UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

__________________________________________________________________

FORM 10-K

__________________________________________________________________

(Mark One)

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the fiscal year ended December 31 , 2022

OR

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from ______________ to ______________

Commission file number 001-40481

__________________________________________________________________

__________________________________________________________________

(Exact name of registrant as specified in its charter)

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | ||||

(Address of Principal Executive Offices) | (Zip Code) | ||||

(949 ) 608-0854

Registrant's telephone number, including area code

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||||||||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports); and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ | ||||||||

☒ | Smaller reporting company | ||||||||||

Emerging growth company | |||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 262(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

The aggregate market value of the voting and non-voting common stock held by non-affiliates of the Registrant on June 30, 2022, based on the closing price of $5.70 for shares of the Registrant’s Class A common stock as reported by the Nasdaq Stock Market LLC, was approximately $657.4 million. Shares of common stock beneficially owned by each executive officer, director, and holder of more than 10% of our common stock have been excluded in that such persons may be deemed to be affiliates. This determination of affiliate status is not necessarily a conclusive determination for other purposes.

The number of shares outstanding of the registrant’s Class A and Class V common stock as of March 21, 2023, was 140,325,777 (excluding 1,725,000 Class A shares held in escrow and 645,002 Class A shares subject to restricted stock awards) and 19,829,941 , respectively.

DOCUMENTS INCORPORATED BY REFERENCE

| Auditor Firm ID: | Auditor Name: | Auditor Location: | |||||||||||||||||||||

FORWARD-LOOKING STATEMENTS

This report contains “forward-looking statements” (within the meaning of Section 21E of the United States Securities Exchange Act of 1934, as amended, and Section 27A of the Securities Act of 1933, as amended). Such statements include, but are not limited to, statements regarding the Company’s future business and financial performance and prospects, and other statements identified by words such as “will likely result,” “expect,” “anticipate,” “estimate,” “believe,” “intend,” “plan,” “project,” “outlook,” “should,” “could,” “may” or words of similar meaning. Such forward-looking statements are based upon the current beliefs and expectations of the Company’s management and are inherently subject to significant business, economic and competitive uncertainties and contingencies, many of which are difficult to predict and generally beyond our control. Actual results and the timing of events may differ materially from the results included in such forward-looking statements. In addition to the factors disclosed under “Risk Factors” in Part I, Item 1A herein, the following factors, among others, could cause actual results and the timing of events to differ materially from the anticipated results or other expectations expressed in such forward-looking statements: downturns or volatility in general economic conditions; the impact of the COVID-19 pandemic or a similar public health crisis; the impact of Russia’s invasion of Ukraine; the Company’s reliance on contract manufacturing and outsourced supply chain and the availability of semiconductors and manufacturing capacity; competitive products and pricing pressures; the Company’s ability to win competitive bid selection processes and achieve additional design wins; the impact of any acquisitions the Company may make, including its ability to successfully integrate acquired businesses and risks that the anticipated benefits of any acquisitions may not be fully realized or take longer to realize than expected; management’s ability to develop, market and gain acceptance for new and enhanced products and expand into new technologies and markets; trade restrictions and trade tensions; and political or economic instability in the Company’s target markets. indie cautions that the foregoing list of factors is not exclusive.

All information set forth herein speaks only as of the date hereof, and the Company disclaims any intention or obligation to update any forward-looking statements made in this report or in its other public filings, whether as a result of new information, future events or otherwise, except as required by law.

References in this Annual Report on Form 10-K to “indie,” the “Company,” “we,” “us,” and “our” refer to indie Semiconductor, Inc., a Delaware corporation, and its consolidated subsidiaries, or (in the case of references prior to the consummation of the business combination (the “Transaction”) with Thunder Bridge Acquisition II, Ltd. (“TB2”) in June 2021) to our predecessor Ay Dee Kay, LLC, a California limited liability company (“ADK LLC”). All references to U.S. dollar amounts are in thousands, other than share amounts, per share amount, date or the context otherwise requires.

TABLE OF CONTENTS

| Page | ||||||||

Item 1A. | Risk Factors | |||||||

Item 7. | Management's Discussion and Analysis of Financial Condition and Results of Operations | |||||||

3

PART I

ITEM 1. BUSINESS

Company Overview

indie offers highly innovative automotive semiconductors and software solutions for Advanced Driver Assistance Systems (“ADAS”), autonomous vehicle, in-cabin, user experience (including connected car) and electrification applications. The Company focuses on edge sensors across multiple modalities spanning light detection and ranging (“LiDAR”), radar, ultrasound and computer vision. These functions represent the core underpinnings of both electric and automated vehicles, while the advanced user interfaces are transforming the in-cabin experience to mirror and seamlessly connect to the mobile platforms people rely on every day. indie is an approved vendor to Tier 1 automotive suppliers and its platforms can be found in marquee automotive manufacturers around the world.

Through innovative analog, digital and mixed-signal integrated circuits (“ICs”) with software running on the embedded processors, we are developing a differentiated, market-leading portfolio of automotive products. Our technological expertise, including cutting-edge design capabilities and packaging skillsets, together with our deep applications knowledge and strong customer relationships, have enabled us to cumulatively ship over 200 million semiconductor devices since our inception.

Our go-to-market strategy focuses on collaborating with key customers and partnering with Tier 1s via aligned product development, in pursuit of solutions addressing the automotive industry’s highest growth applications. We leverage our core capabilities in system-level hardware and software integration to develop highly integrated, ultra-compact and power efficient solutions. Further, our products meet or exceed the quality standards set by the more than 25 global automotive manufacturers who utilize our devices today.

With a global footprint, we support leading customers from our design and application centers located in North and South America, Middle East, Asia and Europe, where our local teams work closely on their unique design requirements.

Recent Acquisitions

Silicon Radar

On February 21, 2023, Symeo GmbH (“Symeo”), one of our wholly-owned subsidiaries, completed its acquisition of all of the outstanding capital stock of Silicon Radar GmbH, a limited liability company organized under the laws of Germany (“Silicon Radar”). The acquisition was consummated pursuant to a Share Purchase Agreement by and among Symeo, indie and the holders of the outstanding capital stock of Silicon Radar. The closing consideration consisted of (i) $9.0 million in cash, (ii) approximately 980,000 shares of indie’s Class A common stock, par value $0.0001 per share and (iii) a contingent consideration payable in cash or in Class A common stock subject to Silicon Radar’s achievement of certain revenue-based and design-win milestones through December 31, 2024. The purchase price is subject to working capital and other adjustments as provided in the merger agreement.

GEO Semiconductor Inc.

On February 9, 2023, we entered into an Agreement and Plan of Merger, pursuant to which Gonzaga Merger Sub Inc., a Delaware corporation and indie’s wholly-owned subsidiary, will merge with and into GEO Semiconductor Inc., a Delaware corporation (“GEO”), with GEO surviving as a wholly-owned subsidiary of indie (the “Merger”). The aggregate consideration for the Merger, which is up to $270.0 million, consisted of (i) $90.0 million payable in cash at closing, (ii) $90.0 million payable in indie shares of Class A common stock, par value $0.0001 per share (the “Common Stock”) at closing, and (iii) up to $90.0 million payable in cash or Common Stock subject to achieving certain GEO-related revenue targets. The purchase price is subject to working capital and other adjustments as provided in the merger agreement. The transaction was completed on March 3, 2023.

Symeo GmbH

On October 21, 2021, we entered into a definitive agreement with Analog Devices (“ADI”) to acquire Symeo GmbH. The acquisition was approved by the German government on January 4, 2022 and closed on the same day. The total consideration paid for this acquisition consisted of (i) $8.7 million in cash at closing, net of cash acquired; (ii) a $10.0 million promissory note payable in January 2023 with a fair market value of $9.7 million; and (iii) an equity-based earn-out of up to 858,369 shares of indie Class A common stock based on future revenue growth. The fair market value of this equity-based earn-out was $7.8 million on January 4, 2022.

4

ON Design Israel Ltd

On October 1, 2021, we entered into a definitive agreement with Onsemi (“Onsemi”) and completed the acquisition of ON Design Israel Ltd. (“ON Design Israel”), for $5.0 million in cash paid upon close (net of cash acquired), $7.5 million of cash in 2022 and up to $7.5 million of cash based on design win performance.

We paid a premium (i.e. goodwill) over the fair value of the net tangible and identified intangible assets acquired as part of the Symeo and On Design acquisitions brought us an engineering development team with broad experience in millimeter wave technology and radar system implementation, respectively, which will accelerate indie’s entry into the radar market and enable us to capture strategic opportunities among Tier 1 customers.

TERAXION, INC

On August 27, 2021, indie entered into a Share Purchase Agreement, pursuant to which indie’s wholly-owned Canadian subsidiary (“Purchaser”) agreed to purchase all of the outstanding capital stock of TeraXion from the existing stockholders. The transaction was completed on October 12, 2021 and TeraXion became a wholly-owned subsidiary of ADK, LLC as a result of this acquisition.

The aggregate purchase price of this acquisition was CAD $200.0 million (the “Purchase Price”), which was payable 50% in cash and 50% in indie’s shares of Class A common stock, subject to various purchase price adjustments. Upon completion of the transaction, the total consideration paid for this acquisition consisted of (i) approximately $75.3 million in cash (including debt paid at closing and net of cash acquired); (ii) the issuance by indie of 5,805,144 shares of indie Class A common stock with a fair value of $65.2 million based on the market value of $11.23 per share; and (iii) the assumption by indie of TeraXion options, which became exercisable to purchase 1,542,332 shares of indie Class A common stock with a fair value of $17.2 million.

TeraXion is a market leader in the design and manufacture of innovative photonic components. We paid a premium (i.e. goodwill) over the fair value of the net tangible and identified intangible assets acquired as this acquisition accelerates indie’s vision of becoming a semiconductor and software level solutions provider for multiple sensor modalities spanning ADAS and autonomous vehicles.

Execution of At-The-Market Agreement

On August 26, 2022, indie entered into an At Market Issuance Agreement (“ATM Agreement”) with B. Riley Securities, Inc., Craig-Hallum Capital Group LLC and Roth Capital Partners, LLC (collectively as “Sales Agents”) relating to shares of our Class A common stock, par value $0.0001 per share. In accordance with the terms of the Sales Agreement, we may offer and sell shares of its Class A common stock having an aggregate offering price of up to $150.0 million from time to time through the Sales Agents, acting as our agent or principal. We implemented this program for the flexibility that it provides to the capital markets and to best time our equity capital needs. As of December 31, 2022, indie has raised gross proceeds of $17.2 million and issued 2,131,759 shares of Class A common stock at an averaged per-share sales price of $8.07 through this program and had approximately $132.8 million available for future issuances under the ATM Agreement. For the fiscal year ended December 31, 2022, indie incurred total issuance costs of $0.4 million.

Reverse Recapitalization with Thunder Bridge Acquisition II

On June 10, 2021, we completed a series of transactions (the “Transaction”) with Thunder Bridge Acquisition II, Ltd (“TB2”) pursuant to the Master Transactions Agreement dated December 14, 2020, as amended on May 3, 2021 (the “MTA”). In connection with the Transaction, Thunder Bridge II Surviving Pubco, Inc, a Delaware corporation (“Surviving Pubco”), was formed to be the successor public company to TB2, TB2 was domesticated into a Delaware corporation and merged with and into a merger subsidiary of Surviving Pubco. Additionally, we consummated a Private Investment in Public Equity (“PIPE”) financing, pursuant to which Surviving Pubco issued 15 million Class A common shares, generating net proceeds of $150 million as a result of the Transaction. Also, on June 10, 2021, Surviving Pubco changed its name to indie Semiconductor, Inc., and listed our shares of Class A common stock, par value $0.0001 per share on The Nasdaq Stock Market LLC under the symbol “INDI.”

The Transaction was accounted for as a reverse recapitalization in accordance with generally accepted accounting principles in the United States of America (“U.S. GAAP”). indie is deemed to be the accounting predecessor of the combined business and is the successor registrant for U.S. Securities and Exchange Commission (“SEC”) purposes, meaning that our financial statements

5

for previous periods will be disclosed in the registrant’s future periodic reports filed with the SEC. The most significant change in our reported financial position and results of operations was gross cash proceeds of $399.5 million from the merger transaction, which includes $150 million in gross proceeds from the PIPE financing that was consummated in conjunction with the Transaction. The increase in cash was offset by transaction costs incurred in connection with the Transaction of approximately $43.5 million plus the retirement of indie’s long-term debt of $15.6 million. Approximately $29.8 million of the transaction costs and all of indie’s long-term debt were paid as of June 30, 2021. Approximately $21.8 million of the transaction costs paid as of June 30, 2021 were paid by TB2 as part of the closing of the Transaction. The remainder of the transaction costs were paid in the third quarter of 2021.

Industry Overview

At the highest level, semiconductors can be classified either as discrete devices, such as individual transistors, or integrated circuits, where a number of transistors and other components are combined to form a more complicated electronic subsystem. ICs can be divided into three primary categories: digital, analog, and mixed-signal. Digital ICs, such as memory devices and microprocessors, can store or perform arithmetic functions with data. Analog ICs, by contrast, handle real-world signals such as temperature, pressure, light, sound or speed, and also perform power management functions such as regulating or converting voltages for electronic devices. Mixed-signal ICs combine digital and analog functions onto a single chip and play an important role in bridging real-world inputs into the digital domain.

Historically, growth in the semiconductor industry has been driven by content expansion in computing, mobile and consumer electronics. However, research analysts anticipate that as each of these markets approaches saturation, the automotive sector will become one of the fastest growing opportunities. Specifically, according to IHS, the global automotive semiconductor market, which was valued at $54 billion in 2021, is projected to reach $130 billion by 2028, registering a compound annual growth rate (“CAGR”) over this period of 13%.

indie’s Market Opportunity

In today’s automobiles, semiconductors perform a variety of functions across multiple electronic components and systems, including sensing, processing data, storing information and converting or controlling signals. Semiconductor architectures vary significantly depending upon the specific function or application of the end product. They also differ based on a number of technical characteristics, including the degree of integration, level of customization, programmability and the underlying process technology utilized in manufacturing and assembly.

While semiconductors have always comprised the core building blocks of automotive electronic systems and equipment, recent technological advances have substantially increased their features, functionality and performance. Today, they support enhanced user interfaces and offer improved power consumption — all with reduced footprints and lower costs. These innovations have resulted in significant growth opportunities spanning diverse end markets and applications.

The three megatrends driving the automotive semiconductor market are catalyzed by: (i) the increasing electrification of vehicle drivetrains leading to the rapid proliferation of electric vehicles (“EVs”); (ii) the adoption of advanced driver assistance systems (“ADAS”) and driving automation functionality to improve road safety and strive towards higher levels of vehicle automation; and (iii) consumer demands for engaging, connected and convenient in-cabin user experience (UX).

Regarding electrification, S&P Global Mobility forecasts a 32% EV CAGR, with total annual EV production growing from 5 million in 2021, to 35 million in 2028, representing greater than one-third of all new light vehicle production. These forecast volumes are driven in part by increasing global governmental mandates to decarbonize road transportation which contributes around 16% of total greenhouse gases (“GHG”) according to the International Energy Agency, but also by improved consumer awareness and preference for low carbon vehicle options. While the state of California has been a global leader in this through its Low-Emission Vehicle (“LEV”), GHG and Zero-Emission Vehicle (“ZEV”) regulations and criteria, there is accelerating international momentum to address the climate change impact of vehicles through global forums such as the United Nations Conference of the Parties (“COP”). At COP26 in 2021, a combination of more than 100 countries, cities, states, vehicle manufacturers - including BYD Auto, Ford Motor Company, General Motors, Mercedes-Benz and Volvo Cars - and other key institutional stakeholders signed the Glasgow Declaration on Zero-Emission Cars and Vans to end the sale of internal combustion engines by 2035 in leading markets, and by 2040 worldwide. These collective initiatives, commitments and regulations – enabled by semiconductor technologies - will drive global EV uptake, reduce harmful emissions and benefit society as a whole. According to IHS, the semiconductor value to support this global drivetrain electrification will grow at a 26% CAGR, from $6.1 billion in 2021, to $30.3 billion in 2028.

6

In parallel to the rapid electrification of vehicles, global ADAS system deployments are expected to increase substantially, driven in part by mandates for increased vehicle safety features by governmental bodies such as the European Commission and the National Highway Traffic Safety Administration (“NHTSA”) in the United States. Better consumer safety awareness and demand created by safety assessment initiatives such as the European and U.S. New Car Assessment Programs (“NCAP”) have also directly influenced vehicle OEMs to incorporate minimum levels of crash safety and mitigation into new vehicles since 1979, and have evolved over time to include sophisticated semiconductor-enabled ADAS and automation capabilities such as Automatic Electronic Braking (“AEB”), Lane Keeping Assist (“LKA”), speed assistance and forward collision warning and, most recently, driver- and occupant monitoring (“DMS”, “OMS”), in order for a vehicle to be awarded a 5-star rating. With these global safety rating programs and governmental regulation, auto manufacturers are delivering more safety features to customers, the ADAS ECU market size will grow from $21 billion in 2021 to reach $50 billion by 2028, with corresponding semiconductor content of $8 billion to $31 billion, respectively, or a 21% CAGR, according to S&P Global.

In addition to electrified vehicle drivetrains and new safety features driving semiconductor content value in vehicles is the demand for improved in-cabin UX. In-cabin UX used to be synonymous with the in-vehicle infotainment (IVI) system, but today UX is defined by much more than IVI; consumers want intuitive, informative, connected and engaging interactions with their vehicle as they have become accustomed to with their portable consumer devices, but they also want enhanced convenience, utility, comfort and customizability of the cabin to their personal preferences, the nature of the journey or even the driver’s mood. Interior lighting, device power delivery, wireless charging, device-to-IVI interfacing, connected car networking and a multitude of utility and comfort functions enabled by small motors (such as electric seats, seat ventilation, air-conditioning vents, etc.) contribute to the wider in-cabin UX, and all require semiconductor-enabled electronics. S&P Global forecasts that the semiconductor content value for in-cabin UX, which includes IVI, connectivity and body and convenience functions, will reach $45 billion in 2028, representing a 10% CAGR from $23 billion in 2021.

indie’s addressable market is not solely dependent on global automotive vehicle volumes, but rather on the increased levels of semiconductor content that are required in vehicles to support the safety and automation systems, enhanced user experiences and electrification applications as introduced above.

Competitive Strengths

indie focuses on delivering leading-edge semiconductor hardware with embedded software solutions. Over the past 10 years, we have built trusted relationships with Tier 1 automotive suppliers. Through focused R&D, leading intellectual property and a curated strategic partner network, we are on multiple Tier 1 Approved Vendor Lists (“AVLs”). Our competitive strengths include the following:

•Positioned in the highest growth areas. Our products serve three types of automotive applications: safety systems, user experience (including connected car) and electrification. According to S&P Global, these key applications are projected to grow at a 13% CAGR, from $54 billion in 2021 to $130 billion by 2028, substantially outpacing the total global semiconductor market, and representing a significant addressable market for indie.

•Differentiated solutions with high barriers to entry. Due to the high degree of regulatory scrutiny and safety requirements in the automotive industry, the semiconductor market is characterized by stringent qualification processes, zero defect quality requirements and functionally safe design architectures. As a result, products must meet high-reliability standards and have extensive design-in timeframes. Further, the automotive environment is harsh, exposing vehicles to fluctuations in temperature and humidity and solutions require specific expertise. Given our extensive industry experience, indie has overcome these high barriers to entry and is well positioned to solve some of the most demanding Autotech design challenges.

•Partner/Customer relationships. We focus on engaging with leading global customers by developing technically differentiated, compelling and sustainable architectures. To win with customers and programs, we bring unique designs that allow major cost savings through higher levels of product integration, reducing the total number of chips needed to support multiple requirements. Toward that end, today indie is approved on multiple Tier 1 AVLs.

•Proven management team. indie’s executive management team brings extensive semiconductor experience, with past successes in delivering leading-edge technologies and creating stockholder value.

Company Strategy

7

We are dedicated to offering our customers a comprehensive portfolio of automotive technology solutions. We focus on designing and delivering the technologies that enable three key automotive dynamics: safety systems, enhanced in-cabin user experience (including connected car) and electrification. Core tenets of our strategy include:

•Enabling diverse, high growth applications. Our system-on-chip solutions are at the epicenter of a diverse set of emerging applications including radar, LiDAR, vision, wireless charging, wired power delivery, interior and exterior lighting, device-to-IVI interfacing, power management and small motor control.

•Delivering on existing wins and extending product reach. Our products currently support multiple Tier 1 automotive supplier platforms. In the medium term, we plan to deliver expanded LiDAR and vision solutions and bring Artificial Intelligence (“AI”) and Machine Learning (“ML”) processor acceleration capabilities into these applications.

•Leveraging our global supply chain. We have built a nimble global network of foundry, test and assembly partners that provide us with the ability to deliver superior supply chain operations. As a fabless semiconductor supplier, this approach has allowed us to maximize scalability while minimizing capital expenditures. To meet demand as the business scales, we are continue to enhance our successful strategic supply chain partnerships.

•Driving margin expansion through innovative designs and development. We intend to expand our margins through the design and development of new, more highly integrated solutions. Our engineering teams develop architectures to improve performance and efficiency while reducing the size and cost of the chip as well as the need for multiple discrete devices.

•Pursuing selective acquisitions. Since the closing of the Transaction, we have completed multiple acquisitions. We continually assess and plan to selectively pursue inorganic opportunities that are complementary to our existing technologies and portfolio of products and/or accelerate our growth initiatives.

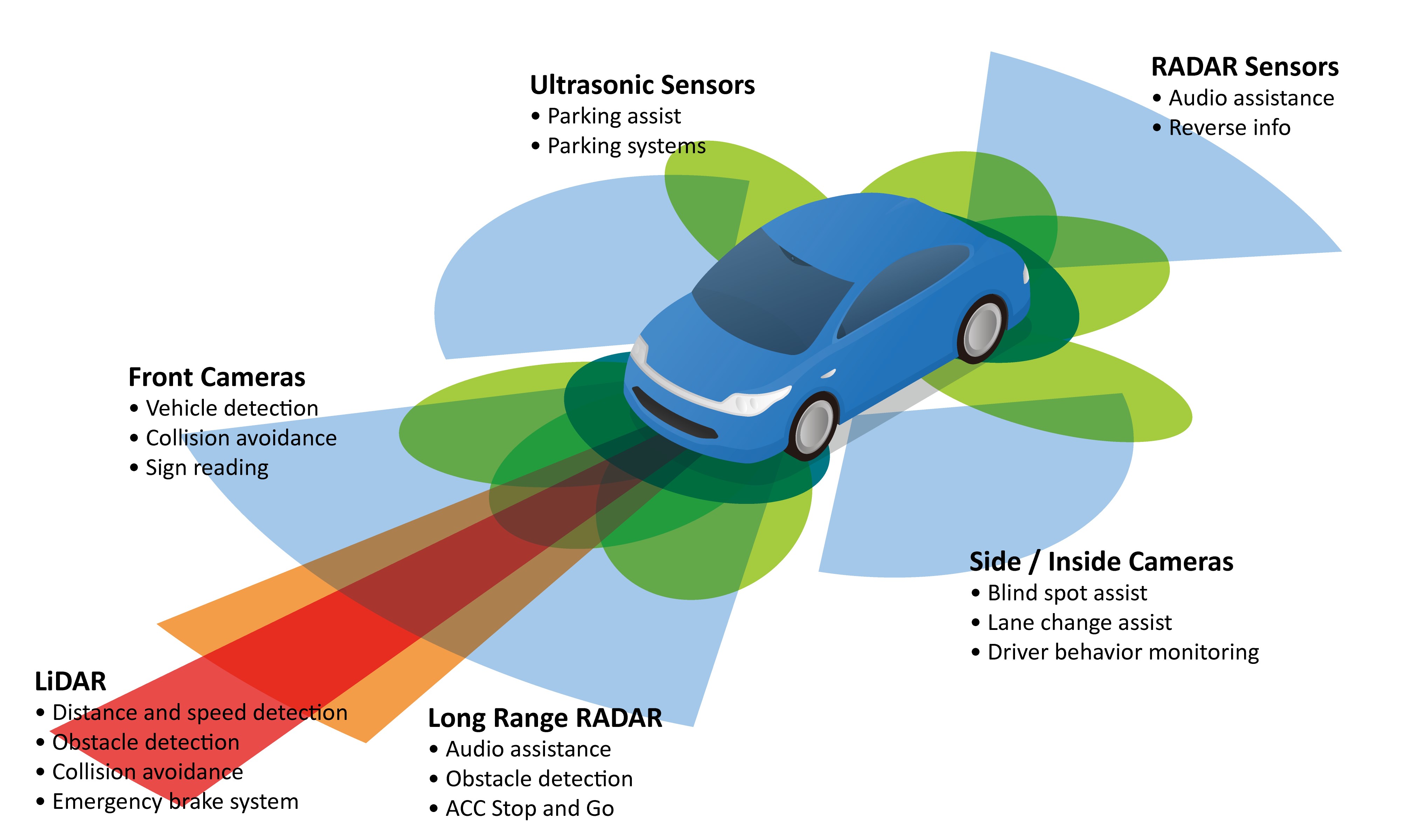

Company Products and Solutions

Our current products include devices for a multitude of automotive applications spanning ultrasound for parking assistance, in-cabin wireless charging and USB power delivery, device interfacing through Apple CarPlay and Android Auto, and LED lighting controllers for interior and exterior applications. Products under development range from FMCW-based LiDAR, radar and vision solutions for ADAS, charging controllers for electric vehicles, smart car access solutions and cybersecurity microcontrollers. Within our ADAS portfolio, we intend to support all key sensor modalities, delivering comprehensive system-level solutions for our customers as depicted below.

8

We have deep design experience and capabilities in core technologies, allowing us to deliver leading-edge Autotech architectures. Our capabilities include, but are not limited to:

•system engineering, optimization and partitioning;

•mixed-signal and RF design;

•analog and power management;

•digital design; and

•Digital Signal Processors (“DSP”) and Arm(R)-based Microcontrollers (“MCU”)

In addition, embedded software is a cornerstone of virtually all of indie’s products. We utilize automotive grade software solutions and Arm 32-bit processors. Through our proprietary design flow, we also enable algorithm development and co-development with hardware.

TeraXion Products and Solutions

TeraXion designs and manufactures innovative photonic components on various technology platforms, including fiber Bragg gratings (“FBG”), low-noise lasers, athermal and tunable packaging, photonic integration and low-noise and high-speed electronics. These components are integrated into solutions for the laser systems, optical sensing and optical communication markets. Importantly, we are integrating TeraXion’s expertise in photonics across our automotive LiDAR offerings.

Manufacturing

Other than specific FBG and semiconductor laser-based products offered by TeraXion, indie continues to utilize a fabless business model, working with a network of third parties to manufacture, assemble and test our products. This approach allows us to focus our engineering and design resources on our core competencies and to control and reduce our fixed costs and capital expenditures.

Wafers, which are the fundamental components of our devices, are manufactured by multiple third-party foundries. Our primary foundry partners are X-FAB, HHGrace, and Global Foundries. We contract with X-FAB for mixed signal and high voltage foundry. HHGrace provides us deeper sub-micron capabilities with embedded Flash Memory.We use Global Foundries as our foundry partner for several process technologies, including advanced nodes. We dual source packaging at ASE, ATX and Hana Semiconductor. We use test services from Sigurd and Terepower. Having several sources and partners provides us with enhanced security of supply.

Manufacturing lead time is 26 weeks. The lead time for wafers is 16 weeks. The backend processing including probe, assembly, and test is about 8 weeks. The finished product is then warehoused and drop-shipped to a specific location. We currently ship products to Greater China (including Hong Kong and Taiwan), the United States, Portugal, Korea, Mexico, and Germany.

In connection with our acquisition of TeraXion in October 2021, we added limited manufacturing capabilities in Quebec City, Canada to assemble and test FBG based products and semiconductor laser-based products.

Sales, Marketing and Customer Support

Our go-to-market strategy provides comprehensive customer coverage. We are partner and standard agnostic, allowing our solutions to be used globally and across multiple platforms and customers. We target innovative Tier 1 automotive suppliers and focus on the semiconductors and software that enable the key systems which underpin the highest growth automotive technology market opportunities.

We often work with customers that have a leading market share in a given application and we deliver unique, tailor-made software and hardware solutions. Given automotive product cycles, we are typically in production with customers for more than seven years with a single design. Through our customer collaboration at the R&D level, our team members are often integrated into a customer’s technology selection and design processes, a key aspect in indie’s winning track record of repeat business.

Since our inception, we have shipped over 200 million devices to customers and our products are powering solutions in over 25 automotive suppliers. By establishing a trusted relationship with the industry’s leading suppliers, indie is well positioned to gain a growing share of new automotive solutions.

9

Revenues for the years ended December 31, 2022 and 2021 include sales to Aptiv, a leading Tier 1 automotive supplier, which represented approximately 37% and 39% of total revenue, respectively. The loss of this customer would have a material impact on our consolidated financial results.

Research and Development Strategy

We have invested a significant amount of time and expense into the design and development of our products and the associated software. Our engineering teams deliver innovative mixed-signal solutions with a focus on meeting our customers’ performance requirements.

As an Autotech company, we believe that our future success depends on our ability to rapidly develop and introduce differentiated products. Our goal is to continually improve both our existing portfolio, while simultaneously introducing new solutions in order to create value for our customers. To outpace market growth, we seek to invest in opportunities that will help extend our product reach, with an emphasis on the industry’s fastest growing segments. Our attention to meeting or exceeding the stringent automotive safety and reliability requirements is fundamental to our research and development process.

To that end, we regularly review our investments to ensure alignment with our growth and profitability goals and make necessary changes in the allocation of resources as needed. In 2022, we spent approximately 109% of our revenues on research and development as we expand product development activities in support of pent-up customer demand.

Our research activities are principally conducted at our headquarters in Aliso Viejo, California and we have design centers and sales offices in Austin, TX; Boston, MA; Detroit, MI; San Francisco and San Jose, CA; Córdoba, Argentina; Budapest, Hungary; Dresden, Frankfurt an der Oder, Munich and Nuremberg, Germany; Edinburgh, Scotland; Rabat, Morocco; Haifa and Tel Aviv, Israel; Quebec City, Canada; Tokyo, Japan; Seoul, South Korea and several locations throughout China.

Process and Packaging Technology

Packaging is becoming increasingly crucial to the performance and reliability of automotive ICs, especially given the challenging operating environment of vehicles. indie’s technology development engineers have long-established expertise in delivering leading-edge capabilities, such as system-in-package (“SiP”) technology. Further, we leverage our packaging capabilities to integrate multiple chips into a single package solution.

Automotive Quality and Safety

We employ wafer and package technologies that meet or exceed the rigorous quality and safety requirements set by industry standards and our customers. Our robust development processes and company guidelines have resulted in indie devices that are capable of exceeding the requirements of AEC Q100 Automotive Grade.

Our dedication to our customers begins with a commitment to design, produce and deliver the highest quality products that meet or exceed the performance levels required for each application. We encourage our customers to frequently visit both our design centers and our manufacturing partners to ensure that the processes and quality meet the standards they have come to expect. We are ISO9001 and ISO26262 certified and intend to pursue further certifications.

Intellectual Property

The core strengths of our business are our intellectual property portfolio and engineering experience, both of which guide product development activities and our approach to patent filings.

Our future success and competitive position depend in part upon our ability to obtain and maintain protection of our proprietary technologies. In general, we have elected to pursue patent protection for aspects of our circuit and device designs that we believe are patentable. We have a number of core technology patents currently in process, including provisions, but we do not rely on any particular patent or patents for our success and have instead relied on our know-how and trade secrets. We also rely on a combination of non-disclosure agreements and other contractual provisions, as well as our employees’ commitment to confidentiality and loyalty, to protect our technology and processes.

The semiconductor industry in general is characterized by frequent claims of infringement and litigation regarding patent and other intellectual property rights. Patent infringement is an ongoing risk, in part because other companies in our industry could

10

have patent rights that may not be identifiable when we initiate development efforts. Litigation may be necessary to enforce our intellectual property rights, and we may have to defend ourselves against infringement claims.

Competition

The market for high-performance analog, digital and mixed-signal semiconductors for automotive applications, is competitive although recent consolidation across the semiconductor industry has reduced the number of viable competitors and created design opportunities for us. Our primary competitors are other automotive-focused semiconductor companies, including Infineon, Monolithic Power Systems, NXP, Renesas and ST Microelectronics.

Some competitors have more financial resources than we do, while others have a more diversified set of products and end markets. Accordingly, such competitors may be able to respond more quickly to customer requests and market developments, and to better withstand external economic or market factors.

However, we believe that our technical and design experience, our existing approved vendor list position across multiple Tier 1 automotive suppliers, and a growing demand for software-embedded solutions with proprietary manufacturing and packaging capabilities, position us to outpace our addressable market.

Corporate Responsibility and Sustainability

We believe responsible and sustainable business practices support our long-term success. As a company, we are committed to protecting and supporting our people, our environment, and our communities. This commitment is reflected through our day-to-day activities, including the adoption of socially responsible policies and procedures, our focus on fostering an inclusive workplace, our constant drive toward more efficient use of materials and energy, our careful management of our supply chain, our products which help enhance road safety, and our ethics and compliance program.

•We seek to protect the human rights and civil liberties of our employees through policies, procedures, and programs that avoid risks of compulsory and child labor, both within our company and throughout our supply chain.

•We foster a workplace of dignity, respect, diversity, and inclusion through our recruiting and advancement practices, internal communications, and employee resource groups.

•We educate our employees annually on relevant ethics and compliance topics, publish accessible guidance on ethical issues and related company resources in our global Code of Business Conduct and Ethics, and encourage reporting of ethical concerns through any of several global and local reporting channels.

•We innovate to reduce the energy used by our products, the energy used to manufacture them, and the amount of new materials required to manufacture them.

Employees

As of December 31, 2022, we had over 600 employees. None of our employees or contract workers are represented by a labor union.

Information about Our Executive Officers

Our executive officers are as follows:

| Name | Age | Position | ||||||||||||

| Donald McClymont | 54 | Chief Executive Officer and Director | ||||||||||||

| Ichiro Aoki | 58 | President and Director | ||||||||||||

| Thomas Schiller | 52 | Chief Financial Officer and EVP of Strategy | ||||||||||||

| Kanwardev Raja Singh Bal | 47 | Chief Accounting Officer | ||||||||||||

| Steven Machuga | 58 | Chief Operating Officer | ||||||||||||

Donald McClymont serves as indie’s Chief Executive Officer and is responsible for formulating its strategic vision, ensuring the execution of business plans and creating shareholder value. Mr. McClymont also serves on indie’s Board of Directors. Prior to co-founding indie in 2007, he was Vice President of Marketing at Axiom Microdevices, tasked with driving company strategy, developing sales engagements and building key industry partnerships. Prior to Axiom, he was a Product Line Director

11

at Skyworks Solutions and Conexant, and a Marketing Manager at Fujitsu. Previously, he was with Thesys (now X-FAB Melexis), and Wolfson (now Cirrus Logic), as a design engineer. Mr. McClymont holds five patents worldwide and earned a Master in Engineering Electronics and Electrical from the University of Glasgow.

Ichiro Aoki serves as indie’s President and as a member of the Board of Directors. He works closely with indie’s executive team and Board to create, update and manage execution of indie’s strategies and technical roadmaps. Prior to co-founding indie in 2007, Dr. Aoki was a co-founder, Board Member and Chief Architect of Axiom Microdevices, which was subsequently sold to Skyworks Solutions. Previously, Dr. Aoki founded and served as co-CEO of PST Eletronica Ltd. in Brazil, which was later sold to Stoneridge, Inc. Dr. Aoki has developed 35 patents worldwide and has authored numerous IEEE papers, two of them having over 400 citations. He is fluent in Japanese, Portuguese and English. Dr. Aoki holds a Ph.D. and Masters in Electrical Engineering from the California Institute of Technology and a Bachelor of Science in Electrical Engineering from the University of Campinas, Sao Paulo, Brazil. He serves as a California Institute of Technology Electrical Engineering Advisory Council Member and is also a Scientific Advisory Board Member with the California Institute of Technology Space-based Solar Power Project.

Thomas Schiller serves as indie’s Chief Financial Officer and Executive Vice President of Strategy. In this role, he leads all corporate financing, reporting, investor relations, treasury, tax, as well as merger and acquisition activities. Prior to joining indie in October 2019, Mr. Schiller was Vice President of Marketing at Marvell Semiconductor, from February to October 2019. From July 2002 to February 2019, he was Vice President of Strategy and Corporate Development at Skyworks Solutions. He earned a Masters of Business Administration from the University of Southern California with specialization in Entrepreneurship and Finance, and holds a Bachelor of Arts in Social Sciences with emphasis in Economics and Political Science from the University of California, Irvine. In addition, Mr. Schiller has completed executive education programs at the University of California, Los Angeles and at Suffolk University, Boston.

Kanwardev Raja Singh Bal, serves as indie's Chief Accounting Officer. In this role, Mr. Bal leads indie’s accounting and finance operations, and works closely with the Chief Financial Officer to oversee financial reporting, tax, global treasury and internal control activities. From January 2020 to December 2022, Mr. Bal served as Senior Vice President - Finance and Controller of indie. Prior to joining indie in January 2020, Mr. Bal served as Operating Partner and Chief Financial Officer for True North Venture Partners and its wholly-owned portfolio companies from October 2017 and December 2019 and as Vice President and Chief Financial Officer for GT Advanced Technologies from January 2014 and October 2017. Previously, Mr. Bal served as Corporate Controller and Treasurer for Skyworks Solutions, where he held finance roles with increasing responsibility. He also has held finance positions with Lucent Technologies and Ernst & Young. Mr. Bal holds a CPA accounting designation, a Master of Management Analytics from Queen’s University’s Smith School of Business, and a Bachelor of Commerce degree from the University of Ottawa's Telfer School of Management.

Steven Machuga, serves as indie’s Chief Operating Officer. He has over 30 years of experience in electronics and semiconductor development and high-volume operations management of the entire supply chain. Prior to joining indie in March 2021, he was Vice President, Worldwide Operations at Skyworks Solutions since 2016. Prior to that, he was Vice President, External Manufacturing Operations & Engineering at Skyworks from 2006. He holds a Masters in Chemical Engineering and Materials Science from the University of Minnesota and a Bachelor of Science in Chemical Engineering, from the University of Connecticut. He holds six U.S. patents and three European patents.

Our executive officers are appointed annually by and serve at the discretion of the Board of Directors.

Available Information

Our primary Internet address is www.indiesemi.com. We make our U.S. Securities and Exchange Commission (“SEC”) periodic reports (Forms 10-Q and Forms 10-K) and current reports (Forms 8-K) available free of charge through our website as soon as reasonably practicable after they are filed electronically with the SEC. Within the Investor Relations section of our website, we provide information concerning corporate governance, including our Audit and Compensation Committee charters, Nominating and Corporate Governance information, Board committee composition and chairs, Code of Ethics for Principal Financial Officers, and other information. The content of our website is not incorporated by reference into this Annual Report on Form 10-K or into any other report or document we file with the SEC, and any references to our websites are intended to be inactive textual references only.

The SEC also maintains an Internet website at http://www.sec.gov that contains reports, proxy and information statements, and other information that we file electronically with the SEC.

12

ITEM 1A. RISK FACTORS

In evaluating our company and our business, you should carefully consider the risks and uncertainties described below, together with the other information in this Annual Report on Form 10-K, including our consolidated financial statements and the related notes and the section titled “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” The occurrence of one or more of the events or circumstances described in these risk factors, alone or in combination with other events or circumstances, may have a material adverse effect on our business, reputation, revenue, financial condition, results of operations or future prospects, in which case the market price of our common stock could decline, and you could lose part or all of your investment. Unless otherwise indicated, reference in this section and elsewhere in this Annual Report on Form 10-K to our business being adversely affected, negatively impacted or harmed will include an adverse effect on, or a negative impact or harm to, our business, reputation, financial condition, results of operations, revenue or our future prospects. The risks and uncertainties described below are not intended to be exhaustive and are not the only ones we face. Additional risks and uncertainties not presently known to us or that we currently deem immaterial may also impair our business. This Annual Report on Form 10-K also contains forward-looking statements that involve risks and uncertainties. Our actual results could differ materially from those anticipated in the forward-looking statements as a result of a number of factors, including the risks described below. See the section titled “Cautionary Statement Regarding Forward-Looking Statements.”

Summary of Risks

An investment in shares of our Class A common stock and warrants involves substantial risks and uncertainties that may adversely affect the value of your investment. Some of the more significant challenges and risks relating to an investment in our company include, among other things, the following:

Risks Related to Our Operations and Industry

•The cyclical nature of the semiconductor industry may limit our net sales and profitability.

•If we fail to compete effectively in the highly competitive semiconductor industry, our business could be adversely affected.

•Declining average selling prices and price erosion may adversely impact our revenue and profitability.

•Failure to win competitive bid selection processes could adversely affect our business.

•Decline in demand for our customers’ end products could adversely impact our revenue and profitability.

•Any downturn in the automotive market could significantly harm our financial results.

•We depend on third parties to manufacture, assemble, test and/or package our products,

•We rely on the timely supply of materials that may only be available from a limited number of suppliers.

•We must develop new products with acceptable profit margins.

•“Strategic backlog” and “design win pipeline” estimations may not result in revenue or profits.

•Mergers, acquisitions, investments and joint ventures could adversely affect our results of operations.

•Future growth could strain our resources, management, information and telecommunication systems and operating and financial controls.

•We may seek additional capital, which may result in dilution to our stockholders.

•We may rely on strategic partnerships, joint ventures and alliances, which may fail for reasons outside of our control.

•We may not be successful in exiting certain programs or businesses or in restructuring our operations, which could adversely impact our business.

•Disruptions in our relationships with any one of our key customers could adversely affect our business.

•We have historically incurred losses and may continue to incur losses.

Risks Related to Our Indebtedness

•Our existing and future indebtedness could adversely affect our ability to operate our business.

•We may not have sufficient funds to repay the indebtedness and repurchase the 2027 Notes or make cash payments upon conversions thereof.

•Provisions in the 2027 Indenture for the 2027 Notes may deter or prevent a business combination that stockholders may consider favorable.

•The accounting method for reflecting the 2027 Notes may adversely affect our reported earnings and financial condition.

•The conditional conversion feature of the 2027 Notes, if triggered, may adversely affect our financial condition and operating results.

13

Risks Related to Our Organizational Structure

•We are dependent upon distributions made by our subsidiaries to make certain payments, and such distributions may be delayed or restricted for reasons outside of our control.

•We are party to a Tax Receivable Agreement, which requires us to make certain payments, and such payment may exceed our actual tax benefits or may be accelerated.

Risks Related to Macroeconomic Conditions

•Geopolitical uncertainty could impact end customer demand and disrupt our supply chain.

•Downturns or volatility in general economic conditions could harm our business.

•Fluctuations in foreign exchange rates could have an adverse effect on our results of operations.

•Our worldwide operations are subject to political, economic and health risks and natural disasters, which could have a material adverse effect on our business operations.

Risks Related to our Intellectual Property, Technology and Cybersecurity.

•Improper use of our intellectual property could have a material adverse effect on our business, financial condition and results of operations.

•Intellectual property claims or litigation could significantly harm our business.

•We license certain third-party software that may not be available to us in the future which may delay product development and production or cause us to incur additional expense.

•Interruptions in information technology systems could adversely affect our business.

•Security breaches and other cybersecurity incidents could adversely impact our business.

Risks Related to Regulatory Compliance and Legal Matters

•If we or our customers fail to comply with a large body of laws and regulations, our business and reputation could be adversely affected.

•We may be adversely affected by product defects and product liability or warranty claims.

•Significant litigation and stockholder activism could impair our reputation and adversely affect our business.

•We are subject to export restrictions and laws affecting trade and investments which could materially and adversely affect our business and results of operations.

•Changes in tax rates or laws or additional tax liabilities could adversely affect our business.

•Failure to comply with anti-corruption laws or our ethics policies could adversely affect our business.

Risks Related to Doing Business in China

•Uncertainties with respect to the PRC legal system could adversely affect our China business.

•China’s economic, political and social conditions may change rapidly with little advance notice, which could adversely affect our business.

•Our China subsidiary may be limited in its ability to make distributions to us.

•Government control of currency conversion may affect the value of our securities.

•Failure to comply with certain regulations may subject us or our PRC employees to fines or sanctions.

•Failure to comply with PRC laws and other obligations regarding data protection could have a material adverse effect on our business.

Risks Related to Financial Reporting, Internal Controls and Being a Public Company

•We may not be able to timely and effectively implement and maintain controls and procedures required by Section 404 of the Sarbanes-Oxley Act that is applicable to us, which could result in materially misstated financial reporting.

•Increased expenses and administrative burdens as a public company could have a material adverse effect on our business.

•Use of exemptions available to emerging growth companies could make our securities less attractive to investors and may make it difficult to compare our performance to that of other public companies.

Risks Related to Ownership of Our Class A Common Stock and Warrants, and Organizational Documents

•We must comply with the continued listing standards of Nasdaq for our Class A common stock.

•We may redeem unexpired warrants prior to their exercise at a time that is disadvantageous to the holder, thereby making such warrants worthless.

•Our warrants may have an adverse effect on the market price of our Class A common stock.

14

•An investment in our Class A common stock may be diluted by future issuances of our Class A common stock or ADK LLC units.

•There may be sales of a substantial amount of Class A common stock by our stockholders, which could cause the price of our securities to fall.

•Provisions in our Certificate of Incorporation and Bylaws limit the ability of stockholders to take certain actions and could delay or discourage takeover attempts.

•Our Certificate of Incorporation designates the Court of Chancery of the State of Delaware as the sole and exclusive forum for certain types of actions and proceedings, which could limit our stockholders’ ability to obtain a favorable judicial forum.

Please see below for a discussion of these and other factors you should consider before making an investment in our securities.

Risks Related to Our Operations and Industry

The cyclical nature of the semiconductor industry may limit our ability to maintain or improve our net sales and profitability.

The semiconductor industry is highly cyclical and is prone to significant downturns from time to time. Cyclical downturns can result in substantial declines in semiconductor demand, production overcapacity, high inventory levels and accelerated erosion of average selling prices. Such downturns result from a variety of market forces including constant and rapid technological change, quick product obsolescence, price erosion, evolving standards, short product life cycles and wide fluctuations in product supply and demand.

For example, commencing in 2020, a variety of factors including the COVID-19 pandemic, ongoing trade disputes between the United States and China, geopolitical factors, such as Russia’s invasion of Ukraine, weakness in demand and pricing for semiconductors across applications, and excess inventory have resulted in downturns in the semiconductor industry. During the second half of fiscal year 2020, customer manufacturing facilities re-opened and demand has returned to normal and continued to grow. While the Company does not anticipate significant adverse effects on its operations in the near- or mid-term, the future effects of COVID-19 are difficult to predict, due to uncertainty about different variants that may evolve, the actions that may be taken to contain or treat future impact, and how quickly and to what extent normal economic and operating conditions resume.

Conversely, significant upturns could cause us to be unable to satisfy demand in a timely and cost-efficient manner, and could result in increased competition for access to third-party foundry, assembly and testing capacity. In the event of such an upturn, we may not be able to expand our workforce and operations in a sufficiently timely manner, procure adequate resources and raw materials, or locate suitable suppliers or other subcontractors to respond effectively to changes in demand for our existing products or to the demand for new products. Accordingly, our business, financial condition and results of operations could be materially and adversely affected.

The semiconductor industry is highly competitive. If we fail to introduce new technologies and products in a timely manner, it could adversely affect business.

The semiconductor industry is highly competitive and characterized by constant and rapid technological change, short product lifecycles, significant price erosion, and evolving standards for quality. Accordingly, the success of our business depends, to a large extent, on our ability to meet evolving industry requirements, introduce new products and technologies designed to satisfy those evolving requirements, and see our products and technologies accepted in the marketplace, both in a timely manner and at prices that are acceptable to customers.

Moreover, the costs related to the research and development necessary to develop new technologies and products are significant and some of our competitors may have greater resources than us. If they significantly increase the resources that they devote to developing and marketing their products, we may not be able to compete effectively. Our competitors’ products, services and technologies may be less costly or may offer superior functionality or better features than ours, which may result in lower than expected selling prices for our products. Additionally, some of our competitors operate and maintain their own fabrication facilities, have longer operating histories, larger customer bases, more comprehensive intellectual property portfolios and greater financial resources.

Further, the semiconductor industry has experienced, and may continue to experience, significant consolidation among companies and vertical integration among customers. Larger competitors resulting from consolidations may have certain advantages over us, including, but not limited to: more efficient cost structures; substantially greater financial and other resources with which to withstand adverse economic or market conditions and pursue development, engineering, manufacturing, marketing and distribution of their products; longer independent operating histories; presence in key markets; intellectual property protection; large purchase quantities; and greater name recognition. In addition, we may be at a

15

competitive disadvantage to our peers if we fail to identify or are unable to finance attractive opportunities to acquire companies to expand our business. Consolidation among our competitors and integration among our customers could erode our market share, negatively impact our capacity to compete and require us to restructure our operations, any of which would have a material adverse effect on our business.

As a result of these competitive pressures, we may face declining sales volumes or lower prices for our products, and may not be able to reduce total costs in line with declining revenue. If any of these risks materialize, they could have a material adverse effect on our business, financial condition and results of operations.

The average selling prices of products in our markets have historically decreased over time and could do so in the future, which could adversely impact our revenue and profitability.

Average selling prices of semiconductor products in the markets we serve have historically decreased over time. Profit margins and financial results may suffer if we are unable to offset any reductions in average selling prices by reducing costs, developing new or enhanced products on a timely basis with higher selling prices or profit margins, or increasing sales volumes. Although in some cases, we have contractual agreements with customers, there is no assurance that those price agreements will be honored. As a result, our average selling prices may decline faster than forecasted. Additionally, increases in the industry semiconductor manufacturing capacity could lead to declines in average selling prices and a decrease in short-term or long-term demand, resulting in industry oversupply, could materially adversely affect our business, results of operations, or financial condition.

Much of our business depends on winning competitive bid selection processes, and the failure to be selected could adversely affect business in those market segments.

The competitive selection processes often require an investment of significant time and capital resources, with no guarantee of winning the contract and generating revenue. In the automotive semiconductor market in which we compete, due to the longer design cycles involved, failure to win a design-in could prevent access to a customer for several years. Our failure to win a significant number of these bids could result in reduced revenues, and hurt our competitive position for future selection processes, which could have a material adverse effect on our business, financial condition and results of operations.

The demand for our products depends on the demand for our customers’ end products.

The vast majority of our revenue is derived from sales to manufacturers in the automotive industry. Demand in this market fluctuates significantly, driven by consumer spending, consumer preferences, the development of new technologies and prevailing economic conditions. In addition, the end products in which our semiconductors are incorporated may not be successful, or may experience price erosion or other competitive factors that could affect the price manufacturers are willing to pay. Such customers have in the past, and may in the future, vary order levels significantly from period to period, request postponements of scheduled delivery dates, modify their orders or reduce lead times. This is particularly common during periods of low demand. This can make managing business difficult, as it limits the predictability of future revenue. It can also affect the accuracy of our financial forecasts.

Furthermore, because we do not manufacture the semiconductors used for our products, we are dependent on third parties to manufacture and assemble our products. Our manufacturing lead times require us to make estimates of customers’ future demand. If our estimates of customer demand are ultimately inaccurate, these conditions could lead to a significant mismatch between supply and demand. This mismatch may result in both product shortages and excess inventory and could significantly harm our financial results. In periods of shortages impacting the semiconductor industry or limited supply or capacity in our supply chain, as we have experienced in the past, the lead time on our orders for certain supply could become extended, heightening these risks.

Furthermore, developing industry trends, including customers’ use of outsourcing and new and revised supply chain models, may affect our revenue, costs and working capital requirements.

Our sales are made primarily to Tier 1 suppliers. Any downturn in the automotive market could significantly harm our financial results.

This automotive concentration of sales exposes us to the risks associated with the automotive market. For example, our anticipated future growth is highly dependent on the adoption of ADAS, user interface, connectivity and electrification technologies, which are expected to have increased sensor and power product content. A downturn in the automotive market could delay automakers’ plans to introduce new vehicles with these features, which would negatively impact the demand for products and our ability to grow our business.

16

The automotive industry continues to undergo consolidation and reorganization and, in some cases, suppliers to the automotive industry have entered bankruptcy. Consolidation or closures of automobile dealers could reduce the aggregate demand for our services in the future and limit the amounts we earn from our products. Such changes in the automotive market could have a material adverse effect on our business, financial condition and results of operations.

We depend on third parties and their technology to manufacture, assemble, test and/or package our products, which exposes us to risks.

The manufacture of our products, including the fabrication of semiconductor wafers, and the assembly and testing of our products, involve highly complex processes. For example, minute levels of contaminants in the manufacturing environment, difficulties in the wafer fabrication process or other factors can cause a substantial portion of the components on a wafer to be nonfunctional. These problems may be difficult to detect at an early stage of the manufacturing process and often are time-consuming and expensive to correct.

From time to time, we have experienced problems achieving acceptable yields at our third-party wafer fabrication partners, resulting in delays in the availability of components. Moreover, an increase in the rejection rate of products during the quality control process before, during or after manufacture and/or shipping of such products, results in lower yields and margins.

In addition, changes in manufacturing processes required as a result of changes in product specifications, changing customer needs and the introduction of new product lines have the potential to significantly reduce manufacturing yields, resulting in low or negative margins on those products. Poor manufacturing yields over a prolonged period of time could adversely affect our ability to deliver products on a timely basis and harm relationships with our customers, which could materially and adversely affect our business, financial condition and results of operations.

We rely on the timely supply of materials and our business could be adversely affected if suppliers fail to meet their delivery obligations or raise prices. Certain materials needed in our manufacturing operations are only available from a limited number of suppliers.

We have a fabless business model, which outsources our manufacturing operations to third-party foundries. The manufacturing operations depend on deliveries of materials in a timely manner and, in some cases, on a just-in-time basis. From time to time, suppliers may extend lead times, limit the amounts supplied or increase prices due to capacity constraints or other factors. Supply disruptions may also occur due to shortages in critical materials or components. Because our products are complex, it is frequently difficult or impossible to substitute one type of material with another. A failure by suppliers to deliver requirements could result in disruptions to our third-party manufacturing operations. Our business, financial condition and results of operations could be harmed if we are unable to obtain adequate supplies of materials in a timely manner or if there are significant increases in the costs of materials.

The semiconductor industry is characterized by continued price erosion, especially after a product has been on the market for a period of time, and we may be unsuccessful in advancing our product technologies, improving efficiencies or developing and selling new products with product margins similar or better than what we have experienced in the past.

One of the results of the rapid innovation in the semiconductor industry is that pricing pressure, especially on products containing older technology, can be intense. Product life cycles are relatively short, and as a result, products tend to be replaced by more technologically advanced substitutes on a regular basis. In turn, demand for older technology falls, causing the price at which such products can be sold to drop, in some cases precipitously.

In order to continue profitably supplying these products, continuous development of new technology, processes and product innovations is necessary. If we cannot advance our process technologies or improve our efficiencies to a degree sufficient to maintain required margins, we will no longer be able to make a profit from the sale of these products. Moreover, we may not be able to cease production of such products, either due to contractual obligations or for customer relationship reasons, and as a result we may be required to bear a loss on such products. We cannot guarantee that competition in our core product markets will not lead to price erosion, lower revenue or lower margins in the future. Should reductions in our manufacturing costs fail to keep pace with reductions in market prices for the products we sell, this could have a material adverse effect on our business, financial condition and results of operations. Further, we have invested and will continue to invest significant resources in our product and technology development efforts. Our development efforts carry inherent risk due to the challenges of foreseeing changes or developments in technology, predicting changes in customer requirements or preferences or anticipating the adoption of new industry standards, and we may be unable to meet our customers’ requirements or gain market acceptance. Should we fail to develop and introduce sufficiently unique products with profit margins similar to or better than what we have experienced in the past or should our product development fail to keep pace with the changing needs of our customers and industry, our business, financial condition and results of operations could be materially and adversely affected.

17

Our strategic backlog and design win pipeline are subject to unexpected adjustments and cancellations and may not be a reliable indicator of future revenues or earnings.

There can be no assurance that the revenues projected in our strategic backlog or design win pipeline will be realized or, if realized, will result in profits. Our strategic backlog estimates represent the revenue we expect to recognize from product orders within the next ten years. The estimate of our strategic backlog requires substantial judgment and is based on a number of assumptions, including management’s current assessment of customer and third-party contracts that exist as of the date the estimate is made, as well as revenues from expected contract renewals and/or expected design wins, to the extent that we believe that recognition of the related revenue will be realizable within the next ten years. Although we believe the assumptions underlying our strategic backlog estimate are reasonable, they are not guarantees and we can give no assurance that we will recognize the revenues reflected in the strategic backlog estimate. A number of factors could result in actual revenues being less than the amounts reflected in strategic backlog. Our customers or third-party partners may attempt to renegotiate or terminate their contracts for a number of reasons, including competitor offerings, mergers, changes in their financial condition, or general changes in economic conditions within their industries or geographic locations, we may experience delays in the development or delivery of products or services specified in customer contracts, or we may be unable to win competitive bid selection processes or achieve additional design wins on the timeline currently anticipated or at all. Because of the possibility of contract cancellations or changes in scope and schedule, we cannot predict with certainty when or if backlog will be realized. In addition, even where a contract proceeds as scheduled, it is possible that contracted parties may default and fail to pay amounts owed to us or poor contract performance could increase the cost associated with a contract. Delays, suspensions, cancellations, payment defaults, scope changes and poor contract execution could materially reduce or eliminate the revenues and profits that we actually realize from our strategic backlog. Accordingly, there can be no assurance that contracts, renewals or expected design wins included in strategic backlog will actually generate the predicted revenues or profits.

We may pursue mergers, acquisitions, investments and joint ventures, which could adversely affect our results of operations.

Our growth strategy includes acquiring or investing in businesses that offer complementary products, services and technologies, or enhance our market coverage or technological capabilities. Any acquisitions or investments we undertake involve risks and uncertainties, including but not limited to:

•Difficulties integrating the operations, employees, technologies or products of acquired companies or working with third parties with which we may partner on joint development or collaboration relationships;

•Inaccuracies in our estimates and assumptions used to assess a transaction may result in us not realizing the expected financial or strategic benefits of any such transaction;

•Disruption of our ongoing business and diversion of our management’s attention;

•Our inability to retain key personnel of acquired businesses;

•Claims or liabilities that we assume from an acquired company or technology or that are otherwise related to an acquisition;

•Dilution of the ownership of our existing stockholders in connection with any equity or debt securities issued in connection with financing any such transaction; and

•U.S. and foreign regulatory approvals required in connection with an acquisition or investment may take longer than anticipated to obtain, may not be forthcoming or may contain burdensome conditions, which may jeopardize, delay or reduce the anticipated benefits to us of the transaction.

The occurrence of any of these risks could have a material adverse effect on our business, operating results or financial condition.

If we do not effectively manage future growth, our resources, systems and controls may be strained, and our results of operations may suffer.