As filed with the Securities and Exchange Commission on February 13, 2023

Registration No. 333-268811

UNITED

STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON D.C. 20549

TO

FORM

REGISTRATION

STATEMENT

UNDER THE SECURITIES ACT OF 1933

(Name of registrant as specified in its charter)

| 6531 | ||||

| (State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification No.) |

6101 Baker Road, Suite 200

Minnetonka, MN 55345

(952) 470-8888

(Address, including zip code, and telephone number,

including area code, or registrant’s principal executive offices)

Christopher Laurence,

CEO

Appreciate Holdings, Inc.

6101 Baker Road, Suite 200

Minnetonka, MN

(952) 470-8888

(Name, address, including zip code, and telephone number,

including area code, of agent for service)

Copies to:

Winthrop & Weinstine.

P.A.

Capella Tower, Suite 3500

Attention: Philip T. Colton

225 South Sixth Street

Minneapolis, MN 55402

Fax: (732) 395-4401

Approximate date of commencement of proposed sale to the public: From time to time after the effective date of this registration statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box. ☒

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If delivery of the Prospectus is expected to be made pursuant to Rule 434, check the following box. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer”, “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act:

| Large accelerated filer | ☐ | ☐ | ||

| Accelerated filer | ☐ | Smaller reporting company | ||

| Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act.

The Registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until this Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. Neither we nor the selling securityholder may sell these securities until the registration statement filed with the U.S. Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

PRELIMINARY PROSPECTUS

SUBJECT TO COMPLETION, DATED February 13, 2023

Appreciate Holdings, INC.

21,052,632 Shares of Class A Common Stock

This prospectus relates to the potential offer and sale from time to time by CF Principal Investments LLC (“Cantor” or the “Holder”) of up to 21,052,632 shares of our Class A Common Stock, par value $0.001 per share (the “Class A Shares” or the “Class A Common Stock”) of Appreciate Holdings, Inc. (“Appreciate,” the “Company,” “we,” “us,” or “our”), that have been or may be issued by us to the Holder pursuant to the Common Stock Purchase Agreement, dated as of May 17, 2022, by and between us and the Holder (the “Purchase Agreement”), establishing a committed equity facility (the “Facility”).

We are not selling any securities under this prospectus and will not receive any of the proceeds from the sale of our Class A Common Stock by the Holder. However, we may receive up to $100.0 million in aggregate gross proceeds from the Holder under the Purchase Agreement in connection with sales of our Class A Common Stock to the Holder pursuant to the Purchase Agreement after the date of this prospectus. In connection with the execution of the Purchase Agreement, we agreed to issue 1,052,632 Class A Shares (such shares, the “Commitment Shares”) to the Holder as consideration for its irrevocable commitment to purchase the Class A Shares at our election in our sole discretion, from time to time after the date of this prospectus, upon the terms and subject to the satisfaction of the conditions set forth in the Purchase Agreement. The purchase price per share that Cantor will pay for the Class A Shares purchased from us under the Purchase Agreement will equal 98% of the then current market price for the Class A Common Stock and will thus fluctuate based on the market price of our Class A Shares at the time we elect to sell shares to Cantor and, further, to the extent that the Company sells Class A Shares under the Facility, substantial amounts of Class A Shares could be issued and resold, which would cause dilution and may impact the Class A Common Stock stock price. See “The Committed Equity Financing” for a description of the Purchase Agreement and the Facility and “Selling Stockholder” for additional information regarding Cantor.

The shares of Class A Common Stock being offered for resale pursuant to this prospectus by the selling stockholder represent approximately 30.84% of shares of common stock outstanding of the Company as of January 23, 2023 (or 27.83% after giving effect to the issuance of shares upon exercise of outstanding public warrants and private placement warrants). As a percentage of our publicly-traded shares of Class A Common Stock, the shares of Class A Common Stock that can be sold pursuant to this Prospectus would constitute approximately 55.24% of such shares if all the shares offered hereby were sold. Given the substantial number of shares of Class A Common Stock being registered for potential resale by the selling securityholder pursuant to this prospectus, the potential sale of shares by the other selling stockholders, or the perception in the market that selling securityholders of a large number of shares intend to sell shares, could increase the volatility of the market price of our Class A Common Stock or result in a significant decline in the public trading price of our Class A Common Stock and could impair our ability to raise capital through the sale of additional equity securities. Even if our trading price is significantly below $10.00, the offering price for the units offered in PTIC II’s IPO, the selling stockholders may still have an incentive to sell shares of our Class A Common Stock because they will acquire shares at prices lower than the current trading price of our Class A Common Stock.

The Holder may offer, sell or distribute all or a portion of the Class A Shares hereby registered publicly or through private transactions at prevailing market prices or at negotiated prices. We will bear all costs, expenses and fees in connection with the registration of these shares, including with regard to compliance with state securities or “blue sky” laws. The timing and amount of any sale are within the sole discretion of the Holder. The Holder is an underwriter under the Securities Act of 1933, as amended (the “Securities Act”) and any profit on sale of the shares by them and any discounts, commissions or concessions received by them may be deemed to be underwriting discounts and commissions under the Securities Act. Although the Holder is obligated to purchase our shares of our Class A Common Stock under the terms of the Purchase Agreement to the extent we choose to sell such shares to it (subject to certain conditions), there can be no assurances that the Holder will sell any or all of the shares purchased under the Purchase Agreement pursuant to this prospectus. The Holder will bear all commissions and discounts, if any, attributable to its sale of shares of Class A Common Stock. See “Plan of Distribution (Conflict of Interest).”

Our Class A Common Stock is listed on The Nasdaq Global Market under the symbol “SFR.” Warrants to purchase 7,671,746 shares of our Class A Common Stock are listed on the Nasdaq Capital Market under the symbol “SFRWW.” On February 10, 2023, the last reported sale price of our Class A Common Stock was $1.62 per share. On such date, the last reported sale price of our Warrants was $0.07 per Warrant.

We are an “emerging growth company” under the federal securities laws and are subject to reduced public company reporting requirements.

Investing in our securities involves a high degree of risk. You should review carefully the risks and uncertainties described under the heading “Risk Factors” beginning on page 11 of this prospectus, and under similar headings in any amendment or supplements to this prospectus.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The date of this prospectus is , 2023.

TABLE OF CONTENTS

i

ABOUT THIS PROSPECTUS

This prospectus is part of a registration statement on Form S-1 that we filed with the Securities and Exchange Commission (the “SEC”) using a “shelf” registration process. Our registration of the securities covered by this prospectus does not mean that either we or the Holder will issue, offer or sell, as applicable, any of the securities registered hereunder. Under this shelf registration process, the Holder may, from time to time, sell the securities offered by it described in this prospectus. We will not receive any proceeds from the sale by the Holder of the securities offered by them described in this prospectus. However, we will receive proceeds from our sale to the Holder of up to 20,000,000 shares of Class A Common Stock, which will fluctuate based on the market price of our shares of Class A Common Stock at the time we elect to sell shares to Cantor pursuant to the terms of the Purchase Agreement, after the date of this prospectus.

Neither we nor the Holder have authorized anyone to provide you with any information other than that provided in this prospectus and any applicable prospectus supplement. Neither we nor the Holder can provide any assurance as to the reliability of any other information that others may give you. Neither we nor the Holder are making an offer of these securities in any jurisdiction where the offer is not permitted. You should not assume that the information in this prospectus, any applicable prospectus supplement is accurate as of any date other than the date of the applicable document. Since the date of this prospectus our business, financial condition, results of operations and prospects may have changed.

We may also provide a prospectus supplement or post-effective amendment to the registration statement to add information to, or update or change information contained in, this prospectus. You should read both this prospectus and any applicable prospectus supplement or post-effective amendment to the registration statement together with the additional information to which we refer you in the section of this prospectus entitled “Where You Can Find More Information.”

You should rely only on the information contained in this prospectus or in any prospectus supplements we may file. Neither we nor the Holder have authorized anyone to provide you with information different from, or in addition to, that contained in this prospectus or in any prospectus supplements we may file. The information contained in this prospectus or in any prospectus supplements we may file is current only as of their respective dates or on the date or dates that are specified in those documents. Our business, financial condition, results of operations and prospects may have changed since those dates.

Unless the context indicates otherwise, references in this prospectus to the “Company,” “Appreciate,” “we,” “us,” “our” and similar terms refer to Appreciate Holdings, Inc., a Delaware corporation, and its consolidated subsidiaries. References to “PTIC II” refer to PropTech Investment Corporation II, Inc, a Delaware corporation. References to “Renters Warehouse” refer to “RW National Holdings, LLC,” a Delaware limited liability company and references to “NewCo LLC” refer to Appreciate Intermediate Holdings, LLC, a Delaware limited liability company.

Unless otherwise indicated, information contained in this prospectus concerning our industry and the markets in which we operate is based on information from independent industry and research organizations, other third-party sources (including industry publications, surveys and forecasts), and management estimates. Management estimates are derived from publicly available information released by independent industry analysts and third-party sources, as well as data from our internal research, and are based on assumptions made by us upon reviewing such data and our knowledge of such industry and markets, which we believe to be reasonable. Although we believe the data from these third-party sources is reliable, we have not independently verified any third-party information. In addition, assumptions and estimates of the future performance of the industry in which we operate and our future performance are necessarily subject to uncertainty and risk due to a variety of factors, including those described in “Risk Factors” and “Cautionary Note Regarding Forward-Looking Statements.” These and other factors could cause results to differ materially from those expressed in the estimates made by the independent parties and by us.

ii

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This prospectus contains “forward-looking statements” within the meaning of Section 27A of the Securities Act and Section 21E of the Exchange Act. Our forward-looking statements include, but are not limited to, statements regarding our or our management team’s expectations, hopes, beliefs, intentions or strategies regarding the future. In addition, any statements that refer to projections, forecasts or other characterizations of future events or circumstances, including any underlying assumptions, are forward-looking statements. The words “anticipate,” “believe,” “continue,” “could,” “estimate,” “expect,” “intends,” “may,” “might,” “plan,” “possible,” “become,” “potential,” “predict,” “project,” “should,” “would,” “opportunity,” “mission,” “goal,” “positioned” and similar expressions may identify forward-looking statements, but the absence of these words does not mean that a statement is not forward-looking.

The forward-looking statements contained in this prospectus are based on our current expectations and beliefs concerning future developments and their potential effects on us taking into account information currently available to us. There can be no assurance that future developments affecting us will be those that we have anticipated. These forward-looking statements involve a number of risks, uncertainties (some of which are beyond our control) or other assumptions that may cause actual results or performance to be materially different from those expressed or implied by these forward-looking statements. These risks include, but are not limited to:

| ● | trends in the real estate industry, the real estate financing industry and Appreciate’s market size, including with respect to the potential total addressable market in the industry; |

| ● | Appreciate’s growth prospects; |

| ● | new product and service offerings Appreciate may introduce in the future; |

| ● | the price of Appreciate’s securities, including volatility resulting from changes in the highly competitive industry in which Appreciate operates and plans to operate, variations in performance across competitors, changes in laws and regulations affecting Appreciate’s business and changes in the combined capital structure; |

| ● | the ability to implement business plans, forecasts, and other expectations as well as identify and realize additional opportunities; and |

| ● | other risks and uncertainties indicated from time to time in filings made with the SEC. |

These risks are not exhaustive. New risk factors emerge from time to time and it is not possible for our management to predict all risk factors, nor can we assess the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements. Should one or more of these risks or uncertainties materialize, they could cause our actual results to differ materially from the forward-looking statements. Except as required by law, we undertake no obligation to update or revise any forward looking statements whether as a result of new information, future events or otherwise. You should not take any statement regarding past trends or activities as a representation that the trends or activities will continue in the future.

The forward-looking statements made by us in this prospectus and any accompanying prospectus supplement speak only as of the date of this prospectus and the accompanying prospectus supplement. Except to the extent required under the federal securities laws and rules and regulations of the SEC, we disclaim any obligation to update any forward-looking statement to reflect events or circumstances after the date on which the statement is made or to reflect the occurrence of unanticipated events. In light of these risks and uncertainties, there is no assurance that the events or results suggested by the forward-looking statements will in fact occur, and you should not place undue reliance on these forward-looking statements.

You may only rely on the information contained in this prospectus or that we have referred you to. We have not authorized anyone to provide you with different information. This prospectus does not constitute an offer to sell or a solicitation of an offer to buy any securities other than the common stock offered by this prospectus. This prospectus does not constitute an offer to sell or a solicitation of an offer to buy any common stock in any circumstances in which such offer or solicitation is unlawful. Neither the delivery of this prospectus nor any sale made in connection with this prospectus shall, under any circumstances, create any implication that there has been no change in our affairs since the date of this prospectus is correct as of any time after its date.

iii

PROSPECTUS SUMMARY

This summary highlights selected information contained elsewhere in this prospectus, and does not contain all of the information that you should consider before investing in our Class A Common Stock. This summary is qualified in its entirety by, and should be read in conjunction with, the more detailed information appearing elsewhere in this prospectus. You should read this entire prospectus carefully, including the information set forth in the sections titled “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our financial statements and related notes thereto included elsewhere in this prospectus before making an investment decision. Unless the context requires otherwise, references in this prospectus to “we,” “us,” “our,” “our company,” the “Company”, “Appreciate” or similar terminology refer to Appreciate Holdings, Inc.

Overview of the Company

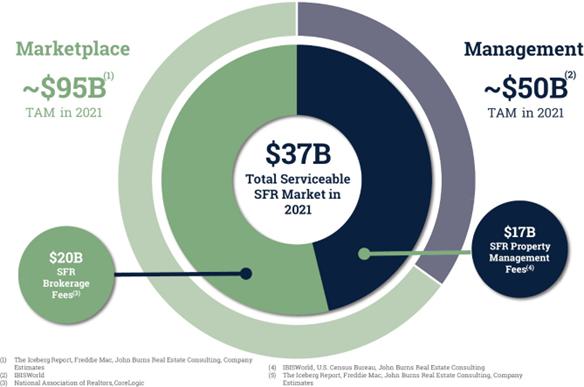

Appreciate Holdings, Inc. (“Appreciate” or the “Company”) is a single family rental (“SFR”) services company serving a diverse base of more than 12,000 individual and institutional investors through an end-to-end technology platform. With a focus on the services segment of the SFR industry, Appreciate operates an asset-light model and does not own SFR real estate. Instead, its platform provides SFR marketplace and management services to both individual and institutional investors. The Company and its franchise operators provide services across 42 locations in 20 states and the District of Columbia. In all of the Company’s locations, we are licensed as a real estate broker, which allows participation in the Multiple Listing Service. We and our franchise operators currently manage approximately 15,000 properties with a gross property value exceeding $4.0 billion.

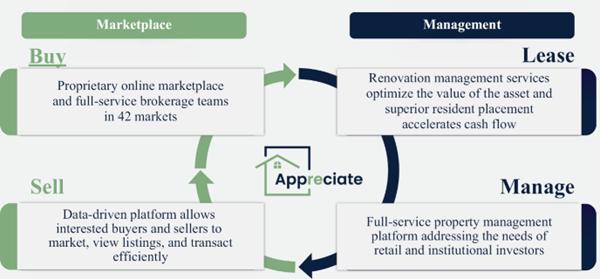

Appreciate aims to democratize SFR ownership by demystifying the end-to-end process of purchasing, owning and managing SFR real estate and bringing the experience closer to the experience of managing other types of investments. The Company accomplishes this by covering the entire lifecycle of a SFR investment through its two business segments: the Marketplace and the Management segments of the SFR market, both of which are described in more detail below. Appreciate’s end-to-end platform, which helps clients buy, lease, manage and sell SFR in one place, creates a strong and iterative network effect. Buyers on the Marketplace frequently become owners on the Management side and owners can sell their properties through the Marketplace.

Appreciate’s Marketplace and Management Segments

| ● | In our Marketplace segment, we assist investors with purchases and sales of SFR properties. For institutional investors looking to build a large, geographically diversified portfolio of high-quality properties, the Company’s acquisition platform leverages its national footprint and technology sophistication to facilitate rapid portfolio growth by targeting acquisitions in multiple markets simultaneously. With the systems and personnel infrastructure to facilitate the acquisition of more than $2.0 billion of SFR properties annually and a true end-to-end service with closed accountability loops ensuring a smooth transition from Marketplace to Management services, they allow institutional clients to fully focus on their growth plans. |

| ● | In Appreciate’s Management segment, the Company efficiently manages properties through an appropriate blend of centralized and decentralized resources. Appreciate’s scalable, centralized technology-based infrastructure supports local market operations with consistently executed resident screening, leasing operations, and customer service and maintenance coordination. Local on-the-ground teams in 42 markets handle operations that benefit from local presence and expertise, including property showings and tenant placement. Appreciate provides clients with visibility to all aspects of our management through transparent access to analytics and reporting. |

Background and Recent Developments

Consummation of the Business Combination

On November 29, 2022, Appreciate Holdings, Inc., a Delaware corporation (formerly known as PropTech Investment Corporation II, Inc., a Delaware corporation (“PTIC II”)), consummated the previously announced business combination transactions with Renters Warehouse.

1

Immediately after giving effect to the business combination transactions the following equity securities of Appreciate were issued and outstanding: (i) 15,689,094 of Class A Common Stock, (ii) 31,200,000 shares of Class B Common Stock, issued to owners of Renters Warehouse as consideration in the business combination, (iii) 7,671,746 warrants to purchase Class A Common Stock issued to holders of the publicly trading Class A Shares in connection with PTIC II initial public offering that remain unexercised (each, a “Public Warrant”), (iv) 4,833,333 shares of Class A Common Stock issuable to PTIC II’s sponsor upon exercise of warrants to purchase Appreciate Class A Common Stock issued in a private placement (each, a “Private Warrant”), and (v) shares of Class A Common Stock that may be issued to certain service providers pursuant to agreements entered into on or about November 29, 2022 in connection with the business combination transaction (the “Service Provider Agreements”). After the Closing Date, PTIC II’s Class A Common Stock and PTIC II’s warrants and units ceased trading on The Nasdaq Capital Market. Class A Common Stock and Appreciate’s Public Warrants commenced trading on The Nasdaq Global Market and the Nasdaq Capital Market under the symbols “SFR” and “SFRWW,” respectively, on November 30, 2022.

Appreciate is continuing the existing business operations of Renters Warehouse as a publicly traded company.

Incremental Financings

Cantor Equity Financing

On May 17, 2022, PTIC entered into a Common Stock Purchase Agreement (the “Purchase Agreement”) with CF Principal Investments LLC (“Cantor” or the “Holder”) related to a committed equity facility (the “Facility”). Pursuant to the Purchase Agreement, Appreciate has the right, from time to time at its option to sell to Cantor up to $100.0 million in aggregate gross purchase price of newly issued shares of Class A Common Stock subject to certain conditions and limitations set forth in the Purchase Agreement.

Sales of Class A Shares to Cantor under the Purchase Agreement, and the timing of any sales, will be determined by Appreciate from time to time in its sole discretion and will depend on a variety of factors, including, among other things, market conditions, the trading price of the Class A Common Stock and determinations by Appreciate regarding the use of proceeds of such Class A Shares, and will be subject to the conditions set forth in the Purchase Agreement (see “The Committed Equity Financing”). The net proceeds from any sales under the Purchase Agreement will depend on the frequency with, and prices at, which the Class A Shares are sold to Cantor. Appreciate expects to use the proceeds from any sales under the Purchase Agreement for working capital and general corporate purposes, including servicing our ongoing debt and service provider obligations.

Upon the initial satisfaction of the conditions to Cantor’s obligation to purchase Class A Shares set forth in the Purchase Agreement (the “Commencement”), including that a registration statement registering the resale by Cantor of the common stock under the Securities Act, purchased pursuant to the Purchase Agreement (the “Cantor Resale Registration Statement”) is declared effective by the SEC and a final prospectus relating thereto is filed with the SEC, and subject to certain ongoing conditions, Appreciate will have the right, but not the obligation, from time to time at its sole discretion until no later than the first day of the month next following the 36-month period from and after the date that the Cantor Resale Registration Statement is declared effective, to direct Cantor to purchase up to a specified maximum amount of Class A Common Stock as set forth in the Purchase Agreement by delivering written notice to Cantor prior to the commencement of trading on any trading day. The purchase price of the Class A Common Stock that Appreciate elects to sell to Cantor pursuant to the Purchase Agreement will be 98% of the VWAP of the Class A Shares during the applicable purchase date on which Appreciate has timely delivered written notice to Cantor directing it to purchase Class A Common Stock under the Purchase Agreement; accordingly, the purchase price per share that Cantor will pay for the Class A Shares purchased from us under the Purchase Agreement will fluctuate based on the market price of our Class A Shares at the time we elect to sell shares to Cantor.

In connection with the execution of the Purchase Agreement, Appreciate agreed to issue on Commencement a number of Class A Shares equal to the quotient obtained by dividing (i) $2,000,000 and (ii) the closing price of the Class A Shares on the earlier to occur of (x) the second trading day prior to the filing of the initial registration statement relating to Facility and (ii) the date that Cantor sends an invoice to Appreciate for the commitment fee as consideration for its irrevocable commitment to purchase the Class A Shares upon the terms and subject to the satisfaction of the conditions set forth in the Purchase Agreement. In addition, pursuant to the Purchase Agreement, Appreciate has agreed to reimburse Cantor for certain expenses incurred in connection with the Facility. Issuances of Class A Shares under the Purchase Agreement are subject to a beneficial ownership “blocker” provision, preventing issuances of Class A Common Stock resulting in ownership in excess of 4.99% beneficial ownership of shares of Appreciate’s common stock by Cantor and its affiliates. The Purchase Agreement contains customary representations, warranties, conditions and indemnification obligations by each party. The use of the Facility is subject to certain conditions, including the effectiveness of the Cantor Resale Registration Statement. Therefore, funds from the $100 million gross purchase price will not be immediately available to Appreciate upon the business combination, and there can be no assurances that such purchase price will ever become available.

2

The representations, warranties and covenants contained in the Purchase Agreement were made only for the purposes of the Purchase Agreement and as of specific dates, were solely for benefit of the parties to such agreement and are subject to certain important limitations. Appreciate has the right to terminate the Purchase Agreement at any time after the Commencement, at no cost or penalty upon 3 trading days’ prior written notice.

Although Appreciate cannot predict the number of Class A Shares that will actually be issued in connection with any sales under the Facility, it is possible that such issuances may result in large numbers of shares being sold. For example, if the Facility is used in its entirety for $100.0 million, the number of shares to be issued at a trading price of each of $13.00 per share, $6.00 per share, or $3.00 per share would be 7.69 million shares, 16.67 million shares or 33.33 million shares, respectively. To the extent the Company sells Class A Shares under the Facility (along with other issuances and resales of Class A Shares including shares subject to our public and private warrants, as well as the resale of Class A Shares by other holders, and pursuant to the Company’s equity incentive plan or otherwise), substantial amounts of Class A Shares could be issued and resold, which would cause dilution and represent a significant percentage of our public float and, further, may result in substantial decreases to the Company’s stock price. See “Risk Factors—Risks Related to the Committed Equity Financing—Future resales and/or issuances of Class A Shares, including pursuant to this prospectus may cause the market price of our shares to drop significantly” and “The Committed Equity Financing”.

The shares of Class A Common Stock being offered for resale pursuant to this prospectus by the selling stockholder represent approximately 30.84% of shares outstanding of the Company as of January 23, 2023 (or 27.83% after giving effect to the issuance of shares upon exercise of outstanding public warrants and private placement warrants). As a percentage of our publicly-traded shares of Class A Common Stock, the shares of Class A Common Stock that can be sold pursuant to this Prospectus would constitute approximately 55.24% of such shares if all the shares offered hereby were sold. Given the substantial number of shares of Class A Common Stock being registered for potential resale by the selling securityholder pursuant to this prospectus, the potential sale of shares by the other selling stockholders, or the perception in the market that selling securityholders of a large number of shares intend to sell shares, could increase the volatility of the market price of our Class A Common Stock or result in a significant decline in the public trading price of our Class A Common Stock. Even if our trading price is significantly below $10.00, the offering price for the units offered in PTIC II’s IPO, the selling stockholders may still have an incentive to sell shares of our Class A Common Stock because they will acquire shares at prices lower than the current trading price of our Class A Common Stock.

To the extent that Appreciate sells Class A Shares under the Facility, substantial amounts of Appreciate’s Class A Common Stock will be issued, which would cause dilution and may result in substantial decreases to Appreciate’s stock price. See “Risk Factors—Risks Related to Ownership of Appreciate Securities.” The selling stockholder will be able to sell all shares acquired pursuant to the Facility for so long as the registration statement to which this prospectus forms a part is available for use.

Forward Purchase Agreement

In November 2022, PTIC II and Vellar Opportunity Fund SPV LLC – Series 9 (“Vellar”), entered into a Forward Purchase Agreement for an OTC Equity Prepaid Forward Transaction. PTIC became aware of Vellar though an acquaintance with Brandon Sun, a Managing Director at Vellar’s affiliate Cohen & Company. PTIC came to know Mr. Sun through Mr. Sun’s prior role at Deutsche Bank. Following discussions that began in July 2022, Mr. Sun introduced PTIC II to Mssrs. Solomon Cohen and John Salemi, also of Cohen & Company, to discuss their SPAC-related financial product offerings. Preliminary discussions were halted based on advice from Vellar’s counsel, and substantive discussions and negotiations began after the PTIC II redemption date.

3

Subsequent to entering into the Forward Purchase Agreement with Vellar, the Company and the Renters Warehouse entered into separate assignment and novation agreements with Polar Multi-Strategy Master Fund (“Polar”) and Meteora Special Opportunity Fund I, LP, Meteora Select Trading Opportunities Master, LP and Meteora Capital Partners, LP (collectively “Meteora”), pursuant to which Vellar assigned its obligations as to 3,000,000 shares of the Class A Common Stock to be purchased to each of Polar and Meteora. Vellar, Polar and Meteora are sometimes referred to as the “FPA Parties.”

Pursuant to the terms of the agreement, the FPA Parties intended, but were not obligated, to purchase in the open market (through a broker) shares of Class A Common Stock. The purchases were to occur after the date of the agreement and after the expiration of PTIC II’s redemption deadline for holders to redeem shares in connection with the Business Combination. The maximum amount to be purchased was 9,000,000 shares of PTIC II Class A Common Stock; provided that none of the FPA Parties can beneficially own greater than 9.9% of the issued and outstanding shares of Class A Common Stock on a post-Business Combination pro forma basis. The price to be paid for the shares was the redemption price or as subsequently determined, approximately $10.08 per Share (based on an amount of $231,870,089.06 held in the Trust Account). The FPA Parties agreed to waive any redemption rights with respect to any shares of PTIC II Class A Common Stock acquired.

Among the reasons that Company entered into the Forward Purchase Agreement was to reduce the number of redemptions in connection with the Business Combination to help ensure that, following completion of the Business Combination, the Company’s stockholder base would comply with NASDAQ listing standards. Specifically, the Company was concerned that if it did not enter into the Forward Purchase Agreement, given high SPAC redemptions, the Company would likely have not met NASDAQ’s requirement for the market value of unrestricted publicly-held shares and the required number of round lot holders. The waiver also reduced the number of shares of PTIC II Class A Common Stock redeemed in connection with the Business Combination, which reduction could alter the perception of the potential strength of the Business Combination. In addition, the FPA Parties advanced approximately $5.0 million to the Company for amounts due the Company under the Forward Purchase Agreement, and Appreciate is eligible to receive an additional approximately $4.0 million on the date that the SEC declares a registration statement registering the resale of all shares held by the FPA Parties effective.

As contemplated by the Forward Purchase Agreement, the FPA Parties collectively purchased approximately 8.8 million shares of Class A Common Stock directly from stockholders prior to the closing of the Business Combination. The average purchase price of the shares purchased was $10.08 per share. The FPA Parties waived their redemption rights with respect to the acquired shares. One business day following the closing of the Business Combination, Appreciate paid approximately $89.1 million from the cash held in the trust account to Vellar, Polar and Meteora for the shares purchased, approximately $5.0 million for additional share consideration (i.e., the value of the 499,999 shares issued as consideration), and approximately $0.4 million in related expense amounts.

To partially recoup the approximately $5.0 million advanced to the Company, 279,915 shares of Class A Common Stock have been sold by an FPA Party other than Vellar and Polar prior to the date of this Prospectus. Given that payments from cash held in the trust account were forwarded to the FPA Parties for shares purchased, the Company estimates that the capital at risk by the FPA Parties is equal to the amount of the advances to Appreciate, less proceeds from the sales described above. As of the date of this Prospectus, the Company believes that the amount of capital at risk is approximately $4.2 million, which would increase to $8.1 million if the additional amount due to the Company on registration were paid.

Prior to the Maturity Date of the FPA (three years from the date of the agreement), Vellar, Polar or Meteora may, in their sole discretion, sell some or all of the shares acquired. For any share sold, Appreciate will receive an amount defined as the Reset Price. Based on trading in the Company’s Class A Common Stock, the Reset Price will now not be higher than the floor of $5.00 per share. It could adjust to a lower price if any securities (or securities convertible into shares of Class A Common Stock) are issued or sold by the Company at a price lower than $5.00. At a Reset Price of $5.00, the maximum amount the Company could receive from sales under the FPA is approximately $42.8 million.

Based on the trading levels of the Company’s Common Stock, a Trigger Event has occurred under the agreement that gives the FPA Parties the right to accelerate the Maturity Date. However, as of the date of this Prospectus, none of the FPA Parties has elected to do so. At the Maturity Date and if required by an FPA Party, Appreciate is required to purchase from an FPA Party any unsold shares of Class A Common Stock for consideration in cash or, at the sole discretion of the Company, shares of Class A Common Stock (the “Maturity Consideration”). The Maturity Consideration is $1.75 per share, although the amount rises to $2.00 per share if the Company has failed to register the shares. Based on $1.75 per share amount and the remaining shares held by the FPA Parties, the total Maturity Consideration that would be owed is approximately $15.0 million. If shares are used to satisfy the Maturity Consideration, they are valued at the volume-weighted average price for 30 trading days prior to the Maturity Date. If the shares are not registered, the FPA contains provisions for providing additional penalty shares which are returned once the shares are registered. Based on the trailing 30 day VWAP, if the $1.75 consideration were paid in shares and all FPA Parties elected to trigger the Maturity Date, the Company would be required to issue an aggregate of approximately 9.4 million shares to the FPA Parties. A required purchase of unsold shares would adversely affect the Company’s liquidity, attempts to raise additional capital and the Company’s ability to fund operations on a prospective basis.

4

Deferred Service Provider Agreements

Effective as of November 29, 2022, a number of service providers to PTIC II and Renters Warehouse entered into agreements to defer amounts due to these service providers (the “Deferred Fees and Expenses”) until such time when sufficient funds become available to Appreciate to pay such Deferred Fees and Expenses in cash (each, a “Deferred Agreement,” and collectively, the “Deferred Agreements”). The amounts of the Deferred Fees and Expenses for the service providers are set forth below:

| Provider | Deferred Fees and Expenses | Additional Agreements(1) | ||||||

| Gateway Investor Relations | $ | 40,000 | NA | |||||

| Northland Securities, Inc. | $ | 6,005,000 | (2) | |||||

| Northern Pacific Group | $ | 5,226,528 | NA | |||||

| HC PropTech Partners II, LLC | $ | 317,500 | NA | |||||

| Kirkland & Ellis (“K&E”) | $ | 7,700,000 | (2) | |||||

| McKinsey & Company | $ | 2,700,000 | Deferred Fees and Expenses accrue interest at the rate of 1% per month until the date of payment. | |||||

| D.A. Davidson | $ | 750,000 | The Deferred Fees and Expenses are due June 30, 2023. | |||||

| Moelis & Company LLC | $ | 3,750,000 | (2)(3) | |||||

| MKM Partners LLC | $ | 300,000 | NA | |||||

| (1) | No Deferred Other Advisor Fee may be paid in cash until K&E has received (a) the K&E Closing Cash Fee, (b) at least 50% of the proceeds from any committed equity facility (including pursuant to the Purchase Agreement) (each, a “CEF”) and (c) in respect of any payments other than in connection with a CEF, a pro rata portion of the then-remaining K&E Remainder Fee is paid, determined by reference to the then-remaining amount of the K&E Remainder Fee and the then-remaining amounts of the Deferred Other Advisor Fees, in each case, within ten (10) business days. Except to the extent that any unpaid K&E Remainder Fee has been converted to Appreciate Class A Common Stock, such balance shall bear interest at the rate of eight percent (8%) per annum, compounded quarterly, and such interest shall be due and payable in full at such time as the unpaid K&E Fees are otherwise paid or payable. |

| (2) | Within ten (10) business days of the effective date of the first resale registration statement on Form S-1 filed by Appreciate, Appreciate is required to pay (a) to K&E, $2,000,000 USD (the “K&E Closing Cash Fee”), (b) to Cantor Fitzgerald & Co, $2,200,000 USD, (c) to Moelis & Company LLC (“Moelis”) $2,250,000 USD (the “Moelis Deferred Cash Fee”) and (d) to Northland Securities Inc., $300,000 USD, respectively, with each such amount to be paid in cash simultaneously. With respect to the remaining $5,700,000 in Deferred Fees and Expenses due to K&E (the “K&E Remainder Fee”), fifty percent (50%) of the proceeds received in connection with any CEF shall be used to pay the K&E Remainder Fee, promptly, and in any event within ten (10) business days of receipt of such proceeds and in priority to any then-unpaid expenses due and payable in cash to Appreciate’s advisors, equityholders or affiliates (the “Deferred Other Advisor Fees”) in connection with the Business Combination. |

| (3) | Moelis shall receive a non-refundable fee of $2,250,000 (the “Moelis Deferred Cash Fee”) upon the effectiveness of any registration statement (the “First Effectiveness Date”). Moelis shall also receive Appreciate Class A Common Stock (the “Deferred stock Consideration”) delivered at the option of Moelis, either (i) within four business days of the First Effectiveness Date equal to $1,500,000, divided by daily VWAP price over the fewer of (a) 20 scheduled trading days ending on the trading day immediately prior to the First Effectiveness Date and (b) all of the scheduled trading days beginning at Closing and ending the trading day immediately prior to the First Effectiveness Date or (ii) promptly upon on April 1, 2023 equal to $1,500,000 divided by the daily VWAP price over 20 scheduled trading days ending on the trading day immediately prior to April 1, 2023. Appreciate agrees to keep the registration statement (and/or refile a new registration statement) effective until the earlier of two years or until Moelis resells pursuant to the registration statement all of the Appreciate Class A Common Stock delivered to it or until any unsold Appreciate Class A Common Stock delivered to Moelis is freely tradeable under Rule 144. If either the Moelis Closing Cash Fee or the Moelis Deferred Cash Fee is not paid at the agreed-upon times described herein, a total of $5,860,000 shall be due and payable by Appreciate to Moelis immediately. |

5

Summary Risk Factors

The following is a summary of select risks and uncertainties that could materially adversely affect us and our business, financial condition and results of operations. Before you invest in our Class A Shares, you should carefully consider all the information in this prospectus, including matters set forth under the heading “Risk Factors,” immediately following this prospectus summary. These risks include the following, among others:

Risks Related to the Committed Equity Financing

| ● | It is not possible to predict the actual number of shares of Class A Common Stock, if any, we will sell under the Purchase Agreement to Cantor, or the actual gross proceeds resulting from those sales. |

| ● | Investors who buy Class A Shares from the Holder at different times will likely pay different prices. |

| ● | We may use proceeds from sales of our Class A Common Stock made pursuant to the Purchase Agreement in ways with which you may not agree or in ways which may not yield a significant return. |

| ● | Future resales and/or issuances of Class A Shares, including pursuant to this prospectus may cause the market price of our shares to drop significantly. |

| ● | Cantor will have an incentive to sell shares acquired under the Facility because such shares will be acquired at a discount to the market price. |

| ● | Shares sold pursuant to this Prospectus constitute a significant percentage of our outstanding Common Stock and a considerable percentage of our public float. | |

| ● | Sales of a substantial number of shares of Class A Common Stock in the public market pursuant to the Cantor Facility and/or by our other existing securityholders, or the perception that those sales might occur, could result in a significant decline in the public trading price of our Class A Common Stock, would cause dilution and could impair our ability to raise capital through the sale of additional equity securities. |

Risks Related to Our Business and Operations

| ● | We have a relatively short operating history in a rapidly evolving industry, which makes it difficult to evaluate our future prospects and may increase the risk that we will not be successful. As our costs increase, we may not be able to generate sufficient revenue to maintain profitability in the future. We also have a history of losses and may not achieve profitability in the future. |

| ● | If we do not successfully develop and deploy new software, platform features or services to address the needs of our clients, our business, financial condition, and results of operations could suffer. |

| ● | If we fail to retain our existing clients and consumers or to acquire new clients and consumers in a cost-effective manner, our revenue may decrease and our business may be harmed. |

| ● | If we fail to expand effectively into new markets, our revenue and business will be adversely affected. |

| ● | If we fail to manage our growth effectively, our brand, business and operating results could be harmed. The growth of our business depends on our ability to accurately predict trends in the real estate industry, successfully offer new services, improve existing services and expand into new markets. |

| ● | If we are unable to recruit, train, retain and motivate key personnel, we may not achieve our business objectives. |

| ● | If our current marketing model is not effective in attracting new clients, we may need to employ higher-cost sales and marketing methods to attract and retain clients, which could adversely affect our profitability. |

| ● | We may be unable to scale and adapt our existing technology and network infrastructure in a timely or effective manner to ensure that our platform is accessible, which would harm our reputation, business and operating results. |

6

| ● | Interruptions to, or perceived errors, failures, or bugs in our platform and other cyber-events affecting our platform or our systems could adversely affect our operating results and growth prospects. |

| ● | The impact of global, regional or local economic and market conditions or catastrophic events, including health crises, may adversely affect our business, operating results and financial condition. |

| ● | Fluctuations in our quarterly and annual operating results may adversely affect our business and prospects. |

| ● | Investors are cautioned not to rely on outdated financial projections. |

| ● | We may improve our products and solutions in ways that forego short-term gains. |

| ● | We are subject to a variety of standards, governmental laws, regulations and other legal obligations and any actual or perceived failure to comply with such obligations could harm our business. Changes to such standards, laws, regulations and other obligations may have material adverse effect on our business, cash flow, financial condition or operating results. |

| ● | Future investments in our growth strategy, including acquisitions, could disrupt our business and adversely affect our operating results, financial condition and cash flows. |

| ● | The terms of the agreements governing our funding, our service provider obligations and existing defaults under our debt may restrict our operations. |

| ● | We will need to raise additional capital, which may not be available on favorable terms, if at all, causing dilution to our stockholders, restricting our operations or adversely affecting our ability to operate our business. We may be unable to obtain additional financing to fund our operations or growth. |

| ● | We have obligations secured by a security interest in substantially all of our assets; in the event of a default that is not waived, the debtholders could foreclose on, liquidate and/or out take possession of our assets. |

| ● | We may be subject to potential adverse tax consequences both domestically and in foreign jurisdictions and we may not be able to utilize any net operating loss and tax credit carryforwards. |

| ● | Changes in accounting standards or other factors could negatively impact our future effective tax rate. |

| ● | Certain taxing authorities may successfully assert that Appreciate should have collected or that in the future Appreciate should collect sales and use or similar taxes for certain services which could adversely affect our results of operations. |

Additional Risks Related to the Real Estate Industry

| ● | Our success depends on general economic conditions, the health of the U.S. real estate industry generally, and risks generally incident to the ownership and leasing of single-family rental real estate, and our business may be negatively impacted by economic and industry downturns, including seasonal and cyclical trends, and volatility in the single-family rental real estate lease market. |

| ● | Our marketplace faces significant competition with larger established players. |

Risks Related to Appreciate’s Intellectual Property

| ● | We may in the future be, subject to disputes and assertions by third parties with respect to alleged violations of intellectual property rights. These disputes could be costly to defend and could harm our business and operating results. |

| ● | Some of our solutions contain open source software, which may pose particular risks to our proprietary software and solutions. |

| ● | The success of our business heavily depends on our ability to protect and enforce our intellectual property rights. |

7

Risks Related to Our Securities and Certain Tax Matters

| ● | The price of our securities may be volatile. |

| ● | We do not intend to pay cash dividends for the foreseeable future. |

| ● | We are subject to securities and other general litigation, which is expensive and could divert management attention. |

| ● | The issuance of our Class A Shares in connection with the Service Provider Agreements and upon exchange of the Class B Common Stock could cause substantial dilution, which could materially affect the trading price of our Class A Shares. |

| ● | A significant portion of our total outstanding shares may be sold into the market in the near future, including the shares being registered for resale pursuant to this prospectus and resales of our Class A Common Stock pursuant to the forward purchase agreement and the committed equity facility and exchange of the Class B Common Stock issued in connection with the business combination transactions. This could cause the market price of our Class A Shares to drop significantly, even if our business is doing well. The selling securityholder will be able to sell all of their shares for so long as the registration statement of which this prospectus is a part is available for use. |

| ● | Future resales and/or issuance of shares of Class A Common Stock may cause the market price of our shares to drop significantly. |

| ● | If securities or industry analysts do not publish or cease publishing research or reports about us, our business, or our market, or if they change their recommendations regarding our common stock adversely, the price and trading volume of our Class A Common Stock could decline. |

| ● | We may amend the terms of the public and private warrants in a manner that may be adverse to holders with the approval by the holders of at a majority of then outstanding public or private warrant, respectively. As a result, the exercise price of warrants could be increased, the exercise period could be shortened, the exercise period decreased and the number of Class A Shares purchasable upon exercise of a warrant could be decreased, all without warrant holder approval. |

| ● | We are an emerging growth company within the meaning of the Securities Act, and if we take advantage of certain exemptions from disclosure requirements available to emerging growth companies, this could make our securities less attractive to investors and may make it more difficult to compare our performance with other public companies. |

| ● | We have and will continue to incur increased costs as a result of operating as a public company and our management has and will continue to devote a substantial amount of time to new compliance initiatives. |

| ● | Our failure to timely and effectively implement controls and procedures required by Section 404(a) of the Sarbanes-Oxley Act could have a material adverse effect on our business. |

| ● | Anti-takeover provisions in our certificate of incorporation and bylaws and under Delaware law could delay or prevent a change in control, limit the price investors may be willing to pay in the future for our Class A Shares and could entrench management. |

| ● | Our largest stockholders and certain members of our management own more than a majority of our outstanding common stock and are able to exert significant control over matters subject to stockholder approval. |

| ● | Future sales and issuances of our Class A Common Stock, including pursuant to our equity incentive and other compensatory plans, will result in additional dilution of the percentage ownership of our stockholders and could cause our share price to fall. |

8

Corporate Information

We were originally formed on August 6, 2020 under the name “PropTech Investment Corporation II,” as a blank check company incorporated in the state of Delaware, incorporated for the purpose of effecting a merger, amalgamation, share exchange, asset acquisition, share purchase, reorganization or similar business combination with one or more businesses. On November 29, 2022, we completed the previously announced business combination transactions with Renters Warehouse and we changed our name to Appreciate Holdings, Inc.

Our principal executive office is located at 6101 Baker Road, Suite 200, Minnetonka, Minnesota 55345. Our telephone number is (952) 470-8888. Our website address is www.appreciate.rent. Information contained on our website is not a part of this prospectus, and the inclusion of our website address in this prospectus is an inactive textual reference only.

Legal Proceedings

From time to time, we may become involved in legal or regulatory proceedings arising in the ordinary course of our business. We do not currently, however, expect such legal proceedings to have a material adverse effect on our business, operating results or financial condition. However, depending on the nature and timing of a given dispute, an unfavorable resolution could materially affect our current or future results of operations or cash flows.

Some of these claims, lawsuits and other proceedings may involve highly complex issues that are subject to substantial uncertainties and could result in damages, fines, penalties, non-monetary sanctions, or relief. We recognize provisions for claims or pending litigation when we determine that an unfavorable outcome is probable and the amount of loss can be reasonably estimated. Due to the inherent uncertain nature of litigation, the ultimate outcome or actual cost of settlement may materially vary from estimates. Currently, although we are parties to a number of legal proceedings, individually and collectively we do not believe that these proceedings are material to our operations. See “Business – Legal Proceedings” for more information.

Smaller Reporting Company

We are a “smaller reporting company” and will remain a smaller reporting company if either (i) the market value of our stock held by non-affiliates was less than $250 million as of the last business day of our most recently completed second fiscal quarter, or (ii) our annual revenue was less than $100 million during our most recently completed fiscal year and the market value of our stock held by non-affiliates was less than $700 million as of the last business day of our most recently completed second fiscal quarter. We intend to rely on exemptions from certain disclosure requirements that are available to smaller reporting companies, such as reduced disclosure obligations regarding executive compensation in this prospectus and our periodic reports and proxy statements. For so long as we remain a smaller reporting company, we are permitted and intend to rely on exemptions from certain disclosure and other requirements that are applicable to other public companies that are not smaller reporting companies.

Emerging Growth Company

Section 102(b)(1) of the Jumpstart Our Business Startups Act of 2012 (the “JOBS Act”) exempts emerging growth companies from being required to comply with new or revised financial accounting standards until private companies (that is, those that have not had a registration statement under the Securities Act declared effective or do not have a class of securities registered under the Exchange Act) are required to comply with the new or revised financial accounting standards. The JOBS Act provides that a company can elect to opt out of the extended transition period and comply with the requirements that apply to non-emerging growth companies but any such an election to opt out is irrevocable. We have elected not to opt out of such extended transition periods which means that when a standard is issued or revised and it has different application dates for public or private companies, we, as an emerging growth company, can adopt the new or revised standard at the time private companies adopt the new or revised standard. This may make comparison of Appreciate’s financial statements with those of another public company that is neither an emerging growth company nor an emerging growth company that has opted out of using the extended transition period difficult or impossible because of the potential differences in accounting standards used.

9

THE OFFERING

| Issuer | Appreciate Holdings, Inc. | |

| Common Shares offered by the Holder | Up to 21,052,632 shares of Class A Common Stock, consisting of: | |

| ● | the Commitment Shares, which are the 1,052,632 shares of Class A Common Stock that we have issued to Cantor in consideration of its irrevocable commitment to purchase Class A Shares at our election under the Purchase Agreement; and | |

| ● | up to 20,000,000 shares of Class A Common Stock consisting of Class A Shares that we may elect, in our sole discretion, to issue and sell to Cantor, from time to time from and after the Commencement Date (as defined below) under the Purchase Agreement. | |

| Use of Proceeds | We will not receive any proceeds from any sale of shares of Class A Common Stock by the Holder. However, we may receive up to $100.0 million in aggregate gross proceeds from the Holder under the Purchase Agreement in connection with sales of our Class A Common Stock to the Holder pursuant to the Purchase Agreement after the date of this prospectus. We intend to use any proceeds from the Facility for working capital and general corporate purposes, including servicing our ongoing debt and service provider obligations. See “Use of Proceeds.” | |

| Market for Class A Common Stock and Warrants | The Class A Shares are currently traded on The Nasdaq Global Market under the symbol “SFR.” The Warrants are currently traded on the NASDAQ Capital Market under the symbol “SFRWW.” | |

| Conflict of Interest | Cantor is an affiliate of Cantor Fitzgerald & Co. (“CF&CO”) a FINRA member. CF&CO is expected to act as an executing broker for the sale of the Class A Shares sold by Cantor pursuant to the Committed Equity Financing. | |

| The receipt by Cantor of all the proceeds from sales of Class A Common Stock to the public made through CF&CO results in a “conflict of interest” under Financial Industry Regulatory Authority, Inc. (“FINRA”) Rule 5121. Accordingly such sales will be conducted in compliance with FINRA Rule 5121. See “Plan of Distribution (Conflict of Interest).” | ||

| Risk Factors | See “Risk Factors” and other information included in this prospectus for a discussion of factors you should consider before investing in our securities. | |

Outstanding Shares of Common Stock

48,257,226 shares of Company common stock were issued and outstanding as of January 23, 2023, which calculation includes (i) 17,057,226 shares of the Company’s Class A Common Stock and (ii) 31,200,000 shares of the Company’s Class B Common Stock. Such amount does not include shares of Class A Common Stock issuable on exercise of warrants or options.

For additional information concerning the offering, see “Plan of Distribution”.

10

RISK FACTORS

Our business involves a high degree of risk. You should carefully consider the risks described below, together with the other information contained in this prospectus, including our condensed consolidated financial statements and the related notes appearing elsewhere in this prospectus, as well as the risks, uncertainties and other information set forth in the reports and other materials filed or furnished by us with the SEC. We cannot assure you that any of the events discussed in the risk factors below will not occur. These risks could have a material and adverse impact on our business, prospects, results of operations, financial condition and cash flows. If any such events were to happen, the trading shares of our Class A Shares could decline, and you could lose all or part of your investment.

Risks Related to the Committed Equity Financing

It is not possible to predict the actual number of shares of Class A Common Stock, if any, we will sell under the Purchase Agreement to Cantor, or the actual gross proceeds resulting from those sales. The issuance of a significant number of shares of Class A Common Stock would cause dilution to existing stockholders.

On May 17, 2022, we entered into the Purchase Agreement with Cantor, pursuant to which Cantor has committed to purchase up to $100.0 million of our shares of Class A Common Stock, subject to certain limitations and conditions set forth in the Purchase Agreement. The Class A Shares that may be issued under the Purchase Agreement may be sold by us to Cantor at our discretion from time to time until the first day of the month next following the 36-month period commencing on the date of this prospectus.

Sales of our Class A Common Stock, if any, to Cantor under the Purchase Agreement will depend upon market conditions and other factors to be determined by us, as well as the satisfaction of certain conditions set forth in the Purchase Agreement. We may ultimately decide to sell to Cantor all, some or none of the shares of Class A Common Stock that may be available for us to sell to Cantor pursuant to the Purchase Agreement.

Because the purchase price per share of Class A Shares to be paid by Cantor for the shares of Class A Common Stock that we may elect to sell to Cantor under the Purchase Agreement, if any, will fluctuate based on the market prices of our shares of Class A Common Stock at the time we elect to sell shares to Cantor pursuant to the Purchase Agreement, if any, it is not possible for us to predict, as of the date of this prospectus and prior to any such sales, the number of Class A Shares that we will sell to Cantor under the Purchase Agreement, the purchase price per share that Cantor will pay for shares of Class A Common Stock purchased from us under the Purchase Agreement, or the aggregate gross proceeds that we will receive from those purchases by Cantor under the Purchase Agreement.

Although the Purchase Agreement provides that we may, in our discretion, from time to time after the date of this prospectus and during the term of the Purchase Agreement, direct Cantor to purchase our shares of Class A Common Stock from us in one or more purchases under the Purchase Agreement, for a maximum aggregate purchase price of up to $100.0 million, only 20,000,000 Class A Shares for potential purchase by Cantor are being registered for resale under the registration statement (excluding the Commitment Shares) that includes this prospectus. However, because the market prices of our shares of Class A Common Stock may fluctuate from time to time after the date of this prospectus and, as a result, the actual purchase prices to be paid by Cantor for our shares of Class A Common Stock that we direct it to purchase under the Purchase Agreement, if any, also may fluctuate significantly based on the market price of our shares of Class A Common Stock.

If we decide to issue and sell to Cantor under the Purchase Agreement more than the 21,052,632 Class A Shares being registered for resale under this registration statement in order to receive additional proceeds (which we may elect to do, at our sole discretion, up to aggregate gross proceeds of $100.0 million), we must file with the SEC one or more additional registration statements to register the resale under the Securities Act by Cantor of any such additional shares of Class A Common Stock we wish to sell from time to time under the Purchase Agreement, which the SEC must declare effective before we may elect to sell any such additional shares of Class A Common Stock to Cantor under the Purchase Agreement. Any issuance and sale by us under the Purchase Agreement of a substantial amount of shares of Class A Common Stock in addition to the 21,052,632 shares of Class A Common Stock being registered for resale by Cantor under this prospectus could cause additional substantial dilution to our stockholders. The number of Class A Shares ultimately offered for sale by Cantor is dependent upon the number of Class A Shares, if any, we ultimately elect to sell to Cantor under the Purchase Agreement. However, even if we elect to sell Class A Shares to Cantor pursuant to the Purchase Agreement, Cantor may resell all, some or none of such shares at any time or from time to time in its sole discretion and at different prices.

11

Additionally, Cantor’s obligations to accept purchase notices and to purchase our shares of Class A Common Stock under the Purchase Agreement are subject to the satisfaction of a number of conditions, which conditions include, without limitation, that (i) the representation and warranties of the Company included in the Purchase Agreement are accurate in all material respects, (ii) the Company has performed, satisfied and complied in all material respects with all covenants, agreements and conditions required by the Purchase Agreement to be performed, satisfied or complied with by the Company, (iii) no condition, occurrence, state of facts or event constituting a Material Adverse Effect (as such term is defined in the Purchase Agreement) shall have occurred and be continuing, and (iv) the delivery of various opinions, comfort letters and other items, among other conditions. Accordingly, there can be no assurances that the Facility will be available to us at all times during its term.

In addition, the Purchase Agreement can be terminated by the Company at any time upon 3 trading days prior notice. The Purchase Agreement may also be terminated by Cantor upon 3 trading days prior notice upon the occurrence of certain events, including but not limited to, the existence of an event constituting a material adverse event, a change of control or other fundamental transaction has occurred with Appreciate. Cantor may also terminate the Purchase Agreement immediately upon the occurrence of additional specified events. See “The Committed Equity Financing—Termination of the Purchase Agreement” for more detail.

Investors who buy Class A Shares from Cantor at different times will likely pay different prices.

Pursuant to the Purchase Agreement, we will have discretion, to vary the timing, price and number of shares sold to Cantor. If and when we elect to sell shares of Class A Common Stock to Cantor pursuant to the Purchase Agreement, after Cantor has acquired such shares, Cantor may resell all, some or none of such shares at any time or from time to time in its sole discretion and at different prices. As a result, investors who purchase shares from Cantor in this offering at different times will likely pay different prices for those shares, and so may experience different levels of dilution and in some cases substantial dilution and different outcomes in their investment results. Additionally, existing holders of our shares of Class A Common Stock may have acquired such shares at higher prices than Cantor may obtain and/or resell shares of Class A Common Stock under the Facility and such existing holders may not experience a similar rate of return on their shares due to these variations in share prices. Investors may experience a decline in the value of the shares they purchase from Cantor in this offering as a result of future sales made by us to Cantor at prices lower than the prices such investors paid for their shares in this offering. In addition, if we sell a substantial number of shares to Cantor under the Purchase Agreement, or if investors expect that we will do so, the actual sales of shares or the mere existence of our arrangement with Cantor may depress the market price of our Class A Common Stock and make it more difficult for us to sell equity or equity-related securities in the future at a time and at a price that we might otherwise wish to effect such sales.

We may use proceeds from sales of our Class A Shares made pursuant to the Purchase Agreement in ways with which you may not agree or in ways which may not yield a significant return.

We will have broad discretion over the use of proceeds from sales of our shares of Class A Common Stock made pursuant to the Purchase Agreement, including for any of the purposes described in the section entitled “Use of Proceeds,” and you will not have the opportunity, as part of your investment decision, to assess whether the proceeds are being used appropriately. However, we have not determined the specific allocation of any net proceeds among these potential uses, and the ultimate use of the net proceeds may vary from the currently intended uses. The net proceeds may be used for corporate purposes that do not increase our operating results or enhance the value of our shares of Class A Common Stock.

Future resales and/or issuances of Class A Shares, including pursuant to this prospectus may cause the market price of our shares to drop significantly.

To the extent the Company sells shares of Class A Common Stock under the Cantor Equity Facility, substantial amounts of Class A Shares will be issued and available for resale by Cantor, which would cause dilution and represent a significant portion of our public float and may result in substantial decreases to the Company’s stock price. Cantor will acquire shares of Class A Common Stock at a purchase price that will be equal to 98% of the then current market price. Because Cantor will acquire shares of Class A Common Stock under the Facility at a discount to the market price, they will have an incentive to sell such shares. If all of the 21,052,632 shares of Class A Common Stock offered for resale by Cantor under this prospectus were issued and outstanding as of January 23, 2023, such shares of Class A Common Stock would represent approximately 30.84% of the total number of our shares of Common Stock outstanding after giving effect to such issuance. As a percentage of our publicly-traded shares of Class A Common Stock, the shares of Class A Common Stock that can be sold pursuant to this Prospectus would constitute approximately 55.24% of such shares if all the shares offered hereby were sold.

Further, similar dilution and potentially depressive effects may occur to the extent that the resales of currently unregistered shares of Common Stock were to occur. Additionally, there are 7,671,746 outstanding public warrants to purchase shares of Class A Common stock at an exercise price of $11.50 per share, which warrants will became exercisable on December 29, 2022. In addition, there are 4,833,333 private placement warrants outstanding exercisable for 4,833,333 shares of common stock at an exercise price of $11.50 per share. To the extent such warrants are exercised, additional shares of common stock will be issued, which, along with the shares being registered for resale under this prospectus, will result in dilution to the holders of our common stock and increase the number of shares eligible for resale in the public market. Sales of substantial numbers of such shares in the public market could adversely affect the market price of our common stock. Future sales and issuances of our Class A Shares, including pursuant to our equity incentive and other compensatory plans, will result in additional dilution of the percentage ownership of our shareholders and could cause our share price to fall.

12

Risks Related to Liquidity and Capital Resources

We must raise additional capital to fund our operations in order to continue as a going concern.

We have included disclosure in our Management’s Discussion and Analysis of Financial Condition and Results of Operations indicating that our current liquidity position raises substantial doubt about our ability to continue as a going concern. If we are unable to improve our liquidity position, we may not be able to continue as a going concern. Our ability to raise the capital needed to improve our financial condition may be hindered by the resale of a significant number of shares of our Class A Common Stock acquired pursuant to the Facility or otherwise as well as the maturity right held by parties to the Forward Purchase Agreement dated November 20, 2022 (which could require the repurchase of shares of our Class A Common Stock held by them or significant cash payments if triggered and exercised) and defaults in our indebtedness as well as the substantial amount of service provider obligations. The accompanying consolidated financial statements do not include any adjustments that might result if we are unable to continue as a going concern and, therefore, be required to realize our assets and discharge our liabilities other than in the normal course of business which could cause investors to suffer the loss of all or a substantial portion of their investment.

We anticipate that our principal sources of liquidity will only be sufficient to fund our activities and debt service needs through March 31, 2023. In order to have sufficient cash to fund our operations beyond March 31, 2023, we will need to raise additional equity or debt capital in order to continue as a going concern and we cannot provide any assurance that we will be successful in doing so.

We may not be able to refinance, extend or repay our substantial indebtedness owed to our senior secured lender or obligations owed to service providers, which would have a material adverse effect on our financial condition and ability to continue as a going concern.