Registration No. 333-__________

As filed with the Securities and Exchange Commission on September 13, 2021

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933

(Exact name of registrant as specified in its charter)

| 3571 | ||||

| (State or jurisdiction of | (Primary Standard Industrial | (I.R.S. Employer | ||

| incorporation or organization) | Classification Code Number) | Identification No.) |

(

(Address, including zip code, and telephone number, including area code of registrant’s principal executive offices)

Telephone:

(

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

Mark Crone, Esq. Liang Shih, Esq. The Crone Law Group, P.C. 500 Fifth Avenue, Suite 938 New York, New York 10110 Telephone: (646) 861-7891 |

Kevin Sun, Esq. Bevilacqua PLLC 1050 Connecticut Avenue, NW, Suite 500 Washington, D.C. 20036 Telephone: (202) 869-0888 |

Approximate date of commencement of proposed sale to the public: As soon as practicable and from time to time after this Registration Statement is declared effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box. ☐

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer”, “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| ☒ | Smaller reporting company | ||

| Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

CALCULATION OF REGISTRATION FEE

| Title of Class of Securities to be Registered | Proposed Maximum Aggregate Offering Price | Amount of Registration Fee | ||||||

| Underwritten Offering | ||||||||

| Common stock, $0.001 par value per share (1)(2)(3) | $ | 57,500,000 | $ | |||||

| Underwriter’s Warrants (4) | - | - | ||||||

| Common Stock, $0.001 par value per share, issuable upon exercise of Underwriter’s Warrants (1)(2)(3)(5) | $ | 4,312,500 | $ | |||||

| Total | 61,812,500 | $ | 6,743.74 | |||||

| (1) | Estimated solely for the purpose of calculating the registration fee in accordance with Rule 457(o) of the Securities Act of 1933, as amended (the “Securities Act”).. |

| (2) | Includes the aggregate offering price of additional shares that the underwriters have a 45-day option to purchase to cover over-allotments, if any. |

| (3) | Pursuant to Rule 416 under the Securities Act, the securities being registered hereunder include such indeterminate number of additional shares of common stock as may be issued after the date hereof as a result of stock splits, stock dividends or similar transactions. |

| (4) | No separate registration fee required pursuant to Rule 457(g) under the Securities Act of 1933, as amended. |

| (5) | The Underwriter’s Warrants are exercisable for up to 6.0% of the aggregate number of shares of common stock sold in the primary offering at a per share exercise price equal to 125.0% of the public offering price of the shares of common stock in the primary offering. |

The registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, or until this Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to Section 8(a), may determine.

THE INFORMATION IN THIS PROSPECTUS IS NOT COMPLETE AND MAY BE CHANGED. WE MAY NOT SELL THESE SECURITIES UNTIL THE REGISTRATION STATEMENT FILED WITH THE SECURITIES AND EXCHANGE COMMISSION IS EFFECTIVE. THIS PROSPECTUS IS NOT AN OFFER TO SELL THESE SECURITIES AND IS NOT SOLICITING AN OFFER TO BUY THESE SECURITIES IN ANY STATE WHERE THE OFFER OR SALE IS NOT PERMITTED.

SUBJECT TO COMPLETION, DATED SEPTEMBER 13, 2021

PRELIMINARY PROSPECTUS

WETOUCH TECHNOLOGY INC.

shares of Common Stock

We are offering to sell shares of our common stock, $0.001 par value per share, in a firm commitment underwritten offering (the “Underwritten Offering”).

Our common stock is currently traded on the OTCQB Marketplace operated by the OTC Markets Group, Inc. (the “OTCQB”) under the symbol “WETH.” On September 10, 2021, the last reported sale price for our common stock was $2.69 per share. We intend to apply to list our common stock on the Nasdaq Capital Market under the symbol “WETH”. We believe that upon completion of the offering contemplated by this prospectus, we will meet the standards for listing on the Nasdaq Capital Market. No assurance can be given that our application will be approved or that the trading prices of our common stock on the OTCQB will be indicative of the prices of our common stock if our common stock were traded on the Nasdaq Capital Market. We currently estimate that the public offering price will be between $ and $ per share.

The offering price of our shares of common stock in the Underwritten Offering will be determined between the underwriters and us at the time of pricing, considering our historical performance and capital structure, prevailing market conditions, and overall assessment of our business, and may be at a discount to the current market price. Therefore, the recent market price of our common stock and the public offering price of the common stock used throughout this prospectus may not be indicative of the actual public offering price for the shares of common stock.

INVESTING IN OUR SECURITIES INVOLVES A HIGH DEGREE OF RISK. BEFORE MAKING ANY INVESTMENT DECISION, YOU SHOULD CAREFULLY REVIEW AND CONSIDER ALL THE INFORMATION IN THIS PROSPECTUS AND THE DOCUMENTS INCORPORATED BY REFERENCE HEREIN, INCLUDING THE RISKS AND UNCERTAINTIES DESCRIBED UNDER “RISK FACTORS” BEGINNING ON PAGE 10.

The Underwritten Offering is being underwritten on a firm commitment basis. We have granted the underwriters an option to buy up to an additional shares of common stock to cover over-allotments. The underwriters may exercise this option at any time and from time to time during the 45-day period from the date of this prospectus.

| Per Share | Total | |||||||

| Public offering price | $ | $ | ||||||

| Underwriting discounts and commissions(1)(2) | $ | $ | ||||||

| Proceeds to us, before expenses | $ | $ | ||||||

| Proceeds to the selling stockholders, before expenses | $ | $ | ||||||

(1) We have agreed to reimburse the underwriter(s) for certain expenses. Underwriting discounts and commissions do not include a non-accountable expense allowance equal to $100,000 payable to the underwriters. The underwriter(s) will receive an underwriting discount equal to 7.5% of the gross proceeds in this offering. In addition, we have agreed to pay up to a maximum of $180,000 of the fees and expenses of the underwriters in connection with this offering, which includes the fees and expenses of underwriter(s)’ counsel. See “Underwriting” Section for more information.

(2) We have also agreed to issue to Craft Capital Management LLC and R.F. Lafferty & Co., Inc. (collectively the “Representatives”) warrants to purchase up to an aggregate of shares of our common stock. See “Underwriting” beginning on page 84 for additional information regarding these warrants and underwriting compensation generally.

The Underwritten Offering is being conducted on a firm commitment basis. The underwriter(s) are obligated to take and pay for all the shares of common stock offered by this prospectus if the Underwritten Offering is consummated.

We have granted the underwriters a 45-day option to purchase up to an additional shares of common stock from us at the public offering price, to cover over-allotments, if any (such shares not to exceed, in the aggregate, 15% of the shares offered hereby).

The underwriter(s) expect to deliver the shares on or about , 2021.

NEITHER THE SECURITIES AND EXCHANGE COMMISSION NOR ANY STATE SECURITIES COMMISSION HAS APPROVED OR DISAPPROVED OF THESE SECURITIES OR DETERMINED IF THIS PROSPECTUS IS TRUTHFUL OR COMPLETE. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

| CRAFT CAPITAL MANAGEMENT LLC | R.F. Lafferty & Co., Inc. |

The date of this prospectus is , 2021

WETOUCH TECHNOLOGY INC.

TABLE OF CONTENTS

You should rely only on the information contained in this prospectus. Neither we nor the underwriters have authorized anyone to provide you with different information. We are offering to sell, and seeking offers to buy, shares of common stock only in jurisdictions where offers and sales are permitted. The information in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or of any sale of shares of our common stock. Our business, financial condition, operating results and prospects may have changed since that date.

No action is being taken in any jurisdiction outside the United States to permit a public offering of our shares or possession or distribution of this prospectus in any such jurisdiction. Persons who come into possession of this prospectus in jurisdictions outside the United States are required to inform themselves about and to observe any restrictions as to this offering and the distribution of this prospectus applicable to that jurisdiction.

Through and including , 2021 (25 days after the commencement of this offering), all dealers that buy, sell or trade shares of our common stock, whether or not participating in this offering, may be required to deliver a prospectus. This delivery requirement is in addition to the dealers’ obligation to deliver a prospectus when acting as underwriters and with respect to their unsold allotments or subscriptions.

| i |

COMMONLY USED DEFINED TERMS

Unless otherwise indicated or the context requires otherwise, references in this registration statement to:

| ● | “China” or the “PRC” are to the People’s Republic of China, excluding Taiwan and the special administrative regions of Hong Kong and Macau for the purposes of this registration statement only; |

| ● | Unless the context provides otherwise, “we,” “us,” “our company,” “our,” “the Company” and “Wetouch” is to Wetouch Technology Inc., a Nevada company and where appropriate, its wholly-owned subsidiaries, Wetouch Holding Group Limited, Hong Kong Wetouch Technology Limited, and Sichuan Vtouch Technology Co., Ltd; |

| ● | “BVI” is to the British Virgin Islands; |

| ● | “BVI Wetouch” is to Wetouch Holding Group Limited, a limited company organized under the laws of British Virgin Islands and a wholly owned subsidiary of Wetouch; |

| ● | “Hong Kong Wetouch” is to Hong Kong Wetouch Electronics Technology Limited (香港偉易達電子科技有限公司), a limited company organized under the laws of Hong Kong and a wholly owned subsidiary of BVI Wetouch. On June 18, 2021, Hong Kong Wetouch submitted its application for dissolution, which requires approximately one year for governmental approval. During such period, Hong Kong Wetouch is no longer engaged in any operations; |

| ● | “HK Wetouch” is to Hong Kong Wetouch Technology Limited (香港偉易達科技有限公司), a limited company organized under the laws of Hong Kong and a wholly owned subsidiary of BVI Wetouch; |

| ● | “Sichuan Wetouch” is to Sichuan Wetouch Technology Co., Ltd (四川伟易达科技有限公司), a limited liability company organized under the laws of China and prior wholly foreign owned subsidiary of Hong Kong Wetouch. The Company has dissolved Sichuan Wetouch, and its business and operations have been assumed by Sichuan Vtouch; |

| ● | “Sichuan Vtouch” is to Sichuan Vtouch Technology Co., Ltd (四川伟大奇科技有限公司), a limited liability company organized under the laws of China and a wholly foreign owned subsidiary of HK Wetouch; |

| ● | “Qixun Samoa” is to Qixun Technology (Samoa) Limited, a limited liability company organized under the laws of Samoa and a shareholder of Wetouch, holding 2,257,143 shares of the Company; |

| ● | “Qihong Samoa” is to Qihong Technology (Samoa) Limited, a limited liability company organized under the laws of Samoa and a shareholder of Wetouch, holding 4,497,143 shares of the Company; |

| ● | “Shares,” “shares” or “shares of common stock” are to the shares of common stock of Wetouch Technology Inc., with par value of $0.001 per share; |

| ● | All references to “Renminbi,” “RMB” or “Chinese Yuan” is to the legal currency of China; |

| ● | All references to “U.S. dollars,” “dollars,” “USD” or “$” are to the legal currency of the United States; and |

| ● | “Websites” are to our websites at www.wetouchinc.com and www.wetouch.com.cn, the latter of which is only accessible in the PRC. |

This registration statement contains translations of certain RMB amounts into U.S. dollar amounts at specified rates solely for the convenience of the reader. The relevant exchange rates are listed below:

| For the six months Ended June 30, 2021 | For the year Ended December 31, 2020 | For the Year Ended December 31, 2019 | ||||||||||

| Period Ended RMB: USD exchange rate | 6.4566 | 6.5250 | 6.9618 | |||||||||

| Period Average RMB: USD exchange rate | 6.4702 | 6.9042 | 6.9081 | |||||||||

Numerical figures included in this registration statement have been subject to rounding adjustments. Accordingly, numerical figures shown as totals in various tables may not be arithmetic aggregations of the figures that precede them.

For the sake of clarity, this registration statement follows the English naming convention of first name followed by last name, regardless of whether an individual’s name is Chinese or English. For example, the name of our Chairman will be presented as “Guangde Cai” even though, in Chinese, Mr. Cai’s name is presented as “Cai Guangde.”

We have relied on statistics provided by a variety of publicly-available sources regarding China’s expectations of growth. We did not, directly or indirectly, sponsor or participate in the publication of such materials, and these materials are not incorporated in this registration statement other than to the extent specifically cited herein. We have sought to provide current information in this registration statement and believe that the statistics provided in this registration statement remain up-to-date and reliable, and these materials are not incorporated in this registration statement other than to the extent specifically cited in this registration statement.

| ii |

PROSPECTUS SUMMARY

This summary highlights information contained elsewhere in this prospectus. This summary provides an overview of selected information and does not contain all of the information you should consider before investing in our securities. You should read the entire prospectus carefully, especially the “Risk Factors,” and our financial statements and the accompanying notes to those statements, included elsewhere in this prospectus, before making an investment decision. Unless the context requires otherwise, references to the “Company,” “we,” “us,” and “our” refer to Wetouch Technology Inc., a Nevada corporation.

Overview

We were originally incorporated under the laws of the state of Nevada on August 31, 1992. On October 9, 2020, we entered into a share exchange agreement (the “Share Exchange Agreement”) with BVI Wetouch, and all the shareholders of BVI Wetouch (each a “Shareholder” and collectively the “Shareholders”), to acquire all the issued and outstanding capital stock of BVI Wetouch in exchange for the issuance to the Shareholders an aggregate of 28 million shares of our common stock (the “Reverse Merger”). The Reverse Merger closed on October 9, 2020. Immediately after the closing of the Reverse Merger, we had a total of 31,396,394 issued and outstanding shares of common stock. As a result of the Reverse Merger, BVI Wetouch is now our wholly-owned subsidiary.

Through our wholly-owned subsidiaries, we are engaged in the research, development, manufacturing, sales and servicing of medium to large sized projected capacitive touchscreens. We specialize in large-format touchscreens, which are developed and designed for a wide variety of markets and used in the financial terminals, automotive, POS, gaming, lottery, medical, HMI, and other specialized industries.

Our product portfolio comprises medium to large sized projected capacitive touchscreens ranging from 7.0 inch to 42 inch screens. In terms of the structures of touch panels, we offer (i) Glass-Glass (“GG”), primarily used in GPS/car entertainment panels in mid-size and luxury cars, industrial HMI, financial and banking terminals, POS and lottery machines; (ii) Glass-Film-Film (“GFF”), mostly used in high-end GPS and entertainment panels, industrial HMI, financial and banking terminals, lottery and gaming industry; (iii) Plastic-Glass (“PG”), typically adopted by touchscreens in GPS/entertainment panels motor vehicle GPS, smart home, robots and charging stations; and (iv) Glass-Film (“GF”), mostly used in industrial HMI.

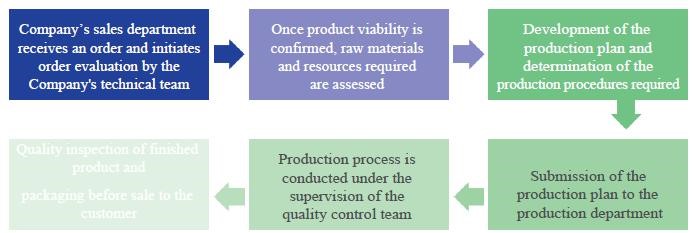

Maintaining the industry standards for product quality and sustainability is one of our core values. Touchscreens produced by us not only have long life span with low maintenance, but also have strong anti-interference and anti-corrosion solutions, coupled with multi-touch capability and high light-transmittance ratio and stability. As a high technology company, we have received certifications from domestic and international institutions, such as ISO9001 Quality Management Systems (QMS) Certification of Registration, ISO 14001 Environmental Management System (EMS) Certification of Registration, and RoHS SGS Certification (Restriction of Hazardous Substance Testing Certification).

We generate revenues through sales of our various touchscreen products. For the six months ended June 30, 2021 and 2020, we recognized approximately $25.9 million and $8.8 million, respectively, in revenues. For the years ended December 31, 2020 and 2019, we recognized approximately $31.3 million and $40 million, respectively, in revenues.

We sell our touchscreen products both domestically in China and internationally, covering major areas in China, including but not limited to the eastern, southern, northern and southwest regions of China, Taiwan, South Korea, and Germany. We have established a strong and diversified client base. For the six-month periods ended June 30, 2021 and 2020, our domestic sales accounted for 65.3% and 63.6%, respectively, of our revenues, and our international sales accounted for 34.7% and 36.4%, respectively, of our revenues. For the years ended December 31, 2020 and 2019, our domestic sales accounted for 68.4% and 66.2%, respectively, of our revenues, and our international sales accounted for 31.6% and 33.8%, respectively, of our revenues.

| 1 |

As of the date of this registration statement, we have a total of 126 employees. We have no part time employees or independent contractors.

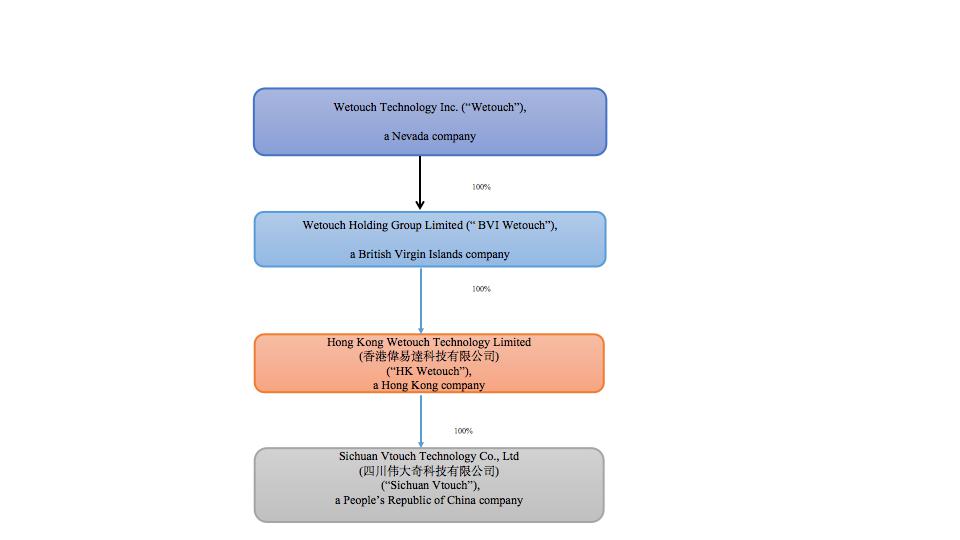

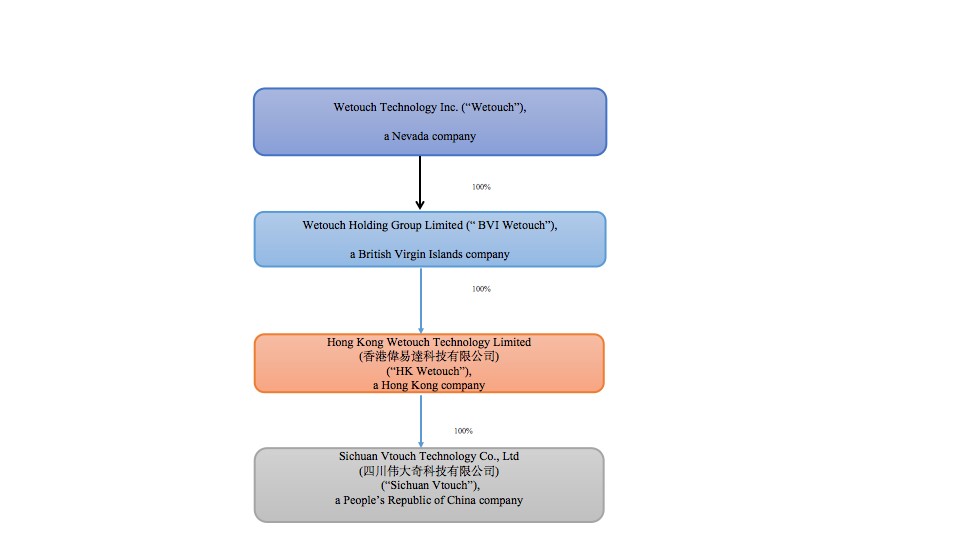

Corporate History and Structure

We were originally incorporated under the laws of the state of Nevada on August 31, 1992 as Gulf West Investment Properties, Inc, and were dormant and had no operations for many years.

On February 26, 2019, the Eighth Judicial District Court in and for Clark County, Nevada, Case No. A-19-787151-B, appointed Custodian Ventures LLC, an affiliate of David Lazar, as custodian of the Company (the “Custodian”). Mr. Lazar was appointed as the sole officer and director of the Company. On March 11, 2019, 1,714,286 shares of common stock of the Company were issued to the Custodian in consideration for the payment of cash and the issuance of a promissory note by the Custodian to the Company. Effective as of June 11, 2019, the court discharged the Custodian’s duties.

On June 18, 2020, we consummated the transactions contemplated by a Stock Purchase Agreement among the Company, the Custodian, Qixun Samoa and Qihong Samoa (Qixun Samoa and Qixun Samoa are referred to as the “Buyers”). Pursuant to the Stock Purchase Agreement, the Buyers acquired all of the 1,714,286 shares of the Company owned by the Custodian, representing 50.47% of the issued and outstanding shares of the Company. The Custodian and the Company agreed to indemnify the Buyers from any liabilities of the Company occurring prior to June 18, 2020, and the promissory note issued by the Custodian to the Company was canceled. Immediately following the closing, David Lazar resigned as the sole officer and director of the Company and Jiaying Cai was appointed as president, secretary and treasurer of the Company and as the sole director.

Name Change/Reverse Stock Split

Effective September 30, 2020, we changed our name from Gulf West Investment Properties, Inc. to Wetouch Technology Inc. by filing an Amended and Restated Articles of Incorporation with the Nevada Secretary of State to give effect to a name change. The Amended and Restated Articles also effectuated a reverse split of our authorized, issued and outstanding shares of common stock on a 70 for 1 new basis whereby each 70 shares of outstanding common stock was exchanged for one (1) share of new common stock (the “Reverse Split” and, for avoidance of doubt, all share amounts set forth herein shall be post Reverse Split unless otherwise specified) and, consequently, our authorized common stock increased to 300,000,000 shares of common stock and 10,000,000 shares of preferred stock, and our then issued and outstanding common shares decreased from 237,742,066 to 3,396,394 shares, all with a par value of $0.001. All share and per share numbers relating to our common stock prior to the effectiveness of the Reverse Split have been adjusted to give effect to the Reverse Split.

As a result of the name change, we changed our trading symbol from “GLFW” to “WETH,” effective November 3, 2020.

Acquisition of BVI Wetouch

On October 9, 2020, we entered into a Share Exchange Agreement (the “Share Exchange Agreement”) with BVI Wetouch and all of the shareholders of BVI Wetouch (each a “BVI Shareholder” and collectively the “BVI Shareholdres”), to acquire all the issued and outstanding capital stock of BVI Wetouch in exchange for the issuance to the BVI Shareholders an aggregate of 28,000,000 shares of our common stock (the “Reverse Merger”). In the Reverse Merger, each ordinary share of BVI Wetouch was exchanged for 560 shares of common stock of Wetouch. Immediately after the closing of the Reverse Merger on October 9, 2020, we had a total of 31,396,394 issued and outstanding shares of common stock. As a result of the Reverse Merger, BVI Wetouch is now our wholly-owned subsidiary.

On October 12, 2020, Guangde Cai was appointed as an additional director and Chairman of the Company. On October 12, 2020, Mr. Zongyi Lian was appointed as president and chief executive officer of the Company, and Mr. Yuhua Huang was appointed as chief financial officer of the Company. On the same day, Jiaying Cai resigned from the capacity of president and treasurer of the Company, but remains the secretary and director of the Company.

BVI Wetouch was established under the laws of British Virgin Islands on August 14, 2020 to acquire all the shares of Hong Kong Wetouch Electronics Technology Limited (“Hong Kong Wetouch”). On September 11, 2020, BVI Wetouch acquired all the outstanding shares of Hong Kong Wetouch from the shareholders of Hong Kong Wetouch in consideration of HK$10,000 pursuant to instruments of transfer in accordance with Hong Kong law. As a result of the acquisition, Hong Kong Wetouch became a wholly-owned subsidiary of BVI Wetouch. The shareholders of Hong Kong Wetouch became the shareholders of BVI Wetouch in said transaction, and therefore the shareholders who controlled Hong Kong Wetouch became the controlling shareholders of BVI Wetouch.

| 2 |

Hong Kong Wetouch was incorporated on May 5, 2016 under the laws of Hong Kong. On July 19, 2016, Hong Kong Wetouch acquired all the shares of Sichuan Wetouch, a PRC company established in Meishan, Sichuan on May 6, 2011. As a result of the acquisition, Sichuan Wetouch became a wholly owned subsidiary of Hong Kong Wetouch.

As BVI Wetouch owns all the outstanding shares of Hong Kong Wetouch, which, in turn, owns all the outstanding shares of Sichuan Wetouch, the Company owns indirectly all the business of Sichuan Wetouch. As a result of the Reverse Merger in which the Company acquired all the outstanding shares of BVI Wetouch, Hong Kong Wetouch and Sichuan Wetouch become our indirect wholly-owned subsidiaries.

Hong Kong Wetouch Technology Limited, a limited company organized under the laws of Hong Kong (“HK Wetouch”), an affiliate of Guangde Cai, our Chairman and Director, was incorporated on December 3, 2020 under the laws of Hong Kong. HK Wetouch was established to own all the outstanding shares of Sichuan Vtouch Technology Co., Ltd., which was incorporated on December 30, 2020 (“Sichuan Vtouch”) in Chengdu, Sichuan, under the laws of The People’s Republic of China (“PRC”).

On March 12, 2021, Wetouch Holding Group Limited (“BVI Wetouch”), the Company’s wholly owned subsidiary, acquired all the outstanding shares of HK Wetouch from the sole shareholder of HK Wetouch, Guangde Cai, in consideration of the payment of HK$10,000 pursuant to instruments of transfer in accordance with Hong Kong law. As a result of the acquisition, HK Wetouch became a wholly-owned subsidiary of BVI Wetouch. BVI Wetouch owns (i) all the outstanding shares of Hong Kong Wetouch, which, in turn, owns all the outstanding shares of Sichuan Wetouch and (ii) all of the outstanding shares of HK Wetouch, which owns all the shares of Sichaun Vtouch Technology Co., Ltd., a company incorporated under the laws of PRC.

Recent Developments

Pursuant to local PRC government guidelines on local environmental issues and the national overall plan, Sichuan Wetouch is under the government-directed relocation order to relocate no later than December 31, 2021 and received compensation accordingly.

On March 16, 2021, Sichuan Wetouch entered into an Agreement of Compensation on Demolition (“Compensation Agreement”) with Sichuan Renshou Shigao Tianfu Investment Co., Ltd, a limited company owned by the local government (Sichuan Renshou”), for the withdrawal of our right to use of state-owned land and the demolition of all buildings, facilities and equipment on such land where we maintain our executive offices, research and development facilities and factories at No.29, Third Main Avenue, Shigao Town, Renshou County, Meishan City, Sichuan, China (the “Property”). The Property, all buildings, facilities, equipment and all other appurtenances on the Property are collectively referred to as “Properties”. The Compensation Agreement was executed and delivered as a result of guidelines (the “Guidelines”) published by the local government of with respect to local environmental issues and a national overall plan on Tianfu New District, Meishan City, Sichuan, PRC. In accordance with the Guidelines, a project named “Chaisang River Ecological Wetland Park” is under construction in the areas where the manufacturing facilities and properties of the Company are located. As a result, Sichuan Wetouch must relocate. In consideration for such relocation, the owner of the buildings on the state-owned land will be compensated.

In order to minimize the interruption of our business, Sichuan Vtouch entered into a Leaseback Agreement with Sichuan Renshou on March 16, 2021. The Leaseback Agreement entitles us to lease back the Properties commencing from April 1, 2021 until December 31, 2021, at a monthly rent of RMB300,000 (approximately $46,154).

On March 18, 2021, Sichuan Wetouch received a total amount of RMB115.2 million (approximately $17.7 million) as the total amount of compensation from Sichuan Renshou, including RMB100.2 million ($15.4 million) based upon the appraised value of the Properties plus an extra 15% relocation bonus of RMB15.0 million ($2.3 million).

We are actively searching for an appropriate parcel in Chengdu Medicine City (Technology Park), Wenjiang District, Chengdu for the construction of our new production facilities and office buildings. As of the date of this prospectus, we estimate that our capital needs for this acquisition and construction will be approximately RMB170.0 million (approximately $26.2 million), but there is no assurance that the estimated amount is sufficient to achieve our goals. We may need additional financing for our business development. In addition, we expect that this acquisition and construction will be completed prior to December 31, 2021, but there is no assurance and we may need extended time to achieve our business plan. Pursuant to local PRC government guidelines on local environment issues and the national overall plan, Sichuan Wetouch was under the government directed relocation order to relocate no later than December 31, 2021 and was compensated for RMB115.2 million ($17.8 million) from the local government for the withdrawal of the right to use of state-owned land and the demolition of all buildings, facilities, equipment and all other appurtenances on the land.

On March 2, 2021, HK Wetouch acquired all shares of Hong Kong Wetouch. On June 18, 2021, Hong Kong Wetouch submitted its application for dissolution, which requires approximately one year for governmental approval. During such period, Hong Kong Wetouch is no longer engaged in any operations. In addition, as of March 31, 2021, the Company has dissolved Sichuan Wetouch, and its business and operations have been assumed by Sichuan Vtouch.

| 3 |

The following diagram illustrates our current corporate structure:

SEC Filing Obligations

We became subject to the filing requirements of the Securities Exchange Act of 1934, as amended, as a result of our Form 10 being declared effective by the Securities and Exchange Commission (the “Commission”) on December 11, 2020.

We filed a Form S-1 registration statement with respect to the resale by 44 selling stockholders identified in the prospectus for an aggregate of 15,889,371 shares of common stock of the Company. The registration statement was declared effective by the Commission on January 7, 2021 (Registration No. 333-251845).

Listing on OTCQB Market

On February 15, 2021, we applied to the OTC Markets to have our shares quoted on the OTCQB, which was approved on March 26, 2021. Effective March 29, 2021, our shares started trading on OTCQB under the symbol “WETH.”

Listing on the Nasdaq Capital Market

Our common stock is currently quoted on the OTCQB under the symbol “WETH.” In connection with this offering, we intend to apply to list our common stock on the Nasdaq Capital Market (“Nasdaq”) under the symbol “WETH.” If our listing application is approved, we expect to list our common stock on Nasdaq upon consummation of the offering, at which point our common stock will cease to be traded on the OTCQB. No assurance can be given that our listing application will be approved. Nasdaq listing requirements include, among other things, a stock price threshold. As a result, prior to effectiveness, we will need to take the necessary steps to meet Nasdaq listing requirements, which may include, but not limited to, effectuating a reverse split of our common stock at a ratio between 1-for 2 and 1-for 4 (estimated based on the current market price of our common stock). There can be no assurance that our common stock will be listed on the Nasdaq.

| 4 |

Effects of COVID-19

The COVID-19 pandemic and resulting global disruptions have affected our businesses, as well as those of our customers and suppliers. To serve our customers while also providing for the safety of our employees and service providers, we have modified numerous aspects of our logistics, transportation, supply chain, purchasing, and after-sale processes. Beginning in Q1 2020, we made numerous process updates across our operations worldwide, and adapted our fulfillment network, to implement employee and customer safety measures, such as enhanced cleaning and physical distancing, personal protective gear, disinfectant spraying, and temperature checks. We will continue to prioritize employee and customer safety and comply with evolving state and local standards as well as to implement standards or processes that we determine to be in the best interests of our employees, customers, and communities.

Due to the COVID-19 pandemic, our subsidiary Sichuan Wetouch was temporarily shut down from early February 2020 to early March 2020 in accordance with the requirement of the local governments. Our business was negatively impacted and generated lower revenue and net income in 2020. The Company has taken proactive measures to promote products to new customers and entering more regions during the six-month period ended June 30, 2021. The extent of the impact of COVID-19 on the Company’s results of operations and financial condition will depend on the virus’ future developments, including the duration and spread of the outbreak and the impact on the Company’s customers, which are still uncertain and cannot be reasonably estimated at this point of time.

Competitive Strengths

We are dedicated to the production of high quality products that are tailored to customers’ requirements and commercial needs. Our competitive strengths include:

| ● | Our economy of scale lowers our cost and appeals to big clients with large quantity purchase orders; |

| ● | Our centralized manufacturing facility enables us to produce all different products within the same location with batch consistency and quality assurance; |

| ● | Our proprietary technology allows us to produce touchscreens with high light-transmittance ratio and stability, low maintenance with minimal or no need of recalibration after production, long life span, anti-interference, anti-corrosion and multi-touch capability, supporting up to 20 points of contact with the screen and 20 gestures, and in different structures and sizes for a wide range of different applications. |

Our Growth Strategies

We will continue to adhere to our business principles of providing high quality and safe products to our consumers and promoting social responsibility. We believe that our pursuit of these goals will lead to sustainable growth driven by our capacity expansion based on market demand, solidify our position in the industry, and create long-term value for our shareholders, employees and other stakeholders.

| ● | Improve existing technology. We intend to improve our existing technology and occupy more market share. Our products are categorized into the following three main structures: GG (Glass + Glass), GFF (Glass + Film + Film), and PG (Plastic Glass). GG is mainly used in the automobile and banking and finance industries. We plan to make technological improvements on GG structure and mainly focus on improving its production capability and delivering quality products for brand customers. GFF is mostly applied in industrial HMI and lottery and gaming industries. We plan to continue to concentrate on high-end industrial HMI products. PG is primarily employed in smart home, robotics and charging stations industries. We plan to upgrade the production line of PG to improve its production capability and create greater adaptability to changes in product size. We have developed the industry 4.0 intelligent system, which is still under testing as of the date of this prospectus. Upon successfully passing the testing phase and registering the patent, we plan to apply it to various manufacturing industries. As of the date of this prospectus, we have sufficient funds to effectuate our plans. |

| ● | Solidify our industry position by gaining additional market share. Our goal is to strengthen our market position and accelerate our expansion by expanding our scale and gaining additional market share. We plan to increase investment in our business and expand our production capacity through horizontal or vertical acquisitions, strategic partnerships and joint ventures. We plan to invest additional capital in technology research and development and acquiring new equipment to increase production capacity. In addition, we plan to participate in more expos or exhibitions domestically and internationally. With more exposure and promotion, we believe our product and brand will be better recognized. Currently we have no agreements or letters of intent for any acquisitions, partnerships or ventures. |

| 5 |

| ● | Uphold our commitment to product quality. We intend to uphold our commitment to product quality to ensure consistently high standards throughout our operations. We intend to achieve greater traceability of our products and maintain the highest quality standards in all of our business units. To this end, we plan to continue to maintain our quality monitoring systems across the entire operation by strictly selecting suppliers and meeting clients’ technology requirements, closely monitoring quality, keeping records of everyday operations, and complying with national and local laws and regulations on product quality, employees, and environment sustainability. We believe such practice largely conforms with the industry’s best practices in China. |

| ● | Expand our sales and distribution network. We hope to expand our sales and distribution network to penetrate new geographic markets, further gaining market share in existing markets and accessing a broader range of customers. We will continue to expand our sales network, leveraging our local resources to quickly enter new markets, while also minimizing requirements for capital outlay. We plan to focus on brand clients and concentrate on high-end industry such as industrial HMI, banking and finance, medical instruments, military, aviation, and POS and increase our presence in both new and existing markets. |

| ● | Enhance our ability to attract, incentivize and retain talented professionals. We believe our success greatly depends on our ability to attract, incentivize and retain talented professionals. With a view to maintaining and improving our competitive advantage in the market, we plan to implement a series of initiatives to attract additional and retain mid- to high-level personnel, including formulating a market-oriented employee compensation structure and implementing a standardized multi-level performance review mechanism. |

Competition

The markets for touchscreen products are highly competitive and subject to rapid technological change. We believe that the principal competitive factors in its markets are product characteristics such as touch performance, durability, optical clarity and price, as well as supplier characteristics such as quality, service, delivery time and reputation. We believe that we compete favorably with respect to these factors, although there can be no assurance that the Company will be able to continue to compete successfully in the future.

Despite that touchscreen products are highly competitive as a whole, we face fewer competitors, as we produce medium to large size touchscreens which are specially tailored to certain industries, such as industrial HMI, gaming, financing, lottery, automotive, medical, and POS, among others, and require more stable supply and longer guaranty and life span, compared with small size touchscreens, which are characterized by shorter life cycles and guaranty but more demand in quantity.

We believe the following companies may be our competitors:

| ● | Apex Material Technology Corp., founded in 1998, is committed to the development and innovation of resistive and projected capacitive (PCI or PCAP) total touch solutions. With its headquarter based in Keelung, Taiwan and a subsidiary located in Milwaukee, Wisconsin, it designs and manufactures advanced high-performance touch products for industrial and medical applications. Compared with us, although it has a longer history and geographical advantages, it mainly focuses on resistive touch panels and recently started production of capacitive touchscreens mostly applicable to the industrial HMI and medical industries, while our products are more widely used in a variety of industries. |

| ● | Elo Touch Systems Inc., based and headquartered in the United States, has a history of over 40 years for the production of touchscreens. Its product portfolio includes a broad selection of interactive touchscreen displays from 10-70 inches, all-in-one touchscreen computers, OEM touchscreens and touchscreen controllers and touchscreen monitors. Compared with us, although it has a longer history and geographical advantages when it comes to the competition for U.S. customers and other international customers, it recently started the production of capacitive touchscreens mostly applicable to POS and inquiry machines, while our products are more widely used in a variety of industries. |

| ● | AbonTouch System Inc, established in 2005, mainly focuses on manufacturing and sales of mid to large size (7”~86”) “Projective Capacitive Sensors,” (7”~21.5”) “Five-Wire Resistive Zero-Bezel Touch Panels” and (5”~21.5”) “Five-Wire Resistive Touch Panels.” Compared with us, although it has a longer history and geographical advantages, it mainly focuses on resistive touch panels and recently started production of capacitive touchscreens mostly applicable to POS, inquiry machines and industrial HMI, while our products are more widely used in a variety of industries. |

| 6 |

Risk Factors Summary

Our business is subject to a number of risks. You should be aware of these risks before making an investment decision. These risks are discussed more fully in the section of this registration statement titled “Risk Factors”. These risks include, among others, the following:

| ● | The current COVID-19 pandemic, as well as other epidemics, natural disasters, terrorist activities, political unrest, and other outbreaks could disrupt our delivery and operations, which could materially and adversely affect our business, financial condition, and results of operations. | |

| ● | We are heavily dependent on our top customers. If we fail to acquire new customers or retain existing customers in a cost-effective manner, our business, financial condition and results of operations may be materially and adversely affected. | |

| ● | We have a significant amount of accounts receivable, which could become uncollectible. | |

| ● | Failure to maintain the quality and safety of our products could have a material and adverse effect on our reputation, financial condition and results of operations. | |

| ● | We face intense competition in the touchscreen industry in general. If we fail to compete effectively, we may lose market share and customers, and our business, financial condition and results of operations may be materially and adversely affected. | |

| ● | If we do not obtain substantial additional financing, our ability to execute on our business plan as outlined in this prospectus will be impaired. | |

| ● | Failure to secure a new piece of parcel for the construction of our new buildings and facilities, and failure to acquire and install new production lines on the new parcel, our business, financial condition and results of operations may be materially and adversely affected. | |

| ● | Mr. Guangde Cai, our Chairman, beneficially owns 21.23% of our outstanding shares and his interests may differ from the interests of other shareholders, which could cause a material decline in the value of our shares. | |

| ● | Any adjustment of related party transaction pricing could lead to additional taxes, and therefore substantially reduce our consolidated net income and the value of your investment. | |

| ● | If our preferential tax treatments and government subsidies are revoked or become unavailable or if the calculation of our tax liability is successfully challenged by the PRC tax authorities, we may be required to pay tax, interest and penalties in excess of our tax provisions. | |

| ● | A significant interruption in the operations of our third-party suppliers could potentially disrupt our operations. | |

| ● | We face the risk of fluctuations in the cost, availability and quality of our raw materials, which could adversely affect our results of operations. | |

| ● | We are dependent upon key executives and highly qualified managers and we cannot assure their retention. | |

| ● | We do not have long-term contracts with our suppliers and they can reduce order quantities or terminate their sales to us at any time. | |

| ● | If we fail to adopt new technologies to evolving customer needs or emerging industry standards, our business may be materially and adversely affected. | |

| ● | We may experience significant liability claims or complaints from customers, or adverse publicity involving our products and our services. | |

| ● | PRC regulations relating to the establishment of offshore special purpose companies by PRC residents may subject our PRC resident beneficial owners or our PRC subsidiary to liability or penalties, limit our ability to inject capital into our PRC subsidiary, limit our PRC subsidiary’ ability to increase their registered capital or distribute profits to us, or may otherwise adversely affect us. | |

| ● | We have no business liability or disruption insurance, which could expose us to significant costs and business disruption. | |

| ● | We may incur liabilities that are not covered by insurance. |

| 7 |

| ● | Adverse regulatory developments in China may subject us to additional regulatory review and expose us to government restrictions, and additional disclosure requirements and regulatory scrutiny to be adopted by the SEC in response to risks related to recent regulatory developments in China may impose additional compliance requirements for companies with significant China-based operations, all of which could increase our compliance costs, subject us to additional disclosure requirements, and/or suspend or terminate our future securities offerings, making capital-raising more difficult. | |

| ● | Recent joint statement by the SEC and the Public Company Accounting Oversight Board (United States), or the PCAOB, proposed rule changes submitted by Nasdaq, and the newly enacted Holding Foreign Companies Accountable Act all call for additional and more stringent criteria to be applied to emerging market companies upon assessing the qualification of their auditors, especially the non-U.S. auditors who are not inspected by the PCAOB. These developments could add uncertainties to the trading of our ADSs on U.S. stock exchanges. | |

| ● | Changes in China’s economic, political or social conditions or government policies could have a material adverse effect on our business and operations. | |

| ● | Uncertainties with respect to the PRC legal system and changes in laws and regulations in China could adversely affect us. | |

| ● | You may experience difficulties in effecting service of legal process, enforcing foreign judgments or bringing actions in China against us or our management based on foreign laws. | |

| ● | Government control of currency conversion may affect the value of your investment. | |

| ● | Fluctuations in exchange rates could have a material and adverse effect on our results of operations and the value of your investment. | |

| ● | Governmental control of currency conversion may limit our ability to utilize our revenues effectively and affect the value of your investment. | |

| ● | Certain political and economic considerations relating to the PRC could adversely affect our Company. | |

| ● | The Chinese government exerts substantial influence over the manner in which we must conduct our business activities. | |

| ● | The PRC government may issue further restrictive measures in the future. | |

| ● | Interpretation of PRC laws and regulations involve uncertainty. |

Corporate Information

We are incorporated under the laws of Nevada. Our principal executive offices are located at No. 29, Third Main Avenue, Shigao Town, Renshou County, Meishan, Sichuan, China. Our telephone number is (86) 028-37390666. Our Websites are www.wetouchinc.com and www.wetouch.com.cn, the latter of which is only accessible in the PRC. Information contained in, or that can be accessed through, our Websites is not incorporated by reference into this registration statement, and you should not consider information on our Websites to be part of this registration statement.

THE OFFERING

| Issuer | Wetouch Technology Inc. | |

| Common stock outstanding prior to the Underwritten Offering | 31,811,523 shares | |

| Common stock offered by us in the Underwritten Offering | shares of our common stock. ( shares if the underwriters exercise their over-allotment option in full). | |

| Offering price for shares sold in the Underwritten Offering | $ per share | |

| Over-allotment option | The underwriters have an option for a period of 45 days to purchase up to additional shares of our common stock (15% of the number of shares sold in the Underwritten Offering) to cover over-allotments, if any, at the public offering price, less underwriting discounts and commissions. |

| 8 |

| Common stock outstanding after completion of the Underwritten Offering | shares. ( shares if the underwriters exercise their over-allotment option in full). | |

| Common Stock issuable upon the exercise of Underwriter’s Warrants | The registration statement of which this prospectus is a part also registers for sale common stock underlying warrants (the “Underwriter’s Warrants”) to purchase shares issuable to the Representatives, which is equal to 6.0% of the number of shares sold in the Underwritten Offering, as a portion of the underwriting compensation payable to the Representatives in connection with the Underwritten Offering. The Underwriter’s Warrants will be exercisable at any time, and from time to time, in whole or in part, during the four and one-half year period commencing 180 days following the closing date of the Underwritten Offering at an exercise price of $ (125.0% of the public offering price per share). | |

| Lock-up Agreements | We and our directors, officers and certain principal shareholders have agreed with the Underwriter not to offer for sale, issue, sell, contract to sell, pledge or otherwise dispose of any of our common stock or securities convertible into common stock for a period of 180 days after the date of this prospectus. See “Underwriting – Lock-Up Agreements.” | |

| Use of proceeds | We intend to use the net proceeds from the Underwritten Offering after deducting the estimated underwriting discounts and estimated offering expenses for sales and marketing activities, product development, and capital expenditures, and we may also use a portion of the net proceeds for the acquisition of, or investment in, technologies, solutions or businesses that complement our business, and for working capital and general corporate purposes. See “Use of Proceeds” on page 28 of this prospectus. | |

| OTCQB Symbol | WETH | |

| Proposed Nasdaq Symbol | WETH | |

| Risk factors | Investing in our securities involves a high degree of risk. See “Risk Factors” beginning on page 10. |

Unless we indicate otherwise, the number of shares of our common stock that will be outstanding immediately after the Underwriting Offering is based on 31,811,523 shares of common stock outstanding as of September 13, 2021. The number excludes the following:

| (i) | 841,440 shares of common stock issuable upon the exercise of outstanding common stock purchase warrants; and | |

| (ii) | shares of common stock underlying the warrants to be issued to the Representatives in connection with this offering. |

Except as otherwise indicated herein, all information in this prospectus assumes no exercise by the underwriter of its over-allotment option to purchase additional shares.

| 9 |

RISK FACTORS

Investing in our common stock involves a high degree of risk. Before investing in our common stock, you should carefully consider the risks described below, as well as the other information in this prospectus, including our consolidated financial statements and the related notes. In addition, we may face additional risks and uncertainties not currently known to us, or which as of the date of this registration statement we might not consider significant, which may adversely affect our business. If any of the following risks occur, our business, financial condition and results of operations could be materially adversely affected. In such case the trading price of our common stock could decline due to any of these risks or uncertainties, and you may lose part or all of your investment.

Risks Related to Our Business and Industry

The current COVID-19 pandemic, as well as other epidemics, natural disasters, terrorist activities, political unrest, and other outbreaks could disrupt our delivery and operations, which could materially and adversely affect our business, financial condition, and results of operations.

For the six months ended June 30, 2021, our revenues were approximately $25.9 million, an increase of 17.1% from $8.8 million for the six months ended June 30, 2020. The current COVID-19 pandemic adversely affected many aspects of our business, including production, supply chain, and sales and delivery. Our manufacturing facility underwent temporary yet prolonged closure in February 2020 as part of China’s nationwide efforts to contain the spread of the novel coronavirus. Even though our business is currently operational, our production capacity, delivery, warranty services including after-sale services and technical support, and operational efficiency are still adversely affected by the COVID-19 pandemic due to insufficient workforce in production, sales, and delivery as a result of temporary travel restrictions in China and the necessity to comply with disease control protocols in our business establishments and manufacturing facility. Our suppliers’ abilities to timely deliver raw materials, parts and components, or other services were also adversely affected for similar reasons. The global spread of COVID-19 may also affect our overseas sales. As a result of varying levels of travel and other restrictions for public health concerns in various regions of China, we also temporarily postponed the delivery of our products to our customers. While the duration of the impact of the pandemic on our business and related financial impacts cannot be reasonably estimated at this time, our results of operations for the first half of 2020 were adversely affected with potential continuing impacts on subsequent periods. In addition, we expect that the COVID-19 pandemic may adversely affect our manufacturing ability, our delivery and after-sale services in China, which may adversely affect our sales and delivery growth in 2020. COVID-19 has had a global economic impact on the financial markets. The global spread of COVID-19 pandemic may result in global economic distress, and the extent to which it may affect our results of operations will depend on future developments, which are highly uncertain and cannot be predicted. We cannot assure you that the COVID-19 pandemic can be eliminated or contained in the near future, or at all, or a similar outbreak will not occur again. If the COVID-19 pandemic and the resulting disruption to our business were to extend over a prolonged period, it could materially and adversely affect our business, financial condition, and results of operations.

Global pandemics, epidemics in China or elsewhere in the world, or fear of spread of contagious diseases, such as Ebola virus disease (EVD), coronavirus disease 2019 (COVID-19), Middle East respiratory syndrome (MERS), severe acute respiratory syndrome (SARS), H1N1 flu, H7N9 flu, and avian flu, as well as hurricanes, earthquakes, tsunamis, or other natural disasters could disrupt our business operations, reduce or restrict our supply of products and services, incur significant costs to protect our employees and facilities, or result in regional or global economic distress, which may materially and adversely affect our business, financial condition, and results of operations. Actual or threatened war, terrorist activities, political unrest, civil strife, and other geopolitical uncertainty could have a similar adverse effect on our business, financial condition, and results of operations. Any one or more of these events may impede our production and delivery efforts and adversely affect our sales results, or even for a prolonged period of time, which could materially and adversely affect our business, financial condition, and results of operations.

We are also vulnerable to natural disasters and other calamities. We cannot assure you that we are adequately protected from the effects of fire, floods, typhoons, earthquakes, power loss, telecommunications failures, break-ins, war, riots, terrorist attacks, or similar events. Any of the foregoing events may give rise to interruptions, damage to our property, delays in production, breakdowns, system failures, technology platform failures, or internet failures, which could cause the loss or corruption of data or malfunctions of our manufacturing facility as well as adversely affect our business, financial condition, and results of operations.

We are heavily dependent on our top customers. If we fail to acquire new customers or retain existing customers in a cost-effective manner, our business, financial condition and results of operations may be materially and adversely affected.

We are heavily dependent on our top customers. We currently sell our products primarily through direct customers in the PRC and to some extent, the overseas customers in European countries and East Asia such as South Korea and Taiwan. For the year ended December 31, 2020 and 2019, our top five customers accounted for an aggregate of approximately 73.31% and 74.7%, respectively, of our revenues.

| 10 |

Our ability to cost-effectively attract new customers and retain existing customers, especially our top customers, is crucial to driving net revenues growth and achieving profitability. We have invested significantly in branding, sales and marketing to acquire and retain customers since our inception. For example, we attend domestic and international expos and exhibitions in marketing our products and attracting new customers. We also expect to continue to invest significantly to acquire new customers and retain existing ones, especially our top customers. There can be no assurance that new customers will stay with us, or the net revenues from new customers we acquire will ultimately exceed the cost of acquiring those customers. In addition, if our existing customers, especially our existing top customers no longer find our products appealing, or if our competitors offer more attractive products, prices, discounts or better customer services, our existing customers may lose interest in us, decrease their orders or even stop ordering from us. If we are unable to retain our existing customers, especially our top customers or to acquire new customers in a cost-effective manner, our revenues may decrease and our results of operations will be adversely affected.

We have a significant amount of accounts receivable, which could become uncollectible.

As of June 30, 2021, we had approximately 11.6 million in accounts receivable. Our accounts receivable primarily includes balance due from customers when our products are sold and delivered to customers. Our customers are required to make full payment within three to five months from delivery date, although our industry typical payment term is 180 days from delivery. As a result of the COVID-19 outbreak in January 2020, collection activities from some of our customers affected by the pandemic resulted in longer payment terms. We impliedly granted extended payment terms until December 31, 2020 to some of our customers. As of December 31, 2020, we collected all overdue accounts receivable and resumed our typical payment term. Deteriorating conditions in, bankruptcies, or financial difficulties of a customer or within their industries generally may impair the financial condition of our customers and hinder their ability to pay us on a timely basis or at all, and accounts receivable are written off against allowances only after exhaustive collection efforts. The failure or delay in payment by one or more of our customers could reduce our cash flows and adversely affect our liquidity and results of operations.

Failure to maintain the quality and safety of our products could have a material and adverse effect on our reputation, financial condition and results of operations.

The quality and safety of our products are critical to our success. We pay close attention to quality control, monitoring each step in the process from procurement to production and from warehouse to delivery. Yet, maintaining consistent product quality depends significantly on the effectiveness of our quality control system, which in turn depends on a number of factors, including but not limited to the design of our quality control system, employee training to ensure that our employees adhere to and implement our quality control policies and procedures and the effectiveness of monitoring any potential violation of our quality control policies and procedures. There can be no assurance that our quality control system will always prove to be effective.

In addition, the quality of the products or services provided by our suppliers or service providers is subject to factors beyond our control, including the effectiveness and the efficiency of their quality control system, among others. There can be no assurance that our suppliers or service providers may always be able to adopt appropriate quality control systems and meet our stringent quality control requirements in respect of the products or services they provide. Any failure of our suppliers or service providers to provide satisfactory products or services could harm our reputation and adversely impact our operations. In addition, we may be unable to receive sufficient compensation from suppliers and service providers for the losses caused by them.

We face intense competition in the touchscreen industry in general. If we fail to compete effectively, we may lose market share and customers, and our business, financial condition and results of operations may be materially and adversely affected.

The touchscreen industry is intensely competitive in general. We face few competition as we produce medium to large size capacitive touchscreens which are specially tailored to certain industries, such as industrial HMI, gaming, financing, lottery, automotive, medical, and POS, etc., and requires more stable supply, longer guaranty and life span, compared with small size touchscreens which is characteristic with shorter life cycle and guaranty but more demand in quantity. However, we still have some competitors competing in China and globally with us. Our competitors may have more financial, technical, geographical advantage, marketing and other resources than we do and may be more experienced and able to devote greater resources to the development, promotion and support of their business. Some competitors are well-established in China and globally and any defensive measures they take in response to our expansion could hinder our growth and adversely affect our sales and results of operations.

| 11 |

Furthermore, increased competition may reduce our market share and profitability and require us to increase our sales and marketing efforts and capital commitment in the future, which could negatively affect our results of operations or force us to incur further losses. Although we have accumulated some and continuously growing our customer base, there is no assurance that we will be able to continue to do so in the future against current or future competitors, and such competitive pressures may have a material adverse effect on our business, financial condition and results of operations.

If we do not obtain substantial additional financing, our ability to execute on our business plan as outlined in this prospectus will be impaired.

Due to the withdrawal of the land use right to the Property and cancellation of our ownership certificates pertaining to the buildings on the Property by the local government pursuant to the Guidelines and the Compensation Agreement, we are actively searching for an appropriate parcel in Chengdu Medicine City (Technology Park), Wenjiang District, Chengdu for the construction of our new production facilities and office buildings. As of the date of this prospectus, our management estimates that our capital needs for this acquisition and construction will be approximately RMB170.0 million ($26.2 million), but there is no assurance that the estimated amount is sufficient to achieve our goals. We may need additional financing for our business development.

In addition, our plans call for significant new investments in research and development, marketing, expanded productions capacity, and working capital for raw materials and other items. Should our capital needs be higher than our estimation, we will be required to seek additional investments, loans or debt financing to fully pursue our business plans. Such additional investment may not be available to us on terms which are favorable or acceptable. Should we be unable to meet our full capital needs, our ability to fully implement our business plan will be impaired.

Failure to secure a new piece of parcel for the construction of our new buildings and facilities, and failure to acquire and install new production lines on the new parcel, our business, financial condition and results of operations may be materially and adversely affected.

As of the date of this prospectus, our use right to the Property was withdrawn by the local government and all ownership certificates pertaining to the buildings on the Property were returned to the local government for cancellation.

In order to minimize the interruption of our business, Sichuan Vtouch entered into a Leaseback Agreement with Sichuan Renshou on March 16, 2021. The Leaseback Agreement entitles us to lease back the Properties commencing from April 1, 2021 until December 31, 2021, at a monthly rent of RMB300,000 (approximately $46,154).

As of the date of this prospectus, we are actively searching for an appropriate parcel in Chengdu Medicine City (Technology Park), Wenjiang District, Chengdu for the construction of our new production facilities and office buildings. We estimate the acquisition of the new parcel and new production lines and construction of the new facilities and office buildings on the new parcel will be completed prior to December 31, 2021, but there is no assurance and we may need extended time to achieve our business plan. If we fail to secure such acquisition and construction prior to December 31, 2021 and the extended period, if any, our business, financial condition and results of operations may be materially and adversely affected.

Mr. Guangde Cai, our Chairman, beneficially owns 21.23% of our outstanding shares and his interests may differ from the interests of other shareholders, which could cause a material decline in the value of our shares.

Since Mr. Guangde Cai, our Chairman, beneficially owns 21.23% of our outstanding shares, he could have significant influence on determining the outcome of any matters submitted to the shareholders for approval, including mergers, consolidations, the election of directors and other significant corporate actions. Without his consent, we may be prevented from entering into transactions that could be beneficial to us or our minority shareholders. His interest may differ from the interests of our other shareholders. The concentration in the ownership of our shares may cause a material decline in the value of our shares.

We cannot assure you that Mr. Cai will act in our best interests given Mr. Cai’s ability to control related parties, such as Chengdu Wetouch, Meishan Wetouch and Xinjiang Wetouch Electronic Technology Co., Ltd. See “Certain Relationships and Related Transactions, and Director Independence.”

Any adjustment of related party transaction pricing could lead to additional taxes, and therefore substantially reduce our consolidated net income and the value of your investment.

The tax regime in China is rapidly evolving and there is significant uncertainty for taxpayers in China as PRC tax laws may be interpreted in significantly different ways. The PRC tax authorities may assert that we or our subsidiaries owe and/or are required to pay additional taxes on previous or future revenue or income. In particular, under applicable PRC laws, rules and regulations, arrangements and transactions among related parties may be subject to audit or challenge by the PRC tax authorities. If the PRC tax authorities determine that any contractual arrangements were not entered into on an arm’s length basis and therefore constitute a favorable transfer pricing, the PRC tax liabilities of the relevant subsidiaries could be increased, which could increase our overall tax liabilities. In addition, the PRC tax authorities may impose late payment interest. Our net income may be materially reduced if our tax liabilities increase.

| 12 |

If our preferential tax treatments and government subsidies are revoked or become unavailable or if the calculation of our tax liability is successfully challenged by the PRC tax authorities, we may be required to pay tax, interest and penalties in excess of our tax provisions.

The Chinese government has provided tax incentives to our former subsidiary in China, Sichuan Wetouch, including reduced enterprise income tax rates. For example, under the PRC Enterprise Income Tax Law and its implementation rules, the statutory enterprise income tax rate is 25%. However, the income tax of an enterprise that has been determined to be a qualified enterprise located in western region of PRC can be reduced to a preferential rate of 15%. The qualification of preferential tax rate is effective for a renewable three-year permitted. As we have dissolved Sichuan Wetouch, and its business and operations have been assumed by our PRC subsidiary Sichuan Vtouch, Sichuan Vtouch has reapplied for the preferential rate of 15% as a qualified enterprise. Such application is currently pending with the PRC tax authorities. If our PRC subsidiary’s application for the qualification of preferential tax rate benefit is not approved, our PRC subsidiary will be subject to the statutory enterprise income tax rate of 25%. Further, in the ordinary course of our business, we are subject to complex income tax and other tax regulations, and significant judgment is required in the determination of a provision for income taxes. Although we believe our tax provisions are reasonable, if the PRC tax authorities successfully challenge our position and we are required to pay tax, interest, and penalties in excess of our tax provisions, our financial condition and results of operations would be materially and adversely affected.

A significant interruption in the operations of our third-party suppliers could potentially disrupt our operations.

We have limited control over the operations of our third-party suppliers and other business partners and any significant interruption in their operations may have an adverse impact on our operations. For example, a significant interruption in the operations of our supplier’s manufacturing facilities could cause delay or termination of shipment of the raw materials to us, which may cause delay or termination of shipment of our products to our customers, thus resulting in penalties or fines due to our breach of contract. If we could not solve the impact of the interruptions of operations of our third-party suppliers, our business operations and financial results may be materially and adversely affected.

We face the risk of fluctuations in the cost, availability and quality of our raw materials, which could adversely affect our results of operations.

The cost, availability and quality of the raw materials, such as indium tin oxide glasses, panels, are important to our operations. If the cost of raw materials increases due to large market price fluctuation or due to any other reason, our business and results of operations could be adversely affected. Lack of availability of these raw materials, whether due to shortages in supply, delays or interruptions in processing, failure of timely delivery or otherwise, could interrupt our operations and adversely affect our financial results.

We are dependent upon key executives and highly qualified managers and we cannot assure their retention.

Our success depends, in part, upon the continued services of key members of our management. Our executives’ and managers’ knowledge of the market, our business and our Company represents a key strength of our business, which cannot be easily replicated. The success of our business strategy and our future growth also depend on our ability to attract, train, retain and motivate skilled managerial, sales, administration, development and operating personnel.

There can be no assurance that our existing personnel will be adequate or qualified to carry out our strategy, or that we will be able to hire or retain experienced, qualified employees to carry out our strategy. The loss of one or more of our key management or operating personnel, or the failure to attract and retain additional key personnel, could have a material adverse effect on our business, financial condition and results of operations.

We do not have long-term contracts with our suppliers and they can reduce order quantities or terminate their sales to us at any time.

We do not have long term contracts with our suppliers. At any time, our suppliers can reduce the quantities of products they sell to us, or cease selling products to us altogether. Such reductions or terminations could have a material adverse impact on our revenues, profits and financial condition.

| 13 |

If we fail to adopt new technologies to evolving customer needs or emerging industry standards, our business may be materially and adversely affected.

To remain competitive, we must continue to stay abreast of the constantly evolving industry trends and to enhance and improve our technology accordingly. Our success will depend, in part, on our ability to identify, develop, acquire or license leading technologies useful in our business. There can be no assurance that we will be able to use new technologies effectively or meet customer’s requirements. If we are unable to adapt in a cost-effective and timely manner in response to changing market conditions or customer preferences, whether for technical, legal, financial or other reasons, our business may be materially and adversely affected.

We may experience significant liability claims or complaints from customers, or adverse publicity involving our products and our services.

We face an inherent risk of liability claims or complaints from our customers. We take our customers’ complaints seriously and endeavor to reduce such complaints by implementing various remedial measures. Nevertheless, we cannot assure you that we can successfully prevent or address all customer complaints.

Any complaints or claims against us, even if meritless and unsuccessful, may divert management attention and other resources from our business and adversely affect our business and operations. Customers may lose confidence in us and our brand, which may adversely affect our business and results of operations. Furthermore, negative publicity including but not limited to negative online reviews on social media and crowd-sourced review platforms, industry findings or media reports related to safety and quality of our products, whether or not accurate, and whether or not concerning our products, can adversely affect our business, results of operations and reputation.

PRC regulations relating to the establishment of offshore special purpose companies by PRC residents may subject our PRC resident beneficial owners or our PRC subsidiary to liability or penalties, limit our ability to inject capital into our PRC subsidiary, limit our PRC subsidiary’ ability to increase their registered capital or distribute profits to us, or may otherwise adversely affect us.