prices and pricing structure for our products and services, which may impact our financial results. |

| ● | Our business faces significant competition, and if we are unable to compete effectively, our business and operating results could be materially and adversely affected. |

| ● | The anticipated expansion of our operations, including in areas not part of our current operations, subjects us to additional risks that can adversely affect our operating results. |

| ● | Our business depends on hiring, developing and retaining highly skilled and dedicated employees, and any failure to do so, could have a material adverse effect on our business. |

| ● | Consumer tastes and preferences change over time and from time to time, as may public perception of us, which could be adversely affected by any negative publicity or reputational effects attributable to us or any of our affiliates or Outreach Program participants, which may impact our consumer and business members’ desire to utilize the Platform and materially affect our business and operating results. |

| ● | If we cannot maintain our company culture as we grow, our success, business and competitive position may be harmed. |

| ● | Our success depends on establishing and maintaining a strong brand and active engagement by business and consumer members and advertisers on the Platform, and any failure to establish and maintain a strong brand and member base, or adverse change in advertisers’ willingness to pay for advertising on the Platform, would adversely affect our future growth prospects. |

| ● | Our five core values may not always align with the interests of our business or our stockholders. |

| ● | Any failure by us to attract advertisers or any change in or loss of relationships with our existing advertisers or the amounts advertisers are able or willing to spend to advertise on the Platform could adversely affect our business and results of operations. |

13

| ● | If member engagement by business or consumer members on the Platform fails to increase or declines, we may not be able to maintain or expand our advertising revenue and our business and operating results will be harmed. |

| ● | Changes to our existing platform and services could fail to attract engagement by consumer and business members with, or advertising spending on, the Platform, which could materially affect our ability to generate revenues. |

| ● | We may not be able to able to expand into or to compete successfully in one or more of the highly competitive business areas in which we anticipate expanding, including e-commerce and the B2B market, or recently expanded into, including the D2C market that we recently entered into with our launch of EveryLife in July 2023. |

| ● | We are subject to payments-related risks. |

| ● | Uncertain global macro-economic and political conditions could materially adversely affect our results of operations and financial condition. |

| ● | We may in the future make acquisitions, and such acquisitions could disrupt our operations, and may have an adverse effect on our operating results. |

| ● | We are or may be subject to numerous risks relating to the need to comply with data and information privacy laws. |

| ● | We are subject to cybersecurity risks and interruptions or failures in our information technology systems and as we grow, we will need to expend additional resources to enhance our protection from such risks. |

|

|

● |

Management identified a material weakness in our internal control over financial reporting as of December 31, 2023. If we are unable to develop and maintain an effective system of internal control over financial reporting, we may not be able to accurately report our financial results in a timely manner, which may adversely affect investor confidence in us and materially and adversely affect our business and operating results. |

| ● | If we fail to adequately protect our proprietary intellectual property (“IP”) rights, our competitive position could be impaired and we may lose valuable assets, generate reduced revenue and incur costly litigation to protect our rights. |

| ● | Our business depends on continued and unimpeded access to our directory information and services on the internet, which in turn relies on third-party telecommunications and internet service providers. |

| ● | We may be unable to successfully grow our business if we fail to compete effectively with others to attract and retain our executive officers and other key management and technical personnel. |

| ● | The consumer finance and buy-now-pay-later (“BNPL”) industry has become subject to increased regulatory scrutiny, and Credova’s failure to manage Credova’s business to comply with new regulations would materially and adversely affect Credova’s business, results of operations and financial condition. | |

| ● | Credova’s results depend on prominent presentation, integration, and support of its platform by its merchants. | |

| ● | Current and future government regulations may negatively impact the demand for Credova’s merchants’ products and Credova’s operations and financial results. |

| ● | We may be exposed to risk if we cannot enhance, maintain, and adhere to our internal controls and procedures. |

| ● | Litigation or legal proceedings could expose us to significant liabilities and have a negative impact on our reputation or business. |

| ● | The consumer finance and BNPL industry is subject to various state and federal laws in the United States and federal law concerning consumer finance, and the costs to maintain compliance with such laws and regulations may be significant. |

| ● | Compliance obligations imposed by new privacy laws, laws regulating social media platforms and online speech in the U.S., or industry practices may adversely affect our business. |

| ● | We are a “controlled company” within the meaning of NYSE listing standards and comply with reduced corporate governance standards as a result. |

| ● | Natural disasters, including and not limited to unusual weather conditions, epidemic outbreaks, terrorist acts and political events could disrupt our business schedule. |

| ● | We may require substantial additional funding to finance our operations, but adequate additional financing may not be available when we need it, on acceptable terms or at all. |

14

Risks Related to Our Financial Performance and Operation Risks Related to Our Business

We have a very limited operating history, which makes it difficult to evaluate our business and prospects.

We have a very limited operating history, which makes it difficult to evaluate our business and prospects or forecast our future results. We are subject to the same risks and uncertainties frequently encountered by new companies in rapidly evolving markets. Our financial results in any given quarter can be influenced by numerous factors, many of which we are unable to predict or are outside of our control, including:

| ● | market adoption of the Platform; |

| ● | our ability to maintain and grow the Platform offerings, traffic, and engagement; |

| ● | our ability to attract and retain consumers and business members and advertisers; |

| ● | the success of our Outreach Program; |

| ● | the amount of advertising we can attract to the Platform and the pricing of our advertising products; |

| ● | the diversification and growth of our revenue sources beyond current sources, including our ability to successfully launch new products and realize revenues from increased e-commerce functionality on the Platform, including through consumer transactions executed in the Platform, and through the sale of our own D2C branded products; |

| ● | our ability to grow and generate revenue from our B2B offerings once launched; |

| ● | the development and introduction of new products, or services by us or our competitors; |

| ● | increases in marketing, sales, and other operating expenses that we may incur to grow and expand our operations and to remain competitive, and increased expenses we have incurred and will continue to incur as a public company; |

| ● | legislation and regulation that forces us to change our content policies and practices (including those relating to our products, services and advertisements of our business members); |

| ● | our ability to maintain and increase operating margins; |

| ● | system failures or breaches of security or privacy; |

| ● | competition in the markets in which we operate, and our ability to successfully compete; and |

| ● | negative publicity we may encounter as we seek to grow our values-focused business. |

To date, we have not generated significant revenues or achieved profitability, and may never generate significant revenues or become profitable.

We have incurred net losses since our inception, and we may not be able to achieve or maintain profitability in the future. We incurred net losses of $53.3 million and $7.0 million for the years ended December 31, 2023 and 2022. We generated revenue of $5.7 million and $0.5 million for the years ended December 31, 2023 and 2022. Our expenses will likely increase in the future as we develop and launch new offerings and platform features, expand in existing and new markets, increase our sales and marketing efforts and continue to invest in the Platform, as well as a result of our becoming a public company. Our efforts to grow our business may be more costly than we expect and may not result in increased revenue or growth in our business. We may be required to make significant capital investments and incur recurring or new costs, and our investments may not generate sufficient returns and our results of operations, financial condition and liquidity may be adversely affected. Any failure to increase our revenue sufficiently to keep pace with our investments and other expenses could prevent us from achieving or maintaining profitability or positive cash flow on a consistent basis or at all. If we are unable to successfully address these risks and challenges as we encounter them, our business, financial condition, results of operations and prospects could be adversely affected. If we are unable to generate adequate revenue growth and manage our expenses, we may continue to incur net losses in the future, which may be substantial, and we may never be able to achieve or maintain profitability. We also expect our costs and expenses to increase in future periods, which could negatively affect our future results of operations if our revenue does not increase. In particular, we intend to continue to expend significant funds to further develop the Platform. We will also face increased compliance costs associated with growth, the expansion of our business and consumer member base, and being a public company. Our efforts to grow our business may be more costly than we expect, or the rate of our growth in revenue may be slower than we expect, and we may not be able to increase our revenue enough to offset our increased operating expenses. We may incur significant losses in the future for a number of reasons, including the other risks described herein, and unforeseen expenses, difficulties, complications or delays, and other unknown events. If we are unable to achieve and sustain profitability, the value of our business may significantly decrease.

15

We believe there is a significant market opportunity for our business, and we intend to invest aggressively to capitalize on this opportunity. These efforts may be more costly than we expect and may not result in increased revenue or growth in our business. Any failure to increase our revenue sufficiently to keep pace with our investments and other expenses could prevent us from achieving or maintaining profitability or positive cash flow. Furthermore, if our future growth and operating performance fail to meet investor or analyst expectations, or if we have future negative cash flow or losses resulting from our investment in acquiring platform consumers and businesses or expanding our operations, this could have a material adverse effect on our business, financial condition and results of operations. We cannot assure you that we will ever achieve or sustain profitability and may continue to incur significant losses going forward. Any failure by us to achieve or sustain profitability on a consistent basis could cause the value of our Class A Common Stock and Private Warrants to decline.

Inflationary pressures, particularly in the United States, could have a material adverse effect on our business, cash flows and results of operations. The U.S. economy is currently experiencing a bout of inflation, in part due to a collision of booming demand with constrained supply, forcing prices to rise. To combat inflation, the U.S. Federal Reserve as well as counterparts in other countries have made a series of aggressive interest rate hikes commencing in 2022 and extending into early 2023 in an attempt to cool global economies. Inflation did not have a significant impact on our results of operations for the years ended December 31, 2023 and 2022. We anticipate a material increase in cost of sales – services and cost of goods sold for at least the remainder of 2024, if not longer.

We may require substantial additional funding to finance our operations, but adequate additional financing may not be available when we need it, on acceptable terms or at all.

Since our inception, we have financed our operations and capital expenditures primarily through equity investments. In the future, we could be required to raise capital through public or private financing or other arrangements. Such financing may not be available on acceptable terms, or at all, and our failure to raise capital when needed could harm our business. In addition, inflation rates in the U.S. have been higher than in previous years, which may result in higher costs of capital and constrained credit and liquidity. The Federal Reserve has raised, and may again raise, interest rates in response to concerns over inflation risk. Increases in interest rates could impact our ability to access the capital markets. We may sell equity securities or debt securities in one or more transactions at prices and in a manner as we may determine from time to time. If we sell any such securities in subsequent transactions, our current investors may be materially diluted. Any debt financing, if available, may involve restrictive covenants and could reduce our operational flexibility or achieve profitability. If we cannot raise funds on acceptable terms, we may not be able to grow our business or respond to competitive pressures and consumer member demand.

We may need to raise additional funds, and we may not be able to obtain additional debt or equity financing on favorable terms, if at all. If we raise additional equity financing, our shareholders may experience significant dilution of their ownership interests and the per share value of our Class A Common Stock and Private Warrants could decline. Furthermore, if we engage in debt financing, the holders of debt would have priority over the holders of our equity holders, and we may be required to accept terms that restrict our ability to incur additional indebtedness. We may also be required to take other actions that would otherwise be in the interests of the debt holders and force us to maintain specified liquidity or other ratios, any of which could harm our business, results of operations, and financial condition. If we need additional capital and cannot raise it on acceptable terms, we may not be able to, among other things:

| ● | develop or enhance our products; |

| ● | to expand our sales and marketing and research and development organizations; |

| ● | acquire complementary technologies, products or businesses; |

| ● | expand operations in the United States or internationally; |

16

| ● | hire, train, and retain employees; or |

| ● | respond to competitive pressures or unanticipated working capital requirements. |

Our failure to have sufficient capital to do any of these things could harm our business, financial condition, and results of operations.

Our past successful fundraising efforts do not guarantee long term liquidity, and we may be unable to obtain additional financing to fund the operation and growth of our business.

We may require additional financing to fund the operations or growth of our business but cannot guarantee that any such fundraising efforts will be successful and our past fundraising success should not be viewed as predictive of our ability to raise funds in the future. The failure to secure additional financing could have a material adverse effect on the continued development or growth of our business.

Our growth to date may not be sustainable or indicative of future performance.

We have experienced significant member growth in the number of business and consumer members participating on the Platform since our inception as Private PSQ in 2021. Our month over month (“MoM”) consumer member growth rate (as measured by the number of active consumer members as of the last day of each month) was 22% for the period from June 1, 2022 through December 31, 2023 and our MoM business growth rate (as measured by the number of business members that have joined the Platform as of the last day of each month) was 12% for the period from June 1, 2022, through December 31, 2023. Our growth has placed and is expected to continue to place significant demands on our management, financial, operational, technological and other resources. The growth and expansion of our business depends on a number of factors, including our ability to:

| ● | increase awareness of our brand and successfully compete with other companies that compete against us; |

| ● | launch new lines of products, services and functionality, including the ability to conduct e-commerce transactions in the Platform and our ability to expand our D2C product offerings; |

| ● | continue to innovate and introduce new offerings on the Platform; |

| ● | maintain and improve our technology platform supporting our app-based platform; |

| ● | identify and maintain key supplier and manufacturer relationships to support our D2C brands; |

| ● | maintain quality control over our product offerings; and |

| ● | expand the number of consumer and business members and advertisers using the Platform. |

The growth and expansion of our business, including launching new offerings, products, services and functionality such as e-commerce and D2C product sales, has and will continue to place significant demands on our management, technology and operations teams and require significant additional resources, financial and otherwise, to meet our needs, which may not be available in a cost-effective manner, or at all. We expect to expend substantial resources on:

| ● | sales and marketing efforts to increase brand awareness, further engaging our existing and prospective consumer and business members, and driving use of the Platform and sales of products and services through the Platform and supporting our D2C initiatives; |

| ● | product innovation, development and/or acquisition, distribution, marketing and sales efforts; |

| ● | technology platform maintenance to support sales of our products; and |

| ● | general administration, including increased finance, legal, compliance and accounting expenses associated with being a public company. |

17

Our investments may not result in the growth of our business. Even if these investments do result in the growth of our business, if we do not effectively manage our growth, we may not be able to successfully execute on our business plan, respond to competitive pressures, take advantage of market opportunities, satisfy the expectations of consumer or business members or maintain high-quality product offerings, any of which could adversely affect our business, financial condition, results of operations and prospects. You should not rely on our historical rate of growth as an indication of our future performance or the rate of growth we may experience going forward or with respect to any new products or services we may introduce.

In addition, to support continued growth, we must effectively integrate, develop and motivate existing and new employees while maintaining our corporate culture. We face significant competition for personnel. To attract top talent, we will need to offer competitive compensation and benefits packages. We may also need to increase our employee compensation levels to remain competitive in attracting and retaining talented employees. In addition, we may face challenges in attracting employees whose values align with our own. The risks associated with a rapidly growing workforce may be particularly acute as we expand further into areas, such as the D2C market. Additionally, we may not be able to hire new employees quickly enough to meet our needs. If we fail to effectively manage our hiring needs or successfully integrate new hires, our efficiency, ability to meet forecasts and employee morale, productivity and retention could suffer, which could have an adverse effect on our business, financial condition, results of operations and prospects.