UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

___________________________

FORM 10-Q

___________________________

(Mark One)

QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the quarterly period ended March 31, 2022

or

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from to

Commission File Number: 001-39653

___________________________

(Exact name of registrant as specified in its charter)

___________________________

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||||||||

| (address of principal executive offices) | |||||||||||

(212 ) 419-3000

(Registrant’s telephone number, including area code)

___________________________

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading symbol(s) | Name of each exchange on which registered | ||||||||||||

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| ☒ | Accelerated filer | o | ||||||||||||

| Non-accelerated filer | o | Smaller reporting company | ||||||||||||

| Emerging growth company | ||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date.

| Class | Outstanding at May 4, 2022 | |||||||

| Class A common stock, par value $0.0001 | ||||||||

| Class B common stock, par value $0.0001 | ||||||||

| Class C common stock, par value $0.0001 | ||||||||

| Class D common stock, par value $0.0001 | ||||||||

TABLE OF CONTENTS

| Page | ||||||||

Item 4. | Mine Safety Disclosures | |||||||

DEFINED TERMS

| Assets Under Management or AUM | Refers to the assets that we manage, and are generally equal to the sum of (i) net asset value (“NAV”); (ii) drawn and undrawn debt; (iii) uncalled capital commitments; and (iv) total managed assets for certain Real Estate products. | |||||||

| Annual Report | Refers to our annual report for the year ended December 31, 2021, filed with the SEC on Form 10-K on February 28, 2022. | |||||||

| our BDCs | Refers to our business development companies, as regulated under the Investment Company Act of 1940, as amended: Owl Rock Capital Corporation (NYSE: ORCC) (“ORCC”), Owl Rock Capital Corporation II (“ORCC II”), Owl Rock Capital Corporation III (“ORCC III”), Owl Rock Technology Finance Corp. (“ORTF”), Owl Rock Technology Finance Corp. II (“ORTF II”), Owl Rock Core Income Corp. (“ORCIC”) and Owl Rock Technology Income Corp. (“ORTIC”). | |||||||

| Blue Owl, the Company, the firm, we, us, and our | Refers to the Registrant and its consolidated subsidiaries. | |||||||

| Blue Owl Carry | Refers to Blue Owl Capital Carry LP. | |||||||

| Blue Owl GP | Refers collectively to Blue Owl Capital Holdings GP LLC and Blue Owl Capital GP LLC, which are directly or indirectly wholly owned subsidiaries of the Registrant that hold the Registrants interests in the Blue Owl Operating Partnerships. | |||||||

| Blue Owl Holdings | Refers to Blue Owl Capital Holdings LP. | |||||||

| Blue Owl Operating Group | Refers collectively to the Blue Owl Operating Partnerships and their consolidated subsidiaries. | |||||||

| Blue Owl Operating Group Units | Refers collectively to a unit in each of the Blue Owl Operating Partnerships. | |||||||

| Blue Owl Operating Partnerships | Refers to Blue Owl Carry and Blue Owl Holdings, collectively. | |||||||

| Blue Owl Securities | Refers to Blue Owl Securities LLC, a Delaware limited liability company. Blue Owl Securities is a broker-dealer registered with the SEC, a member of FINRA and the SIPC. Blue Owl Securities is wholly owned by Blue Owl and provides distribution services to all Blue Owl Divisions. | |||||||

| Business Combination | Refers to the transactions contemplated by the Business Combination Agreement, which were completed on May 19, 2021. | |||||||

| Business Combination Agreement or BCA | Refers to the agreement dated as of December 23, 2020 (as the same has been or may be amended, modified, supplemented or waived from time to time), by and among Altimar Acquisition Corporation, Owl Rock Capital Group LLC, Owl Rock Capital Feeder LLC, Owl Rock Capital Partners LP and Neuberger Berman Group LLC. | |||||||

| Business Combination Date | Refers to May 19, 2021. | |||||||

| Class A Shares | Refers to the Class A common stock, par value $0.0001 per share, of the Registrant. | |||||||

| Class B Shares | Refers to the Class B common stock, par value $0.0001 per share, of the Registrant. | |||||||

| Class C Shares | Refers to the Class C common stock, par value $0.0001 per share, of the Registrant. | |||||||

| Class D Shares | Refers to the Class D common stock, par value $0.0001 per share, of the Registrant. | |||||||

| Class E Shares | Refers to the Class E common stock, par value $0.0001 per share, of the Registrant. | |||||||

| Direct Lending | Refers to our Direct Lending products, which offer private credit solutions to middle-market companies through four investment strategies: diversified lending, technology lending, first lien lending and opportunistic lending. Direct Lending products are managed by the Owl Rock division of Blue Owl. | |||||||

| Dyal Capital | Refers to the Dyal Capital Partners business, which was acquired from Neuberger Berman Group LLC in connection with the Business Combination, and is now a division of Blue Owl. | |||||||

| Fee-Paying AUM or FPAUM | Refers to the AUM on which management fees are earned. For our BDCs, FPAUM is generally equal to total assets (including assets acquired with debt but excluding cash). For our other Direct Lending products, FPAUM is generally equal to NAV or investment cost. FPAUM also includes uncalled committed capital for products where we earn management fees on such uncalled committed capital. For our GP Capital Solutions products, FPAUM for the GP minority equity investments strategy is generally equal to capital commitments during the investment period and the cost of unrealized investments after the investment period. For GP Capital Solutions’ other strategies, FPAUM is generally equal to investment cost. For Real Estate, FPAUM is generally based on total assets (including assets acquired with debt). | |||||||

| Financial Statements | Refers to our consolidated and combined financial statements included in this report. | |||||||

| GP Capital Solutions | Refers to our GP Capital Solutions products, which primarily focus on acquiring equity stakes in, or providing debt financing to, large, multi-product private equity and private credit platforms through three existing investment strategies: GP minority equity investments, GP debt financing and professional sports minority investments. GP Capital Solutions products are managed by the Dyal Capital division of Blue Owl. | |||||||

| NYSE | Refers to the New York Stock Exchange. | |||||||

| Oak Street | Refers to the investment advisory business of Oak Street Real Estate Capital, LLC that was acquired on December 29, 2021, and is now a division of Blue Owl. | |||||||

| Oak Street Acquisition | Refers to the acquisition of Oak Street completed on December 29, 2021. | |||||||

| Owl Rock | Refers collectively to the combined businesses of Owl Rock Capital Group LLC (“Owl Rock Capital Group”) and Blue Owl Securities LLC (formerly, Owl Rock Capital Securities LLC), which was the predecessor of Blue Owl for accounting and financial reporting purposes. References to the Owl Rock division refer to Owl Rock Capital Group and its subsidiaries that manage our Direct Lending products. | |||||||

| Partner Manager | Refers to alternative asset management firms in which the GP Capital Solution products invest. | |||||||

| Part I Fees | Refers to quarterly performance income on the net investment income of our BDCs and similarly structured products, subject to a fixed hurdle rate. These fees are classified as management fees throughout this report, as they are predictable and recurring in nature, not subject to repayment, and cash-settled each quarter. | |||||||

| Part II Fees | Generally refers to fees from our BDCs and similarly structured products that are paid in arrears as of the end of each measurement period when the cumulative aggregate realized capital gains exceed the cumulative aggregate realized capital losses and aggregate unrealized capital depreciation, less the aggregate amount of Part II Fees paid in all prior years since inception. Part II Fees are classified as realized performance income throughout this report. | |||||||

| Principals | Refers to our founders and senior members of management who hold, or in the future may hold, Class B Shares and Class D Shares. Class B Shares and Class D Shares collectively represent 80% of the total voting power of all shares. | |||||||

| Real Estate | Refers, unless context indicates otherwise, to our Real Estate products, which primarily focus on providing investors with predictable current income, and potential for appreciation, while focusing on limiting downside risk through a unique net lease strategy. Real Estate products are managed by the Oak Street division of Blue Owl. | |||||||

| Registrant | Refers to Blue Owl Capital Inc. | |||||||

| SEC | Refers to the U.S. Securities and Exchange Commission. | |||||||

| Tax Receivable Agreement or TRA | Refers to the Amended and Restated Tax Receivable Agreement, dated as of October 22, 2021, as may be amended from time to time by and among the Registrant, Blue Owl Capital GP LLC, the Blue Owl Operating Partnerships and each of the Partners (as defined therein) party thereto. | |||||||

AVAILABLE INFORMATION

We file annual, quarterly and current reports, proxy statements and other information required by the Securities Exchange Act of 1934, as amended (the “Exchange Act”) with the SEC. We make available free of charge on our website (www.blueowl.com) our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, proxy statements and other filing as soon as reasonably practicable after such material is electronically filed with or furnished to the SEC. We also use our website to distribute company information, including assets under management and performance information, and such information may be deemed material. Accordingly, investors should monitor our website, in addition to our press releases, SEC filings and public conference calls and webcasts.

Also posted on our website in the “Investor Relations—Governance” section is the charter for our Audit Committee, as well as our Corporate Governance Guidelines and Code of Business Conduct governing our directors, officers and employees. Information on or accessible through our website is not a part of or incorporated into this report or any other SEC filing. Copies of our SEC filings or corporate governance materials are available without charge upon written request to Blue Owl Capital Inc., 399 Park Avenue, 38th Floor, New York, New York 10022, Attention: Office of the Secretary. Any materials we file with the SEC are also publicly available through the SEC’s website (www.sec.gov).

No statements herein, available on our website or in any of the materials we file with the SEC constitute, or should be viewed as constituting, an offer of any fund.

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This report contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Exchange Act, which reflect our current views with respect to, among other things, future events, operations and financial performance. You can identify these forward-looking statements by the use of forward-looking words such as “outlook,” “believes,” “expects,” “potential,” “continues,” “may,” “will,” “should,” “seeks,” “approximately,” “predicts,” “projects,” “intends,” “plans,” “estimates,” “anticipates” or the negative version of those words, other comparable words or other statements that do not relate to historical or factual matters. The forward-looking statements are based on our beliefs, assumptions and expectations of our future performance, taking into account all information currently available to us. Such forward-looking statements are subject to various risks, uncertainties (some of which are beyond our control) or other assumptions relating to our operations, financial results, financial condition, business prospects, growth strategy and liquidity that may cause actual results or performance to be materially different from those expressed or implied by these forward-looking statements. Some of these factors are described under the headings “Item 1A. Risk Factors” and “Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations.” These factors should not be construed as exhaustive and should be read in conjunction with the risk factors and other cautionary statements that are included in this report and in our other periodic filings. If one or more of these or other risks or uncertainties materialize, or if our underlying assumptions prove to be incorrect, our actual results may vary materially from those indicated in these forward-looking statements. New risks and uncertainties arise over time, and it is not possible for us to predict those events or how they may affect us. Therefore, you should not place undue reliance on these forward-looking statements. Any forward-looking statement speaks only as of the date on which it is made. We do not undertake any obligation to publicly update or review any forward-looking statement, whether as a result of new information, future developments or otherwise, except as required by law.

PART I - FINANCIAL INFORMATION

Item 1. Financial Statements.

The information required by this item is included in the Financial Statements set forth in the F-pages of this report.

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

The following Management’s Discussion and Analysis of Financial Condition and Results of Operations (“MD&A”), should be read in conjunction with the unaudited consolidated and combined financial statements and the related notes included in this report. For a description of our business, please see “Business of Blue Owl” in the Annual Report.

2022 First Quarter Overview

| Three Months Ended March 31, | |||||||||||

| (dollars in thousands) | 2022 | 2021 | |||||||||

| Net (Loss) Income Attributable to Blue Owl Capital Inc. (After May 19, 2021) / Owl Rock (Prior to May 19, 2021) | $ | (11,815) | $ | 39,414 | |||||||

Fee-Related Earnings(1) | $ | 171,383 | $ | 46,350 | |||||||

Distributable Earnings(1) | $ | 155,726 | $ | 40,254 | |||||||

(1) For the specific components and calculations of these Non-GAAP measures, as well as a reconciliation of these measures to the most comparable measure in accordance with GAAP, see “—Non-GAAP Analysis” and “—Non-GAAP Reconciliations.”

Our results for first quarter of 2021 do not include the results of Dyal Capital or Oak Street; therefore, prior period amounts are not comparable to current period. Please see “—GAAP Results of Operations Analysis” and “—Non-GAAP Analysis” for a detailed discussion of the underlying drivers of our results, including the accretive impacts of the Dyal Acquisition and Oak Street Acquisition.

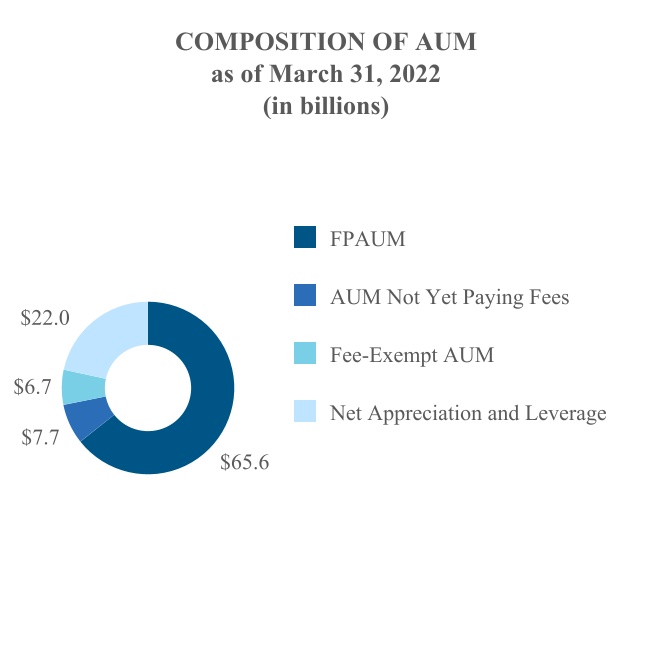

Assets Under Management

Blue Owl AUM: $102.0 billion FPAUM: $65.6 billion | ||||||||||||||

Direct Lending Products AUM: $44.8 billion FPAUM: $32.7 billion | GP Capital Solutions Products AUM: $41.2 billion FPAUM: $23.7 billion | Real Estate Products AUM: $16.1 billion FPAUM: $9.3 billion | ||||||||||||

Diversified Lending Commenced 2016 AUM: $30.4 billion FPAUM: $21.1 billion | GP Minority Equity Commenced 2010 AUM: $39.6 billion FPAUM: $22.8 billion | Net Lease Commenced 2009 AUM: $16.1 billion FPAUM: $9.3 billion | ||||||||||||

Technology Lending Commenced 2018 AUM: $8.9 billion FPAUM: $7.7 billion | GP Debt Financing Commenced 2019 AUM: $1.3 billion FPAUM: $0.7 billion | |||||||||||||

First Lien Lending Commenced 2018 AUM: $3.5 billion FPAUM: $2.5 billion | Professional Sports Minority Investments Commenced 2021 AUM: $0.2 billion FPAUM: $0.2 billion | |||||||||||||

Opportunistic Lending Commenced 2020 AUM: $2.1 billion FPAUM: $1.4 billion | ||||||||||||||

7

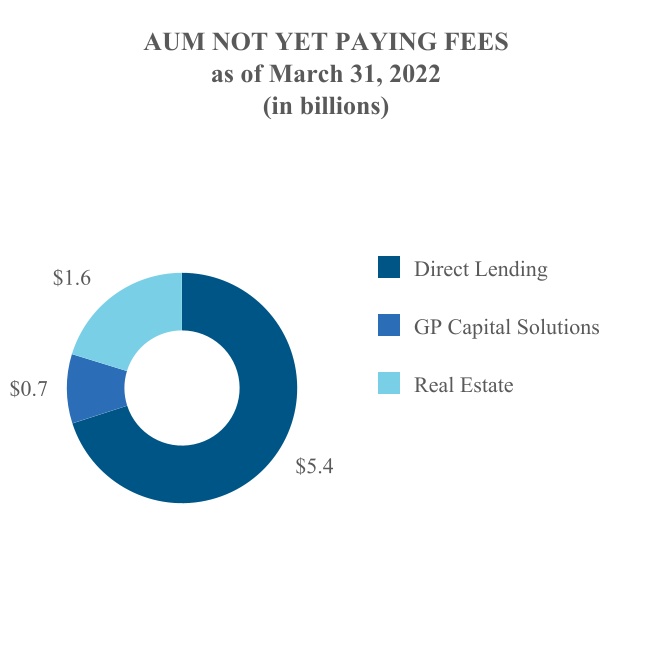

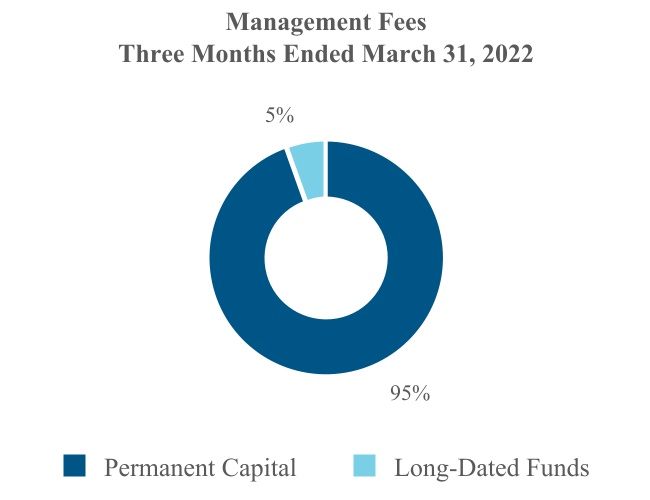

We finished the quarter with $102.0 billion of AUM, which included $65.6 billion of FPAUM. During the first quarter of 2022, approximately 95% of our management fees were earned on AUM that we refer to as permanent capital. As of March 31, 2022, we have approximately $7.7 billion in AUM not yet paying fees, providing approximately $105.0 million of annualized management fees once deployed or upon the expiration of certain fee holidays. See “—Assets Under Management” for additional information, including important information on how we define these metrics.

Business Environment

Our business is impacted by conditions in the financial markets and economic conditions in the U.S., and to a lesser extent, elsewhere in the world.

The public markets have witnessed volatility and dispersion in the first quarter of 2022 resulting from unexpectedly high and persistent inflation, a shifting interest rate environment, geopolitical events, and ongoing impact from COVID-19 globally. Allocations to alternative strategies have unsurprisingly created some near-term headwinds to industry-wide M&A and capital markets activity as investors paused to react to updated information, market expectations, and a changing investment landscape. We have benefited from this market volatility as an increasing number of sponsors and private companies have looked to Direct Lending for flexible and dependable financing, and capital that managers need to expand and diversify their platforms through our GP Capital Solutions products.

Higher than expected inflation has impacted expectations for the pace of rate hikes, driving market volatility and adjusting investors’ views on earnings growth for many public companies. We anticipate a net positive effect on our business from a rising rate environment. We expect our Direct Lending products to be a beneficiary of rising rates, as investor demand increases for senior secured floating rate assets focused on downside protection, and over time, the effect of rising rates would be positive for the net interest income of our Direct Lending products’ loan portfolios. For GP Capital Solutions, market volatility should drive demand for products managed by large, diversified managers, benefiting the types of firms our GP Capital Solutions products have typically taken stakes in. With respect to our Real Estate products, we believe there will continue to be strong demand for real estate strategies with long-term, contractual income that are positively correlated to inflation and backed by investment grade tenants, and that rising corporate borrowing costs will drive incremental demand for our Real Estate net lease solutions.

We believe that our disciplined investment philosophy across our distinct but complementary products contributes to the stability of our performance throughout market cycles. Our products have a stable base of permanent or long-term capital enabling us to invest in assets with a long-term focus over different points in a market cycle.

Assets Under Management

We present information regarding our AUM, FPAUM and various other related metrics throughout this MD&A to provide context around our fee generating revenues results, as well as indicators of the potential for future earnings from existing and new products. Our calculations of AUM and FPAUM may differ from the calculation methodologies of other asset managers, and as a result these measures may not be comparable to similar measures presented by other asset managers. In addition, our calculation of AUM includes amounts that are fee exempt (i.e., not subject to fees).

As of March 31, 2022, our assets under management include approximately $2.2 billion related to us, our executives and other employees. A portion of these assets under management relate to accrued carried interests, as well as investments that are not charged fees.

Composition of Assets Under Management

Our AUM consists of FPAUM, AUM not yet paying fees, fee-exempt AUM and net appreciation and leverage in products on which fees are based on commitments or investment cost. AUM not yet paying fees generally relates to unfunded capital commitments (to the extent such commitments are not already subject to fees), undeployed debt (to the extent we earn fees based on total asset values or investment cost, inclusive of assets purchased using debt) and AUM that is subject to a temporary fee holiday. Fee-exempt AUM represents certain investments by us, our employees, other related parties and third parties, as well as certain co-investment vehicles on which we do not earn fees.

8

Management uses AUM not yet paying fees as an indicator of management fees that will be coming online as we deploy existing assets in products that charge fees based on deployed and not uncalled capital, as well as AUM that is currently subject to a fee holiday that will expire at a predetermined time in the future. AUM not yet paying fees could provide approximately $105.0 million of additional annualized management fees once deployed or upon the expiration of the relevant fee holidays. Approximately $2.2 billion of AUM not yet paying fees moved to FPAUM on January 1, 2022, driven primarily by the expiration of certain fee holidays in Dyal Fund V, which was offset by a decrease in FPAUM for a step down in fee basis in Dyal Fund III of $0.9 billion.

Permanency and Duration of Assets Under Management

Our capital base is heavily weighted toward permanent capital. We use the term “permanent capital” to refer to AUM in our products that do not have ordinary redemption provisions or a requirement to exit investments and return the proceeds to investors after a prescribed period of time. Some of these products, however, may be required, or elect, to return all or a portion of capital gains and investment income. Permanent capital includes certain products that are subject to management fee step downs and/or roll-offs over time. Substantially all of our remaining AUM is in what we refer to as “long-dated funds.” These are funds in which the contractual remaining life is five years or more.

9

We view the permanency and duration of the products that we manage as a differentiator in our industry and as a means of measuring the stability of our future revenues stream. The chart below presents the composition of our management fees by remaining product duration. Changes in these relative percentages will occur over time as the mix of products we offer changes. For example, our Real Estate products have a higher concentration in long-dated funds, which in isolation may cause our percentage of management fees from permanent capital to decline.

Changes in AUM

| Three Months Ended March 31, 2022 | Three Months Ended March 31, 2021 | ||||||||||||||||||||||||||||||||||||||||||||||

| (dollars in millions) | Direct Lending | GP Capital Solutions | Real Estate | Total | Direct Lending | GP Capital Solutions | Real Estate | Total | |||||||||||||||||||||||||||||||||||||||

| Beginning Balance | $ | 39,227 | $ | 39,906 | $ | 15,362 | $ | 94,495 | $ | 27,101 | $ | 26,220 | $ | — | $ | 53,321 | |||||||||||||||||||||||||||||||

| Acquisition | — | — | — | — | — | — | — | — | |||||||||||||||||||||||||||||||||||||||

| New capital raised | 1,938 | 1,566 | 360 | 3,864 | 235 | 911 | — | 1,146 | |||||||||||||||||||||||||||||||||||||||

| Change in debt | 3,618 | — | — | 3,618 | 329 | — | — | 329 | |||||||||||||||||||||||||||||||||||||||

| Distributions | (284) | (758) | (165) | (1,207) | (181) | (74) | — | (255) | |||||||||||||||||||||||||||||||||||||||

| Change in value / other | 276 | 439 | 533 | 1,248 | 293 | 3,139 | — | 3,432 | |||||||||||||||||||||||||||||||||||||||

| Ending Balance | $ | 44,775 | $ | 41,153 | $ | 16,090 | $ | 102,018 | $ | 27,777 | $ | 30,196 | $ | — | $ | 57,973 | |||||||||||||||||||||||||||||||

Direct Lending. Increase in AUM was driven by a combination of continued fundraising and debt deployment across the strategy.

•$1.2 billion new capital raised in Diversified Lending, primarily driven by retail fundraising in ORCIC.

•$0.7 billion new capital raised in Technology Lending, driven by continued fundraising in ORTF II, our second technology-focused BDC.

•$3.6 billion of debt deployment across all of Direct Lending, as we continue to opportunistically deploy leverage in our BDCs.

GP Capital Solutions. Increase in AUM was driven by new capital raised, primarily in Dyal Fund V, and overall appreciation across all of our major products.

Real Estate. There was no material increase or decrease in AUM.

10

Changes in FPAUM

| Three Months Ended March 31, 2022 | Three Months Ended March 31, 2021 | ||||||||||||||||||||||||||||||||||||||||||||||

| (dollars in millions) | Direct Lending | GP Capital Solutions | Real Estate | Total | Direct Lending | GP Capital Solutions | Real Estate | Total | |||||||||||||||||||||||||||||||||||||||

| Beginning Balance | $ | 32,029 | $ | 21,212 | $ | 8,203 | $ | 61,444 | $ | 20,862 | $ | 17,608 | $ | — | $ | 38,470 | |||||||||||||||||||||||||||||||

| Acquisition | — | — | — | — | — | — | — | — | |||||||||||||||||||||||||||||||||||||||

| New capital raised / deployed | 2,200 | 1,171 | 1,077 | 4,448 | 482 | 1,011 | — | 1,493 | |||||||||||||||||||||||||||||||||||||||

| Fee basis change | — | 1,268 | — | 1,268 | — | — | — | — | |||||||||||||||||||||||||||||||||||||||

| Distributions | (278) | — | (161) | (439) | (149) | 11 | — | (138) | |||||||||||||||||||||||||||||||||||||||

| Change in value / other | (1,293) | — | 156 | (1,137) | 276 | — | — | 276 | |||||||||||||||||||||||||||||||||||||||

| Ending Balance | $ | 32,658 | $ | 23,651 | $ | 9,275 | $ | 65,584 | $ | 21,471 | $ | 18,630 | $ | — | $ | 40,101 | |||||||||||||||||||||||||||||||

Direct Lending. Increase in FPAUM was driven by a combination of continued fundraising and debt deployment as discussed in the AUM section above, partially offset by a change in methodology that reduced FPAUM by approximately $1.5 billion.

GP Capital Solutions. Increase in FPAUM was driven by new capital raised, primarily in Dyal Fund V, and the expiration of certain fee holidays on January 1, 2022. The expiration of the fee holiday drove an increase in FPAUM of $2.2 billion, which was partially offset by a decrease in FPAUM for a step down in fee basis in Dyal Fund III of $0.9 billion.

Real Estate. There was no material increase or decrease in FPAUM.

Product Performance

Product performance for certain of our products is included throughout this discussion with analysis to facilitate an understanding of our results of operations for the periods presented. The performance information of our products reflected is not indicative of our performance. An investment in Blue Owl is not an investment in any of our products. Past performance is not indicative of future results. As with any investment, there is always the potential for gains as well as the possibility of losses. There can be no assurance that any of these products or our other existing and future products will achieve similar returns. MoIC and IRR data has not been presented for products that have launched within the last two years as such information is generally not meaningful (“NM”).

Direct Lending

| MoIC | IRR | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| (dollars in millions) | Year of Inception | AUM | Capital Raised (1) | Invested Capital (2) | Realized Proceeds (3) | Unrealized Value (4) | Total Value | Gross (5) | Net (6) | Gross (7) | Net (8) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Diversified Lending | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| ORCC | 2016 | $ | 14,616 | $ | 6,018 | $ | 6,030 | $ | 2,024 | $ | 5,871 | $ | 7,895 | 1.41x | 1.31x | 11.8 | % | 8.9 | % | ||||||||||||||||||||||||||||||||||||||||||||||

| ORCC II (9) | 2017 | $ | 2,614 | $ | 1,383 | $ | 1,355 | $ | 269 | $ | 1,342 | $ | 1,611 | NM | 1.19x | NM | 7.0 | % | |||||||||||||||||||||||||||||||||||||||||||||||

| ORCC III | 2020 | $ | 3,651 | $ | 1,709 | $ | 1,659 | $ | 101 | $ | 1,664 | $ | 1,765 | NM | NM | NM | NM | ||||||||||||||||||||||||||||||||||||||||||||||||

| ORCIC | 2020 | $ | 8,376 | $ | 2,810 | $ | 2,780 | $ | 71 | $ | 2,763 | $ | 2,834 | NM | NM | NM | NM | ||||||||||||||||||||||||||||||||||||||||||||||||

| Technology Lending | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| ORTF | 2018 | $ | 7,185 | $ | 3,195 | $ | 3,196 | $ | 278 | $ | 3,457 | $ | 3,735 | 1.22x | 1.17x | 15.2 | % | 11.2 | % | ||||||||||||||||||||||||||||||||||||||||||||||

| First Lien Lending (10) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Owl Rock First Lien Fund Levered | 2018 | $ | 2,948 | $ | 1,161 | $ | 813 | $ | 116 | $ | 836 | $ | 952 | 1.22x | 1.18x | 10.2 | % | 8.1 | % | ||||||||||||||||||||||||||||||||||||||||||||||

| Owl Rock First Lien Fund Unlevered | 2019 | $ | 150 | $ | 144 | $ | 7 | $ | 147 | $ | 154 | 1.11x | 1.08x | 5.3 | % | 3.5 | % | ||||||||||||||||||||||||||||||||||||||||||||||||

(1)Includes reinvested dividends and share repurchases, if applicable.

(2)Invested capital includes capital calls, reinvested dividends and periodic investor closes, as applicable.

(3)Realized proceeds represent the sum of all cash distributions to investors.

(4)Unrealized value represents the product’s NAV. There can be no assurance that unrealized values will be realized at the valuations indicated.

(5)Gross multiple of invested capital (“MoIC”) is calculated by adding total realized proceeds and unrealized values of a product’s investments and dividing by the total amount of invested capital. Gross MoIC is before giving effect to management fees (including Part I Fees) and Part II Fees, as applicable.

(6)Net MoIC measures the aggregate value generated by a product’s investments in absolute terms. Net MoIC is calculated by adding total realized proceeds and unrealized values of a product’s investments and dividing by the total amount of invested capital. Net MoIC is calculated after giving effect to management fees (including Part I Fees) and Part II Fees, as applicable, and all other expenses.

11

(7)Gross IRR is an annualized since inception gross internal rate of return of cash flows to and from the product and the product’s residual value at the end of the measurement period. Gross IRRs are calculated before giving effect to management fees (including Part I Fees) and Part II Fees, as applicable.

(8)Net IRRs are calculated consistent with gross IRRs, but after giving effect to management fees (including Part I Fees) and Part II Fees, as applicable, and all other expenses. An individual investor’s IRR may be different to the reported IRR based on the timing of capital transactions.

(9)For the purposes of calculating Gross IRR, the expense support provided to the fund would be impacted when assuming a performance excluding management fees (including Part I Fees) and Part II Fees, and therefore is not meaningful for ORCC II.

(10)Owl Rock First Lien Fund is comprised of three feeder funds: Onshore Levered, Offshore Levered and Insurance Unlevered. The gross and net MoIC and IRR presented in the chart are for Onshore Levered and Insurance Unlevered as those are the largest of the levered and unlevered feeder funds. The gross and net MoIC for the Offshore Levered feeder fund is 1.21x and 1.14x, respectively. The gross and net IRR for the Offshore Levered feeder is 9.6% and 6.4%, respectively. All other values for Owl Rock First Lien Fund Levered are for Onshore Levered and Offshore Levered combined. AUM is presented as the aggregate of the three Owl Rock First Lien Fund feeders. Owl Rock First Lien Fund Unlevered Investor equity and note commitments are both treated as capital for all values.

GP Capital Solutions

| MoIC | IRR | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| (dollars in millions) | Year of Inception | AUM | Capital Raised | Invested Capital (2) | Realized Proceeds (3) | Unrealized Value (4) | Total Value | Gross (5) | Net (6) | Gross (7) | Net (8) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

| GP Minority Equity (1) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Dyal Fund I | 2011 | $ | 954 | $ | 1,284 | $ | 1,248 | $ | 583 | $ | 721 | $ | 1,304 | 1.19x | 1.04x | 3.8 | % | 0.5 | % | ||||||||||||||||||||||||||||||||||||||||||||||

| Dyal Fund II | 2014 | $ | 2,590 | $ | 2,153 | $ | 1,846 | $ | 421 | $ | 2,028 | $ | 2,449 | 1.48x | 1.33x | 11.9 | % | 7.8 | % | ||||||||||||||||||||||||||||||||||||||||||||||

| Dyal Fund III | 2015 | $ | 8,174 | $ | 5,318 | $ | 3,241 | $ | 2,591 | $ | 4,272 | $ | 6,863 | 2.54x | 2.12x | 31.8 | % | 23.9 | % | ||||||||||||||||||||||||||||||||||||||||||||||

| Dyal Fund IV | 2018 | $ | 14,330 | $ | 9,041 | $ | 4,807 | $ | 2,352 | $ | 6,667 | $ | 9,019 | 2.25x | 1.88x | 127.3 | % | 81.2 | % | ||||||||||||||||||||||||||||||||||||||||||||||

| Dyal Fund V | 2020 | $ | 7,798 | $ | 6,787 | $ | 926 | $ | — | $ | 1,758 | $ | 1,758 | NM | NM | NM | NM | ||||||||||||||||||||||||||||||||||||||||||||||||

(1)Valuation-related amounts and performance metrics are presented on a quarter lag and are exclusive of investments made by us and the related carried interest vehicles of the respective products.

(2)Invested capital includes capital calls.

(3)Realized proceeds represent the sum of all cash distributions to investors.

(4)Unrealized value represents the product's NAV. There can be no assurance that unrealized values will be realized at the valuations indicated.

(5)Gross MoIC is calculated by adding total realized proceeds and unrealized values of a product’s investments and dividing by the total amount of invested capital. Gross MoIC is before giving effect to management fees and carried interest, as applicable.

(6)Net MoIC measures the aggregate value generated by a product's investments in absolute terms. Net MoIC is calculated by adding total realized proceeds and unrealized values of a product's investments and dividing by the total amount of invested capital. Net MoIC is calculated after giving effect to management fees and carried interest, as applicable, and all other expenses.

(7)Gross IRR is an annualized since inception gross internal rate of return of cash flows to and from the product and the product’s residual value at the end of the measurement period. Gross IRRs are calculated before giving effect to management fees and carried interest, as applicable.

(8)Net IRR is an annualized since inception net internal rate of return of cash flows to and from the product and the product's residual value at the end of the measurement period. Net IRRs reflect returns to all investors. Net IRRs are calculated after giving effect to management fees and carried interest, as applicable, and all other expenses. An individual investor's IRR may be different to the reported IRR based on the timing of capital transactions.

Real Estate

| MoIC | IRR | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| (dollars in millions) | Year of Inception | AUM | Capital Raised | Invested Capital (2) | Realized Proceeds (3) | Unrealized Value (4) | Total Value | Gross (5) | Net (6) | Gross (7) | Net (8) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Net Lease (1) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Oak Street Real Estate Capital Fund IV | 2017 | $ | 1,322 | $ | 1,250 | $ | 1,239 | $ | 923 | $ | 883 | $ | 1,806 | 1.60x | 1.46x | 27.2 | % | 21.4 | % | ||||||||||||||||||||||||||||||||||||||||||||||

| Oak Street Real Estate Capital Net Lease Property Fund | 2019 | $ | 5,671 | $ | 3,161 | $ | 2,600 | $ | 164 | $ | 2,951 | $ | 3,115 | 1.21x | 1.20x | 22.5 | % | 21.4 | % | ||||||||||||||||||||||||||||||||||||||||||||||

| Oak Street Real Estate Capital Fund V | 2020 | $ | 3,621 | $ | 2,500 | $ | 1,147 | $ | 304 | $ | 1,089 | $ | 1,393 | NM | NM | NM | NM | ||||||||||||||||||||||||||||||||||||||||||||||||

| Oak Street Asset-Backed Securitization (9) | 2020 | $ | 3,001 | $ | 2,713 | $ | 342 | $ | 48 | $ | 352 | $ | 400 | NM | NM | NM | NM | ||||||||||||||||||||||||||||||||||||||||||||||||

(1)Valuation-related amounts and performance metrics, as well as invested capital and realized proceeds, are presented on a quarter lag where applicable.

(2)Invested capital includes investments by the general partner, capital calls, dividends reinvested and periodic investors closes, as applicable.

(3)Realized proceeds represent the sum of all cash distributions to all investors.

(4)Unrealized value represents the fund’s NAV. There can be no assurance that unrealized values will be realized at the valuations indicated.

(5)Gross MoIC is calculated by adding total realized proceeds and unrealized values of a product’s investments and dividing by the total amount of invested capital. Gross MoIC is before giving effect to management fees and carried interest, as applicable.

(6)Net MoIC measures the aggregate value generated by a product's investments in absolute terms. Net MoIC is calculated by adding total realized proceeds and unrealized values of a product's investments and dividing by the total amount of invested capital. Net MoIC is calculated after giving effect to management fees and carried interest, as applicable, and all other expenses.

(7)Gross IRR is an annualized since inception gross internal rate of return of cash flows to and from the product and the product’s residual value at the end of the measurement period. Gross IRRs are calculated before giving effect to management fees and carried interest, as applicable.

12

(8)Net IRR is an annualized since inception net internal rate of return of cash flows to and from the product and the product's residual value at the end of the measurement period. Net IRRs reflect returns to all investors. Net IRRs are calculated after giving effect to management fees and carried interest, as applicable, and all other expenses. An individual investor's IRR may be different to the reported IRR based on the timing of capital transactions.

(9)Capital raised for this product includes the par value of notes issued in the securitization. Invested capital, realized proceeds, unrealized and total values relate to the subordinated notes/equity of the securitization.

GAAP Results of Operations Analysis

As a result of the Dyal Acquisition and Oak Street Acquisition, prior year amounts are not comparable to current year amounts or expected future trends. Dyal Capital’s and Oak Street’s results of operations are included from the Business Combination Date and December 29, 2021, respectively.

Three Months Ended March 31, 2022, Compared to the Three Months Ended March 31, 2021

| Three Months Ended March 31, | |||||||||||||||||

| (dollars in thousands) | 2022 | 2021 | $ Change | ||||||||||||||

| Revenues | |||||||||||||||||

Management fees, net (includes Part I Fees of $46,739 and 28,914) | $ | 247,632 | $ | 94,713 | $ | 152,919 | |||||||||||

| Administrative, transaction and other fees | 28,345 | 13,511 | 14,834 | ||||||||||||||

| Total Revenues, Net | 275,977 | 108,224 | 167,753 | ||||||||||||||

| Expenses | |||||||||||||||||

| Compensation and benefits | 193,892 | 47,984 | 145,908 | ||||||||||||||

| Amortization of intangible assets | 61,526 | — | 61,526 | ||||||||||||||

| General, administrative and other expenses | 43,294 | 14,860 | 28,434 | ||||||||||||||

| Total Expenses | 298,712 | 62,844 | 235,868 | ||||||||||||||

| Other (Loss) Income | |||||||||||||||||

| Net gains on investments | 5 | — | 5 | ||||||||||||||

| Interest expense | (12,834) | (5,858) | (6,976) | ||||||||||||||

| Change in TRA liability | (9,652) | — | (9,652) | ||||||||||||||

| Change in warrant liability | 17,758 | — | 17,758 | ||||||||||||||

| Change in earnout liability | (496) | — | (496) | ||||||||||||||

| Total Other (Loss) Income | (5,219) | (5,858) | 639 | ||||||||||||||

| (Loss) Income Before Income Taxes | (27,954) | 39,522 | (67,476) | ||||||||||||||

| Income tax (benefit) expense | (5,038) | 188 | (5,226) | ||||||||||||||

| Consolidated and Combined Net (Loss) Income | (22,916) | 39,334 | (62,250) | ||||||||||||||

| Net loss attributable to noncontrolling interests | 11,101 | 80 | 11,021 | ||||||||||||||

| Net (Loss) Income Attributable to Blue Owl Capital Inc. | $ | (11,815) | $ | 39,414 | $ | (51,229) | |||||||||||

Revenues, Net

Management Fees. Management fees increased primarily due to the $96.8 million accretive impact of GP Capital Solution’s management fees and $17.2 million of Real Estate’s management fees as well as overall growth in FPAUM across all of our Diversified Lending product strategies. See Note 5 to our consolidated and combined financial statements for additional details on our GAAP management fees by product and strategy.

Administrative, Transaction and Other Fees. The increase in administrative, transaction and other fees was driven primarily by a $4.8 million increase of dealer manager revenue, a $2.6 million increase of administrative fees related to our Direct Lending products and $3.1 million increase of administrative fees related to our GP Capital Solutions products due to higher compensation and benefits being recovered from our products, which are included from the Business Combination Date. Also contributing to the year-over-year increase was a $4.3 million increase in fee income earned for services provided to portfolio companies.

Expenses

Compensation and Benefits. Compensation and benefits expenses increased by $96.2 million related to amortization of equity grants, $16.1 million related to acquisition related cash earnouts for Oak Street and an additional $33.6 million related to growth in our employee headcount as a result of the Dyal and Oak Street acquisitions as well as organic growth.

13

Amortization of Intangible Assets. These expenses relate to the amortization of intangible assets acquired in connection with the Dyal Acquisition and the Oak Street Acquisition.

General, Administrative and Other Expenses. The increase in general, administrative and other expenses was due to Transaction Expenses of $9.6 million, a $7.6 million increase in distribution costs due to placement fees associated with Dyal Fund V and certain private fund closes in Direct Lending as well as ongoing trail fees for historical fundraise Dyal products which are included from the Business Combination Date. The remaining net increase was driven primarily by our continued growth as a public company and transitioning back to the office from a remote workforce.

Other Loss

Interest expense. The increase in interest expense was driven by higher average debt outstanding, as in 2021 our long-term debt outstanding related to the $250.0 million term loan agreement (the “Term Loan”) that was repaid in the second quarter of 2021 using proceeds from the $700.0 million of 2031 Notes, a larger size facility. Further, we issued the $350.0 million of 2051 Notes during the fourth quarter of 2021 and $400.0 million of 2032 Notes during the first quarter of 2022. The impact of higher average borrowing outstanding in fiscal quarter 2022 was partially offset by lower average borrowing rates on the Notes in 2022 compared to the Term Loan in 2021.

Change in TRA liability. The change in TRA liability in 2022 was due to the impact of the time value of money on the portion of the TRA that is carried at fair value (i.e., Dyal Acquisition contingent consideration). The TRA was entered into in connection with the Business Combination in May 2021.

Change in warrant liability. The change in warrant liability in 2022 was driven by the decrease in the price of our Public Warrants, as such price directly impacts the valuation of our Private Placement Warrants. The warrants were issued in connection with the Business Combination in May 2021.

Change in earnout liability. There was no material change to the earnout liability.

Income Tax Benefit

Prior to the Business Combination, our income was generally subject to New York City Unincorporated Business Tax (“UBT”), as the operating entities are partnerships for U.S. federal income tax purposes. As a result of the Business Combination, the portion of income allocable to the Registrant is now also generally subject to corporate tax rates at the U.S. federal and state and local levels. This resulted in an increase in income tax benefit in the current year period. Please see Note 9 to our Financial Statements for a discussion of the significant tax differences that impacted our effective tax rate.

Net Loss Attributable to Noncontrolling Interest

Net loss attributable to noncontrolling interests in the current year primarily represents the allocation to Common Units of their pro rata share of the Blue Owl Operating Group’s post-Business Combination net loss due to the drivers discussed above. The Common Units represented an approximately 71% weighted average economic interest in the Blue Owl Operating Group during the first quarter of 2022. Prior to the Business Combination, amounts attributable to noncontrolling interests were not significant, and related primarily to third-party interests held in certain of our consolidated investment advisor holding companies.

Non-GAAP Analysis

In addition to presenting our consolidated and combined results in accordance with GAAP, we present certain other financial measures that are not presented in accordance with GAAP. Management uses these measures to assess the performance of our business, and we believe that this information enhances the ability of shareholders to analyze our performance from period to period. These non-GAAP financial measures supplement and should be considered in addition to and not in lieu of our GAAP results, and such measures should not be considered as indicative of our liquidity. Our non-GAAP measures may not be comparable to other similarly titled measured used by other companies. Please see “—Non-GAAP Reconciliations” for reconciliations of these measures to the most comparable measures prepared in accordance with GAAP.

14

Fee-Related Earnings and Related Components

Fee-Related Earnings is a supplemental non-GAAP measure of operating performance used to make operating decisions and assess our operating performance. Fee-Related Earnings excludes certain items that are required for the presentation of our results on a GAAP basis. Management also reviews the components that comprise Fee-Related Earnings (i.e., FRE Revenues and FRE Expenses) on the same basis used to calculate Fee-Related Earnings, and such components are also non-GAAP measures and have been identified with the prefix “FRE” in the tables and discussion below. Management believes that by excluding these items, which are described below, Fee-Related Earnings and its components can be useful as supplemental measures to our GAAP results in assessing our operating performance and focusing on whether our recurring revenues, primarily consisting of management fees, are sufficient to cover our recurring operating expenses.

Fee-Related Earnings exclude various items that are required for the presentation of our results under GAAP, including the following: noncontrolling interests in the Blue Owl Operating Partnerships; equity-based compensation expense; compensation expenses related to capital contributions in certain subsidiary holding companies that are in-turn paid as compensation to certain employees, as such contributions are not included in Fee-Related Earnings or Distributable Earnings; amortization of acquisition-related earnouts; amortization of intangible assets; “Transaction Expenses” as defined below; net gains (losses) on investments, changes in TRA, earnout and warrant liabilities; net losses on retirement of debt; interest and taxes. In addition, management reviews revenues by reducing GAAP administrative, transaction and other fees for certain expenses related to reimbursements from our products, which are presented gross for GAAP but net for non-GAAP measures. Transaction Expenses are expenses incurred in connection with the Business Combination and other acquisitions and strategic transactions, including subsequent adjustments related to such transactions, that were not eligible to be netted against consideration or recognized as acquired assets and assumed liabilities in the relevant transaction. Starting in the first quarter of 2022, Transaction Expenses also include expenses paid on behalf of certain products that are expected to be reimbursed in subsequent periods; such amounts were not material to the prior periods presented, and therefore such periods have not be restated for this change.

Distributable Earnings

Distributable Earnings is a supplemental non-GAAP measure of operating performance that equals Fee-Related Earnings plus or minus, as relevant, realized performance income and related compensation, interest expense, as well as amounts payable for taxes and payments made pursuant to the TRA. Amounts payable for taxes presents the current income taxes payable related to the respective period’s earnings, assuming that all Distributable Earnings were allocated to the Registrant, which would occur following the exchange of all Blue Owl Operating Group Units for Class A Shares. Current income taxes payable and payments made pursuant to the TRA reflect the benefit of tax deductions that are excluded when calculating Distributable Earnings (e.g., equity-based compensation expenses, net losses on retirement of debt, Transaction Expenses, tax goodwill, etc.). If these tax deductions were to be excluded from amounts payable for taxes, Distributable Earnings would be lower and our effective tax rate would appear to be higher, even though a lower amount of income taxes would have been paid or payable for a period’s earnings. We make these adjustments when calculating Distributable Earnings to more accurately reflect the net realized earnings that are expected to be or become available for distribution or reinvestment into our business. Management believes that Distributable Earnings can be useful as a supplemental performance measure to our GAAP results assessing the amount of earnings available for distribution.

Fee-Related Earnings and Distributable Earnings Summary

| Three Months Ended March 31, | |||||||||||

| (dollars in thousands) | 2022 | 2021 | |||||||||

| FRE revenues | $ | 272,598 | $ | 103,771 | |||||||

| FRE expenses | (101,735) | (57,501) | |||||||||

| Net loss allocated to noncontrolling interests included in Fee-Related Earnings | 520 | 80 | |||||||||

| Fee-Related Earnings | $ | 171,383 | $ | 46,350 | |||||||

| Distributable Earnings | $ | 155,726 | $ | 40,254 | |||||||

Fee-Related Earnings and Distributable Earnings increased year-over-year as a result of the accretive impact of the Dyal Acquisition and Oak Street Acquisition, as well as higher FRE revenues from our Direct Lending products. These increases were offset by higher FRE expenses, primarily due to compensation and benefits as discussed further below.

15

FRE Revenues

| Three Months Ended March 31, | |||||||||||

| (dollars in thousands) | 2022 | 2021 | |||||||||

| Direct Lending Products | |||||||||||

| Diversified lending | $ | 105,452 | $ | 76,478 | |||||||

| Technology lending | 23,030 | 13,857 | |||||||||

| First lien lending | 3,681 | 3,815 | |||||||||

| Opportunistic lending | 1,541 | 563 | |||||||||

| Management Fees, Net | 133,704 | 94,713 | |||||||||

| Administrative, transaction and other fees | 14,473 | 9,058 | |||||||||

| FRE Revenues - Direct Lending Products | 148,177 | 103,771 | |||||||||

| GP Capital Solutions Products | |||||||||||

| GP minority equity investments | 102,100 | — | |||||||||

| GP debt financing | 3,092 | — | |||||||||

| Professional sports minority investments | 500 | — | |||||||||

| Management Fees, Net | 105,692 | — | |||||||||

| Administrative, transaction and other fees | 1,571 | — | |||||||||

| FRE Revenues - GP Capital Solutions Products | 107,263 | — | |||||||||

| Real Estate Products | |||||||||||

| Net lease | 17,158 | — | |||||||||

| Management Fees, Net | 17,158 | — | |||||||||

| FRE Revenues - Real Estate Products | 17,158 | — | |||||||||

| Total FRE Revenues | $ | 272,598 | $ | 103,771 | |||||||

FRE revenues increased due to the accretive impact of the Dyal Capital and Oak Street acquisitions. FRE revenues also increased as a result of overall growth in FPAUM across all of our Diversified Lending product strategies. Also contributing to the increase were higher administrative, transaction and other fees due to higher fee income earned for services provided to portfolio companies.

FRE Expenses

| Three Months Ended March 31, | |||||||||||

| (dollars in thousands) | 2022 | 2021 | |||||||||

| FRE compensation and benefits | $ | (74,969) | $ | (44,530) | |||||||

| FRE general, administrative and other expenses | (26,766) | (12,971) | |||||||||

| Total FRE Expenses | $ | (101,735) | $ | (57,501) | |||||||

FRE expenses increased primarily due to higher FRE compensation and benefits as a result of increased headcount, both in the legacy Owl Rock business, as well as due to an increase related to the Dyal Acquisition and Oak Street Acquisition. FRE general, administrative and other expenses increased primarily due to increased distribution costs, increased costs related to being a public company and increased travel and office-related expenses as we transition from working remotely back to the office. See “—GAAP Results of Operations Analysis” for additional information on these drivers.

16

Non-GAAP Reconciliations

The table below presents the reconciliation of the non-GAAP measures presented throughout this MD&A. Please see “—Non-GAAP Analysis” for important information regarding these measures.

| Three Months Ended March 31, | |||||||||||

| (dollars in thousands) | 2022 | 2021 | |||||||||

| GAAP (Loss) Income Before Income Taxes | $ | (27,954) | $ | 39,522 | |||||||

| Net loss allocated to noncontrolling interests included in Fee-Related Earnings | 520 | 80 | |||||||||

| Strategic Revenue-Share Purchase consideration amortization | 8,922 | — | |||||||||

| Equity-based compensation | 96,601 | — | |||||||||

| Capital-related compensation | 830 | — | |||||||||

| Acquisition-related cash earnout amortization | 16,082 | — | |||||||||

| Amortization of intangible assets | 61,526 | — | |||||||||

| Transaction Expenses | 9,637 | 890 | |||||||||

| Interest expense | 12,834 | 5,858 | |||||||||

| Net gains on investments | (5) | — | |||||||||

| Change in TRA liability | 9,652 | — | |||||||||

| Change in warrant liability | (17,758) | — | |||||||||

| Change in earnout liability | 496 | — | |||||||||

| Fee-Related Earnings | 171,383 | 46,350 | |||||||||

| Interest expense | (12,834) | (5,858) | |||||||||

| Taxes and TRA payments | (2,823) | (238) | |||||||||

| Distributable Earnings | 155,726 | 40,254 | |||||||||

| Interest expense | 12,834 | 5,858 | |||||||||

| Taxes and TRA payments | 2,823 | 238 | |||||||||

| Fixed assets depreciation and amortization | 218 | 131 | |||||||||

| Adjusted EBITDA | $ | 171,601 | $ | 46,481 | |||||||

| Three Months Ended March 31, | |||||||||||

| (dollars in thousands) | 2022 | 2021 | |||||||||

| GAAP Revenues | $ | 275,977 | $ | 108,224 | |||||||

| Strategic Revenue-Share Purchase consideration amortization | 8,922 | — | |||||||||

| Administrative and other fees | (12,301) | (4,453) | |||||||||

| FRE Revenues | $ | 272,598 | $ | 103,771 | |||||||

| Three Months Ended March 31, | |||||||||||

| (dollars in thousands) | 2022 | 2021 | |||||||||

| GAAP Compensation and Benefits | $ | 193,892 | $ | 47,984 | |||||||

| Equity-based compensation | (96,188) | — | |||||||||

| Capital-related compensation | (830) | — | |||||||||

| Acquisition-related cash earnout amortization | (16,082) | — | |||||||||

| Administrative and other expenses | (5,823) | (3,454) | |||||||||

| FRE Compensation and Benefits | $ | 74,969 | $ | 44,530 | |||||||

| Three Months Ended March 31, | |||||||||||

| (dollars in thousands) | 2022 | 2021 | |||||||||

| GAAP General, Administrative and Other Expenses | $ | 43,294 | $ | 14,860 | |||||||

| Transaction Expenses | (9,637) | (890) | |||||||||

| Equity-based compensation | (413) | — | |||||||||

| Administrative and other expenses | (6,478) | (999) | |||||||||

| FRE General, Administrative and Other Expenses | $ | 26,766 | $ | 12,971 | |||||||

17

Liquidity and Capital Resources

Overview

We rely on management fees as the primary source of our operating liquidity. From time to time we may rely on the use of revolving credit facilities between management fee collection dates, which generally occur on a quarterly basis. We may also rely on our Revolving Credit Facility for liquidity needed to fund acquisitions, which we may replace with longer-term financing, subject to market conditions. To the extent that we have excess liquidity, we may invest such excess liquidity in corporate bonds, agency securities and other investments.

We ended the first quarter of 2022 with $186.0 million of cash and cash equivalents and $714.8 million available under our Revolving Credit Facility. Based on management’s experience and our current level of liquidity and assets under management, we believe that our current liquidity position and cash generated from management fees will continue to be sufficient to meet our anticipated working capital needs for at least the next 12 months.

Over the short and long term, we may use cash and cash equivalents, issue additional debt or equity securities, or may seek other sources of liquidity to:

•Grow our existing investment management business.

•Expand, or acquire, into businesses that are complementary to our existing investment management businesses or other strategic growth initiatives.

•Pay operating expenses, including cash compensation to our employees.

•Repay debt obligations and interest thereon.

•Opportunistically repurchase Class A Shares pursuant to the Share Repurchase Program (as defined below).

•Pay income taxes and amounts due under the TRA.

•Pay dividends to holders of our Class A Shares, as well as make corresponding distributions to holders of Common Units at the Blue Owl Operating Group level.

•Fund investment commitments to existing or future products.

Debt Obligations

As of March 31, 2022, our long-term debt obligations consisted of $700.0 million of 2031 Notes, $400.0 million of 2032 Notes and $350.0 million of 2051 Notes. We expect to use cash on hand to pay interest and principal due on our financing arrangements over time, which would reduce amounts available for dividends and distributions to our shareholders. We may choose to refinance all or a portion of any amounts outstanding on or prior to their respective maturity dates by issuing new debt, which could result in higher borrowing costs. We may also choose to repay borrowing by using proceeds from the issuance of equity or other securities, which would dilute shareholders. See Note 3 to our consolidated and combined financial statements in this report for additional information regarding our debt obligations.

Management regularly reviews Adjusted EBITDA to assess our ability to service our debt obligations. Adjusted EBITDA is equal to Distributable Earnings plus interest expense, taxes payable and TRA payments, and fixed assets depreciation and amortization. Adjusted EBITDA is a non-GAAP financial measure that supplements and should be considered in addition to and not in lieu of our GAAP results, and such measure should not be considered as indicative of our liquidity. Adjusted EBITDA may not be comparable to other similarly titled measured used by other companies. Adjusted EBITDA was $171.6 million for the quarter ended March 31, 2022. Please see “—Non-GAAP Reconciliations” for reconciliations of Adjusted EBITDA to the most comparable measures prepared in accordance with GAAP.

Tax Receivable Agreement

As discussed in Note 10 to our consolidated and combined financial statements in this report, we may in the future be required to make payments under the TRA. As of March 31, 2022, assuming no material changes in the relevant tax law and that we generate sufficient taxable income to realize the full tax benefit of the increased amortization resulting from the increase in tax basis of certain Blue Owl Operating Group assets, we expect to pay approximately $806.5 million under the TRA. Future cash savings and related payments under the TRA in respect of subsequent exchanges of Blue Owl Operating Group Units for Class A or B Shares would be in addition to these amounts.

18

Payments under the tax receivable agreement are anticipated to increase the tax basis adjustment and, consequently, result in increasing annual amortization deductions in the taxable years of and after such increases to the original basis adjustments, and potentially will give rise to increasing tax savings with respect to such years and correspondingly increasing payments under the TRA.

The obligation to make payments under the tax receivable agreement is an obligation of Blue Owl GP, and any other corporate taxpaying entities that in the future may hold GP Units, and not of the Blue Owl Operating Group. We may need to incur debt to finance payments under the TRA to the extent the Blue Owl Operating Group does not distribute cash to Registrant or Blue Owl GP in an amount sufficient to meet our obligations under the TRA.

The actual increase in tax basis of the Blue Owl Operating Group assets resulting from an exchange or from payments under the TRA, as well as the amortization thereof and the timing and amount of payments under the TRA, will vary based upon a number of factors, including the following:

•The amount and timing of our taxable income will impact the payments to be made under the TRA. To the extent that we do not have sufficient taxable income to utilize the amortization deductions available as a result of the increased tax basis in the Blue Owl Operating Partnerships’ assets, payments required under the TRA would be reduced.

•The price of our Class A Shares at the time of any exchange will determine the actual increase in tax basis of the Blue Owl Operating Partnerships’ assets resulting from such exchange; payments under the TRA resulting from future exchanges, if any, will be dependent in part upon such actual increase in tax basis.

•The composition of the Blue Owl Operating Group assets at the time of any exchange will determine the extent to which we may benefit from amortizing the increased tax basis in such assets and thus will impact the amount of future payments under the TRA resulting from any future exchanges.

•The extent to which future exchanges are taxable will impact the extent to which we will receive an increase in tax basis of the Blue Owl Operating Group assets as a result of such exchanges, and thus will impact the benefit derived by us and the resulting payments, if any, to be made under the TRA.

•The tax rates in effect at the time any potential tax savings are realized, which would affect the amount of any future payments under the TRA.

Depending upon the outcome of these and other factors, payments that we may be obligated to make under the TRA in respect of exchanges could be substantial. In light of the numerous factors affecting our obligation to make payments under the TRA, the timing and amounts of any such actual payments are not reasonably ascertainable.

Warrants

We classify the warrants issued in connection with the Business Combination as liabilities in our consolidated and combined statements of financial condition, as in the event of a change in control, warrant holders have the ability to demand cash settlement from us. In addition, we have the option to cash settle outstanding warrants when certain criteria is met, as described in Note 2 to our Financial Statements. To the extent we have insufficient cash on hand or that we opt to, we may rely on debt or equity financing to facilitate these transactions in the future if needed.

Oak Street Cash Earnout

A portion of the Oak Street Cash Earnout is classified as a liability and represents the fair value of the obligation to make future cash payments that would need to be made if all the respective Oak Street Triggering Events occur. Further, the portion classified as compensation expense will be expensed and a corresponding accrued compensation liability will be recorded over the service period. To the extent we have insufficient cash on hand or that we opt to, we may rely on debt or equity financing to facilitate these transactions in the future. See Note 2 to our Financial Statements for additional information.

19

Dividends and Distributions

We intend to continue to pay to Class A Shareholders (and Class B Shareholders in the future to the extent any Class B Shares are outstanding) a quarterly dividend representing approximately 85% of Distributable Earnings following the end of each quarter. Blue Owl Capital Inc.’s share of Distributable Earnings, subject to adjustment as determined by our Board to be necessary or appropriate to provide for the conduct of our business, to make appropriate investments in our business and products, to comply with applicable law, any of our debt instruments or other agreements, or to provide for future cash requirements such as tax-related payments, operating reserves, clawback obligations and dividends to shareholders for any ensuing quarter. All of the foregoing is subject to the qualification that the declaration and payment of any dividends are at the sole discretion of our Board, and our Board may change our dividend policy at any time, including, without limitation, to reduce or eliminate dividends entirely.

The Blue Owl Operating Partnerships will make cash distributions (“Tax Distributions”) to the partners of such partnerships, including to Blue Owl GP, if we determine that the taxable income of the relevant partnership will give rise to taxable income for its partners. Generally, Tax Distributions will be computed based on our estimate of the taxable income of the relevant partnership allocable to a partner multiplied by an assumed tax rate equal to the highest effective marginal combined U.S. federal, New York State and New York City income tax rates prescribed for an individual or corporate resident in New York City (taking into account certain assumptions set forth in the relevant partnership agreements). Tax Distributions will be made only to the extent distributions from the Blue Owl Operating Partnerships for the relevant year were otherwise insufficient to cover the estimated assumed tax liabilities.

Holders of our Class A and B Shares may not always receive distributions or may receive lower distributions on a per share basis at a time when we, indirectly through Blue Owl GP, and holders of our Common Units are receiving distributions on their interests, as distributions to the Registrant and Blue Owl GP may be used to settle tax and TRA liabilities, if any, and other obligations.

Dividends are expected to be treated as qualified dividends under current law to the extent of the Company’s current and accumulated earnings and profits, with any excess dividends treated as a return of capital to the extent of a shareholder’s basis, and any remaining excess generally treated as gain realized on the sale or other disposition of stock.

Risks to our Liquidity

Our ability to obtain financing provides us with additional sources of liquidity. Any new financing arrangement that we may enter into may have covenants that impose additional limitations on us, including with respect to making distributions, entering into business transactions or other matters, and may result in increased interest expense. If we are unable to secure financing on terms that are favorable to us, our business may be adversely impacted. No assurance can be given that we will be able to issue new debt, enter into new credit facilities or issue equity or other securities in the future on attractive terms or at all.

Adverse market conditions, including from unexpectedly high and persistent inflation, a shifting interest rate environment, geopolitical events, and ongoing impact from COVID-19 globally, may negatively impact our liquidity. Cash flows from management fees may be impacted by a slowdown or a decline in fundraising and deployment, as well as declines in the value of investments held in certain of our products.

LIBOR Transition

On March 5, 2021, the UK Financial Conduct Authority announced that it would phase out LIBOR as a benchmark immediately after December 31, 2021, for sterling, euro, Japanese yen, Swiss franc and 1-week and 2-month U.S. Dollar settings and immediately after June 30, 2023, the remaining U.S. Dollar settings. Our Notes are fixed rate borrowings, and therefore the LIBOR phase out will not have an impact on this borrowing. The Revolving Credit Facility is subject to SOFR rates at our option, or alternative rates that are not tied to LIBOR. Certain of our products hold investments and have borrowings that are tied to LIBOR, and we continue to focus on managing any risk related to those exposures. Our senior management has oversight of these transition efforts. See “Risk Factors—Risks Related to Legal and Regulatory Environment—Changes to the method of determining the London Interbank Offered Rate (“LIBOR”) or the selection of a replacement for LIBOR may affect the value of investments held by our products and could affect our results of operations and financial results.”

20

Cash Flows Analysis

| Three Months Ended March 31, | |||||||||||||||||

| (dollars in thousands) | 2022 | 2021 | $ Change | ||||||||||||||

| Net cash provided by (used in): | |||||||||||||||||

| Operating activities | $ | 93,204 | $ | 587 | $ | 92,617 | |||||||||||

| Investing activities | (22,607) | (295) | (22,312) | ||||||||||||||

| Financing activities | 72,788 | (3,358) | 76,146 | ||||||||||||||

| Net Change in Cash and Cash Equivalents | $ | 143,385 | $ | (3,066) | $ | 146,451 | |||||||||||

Operating Activities. Our net cash flows from operating activities are generally comprised of management fees, less cash used for operating expenses, including interest paid on our debt obligations. One of our largest operating cash outflows generally relates to bonus expense, which are generally paid out during the first quarter of the year following the expense.

Net cash flows from operating activities increased from the prior year period due to the inclusion of the GP Capital Solutions and Real Estate related cash flows, as well as higher management fees from our Direct Lending products. These increases were partially offset by higher 2021 discretionary bonuses, which were paid in the first quarter of 2022, as compared to discretionary bonuses in 2020, which were paid in the first quarter of 2021.

Investing Activities. Cash flows from investing activities for 2022 were primarily related to leasehold improvements associated with certain office spaces. In 2021, cash flows related to investing activities were not material.

Financing Activities. Cash flows from financing activities for 2022 were primarily driven by dividends on our Class A Shares and related distributions on our Common Units (noncontrolling interests). Our cash flows from financing activities also benefited from a net increase to our debt as a result of the proceeds from our 2032 Notes, which were used to finance working capital needs and general capital purposes, partially offset by repayments under our Revolving Credit Facility.

Our 2021 cash flows related to financing activities included borrowings and repayments under our previously outstanding revolving credit facilities. In addition, distributions related to pre-Business Combination-related earnings was another significant financing cash flow in the prior-year period.

Critical Accounting Estimates

We prepare our Financial Statements in accordance with U.S. GAAP. In applying many of these accounting principles, we make estimates that affect the reported amounts of assets, liabilities, revenues and expenses in our consolidated and combined financial statements. We base our estimates on historical experience and other factors that we believe are reasonable under the circumstances. These estimates, however, are subjective and subject to change, and actual results may differ materially from our current estimates due to the inherent nature of these estimates, including uncertainty in the current economic environment due to unexpectedly high and persistent inflation, a shifting interest rate environment, geopolitical events, and ongoing impact from COVID-19 globally. For a summary of our significant accounting policies, see Note 2 to our Financial Statements.

Estimation of Fair Values

Investments Held by our Products

The fair value of the investments held by our Direct Lending products is the primary input to the calculation for the majority of our management fees. Management fees from our GP Capital Solutions and Real Estate products are generally based on commitments or investment cost, so our management fees are generally not impacted by changes in the estimated fair values of investments held by these products. However, to the extent that management fees are calculated based on investment cost of the product’s investments, the amount of fees that we may charge will increase or decrease from the effect of changes in the cost basis of the product’s investments, including potential impairment losses. In the absence of observable market prices, we use valuation methodologies applied on a consistent basis and assumptions that we believe market participants would use to determine the fair value of the investments. For investments where little market activity exists, the determination of fair value is based on the best information available, we incorporate our own assumptions and involves a significant degree of judgment, and the consideration of a combination of internal and external factors.

21

Our products generally value their investments at fair value, as determined in good faith by each product’s respective board of directors or valuation committee, as applicable, based on, among other things, the input of third party valuation firms and taking into account the nature and realizable value of any collateral, an investee’s ability to make payments and its earnings, the markets in which the investee operates, comparison to publicly traded companies, discounted cash flows, current market interest rates and other relevant factors. Because such valuations are inherently uncertain, the valuations may fluctuate significantly over time due to changes in market conditions. These valuations would, in turn, have corresponding proportionate impacts on the amount of management fees that we may earn from certain products on which revenues are based on the fair value of investments.

TRA Liability