Table of Contents

(State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

Alan Hambelton Garth Osterman Julia Stark Cooley LLP 1700 Seventh Avenue, Suite 1900 Seattle, Washington 98101-1355 Tel: (206) 452-8700 |

Michael P. Heinz Joshua G. DuClos Jocelyne E. Kelly Sidley Austin LLP One South Dearborn Street Chicago, Illinois 60603 Tel: (312) 853-7000 |

Large accelerated filer |

☐ |

Accelerated filer |

☐ | |||

☒ |

Smaller reporting company |

|||||

Emerging growth company |

||||||

Table of Contents

The information in this preliminary proxy statement/prospectus is not complete and may be changed. The registrant may not sell the securities described in this preliminary proxy statement/prospectus until the registration statement filed with the Securities and Exchange Commission is declared effective. This preliminary proxy statement/prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

PRELIMINARY PROXY STATEMENT AND PROSPECTUS

DATED OCTOBER 3, 2023, SUBJECT TO COMPLETION

7GC & CO. HOLDINGS INC.

388 Market Street, Suite 1300

San Francisco, CA 94111

Dear Stockholders of 7GC & Co. Holdings Inc.:

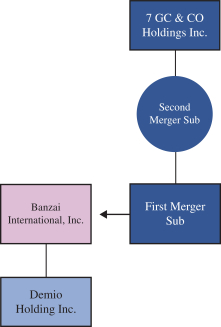

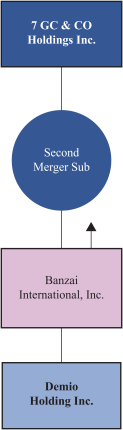

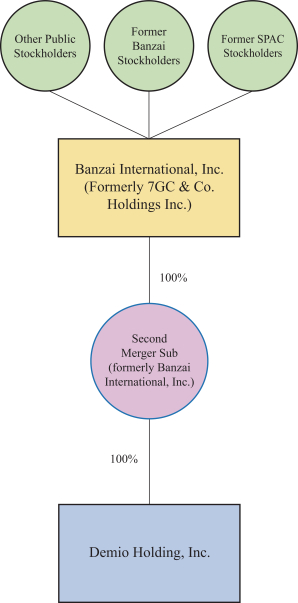

On December 8, 2022, 7GC & Co. Holdings Inc., a Delaware corporation (“7GC”), entered into an Agreement and Plan of Merger and Reorganization (the “Original Merger Agreement”), by and among Banzai International, Inc., a Delaware corporation (“Banzai”), 7GC Merger Sub I, Inc., a Delaware corporation and an indirect wholly owned subsidiary of 7GC (“First Merger Sub”), and 7GC Merger Sub II, LLC, a Delaware limited liability company and a direct wholly owned subsidiary of 7GC (“Second Merger Sub” and, together with First Merger Sub, the “Merger Subs” and each, a “Merger Sub”), as amended by the Amendment to Agreement and Plan of Merger, dated as of August 4, 2023, by and between 7GC and Banzai (the “Amendment” and together with the Original Merger Agreement, the “Merger Agreement”). Pursuant to the terms of the Merger Agreement, the parties thereto will enter into a business combination transaction (the “Business Combination” and together with the other transactions contemplated by the Merger Agreement, the “Transactions”), pursuant to which, among other things, (i) First Merger Sub will merge with and into Banzai (the “First Merger”), with Banzai surviving the First Merger as an indirect wholly owned subsidiary of 7GC (the “Surviving Corporation”), and, (ii) immediately following the First Merger, the Surviving Corporation will merge with and into Second Merger Sub (the “Second Merger” and, together with the First Merger, the “Mergers”), with the Second Merger Sub surviving the Second Merger as a direct wholly owned subsidiary of 7GC. At the closing of the Business Combination, 7GC will change its name to Banzai International, Inc. (“New Banzai”), and its Class A common stock is expected to be listed on The Nasdaq Capital Market (“Nasdaq”) under the ticker symbol “BNZI”. It is a condition to the consummation of the Merger Agreement that the Class A common stock, par value $0.0001 per share (“New Banzai Class A Shares”), of New Banzai has been listed on Nasdaq, subject to official notice of issuance.

The aggregate consideration payable to securityholders of Banzai at the closing of the Transactions (the “Closing”) will consist of a number of newly issued New Banzai Class A Shares of 7GC (“7GC Class A Common Stock”) or a number of newly issued shares of Class B common stock, par value $0.0001 per share (“New Banzai Class B Shares”), of 7GC (“7GC Class B Common Stock”), and cash in lieu of any fractional New Banzai Class A Shares or New Banzai Class B Shares that would otherwise be payable to any Banzai securityholders, equal to $100,000,000.

At the effective time of the First Merger (the “First Effective Time”), each outstanding share of Class A common stock of Banzai, par value $0.0001 per share (the “Banzai Class A Common Stock”), including each of the outstanding shares of preferred stock, par value $0.0001 per share, of Banzai that will have been converted into Banzai Class A Common Stock immediately prior to the First Effective Time, and each outstanding share of Class B common stock of Banzai par value $0.0001 per share (the “Banzai Class B Common Stock”) (in each case, other than dissenting shares and any shares held in the treasury of Banzai) shall be cancelled and converted into the right to receive a number of New Banzai Class A Shares or New Banzai Class B Shares, respectively, equal to (x) the Per Share Value (as defined below) divided by (y) $10.00 (the “Exchange Ratio”). “Per Share Value” equals (i) an amount equal to $100,000,000, payable in New Banzai Class A Shares or New Banzai Class B Shares, as applicable (the “Total Consideration”), divided by (ii) (A) the total number of shares of Banzai Class A Common Stock and Banzai Class B Common Stock issued and outstanding as of immediately prior to the First Effective Time, (B) the maximum aggregate number of shares of Banzai Class A Common Stock issuable upon full exercise of options of Banzai to purchase Banzai Class A Common Stock (the “Banzai Options”) issued, outstanding, and vested immediately prior to the First Effective Time, (C) the maximum aggregate number of shares of Banzai Class A Common Stock issuable upon conversion of certain senior convertible notes outstanding as of immediately prior to the First Effective Time at the applicable conversion price, (D) the maximum aggregate number of shares of Banzai Class A Common Stock issuable upon conversion of all of the outstanding principal and interest under certain subordinated convertible promissory notes as of immediately prior to the First Effective Time at the applicable conversion price, and (E) the maximum aggregate number of shares of Banzai Class A Common Stock issuable upon conversion of the SAFE Purchase Amount (as defined herein) under each SAFE Right (as defined herein) as of immediately prior to the First Effective Time at the applicable SAFE Conversion Price (as defined herein). See the section titled “Stockholder Proposal No. 1 — The Business Combination Proposal” on page 87 of the accompanying proxy statement/prospectus for further information on the consideration payable to Banzai securityholders.

On the terms and subject to the conditions set forth in the Merger Agreement, at the effective time of the Second Merger (the “Second Effective Time”), each share of common stock of the Surviving Corporation issued and outstanding immediately prior to the Second Effective Time shall be cancelled and no consideration shall be delivered therefor.

7GC’s units, Class A common stock and public warrants are currently listed on Nasdaq, under the symbols “VIIAU,” “VII,” and “VIIAW,” respectively. 7GC has applied to continue the listing of its Class A common stock and public warrants on Nasdaq under the symbols “BNZI” and “BNZIW,” respectively, upon the Closing. At the Closing, each of 7GC’s units will separate into its component parts consisting of one share of 7GC’s Class A common stock and one-half of one of 7GC’s public warrants and, as a result, will no longer trade as a separate security.

Following the completion of the Closing, New Banzai will have two classes of authorized and outstanding common stock. Each New Banzai Class A Share and New Banzai Class B Share entitles its holder to one vote and ten votes, respectively, on all matters presented to our stockholders generally. New Banzai’s dual class common stock structure will have the effect of concentrating more than 50% of voting power with New Banzai’s Chief Executive Officer and Co-Founder, Joseph Davy, and his affiliates and permitted transferees which limits an investor’s ability to influence the outcome of important transactions, including a change in control. As a result, at Closing, New Banzai will be considered a “controlled company” within the meaning of Nasdaq corporate governance listing standards and will qualify for, and if New Banzai so elects, may rely on exemptions from certain Nasdaq corporate governance listing standards. However, New Banzai currently does not intend to avail itself of the controlled company exemption under the Nasdaq corporate governance standards. At Closing, New Banzai will issue shares of New Banzai Class A Shares and shares of New Banzai Class B Shares, which immediately after the Closing will represent in the aggregate % and % of our total outstanding shares of common stock, respectively.

7GC will hold a special meeting of its stockholders in lieu of its 2023 annual meeting of stockholders (the “Special Meeting”) to consider matters relating to the proposed Business Combination. 7GC and Banzai cannot complete the Business Combination unless 7GC’s stockholders consent to the approval of the Merger Agreement and the Transactions, including the issuance of New Banzai Class A Shares and New Banzai Class B Shares to be issued as the merger consideration. 7GC is sending you this proxy statement/prospectus to ask you to vote in favor of these and the other matters described in this proxy statement/prospectus.

The Special Meeting will be held virtually via live webcast at , Eastern Time, on , 2023. As such, 7GC stockholders may attend the Special Meeting by visiting the Special Meeting website at , where you will be able to listen to the meeting live and vote during the meeting.

Table of Contents

After careful consideration, the 7GC board of directors has unanimously approved the Business Combination and unanimously recommends that stockholders vote “FOR” the adoption of the Business Combination Proposal (as defined in the accompanying proxy statement/prospectus) and “FOR” all other proposals to be presented to 7GC’s stockholders at the Special Meeting. When you consider the recommendation of these proposals by the 7GC board of directors, you should keep in mind that 7GC’s directors and officers have interests in the Business Combination that may conflict with your interests as a stockholder. See the section titled “Stockholder Proposal No. 1 — The Business Combination Proposal — Interests of 7GC’s Directors and Executive Officers in the Business Combination” in the accompanying proxy statement/prospectus for a further discussion of these considerations.

The approval of each of the Charter Proposals (as defined in the accompanying proxy statement/prospectus) requires an affirmative vote of the holders of at least a majority of the outstanding shares of 7GC Class A Common Stock and 7GC Class B Common Stock (together, the “7GC Common Stock”) entitled to vote thereon, voting together as a single class, an affirmative vote of the holders of at least a majority of the outstanding shares of 7GC Class A Common Stock entitled to vote thereon, voting separately as a single class, and an affirmative vote of the holders of at least a majority of the outstanding shares of 7GC Class B Common Stock entitled to vote thereon, voting separately as a single class. The approval of the Business Combination Proposal, Nasdaq Proposal, Incentive Plan Proposal, ESPP Proposal, and Adjournment Proposal (each, as defined in the accompanying proxy statement/prospectus) require the affirmative vote of a majority of the votes cast by the holders of 7GC Common Stock represented electronically or by proxy at the Special Meeting and entitled to vote thereon. The approval of the election of each director nominee pursuant to the Director Election Proposal (as defined in the accompanying proxy statement/prospectus) requires the affirmative vote of a plurality of the votes cast by the holders of 7GC Common Stock represented electronically or by proxy at the Special Meeting and entitled to vote thereon.

Your vote is very important. Whether or not you plan to attend the Special Meeting, please vote as soon as possible by following the instructions in the accompanying proxy statement/prospectus to make sure that your shares are represented at the Special Meeting. If you hold your shares in “street name” through a bank, broker, or other nominee, you will need to follow the instructions provided to you by your bank, broker, or other nominee to ensure that your shares are represented and voted at the Special Meeting. In most cases you may vote by telephone or over the Internet as instructed. The transactions contemplated by the Merger Agreement will be consummated only if the Business Combination Proposal, the Binding Charter Proposal (as defined in the accompanying proxy statement/prospectus), the Director Election Proposal, the Nasdaq Proposal, the Incentive Plan Proposal, and the ESPP Proposal (collectively, the “Condition Precedent Proposals”) are approved at the Special Meeting. Each of the Condition Precedent Proposals is cross-conditioned on the approval of the others. The Advisory Charter Proposals (as defined in the accompanying proxy statement/prospectus) and the Adjournment Proposal are not conditioned upon the approval of any other proposal set forth in the accompanying proxy statement/prospectus.

The accompanying proxy statement/prospectus and accompanying proxy card are being provided to 7GC’s stockholders in connection with the solicitation of proxies to be voted at the Special Meeting and at any adjournment of the Special Meeting. Whether or not you plan to attend the Special Meeting, all of 7GC’s stockholders are urged to read this proxy statement/prospectus, including the annexes and the documents referred to herein, carefully and in their entirety. You should also carefully consider the risk factors described in the section titled “Risk Factors” beginning on page 29 of the accompanying proxy statement/prospectus.

If you have any questions regarding the accompanying proxy statement/consent solicitation statement/prospectus, you may contact Morrow Sodali LLC, 7GC’s proxy solicitor, by calling (800) 662-5200, or by emailing vii.info@investor.morrowsodali.com.

TO EXERCISE YOUR REDEMPTION RIGHTS, YOU MUST IDENTIFY YOURSELF IN WRITING AS A BENEFICIAL HOLDER AND PROVIDE YOUR LEGAL NAME, PHONE NUMBER AND ADDRESS TO 7GC’S TRANSFER AGENT AND DEMAND IN WRITING THAT YOUR SHARES OF 7GC CLASS A COMMON STOCK ARE REDEEMED FOR A PRO RATA PORTION OF THE FUNDS HELD IN THE TRUST ACCOUNT AND TENDER YOUR SHARES TO 7GC’S TRANSFER AGENT AT LEAST TWO BUSINESS DAYS PRIOR TO THE VOTE AT THE SPECIAL MEETING. YOU MAY TENDER YOUR SHARES BY EITHER DELIVERING YOUR SHARE CERTIFICATE TO THE TRANSFER AGENT OR BY DELIVERING YOUR SHARES ELECTRONICALLY USING THE DEPOSITORY TRUST COMPANY’S DWAC (DEPOSIT WITHDRAWAL AT CUSTODIAN) SYSTEM. IF THE BUSINESS COMBINATION IS NOT COMPLETED, THEN THESE SHARES WILL BE RETURNED TO YOU OR YOUR ACCOUNT. IF YOU HOLD THE SHARES IN STREET NAME, YOU WILL NEED TO INSTRUCT THE ACCOUNT EXECUTIVE AT YOUR BANK OR BROKER TO WITHDRAW THE SHARES FROM YOUR ACCOUNT IN ORDER TO EXERCISE YOUR REDEMPTION RIGHTS.

On behalf of 7GC’s board of directors, we would like to thank you for your support and look forward to the successful completion of the Business Combination.

Sincerely,

| Jack Leeney |

| Chairman and Chief Executive Officer 7GC & Co. Holdings Inc. |

NEITHER THE SECURITIES AND EXCHANGE COMMISSION NOR ANY STATE SECURITIES REGULATORY AGENCY HAS APPROVED OR DISAPPROVED THE TRANSACTIONS DESCRIBED IN THE ACCOMPANYING PROXY STATEMENT/PROSPECTUS, PASSED UPON THE MERITS OR FAIRNESS OF THE BUSINESS COMBINATION OR RELATED TRANSACTIONS OR PASSED UPON THE ADEQUACY OR ACCURACY OF THE DISCLOSURE IN THE ACCOMPANYING PROXY STATEMENT/PROSPECTUS. ANY REPRESENTATION TO THE CONTRARY CONSTITUTES A CRIMINAL OFFENSE.

This proxy statement/prospectus is dated , 2023, and is first being mailed to stockholders of 7GC on or about , 2023.

Table of Contents

TABLE OF CONTENTS

| Page | ||||

| NOTICE OF SPECIAL MEETING IN LIEU OF 2023 ANNUAL MEETING OF STOCKHOLDERS |

iii | |||

| viii | ||||

| ix | ||||

| xv | ||||

| xvi | ||||

| 1 | ||||

| 7 | ||||

| 29 | ||||

| 74 | ||||

| UNAUDITED PRO FORMA CONDENSED COMBINED FINANCIAL INFORMATION |

75 | |||

| STOCKHOLDER PROPOSAL NO. 1 — THE BUSINESS COMBINATION PROPOSAL |

87 | |||

| 135 | ||||

| 138 | ||||

| 140 | ||||

| 141 | ||||

| 143 | ||||

| 152 | ||||

| 157 | ||||

| 158 | ||||

| 166 | ||||

| 7GC MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

173 | |||

| 180 | ||||

| 187 | ||||

| BANZAI MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

196 | |||

| 220 | ||||

| 224 | ||||

| 230 | ||||

| 235 | ||||

| 240 | ||||

| 253 | ||||

| SECURITIES ACT RESTRICTIONS ON RESALE OF NEW BANZAI SECURITIES |

259 | |||

| 261 | ||||

| 262 | ||||

| 263 | ||||

| 264 | ||||

| 265 | ||||

| 266 | ||||

| 267 | ||||

| F-1 | ||||

| A-1 | ||||

| A-2 | ||||

| B-1 | ||||

| C-1 | ||||

| D-1 | ||||

| E-1 |

i

Table of Contents

Table of Contents

7GC & CO. HOLDINGS INC.

A Delaware Corporation

388 Market Street, Suite 1300

San Francisco, CA 94111

NOTICE OF SPECIAL MEETING IN LIEU OF 2023 ANNUAL MEETING OF STOCKHOLDERS

TO BE HELD ON , 2023

TO THE STOCKHOLDERS OF 7GC & CO. HOLDINGS INC.:

NOTICE IS HEREBY GIVEN that a special meeting in lieu of 2023 annual meeting of stockholders (the “Special Meeting”) of 7GC & Co. Holdings Inc., a Delaware corporation (“7GC”), will be held virtually via live webcast, at , on , 2023. As such, 7GC stockholders may attend the Special Meeting by visiting the Special Meeting website at , where they will be able to listen to the meeting live and vote during the meeting. We are pleased to utilize virtual stockholder meeting technology to provide ready access and cost savings for 7GC stockholders. You are cordially invited to attend the Special Meeting, which will be held for the following purposes:

Proposal No. 1 — The Business Combination Proposal — to consider and vote upon a proposal to approve and adopt the Agreement and Plan of Merger (the “Original Merger Agreement”), dated as of December 8, 2022, by and among 7GC, Banzai International, Inc., a Delaware corporation (“Banzai”), 7GC Merger Sub I, Inc., a Delaware corporation and an indirect wholly owned subsidiary of 7GC (“First Merger Sub”), and 7GC Merger Sub II, LLC, a Delaware limited liability company and a direct wholly owned subsidiary of 7GC (“Second Merger Sub” and, together with First Merger Sub, the “Merger Subs” and each, a “Merger Sub”), as amended by the Amendment to Agreement and Plan of Merger, dated as of August 4, 2023, by and between 7GC and Banzai (the “Amendment” and, together with the Original Merger Agreement, the “Merger Agreement”), and the transactions contemplated by the Merger Agreement (the “Transactions”), including the Mergers (as defined herein), as more fully described elsewhere in the accompanying proxy statement/prospectus (the “Business Combination Proposal”);

Proposal No. 2 — The Binding Charter Proposal — to consider and vote upon a proposal to approve the proposed Second Amended and Restated Certificate of Incorporation of 7GC (the “Proposed Charter”), the full text of which is attached to the accompanying proxy statement/prospectus as Annex H, which will replace 7GC’s current amended and restated certificate of incorporation (the “Existing Charter”) and will be in effect upon the Closing (the “Binding Charter Proposal”);

Proposal No. 3 — The Advisory Charter Proposals — to consider and vote upon separate proposals to approve, on a non-binding advisory basis, the following material differences between the Proposed Charter and the Existing Charter, which are being presented in accordance with SEC guidance as separate sub-proposals (the “Advisory Charter Proposals” and, together with the Binding Charter Proposal, the “Charter Proposals”):

| • | Proposal No. 3A — to increase the authorized shares of New Banzai Common Stock (as defined herein) to 275,000,000 shares, consisting of 250,000,000 New Banzai Class A Shares (as defined herein) and 25,000,000 New Banzai Class B Shares (as defined herein), and authorized shares of New Banzai Preferred Stock (as defined herein) to 75,000,000 (“Proposal No. 3A”); |

| • | Proposal No. 3B — to provide that the holders of New Banzai Class A Shares will be entitled to cast one vote per New Banzai Class A Share, and holders of New Banzai Class B Shares will be entitled to cast ten votes per New Banzai Class B Share on each matter properly submitted to the stockholders entitled to vote thereon (“Proposal No. 3B”); |

iii

Table of Contents

| • | Proposal No. 3C — to require the approval of Mr. Joseph Davy to amend, repeal, waive, or alter any provision in Section A of Article IV of the Proposed Charter that would adversely affect the rights of holders of New Banzai Class B Shares (“Proposal No. 3C”); |

| • | Proposal No. 3D — to require an affirmative vote of 66 2/3% of the voting power of the shares of capital stock of New Banzai (as defined herein) entitled to vote on the election of directors to alter, amend, or repeal the proposed Amended and Restated Bylaws, the full text of which are attached to the accompanying proxy statement/prospectus as Annex I (the “Proposed Bylaws”) (“Proposal No. 3D”); |

| • | Proposal No. 3E — to require an affirmative vote of 66 2/3% of the voting power of the shares of capital stock of New Banzai entitled to vote thereon to alter, amend, or repeal Articles V, VI, VII, and VIII of the Proposed Charter (“Proposal No. 3E”); |

| • | Proposal No. 3F — to require an affirmative vote of 66 2/3% of the voting power of the shares of capital stock of New Banzai entitled to vote on the election of directors to remove a director with cause (“Proposal No. 3F”); and |

| • | Proposal No. 3G — to approve and adopt the Proposed Charter that includes the approval of Proposals 3A, B, C, D, E and F and provides for certain additional changes, including changing 7GC’s name from “7GC & Co. Holdings Inc.” to “Banzai International, Inc.” and eliminate the provisions relating to 7GC’s status as a blank check company, which the 7GC Board believes are necessary to adequately address the needs of New Banzai immediately following the consummation of the Business Combination (as defined herein) and approval of the Proposed Charter (“Proposal No. 3G”); |

Proposal No. 4 — The Director Election Proposal — to consider and vote upon a proposal to elect, effective at the closing of the Business Combination (the “Closing”), seven directors to serve staggered terms on the New Banzai Board (as defined herein) until the 2024, 2025, and 2026 annual meetings of the stockholders, respectively, or until the election and qualification of their respective successors in office, subject to their earlier death, resignation, or removal (the “Director Election Proposal”);

Proposal No. 5 — The Nasdaq Proposal — to consider and vote upon a proposal to approve, for purposes of complying with the applicable listing rules of The Nasdaq Capital Market (“Nasdaq”): (i) the issuance of New Banzai Class A Shares pursuant to the Merger Agreement; and (ii) the related change of control of 7GC that will occur in connection with the consummation of the Mergers and the other transactions contemplated by the Merger Agreement (the “Nasdaq Proposal”);

Proposal No. 6 — The Incentive Plan Proposal — to consider and vote upon a proposal to approve and adopt the Banzai International, Inc. 2023 Equity Incentive Plan (the “Equity Incentive Plan”) (the “Incentive Plan Proposal”);

Proposal No. 7 — The ESPP Proposal — to consider and vote upon a proposal to approve the Banzai International, Inc. 2023 Employee Stock Purchase Plan (the “ESPP”) (the “ESPP Proposal”); and

Proposal No. 8 — The Adjournment Proposal — to consider and vote upon a proposal to approve the adjournment of the Special Meeting to a later date or dates, if necessary, to permit further solicitation and vote of proxies in the event that there are insufficient shares represented to constitute a quorum necessary to conduct business at the Special Meeting or votes for the approval of one or more proposals at the Special Meeting or to the extent necessary to ensure that any required supplement or amendment to the accompanying proxy statement/prospectus is provided to 7GC stockholders (the “Adjournment Proposal”).

Each of Proposals No. 1, 2, 4, 5, 6, and 7 (the “Condition Precedent Proposals”) is cross-conditioned on the approval of the others. Proposals No. 3 and 8 are not conditioned upon the approval of any other proposal set forth in the accompanying proxy statement/prospectus.

These items of business are described in the accompanying proxy statement/prospectus, which we encourage you to read carefully and in its entirety before voting.

iv

Table of Contents

Only holders of record of Class A common stock, par value $0.0001 per share, of 7GC (the “7GC Class A Common Stock”) and Class B common stock, par value $0.0001 per share, of 7GC (the “7GC Class B Common Stock,” and together with the 7GC Class A Common Stock, the “7GC Common Stock”) at the close of business on , 2023 are entitled to notice of and to vote and have their votes counted at the Special Meeting and any adjournment of the Special Meeting.

The accompanying proxy statement/prospectus and accompanying proxy card is being provided to 7GC’s stockholders in connection with the solicitation of proxies to be voted at the Special Meeting and at any adjournment of the Special Meeting. Whether or not you plan to attend the Special Meeting, all of 7GC’s stockholders are urged to read this proxy statement/prospectus, including the annexes and the documents referred to herein, carefully and in their entirety. You should also carefully consider the risk factors described in the section titled “Risk Factors” beginning on page 29 of the accompanying proxy statement/prospectus.

After careful consideration, 7GC’s board of directors (the “7GC Board”) has unanimously approved the Business Combination and unanimously recommends that stockholders vote “FOR” the adoption of the Business Combination Proposal and “FOR” all other proposals to be presented to 7GC’s stockholders at the Special Meeting. When you consider the recommendation of these proposals by the 7GC Board, you should keep in mind that 7GC’s directors and officers have interests therein that may conflict with your interests as a stockholder. See the section titled “Stockholder Proposal No. 1 — The Business Combination Proposal — Interests of 7GC’s Directors and Executive Officers in the Business Combination” in the accompanying proxy statement/prospectus for a further discussion of these considerations.

Pursuant to the Existing Charter, a holder of public shares (as defined herein) originally sold as part of the units issued in 7GC’s initial public offering (the “IPO”) may request of 7GC that 7GC redeem all or a portion of its public shares for cash, out of funds legally available therefor, if the Business Combination is consummated. As a holder of public shares, you will be entitled to receive cash for any public shares to be redeemed only if you:

| (i) | (a) hold public shares, or (b) if you hold public shares through 7GC Units (as defined herein), you elect to separate your 7GC Units into the underlying public shares and public warrants (as defined herein) prior to exercising your redemption rights with respect to the public shares; |

| (ii) | submit a written request to Continental Stock Transfer & Trust (“Continental”), 7GC’s transfer agent, in which you (a) request that 7GC redeem all or a portion of your public shares for cash, and (b) identify yourself as the beneficial holder of the public shares and provide your legal name, phone number, and address; and |

| (iii) | deliver your public shares to Continental, physically or electronically through The Depository Trust Company (“DTC”). |

Holders must complete the procedures for electing to redeem their public shares in the manner described above prior to 5:00 p.m., Eastern Time, on , 2023 (two business days before the Special Meeting) in order for their public shares to be redeemed.

Holders of units must elect to separate their units into the underlying public shares and public warrants prior to exercising redemption rights with respect to the public shares. If holders hold their units in an account at a brokerage firm or bank, holders must notify their broker or bank that they elect to separate their units into the underlying public shares and public warrants, or if a holder holds units registered in its own name, the holder must contact Continental directly and instruct them to do so. Holders may elect to redeem public shares regardless of how they vote in respect of the Business Combination Proposal. If the Business Combination is not consummated, the public shares submitted for redemption will be returned to the respective holder, broker, or bank.

If the Business Combination is consummated, and if a public stockholder properly exercises its right to redeem all or a portion of the public shares that it holds and timely delivers its shares to Continental, 7GC will

v

Table of Contents

redeem such public shares for a per-share price, payable in cash, equal to the pro rata portion of the Trust Account established at the consummation of our initial public offering (the “Trust Account”), calculated as of two business days prior to the consummation of the Business Combination. For illustrative purposes, as of , 2023, this would have amounted to approximately $ per issued and outstanding public share. If a public stockholder exercises its redemption rights in full, then it will be electing to exchange its public shares for cash and will no longer own shares of 7GC Class A Common Stock. Public shares will be redeemed immediately after consummation of the Business Combination. See the section titled “Special Meeting of 7GC — Redemption Rights” in the accompanying proxy statement/prospectus for a detailed description of the procedures to be followed if you wish to redeem your public shares for cash.

Notwithstanding the foregoing, a public stockholder, together with any affiliate of such public stockholder or any other person with whom such public stockholder is acting in concert or as a “group” (as defined in Section 13(d)(3) of the Securities and Exchange Act, as amended (the “Exchange Act”)), will be restricted from redeeming its public shares with respect to more than an aggregate of 15% of the public shares without the prior consent of 7GC. Accordingly, if a public stockholder, alone or acting in concert or as a group, seeks to redeem more than 15% of the public shares, then any such shares in excess of that 15% limit would not be redeemed for cash without the prior consent of 7GC.

7GC & Co. Holdings LLC, a Delaware limited liability company and stockholder of 7GC (the “Sponsor”), and each officer and director of 7GC (together with the Sponsor, the “Sponsor Persons”) have agreed to, among other things, vote in favor of any proposed business combination and to waive their redemption rights in connection with such stockholder approval. The Sponsor has also agreed to, among other things, vote in favor of the Business Combination Proposal and the transactions contemplated thereby, including the other Condition Precedent Proposals. The shares of 7GC Common Stock held by the Sponsor Persons will be excluded from the pro rata calculation used to determine the per-share redemption price. As of the date of the accompanying proxy statement/prospectus, the Sponsor Persons, collectively, own approximately 5,750,000 (or %) of the issued and outstanding shares of 7GC Common Stock (5,650,000 of which are held by the Sponsor (396,500 shares of which are subject to forfeiture at closing of an initial business combination of 7GC pursuant to the Non-Redemption Agreements (as defined herein)), and 100,000 of which, in the aggregate, are held by the independent directors).

The approval of the Charter Proposals requires an affirmative vote of the holders of at least a majority of the outstanding shares of 7GC Common Stock entitled to vote thereon, voting together as a single class, an affirmative vote of the holders of at least a majority of the outstanding shares of 7GC Class A Common Stock entitled to vote thereon, voting separately as a single class, and an affirmative vote of the holders of at least a majority of the outstanding shares of 7GC Class B Common Stock entitled to vote thereon, voting separately as a single class. The approval of the Business Combination Proposal, Nasdaq Proposal, Incentive Plan Proposal, ESPP Proposal, and Adjournment Proposal require the affirmative vote of a majority of the votes cast by the holders of 7GC Common Stock represented electronically or by proxy at the Special Meeting and entitled to vote thereon. The approval of the election of each director nominee pursuant to the Director Election Proposal requires the affirmative vote of a plurality of the votes cast by the holders of 7GC Common Stock represented electronically or by proxy at the Special Meeting and entitled to vote thereon.

Your vote is very important. Whether or not you plan to attend the Special Meeting, please vote as soon as possible by following the instructions in the accompanying proxy statement/prospectus to make sure that your shares are represented at the Special Meeting. If you hold your shares in “street name” through a bank, broker, or other nominee, you will need to follow the instructions provided to you by your bank, broker or other nominee to ensure that your shares are represented and voted at the Special Meeting. In most cases you may vote by telephone or over the Internet as instructed. The transactions contemplated by the Merger Agreement will be consummated only if the Condition Precedent Proposals are approved at the Special Meeting. Each of the Condition Precedent Proposals is cross-conditioned on the approval of the others. The Advisory Charter Proposals and the Adjournment Proposal are not conditioned upon the approval of any other proposal set forth in the accompanying proxy statement/prospectus.

vi

Table of Contents

If you sign, date, and return your proxy card without indicating how you wish to vote, your proxy will be voted FOR each of the proposals presented at the Special Meeting. If you fail to return your proxy card or fail to instruct your bank, broker, or other nominee how to vote, and do not attend the Special Meeting, the effect will be, among other things, that your shares will not be counted for purposes of determining whether a quorum is present at the Special Meeting and will not be voted. An abstention will be counted towards the quorum requirement but will not count as a vote cast at the Special Meeting. A broker non-vote will not count as a vote cast at the Special Meeting. A broker non-vote with respect to some, but not all, of the proposals to be presented at the Special Meeting will be considered present for purposes of establishing a quorum. If you are a stockholder of record and you attend the Special Meeting and wish to vote, you may withdraw your proxy and vote virtually.

Your attention is directed to the remainder of the accompanying proxy statement/prospectus following this notice (including the annexes and other documents referred to herein) for a more complete description of the proposed Business Combination and related transactions and each of the proposals. You are encouraged to read the accompanying proxy statement/prospectus carefully and in its entirety, including the annexes and other documents referred to herein. If you have any questions or need assistance voting your shares of 7GC Common Stock, please contact Morrow Sodali LLC, 7GC’s proxy solicitor (the “Proxy Solicitor”), by calling (800) 662-5200, or by emailing vii.info@investor.morrowsodali.com, or banks and brokers can call collect at (203) 658-9400.

Thank you for your participation. We look forward to your continued support.

| By Order of the 7GC Board,

|

| Jack Leeney |

| Chairman and Chief Executive Officer 7GC & Co. Holdings Inc. |

TO EXERCISE YOUR REDEMPTION RIGHTS, YOU MUST DEMAND IN WRITING THAT YOUR PUBLIC SHARES ARE REDEEMED FOR A PRO RATA PORTION OF THE FUNDS HELD IN THE TRUST ACCOUNT AND TENDER YOUR SHARES TO 7GC’S TRANSFER AGENT AT LEAST TWO BUSINESS DAYS PRIOR TO THE VOTE AT THE SPECIAL MEETING. YOU MAY TENDER YOUR SHARES BY EITHER DELIVERING YOUR SHARE CERTIFICATE TO THE TRANSFER AGENT OR BY DELIVERING YOUR SHARES ELECTRONICALLY USING THE DEPOSITORY TRUST COMPANY’S DWAC (DEPOSIT WITHDRAWAL AT CUSTODIAN) SYSTEM. IF THE BUSINESS COMBINATION IS NOT CONSUMMATED, THEN THESE SHARES WILL BE RETURNED TO YOU OR YOUR ACCOUNT. IF YOU HOLD THE SHARES IN STREET NAME, YOU WILL NEED TO INSTRUCT THE ACCOUNT EXECUTIVE AT YOUR BANK OR BROKER TO WITHDRAW THE SHARES FROM YOUR ACCOUNT IN ORDER TO EXERCISE YOUR REDEMPTION RIGHTS.

vii

Table of Contents

REFERENCES TO ADDITIONAL INFORMATION

This proxy statement/prospectus incorporates important business and financial information that is not included in or delivered with this proxy statement/prospectus. This information is available for you to review through the United States Securities and Exchange Commission (“SEC”) website at www.sec.gov. You may request copies of this proxy statement/prospectus and any of the documents incorporated by reference into this proxy statement/prospectus or other publicly available information concerning 7GC, without charge, by written request to 7GC at 7GC & Co. Holdings Inc., 388 Market Street, Suite 1300, San Francisco, CA 94111, or by telephone request at (628) 400-9284; or the Proxy Solicitor, by calling (800) 662-5200, or banks and brokers can call collect at (203) 658-9400, or by emailing vii.info@investor.morrowsodali.com; or from the SEC through the SEC website at the address provided above.

In order for 7GC’s stockholders to receive timely delivery of the documents in advance of the Special Meeting to be held on , 2023, you must request the information no later than , 2023 (five business days prior to the date of the Special Meeting).

viii

Table of Contents

TRADEMARKS

This document contains references to trademarks, trade names, and service marks belonging to other entities. Solely for convenience, trademarks, trade names, and service marks referred to in this proxy statement/prospectus may appear without the ® or TM symbols, but such references are not intended to indicate, in any way, that the applicable licensor will not assert, to the fullest extent under applicable law, its rights to these trademarks and trade names. Neither 7GC nor Banzai intends its use or display of other companies’ trade names, trademarks, or service marks to imply a relationship with, or endorsement or sponsorship of it, by any other companies.

ix

Table of Contents

SELECTED DEFINITIONS

Unless otherwise stated in this proxy statement/prospectus or the context otherwise requires, references to:

| • | “7GC” and, except as otherwise noted, “we,” “us,” and “our,” are to 7GC & Co. Holdings Inc., a Delaware corporation; |

| • | “7GC Preferred Stock” are to shares of preferred stock of 7GC, par value $0.0001 per share; |

| • | “7GC Private Placement Warrants” are to the 7,350,000 7GC Warrants that were issued to the Sponsor in a private placement (the “Private Placement”) in connection with the IPO; |

| • | “7GC Public Warrants” or “public warrants” are to the 11,500,000 7GC Warrants, a fraction equal to one-half of which was included in each unit sold as part of the IPO, and which are issued and outstanding immediately prior to the First Effective Time; |

| • | “7GC Units” or “units” are to each issued and outstanding unit of 7GC prior to the First Effective Time; |

| • | “7GC Warrants” are to warrants to purchase one share of 7GC Class A Common Stock at an exercise price of $11.50; |

| • | “A&R Company Support Agreement” are to that certain amended and restated support agreement, dated as of August 4, 2023, by and between Banzai and certain stockholders of Banzai set forth on Schedule I thereto (each a “Banzai Stockholder” and, collectively, the “Banzai Stockholders”), a copy of which is attached to this proxy statement/prospectus as Annex C and which agreement amended and restated the Original Company Support Agreement (as defined herein) in its entirety; |

| • | “A&R Registration Rights Agreement” are to the Amended and Restated Registration Rights Agreement to be entered into at the Closing by and among New Banzai, the Sponsor, other Pre-IPO Holders (as defined therein), and certain persons receiving shares of New Banzai Common Stock pursuant to the Mergers, the form of which is attached to this proxy statement/prospectus as Annex E; |

| • | “Ancillary Documents” are to the Merger Agreement, the A&R Registration Rights Agreement, the Lock-up Agreements, the A&R Company Support Agreement, the Sponsor Support Agreement, each letter of transmittal and each other agreement, document, instrument and/or certificate contemplated by the Merger Agreement to be executed in connection with the transactions contemplated thereby; |

| • | “Banzai Class A Common Stock” are to shares of Class A common stock of Banzai, par value $0.0001 per share; |

| • | “Banzai Class B Common Stock” are to shares of Class B common stock of Banzai, par value $0.0001 per share; |

| • | “Banzai Common Stock” are to shares of Banzai Class A Common Stock and shares of Banzai Class B Common Stock, collectively; |

| • | “Banzai Management Stockholders” are to Joseph Davy, Simon Baumer, Mark Musburger, Rachel Stanley, and Ashley Levesque; |

| • | “Business Combination” are to the combination of 7GC, Banzai, First Merger Sub, and Second Merger Sub pursuant to the transactions provided for and contemplated in the Merger Agreement; |

| • | “Code” are to the Internal Revenue Code of 1986, as amended; |

| • | “Company Expenses” are to, without duplication, the aggregate unpaid amount due and payable as of the Second Effective Time by any Banzai or its subsidiaries, for (i) out-of-pocket fees, costs and expenses incurred in connection with the negotiation, preparation or execution of the Merger |

x

Table of Contents

| Agreement or any Ancillary Documents and the consummation of the transactions contemplated hereby and thereby (including the fees and expenses of outside legal counsel, accountants, advisors, investment bankers, brokers, consultants or other agents (including, for the avoidance of doubt, to perform any compensation studies)), (ii) the cost of the Company D&O Tail Policy (as defined in the Merger Agreement) to be obtained pursuant to Section 5.5 of the Merger Agreement, (iii) the costs and expenses of any consultant or advisor engaged to prepare a compensation study in connection with implementation of the New Incentive Plan (as defined in the Merger Agreement), (iv) any filing fee to be paid pursuant to the HSR Act, (v) the filing fee to be paid for the Registration Statement / Proxy Statement, and (vi) any other fees, expenses, commissions or other amounts that are expressly allocated to any Banzai or its subsidiaries, or the Pre-Closing Holders pursuant to the Merger Agreement or any Ancillary Document, in each case as of the Second Effective Time. |

| • | “Conversion Amount” are to with respect to each Senior Convertible Note means, on any date of determination, the outstanding principal, accrued and unpaid interest, and all fees and other obligations then payable in respect of such Senior Convertible Note; |

| • | “DGCL” are to the General Corporation Law of the State of Delaware; |

| • | “Exchange Ratio” are to the quotient obtained by dividing (i) the Per Share Value by (ii) $10.00; |

| • | “Existing Banzai Securityholders” are to the holders of Banzai’s securities immediately prior to the Closing; |

| • | “Existing Organizational Documents” are to 7GC’s Bylaws, dated as of September 18, 2020, and the Existing Charter; |

| • | “Extension” are to the extension of the date by which 7GC must consummate its initial business combination from December 28, 2022 to June 28, 2023, or such earlier date as determined by the 7GC Board, approved by the public stockholders at the Extension Meeting; |

| • | “Extension Meeting” are to the special meeting in lieu of an annual meeting of the stockholders of 7GC held on December 21, 2022; |

| • | “First Effective Time” are to the time at which the First Merger shall become effective in accordance with the terms of the Merger Agreement; |

| • | “First Merger” are to the merger of First Merger Sub with and into Banzai, with Banzai as the Surviving Corporation, in accordance with the terms and subject to the conditions set forth in the Merger Agreement; |

| • | “founder shares” are to the shares of 7GC Class B Common Stock initially purchased by the Sponsor in a private placement prior to the IPO; |

| • | “GAAP” are to accounting principles generally accepted in the United States of America; |

| • | “HSR Act” are to the Hart-Scott-Rodino Antitrust Improvements Act of 1976, as amended; |

| • | “Investment Company Act” are to the Investment Company Act of 1940, as amended; |

| • | “IPO registration statement” are to the Registration Statement on Form S-1 (333-251162) filed by 7GC in connection with its IPO, which became effective on December 22, 2020; |

| • | “IRS” are to the U.S. Internal Revenue Service; |

| • | “Lock-up Agreements” are to those certain lock-up agreements between New Banzai and certain stockholders of Banzai to be entered into at Closing, a copy of the form of which is attached to this proxy statement/prospectus as Annex D; |

| • | “Mergers” are to the First Merger and the Second Merger, together; |

xi

Table of Contents

| • | “New Award Grants” are to equity awards to be issued to employees and management of New Banzai under the Equity Incentive Plan; |

| • | “New Banzai” are to 7GC immediately following the consummation of the Business Combination and approval of the Proposed Charter; |

| • | “New Banzai Board” are to the board of directors of New Banzai following the consummation of the Business Combination and the election of directors pursuant to the Director Election Proposal; |

| • | “New Banzai Common Stock” are to the New Banzai Class A Shares and the New Banzai Class B Shares, collectively, following the consummation of the Business Combination and approval of the Proposed Charter; |

| • | “New Banzai Class A Shares” are to shares of Class A common stock of New Banzai, par value $0.0001 per share, following the consummation of the Business Combination and approval of the Proposed Charter; |

| • | “New Banzai Class B Shares” are to shares of Class B common stock of New Banzai, par value $0.0001 per share, following the consummation of the Business Combination and approval of the Proposed Charter; |

| • | “New Banzai Preferred Stock” are to shares of preferred stock of New Banzai, par value $0.0001 per share, following the consummation of the Business Combination and approval of the Proposed Charter; |

| • | “New Banzai Warrants” are to warrants to purchase one Banzai Class A Share at an exercise price of $11.50, following the consummation of the Business Combination; |

| • | “Original Company Support Agreement” are to that certain support agreement, dated as of December 8, 2022, by and between Banzai and the Banzai Stockholders; |

| • | “Per Share Value” are to (i) an amount equal to $100,000,000, payable in New Banzai Class A Shares or New Banzai Class B Shares, as applicable, divided by (ii) (A) the total number of shares of Banzai Class A Common Stock and Banzai Class B Common Stock issued and outstanding as of immediately prior to the First Effective Time, (B) the maximum aggregate number of shares of Banzai Class A Common Stock issuable upon full exercise of options of Banzai to purchase Banzai Class A Common Stock (the “Banzai Options”) issued, outstanding and vested immediately prior to the First Effective Time, (C) the maximum aggregate number of shares of Banzai Class A Common Stock issuable upon conversion of the Conversion Amount under each Senior Convertible Note as of immediately prior to the First Effective Time at the applicable Senior Convertible Note Conversion Price, (D) the maximum aggregate number of shares of Banzai Class A Common Stock issuable upon conversion of all of the outstanding principal and interest under each Subordinated Convertible Note as of immediately prior to the First Effective Time at the applicable Subordinated Convertible Note Conversion Price, and (E) the maximum aggregate number of shares of Banzai Class A Common Stock issuable upon conversion of the SAFE Purchase Amount under each SAFE Right as of immediately prior to the First Effective Time at the applicable SAFE Conversion Price; |

| • | “Pre-Closing Holder” are to direct or indirect securityholders of Banzai immediately prior to the First Effective Time; |

| • | “Promissory Note” are to an unsecured promissory note, dated as of December 21 2022, issued by 7GC to the Sponsor, pursuant to which 7GC may borrow up to $2,300,000 from the Sponsor; |

| • | “public shares” are to shares of 7GC Class A Common Stock (including those included in the units) that were offered and sold by 7GC in its initial public offering and registered pursuant to the IPO registration statement; |

xii

Table of Contents

| • | “public stockholders” are to holders of public shares, whether acquired in the IPO or acquired in the secondary market; |

| • | “SAFE Conversion Price” are to, with respect to each SAFE Right, the Valuation Cap Price (as defined in each SAFE Agreement); |

| • | “SAFE Purchase Amount” are to, with respect to each SAFE Right, the Purchase Amount (as defined in the applicable SAFE Agreement that governs such SAFE Right); |

| • | “SAFE Right” are to the right of each SAFE investor to receive a portion of the Total Consideration pursuant to certain Simple Agreements for Future Equity (each, a “SAFE Agreement”); |

| • | “Sarbanes-Oxley Act” are to the Sarbanes-Oxley Act of 2002; |

| • | “Second Effective Time” are to the time at which the Second Merger shall become effective in accordance with the terms of the Merger Agreement; |

| • | “Second Extension” are to the extension of the date by which 7GC must consummate its initial business combination from June 28, 2023 to December 28, 2023, or such earlier date as determined by the 7GC Board, approved by the public stockholders at the Second Extension Meeting; |

| • | “Second Extension Meeting” are to the special meeting in lieu of an annual meeting of the stockholders of 7GC held on June 26, 2023; |

| • | “Second Merger” are to the merger of the Surviving Corporation with and into Second Merger Sub, with Second Merger Sub as the surviving entity in accordance with the terms and subject to the conditions set forth in the Merger Agreement; |

| • | “Securities Act” are to the Securities Act of 1933, as amended; |

| • | “Senior Convertible Notes” are to the Convertible Promissory Note issued by Banzai to CP BF Lending, LLC, dated as of February 19, 2021, in the principal amount of $1,500,000, and the Convertible Promissory Note issued by Banzai to CP BF Lending, LLC, dated as of October 10, 2022, in the principal amount of $321,345.31; |

| • | “Senior Convertible Note Conversion Price” are to, with respect to each Senior Convertible Note, the Conversion Price (as defined in and determined pursuant to the terms of such Senior Convertible Note); |

| • | “Sponsor Forfeiture Agreement” are to that certain sponsor forfeiture agreement, dated as of August 4, 2023, by and between 7GC, Banzai, and the Sponsor, a copy of which is attached to this proxy statement/prospectus as Annex K; |

| • | “Sponsor Support Agreement” are to that certain agreement, dated as of December 8, 2022, by and between 7GC, Banzai, and the Sponsor, a copy of which is attached to this proxy statement/prospectus as Annex B; |

| • | “Subordinated Convertible Notes” are to the Subordinated Convertible Promissory Notes set forth in Section 1.1(a) of the Company Schedules (as defined in the Merger Agreement); |

| • | “Subordinated Convertible Note Conversion Price” are to, with respect to each Subordinated Convertible Note, the quotient obtained by dividing the Valuation Cap by the Fully Diluted Capitalization, each as defined in and determined pursuant to the terms of such Subordinated Convertible Note; |

| • | “Surviving Corporation” are to the surviving corporation of the First Merger; |

| • | “Total Consideration” are to $100,000,000, payable in New Banzai Class A Shares or New Banzai Class B Shares, as applicable; |

xiii

Table of Contents

| • | “Treasury Regulations” are to the regulations, including proposed and temporary regulations, promulgated under the Code; |

| • | “Trust Agreement” are to the Investment Management Trust Agreement, dated December 22, 2020, by and between 7GC and Continental, as trustee; and |

| • | “Working Capital Loans” are to the funds that the Sponsor or an affiliate of the Sponsor may loan to 7GC as may be required. |

Unless otherwise stated in this proxy statement/prospectus or the context otherwise requires, all references in this proxy statement/prospectus to shares of 7GC Class A Common Stock, public shares, 7GC Public Warrants, or 7GC Warrants include any such securities underlying the 7GC Units, as applicable.

xiv

Table of Contents

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

Certain statements included in this proxy statement/prospectus are not historical facts but are forward-looking statements, including for purposes of the safe harbor provisions under the United States Private Securities Litigation Reform Act of 1995. Forward-looking statements generally are accompanied by words such as “believe,” “may,” “will,” “estimate,” “continue,” “anticipate,” “intend,” “expect,” “should,” “would,” “plan,” “project,” “forecast,” “predict,” “potential,” “seem,” “seek,” “future,” “outlook,” “target,” and similar expressions that predict or indicate future events or trends or that are not statements of historical matters, but the absence of these words does not mean that a statement is not forward-looking. These forward-looking statements include, but are not limited to, (1) references with respect to the anticipated benefits of the Business Combination and anticipated closing timing; (2) the sources and uses of funds for the Business Combination, (3) the anticipated capitalization and enterprise value of the combined company following the consummation of the Business Combination; and (4) current and future potential commercial and customer relationships. These statements are based on various assumptions, whether or not identified in this proxy statement/prospectus, and on the current expectations of 7GC’s and Banzai’s management and are not predictions of actual performance. These forward-looking statements are provided for illustrative purposes only and are not intended to serve as, and must not be relied on by any investor as, a guarantee, an assurance, a prediction or a definitive statement of fact or probability. Actual events and circumstances are difficult or impossible to predict and will differ from assumptions. Many actual events and circumstances are beyond the control of 7GC and Banzai. These forward-looking statements are subject to a number of risks and uncertainties, including: changes in domestic and foreign business, market, financial, political and legal conditions; the inability of the parties to successfully or timely consummate the Business Combination, including the risk that any required stockholder or regulatory approvals are not obtained, are delayed or are subject to unanticipated conditions that could adversely affect the combined company; failure to realize the anticipated benefits of the Business Combination; risks relating to the uncertainty of the projected financial information with respect to Banzai; Banzai’s ability to successfully and timely develop, sell and expand its technology and products, and otherwise implement its growth strategy; risks relating to Banzai’s operations and business, including information technology and cybersecurity risks, loss of customers and deterioration in relationships between Banzai and its employees; risks related to increased competition; risks relating to potential disruption of current plans, operations and infrastructure of Banzai as a result of the announcement and consummation of the Business Combination; risks that the post-combination company experiences difficulties managing its growth and expanding operations; the amount of redemption requests made by 7GC’s stockholders; the impact of geopolitical, macroeconomic and market conditions, including the COVID-19 pandemic; the ability to successfully select, execute or integrate future acquisitions into the business, which could result in material adverse effects to operations and financial conditions; and those other factors discussed in the section titled “Risk Factors” contained in this proxy statement/prospectus. If any of these risks materialize or our assumptions prove incorrect, actual results could differ materially from the results implied by these forward-looking statements. The risks and uncertainties above are not exhaustive, and there may be additional risks that neither 7GC nor Banzai presently know or that 7GC and Banzai currently believe are immaterial that could also cause actual results to differ from those contained in the forward-looking statements. In addition, forward-looking statements reflect 7GC’s and Banzai’s expectations, plans or forecasts of future events and views as of the date of this proxy statement/prospectus. 7GC and Banzai anticipate that subsequent events and developments will cause 7GC’s and Banzai’s assessments to change. However, while 7GC and Banzai may elect to update these forward-looking statements at some point in the future, 7GC and Banzai specifically disclaim any obligation to do so. These forward-looking statements should not be relied upon as representing 7GC’s and Banzai’s assessments as of any date subsequent to the date of this proxy statement/prospectus. Accordingly, undue reliance should not be placed upon the forward-looking statements.

xv

Table of Contents

QUESTIONS AND ANSWERS

The questions and answers below highlight only selected information from this document and only briefly address some commonly asked questions about the proposals to be presented at the Special Meeting, including with respect to the proposed Business Combination. The following questions and answers do not include all the information that is important to 7GC’s stockholders. 7GC urges stockholders to read this proxy statement/prospectus, including the annexes and the other documents referred to herein, carefully and in their entirety to fully understand the proposed Business Combination and the voting procedures for the Special Meeting.

| Q: | Why am I receiving this proxy statement/prospectus? |

| A: | You are receiving these materials because you are a stockholder of record or a beneficial holder of 7GC on , 2023, the record date for the Special Meeting. 7GC and Banzai have agreed to a business combination through a series of transactions, including the Mergers, subject to the terms and conditions of the Merger Agreement and the Ancillary Documents. A copy of the Original Merger Agreement is attached to this proxy statement/prospectus as Annex A-1 and a copy of the Amendment is attached to this proxy statement/prospectus as Annex A-2. 7GC stockholders are being asked to consider and vote upon a proposal to approve the Business Combination and a number of other proposals. See the section titled “Stockholder Proposal No. 1 — The Business Combination Proposal” for more detail. |

THE VOTE OF STOCKHOLDERS IS IMPORTANT. STOCKHOLDERS ARE ENCOURAGED TO VOTE AS SOON AS POSSIBLE AFTER CAREFULLY REVIEWING THIS PROXY STATEMENT/ PROSPECTUS IN ITS ENTIRETY, INCLUDING THE ANNEXES AND THE ACCOMPANYING FINANCIAL STATEMENTS OF 7GC AND BANZAI.

| Q: | How do I attend the meeting virtually? |

| A: | The Special Meeting will be accessible virtually via a live webcast at , at , Eastern Time, on , 2023. To participate in the virtual meeting, including the voting of shares, 7GC stockholders of record will need to enter the control number shown on their proxy card. |

The Special Meeting webcast will begin promptly at , Eastern Time. 7GC stockholders are encouraged to access the Special Meeting prior to the start time. If you encounter any difficulties accessing the virtual meeting or during the meeting time, please call the technical support number that will be posted on the virtual meeting login page.

| Q: | What are the transactions described in this document? |

| A: | On December 8, 2022, 7GC entered into the Original Merger Agreement, and further, on August 4, 2023, entered into the Amendment, which amended and restated certain terms and conditions of and exhibits to the Original Merger Agreement. Pursuant to the Merger Agreement, the parties thereto will enter into the Business Combination, pursuant to which, among other things, (i) First Merger Sub will merge with and into Banzai, with Banzai being the Surviving Corporation, and (ii) promptly following the First Merger, the Surviving Corporation will merge with and into Second Merger Sub, with Second Merger Sub being the surviving entity of the Second Merger. Following the Mergers, Banzai shall continue its existence under the DGCL as a wholly owned subsidiary of 7GC. The 7GC Units, 7GC Class A Common Stock and 7GC Public Warrants are currently listed on Nasdaq, under the symbols “VIIAU,” “VII,” and “VIIAW,” respectively. 7GC has applied to continue the listing of 7GC Class A Common Stock and 7GC Public Warrants on Nasdaq under the symbols “BNZI” and “BNZIW,” respectively, upon the Closing. At the Closing, each 7GC Unit will separate into its components consisting of one share of 7GC Class A Common Stock and one-half of one 7GC Public Warrant and, as a result, will no longer trade as a separate security. At the Closing, 7GC will change its name to Banzai International, Inc. |

xvi

Table of Contents

| Q: | What will happen in the Mergers? |

| A: | Effect of the First Merger. On the terms and subject to the conditions set forth in the Merger Agreement, at the First Effective Time, each outstanding share of Banzai Class A Common Stock and each outstanding share of Banzai Class B Common Stock (in each case, other than dissenting shares and any shares held in the treasury of Banzai) shall be cancelled and converted into the right to receive a number of New Banzai Class A Shares or New Banzai Class B Shares, respectively, equal to the Exchange Ratio. |

Treatment of Outstanding Equity Awards

In addition, as of the First Effective Time: (i) each Banzai Option, whether vested or unvested, that is outstanding immediately prior to the First Effective Time and held by a Pre-Closing Holder who is providing services to Banzai immediately prior to the First Effective Time (a “Pre-Closing Holder Service Provider”), will be assumed and converted into an option (a “7GC Option”) with respect to a number of New Banzai Class A Shares calculated in the manner set forth in the Merger Agreement; and (ii) the vested portion of each Banzai Option that is outstanding at such time and held by a Pre-Closing Holder who is not then providing services to Banzai (a “Pre-Closing Holder Non-Service Provider”) will be assumed and converted into a 7GC Option with respect to a number of New Banzai Class A Shares calculated in the manner set forth in the Merger Agreement.

Treatment of SAFE Rights

As of the First Effective Time, each SAFE Right that is outstanding immediately prior to the First Effective Time shall be cancelled and converted into and become the right to receive a number of New Banzai Class A Shares equal to (i) the SAFE Purchase Amount in respect of such SAFE Right divided by the SAFE Conversion Price in respect of such SAFE Right multiplied by (ii) the Exchange Ratio.

Treatment of Convertible Notes

As of the First Effective Time, (i) each Subordinated Convertible Note that is outstanding immediately prior to the First Effective Time will be cancelled and converted into the right to receive a number of shares of 7GC Class A Common Stock equal to (1) all of the outstanding principal and interest in respect of such Subordinated Convertible Note, divided by the Subordinated Convertible Note Conversion Price in respect of such Subordinated Convertible Note, multiplied by (2) the Exchange Ratio, and (ii) each Senior Convertible Note that is outstanding immediately prior to the First Effective Time will be cancelled and converted into the right to receive a number of New Banzai Class A Shares equal to (1) the Conversion Amount in respect of such Senior Convertible Note, multiplied by (2) the Exchange Ratio.

Effect of the Second Merger. On the terms and subject to the conditions set forth in the Merger Agreement, at the Second Effective Time, by virtue of the Second Merger, each share of common stock of the Surviving Corporation issued and outstanding immediately prior to the Second Effective Time shall be cancelled and no consideration shall be delivered therefor.

| Q: | How will New Banzai be managed following the Business Combination? |

| A: | Following the Closing, it is expected that the current management of Banzai will become the management of New Banzai, and the New Banzai Board will consist of seven directors, who will be divided into three classes: (i) two Class I New Banzai directors, whose initial term shall expire at the 2024 annual meeting of the stockholders of New Banzai, (ii) two Class II New Banzai directors, whose initial term shall expire at the 2025 annual meeting of the stockholders of New Banzai, and (iii) three Class III New Banzai directors, whose initial term shall expire at the 2026 annual meeting of the stockholders of New Banzai. |

Please see the section titled “Management of New Banzai after the Business Combination.”

xvii

Table of Contents

| Q: | Is the completion of the Business Combination subject to any conditions? |

| A: | Yes. The respective obligations of each party to effect the Closing are subject to the fulfillment (or, to the extent permitted by applicable law, waiver) of certain conditions specified in the Merger Agreement. |

The Merger Agreement provides that the obligations of the parties to consummate the Transactions are conditioned on, among other things: (i) approval of the Condition Precedent Proposals by the requisite 7GC stockholders, (ii) the expiration or termination of the waiting period under the HSR Act, (iii) no order, statute, rule or regulation enjoining or prohibiting the consummation of the Transactions being in force, (iv) having this proxy statement/prospectus declared effective under the Securities Act, (v) the New Banzai Class A Shares to be issued pursuant to the Merger Agreement having been approved for listing on Nasdaq, (vi) 7GC having at least $5,000,001 of net tangible assets remaining after redemptions by 7GC stockholders, and (vi) customary bring-down conditions related to the representations, warranties, and pre-Closing covenants in the Merger Agreement. Additionally, the obligations of Banzai and its subsidiaries to consummate the Transactions are also conditioned upon, among other things, (a) 7GC having delivered to Banzai executed copies of the A&R Registration Rights Agreement and the Exchange Agent Agreement (as defined in the Merger Agreement), and evidence that the Proposed Charter has been filed with the Secretary of State of Delaware, and (b) the sum of (i)(A) the cash proceeds to be received by 7GC at Closing from the Trust Account (after, for the avoidance of doubt, giving effect to redemptions by 7GC stockholders), (B) the cash proceeds to be received by 7GC or any of Banzai or its subsidiaries from any financing, whether equity or debt, at or immediately following the Closing, and (C) the unrestricted cash on the balance sheet of Banzai as of immediately prior to the Closing, minus (ii) the 7GC Transaction Expenses, minus (iii) the Company Expenses equaling or exceeding $5,000,000. 7GC’s obligation to consummate the Business Combination is also subject to there having been no “Company Material Adverse Effect” (as defined in the Merger Agreement) since the date of the Merger Agreement that is continuing and uncured.

To the extent that the 7GC Board determines that any modifications by the parties, including any waivers of any conditions to the Closing, materially change the terms of the Business Combination, 7GC and Banzai will notify their respective equityholders in a manner reasonably calculated to inform them about the modifications as may be required by law, by publishing a press release, and/or filing a current report on Form 8-K, and by circulating a supplement to this proxy statement/prospectus to resolicit the votes of 7GC stockholders, if required. For more information about conditions to the consummation of the Business Combination, see the section titled “Stockholder Proposal No. 1 — The Business Combination Proposal — Summary of the Merger Agreement — Conditions to Closing.”

| Q: | Following the Business Combination, will 7GC’s securities continue to trade on a stock exchange? |

| A: | Yes. We anticipate that, following the Business Combination, 7GC Class A Common Stock and 7GC Public Warrants will continue trading on Nasdaq under the new symbols “BNZI” and “BNZIW,” respectively. The 7GC Units will automatically separate into the component securities upon consummation of the Business Combination and, as a result, will no longer trade as a separate security. |

| Q: | What proposals are stockholders of 7GC being asked to vote upon? |

| A: | At the Special Meeting, 7GC is asking holders of 7GC Common Stock to consider and vote upon: |

Proposal No. 1 — The Business Combination Proposal — a proposal to approve and adopt the Merger Agreement and the transactions contemplated by the Merger Agreement, including the Mergers, as more fully described elsewhere in this proxy statement/prospectus;

Proposal No. 2 — The Binding Charter Proposal — a proposal to approve the Proposed Charter, which will replace the Existing Charter and will be in effect upon the Closing;

xviii

Table of Contents

Proposal No. 3 — The Advisory Charter Proposals — separate proposals to approve, on a non-binding advisory basis, the following material differences between the Proposed Charter and the Existing Charter, which are being presented in accordance with the SEC guidance as separate sub-proposals:

| • | Proposal No. 3A — to increase the authorized shares of New Banzai Common Stock to 275,000,000 shares, consisting of 250,000,000 New Banzai Class A Shares and 25,000,000 New Banzai Class B Shares, and authorized shares of New Banzai Preferred Stock to 75,000,000; |

| • | Proposal No. 3B — to provide that the holders of New Banzai Class A Shares will be entitled to cast one vote per New Banzai Class A Share, and holders of New Banzai Class B Shares will be entitled to cast ten votes per New Banzai Class B Share on each matter properly submitted to the stockholders entitled to vote thereon; |

| • | Proposal No. 3C — to require the approval of Mr. Joseph Davy to amend, repeal, waive, or alter any provision of Section A of Article IV of the Proposed Charter that would adversely affect the rights of holders of New Banzai Class B Shares; |

| • | Proposal No. 3D — to require an affirmative vote of 66 2/3% of the voting power of the shares of capital stock of New Banzai entitled to vote on the election of directors to alter, amend, or repeal the Proposed Bylaws; |

| • | Proposal No. 3E — to require an affirmative vote of 66 2/3% of the voting power of the shares of capital stock of New Banzai entitled to vote thereon to alter, amend, or repeal Articles V, VI, VII, and VIII of the Proposed Charter; |

| • | Proposal No. 3F — to require an affirmative vote of 66 2/3% of the voting power of the shares of capital stock of New Banzai entitled to vote on the election of directors to remove a director with cause; and |

| • | Proposal No. 3G — to approve and adopt the Proposed Charter that includes the approval of Proposals 3A, B, C, D, E and F and provides for certain additional changes, including changing 7GC’s name from “7GC & Co. Holdings Inc.” to “Banzai International, Inc.” and eliminate the provisions relating to 7GC’s status as a blank check company, which the 7GC Board believes are necessary to adequately address the needs of New Banzai immediately following the consummation of the Business Combination and approval of the Proposed Charter; |

Proposal No. 4 — The Director Election Proposal — a proposal to elect, effective at the Closing, seven directors to serve staggered terms on the New Banzai Board until the 2024, 2025, and 2026 annual meetings of the stockholders, respectively, or until the election and qualification of their respective successors in office, subject to their earlier death, resignation, or removal;

Proposal No. 5 — The Nasdaq Proposal — proposal to approve, for purposes of complying with the applicable listing rules of Nasdaq: (i) the issuance of New Banzai Class A Shares pursuant to the Merger Agreement, and (ii) the related change of control of 7GC that will occur in connection with the consummation of the Mergers and the other transactions contemplated by the Merger Agreement;

Proposal No. 6 — The Incentive Plan Proposal — a proposal to approve and adopt the Equity Incentive Plan;

Proposal No. 7 — The ESPP Proposal — a proposal to approve the ESPP; and

Proposal No. 8 — The Adjournment Proposal — a proposal to approve the adjournment of the Special Meeting to a later date or dates, if necessary, to permit further solicitation and vote of proxies in the event that there are insufficient shares represented to constitute a quorum necessary to conduct business at the Special Meeting or votes for the approval of one or more proposals at the Special Meeting or to the extent necessary to ensure that any required supplement or amendment to the accompanying proxy statement/prospectus is provided to 7GC stockholders.

xix

Table of Contents

If our stockholders do not approve each of the Condition Precedent Proposals, then unless certain conditions in the Merger Agreement are waived by the applicable parties to the Merger Agreement, the Merger Agreement may be terminated and the Business Combination may not be consummated. See the section titled “Stockholder Proposal No. 1 — The Business Combination Proposal,” “Stockholder Proposal No. 2 — The Binding Charter Proposal,” “Stockholder Proposal No. 3 – The Advisory Charter Proposals,” “Stockholder Proposal No. 4 — The Director Election Proposal,” “Stockholder Proposal No. 5 — The Nasdaq Proposal,” “Stockholder Proposal No. 6 — The Incentive Plan Proposal,” “Stockholder Proposal No. 7 — The ESPP Proposal,” and “Stockholder Proposal No. 8 — The Adjournment Proposal.”

7GC will hold the Special Meeting to consider and vote upon these proposals. This proxy statement/prospectus contains important information about the Business Combination and the other matters to be acted upon at the Special Meeting. Stockholders of 7GC should read it carefully.

| Q: | Did the 7GC Board recommend the Business Combination Proposal and the other proposals? |

| A: | After careful consideration, the 7GC Board has determined that the Business Combination Proposal, the Charter Proposals, the Director Election Proposal, the Nasdaq Proposal, the Incentive Plan Proposal, the ESPP Proposal, and the Adjournment Proposal are in the best interests of 7GC and its stockholders and unanimously recommends that you vote or give instruction to vote “FOR” each of those proposals. |

The existence of financial and personal interests of one or more of 7GC’s directors may result in a conflict of interest on the part of such director(s) between what he, she or they may believe is in the best interests of 7GC and its stockholders and what he, she or they may believe is best for himself, herself, or themselves in determining to recommend that stockholders vote for the proposals. In addition, 7GC’s officers have interests in the Business Combination that may conflict with your interests as a stockholder. See the section titled “Stockholder Proposal No. 1 — The Business Combination Proposal — Interests of 7GC’s Directors and Executive Officers in the Business Combination” for a further discussion of these considerations.

| Q: | Are the proposals conditioned on one another? |

| A: | Each of the Condition Precedent Proposals is cross-conditioned on the approval of the others. If our stockholders do not approve each of the Condition Precedent Proposals, then unless certain conditions in the Merger Agreement are waived by the applicable parties to the Merger Agreement, the Merger Agreement may be terminated and the Business Combination may not be consummated. Proposal No. 3 and Proposal No. 8 are not conditioned upon the approval of any other proposal set forth in this proxy statement/prospectus. |

| Q: | Why is 7GC proposing the Business Combination? |

| A: | 7GC was incorporated to effect a merger, capital stock exchange, asset acquisition, stock purchase, reorganization, or similar business combination, with one or more businesses. |