UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM

(Mark One)

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended

OR

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ____________________ to ____________________

Commission File Number:

(Exact Name of Registrant as Specified in its Charter)

( State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer |

(Address of principal executive offices) |

(Zip Code) |

Registrant’s telephone number, including area code: (

Securities registered pursuant to Section 12(b) of the Act:

Title of each class |

|

Trading Symbol(s) |

|

Name of each exchange on which registered |

|

|

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ☐

Indicate by check mark whether the Registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the Registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer |

|

☐ |

|

|

☒ |

|

|

|

|

|

|||

Non-accelerated filer |

|

☐ |

|

Smaller reporting company |

|

|

|

|

|

|

|

|

|

Emerging growth company |

|

|

|

|

|

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No

The aggregate market value of Class A common stock held by non-affiliates of the Registrant on June 30, 2024, the last business day of the Registrant's most recently completed second fiscal quarter was approximately $

As of February 24, 2025, there were

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Registrant’s definitive proxy statement relating to its 2025 annual meeting of stockholders (the “2025 Proxy Statement”) are incorporated by reference into Part III of this Annual Report on Form 10-K where indicated. The 2025 Proxy Statement will be filed with the U.S. Securities and Exchange Commission within 120 days after the end of the fiscal year to which this report relates.

Table of Contents

|

|

Page |

|

|

|

Item 1. |

5 |

|

Item 1A. |

22 |

|

Item 1B. |

51 |

|

Item 1C. |

51 |

|

Item 2. |

51 |

|

Item 3. |

52 |

|

Item 4. |

52 |

|

|

|

|

|

|

|

Item 5. |

53 |

|

Item 6. |

54 |

|

Item 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

55 |

Item 7A. |

70 |

|

Item 8. |

72 |

|

Item 9. |

Changes in and Disagreements With Accountants on Accounting and Financial Disclosure |

113 |

Item 9A. |

113 |

|

Item 9B. |

113 |

|

Item 9C. |

Disclosure Regarding Foreign Jurisdictions that Prevent Inspections |

113 |

|

|

|

|

|

|

Item 10. |

114 |

|

Item 11. |

114 |

|

Item 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

114 |

Item 13. |

Certain Relationships and Related Transactions, and Director Independence |

114 |

Item 14. |

114 |

|

|

|

|

|

|

|

Item 15. |

115 |

|

Item 16. |

117 |

|

|

118 |

This Annual Report on Form 10-K ("Form 10-K") includes certain information regarding the historical performance of our specialized investment vehicles, which include specialized funds and customized separate accounts. An investment in shares of our Class A common stock is not an investment in our specialized investment vehicles. In considering the performance information relating to our specialized investment vehicles contained herein, prospective Class A common stockholders should bear in mind that the performance of our specialized investment vehicles is not indicative of the possible performance of shares of our Class A common stock and is also not necessarily indicative of the future results of our specialized investment vehicles, even if fund investments were in fact liquidated on the dates indicated, and there can be no assurance that our specialized investment vehicles will continue to achieve, or that future specialized investment vehicles will achieve comparable results.

We own or have rights to trademarks, service marks or trade names that we use in connection with the operation of our business. In addition, our names, logos and website names and addresses are owned by us or licensed by us. We also own or have the rights to copyrights that protect the content of our solutions. Solely for convenience, the trademarks, service marks, trade names and copyrights referred to in this Form 10-K are listed without the ©,® and ™ symbols, but we will assert, to the fullest extent under applicable law, our rights or the rights of the applicable licensors to these trademarks, service marks, trade names and copyrights.

This Form 10-K may include trademarks, service marks or tradenames of other companies. Our use or display of other parties’ trademarks, service marks, trade names or products is not intended to, and does not imply a relationship with, or endorsement or sponsorship of us by, the trademark, service mark or tradename owners.

Unless otherwise indicated, information contained in this Form 10-K concerning our industry and the markets in which we operate is based on information from independent industry and research organizations, other third-party sources (including industry publications, surveys and forecasts), and management estimates. Management estimates are derived from publicly available information released by independent industry analysts and third-party sources, as well as data from our internal research, and are based on assumptions made by us upon reviewing such data and our knowledge of such industry and markets that we believe to be reasonable. Although we believe the data from these third-party sources is reliable, we have not independently verified any third-party information. In addition, projections, assumptions and estimates of the future performance of the industry in which we operate and our future performance are necessarily subject to uncertainty and risk due to a variety of factors, including those described in “Risk Factors” and “Forward-Looking Statements.” These and other factors could cause results to differ materially from those expressed in the estimates made by the independent parties and by us.

Our principal operating brands are RCP Advisors 2, LLC (“RCP 2”) and RCP Advisors 3, LLC (“RCP 3”, and collectively with RCP 2, “RCP Advisors”), TrueBridge Capital Partners LLC (“TrueBridge”), Five Points Capital, Inc. (“Five Points”), Reynolda Equity Partners ("Reynolda"), Enhanced Capital Group, LLC (“ECG” or “Enhanced”), Bonaccord Capital Advisors LLC ("Bonaccord"), Hark Capital Advisors, LLC ("Hark"), P10 Advisors, LLC (“P10 Advisors”), and Westech Investment Advisors LLC (“WTI”).

Unless otherwise indicated or the context otherwise requires, all references in this Form 10-K to “we, ”“us,” “our,” the “Company,” “P10”and similar terms refer to P10, Inc. and its subsidiaries and, to the extent applicable, its predecessors. As used in this Form 10-K, (i) the term “P10 Holdings” refers to P10 Holdings, Inc. for all periods and (ii) the term “P10, Inc.” refers solely to P10, Inc., a Delaware corporation, and not to any of its subsidiaries.

FORWARD-LOOKING STATEMENTS

This Form 10-K contains forward-looking statements, which reflect our current views with respect to, among other things, future events and financial performance, our operations, strategies and expectations. The words “believe,” “may,” “will,” “estimate,” “continue,” “anticipate,” “intend,” “expect,” “plan” and similar expressions are intended to identify forward-looking statements. Any forward-looking statements contained in this Form 10-K are based upon our historical performance and on our current plans, estimates and expectations. The inclusion of this or any forward-looking information should not be regarded as a representation by us or any other person that the future plans, estimates or expectations

2

contemplated by us will be achieved. Such forward-looking statements are subject to various risks, uncertainties and assumptions, including but not limited to global and domestic market and business conditions, our successful execution of business and growth strategies and regulatory factors relevant to our business, as well as assumptions relating to our operations, financial results, financial condition, business prospects, growth strategy and liquidity. Accordingly, there are or will be important factors that could cause actual outcomes or results to differ materially from those indicated in these statements. We believe these factors include, but are not limited to, those described under “Risk Factors.” These factors should not be construed as exhaustive and should be read in conjunction with the other cautionary statements that are included in this Form 10-K. We operate in a very competitive and rapidly changing environment. New risks emerge from time to time. It is not possible for our management to predict all risks, nor can we assess the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements we may make. We undertake no obligation to publicly update or review any forward-looking statement, whether as a result of new information, future developments or otherwise.

SUMMARY RISK FACTORS

Investing in our Class A common stock involves numerous risks, including the risks described in “Part I, Item 1A. Risk Factors” of this Annual Report. Below are some of these risks, any one of which could materially adversely affect our business, financial condition, results of operations, and prospects.

3

4

PART I

Item 1. Business.

Our Company

We are a leading multi-asset class private market solutions provider in the alternative asset management industry. Our mission is to provide our investors differentiated access to a broad set of investment solutions that address their diverse investment needs within private markets. We structure, manage and monitor portfolios of private market investments, which include specialized funds and customized separate accounts within primary investment funds, secondary investments, direct investments and co-investments, (collectively, “specialized investment vehicles”) across highly attractive asset classes and geographies in the middle and lower middle markets that generate superior risk-adjusted returns. Our existing portfolio of private solutions include Private Equity, Venture Capital, and Private Credit. Our deep industry relationships, differentiated investment access and structure, proprietary data analytics, and our portfolio monitoring and reporting capabilities provide our investors the ability to navigate the increasingly complex and difficult to access private markets investments.

Our revenue is composed almost entirely of recurring management and advisory fees, with the vast majority of fees earned on committed capital that is typically subject to ten to fifteen year lock up agreements. We have an attractive business model that is underpinned by highly recurring, diversified management and advisory fee revenues, and strong free cash flow. The nature of our solutions and the integral role that our solutions play in our investors’ investment decisions have translated into high revenue visibility and investor retention. As of December 31, 2024, we had FPAUM of $25.7 billion.

We are differentiated by the scale, depth, diversity and investment performance of our solutions, which are bolstered by the investment expertise of our investment team, our long-standing access to leading fund managers, our robust and constantly expanding data capabilities and our disciplined investment process. We market our solutions under well-established brands within the specialized markets in which we operate. These include RCP Advisors, Bonaccord Capital, and P10 Advisors, our Private Equity solutions; TrueBridge, our Venture Capital solution; and Enhanced, Five Points, Hark Capital, and WTI, our Private Credit solutions (of which Five Points also offers certain private equity solutions). In addition, in September 2024, we entered into an agreement to acquire Qualitas Equity Funds SGEIC, S.A. ("Qualitas"). We believe adding new asset class solutions or new geographies will foster deeper manager relationships, enabling managers and portfolio companies alike to benefit from our offering and expect to expand within other asset classes and geographies through additional acquisitions and future planned organic growth by providing additional specialized investment vehicles within our existing investment asset class solutions. We expect the Qualitas acquisition to close in the first quarter of 2025, subject to customary closing conditions and regulatory approvals, and continue to pursue additional acquisitions and other growth opportunities.

Our success and growth have been driven by our long history of strong performance and our position in the private markets ecosystem. We believe our growing scale in the middle and lower-middle market provides us a competitive advantage with investors and fund managers. In addition, our senior investment professionals have developed strong and long-tenured relationships with leading middle and lower middle market private equity and venture capital firms, which we believe provides us with differentiated access to the relationship-driven middle and lower-middle market private equity and venture capital sectors. As we expand our offerings, our investors entrust us with additional capital, which strengthens our relationships with our fund managers, drives additional investment opportunities, sources more data, enables portfolio optimization and enhances returns, and in turn attracts new investors. We believe this powerful feedback process will continue to strengthen our position within the private markets ecosystem. In addition, our multi-asset class solutions are highly synergistic, and coupled with our vast network of general partners and portfolio companies, drive cross-solution sourcing opportunities.

Our global investor base includes some of the world’s largest institutional investors, including pension funds, endowments, foundations, corporate pensions and financial institutions. In addition, we have a strong footprint within some of the most prominent family offices and high net worth individuals. We have a significant presence within the middle and lower middle-market private markets industry in North America, where the majority of our capital is currently being deployed as we leverage our differentiated solutions to serve our global investors.

As of December 31, 2024, we had 267 employees, including 112 investment professionals across 11 offices located in 9 states.

5

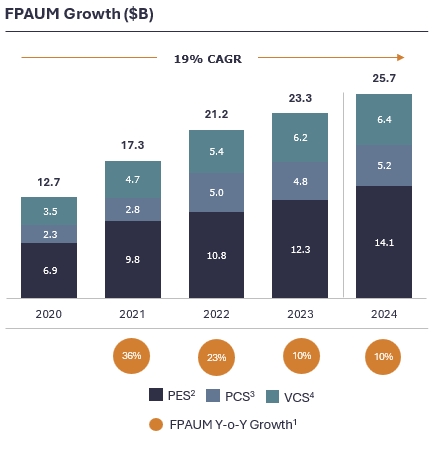

We managed $25.7 billion in FPAUM from which we earn management and advisory fees as of December 31, 2024. In addition, our FPAUM has grown at a compound annual growth rate ("CAGR") of 19% from December 31, 2020 to December 31, 2024.

1. Q4'24 FPAUM growth is the FPAUM growth from Q4'23 to Q4'24.

2. Private Equity Solutions ("PES")

3. Private Credit Solutions ("PCS")

4. Venture Capital Solutions ("VCS")

Our Solutions

We operate and invest across private markets through a number of specialized investment solutions. We offer the following solutions to our investors:

Private Equity Solutions "PES"

Under PES, we make direct and indirect investments in middle and lower- middle market private equity primarily across North America and Europe. PES also makes minority equity investments in a diversified portfolio of mid-sized managers across private equity, private credit, real estate and real assets. The PES investment team, which is comprised of 42 investment professionals with an average of 26+ years of experience, has deep and long-standing investor and fund manager relationships in the middle and lower-middle market which it has cultivated over the past 20 years, including over 2,280+ investors, 285+ fund managers, 560+ private market funds and 5,100+ portfolio companies. We have 57 active investment vehicles. PES occupies a differentiated position within the private markets ecosystem helping our investors access, perform due diligence, analyze and invest in what we believe are attractive middle and lower-middle market private equity opportunities. We are further differentiated by the scale, depth, diversity and accuracy of our constantly expanding proprietary private markets database that contains comprehensive information on more than 6,000 investment firms, 11,100 funds, 49,000 individual transactions, 32,600 private companies and 458,000 financial metrics. As of December 31, 2024, PES managed $14.1 billion of FPAUM.

Venture Capital Solutions "VCS"

Under VCS, we make investments in venture capital funds across North America and specialize in targeting high-performing, access-constrained opportunities. The VCS investment team, which is comprised of 16 investment professionals

6

with an average of 24+ years of experience, has deep and long-standing investor and fund manager relationships in the venture market which it has cultivated over the past 14+ years, including over 1,980+ investors, 110+ fund managers, 100+ direct investments, 415+ private market funds and 14,700+ portfolio companies. We have 20 active investment vehicles. VCS is differentiated by our innovative strategic partnerships and our vantage point within the venture capital and technology ecosystems, maximizing advantages for our investors. In addition, since 2011, we have partnered with Forbes to publish the Midas List, a ranking of the top value-creating venture capitalists. As of December 31, 2024, VCS managed $6.4 billion of FPAUM.

Private Credit Solutions "PCS"

Under PCS, we primarily make debt investments across North America, targeting lower middle market companies owned by leading financial sponsors and also offer certain private equity solutions. PCS also provides loans to mid-life, growth equity, venture and other funds backed by the unrealized investments at the fund level and provide financing for companies that would otherwise require equity. The PCS investment team, which is comprised of 54 investment professionals with an average of 25+ years of experience, has deep and long-standing relationships in the private credit market which it has cultivated over the past 22 years, including 440+ investors across 49 active investment vehicles and 1,800+ portfolio companies with $9.8+ billion capital deployed. Our PCS is differentiated by our relationship-driven sourcing approach providing capital solutions for growth-oriented companies. We are further synergistically strengthened by our PES network of fund managers, characterized by more than 630 credit opportunities annually. We currently maintain 80+ active sponsor relationships and have 125+ platform investments. Within PCS, the Company has investments that target renewable energy development and historic building renovation projects, as well as provide capital to small businesses that are woman or minority owned or operated in underserved communities. These investments are differentiated in both the breadth of impact areas served, the type of capital deployed and the duration of the impact investing track record. From the impact investing inception in 1999 through December 31, 2024, inclusive of proprietary assets and assets managed by affiliates, the Company has raised a total of $6.4 billion. Of the total AUM, impact assets represent $4.2 billion invested in over 1,000 projects and businesses across 40 states, Washington DC, and Puerto Rico and does not include investments made by non-impact affiliates. Investments in clean energy have generated an estimate of over 2,900 GWh of renewable energy from inception to December 31, 2024. As of December 31, 2024, PCS managed approximately $5.2 billion of FPAUM.

Our Vehicles

We have a flexible business model whereby our investors engage us across multiple specialized private market solutions through different specialized investment vehicles. Our vehicles have traditional, stable fee structures that generate performance fees, which are generally not accrued to P10 due to our structure. P10’s revenue associated with the funds are from the management fees while employees of P10 receive the vast majority of performance fees directly from the vehicles.

7

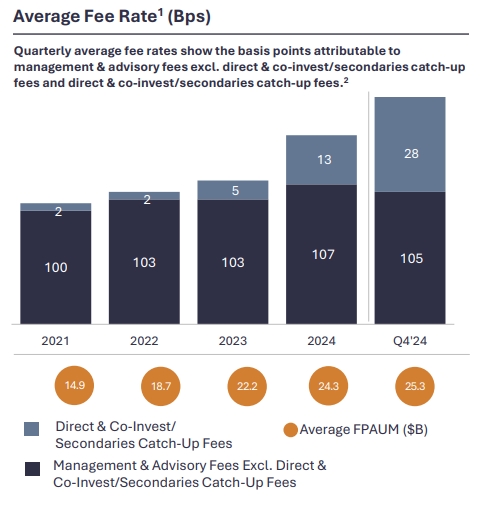

Our average annual fee rates remain stable at approximately 1% of average fee paying assets under management. Fees for our funds are often structured such that they step down, or decrease, over the life of the fund.

1. The average fee rates shown in the graph are calculated as Management and advisory fees divided by average FPAUM.

2. Catch-up fees are earned from investors that committed during the fundraising period of funds originally launched in prior periods, and as such, the investors are required to pay a catch-up fee as if they had committed to the fund at the first closing. While catch-up fees are not a significant component of our overall revenue stream, they may result in a temporary increase in our revenues in the period in which they are recognized.

8

We offer the following vehicles for our investors:

Primary Investment Funds

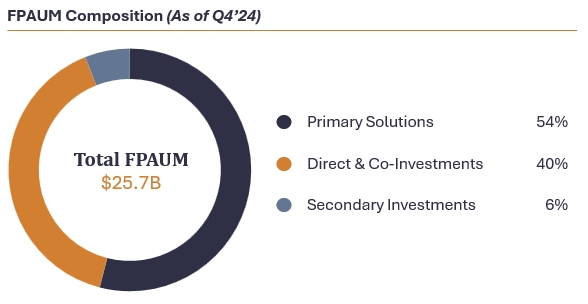

Primary investment funds refer to investment vehicles which target investments in new private markets funds, which in turn invest directly in portfolio companies. P10’s primary investment funds include both commingled investment vehicles with multiple investors, as well as our customized separate accounts, which typically include one investor. Primary investments are made during a fundraising period in the form of capital commitments, which are called upon by the fund manager and utilized to finance its investments in portfolio companies during a predefined investment period. We receive a fee stream that is typically based on our investors’ committed, locked-in capital. Capital commitments typically average ten to fifteen years, though they may vary by fund and strategy. We offer primary investment funds across our private equity and venture capital solutions. Our primary funds comprise approximately $13.9 billion of our FPAUM as of December 31, 2024.

Direct and Co-Investment Funds

Direct and co-investments involve acquiring an equity interest in or making a loan to an operating company, project, property, alternative asset manager, or asset, typically by co-investing alongside an investment by a fund manager or by investing directly in the underlying asset. P10’s direct and co-investment funds include both commingled investment vehicles with multiple investors as well as our customized separate accounts, which typically include one investor. Capital committed to direct investments and co-investments is typically invested immediately, thereby advancing the timing of expected returns on investment. We typically receive fees from investors based upon committed capital, with some funds receiving fees based on invested capital; capital commitments which typically average ten to fifteen years, though they may vary by fund. We offer direct and co-investment funds across our private equity, venture capital, and private credit solutions. Our direct investing platform comprises approximately $10.2 billion of our FPAUM as of December 31, 2024.

Secondaries

Secondaries refer to investments in existing private markets funds through the acquisition of an existing interest in a private markets fund by one investor from another in a negotiated transaction. In so doing, the buyer agrees to take on future funding obligations in exchange for future returns and distributions. Because secondary investments are generally made when a primary investment fund is three to seven years into its investment period and has deployed a significant portion of its capital into portfolio companies, these investments are viewed as more mature. We typically receive fees from investors on committed capital for a decade, the typical life of the fund. We currently offer secondaries funds across our private equity solutions. Our secondary funds comprise approximately $1.6 billion of our FPAUM as of December 31, 2024.

9

Our Investors

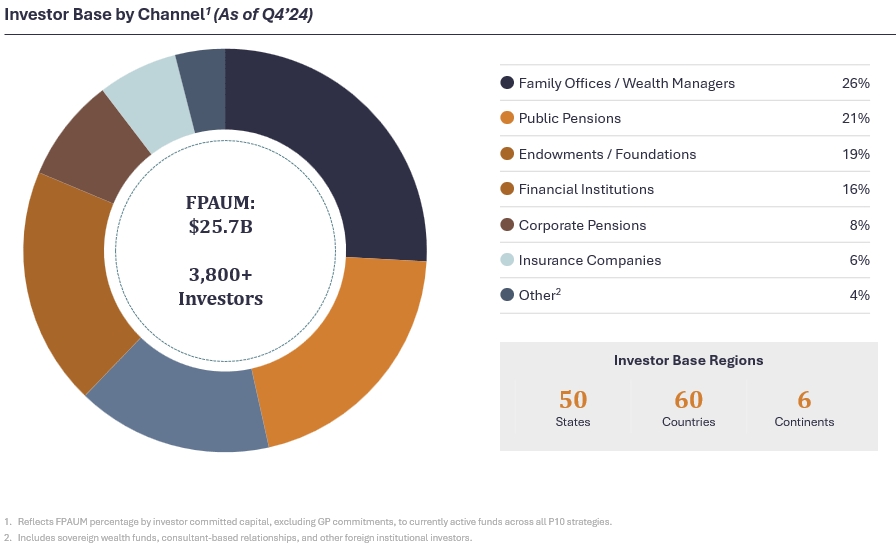

We believe our comprehensive value proposition across our private market solutions, vehicles offering, data analytics, portfolio monitoring and reporting has enabled us to build strong relationships with our existing investors and to attract new high-quality investors. We leverage our differentiated approach to serve a broad set of investors across multiple geographies. As of December 31, 2024, we have a global investor base of over 3,800 investors, across 50 states, 60 countries and 6 continents – including some of the world’s largest pension funds, endowments, foundations, corporate pensions and financial institutions. In addition, we have a strong footprint within some of the most prominent family offices and high net worth individuals.

The following chart illustrates the diversification of our investor base as of December 31, 2024:

Our Distribution and Marketing

We continuously seek to strengthen and expand our relationships with our current and prospective investors. We have a dedicated team of business development and investor relations professionals who maintain an active and transparent dialogue with an expansive list of existing and prospective investors and while we have a significant presence in North America, we have cultivated relationships with a number of international investors.

Our business development and investor relations professionals frequent dialogue with existing and prospective investors, enable us to monitor investor preferences and tailor future product offerings to meet investor demand. Prospective investors that desire to learn more about us often visit our offices to conduct in-depth due diligence. Our business development and investor relations professionals lead this process, coordinate meetings, and continue to be the prospective investor’s principal point of contact throughout their decision-making process. Our business development and investor relations professionals are also responsible for being the principal points of contact for our existing investors, and for our customized separate accounts, we work with each investor to design and implement a specific strategic plan in accordance with the investment guidelines agreed to by us and the investor.

10

Our Investment Performance

We believe the performance of our investment vehicles acts as a key retention mechanism for our existing investors and a primary attribute for prospective investors. We attribute our strong investment performance to several factors, including: our broad private market relationships and access, our diligent and responsible investment process, our tenured investing experience and our premier data capabilities. In concert, these factors enable us to pursue attractive, risk-adjusted investment opportunities to meet our investors’ investment objectives.

Our History

P10’s mission is to be the premier private markets solutions provider focused on the middle and lower middle market. We provide global institutional investors differentiated access to a broad set of solutions and specialized investment vehicles across attractive asset classes and geographies generating competitive risk-adjusted returns. As of December 31, 2024, we have $25.7 billion in fee paying assets under management. We offer a comprehensive set of investment strategies to clients, including both commingled funds and customized separate accounts within our primary investment funds, secondary, direct investment, co-investment vehicles, and advisory solutions. Since October 2017, we have been focused on building best-in-class solutions aimed at growing our fee paying assets under management. Prior to October 2017, the Company took strategic actions designed to lay the foundation for what is now known as P10.

The Company's history began with founding P10 Holdings as a Texas corporation in 1992 and reincorporating in Delaware in 2000. On November 19, 2016, P10 Holdings completed the sale of substantially all of its assets and liabilities and operations and became a non-operating company focused on monetizing our retained intellectual property and acquiring profitable businesses and our business primarily consisted of cash, certain retained intellectual property assets and our net operating losses and other tax benefits. In March 2017, P10 Holdings filed for re-organization under Chapter 11 of the Federal Bankruptcy Code, using a prepackaged plan of reorganization. In connection with the filing, P10 Holdings entered into a Restructuring Support Agreement with 210/P10 Investment LLC, as well as a Restructuring Support Agreement with the 2016 purchaser of our assets. P10 Holdings emerged from bankruptcy on May 3, 2017. A key feature of the Restructuring Support agreement included 210/P10 Investment LLC providing capital and management for the company post-bankruptcy.

Our entry into the alternative asset management industry originated with the acquisitions of RCP Advisors (RCP 2 and RCP 3). RCP Advisors was founded in 2001 and is a leading sponsor of private equity, funds-of-funds, secondary funds and co-investment funds. On October 5, 2017, we closed on the acquisition of RCP 2 and entered into a purchase agreement to acquire RCP 3 on January 2018. On January 3, 2018, we closed on the acquisition of RCP 3. RCP 2 and RCP 3 are registered investment advisors with the United States Securities and Exchange Commission.

On April 1, 2020, we completed the acquisition of Five Points Capital, Inc., a leading lower middle market alternative investment manager focused on providing equity and debt capital to private, growth-oriented companies and limited partner capital to other private equity funds. Five Points is focused exclusively in the U.S. lower middle market. Five Points is a registered investment advisor with the United States Securities and Exchange Commission.

On October 2, 2020, we completed the acquisition of TrueBridge, an investment firm focused on investing in venture capital through fund-of-funds, co-investments, and separate accounts. TrueBridge is a registered investment advisor with the United States Securities and Exchange Commission.

On December 14, 2020, the Company completed the acquisition of 100% of the equity interest in ECG, and a non-controlling interest in Enhanced Capital Partners, LLC (“ECP”, and collectively with ECG, “Enhanced”). Enhanced undertakes and manages equity and debt investments in impact initiatives across North America, targeting underserved areas and other socially responsible end markets including renewable energy, historic building renovations, and affordable housing. ECP is a registered investment advisor with the United States Securities and Exchange Commission.

On September 30, 2021, we completed the acquisitions of Hark Capital and Bonaccord Capital Advisors. Hark provides loans to mid-life private equity, growth equity, venture and other funds. These loans are backed by the unrealized investments at the fund level and provide financing for companies that would otherwise require equity. Bonaccord acquires minority equity investments in a diversified portfolio of alternative markets asset managers with a focus on mid-sized managers across private equity, private credit and real assets.

11

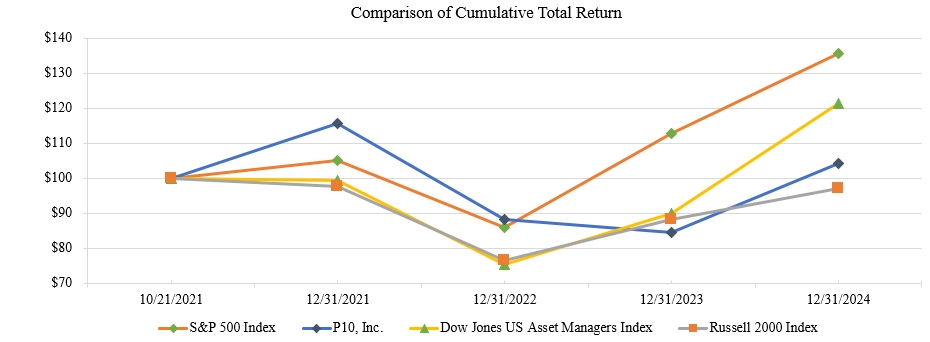

During 2021, the Company began exploring the benefits of going public on a listed exchange and raising additional capital through an equity issuance. On October 18, 2021, the Company announced an Initial Public Offering ("IPO") and corporate reorganization that would make P10 Holdings a wholly-owned subsidiary of P10, Inc. The IPO priced on October 20, 2021, and P10’s Class A common stock began trading on the NYSE on October 21, 2021 under the ticker “PX”. Investors purchased 23,000,000 Class A shares in conjunction with the IPO and the Company gained a top-tier set of institutional investors. The IPO process is described in more detail below.

In June 2022, the Company formed P10 Advisors, a fully consolidated subsidiary, to manage investment opportunities that are sourced across the P10 platform but do not fit within an existing investment mandate.

On October 13, 2022, the Company completed the acquisition of all of the issued and outstanding membership interests of WTI. WTI provides senior secured financing to early-stage and emerging stage life sciences and technology companies. WTI is a registered investment advisor with the United States Securities and Exchange Commission.

Simultaneously with the acquisition of WTI, the Company completed a restructuring of P10 Intermediate and subsidiaries to LLC entities that are considered disregarded entities for federal income tax purposes. This allowed the WTI sellers to obtain a partnership interest in P10 Intermediate and all of its subsidiaries. As a result of the acquisition, the WTI sellers obtained 3,916,666 membership units of P10 Intermediate, which can be exchanged into 3,916,666 shares of P10 class A common stock, following applicable restrictive periods.

The results of WTI’s operations have been included in the consolidated financial statements effective October 13, 2022. The Company reports noncontrolling interest related to the partnership interests which are owned by the WTI sellers. This is recorded as noncontrolling interest on the Consolidated Balance Sheets and Consolidated Statements of Operations. Noncontrolling interest is allocated a share of income or loss in the respective consolidated subsidiaries in proportion to their relative ownership interest. Additionally, the Company makes periodic distributions to the WTI sellers for tax related and other agreed upon expenses as disclosed in the purchase agreement.

On September 16, 2024, the Company entered into an equity purchase agreement of Qualitas, which is expected to close in the first quarter of 2025. Qualitas is a leading European lower middle market private equity fund-of-funds manager based in Madrid, Spain with roughly $1 billion in fee-paying assets under management. The transaction does not include any carried interest for legacy funds. This acquisition established an European presence and meaningfully grows P10's investor base, positioning the Company as a leading global, multi-strategy private markets firm focused on the middle and lower-middle markets.

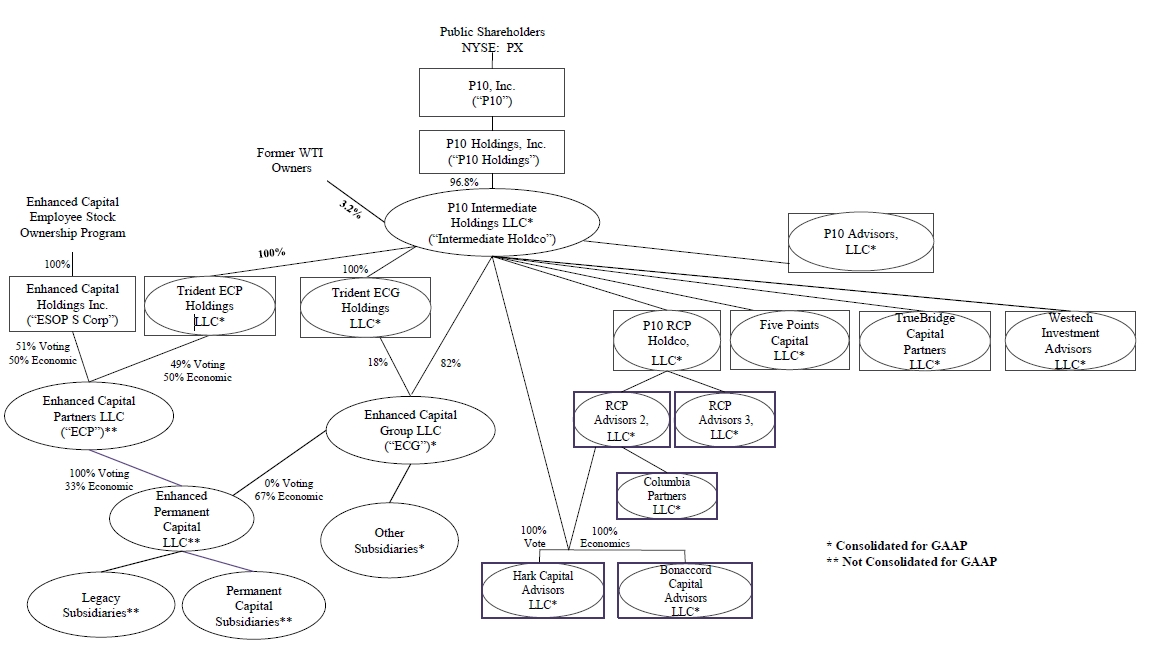

ORGANIZATIONAL STRUCTURE

We completed an offering in connection with our IPO and concurrent listing on the New York Stock Exchange. On October 21, 2021, we issued 11,500,000 shares of our Class A common stock to the purchasers in the offering and selling stockholders sold 8,500,000 shares of our Class A common stock. Pursuant to our issuance of Class A common stock, we received net proceeds of approximately $129.4 million after deducting underwriting discounts and commissions but before expenses based on the initial public offering price of $12.00 per share. On November 19, 2021, we announced that the underwriters of the public offering fully exercised their option to acquire an additional 3,000,000 shares of Class A common stock at the public offering price of $12.00 per share, less underwriting discounts and commissions. These shares were sold by certain stockholders of P10 and P10 did not receive any proceeds from the sale.

Simultaneously with the acquisition of WTI, the Company completed a restructuring of P10 Intermediate and subsidiaries to LLC entities that are considered disregarded entities for federal income tax purposes. This allowed the sellers to obtain a partnership interest in P10 Intermediate and all of its subsidiaries. As a result of the acquisition, the WTI sellers obtained 3,916,666 membership units of P10 Intermediate, which can be exchanged into 3,916,666 shares of P10 class A common stock, following applicable restrictive periods.

12

The diagram below illustrates our structure and does not include all unconsolidated entities in which we hold non-controlling equity method investments.

Our Class B Common Stock

We have 43,461,442 outstanding shares of Class B common stock held of record by approximately 2,710 stockholders as of December 31, 2024. Each share of our Class B common stock entitles its holder to ten votes per share until a Sunset ("Sunset") occurs. A Sunset will occur on the earliest of the following: (a) the Sunset Holders cease to maintain direct or indirect beneficial ownership of 10% of the outstanding shares of Class A Common Stock (determined assuming all outstanding shares of Class B Common Stock have been converted into Class A Common Stock) (b) the Sunset Holders collectively cease to maintain direct or indirect beneficial ownership of at least 25% of the aggregate voting power of the outstanding shares of Common Stock and (c) upon the tenth anniversary of the effective date of our amended and restated certificate of incorporation. After a Sunset becomes effective, each share of Class B common stock will automatically convert into Class A common stock. In addition, each share of Class B common stock will automatically convert into Class A common stock upon any transfer except to certain permitted holders.

Because a Sunset may not take place for some time, it is expected that the Class B common stock will continue to entitle its holders to ten votes per share, and the Class B Holders will continue to exercise voting control over the Company, for the near future. The Class B Holders have approximately 87% of the combined voting power of our common stock.

Upon any transfer, Class B common stock converts automatically on a one-for-one basis to shares of Class A common stock, except in the case of transfers to certain permitted transferees. In addition, holders of Class B common stock may elect to convert shares of Class B common stock on a one-for-one basis into Class A common stock at any time.

Our current stockholders believe that the contributions of the current ownership group and management team have been critical in P10’s growth to date. We have a history of employee equity participation and believe that this practice has been instrumental in attracting and retaining a highly experienced team and will continue to be an important factor in maximizing long-term stockholder value. We believe that ensuring that our key decision-makers will continue to guide the direction of P10 results in a high degree of alignment with our stockholders, and voting members of the Class B common stock have ten votes per share which will help maintain this continuity.

13

Our Class A Common Stock

The Class A common stock have one vote per share and share ratably with our Class B common stock in all distributions.

Stockholders Agreement and Registration Rights

P10, Inc. entered into a stockholders agreement (the “Stockholders Agreement”) with certain investors, including employees, pursuant to which the investors were granted piggyback and demand registration rights prior to the IPO.

NYSE Controlled Company Agreement

P10, Inc. entered into a controlled company agreement (the “Controlled Company Agreement”) on October 20, 2021, with principals of 210 Capital, L.L.C. (“210 Capital”) and certain of their affiliates (the “210 Group”), RCP Advisors and certain of their affiliates (the “RCP Group”) and TrueBridge and certain of their affiliates (the “TrueBridge Group”), granting each party certain board designation rights. So long as the RCP Group and any of their permitted transferees who hold shares of common stock as of the applicable time continue to collectively hold a combined voting power of at least 5% of the shares of common stock outstanding immediately following the IPO, P10, Inc. shall include in its slate of nominees one (1) director designated by the RCP Stockholders. So long as TrueBridge and any of its permitted transferees who hold shares of common stock as of the applicable time continue to collectively hold a combined voting power of at least 5% of the shares of common stock outstanding immediately following the IPO, P10, Inc. shall include in its slate of nominees one (1) director designated by the TrueBridge Group.

On December 19, 2024, the Company entered into an amendment (the “Amendment”) to the Controlled Company Agreement to, among other things: (i) remove 210/P10 Acquisition Partners, LLC and certain members of the RCP Group thereunder, and (ii) remove the board nomination and other rights of 210/P10 Acquisition Partners, LLC. In connection with its entry into the Amendment, 210/P10 Acquisition Partners, LLC converted all shares of Class B Common Stock of the Company held by it into shares of Class A Common Stock of the Company.

The RCP Group and TrueBridge Group each have the right to nominate one director. These board designation rights are subject to certain limitations and exceptions.

Our Investment Process

We maintain rigorous investment, monitoring and risk management processes across each of our specialized private market solutions, all unified by a common philosophy and a focus on comprehensive analysis of fund managers and/or portfolio companies.

We believe our investment performance is attributable to a number of factors, including most notably our seasoned, dedicated investment teams and our methodical approach to investing that help us consistently source and analyze opportunities effectively. Our investment professionals are responsible for sourcing, selecting, evaluating, underwriting, diligencing, negotiating, executing, managing and exiting our investments. In addition, our investment professionals regularly develop new investor relationships and networks of industry insiders to proactively source new investments. Our ability to access top-tier, capacity constrained fund managers through a proactive and systematic sourcing process we believe is a significant differentiating factor for our investors.

Our investment committee members across our solutions have significant private markets experience and fully participate in the diligence process, which ensures consistent application of investment strategy, process, diversification and portfolio construction. In addition, the investment committees of our respective solutions review and evaluate investment opportunities through a comprehensive framework that includes both a qualitative and a quantitative assessment of the key risks of investments.

The details of our investment process are outlined below:

Opportunities Tracked

As of December 31, 2024, we track thousands of potential investment opportunities across private markets, spanning primary investment funds, secondaries and direct and co-investments. Our attractive positioning within the private markets

14

ecosystem, coupled with our synergistic network of general partners and extensive database has enabled us to cultivate a comprehensive funnel of what we believe are premier investment opportunities.

Initial Screen

Leveraging our extensive database, investment professionals submit investment opportunities for initial review, subject to delineated exceptions set forth in our funds’ investment committee charters or resolutions. To facilitate the initial review, the investment team summarizes the opportunity in a preliminary evaluation report and the opportunity is subsequently reviewed by senior members of the team for potential further consideration and investment.

Annual Due Diligence

For each potential investment opportunity, the responsible investment team gathers, analyzes and reviews available information on the underlying asset. The due diligence process is augmented further by our extensive database, which enables us to analyze and compare the investment opportunity to what we believe are precedent transactions. As part of the due diligence process, we also conduct operational due diligence and legal diligence, which evaluate the potential risks associated with the investment opportunity’s operational framework and legal standing. More specifically, our operational due diligence team focuses on legal, financial, IT and background checks, while our legal due diligence team focuses on review of legal documents, fund agreements and compliance.

Annual Investments Made

After our due diligence is completed, the responsible investment team works with the relevant Investment Committee to validate that each investment opportunity meets the investment objective of the portfolio at hand. The Investment Committee provides feedback on the general partner (and investment merits in the case of secondaries and direct and co-investments), risks and prospects of each investment opportunity. Provided that the opportunity meets the appropriate criteria, the investment committee issues an indicative approval to proceed with confirmatory due diligence. Upon successful confirmatory due diligence the Investment Committee will reconvene to review the investment for a final vote. Once final approval has been obtained, the investment team may proceed with commitments or funding.

Our Risk Management Process

Our risk management process includes risk identification, measurement, mitigation, monitoring and management/reporting, with particular risk assessments tailored by solution, vehicle and individual client. We apply our risk management framework across three distinct areas of our investment process: (a) the general partner, (b) the investment fund, and (c) the portfolio company. We seek to mitigate risk through prudent portfolio diversification and through comprehensive due diligence on general partners, investment funds and portfolio companies.

General Partner

We perform extensive, upfront due diligence on general partners prior to making an investment and all our current period partners are subject to our ongoing risk management framework. Key components of our ongoing risk management of general partners include monitoring the firm’s historical and current strategy, historical track record and anticipated performance, current team composition and remuneration, decision-making process, ability to add value, deal flow and fund terms. Furthermore, our risk management processes include reviewing information related to the general partners target asset classes, sector/sub-sectors, investment specialties, key personnel, and primary geographical regions in which the general partner invests.

Investment Fund

Investment Funds are also subject to our due diligence and risk management framework. Key components of our ongoing risk management of investment funds include monitoring vintage year, fund size, currency, as well as measures of historical performance (including percent of commitments called, distributions to paid in capital, residual value to paid in capital, net total value multiple of invested capital, net internal rate of return, and the date performance results were last updated), historical investments and benchmarking.

15

Portfolio Company

Key components of our ongoing risk management of portfolio companies include monitoring cash flow details, financial and operating metrics, and other relevant performance measurements. Our investments in our portfolio companies include both debt and equity.

In addition to our distinct ongoing risk management processes we participate in board meetings, investment funds’ annual meetings, maintain membership on limited partnership boards and advisory boards and remain in frequent dialogue with portfolio companies in an effort to remain appraised of relevant developments in the investment funds. We are also recipients of monthly and quarterly performance reporting packages, annual audited financial statements, along with K-1 tax reporting packages and evaluations of the state of the market generally.

Our ongoing monitoring efforts culminate in annual summaries featuring extensive qualitative and quantitative information of each portfolio company. The annual summaries help us benchmark each general partner to ensure each portfolio we invest in to ensure each portfolio is performing as expected.

Our Responsible Investment Philosophy

Responsible investment, which encompasses environmental, social and governance (“ESG”) and impact investing considerations, is important to our operating and investment philosophies. We believe that integration of an ESG framework into both our investment process and internal operations may improve long-term, risk-adjusted returns for our clients. Certain of our subsidiaries have developed a responsible investment policy. In addition, two of our subsidiaries are a signatory to the United Nations Principles for Responsible Investment (“UNPRI”). We aim to continually improve and evolve, and plan to review our policy annually.

Given our scale and position in the private markets ecosystem, we believe we are well positioned to help educate the broader investor and fund manager community on how best to integrate responsible investment considerations in their investment process and programs.

Our Fees and Other Key Contractual Terms

Specialized Investment Vehicles

While the terms of each fund may vary, we have outlined the key terms of the customized separate accounts and commingled funds within our specialized investment vehicles below:

Commingled Investment Vehicles

Capital Commitments

Investors in our investment funds generally make commitments to provide capital at the outset of a fund and deliver capital when called upon by us, as investment opportunities become available and to fund operational expenses and other obligations. The commitments are generally available for investment for 1 to 5 years, during what we call the commitment period. We typically have invested the capital committed to our funds, over a 3 to 5-year period.

Structure

Our investment funds are structured as limited partnerships organized by us accepting commitments or funds from our investors. Our investors become limited partners in our funds and a separate entity that we form and control acts as the general partner. Funds managed by the Company, who act as the general partner, make capital commitments to the limited partnership which are generally 1% of total capital commitments. Contingent upon the solution, each investment fund will have a designated “Manager”, which generally serves as the investment manager of the fund, responsible for all investment diligence, decision making and monitoring.

16

Fees

We earn management and advisory fees based on a percentage of investors’ capital commitments to, in funds or deployed capital. Management and advisory fees during the commitment period are charged on capital commitments and after the commitment period (or a defined anniversary of the fund’s initial closing) is reduced by a percentage of the management and advisory fees for the preceding years or charged on net invested capital or NAV, in select cases.

Duration and Termination

Our primary investment funds, secondaries funds and direct and co-investment funds are typically ten to fifteen years in duration, terminating either on a specific anniversary date, or after a determined number of years after the fund’s final close. Our funds are generally subject to extensions for up to 3 years at the discretion of the general partner and thereafter if consent of the requisite majority of investors, or in some cases, the fund’s advisory committee is obtained.

Separate Accounts

Capital Commitments

Investors in our separate accounts generally make commitments to provide capital at the outset of a fund and deliver capital when called upon by us, as investment opportunities become available and to fund operational expenses and other obligations. The commitments are generally available for investment for 4 to 5 years, during what we call the commitment period. We typically have invested the capital committed to our investment funds over a 5-year period.

Structure

Most of our separate accounts are contractual arrangements involving an investment management agreement between us and our investor. Within agreed-upon investment guidelines, we generally have full discretion to buy, sell or otherwise effect investment transactions involving the assets in the account, in the name and on behalf of our investor, although in some cases certain investors have the right to veto investments. The discretion to invest committed capital generally is subject to investment guidelines established by our investors or by us in conjunction with our investors. In some cases, at the investor’s request, we establish a separate investment vehicle, generally a limited partnership with our investor as the sole limited partner and a wholly owned subsidiary as the general partner. Our capital commitment to the limited partnership is typically 1% of total capital commitments. We manage the limited partnership under an investment management agreement between our investor and us.

Fees

We earn management and advisory fees based on a percentage of investors’ capital commitments to or, in select cases, net invested capital in, or NAV of, our investment funds. These fees often decrease over the life of the contract due to built-in declines in contractual rates and/or as a result of lower net invested capital balances or NAV as capital is returned to investors.

Duration and Termination

Separate account contracts typically can be terminated by our investors for specified reasons, but specific terms vary significantly from investor to investor and certain contracts may be terminated for any reason, typically with 5 to 90 days’ notice.

Our Competition

We compete in all aspects of our business with a large number of asset management firms, commercial banks, broker-dealers, insurance companies and other financial institutions. With respect to our investment strategies, we primarily compete with other private markets solutions providers within North America that specialize in private equity, venture capital, impact investing and private credit. We seek to maintain excellent relationships with general partners and managers of investment funds, including those in which we have previously made investments for our investors and those in which we may invest in the future, as well as sponsors of investments that might provide co-investment opportunities in portfolio companies alongside the sponsoring fund manager. However, because of the number of investors seeking to gain access to investment funds and co-investment opportunities managed or sponsored by the top performing fund managers, there can be no

17

assurance that we will be able to secure the opportunity to invest on behalf of our investors in all or a substantial portion of the investments we select, or that the size of the investment opportunities available to us will be as large as we would desire. Access to secondary investment opportunities is also highly competitive and is often controlled by a limited number of general partners, fund managers and intermediaries. Our ability to continue to compete effectively will depend upon our ability to attract highly qualified investment professionals and retain existing employees.

In order to grow our business, we must maintain our existing investor base and attract new investors. Historically, we have competed principally on the basis of the factors listed below:

The asset management business is intensely competitive, and in addition to the above factors, our ability to continue to compete effectively will depend upon our ability to attract highly qualified investment professionals and retain existing employees.

Regulatory and Compliance Matters

Our business is subject to extensive regulation in the United States at both the federal and state level and, in certain circumstances, outside the United States. Under these laws and regulations, the SEC, relevant state securities authorities and other foreign regulatory agencies have broad administrative powers, including the power to limit, restrict or prohibit an investment advisor from carrying on its business if it fails to comply with such laws and regulations. Possible sanctions that may be imposed include the suspension of individual employees, limitations on engaging in certain lines of business for specified periods of time, revocation of investment advisor and other registrations, censures and fines.

SEC Regulation

Certain subsidiaries of P10 are registered as investment advisers with the SEC. As a registered investment adviser, each is subject to the requirements of the Investment Advisers Act, and the rules promulgated thereunder, as well as to examination by the SEC’s staff. The Investment Advisers Act imposes substantive regulation on virtually all aspects of our business and our relationships with our investors and funds. Applicable requirements relate to, among other things, fiduciary duties to investors, engaging in transactions with investors, maintaining an effective compliance program, political contributions, personal trading, incentive fees, allocation of investments, conflicts of interest, custody, advertising, recordkeeping, reporting and disclosure requirements. The Investment Advisers Act also regulates the assignment of advisory contracts by the investment adviser. The SEC is authorized to institute proceedings and impose sanctions for violations of the Investment Advisers Act, ranging from fines and censures to termination of an investment adviser’s registration. The failure of any Adviser to comply with the requirements of the Investment Advisers Act or the SEC could have a material adverse effect on us.

Our separate accounts and funds are not registered under the Investment Company Act because we generally only form separate accounts for, and offer interests in our funds to, persons who we reasonably believe to be “qualified purchasers” as defined in the Investment Company Act. In addition, certain funds are not registered under the Investment Company Act because we limit such funds to 100 or fewer “persons” as defined in the Investment Company Act. In addition, certain WTI funds are registered under the Investment Company Act and must comply with the reporting and governance requirements of

18

the Investment Company Act. Compliance with the Investment Company Act can be complex and failure to comply can result in significant fines, penalties, loss to reputation and other material adverse effects on us.

ERISA-Related Regulation

Some of our funds are treated as holding “plan assets” as defined under the Employee Retirement Income Security Act of 1974, as amended (“ERISA”), as a result of investments in those funds by benefit plan investors. By virtue of its role as investment manager of these funds, each applicable Adviser is a “fiduciary” under ERISA with respect to such benefit plan investors. ERISA and the Code impose certain duties on persons that are fiduciaries under ERISA, prohibit certain transactions involving benefit plans and “parties in interest” or “disqualified persons” to those plans, and provide for monetary penalties for violations of these prohibitions. With respect to these funds' regulations, each Adviser relies on particular statutory and administrative exemptions from certain ERISA prohibited transactions, which exemptions are highly complex and may in certain circumstances depend on compliance by third parties whom we do not control. The failure of any Adviser or us to comply with these various requirements could have a material adverse effect on our business.

In addition, with respect to other investment funds in which benefit plan investors have invested, but which are not treated as holding “plan assets,” each Adviser relies on certain rules under ERISA in conducting investment management activities. These rules are sometimes highly complex and may in certain circumstances depend on compliance by third parties that we do not control. If for any reason these rules were to become inapplicable, each Adviser could become subject to regulatory action or third-party claims that could have a material adverse effect on our business.

Foreign Regulation

We provide investment advisory and other services and raise funds in a number of countries and jurisdictions outside the United States. In many of these countries and jurisdictions, which include the European Union ("EU"), the European Economic Area ("EEA"), the individual member states of each of the EU and EEA, Central and South America, Australia and other countries in the South Pacific, we and our operations, and in some cases our personnel, are subject to regulatory oversight and requirements. In general, these requirements relate to registration, licenses for our personnel, periodic inspections, the provision and filing of periodic reports, and obtaining certifications and other approvals. Across the EU, we are subject to the Alternative Investment Fund Managers Directive ("AIFMD") requirements regarding, among other things, registration for marketing activities, the structure of remuneration for certain of our personnel and reporting obligations. Individual member states of the EU have imposed additional requirements that may include internal arrangements with respect to risk management, liquidity risks, asset valuations, and the establishment and security of depositary and custodial requirements.

It is expected that additional laws and regulations will come into force in the UK, the EEA, the EU, and other countries in which we operate over the coming years. There have also been significant legislative developments affecting the private equity industry in Europe and there continues to be discussion regarding enhancing governmental scrutiny and/or increasing regulation of the private equity industry.

SBA Regulations

Several of our Advisers provide investment advisory and other services to funds which operate as Small Business Investment Companies ("SBICs") and are licensed by the Small Business Administration ("SBA"). SBICs supply small businesses with financing in both the equity and debt arenas. There are various requirements that apply to SBICs under SBA rules and regulations. These rules and regulations are sometimes highly complex. The SBA is authorized to institute proceedings and impose sanctions for violations of rules and regulations applicable to SIBCs, including forcing the liquidation of an SBIC. The failure of an Adviser to comply with the requirements of the SBA could have a material adverse effect on us.

Privacy and Cybersecurity Regulation

Certain of our businesses are subject to laws and regulations enacted by U.S. federal and state governments, the E.U. or other non-U.S. jurisdictions and/or enacted by various regulatory organizations or exchanges relating to the privacy and data security of the information of clients, employees or others, or to our cybersecurity measures in general, including the U.S. Gramm-Leach-Bliley Act of 1999, the European Union’s General Data Protection Regulation (“EU GDPR”), the U.K.

19

GDPR, China’s Personal Information Protection Law (PIPL), Canada’s Personal Information Protection and Electronic Documents Act (PIPEDA) and territorial Canadian privacy laws, and the Privacy Acts of Australia and New Zealand. In addition, California and at least nineteen other states have enacted comprehensive consumer privacy laws that impose compliance obligations with regard to the collection, use and disclosure of personal data, as well as cybersecurity requirements to protect personal data and our data systems in general. These privacy and cybersecurity laws and regulations have heightened our privacy and cybersecurity compliance obligations, impacted our businesses’ collection, processing and retention of personal data, including how we protect that data, and imposed strict standards for reporting data breaches. Many of these privacy and cybersecurity laws and regulations also provide significant penalties for non-compliance. For more information, see “Risk Factors—Risks Related to Our Industry.”

Future Developments

The SEC and various self-regulatory organizations and state securities regulators have in recent years increased their regulatory activities, including regulation, examination and enforcement in respect of asset management firms.

As described above, certain of our businesses are subject to compliance with laws and regulations of U.S. federal and state governments, non-U.S. governments, their respective agencies and/or various self-regulatory organizations or exchanges, and any failure to comply with these regulations could expose us to liability and/or damage our reputation. Our businesses have operated for many years within a legal framework that requires us to monitor and comply with a broad range of legal and regulatory developments that affect our activities. However, additional legislation, changes in rules promulgated by financial regulatory authorities or self-regulatory organizations or changes in the interpretation or enforcement of existing laws and rules, either in the United States or elsewhere, may directly affect our mode of operation and profitability.

Compliance

Each Adviser has a Chief Compliance Officer. Certain Advisers also maintain in-house legal staff as well as additional compliance staff. Each Adviser generally engages outside counsel to review, analyze and negotiate the terms of the documents relating to impact, primary, secondary and direct/co-investments. Because most of our separate account investors and certain of our advisory investors rely on us to negotiate terms, including terms about which certain investors are particularly sensitive or which are investor-specific, our compliance and legal teams work closely with both the investors and outside counsel. Our compliance and legal teams also work closely with our investment teams during negotiations. Typically, outside counsel negotiates directly with fund managers and deal sponsors and their counsel the terms of all limited partnership agreements, subscription documents, side letters, purchase agreements and other documents relating to primary, secondary and direct co-investments. Our compliance and legal teams review and make recommendations regarding amendments and requests for consents presented by the fund managers from time to time. In addition, our compliance and legal teams work with outside counsel as we deem necessary to prepare, review and negotiate all documents relating to the formation and operation of our funds.

Each Adviser’s compliance team is responsible for overseeing and enforcing our policies and procedures relating to compliance with the laws applicable to our business both U.S. and foreign. This includes our code of ethics and personal trading policies.

We have an outsourced Internal Audit group, which have disclosure controls and procedures and internal controls over financial reporting, which are documented and assessed for design and operating effectiveness in accordance with the U.S. Sarbanes-Oxley Act of 2002. Our Internal Audit group independently reports to an audit committee of our board of directors, operates with a global mandate and is responsible for the examination and evaluation of the adequacy and effectiveness of the organization’s governance and risk management processes and internal controls, as well as the quality of performance in carrying out assigned responsibilities to achieve the organization’s stated goals and objectives.

Human Capital

The Company believes that a strong focus on human capital through the talent we hire and retain is critical to maintaining our competitiveness. As of December 31, 2024, we have 267 full-time equivalent employees, primarily located in the United States, including 112 investment professionals. Our employees are not represented by a collective bargaining group. We consider our employee relations to be strong and have not experienced interruptions of operations due to labor disagreements.

20

Human Capital Objectives

Our business is built on strong, trusted and relationships with stakeholders: employees, limited partners, general partners, and our public stockholders. As such, attracting, recruiting, developing, and retaining diverse talent is vital to our success. The Company is focused on supporting our employees, and we consider talent management to be essential to the ongoing success of our business. Our Board of Directors and Committees provide oversight of our human capital management strategy.

Sustainability

The Company’s executive leadership team and Board recognize that ESG is a strategic and operational imperative and established an internal team that is tasked with driving progress. In partnership with our employees, we are committed to protecting the natural environment and our communities through sustainable practices. We emphasize a culture of accountability and conduct our business in a manner that is fair, ethical, and responsible to earn the trust of our employees.

Employee Attraction, Recruitment, Development and Retention

We are also committed to pay equity and regularly review our compensation model to ensure fair and inclusive pay practices across our business. We offer competitive benefits packages that reflect the needs of our workforce. In the U.S., we provide all full-time employees medical, dental, and vision benefits, life and disability coverage, parental leave, education reimbursement, and paid time off. We provide retirement benefits including a 401(k)-match program. In addition to base salary, our employees participate in incentive plans that support our organizational philosophy of pay and performance. Our executive compensation program is designed to align incentives with achievement of the Company’s strategic plan and both short- and long-term operating objectives.

Health & Safety

We take the health and safety of our employees seriously. We expect each employee to follow our safety standards and protocols. We continue to utilize employee feedback and surveys to gather information to best serve our team members. Members of our human resource department annually review benefits to ensure we can meet the well-being of our employees and their families.

Diversity and Inclusion

Our commitment to Diversity and Inclusion "D&I" starts with our goal of developing a workforce that is diverse in background, knowledge, skill, and experience. We have implemented policies and training focused on non-discrimination and harassment prevention. We embrace diversity and inclusion, which we believe fosters leadership through new ideas and perspectives. In 2024, we continued the evolution of our D&I strategy and objectives and recognize it as an ongoing business imperative.

AVAILABLE INFORMATION

We maintain a website with the address https://ir.p10alts.com/. We are not including the information contained on our website as part of, or incorporating it by reference into, this Form 10-K. Through our website, we make available free of charge our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to these reports in a timely manner after we provide them to the Securities and Exchange Commission (“SEC”).

21

Item 1A. Risk Factors.

Risks Related to Our Business

Our revenue in any given period is dependent on the number of fee-paying clients in such period. While most of our revenue is derived from management and advisory fees based on committed capital that is typically subject to multi-year lock up agreements, under certain limited circumstances, the committed capital can be withdrawn early, or we can be removed or terminated as the adviser or general partner to a particular client.

Our revenue is comprised virtually entirely of management and advisory fees from our registered investment adviser subsidiaries (each, an “Adviser”), with the vast majority of fees earned on committed capital that is typically subject to between 10 and 15 year lock up agreements, although in many cases, the contractual fees decline over the period, after the investment period of three to five years ends. Our investors engage us across multiple private markets solutions through different vehicles, including primary investment funds, direct and co-investment funds and secondary funds. Primary investment funds and direct and co-investment funds include both commingled investment vehicles with multiple investors as well as customizable separate accounts, which typically include one customer. Our revenue in any given period is dependent on the number of fee-paying investors in such period. For our specialized, commingled funds, our fees may terminate if we are removed for certain cause events such as a key person event or without cause by a super majority of investors. Our customized separate account and advisory account business operates in a highly competitive environment. While clients of our separate account and advisory account businesses may have multi-year contracts, certain of these contracts only provide for fees to the extent a client elects to make an investment. In addition, the separate accounts and advisory contracts may be terminated by the client for cause or without cause upon advance notice to us. In connection with these terminable contracts, we may lose clients as a result of the sale or merger of a client, a change in a client's senior management, competition from other financial advisors and financial institutions and other causes. Moreover, certain of our contracts with state government-sponsored clients are secured through such government’s request for proposal process, and can be subject to renewal. If multiple clients were to exercise their termination rights or fail to renew their existing contracts or investors removed us from managing a fund and we were unable to secure new clients, our fees would decline. In the case of any such events, the management fees and advisory fees we earn in connection with managing such account or fund would immediately cease, which could result in an adverse effect on our revenues. If we experience a change of control (as defined under the Investment Advisers Act of 1940, as amended (the “Investment Advisers Act”), or as otherwise set forth in the governing documents of our funds), continuation of the investment management agreements with our funds and our separate account clients would be subject to investor or client consent. We cannot assure you that required consents will be obtained if such a change of control occurs.

If the investments we make on behalf of our specialized investment vehicles perform poorly, our ability to raise capital for future specialized investment vehicles may be materially and adversely affected.

Our revenue from our investment management business is derived from fees earned for our management of our specialized investment vehicles and advisory accounts and with respect to certain of our specialized investment vehicles. We have no economic interest, ownership in or beneficiary interest in the performance of the funds (except for a 5% carried interest in RCP FF Small Buyout Co-Investment Fund, LP). Our subsidiaries serve as the advisors of the affiliated private equity funds, funds-of-funds, secondary funds and co-investment funds and receive management and advisory fees for the services performed. In the event that our specialized investment vehicles or individual investments perform poorly, the fund manager’s revenues and earnings derived from incentive fees will decline, which may result in a decrease in our management and advisory fee revenue and make it more difficult for us to raise capital for new specialized funds or gain new customized separate account clients in the future.