As filed with the Securities and Exchange Commission on April 25, 2023

No. 333-265748

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

POST-EFFECTIVE

TO

FORM

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

(Exact name of registrant as specified in its charter)

Delaware (State or other jurisdiction of incorporation or organization) | 4700 (Primary Standard Industrial | 98-0598290 |

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Eric J. Bock, Esq.

Chief Legal Officer

Global Business Travel Group, Inc.

666 3rd Avenue, 4th Floor

New York, NY 10017

Telephone: (480) 909-1740

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies of all communications, including communications sent to agent for service, should be sent to:

Gregory A Fernicola, Esq.

Skadden, Arps, Slate, Meagher & Flom LLP

One Manhattan West

New York, NY 10001-8602

Telephone: (212) 735-3000

Approximate date of commencement of proposed sale to the public: From time to time on or after the effective date of this registration statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, as amended (the “Securities Act”), check the following box: ☐

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Securities Exchange Act of 1934, as amended (the “Exchange Act”).

Large accelerated filer | ☐ | Accelerated filer | ☐ |

☒ | Smaller reporting company | ||

Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until this registration statement shall become effective on such date as the SEC acting pursuant to said Section 8(a), may determine.

EXPLANATORY NOTE

On June 21, 2022, the registrant filed a Registration Statement on Form S-1 (Registration No. 333-265748), which was subsequently declared effective by the U.S. Securities and Exchange Commission (the “SEC”) on August 5, 2022 (such registration statement, as amended and/or supplemented, the “Existing Registration Statement”).

This Post-Effective Amendment No. 1 to the Existing Registration Statement is being filed to update the Existing Registration Statement to include information contained in the registrant’s Annual Report on Form 10-K and certain other information in the Existing Registration Statement. No additional securities are being registered under this post-effective amendment. All applicable registration fees were paid at the time of the original filing of the Existing Registration Statement.

On October 12, 2022, we completed an exchange offer and consent solicitation (the “Exchange Offer and Consent Solicitation”) relating to all of our outstanding warrants, consisting of (i) the warrants sold as part of the units issued in Apollo Strategic Growth Capital’s initial public offering (“APSG IPO”) on October 6, 2020 (the “Public Warrants”) and (ii) the warrants sold as part of the units issued in a private placement that occurred simultaneously with the APSG IPO (together with the Public Warrants, the “Warrants”), each whole Warrant exercisable for one share of our Class A common stock, $0.0001 par value per share (“Class A Common Stock”), at an exercise price of $11.50 per share. We issued 10,444,363 shares of Class A Common Stock in exchange for the Warrants tendered in the Exchange Offer and Consent Solicitation.

On October 12, 2022, we entered into an amendment to the warrant agreement governing the Warrants related to the previously completed Exchange Offer and Consent Solicitation (the “Warrant Amendment”). We exercised our right under the Warrant Amendment to acquire and retire all remaining untendered Warrants in exchange for 364,147 shares of Class A Common Stock (the “Warrant Amendment Exchange”) and we settled the Warrant Amendment Exchange on October 31, 2022. As a result of the Exchange Offer and Consent Solicitation and the Warrant Amendment Exchange, no Warrants remain outstanding.

On January 26, 2023, we completed an exchange offer (the “MIP Option Exchange”) relating to certain of our outstanding stock options (the “GBTG MIP Options”). As a result of the MIP Option Exchange, 12,788,639 GBTG MIP Options were either cancelled or exercised.

STATEMENT PURSUANT TO RULE 429

The registrant is filing a single prospectus in this registration statement pursuant to Rule 429 under the Securities Act of 1933, as amended (the “Securities Act”). The prospectus is a combined prospectus relating to (i) the resale by certain of the selling securityholders of up to 466,649,054 shares of Class A Common Stock, all of which are being registered hereunder and (ii) the issuance by us of 21,402,684 shares of Class A Common Stock underlying GBTG MIP Options, registered under Form S-4 (File No. 333-261820), originally filed with the Securities and Exchange Commission (the “SEC”) on December 21, 2021 and subsequently declared effective (the registration statement referenced in the preceding clause (ii), as amended and/or supplemented, the “Prior Registration Statement”). Pursuant to Rule 429 under the Securities Act, this registration statement on Form S-1 upon effectiveness will serve as a post-effective amendment to the Prior Registration Statement. Such post-effective amendment shall hereafter become effective concurrently with the effectiveness of this registration statement and in accordance with Section 8(c) of, and Rule 429 under, the Securities Act.

The information in this preliminary prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities, nor does it seek an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED APRIL 25, 2023

PRELIMINARY PROSPECTUS

GLOBAL BUSINESS TRAVEL GROUP, INC.

ISSUANCE OF UP TO 21,402,684 SHARES OF CLASS A COMMON STOCK

AND

RESALE OF UP TO 466,649,054 SHARES OF CLASS A COMMON STOCK

BY THE SELLING SECURITYHOLDERS

This prospectus relates to the issuance by us of up to 21,402,684 shares of Class A Common Stock issuable upon the exercise of GBTG MIP Options with an exercise price ranging from $5.74 to $14.58, with each GBTG MIP Option exercisable for one share of Class A Common Stock.

This prospectus also relates to the resale by the selling securityholders named in this prospectus, or the Selling Securityholders, of up to 466,649,054 shares of Class A Common Stock, which consists of (i) 394,448,481 shares of Class A Common Stock issuable upon the exchange of GBT JerseyCo B Ordinary Shares (with automatic surrender for cancellation of an equal number of shares of Class B Common Stock) held by the Continuing JerseyCo Owners originally, which they received in exchange for their GBT JerseyCo shares pursuant to the Business Combination Agreement, with each GBT JerseyCo B Ordinary Share exchangeable for one share of Class A Common Stock; (ii) 14,435,817 shares of Class A Common Stock issuable upon the conversion of “earnout” shares held by the Continuing JerseyCo Owners and certain of our officers and directors (and, in the case of the Continuing JerseyCo Owners, upon the subsequent exchange of GBT JerseyCo B Ordinary Shares (with automatic surrender for cancellation of an equal number of shares of Class B Common Stock) into which such “earnout” shares will convert) issued pursuant to the Business Combination Agreement, to such holders, as holders of GBT JerseyCo shares, without the payment of any additional purchase price, with each “earnout” share convertible into one share of Class A Common Stock; (iii) 5,644,506 shares of Class A Common Stock issuable upon the exercise of GBTG MIP Options held by certain of our officers and directors with an exercise price ranging from $5.74 to $14.58, with each GBTG MIP Option exercisable for one share of Class A Common Stock; (iv) 31,700,000 shares of Class A Common Stock issued in the PIPE Investment originally issued at a price of $10.00 per share; and (v) 20,420,250 converted Founder Shares originally issued at a price of $0.00087 per share.

We believe the likelihood that GBTG MIP Option holders will exercise their GBTG MIP Options, and therefore the amount of cash proceeds that we would receive is, among other things, dependent upon the market price of our Class A Common Stock. If the market price for our Class A Common Stock is less than the applicable exercise price ($5.74 to $14.58 for the GBTG MIP Options), we believe such holders will be unlikely to exercise their GBTG MIP Options. For additional information, see “Risk Factors —Risks Relating to Ownership of the Class A Common Stock.”

See “Selected Definitions” below for certain defined terms used in this prospectus.

We are registering the resale of the shares of Class A Common Stock pursuant to the Registration Rights Agreement and the PIPE Subscription Agreements. Our registration of the securities covered by this prospectus does not mean that the Selling Securityholders will offer or sell any of the shares of Class A Common Stock. Subject to the terms of the applicable agreements, the Selling Securityholders may offer, sell or distribute all or a portion of their shares of Class A Common Stock publicly or through private transactions at prevailing market prices or at negotiated prices. We provide more information about how the Selling Securityholders may sell the shares of Class A Common Stock in the section entitled “Plan of Distribution.”

We will receive the proceeds from any exercise of GBTG MIP Options for cash, but not from the resale of the shares of Class A Common Stock by the Selling Securityholders. To the extent that the GBTG MIP Options are exercised on a “cashless basis,” the amount of cash we would receive from the exercise of the GBTG MIP Options will decrease.

We will bear all costs, expenses and fees in connection with the registration of the shares of Class A Common Stock. The Selling Securityholders will bear all commissions and discounts, if any, attributable to their respective sales of the shares of Class A Common Stock.

Our Class A Common Stock is listed on the New York Stock Exchange (the “NYSE”) under the symbol “GBTG”. On April 21, 2023, the last reported sale price for our Class A Common Stock as reported on the NYSE was $6.63 per share.

The shares of Class A Common Stock being registered for resale in this prospectus represent a substantial percentage of our public float and of our outstanding shares of Class A Common Stock. The shares being registered in this prospectus (which include shares issuable upon exercise, conversion or exchange of other securities) exceed the total number of outstanding shares of Class A Common Stock (69,912,660 shares of Class A Common Stock outstanding as of April 21, 2023). In addition, the securities beneficially owned by Continuing JerseyCo Owners, holders of GBTG MIP Options and holders of GBT MIP Shares represent over 80% of the total outstanding shares of Class A Common Stock, and these holders will have the ability to sell all of their shares pursuant to the registration statement of which this prospectus forms a part so long as it is available for use. The sale of the securities being registered in this prospectus therefore could result in a significant decline in the public trading price of Class A Common Stock.

In addition, some of the shares being registered for resale were or may be acquired by the Selling Securityholders for no consideration or purchased for prices considerably below the current market price of the Class A Common Stock. Even though the current market price is significantly below the price at the time of the APSG IPO, certain Selling Securityholders have an incentive to sell because they will still profit on sales due to the lower price at which they acquired their shares as compared to the public investors. In particular, the Sponsor, the Continuing JerseyCo Owners and certain of our officers and directors may experience a positive rate of return on the securities they purchased due to the differences in the purchase prices described above, to the extent they acquired such securities for less than the relevant trading price, and the public securityholders may not experience a similar rate of return on the securities they purchased due to the differences in the purchase prices described above. Based on the last reported sale price of Class A Common Stock referenced above, shares acquired for less than such last reported sale price (including (i) shares issuable upon the exchange of GBT JerseyCo B Ordinary Shares, (ii) shares issuable upon the conversion of “earnout” shares, and (iii) the converted Founder Shares) the Selling Securityholders may experience potential profit up to $6.63 per share.

Investing in our securities involves a high degree of risk. You should carefully read the discussion in “Risk Factors” beginning on page 7 of this prospectus.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

Prospectus dated , 2023

TABLE OF CONTENTS

iii | |

iii | |

iii | |

xi | |

1 | |

7 | |

44 | |

45 | |

46 | |

Management’s Discussion and Analysis of Financial Condition and Results of Operations | 77 |

106 | |

114 | |

126 | |

145 | |

148 | |

Security Ownership of Certain Beneficial Owners And Management | 158 |

161 | |

166 | |

169 | |

170 | |

170 | |

170 | |

F-1 |

i

ABOUT THIS PROSPECTUS

You should rely only on the information contained in this prospectus or in any applicable prospectus supplement prepared by us or on our behalf. Neither we nor the Selling Securityholders have authorized anyone to provide any information or to make any representations other than those contained in this prospectus, any accompanying prospectus supplement or any free writing prospectus we have prepared. We and the Selling Securityholders take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. This prospectus is an offer to sell only the securities offered hereby and only under circumstances and in jurisdictions where it is lawful to do so. No dealer, salesperson or other person is authorized to give any information or to represent anything not contained in this prospectus, any applicable prospectus supplement or any related free writing prospectus. This prospectus is not an offer to sell securities, and it is not soliciting an offer to buy securities, in any jurisdiction where the offer or sale is not permitted. You should assume that the information appearing in this prospectus or any prospectus supplement is accurate only as of the date on the front of those documents only, regardless of the time of delivery of this prospectus or any applicable prospectus supplement, or any sale of a security. Our business, financial condition, results of operations and prospects may have changed since those dates.

This prospectus is part of a registration statement on Form S-1 that we filed with the Securities and Exchange Commission (the “SEC”) using the “shelf” registration process. Under this shelf registration process, the Selling Securityholders hereunder may, from time to time, sell the securities offered by them described in this prospectus. We will not receive any proceeds from the sale by such Selling Securityholders of the securities offered by them described in this prospectus.

A prospectus supplement may also add, update or change information included in this prospectus. Any statement contained in this prospectus will be deemed to be modified or superseded for purposes of this prospectus to the extent that a statement contained in such prospectus supplement modifies or supersedes such statement. Any statement so modified will be deemed to constitute a part of this prospectus only as so modified, and any statement so superseded will be deemed not to constitute a part of this prospectus. You should rely only on the information contained in this prospectus, any applicable prospectus supplement or any related free writing prospectus. See “Where You Can Find More Information.”

This prospectus contains summaries of certain provisions contained in some of the documents described herein, but reference is made to the actual documents for complete information. All of the summaries are qualified in their entirety by the actual documents. Copies of some of the documents referred to herein have been filed, will be filed or will be incorporated by reference as exhibits to the registration statement of which this prospectus is a part, and you may obtain copies of those documents as described in the section entitled under “Where You Can Find More Information.”

Unless the context otherwise requires, the “Company,” “GBT,” “our,” “we” or “us” refers to GBTG and its consolidated subsidiaries following the consummation of the Business Combination, other than certain historical information which refers to the business of GBT JerseyCo and its consolidated subsidiaries prior to the consummation of the Business Combination. Unless the context otherwise requires, references to “APSG” refers to Apollo Strategic Growth Capital, a blank check company incorporated as a Cayman Islands exempted company, prior to the Closing, references to “GBT JerseyCo” refers to GBT JerseyCo Limited, a company limited by shares incorporated under the laws of Jersey, prior to the Closing, and references to “GBTG” refers to Global Business Travel Group, Inc., a Delaware corporation.

ii

TRADEMARKS, TRADE NAMES AND SERVICE MARKS

This prospectus contains references to trademarks and service marks belonging to other entities. Solely for convenience, trademarks, trade names and service marks referred to in this prospectus may appear without the ®, ™ or ℠ symbols, but such references are not intended to indicate, in any way, that the applicable licensor will not assert, to the fullest extent under applicable law, its rights to these trademarks, trade names and service marks. We do not intend our use or display of other companies’ trade names, trademarks or service marks to imply a relationship with, or endorsement or sponsorship of us by, any other companies.

MARKET, INDUSTRY AND OTHER DATA

Market, industry and other data used in this prospectus have been obtained from independent industry sources and publications, including the following:

| ● | Global Business Travel Association (“GBTA BTI Outlook Annual Global Report & Forecast: Prospects for Global Business Travel 2020-2024,” January 2021, Global Business Travel Association); |

| ● | World Travel & Tourism Council (“Travel & Tourism: Economic Impact 2021,” April 2021, World Travel & Tourism Council); |

| ● | Travel Weekly (“2022 Power List,” June 2022, Travel Weekly); |

| ● | Business Travel News (“2022 Corporate Travel 100,” September 2022, Business Travel News); |

| ● | Skift Research (“The Travel Industry Turned Upside Down,” September 2020, Skift Research in Partnership With McKinsey & Company); |

| ● | The American Lawyer (“The 2021 Am Law 100: Ranked by Gross Revenue,” April 2021, The American Lawyer); and |

| ● | Fortune 500® (“Fortune 500,” 2022, FORTUNE and “100 Best Companies to Work For,” 2022, FORTUNE). |

Market and industry data, statistics and forecasts used throughout this prospectus are based on publicly available information, industry publications and surveys, reports by market research firms and our estimates based on our management’s knowledge of, and experience in, the travel industry and customer segments in which we compete. Third-party industry publications and forecasts generally state that the information contained therein has been obtained from sources generally believed to be reliable. In addition, certain information contained in this prospectus, including information relating to the proportion of new opportunities we pursue, represents our management’s estimates. While we believe our internal estimates to be reasonable, and we are not aware of any misstatements regarding the industry data presented herein, they have not been verified by any independent sources. Such data involve risks and uncertainties and are subject to change based on various factors, including those discussed under the captions “Risk Factors,” “Cautionary Statement Regarding Forward-Looking Statements” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

SELECTED DEFINITIONS

When used in this prospectus, unless otherwise stated or the context otherwise requires:

| ● | “2020 Executive LTIP” refers to the 2020 Executive Long-Term Cash Incentive Award Plan. |

| ● | “2021 Executive LTIP” refers to the 2021 Executive Long-Term Cash Incentive Award Plan. |

| ● | “2022 Plan” refers to the Global Business Travel Group, Inc. 2022 Equity Incentive Plan. |

| ● | “Adjusted EBITDA” refers to net income (loss) before interest income, interest expense, gain (loss) on early extinguishment of debt, benefit from (provision for) income taxes, depreciation and amortization and as further adjusted to exclude costs that our management believes are non-core to our underlying business, consisting of restructuring costs, integration costs, costs |

iii

| related to mergers and acquisitions, non-cash equity-based compensation, long-term incentive plan costs, certain corporate costs, fair value movements on earnouts and warrants derivative liabilities, foreign currency gains (losses), non-service components of net periodic pension benefit (costs) and gains (losses) on disposal of businesses. |

| ● | “Adjusted EBITDA Margin” refers to Adjusted EBITDA divided by revenue. |

| ● | “Adjusted Operating Expenses” refers to total operating expenses excluding depreciation and amortization and costs that our management believes are non-core to our underlying business, consisting of restructuring costs, integration costs, costs related to mergers and acquisitions, non-cash equity-based compensation, long-term incentive plan costs and certain corporate costs. |

| ● | “Amended & Restated GBT MIP” refers to the GBT JerseyCo Limited Amended and Restated Management Incentive Plan, effective as of December 2, 2021. |

| ● | “American Express” refers to American Express Company and its consolidated subsidiaries. |

| ● | “Amex HoldCo.” refers to American Express Travel Holdings Netherlands Coöperatief U.A. |

| ● | “Apollo” refers to Apollo Global Management, Inc., together with its consolidated subsidiaries. |

| ● | “APSG” refers, prior to the Domestication and the Closing, to Apollo Strategic Growth Capital, a blank check company incorporated as a Cayman Islands exempted company. |

| ● | “APSG Class A Ordinary Shares” refers to Class A ordinary shares, par value $0.00005 per share, of APSG prior to the Domestication and the Closing. |

| ● | “APSG Class B Ordinary Shares” refers to the Class B ordinary shares, par value $0.00005 per share, of APSG prior to the Domestication and the Closing. |

| ● | “APSG IPO” refers to APSG’s initial public offering on October 6, 2020. |

| ● | “APSG Shareholders” refers to the holders of APSG Class A Ordinary Shares and holders of APSG Class B Ordinary Shares prior to Domestication and the Closing. |

| ● | “B2B” refers to business-to-business. |

| ● | “B2B travel” refers to travel for business purposes that is purchased and fulfilled through a company-sponsored and managed channel. |

| ● | “B2C” refers to channels or platforms used by consumers to book and fulfill travel, including directly with suppliers or through intermediaries such as online travel agencies. B2C may include business travelers who purchase travel outside of a company-sponsored and managed channel, or whose companies does not have such a channel. |

| ● | “BHC Act” refers to the Bank Holding Company Act of 1956, as amended. |

| ● | “Board” refers to the board of directors of GBTG. |

| ● | “Business Combination” refers to the transactions contemplated by the Business Combination Agreement. |

| ● | “Business Combination Agreement” refers to the Business Combination Agreement, dated as of December 2, 2021 (as the same has been amended, modified, supplemented or waived from time to time in accordance with its terms), by and between GBTG (formerly known as Apollo Strategic Growth Capital) and GBT JerseyCo. |

iv

| ● | “Bylaws” refers to the Bylaws of GBTG. |

| ● | “CAGR” refers to a compound annual growth rate. |

| ● | “Certares” refers to Certares Management LLC. |

| ● | “Certificate of Incorporation” refers, collectively, to the Certificate of Incorporation of GBTG, the Certificate of Designations for the Class A-1 Preferred Stock and the Certificate of Designations for the Class B-1 Preferred Stock. |

| ● | “Class A Common Stock” refers to the Class A common stock, par value $0.0001 per share, of GBTG. |

| ● | “Class A Stock” refers to (a) if no shares of Class A-1 Preferred Stock or Class B-1 Preferred Stock have been issued pursuant to and in accordance with the Shareholders Agreement, Class A Common Stock, and (b) if any shares of Class A-1 Preferred Stock or Class B-1 Preferred Stock have been so issued, (i) Class A Common Stock or Class A-1 Preferred Stock and (ii) where the context requires, Class A Common Stock and Class A-1 Preferred Stock, collectively. |

| ● | “Class B Common Stock” refers to the Class B common stock, par value $0.0001 per share, of GBTG. |

| ● | “Class B Stock” refers to (a) if no shares of Class A-1 Preferred Stock or Class B-1 Preferred Stock have been issued pursuant to and in accordance with the Shareholders Agreement, Class B Common Stock, and (b) if any shares of Class A-1 Preferred Stock or Class B-1 Preferred Stock have been so issued, (i) Class B Common Stock or Class B-1 Preferred Stock and (ii) where the context requires, Class B Common Stock and Class B-1 Preferred Stock, collectively. |

| ● | “Closing” refers to the consummation of the transactions contemplated by the Business Combination. |

| ● | “Closing Date” refers to May 27, 2022, the date of the closing of the Business Combination. |

| ● | “Code” refers to the U.S. Internal Revenue Code of 1986, as amended. |

| ● | “Common Stock” refers to Class A Common Stock and Class B Common Stock. |

| ● | “Company,” “GBT,” “our,” “we” or “us” refers to GBTG and its consolidated subsidiaries following the consummation of the Business Combination, other than certain historical information which refers to the business of GBT JerseyCo Limited and its consolidated subsidiaries prior to the consummation of the Business Combination. |

| ● | “Continuing JerseyCo Owners” refers to Amex HoldCo., Juweel and Expedia, which hold GBT JerseyCo B Ordinary Shares, shares of Class B Common Stock and “earnout” shares following the Closing. |

| ● | “DGCL” refers to the Delaware General Corporation Law, as amended. |

| ● | “dollars” or “$” refers to U.S. dollars. |

| ● | “Domestication” refers to the domestication of APSG as a Delaware corporation, with the APSG shares becoming shares of Common Stock of GBTG under the applicable provisions of the Cayman Islands Companies Act (2021 Revision) of the Cayman Islands as the same may be amended from time to time and the DGCL. |

| ● | “EBITDA” refers to net income (loss) before interest income, interest expense, gain (loss) on early extinguishment of debt, benefit from (provision for) income taxes and depreciation and amortization. |

| ● | “Egencia” refers to the business acquired in the Egencia Acquisition. |

| ● | “Egencia Acquisition” refers to GBT JerseyCo’s acquisition of the Egencia business from Expedia pursuant to the Egencia Equity Contribution Agreement. |

v

| ● | “Egencia Equity Contribution Agreement” refers to the Equity Contribution Agreement, dated as of August 11, 2021, by and among Expedia, Inc., GBT JerseyCo and Juweel, in connection with the Egencia Acquisition. |

| ● | “Equity Commitment Letters” refers to the equity commitment letters entered into by Juweel and Amex HoldCo. with GBT JerseyCo, each dated as of August 25, 2020, and each as amended on January 20, 2021. Such equity commitment letters, and the then-remaining commitments thereunder, were terminated at Closing. |

| ● | “ESPP” refers to the Global Business Travel Group, Inc. Employee Stock Purchase Plan. |

| ● | “Exchange Act” refers to the Securities Exchange Act of 1934, as amended. |

| ● | “Exchange Agreement” refers to the Exchange Agreement, dated May 27, 2022, by and among GBTG, GBT JerseyCo and each holder of GBT JerseyCo B Ordinary Shares from time to time party thereto. |

| ● | “Exchange Committee” refers to a committee of the Board comprising solely of independent directors not nominated by a Continuing JerseyCo Owner who are disinterested with respect to any particular exchange under the Exchange Agreement. The Exchange Committee may be (and the term “Exchange Committee” shall be construed to include) either (a) a standalone committee of the Board or (b) the Audit and Finance Committee of the Board or another committee of the Board that meets the requirements specified in this definition, for so long as the Board has delegated the functions of the Exchange Committee to the Audit and Finance Committee or such other committee, as applicable; provided that, if (i) the Exchange Committee is a standalone committee of the Board, no nominee of a Continuing JerseyCo Owner may be a member of the Exchange Committee, and (ii) the Board has delegated the functions of the Exchange Committee to the Audit and Finance Committee and the members of the Audit and Finance Committee include one or more nominees of a Continuing JerseyCo Owner, then each such nominee of must recuse himself or herself from any and all business of such committee concerning an exchange. |

| ● | “Expedia” refers to EG Corporate Travel Holdings LLC, a Delaware limited liability company. |

| ● | “Founder Shares” refers to the 20,420,250 APSG Class B Ordinary Shares held in the aggregate by the Sponsor and the Insiders, which were converted into shares of our Class A Common Stock at the Closing. |

| ● | “Free Cash Flow” refers to net cash from (used in) operating activities, less cash used for additions to property and equipment. |

| ● | “GAAP” refers to United States generally accepted accounting principles, consistently applied. |

| ● | “GBTG” refers to Global Business Travel Group, Inc., a Delaware corporation. |

| ● | “GBT JerseyCo” refers to GBT JerseyCo Limited, a company limited by shares incorporated under the laws of Jersey, prior to the Closing. |

| ● | “GBT JerseyCo A Ordinary Shares” refers to voting redeemable shares of GBT JerseyCo, designated as “A Ordinary Shares” in the GBT JerseyCo Amended and Restated M&A with a nominal value of €0.00001. |

| ● | “GBT JerseyCo Amended and Restated M&A” refers to the Fourth Amended & Restated Memorandum of Association of GBT JerseyCo and the Third Amended & Restated GBT JerseyCo Articles of Association. |

| ● | “GBT JerseyCo B Ordinary Shares” refers to non-voting redeemable shares of GBT JerseyCo, designated as “B Ordinary Shares” in the GBT JerseyCo Amended and Restated M&A with a nominal value of €0.00001. |

| ● | “GBT JerseyCo C Ordinary Shares” or “earnout shares” refers to non-voting redeemable shares of GBT JerseyCo, designated as “C Ordinary Shares” in the GBT JerseyCo Amended and Restated M&A with a nominal value of €0.00001. |

| ● | “GBT JerseyCo Capital Stock” refers to the GBT JerseyCo A Ordinary Shares, GBT JerseyCo B Ordinary Shares, GBT JerseyCo C Ordinary Shares and the GBT JerseyCo Z Ordinary Share. |

vi

| ● | “GBT JerseyCo Z Ordinary Share” refers to non-voting non-redeemable shares of GBT JerseyCo, designated as the “Z Ordinary Share” in the GBT JerseyCo Amended and Restated M&A with a nominal value of €0.00001. |

| ● | “GBT Legacy MIP Option” refers to an option to purchase GBT MIP Shares that were granted prior to 2021. |

| ● | “GBT MIP Option” refers to an option to purchase GBT MIP Shares granted under the Amended & Restated GBT MIP (or any predecessor plan), including GBT Legacy MIP Options. |

| ● | “GBT MIP Shares” refers to the MIP Shares (as such term is defined in GBT JerseyCo’s memorandum of association and articles of association) of €0.00001 each of GBT JerseyCo, issuable in respect of GBT MIP Options. |

| ● | “GBT Partner Solutions” refers to GBT’s program, whereby participating travel agencies can benefit from, among other things, GBT’s global supplier network, long-standing relationships with suppliers and access to GBT’s products, services, and technology. |

| ● | “GBT Supply MarketPlace” refers to our proprietary capability to source, distribute and manage travel and travel-related content to travelers, clients and Network Partners, through both GBT and third-party technology, as well as GBT’s supplier content and management processes and expertise. |

| ● | “GBT UK” refers to GBT Travel Services UK Limited, our wholly owned indirect subsidiary. |

| ● | “GBTG MIP” refers to the Global Business Travel Group Management Incentive Plan. |

| ● | “GBTG MIP Option” or “Options” refers to an option relating to shares of Class A Common Stock upon substantially the same terms and conditions as are in effect with respect to the GBT MIP Option immediately prior to the Closing from which such GBTG MIP Option was converted in connection with the Business Combination. |

| ● | “GDPR” refers to the European General Data Protection Regulation, which took effect on May 25, 2018. |

| ● | “GDS” refers to the three major global distribution systems (Amadeus, Sabre and Travelport, inclusive of their constituent GDS) used by GBT as a source for air and other travel content. Global Distribution Systems are common technology infrastructure used by airlines and some other travel suppliers to distribute their content to Points of Sale (“POS”). |

| ● | “HRG Pension Scheme” refers to the defined benefit scheme for certain of associates and retirees of GBT and its affiliates in the United Kingdom (“UK”). |

| ● | “Insiders” refers to Jennifer Fleiss, Mitch Garber and James H. Simmons III. |

| ● | “Juweel” refers to Juweel Investors (SPC) Limited, an exempted segregated portfolio company with limited liability incorporated under the laws of the Cayman Islands, successor-in-interest to Juweel Investors Limited, a company incorporated as an exempted company with limited liability under the laws of the Cayman Islands. |

| ● | “Net Debt” refers to total debt outstanding consisting of current and non-current portion of long-term debt (defined as debt (excluding lease liabilities) with original contractual maturity dates of one year or greater), net of unamortized debt discount and unamortized debt issuance costs, minus cash and cash equivalents. |

| ● | “Network Partners” refers to third-party travel management companies (“TMCs”) and independent advisors that are clients of GBT Partner Solutions who, through GBT Partner Solutions, can access GBT’s technology platform and content or, in the case of our TPN, benefit from our client referrals and management network. |

| ● | “NYSE” refers to the New York Stock Exchange. |

| ● | “Ovation” refers to Ovation Travel, LLC, GBT’s subsidiary, and includes the Ovation, Ovation Vacations and Lawyers Travel brands. |

vii

| ● | “PIPE Investment” refers to the private placement pursuant to which PIPE Investors subscribed for an aggregate of 32,350,000 newly-issued shares of Class A Common Stock at a purchase price of $10.00 per share for an aggregate purchase price of $323.5 million pursuant to the PIPE Subscription Agreements, which was completed at the Closing. |

| ● | “PIPE Investors” refers to the investors that signed PIPE Subscription Agreements and funded their committed amounts. |

| ● | “PIPE Securities” refers to the shares of Class A Common Stock sold to the PIPE Investors pursuant to the PIPE Subscription Agreements. |

| ● | “PIPE Subscription Agreements” refers to the subscription agreements, dated as of December 2, 2021, by and between APSG and the PIPE Investors, pursuant to which the PIPE Investment was consummated. |

| ● | “Private Placement Warrants” refers to the warrants that were initially issued to the Sponsor in a private placement simultaneously with the closing of the APSG IPO. |

| ● | “Public Warrants” refers to the redeemable warrants underlying the units that were initially offered and sold by APSG as part of the APSG IPO. |

| ● | “Registration Rights Agreement” refers to the Amended and Restated Registration Rights Agreement, dated as of May 27, 2022, between GBTG, the Sponsor, the Insiders and the Continuing JerseyCo Owners, as the same may be amended, modified, supplemented or waived from time to time in accordance with its terms. |

| ● | “Rule 144” refers to Rule 144 under the Securities Act. |

| ● | “S&P” refers to the rating agency, Standard & Poor’s. |

| ● | “SEC” refers to the U.S. Securities and Exchange Commission. |

| ● | “Securities Act” refers to the Securities Act of 1933, as amended. |

| ● | “Senior Secured Credit Agreement” refers to that certain senior secured credit agreement, dated as of August 13, 2018, by and among GBT Group Services B.V., as borrower, GBT III B.V., as the original parent guarantor, the other loan parties from time to time party thereto, Morgan Stanley Senior Funding, Inc., as administrative agent and as collateral agent, and the lenders and letter of credit issuers from time to time party thereto, as amended from time to time. |

| ● | “Senior Secured Initial Term Loans” refers to the $250 million initial senior secured term loan facility that was obtained under the Senior Secured Credit Agreement on August 13, 2018. |

| ● | “Senior Secured New Tranche B-3 Term Loan Facilities” refers to the $1,000 million new tranche B-3 senior secured term loan facilities that were established under the Senior Secured Credit Agreement on December 16, 2021. |

| ● | “Senior Secured New Tranche B-4 Term Loan Facility” refers to the $135 million new tranche B-4 senior secured term loan facility that was established under the Senior Secured Credit Agreement on January 25, 2023. |

| ● | “Senior Secured Prior Tranche B-1 Term Loans” refers to the $400 million tranche B-1 senior secured incremental term loan facility that was obtained under the Senior Secured Credit Agreement on September 4, 2020, which facility was subsequently refinanced and repaid in full on December 16, 2021 |

| ● | “Senior Secured Prior Tranche B-2 Term Loan Facility” refers to the $200 million tranche B-2 senior secured delayed draw incremental term loan facility that was established under the Senior Secured Credit Agreement on January 20, 2021, which facility was subsequently refinanced and repaid in full, and the remaining unused commitments thereunder terminated, on December 16, 2021. |

| ● | “Senior Secured Revolving Credit Facility” refers to the $50 million senior secured revolving credit facility under the Senior Secured Credit Agreement. |

viii

| ● | “Shareholders Agreement” refers to the Shareholders Agreement, dated May 27, 2022, between GBTG, GBT JerseyCo, Amex HoldCo., Juweel and Expedia, as the same may be amended, modified, supplemented or waived from time to time in accordance with its terms. |

| ● | “SME” or “SME clients” refer to clients GBT considers small-to-medium-sized enterprises, which GBT generally defines as having an expected annual spend on air travel of less than $20 million. This criterion can vary by country and client needs. |

| ● | “Sponsor” refers to APSG Sponsor, L.P., a Cayman Islands exempted limited partnership. |

| ● | “Sponsor Side Letter” refers to the letter agreement, dated as of December 2, 2021, by and among the Sponsor, the Insiders, APSG and GBT JerseyCo, as the same may be amended, modified, supplemented or waived from time to time in accordance with its terms. |

| ● | “Sponsor Side Letter Vesting Period” refers to the five years following the Closing. |

| ● | “Total New Wins Value” is calculated using expected annual average Total Transaction Value over the contract term from all new client wins over the last twelve months, based on current recovery levels. |

| ● | “Total Transaction Value” or “TTV” refers to the sum of the total price paid by travelers for air, hotel, rail, car rental and cruise bookings, including taxes and other charges applied by suppliers at point of sale, less cancellations and refunds. |

| ● | “TPN” refers to GBT’s Travel Partner Network, consisting of third-party travel management companies, through which GBT services clients globally. All TPNs are Network Partners. |

| ● | “Transaction Growth (Decline)” refers to year-over-year growth (or decline) as a percentage of the total transactions, including air, hotel, car rental, rail or other travel-related transactions, recorded at the time of booking, and is calculated on a gross basis to include cancellations, refunds and exchanges. |

| ● | “Transactions” refers the completion of the Business Combination and the other transactions contemplated by the Business Combination Agreement. |

| ● | “Transfer Agent” refers to Continental Stock Transfer & Trust Company. |

| ● | “Treasury Regulations” refers to the regulations promulgated under the Code by the United States Department of the Treasury (whether in final, proposed or temporary form), as the same may be amended from time to time. |

| ● | “Trust Account” refers to the trust account of APSG, which held the net proceeds from the APSG IPO and certain of the proceeds from the sale of the Private Placement Warrants, together with interest earned thereon, less amounts released to pay taxes. |

| ● | “UK Data Protection Act” refers to the Data Protection Act the UK implemented, effective in May 2018 and statutorily amended in 2019. |

| ● | “UK GDPR” refers to the UK-only adaption of the GDPR, which took effect on January 1, 2021. |

| ● | “VWAP” refers to dollar volume-weighted average price. |

| ● | “Warrants” refers to the Public Warrants and the Private Placement Warrants. |

All financial statements presented in this prospectus have been prepared in accordance with GAAP and, unless otherwise noted, are presented in U.S. dollars.

Certain monetary amounts, percentages and other figures included elsewhere in this prospectus have been subject to rounding adjustments. Accordingly, figures shown as totals in certain tables or charts may not be the arithmetic aggregation of the figures that precede them, and figures expressed as percentages in the text may not total 100% or, as applicable, when aggregated may not be the arithmetic aggregation of the percentages that precede them.

ix

This prospectus contains “non-GAAP financial measures” that are financial measures that either exclude or include amounts that are not excluded or included in the most directly comparable measures calculated and presented in accordance with GAAP. Specifically, we use “EBITDA,” “Adjusted EBITDA,” “Adjusted EBITDA Margin,” “Adjusted Operating Expenses,” “Free Cash Flow” and “Net Debt (Cash)” as non-GAAP financial measures. For a discussion on our use of non-GAAP financial measures and a reconciliation to the most directly comparable GAAP measures, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations — Key Operating and Financial Metrics — Non-GAAP Financial Measures.”

The COVID-19 pandemic severely restricted the level of economic activity around the world and has continued to have an unprecedented effect on the global travel industry, decreasing business travel significantly below 2019 levels. Accordingly, our last year of normalized operations before the COVID-19 pandemic was the year ended December 31, 2019. In various discussions of our business trends and performance, we have excluded a discussion of our performance for the years ended December 31, 2022, 2021 and 2020 in this prospectus because we do not believe those results are indicative of our normal operations and the travel industry more generally due to the unprecedented impact of the COVID-19 pandemic. We believe the historical track record of growth and the emergent recovery of business travel as travel restrictions have been relaxed supports the fundamental growth drivers and long-term growth potential of business travel worldwide in the future. However, the profile, extent and timing of economic and travel recovery and the pace of future growth remains inherently uncertain given the nature of the COVID-19 pandemic and changes to business practices that may become permanent and reduce the need for business travel. There can be no assurance that any emerging growth patterns will continue or that we will replicate our historical growth in the future. For information on the impact of the COVID-19 pandemic on business travel, see “Business — Key Factors Affecting Our Results of Operations — Impact of the COVID-19 Pandemic,” “Business — Recent Performance and COVID-19 Update,” “Management’s Discussion and Analysis of Financial Condition and Result of Operations — Overview — Impact of the COVID-19 Pandemic” and “Risk Factors — Risks Relating to Our Business and Industry.”

x

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

Certain statements made in this prospectus are “forward looking statements” within the meaning of Section 27A of the Securities Act and Section 21E of the Exchange Act, and are subject to the safe harbor created thereby under the Private Securities Litigation Reform Act of 1995. Words such as “estimates,” “projected,” “expects,” “estimated,” “anticipates,” “projects,” “forecasts,” “plans,” “intends,” “believes,” “seeks,” “may,” “will,” “would,” “should,” “could,” “future,” “propose,” “target,” “goal,” “objective,” “outlook” and variations of these words or similar expressions (or the negative versions of such words or expressions) are intended to identify forward-looking statements. These forward-looking statements are not guarantees of future performance, conditions or results, and involve a number of known and unknown risks, uncertainties, assumptions and other important factors, many of which are outside the control of the parties, that could cause actual results or outcomes to differ materially from those discussed in the forward-looking statements. Important factors, among others, that may affect actual results or outcomes include:

| ● | changes to projected financial information or our ability to achieve our anticipated growth rate and execute on industry opportunities; |

| ● | our ability to maintain our existing relationships with customers and suppliers and to compete with existing and new competitors; |

| ● | various conflicts of interest that could arise among us, affiliates and investors; |

| ● | our success in retaining or recruiting, or changes required in, our officers, key employees or directors; |

| ● | factors relating to our business, operations and financial performance, including market conditions and global and economic factors beyond our control; |

| ● | the impact of the COVID-19 pandemic, geopolitical conflicts and related changes in base interest rates, inflation and significant market volatility on our business, the travel industry, travel trends and the global economy generally; |

| ● | the sufficiency of our cash, cash equivalents and investments to meet our liquidity needs; |

| ● | the effect of a prolonged or substantial decrease in global travel on the global travel industry; |

| ● | political, social and macroeconomic conditions (including the widespread adoption of teleconference and virtual meeting technologies which could reduce the number of in-person business meetings and demand for travel and our services); |

| ● | the effect of legal, tax and regulatory changes; and |

| ● | other factors detailed under the section entitled “Risk Factors.” |

The forward-looking statements contained in this prospectus are based on our current expectations and beliefs concerning future developments and their potential effects on us. There can be no assurance that future developments affecting us will be those that we have anticipated. These forward-looking statements involve a number of risks, uncertainties (some of which are beyond our control) or other assumptions that may cause actual results or performance to be materially different from those expressed or implied by these forward-looking statements. These risks and uncertainties include, but are not limited to, those factors described under the heading “Risk Factors” in this prospectus. Should one or more of these risks or uncertainties materialize, or should any of our assumptions prove incorrect, actual results may vary in material respects from those projected in these forward-looking statements. We undertake no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws.

xi

PROSPECTUS SUMMARY

This summary highlights selected information contained in this prospectus. This summary is not complete and does not contain all of the information that you should consider before making an investment decision. You should carefully read this entire prospectus, including the information presented under the sections titled “Risk Factors,” “Cautionary Statement Regarding Forward-Looking Statements,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the consolidated financial statements and the related notes thereto included elsewhere in this prospectus before making an investment decision. The definition of some of the terms used in this prospectus are set forth under the section “Selected Definitions.”

Company Overview

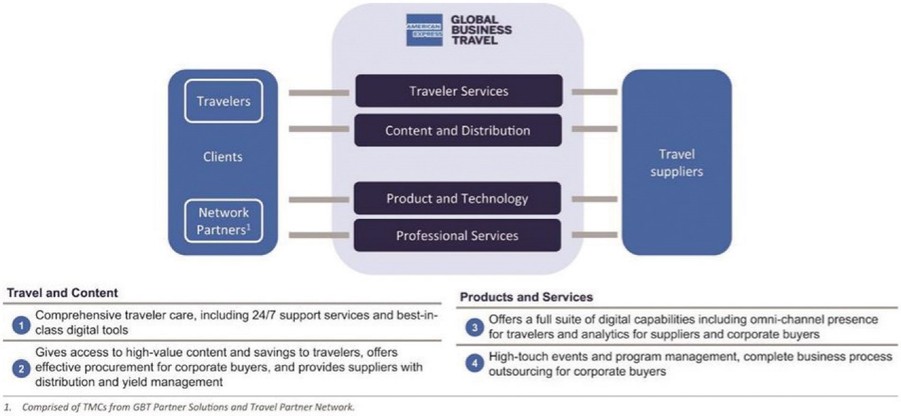

GBTG operates American Express Global Business Travel, the world’s leading B2B travel platform, measured by 2021 TTV, according to Travel Weekly (“2022 Power List,” June 2022, Travel Weekly). We provide a full suite of differentiated, technology-enabled solutions to business travelers and business clients, suppliers of travel content (such as airlines, hotels, ground transportation and aggregators) and third-party travel agencies. We differentiate our value proposition through our commitment to deliver to our customers unrivaled choice, value and experience, with the powerful backing of American Express GBT.

We are at the center of the global B2B travel ecosystem, managing the end-to-end logistics of business travel and providing an important link between businesses, their employees, travel suppliers and other industry participants. We service our clients in the following ways:

| ● | Our portfolio of travel management solutions, built around and targeting the needs of key client segments we serve, provide extensive access to flights, hotel rooms, car rentals and other travel services as well as meeting and events solutions, including exclusive negotiated content, supported by a full suite of services that allows our clients to design and operate an efficient travel program and solve complex travel requirements across all stages of the business process from planning, booking, on trip, and post trip activities. |

| ● | Our award-winning client facing proprietary platforms are built to deliver business value through optimized user experiences across the act of business travel. These platforms, accessible over web and mobile interfaces and powered by our data management infrastructure and built by one of the world’s largest product engineering teams dedicated to driving technical innovation across the business travel industry. These client facing platforms are known to the market as: |

| ● | Egencia primarily focuses on digital-first clients (more than 90% of transactions were served through digital channels in 2022) who value a simple, easy to use and standardized end-to-end solution. |

| ● | The GBT platform is a modular solution primarily focused on flexibility of service offerings; seamlessly integrating a wide range of third-party and proprietary software and services in to one complete travel solution designed and built around the needs of each customer. |

| ● | GBT Partner Solutions extends our platform to our Network Partners, TMCs and independent advisors, by offering them access to our differentiated content and technology. Through GBT Partner Solutions, we aggregate business travel demand serviced by our Network Partners at low incremental cost, which we believe enhances the economics of our platform, generates increased return on investment and expands our geographic and segment footprint. |

| ● | GBT Supply MarketPlace provides travel suppliers with efficient access to business travel clients serviced by our diverse portfolio of leading travel management solutions and Network Partners. We believe this access allows travel suppliers to benefit from premium demand (which we generally view as demand that is differentially valuable and profitable to suppliers) without incurring the costs associated with directly marketing to, and servicing the complex needs of, our business clients. Our travel supplier relationships generate efficiencies and cost savings that can be passed on to our business clients. |

In June 2014, American Express established the joint venture (“JV”) comprising the GBT JerseyCo operations with a predecessor of Juweel held by a group of institutional investors led by an affiliate of Certares. Since the formation of the JV in 2014, we have evolved from a leading TMC into a complete B2B travel platform, becoming one of the leading marketplaces in travel for business clients and travel suppliers according to Travel Weekly (“2022 Power List,” June 2022, Travel Weekly). Before June 2014, our operations were owned by American Express and primarily consisted of providing business travel solutions for business clients.

In May 2022, we executed long-term commercial agreements with American Express, including an amended and restated trademark license agreement (the “A&R Trademark License Agreement”), pursuant to which we continue to license the American Express trademarks used in the American Express Global Business Travel brand, and we license the American Express trademarks used in the American Express GBT Meetings & Events brand for business travel, meetings and events, business consulting and other

services related to business travel, in each case on an exclusive and worldwide basis. The term of the A&R Trademark License Agreement is for 11 years from the Closing Date, unless earlier terminated or extended.

The Business Combination

On May 25, 2022, APSG held an extraordinary general meeting of its shareholders at which the APSG Shareholders considered and adopted, among other matters, a proposal to approve the Business Combination pursuant to the terms of the Business Combination Agreement. Upon the completion of the Business Combination and the other transactions contemplated by the Business Combination Agreement on May 27, 2022, GBT JerseyCo became a direct subsidiary of APSG, with APSG being re-domesticated as a Delaware corporation and renamed “Global Business Travel Group, Inc.” and conducting its business through GBT JerseyCo in an umbrella partnership-C corporation structure.

As a result of the Business Combination, we raised gross proceeds of approximately $365 million, comprising (i) the contribution of approximately $42 million of cash held in the Trust Account from the APSG IPO, net of the redemption of APSG Class A Ordinary Shares held by APSG Shareholders of approximately $776 million and (ii) $323.5 million PIPE Investment at $10.00 per share of our Class A Common Stock. As a result of the Business Combination, we received net proceeds of approximately $128 million, net of transaction costs related to the Business Combination of approximately $69 million and redemption of approximately $168 million of GBT JerseyCo’s preferred shares (including dividend accrued thereon). See “Management’s Discussion and Analysis of Financial Condition and Results of Operations” elsewhere in this prospectus for more information.

There is no assurance whether or when the GBTG MIP Options may be exercised, which could impact our liquidity position. To the extent that the GBTG MIP Options are exercised on a “cashless basis,” the amount of cash we would receive from the exercise of the GBTG MIP Options will decrease. We believe the likelihood that GBTG MIP Option holders will exercise their GBTG MIP Options, and therefore the amount of cash proceeds that we would receive is, among other things, dependent upon the market price of our Class A Common Stock. If the market price for our Class A Common Stock is less than the applicable exercise price ($5.74 to $14.58 for the GBTG MIP Options), we believe such holders will be unlikely to exercise their GBTG MIP Options. We believe, based on our current operating plan, that our existing cash and cash equivalents, together with the Senior Secured Revolving Credit Facility, and cash flows from operating activities, will be sufficient to meet our anticipated cash needs for working capital, financial liabilities, capital expenditures and business expansion for at least the next 12 months.

The shares of Class A Common Stock being registered for resale in this prospectus represent a substantial percentage of our public float and of our outstanding shares of Class A Common Stock. The shares being registered in this prospectus (which include shares issuable upon exercise, conversion or exchange of other securities) exceed the total number of outstanding shares of Class A Common Stock (69,912,660 shares of Class A Common Stock outstanding as of April 21, 2023). In addition, the securities beneficially owned by Continuing JerseyCo Owners, holders of GBTG MIP Options and holders of GBT MIP Shares represent over 80% of the total outstanding shares of Class A Common Stock, and these holders will have the ability to sell all of their shares pursuant to the registration statement of which this prospectus forms a part so long as it is available for use. The sale of the securities being registered in this prospectus therefore could result in a significant decline in the public trading price of Class A Common Stock.

The PIPE Investment

Pursuant to subscription agreements entered into in connection with the Business Combination Agreement and funded at the Closing, certain investors subscribed for an aggregate of 32,350,000 newly-issued shares of Class A Common Stock at a purchase price of $10.00 per share for an aggregate purchase price of $323.5 million. At the Closing, the Company consummated the PIPE Investment.

As of the date of this prospectus, we have 69,912,660 shares of Class A Common Stock issued and outstanding, 394,448,481 shares of Class B Common Stock issued and outstanding, 21,402,684 GBTG MIP Options to purchase Class A Common Stock issued and outstanding.

Earnout

In connection with the Closing, 15 million “earnout” shares were issued to the holders of GBT JerseyCo Capital Stock and GBT Legacy MIP Options. Each earnout share is in the form of GBT JerseyCo C Ordinary Share. The earnout shares are subject to earnout achievement milestones based on the dollar VWAP of the Class A Common Stock.

2

Summary of Risk Factors

In addition to the other information contained in this prospectus, the following risks have the potential to impact our business and operations. An investment in our securities involves a high degree of risk. You should consider carefully all of the risks described in this prospectus, together with the other information contained in this prospectus. These risk factors are not exhaustive and all investors are encouraged to perform their own investigation with respect to our business, financial condition and prospects. The occurrence of any of the following risks or additional risks and uncertainties not presently known to us or that we currently believe are immaterial could have a material adverse effect on our business, financial condition, results of operations and prospects. In that event, the trading price of our securities could decline, and you could lose all or part of your investment. Such risks include, but are not limited to, the following:

Risks Relating to Our Business and Industry

| ● | The COVID-19 pandemic has had, and may continue to have, an adverse impact on our business, including our financial results and prospects, and the travel suppliers on which our business relies. |

| ● | The ongoing impact of the COVID-19 pandemic on our business and the impact on our results of operations is uncertain. |

| ● | Our revenue is derived from the global travel industry, and a prolonged or substantial decrease in global travel, particularly air travel, could adversely affect us. |

| ● | The widespread adoption of teleconference and virtual meeting technologies could reduce the number of in-person business meetings and demand for travel and our services, which could adversely affect our business, financial condition and results of operations. |

| ● | The travel industry is highly competitive. |

| ● | Consolidation in the travel industry may result in lost bookings and reduced revenue. |

| ● | Our business and results of operations may be adversely affected by macroeconomic conditions. |

| ● | Downturns in domestic or global economic conditions, or other macroeconomic factors more generally, could have adverse effects on our results of operations. |

| ● | Our international business exposes us to geopolitical and economic risks associated with doing business in foreign countries. |

Risks Relating to Our Indebtedness

| ● | Our indebtedness could adversely affect our business and growth prospects. |

| ● | The terms of the Senior Secured Credit Agreement restrict our current and future operations, particularly our ability to respond to changes or to take certain actions. |

Risks Relating to Our Dependence on Third Parties

| ● | If we are unable to maintain existing, and establish new, arrangements with travel suppliers, or if our travel suppliers and partners reduce or eliminate the commission and other compensation they pay us, our business and results of operations would be negatively impacted. |

| ● | Our business and results of operations could be adversely affected if one or more of our major travel suppliers suffers a deterioration in its financial condition or restructures its operations or, as a result of consolidation in the travel industry, loses bookings and revenue. |

3

Risks Relating to Employee Matters, Managing Our Growth and Other Risks Relating to Our Business

| ● | Our ability to identify, hire and retain senior management and other qualified personnel is critical to our results of operations and future growth. |

Risks Relating to Intellectual Property, Information Technology, Data Security and Privacy

| ● | Any termination of the A&R Trademark License Agreement for rights to the American Express trademarks used in our business, including failure to renew the license upon expiration, could adversely affect our business and results of operations. |

| ● | Any failure to maintain or enhance the reputation of our brands, including brands in which we use the licensed American Express trademarks, could adversely affect our business and results of operations. |

| ● | We rely on information technology to operate our business. System interruptions, defects and slowdowns, including with respect to information technology provided by third parties, may cause us to lose travelers or business opportunities or to incur liabilities. |

| ● | Our processing, storage, use and disclosure of personal data, including of travelers and our employees, exposes us to risks stemming from possible failure to comply with governmental law and regulation and other legal obligations. |

| ● | Cybersecurity attacks or security breaches could adversely affect our ability to operate, could result in personal information and our proprietary information being lost, stolen, made inaccessible, improperly disclosed or misappropriated and may cause us to be held liable or subject to regulatory penalties and sanctions and to litigation (including class action litigation), which could have a material adverse effect on our reputation and business. |

Risks Relating to Regulatory, Tax and Litigation Matters

| ● | We are subject to taxes in many jurisdictions globally. |

Risks Relating to Our Organization and Structure

| ● | We conduct certain of our operations through joint ventures where we are generally the majority owner, but in some cases, we have only a minority interest. Disagreements with our partners could adversely affect our interest in the joint ventures. |

| ● | The interests of the Continuing JerseyCo Owners may not always coincide with our interests or the interests of our other stockholders and may result in conflicts of interest. |

| ● | GBTG is a holding company, the principal asset of which is an equity interest in GBT JerseyCo and GBTG’s ability to pay taxes and expenses will depend on distributions made by its subsidiaries and may be otherwise limited by our structure and the terms of our existing and future indebtedness. |

Risks Relating to Our Securities

| ● | The market price of the Class A Common Stock may be volatile and could decline significantly. |

Corporate Information

Our website address is www.amexglobalbusinesstravel.com. The information on, or that can be accessed through, our website is not part of this prospectus, and you should not consider information contained on our website in deciding whether to purchase shares of our Class A Common Stock.

Our principal executive office is located at 666 3rd Avenue, 4th Floor, New York, NY 10017. Our telephone number is (480) 909-1740.

4

THE OFFERING

Issuer |

| Global Business Travel Group, Inc. |

Issuance of Class A Common Stock | ||

Total shares of Class A Common Stock issuable upon the exercise of all GBTG MIP Options | 21,402,684 shares | |

Use of proceeds | We will receive up to an aggregate of approximately $151,362,316 million from the exercise of all GBTG MIP Options, assuming the exercise in full of all such options for cash. We expect to use the net proceeds from such exercises for general corporate purposes, which may include acquisitions and other business opportunities and the repayment of indebtedness. To the extent that the GBTG MIP Options are exercised on a “cashless basis,” the amount of cash we would receive from the exercise of the GBTG MIP Options will decrease. We believe the likelihood that GBTG MIP Option holders will exercise their GBTG MIP Options, and therefore the amount of cash proceeds that we would receive is, among other things, dependent upon the market price of our Class A Common Stock. If the market price for our Class A Common Stock is less than the applicable exercise price ($5.74 to $14.58 for the GBTG MIP Options), we believe such holders will be unlikely to exercise their GBTG MIP Options. See the section of this prospectus titled “Use of Proceeds” appearing elsewhere in this prospectus for more information. | |

Resale of Class A Common Stock | ||

Shares of Class A Common Stock that may be offered and sold from time to time by the Selling Securityholders | 466,649,054 shares of Class A Common Stock | |

Use of proceeds | All of the shares of Class A Common Stock offered by the Selling Securityholders pursuant to this prospectus will be sold by the Selling Securityholders for their respective accounts. We will not receive any of the proceeds from such sales. | |

Transfer Restrictions | The shares of Class A Common Stock issued upon conversion of the Founder Shares are subject to transfer restrictions pursuant to the Sponsor Side Letter. The Sponsor and the Insiders are not permitted to transfer such shares of Class A Common Stock, subject to certain permitted exceptions, until the earlier to occur of (a) one year following the Closing and (b) the date which the VWAP of Class A Common Stock exceeds $12.00 per share for any 20 trading days within a period of 30 consecutive trading days. See the section titled “Certain Relationships and Related Party Transactions — GBT Related Party Transactions — Sponsor Side Letter Amendment.” | |

Dividend Policy | We have not paid any cash dividends on our Class A Common Stock to date. The payment of any cash dividends in the future will be within the discretion of our Board at such time. |

5

Furthermore, our ability to pay dividends is limited by the Senior Secured Credit Agreement and may be limited by covenants under other indebtedness we and our subsidiaries incur in the future, as well as other limitations and restrictions imposed by law. We currently expect to retain future earnings to finance operations and grow our business, and we do not expect to declare or pay cash dividends for the foreseeable future. Pursuant to the Senior Secured Credit Agreement, so long as GBT JerseyCo is treated as a partnership or a disregarded entity for U.S. federal income tax purposes, GBT JerseyCo may make Tax Distributions (as defined and set forth in the Shareholders Agreement after the effectiveness thereof), subject to certain limitations on future amendments, if any, to the Shareholders Agreement and certain restrictions on making Tax Distributions with respect to any income included under Section 965(a) of the Code. GBTG may receive tax distributions from GBT JerseyCo significantly in excess of its tax liabilities. If we become a guarantor under the Senior Secured Credit Agreement, then our ability to make dividends on the Class A Common Stock in the amount of any excess cash balances from such tax distributions, as well as certain other cash dividends, would be subject to fixed-dollar caps set forth in the Senior Secured Credit Agreement in the event that the total leverage ratio (calculated in a manner set forth in the Senior Secured Credit Agreement) would be greater than 3.00:1.00 after giving pro forma effect to such dividends. If we do not become a guarantor, then the ability of our subsidiaries to make certain cash dividends to us will be subject to similar restrictions. | ||

NYSE Symbol | “GBTG” for our Class A Common Stock. | |

Risk Factors | See the section titled “Risk Factors” beginning on page 7 of this prospectus and other information included in this prospectus for a discussion of factors that you should consider carefully before deciding to invest in our Class A Common Stock. |

6

RISK FACTORS

An investment in our securities involves a high degree of risk In addition to the other information contained in this prospectus, the following risks have the potential to impact our business and operations. These risk factors are not exhaustive and all investors are encouraged to perform their own investigation with respect to our business, financial condition and prospects. The occurrence of any of the following risks or additional risks and uncertainties not presently known to us or that we currently believe are immaterial could have a material adverse effect on our business, financial condition, results of operations and future growth prospects. The trading price of our securities could decline due to any of these risks, and, as a result, you may lose all or part of your investment.

Risks Relating to Our Business and Industry

The COVID-19 pandemic has had, and may continue to have, an adverse impact on our business, including our financial results and prospects, and the travel suppliers on which our business relies.

In response to the COVID-19 pandemic, many governments around the world implemented, and continue to implement, a variety of measures to reduce the spread of COVID-19, including travel restrictions and bans, instructions to residents to practice social distancing, quarantine advisories, shelter-in-place orders, required closures of non-essential businesses and additional restrictions on businesses as part of re-opening plans. These government mandates have had a significant negative impact on the travel industry and many of the travel suppliers on which our business relies, as well as on our workforce, operations and clients. While restrictions have been fully or partly lifted in many geographies, some restrictions remain in place or may be reinstated in the future. There remains uncertainty around when remaining restrictions will be lifted, the potential impact of the new variants of COVID-19, if additional restrictions may be initiated, if there will be changes to travel behavior patterns when government restrictions are fully lifted, the continued efficacy of existing vaccines and other preventative therapies against the new variants and the timing of distribution and administration of vaccines and other preventative therapies globally.

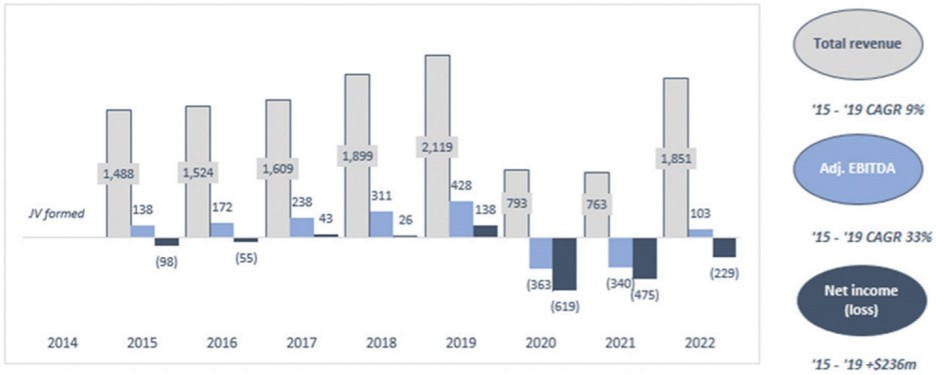

The COVID-19 pandemic and the resulting economic conditions and government orders forced many of our travel suppliers, including airlines and hotels, to pursue cost reduction measures and seek financing, including government financing and support, in order to reduce financial distress and continue operating, and to curtail drastically their service offerings. The COVID-19 pandemic has resulted, and may continue to result, in the restructuring or bankruptcy of certain of those travel suppliers, and renegotiation of the terms of our agreements with them. In addition, the COVID-19 pandemic resulted in a material decrease in business and consumer spending and an unprecedented decline in transaction volumes in the global travel industry. Our financial results and prospects are largely dependent on these transaction volumes. As a result, our financial results for the years ended December 31, 2022, 2021 and 2020 were significantly and negatively impacted, with a material decline in total revenues, net income, cash flow from operations and Adjusted EBITDA (as defined in “Selected Definitions”) as compared to 2019, our last year of normalized operations. Our revenue for the years ended December 31, 2022, 2021 and 2020 was $1,851 million, $763 million and $793 million, respectively, compared to revenue of $2,119 million for the year ended December 31, 2019. Further, (i) we incurred a net loss of $229 million, $475 million and $619 million for the years ended December 31, 2022, 2021 and 2020, respectively, compared to a net income of $138 million for the year ended December 31, 2019, (ii) we had cash outflow from operations of $394 million, $512 million and $250 million for the years ended December 31, 2022, 2021 and 2020, respectively, compared to cash inflow from operations of $227 million for the year ended December 31, 2019 and (iii) our Adjusted EBITDA was $103 million, $(340) million and $(363) million for the years ended December 31, 2022, 2021 and 2020, respectively, compared to Adjusted EBITDA of $428 million for the year ended December 31, 2019.

Starting late in the fourth quarter of 2020, initial COVID-19 vaccines were approved for widespread distribution across the world. With vaccination programs well advanced in many countries, many governments around the world have lifted restrictions and transaction volumes in the global travel industry have experienced a material recovery. During the three months ended December 31, 2022, transaction volumes, including Egencia and Ovation, were approximately 72% of 2019 levels. However there remains uncertainty around the path to full economic and travel recovery from the COVID-19 pandemic. As a result, we are unable to predict accurately the impact that the COVID-19 pandemic will have on our business going forward. While travel has historically been resilient to macroeconomic events, with the continued spread of COVID-19 and other variants throughout the world, the COVID-19 pandemic and its effects could continue to have an adverse impact on our business, financial condition, results of operations and cash flows for the foreseeable future.

7

The ongoing impact of the COVID-19 pandemic on our business and the impact on our results of operations is uncertain.