UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM

(Mark One)

THE SECURITIES EXCHANGE ACT OF 1934

OR

THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended

OR

THE SECURITIES EXCHANGE ACT OF 1934

OR

THE SECURITIES EXCHANGE ACT OF 1934

Date of event requiring this shell company report ________

For the transition period from ________ to ________

Commission file number

(Exact name of Registrant as specified in its charter)

Not Applicable

(Translation of Registrant’s name into English)

(Jurisdiction of incorporation or organization)

Yue Xing Sixth Road, Nanshan District,

People’s Republic of

(Address of principal executive offices)

kang@mcvrar.com

Tel:

Yue Xing Sixth Road, Nanshan District,

People’s Republic of

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading symbol(s) | Name of each exchange on which registered | ||

| (1) | The Stock Market LLC | |||

| The Stock Market LLC |

| (1) | ||

| (2) |

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act.

None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report: As of December 31, 2023, there were ordinary shares issued and outstanding, par value US$0.001 per share (retroactively adjusted to reflect the 10-to-1 Share Consolidation effected on February 2, 2024).

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ☐ Yes ☒

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Sectiokn 13 or 15(d) of the Securities Exchange Act of 1934. ☐ Yes ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ☒

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). ☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |

| ☒ | Emerging growth company |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act.

| † | The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012. |

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| International Financial Reporting Standards as issued by the International Accounting Standards Board ☐ | Other ☐ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement Item the registrant has elected to follow. ☐ Item 17 ☐ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ☐ Yes ☒

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING

THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. ☐ Yes ☐ No

TABLE OF CONTENTS

i

INTRODUCTION

Except where the context otherwise requires and for purposes of this annual report only:

| ● | unless otherwise noted, all references to years are to the calendar years from January 1 to December 31 and references to our fiscal year or years are to the fiscal year or years ended December 31. |

| ● | “CAC” refers to the Cyberspace Administration of China. |

| ● | “China” or the “PRC”, in each case, refers to the People’s Republic of China, including Hong Kong, Macau and Taiwan. The term “Chinese” has a correlative meaning for the purpose of this annual report. When used in the case of laws and regulations, of “China” or “the PRC”, it refers to only such laws and regulations of mainland China. |

| ● | “Company” refers to MicroCloud Hologram Inc. (f/k/a Golden Path Acquisition Corporation), a Cayman Islands exempted company. |

| ● | “CSRC” refers to the China Securities Regulatory Commission. |

| ● | “EIT” refers to enterprise income tax. |

| ● | “PRC law(s) and regulation(s)” refers to the laws and regulations of mainland China. |

| ● | “MIIT” refers to the Ministry of Industry and Information Technology of China. |

| ● | “GAAP” refers to the generally accepted accounting principles in the United States; |

| ● | “SAFE” are to the State Administration for Foreign Exchange; |

| ● | “MOFCOM” are to the Ministry of Commerce of the People’s Republic of China; |

| ● | “RMB”refer to the legal currency of mainland China. |

| ● | “US$” and “U.S. dollars” refer to the legal currency of the United States. |

| ● | “U.S. GAAP” refers to generally accepted accounting principles in the United States. |

| ● | “HOLO”, “MicroCloud”,“we”, “us”, “our company”, “the company”, “our”, or similar terms used in this annual report refer to MicroCloud Hologram Inc., a Cayman Islands exempted company, including its wholly-owned and majority-owned subsidiaries and, in the context of describing our operations and consolidated financial information. |

This annual report includes our audited consolidated financial statements for the years ended December 31, 2021, 2022 and 2023, and the related notes. Our ordinary shares and warrants are listed on the Nasdaq Stock Market LLC (the “Nasdaq”) under the symbols “HOLO” and “HOLOW,” respectively

Our reporting currency is the Renminbi. This annual report on Form 20-F also contains translations of certain foreign currency amounts into U.S. dollars for the convenience of the reader. Unless otherwise stated, all translations from Renminbi to U.S. dollars were made at the rate of RMB 1.00 to USD 0.1412, representing the mid-point reference rate set by People’s Bank of China on December 29, 2023, the last business day for the year ended December 31, 2023. We make no representation that the Renminbi or U.S. dollar amounts referred to in this annual report could have been or could be converted into U.S. dollars or Renminbi, as the case may be, at any particular rate or at all. The PRC government imposes control over its foreign currency reserves in part through direct regulation of the conversion of Renminbi into foreign exchange and through restrictions on foreign trade.

ii

FORWARD-LOOKING STATEMENTS

This annual report on Form 20-F contains forward-looking statements that are based on our current expectations, assumptions, estimates and projections about us and our industry. All statements other than statements of historical facts in this annual report are forward-looking statements. In some cases, these forward-looking statements can be identified by words and phrases such as “may,” “should,” “intend,” “predict,” “potential,” “continue,” “will,” “expect,” “anticipate,” “estimate,” “plan,” “believe,” “is /are likely to” or the negative form of these words and phrases or other comparable expressions. The forward-looking statements included in this annual report relate to, among others:

| ● | our goals and strategies; |

| ● | our future prospects and market acceptance of our products and services; |

| ● | our future business development, financial condition and results of operations; |

| ● | expected changes in our revenue, costs or expenditures; |

| ● | anticipated cash needs and its needs for additional financing; |

| ● | growth of and competition trends in our industry; |

| ● | our ability to successfully integrate acquisitions; |

| ● | our expectations regarding demand for, and market acceptance of, our products; |

| ● | expectations with respect to the success of our research and development efforts; |

| ● | expectations regarding our growth rates, growth plans and strategies; |

| ● | general economic and business conditions in the markets in which we operate; |

| ● | relevant government policies and regulations relating to our business and industry; |

| ● | PRC laws, regulations and policies, including those applicable ; |

| ● | competition landscape in China’s holographic digitalization technology service industry; |

| ● | assumptions underlying or related to any of the foregoing. |

These forward-looking statements involve various risks, assumptions and uncertainties. Although we believe that our expectations expressed in these forward-looking statements are reasonable, our expectations may turn out to be incorrect. Our actual results could be materially different from our expectations.

The forward-looking statements made in this annual report relate only to events or information as of the date on which the statements are made in this annual report. All forward-looking statements included herein attributable to us or other parties or any person acting on our behalf are expressly qualified in their entirety by the cautionary statements contained or referred to in this section and under the heading “Risk Factors” below. Except to the extent required by applicable laws and regulations, we undertake no obligation to update any forward-looking statements to reflect events or circumstances after the date on which the statements are made or to reflect the occurrence of unanticipated events.

iii

PART I

| ITEM 1. | IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS |

Not applicable.

| ITEM 2. | OFFER STATISTICS AND EXPECTED TIMETABLE |

Not applicable.

| ITEM 3. | KEY INFORMATION |

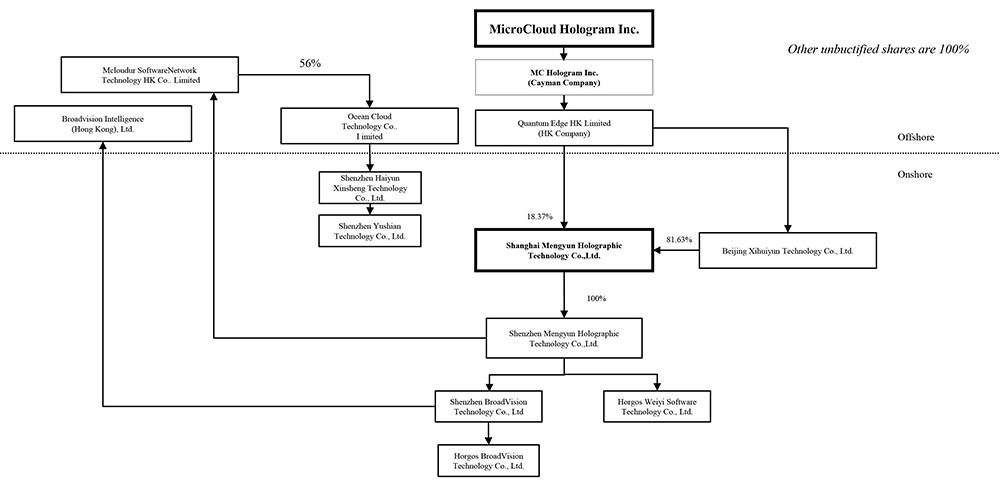

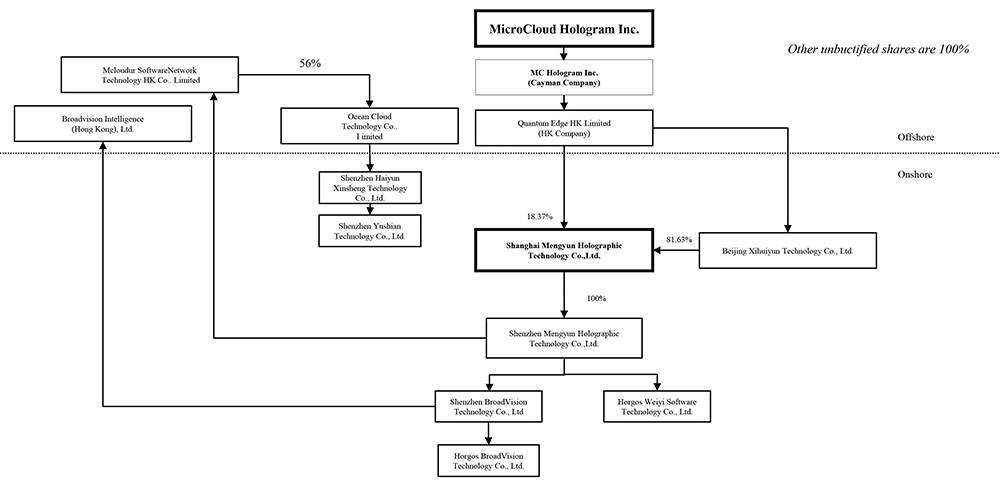

Our Holding Company Structure

MicroCloud Hologram Inc. (formerly known as Golden Path Acquisition Corporation) (“Golden Path” or “the Company”), a Cayman Islands exempted company, entered into the Merger Agreement dated September 10, 2021 (as amended on August 5, 2022 and August 10, 2022), by and among Golden Path, Golden Path Merger Sub, a Cayman Islands exempted company incorporated for the purpose of effectuating the business combination, and MC, a Cayman Islands exempted company.

Pursuant to the Merger Agreement, MC merged with the Golden Path Merger Sub and survive the merger and continue as the surviving company and a wholly owned subsidiary of Golden Path and continue its business operations (the “Merger”, and, collectively with the other transactions described in the Merger Agreement, the “Business Combination”).

Our ordinary shares and Public Warrants are listed on the Nasdaq Stock Market LLC (“NASDAQ”) under the trading symbols “HOLO” and “HOLOW” respectively.

MicroCloud is not an operating company, but a holding company incorporated in the Cayman Islands. MicroCloud operates its business through its subsidiaries in the PRC in which it owns equity interests.

The following diagram illustrates our corporate structure as of December 31, 2023, including our major subsidiaries.

1

Permission Required from the PRC Authorities for Our Operations

We conduct our business primarily through our subsidiaries in China. Our operations in China are governed by PRC laws and regulations. As of the date of this annual report, our consolidated affiliated Chinese entities have obtained the requisite licenses and permits from the PRC government authorities that are material for the business operations of our holding company, our subsidiaries in China. However, given the uncertainties of interpretation and implementation of relevant laws and regulations and the enforcement practice by government authorities, we cannot assure you that we have obtained all the permits or licenses required for conducting our business in China. We may be required to obtain additional licenses, permits, filings or approvals for our functions and services in the future. For more detailed information, see “Item 3. Key Information — D. Risk Factors — Risk Factors Relating to Our Business and Industry.”

In connection with our previous issuance of securities to foreign investors, under current PRC laws, regulations and regulatory rules, as of the date of this annual report, we, our PRC subsidiaries, (i) are not required to obtain permissions from the CSRC, (ii) are not required to go through cybersecurity review by the Cyberspace Administration of China, or the CAC, and (iii) have not received or were denied such requisite permissions by any PRC authority.

However, the PRC government has recently indicated an intent to exert more oversight and control over offerings that are conducted overseas and/or foreign investment in China-based issuers. On February 17, 2023, the CSRC released the Trial Administrative Measures of Overseas Securities Offering and Listing by Domestic Companies and five supporting guidelines, or, collectively, the Trial Measures, which came into effect on March 31, 2023. According to the Trial Measures, domestic companies in the Chinese mainland that directly or indirectly offer or list their securities in an overseas market are required to file with the CSRC. In addition, an overseas-listed company must also submit the filing with respect to its follow-on offerings, issuance of convertible corporate bonds and exchangeable bonds, and other equivalent offering activities, within a specific time frame requested under the Trial Measures. Therefore, we will be required to file with the CSRC for our overseas offering of equity and equity linked securities in the future within the applicable scope of the Trial Measures. For more detailed information, see “Item 3. Key Information — D. Risk Factors — Risk Factors Relating to Doing Business in China.”

The Holding Foreign Companies Accountable Act

The Holding Foreign Companies Accountable Act, or the HFCA Act, was enacted on December 18, 2020. The HFCA Act states that if the SEC determines that we have filed audit reports issued by a registered public accounting firm that has not been subject to inspection by the PCAOB for three consecutive years beginning in 2021, the SEC will prohibit our ordinary shares from being traded on a national securities exchange or in the over-the-counter trading market in the United States.

On December 2, 2021, the SEC adopted final amendments to its rules implementing the HFCA Act. Such final rules establish procedures that the SEC will follow in (i) determining whether a registrant is a “Commission-Identified Issuer” (a registrant identified by the SEC as having filed an annual report with an audit report issued by a registered public accounting firm that is located in a foreign jurisdiction and that the PCAOB is unable to inspect or investigate completely because of a position taken by an authority in that jurisdiction) and (ii) prohibiting the trading of an issuer that is a Commission-Identified Issuer for three consecutive years under the HFCA Act. The SEC began identifying Commission-Identified Issuers for the fiscal years beginning after December 18, 2020. A Commission-Identified Issuer is required to comply with the submission and disclosure requirements in the annual report for each year in which it was identified.

2

As of the date of this annual report, we have not been, and do not expect to be identified by the SEC under the HFCA Act. However, whether the PCAOB will continue to conduct inspections and investigations completely to its satisfaction of PCAOB-registered public accounting firms headquartered in mainland China and Hong Kong is subject to uncertainty and depends on a number of factors out of our, and our auditor’s control including positions taken by authorities of the PRC.

On December 16, 2021, the PCAOB issued its determination that the PCAOB is unable to inspect or investigate completely PCAOB-registered public accounting firms headquartered in mainland China and in Hong Kong, because of positions taken by PRC authorities in those jurisdictions, and the PCAOB included in the report of its determination a list of the accounting firms that are headquartered in the PRC or Hong Kong. This list does not include our auditor, Assentsure PAC.

On August 26, 2022, the PCAOB announced that it had signed a Statement of Protocol (the “Statement of Protocol”) with the CSRC and the Ministry of Finance of China (“MOF”). The terms of the Statement of Protocol would grant the PCAOB complete access to audit work papers and other information so that it may inspect and investigate PCAOB-registered accounting firms headquartered in mainland China and Hong Kong.

On December 15, 2022, the PCAOB announced that it has secured complete access to inspect and investigate registered public accounting firms headquartered in mainland China and Hong Kong and voted to vacate the previous 2021 determination report to the contrary. On December 29, 2022, a legislation entitled “Consolidated Appropriations Act, 2023” (the “Consolidated Appropriations Act”) was signed into law by President Biden. The Consolidated Appropriations Act contained, among other things, an identical provision to the Accelerating Holding Foreign Companies Accountable Act, which reduces the number of consecutive non-inspection years required for triggering the prohibitions under the Holding Foreign Companies Accountable Act from three years to two. As a result of the Consolidated Appropriations Act, the HFCA Act now also applies if the PCAOB’s inability to inspect or investigate the relevant accounting firm is due to a position taken by an authority in any foreign jurisdiction. The denying jurisdiction does not need to be where the accounting firm is located. Our current auditor, Assentsure PAC, as an auditor of companies that is a firm registered with the PCAOB, is subject to laws in the United States pursuant to which the PCAOB conducts regular inspections to assess its compliance with the applicable professional standards. Notwithstanding the foregoing, in the future, if there is any regulatory change or step taken by PRC regulators that does not permit our auditor to provide audit documentations located in China to the PCAOB for inspection or investigation, investors may be deprived of the benefits of such inspection. Any audit reports not issued by auditors that are completely inspected by the PCAOB, or a lack of PCAOB inspections of audit work undertaken in China that prevents the PCAOB from regularly evaluating our auditors’ audits and their quality control procedures, could result in a lack of assurance that our financial statements and disclosures are adequate and accurate, then such lack of inspection could cause our securities to be delisted from the stock exchange.The delisting of our ordinary shares, or the threat of their being delisted, may materially and adversely affect the value of your investment.”

3

The PCAOB is required under the HFCA Act to make its determination on an annual basis with regards to its ability to inspect and investigate completely accounting firms based in the mainland China and Hong Kong, among other jurisdictions. The possibility of being a “Commission-Identified Issuer” and risk of delisting could continue to adversely affect the trading price of our securities. Should the PCAOB again encounter impediments to inspections and investigations in mainland China or Hong Kong as a result of positions taken by any authority in either jurisdiction, the PCAOB will make determinations under the HFCA Act as and when appropriate.

Cash and Asset Flows through Our Organization

The Company is a holding company with no material operations of its own. We conduct our operations primarily through our subsidiaries in China. As a result, the Company’s ability to pay dividends depends upon dividends paid by our subsidiaries in China. If our existing PRC subsidiaries or any newly formed ones incur debt on their own behalf in the future, the instruments governing their debt may restrict their ability to pay dividends to us.

We are permitted under PRC laws and regulations as an offshore holding company to provide fundings to our wholly foreign-owned subsidiary in China only through loans or capital contributions, subject to the record-filing and registration with government authorities and limit on the amount of loans. Subject to satisfaction of the applicable government registration requirements, we may extend inter-company loans to our wholly foreign-owned subsidiaries in China or make additional capital contributions to the wholly foreign-owned subsidiaries to fund their capital expenditures or working capital. If we provide fundings to our wholly foreign-owned subsidiaries through loans, the total amount of such loans may not exceed the difference between the entity’s total investment as registered with the foreign investment authorities and our registered capital. Such loans must also be registered with SAFE (as defined herein) or their local branches. For more detailed information and risks associated with a transfer of funds by the Company to our PRC subsidiaries in the form of a loan or capital injection, please refer to our Annual Report on 20-F in the section “Risk Factors — Risk Factors Relating to Doing Business in China.”

| A. | Selected Financial Data |

The following selected consolidated statements of operations data and selected consolidated statements of cash flow data for the years ended December 31, 2021, 2022 and 2023 and the selected consolidated balance sheet data as of December 31, 2022 and 2023 have been derived from our audited consolidated financial statements, which are included in this annual report beginning on page F-1. Our historical results are not necessarily indicative of results expected for future periods. You should read this selected financial data together with our audited consolidated financial statements and the related notes and information under “Item 5. Operating and Financial Review and Prospects” in this annual report. Our consolidated financial statements are prepared and presented in accordance with accounting principles generally accepted in the United States of America, or U.S. GAAP.

4

The following table sets forth our selected consolidated statements of operations data for the years indicated.

| For the Year Ended December 31, | ||||||||||||||||

| Selected Consolidated Statements of Operations Data | 2021 | 2022 | 2023 | |||||||||||||

| RMB | RMB | RMB | US$ | |||||||||||||

| Revenues | 358,649,298 | 487,938,864 | 203,548,005 | 28,885,579 | ||||||||||||

| Cost of Revenues | (108,623,048 | ) | (264,679,547 | ) | (129,296,306 | ) | (18,348,491 | ) | ||||||||

| GROSS PROFIT | 250,026,250 | 223,259,317 | 74,251,699 | 10,537,088 | ||||||||||||

| Selling expenses | (5,257,331 | ) | (8,824,405 | ) | (6,692,316 | ) | (949,709 | ) | ||||||||

| General and administrative expenses | (20,058,463 | ) | (22,936,520 | ) | (65,354,201 | ) | (9,274,441 | ) | ||||||||

| Research and development expenses | (145,346,168 | ) | (331,274,831 | ) | (78,655,572 | ) | (11,162,043 | ) | ||||||||

| Provision for doubtful accounts | (515,345 | ) | (2,976,474 | ) | (857,713 | ) | (121,718 | ) | ||||||||

| Change in fair value of warrant liabilities | - | 4,415,328 | 372,961 | 52,927 | ||||||||||||

| Total operating expenses | (171,177,307 | ) | (361,596,902 | ) | (151,186,841 | ) | (21,454,984 | ) | ||||||||

| INCOME (LOSS) FROM OPERATIONS | 78,848,943 | (138,337,585 | ) | (76,935,142 | ) | (10,917,896 | ) | |||||||||

| OTHER INCOME (EXPENSE) | ||||||||||||||||

| Finance income, net | 626,796 | 1,669,078 | 3,363,084 | 477,257 | ||||||||||||

| Impairment loss for unconsolidated entities | - | (1,600,000 | ) | - | - | |||||||||||

| Profit or loss on disposal of subsidiaries | - | - | (15,278,949 | ) | (2,168,242 | ) | ||||||||||

| Other income, net | 973,932 | 983,466 | 3,124,103 | 443,343 | ||||||||||||

| Total other income (expenses), net | 1,600,728 | 1,052,544 | (8,791,762 | ) | (1,247,642 | ) | ||||||||||

| INCOME (LOSS) BEFORE INCOME TAXES | 80,449,671 | (137,285,041 | ) | (85,726,904 | ) | (12,165,538 | ) | |||||||||

| Income tax credit | 794,803 | 826,140 | 4,138,906 | 587,354 | ||||||||||||

| NET INCOME (LOSS) | 81,244,474 | (136,458,901 | ) | (81,587,998 | ) | (11,578,184 | ) | |||||||||

| Less: Net income (loss) attributable to non-controlling interests | (66 | ) | 291,987 | (205,725 | ) | (29,195 | ) | |||||||||

| NET INCOME (LOSS) ATTRIBUTABLE TO MICROCLOUD HOLOGRAM INC. ORDINARY SHAREHOLDERS | 81,244,540 | (136,750,888 | ) | (81,382,273 | ) | (11,548,989 | ) | |||||||||

| OTHER COMPREHENSIVE INCOME (LOSS) | ||||||||||||||||

| Foreign currency translation adjustment | (32,022 | ) | 995,415 | 1,817,059 | 257,860 | |||||||||||

| COMPREHENSIVE INCOME (LOSS) | 81,212,452 | (135,463,486 | ) | (79,770,939 | ) | (11,320,324 | ) | |||||||||

| Less: Comprehensive income (loss) attributable to non-controlling interests | (66 | ) | 291,987 | (205,725 | ) | (29,195 | ) | |||||||||

| COMPREHENSIVE INCOME ATTRIBUTABLE TO MICROCLOUD HOLOGRAM INC. ORDINARY SHAREHOLDERS | 81,212,518 | (135,755,473 | ) | (79,565,214 | ) | (11,291,129 | ) | |||||||||

| WEIGHTED AVERAGE NUMBER OF ORDINARY SHARES | ||||||||||||||||

| Basic and diluted | 13,200,000 | 2,007,160 | 2,167,379 | 2,167,379 | ||||||||||||

| EARNINGS (LOSS) PER SHARE1 | ||||||||||||||||

| Basic and diluted | 6.15 | (68.13 |

) |

(37.55 | ) | (5.33 | ) | |||||||||

| 1 | All period results have been adjusted for the reverse stock split effective February 2, 2024. |

5

The following table sets forth our selected consolidated balance sheet data as of the dates indicated.

| As of December 31, | ||||||||||||

| Selected Consolidated Balance Sheet Data: | 2022 | 2023 | 2023 | |||||||||

| RMB | RMB | USD | ||||||||||

| ASSETS | ||||||||||||

| CURRENT ASSETS | ||||||||||||

| Cash and cash equivalents | 151,119,985 | 126,037,538 | 17,795,126 | |||||||||

| Accounts receivable, net | 80,352,463 | 9,842,827 | 1,389,700 | |||||||||

| Prepayments and other current assets | 6,169,398 | 14,876,106 | 2,100,344 | |||||||||

| Due from related parties | 60,280 | - | - | |||||||||

| Inventories, net | 1,757,949 | 1,373,911 | 193,981 | |||||||||

| Total current assets | 239,460,075 | 152,130,382 | 21,479,151 | |||||||||

| NON-CURRENT ASSETS | ||||||||||||

| Prepayment and deposits, net | 417,004 | 310,468 | 43,835 | |||||||||

| Property and equipment, net | 1,647,876 | 1,598,134 | 225,639 | |||||||||

| Intangible assets, net | 15,376,524 | - | - | |||||||||

| Investments in unconsolidated entities | - | 600,000 | 84,713 | |||||||||

| Right-of-use assets, net | 4,064,525 | 2,988,691 | 421,971 | |||||||||

| Goodwill | 21,155,897 | - | - | |||||||||

| Deferred tax assets | - | 2,931,528 | 413,900 | |||||||||

| Total non-current assets | 42,661,826 | 8,428,821 | 1,190,058 | |||||||||

| Total assets | 282,121,901 | 160,559,203 | 22,669,209 | |||||||||

| LIABILITIES AND SHAREHOLDERS’ EQUITY | ||||||||||||

| CURRENT LIABILITIES | ||||||||||||

| Accounts payable | 61,208,297 | 1,314,370 | 185,575 | |||||||||

| Advance from customers | 3,404,038 | 2,230,852 | 314,972 | |||||||||

| Other payables and accrued liabilities | 13,549,553 | 9,097,870 | 1,284,520 | |||||||||

| Due to related parties | 350,000 | - | - | |||||||||

| Operating lease liabilities - current | 1,596,584 | 1,063,396 | 150,140 | |||||||||

| Loan payable | 410,000 | 2,903,896 | 409,998 | |||||||||

| Taxes payable | 602,254 | 625,608 | 88,329 | |||||||||

| Total current liabilities | 81,120,726 | 17,235,992 | 2,433,534 | |||||||||

| NON-CURRENT LIABILITIES | ||||||||||||

| Operating lease liabilities - non-current | 2,574,711 | 2,058,068 | 290,577 | |||||||||

| Deferred tax liabilities | 1,106,519 | - | - | |||||||||

| Warrant liabilities | 425,619 | 62,200 | 8,782 | |||||||||

| Total non-current liabilities | 4,106,849 | 2,120,268 | 299,359 | |||||||||

| Total liabilities | 85,227,575 | 19,356,260 | 2,732,893 | |||||||||

| COMMITMENTS AND CONTINGENCIES | ||||||||||||

| SHAREHOLDERS’ EQUITY | ||||||||||||

| Ordinary shares1 ($0.001 par value; 5,941,204 shares authorized; 5,081,204 and 5,941,204 shares issued and outstanding as of December 31, 2022 and December 31, 2023, respectively.) | 36,144 | 42,318 | 5,941 | |||||||||

| Additional paid-in capital | 254,138,709 | 286,296,970 | 41,180,750 | |||||||||

| Accumulated deficit | (65,500,622 | ) | (146,909,851 | ) | (20,668,617 | ) | ||||||

| Statutory reserves | 11,110,699 | 3,052,776 | 431,019 | |||||||||

| Accumulated other comprehensive loss | (3,182,525 | ) | (1,365,466 | ) | (1,026,964 | ) | ||||||

| Total MICROCLOUD HOLOGRAM INC. shareholders’ equity | 196,602,405 | 141,116,747 | 19,922,129 | |||||||||

| NON-CONTROLLING INTERESTS | 291,921 | 86,196 | 14,187 | |||||||||

| Total equity | 196,894,326 | 141,202,943 | 19,936,316 | |||||||||

| Total liabilities and shareholders’ equity | 282,121,901 | 160,559,203 | 22,669,209 | |||||||||

| 1 | All period results have been adjusted for the reverse stock split effective February 2, 2024. |

6

The following table sets forth our selected consolidated statements of cash flow data for the years indicated.

| For the Year Ended December 31, | ||||||||||||||||

| Selected Consolidated Statements of Cash Flow Data: | 2021 | 2022 | 2023 | 2023 | ||||||||||||

| RMB | RMB | RMB | USD | |||||||||||||

| CASH FLOWS FROM OPERATING ACTIVITIES: | ||||||||||||||||

| Net income (loss) | 81,244,474 | (136,458,901 | ) | (81,587,998 | ) | (11,578,184 | ) | |||||||||

| Adjustments to reconcile net income to net cash provided by (used in) operating activities: | ||||||||||||||||

| Depreciation and amortization | 6,674,311 | 6,844,237 | 6,161,834 | 874,428 | ||||||||||||

| Amortization of operating lease right-of-use assets | - | 1,589,078 | 1,075,834 | 152,672 | ||||||||||||

| Provision for doubtful accounts | 515,345 | 2,976,474 | (274,155 | ) | (38,906 | ) | ||||||||||

| Deferred tax expense (benefits) | (841,948 | ) | (880,475 | ) | (4,038,047 | ) | (573,041 | ) | ||||||||

| Provision for inventory reserve | 88,047 | - | - | - | ||||||||||||

| Interest income | (626,054 | ) | - | - | - | |||||||||||

| Impairment loss for unconsolidated entities | - | 1,600,000 | - | - | ||||||||||||

| Loss on disposal fixed assets | 365,636 | 3,285 | - | - | ||||||||||||

| Change in fair value of warrant liabilities | - | (4,415,328 | ) | (372,961 | ) | (52,927 | ) | |||||||||

| Stock compensation expense | - | - | 32,164,435 | 4,564,468 | ||||||||||||

| Impairment loss for intangible assets | - | - | 3,854,547 | 547,000 | ||||||||||||

| Impairment loss for goodwill | - | - | 21,155,897 | 3,002,242 | ||||||||||||

| Loss on disposal of subsidiaries | - | - | (1,900,379 | ) | (269,684 | ) | ||||||||||

| Change in operating assets and liabilities: | ||||||||||||||||

| Accounts receivable | 11,479,621 | (15,072,501 | ) | 70,783,791 | 10,044,956 | |||||||||||

| Prepayment and other current assets | 4,324,504 | (5,544,532 | ) | (8,706,708 | ) | (1,235,572 | ) | |||||||||

| Inventories | 2,855,093 | 167,562 | 384,038 | 54,499 | ||||||||||||

| Prepayments and deposits | 177,350 | 32,688 | 106,536 | 15,119 | ||||||||||||

| Accounts payable | (6,012,590 | ) | 14,191,808 | (59,893,927 | ) | (8,499,571 | ) | |||||||||

| Operating lease liabilities |

- |

(1,482,308 | ) | (1,049,831 | ) | (148,982 | ) | |||||||||

| Advance from customers | (698,465 | ) | 2,545,326 | (1,173,186 | ) | (166,487 | ) | |||||||||

| Other payables and accrued liabilities | 2,066,507 | 1,891,849 | (4,451,683 | ) | (631,740 | ) | ||||||||||

| Taxes payable | 1,382,989 | (2,647,030 | ) | 23,354 | 3,314 | |||||||||||

| Net cash provided by (used in) operating activities | 102,994,820 | (134,658,768 | ) | (27,738,609 | ) | (3,936,396 | ) | |||||||||

| CASH FLOWS FROM INVESTING ACTIVITIES: | ||||||||||||||||

| Payments for business acquisition payable - related parties | (50,000,000 | ) | - | - | - | |||||||||||

| Loan proceeds to third parties | (90,268,908 | ) | (10,339,518 | ) | - | - | ||||||||||

| Loan repayment from third parties | 57,906,587 | 23,668,959 | - | - | ||||||||||||

| Purchases of property and equipment | (135,676 | ) | (1,821,918 | ) | (774,615 | ) | (109,926 | ) | ||||||||

| Cash received on fixed assets disposal | 600 | - | - | - | ||||||||||||

| Investments in unconsolidated entities | (1,600,000 | ) | - | (600,000 | ) | (85,146 | ) | |||||||||

| Net cash provided by (used in) investing activities | (84,097,397 | ) | 11,507,523 | (1,374,615 | ) | (195,072 | ) | |||||||||

| CASH FLOWS FROM FINANCING ACTIVITIES: | ||||||||||||||||

| Amounts advanced from related parties | 1,806,084 | - | - | - | ||||||||||||

| Amounts advanced to related parties | - | (40,280 | ) | - | - | |||||||||||

| Repayments from related parties | 8,703,084 | - | 60,280 | 8,554 | ||||||||||||

| Repayments to related parties | (10,643,080 | ) | (370 | ) | (350,000 | ) | (49,669 | ) | ||||||||

| Repayments of third-party loan | (1,167,504 | ) | (90,000 | ) | (7,406,104 | ) | (1,051,003 | ) | ||||||||

| Cash received from recapitalization | - | 223,513,290 | - | - | ||||||||||||

| Proceeds of third-party loan | 500,000 | 9,900,000 | 1,404,913 | |||||||||||||

| Net cash provided by (used in) financing activities | (1,301,416 | ) | 223,882,640 | 2,204,176 | 312,795 | |||||||||||

| EFFECT OF EXCHANGE RATE ON CASH AND CASH EQUIVALENTS | (271,402 | ) | 2,381,611 | 1,826,601 | (296,539 | ) | ||||||||||

| CHANGE IN CASH AND CASH EQUIVALENTS | 17,324,605 | 103,113,006 | (25,082,447 | ) | (4,115,212 | ) | ||||||||||

| CASH AND CASH EQUIVALENTS, beginning of period | 30,682,374 | 48,006,979 | 151,119,985 | 21,910,338 | ||||||||||||

| CASH AND CASH EQUIVALENTS, end of period | 48,006,979 | 151,119,985 | 126,037,538 | 17,795,126 | ||||||||||||

| SUPPLEMENTAL CASH FLOW INFORMATION: | ||||||||||||||||

| Cash paid for income taxes | 72,041 | 4,201 | - | - | ||||||||||||

| Cash paid for interest | 20,177 | 38,084 | 26,442 | 3,752 | ||||||||||||

| NON-CASH INVESTING AND FINANCING ACTIVITIES: | ||||||||||||||||

| Initial recognition of right-of-use assets and lease liabilities | - | 5,653,603 | 932,174 | 132,285 | ||||||||||||

7

MICROCLOUD HOLOGRAM INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF SHAREHOLDERS’ EQUITY

| Ordinary shares | Additional | Retained earnings (Deficit) | Accumulated other |

Non- | ||||||||||||||||||||||||||||||||

| Par | paid-in | Statutory | comprehensive | controlling | ||||||||||||||||||||||||||||||||

| Shares1 | value1 | capital | reserves | Unrestricted | (loss) | Interest | Total | Total | ||||||||||||||||||||||||||||

| RMB | RMB | RMB | RMB | RMB | RMB | RMB | USD | |||||||||||||||||||||||||||||

| BALANCE, December 31, 2020 | 13,200,000 | 86,093 | 29,910,089 | 5,802,662 | (4,686,228 | ) | (25,795 | ) | - | 31,086,821 | 4,878,586 | |||||||||||||||||||||||||

| Net income | 81,244,540 | (66 | ) | 81,244,474 | 12,750,031 | |||||||||||||||||||||||||||||||

| Statutory reserves | 2,738,633 | (2,738,633 | ) | - | - | |||||||||||||||||||||||||||||||

| Foreign currency translation | (32,022 | ) | (32,022 | ) | (5,025 | ) | ||||||||||||||||||||||||||||||

| BALANCE, December 31, 2021 | 13,200,000 | 86,093 | 29,910,089 | 8,541,295 | 73,819,679 | (57,817 | ) | (66 | ) | 112,299,273 | 17,623,592 | |||||||||||||||||||||||||

| Net income | (136,750,888 | ) | 291,987 | (136,458,901 | ) | (20,279,224 | ) | |||||||||||||||||||||||||||||

| Statutory reserves | 2,569,404 | (2,569,404 | ) | |||||||||||||||||||||||||||||||||

| Cancellation of the outstanding shares in MC held by former MC shareholders | (13,200,000 | ) | (86,093 | ) | (86,093 | ) | (13,511 | ) | ||||||||||||||||||||||||||||

| Initial common shares of Golden Path | 170,800 | 1,215 | 1,215 | 171 | ||||||||||||||||||||||||||||||||

| Initial common shares of Golden Path subject to possible redemption | 575,000 | 4,090 | 4,090 | 575 | ||||||||||||||||||||||||||||||||

| Shares converted from rights | 60,205 | 428 | 428 | 60 | ||||||||||||||||||||||||||||||||

| Issuance of common stock to Finder | 38,000 | 270 | 270 | 38 | ||||||||||||||||||||||||||||||||

| Issuance of common stock as consideration of business combination | 4,455,446 | 31,694 | 224,228,620 | 224,260,314 | 32,011,551 | |||||||||||||||||||||||||||||||

| Redemption of common stock | (218,247 | ) | (1,553 | ) | (1,553 | ) | (218 | ) | ||||||||||||||||||||||||||||

| Foreign currency translation | (3,124,717 | ) | (3,124,717 | ) | (796,039 | ) | ||||||||||||||||||||||||||||||

| BALANCE, December 31, 2022 | 5,081,204 | 36,144 | 254,138,709 | 11,110,699 | (65,500,622 | ) | (3,182,525 | ) | 291,921 | 196,894,326 | 28,546,995 | |||||||||||||||||||||||||

| Net income | (81,382,273 | ) | (205,725 | ) | (81,587,998 | ) | (11,578,184 | ) | ||||||||||||||||||||||||||||

| Statutory reserves | 26,956 | (26,956 | ) | - | - | |||||||||||||||||||||||||||||||

| Issuance of common stock to employees in employee benefit plans | 860,000 | 6,174 | 32,158,261 | 32,164,435 | 4,480,600 | |||||||||||||||||||||||||||||||

| Disposal of subsidiaries | (8,084,879 | ) | (8,084,879 | ) | (1,770,955 | ) | ||||||||||||||||||||||||||||||

| Foreign currency translation | 1,817,059 | 1,817,059 | 257,860 | |||||||||||||||||||||||||||||||||

| BALANCE, December 31, 2023 | 5,941,204 | 42,318 | 286,296,970 | 3,052,776 | (146,909,851 | ) | (1,365,466 | ) | 86,196 | 141,202,943 | 19,936,316 | |||||||||||||||||||||||||

| 1 | All period results have been adjusted for the reverse stock split effective February 2, 2024. |

8

| B. | CAPITALIZATION AND INDEBTEDNESS |

Not applicable.

| C. | REASONS FOR THE OFFER AND USE OF PROCEEDS |

Not applicable.

| D. | RISK FACTORS |

You should carefully consider the risks and uncertainties described below, together with all the other information in this Annual Report on Form 20-F including “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the consolidated financial statements and the related notes. If any of the following risks actually occurs (or if any of those discussed elsewhere in this Annual Report on Form 20-F occurs), our business, reputation, financial condition, results of operations, revenue, and future prospects could be seriously harmed. The risks and uncertainties described below are not the only ones we face. Additional risks and uncertainties that we are unaware of, or that we currently believe are not material, may also become important factors that adversely affect our business. Unless otherwise indicated, references to our business being seriously harmed in these risk factors will include harm to our business, reputation, financial condition, results of operations, revenue, and future prospects. In that event, the market price of our common stock could decline, and you could lose part or all of your investment.

9

Risk Factors Relating to Our Business and Industry

The holographic technology service industry is developing rapidly and affected by continuous technological changes, with the risk that we cannot continue to make the correct strategic investment and develop new products to meet customer needs.

The holographic service industry develops rapidly, and our success depends on our ability to continuously develop and implement services and solutions that predict and respond to rapid and ongoing changes in holographic technology and the industry, and to continuously provide services that meet the changing needs of customers. If we do not invest enough in new technologies, or if we do not make the right strategic investments to address these developments and drive innovation, our competitive advantages may be negatively impacted. To maintain and enhance our current competitive position, we need to continuously introduce new solutions and services to meet customers’ needs.

Research and development of new technologies and solutions require substantial investments of human resources and capital. However, there is no guarantee that our research and development will be successful, or that we could achieve the excepted return on our human resources and capital investments. While we intend to invest substantial resources to remain on the forefront of technological development, continuing changes in holographic technology and the markets, including the ADAS and autonomous driving industries, LiDAR and holographic digital twin technology service industries, could adversely affect adoption of holographic technology and/or our products, either generally or for particular applications. Our future success will depend upon our ability to develop and introduce a variety of new capabilities and innovations to our existing product offerings, as well as the ability to introduce a variety of new product offerings, to address the changing needs of the markets. If we are unable to devote adequate resources to develop products or cannot otherwise successfully develop products or system configurations that meet customer requirements on a timely basis or that remain competitive with technological alternatives, our products could lose market share, our revenue may decline, and our business and prospects may be adversely affected.

In addition, our success to date has been based on the delivery of holography-centered software and hardware solutions to research and development programs in which developers are investing substantial capital to develop new systems. Our continued success relies on the success of the research and development phase of these customers as they expand into commercialized projects. For example, with respect to our holographic ADAS segment, most of our automotive customers are just beginning on the path to commercialization, as large-scale commercialization of the autonomous driving industry is yet to start. As holographic technology reaches the stage of large-scale commercialization, we will be required to develop and deliver holography-centered software and hardware solutions at price points that enable wider and ultimately mass-market adoption. In addition, the delays in introducing products and innovations, and the failure to choose correctly among technical alternatives or the failure to offer innovative products or configurations at competitive prices may cause existing and potential customers to purchase our competitors’ products or turn to alternative technologies.

Our competitive position and results of operations could be harmed if we do not compete effectively.

The holographic service market is characterized by intense competition, new industry standards, limited barriers to entry, disruptive technology developments, short product life cycles, customer price sensitivity and frequent product introductions (including alternatives with limited functionality available at lower costs or free of charge). Any of these factors could create downward pressure on pricing and profitability and could adversely affect our ability to retain current customers or attract new customers. Our future success will depend on the ability to continuously enhance and integrate our existing products and services, introduce new products and services in a timely and cost-effective manner, meet changing customer expectations and needs, extend our core technology into new applications, and anticipate emerging standards, business models, software delivery methods and other technological developments.

Furthermore, some of our current and potential competitors enjoy competitive advantages such as greater financial, technical, sales, marketing and other resources, broader brand awareness, and access to larger customer bases. As a result of these advantages, potential and current customers might select the products and services of our competitors, which may cause a loss of market share to us.

10

Adverse conditions in the related industries, such as the automotive industry, or the global economy in general could have adverse effects on our results of operations.

Our business is dependent, in large part on, and directly affected by, business cycles and other factors affecting the related industries, such as the automobile industry, and the global economy in general. Automotive production and sales are highly cyclical and depend on general economic conditions and other factors, including consumer spending and preferences, changes in interest rates and credit availability, consumer confidence, fuel costs, fuel availability, environmental impact, governmental incentives and regulatory requirements, and political volatility, especially in energy-producing countries and growth markets. In addition, automotive production and sales can be affected by our automotive customers’ ability to continue operating in response to challenging economic conditions and in response to labor relations issues, regulatory requirements, trade agreements and other factors. The volume of automotive production in China has fluctuated, sometimes significantly, from year to year, and we expect such fluctuations to give rise to fluctuations in the demand for our products. In addition, adverse conditions in the global economy in general could also adversely affect the results of operations of our customers. Any significant adverse changes in the results of operations of our customers could in turn have material adverse effects on our business, results of operations and financial position.

The market adoption of LiDAR, especially holographic LiDAR technology, is uncertain. If market adoption of LiDAR does not continue to develop, or develops more slowly than we expect, our business will be adversely affected.

Our holographic LiDAR-based ADAS solutions can be applied to different use cases across end markets. Despite the fact that the automotive industry has engaged in considerable effort to research and test LiDAR products for ADAS and autonomous driving applications, the application of LiDAR products, especially holographic LiDAR products, in commercially available vehicles has been generally limited. We continually study emerging and competing sensing technologies and methodologies and we may add new sensing technologies to address LiDAR’s relative deficiencies in detecting colors and low reflectivity objects and performing in extreme weather conditions. However, LiDAR products remain relatively new, and it is possible that other sensing modalities, or a new disruptive modality based on new or existing technology, including a combination of different technologies, will achieve acceptance or leadership in the ADAS and autonomous driving industries. Even if LiDAR products are used in initial generations of autonomous driving technology and certain ADAS products, we cannot guarantee that LiDAR products will be designed into or included in subsequent generations of such commercialized technology.

Market growth potentials for ADAS or autonomous vehicles is difficult to predict, especially in light of the economic consequences of the COVID-19 pandemic. By the time mass market adoption of autonomous vehicle technology is achieved, we expect competition among providers of sensing technology based on LiDAR and other modalities to increase substantially. If commercialization of LiDAR products is not successful, or not as successful as we or the market expect, or if other sensing modalities gain acceptance by market participants and regulators by the time autonomous vehicle technology achieves mass market adoption, our business, results of operations and financial condition will be materially and adversely affected.

We are investing in and pursuing market opportunities outside of the automotive markets, including but not limited to industrial and security robots, mapping applications for topography and surveying and smart city initiatives. We believe that our future revenue growth, if any, will depend in part on our ability to expand within new markets such as these and to enter new markets as they emerge. Each of these markets presents distinct risks and, in many cases, requires us to address the particular requirements of that market. Addressing these requirements can be time-consuming and costly. The market for LiDAR technology outside of automotive applications is relatively new, rapidly developing and unproven in many markets or industries. Many of our customers outside of the automotive industry are still in the testing and development phases and we cannot be certain that they will commercialize products or systems with our LiDAR products or at all. We cannot be certain that LiDAR will be sold into these markets, or any market outside of automotive market, at scale. If LiDAR technology does not achieve commercial success outside of the automotive industry, or if the market develops at a pace slower than we expect, our business, results of operation and financial condition will be materially and adversely affected.

11

Our results of operations could materially suffer in the event of insufficient pricing to enable us to meet profitability expectations.

If we are not able to obtain sufficient pricing for our services and solutions, our revenues and profitability could materially suffer. The rates we are able to charge for services and solutions are affected by a number of factors, including:

| ● | general economic and political conditions; |

| ● | the competitive environment in our industry; |

| ● | market price of our service and products provided; |

| ● | our bargaining power when entering into contract with customers; |

| ● | our customers’ preferences and desire to reduce their costs; and |

| ● | our ability to accurately estimate, monitor and manage our contract revenues, costs of sales, profit margins and cash flows over the full contract period. |

In addition, our profitability with respect to services and solutions for new technologies may be different when compared to the profitability of our current business, due to factors such as the use of alternative pricing, the mix of work and the number of service providers, among others.

The competitive environment in the holographic technology service industry and related industries in the PRC affects our ability to obtain favorable pricing in a number of ways, any of which could have a material negative impact on our results of operations. The less we are able to differentiate and/or clearly convey the value of our services and solutions, the more likely that price will become the driving factor in selecting a service provider. In addition, the introduction of new services or products by competitors could reduce our ability to obtain favorable pricing for the services or products that we offer. Competitors may be willing, at times, to price contracts lower than us in an effort to enter new markets or increase market share. Further, if competitors develop and implement methodologies that yield greater efficiency and productivity, they may be better positioned to offer similar services at lower prices. As such, failure to adopt a sufficient pricing policy or adjust our pricing policy in a timely and effective manner could adversely and materially affect our competitive position in the industry, which could adversely and materially affect our operations and financial conditions.

We expect to incur substantial research and development costs and devote significant resources to identifying and commercializing new products, which could significantly reduce our profitability, and there is no guarantee that such efforts would eventually generate revenue for us.

Our future growth depends on penetrating new markets, adapting existing technologies and products to new applications and customer requirements, and introducing new services and products that achieve market acceptance. We plan to incur substantial and potentially increasing, research and development costs as part of our efforts to design, develop, manufacture, and commercialize new products and enhance existing products. Because we account for research and development as an operating expense, these expenditures will adversely affect our results of operations in the future. Further, the performance of holographic LiDAR depends on software and hardware solutions involving the integration of automotive integrated circuit (IC), holographic image processing and algorithm software. Production of these complex components may require extremely high cost, which may reduce our profit margins or increase our losses.

We may need to raise additional capital in the future in order to execute our business plan, which may not be available on terms acceptable to us, or at all.

In the future, we may require additional capital to respond to technological advancements, competitive dynamics or technologies, customer demands, business opportunities, challenges, acquisitions or unforeseen circumstances and we may determine to engage in equity or debt financings, or to enter into credit facilities for other reasons. In order to further business relationships with current or potential customers and partners, we may issue equity or equity-linked securities to such current or potential customers or partners. We may not be able to timely secure additional debt or equity financing on favorable terms, or at all. If we raise additional funds through the issuance of equity or convertible debt or other equity-linked securities or if we issue equity or equity-linked securities to current or potential customers to further business relationships, our existing shareholders could experience significant dilution. Any debt financing obtained by us in the future could involve restrictive covenants relating to our capital raising activities and other financial and operational matters, which may make it more difficult for us to obtain additional capital and to pursue business opportunities, including potential acquisitions. If we are unable to obtain adequate financing or financing on terms satisfactory to us, our ability to continue to grow or support our business and to respond to business challenges could be significantly limited.

12

Market share of our holographic LiDAR products will be materially adversely affected if such products are not adopted by the automotive original equipment manufacturers (OEMs) or their supplier for ADAS applications.

The OEMs and their suppliers have been developing applications in the autonomous driving and ADAS industries over the years. These OEMs manufacturers and suppliers perform extensive testing or identification processes before ordering a large number of LiDAR products, as such products would function as part of a larger system or platform and must comply with certain other specifications. In the future, we may spend a lot of time and resources to have our products selected by automotive OEMs and their suppliers, which is called “design win.” In terms of autonomous driving and ADAS technology, a design win means that our holographic LiDAR products have been selected for use in specific models. If our products are not selected by the OEMs or their suppliers for one model, or if our products are not successful on that model, it is unlikely to be deployed on other models of that OEM. If we fail to win a large number of models from one or more automotive OEMs or their suppliers, our business will be materially adversely affected.

We have material customer concentration, with a limited number of customers accounting for a material portion of our revenues for the years ended December 31, 2022 and 2023.

For the year ended December 31, 2023, our five largest customers in aggregate accounted for approximately 57.7% of our revenues, and our largest customer accounted for approximately 25.0% of our revenues. There are inherent risks whenever a large percentage of total revenues are concentrated with a limited number of customers. It is not possible for us to predict the future level of demand for our products and services that will be generated by these customers, or to predict the future demand for the products and services of these customers in the end-user marketplace. In addition, revenues from these customers may fluctuate from time to time, which may be affected by market conditions or other factors, some of which may be outside of our control. Further, we may not be able to maintain and solidify our relationships with these major customers on commercially reasonable terms, or at all. As such, any declines in revenues from our major customers could have an adverse effect on our business, results of operations and financial condition.

We and our subsidiaries depend on a limited number of vendors for a significant portion of our purchase which may result in heightened concentration risk.

We and our subsidiaries, also conduct business with a limited number of vendors. For the years ended December 31, 2022 and 2023, 13.8% and 62.6% of our total purchases were from one and three vendors, respectively.

Our financial results could be materially and adversely affected if any one supplier fails to fulfill our contractual obligations, or if we are unable to find other suppliers to provide the same level of supplies. In addition, we cannot assure you that performance by third-party vendors will be satisfactory, and if they under-perform, it will have a material adverse effect on the cash flows or profitability of our business.

The period of time from a “design win” to implementation is long, and we are subject to the risks of cancellation or postponement of the contract or unsuccessful implementation

Prospective customers, including those in the automotive industry, generally must make significant commitments of resources to test and validate our products and confirm that they can integrate with other technologies before including them in any particular system, product or model. The development cycles of our products with new customers varies widely depending on the application, market, customer and the complexity of the product. In the automotive market, for example, this development cycle can be five to seven or more years. The development cycle in certain other markets can be months to one or two years. These development cycles result in our investment of resources prior to realizing any revenue from the commercialization. Further, we are subject to the risk that customers cancel or postpone implementation of our technology, as well as that we will not be able to integrate our technology successfully into a larger system with other sensing modalities. Further, our revenue could be less than forecasted if the system, product or vehicle model that includes our LiDAR products is unsuccessful, including for reasons unrelated to our technology. Long development cycles and product cancellations or postponements may adversely affect our business, results of operations and financial condition.

13

The complexity of our products could result in unforeseen delays or expenses from undetected defects, errors or bugs in hardware or software which could reduce the market adoption of our new products, damage our reputation with current or prospective customers, result in product returns or expose us to product liability and other claims and adversely affect our operating costs.

Our products are highly technical and very complex and require high standards to manufacture. These products have in the past and will likely in the future experience defects, errors or bugs at various stages of development. We may be unable to timely release new products, manufacture existing products, correct problems that have arisen or correct such problems to our customers’ satisfaction. Additionally, undetected errors, defects or security vulnerabilities, especially as new products are introduced or as new versions are released, could result in (i) serious injury to the end users of technology incorporating our products, or those in the surrounding area, (ii) customers never being able to commercialize technology incorporating our products, and (iii) litigation against us, negative publicity and other consequences. These risks are particularly prevalent in the highly competitive autonomous driving and ADAS markets. Some errors or defects in our products may only be discovered after they have been tested, commercialized and deployed by customers. If that is the case, we may incur significant additional development costs and product recall, repair or replacement costs. Furthermore, we could also experience higher levels of product returns in such cases, which could adversely affect our financial results. These problems may also result in claims against us by our customers or others. our reputation or brand may be damaged as a result of these problems, and customers may be reluctant to buy our products, which could adversely affect our ability to retain existing customers and attract new customers.

Failure in cost control may negatively impact the market adoption and profitability of our products.

Our production output depends on our ability to produce and/or procure certain key components and raw materials at an acceptable price. If we fail to reduce or control costs to be incurred thereof, we might not be able to price our products competitively, which in turn may reduce the market adoption rate of our products. In addition, failure in cost control may also result in material adverse effects on our profitability. As such, our results of operations and financial position will be adversely affected.

Continued pricing pressures may result in low profitability, or even losses to us.

Automotive OEMs possess significant leverage over their suppliers, including us, because the automotive component supply industry is highly competitive and has a high fixed cost base. Accordingly, we expect to be subject to substantial continuing pressure from automotive OEMs and their suppliers to reduce the price of our products. It is possible that pricing pressures could intensify beyond our expectations as automotive OEMs pursue restructuring, consolidation and cost-cutting initiatives. If we are unable to generate sufficient production cost savings in the future to offset price reductions, our profitability would be adversely affected.

We have a limited operating history, and we may not be able to sustain rapid growth, effectively manage growth or implement business strategies.

We have a limited operating history. Although we have experienced significant growth since launching our business, our historical performance results and growth rate may not be indicative of our future performance. We may not be able to achieve similar results or grow at the same rate as we have in the past. To keep pace with the development of the holographic technology service industry in the PRC, we may need to adjust and upgrade our product and service offerings or modify our business model. These adjustments may not achieve expected results and may have a material and adverse impact on our financial conditions and results of operations.

In addition, our rapid growth and expansion have placed, and is expected to continue to place, a significant strain on our management and resources. There is no assurance that our future growth will be sustained at a similar rate or at all. We believe that our revenue, expenses and operating results may vary from period to period in response to a variety of factors beyond our control, which primarily include general economic conditions, emergencies and changes in policies, laws and regulations that may affect our business operations and our ability to monitor costs. In addition, our ability to develop new sources of revenues, diversify monetization methods, attract and retain customers, continue developing innovative technologies, increase brand awareness, expand into new market segments, and adjust to the rapidly changing regulatory environment in the PRC, will also affect our future growth to a great extent. Therefore, our historical results are not predictive of our future financial performance.

14

If we fail to attract, retain and engage appropriately-skilled personnel, including senior management and technology professionals, our business may be harmed.

Our future success depends on the retention of highly skilled executives and employees. Competition for well-qualified and skilled employees is intense. Our future success also depends on the continuing ability to attract, develop, motivate and retain highly qualified and skilled employees, including, in particular, software engineers, LiDAR scientists and holographic technology professionals. Our continued ability to compete effectively depends on the ability to attract new employees and to retain and motivate existing employees. If any member of our senior management team or other key employees leave, our ability to successfully operate the business and execute the business strategy could be adversely affected. We may also have to incur significant costs in identifying, hiring, training and retaining replacements of departing employees.

Our business depends substantially on the market recognition of our brand, and negative media coverage could adversely affect our business.

We believe that enhancing our brand and extending our customer base are cornerstones to sustaining our competitive advantages. Negative publicity about us and our business, shareholders, affiliates, directors, officers, and other employees, as well as the industry in which we operate, could be devastating and could materially and adversely affect the public perception of our brand, and in turn, reduce the sales of our products and services. Negative publicity concerning could be related to a wide variety of matters, including:

| ● | alleged misconduct or other improper activities committed by our shareholders, affiliates, directors, officers and other employees; |

| ● | false or malicious allegations or rumors about us or our shareholders, affiliates, directors, officers, and other employees; |

| ● | user complaints about the quality of our products and services; |

| ● | copyright or patent infringements involving us and contents offered on our platforms; and |

| ● | governmental and regulatory investigations or penalties resulting from our failure to comply with applicable laws and regulations. |

In addition to traditional media, there has been an increasing use of social media platforms and similar devices in China, including instant messaging applications, social media websites and other forms of internet-based communications that provide individuals with access to a broad audience of users and other interested persons. The availability of information on instant messaging applications and social media platforms is virtually immediate as its impact without affording us an opportunity for redress or correction. The opportunity for dissemination of information, including inaccurate information, is seemingly limitless and readily available. Information concerning us, shareholders, directors, officers and employees may be posted on such platforms at any time. Risks associated with any such negative publicity or incorrect information cannot be eliminated entirely or mitigated, and may materially harm our reputation, business, financial condition and results of operations.

Failure to maintain, protect, and enhance our brand or to enforce our intellectual property rights may damage the results of our business and operations.

We believe that the protection of trade secrets, patents, trademarks and domain names is key to our success. In particular, we must maintain, protect, and strengthen our intellectual property rights related to our holographic technical services. Its intellectual property is essential to expanding the population of individuals and corporate users as well as increasing their trust in our services. We are committed to protecting our intellectual property rights in accordance with PRC laws and relevant agreements. We usually enter into confidentiality agreements with our employees to restrict the access, disclosure, and use of our proprietary information. However, we cannot guarantee that the contractual arrangements and other measures taken by us are sufficient to prevent the theft of our proprietary information, to prevent competitors from independently developing similar technologies, or to prevent any attempt to imitate it. Preventing unauthorized use of our intellectual property is difficult and costly, and the measures we take may not be enough to prevent intellectual property theft. If we sue for enforcing intellectual property, the litigation may result in huge costs and dispersion of our management and financial resources. Failure to protect our intellectual property rights may have a significant adverse impact on our business, financial position and operating performance.

15

We may be vulnerable to intellectual property infringement charges filed by other companies.

Although we developed and owns the core intellectual properties, the interpretation of PRC intellectual property laws and intellectual property standards are constantly evolving and may be uncertain. As a result, there might be litigations based on allegations of infringement, misappropriation or other violations of intellectual property rights. our defense of intellectual property rights claims brought against us or our customers, suppliers and channel partners, with or without merit, could be time-consuming, expensive to litigate or settle, divert management resources and attention and force us to acquire intellectual property rights and licenses, which may involve substantial royalty or other payments. An adverse determination also could invalidate our intellectual property rights and adversely affect our ability to offer our products to our customers and may require that we procure or develop substitute products that do not infringe, which could require significant effort and expense. A claim that our products infringe a third party’s intellectual property rights, even if untrue, could adversely affect our relationships with our customers, may deter future customers from purchasing our products and could expose us to costly litigation and settlement expenses. Any of these events could adversely affect our business, operating results, financial condition and prospects.

We may not be able to protect our source code from copying if there is an unauthorized disclosure.

Source code, the detailed program commands for our middleware and software programs and solutions, is critical to our business. Although we license portions of our application and operating system source code to several licensees, we take significant measures to protect the secrecy of large portions of our source code. If our source code leaks, we might lose future trade secret protection for that code. It may then become easier for third parties to compete with us by copying functionality, which could adversely affect our results of operations.

Third parties may register trademarks or domain names or purchase internet search engine keywords that are similar to our trademarks, brand or websites, or misappropriate our data and copy our platform, all of which could cause confusion to our users, divert online customers away from our products and services or harm our reputation.

To divert potential customers from us to such competitors’ or third parties’ websites or platforms, competitors and other third parties may purchase (i) trademarks that are similar to our trademarks and (ii) keywords that are confusingly similar to our brand or websites in internet search engine advertising programs and in the header and text of the resulting sponsored links or advertisements in order to divert our potential customers to such competitors’ or third parties’ websites or platforms. Preventing such unauthorized use is inherently difficult. If we are unable to prevent such unauthorized use, competitors and other third parties may continue to drive potential customers away from our platform to competing, irrelevant or potentially offensive platform, which could harm our reputation and cause us to lose revenue.

Our business is highly dependent on the proper functioning and improvement of our information technology systems and infrastructure. Our business and operating results may be harmed by service disruptions, or by our failure to timely and effectively scale up and adjust our existing technology and infrastructure.

Our business depends on the continuous and reliable operation of our information technology (“IT”) systems. Our IT systems are vulnerable to damage or interruption as a result of fires, floods, earthquakes, power losses, telecommunications failures, undetected errors in software, computer viruses, hacking and other attempts to harm our IT systems. Disruptions, failures, unscheduled service interruptions or a decrease in connection speeds could damage our reputation and cause our customers and end-users to migrate to our competitors’ platforms. If we experience frequent or constant service disruptions, whether caused by failures of our own IT systems or those of third-party service providers, then our user experience may be negatively affected, which in turn may have a material and adverse effect on our reputation and business. We may not be successful in minimizing the frequency or duration of service interruptions. As the number of our end-users increases and more user data are generated on our platform, we may be required to expand and adjust technology and infrastructure to continue to reliably store and process content.

16

Our operations depend on the performance of the Internet infrastructure and fixed telecommunications networks in China, which may experience unexpected system failure, interruption, inadequacy or security breaches.

Almost all access to the Internet in China is maintained through state-owned telecommunication operators under the administrative control and regulatory supervision of the Ministry of Industry and Information Technology, or the MIIT. Moreover, we primarily rely on a limited number of telecommunication service providers to provide us with data communications capacity through local telecommunications lines and Internet data centers to host our servers. We have limited access to alternative networks or services in the event of disruptions, failures or other problems with China’s Internet infrastructure or the fixed telecommunications networks provided by telecommunication service providers. Web traffic in China has experienced significant growth during the past few years. Effective bandwidth and server storage at Internet data centers in large cities such as Beijing and Shenzhen are scarce. With the expansion of our business, we may be required to upgrade technology and infrastructure to keep up with the increasing traffic on our platform. We cannot assure you that the Internet infrastructure and the fixed telecommunications networks in China will be able to support the demands associated with the continued growth in Internet usage. If we cannot increase our capacity to deliver online services, then we may not be able to expand our customer base, and the adoption of our services may be hindered, which could adversely impact our business and profitability.

In addition, we have no control over the costs of the services provided by telecommunication service providers. If the prices we pay for telecommunications and Internet services rise significantly, our results of operations may be materially and adversely affected. Furthermore, if Internet access fees or other charges to Internet users increase, some users may be prevented from accessing the mobile Internet and thus cause the growth of mobile Internet users to decelerate. Such deceleration may adversely affect our ability to continue to expand our user base.