Exhibit 99.1

|

|

Bowlero, World’s Largest Owner and Operator

of Bowling Centers, Outperforms Q1 2022

Fiscal Year Expectations and Dramatically Outpaces Pre-Pandemic Performance

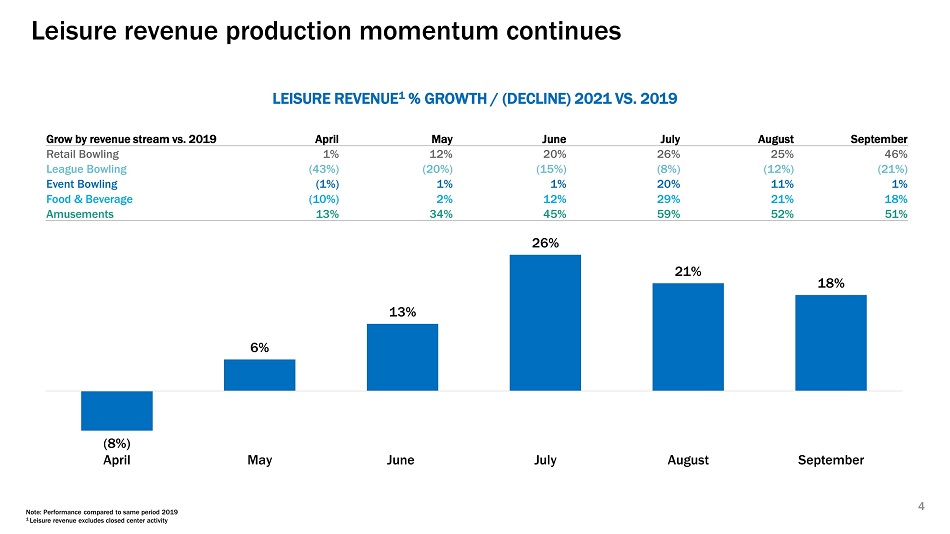

| ● | Leisure revenue, which accounts for the bulk of total revenue, rose 22% from pre-pandemic levels. | |

| ● | Net Income for the quarter was $25 million vs. a loss of $20 million in the first quarter of fiscal year 2021 | |

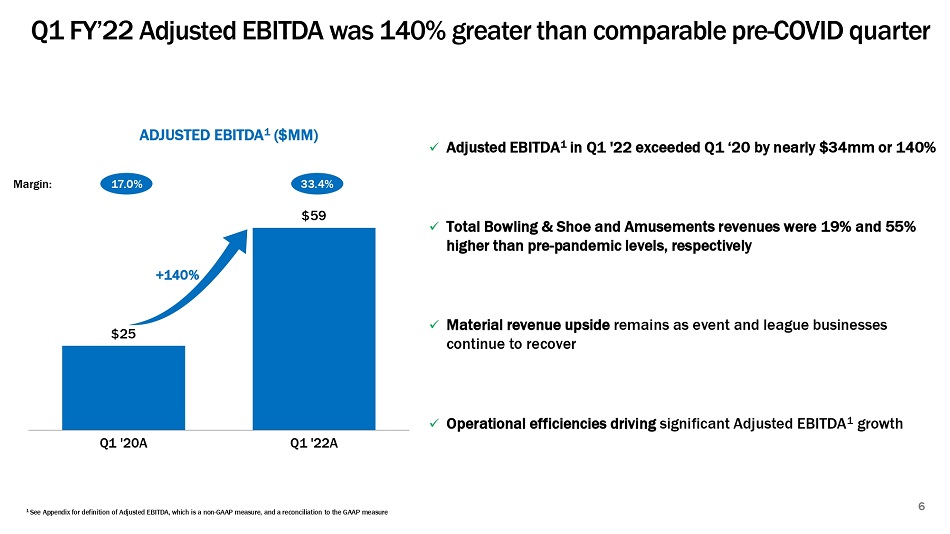

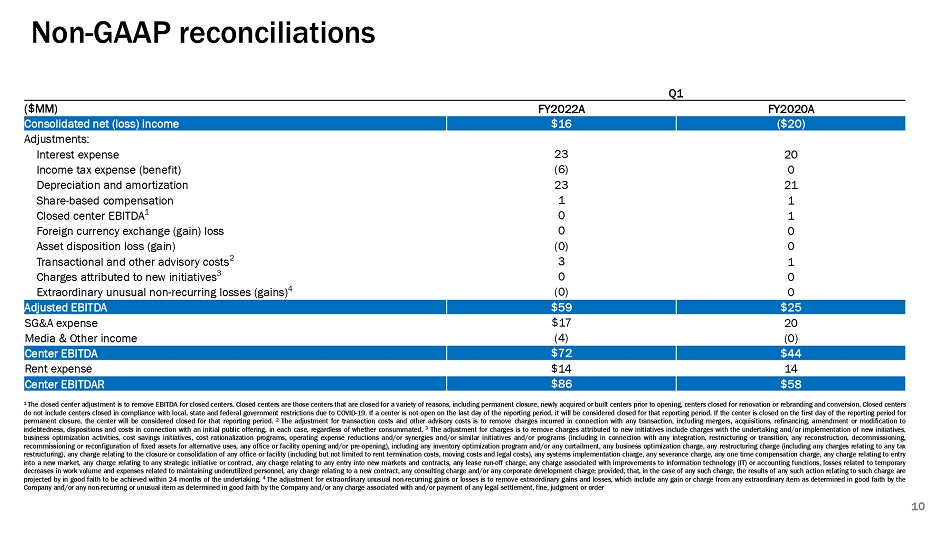

| ● | Adjusted EBITDA rose 140% vs. pre-pandemic quarter to $59 million, as operational efficiencies continue to drive significant margin expansion. | |

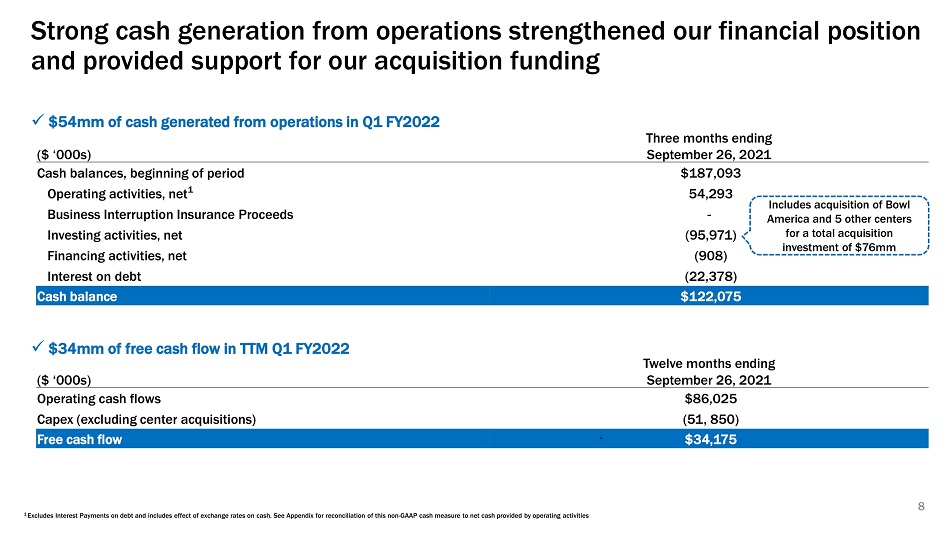

| ● | Balance sheet further strengthened by $54 million of cash generated from operating activities, net over the period. | |

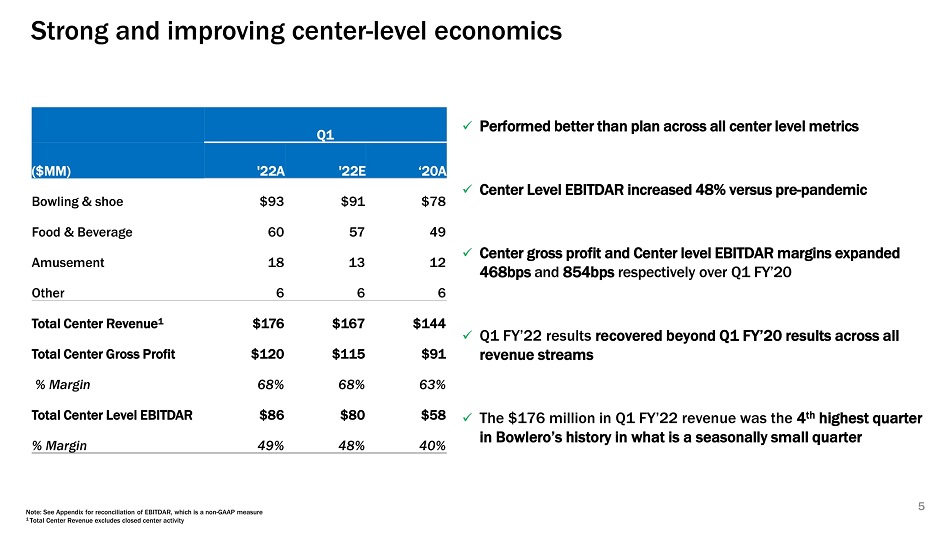

| ● | Total bowling center revenue, gross profit, EBITDAR, and EBITDAR margin outperformed expectations. | |

| ● | Fourth highest revenue quarter in Bowlero’s history, in what is seasonally a lower sales volume quarter. |

RICHMOND, VA – November 15, 2021 – Bowlero Corp (“Bowlero”), the world’s largest owner and operator of bowling centers and owner of the Professional Bowlers Association (“PBA”), today announced that it had outperformed Q1 2022 fiscal year expectations for the quarter ended September 30, 2021 and posted material growth compared to the pre-pandemic levels. Bowlero achieved its fourth best quarter ever, as measured by total center revenue, in what is seasonally a lower sales volume quarter. This follows Bowlero significantly outperforming expectations for fiscal year 2021, which ended June 26, 2021.

Leisure revenue, which accounts for the bulk of revenue, rose 22% from pre-pandemic levels. Bowlero generated $25 million in Net Income for the quarter ended September 30, 2021, compared to a $20 million loss for the most recent, pre-pandemic quarter ended September 29, 2019. Adjusted EBITDA rose 140% from pre-pandemic levels as operational efficiencies continue to drive significant margin expansion. $54 million of cash was generated during the period. Bowling center level EBITDAR increased 48% from pre-pandemic levels.

In July, Bowlero announced plans to list on the NYSE through a merger with Isos Acquisition Corporation (NYSE: ISOS.U, “Isos”). Upon the closing of the transaction with Isos, Bowlero’s common stock and warrants are expected to trade on NYSE under the new ticker symbols “BOWL” and “BOWL WS”.

“Our performance speaks to our ability to drive significant revenue and improve our margins through increasing operational efficiency across all of our bowling centers. As league and event businesses continue to recover, we are well-positioned to continue to perform strongly in those areas as well, both in terms of revenue and EBITDAR,” said Tom Shannon, Founder, Chairman and Chief Executive Officer.

Bowling center revenue in the quarter ended September 30, 2021 was $176 million and EBITDAR (Adjusted EBITDA + Rent) was $86 million, compared with expected revenue of $167 million and expected EBITDAR of $80 million. Adjusted EBITDA for the first quarter of fiscal year 2022 was $59 million, up 140% from the comparable pre-pandemic quarter, driven by materially improved revenues and margin expansion resulting from increased operational efficiencies. Adjusted EBITDA reflects certain items that are added to EBITDA as defined in Isos’ registration statement filed on Form S-4 with the U.S. Securities and Exchange Commission (the “SEC”).

Bowlero performed better than guided across nearly all center level metrics and results in the first quarter of fiscal year 2022. Bowlero outperformed revenue and Adjusted EBITDA guidance by $8.7million (5.2%) and $5.2 million (9.7%), respectively.

“Our rapid recovery from the Covid-19 pandemic disruption has continued into the first quarter of fiscal year 2022, as evidenced by our more than 140% increase in Adjusted EBITDA compared to numbers of the same quarter, pre-pandemic, and outperforming guidance for the second consecutive quarter,” said Brett Parker, President and Chief Financial Officer. “Strong cash generation from our operations over the quarter has further strengthened our financial position and provided support for our acquisition funding.”

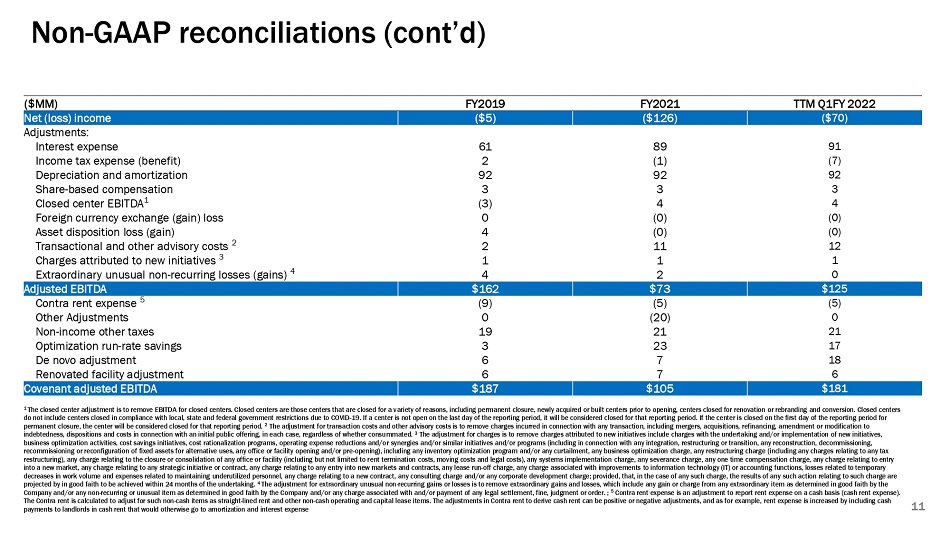

This press release contains references to Adjusted EBITDA and adjusted cash flow from operations, each of which measures are not based on accounting principles generally accepted in the United States, or non-GAAP financial measures. These non-GAAP financial measures are in addition to, not a substitute for or superior to, measures of financial performance prepared in accordance with GAAP. The non-GAAP financial measures used by the Company may differ from the non-GAAP financial measures used by other companies. Refer to the Appendix section of the earnings presentation for definitions of these terms and reconciliations to the most comparable GAAP measures.

Investor Webcast Information

Listeners may access an investor webcast hosted by Bowlero. The webcast and results presentation are accessible in the Investor Relations section of the Isos website at www.isosacquisitioncorp.com/investor-relations.

About Bowlero Corp

Bowlero Corp is the worldwide leader in bowling entertainment, media, and events. With more than 300 bowling centers across North America, Bowlero Corp serves more than 26 million guests each year through a family of brands that includes Bowlero, Bowlmor Lanes, and AMF. In 2019, Bowlero Corp acquired the Professional Bowlers Association, the major league of bowling, which boasts thousands of members and millions of fans across the globe. For more information on Bowlero Corp, please visit BowleroCorp.com.

About Isos Acquisition Corporation

Isos Acquisition Corporation (NYSE: ISOS.U) is a blank check company formed for the purpose of effecting a merger, share exchange, asset acquisition, share purchase, reorganization or similar business combination with one or more businesses. The Company is led by Co-Chief Executive Officers George Barrios and Michelle Wilson. For more information on Isos Acquisition Corporation, please visit www.isosacquisitioncorp.com.

2

Forward Looking Statements

Some of the statements contained in this press release are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. These forward-looking statements are generally identified by the use of words such as “anticipate,” “believe,” “could,” “estimate,” “expect,” “intend,” “may,” “plan,” “potential,” “predict,” “project,” “should,” “target,” “will,” “would” and, in each case, their negative or other various or comparable terminology. These forward-looking statements reflect our views with respect to future events as of the date of this release and are based on our management’s current expectations, estimates, forecasts, projections, assumptions, beliefs and information. Although management believes that the expectations reflected in these forward-looking statements are reasonable, it can give no assurance that these expectations will prove to have been correct. All such forward-looking statements are subject to risks and uncertainties, many of which are outside of our control, and could cause future events or results to be materially different from those stated or implied in this document. It is not possible to predict or identify all such risks. These risks include, but are not limited to: the occurrence of any event, change or other circumstances that could give rise to the termination of the business combination; the outcome of any legal proceedings that may be instituted against ISOS, Bowlero or others following announcement of the business combination and the transactions contemplated therein; the inability to complete the transactions contemplated by the business combination due to the failure to obtain approval of the shareholders of Isos or Bowlero or other conditions to closing in the business combination agreement; the risk that the proposed business combination disrupts current plans and operations as a result of the announcement and consummation of the business combination; the ability to recognize the anticipated benefits of the business combination, which may be affected by, among other things, the ability of Bowlero to grow and manage growth profitably, maintain relationships with customers, compete within its industry and retain its key employees; costs related to the proposed business combination; the possibility that Isos or Bowlero may be adversely impacted by other economic, business, and/or competitive factors; the risk that the market for Bowlero’s entertainment offerings may not develop on the timeframe or in the manner that Bowlero currently anticipates; general economic conditions and uncertainties affecting markets in which Bowlero or operates and economic volatility that could adversely impact its business, including the COVID-19 pandemic; the ability of Bowlero to attract new customers and retain existing customers; changes in consumer preferences and buying patterns; inability to compete successfully against current and future competitors in the highly competitive out-of-home and home-based entertainment markets; inability to operate venues, or obtain and maintain licenses and permits necessary for such operation, in compliance with laws, regulations and other requirements; damage to brand or reputation; its ability to successfully defend litigation brought against it; its ability to adequately obtain, maintain, protect and enforce our intellectual property and proprietary rights and claims of intellectual property and proprietary right infringement, misappropriation or other violation by competitors and third parties; failure to hire and retain qualified employees and personnel; fluctuations in Bowlero’s operating results; security breaches, cyber-attacks and other interruptions to its and its third-party service providers’ technological and physical infrastructures; catastrophic events, including war, terrorism and other international conflicts, adverse weather conditions, public health issues or natural catastrophes and accidents; risk of increased regulation of its operations; the projected financial information, anticipated growth rate, and market opportunity of Bowlero; the ability to obtain or maintain the listing of new Bowlero’s Class A common stock and warrants on the NYSE following the completion of the business combination; Isos’s and Bowlero’s public securities’ potential liquidity and trading; future capital needs of Bowlero following the completion of the business combination; the significant uncertainty created by the COVID-19 pandemic and the negative impact of the COVID-19 pandemic on Bowlero; and factors described under the section titled “Risk Factors” in the registration statement on Form S-4 filed with the SEC relating to a potential business combination between Isos and Bowlero, as well as other filings that Bowlero will make with the SEC, such as Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q and Current Reports on Form 8-K. Forward-looking statements speak only as of the date the statements are made. Neither Isos nor Bowlero assume any obligation to update forward-looking statements to reflect actual results, subsequent events or circumstances or other changes affecting forward-looking information except to the extent required by applicable securities laws.

Contacts:

For Media:

ICR, Inc.

Tom Vogel

Tom.Vogel@icrinc.com

For Investors:

ICR, Inc.

Ryan Lawrence

Ryan.Lawrence@icrinc.com

Ashley DeSimone

Ashley.desimone@icrinc.com

3