Table of Contents

As filed with the Securities and Exchange Commission on February 14, 2023

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-4

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

ALPHA HEALTHCARE ACQUISITION CORP. III

(Exact name of Registrant as specified in its charter)

| Delaware | 6770 | 86-1645738 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification No.) |

1177 Avenue of the Americas, 5th Floor

New York, New York 10036

Telephone: (646) 494-3296

(Address, including zip code and telephone number, including area code, of Registrant’s principal executive offices)

Rajiv Shukla

Chairman and Chief Executive Officer

1177 Avenue of the Americas, 5th Floor

New York, New York 10036

(646) 494-3296

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

| Laurie A. Burlingame Jocelyn M. Arel |

Scott R. Jones Troutman Pepper Hamilton Sanders LLP 400 Berwyn Park 899 Cassatt Road Berwyn, PA 19312 (610) 640-7800 |

Approximate date of commencement of proposed sale of the securities to the public: As soon as practicable after this Registration Statement is declared effective and all other conditions to the transactions contemplated by the Business Combination Agreement described in the enclosed proxy statement/prospectus have been satisfied or waived.

If the securities being registered on this Form are being offered in connection with the formation of a holding company and there is compliance with General Instruction G, check the following box. ☐

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |||

| Non-accelerated filer | ☒ | Smaller reporting company | ☒ | |||

| Emerging growth company | ☒ | |||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

If applicable, place an X in the box to designate the appropriate rule provision relied upon in conducting this transaction:

|

|

Exchange Act Rule 13e-4(i) (Cross-Border Issuer Tender Offer) |

☐ | ||||

| Exchange Act Rule 14d-1(d) (Cross-Border Third-Party Tender Offer) |

☐ |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said section 8(a), may determine.

Table of Contents

The information in this preliminary proxy statement/prospectus is not complete and may be changed. These securities may not be issued until the registration statement filed with the U.S. Securities and Exchange Commission is effective. This preliminary proxy statement/prospectus does not constitute an offer to sell or a solicitation of offers to buy these securities in any jurisdiction in which such offer or sale is not permitted.

PRELIMINARY — SUBJECT TO COMPLETION, DATED FEBRUARY 14, 2023

PROXY STATEMENT FOR SPECIAL MEETING OF

ALPHA HEALTHCARE ACQUISITION CORP. III

PROSPECTUS FOR 15,000,000 SHARES OF CLASS A COMMON STOCK

All of the members of the board of directors of Alpha Healthcare Acquisition Corp. III, a Delaware corporation (“ALPA”), voting on the transaction approved the Business Combination Agreement, dated as of January 4, 2023 (as amended from time to time, the “Business Combination Agreement”), by and among ALPA, Candy Merger Sub, Inc., a Delaware corporation and wholly owned subsidiary of ALPA (“Merger Sub”), and Carmell Therapeutics Corporation (“Carmell”), pursuant to which Merger Sub will merge with and into Carmell™, with Carmell surviving as a wholly owned subsidiary of ALPA (the “Business Combination”). In connection with the consummation of the Business Combination, ALPA will change its corporate name to “Carmell Therapeutics Corporation” In this proxy statement/prospectus, when we refer to “Carmell” we mean Carmell Therapeutics Corporation prior to the consummation of the Business Combination, and when we refer to “New Carmell” or the “Combined Company” we mean Alpha Healthcare Acquisition Corp. III, under its new corporate name after the consummation of the Business Combination.

At the effective time of the Business Combination (the “Effective Time”), (i) each outstanding share of Carmell common stock will be cancelled and converted into the right to receive a number of shares of common stock of New Carmell (the “New Carmell common stock”) equal to the Exchange Ratio (as defined in this proxy statement/prospectus); (ii) each outstanding share of Carmell preferred stock will be cancelled and converted into the right to receive a number of shares of New Carmell common stock equal to (A) the aggregate number of shares of Carmell common stock that would be issued upon conversion of the shares of Carmell preferred stock based on the applicable conversion ratio immediately prior to the Effective Time, multiplied by (B) the Exchange Ratio; and (iii) each outstanding Carmell option or warrant will be converted into an option or warrant, as applicable, to purchase a number of shares of Class A Common Stock equal to (A) the number of shares of Carmell common stock subject to such option or warrant multiplied by (B) the Exchange Ratio at an exercise price per share equal to the current exercise price per share for such option or warrant divided by the Exchange Ratio; in each case, rounded down to the nearest whole share. See the section titled “Proposal 1: The Business Combination Proposal.” Based on an assumed closing date of [●], 2023 for the Business Combination, the Exchange Ratio is approximately [●]. Based on this Exchange Ratio, the total number of shares of New Carmell common stock expected to be issued in connection with the Business Combination (not including shares that will be issuable as consideration or upon exercise of outstanding stock options) is approximately [●] shares, and these shares are expected to represent approximately [●]% and [●]% of the issued and outstanding shares of New Carmell common stock immediately following the closing of the Business Combination, assuming no redemptions occur and maximum redemptions occur, respectively.

Proposals to approve the Business Combination Agreement and the other matters discussed in this proxy statement/prospectus will be presented for approval by ALPA’s stockholders at the special meeting of stockholders of ALPA (the “Special Meeting”) scheduled to be held on [●], 2023, in virtual format.

ALPA’s units, Class A Common Stock and warrants are currently listed on The Nasdaq Capital Market (“Nasdaq”) under the symbols ALPAU, ALPA and ALPAW, respectively. Each unit consists of one share of Class A Common Stock and one-fourth of one warrant. ALPA intends to apply to continue the listing of the shares of New Carmell common stock and warrants effective upon the consummation of the Business Combination on Nasdaq under the proposed symbols “CTCX” and “CTCXW,” respectively. ALPA will not have units traded on Nasdaq following consummation of the Business Combination. It is a condition of the consummation of the Business Combination that the New Carmell common stock is approved for listing on Nasdaq (subject only to official notice of issuance thereof and initial listing requirements), but there can be no assurance such listing condition will be met. If such listing condition is not met, the Business Combination will not be consummated unless the listing condition set forth in the Business Combination Agreement is waived by the parties to that agreement.

ALPA is an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012, as amended, and has elected to comply with certain reduced public company reporting requirements.

This proxy statement/prospectus incorporates by reference important business and financial information about ALPA from documents that are not included in or delivered with this proxy statement/prospectus. You can obtain documents incorporated by reference in this proxy statement/prospectus and other filings of ALPA with the Securities and Exchange Commission (the “SEC”) by visiting its website at www.sec.gov or requesting them in writing or by telephone from ALPA at the following address:

1177 Avenue of the Americas, 5th Floor

New York, New York 10036

Telephone: (646) 494-3296

You will not be charged for any of these documents that you request. Stockholders requesting documents should do so by [●], 2023 (five business days prior to the date of the Special Meeting) in order to receive them before the Special Meeting.

This proxy statement/prospectus provides you with detailed information about the Business Combination and other matters to be considered at the Special Meeting. We urge you to carefully read this entire document and the documents incorporated herein by reference. You should also carefully consider the risk factors described in “Risk Factors” beginning on page 24 of this proxy statement/prospectus.

Neither the SEC nor any state securities commission has approved or disapproved of the transactions described in this proxy statement/prospectus or the securities referenced herein, passed upon the merits or fairness of the Business Combination or related transactions, or passed upon the adequacy or accuracy of this proxy statement/prospectus. Any representation to the contrary is a criminal offense.

The proxy statement/prospectus is dated [●], 2023 and is first being mailed to stockholders of ALPA on or about [●], 2023.

Table of Contents

NOTICE OF SPECIAL MEETING OF STOCKHOLDERS

OF ALPHA HEALTHCARE ACQUISITION CORP. III

To Be Held On [●], 2023

To the Stockholders of Alpha Healthcare Acquisition Corp.:

NOTICE IS HEREBY GIVEN that a special meeting of stockholders (the “Special Meeting”) of Alpha Healthcare Acquisition Corp. III, a Delaware corporation (“ALPA,” “we,” “our” or “us”), will be held on [●], 2023, at [●]A.M. Eastern time, via live webcast at the following address: [●]. You will need the 12-digit meeting control number that is printed on your proxy card to enter the Special Meeting. ALPA recommends that you log in at least 15 minutes before the Special Meeting to ensure you are logged in when the Special Meeting starts. Please note that you will not be able to attend the Special Meeting in person. You are cordially invited to attend the Special Meeting to consider the following proposals (the “Proposals”):

| 1. | to (a) adopt and approve the Business Combination Agreement, dated as of January 4, 2023 (the “Business Combination Agreement”), among ALPA, Candy Merger Sub, Inc., a Delaware corporation and a wholly owned subsidiary of ALPA (“Merger Sub”), and Carmell Therapeutics Corporation, a Delaware corporation (“Carmell”), pursuant to which Merger Sub will merge with and into Carmell, with Carmell surviving the merger as a wholly-owned subsidiary of ALPA (the “Combined Company”) and (b) approve such merger and the other transactions contemplated by the Business Combination Agreement (the “Business Combination”). Subject to the terms and conditions set forth in the Business Combination Agreement, at the effective time of the Business Combination (the “Effective Time”): |

| (i) | each outstanding share of Carmell common stock will be cancelled and converted into the right to receive a number of shares of common stock of New Carmell (the “New Carmell common stock”) equal to the Exchange Ratio (as defined in the accompanying proxy statement/prospectus); |

| (ii) | each outstanding share of Carmell preferred stock will be cancelled and converted into the right to receive a number of shares of New Carmell common stock equal to (A) the aggregate number of shares of Carmell common stock that would be issued upon conversion of the shares of Carmell preferred stock based on the applicable conversion ratio immediately prior to the Effective Time, multiplied by (B) the Exchange Ratio (as defined in the Business Combination Agreement); |

| (iii) | each outstanding Carmell option or warrant will be converted into an option or warrant, as applicable, to purchase a number of shares of Class A Common Stock equal to (A) the number of shares of Carmell common stock subject to such option or warrant multiplied by (B) the Exchange Ratio at an exercise price per share equal to the current exercise price per share for such option or warrant divided by the Exchange Ratio; in each case, rounded down to the nearest whole share; and |

| (iv) | each share of Class A Common Stock and each share of Class B Common Stock that is issued and outstanding immediately prior to the Effective Time shall become one share of New Carmell Common Stock. |

We refer to this proposal as the “Business Combination Proposal.” A copy of the Business Combination Agreement is attached to the accompanying proxy statement/prospectus as Annex A;

| 2. | to approve, assuming the Business Combination Proposal is approved and adopted, a proposed third amended and restated certificate of incorporation (the “Proposed Charter,” a copy of which is attached to the accompanying proxy statement/prospectus as Annex C), which will amend and restate ALPA’s current Second Amended and Restated Certificate of Incorporation (the “Current Charter”), and which Proposed Charter will be in effect upon the closing (the “Closing”) of the Business Combination (the “Charter Amendment Proposal”); |

Table of Contents

| 3. | to approve, on a non-binding advisory basis, the following material differences between the Proposed Charter and the Current Charter, which are being presented pursuant to guidance of the Securities and Exchange Commission as seven separate sub-proposals (the “Advisory Charter Amendment Proposals”): |

| (a) | Advisory Charter Proposal A — to change the corporate name of the Combined Company to “Carmell Therapeutics Corporation”; |

| (b) | Advisory Charter Proposal B — to increase the authorized shares of common stock of ALPA to 250,000,000 shares; |

| (c) | Advisory Charter Proposal C — to increase the authorized shares of “blank check” preferred stock that the Combined Company’s board of directors could issue to 20,000,000 shares; |

| (d) | Advisory Charter Proposal D — to provide that the removal of any director be only for cause and by the affirmative vote of at least 66 2⁄3% of the Combined Company’s then-outstanding shares of capital stock entitled to vote generally in the election of directors; |

| (e) | Advisory Charter Proposal E — to provide that certain amendments to provisions of the Proposed Charter will require the approval of at least 66 2⁄3% of the Combined Company’s then-outstanding shares of capital stock entitled to vote on such amendment; |

| (f) | Advisory Charter Proposal F — to make the Combined Company’s corporate existence perpetual instead of requiring ALPA to be dissolved and liquidated 24 months following the closing of ALPA’s initial public offering (the “Initial Public Offering”), and to remove from the Proposed Charter the various provisions applicable only to special purpose acquisition companies; and |

| (g) | Advisory Charter Proposal G — to remove the provision that allows the Class B common stockholders to act by written consent as opposed to holding a stockholders meeting; |

| 4. | to approve, assuming the Business Combination Proposal is approved and adopted, for purposes of complying with the applicable provisions of Nasdaq Stock Exchange Listing Rule 5635 (the “Nasdaq Listing Rule”), the issuance of up to 15,000,000 shares of New Carmell common stock in connection with the Business Combination, which amount will be determined as described in more detail in the accompanying proxy statement/prospectus (the “Nasdaq Proposal”); |

| 5. | to approve, assuming the Business Combination Proposal is approved and adopted, the appointment of nine directors who, upon consummation of the Business Combination, will become directors of the Combined Company (the “Director Election Proposal”); |

| 6. | to approve, assuming the Business Combination Proposal is approved and adopted, the Carmell Therapeutics Corporation 2023 Long-Term Incentive Plan, a copy of which is attached to the accompanying proxy statement/prospectus as Annex D, which will become effective as of and contingent on the consummation of the Business Combination (the “Incentive Plan Proposal”); and |

| 7. | to approve a proposal to adjourn the Special Meeting to a later date or dates if it is determined that more time is necessary or appropriate, in the judgment of the board of directors of ALPA (the “Board”) or the officer presiding over the Special Meeting, for ALPA to consummate the Business Combination (the “Adjournment Proposal”). |

Only holders of record of Class A Common Stock and Class B Common Stock of ALPA (collectively, the “ALPA Common Stock”) at the close of business on [●], 2023 (the “Record Date”) are entitled to notice of the Special Meeting and to vote at the Special Meeting and any adjournments or postponements of the Special Meeting. A complete list of ALPA stockholders of record entitled to vote at the Special Meeting will be available for ten days before the Special Meeting at the principal executive offices of ALPA for inspection by stockholders during ordinary business hours for any purpose germane to the Special Meeting.

Pursuant to the Current Charter, ALPA is providing its public stockholders (“Public Stockholders”) with the opportunity to redeem, upon the Closing, the shares of Class A Common Stock (the “Public Shares”) issued in

Table of Contents

the Initial Public Offering then held by them for cash equal to their pro rata share of the aggregate amount on deposit (as of two business days prior to the Closing) in the trust account (the “Trust Account”) that holds the proceeds (including interest but less franchise and income taxes payable) of the Initial Public Offering. For illustrative purposes, based on funds in the Trust Account of approximately $[●] on the Record Date, the estimated per share redemption price would have been approximately $[●]. Public Stockholders may elect to redeem Public Shares even if they vote for the Business Combination Proposal. A Public Stockholder, together with any of his, her or its affiliates or any other person with whom it is acting in concert or as a “group” (as defined under Section 13 of the Securities Exchange Act of 1934, as amended), will be restricted from redeeming in the aggregate his, her or its shares or, if part of such a group, the group’s shares, with respect to 20% or more of the Public Shares issued in the Initial Public Offering. The Sponsor and ALPA’s other initial stockholders have agreed to waive their redemption rights with respect to any shares of ALPA Common Stock they may hold in connection with the Closing, and such shares will be excluded from the pro rata calculation used to determine the per-share redemption price. The Sponsor and ALPA’s other initial stockholders have agreed to vote any shares of ALPA Common Stock owned by them in favor of the Business Combination Proposal, which represent approximately [●]% of the voting power of ALPA as of the Record Date. These holders also have agreed to vote their shares in favor of all other Proposals being presented at the Special Meeting.

Pursuant to ALPA’s bylaws, a majority of the shares of ALPA Common Stock entitled to vote, represented at the Special Meeting or by proxy, will constitute a quorum for the transaction of business at the Special Meeting. Under the Delaware General Corporation Law, shares that are voted “abstain” or “withheld” are counted as present for purposes of determining whether a quorum is present at the Special Meeting. Because the Proposals are “non-discretionary” items, your broker will not be able to vote uninstructed shares for any of the Proposals. As a result, if you do not provide voting instructions, a broker “non-vote” will be deemed to have occurred for each of the Proposals. Broker “non-votes” will not be counted as present for purposes of determining whether a quorum is present.

The approval of the Business Combination Proposal, of the Advisory Charter Amendment Proposals, the Nasdaq Proposal, the Incentive Plan Proposal and the Adjournment Proposal each require the affirmative vote of the holders of a majority of the shares of ALPA Common Stock cast by the stockholders represented in person (which would include presence at a virtual meeting) or by proxy and entitled to vote thereon at the Special Meeting, voting together as a single class.

The approval of the Charter Amendment Proposal requires the affirmative vote of a majority of the issued and outstanding shares of each of the ALPA Class A Common Stock and ALPA Class B Common Stock, voting separately.

The approval of the Director Election Proposal requires a plurality vote of the ALPA Common Stock present (which would include presence at a virtual meeting) or represented by proxy and entitled to vote at the Special Meeting. “Plurality” means that the individuals who receive the largest number of votes cast “FOR” are elected as directors. Consequently, any shares not voted “FOR” a particular nominee (whether as a result of an abstention, a direction to withhold authority or a broker non-vote) will not be counted in the nominee’s favor.

If the Business Combination Proposal is not approved, the Nasdaq Proposal, the Charter Amendment Proposal, the Advisory Charter Amendment Proposals, the Director Election Proposal and the Incentive Plan Proposal will not be presented to the ALPA stockholders for a vote. The approval of the Business Combination Proposal, the Nasdaq Proposal, the Charter Amendment Proposal, the Director Election Proposal and the Equity Incentive Plan Proposal are preconditions to the Closing.

As of the Record Date, there was approximately $[●] in the Trust Account. Each redemption of Public Shares by Public Stockholders will decrease the amount in the Trust Account. ALPA will not redeem Public Shares in an amount that would cause it to have net tangible assets of less than $5,000,001.

Table of Contents

Your attention is directed to the proxy statement/prospectus accompanying this notice (including the Annexes thereto) for a more complete description of the proposed Business Combination and related transactions and each of the Proposals. We encourage you to read this proxy statement/prospectus carefully. If you have any questions or need assistance voting your shares, please call us at (646) 494-3296.

| [●], 2023 | ||

| By Order of the Board of Directors | ||

| Rajiv Shukla | ||

| Chief Executive Officer and Chairman of the Board | ||

Table of Contents

| Page | ||||

| 1 | ||||

| 1 | ||||

| 2 | ||||

| 5 | ||||

| 14 | ||||

| 22 | ||||

| 24 | ||||

| 65 | ||||

| 70 | ||||

| UNAUDITED PRO FORMA CONDENSED COMBINED FINANCIAL INFORMATION |

115 | |||

| 133 | ||||

| 135 | ||||

| 137 | ||||

| 139 | ||||

| 141 | ||||

| 147 | ||||

| 148 | ||||

| 160 | ||||

| 218 | ||||

| 220 | ||||

| DESCRIPTION OF NEW CARMELL’S SECURITIES AFTER THE BUSINESS COMBINATION |

225 | |||

| 233 | ||||

| 244 | ||||

| 256 | ||||

| 256 | ||||

| STOCKHOLDER COMMUNICATIONS AND DELIVERY OF DOCUMENTS TO STOCKHOLDERS |

256 | |||

| 256 | ||||

| F-1 | ||||

| A-1 | ||||

| B-1 | ||||

| C-1 | ||||

| Annex D Carmell Therapeutics Corporation 2023 Long-Term Incentive Plan |

D-1 | |||

Table of Contents

Certain information contained in this document relates to or is based on studies, publications, surveys and other data obtained from third-party sources and ALPA’s own internal estimates and research. While we believe these third-party sources to be reliable as of the date of this proxy statement/prospectus, we have not independently verified the market and industry data contained in this proxy statement/prospectus or the underlying assumptions relied on therein. Finally, while we believe our own internal research is reliable, such research has not been verified by any independent source.

This document contains references to trademarks, trade names and service marks belonging to other entities. Solely for convenience, trademarks, trade names and service marks referred to in this proxy statement/prospectus may appear without the ® or TM symbols, but such references are not intended to indicate, in any way, that the applicable licensor will not assert, to the fullest extent under applicable law, its rights to these trademarks and trade names. We do not intend our use or display of other companies’ trade names, trademarks or service marks to imply a relationship with, or endorsement or sponsorship of us by, any other companies.

1

Table of Contents

As used in this proxy statement/prospectus, unless otherwise noted or the context otherwise requires, references to:

“2023 Plan” means the Carmell Therapeutics Corporation 2023 Long-Term Incentive Plan, approved by the Board of ALPA, effective as of and contingent on the consummation of the Business Combination.

“ALPA” means Alpha Healthcare Acquisition Corp. III, a Delaware corporation.

“ALPA Common Stock” means the Class A Common Stock and Class B Common Stock of ALPA.

“ALPA’s initial stockholders” means the Sponsor and the independent directors of ALPA.

“Board” means ALPA’s board of directors.

“Business Combination” means the transactions contemplated by the Business Combination Agreement.

“Business Combination Agreement” means the Business Combination Agreement, dated as of January 4, 2023, by and among ALPA, Merger Sub and Carmell, as amended from time to time.

“Business Combination Consideration” means the consideration to be paid to holders of Carmell common stock, Carmell preferred stock, Carmell options and Carmell warrants upon the closing of the Business Combination pursuant to the Business Combination Agreement.

“Carmell” means Carmell Therapeutics Corporation, a Delaware corporation.

“Carmell common stock” means the common stock, par value $0.001 per share, of Carmell.

“Carmell options” means options to purchase Carmell common stock, whether vested or unvested.

“Carmell preferred stock” means the preferred stock, par value $0.001 per share, of Carmell designated as Series A redeemable convertible preferred stock (“Series A preferred”), Series B redeemable convertible preferred stock (“Series B preferred”), and Series C redeemable convertible preferred stock (“Series C preferred”).

“Carmell warrants” means warrants to purchase Carmell common stock.

“Class A Common Stock” means the Class A Common Stock of ALPA.

“Class B Common Stock” means the Class B Common Stock of ALPA, which is convertible into shares of Class A Common Stock on a one-for-one basis.

“Closing” means the closing of the Business Combination.

“Code” means the Internal Revenue Code of 1986, as amended.

“Combined Company” means ALPA subsequent to the Business Combination (also referred to herein as “New Carmell”).

“Continental” means Continental Stock Transfer & Trust Company, transfer agent for ALPA.

“Current Charter” means ALPA’s second amended and restated certificate of incorporation.

2

Table of Contents

“DGCL” means the Delaware General Corporation Law, as amended.

“Dollars” or “$” means U.S. dollars.

“Effective Time” means the effective time of the Business Combination.

“Exchange Act” means the Securities Exchange Act of 1934, as amended.

“Exchange Ratio” shall have the meaning given to such term in the Business Combination Agreement.

“Founder Shares” mean the shares of Class B Common Stock initially purchased by the Sponsor, and the shares of Class A Common Stock issuable upon conversion thereof.

“HSR Act” means the Hart-Scott-Rodino Antitrust Improvements Act of 1976, as amended.

“Initial Public Offering” means the initial public offering of ALPA, which closed on July 29, 2021.

“Investor Rights Agreement” means the investor rights agreement into which ALPA, certain of the Carmell stockholders and certain of the ALPA stockholders will enter into at the Effective Time.

“JOBS Act” means the Jumpstart Our Business Startups Act of 2012, as amended.

“Cabrillo” means Cabrillo Capital Markets, LLC, ALPA’s financial advisor in connection with the Business Combination.

“Merger Sub” means Candy Merger Sub, Inc., a Delaware corporation and wholly owned subsidiary of ALPA.

“Nasdaq” means The Nasdaq Capital Market.

“New Carmell” refers the Combined Company following the consummation of the Business Combination.

“New Carmell Board” means the board of directors of New Carmell.

“New Carmell common stock” means the common stock, par value $0.0001 per share, of New Carmell.

“New Carmell Public Warrant” means each Public Warrant after the Business Combination.

“Private Placement Shares” means the shares of Class A Common Stock that were issued in the private placement that closed concurrently with the Initial Public Offering.

“Proposals” means each of the Proposals to be considered for approval at the Special Meeting.

“Proposed Charter” means the third amended and restated certificate of incorporation of ALPA, attached to this proxy statement/prospectus as Annex C.

“Public Shares” means the shares of Class A Common Stock issued in the Initial Public Offering.

“Public Stockholders” means holders of Class A Common Stock.

“Public Warrant” means each whole Warrant issued in the Initial Public Offering.

“Record Date” means [●], 2023.

3

Table of Contents

“Sarbanes-Oxley Act” means the Sarbanes-Oxley Act of 2002.

“Securities Act” means the Securities Act of 1933, as amended.

“Special Meeting” means the special meeting of stockholders of ALPA, scheduled to be held on [●], 2023 at [●]A.M.

“Sponsor” means AHAC Sponsor III LLC, a Delaware limited liability company.

“Trust Account” means the trust account maintained by Continental, acting as trustee, established for the benefit of holders of Class A Common Stock in connection with the Initial Public Offering.

“Units” mean units of ALPA consisting of one share of Class A Common Stock and one-fourth of one Warrant.

“Warrants” means warrants to purchase Class A Common Stock.

4

Table of Contents

The questions and answers below highlight only selected information from this proxy statement/prospectus and only briefly address some commonly asked questions about the Special Meeting and the Proposals to be presented at the Special Meeting, including with respect to the proposed Business Combination. The following questions and answers do not include all the information that may be important to ALPA stockholders. ALPA stockholders are urged to read this entire proxy statement/prospectus, including the Annexes and the other documents referred to herein.

QUESTIONS AND ANSWERS ABOUT THE BUSINESS COMBINATION

| Q: | What is the Business Combination? |

| A: | ALPA, Merger Sub, and Carmell have entered into the Business Combination Agreement, pursuant to which Merger Sub will merge with and into Carmell, with Carmell surviving the Business Combination as a wholly owned subsidiary of ALPA. |

| Q: | Why am I receiving this proxy statement/prospectus? |

| A: | ALPA and Carmell have agreed to a Business Combination under the terms of the Business Combination Agreement that is described in this proxy statement/prospectus. A copy of the Business Combination Agreement is attached to this proxy statement/prospectus as Annex A, and ALPA encourages its stockholders to read it in its entirety. ALPA’s stockholders are being asked to consider and vote upon a proposal to approve the Business Combination Agreement, which, among other things, provides for the Business Combination whereby Merger Sub will merge with and into Carmell, with Carmell surviving as a wholly owned subsidiary of ALPA. See the section titled “Proposal 1: The Business Combination Proposal.” |

This document is a proxy statement because the Board is soliciting proxies using this proxy statement/prospectus from its stockholders. It is a prospectus because ALPA, in connection with the Business Combination, is offering shares of New Carmell common stock in exchange for the outstanding shares of Carmell common stock and Carmell preferred stock. See the section titled “Proposal 1: The Business Combination Proposal.”

| Q: | What will Carmell stockholders and holders of Carmell options and Carmell warrants receive in the Business Combination? |

| A: | If the Business Combination is completed: |

| • | Each outstanding share of Carmell common stock will be cancelled and converted into the right to receive a number of shares of New Carmell common stock equal to the Exchange Ratio (rounded down to the nearest whole share). |

| • | Each outstanding share of Carmell preferred stock will be cancelled and converted into the right to receive a number of shares of New Carmell common stock equal to (A) the aggregate number of shares of Carmell common stock that would be issued upon conversion of the shares of Carmell preferred stock based on the applicable conversion ratio immediately prior to the Effective Time, multiplied by (B) the Exchange Ratio (rounded down to the nearest whole share). |

| • | Each outstanding Carmell option or Carmell warrant will be converted into an option or warrant, as applicable, to purchase a number of shares of New Carmell common stock equal to (A) the number of shares of Carmell common stock subject to such option or warrant multiplied by (B) the Exchange Ratio at an exercise price per share equal to the current exercise price per share for such option or warrant divided by the Exchange Ratio (rounded down to the nearest whole share). Each option and warrant to purchase shares of New Carmell common stock will otherwise be subject to the same terms as the Carmell option and Carmell warrants, as applicable, prior to such conversion. |

5

Table of Contents

The consideration described in the foregoing bullets is referred to collectively as the “Business Combination Consideration.” Based on the number of shares of Carmell common stock and Carmell preferred stock outstanding and the number of shares of Carmell common stock underlying outstanding Carmell options and Carmell warrants, in each case as of the Record Date, the total number of shares of New Carmell common stock expected to be issued as Business Combination Consideration is approximately shares. See the section titled “Proposal 1: The Business Combination Proposal — Structure of the Business Combination.”

| Q: | When do you expect the Business Combination to be completed? |

| A: | It is currently anticipated that the Business Combination will be consummated promptly following the Special Meeting, which is set for [●], 2023; however, the Special Meeting could be adjourned, as described herein. ALPA cannot assure you of when or if the Business Combination will be completed, and it is possible that factors outside of the control of ALPA and Carmell could result in the Business Combination being completed at a different time or not at all. ALPA must first obtain the approval of its stockholders for certain of the Proposals set forth in this proxy statement/prospectus. |

| Q: | What happens if the Business Combination is not consummated? |

| A: | If ALPA does not complete the Business Combination with Carmell, for whatever reason, ALPA will search for another target business with which to complete a business combination. If ALPA does not complete the Business Combination with Carmell or another business combination by July 29, 2023 (or such later date as may be approved by ALPA stockholders in an amendment to its Current Charter), ALPA must redeem 100% of the Public Shares, at a per-share price, payable in cash, equal to the aggregate amount then on deposit in the Trust Account, including interest earned on the funds held in the Trust Account and not previously released to ALPA to pay its franchise and income taxes on such amounts (less up to $100,000 of such interest to pay dissolution expenses), divided by the number of then outstanding shares of Class A Common Stock. The Sponsor and ALPA’s officers and directors have waived their redemption rights with respect to their Founder Shares in the event a business combination is not effected by ALPA in the required time period, and, accordingly, the Founder Shares held by them will be worthless. Additionally, in the event of such liquidation, there will be no distribution with respect to the outstanding Warrants. Accordingly, the Warrants will expire worthless. In addition, recent changes in U.S. federal tax law may increase ALPA’s tax liabilities if the stockholder redemption occurs on or after January 1, 2023. |

| Q: | Did the Board obtain a third-party valuation or fairness opinion in determining whether or not to proceed with the Business Combination? |

| A: | Yes, the Board obtained a fairness opinion from Cabrillo in connection with its determination to approve the Business Combination. See “Proposal 1: The Business Combination Proposal — Opinion of ALPA’s Financial Advisor” for further information regarding this opinion. |

| Q: | What is the expected per share value of the cash consideration to be received by Carmell in the Business Combination? |

| A: | The net cash to the balance sheet of Carmell and the total number of New Carmell common stock will depend upon the extent to which Public Stockholders exercise their redemption rights with respect to Public Shares. Although the parties to the Business Combination have deemed the value of New Carmell common stock to be equal to $10.00 per share for determining the number of New Carmell common stock issuable to holders of Carmell’s securities the cash value per share of New Carmell common stock and the trading price of New Carmell common stock following the Business Combination may be substantially less than $10.00 per share. Set forth below is a calculation of the net cash per New Carmell common stock resulting from the proceeds of the Trust Account in a no redemption scenario, 25% redemption scenario, 75% redemption scenario, and the maximum redemption scenario. Such calculations are based upon (i) cash held in the Trust |

6

Table of Contents

| Account as of the Record Date of approximately $[●] per Public Share (rounded to the nearest cent) and (ii) transaction expenses of $[●] million. The calculations do not assume the receipt of any debt or equity financing in connection with the closing of the Business Combination. |

| Assuming No Redemption(1) |

Assuming Redemption(2) |

Assuming Redemption(3) |

Assuming Redemption(4) | |||||

| New Carmell common stock not redeemed | [●] | [●] | [●] | [●] | ||||

| Gross Cash Proceeds of Trust Account at $[●] per share | [●] | [●] | [●] | [●] | ||||

| Transaction Expenses | [●] | [●] | [●] | [●] | ||||

| Net Cash Proceeds of Trust Account at $[●] | [●] | [●] | [●] | [●] | ||||

| Total Shares Outstanding | [●] | [●] | [●] | [●] | ||||

| Net Cash per New Carmell common stock Outstanding | [●] | [●] | [●] | [●] |

| (1) | This scenario assumes that no Public Shares are redeemed by the Public Stockholders. |

| (2) | This scenario assumes that [●] Public Shares are redeemed by the Public Stockholders. |

| (3) | This scenario assumes that [●] Public Shares are redeemed by the Public Stockholders. |

| (4) | This scenario assumes that [●] Public Shares are redeemed by the Public Stockholders. |

QUESTIONS AND ANSWERS ABOUT ALPA’S SPECIAL MEETING

| Q: | How do I attend a virtual meeting? |

| A: | As a registered stockholder, along with this proxy statement/prospectus, you received a proxy card from Continental, ALPA’s transfer agent, which contains instructions on how to attend the virtual Special Meeting, including the URL address and your control number. You will need your control number for access. If you do not have your control number, contact Continental at (917) 262-2373, or email Continental at proxy@continentalstock.com. |

You can pre-register to attend the virtual Special Meeting starting on [●], 2023 (five business days prior to the meeting). Enter the following URL address into your browser ([●]), then enter your control number, name and email address. Once you pre-register, you can vote or enter questions in the chat box. At the start of the Special Meeting, you will need to re-login using the same control number and, if you want to vote during the meeting, you will be prompted to enter your control number again.

Beneficial owners who own their Class A Common Stock through a bank, broker or other nominee will need to contact Continental to receive a control number. If you plan to vote at the Special Meeting, you will need to have a legal proxy from your broker, bank or other nominee or, if you would like to join and not vote, Continental can issue you a guest control number with proof of ownership. Either way you must contact Continental at the number or email address above for specific instructions on how to receive the control number. Please allow up to 72 hours prior to the meeting for processing your control number.

If you do not have internet capabilities, you can listen only to the Special Meeting by dialing 1-877-770-3647 (toll-free, within the U.S. and Canada) or 1-312-780-0854 (with toll, outside the U.S. or Canada) and when prompted, enter the pin [●]#. This method supports listening only, so you will not be able to vote or enter questions during the Special Meeting.

| Q: | Are there any other matters being presented to ALPA stockholders at the meeting? |

| A: | In addition to voting on the Business Combination Proposal, assuming it is approved and adopted, the stockholders of ALPA will vote on the following: |

| 1. | To approve the Proposed Charter, which will amend and restate the Current Charter, which Proposed Charter will be in effect upon the Closing. See the section titled “Proposal 2: The Charter Amendment Proposal.” A copy of the Proposed Charter is attached to this proxy statement/prospectus as Annex C. |

7

Table of Contents

| 2. | Separate Proposals to approve, on a non-binding advisory basis, the following material differences between the Proposed Charter and the Current Charter: (i) to change the corporate name of the Combined Company to “Carmell Therapeutics Corporation”; (ii) to increase the authorized shares of ALPA Common Stock to 250,000,000 shares; (iii) to increase the authorized shares of “blank check” preferred stock that the Combined Company’s board of directors could issue to 20,000,000 shares; (iv) to provide that the removal of any director be only for cause and by the affirmative vote of at least 66 2⁄3% of the Combined Company’s then-outstanding shares of capital stock entitled to vote generally in the election of directors; (v) to provide that certain amendments to provisions of the Proposed Charter will require the approval of at least 66 2⁄3% of the Combined Company’s then-outstanding shares of capital stock entitled to vote on such amendment; (vi) to make the Combined Company’s corporate existence perpetual instead of requiring ALPA to dissolve and liquidate 24 months following the closing of its Initial Public Offering and to remove from the Proposed Charter the various provisions applicable only to special purpose acquisition corporations; and (vii) to remove the provision that allows Class B stockholders to act by written consent as opposed to holding a stockholders meeting (together, the “Advisory Charter Amendment Proposals”). See the section titled “Proposal 3: The Advisory Charter Amendment Proposals.” |

| 3. | To approve the issuance of up to 15,000,000 shares of New Carmell common stock in connection with the Business Combination in order to comply with applicable Nasdaq Listing Standards. See the section titled “Proposal 4: The Nasdaq Proposal.” |

| 4. | To approve the appointment of nine directors who, upon consummation of the Business Combination, will become the directors of the Combined Company. See the section titled “Proposal 5: The Director Election Proposal.” |

| 5. | To approve the 2023 Plan. See the section titled “Proposal 6: The Incentive Plan Proposal.” A copy of the 2023 Plan is attached to this proxy statement/prospectus as Annex D. |

| 6. | To adjourn the Special Meeting to a later date or dates if it is determined that more time is necessary or appropriate, in the judgment of the Board or the officer presiding over the Special Meeting, for ALPA to consummate the Business Combination (including to solicit additional votes in favor of any of the foregoing Proposals). See the section titled “Proposal 7: The Adjournment Proposal.” |

ALPA will hold the Special Meeting to consider and vote upon these Proposals. This proxy statement/prospectus contains important information about the proposed Business Combination and the other matters to be acted upon at the Special Meeting. Stockholders should read it carefully.

Consummation of the Business Combination is conditioned on approval of the Business Combination Proposal, the Charter Amendment Proposal, the Nasdaq Proposal, the Director Election Proposal and the Incentive Plan Proposal (and each such Proposal is cross-conditioned on the approval of such other Proposals). If any of these Proposals is not approved, the other Proposals will not be presented to stockholders for a vote.

The vote of stockholders is important. ALPA stockholders are encouraged to vote as soon as possible after carefully reviewing this proxy statement/prospectus.

| Q: | I am an ALPA Warrant holder. Why am I receiving this proxy statement/prospectus? |

| A: | After the consummation of the Business Combination, the holders of the Warrants will be entitled to purchase New Carmell common stock at a purchase price of $11.50 per share beginning 30 days after the Closing. This proxy statement/prospectus includes important information about ALPA and the business of New Carmell following the Closing. Because holders of Warrants will be entitled to purchase New Carmell common stock 30 days after the Closing, we urge you to read the information contained in this proxy statement/prospectus carefully. |

8

Table of Contents

| Q: | What will happen to ALPA’s securities upon consummation of the Business Combination? |

| A: | ALPA’s Units, Class A Common Stock and Warrants are currently listed on Nasdaq under the symbols ALPAU, ALPA and ALPAW, respectively. Upon the Closing, the Combined Company will have one class of common stock — referred to herein as New Carmell common stock — which will be listed on Nasdaq under the symbol CTCX, and its warrants will be listed on Nasdaq under the symbol CTCXW. ALPA will not have Units traded on Nasdaq following the Closing, and its Units will automatically be separated into their component securities without any action needed to be taken on the part of the holders. Public Stockholders who do not elect to have their Public Shares redeemed for a pro rata share of the Trust Account need not submit Public Shares, and such shares of stock (which will be New Carmell common stock upon the Closing) will remain outstanding. Each outstanding Warrant will entitle the holder to purchase shares of New Carmell common stock beginning 30 days after the Closing. Each outstanding share of Class B Common Stock, by its terms, will automatically convert into one share of New Carmell common stock upon the Closing. |

| Q: | Why is ALPA proposing the Business Combination? |

| A: | ALPA was organized to effect a merger, capital stock exchange, asset acquisition, stock purchase, reorganization or other similar business combination with one or more businesses or entities. |

On July 29, 2021, ALPA closed its Initial Public Offering of 15,000,000 units at a price of $10.00 per unit generating gross proceeds of $150,000,000 before transaction costs (including deferred underwriting expenses to be paid upon completion of ALPA’s initial business combination). Each unit consisted of one share of Class A Common Stock and one-fourth of one redeemable warrant. Each whole warrant entitles the holder thereof to purchase one share of Class A Common Stock for $11.50 per share, subject to certain adjustments.

Carmell is a regenerative medicine biotech company focused on leveraging its core platform technology to stimulate tissue repair or growth after severe injury, disease or aging.

Based on its due diligence investigations of Carmell and the industry in which it operates, including the financial and other information provided by Carmell in the course of the negotiations in connection with the Business Combination Agreement, ALPA believes that Carmell has an appealing market opportunity and growth profile and a compelling valuation. As a result, ALPA believes that the Business Combination with Carmell will provide ALPA stockholders with an opportunity to participate in the ownership of a company with significant value. See the section titled “Proposal 1: The Business Combination Proposal — The Board’s Reasons for Approval of the Business Combination.”

| Q: | Do I have redemption rights? |

| A: | If you are an ALPA stockholder holding Public Shares, you have the right to demand that ALPA redeem your Public Shares for a pro rata portion of the cash held in the Trust Account. We sometimes refer to these rights to demand redemption of the Public Shares as “redemption rights.” |

Notwithstanding the foregoing, a stockholder, together with any affiliate or any other person with whom such holder is acting in concert or as a “group” (as defined in Section 13(d)(3) of the Exchange Act), will be restricted from seeking redemption rights with respect to 20% or more of the Public Shares without the prior consent of ALPA.

| Q: | How do I exercise my redemption rights? |

| A: | A Public Stockholder may exercise redemption rights regardless of whether it votes on the Business Combination Proposal or if it is a stockholder on the Record Date. If you are a Public Stockholder and wish to exercise your redemption rights, you must demand that ALPA redeem your Public Shares for cash and |

9

Table of Contents

| deliver your Public Shares to ALPA’s transfer agent, Continental, at Continental Stock Transfer & Trust Company, One State Street Plaza, 30th Floor, New York, New York 10004, Attn: Mark Zimkind, physically or electronically using mzimkind@continentalstock.com, at least two business days before the Special Meeting, or [●], 2023. As opposed to delivering your Public Shares directly to Continental, you may deliver your Public Shares either physically or electronically through DTC to Continental at least two business days before the Special Meeting. Any Public Stockholder seeking redemption will be entitled to a full pro rata portion of the amount then in the Trust Account (which, for illustrative purposes, was $[●], or $[●] per share, as of the Record Date), less any owed but unpaid taxes on the funds in the Trust Account. Such amount will be paid promptly upon consummation of the Business Combination. There are currently no owed but unpaid income taxes on the funds in the Trust Account. |

Any request for redemption, once made by a Public Stockholder, may be withdrawn at any time prior to the time the vote is taken with respect to the Business Combination Proposal at the Special Meeting. If you deliver your Public Shares for redemption directly to Continental, or deliver your Public Shares either physically or electronically through DTC to Continental, and later decide prior to the Special Meeting not to elect redemption, you may request that Continental return the shares (physically or electronically). You may make such request by contacting Continental at the phone number or address set forth in this proxy statement/prospectus.

Any written demand of redemption rights must be received by Continental at least two business days prior to the vote taken on the Business Combination Proposal at the Special Meeting. No demand for redemption will be honored unless the holder’s stock has been delivered (either physically or electronically) to Continental.

If you are a Public Stockholder and you exercise your redemption rights, it will not result in the loss of any Warrants that you may hold. Your Warrants will each become exercisable to purchase one share of New Carmell common stock for a purchase price of $11.50 beginning 30 days after consummation of the Business Combination.

| Q: | If I am a holder of Units, can I exercise redemption rights with respect to my Units? |

| A: | No. Holders of issued and outstanding Units must elect to separate their Units into the underlying Public Shares and Warrants prior to exercising redemption rights with respect to the Public Shares. If you hold your Units in an account at a brokerage firm or bank, you must notify your broker or bank that you elect to separate the Units into the underlying Public Shares and Warrants and instruct them to do so. The redemption rights include the requirement that a holder must identify itself in writing as a beneficial holder and provide its legal name, phone number and address to Continental in order to validly redeem its shares. You are required to cause your Public Shares to be separated and delivered to Continental, ALPA’s transfer agent, by , 2023 (two business days before the Special Meeting) in order to exercise your redemption rights with respect to your Public Shares. |

| Q: | Do I have appraisal rights if I object to the proposed Business Combination? |

| A: | No. Neither ALPA stockholders nor holders of its Units or Warrants have appraisal rights in connection with the Business Combination under Delaware law. |

| Q: | What happens if a substantial number of stockholders votes in favor of the Business Combination Proposal and exercise redemption rights? |

| A: | Public Stockholders may vote in favor of the Business Combination and still exercise their redemption rights and are not required to vote in any way to exercise redemption rights. Accordingly, the Business Combination may be consummated even though the funds available from the Trust Account and the number of Public Shares are substantially reduced as a result of redemption by Public Stockholders (however, the |

10

Table of Contents

| condition to the consummation of the Business Combination requiring that ALPA have at least $5,000,001 of net tangible assets may not be waived). Also, with fewer Public Shares and Public Stockholders, the trading markets for New Carmell common stock and warrants following the closing of the Business Combination may be less liquid than the market for Class A Common Stock and Warrants were prior to the Business Combination and New Carmell may not be able to meet the listing standards of a national securities exchange. In addition, with fewer funds available from the Trust Account, the capital infusion from the Trust Account into New Carmell’s business will be reduced and New Carmell may not be able to achieve its business plans. |

| Q: | How do the Sponsor and the officers and directors of ALPA intend to vote on the Proposals? |

| A: | The Sponsor, as well as ALPA’s officers and directors, beneficially own and are entitled to vote an aggregate of [●]% of the outstanding ALPA Common Stock as of the Record Date. These holders have agreed to vote their shares in favor of the Business Combination Proposal. These holders have also agreed to vote their shares in favor of all other Proposals being presented at the Special Meeting. |

| Q: | What do I need to do now? |

| A: | ALPA urges you to carefully read and consider the information contained in this proxy statement/prospectus, including the Annexes, and to consider how the Business Combination will affect you as a stockholder and/or warrant holder of ALPA. ALPA stockholders should then vote as soon as possible in accordance with the instructions provided in this proxy statement/prospectus and on the enclosed proxy card. |

| Q: | How do I vote? |

| A: | If you are a holder of record of ALPA Common Stock on the Record Date, you may vote virtually at the Special Meeting or by submitting a proxy for the Special Meeting. You may submit your proxy by completing, signing, dating and returning the enclosed proxy card in the accompanying pre-addressed postage paid envelope. If you hold your shares in “street name,” which means your shares are held of record by a broker, bank or nominee, you should contact your broker, bank or nominee to ensure that votes related to the shares you beneficially own are properly counted. In this regard, you must provide the broker, bank or nominee with instructions on how to vote your shares or, if you wish to attend the meeting and vote in person (which would include presence at a virtual meeting), obtain a legal proxy from your broker, bank or nominee. |

If you do not give instructions to your brokerage firm, the brokerage firm will not be allowed to vote your shares with respect to Proposals. The Proposals are “non-discretionary” items. Your broker may not vote for non-discretionary items, and those votes will be counted as broker “non-votes.”

After obtaining a valid legal proxy from your broker, bank or other agent, to register to attend the Special Meeting, you must submit proof of your legal proxy reflecting the number of your shares along with your name and email address to Continental at proxy@continentalstock.com. Beneficial owners who e-mail a valid legal proxy will be issued a 12-digit meeting control number that will allow them to register to attend and participate in the Special Meeting. Beneficial owners who wish to attend the special meeting online should contact Continental no later than [●], 2023 to obtain this information. Written requests can be emailed to proxy@continentalstock.com.

| Q: | If my shares are held in “street name,” will my broker, bank or nominee automatically vote my shares for me? |

| A: | No. Your broker, bank or nominee cannot vote your shares unless you provide instructions on how to vote in accordance with the information and procedures provided to you by your broker, bank or nominee. |

11

Table of Contents

| Q: | May I change my vote after I have mailed my signed proxy card? |

| A: | Yes. ALPA stockholders may send a later-dated, signed proxy card to Continental at the address set forth above so that it is received prior to the vote at the Special Meeting or attend the Special Meeting virtually and vote. ALPA stockholders also may revoke their proxy by sending a notice of revocation to Continental, which must be received prior to the vote at the Special Meeting. |

| Q: | What happens if I fail to take any action with respect to the Special Meeting? |

| A: | If you fail to take any action with respect to the Special Meeting and the Business Combination is approved by stockholders and consummated, you will continue to be a holder of New Carmell common stock or warrants, as applicable. As a corollary, failure to deliver your stock certificate(s) to ALPA’s transfer agent (either physically or electronically) no later than two business days prior to the Special Meeting means you will not have any right in connection with the Business Combination to exchange your Public Shares for a pro rata share of the funds held in the Trust Account. If you fail to take any action with respect to the Special Meeting and the Business Combination is not approved, you will continue to be a stockholder or Warrant holder of ALPA, as applicable. |

| Q: | What should I do with my share or Warrant certificates? |

| A: | Warrant holders and those Public Stockholders who do not elect to have their Public Shares redeemed for a pro rata share of the Trust Account need not submit their certificates. Public Stockholders who exercise their redemption rights must deliver their share certificates to Continental (either physically or electronically) or through DTC to Continental at least two business days before the Special Meeting as described above. |

| Q: | What should I do if I receive more than one set of voting materials? |

| A: | ALPA stockholders may receive more than one set of voting materials, including multiple copies of this proxy statement/prospectus and multiple proxy cards or voting instruction cards. For example, if you hold your ALPA shares in more than one brokerage account, you will receive a separate voting instruction card for each brokerage account in which you hold such shares. If you are a holder of record and your ALPA shares are registered in more than one name, you will receive more than one proxy card. Please complete, sign, date and return each proxy card and voting instruction card that you receive in order to cast a vote with respect to all of your ALPA shares. |

| Q: | Who can help answer my questions? |

| A: | If you have questions about the Business Combination or if you need additional copies of this proxy statement/prospectus or the enclosed proxy card, you should contact: |

Morrow Sodali LLC

470 West Avenue

Stamford, Connecticut 06902

Individuals call toll-free (800) 662-5200

Banks and brokers call (203) 658-9400

Email:

You may also obtain additional information about ALPA from documents filed with the SEC by following the instructions in the section titled “Where You Can Find More Information.” If you are an ALPA stockholder and you intend to seek redemption of your shares, you will need to deliver your Public Shares (either physically or

12

Table of Contents

electronically) to Continental (or through DTC to Continental) at the address listed below at least two business days prior to the vote at the Special Meeting. If you have questions regarding the certification of your position or delivery of your stock, please contact:

Continental Stock Transfer & Trust Company

One State Street Plaza, 30th Floor

New York, New York 10004

Attn: Mark Zimkind

E-mail: mzimkind@continentalstock.com

13

Table of Contents

This summary highlights selected information from this proxy statement/prospectus and does not contain all of the information that is important to you. To better understand the proposals to be submitted for a vote at the Special Meeting, including the Business Combination Proposal, you should read this entire document carefully, including the Annexes attached to this proxy statement/prospectus. The Business Combination Agreement is the legal document that governs the Business Combination and other transactions that will be undertaken in connection with the Business Combination. It is also described in detail in this proxy statement/prospectus in the section titled “Proposal 1: The Business Combination Proposal.”

The Parties

ALPA

Alpha Healthcare Acquisition Corp. III (“ALPA”) is a blank check company formed in order to effect a merger, capital stock exchange, asset acquisition, stock purchase, reorganization or similar business combination with one or more businesses or entities. ALPA was incorporated under the laws of the State of Delaware on January 21, 2021.

On July 29, 2021, ALPA closed its Initial Public Offering of 15,000,000 units at a price of $10.00 per unit generating gross proceeds of $150,000,000 before transaction costs (including deferred underwriting expenses to be paid upon completion of ALPA’s initial business combination). Each unit consisted of one share of Class A common Stock and one-fourth of one redeemable warrant. Each whole warrant entitles the holder thereof to purchase one share of Class A common stock for $11.50 per share, subject to certain adjustments. Simultaneous with the closing of the Initial Public Offering, ALPA completed the sale of 464,000 units in a private placement at a price of $10.00 per unit to Sponsor, BofA Securities and PJT Partners. In connection with the Initial Public Offering, ALPA also granted the underwriters a 45-day option to purchase an additional 2,250,000 units at a price of $10.00 per unit. On August 3, 2021, the underwriters exercised their option to purchase 444,103 additional units for the total amount of $4,441,030, received on August 6, 2021. On August 6, 2023, ALPA also issued 8,882 units in a private placement, generating additional $88,820 in gross proceeds. The units sold in the private placement are identical to the units sold in the Initial Public Offering except that the shares of Class A common stock issued in such units do not have associated redemption rights. A total of $[●] million, comprised of $[●] million of the proceeds from the Initial Public Offering and the partial exercise of the option (which amount includes up to $[●] of the underwriters’ deferred fees) and $[●] of the proceeds from the concurrent private placement, was deposited into the Trust Account, and the remaining proceeds, net of underwriting discounts and commissions and other costs and expenses, became available to be used as working capital to provide for business, legal and accounting due diligence on prospective business combinations and continuing general and administrative expenses. As of the Record Date, there was approximately $[●] held in the Trust Account.

ALPA’s Units, Class A Common Stock and Warrants are listed on Nasdaq under the symbols ALPAU, ALPA and ALPAW, respectively.

The mailing address of ALPA’s principal executive office is 1177 Avenue of the Americas, 5th Floor, New York, New York 10036, and its telephone number is (646) 494-3296. After the consummation of the Business Combination, ALPA’s principal executive office will be that of Carmell.

For additional information about ALPA, see the section titled “Information about ALPA.”

14

Table of Contents

Merger Sub

Merger Sub is a wholly owned subsidiary of ALPA formed solely for the purpose of effectuating the Business Combination described herein. Merger Sub was incorporated under the laws of Delaware as a corporation on January 4, 2023. Merger Sub owns no material assets and does not operate any business.

The mailing address of Merger Sub’s principal executive office is 1177 Avenue of the Americas, 5th Floor, New York, New York 10036, and its telephone number is (646) 494-3296. After the consummation of the Business Combination, Merger Sub will cease to exist.

Carmell

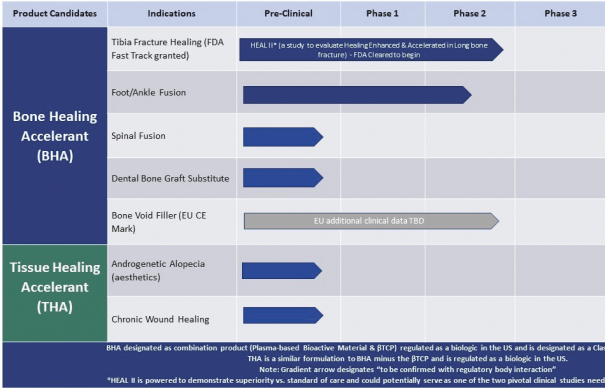

Carmell Therapeutics Corporation is a regenerative medicine biotech company focused on leveraging its core platform technology, Plasma-based Bioactive Material (“PBM”) to stimulate tissue repair or growth after severe injury, disease or aging. The technology is a proprietary method of utilizing fresh frozen platelet-enriched plasma to manufacture multiple forms to be placed directly at the anatomical site in need of enhanced and accelerated healing with the ability to reside in the local tissue for weeks to months. Carmell’s PBM technology is based on patents licensed from Carnegie Mellon University (“CMU”) that claim the ability to plasticize allogeneic platelet-enriched plasma and crosslink proteins with genipin, a derivative of the gardenia plant, to provide a controlled degradation profile in vivo. Carmell’s lead product candidate, Bone Healing Accelerant (“BHA”), a biologic, has been designated by U.S. Food and Drug Administration (“FDA”) as a potential combination product, containing the Carmell’s core technology of PBM plus ß Tri-Calcium Phosphate (“ß-TCP”) an already approved medical device.

Carmell was incorporated under the laws of the State of Delaware on November 5, 2008. The mailing address of Carmell’s principal executive office is 2403 Sidney Street, Suite 300, Pittsburg, PA 15293, and its telephone number is 412-894-8248.

For additional information about Carmell, see the section titled “Information about Carmell.”

Emerging Growth Company

ALPA is an “emerging growth company,” as defined under the JOBS Act. As an emerging growth company, ALPA is eligible to take advantage of certain exemptions from various reporting requirements that are applicable to other public companies that are not emerging growth companies. These include, but are not limited to, not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act, reduced disclosure obligations regarding executive compensation in its periodic reports and proxy statements, and exemptions from the requirements of holding a nonbinding advisory vote on executive compensation and the requirement to obtain stockholder approval of any golden parachute payments not previously approved.

New Carmell will remain an emerging growth company until the earlier of (1) December 31, 2026 (the last day of the fiscal year following the fifth anniversary of the consummation of the Initial Public Offering), (2) the last day of the fiscal year in which New Carmell has total annual gross revenue of at least $1.07 billion, (3) the last day of the fiscal year in which New Carmell is deemed to be a “large accelerated filer,” as defined in the Exchange Act, and (4) the date on which New Carmell has issued more than $1.0 billion in nonconvertible debt securities during the prior three-year period.

The Business Combination Proposal

Pursuant to the Business Combination Agreement, a Business Combination between ALPA and Carmell will be effected whereby Merger Sub will merge with and into Carmell, with Carmell surviving as a wholly owned subsidiary of ALPA.

15

Table of Contents

After consideration of the factors identified and discussed in the section titled “Proposal 1: The Business Combination Proposal — The Board’s Reasons for Approval of the Business Combination,” the Board concluded that the Business Combination met all of the requirements disclosed in the prospectus for its Initial Public Offering, including that Carmell has a fair market value equal to at least 80% of the balance of the funds in the Trust Account (excluding the deferred underwriting commissions and taxes payable on the interest earned on the Trust Account) at the time of the execution of the Business Combination Agreement.

The terms and conditions of the Business Combination are contained in the Business Combination Agreement, which is attached to this proxy statement/prospectus as Annex A and is incorporated by reference herein in its entirety. ALPA encourages you to read the Business Combination Agreement carefully, as it is the legal document that governs the Business Combination. For more information on the Business Combination Agreement, see the section titled “Proposal 1: The Business Combination Proposal.”

Business Combination Consideration

Pursuant to the Business Combination Agreement:

| • | Each outstanding share of Carmell common stock will be cancelled and converted into the right to receive a number of shares of New Carmell common stock equal to the Exchange Ratio (rounded down to the nearest whole share). |

| • | Each outstanding share of Carmell preferred stock will be cancelled and converted into the right to receive a number of shares of New Carmell common stock equal to (A) the aggregate number of shares of Carmell common stock that would be issued upon conversion of the shares of Carmell preferred stock based on the applicable conversion ratio immediately prior to the Effective Time, multiplied by (ii) the Exchange Ratio (rounded down to the nearest whole share). |

| • | Each outstanding Carmell option or warrant will be converted into an option or warrant, as applicable, to purchase a number of shares of Class A Common Stock equal to (A) the number of shares of Carmell common stock subject to such option or warrant multiplied by (B) the Exchange Ratio at an exercise price per share equal to the current exercise price per share for such option or warrant divided by the Exchange Ratio (rounded down to the nearest whole share).See the section titled “Proposal 1: The Business Combination Proposal — Structure of the Business Combination.” |

As of the Record Date, the Exchange Ratio was approximately . Based on this Exchange Ratio, the total number of shares of New Carmell common stock expected to be issued in connection with the Business Combination is approximately shares, and these shares are expected to represent approximately [●]% or [●]% of the issued and outstanding shares of New Carmell common stock immediately following the closing of the Business Combination assuming no redemptions occur and maximum redemptions occur, respectively.

Board’s Reasons for the Business Combination

ALPA was formed in order to effect a merger, capital stock exchange, asset acquisition, stock purchase, reorganization or similar business combination with one or more businesses or entities. With respect to the proposed Business Combination, the Board considered the following positive factors, although not weighted or in any order of significance:

| • | Phase 2-stage biotechnology platform with multiple product candidates. The Board considered Carmell’s Phase 2-stage biotechnology platform with multiple product candidates designed to be: (a) allogeneic, with no need for (i) extraction of blood from patients, (ii) capital equipment to harvest biomaterials at the clinical care facility, (iii) staff training, (b) ready to use off-the-shelf including |

16

Table of Contents

| (i) assured levels of biomaterials, (ii) formulated to be available over weeks and months, providing sustained local tissue bioavailability of growth factors and other bioactive molecules important for healing, (c) eliminating waiting time for tissue processing, (d) eliminating the need to harvest tissue from a patient with existing morbidity. |

| • | Anticipated clinical applications. The Board considered anticipated clinical applications for Carmell’s products including: (a) orthopedic healing applications such as (i) tibia fractures, to treat open fractures of the shinbone that require intramedullary rodding, (ii) fusion hindfoot or ankle arthrodesis, to aid surgical fusion of foot/ankle joint in degenerative arthritis, (iii) spinal fusion, to aid surgical fusion of spinal vertebrae due to deformity, injury or degenerative disease, and (iv) dental bone graft, an alternative to bone grafting in dental restoration/implants. (b) Soft tissue healing applications such as (i) surgical/chronic wounds, to promote healing after surgical incisions or open wounds caused due to diseases such as diabetic foot ulcers, (ii) alopecia, to promote regrowth of hair in men and women, and (iii) cosmetic skin rejuvenation, to improve the appearance of damaged/aged skin. |

| • | Clinical proof of concept. The Board considered that Carmell’s previous Phase 2 trial (HEAL I) in open tibia fractures suggested that the product candidate may have the potential to accelerate bone healing and reduce rate of infections. |

| • | Regulatory considerations. The Board considered the potential regulatory pathways for Carmell’s product candidates, including that Carmell received Fast Track designation from the FDA for its tibia fracture (lead) indication. |

| • | Intellectual property protection. The Board considered Carmell’s intellectual property portfolio, including 21 patents, as well as proprietary biomanufacturing know-how and trade secrets. |

| • | In-house manufacturing. The Board considered Carmell’s in-house manufacturing with 11 release tests developed for lot-to-lot consistency and that Carmell is ISO 13485 certified. |

| • | Experienced management team. The Board believes that Carmell has a proven and experienced management team that will effectively lead the Combined Company after the Business Combination. |

| • | Opinion of Financial Advisor. The Board considered the oral opinion of Cabrillo rendered to the Board, which was subsequently confirmed by delivery of a written opinion that, as of such date and based upon and subject to the assumptions made, procedures followed, matters considered, and qualifications and limitations upon the review undertaken by Cabrillo in preparing its opinion, (i) the consideration to be paid by ALPA to Carmell equityholders in the Business Combination under the Business Combination Agreement is fair, from a financial point of view, to ALPA and (ii) Carmell has a fair market value equal to at least 80% of the balance of funds in Trust Account (excluding deferred underwriting commissions and taxes payable and subject to proportionate adjustments related to Nasdaq’s 80% test), as more fully described below under the heading titled “Proposal 1: The Business Combination Proposal — Opinion of ALPA’s Financial Advisor.” |