Table of Contents

As filed with the Securities and Exchange Commission on November 18, 2020.

Registration Statement No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form F-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

IDEX Biometrics ASA

(Exact name of registrant as specified in its charter)

| Kingdom of Norway | 7373 | Not applicable | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

Dronning Eufemias gate 16

NO-0191 Oslo

Norway

Tel: +47 6783 9119

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

IDEX America Inc.

187 Ballardvale Street, Suite B211

Wilmington, MA 01887

Tel: + 1 (339) 215-8020

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies of all communications, including communications sent to agent for service, should be sent to:

| Joshua A. Kaufman Marc A. Recht David C. Boles Cooley LLP 55 Hudson Yards New York, New York 10001 +1 212 479 6000 |

Carl Garmann Clausen Advokatfirmaet Ræder AS Postboks 2944 Solli NO-0230 Oslo Norway +47 23 27 27 00 |

Approximate date of commencement of proposed sale to public: As soon as practicable after this Registration Statement becomes effective.

If any of the securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ☒

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act.

Emerging growth company ☒

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

CALCULATION OF REGISTRATION FEE

|

| ||||||||

| Title of Each Class of Securities to be Registered |

Amount to be Registered(1) |

Proposed Maximum Offering

Price |

Proposed Maximum Aggregate Offering Price |

Amount of Registration Fee | ||||

| Ordinary shares, nominal value NOK 0.15 per ordinary share(3)(4) |

60,000,000 | $0.20 | $12,000,000 | $1,310 | ||||

|

| ||||||||

|

| ||||||||

| (1) | The registrant is filing this registration statement with respect to an aggregate of 60,000,000 ordinary shares held by the shareholders identified herein. |

| (2) | Estimated solely for the purpose of computing the amount of the registration fee pursuant to Rule 457(c) under the Securities Act of 1933, as amended, based on the average of the high and low trading prices of the ordinary shares on Oslo Børs, a market operated by the Oslo Stock Exchange, on November 13, 2020 (NOK 1.79 , as expressed in U.S. dollars based on an exchange rate of NOK 9.1658 per U.S. dollar, as reported by Bloomberg L.P. on November 13, 2020). |

| (3) | These ordinary shares are represented by American Depositary Shares, or ADSs, each of which represents 75 ordinary shares of the registrant. |

| (4) | ADSs issuable upon deposit of the ordinary shares registered hereby are being registered pursuant to a separate registration statement on Form F-6 (File No. 333- ). |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended or until the registration statement shall become effective on such date as the Commission, acting pursuant to such Section 8(a), shall determine.

| † | The term “new or revised financial accounting standards” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012. |

Table of Contents

The information contained in this prospectus is not complete and may be changed. No securities may be sold pursuant to this prospectus until the registration statement filed with the Securities and Exchange Commission with respect to such securities has been declared effective. This prospectus is not an offer to sell these securities and no offers to buy these securities are being solicited in any jurisdiction where their offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED November 18, 2020

PROSPECTUS

60,000,000 Ordinary Shares

Represented by 800,000 American Depositary Shares

We have applied to list American Depositary Shares, or ADSs, each representing 75 ordinary shares of IDEX Biometrics ASA, on the Nasdaq Capital Market, or Nasdaq, under the symbol “IDBA”. The ADSs are expected to begin trading on Nasdaq on , 2020. Our ordinary shares are currently traded on Oslo Børs under the symbol “IDEX”. The closing price of our ordinary shares on Oslo Børs on , 2020 was NOK per ordinary share, which is equivalent to a price of $ per share based on the noon buying rate of the Federal Reserve Bank of New York on , 2020, or $ per ADS, after giving effect to the ratio of one ADS for every 75 ordinary shares. We have appointed The Bank of New York Mellon to act as the depositary for the ADSs representing our ordinary shares, including the Registered Shares, as defined below. Upon the effectiveness of the registration statement of which this prospectus forms a part, holders of ordinary shares registered hereby are expected to be able to deposit such ordinary shares with the depositary in exchange for ADSs representing such ordinary shares at the ratio referred to in the first sentence of this paragraph. ADSs representing the ordinary shares registered hereby will be freely tradeable on the effective date of the registration statement of which this prospectus forms a part.

We are filing the registration statement of which this prospectus forms a part with respect to an aggregate of 60,000,000 ordinary shares held by the shareholders identified herein. Holders of all such ordinary shares are identified in this prospectus as the Registered Holders and the aggregate of 60,000,000 ordinary shares registered hereby as the Registered Shares. Any Registered Shares offered and sold in the United States by the Registered Holders will be in the form of ADSs. The Registered Holders are also permitted to sell ordinary shares not represented by ADSs in private transactions, including on Oslo Børs, which resales are not covered by this prospectus. The Registered Holders are offering their securities in order to create a public trading market for our equity securities in the United States. Unlike an initial public offering, any sale by the Registered Holders of the Registered Shares represented by ADSs is not being underwritten by any investment bank. We expect that the opening public price of our ADSs on Nasdaq will be determined by reference to the most recent trading price of our ordinary shares on Oslo Børs, as adjusted for the currency exchange rate and an ADS-to-share ratio of 75 to 1. Thereafter, trades of our ADSs will be made through brokerage transactions on Nasdaq at prevailing market prices or as otherwise provided in the section entitled “Plan of Distribution.” The Registered Holders may, or may not, elect to dispose of Registered Shares represented by ADSs as and to the extent that they may individually determine. Such sales, if any, will be made through brokerage transactions on Nasdaq or other securities exchanges in the United States at prevailing market prices. See the section entitled “Plan of Distribution.” We will not receive proceeds from any sale of Registered Shares in the form of ADSs by Registered Holders.

We are an “emerging growth company” and a “foreign private issuer,” each as defined under the federal securities laws, and, as such, we will be subject to reduced public company reporting requirements. See the section entitled “Prospectus Summary—Implications of Being an Emerging Growth Company and a Foreign Private Issuer” for additional information.

Neither the U.S. Securities and Exchange Commission nor any other regulatory body has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

Investing in ADSs representing our ordinary shares involves a high degree of risk. Before buying any ADSs representing our ordinary shares you should carefully read the discussion of material risks of investing in such securities in “Risk Factors” beginning on page 8 of this prospectus.

Table of Contents

| ii | ||||

| ii | ||||

| 1 | ||||

| 4 | ||||

| 6 | ||||

| 8 | ||||

| 36 | ||||

| 37 | ||||

| 38 | ||||

| 39 | ||||

| 40 | ||||

| 41 | ||||

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

43 | |||

| 61 | ||||

| 79 | ||||

| 92 | ||||

| 94 | ||||

| 96 | ||||

| 97 | ||||

| 119 | ||||

| 128 | ||||

| 130 | ||||

| 138 | ||||

| 141 | ||||

| 142 | ||||

| 142 | ||||

| 142 | ||||

| 143 | ||||

| F-1 | ||||

| II-1 |

i

Table of Contents

We and the Registered Holders are responsible for the information contained in this prospectus and any free writing prospectus that we may prepare or authorize. Neither we nor the Registered Holders have authorized anyone to provide you with different or additional information, and neither we nor they take any responsibility for, or provide any assurance as to the reliability of, any other information that others may give you. Neither we nor the Registered Holders are making an offer to sell ADSs representing our ordinary shares in any jurisdiction where the offer or sale thereof is not permitted. You should not assume that the information contained in this prospectus is accurate as of any date other than the date on the front cover of this prospectus, regardless of the time of delivery of this prospectus or any sale of our ADSs.

For investors outside the United States: Neither we nor the Registered Holders have taken any action to permit the possession or distribution of this prospectus in any jurisdiction other than the United States where action for that purpose is required. Persons outside the United States who come into possession of this prospectus must inform themselves about and observe any restrictions relating to the ADSs and the distribution of this prospectus outside the United States.

We are a public limited company incorporated under the laws of Kingdom of Norway and a majority of our outstanding securities are owned by non-U.S. residents. Under the rules of the U.S. Securities and Exchange Commission, or the SEC, we are currently eligible for treatment as a “foreign private issuer.” As a foreign private issuer, we will not be required to file periodic reports and financial statements with the SEC as frequently or as promptly as domestic registrants whose securities are registered under the Securities Exchange Act of 1934, as amended, or the Exchange Act.

Unless otherwise indicated or the context otherwise requires, all references in this prospectus to the terms “IDEX,” “IDEX Biometrics,” “IDEX Biometrics ASA,” “the company,” “we,” “us” and “our” refer to IDEX Biometrics ASA together with its subsidiaries.

This prospectus includes trademarks, tradenames and service marks, certain of which belong to us, including IDEX, TrustedBio and the IDEX logo, and others that are the property of other organizations. Solely for convenience, trademarks, tradenames and service marks referred to in this prospectus appear without the ®, ™ and SM symbols, but the absence of those symbols is not intended to indicate, in any way, that we will not assert our rights or that the applicable owner will not assert its rights to these trademarks, tradenames and service marks to the fullest extent under applicable law. We do not intend our use or display of other parties’ trademarks, trade names or service marks to imply, and such use or display should not be construed to imply, a relationship with, or endorsement or sponsorship of us by, these other parties.

PRESENTATION OF FINANCIAL AND SHARE INFORMATION

We maintain our books and records in the local currency where we operate and report our consolidated financial statements in U.S. dollars in conformity with International Financial Reporting Standards, or IFRS, as issued by the International Accounting Standards Board, or IASB, and in conformity with IFRS as adopted by the European Union. None of the financial statements included in this prospectus were prepared in accordance with generally accepted accounting principles in the United States. All references in this prospectus to “$” are to U.S. dollars and all references to “NOK” are to Norwegian krone, the currency of our home country. We make no representation that any Norwegian krone or U.S. dollar amounts referred to in this prospectus could have been, or could be, converted into U.S. dollars or Norwegian krone, as the case may be, at any particular rate, or at all. These translations should not be considered representations that any such amounts have been, could have been or could be converted from Norwegian krone into U.S. dollars at that or any other exchange rate as of that or any other date.

ii

Table of Contents

We have made rounding adjustments to some of the figures included in this prospectus. Accordingly, numerical figures shown as totals in some tables may not be an arithmetic aggregation of the figures that preceded them.

All references to “shares” in this prospectus refer to ordinary shares of IDEX Biometrics ASA with a nominal value of NOK 0.15 per share.

iii

Table of Contents

This summary highlights information contained elsewhere in this prospectus and does not contain all of the information you should consider in making your investment decision. Before investing in our ADSs, you should read this entire prospectus carefully, including the sections of this prospectus entitled “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and our consolidated financial statements and the related notes, in each case contained elsewhere in this prospectus. You should carefully consider, among other things, the matters discussed in the section of this prospectus titled “Business” before making an investment decision.

Overview

We are a biometrics company specializing in the design, development and sale of fingerprint identification and authentication solutions. Our fingerprint sensors and biometric solutions are used in dual interface and contactless or touch-free smart cards, including payment cards, and a range of electronic devices.

We offer fingerprint sensors and biometric solutions to smart card manufacturers and other integrators of biometric fingerprint sensor technology in a broad range of markets, including payments, identification, access control, healthcare and the Internet of Things, or IoT. Based on an analysis by Zion Market Research in February 2020, the size of the global fingerprint sensor market is estimated to be $3.6 billion in 2020 and is projected to expand at a compound annual growth rate, or CAGR, of nearly 15% to $6.7 billion by 2025.

Our largest market opportunity is the biometric payment card market and more specifically our addressable market includes chip enabled cards which also include contactless payment cards. According to EMVCo, the industry standard organization, there are more than 8.2 billion chip-enabled consumer cards—credit and debit—now in use across the world. We believe the addition of a biometric sensor to the payment cards will significantly reduce the opportunity for fraud while making the transaction more convenient while using existing point of sale infrastructure. We believe the continue migration towards contactless payment cards will provide additional opportunities for our technologies. A report, Contactless Payment Market Global Forecast to 2025, published by Markets and Markets indicates that the global contactless credit/debit card payment market size is expected to grow from $10.3 billion in 2020 to $18.0 billion by 2025. This represents a CAGR of 11.7% during the forecast period. The major advantage offered by contactless payments is that customers can instantly complete transactions with the tap of a card. This increases the speed of transactions, making contactless payments even more efficient stated the Markets and Markets report.

In addition, following the COVID-19 outbreak, we believe consumers increasingly are motivated to go cashless. With many businesses discouraging the use of cash, in part due to hygiene questions linked to handling money, the prevalence of contactless payments has increased significantly in 2020. For example, a survey in March of 2020 in 19 countries around the world indicated a 25% increase in contactless payments (out of all credit card payments) compared to March 2019, and approximately 79% of consumers worldwide are now using tap and go payments. In an increasingly cashless and contactless society, there is a growing risk of card fraud. We, and other industry participants, believe that this could have a positive impact on the sale of biometric solutions going forward.

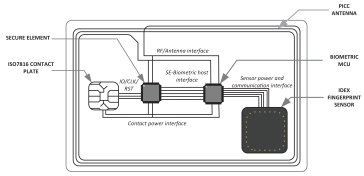

Our patent-protected fingerprint sensors can be integrated on the front side of a payment card, thereby enabling the card to use biometric fingerprint recognition instead of a personal identification number, or PIN, to authenticate the cardholder. To use this feature the cardholder first enrolls their fingerprint. A biometric template, which is representative of the fingerprint, is created and securely stored on the card. When the cardholder uses the card to make a payment, he or she places his or her finger on the card’s sensor. Through fingerprint sensing and biometric authentication, the card can determine if the person using the card is the enrolled user or not.

1

Table of Contents

Our portfolio of products includes fingerprint sensors, fingerprint modules with software and algorithms and remote enrollment devices. Our fingerprint sensors can be used in dual interface, contactless-only and contact-only payment cards. Our fingerprint modules offer a complete biometric solution that integrates fingerprint sensing with additional biometric processing and system power management functions. Additionally, with our remote enrollment solutions, cardholders can easily enroll their fingerprints at home and without the need to visit a bank branch.

Our sensors use a patented off-chip design, which separates the fingerprint sensor into two key components: the sensor array and the silicon chip (Application Specific Integrated Circuit, or ASIC). This off-chip design architecture allows the sensor array to be made from a flexible and cost-efficient polymer substrate while minimizing the silicon area needed for the ASIC. Compared to conventional silicon sensors, for which the sensor array is made of silicon, the off-chip design allows for a larger sensing area, better matching reliability and lower costs. We believe that we are the only provider supplying capacitive off-chip sensors and biometric algorithms optimized for integration with payment cards. This year, we launched TrustedBio, our next generation of dual interface products and solutions designed to reduce biometric smart card cost while improving both performance and security. TrustedBio utilizes advanced semiconductor technology to transform the sensor ASIC into a complete biometric system on chip, while maintaining all the benefits of the capacitive off-chip sensor architecture.

Our current generation products are commercially available, and we have begun to ship samples of our products on our TrustedBio platform. To date, product revenue has not been material; however, we have seen an increase in product revenues. For the year ended December 31, 2019, product revenues were $0.2 million and in the nine months ended September 30, 2020, product revenues were $0.4 million.

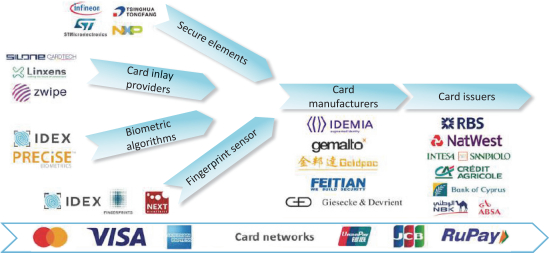

We market our products and solutions to smart card manufacturers and other integrators of biometric sensor technology, such as keyboards, dongles and other information and physical access control devices. We do not own or operate industrial manufacturing facilities, which could be potentially costly. Instead, we work closely with our customers on manufacturing and alongside other component suppliers within the card ecosystem. We have also established partnerships with secure element, or SE, producers, card inlay providers and card networks to help bring biometric smart cards to market. Our strategic rationale is to ensure that all the crucial components, within the biometric smart card ecosystem, are compatible and ready for mass production and to enhance our ability to offer comprehensive solutions to the market.

Over the past three years, we have built a research and development, or R&D, team with deep industry expertise, comprised of systems and technology engineers, software engineers, silicon engineers, sensor engineers and packaging technologists. We are an integrated systems company and we maintain in-house design, testing and supply chain management functions. Manufacturing is outsourced to large and established semiconductor fabrication companies as well as other providers of components and manufacturing services.

During 2019, we raised a total of $34.2 million in capital. In May 2020, we raised $10.2 million in a private placement. On November 9, 2020, our board of directors resolved an additional private placement with existing and new shareholders for gross proceeds of approximately $7.8 million. Subscribers in this private placement have each committed to acquire and pay for their respective subscription amount by November 20, 2020. For further financial information, see the section titled “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

While we are preparing to fully commercialize our products and services, we have begun to generate revenue through the sale of biometric sensors and system solutions that incorporate our technology. In 2019, we generated revenue of $0.4 million, $0.2 million of which related to product sales and $0.2 million of which related to engineering services. In the nine months ended September 30, 2020, we generated revenue of $0.5

2

Table of Contents

million, $0.4 million of which related to product sales and $0.1 million of which related to engineering services. We had net losses of $32.4 million and $19.5 million in 2019 and the nine months ended September 30, 2020, respectively.

Corporate Information

We were incorporated as a public limited company under the laws of Kingdom of Norway on July 24, 1996. Our principal executive offices are located at Dronning Eufemias gate 16, NO-0191 Oslo, Norway, which is also our registered office address, and our telephone number is +47 6783 9119. Our ordinary shares are traded on Oslo Børs under the symbol “IDEX”. Our website address is www.idexbiometrics.com. The information contained on, or that can be accessed from, our website does not form part of this prospectus.

Our agent for service of process in the United States is IDEX America Inc., with a registered address at 187 Ballardvale Street, Suite B211, Wilmington, MA 01887.

Risks Associated with Our Business

Our business is subject to a number of risks of which you should be aware before making an investment decision. You should carefully consider all of the information set forth in this prospectus and, in particular, should evaluate the specific factors set forth in the section titled “Risk Factors” before deciding whether to invest in our ADSs. Among these important risks are, but not limited to, the following:

| • | Our largest potential market, the biometric payment card market, is an undeveloped and emerging market and it is difficult to predict how large this market could be; |

| • | Our biometric technology has not yet gained, and may never gain, widespread market acceptance; |

| • | If the estimates and assumptions we have used to calculate the size of our target markets are inaccurate, our future growth rate may be limited. |

| • | We have a history of operating losses and may not achieve or sustain profitability in the future; |

| • | Based on our limited revenue to date and recurring losses from operations, we and our independent registered public accounting firm have expressed substantial doubt about our ability to continue as a going concern; |

| • | We will require additional funding to finance our operations, and if we are unable to raise capital when needed, we could be forced to delay, reduce or terminate certain of our development activities or other operations; |

| • | We expect fluctuations in our financial results, making it difficult to project future results, and if we fail to meet the expectations of securities analysts or investors with respect to our results of operations, our stock price could decline; |

| • | The markets in which we operate are highly competitive, and if we do not compete effectively, our business, financial condition, and results of operations could be harmed; |

| • | If we fail to innovate in response to changing customer needs and new technologies and other market requirements, our business, financial condition, and results of operations could be harmed; and |

| • | Even though we have not experienced significant delays in development activities to date, the COVID-19 pandemic could have an adverse impact on our business, operations, and the markets and communities in which we, our partners, and customers operate. |

3

Table of Contents

| Proposed Nasdaq Stock Market trading symbol for our ADSs |

We have applied to list ADSs representing our ordinary shares on the Nasdaq Capital Market under the symbol “IDBA” |

| Oslo Børs trading symbol for our ordinary shares |

“IDEX” |

| Registered Shares being registered on behalf of the Registered Holders |

60,000,000 ordinary shares, represented by an aggregate of 800,000 ADSs |

| Ordinary shares issued and outstanding immediately before and after the effectiveness of the registration statement of which this prospectus forms a part |

788,090,650 ordinary shares |

| ADSs issued and outstanding immediately after the effectiveness of the registration statement of which this prospectus forms a part |

800,000 ADSs (assuming deposit with the depositary of all the ordinary shares registered hereby) |

| American Depositary Shares |

Each ADS represents 75 ordinary shares, nominal value NOK 0.15 per ordinary share. Holders of ADSs have the rights of an ADS holder or beneficial owner of ADSs (as applicable) as provided in the deposit agreement among us, the depositary and holders and beneficial owners of ADSs issued thereunder from time to time. To better understand the terms of the ADSs representing our ordinary shares, see the section of this prospectus captioned “Description of American Depositary Shares.” We also encourage you to read the deposit agreement, the form of which is filed as an exhibit to the registration statement of which this prospectus forms a part. |

| Depositary |

The Bank of New York Mellon |

| Use of proceeds |

We will not receive proceeds from the sale, if any, of Registered Shares in the form of ADSs by the Registered Holders. |

| Risk factors |

See “Risk Factors” and the other information included in this prospectus for a discussion of factors you should carefully consider before deciding to invest in our ADSs. |

Unless otherwise stated in this prospectus, the number of our ordinary shares set forth herein is as of September 30, 2020 and is based on 788,090,650 ordinary shares issued and outstanding on such date but excludes:

| • | 54,837,143 ordinary shares issuable upon the exercise of outstanding share option awards (also known as “subscription rights” in Norway) as of September 30, 2020, at a weighted average exercise price of NOK 3.46 per share; |

4

Table of Contents

| • | 69,448,473 ordinary shares reserved for future issuance under our 2020 Subscription Rights Incentive Plan, as of September 30, 2020; and |

| • | 35,899,436 ordinary shares reserved for future issuance under our 2020 Employee Share Purchase Plan, as of September 30, 2020. |

Implications of Being an Emerging Growth Company and a Foreign Private Issuer

Emerging Growth Company

We are an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012, or the JOBS Act. As such, we may take advantage of certain exemptions from various reporting requirements that are applicable to other publicly traded entities that are not emerging growth companies. These exemptions include:

| • | the option to present only two years of audited financial statements and related discussion in the section titled “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in this prospectus; |

| • | not being required to comply with the auditor attestation requirements of Section 404(b) of the Sarbanes-Oxley Act of 2002; and |

| • | to the extent that we no longer qualify as a foreign private issuer, (1) reduced disclosure obligations regarding executive compensation in our periodic reports and proxy statements and (2) exemptions from the requirements of holding a non-binding advisory vote on executive compensation, including golden parachute compensation. |

We will remain an emerging growth company until the earliest of: (1) the last day of the first fiscal year in which our annual gross revenues exceed $1.07 billion; (2) the last day of 2025; (3) the date that we become a “large accelerated filer” as defined in Rule 12b-2 under the Exchange Act, which would occur on the last day of any fiscal year that the aggregate worldwide market value of our common equity held by non-affiliates exceeds $700 million as of the last business day of our most recently completed second fiscal quarter; or (4) the date on which we have issued more than $1.0 billion in non-convertible debt securities during any three-year period.

Foreign Private Issuer

Upon the effectiveness of the registration statement of which this prospectus forms a part, we will report under the Exchange Act as a non-U.S. company with foreign private issuer status. Even after we no longer qualify as an emerging growth company, as long as we qualify as a foreign private issuer under the Exchange Act, we will be exempt from certain provisions of the Exchange Act that are applicable to U.S. domestic public companies, including:

| • | the sections of the Exchange Act regulating the solicitation of proxies, consents or authorizations in respect of a security registered under the Exchange Act; |

| • | the sections of the Exchange Act requiring insiders to file public reports of their stock ownership and trading activities and liability for insiders who profit from trades made in a short period of time; and |

| • | the rules under the Exchange Act requiring the filing with the SEC of quarterly reports on Form 10-Q containing unaudited financial and other specific information, and current reports on Form 8-K upon the occurrence of specified significant events. |

Foreign private issuers are also exempt from certain more stringent executive compensation disclosure rules. Thus, even if we no longer qualify as an emerging growth company, but remain a foreign private issuer, we will continue to be exempt from the more stringent compensation disclosures required of companies that are neither an emerging growth company nor a foreign private issuer.

5

Table of Contents

SUMMARY CONSOLIDATED FINANCIAL DATA

The following tables present summary consolidated financial data as of the dates and for the periods indicated. We have derived the summary consolidated statements of profit and loss data for the years ended December 31, 2018 and 2019 and the statements of financial position as of December 31, 2018 and 2019 from our audited consolidated financial statements included elsewhere in this prospectus. We have derived the summary consolidated statements of profit or loss data for the nine months ended September 30, 2019 and 2020 and the summary consolidated statements of financial position data as of September 30, 2020 from the unaudited interim condensed consolidated financial statements included elsewhere in this prospectus. We have prepared the unaudited interim condensed consolidated financial statements on the same basis as the audited consolidated financial statements, and the unaudited financial data include all adjustments, consisting only of normal recurring adjustments, that we consider necessary for a fair presentation of our consolidated financial position and results of operations as of and for the periods presented.

Our consolidated financial statements are prepared and presented in accordance with IFRS as issued by the IASB, and in conformity with IFRS as adopted by the European Union, and audited in accordance with the standards of the PCAOB (United States). IFRS differ in certain significant respects from U.S. GAAP. Our historical results are not necessarily indicative of results expected for future periods and our operating results for the nine months ended September 30, 2020 are not necessarily indicative of the results that may be expected for the entire year ending December 31, 2020. You should read this data together with our consolidated financial statements and related notes appearing elsewhere in this prospectus and the information under the sections titled “Selected Consolidated Financial Data” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

Summary Consolidated Statements of Profit and Loss Data:

| Year Ended December 31, |

Nine Months Ended September 30, |

|||||||||||||||

| (In thousands, except per share data) | 2018 | 2019 | 2019 | 2020 | ||||||||||||

| Revenue: |

||||||||||||||||

| Product |

$ | 268 | $ | 159 | $ | 106 | $ | 420 | ||||||||

| Service |

172 | 265 | 247 | 77 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total revenue |

440 | 424 | 353 | 497 | ||||||||||||

| Operating expenses: |

||||||||||||||||

| Purchases, net of inventory variation |

185 | 62 | 47 | 97 | ||||||||||||

| Payroll expenses |

19,770 | 21,750 | 15,074 | 12,466 | ||||||||||||

| Research and development expenses |

5,631 | 4,385 | 3,025 | 2,039 | ||||||||||||

| Other operating expenses |

3,919 | 4,641 | 3,395 | 3,779 | ||||||||||||

| Amortization and depreciation |

842 | 1,633 | 1,201 | 1,280 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total operating expenses |

30,347 | 32,471 | 22,742 | 19,661 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Loss from operations |

(29,907 | ) | (32,047 | ) | (22,389 | ) | (19,164 | ) | ||||||||

| Finance income |

134 | 135 | 114 | 21 | ||||||||||||

| Finance cost |

(411 | ) | (351 | ) | (296 | ) | (508 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Loss before tax |

(30,184 | ) | (32,263 | ) | (22,571 | ) | (19,651 | ) | ||||||||

| Income tax benefit (expense) |

(41 | ) | (160 | ) | (378 | ) | 144 | |||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net loss for the year |

$ | (30,225 | ) | $ | (32,423 | ) | $ | (22,949 | ) | $ | (19,507 | ) | ||||

|

|

|

|

|

|

|

|

|

|||||||||

| Loss per share, basic and diluted(1) |

$ | (0.06 | ) | $ | (0.05 | ) | $ | (0.04 | ) | $ | (0.03 | ) | ||||

|

|

|

|

|

|

|

|

|

|||||||||

6

Table of Contents

| (1) | See Note 9 to our audited consolidated financial statements and unaudited interim condensed consolidated financial statements included elsewhere in this prospectus for further details regarding the calculation of basic and diluted loss per share. |

Selected Data from Our Consolidated Statements of Financial Position:

| (In thousands) | December 31, 2018 |

December 31, 2019 |

September 30, 2020 |

|||||||||

| Cash and cash equivalents |

$ | 9,635 | $ | 14,126 | $ | 5,704 | ||||||

|

|

|

|

|

|

|

|||||||

| Total assets |

17,990 | 23,470 | 13,847 | |||||||||

| Total liabilities |

3,807 | 5,658 | 3,765 | |||||||||

| Total equity and liabilities |

17,990 | 23,470 | 13,847 | |||||||||

7

Table of Contents

Our operations and financial results are subject to various risks and uncertainties including those described below. You should consider carefully the risks and uncertainties described below, in addition to other information contained in this Registration Statement on Form F-1, including our consolidated financial statements and related notes. The risks and uncertainties described below are not the only ones we face. Additional risks and uncertainties that we are unaware of, or that we currently believe are not material, may also become important factors that adversely affect our business. If any of the following risks or others not specified below materialize, our business, financial condition and results of operations could be materially and adversely affected.

Risks Related to Our Financial Condition, Business and Industry

Since our inception, we have only generated limited revenue and we have incurred significant operating losses and negative cash flows.

We have only generated limited revenue and have incurred significant operating losses and negative cash flows since our inception. We generated net losses of $30.2 million, $32.4 million and $19.5 million for the years ended December 31, 2018 and 2019 and the nine months ended September 30, 2020, respectively. As of September 30, 2020, we had an accumulated deficit of $217.7 million. We are not certain whether or when we will obtain a high enough volume of sales in the future to generate significant revenue, grow our business or achieve or maintain profitability. We also expect our costs and expenses to increase in future periods, which could negatively affect our future results of operations even if we are able to significantly increase our revenue. In particular, we intend to continue to expend significant funds to develop future generations of our products and software solutions, including by introducing new products and functionality, and to expand use cases and integrations. We will also face increased compliance costs associated with growth, the expansion of our customer base, and as a result of the fact that we are publicly listed in both Norway and the United States. Our efforts to grow our business may be costlier than we expect, or the rate of our growth in revenue may be slower than we expect, and we may not be able to increase our revenue enough to offset our operating expenses. We may incur significant losses in the future for a number of reasons, including the other risks described herein, and unforeseen expenses, difficulties, complications or delays, and other unknown events. If we are unable to generate significant revenue and/or achieve and sustain profitability, the value of our business and ordinary shares may significantly decrease.

Based on our limited revenue to date and recurring losses from operations, we and our independent registered public accounting firm have expressed substantial doubt about our ability to continue as a going concern.

Among other factors, our history of losses, limited revenue and negative cash flows from operations raise substantial doubt about our ability to continue as a going concern. As a result, our independent registered public accounting firm has included an explanatory paragraph in their opinion for the year ended December 31, 2019 as to the substantial doubt about our ability to continue as a going concern. Our financial statements have been prepared in accordance with the IFRS, as issued by the IASB, which contemplate that we will continue to operate as a going concern. Historically, we have been able to raise funds through private placements of shares, including a private placement of shares that raised $10.2 million before expenses in May 2020. On November 9, 2020, our board of directors resolved an additional private placement with existing and new shareholders for gross proceeds of approximately $7.8 million. Subscribers in this private placement have each committed to acquire and pay for their respective subscription amount by November 20, 2020. We continue to review all strategic options to fund ongoing operations, research and development projects and working capital needs, including a best efforts capital raise. While we have been successful in raising funds through private placements of shares, there can be no assurance that we will be successful this time.

We will require additional funding to finance our operations. If we are unable to raise capital when needed, we could be forced to delay, reduce or terminate certain of our development activities or other operations.

We cannot be certain when, or if, our operations will generate sufficient cash to fully fund our ongoing operations or the growth of our business. We intend to continue to make investments to support our business,

8

Table of Contents

which may require us to engage in equity or debt financings to secure additional funds. We continue to review all strategic options to fund ongoing operations, research and development projects and working capital needs, including a best efforts capital raise. While we have been able to raise funds in the past through private placements of our shares, additional financing may not be available on terms favorable to us, if at all. If adequate funds are not available on acceptable terms, we may be unable to invest in future growth opportunities, which could harm our business, operating results, and financial condition. If we incur debt, the debt holders would have rights senior to holders of ordinary shares to make claims on our assets, and the terms of any debt could restrict our operations, including our ability to pay dividends on our ordinary shares. Furthermore, if we issue additional equity securities, shareholders will experience dilution. Because our decision to issue securities in the future will depend on numerous considerations, including factors beyond our control, we cannot predict or estimate the amount, timing, or nature of any future issuances of debt or equity securities, and if we are unable to raise sufficient funds we may be unable to maintain our operations. As a result, our shareholders bear the risk of future issuances of debt or equity securities reducing the value of our ordinary shares and diluting their interests.

Our largest potential market is the biometric payment card market. The market for biometric payment cards is an undeveloped and emerging market and it is difficult to predict how large this market could be. In addition, our biometric technology has not yet gained, and may never gain, widespread market acceptance.

We primarily market and sell biometric products and software solutions to the payment card and access control markets. The market for biometric payment cards is an undeveloped and emerging market and it is difficult to predict how large this market could be. Our technology represents a novel security solution and we have not yet generated significant sales. Although recent security concerns relating to identification of individuals and appearance of biometric readers on popular consumer products, including the smart phones, have increased interest in biometrics generally, it remains an undeveloped and emerging market. Biometric based solutions compete with more traditional security methods including keys, cards, personal identification numbers and security personnel. In addition, our biometric technology has not yet gained, and may never gain, widespread market acceptance. Acceptance of biometrics and our technology as an alternative to such traditional methods depends upon a number of factors including:

| • | national or international events, such as the ongoing COVID-19 pandemic, which may affect the need for or interest in biometric solutions; |

| • | the performance and reliability of biometric solutions; |

| • | marketing efforts and publicity regarding these solutions; |

| • | public perception regarding privacy concerns; |

| • | costs involved in adopting and integrating biometric solutions; |

| • | proposed or enacted legislation related to privacy of information; and |

| • | competition from non-biometric technologies that provide more affordable, but less robust, authentication. |

For these reasons, we are uncertain whether our biometric technology will gain widespread acceptance in any commercial markets or that demand will be sufficient to create a market large enough to produce significant revenue or earnings. Our future success depends, in part, upon business customers adopting biometrics generally, and our solutions specifically.

If the estimates and assumptions we have used to calculate the size of our target markets are inaccurate, our future growth rate may be limited.

Our projections, assumptions and estimates of future opportunities within our target markets are necessarily subject to a high degree of uncertainty and risk due to a variety of factors, including those described in this

9

Table of Contents

prospectus. If third-party or internally generated data prove to be inaccurate or we make errors in our assumptions based on that data, our future growth rate may be limited. In addition, these inaccuracies or errors may cause us to misallocate capital and other business resources, which could harm our business. Even if our target markets meet our size estimates and experiences the forecasted growth, we may not grow our business at similar rates, or at all. Our growth is subject to many factors, including our success in implementing our business strategy, which is subject to many risks and uncertainties. Accordingly, the expectations of market growth included in this prospectus should not be taken as indicative of our future growth.

We are subject to lengthy development periods and product acceptance cycles, which can result in development and engineering costs without any future revenue.

We provide fingerprint sensors and related software solutions that are incorporated by card manufacturers into the products they sell. They make the determination during their product development programs whether to incorporate our solutions or pursue other alternatives. This process requires us to make significant investments of time and resources in the design of fingerprint sensors and related software solutions for our products well before our customers introduce their products incorporating our solutions into the market, and before we can be sure that we will generate any significant sales to our customers or even recover our investment. During a customer’s entire product development process, we face the risk that our solutions will fail to meet our customer’s technical, performance, or cost requirements, or that our products will be replaced by competitive products or alternative technological solutions. Even if we complete our design process in a manner satisfactory to our customer, the customer may delay or terminate its product development efforts. The occurrence of any of these events could cause sales to not materialize, be deferred, or be cancelled, which could adversely affect our operating results.

A significant portion of our sales comes from one or more large customers, the loss of which could harm our business, financial condition, and operating results.

We have historically generated limited revenue, and most of our revenue we have generated has come from a limited number of customers. During 2018, three customers, Mastercard, IDEMIA France SAS and Yoyon Electronics Technology Co Ltd., accounted for approximately 39%, 36% and 13% of the Company’s revenue, respectively. During 2019, two customers, Bloomberg L.P. and IDEMIA France SAS, accounted for approximately 69% and 10% of the Company’s revenue, respectively. During the first nine months of 2020, Bloomberg L.P. accounted for approximately 84% of the Company’s revenue. While we work to maintain our relationships with our current customers and seek out new business, we may continue to face challenges in diversifying our customer base. The loss of major customers, or a decrease in demand for our products by these customers within a short period of time, could adversely affect our current and future revenue, financial condition and business. The adverse effect could be more substantial if our other customers do not increase their orders or if we are unsuccessful in generating orders for our solutions with new customers. Many of these card manufacturers sell to the same card issuers, and therefore we may be reliant on certain card manufacturers. Concentration in our customer base and partner relationship, now and in the future, may make fluctuations in revenue and earnings more severe and make business planning more difficult.

If we are unable to attract new customers and to retain our existing customers, our growth prospects will be adversely affected.

Our ability to grow our business depends on retaining and expanding our customer base. We must convince prospective customers of the benefits of our services and our existing customers of the continuing value of our services. Our ability to attract new customers and retain existing customers depends in large part on our ability to continue to offer competitive technologies and products. As consumer preferences and technological changes shift market dynamics, we will need to enhance and improve our existing products, introduce new products, and maintain our competitive position with additional technological advances. If we fail to keep pace with technological advances or fail to offer compelling product offerings to meet consumer demands, our ability to grow or sustain the reach of our services, attract and retain customers may be adversely affected.

10

Table of Contents

Our products and software solutions may contain defects, which will make it more difficult for us to establish and maintain customers.

Although we have completed the development of multiple generations of our core biometric technology, it has only been used by a limited number of business customers. Despite extensive testing during development and certifications by third-party testing facilities, our products and software solutions may contain undetected design faults and errors that are discovered only after it has been installed and used by a greater number of customers. Any such defect or error in new or existing products or software solutions could cause delays in delivering our technology or require design modifications. These could adversely affect our competitive position and cause us to lose potential customers or opportunities. Errors or defects in our software or products could lead to mismatches in fingerprint scans. Since our technologies are intended to be utilized to secure payments and physical and electronic information access, the effect of any such bugs or delays will likely have a detrimental impact on us. In addition, given that biometric technology generally, and our biometric technology specifically, to certain extent, has yet to gain widespread market acceptance, any delays would likely have a more detrimental impact on our business than if we were a more established company.

Potential strategic alliances may not achieve their objectives, and the failure to do so could impede our growth.

We have entered, and we anticipate that we will continue to enter, into strategic alliances. We continually explore strategic alliances designed to enhance or complement our technology or to work in conjunction with our technology; to provide necessary know-how, components, or supplies, and to develop, introduce, and distribute products utilizing our technology. Certain strategic alliances may not achieve their intended objectives, and parties to our strategic alliances may not perform as contemplated. The failure of these alliances to achieve their objectives may impede our ability to introduce new products and enter new markets.

We face intense competition.

We compete with both established companies and startup enterprises that provide biometric solutions, as well as providers of more traditional security methods. Our competitors include, among others, Fingerprint Cards AB, NEXT Biometrics ASA and ELAN Microelectronics Corp. Some of our competitors have substantially greater financial and marketing resources than we do, and may independently develop superior technologies, which may result in our technology becoming less competitive or obsolete. If we are unable to develop new applications or enhance our existing technology in a timely manner in response to technological changes, we will be unable to compete in our chosen markets. Our actual and potential competitors may also have greater name recognition and more extensive customer bases. In addition, if one or more other biometric technologies such as voice, face, iris, hand geometry or blood vessel recognition are widely adopted, it would significantly reduce the potential market for our fingerprint identification technology in certain industries.

Our ability to compete successfully depends on a number of factors, which may be outside our control. These factors include the following:

| • | our success in designing and introducing new fingerprint sensors and related software solutions, including those implementing new technologies; |

| • | our ability to predict the evolving needs of our customers and to assist them in incorporating our technologies into their new and existing products; |

| • | our ability to meet our customers’ requirements for ease of use, reliability and durability; |

| • | our ability to meet our customers’ price and performance requirements; |

| • | the quality of our customer service and support; |

| • | the rate at which customers incorporate our fingerprint sensors and related software solutions into their own products; |

11

Table of Contents

| • | product or technology introductions by our competitors; and |

| • | currency fluctuations, which may cause a competitor’s products to be priced significantly lower than our products. |

Moreover, additional competitors may enter the biometrics market and become significant long-term competitors. In the future, we may encounter competition from other larger, well-established and well-financed entities that may continue to acquire, invest in or form joint ventures with providers of fingerprint recognition technology, and existing providers may elect to consolidate. Our position in the existing markets could be eroded rapidly by product or technology enhancements or the development of new, superior products and technology by competitors. Increased competition could result in price reductions, fewer customer orders, reduced gross margins and lower market prices of our ordinary shares.

The effects of national and global epidemics, including the recent COVID-19 pandemic, could have an adverse impact on our business, operations, and the markets and communities in which we operate.

In March 2020, the World Health Organization declared the outbreak of COVID-19 a pandemic. Our business and operations could be adversely affected by national and global epidemics, including the recent COVID-19 pandemic, impacting the markets and communities in which we operate.

In response to the COVID-19 pandemic, many state, local, and national governments have put in place, and others in the future may put in place, quarantines, executive orders, shelter-in-place orders, and similar government orders and restrictions in order to control the spread of the disease. Although there have not been significant delays in our development activities to date, such orders or restrictions, or the perception that such orders or restrictions could occur, have resulted in business closures, work stoppages, slowdowns and delays, work-from-home policies, and travel restrictions, among other effects that could negatively impact productivity and disrupt our operations. We have implemented a work-from-home policy for employees, and we may take further actions that alter our operations as may be required by federal, state, or local authorities or which we determine are in the best interests of our employees and shareholders.

In addition, while the potential impact and duration of the COVID-19 pandemic on the global economy and our business in particular may be difficult to assess or predict, the pandemic has resulted in, and may continue to result in, significant disruption of global financial markets, potentially reducing our ability to access capital, which could in the future negatively affect our liquidity. The COVID-19 pandemic also could reduce the demand for our customers’ products and services, which could negatively impact our customers’ willingness to renew or enter into contracts with us or our ability to collect accounts receivable on a timely basis, which, if significant, could materially and adversely affect our business, results of operations, and financial condition. For example, many of our business partners in Asia were impacted by the COVID-19 pandemic in the first quarter of 2020, although we believe a majority of such business partners, if not all, have now returned to their offices and factories.

The global pandemic of COVID-19 continues to rapidly evolve, and we will continue to monitor the COVID-19 situation closely. While the pandemic may increase end-user awareness of the benefits of contactless payment solutions such as the ones we offer, and therefore may increase the demand for our products, the ultimate impact of the COVID-19 pandemic or a similar health epidemic is highly uncertain and subject to change. We do not yet know the full extent of potential delays or impacts on our business, operations, or the global economy as a whole, which makes our future results difficult to predict.

Unfavorable conditions in the global economy or the vertical markets we serve could limit our ability to grow our business and negatively affect our operating results.

General worldwide economic conditions have experienced significant instability due to the global economic uncertainty and financial market conditions caused by the COVID-19 pandemic. These conditions make it

12

Table of Contents

extremely difficult for customers and us to accurately forecast and plan future business activities and could cause customers to reduce or delay their spending. At this time, the potential impact on customer spend from the COVID-19 pandemic is difficult to predict and, therefore, it is not possible to fully determine the impact on our future results. Historically, economic downturns have resulted in overall reductions in spending. If macroeconomic conditions deteriorate or are characterized by uncertainty or volatility, customers may curtail or freeze spending in general and for biometric products such as ours specifically, which could have an adverse impact on our business, financial condition, and operating results.

We target generating revenue from customers in the payment cards and access control verticals. While these verticals have not been affected as severely by weak economic conditions caused by COVID-19 as the retail, hospitality, and entertainment industries, we cannot assure these verticals will not suffer more severe losses in the future as they are in turn impacted by consumer demand and the performance of the retail, hospitality and entertainment industries. Furthermore, we cannot predict the timing, strength, or duration of any economic slowdown or recovery. In addition, even if the overall economy is robust, we cannot assure the market for services such as ours will experience growth or that we will experience growth. Additionally, the increased use of digital payments and virtual credit cards by consumers could pose an obstacle to the growth of our business.

War, terrorism, other acts of violence or natural or manmade disasters such as a global pandemic may affect the markets in which we operate, our customers, our delivery of products and customer service, and could have a material adverse impact on our business, results of operations, or financial condition.

Our business may be adversely affected by instability, disruption or destruction in a geographic region in which we operate, regardless of cause, including war, terrorism, riot, civil insurrection or social unrest, and natural or manmade disasters, including famine, food, fire, earthquake, storm or pandemic events, including COVID-19.

Such events may cause customers to suspend or delay their decisions on using our products and services, make it difficult or impossible to access some of our inventory, and give rise to sudden significant changes in regional and global economic conditions and cycles that could interfere with purchases of goods or services. These events also pose significant risks to our personnel and to physical facilities, which could materially adversely affect our financial results.

We rely on the performance of highly skilled personnel, including senior management and our engineering, professional services, sales and technology professionals; if we are unable to retain or motivate key personnel or hire, retain and motivate qualified personnel, our business would be harmed.

We believe our success has depended, and continues to depend, on the efforts and talents of our senior management team and our highly skilled team members, including our sales personnel, engineering and support personnel. From time to time, there may be changes in our senior management team resulting from the termination or departure of our executive officers and key employees. Our senior management and key employees are employed on an at-will basis, which means that they could terminate their employment with us at any time. Many of our executive officers and key employees receive equity compensation as a portion of their overall compensation package. A substantial decrease in the market price of our ordinary shares would effectively reduce the compensation of such persons and could increase the risk that they depart from our company. The loss of any of our senior management or key employees could adversely affect our ability to build on the efforts they have undertaken and to execute our business plan, and we may not be able to find adequate replacements. We cannot ensure that we will be able to retain the services of any members of our senior management or other key employees.

Our ability to successfully pursue our growth strategy also depends on our ability to attract, motivate and retain our personnel. Competition for well-qualified employees in all aspects of our business, including sales personnel, professional services personnel, and engineering and support personnel, is intense. Our continued

13

Table of Contents

ability to compete effectively depends on our ability to attract new employees and to retain and motivate existing employees. If we do not succeed in attracting well-qualified employees or retaining and motivating existing employees, our business would be adversely affected.

Because many rapidly growing markets for our products are international, our business is susceptible to risks associated with international operations.

Biometric products including ours are often marketed and sold globally. We currently have offices in Norway, the United States, the UK and China, which focus on selling and implementing our fingerprint sensors and related software solutions in those regions. In the future, we may expand within these countries or to other international locations. This reliance on international sales and marketing subjects us to the risks of conducting business internationally, including risks associated with political and economic instability, global health conditions, currency controls, exchange rate fluctuations and changes in import/export regulations, and tariff and freight rates. For example, the political or economic instability in a given region may have an adverse impact on the financial position of end users in the region, which could affect future orders and harm our results of operations. Our international sales operations involve a number of other risks including, but not limited to:

| • | longer sales and payment cycles; |

| • | changes to countries’ banking and credit requirements; |

| • | unexpected changes in government regulatory requirements; |

| • | sales, value added tax, or other indirect tax regulations and treaties and potential changes in regulations and treaties in the Kingdom of Norway, the United States, the United Kingdom, China and in and between countries in which we market or sell our products; |

| • | different, complex and changing laws governing intellectual property rights, which in certain countries sometimes afford reduced protection of intellectual property rights; |

| • | any changes in international trade policies, including potential adoption and expansion of trade restrictions, higher tariffs, or cross border taxation that might impact overall customer demand for our products or affect our ability to manufacture and/or sell our products overseas; |

| • | changes to economic, social, or political conditions in countries where we have significant operations; |

| • | operating in countries with a higher incidence of corruption and fraudulent business practices; |

| • | challenges in providing solutions across a significant distance in different languages and among different cultures; |

| • | the burdens of complying with a variety of various country laws in which we operate; |

| • | difficulties in staffing and managing international operations; and |

| • | rapid changes in government, economic and political policies and conditions, political or civil unrest or instability, terrorism or pandemics (including but not limited to the COVID-19 pandemic) and other similar outbreaks or events. |

We cannot guarantee that any potential future expansion efforts that we may undertake will be successful. If we invest substantial time and resources to expand our international operations and are unable to do so successfully and in a timely manner, our business and operating results will suffer.

Legal, political and economic uncertainty surrounding the exit of the UK from the EU, may be a source of instability in international markets, create significant currency fluctuations, adversely affect our operations in the UK and pose additional risks to our business, revenue, financial condition, and results of operations.

On June 23, 2016, the UK voted to leave the EU in an advisory referendum, which is generally referred to as Brexit. In January 2020, the UK and EU entered into a withdrawal agreement pursuant to which the UK formally

14

Table of Contents

withdrew from the EU on January 31, 2020. Following such withdrawal, the UK entered into a transition period scheduled to end on December 31, 2020, or the Transition Period. During the Transition Period, the UK will remain subject to EU law and maintain access to the EU single market and to the global trade deals negotiated by the EU on behalf of its members. During the Transition Period, negotiations are expected to continue in relation to the future customs and trading relationship between the UK and the EU following the expiry of the Transition Period. Due to the COVID-19 pandemic, negotiations between the UK and the EU that have been scheduled since March have either been postponed or occurring in a reduced forum via video conference. There is, therefore, an increased likelihood that the Transition Period may need to be extended beyond December 31, 2020 (although it remains the position of the UK government that it will not be extended).

The uncertainty concerning the UK’s legal, political and economic relationship with the EU after the Transition Period may be a source of instability in the international markets, create significant currency fluctuations, and/or otherwise adversely affect trading agreements or similar cross-border co-operation arrangements (whether economic, tax, fiscal, legal, regulatory or otherwise).

These developments, or the perception that any of them could occur, have had, and may continue to have, a significant adverse effect on global economic conditions and the stability of global financial markets, and could significantly reduce global market liquidity and limit the ability of key market participants to operate in certain financial markets. Asset valuations, currency exchange rates and credit ratings may also be subject to increased market volatility.

If the UK and the EU are unable to negotiate acceptable trading and customs terms or if other EU member states pursue withdrawal, barrier-free access between the UK and other EU member states or among the European Economic Area, or EEA, overall could be diminished or eliminated. The long-term effects of Brexit will depend on any agreements (or lack thereof) between the UK and the EU and, in particular, any arrangements for the UK to retain access to EU markets after the Transition Period.

Such a withdrawal from the EU is unprecedented, and it is unclear how the UK’s access to the European single market for goods, capital, services and labor within the EU, or single market, and the wider commercial, legal and regulatory environment, will impact our UK operations following the expiry of the Transition Period. Our UK operations could be disrupted by Brexit.

We may also face new regulatory costs and challenges as a result of Brexit that could have an adverse effect on our operations. For example, the European Parliament and the Council of the EU adopted a comprehensive general data protection regulation, or GDPR, in 2016 to replace the current European Union Data Protection Directive and related country-specific legislation. Although the UK enacted the Data Protection Act 2018, which is consistent with the GDPR, uncertainty remains regarding how data transfers to and from the UK will be regulated following the Transition Period.

There may continue to be legal, political and economic uncertainty surrounding the consequences of Brexit, which could adversely impact customer confidence resulting in customers reducing their spending budgets on our products and software solutions, which, in turn, could adversely affect our business, revenue, financial condition and results of operations.

If currency exchange rates fluctuate substantially in the future, our financial results, which are reported in U.S. Dollars, could be adversely affected.

We incur expenses for employee compensation, property leases, and other operating expenses in the local currencies of the jurisdictions in which we operate. Fluctuations in the exchange rates between the U.S. Dollar and other currencies may impact expenses as well as revenue, and consequently have an impact on margin and the reported operating results. This could have a negative impact on our reported operating results. To date, we have not engaged in any hedging strategies, and any such strategies, such as forward contracts, options and

15

Table of Contents

foreign exchange swaps related to transaction exposures that we may implement to mitigate this risk may not eliminate our exposure to foreign exchange fluctuations.

We may pursue strategic acquisitions, including acquiring other biometric companies, as part of our growth strategy and that may disrupt our business.

We may pursue strategic acquisitions in the future. Risks in acquisition transactions include difficulties in the integration of acquired businesses into our operations and control environment, difficulties in assimilating and retaining employees and intermediaries, difficulties in retaining the existing customers of the acquired entities, assumed or unforeseen liabilities that arise in connection with the acquired businesses, the failure of counterparties to satisfy any obligations to indemnify us against liabilities arising from the acquired businesses, and unfavorable market conditions that could negatively impact our growth expectations for the acquired businesses. Fully integrating an acquired company or business into our operations may take a significant amount of time. We cannot assure you that we will be successful in overcoming these risks or any other problems encountered with acquisitions and other strategic transactions. These risks may prevent us from realizing the expected benefits from acquisitions and could result in the failure to realize the full economic value of a strategic transaction or the impairment of goodwill and/or intangible assets recognized at the time of an acquisition. These risks could be heightened if we complete a large acquisition or multiple acquisitions within a short period of time. Additional risks may include:

| • | difficulties in integrating operations, technologies, services and personnel; |

| • | the diversion of financial and management resources from existing operations; |

| • | the risk of entering new markets; |

| • | the potential loss of existing customers following an acquisition; |

| • | the potential loss of key employees and the associated risk of competitive efforts from such departed personnel; and |

| • | the inability to generate sufficient revenue to offset acquisition or investment costs. |

As a result, if we fail to properly evaluate and execute any acquisitions or investments, our business and prospects may be seriously harmed.

Risks Related to Government Regulation, Data Collection, Intellectual Property and Litigation

Our business is subject to a variety of laws around the world. Any changes in government regulations relating to our business or other unfavorable developments may adversely affect our business, operating results, and financial condition.

We are an international company that is registered under the laws of the Kingdom of Norway, with offices and/or operations in the United States, the UK and China. As a result of this organizational structure and the scope of our operations, we are subject to a variety of laws in different countries. The scope and interpretation of the laws that are or may be applicable to us are often uncertain and may be conflicting. It is also likely that if our business grows and evolves and our solutions are used more globally, we will become subject to laws and regulations in additional jurisdictions. It is difficult to predict how existing laws will be applied to our business and the new laws to which we may become subject.

We are subject to various business regulations and laws. Such laws and regulations include, but are not limited to, labor, advertising and marketing, real estate, taxation, user privacy, data collection and protection, intellectual property, anti-corruption, anti-money laundering, sanctions, foreign exchange controls, antitrust and competition, electronic contracts, telecommunications, sales procedures, credit card processing procedures and consumer protections. We cannot guarantee that we have been or will be fully compliant in every jurisdiction in

16

Table of Contents

which we are subject to regulation, as existing laws and regulations governing issues such as intellectual property, privacy, taxation, and consumer protection, among others, are constantly changing. The adoption or modification of laws or regulations relating to our product development or other areas of our business could limit or otherwise adversely affect the manner in which we currently conduct our business. Further, compliance with laws, regulations, and other requirements imposed upon our business may be onerous and expensive, and they may be inconsistent from jurisdiction to jurisdiction, further increasing the cost of compliance and doing business.