Our nationwide logistics infrastructure facilitates the fulfillment and delivery of parcels purchased on our Marketplace and our Direct Sales businesses in an efficient and reliable way. In the year ended December 31, 2022, we significantly expanded our warehouse infrastructure, consisting of fulfillment and sorting centers and our dark store network. In the year ended December 31, 2022, our operations utilized approximately 1.4 million square meters of warehouse capacity, compared to our warehouse capacity of 1 million square meters in the year ended December 31, 2021.

We are a technology-driven company with a strong culture of innovation. Our secure and scalable technology infrastructure, developed by our in-house research and development team, provides the foundation for seamless buyer and seller experiences on our platform, as well as for our supply chain operations, business intelligence, traffic and search optimization, customer relationship management operations and payments.

We believe that developing complementary products and services will help us to grow our core business and our market share. We have developed and successfully launched adjacent verticals, such as our Fintech services (see Item 4.B “Information on the Company—Business Overview—Our Business Operations—Financial Services Offerings”) and Ozon fresh, our expedited parcel delivery service for select products offered on our platform (see Item 4.B “Information on the Company—Business Overview—Our Business Operations—Ozon fresh”), as well as advertising and logistics services for sellers.

Our Business Operations

Marketplace

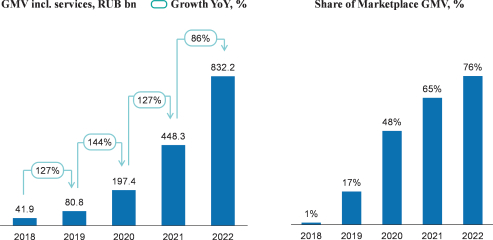

The OZON Marketplace is our core business, which enables thousands of sellers to offer a wide assortment of products to our buyers. We launched our Marketplace in September 2018, and it has since grown to account for 76% of our total GMV incl. services in the year ended December 31, 2022, while our Direct Sales business accounted for 19% of our total GMV incl. services in the year ended December 31, 2022. We offer sellers three logistics models, the fulfillment-by-Ozon (“FBO”) model, the fulfillment-by-seller (“FBS”) model and the Storefront model, to use individually or together, when selling their products on our Marketplace. Through these three models, our sellers are able to leverage our nationwide fulfillment and delivery infrastructure according to their business needs. Our FBO model is an attractive option for sellers who do not have their own storage facilities or are unable to fulfill orders by themselves. Our FBS model, in contrast, is suitable for sellers who do not want to supply, or would not benefit from supplying, inventory to our fulfillment centers, such as sellers who sell their products on several marketplaces simultaneously and do not want to commit their inventory to a single marketplace or sellers who sell heavy and bulky products, such as furniture. Our Storefront model allows sellers to use their own fulfillment and delivery capacities to deliver goods directly to customers, bypassing our fulfillment and delivery infrastructure altogether. Under all three models, we collect payments for each order made by our buyers and make aggregate payments, net of our marketplace commissions, to our sellers on a twice-monthly basis. Our Marketplace commission consists of a referral fee, which is a percentage of the total sales price of the product and, where applicable, other fees, such as delivery or storage fees collected from sellers. Our marketplace commissions increased to ₽106.4 billion in the year ended December 31, 2022 from ₽44.3 billion and ₽16.5 billion in the years ended December 31, 2021 and 2020, respectively.

54