As filed with the U.S. Securities and Exchange Commission on August 31, 2021

Registration No. 333-

UNITED

STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM F-1

REGISTRATION

STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Kepuni Holdings Inc.

(Exact name of registrant as specified in its charter)

| Cayman Islands | Not Applicable | Not Applicable | ||

| (State

or other jurisdiction of incorporation or organization) |

(Primary

Standard Industrial Classification Code Number) |

(I.R.S.

Employer Identification Number) |

No. 318 Yongping Road,

Science and Technology Industrial Park

Taizhou City, Jiangsu Province

People’s

Republic of China, 225300

+86-52382988888

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

(Name, address, including zip code, and telephone number, including area code, of agent for service)

With a Copy to:

William S. Rosenstadt, Esq. Mengyi “Jason” Ye, Esq. Yarona L. Yieh, Esq. Ortoli

Rosenstadt LLP |

Benjamin A. Tan Sichenzia Ross Ference LLP 1185 6th Avenue, 37th Floor New York, NY 10036 212-930-9700 |

Approximate date of commencement of proposed sale to the public: Promptly after the effective date of this registration statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box. ☐

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933

Emerging growth company ☒

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

CALCULATION OF REGISTRATION FEE

| Title of Each Class of Securities to be Registered | Proposed Maximum Aggregate Offering Price(1) | Amount of Registration Fee(2) | ||||||

| Ordinary Shares, par value US$0.001 per share(3) | US$ | 28,750,000 | US$ | 3,136.63 | ||||

| Underwriters’ Warrants(4) | - | - | ||||||

| Ordinary Shares underlying Underwriters’ Warrants | US$ | 2,012,500 | US$ | 219.56 | ||||

| Total | US$ | 30,762,500 | US$ | 3,356.19 | ||||

| (1) | Estimated solely for the purpose of calculating the amount of the registration fee in accordance with Rule 457(a) under the Securities Act. Includes the offering price attributable to additional ordinary shares that the underwriters have the option to purchase to cover over-allotments, if any. |

| (2) | Calculated pursuant to Rule 457(a) under the Securities Act, based on an estimate of the proposed maximum aggregate offering price. |

| (3) | In accordance with Rule 416(a), we are also registering an indeterminate number of additional ordinary shares that shall be issuable pursuant to Rule 416 to prevent dilution resulting from share splits, share dividends or similar transactions. |

| (4) | We have agreed to issue to the Underwriter and to register herein warrants to purchase up to ordinary shares (equal to seven percent (7%) of the ordinary shares sold in this offering, inclusive of the Underwriter Over-Allotment option to purchase an additional ordinary shares) and to also register herein such underlying ordinary shares. The warrants will be at any time, and from time to time, in whole or in part, commencing from the closing of the offering and expiring five years from the effectiveness of the offering. The warrants are exercisable at 100% of the offering price of the ordinary shares. The Underwriter Warrant shall not be callable or cancellable. |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to such Section 8(a), may determine.

The information in this preliminary prospectus is not complete and may be changed. We may not sell the securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities, and we are not soliciting any offer to buy these securities in any jurisdiction where such offer or sale is not permitted.

| SUBJECT TO COMPLETION | PRELIMINARY

PROSPECTUS DATED [*], 2021 |

Kepuni Holdings Inc.

[*] Ordinary Shares

This is the initial public offering of our ordinary shares and we are offering ordinary shares, par value $0.001 per share. The offering price of our ordinary shares in this offering will be between US$ and US$ per share. Prior to this offering, there has been no public market for our ordinary shares.

We plan to list our ordinary shares on the Nasdaq Capital Market, or NASDAQ, under the symbol “KPNT”. NASDAQ might not approve such application, and if our application is not approved, this offering cannot be completed.

We are an “emerging growth company” as defined under federal securities laws and, as such, will be subject to reduced public company reporting requirements. See “Prospectus Summary— Implications of Being an Emerging Growth Company and a Foreign Private Issuer” for additional information.

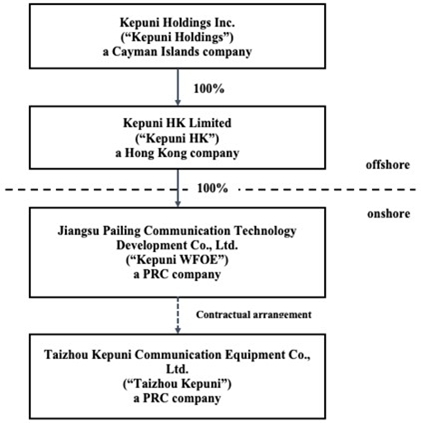

We are incorporated in the Cayman Islands. As a holding company with no material operations of our own, we conduct our operations in China through our variable interest entity, Taizhou Kepuni Communication Equipment Co. Ltd., or Taizhou Kepuni in the PRC. Neither we nor our subsidiaries own any share in Taizhou Kepuni. Instead, we control and receive the economic benefits of Taizhou Kepuni’s business operation through a series of contractual agreements, or the VIE Agreements. The VIE Agreements are designed to provide our wholly-foreign owned entity (“WFOE”), Jiangsu Pailing Communication Technology Co. Ltd., with the power, rights and obligations equivalent in all material respects to those it would possess as the principal equity holder of Taizhou Kepuni, including absolute control rights and the rights to the assets, property and revenue of Taizhou Kepuni. As a result of our indirect ownership in the WFOE and the VIE Agreements, we are regarded as the primary beneficiary of our VIE. The VIE structure is used to replicate foreign investment in Chinese-based companies where Chinese law prohibits direct foreign investment in the operating companies, and that investors may never directly hold equity interests in the Chinese operating entities. For a detailed description of the VIE Agreements, see “Corporate History and Structure” on page 2.

Because of our corporate structure, we are subject to risks due to uncertainty of the interpretation and the application of the PRC laws and regulations, including but not limited to limitation on foreign ownership of internet technology companies, and regulatory review of oversea listing of PRC companies through a special purpose vehicle, and the validity and enforcement of the VIE Agreements. We are also subject to the risks of uncertainty about any future actions of the PRC government in this regard. Our VIE Agreements may not be effective in providing control over Taizhou Kepuni. We may also subject to sanctions imposed by PRC regulatory agencies including Chinese Securities Regulatory Commission if we fail to comply with their rules and regulations. If the Chinse regulatory authorities disallow this VIE structure in the future, it will likely result in a material change in our financial performance and our results of operations and/or the value of our ordinary shares, which could cause the value of such securities to significantly decline or become worthless. For a detailed description of the risks relating to our VIE structure, doing business in the PRC, and the offering as a result of the structure, see “Risk Factors - Risks Relating to Our Corporate Structure,” “Risk Factors - Risks Relating to Doing Business in the PRC” and “Risk Factors – Risks Relating to this Offering,” beginning on page 11.

Additionally, we are subject to certain legal and operational risks associated with our VIE’s operations in China. PRC laws and regulations governing our current business operations are sometimes vague and uncertain, and therefore, these risks may result in a material change in our VIE’s operations, significant depreciation of the value of our ordinary shares, or a complete hinderance of our ability to offer or continue to offer our securities to investors. Recently, the PRC government initiated a series of regulatory actions and statements to regulate business operations in China with little advance notice, including cracking down on illegal activities in the securities market, enhancing supervision over China-based companies listed overseas using variable interest entity structure, adopting new measures to extend the scope of cybersecurity reviews, and expanding the efforts in anti-monopoly enforcement. Since these statements and regulatory actions are new, it is highly uncertain how soon legislative or administrative regulation making bodies will respond and what existing or new laws or regulations or detailed implementations and interpretations will be modified or promulgated, if any, and the potential impact such modified or new laws and regulations will have on our daily business operation, the ability to accept foreign investments and list on an U.S. or other foreign exchange.

Investing in our ordinary shares involves a high degree of risk. Before buying any ordinary shares, you should carefully read the discussion of material risks of investing in our ordinary shares in “Risk Factors” beginning on page 11 of this prospectus.

Neither the Securities and Exchange Commission nor any other regulatory body has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

| PER SHARE | TOTAL (4) | |||||||

| Initial public offering price(1) | $ | $ | ||||||

| Underwriting discounts(2) | $ | $ | ||||||

| Proceeds, before expenses, to us(3) | $ | $ | ||||||

| (1) | Initial public offering price per share is assumed as $ per share, which is the midpoint of the range set forth on the cover page of this prospectus. |

| (2) | We have agreed to pay the underwriter a discount equal to (i)7% of the gross proceeds of the offering. In addition, we have agreed to issue to the Underwriter, on the applicable closing date of this offering, warrants in an amount equal to 7% of the aggregate number of ordinary shares sold by us in this offering (the “Underwriter’s Warrants”) (not including over-allotment shares), exercisable at 100% of the offering price per ordinary share for five years. For a description of other terms of the Underwriter’s Warrants and a description of the other compensation to be received by the Underwriter, see “Underwriting” beginning on page 103. |

| (3) | Excludes fees and expenses payable to the Underwriter. The total amount of Underwriter’s expenses related to this offering is set forth in the section entitled “Underwriting.” |

| (4) | Assumes that the Underwriter does not exercise any portion of their over-allotment option. |

We expect our total cash expenses for this offering (including cash expenses payable to our Underwriter for its out-of-pocket expenses) to be approximately $ , exclusive of the above discounts. In addition, we will pay additional items of value in connection with this offering that are viewed by the Financial Industry Regulatory Authority, or FINRA, as underwriting compensation. These payments will further reduce proceeds available to us before expenses. See “Underwriting” beginning on page 103.

This offering is being conducted on a firm commitment basis. Boustead Securities, LLC, the Underwriter, is obligated to take and pay for all of the ordinary shares if any such ordinary shares are taken. We have granted the Underwriter an option for a period of 45 days after the closing of this offering to purchase up to 15% of the total number of our ordinary shares to be offered by us pursuant to this offering, solely for the purpose of covering over-allotments, at the initial public offering price less the underwriting discounts. If the underwriters exercise their option in full, the total underwriting discounts payable will be $ based on an assumed offering price of $ per ordinary share, and the total gross proceeds to us, before underwriting discounts and expenses, will be $ . If we complete this offering, net proceeds will be delivered to us on the applicable closing date. We will not be able to use such proceeds in China, however, until we complete capital contribution procedures that require prior approval from each of the respective local counterparts of China’s Ministry of Commerce, the State Administration for Industry and Commerce, and the State Administration of Foreign Exchange. See remittance procedures in the section titled “Use of Proceeds” beginning on page 45.

The Underwriter expects to deliver the ordinary shares against payment as set forth under “Underwriting”, on or about , 2021.

Boustead Securities, LLC

Prospectus dated , 2021.

TABLE OF CONTENTS

i

About this Prospectus

We and the Underwriter have not authorized anyone to provide any information or to make any representations other than those contained in this prospectus or in any free writing prospectuses prepared by us or on our behalf or to which we have referred you and which we have filed with the U.S. Securities and Exchange Commission (the “SEC”). We take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. This prospectus is an offer to sell only the ordinary shares offered hereby, but only under circumstances and in jurisdictions where it is lawful to do so. We are not making an offer to sell these securities in any jurisdiction where the offer or sale is not permitted or where the person making the offer or sale is not qualified to do so or to any person to whom it is not permitted to make such offer or sale. For the avoidance of doubt, no offer or invitation to subscribe for our ordinary shares is made to the public in the Cayman Islands. The information contained in this prospectus is current only as of the date on the front cover of the prospectus. Our business, financial condition, results of operations and prospects may have changed since that date.

Other Pertinent Information

Unless otherwise indicated or the context requires otherwise, references in this prospectus to:

| ● | “Affiliated Entities” are referred to our subsidiaries, and Taizhou Kepuni, our VIE; | |

| ● | “China” or the “PRC” are referred to the People’s Republic of China, excluding Taiwan and the special administrative regions of Hong Kong and Macau for the purposes of this prospectus only; | |

| ● | “Kepuni HK” is referred to Kepuni Limited, a limited liability company organized under the laws of Hong Kong; | |

| ● | “Kepuni WFOE” is referred to Jiangsu Pailing Communication Technology Co. Ltd, a limited liability company organized under the laws of the PRC, which is wholly-owned by Kepuni HK; | |

| ● | “Ordinary shares” refer to the ordinary shares of the Company, par value US$0.001 per share; | |

| ● | “VIE” is referred to Taizhou Kepuni, our variable interest entity; | |

| ● | “VIE Agreements” are referred to a series of contractual arrangements, including the Exclusive Business Cooperation Agreement, the Exclusive Option Agreement and the Share Pledge Agreement between Kepuni WFOE and VIE; | |

| ● | “we,” “us,” or “the Company” are referred to one or more of Kepuni Holdings Inc., and its subsidiaries and VIE, as the case may be; | |

| ● | “Taizhou Kepuni” is referred to Taizhou Kepuni Communication Equipment Co., Ltd., our VIE in the PRC. |

Our business is conducted by Taizhou Kepuni, our VIE in the PRC, using Renminbi, or RMB, the official currency of China. Our consolidated financial statements are presented in United States dollars. In this prospectus, we refer to assets, obligations, commitments and liabilities in our consolidated financial statements in United States dollars. These dollar references are based on the exchange rate of RMB to United States dollars, determined as of a specific date or for a specific period. Changes in the exchange rate will affect the amount of our obligations and the value of our assets in terms of United States dollars which may result in an increase or decrease in the amount of our obligations (expressed in dollars) and the value of our assets, including accounts receivable (expressed in dollars).

ii

The following summary is qualified in its entirety by, and should be read in conjunction with, the more detailed information and financial statements included elsewhere in this prospectus. In addition to this summary, we urge you to read the entire prospectus carefully, especially the risks of investing in our ordinary share, discussed under “Risk Factors,” before deciding whether to buy our ordinary share.

Overview

We are incorporated in the Cayman Islands on January 8, 2020. As a holding company with no material operations of our own, we conduct our operations in China through our variable interest entity, Taizhou Kepuni Communication Equipment Co. Ltd., or Taizhou Kepuni in the PRC. Neither we nor our subsidiaries own any share in Taizhou Kepuni. Instead, we control and receive the economic benefits of Taizhou Kepuni’s business operation through a series of contractual agreements, or the VIE Agreements. The VIE Agreements are designed to provide our wholly-foreign owned entity (“WFOE”), Jiangsu Pailing Communication Technology Co. Ltd, with the power, rights and obligations equivalent in all material respects to those it would possess as the principal equity holder of Taizhou Kepuni, including absolute control rights and the rights to the assets, property and revenue of Taizhou Kepuni. As a result of our indirect ownership in the WFOE and the VIE Agreements, we are regarded as the primary beneficiary of our VIE.

Taizhou Kepuni Communication Equipment Co., Ltd. is a high-tech enterprise integrating nautical communication electrical system solutions to provide services for the ocean. Founded in 2012, Taizhou Kepuni has specialized in the nautical communications and electronic equipment industries in China. Our factory has passed the certification of ISO 9001:2015.

We are a professional integrator of scheme design, research and development, and sales of supporting communication equipment for nautical engineering, as well as ship communication, navigation, driving control and power distribution.

Our products are customized products and we use a build to order, or BTO, business model which means a flexible order placing model for production scheduling, material procurement, and delivery arrangement according to different customer orders. We adopt an integrated business model to meet our clients’ needs. Customers firstly list their specified requirements to our sales department. The sales department later communicates with its technical department to evaluate the feasibility. After that, the production department produces samples and submits them to the quality inspection department for inspection. The quality inspection department will submit the issued material warranty and inspection report to the sales department. The sales department will submit the samples, inspection report, quality assurance, and quotation to the customer for verification. After receiving the customer’s confirmation, our procurement department will purchase the raw materials and the production department will produce the products. The inspection department will inspect and issue the inspection report. Lastly the production department will pack and deliver the products to the customer.

1

Corporate History and Structure

Kepuni Holding is a Cayman Islands exempted company incorporated on January 8, 2020. We conduct our business in China through Taizhou Kepuni, our VIE. The consolidation of our Company and our Affiliated Entities has been accounted for at historical cost and prepared on the basis as if the aforementioned transactions had become effective as of the beginning of the first period presented in the accompanying consolidated financial statements.

Kepuni HK was incorporated on February 24, 2020 under the law of Hong Kong SAR. Kepuni HK is our wholly-owned subsidiary and is currently not engaging in any active business and merely acting as a holding company.

Kepuni WFOE was incorporated on 27th September, 2020, under the laws of the People’s Republic of China. It is a wholly-owned subsidiary of Kepuni HK and a wholly foreign-owned entity under the PRC laws. The registered principal activity of the company is communication equipment sales and technical services.. Kepuni WFOE had entered into VIE Agreements with Taizhou Kepuni and its shareholders.

Taizhou Kepuni was incorporated on February 14, 2012 under the laws of the People’s Republic of China. It is registered under the category of the computer communications and electronic equipment manufacturing industries. The business scope of Taizhou Kepuni includes nautical communication equipment, nautical electrical equipment, ship automation, etc. Its registered capital amount is approximately $14,781,966 (RMB 100,000,000).

Contractual Agreements

Contractual Arrangements between Kepuni WFOE and Taizhou Kepuni

Due to PRC legal restrictions on foreign ownership, neither we nor our subsidiaries own any direct equity interest in Taizhou Kepuni. Instead, we control and receive the economic benefits of Taizhou Kepuni’s business operation through a series of contractual arrangements. Kepuni WFOE, Taizhou Kepuni and the shareholders of Taizhou Kepuni (“Taizhou Kepuni Shareholders”) entered into a series of contractual arrangements, also known as VIE Agreements, on October 18, 2020. The VIE agreements are designed to provide Kepuni WFOE with the power, rights and obligations equivalent in all material respects to those it would possess as the sole equity holder of Taizhou Kepuni, including absolute control rights and the rights to the assets, property and revenue of Taizhou Kepuni. If Taizhou Kepuni and its subsidiary or the Taizhou Kepuni Shareholders fail to perform their respective obligations under the contractual arrangements, we could be limited in our ability to enforce the contractual arrangements that give us effective control over Taizhou Kepuni and its subsidiary. Furthermore, if we are unable to maintain effective control, we would not be able to continue to consolidate the financial results of our variable interest entity in our financial statements.

2

Each of the VIE Agreements is described in detail below:

Exclusive Option Agreement

Under the Exclusive Option Agreement, the shareholders of Taizhou Kepuni irrevocably granted Kepuni WFOE (or its designee) an exclusive right to purchase, to the extent permitted under PRC law, once or at multiple times, at any time, a portion or whole of the equity interests or assets in Taizhou Kepuni held by the Taizhou Kepuni Shareholders (as hereinafter defined).

The agreement takes effect upon parties signing the agreement, and remains effective for ten years, extendable upon Kepuni WFOE or its designee’s discretion.

Exclusive Business Cooperation Agreement

Pursuant to the Exclusive Business Cooperation Agreement between Taizhou Kepuni and Kepuni WFOE, Kepuni WFOE provides Taizhou Kepuni with technical support, consulting services and other management services relating to its day-to-day business operations and management, on an exclusive basis, utilizing its advantages in technology, business management and information. For services rendered to Taizhou Kepuni by Kepuni WFOE under this agreement, Kepuni WFOE is entitled to collect a service fee that shall be calculated based upon service hours and multiple hourly rates provided by Kepuni WFOE. The service fee should approximately equal to Taizhou Kepuni’s net profit.

The Exclusive Business Cooperation Agreement shall remain in effect for ten years unless earlier terminated upon written confirmation from both Kepuni WFOE and Taizhou Kepuni before expiration. Otherwise, this agreement can only be extended by Kepuni WFOE and Taizhou Kepuni does not have the right to terminate the agreement unilaterally.

Share Pledge Agreement

Under the Share Pledge Agreement between Kepuni WFOE and certain shareholders of Taizhou Kepuni together holding 100% of the equity interests, of Taizhou Kepuni (“Taizhou Kepuni Shareholders”), the Taizhou Kepuni Shareholders pledged all of their equity interests in Taizhou Kepuni to Kepuni WFOE to guarantee the performance of Taizhou Kepuni’s obligations under the Exclusive Business Cooperation Agreement. Under the terms of the Share Pledge Agreement, in the event that Taizhou Kepuni breaches its contractual obligations under the Exclusive Business Cooperation Agreement, Kepuni WFOE, as pledgee, will be entitled to certain rights, including, but not limited to, the right to dispose of dividends generated by the pledged equity interests. The Taizhou Kepuni Shareholders also agreed that upon occurrence of any event of default, as set forth in the Share Pledge Agreement, Kepuni WFOE is entitled to dispose of the pledged equity interest in accordance with applicable PRC laws. The Taizhou Kepuni Shareholders further agree not to dispose of the pledged equity interests or take any actions that would prejudice Kepuni WFOE’s interest.

The Share Pledge Agreement shall be effective until the full payment of the service fees under the Business Cooperation Agreement has been made and upon termination of Taizhou Kepuni’s obligations under the Business Cooperation Agreement.

The purposes of the Share Pledge Agreement are to (1) guarantee the performance of Taizhou Kepuni’s obligations under the Exclusive Business Cooperation Agreement, (2) ensure the shareholders of Taizhou Kepuni do not transfer or assign the pledged equity interests, or create or allow any encumbrance that would prejudice Kepuni WFOE’s interests without Kepuni WFOE’s prior written consent and (3) provide Kepuni WFOE control over Taizhou Kepuni.

3

Currently, all of our beneficial owners, who are PRC residents and hold a total of 100% of equity interests of Taizhou Kepuni, have not completed the Circular 37 Registration. We will ask our prospective shareholders who are Chinese residents to make the necessary applications and filings as required by Circular 37. However, we cannot assure you that each of our shareholders who are PRC residents will, in the future, complete the registration process as required by Circular 37. Shareholders of offshore SPV who are PRC residents and who have not completed their registrations in accordance with Circular 37 are subject to certain absolute restrictions, under which they cannot contribute any registered or additional capital to such SPV for offshore financing purposes. In addition, these shareholders cannot repatriate any profits and dividends from the SPV to China either. Please see “Risk Factors- Our shareholders have not completed the Circular 37 Registration. We cannot provide any assurances that all of our shareholders who are Chinese residents will comply with our request to make or obtain any applicable registration or comply with other requirements required by Circular 37 or other related rules.”

Shareholders who have completed the Circular 37 registration would not be adversely affected and are allowed to contribute assets into the offshore special purpose vehicle and repatriate profits and dividends from them. Since Kepuni WFOE has completed its foreign exchange registration as a foreign investment enterprise, its ability to receive capital contribution, make distributions and pay dividends is not restricted.

Although we took every precaution available to effectively enforce the contractual and corporate relationship above, these contractual arrangements may still be less effective than direct ownership and that the Company may incur substantial costs to enforce the terms of the arrangements. For example, our VIEs and their shareholders could breach their contractual arrangements with us by, among other things, failing to conduct their operations in an acceptable manner or taking other actions that are detrimental to our interests. If we had direct ownership of our VIEs, we would be able to exercise our rights as a shareholder to effect changes in the board of directors of our VIEs, which in turn could implement changes, subject to any applicable fiduciary obligations, at the management and operational level. However, under the current contractual arrangements, we rely on the performance by our VIEs and their shareholders of their obligations under the contracts to exercise control over our VIEs. The shareholders of our consolidated VIEs may not act in the best interests of our company or may not perform their obligations under these contracts. In addition, failure of our VIE shareholders to perform certain obligations could compel the Company to rely on legal remedies available under PRC laws, including seeking specific performance or injunctive relief, and claiming damages, which may not be effective.

All of these contractual arrangements are governed by PRC law and provide for the resolution of disputes through arbitration in the PRC. The legal environment in the PRC is not as developed as in some other jurisdictions, such as the United States. As a result, uncertainties in the PRC legal system could limit our ability to enforce these contractual arrangements. In the event we are unable to enforce these contractual arrangements, we may not be able to exert effective control over our operating entities and we may be precluded from operating our business, which would have a material adverse effect on our financial condition and results of operations. In addition, there is uncertainty as to whether the courts of the Cayman Islands or the PRC would recognize or enforce judgments of U.S. courts against us or such persons predicated upon the civil liability provisions of the securities laws of the United States or any state. For a detailed description of the certainties of the VIE arrangements, see “Risk Factors – Risks Relating to Our Corporate Structure.”

Our Growth Strategy

| ● | Increase Sales – We plan to increase our sales by providing sufficient training to our sales professionals, making full use of our existing client base, taking initiatives to leverage our advantages, and maintaining existing customer relationships. |

| ● | Brand Recognition – We increase our brand recognition through publicity. We plan to promote our brand in terms of industry and geographic regions, including branching into medium and large shipyard markets from small and medium-sized shipyard markets and exploring long-term customer partnerships from the coastal region base. Additionally, we aim to promote ourselves by providing customers with satisfactory and high-quality customer service. We expect our expansion plan to bring sustainable development. |

| ● | Strategic & Management Development – We plan to set clear goals and strategies based on the company’s current situation. We plan to better adapt to market changes, build stronger teamwork, and better judge future trends. |

4

Competitive Advantages

We are committed to offering our customers superior product diversity, quality, and reliability. We offer a flexible order placing model to satisfy our customers’ specialized needs. We believe we have a number of competitive advantages that will enable us to maintain and further increase our market position in the industry for the national market. Our competitive strengths include:

| ● | Top-Notch Technology.. Our technology team has extensive experience and can provide the best solutions for customers promptly at reasonable prices. We have a specialized technology research and development team, which helped us integrate new technologies into product development. |

| ● | Integration of Intelligence System. We have established a sophisticated intelligence system by integrating artificial intelligence and a systematic management platform. |

| ● | Competitive Pricing. We provide reasonable and competitive pricing for our products and services. We also offer guarantees that our prices are comparable to those of the same quality provided by other companies in the industry in China. |

| ● | Rigorous Quality Control and Superior Customer Services. Our products play a critical role in various construction, infrastructure, equipment, and safety applications. Our emphasis on establishing a comprehensive quality management system, manufacturing processes, quality control testing, and product development help us deliver a high-quality product to our customers. We provide a one-year warranty and are dedicated to responding any customer service inquiries or complaints within 24 hours for all our products. |

| ● | Experienced Management Team. Our management team has extensive experience in the nautical electronics industry, has a keen focus on tracking changes in the business environment, and has strong judgment on the industry’s future development trends. Additionally, our production team and inspection team are equally skilled and experienced, ensuring the company’s efficient operation. |

| ● | Manufacture Capacity Efficient Operations with Significant Scale. We are a manufacturing integrator, specializing in integrated information management system design, ship internal communication system, ship automation control system, and ship driving control and power distribution system. Our expertise and our manufacturing facilities are the prerequisites that enable us to maintain lean manufacturing processes, which results in lower procurement costs for shipowners and shipyards, efficient shipyard design, and convenient customer services. |

5

Coronavirus (COVID-19) Update

The ongoing outbreak of a novel strain of coronavirus (COVID-19) has resulted in quarantines, travel restrictions, and the temporary closure of stores and business facilities globally for the past year. In March 2020, the World Health Organization declared the COVID-19 to be a pandemic. Given the rapidly expanding nature of the COVID-19 pandemic, and because substantially all of our business operations and our workforce are concentrated in China, we believe there is a risk that our business, results of operations, and financial condition will be adversely affected. Potential impact to our results of operations will also depend on future developments and new information that may emerge regarding the duration and severity of the COVID-19 and the actions taken by government authorities and other entities to contain the COVID-19 or mitigate its impact, almost all of which are beyond our control.

Our business returned to normal by the end of 2020. We have made some emergency plans for COVID-19 and reminded our personnel to pay attention to the COVID-19. Because of the uncertainty surrounding the COVID-19 outbreak, the business disruption and the related financial impact related to the outbreak of and response to the coronavirus cannot be reasonably estimated at this time. For a detailed description of the risks associated with the novel coronavirus, see “Risk Factors—Risks Relating to Our Business—Our business could be materially harmed by the ongoing coronavirus (COVID-19) pandemic.”

Implications of Being an Emerging Growth Company and a Foreign Private Issuer

As a company with less than $1.07 billion in revenue during our last fiscal year, we qualify as an “emerging growth company” as defined in the Jumpstart Our Business Startups Act, or JOBS Act, enacted in April 2012, and may take advantage of reduced reporting requirements that are otherwise applicable to public companies. These provisions include, but are not limited to:

| ● | being permitted to present only two years of audited financial statements and only two years of related Management’s Discussion and Analysis of Financial Condition and Results of Operations in our filings with the SEC; | |

| ● | not being required to comply with the auditor attestation requirements in the assessment of our internal control over financial reporting; | |

| ● | reduced disclosure obligations regarding executive compensation in periodic reports, proxy statements and registration statements; and | |

| ● | exemptions from the requirements of holding a nonbinding advisory vote on executive compensation and stockholder approval of any golden parachute payments not previously approved. |

We may take advantage of these provisions until the last day of our fiscal year following the fifth anniversary of the date of the first sale of our ordinary shares pursuant to this offering. However, if certain events occur before the end of such five-year period, including if we become a “large accelerated filer,” our annual gross revenues exceed $1.07 billion or we issue more than $1.0 billion of non-convertible debt in any three-year period, we will cease to be an emerging growth company before the end of such five-year period.

In addition, Section 107 of the JOBS Act provides that an “emerging growth company” can take advantage of the extended transition period provided in Section 7(a)(2)(B) of the Securities Act of 1933, as amended, or the Securities Act, for complying with new or revised accounting standards. We have elected to take advantage of the extended transition period for complying with new or revised accounting standards and acknowledge such election is irrevocable pursuant to Section 107 of the JOBS Act.

6

We are a foreign private issuer within the meaning of the rules under the Securities Exchange Act of 1934, as amended (the “Exchange Act”). As such, we are exempt from certain provisions applicable to United States domestic public companies. For example:

| ● | we are not required to provide as many Exchange Act reports, or as frequently, as a U.S. domestic public company; |

| ● | for interim reporting, we are permitted to comply solely with our home country requirements, which are less rigorous than the rules that apply to domestic public companies; | |

| ● | we are not required to provide the same level of disclosure on certain issues, such as executive compensation; | |

| ● | we are exempt from provisions of Regulation FD aimed at preventing issuers from making selective disclosures of material information; | |

| ● | we are not required to comply with the sections of the Exchange Act regulating the solicitation of proxies, consents, or authorizations in respect of a security registered under the Exchange Act; and | |

| ● | we are not required to comply with Section 16 of the Exchange Act requiring insiders to file public reports of their share ownership and trading activities and establishing insider liability for profits realized from any “short-swing” trading transaction. |

We intend to comply with the NASDAQ corporate governance rules applicable to foreign private issuers, which permit us to follow certain corporate governance rules that conform to the Cayman Islands requirements in lieu of many of the NASDAQ corporate governance rules applicable to U.S. companies. As a result, our corporate governance practices may differ from those you might otherwise expect from a U.S. company listed on NASDAQ.

Holding Company Structure

Kepuni Holdings Inc. is a holding company with no operations of its own. We conduct our operations in China primarily through our subsidiary and variable interest entity in China. As a result, although other means are available for us to obtain financing at the holding company level, Kepuni Holdings Inc.’s ability to pay dividends to its shareholders and to service any debt it may incur may depend upon dividends paid by our PRC subsidiaries and license and service fees paid by our PRC consolidated affiliated entities. If any of our subsidiaries incurs debt on its own in the future, the instruments governing such debt may restrict its ability to pay dividends to Kepuni Holdings Inc. In addition, our PRC subsidiary and variable interest entity are required to make appropriations to certain statutory reserve funds, which are not distributable as cash dividends except in the event of a solvent liquidation of the companies.

Current PRC regulations permit our indirect PRC subsidiaries to pay dividends to Kepuni HK only out of their accumulated profits, if any, determined in accordance with Chinese accounting standards and regulations. In addition, each of our subsidiaries in China is required to set aside at least 10% of its after-tax profits each year, if any, to fund a statutory reserve until such reserve reaches 50% of its registered capital. Each of such entity in China is also required to further set aside a portion of its after-tax profits to fund the employee welfare fund, although the amount to be set aside, if any, is determined at the discretion of its board of directors. Although the statutory reserves can be used, among other ways, to increase the registered capital and eliminate future losses in excess of retained earnings of the respective companies, the reserve funds are not distributable as cash dividends except in the event of liquidation.

The PRC government also imposes controls on the conversion of RMB into foreign currencies and the remittance of currencies out of the PRC. Therefore, we may experience difficulties in completing the administrative procedures necessary to obtain and remit foreign currency for the payment of dividends from our profits, if any. Furthermore, if our subsidiaries in the PRC incur debt on their own in the future, the instruments governing the debt may restrict their ability to pay dividends or make other payments. If we or our subsidiaries are unable to receive all of the revenues from our operations through the current VIE Agreements, we may be unable to pay dividends on our ordinary shares.

Cash dividends, if any, on our ordinary shares will be paid in U.S. dollars. If we are considered a PRC tax resident enterprise for tax purposes, any dividends we pay to our overseas shareholders may be regarded as China-sourced income and as a result may be subject to PRC withholding tax at a rate of up to 10.0%.

7

In order for us to pay dividends to our shareholders, we will rely on payments made from Taizhou Kepuni to Kepuni WFOE, pursuant to VIE Agreements between them, and the distribution of such payments to Kepuni HK as dividends from Kepuni WFOE. Certain payments from Taizhou Kepuni to Kepuni WFOE are subject to PRC taxes, including Enterprise Income Tax and VAT. For the fiscal year ended December 31, 2020 and 2019, Taizhou Kepuni did not pay any dividends pursuant to the VIE Agreements to Kepuni WFOE.

Pursuant to the Arrangement between Mainland China and the Hong Kong Special Administrative Region for the Avoidance of Double Taxation and Tax Evasion on Income, or the Double Tax Avoidance Arrangement, the 10% withholding tax rate may be lowered to 5% if a Hong Kong resident enterprise owns no less than 25% of a PRC project. However, the 5% withholding tax rate does not automatically apply and certain requirements must be satisfied, including without limitation that (a) the Hong Kong project must be the beneficial owner of the relevant dividends; and (b) the Hong Kong project must directly hold no less than 25% share ownership in the PRC project during the 12 consecutive months preceding its receipt of the dividends. In current practice, a Hong Kong project must obtain a tax resident certificate from the Hong Kong tax authority to apply for the 5% lower PRC withholding tax rate. As the Hong Kong tax authority will issue such a tax resident certificate on a case-by-case basis, we cannot assure you that we will be able to obtain the tax resident certificate from the relevant Hong Kong tax authority and enjoy the preferential withholding tax rate of 5% under the Double Taxation Arrangement with respect to dividends to be paid by our PRC subsidiary to its immediate holding company, Kepuni HK. As of the date of this prospectus, we have not applied for the tax resident certificate from the relevant Hong Kong tax authority. Kepuni HK intends to apply for the tax resident certificate when WFOE plans to declare and pay dividends to Kepuni HK. See “Risk Factors – Risks Relating to Our Corporate Structure – We are a holding company, and will rely on dividends paid by our subsidiaries for our cash needs. Any limitation on the ability of our subsidiaries to make dividend payments to us, or any tax implications of making dividend payments to us, could limit our ability to pay our parent company expenses or pay dividends to holders of our ordinary shares.” “Risk Factors – Risks Relating to Doing Business in China – We are a holding company and we rely on our subsidiaries for funding dividend payments, which are subject to restrictions under PRC laws.”

PRC Limitation on Oversea Listing

The Regulations on Mergers and Acquisitions of Domestic Companies by Foreign Investors, or the M&A Rules, adopted by six PRC regulatory agencies requires an overseas special purpose vehicle formed for listing purposes through acquisitions of PRC domestic companies and controlled by PRC companies or individuals to obtain the approval of the China Securities Regulatory Commission, or the CSRC, prior to the listing and trading of such special purpose vehicle’s securities on an overseas stock exchange.

Our PRC counsel has advised us based on their understanding of the current PRC laws, rules and regulations that the CSRC’s approval is not required for the listing and trading of our ordinary shares on Nasdaq in the context of this offering, given that: (i) our PRC subsidiary was incorporated as a wholly foreign-owned enterprise by means of direct investment rather than by merger or acquisition of equity interest or assets of a PRC domestic company owned by PRC companies or individuals as defined under the M&A Rules that are our beneficial owners; (ii) the CSRC currently has not issued any definitive rule or interpretation concerning whether offerings like ours under this prospectus are subject to the M&A Rules; and (iii) no provision in the M&A Rules clearly classifies contractual arrangements as a type of transaction subject to the M&A Rules. However, our PRC counsel has further advised us that there remain some uncertainties as to how the M&A Rules will be interpreted or implemented in the context of an overseas offering and its opinions summarized above are subject to any new laws, rules and regulations or detailed implementations and interpretations in any form relating to the M&A Rules. We cannot assure you that relevant PRC government agencies, including the CSRC, would reach the same conclusion as we do. If it is determined that CSRC approval is required for this offering, we may face sanctions by the CSRC or other PRC regulatory agencies for failure to seek CSRC approval for this offering.

For more detailed information, see “Risk Factors – Risks Relating to Doing Business in China – The approval of the China Securities Regulatory Commission may be required in connection with this offering, and, if required, we cannot predict whether we will be able to obtain such approval.”

Corporate Information

Our principal executive office is located at No.318 Yongping Road, Science and Technology Industrial Park Taizhou City, Jiangsu Province People’s Republic of China, 225300. The telephone number of our principal executive offices is +86-52382988888. Our registered agent in the Cayman Islands is Osiris International Cayman Limited. Our registered office and our registered agent’s office in the Cayman Islands are both located at Suite #4-210, Governors Square, 23 Lime Tree Bay Avenue, PO Box 32311, Grand Cayman KY1-1209, Cayman Islands. Our agent for service of process in the United States is [*]

8

THE OFFERING

| Shares Offered | ordinary shares (or ordinary shares assuming that the underwriters exercise their over-allotment option in full) | |

| Over-allotment Option | We have granted the underwriter an option exercisable up to 45 days after the closing of this offering to purchase up to an additional 15% of the ordinary shares sold in this offering on the same terms as the other ordinary shares being purchased by the underwriter from us. | |

| Ordinary share outstanding prior to completion of this offering | ordinary shares | |

| Ordinary share outstanding immediately after this offering | ordinary shares (or ordinary shares assuming that the underwriters exercise their over-allotment option in full) | |

| Use of Proceeds | We estimate that our net proceeds from this offering will be approximately $ , based on an initial public offering price of $ per ordinary share and after deducting estimated underwriting discounts and advisory fee and estimated offering expenses and assuming no exercise of the over-allotment option granted to the underwriters. See “Use of Proceeds” for more information. | |

| Underwriter | Boustead Securities, LLC |

| Underwriters’ Warrants | We have agreed to sell to Boustead Securities, LLC warrants (the “Underwriter’s Warrants”) to purchase up to a total of ordinary shares (equal to 7% of the aggregate number of ordinary shares sold in the offering) at a price equal to the price of our ordinary shares offered hereby. The Underwriter will receive Underwriter’s Warrants if for the portion of the offering pursuant to the over-allotment option. | |

| NASDAQ Trading symbol | We intend to list our ordinary shares on Nasdaq Global Market under the symbol “KPNT”. Our application could be rejected by Nasdaq, and this offering may not close until we have received Nasdaq’s approval for our application. | |

| Transfer Agent | [*] | |

| Risk Factors | Investing in these securities involves a high degree of risk. As an investor, you should be able to bear a complete loss of your investment. You should carefully consider the information set forth in the “Risk Factors” section of, and elsewhere in, this prospectus before deciding to invest in our ordinary shares. | |

| Lock-Up | We, our directors and executive officers, and our existing beneficial owners of 5% or more of our outstanding ordinary shares have agreed with the underwriter, subject to certain exceptions, not to sell, transfer or otherwise dispose of any ordinary shares for a period ending 180 days after the commencement of the trading of the ordinary shares. See “Underwriting” for more information. |

9

The following tables set forth selected historical statements of operations and balance sheet data for the fiscal years ended December 31, 2020 and 2019, which have been derived from our audited financial statements for those periods. Our historical results are not necessarily indicative of the results that may be expected in the future. You should read this data together with our consolidated financial statements and related notes appearing elsewhere in this prospectus as well as “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” appearing elsewhere in the prospectus.

For the Fiscal Years Ended December 31, | ||||||||

| 2020 | 2019 | |||||||

| US$ (audited) | US$ (audited) | |||||||

| Statement of operation data: | ||||||||

| Revenues | $ | 9,366,670 | $ | 8,253,366 | ||||

| Cost of revenues | 5,787,710 | 5,195,091 | ||||||

| Gross profits | 3,578,960 | 3,058,275 | ||||||

| Selling and marketing expense | 339,509 | 329,773 | ||||||

| General and administrative expenses | 1,577,113 | 1,216,115 | ||||||

| Income taxes | (231,700 | ) | (355,408 | ) | ||||

| Net income | 1,351,217 | 1,025,498 | ||||||

| Earnings per share, basic and diluted | ||||||||

| Weighted average ordinary shares outstanding | ||||||||

| Balance sheet data | ||||||||

| Current assets | 6,175,392 | 5,577,197 | ||||||

| Total assets | 11, 045,662 | 9,768,414 | ||||||

| Total liabilities | 7,770,527 | 7,996,818 | ||||||

| Total shareholders’ equity | 3,345,135 | 1,771,596 | ||||||

10

An investment in our ordinary share involves a high degree of risk. Before deciding whether to invest in our ordinary share, you should consider carefully the risks described below, together with all of the other information set forth in this prospectus, including the section titled “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and related notes. If any of these risks actually occurs, our business, financial condition, results of operations or cash flow could be materially and adversely affected, which could cause the trading price of our ordinary share to decline, resulting in a loss of all or part of your investment. The risks described below and in the documents referenced above are not the only ones that we face. Additional risks not presently known to us or that we currently deem immaterial may also affect our business. You should only consider investing in our ordinary share if you can bear the risk of loss of your entire investment.

Risks Related to Our Business

We rely on China’s shipbuilding and maritime supporting industries for our revenues and future growth, the prospects of which are subject to many uncertainties, including government regulations and policies.

We rely on China’s shipbuilding, nautical communication, nautical navigation industries for our revenues and future growth. We have greatly benefited from the rapid growth of China’s maritime industry during the past few years. However, the prospects of China’s maritime industry are subject to many uncertainties, including those relating to general economic conditions in China, government and state infrastructure plans and the costs of shipbuilding. In addition, government policies may have a considerable impact on the growth of the maritime industry in China. The uncertainties related to the strategic developments and state policies may affect the growth prospects of China’s maritime industry, and in turn, reduce the demand for shipbuilding parts and nautical communication equipment and system.

Our business is substantially dependent on our collaboration with our suppliers, including electronic component supplier, material dealers, and shipyard service providers, and our agreements with them typically do not contain long-term contractual commitments.

Our business is substantially dependent on our collaboration with electronic component supplier, material dealers, and shipyard service providers. We generally enter into cooperation agreements with them without imposing any contractual obligations requiring them to maintain their relationships with us beyond the completion of each project or beyond the contractual term. Accordingly, there is no guarantee for future cooperation after the project completion and there is no assurance that we can maintain stable and long-term business relationships with any such shipbuilders. If a significant number of our industry buyers terminate or do not renew their agreements with us and we are not able to replace these business partners on commercially reasonable terms in a timely manner or at all, our business, results of operations and financial condition would be materially and adversely affected.

Adverse worldwide economic or other conditions could result in prolonged reduction in the demand for maritime products and services, adversely impacting our operating results, cash flows and financial and potentially affecting other critical accounting estimates where the change may be material to our operating results.

In addition to health and safety concerns, demand for ships and nautical transportation is affected by international, national, and local economic conditions. Accordingly, as a supplier of nautical communication system, terminal equipment, and data platform, we are highly likely to be impacted by the health and safety concerns as well. Furthermore, weak or uncertain economic conditions may impact consumer confidence and pose a risk as shipyards and major construction companies postpone or reduce product orders. This, in turn, may result in order slowdowns, lower revenues, even after the COVID-19 pandemic has ended and/or related health and safety concerns are reduced.

11

We are exposed to many different economies and our business could be hurt by challenging conditions in any of our markets. Any significant deterioration of international, national, or local economic conditions, including those resulting from geopolitical events and/or international disputes and the current economic and employment impact of the COVID-19 pandemic in countries where our customers reside could result in a prolonged period of order slowdowns and/or reduced revenues, even after the COVID-19 pandemic has ended and/or related health and safety concerns are reduced. The COVID-19 pandemic could cause a global recession, which would have a further adverse impact on our financial condition and results of operations. Additionally, the impact of COVID-19 on the financial markets is complicated and we cannot predict its effect on geopolitical events and/or international trade policies as countries attempt to mitigate the impact as economies re-open.

Increases in the shipbuilding costs, labor costs, and raw material prices may adversely impact our pricing

We may be impacted by economic, market and political conditions in China, such as shipbuilding costs, labor costs, raw materials costs, regulatory requirements, supply disruptions and related infrastructure needs, which make it difficult to predict the total production cost and our product pricings.

According to the industry report by the China State Shipbuilding Association, China’s labor costs and material prices have risen over the past couple of years, significantly impacting on the shipbuilding industry. Shipbuilding costs also fluctuated as a result of changes in exchange rates and interest rates. The rising shipbuilding cost has indirectly affected the profit margin of ship equipment. In order to reduce costs, domestic shipbuilders often pass on the rising costs of labor and raw materials to upstream ship supporting enterprises by reducing procurement costs or improving quality requirements, which indirectly affects the overall profitability of ship supporting industries, especially for ship electrical and automation systems.

We depend on certain key personnel and loss of these key personnel could have a material adverse effect on our business, financial condition and results of operations.

Our success is, to a certain extent, attributable to the management, sales and marketing, and research and development expertise of key personnel. We depend upon the services of Mr. Xiaofei Cui, our Chief Executive Officer and Chairman of the Board, Mr. Fangzhong Ni, our Chief Operating Officer for the continued growth and operation of our Company, due to their industry experience, technical expertise, as well as their personal and business contacts in the PRC. Although we have no reason to believe that our directors and executive officers will discontinue their services with us or Taizhou Kepuni, the interruption or loss of their services would adversely affect our ability to effectively run our business and pursue our business strategy as well as our results of operations. We do not carry key man life insurance for any of our key personnel, nor do we foresee purchasing such insurance to protect against the loss of key personnel.

We may not be able to hire and retain qualified personnel to support our growth and if we are unable to retain or hire these personnel in the future, our ability to improve our products and implement our business objectives could be adversely affected.

We must attract, recruit and retain a sizeable workforce of technically competent employees. Competition for senior management and personnel in the PRC is intense and the pool of qualified candidates in the PRC is limited. We may not be able to retain the services of our senior executives or personnel, or attract and retain high-quality senior executives or personnel in the future. This failure could materially and adversely affect our future growth and financial condition.

12

If we fail to maintain and enhance our brand name recognition, we may face difficulty in attracting new customers and meeting customer demands.

Although our brand is well-respected in the small and medium-sized shipyard equipment industry in the China east coast market, we still believe that maintaining and enhancing our brand name recognition in a cost-effective manner is critical to achieving a transition into a long term development in the medium and large-sized shipyard equipment industry in the national market. The brand recognition is an important element in our effort to increase our customer base. Successful promotion of our brand name will depend largely on our marketing efforts and ability to provide reliable and quality products at competitive prices. Brand promotion activities may not necessarily yield increased revenue, and even if they do, any increased revenue may not offset the expenses we will incur in marketing activities. If we fail to successfully promote and maintain our brand, or if we incur substantial expenses in an unsuccessful attempt to promote and maintain our brand, we may fail to attract new buyers or retain our existing equipment buyers, in which case our business, operating results and financial condition, would be materially adversely affected.

Our success depends on our ability to protect our intellectual property.

Our success depends on our ability to obtain and maintain trademark protection for our brand name, in the PRC and in other countries. There is no assurance that any of our existing and future trademarks will be held valid and enforceable against third-party infringement or that our equipment and services will not infringe any third-party patent or intellectual property. We have owned valid trademarks within PRC. Third parties may oppose our trademark applications or otherwise challenge our use of the trademarks. In the event that our trademarks are successfully challenged, we could be forced to rebrand our products, which could result in loss of brand recognition and could require us to devote resources to advertising and marketing these new brands. Further, our competitors may infringe our trademarks, or we may not have adequate resources to enforce our trademarks.

Adverse publicity associated with our network marketing program, or those of similar companies, could harm our financial condition and operating results.

The results of our operations may be significantly affected by the public’s perception of our products and similar companies. This perception depends upon opinions concerning:

| ● | the safety and quality of the equipment and services we sell; and |

| ● | the safety and quality of similar equipment and services distributed by other companies. |

Adverse publicity concerning any actual or purported failure to comply with applicable laws and regulations regarding product claims and advertising, good manufacturing practices, or other aspects of our business, whether or not resulting in enforcement actions or the imposition of penalties, could have an adverse effect on our goodwill and could negatively affect our sales and ability to generate revenue.

Risks Related to Our Corporate Structure

13

We are a holding company incorporated in the Cayman Islands. As a holding company with no material operations of our own, we conduct all of our operations through our subsidiaries established in PRC and our VIE. We control and receive the economic benefits of our VIE’s business operations through certain contractual arrangements. Our ordinary shares offered in this offering are shares of our offshore holding company instead of shares of our VIE in China. For a description of the VIE contractual arrangements, see “Corporate History and Structure—Contractual Arrangements.”

The VIE contributed 100% of the Company’s consolidated results of operations and cash flows for the years ended December 31, 2020 and 2019, respectively. As of December 31, 2020 and 2019, the VIE accounted for 100% of the consolidated total assets and total liabilities of the Company.

We rely on and expect to continue to rely on our wholly owned PRC subsidiary’s contractual arrangements with Taizhou Kepuni and its shareholders to operate our business. These contractual arrangements may not be as effective in providing us with control over Taizhou Kepuni as ownership of controlling equity interests would be in providing us with control over, or enabling us to derive economic benefits from the operations of Taizhou Kepuni. Under the current contractual arrangements, as a legal matter, if Taizhou Kepuni or any of its shareholders executing the VIE Agreements fails to perform its, his or her respective obligations under these contractual arrangements, we may have to incur substantial costs and resources to enforce such arrangements, and rely on legal remedies available under PRC laws, including seeking specific performance or injunctive relief, and claiming damages, which we cannot assure you will be effective. For example, if shareholders of a variable interest entity were to refuse to transfer their equity interests in such variable interest entity to us or our designated persons when we exercise the purchase option pursuant to these contractual arrangements, we may have to take a legal action to compel them to fulfill their contractual obligations.

If (i) the applicable PRC authorities invalidate these contractual arrangements for violation of PRC laws, rules and regulations, (ii) any variable interest entity or its shareholders terminate the contractual arrangements (iii) any variable interest entity or its shareholders fail to perform its/his/her obligations under these contractual arrangements, or (iv) if these regulations change or are interpreted differently in the future, our business operations in China would be materially and adversely affected, and the value of your shares would substantially decrease or even become worthless. Further, if we fail to renew these contractual arrangements upon their expiration, we would not be able to continue our business operations unless the then current PRC law allows us to directly operate businesses in China.

In addition, if any variable interest entity or all or part of its assets become subject to liens or rights of third-party creditors, we may be unable to continue some or all of our business activities, which could materially and adversely affect our business, financial condition and results of operations. If any of the variable interest entities undergoes a voluntary or involuntary liquidation proceeding, its shareholders or unrelated third-party creditors may claim rights to some or all of these assets, thereby hindering our ability to operate our business, which could materially and adversely affect our business and our ability to generate revenues.

14

All of these contractual arrangements are governed by PRC law and provide for the resolution of disputes through arbitration in the PRC. The legal environment in the PRC is not as developed as in some other jurisdictions, such as the United States. As a result, uncertainties in the PRC legal system could limit our ability to enforce these contractual arrangements. In the event we are unable to enforce these contractual arrangements, we may not be able to exert effective control over our operating entities and we may be precluded from operating our business, which would have a material adverse effect on our financial condition and results of operations.

These contractual arrangements may not be as effective as direct ownership in providing us with control over our VIEs. For example, our VIEs and their shareholders could breach their contractual arrangements with us by, among other things, failing to conduct their operations in an acceptable manner or taking other actions that are detrimental to our interests. If we had direct ownership of our VIEs, we would be able to exercise our rights as a shareholder to effect changes in the board of directors of our VIEs, which in turn could implement changes, subject to any applicable fiduciary obligations, at the management and operational level. However, under the current contractual arrangements, we rely on the performance by our VIEs and their shareholders of their obligations under the contracts to exercise control over our VIEs. The shareholders of our consolidated VIEs may not act in the best interests of our company or may not perform their obligations under these contracts. Such risks exist throughout the period in which we intend to operate certain portions of our business through the contractual arrangements with our VIEs.

If our VIEs or their shareholders fail to perform their respective obligations under the contractual arrangements, we may have to incur substantial costs and expend additional resources to enforce such arrangements. For example, if the shareholders of our VIEs refuse to transfer their equity interest in our VIEs to us or our designee if we exercise the purchase option pursuant to these contractual arrangements, or if they otherwise act in bad faith toward us, then we may have to take legal actions to compel them to perform their contractual obligations. In addition, if any third parties claim any interest in such shareholders’ equity interests in our VIEs, our ability to exercise shareholders’ rights or foreclose the share pledge according to the contractual arrangements may be impaired. If these or other disputes between the shareholders of our VIEs and third parties were to impair our control over our VIEs, our ability to consolidate the financial results of our VIEs would be affected, which would in turn result in a material adverse effect on our business, operations and financial condition.

In the opinion our PRC legal counsel, each of the contractual arrangements among our WFOE, our VIE and its shareholders governed by PRC laws are valid, binding and enforceable, and will not result in any violation of PRC laws or regulations currently in effect. However, our PRC legal counsel has also advised us that there are substantial uncertainties regarding the interpretation and application of current and future PRC laws, regulations and rules. Accordingly, the PRC regulatory authorities may ultimately take a view that is contrary to the opinion of our PRC legal counsel. In addition, it is uncertain whether any new PRC laws or regulations relating to variable interest entity structures will be adopted or if adopted, what they would provide. PRC government authorities may deem that foreign ownership is directly or indirectly involved in our VIE’s shareholding structure. If our corporate structure and contractual arrangements are deemed by the MIIT or the MOFCOM or other regulators having competent authority to be illegal, either in whole or in part, we may lose control of our consolidated VIE and have to modify such structure to comply with regulatory requirements. However, there can be no assurance that we can achieve this without material disruption to our VATS business. Furthermore, if we or our VIE is found to be in violation of any existing or future PRC laws or regulations, or fail to obtain or maintain any of the required permits or approvals, the relevant PRC regulatory authorities would have broad discretion to take action in dealing with such violations or failures, including, without limitation:

| ● | revoking the business license and/or operating licenses of our WFOE or our VIE; |

| ● | discontinuing or placing restrictions or onerous conditions on our operations through any transactions among our WFOE, our VIE and its subsidiaries; |

| ● | imposing fines, confiscating the income from our WFOE, our VIE or its subsidiaries, or imposing other requirements with which we or our VIE may not be able to comply; |

| ● | placing restrictions on our right to collect revenues; |

15

| ● | shutting down our servers or blocking our app/websites; |

| ● | requiring us to restructure our ownership structure or operations, including terminating the contractual arrangements with our VIE and deregistering the equity pledges of our VIE, which in turn would affect our ability to consolidate, derive economic interests from, or exert effective control over our VIE; or |

| ● | restricting or prohibiting our use of the proceeds of this offering to finance our business and operations in China. |

| ● | taking other regulatory or enforcement actions against us that could be harmful to our business. |

The imposition of any of these penalties would result in a material and adverse effect on our ability to conduct our business. In addition, it is unclear what impact the PRC government actions would have on us and on our ability to consolidate the financial results of our VIE in our consolidated financial statements, if the PRC government authorities were to find our corporate structure and contractual arrangements to be in violation of PRC laws and regulations. If the imposition of any of these government actions causes us to lose our right to direct the activities of our VIE or our right to receive substantially all the economic benefits and residual returns from our VIE and we are not able to restructure our ownership structure and operations in a satisfactory manner, we would no longer be able to consolidate the financial results of our VIE in our consolidated financial statements. Either of these results, or any other significant penalties that might be imposed on us in this event, would have a material adverse effect on our financial condition and results of operations.

We rely on contractual arrangements with our variable interest entity and its subsidiary in China for our business operations, which may not be as effective in providing operational control or enabling us to derive economic benefits as through ownership of controlling equity interests.

We rely on and expect to continue to rely on our wholly-owned PRC subsidiary’s contractual arrangements with Taizhou Kepuni and its shareholders to operate our business. These contractual arrangements may not be as effective in providing us with control over Taizhou Kepuni as ownership of controlling equity interests would be in providing us with control over, or enabling us to derive economic benefits from the operations of Taizhou Kepuni. Under the current contractual arrangements, as a legal matter, if Taizhou Kepuni or any of Taizhou Kepuni Shareholders fails to perform its, his or her respective obligations under these contractual arrangements, we may have to incur substantial costs and resources to enforce such arrangements, and rely on legal remedies available under PRC laws, including seeking specific performance or injunctive relief, and claiming damages, which we cannot assure you will be effective. For example, if Taizhou Kepuni Shareholders were to refuse to transfer their equity interests in Taizhou Kepuni to us or our designated persons when we exercise the purchase option pursuant to these contractual arrangements, we may have to take a legal action to compel them to fulfill their contractual obligations.

If (i) the applicable PRC authorities invalidate these contractual arrangements for violation of PRC laws, rules and regulations, (ii) any variable interest entity or its shareholders terminate the contractual arrangements or (iii) any variable interest entity or its shareholders fail to perform its/his/her obligations under these contractual arrangements, our business operations in China would be materially and adversely affected, and the value of your shares would substantially decrease. Further, if we fail to renew these contractual arrangements upon their expiration, we would not be able to continue our business operations unless the then current PRC law allows us to directly operate businesses in China.

In addition, if any variable interest entity or all or part of its assets become subject to liens or rights of third-party creditors, we may be unable to continue some or all of our business activities, which could materially and adversely affect our business, financial condition and results of operations. If any of the variable interest entities undergoes a voluntary or involuntary liquidation proceeding, its shareholders or unrelated third-party creditors may claim rights to some or all of these assets, thereby hindering our ability to operate our business, which could materially and adversely affect our business and our ability to generate revenues.