online store, the greater our own revenue, growth, and profitability. We believe this alignment of interests with our clients is a core tenant to our sustainable, long-term success. This is evidenced by our net revenue retention rate, which has been 105% in 2020 and 2021 and consistently over 100% in the preceding years. These retention rates demonstrate both the strong retention we achieve from our existing brands and their strong growth in GMV by using the Nogin platform.

Since launching our platform in 2013, our business has experienced rapid growth. Our revenues were $41.0 million, $45.5 million and $101.3 million in the years ended December 31, 2019, 2020 and 2021, respectively, representing increases of 11% and 123%, respectively. We were breakeven in 2019 and our net losses were $1.1 million and $0.1 million in the years ended December 31, 2020 and December 31, 2021, respectively, representing an increase of 94% from 2020 to 2021. Our GMV amounted to $182.5 million, $280.2 million and $277.6 million in 2019, 2020 and 2021, respectively, representing an increase of 54% from 2019 to 2020, and a decrease of 1% from 2020 to 2021. In 2021, we began acquiring inventory to assist our clients supply chain issues through the pandemic. As such, we had product revenue in 2021 that we do not anticipate continuing after 2022.

Our revenues were $11.9 million and $25.2 million in the three months ended March 31, 2021 and 2022, respectively, representing an increase of 111%. Net losses were $1.5 million and $9.9 million in the three months ended March 31, 2021 and 2022, respectively, representing an increase in net losses of 565%. Our GMV amounted to $61.9 million and $54.8 million for the three months ended March 31, 2021 and 2022, respectively, representing a decrease of 11.5%.

Key Trends in

E-Commerce

Accelerating shift towards

e-commerce

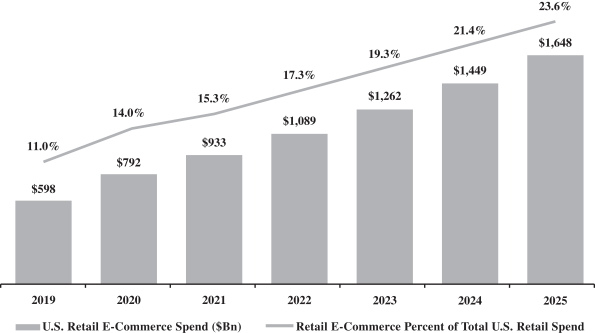

with online sales growth higher than traditional retail sales In 2021, US consumers are expected to spend $933.0 billion on

e-commerce,

representing 15.3% of total retail sales, and by 2025, US consumers are projected to spend $1.64 trillion on e-commerce

representing 23.6% 137