UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

(Mark One)

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended

OR

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE TRANSITION PERIOD FROM TO |

Commission File Number

(Exact name of Registrant as specified in its Charter)

(State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

(Address of principal executive offices) |

(Zip Code) |

Registrant’s telephone number, including area code: (

Securities registered pursuant to Section 12(b) of the Act:

Title of each class |

|

Trading Symbol(s) |

|

Name of each exchange on which registered |

|

|

|||

|

|

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES ☐

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. YES ☐

Indicate by check mark whether the Registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the Registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer |

|

☐ |

|

Accelerated filer |

|

☐ |

|

☒ |

|

Smaller reporting company |

|

||

|

|

|

|

Emerging growth company |

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). YES ☐ NO

The aggregate market value of the voting and non-voting common equity held by non-affiliates of Soaring Eagle Acquisition Corp. (SRNG), our predecessor, on June 30, 2021, based on a closing price of $9.96 for SRNG’s Class A common stock, was approximately $

As of March 17, 2022, there were

Table of Contents

|

|

Page |

|

|

|

Item 1. |

1 |

|

Item 1A. |

51 |

|

Item 1B. |

90 |

|

Item 2. |

90 |

|

Item 3. |

90 |

|

Item 4. |

90 |

|

|

|

|

|

|

|

Item 5. |

91 |

|

Item 6. |

92 |

|

Item 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

93 |

Item 7A. |

112 |

|

Item 8. |

112 |

|

Item 9. |

Changes in and Disagreements With Accountants on Accounting and Financial Disclosure |

112 |

Item 9A. |

112 |

|

Item 9B. |

113 |

|

Item 9C. |

Disclosure Regarding Foreign Jurisdictions that Prevent Inspections |

113 |

|

|

|

|

|

|

Item 10. |

114 |

|

Item 11. |

118 |

|

Item 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

123 |

Item 13. |

Certain Relationships and Related Transactions, and Director Independence |

127 |

Item 14. |

132 |

|

|

|

|

|

|

|

Item 15. |

133 |

|

Item 16. |

137 |

Cautionary Note Regarding Forward Looking Statements

This report includes forward-looking statements regarding, among other things, the plans, strategies and prospects, both business and financial, of Ginkgo. These statements are based on the beliefs and assumptions of the management of Ginkgo. Although Ginkgo believes that its plans, intentions and expectations reflected in or suggested by these forward-looking statements are reasonable, Ginkgo cannot assure you that it will achieve or realize these plans, intentions or expectations. Forward-looking statements are inherently subject to risks, uncertainties and assumptions. Generally, statements that are not historical facts, including statements concerning possible or assumed future actions, business strategies, events or results of operations, are forward-looking statements. These statements may be preceded by, followed by or include the words “believes”, “estimates”, “expects”, “projects”, “forecasts”, “may”, “will”, “should”, “seeks”, “plans”, “scheduled”, “anticipates” or “intends” or similar expressions. Forward-looking statements contained in this annual report on Form 10-K (“Annual Report”) include, but are not limited to, statements about:

These and other factors that could cause actual results to differ from those implied by the forward-looking statements in this Annual Report are more fully described under the heading “Risk Factors” and elsewhere in this report. The risks described under the heading “Risk Factors” are not exhaustive. Other sections of this Annual Report describe additional factors that could adversely affect the business, financial condition or results of Ginkgo. New risk factors emerge from time to time and it is not possible to predict all such risk factors, nor can Ginkgo assess the impact of all such risk factors on the business of Ginkgo, or the extent to which any factor or combination of factors may cause actual results to differ materially from those contained in any forward-looking statements. Forward-looking statements are not guarantees of performance. You should not put undue reliance on these statements, which speak only as of the date hereof. All forward-looking statements attributable to Ginkgo or persons acting on its behalf are expressly qualified in their entirety by the foregoing cautionary statements. Ginkgo undertakes no obligation to update or revise publicly any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law.

Risk Factors Summary

Investing in our securities involves risks. You should carefully consider the risks described in “Risk Factors” beginning on page 51 before making a decision to invest in our Class A common stock. If any of these risks actually occur, our business,

i

financial condition and results of operations would likely be materially adversely affected. Some of the risks related to Ginkgo’s business and industry are summarized below. References in the summary below to “we,” “us,” “our” and “the Company” generally refer to Ginkgo.

ii

iii

PART I

Item 1. Business.

Unless the context otherwise requires, all references in this section to the “Company,” “Ginkgo,” “we,” “us,” or “our” refer to the business of Ginkgo Bioworks Holdings, Inc. and its subsidiaries.

Mission

Our mission is to make biology easier to engineer. That has never changed. Every choice we’ve made with respect to our business model, our platform, our people and our culture is grounded in whether it will advance our mission. Biology inherently offers incredible capabilities that we can only imagine in human-made technologies—self-assembly, self-repair, self-replication—capabilities that can enable more renewable and innovative approaches for nearly every industry. To realize this potential, we are building a platform for cell programming by bringing together unparalleled scale, software, automation, data science and reusable biological knowledge, enabling responsible solutions for the next generation of foods, pharmaceuticals, materials and more.

Overview

Ginkgo is building the industry-standard horizontal platform for cell programming. Our founders are engineers from diverse fields who, more than 20 years ago, were inspired by an astonishing feature of biology: it runs on digital code. It’s just A, T, C, and G rather than 0 and 1. But where computer bits are used to communicate information, genetic code is inherently physical and as it is read, physical structures are made. We program computers to manipulate bits, but we program cells to manipulate atoms. Cells are the building blocks of our food, our environment and even ourselves.

We use our platform to program cells on behalf of our customers. These “cell programs” (or “programs”) are designed to enable biological production of products as diverse as novel therapeutics, key food ingredients, and chemicals currently derived from petroleum. Through 2021, we have worked on 105 Cumulative Programs, which represent the cumulative number of unique programs Ginkgo has commenced in end markets as diverse as specialty chemicals, agriculture, food, consumer products, and pharmaceuticals. Biology did not evolve by end market. All of these applications run on cells which have a common code—DNA—and a common programming platform can enable all of them. Because of this shared platform, we are able to drive scale and learning efficiencies while maintaining flexibility and diversity in our program areas. Ultimately, customers come to us because they believe we maximize the probability of successfully developing their products.

Customers look to Ginkgo to overhaul their manufacturing processes or develop new products through biology. They might, for example, be looking to produce a particular chemical via fermentation, at a lower cost, with enhanced supply chain reliability or sustainability. Or perhaps the customer needs a microbe that will live and grow on the roots of corn and convert nitrogen in the air into usable fertilizer for a plant, resulting in improved plant growth. Or a customer might need an antibody that binds to and neutralizes a certain target, along with a way to produce those antibodies at scale. All of these programs and more run on a common platform at Ginkgo.

We care deeply how our platform is used and recognize biosecurity as a necessary complement to our cell programming work. Biosecurity is ingrained in our platform and in our ethos—we work collaboratively to help ensure responsible research conduct and deployment within our own work and within the broader synthetic biology community. We have additionally invested in developing targeted biosecurity and public health capabilities, including an initiative for pathogen biomonitoring at scale. Through this initiative, known as Concentric by Ginkgo, we serve as a system integrator to implement customizable and accessible biosecurity programs for monitoring and mitigating the spread of COVID-19 in thousands of communities across the country. We are dedicated to setting the industry standard for biosecurity as we continue to scale our platform.

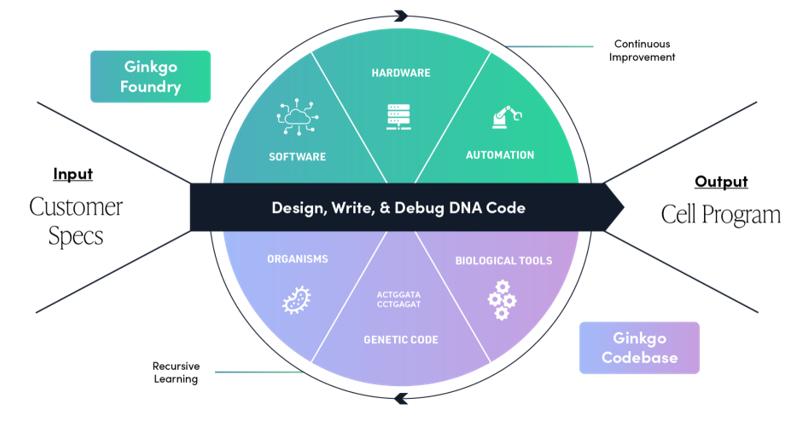

The foundation of our platform includes two core assets that execute a wide variety of cell programs for customers according to their specifications: our Foundry and our Codebase.

1

Figure 1: Our platform is used to design, write, and debug DNA code in engineered organisms to execute programs for our customers. Our Foundry leverages proprietary software, automation, and data analytics to reduce the cost of cell programming. Our Codebase consists of reusable biological assets that helps accelerate the engineering process.

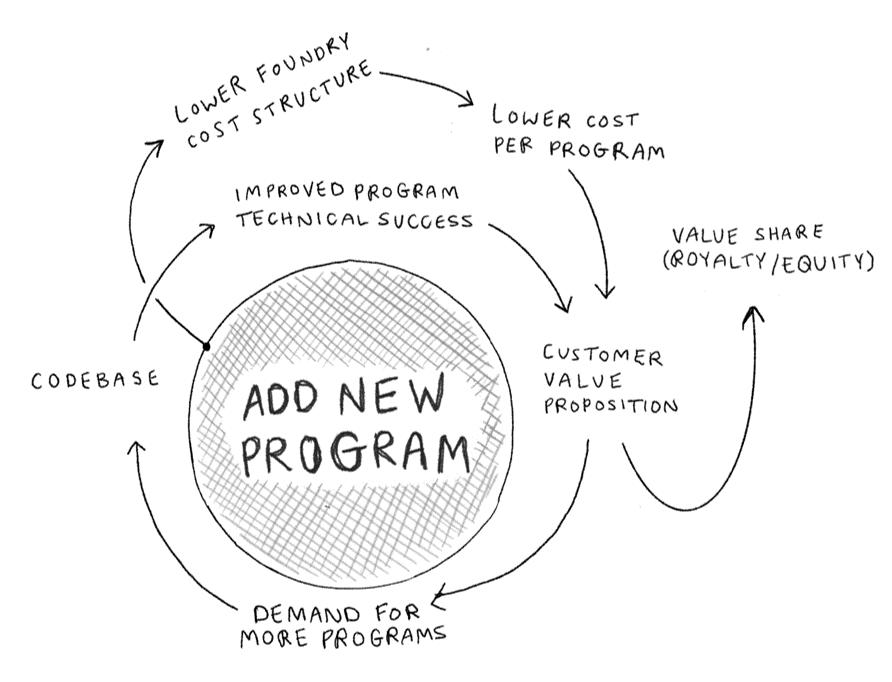

As the platform scales, we have observed a virtuous cycle between our Foundry, our Codebase, and the value we deliver to customers. Sketched below, we believe this virtuous cycle sustains Ginkgo’s growth and differentiated value proposition.

Put simply: we believe that as the platform improves with scale, it drives more scale, which drives further platform improvements, and so on. We believe this positive feedback loop has the potential to drive compounding value creation in the future, as every new program we add contributes to both near-term revenues and has the potential to add significant downstream economics.

2

Figure 2: Ginkgo’s virtuous cycle: as we scale, we see greater efficiency and higher odds of technical success, which helps drive further scaling as our value proposition improves.

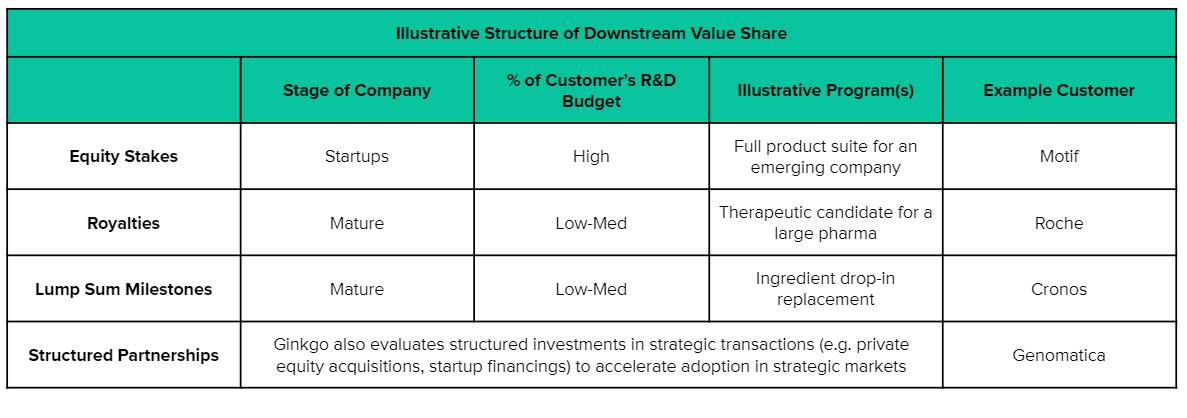

Our business model mirrors the structure of our platform and we are compensated in two primary ways. First, we charge usage fees for Foundry services, in much the same way that cloud computing companies charge usage fees for utilization of computing capacity or contract research organizations (“CROs”) charge for services. The total addressable market for biological research and development (“R&D”) services, including labor and tools, was estimated to be over $40 billion in 2021 and is growing strongly. Additionally, we negotiate a value share with our customers (typically in the form of royalties, milestones, and/or equity interests) in order to align our economics with the success of the programs enabled by our platform. As we add new programs, our portfolio of programs with this “downstream” value potential grows. Through these value shares, we are tapping into what industry sources expect to be a $2 to $4 trillion market for bioengineered products in the next 10 to 20 years.

We believe that cell programming has the potential to be as ubiquitous in the physical world as computer programming has become in the digital world. We believe products in the future will be grown rather than made. To enable that vision, we are building a horizontal platform to make biology easier to engineer. Our business model is aligned with this strategy and with the success of our customers, setting us on what we believe is a path towards sustainable innovation for years to come.

An Introduction to Synthetic Biology

To fully tell the story of cell programming, we have to start four billion years ago. All living things evolved from a single cell, a tiny bubble containing the code that enabled it to assemble and reproduce itself. But, importantly, that process of reproduction wasn’t perfect; each copy introduced new mutations in the code. These changes are responsible for one of the most powerful and defining features of biology: evolution. Over eons, that first cell and all its progeny copied themselves, and their DNA evolved to create new functions: to eat new kinds of foods and to produce new kinds of chemicals, structures, and behaviors. As reproduction became more, well, interactive, organisms developed tools to borrow DNA from each other, accelerating the pace of evolution. These functions, and thus the genetic code programming the functions, stuck around when they helped the organisms survive and create more descendants. This went on and on for four billion years, leaving us the wild codebase of DNA that enables the diversity of life forms we see on the planet today.

3

Synthetic biology’s story begins mere decades ago, as biologists began to decode the molecular secrets of DNA. The billions-year-old tools of cells—enzymes that cut, copy, and paste sequences of DNA code—are now being leveraged by humans to read, write, and edit DNA in the lab. Polymerases that copy DNA are used to enable polymerase chain reaction (“PCR”) tests for COVID-19 and the CRISPR/Cas system from bacteria now enables editing of human genomes to potentially cure genetic diseases.

Today we are using these tools to learn from the full breadth of evolution and biodiversity to write new biological code. Simple soil bacteria produce everything from vital antibiotics to the smell of fresh rain. We can reuse elements of these DNA programs to make new products. Biochemistry is extraordinarily versatile; we’ve reused the same genetic code libraries across applications as diverse as fine fragrances, baking, and consumer electronics. We may be able to develop programs that can digest human-made “forever chemicals” that biology never encountered before.

As cell programmers, we operate with humility and respect for biology. Our tools are simply borrowed, and the history of biotechnology is a mere blink of an eye compared to the history of living things. Today, we write rudimentary code. We believe that someday our children will write poetry in DNA.

Programming life

Figure 3: DNA strands are sequences composed of four chemical bases, or nucleotides, represented by the letters A, T, C and G.

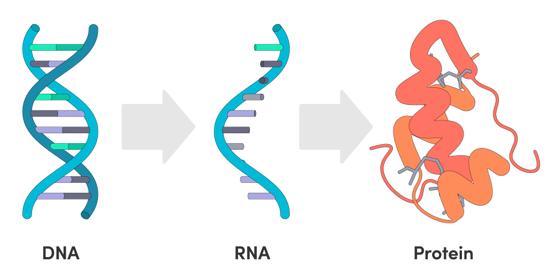

Like computers, cells run on digital code. DNA strands are sequences composed of four chemical bases, or nucleotides, represented by the letters A, T, C and G. The letters along the strand encode the proteins that make up the cell and perform biochemical functions. The translation of DNA to RNA to Protein is known as the “central dogma” of molecular biology.

The Central Dogma of Molecular Biology

Figure 4: The translation of DNA to RNA to Protein is known as the “central dogma” of molecular biology.

“Traditional” genetic engineering uses special types of proteins from bacteria that can cut and paste DNA to move sequences from one organism to another. In 1982, Genentech Inc. partnered with Eli Lilly and Company to bring these techniques to market, producing human insulin inside the bacteria E. coli. Genetic engineers were able to cut the code for the human insulin protein and paste it into the genome of E. coli and “boot up” the sequence: the bacteria could now produce the human protein, which could then be extracted, purified, and used by diabetics. This life-saving development replaced a vastly more expensive and supply-constrained method of extracting insulin from animal pancreases.

4

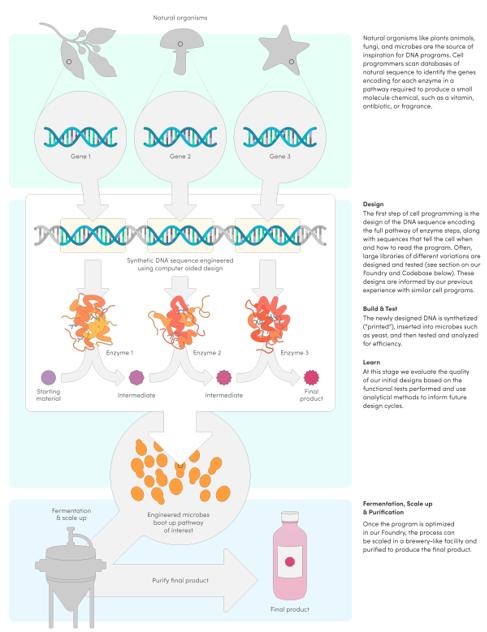

Relatively simple proteins like insulin can be produced by transferring one gene sequence into a simple microorganism. Many other biochemicals require much more complex cell programming and are produced by a series of special proteins, called enzymes, working together. These enzymes transform a starting material, or “feedstock,” such as sugar, into a final product, such as an antibiotic, vitamin, or other valuable small molecule. In this way, biology also programs chemistry. Cell programmers can design such multi-enzyme “pathways” and transfer them into a cell to boot up. For example, the cell programs we’re writing for Cronos Group, Inc. to produce cannabinoids require many different enzymes to convert feedstock into cannabinoids such as cannabidiol.

Once the cell is programmed to produce a new molecule, it can produce the molecule and also replicate itself, creating an exponentially growing number of product-producing cells. Many products of genetic engineering are manufactured in facilities that look like breweries, taking advantage of the centuries old process of industrial fermentation to grow cells at high density, and transforming simple sugars into valuable products that can be extracted and commercialized.

Improved tools for cell programming, including automation, miniaturization, and data science, alongside the decreasing cost of DNA synthesis—writing DNA—are opening up new possibilities for cell programming. For each new program, Ginkgo’s organism engineers design, print, and test hundreds or thousands of different sequences for each step of a pathway, exploring the breadth of biological design space and improving the probability of success. We provide more details about our platform in the sections that follow.

5

Figure 5: An overview of a simple cell program.

The Impact of Cell Programming

The power of biology has never been more apparent. Synthetic biology was featured on the cover of The Economist in April of 2019. A few years later, billions of doses of a novel type of vaccine have been distributed, created by companies such as Pfizer and Moderna and made up of a form of biological code, mRNA. Our own cells read that code to produce viral proteins and stimulate our immune response to fight back against the SARS-CoV-2 virus. We no longer question if biotechnology will transform a given industry, we simply question whether we are creative enough to imagine how, and whether we are ready to utilize biology responsibly.

ESG is in our DNA

Biology affects all of us, and we believe cell programming will change the world. Our customers are developing products with far reaching implications in health and the environment. This potential for extraordinary impact, which reaches to the core of who we are and everything about our natural world, requires extraordinary care in how the tools of cell programming

6

are built and used. Technologies reflect the values of the organizations that build them, so our commitment to Environmental, Social, and Governance (“ESG”) priorities and care must underscore everything we do.

We also must recognize that biotechnologies have not always reflected the values necessary for sustainable and equitable impact and, as a result, remain controversial. Indeed, companies that produce genetically modified organisms (“GMOs”) for human consumption are restricted from certain ESG indices, placing genetic engineering as a major ESG risk alongside the production of weapons, tobacco products, and fossil fuels. We hope to chart a new course built on care so that the world can benefit from the power of biological engineering while avoiding potential risks.

Environmental

We face an urgent environmental crisis that is forcing us to reconsider how we make everything, from our homes, to our food, to our clothing. For centuries, we’ve treated nature as an infinite resource and infinite trash can, extracting raw materials, shaping them through industrial processes that spew out greenhouse gases, and then throwing them away. But these resources are not infinite and there is no “away.” The results have been disastrous—climate change, loss of biodiversity, and pollution have impacted every corner of our world and continue to threaten our way of life.

Cell programming and biological manufacturing are working to address some of the issues that are most contributing to climate change today, from fossil fuel dependency to agricultural emissions, and land use to plastic pollution. Ultimately, biology offers a fundamental shift in how things are made and disposed of: a world where things grow and decay, creating circular, regenerative processes.

There is significant concern that genetic engineering itself creates a form of genetic “pollution” in the environment, with genes from one context introduced into another. This is a concern we take seriously and consider deeply throughout the lifecycle of our programs to ensure that genes introduced will not cause damage—for example, by spreading antibiotic resistance or toxins. We care because the environmental release of certain genetically engineered microbes can also offer tremendous environmental benefit. For example:

And we are just getting started… we believe biology is our best tool to reverse the damage to our planet and chart us on a path towards sustainability in the future.

Social

Technology isn’t neutral. Our values and biases are embedded in the technologies we make, in the applications we consider, and in the ways we address problems. Inclusion of those who have historically been left out of the development of new technologies is essential to building equitable and positive outcomes. Just as biological ecosystems thrive with more diversity, the inclusion of many different voices is essential to growing our company and to ensuring that the viewpoints of historically marginalized people are included in the development of our platform. We have many active efforts in recruiting and retaining diverse talent and will continue to invest in this work (see “—Our People & Culture”).

Marginalized people who have been left out of the development of technologies are also the groups most likely to bear the greatest harm, whether from climate change, pollution, or health disparities. The COVID-19 pandemic has made this inequality starkly clear—in the United States, it has been communities of color that have been disproportionately impacted by the pandemic and have had the least access to testing, treatment, and vaccination.

In March of 2020, we committed to $25 million of pro bono work to help accelerate novel diagnostics, therapeutics, and vaccines to help fight COVID-19. Our early work included efforts to improve the manufacturing of vaccines, with a goal to lower costs and increase accessibility of vaccines worldwide. Shortly thereafter, we launched Concentric by Ginkgo, a service to provide public health testing infrastructure for communities. Our pooled testing service was designed with accessibility and privacy as core design principles, to bring low-cost, easy-to-use testing to K-12 schools in the places that have been most affected by the pandemic. We partnered with school districts such as Baltimore City Public Schools to make

7

sure that our program was designed to serve the community and to build trust with groups who have been excluded, exploited and mistreated by biomedical research in the past.

These values and initiatives are not just a top-down corporate policy, they are an intrinsic part of our culture. Grassroots fundraising challenges to support local and international aid organizations are a regular feature of our internal messaging channels. One of our software engineers even programmed a free tool, @vaccinetime on Twitter, that helped thousands of Massachusetts residents find vaccine appointments.

Governance

Our culture is built on care, transparency, diversity, employee ownership and engagement, and a deep, humble respect for biology. Transparency is essential to how we operate, to enable sharing of the insights and tools that enable our platform to grow, as well as to build trust and accountability with all of our stakeholders. We have advocated for more transparency in our industry, including supporting GMO labeling, and seek to educate policymakers and the general public about the benefits and risks of synthetic biology through our advocacy efforts.

The individuals who work at Ginkgo and build our platform care deeply about how that platform is used and the impact our company will have in the world. We believe a workforce with strong equity ownership will make the wise decisions needed to build long-term value for our company, and a company whose long-term impacts make them proud. That is why we have implemented a multi-class stock structure that permits all employees (current and future), not just founders, to hold high-vote (10 votes per share) common stock. We believe that our multi-class stock structure will help maintain the long-term mentality we have benefited from as a founder-led company.

For more information, see “Risk Factors—Risks Relating to our Organizational Structure and Governance—Only our employees and directors are entitled to hold shares of Ginkgo Class B common stock (including shares of our Class B common stock granted or otherwise issued to our employees and directors in the future), which shares have 10 votes per share. This limits or precludes other stockholders’ ability to influence the outcome of matters submitted to stockholders for approval, including the election of directors, the approval of certain employee compensation plans, the adoption of amendments to our organizational documents and the approval of any merger, consolidation, sale of all or substantially all of our assets, or other major corporate transaction requiring stockholder approval.”

We have selected directors with decades of experience serving as leaders in the life sciences and technology industries. Our board of directors and management team will leverage that experience and consider the interests of stockholders, customers, employees, suppliers, academic researchers, governments, communities, and other stakeholders to pursue long-term value for our company and drive the sustained health of our global community. For more information, see “Risk Factors—Risks Relating to our Organizational Structure and Governance—Our focus on the long-term best interests of our company and our consideration of all of our stakeholders, including our stockholders, workforce, customers, suppliers, academic researchers, governments, communities and other stakeholders that we may identify from time to time, may conflict with short-term or medium-term financial interests and business performance, which may adversely impact the value of our common stock.”

Cell programming is expected to transform all industries

Biology grows. Biology adapts and evolves. Biology heals itself and regenerates. Biology is also, remarkably, programmable, offering us the tools to work with biology to transform how we make stuff. With cell programming, we help our customers across industries grow better products. What does “better” mean? Better products might be more sustainable, have more stable and resilient supply chains, be more accessible, have higher quality and more consistency, and come with lower economic and environmental costs of manufacturing. They can also be truly transformative, fundamentally changing the field of possibilities for what products can do. We have supported many companies that are leveraging our cell programming platform to address some of the world’s most challenging environmental and social issues.

Pharma & Biotech

Biopharma has been a nexus of tremendous innovation in cell programming and synthetic biology. Just in the past year, we have seen the creation and broad adoption of a novel form of biological prophylactic in the form of nucleic acid vaccines. These vaccines contain genetic code that our bodies read to produce viral proteins and stimulate an immune response and antibody production. New nucleic acid vaccines can be programmed quickly, such as the booster vaccines being developed against emerging SARS-CoV-2 variants, offering the potential for rapid response to other future pathogens. They can also be programmed to target a number of other diseases. In the wake of the success of nucleic acid vaccines during the COVID-19 pandemic, new programs for HIV and cancer vaccines, among others, are accelerating.

8

Biologic medicines like insulin and other protein drugs and antibodies are also produced via cell programming, making a difference in the treatment of countless diseases. Over 20% of the therapies approved by the U.S. Food and Drug Administration (“FDA”) in 2021 were biologics. In addition, new modalities enabled by cell programming, such as cell and gene therapies, microbiome therapies, and regenerative medicines, are beginning to come online. We believe human health and the ways we treat disease will be transformed by improvements in cell programming technology.

Ginkgo has been active in this field in recent years and we expect to significantly expand our support of therapeutic applications over coming years. From companies developing “living medicines” (Synlogic, Inc. (“Synlogic”)) to those involved in COVID-19 vaccine production (Moderna and others) to those developing novel antibiotics (Roche), we are using our platform to deliver transformational innovations across a range of disease areas.

Industrials & Environment

Since the industrial revolution, manufacturing techniques have been extractive, wasteful, and unsustainable. Not only must we innovate new manufacturing methods in order to keep up with growing demand, we must also work to remediate issues we have caused historically, by cleaning up our environment and addressing climate change.

Ginkgo is not only working with customers to create cell programs that enable cost-efficient, renewable, and sustainable production of chemicals and materials, such as our work with Genomatica, Inc. (“Genomatica”), but we have also participated in the formation of Allonnia, a company focused on environmental remediation. Plastic waste and many of the pollutants that plague industrial manufacturing and extraction sites are novel in the course of evolutionary history, so biology has not yet evolved to degrade them efficiently. Cell programming can enable the discovery and development of new enzymes capable of degrading recalcitrant pollutants and recycling waste while entirely reimagining manufacturing for the future.

Food & Agriculture

Food is inherently biological: it comes from life and sustains life. Cell programming can be leveraged to improve the availability of essential food and nutrition to a growing population, decrease the environmental impact and cost of food production, and provide consumers with increased choice.

We are working with some of the largest multinational agriculture companies, including Bayer (through our joint venture, Joyn Bio) and Corteva, to develop cell programs that would make crop production more efficient and sustainable, reducing synthetic nitrogen fertilizer and pesticide usage. In food, we have been active in flavors and sweeteners, and we are the principal cell programming platform for Motif FoodWorks, Inc. (“Motif”), a company that is making animal proteins without the need for industrial farming of animals, which launched its first product, HEMAMI™, in 2021.

Consumer & Technology

Most physical goods have biological origins—from the petrochemicals in our fabrics to fine chemicals extracted from plants—but industry does not necessarily leverage biology, or leverage biology efficiently, to produce these items. Petrochemicals, for example, are used in everything from our fabrics to our cosmetics to our paints. These chemicals and polymers are generally created in complex chemical and physical reactions from crude oil, but crude oil is just the result of millions of years of decomposition of previously living matter (they are fossil fuels after all). These biological building blocks can instead be programmed in a living organism to produce these items sustainably, without extracting natural resources. Even in areas where industry does leverage biology, such as extracting raw materials or fine chemicals from plants, we believe the current approaches are woefully inefficient or rife with social consequences.

We have helped some of the world’s largest fragrance companies such as Givaudan use fermentation to much more efficiently produce rare molecules typically extracted from plants. In a related field, we are also supporting Cronos in their effort to biosynthesize cannabinoids, with the goal of reducing cost, improving purity and predictability, and enabling production of rare molecules. We also helped launch a new company in 2021, Arcaea (formerly Kalo Ingredients, LLC), which is focusing on leveraging biology, from proteins to the microbiome, to build a suite of innovative and efficacious personal care products.

Market Opportunity

For several decades in the computing industry, software ran entirely in local environments: companies built and ran their own servers and customized their applications. The dominance of software-as-a-service (“SaaS”) software and cloud computing over the past decade has demonstrated the value in having common architectures and enabling horizontal platforms. What

9

users may have sacrificed in customizability, they more than gained in innovation, efficiency, and scalability. We believe Ginkgo is ushering in a similar transition in cell programming, a programming discipline with the power to shape living things and grow applications across the physical world.

The value of these applications will measure in the trillions of dollars

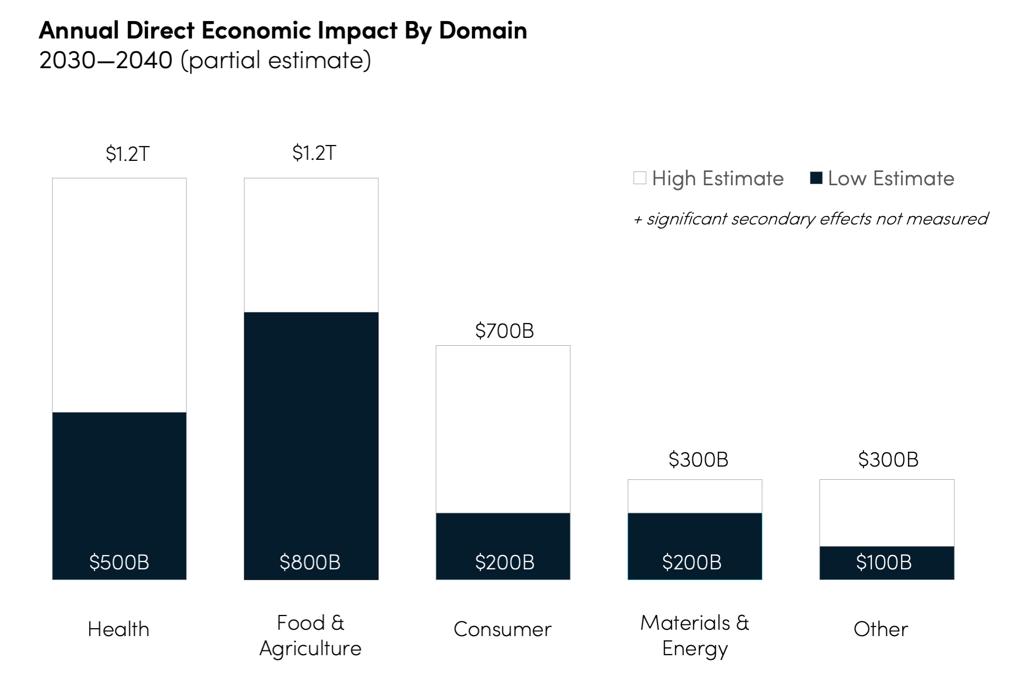

Given the breadth of application areas and the potential of biology (see “—The Impact of Cell Programming”), we believe that the end markets for bioengineered products will be enormous. Industry sources estimate that in the next 10 to 20 years, there will be approximately $2 to $4 trillion of annual direct economic impact from these products, with significant secondary effects. But these applications reflect only what we can already imagine. As we develop a greater ability to program biology and direct it towards novel and more challenging applications, the spectrum of possibilities will undoubtedly grow. Computers were used for little more than counting for decades; we firmly believe the most valuable applications of cell programming are not yet apparent.

Figure 6: Industry sources estimate a $2 to $4 trillion total addressable market for bioengineered products between 2030 and 2040.

Large existing market for “on prem” cell programming research and development

Cell programming today is done in a highly inefficient, distributed manner reminiscent of the early days of computing. Essentially every organization looking to innovate in biology builds its own biology labs in the same way that individual tech companies used to set up their own servers instead of using cloud computing. Scientists spend hours moving liquids around rather than designing novel experiments just as computer programmers once spent most of their time physically writing and debugging code (by punching cards, for example) rather than designing new applications.

Because of the way cell programming is done today, intellectual property that could be useful for multiple applications is tied up by exclusivities that delay the progress of the field overall. Ginkgo’s platform breaks down these silos and democratizes access to the most advanced technologies in the field, enabling customers of all sizes to more efficiently drive innovation.

According to industry sources, the market for cell programming R&D is approximately $40 billion and growing rapidly. This work is being done in a distributed manner, sacrificing benefits from scale and learning economies. Approximately 60% of the spend today is on labor—scientists designing and executing experiments—while the remaining 40% of this is spent on “tools”—things like DNA synthesis, reagents, and equipment. Ginkgo brings efficiencies to both elements of this existing market.

10

As the cost of computing power declined exponentially in computer programming, the demand for computing power increased exponentially as developers dreamed up more and more sophisticated applications. We expect the same to be true in cell programming: as our platform scales in capability and capacity, we hope that the range of applications accessible to cell programming will likewise expand in breadth and sophistication.

Industry Overview

We believe that Ginkgo is changing the structure of the biotechnology industry. In much the same way that cloud computing centralized hosting services and ushered in a wave of SaaS software companies, Ginkgo is scaling the capabilities needed to program cells. By making these tools more accessible, we hope to usher in a wave of innovation in both “hardware” (life science tools) and “software” (cell programs).

At Ginkgo, we have always admired the symbiotic and regenerative nature of biology, which sits in stark contrast to the often extractive nature of existing technologies. We are often asked who we think the “winners” and “losers” in the industry will be as Ginkgo scales, as if it is a given that our growth must come at the expense of others in the ecosystem. We reject that notion. As our platform scales, we seek to drive benefits for all existing players in this ecosystem:

11

Figure 7: Schematic of the synthetic biology industry structure. Ginkgo connects and integrates the hardware and tools provided in the technology layer, creating a platform that can be used by cell programming customers who are building products for end market use.

Program Layer: Ginkgo enables and accelerates product companies, which historically have had to vertically integrate

Ginkgo is not a product company; we are an enabling platform for product companies in a range of end markets. We do not seek to “pick winners” and focus instead on building our platform rather than investing in product-specific risk. Platforms require scale and a relentless focus on innovation while taking a product to market requires many specialized functions that vary depending on the product:

Once the product is developed, major investments are also needed to manufacture, distribute, and market the product. These are the jobs of our customers, the product companies.

12

Historically, product companies have had to invest in their own R&D capabilities, building their own labs and hiring their own scientists. This investment is inefficient due to lack of scale and drains resources away from application testing and product development. Ginkgo’s platform is not application-specific. The same engineering tools can be used for programs in completely different application areas: cells all run on the same genetic code. As product companies develop their products on Ginkgo’s platform, they gain efficiencies and increase their probability of success. New companies that build on our platform never need to make the fixed capital investments to start a lab from scratch; they are able to leapfrog and compete effectively against established companies.

Technology Layer: Ginkgo collaborates with life science tools companies to drive technology advancements

Because we’re constantly thinking about how to enable the next several years of exponential scaling of our platform, we have good insights into future bottlenecks and welcome the opportunity to collaborate to build technologies that will break through those barriers. We are the largest customer for many of our strategic suppliers and, as such, play an important role in advancing new technologies. As a result, we are often able to secure preferred access, often including custom development and leading economic terms, to next-generation technologies and pass those benefits along to customers.

We expect to continue to invest in and support the development of emerging technologies in this space. In certain areas where Ginkgo has unique needs, we may acquire technologies directly, as we did with Gen9, Inc.’s DNA assembly platform, which was particularly valuable for more complex DNA synthesis needs. In many other areas, we will support new and existing technology companies by placing anchor orders and partnering to develop technology roadmaps that break new ground.

By acting as a horizontal platform, Ginkgo can focus on what we do best (cell programming), our customers can focus on what they do best (bringing products to market in their industry), and our suppliers can focus on what they do best (building great hardware and tools). Biology did not evolve by industry and so cell programming is able to benefit from the scale and efficiency of a horizontal platform. Vertical integration is no longer required, allowing each layer of the ecosystem to flourish as we collectively enable more rapid growth across the industry.

Enabling Customer Success

Ginkgo serves diverse customers across a variety of end markets. Some of these customers may have in-house biological R&D teams and others may have never thought biotechnology applied to their business. In either case, they come to us with a challenge—whether it is supply chain volatility, a race to develop an innovative new product, or an existential threat facing an industry on the wrong side of history—and we partner to enable a biological solution. We begin our relationship by working collaboratively to design the set of specifications for the end product(s) our customer desires. Our cell programmers then take that set of specifications and design an engineering plan to create a cell program that meets or exceeds that set of specifications. When we finish, our customers receive the final engineered organism (which either produces or is their product of interest) and a full “tech transfer” package for manufacturing and downstream processing (which they can implement themselves or pass to a contract manufacturer with our support). Our customers then take these organisms and/or purified products through the final stages of product development (e.g., formulations, clinical trials, field trials, etc.).

Our commercial team is organized to both establish new relationships with potential customers (traditional business development) as well as maintain and expand relationships with our existing customers (which we call “alliance management”).

Our business development team has both expertise in relevant industries (Consumer & Technology, Industrial & Environment, Agriculture, Food & Nutrition, Pharma & Biotech and Government & Defense) as well as expertise in our Foundry capabilities and synthetic biology. With this background we are able to identify industry or consumer challenges where biology can serve as a solution. Our categories of customers, independent of industry, include potential customers who have R&D teams with some synthetic biology capabilities where choosing Ginkgo can bring automation, scale, and codebase beyond their own; potential customers who are considering but have not yet built lab-scale capabilities where a partnership with Ginkgo allows them to spend their capital on commercialization efforts; and potential customers who are not yet working in synthetic biology whose industries or products stand to be disrupted by biological solutions. Our business development team, with support from our Codebase and Foundry team members, crafts solutions for each of these types of customers through a strategic discussion of customer needs and fit with Ginkgo capabilities.

To grow existing customers, our alliance management team, through close collaboration on our existing programs, seeks technical and business opportunities for our customers that serve as the basis for consideration of future programs. As our programs demonstrate technical success, our existing customers often bring their next strategic R&D needs to our attention.

13

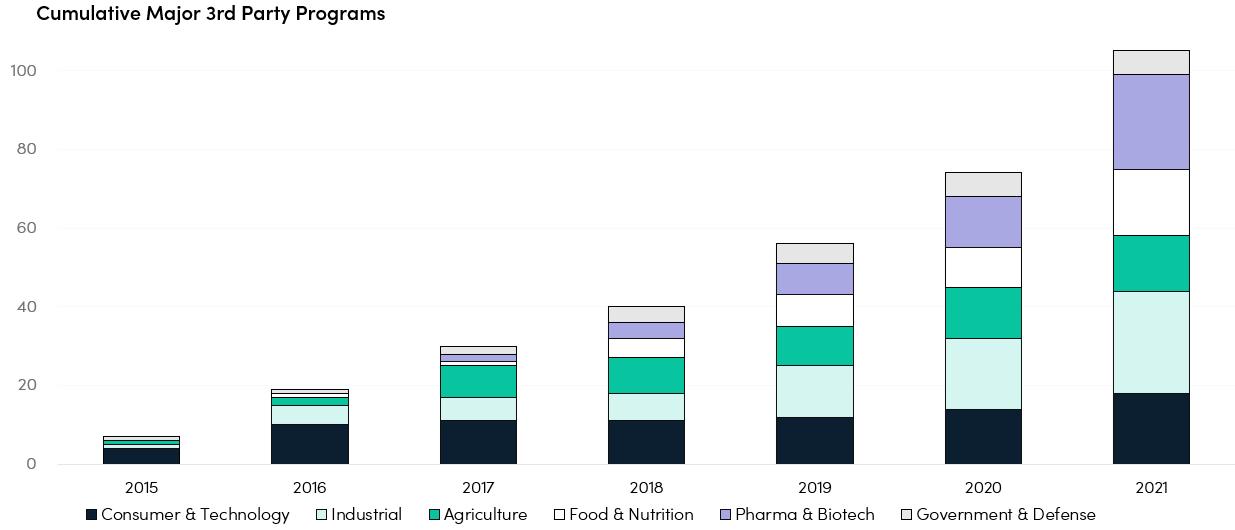

Over 100 Cumulative Programs across diverse industries have run on our platform

While most biotechnology companies focus on building products within a fairly narrow scope, Ginkgo has uniquely pursued a partnered strategy across all end markets. This was not easy. For many years, our platform was less efficient than the status quo of an expert scientist working by-hand at a lab bench. In the early days, the only end markets willing to take a chance on our platform were those without in-house biotechnology capabilities. But as Ginkgo’s platform improved over time and with scale, we were able to win contracts in increasingly sophisticated end markets with more in-house biotechnology expertise. Today, our platform is diversified across all major end markets with marquee customers and a range of focus areas within each.

Figure 8: Cumulative Programs run by third-party customers on Ginkgo’s platform (excluding proof of concept projects and other exploratory work). Today, Ginkgo has a diverse set of programs across all major end markets.

Our customers include large multinational organizations with multibillion dollar R&D budgets as well as startups who are depending on us for essentially all of their bioengineering needs. While these customers and their focus areas may look very different, they are all important and valuable to Ginkgo. All of these programs leverage a common infrastructure, and as we demonstrate the value of this platform, we have the ability to grow significantly with our customers.

Ability to grow with our customers and increasingly complement existing R&D budgets

Ginkgo has grown substantially through inside sales with our existing customers. Some of our customers, such as Motif FoodWorks, never needed to build in-house cell engineering capabilities and so as they grow and expand their product pipeline, we expect their demand for our platform will increase and they will benefit from our improving scale efficiencies over time as well. The relative value of our platform compared to the next best option (building a lab, bioengineering team, and intellectual property from scratch) is immense, which yields extremely high retention rates for customers in this category.

Other customers may already have in-house cell programming capabilities. As Ginkgo demonstrates the value-add of our platform by successfully delivering on programs, we have the opportunity to grow our collaborations with them, complementing their core R&D capabilities. We don’t view this as a “replacement” of customer scientists with Ginkgo’s platform. Rather, we hope to expand our customers’ capacity and need for innovation—giving them more “shots on goal” and enabling them to invest more heavily in R&D as the return on investment of each dollar spent increases.

We have demonstrated this with several customers. With one customer, an initial proof of concept program has turned into a broader strategic relationship with over nine programs today. With another, we launched a relationship with two programs, quickly expanding it to five by the end of the following year. The growth we have seen with our oldest customers means we continue to have significant customer concentration as it takes time for new customers to ramp up their use of Ginkgo’s platform. During 2021, two of our customers each contributed greater than 10% of revenue and collectively they accounted for 28% of total revenue, down from 39% in 2020. We believe customer concentration will decline over time even as we expect to continue to grow our relationships with existing large customers. However, our ability to grow with our customers requires us to maintain satisfied customers, and program or other operational setbacks could impede our ability to meet customer expectations and grow our business.

14

Powerful proof points across categories

Our platform has now been validated by sophisticated customers across a range of industries. As we launch programs in new areas, those provide a toehold for future sales in that space. As an example, our pro bono project for Moderna, Inc. at the start of the COVID-19 pandemic to enhance production of a key raw ingredient through process engineering provided a proof point and initiated us into this emerging segment, leading to a commercial relationship with another nucleic acid vaccine company, as well as a program to produce a key processing enzyme for mRNA vaccines. Similarly, the technical success of programs with Motif FoodWorks, Aldevron, and Cronos Group in 2021 attracted inbound interest from other potential customers.

It is still incredibly challenging to break into new industries and our ability to expand into new sectors may be harder than we expect. However, our recent progress in therapeutics has been a significant milestone given that we are ultimately competing against very strong in-house capabilities. We believe that as more proof points emerge across industries, the barriers to adoption will diminish.

Our Platform

Ginkgo’s platform combines a strong technical foundation with an ecosystem of supporting resources to maximize our partners’ odds of technical and commercial success. In the nucleus of our platform are our Foundry and Codebase, which our scientists leverage to complete customer programs. The Foundry is, in its simplest form, a very large, highly efficient biology lab, enabled by over a decade of investment in proprietary workflows, custom software, robotic automation, and data science and analytics. It is paired with our Codebase, a collection of biological “parts” and a database of biological data, which helps our scientists program cells. But great technology alone is not enough, and we are building a community and ecosystem around our technical platform that provides our partners with end-to-end support.

Our Foundry brings economies of scale to cell programming

Cell programming projects involve a conceptually similar engineering cycle regardless of the specific product or market. Based on customer specifications, Ginkgo’s program team develops designs of proteins, pathways and gene networks (see Figure 5) that might meet the specification, leveraging public and proprietary biological knowledge bases (see “—Our Codebase—organizing the world’s biological code”). Those conceptual designs are developed using computer-aided design tools until the exact DNA sequences for those designs have been determined. Those DNA sequences are then “printed,” assembled and inserted into a cell to execute the new DNA code. These prototype cells are then studied and the output or performance of each is measured and compared to the customer’s desired specification. Learnings using data analytics and data science tools inform a new round of prototypes and this cycle is repeated until either the specification has been met or the customer decides to end the program.

The likelihood of technical success increases with each iterative engineering cycle and with the number of prototypes that are explored per cycle. However, with traditional tools for genetic engineering, each of these cycles can be slow, expensive and error prone. Many projects across the industry run out of budget or time. Conventional R&D teams often look to stay within budget by running rapid engineering cycles using largely manual tools and small numbers of prototypes per cycle. However, the inability to broadly explore the potential design space (there are more possible sequences of a 200 amino acid protein encoded in 600 DNA letters than there are stars in the observable universe) and the reliance on manual tools is a difficult handicap to overcome. Since people can only work so hard and since engineering cycles can’t be shortened beyond the duration of the physical steps, this approach has limited potential to improve in the future.

At Ginkgo, we invest in improving the tools and technology for programming cells in order to maximize program success within the constraints of customer timelines and budgets. We do so by scaling the number of prototypes that can be evaluated in each engineering cycle in an effort to reduce the number of cycles required to meet the customer’s specification and ultimately shorten project timelines. A typical screen for one enzyme step in a program might evaluate 1,000 to 2,000 variants to optimize function, of which the top 10 to 100 might be short-listed for further study. A relatively basic program might have 3 to 5 enzymes working in concert, and so in the process of optimizing the entire pathway, thousands or tens of thousands of enzymes and pathway combinations might be designed, built, and tested in the Foundry. The methods we use to increase scale also tend to reduce the average cost per prototype, which means that more prototypes can be evaluated for a given program budget.

Because diverse cell programs share similarities in process and code, many programs can be run simultaneously in a carefully designed centralized facility. This facility, where we use our investments in advanced cell programming technologies to manage diverse programs, is what we call our Foundry.

15

We make it possible to centralize many cell programming projects in our Foundry by deconstructing programs into a set of common steps and then standardizing those steps. For each step, we have built a specialized functional team that performs that step for all programs. Those teams define a set of standardized services that can be used in concert to execute an end-to-end cell programming process. Each team has access to scientific, software, and robotic engineering resources to replace manual ad hoc operations with standardized, automated, and optimized services. In addition to enabling scale, this approach ensures standard operating procedures, know-how, and human skill become encoded in software that can be more effectively debugged, monitored, controlled, and optimized.

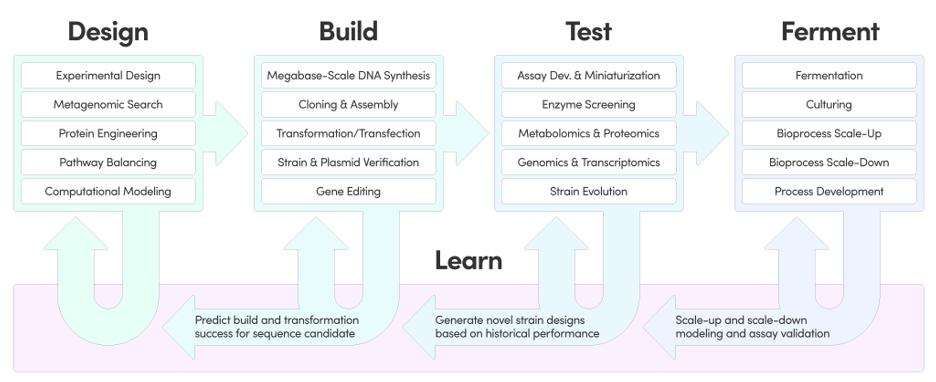

Figure 9: A non-exhaustive summary of the functions performed throughout the lifecycle of a program in the Foundry. At each stage, learnings are generated, driving improved design cycles and functional optimizations.

While the engineering strategies described above have historically been relatively uncommon in the life sciences, they are obviously not our invention. Rather, we are inspired by the lessons from other engineering disciplines and seek to apply those to biology. Automotive manufacturing, semiconductor fabrication, and data centers, among many other industries, demonstrate how automation, data, economies of scale, and continuous improvement can produce compounding gains in scale, costs, and quality. Critically, routine performance of these strategies across dozens of projects gives us the data and experience needed to drive continuous improvement.

As described above, a key strategy in our Foundry is to increase the scale of our operations so that we can run more programs and more prototypes in parallel (i.e., large batch sizes). This approach benefits from operational efficiencies and economies of scale across many dimensions:

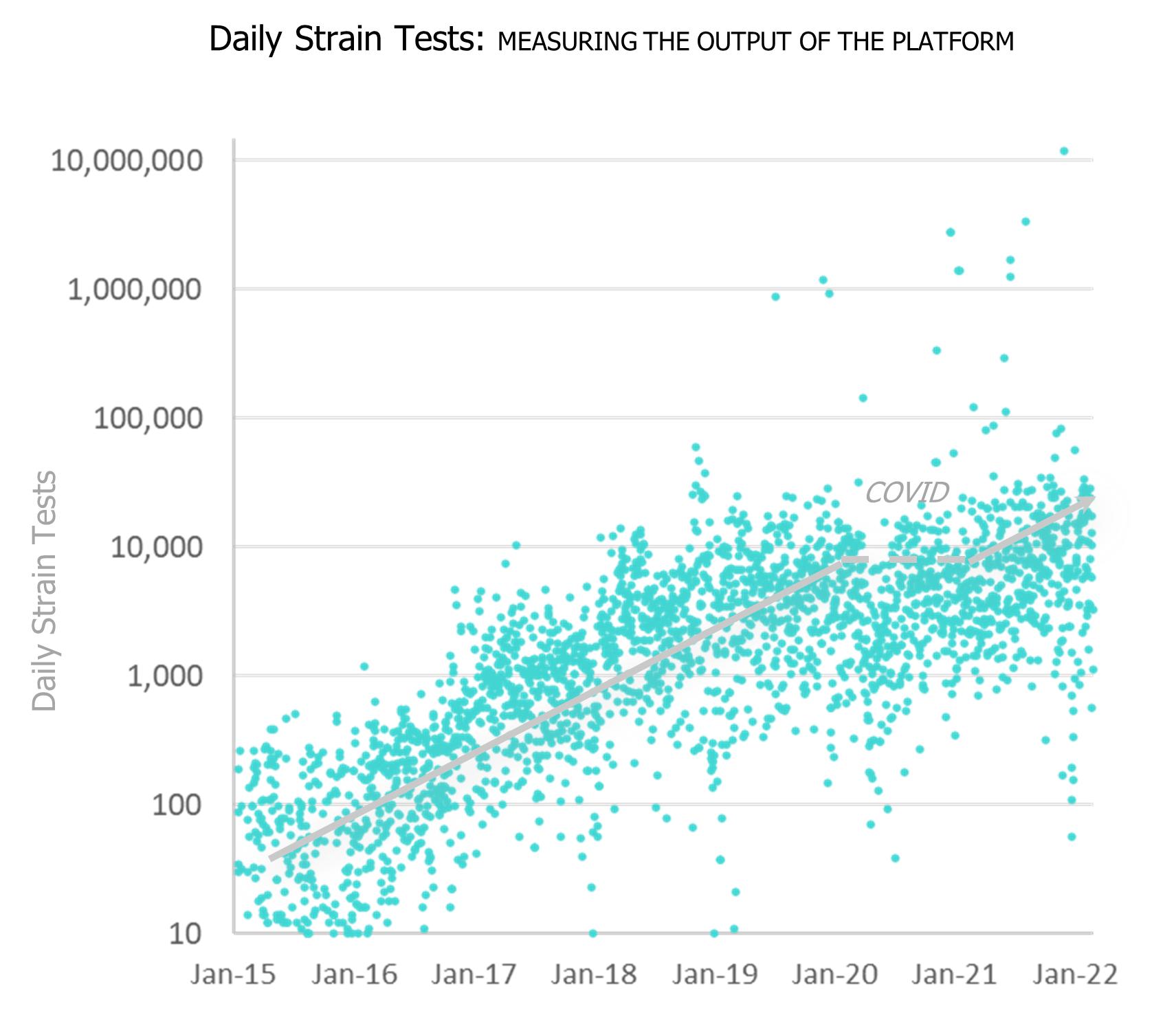

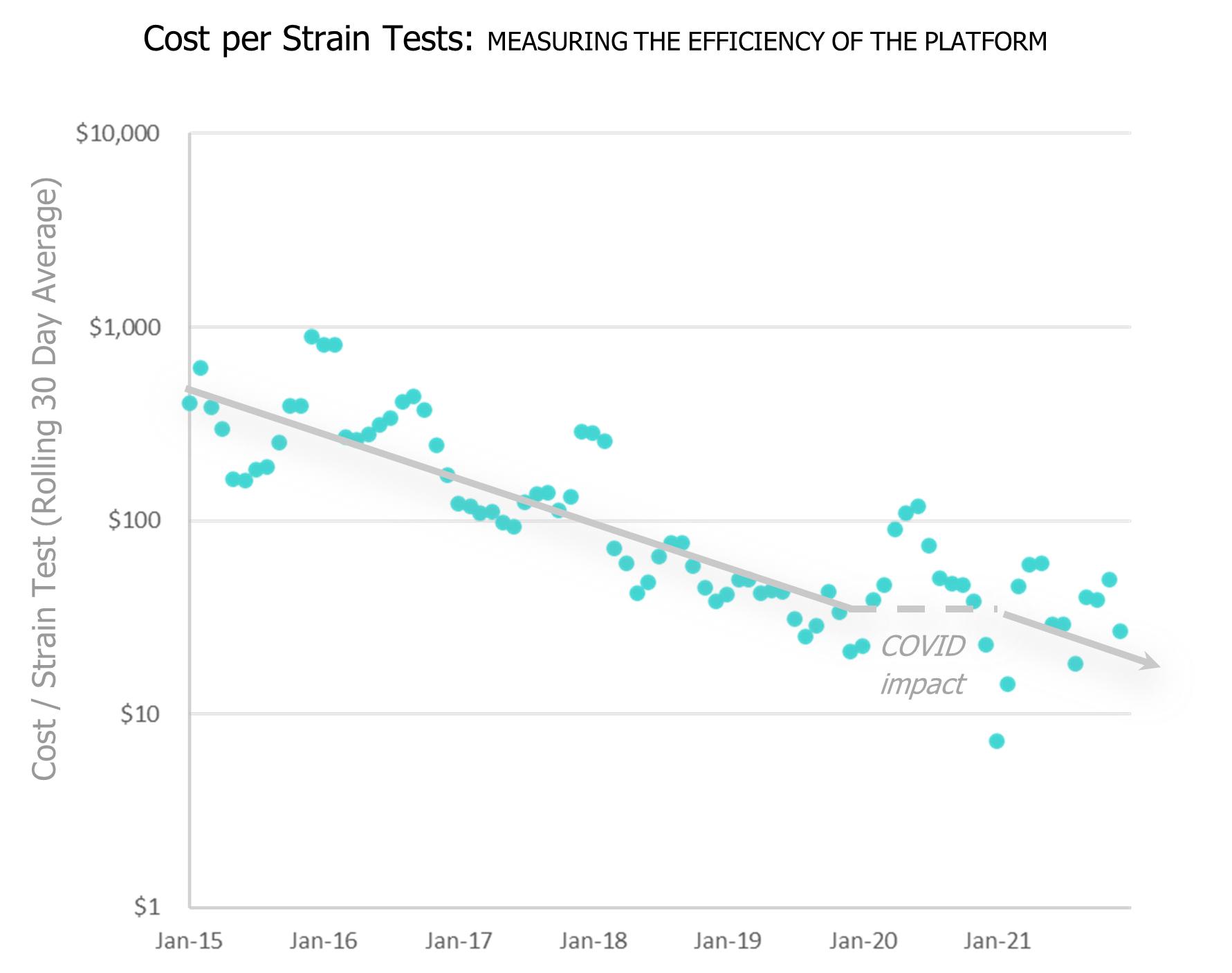

These efficiencies and economies of scale can be observed empirically from a relationship we refer to as “Knight’s Law,” named after Tom Knight, one of our co-founders, and loosely inspired by Moore’s Law for semiconductors. As shown below, we have seen an exponential increase in the output of the Foundry over time alongside an exponential decline in the average cost per unit of output. While this trend was interrupted by temporary lab shutdowns during the COVID-19 pandemic and reduced capacity due to social distancing, we have since continued to drive our business towards achieving these metrics.

16

While Knight’s Law does not provide the full story on our development, it is a useful tool that allows us to continue to build efficiencies of scale. We continue to build our internal metrics around Knight’s Law and believe we can continue to drive this kind of capacity growth in the foreseeable future, though it is dependent on the development of new technologies, which inherently carries risk, and, like Moore’s Law, we will likely hit a limit over time. This feature compares to a conventional facility, where scaling is driven predominantly by the addition of employees, an exponential increase in work would be infeasible and the cost per unit of work would decline little, if at all.

Figure 10: The output of the platform increased by over 3X per year for 5 years (with the exception of 2020), and while we expect that kind of scaling to continue, there is no guarantee that we will be able to do so.

17

Figure 11: As the output of the platform has increased, our total R&D / operational costs per unit of output has decreased by approximately 50% per year.

We are frequently asked, and spend much time thinking about, whether it will be possible for compounding gains in output and productivity to continue for many years in the future. It is important to note that given significantly advanced tools, most steps in cell programming could be miniaturized to a point where single molecules of DNA and single cells are being manipulated and monitored. At that ultimate degree of miniaturization, the costs and timelines of cell programming could be reduced orders of magnitude from where they are today. Newly available microfluidic technologies, such as those developed by our partner, Berkeley Lights, Inc. (“Berkeley Lights”), point to the reality of this future of cell programming at the single-cell level. Additionally, because many of the enabling tools of cell programming are biological in nature (e.g., polymerases and CRISPR), we are able to point the platform at itself, developing new biological tools to reduce the number of steps or the complexity of a certain operation. For example, we could develop better gene editing enzymes or novel ways to screen cells in a multiplexed format using biological sensors. It is easy to theorize about these types of developments, however they are hard to execute, we will undoubtedly run into roadblocks along the way and we will have to invest significantly in developing new technologies in order to enable the types of improvements we seek to achieve.

Recent advances in machine learning, molecular simulation, and other computational techniques also hold great promise to improve our ability to program cells. We believe our Foundry is well-positioned to build the kind of large, well-structured datasets that such computational approaches need to succeed. In time, we believe computational approaches will reduce the need for certain kinds of experiments (for example, we already use machine learning to make protein and enzyme design projects more efficient). If computational approaches can replace certain sets of experiments, we expect to use the recovered Foundry capacity to work on ever-more complex cell programming challenges. The reality is that the cells that we program today accomplish relatively simple functions, such as: “produce as much of molecule X as possible.” Programming cells for complex functions, such as live-cell therapeutics, responsive building materials, multicellular organisms, etc., will require sophisticated sub-systems for environmental sensing, intracellular information processing and feedback, and a multidimensional program that responds to such environmental stimuli. Only when we can deliver such sophisticated programmed cells will we have truly unlocked the potential of biology, and we see the Foundry as being an integral part of the platform for doing so.

Our Codebase—organizing the world’s biological code

Codebase is a familiar term to software developers but is a new concept in biology. Modern software firms develop their own (typically proprietary) codebase of source code and code libraries that can be leveraged by their software developers to more easily create new applications than they could starting from scratch. Additionally, vast repositories of debugged code are

18

shared publicly so that programmers across application areas can leverage prior art in order to innovate faster. This allows software developers to focus their time and effort on developing new features rather than recreating existing logic. Ginkgo’s Codebase is comprised of reusable genetic parts and strains that can be repurposed in new cell programs. We are continually investing in better ways to characterize functional biological code to drive increased reusability. In addition to the raw performance data we generate through our Foundry experiments (more than 24.8 million strain tests run as of December 31, 2021), we have also incorporated many public databases for genetic sequences and have a proprietary data set of over 3.8 billion additional sequences that we leverage in our designs.

Engineering biology is complex—one of the reasons that Foundry scale is important is that it remains highly difficult to predict the performance of a biological “part” in a given context from a DNA sequence alone. The genomics revolution has outpaced biologists’ ability to test the functionality of each DNA sequence as it was discovered, particularly because most of the community is still performing biological experiments by hand without the benefit of automation. Each program performed at Ginkgo involves testing thousands or millions of DNA sequences; with a small fraction of those ending up in our final engineered cells. For that reason, high-performance biological sequences—the handful of designs from thousands of candidate designs that meet our performance goals for an experiment—are hard-won assets and form a key component of Ginkgo’s Codebase. Not to be discounted, the “losing” designs are still valuable, helping inform more effective campaigns in the future that avoid known failure modes.

19

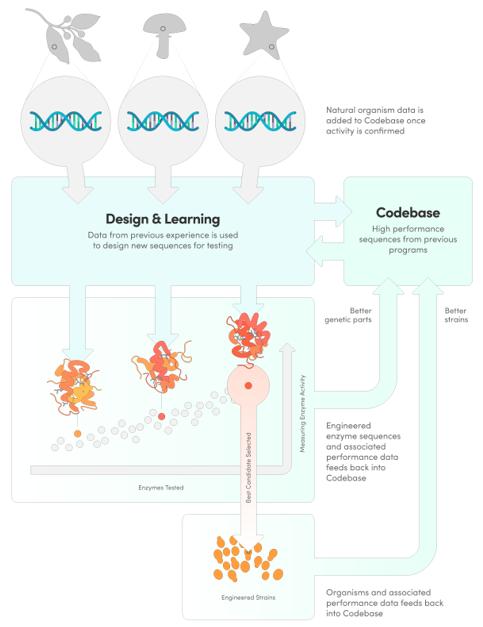

Figure 12: Our Codebase incorporates both biological assets from nature as well as engineered assets and data from our Foundry experiments. Because the Foundry enables us to test many thousands of prototype enzymes, pathways, and strains in individual engineering cycles, we are able to quickly expand the range of characterized biological assets in our Codebase.

In some ways Codebase is a “parts catalog” that we can draw from when developing a new organism. As Ginkgo performs more projects, we contribute new parts to our Codebase that can be reused in new contexts. For example, we developed novel synthetic promoters (DNA sequences that can turn on the expression of a gene of interest) that allowed us to increase production of proteins in yeast. Initially, we tested thousands of designs to arrive at a select number of promoters with high performance. Now those high-performing promoters can be reused in any program that involves producing a protein in yeast; they are a modular piece of genetic code. Over the past 20 years, our team has supported efforts to build these kinds of parts libraries—the International Genetically Engineered Machine (“iGEM”) Parts Registry and AddGene are two notable examples of initiatives to make reusable parts available to researchers in the community. But despite these efforts, we continue to see intellectual property siloed within organizations across the biotechnology industry, leaving many without the additional intellectual property they need to develop their programs. Ginkgo’s Codebase allows our customers to draw from a broader set of biological assets than any single company would develop for a given application. The scale and diversity of our programs have allowed us to develop a large Codebase that grows with the addition of each new program and can be opened to the broad swath of partners and cell programmers using our platform.

Cell programmers must consider not only the genes in the programs that they design, but also the ways that they interact with the cell that “runs” the program. Therefore, Codebase is more than just the individual modular parts we use to design biological programs. The organisms that have been optimized to run the programs, whether because they have been engineered for robust growth or because they are particularly adept at producing certain classes of products, are known as “chassis” strains. These strains can be reused across multiple programs, significantly reducing the amount of work needed to optimize a program and engineer a commercially viable organism. The breadth of Ginkgo’s customer base allows us to use these chassis strains in many more contexts than traditional industrial biotech players.

For example:

Our Foundry and Codebase are inextricably linked. Our Foundry scale allows us to generate unparalleled Codebase assets. These Codebase assets help us improve our designs and provide reusable parts and chassis strains that improve the efficiency

20

and probability of success of our cell programming efforts in the Foundry. As the capabilities of the platform improve, it drives further demand, which increases the rate of learning in our Codebase. The continuous learning and improvements inherent in this relationship is one of the key features of our platform.

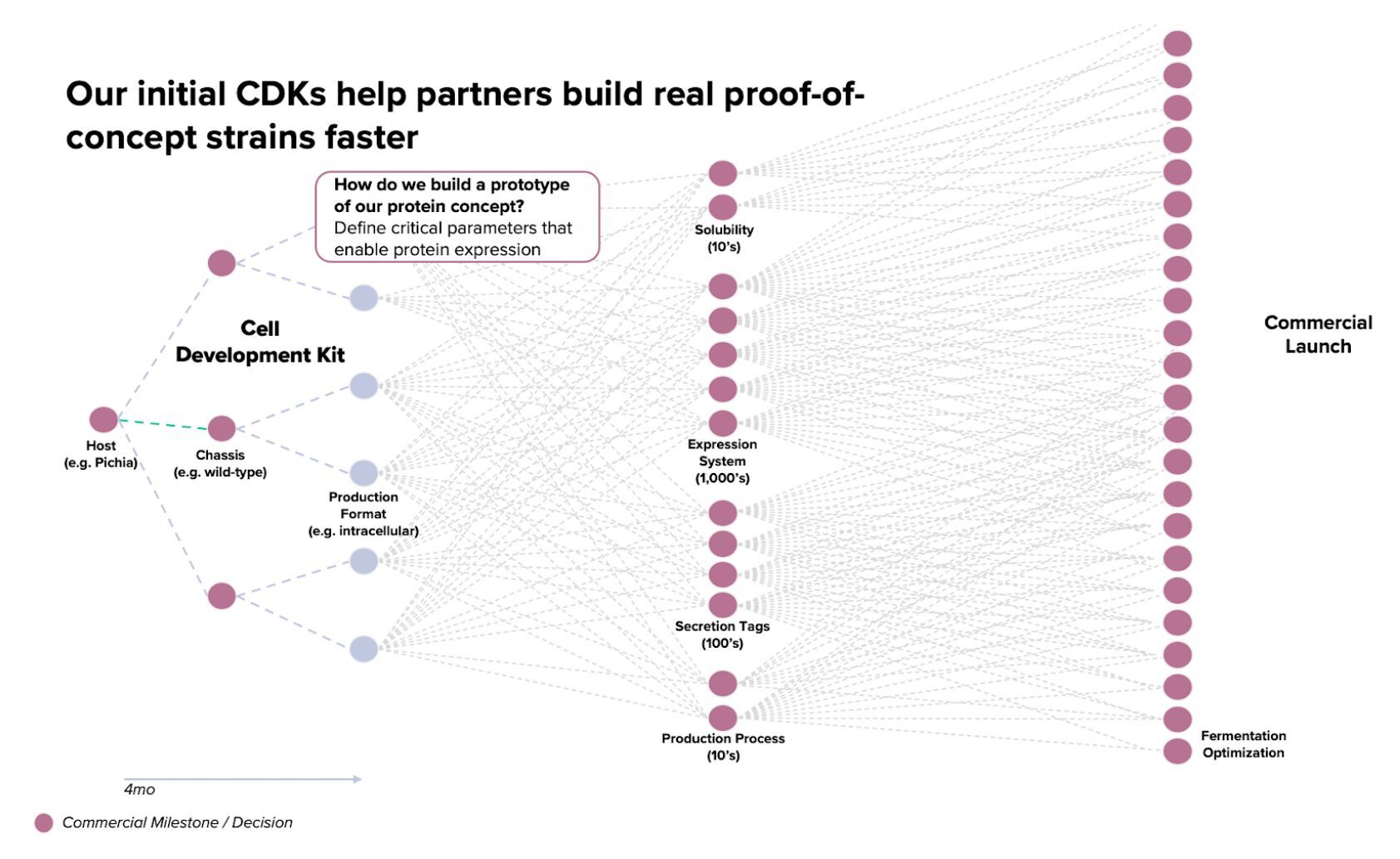

Figure 13: We believe our initial CDKs can help cell programmers build proof-of-concept strains faster.

An ecosystem to support cell programmers

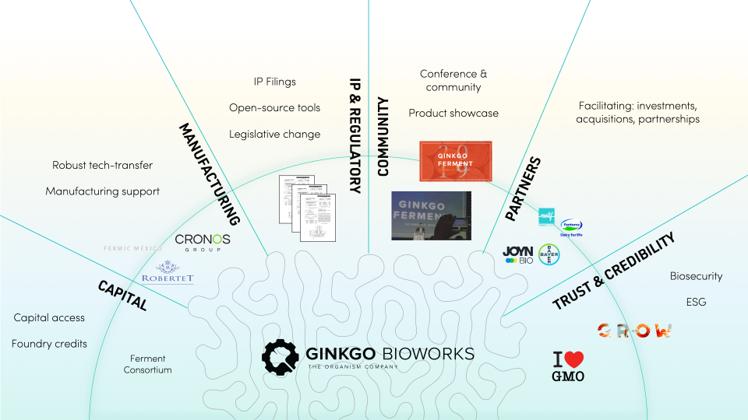

Ginkgo has long recognized that it is critical to build a true ecosystem around our technical platform. We have been inspired by the leading horizontal platforms in information technology, such as Microsoft Windows and Amazon Web Services (“AWS”), which built real developer communities and provided a range of value-added services on top of their core technology. Like these pathbreakers, who set the stage for a generation of computer developers, we too are trying to ensure that the cell programmers who build applications on our platform have the tools they need to succeed beyond the lab.

21

Figure 14: Ginkgo strives to create an ecosystem to ensure that cell programmers have the tools they need to succeed.

Access to capital

As in the early days of computer programming, it is still extremely expensive to program biology. For that reason, it can be easier for larger companies to make investments in innovation around this space. But Ginkgo’s platform gives small companies and innovators access to the same horsepower as larger players and obviates the need to invest in fixed laboratory assets, providing an even greater strategic benefit. To help address this discrepancy, Ginkgo has assisted in launching new companies (such as Motif and Allonnia) by bringing together strategic and financial investors to secure funding for these early stage companies. Going forward, we intend to leverage our own balance sheet and to partner with investors, enabling companies at all stages to benefit from our platform. We believe that, as Ginkgo’s customers demonstrate increasing success, there will be an explosion of capital for cell programming applications and a recognition of Ginkgo’s platform as setting the industry standard and providing the backbone for these development efforts.

Manufacturing support

Our job is to ensure that our cell programs can be executed at scale and we support our customers to ensure successful commercial scale manufacturing. We have built relationships with a number of leading contract manufacturing organizations and have demonstrated that we can transfer our lab-developed protocols to commercial scale (e.g., 50,000+ L fermentation tanks) with predictable performance. We have an in-house deployment team dedicated to supporting our customers’ scale-up and downstream processing needs. We have even helped certain customers, such as Cronos Group, Inc., acquire and build out their own in-house manufacturing capabilities and certain programs, such as our work with Moderna, Inc., focus on manufacturing process optimization.

Intellectual property protection and regulatory support

Ginkgo takes responsibility for the cell engineering intellectual property generated through customer collaborations. Our scientific team works continuously with our intellectual property team to file patent applications and monitor for freedom to operate. We are also active in helping shape and influence the evolving regulatory landscape for biological engineering. While our customers are responsible for handling their own regulatory procedures on a product-by-product basis, our broader view and sphere of influence can help build understanding of and support for novel product classes.

22

Building a community of cell programmers

We launched Ferment, our annual conference, in 2018. The conference highlights developments and thought leadership in the field and brings together scientists, entrepreneurs, investors, and suppliers. Our conference in 2021 brought over 700 participants to our headquarters in Boston. Even prior to launching Ginkgo, our founders focused on building community within the emerging field of cell programming. Tom Knight, one of our founders, was among the professors who launched the iGEM Competition in 2004, which has now had over 70,000 participants from over 40 countries take part in the competition (including dozens of Ginkgo employees and all five founders!).

Facilitating partnerships within our community

Because Ginkgo serves both large market incumbents and smaller startups, our community also serves to facilitate introductions between innovators and those looking to invest in innovation. We believe that investors and large strategic companies have come to recognize Ginkgo’s platform as a key enabler of innovation and are keen to get to know the companies that are building with us. Those relationships can be the source of funding and go-to-market support for the earlier stage companies building on the platform, increasing the odds that they develop successful products.

We invest in building trust and credibility for the entire industry

The most powerful technologies require the most care. Biology is too powerful for us to not care about how our platform is used. We have and will continue to invest heavily to build and maintain trust in bioengineering as a technology platform across all layers of the industry. At the platform layer, we have focused on building robust biosecurity measures. At the application layer, we are proud to enable a diverse set of programs that drive towards environmental sustainability. We are committed to ESG practices and broad stakeholder engagement at a corporate level. We are also engaged in deep conversations around the implications and ethics of biotechnologies through many public forums, helping shape our platform to promote sustainability in our global community.

Biosecurity: A complement to our platform and demonstrated source of value

With a mission to make biology easier to engineer, we have always recognized the imperative to invest in biosecurity as a key component of our platform. We care how our platform is used, and biosecurity is a necessary complement to synthetic biology that helps us ensure our cell programming work is conducted and deployed responsibly. Consideration for biosecurity is ingrained into our cell engineering platform tools, as evidenced through our membership in the International Gene Synthesis Consortium (“IGSC”), and our application of their harmonized protocols to screen synthetic DNA for concerning sequences, as well as our ongoing work with national defense agencies aiming to develop experimental and computational tools that detect or prevent misuse of bioengineering.

During the COVID-19 pandemic, we collectively witnessed the disruptive effects of a biological threat. The pandemic created a renewed sense of urgency for the need to counter biological risk, and triggered a paradigm shift for biosecurity in public and private institutions. Here at Ginkgo, this pandemic has deepened our resolve to advance global biosecurity and accelerated our capabilities to do so. At the start of the pandemic, we made a commitment of $25 million of free access to our platform for partner COVID-19 projects and launched a partnership with Moderna on process optimization for mRNA vaccine manufacturing. Since then, we’ve worked with Aldevron to deliver a breakthrough in the manufacturing of vaccinia capping enzyme for mRNA vaccines, and we’ve advanced discovery of therapeutics. We’ve also participated in the largest wastewater sequencing effort in the United States, supporting Biobot Analytics and the U.S. Department for Health and Human Services (“HHS”) with genomic sequencing capacity.

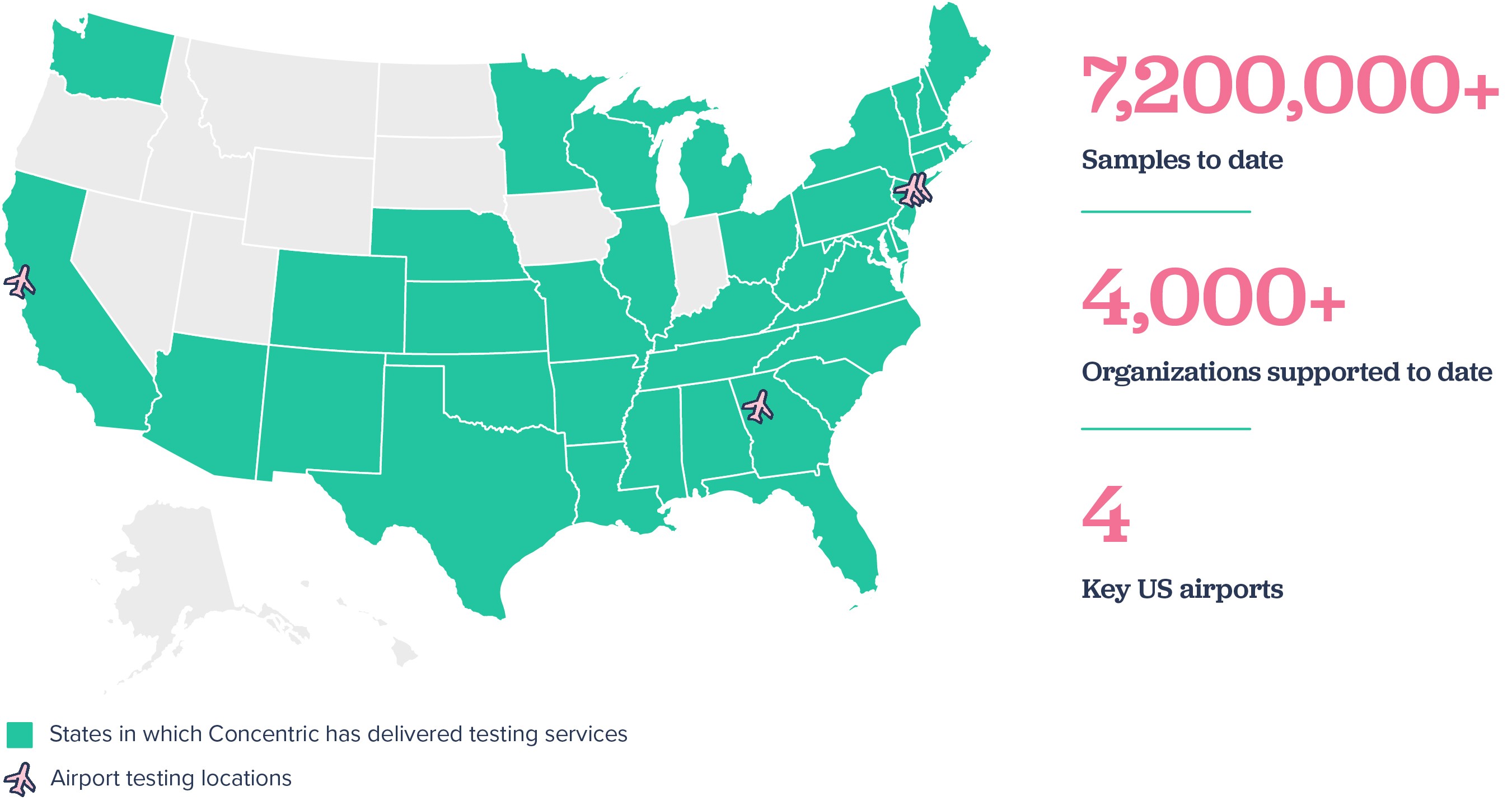

Most strikingly within the biosecurity space, we’ve grown Concentric by Ginkgo into a trusted brand and successful business as a large-scale systems integrator to facilitate COVID-19 testing in communities across the country. We tackled a moment of global crisis head-on through the growth of an innovative, scalable, community-centered apparatus for robust health security.

23

Figure 15: Concentric’s pathogen monitoring network has conducted testing across most of the U.S. Map shading reflects all states in which Concentric has delivered testing since launching in 2020. Not all states have active testing programs as of March 2022.

Through this pathogen monitoring network, we've empowered communities to make informed public health decisions through the many waves of the pandemic. Our tools provide early warning of infection and provide communities with tools that can mitigate outbreaks. We’ve worked closely with national, state, and local public health authorities and educational leaders to make sure that our programs are aligned with broader COVID-19 guidance and mitigation strategies, and are capable of delivering timely data to inform public health decision-making. As a systems integrator, we developed customizable, low-burden programs based on the particular needs of educators, students, parents, guardians, and community members, and grew a world-class customer service system to support each local program in context. This work with educational institutions—organizations that represent the centers of our community—is a meaningful first step in building the pathogen monitoring capabilities critical to the prevention and mitigation of biological risks.

As we sought to evolve our COVID-19 monitoring platform to serve communities in other contexts, we developed strategic partnerships to complement our operational and technical expertise.

We are continually exploring where public and private partnerships can help us scale our platform and further innovate in pathogen biomonitoring.

Our dedication to biosecurity is deeper than our emergency response to the current global pandemic. SARS-CoV-2 will not be the last pathogen we face with pandemic potential, but if we take the necessary steps, it may be the last that catches us

24

unprepared. Ginkgo has been supporting and engaging with domestic and international organizations and governments to help shape the understanding of a robust biosecurity program beyond the COVID-19 pandemic, and we believe there is a meaningful commercial opportunity in such a program driven by increased awareness of the need for prevention and response systems. Given our experience to date, we believe we are well placed to take a leadership position as the biosecurity platform of choice. If we are to harness biology to engineer products for our health, food, energy, and environment as we drive the growth of a sustainable bioeconomy, we must also move with the same speed and vigor to secure biology.

Our Business Model