As filed with the U.S. Securities and Exchange Commission on February 16, 2022.

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

(Exact name of Registrant as specified in its Charter)

Japan |

| 8000 |

| Not Applicable |

(State or other jurisdiction of | (Primary Standard Industrial | (I.R.S. Employer |

MEDIROM Healthcare Technologies Inc.

2-3-1 Daiba, Minato-ku

Tokyo 135-0091, Japan

Tel: +81-(0)3-6721-7364

Fax: +81-(0)3-6721-7365

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Cogency Global Inc.

122 East 42nd Street, 18th Floor

New York, NY 10168

Tel: (800) 221-0102

(Name, address, including zip code, and telephone number, including area code, of agent for service)

With copies to:

Barbara A. Jones |

| Koji Ishikawa Meiji Yasuda Seimei Building, 14F |

| Barry Grossman |

1840 Century Park East, Suite 1900 | 2-1-1 Marunouchi, Chiyoda-ku | Matthew Bernstein | ||

Tel: (310) 586-7773 Fax: (310) 586-0273 | Tokyo 100-0005, Japan Tel: +81(0)3-4510-2200 Fax: +81(0)3-4510-2201 | 1345 Avenue of the Americas Fax: (212) 370-7889 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after this registration statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ☐

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the Registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933.

Emerging Growth Company ☒

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the Registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the Registration Statement shall become effective on such date as the U.S. Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

† | The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012. |

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the U.S. Securities and Exchange Commission is declared effective. This preliminary prospectus is not an offer to sell these securities, nor a solicitation of an offer to buy these securities, in any jurisdiction where the offer, solicitation, or sale is not permitted.

SUBJECT TO COMPLETION, DATED FEBRUARY 16, 2022

PRELIMINARY PROSPECTUS

MEDIROM Healthcare Technologies, Inc.

800,000 American Depositary Shares

Representing 800,000 Common Shares

We are offering American 800,000 Depositary Shares (which we refer to as “ADSs”) representing our common shares, no par value (which we refer to as our “common shares”).

ADSs representing our common shares are listed on The Nasdaq Capital Market under the symbol “MRM.” The last reported sale price of the ADSs on The Nasdaq Capital Market on February 10, 2022 was $7.02 per ADS.

We are organized under the laws of Japan and are an “emerging growth company”, as defined in the Jumpstart Our Business Startups Act of 2012, under applicable U.S. federal securities laws, and are eligible for reduced public company reporting requirements. See “Prospectus Summary — Emerging Growth Company Status.”

Kouji Eguchi, our Chief Executive Officer and director, owns one Class A common share, or “golden share,” with key veto rights, which may limit a shareholder’s ability to influence our business and affairs, including, among others, amendments to our articles of incorporation and the issuance of additional common shares. See “Risk Factors” and “Description of Shares Capital and Articles of Incorporation — Special Voting and Consent Rights — Class A Voting Rights.”

Investing in the ADSs involves a high degree of risk. Before buying any of the ADSs, you should carefully read the discussion of material risks of investing in the ADSs in “Risk Factors” beginning on page 18 of this prospectus.

Neither the U.S. Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| Per ADS |

| Total | |||

Offering price | $ | · | $ | · | ||

Underwriting discounts and commissions(1) | $ | · | $ | · | ||

Proceeds to us (before expenses) | $ | · | $ | · | ||

| (1) | See “Underwriting — Commissions and Discounts” for additional information regarding compensation payable to the underwriters. |

We have granted the underwriters an option to purchase up to 120,000 additional ADSs from us at the public offering price, less underwriting discounts and commissions, for 45 days after the date of this prospectus to cover over-allotments, if any.

The underwriters expect to deliver the ADSs to purchasers on or about ·, 2022.

Maxim Group LLC

The date of this prospectus is ·, 2022.

TABLE OF CONTENTS

Page | |

2 | |

3 | |

13 | |

18 | |

41 | |

42 | |

43 | |

44 | |

SELECTED CONSOLIDATED FINANCIAL INFORMATION AND OPERATING DATA | 46 |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 49 |

70 | |

88 | |

90 | |

96 | |

97 | |

98 | |

105 | |

113 | |

114 | |

119 | |

125 | |

126 | |

126 | |

126 | |

126 | |

F-1 |

You should rely only on the information contained in this prospectus and any free writing prospectus prepared by us. Neither we nor the underwriters have authorized anyone to provide you with information that is different, and neither we nor the underwriters take any responsibility for, and provide any assurance as to the reliability of, any information, other than the information in this prospectus and any free writing prospectus prepared by us. We are offering to sell the ADSs, and seeking offers to buy the ADSs, only in jurisdictions where such offers and sales are permitted. This prospectus is not an offer to sell, or a solicitation of an offer to buy, the ADSs in any jurisdictions where, or under any circumstances under which, the offer, sale, or solicitation is not permitted. The information in this prospectus and in any free writing prospectus prepared by us is accurate only as of the date on its respective cover, regardless of the time of delivery of this prospectus or any free writing prospectus or the time of any sale of the ADSs. Our business, results of operations, financial condition, or prospects may have changed since those dates.

Before you invest in the ADSs, you should read the registration statement (including the exhibits thereto and the documents incorporated by reference therein) of which this prospectus forms a part.

For investors outside of the United States:Neither we nor the underwriters have done anything that would permit this offering, or the possession or distribution of this prospectus, in any jurisdiction where action for that purpose is required, other than in the United States. You are required to inform yourselves about, and observe any restrictions relating to, this offering and the distribution of this prospectus.

i

ABOUT THIS PROSPECTUS

As used in this prospectus, unless the context otherwise requires or otherwise states, references to “Medirom,” our “Company,” “we,” “us,” “our,” and similar references refer to MEDIROM Healthcare Technologies Inc., a joint stock corporation with limited liability organized under the laws of Japan, and its subsidiaries.

Our functional currency and reporting currency is the Japanese yen (which we refer to as “JPY” or “¥”). The terms “dollar,” “USD,” “US$” or “$” refer to U.S. dollars, the legal currency of the United States. Convenience translations included in this prospectus of Japanese yen into U.S. dollars have been made at the exchange rate of ¥111.0500 = US$1.00, which was the foreign exchange rate on June 30, 2021 as reported by the Board of Governors of the Federal Reserve System (which we refer to as the “U.S. Federal Reserve”) in its weekly release on July 6, 2021. Historical and current exchange rate information may be found at www.federalreserve.gov/releases/h10/.

Our financial statements are prepared in accordance with U.S. generally accepted accounting principles (which we refer to as “U.S. GAAP”). Our fiscal year ends on December 31 of each year as does our reporting year. Therefore, any references to 2020 and 2019 are references to the fiscal and reporting years ended December 31, 2020 and December 31, 2019, respectively. Our most recent fiscal year ended on December 31, 2020. See Note 1 to our audited consolidated financial statements as of and for the years ended December 31, 2020 and 2019 included elsewhere in this prospectus, for a discussion of the basis of presentation and translation of financial statements.

We have made rounding adjustments to some of the figures included in this prospectus. Accordingly, numerical figures shown as totals in some tables may not be an arithmetic aggregation of the figures that precede them.

Non-GAAP Financial Measures

In addition to U.S. GAAP measures, we also use Adjusted EBITDA and Adjusted EBITDA Margin, as described under “Management’s Discussion and Analysis of Financial Condition and Results of Operations — Non-GAAP Financial Measures”, in various places in this prospectus. These financial measures are presented as supplemental disclosure and should not be considered in isolation of, as a substitute for, or superior to, the financial information prepared in accordance with U.S. GAAP, and should be read in conjunction with our consolidated financial statements and the notes thereto included elsewhere in this prospectus. Adjusted EBITDA and Adjusted EBITDA Margin may differ from similarly titled measures presented by other companies.

Please see “Selected Consolidated Financial Information and Operating Data” for a reconciliation of non-GAAP financial measures to the most directly comparable financial measure calculated in accordance with U.S. GAAP.

Market and Industry Data

This prospectus contains references to market data and industry forecasts and projections, which were obtained or derived from publicly available information, reports of governmental agencies, market research reports, and industry publications and surveys. These sources generally state that the information contained therein has been obtained from sources believed to be reliable, but that the accuracy and completeness of that information is not guaranteed. Although we believe such information to be accurate, we have not independently verified the data from these sources. Forecasts and other forward-looking information obtained from these sources are subject to the same qualifications and additional uncertainties and risks regarding the other forward-looking statements in this prospectus due to a variety of factors, including those described in the section entitled “Cautionary Note Regarding Forward-Looking Statements” and “Risk Factors” and elsewhere in this prospectus. These and other factors could cause results to differ materially from those expressed in the forecasts and estimates.

1

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

Various statements contained in this prospectus, including those that express a belief, expectation or intention, as well as those that are not statements of historical fact, are forward-looking statements. These forward-looking statements may include projections and estimates concerning our possible or assumed future results of operations, financial condition, business strategies and plans, market opportunity, competitive position, industry environment, and potential growth opportunities. In some cases, you can identify forward-looking statements by terms such as “may”, “will”, “should”, “believe”, “expect”, “could”, “intend”, “plan”, “anticipate”, “estimate”, “continue”, “predict”, “project”, “potential”, “target,” “goal” or other words that convey the uncertainty of future events or outcomes. You can also identify forward-looking statements by discussions of strategy, plans or intentions. We have based these forward-looking statements on our current expectations and assumptions about future events. While our management considers these expectations and assumptions to be reasonable, because forward-looking statements relate to matters that have not yet occurred, they are inherently subject to significant business, competitive, economic, regulatory and other risks, contingencies and uncertainties, most of which are difficult to predict and many of which are beyond our control. These and other important factors, including, among others, those discussed in this prospectus under the headings “Risk Factors”, “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “Our Business”, may cause our actual results, performance or achievements to differ materially from any future results, performance or achievements expressed or implied by the forward-looking statements in this prospectus. Some of the factors that could cause actual results to differ materially from those expressed or implied by the forward-looking statements in this prospectus include:

| ● | our ability to attract and retain customers; |

| ● | our ability to successfully enter new markets and manage our business expansion; |

| ● | our ability to develop or acquire new products and services, improve our existing products and services and increase the value of our products and services in a timely and cost-effective manner; |

| ● | our ability to compete in the relaxation salon market; |

| ● | our expectations regarding our customer growth rate and the usage of our services; |

| ● | our ability to increase our revenues and our revenue growth rate; |

| ● | our ability to timely and effectively scale and adapt our existing technology and network infrastructure; |

| ● | our ability to successfully acquire and integrate companies and assets; |

| ● | our ability to respond to national disasters, such as earthquakes and tsunamis, and to global pandemics, such as COVID-19; |

| ● | our future business development, results of operations and financial condition; and |

| ● | the regulatory environment in which we operate. |

Given the foregoing risks and uncertainties, you are cautioned not to place undue reliance on the forward-looking statements in this prospectus. The forward-looking statements contained in this prospectus are not guarantees of future performance and our actual results of operations and financial condition may differ materially from such forward-looking statements. In addition, even if our results of operations and financial condition are consistent with the forward-looking statements in this prospectus, they may not be predictive of results or developments in future periods.

Any forward-looking statement that we make in this prospectus speaks only as of the date of this prospectus. Except as required by law, we do not undertake any obligation to update or revise, or to publicly announce any update or revision to, any of the forward-looking statements in this prospectus, whether as a result of new information, future events or otherwise, after the date of this prospectus.

2

PROSPECTUS SUMMARY

This summary highlights selected information presented in greater detail elsewhere in this prospectus. This summary does not include all the information you should consider before investing in the ADSs. You should read this summary together with the more detailed information appearing elsewhere in this prospectus, including our audited and unaudited financial statements and related notes and the sections entitled “Risk Factors” on page 18 and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” elsewhere in this prospectus. Some of the statements in this summary and elsewhere in this prospectus constitute forward-looking statements. See “Cautionary Note Regarding Forward-looking Statements.”

Business Overview

MEDIROM Healthcare Technologies Inc., which we refer to in this prospectus as Medirom, is one of the leading holistic health services providers in Japan. Medirom is a franchiser and operator of healthcare salons across Japan and is a preferred platform partner for health insurance providers under the government health insurance system to affect positive health outcomes. Through our well-known retail salon brands, including primarily Re.Ra.Ku®, nascent tech platforms, and targeted health consulting and marketing, we have formed a “healthtech” segment. The healthtech segment’s goal is to improve health outcomes and the satisfaction of our customers.

3

We operate two synergistic lines of businesses: (1) Relaxation Salon Segment (retail); and (2) Digital Preventative Healthcare Segment (healthtech). By combining brand strength and core retail competencies, including a broad physical footprint in population dense areas across the country, with proprietary technologies and partnerships, our business provides unique, value-added healthcare services to our customers with scale, customization, and cross-network effects that we believe few other companies in the industry can emulate.

Our core business is the operation and franchising of relaxation salons in Japan. Our salon locations cover major cities throughout Japan, with strong market presence in the Tokyo metropolitan area, which includes Tokyo, Yokohama, and Saitama. Our goal is to improve our customers’ quality of life by providing alternative, non-invasive wellness care. We use therapeutic techniques encompassing finger-pressure style bodywork therapy, stretch therapy, posture and joint alignment, as well as physical therapy elements. Our salons are designed to appeal to individuals seeking to improve their mental and/or physical well-being. Our customers vary from individuals seeking stress and pain relief to other individuals who are just looking to improve their overall mental and physical health. We offer a variety of individual services at our salons, including anti-fatigue therapy, athletic support therapy, slim-down therapy and reflexology. Each therapy is unique and designed to target specific areas of the body.

As of December 31, 2021, the Relaxation Salon Segment has 312 locations across major cities in Japan. Our customer management system is a cloud-based customer relationship management system which we use to record customer data and which facilities reservation, point-of-sale and business intelligence functions. Our salons are generally located in train and subway stations, shopping malls, plazas and high-traffic streets. The Relaxation Salon Segment is our core business and accounted for ¥3,865 million (US$34.8 million), or substantially all of our total revenue for the year ended December 31, 2019, ¥3,316 million (US$29.9 million), or substantially all of our total revenue for the year ended December 31, 2020, ¥1,345 million (US$12.1 million), or substantially all of our total revenue for the six months ended June 30, 2020 and ¥2,111 million (US$19.0 million), or substantially all of our total revenue for the six months ended June 30, 2021.

The Digital Preventative Healthcare Segment is a business line that we expect to grow and accounted for approximately 1% of our total revenue for the years ended December 31, 2019 and 2020 and for the six months ended June 30, 2020 and 2021. The Digital Preventative Healthcare Segment mainly consists of the following operations: government-sponsored Specific Health Guidance program, utilizing our internally- developed on-demand health monitoring smartphone application, Lav®; our MOTHER Bracelet™ (formerly known as MOTHER Tracker®) for fitness applications; and preventative healthcare services utilizing our digital application and devices.

Competitive Strengths

We are a defined leader in Japan’s health and wellness space. We provide ground-up educational and training services for aspiring specialists, as well as top of the line health services for our customers. As we continue to grow and expand, the brand recognition that we enjoy across Japan will help promote our new digital business lines. We believe the following strengths have contributed to our initial success and will position us well for future growth:

Innovative Services. Our salon services are innovative and differ from traditional shiatsu-style bodywork. For example, we created our unique wing stretch method, which focuses especially on the shoulder blades. This is important because the shoulder blades are a critical part of the body, as they connect and balance the bones from the neck to the lower back and support the body to ensure the body moves smoothly. Further, traditional shiatsu-style bodywork therapists typically use their body weight to put pressure on the muscles, which can cause damage. Our relaxation therapists use stretch techniques on the muscles, rather than body weight pressure, thereby preventing damage. We believe our non-pressure method mitigates the risk of severe malpractice and other similar

4

claims. Finally, our relaxation therapists are trained to converse with our customers, to ask our customers questions in order to tailor the therapy to the customers’ unique needs, and to promote self-care by communicating with our customers about their current body ailments and to give advice for future visits.

Brand Value. We believe our trademarks and other intellectual property create a strong competitive advantage in both our Relaxation Salon Segment and Digital Preventative Healthcare Segment. With widespread recognition in the Kanto region and across Japan, our Company benefits from a loyal customer base and brand recognition that allows for smooth scaling of growth businesses.

Employee Satisfaction. We employ a majority of our therapists on a salaried basis, rather than a commission-based contractor model normally used in the industry. We have also invested culturally and economically in creating a career progression for therapists, which helps give structure, purpose, and incentives to stay with the Company and improve skills. While this increases our operating leverage, we believe it a core strategic need and advantage as labor is a key gating factor currently in the relaxation sector. We believe that our industry-leading employee satisfaction levels, which is evidenced by the fact that we were awarded the Grand Prix for the relaxation sector's top therapist and best store award in Japan in 2019, as well as the Semi-Grand Prix for the individual therapist and the Grand Prix for the best store award in 2021. contributed to employees’ high morale. This is particularly important as high turnover reduces or disrupts available investment in capital because of the costs associated with hiring and training new employees. In August 2020, we started an online exit survey for our leaving employees, including franchisees’ employees, to better assess the reasons for employee turnover. We continue to optimize our work environment for therapists in an effort to improve morale, productivity and a long-term commitment to work and promotion within our Company.

Hiring Activities. We own and run our own job portal website targeting prospective therapist candidates. The job portal website was launched on February 1, 2020, and during the first half of 2021, 41.2% of our new therapists have been hired through the site. As labor shortages and costly recruiting of therapists remain the primary gating factors for a successful salon operation, we believe our streamlined and cost-efficient recruiting method allows continued operating strength at expanded profit margins. Combined with our brand, this hiring approach at scale puts us in an advantageous position relative to our peers in the industry.

Re.Ra.Ku® College. We believe we own the largest in scale and best in class education and training facility for relaxation therapists in the Japanese relaxation industry, which enables us to provide continuous training to our franchise owners and salon staff, as well as continuous direct access to a pool of newly trained and job-ready staff. We believe that regular training ensures that quality service and therapy are consistently provided to our customers throughout all of our salons. The strength of our Company’s training and education program is in providing our therapists learning opportunities to keep improving their service skills after commencing at our Company’s salons. Medirom requires a higher threshold of training before allowing students to work with our clients in our salons. We find that this rigorous skill grading system better prepares our students and has proven effective for our salons. We provide one of the longest training programs (54 hours) in the industry. Each training module can be taken randomly, rather than in a series, for the trainees’ convenience. Moreover, we provide the follow-up training courses, based on which we evaluate and grade the practitioners’ skills. We believe this is a different approach from certain of our competitors, who tend to utilize practitioners on a contract basis. Our training package enables our therapists to improve their treatment skills continuously and, importantly, to maintain high morale.

5

Specific Health Guidance Program. As a leading provider of holistic health services, we support the government-initiated program, Specific Health Guidance Program. Other notable supporters include SOMPO Health Support, Benefit One Inc., and FitsPlus Inc. As a government (Ministry of Health, Labour and Welfare)-subsidized program, participating companies need to maintain quality controls. Partners and service providers are vetted and must adhere to standards that are established by each of the health insurance providers. By satisfying each standard, we have been engaged in supporting the program by health insurance providers and continues to expand its prospective clients. In addition, we have an on-demand health monitoring application, Lav®, which can provide user-friendly interfaces and experiences. This application, among other digital tools, allows for seamless functionality with our partners and service providers as well as optionality in future monetization of the end user base. As a result, we have successfully managed to acquire several corporate clients, including blue chip companies’ and local governments’ health insurance providers. We believe this B2G/B2B business provides opportunities for multi-year contracts and high margins, particularly given the significant barriers to entry that require a well-recognized health and consumer brand and blue-chip enterprise relationships. We launched the upgraded version of Lav® as a subscription- based B2C application on July 1, 2021. The updated Lav® application offers menus such as detox, weight control, and exercise programs.

Until recently, the goals of health checkups and health guidance have been early identification and treatment of sickness. By focusing on visceral-fat obesity, specific health checkups and specific health guidance are intended to decrease the numbers of those who suffer from, or are at risk for, lifestyle-related conditions such as diabetes, through providing health guidance to help them improve the living habits that cause visceral-fat obesity (i.e., disease prevention). Since lifestyle-related conditions progress with no visible symptoms, specific health checkups, which are comprised of health screenings intended to identify those who require health guidance to prevent lifestyle-related conditions, are considered to be an excellent opportunity to review the individual’s living habits. Health guidance is provided to help the individual change his or her behavior. All those who have undergone specific health checkups are provided with information suited to their own individual circumstances.

Based on the results of specific health checkups, persons eligible for specific health guidance are identified by level (that is, those eligible for motivational support and those eligible for active support) in accordance with their risk levels, by focusing on the degree of visceral fat buildup and numbers of risk factors. The goals of specific health guidance are to enable eligible persons to be aware of their own health conditions and make voluntary efforts, on a continual basis, to improve their own living habits. Participants are provided with a variety of motivational information and advice to help them live healthier lifestyles on their own. Motivational support provides support to encourage improvements in living habits, in principle, one time. An action plan is prepared with the guidance of doctors, health nurses, and a senior nutritionist; specialists provide motivational support for efforts to improve living habits. Evaluations are performed to determine whether results have been achieved as planned.

Active support provides continual support in multiple sessions over three months or longer. An action plan is prepared with the guidance of doctors, health nurses, and a senior nutritionist. We retain several experienced nutritionists and healthcare professionals, by entering into service agreements with workers dispatching companies. These therapists and nutritionists help provide an integrated bodywork (physical body), encouragement and inspiration (mental), and dietary guidelines (metabolic/diet). Specialists provide regular, continual support for efforts to improve living habits over a period of three months or longer.

6

We have received subscription orders from 43 corporate insurance associations for our Specific Health Guidance Program as of December 31, 2021. Other individual consumers can also purchase the program and access it via the upgraded Lav® app. For the consumer version of the Lav® app, we expect to engage our in-house therapists as coaches to increase such therapists’ income. We also aim to leverage our existing salon customer base to accelerate the program’s development.

MOTHER Bracelet™. Our MOTHER Bracelet™ fitness device is designed to track and collect the health data of the wearer, such as calorie consumption, activity and sleep patterns. We believe our MOTHER Bracelet™ will be the only fitness tracker that requires no electric charging as it will utilize innovative technology such as Gemini TEG (Thermoelectric Generator) and Mercury Boost Converter to enable the user’s body heat to generate electricity. We are not aware of any other wearable devices equipped with NFC currently in the market with equivalent capabilities at this time. We believe we are the first relaxation salon operator in Japan to launch a health-monitoring wearable device. We believe our MOTHER Bracelet™ is an important complement to our holistic approach to providing health services.

In June 2020, we received a pre-order for the MOTHER Bracelet™ from Kansai Medical University Hospital (headquartered in Osaka, Japan) for the purpose of health and activities tracking for the patients on an experimental basis. We intend to pursue other opportunities in Japan and the United States for large- scale private label contracts for this device. MOTHER Bracelet™ received an encouraging response from the crowd-funding campaign in Japan. It has been featured in various Japanese media and was ranked 24th in “the Nikkei Trend 2022 Hit Predictions 30.”

In May 2021, we entered into a Master Manufacturing Agreement with Sanei Electronics Inc. in Tokyo, Japan, with respect to the production of the MOTHER Bracelet™ and commenced preparations for production and shipment. MOTHER Bracelet™ is unique in its SDK open policy. The policy is intended to increase the use of the device among medical institutions and other corporations in future, and we have received inquiries on the device across a number of business segments. By opening up the SDK, we allow and encourage software and hardware developers to customize the management of healthcare data for their own purposes. We are building this data management platform to serve the various lifestyles of users. We are planning to upgrade the device for the medical field by incorporating the requests from medical institutions in the future. MOTHER Bracelet™ records wearers’ activities, sleep duration and pattern, body temperature, and heart rate 24/7 without losing data. We are planning to apply for the license for the next generation of the device. The device production will commence in 2022, and the MOTHER Bracelet™ brand website and e-commerce website are currently under development. Our standard character trademark application for MOTHER Bracelet™ was approved by the Japan Patent Office in February 2022. In December 2021, we entered into a Memorandum of Understanding with Juju Holdings Kabushiki Kaisha, an operator of home-based nursing care facilities in Japan, to form a business alliance to jointly develop a centralized management system utilizing MOTHER Bracelet™ in nursing facilities.

Our Growth Strategy

Our goal is not only to capture a significant share of the existing market for relaxation salons but also to expand our digital health business lines. We expect to employ a variety of strategic initiatives, including increasing the number of directly-operated and franchised salons and expanding marketing and advertising efforts throughout strategic locations.

Organic Growth in the Japanese Market. According to the 2022 Yano Report, in terms of the number of salons, we are one of the top three companies, on a consolidated basis, in the Kanto region (Tokyo, Kanagawa, Saitama, Chiba, Gunma, Ibaraki and Tochigi), and in the top four nationwide. The total number of relaxation salons under major brands in Japan according to the 2022 Yano Report was 2,944, with the largest operator having 613 salons. We believe that the Japanese market has capacity for approximately 1,000 of our salons in the future, based upon our assessment of suitable real estate that fits the underwriting requirements for our business. We aim to achieve this capacity goal through a combination of franchising, direct ownership, and our

7

new salon sales and management contract model. If we are able to achieve this goal, we believe that we would then have the largest salon network in Japan.

Lead Industry Consolidation Via Targeted Acquisitions. As the domestic Japanese relaxation sector faces structural changes that accelerate consolidation, we believe that we are positioned strategically to harness value, acquire synergies, and maximize our pipeline of suitable bids at bargain prices. Our corporate acquisitions team aims to buy businesses at a small multiple to ours, leveraging our brand, the well- regarded reputation of our founder CEO, and the halo effect of joining Japan’s first publicly listed relaxation company in the United States. We believe we have a competitive advantage and significant negotiating powerto structure accretive deals, integrate both culture and operations of target companies, and grow long-term value. In May 2021, we acquired 100% of the interests in SAWAN CO. LTD. (“SAWAN”), a relaxation salon operator of “Ruam Ruam,” a luxury relaxation salon brand. This acquisition resulted in the addition of 13 directly-operated salons under the brand of “Ruam Ruam” to our relaxation salon segment. In January 2022, we completed the acquisition of ZACC Kabushiki Kaisha, a high-end hair salon company. Please refer to “Business — The Roots of our Business” for details.

Update of Business Model.Currently, Wing Inc. (fka Bell Epoc Wellness, Inc.), our wholly owned subsidiary, manages a majority of our relaxation salon operations, excluding those located in spa facilities or under “Ruam Ruam” brand. While we continue to grow the total number of our franchised salons, we expect to become more selective in new franchise salon owners. As of December 31, 2021, we entered into Salon Sales Agreements to sell a total of 14 previously directly-operated salons to investors for aggregate gross proceeds of JPY662 million. Such investors are required to enter into Service Agreements with Wing Inc.to manage the operation of the purchased salons, pursuant to which we are entitled to a contingent fee equal to 80% of the amount of profit that exceeds 6% to 8% investment yield on the purchase price of each purchased salon. We believe this model will maximize the return on capital investment in our relaxation salon segment, accelerate salon openings by reinvesting the proceeds from the sales of salons, improve operational efficiency by focusing on salon operations, and generate additional income from the salons that were sold to investors and are under management by us.

Focus on Margin Improvement and Leveraged Use of Infrastructure.We believe our corporate infrastructure is positioned to support a customer base greater than our existing footprint. As we are still recovering from the impact of the COVID-19 pandemic, we believe we have a great potential to attract more customers, utilize our currently idle capacities at certain of our salons, and improve our workforce management. We plan to closely monitor our operational metrics such as sales per salon, number of customers served per salon, sales per customer, total working hours per salon and total hours in service per salon. We also plan to replace our existing employee evaluation and incentive systems to better motivate our employees to meet certain performance targets assigned to them.

As we continue to grow, we expect to drive greater efficiencies across our operations and development and marketing organizations and further leverage our technology and existing support infrastructure. We believe we will be able to reduce percentage of corporate costs to revenue over time to enhance margins as general and administrative expenses are expected to grow at a slower rate due to efficiencies of scale as we expand our salon network.

Marketing and Advertising Strategy. We conduct most of our marketing and advertising on our website and through print advertisements in magazines. In addition, our salons are strategically located in areas near train stations and shopping centers that are in and of themselves advertising and marketing drivers. Furthermore, in addition to our effort to improve margins at our relaxation salons, we plan to enhance our digital marketing initiatives to increase revenue, including developing our brands’ smart phone apps to retain our repeat customers and improve the frequency of customer visits.

Healthtech Strategy. We plan to invest in and grow the Digital Preventative Healthcare Segment with a higher margin. We intend to increase the number of Lav® users via the Specific Health Guidance Program promoted by the Ministry of Health, Labor and Welfare of Japan. In addition, we expect to expand the billing user base for the upgraded Lav® application. We also intend to accelerate the development and production of our MOTHER Bracelet™. Our sales and distribution model is primarily B2B with an emphasis on large and recurring contract orders placed by corporate sponsors, healthcare and medical facilities, and government entities, who in turn distribute to the end consumer. In addition, we may sell to consumers both in Japan and internationally through distributors, online commerce, and strategic partners including retail placements at select big box stores.

Summary Risk Factors

There are a number of risks that you should carefully consider before making an investment decision regarding this offering. These risks are discussed more fully in the section entitled “Risk factors” beginning on page 18 of this prospectus. You should read

8

and carefully consider these risks and all of the other information in this prospectus, including the financial statements and the related notes thereto included in this prospectus, before deciding whether to invest in the ADSs. If any of these risks actually occur, our business, financial condition, operating results and cash flows could be materially adversely affected. In such case, the trading price of the ADSs would likely decline, and you may lose all or part of your investment. These risk factors include, but are not limited to:

Risks Related to Our Company and Our Business

Risks and uncertainties relating to our company and industry include, but are not limited to, the following:

| ● | We may not achieve our development goals, which could adversely affect our operations and financial results. |

| ● | We are implementing new growth strategy, priorities and initiatives and any inability to execute and evolve our strategy over time could adversely impact our financial condition and results of operations. |

| ● | We are actively expanding mainly in Japan and overseas markets, and we may be adversely affected if Japanese and global economic conditions and financial markets deteriorate. |

| ● | We have generated only limited revenue from our Digital Preventative Healthcare Segment, and we may never achieve or sustain profitability. |

| ● | Our success depends substantially on the value of our brands. |

| ● | The failure to enforce and maintain our trademarks and protect our other intellectual property could materially adversely affect our business, including our ability to establish and maintain brand awareness. |

| ● | We are exposed to the risk of natural disasters, unusual weather conditions, pandemic outbreaks such as COVID-19, political events, war and terrorism that could disrupt business and result in lower sales, increased operating costs and capital expenditures. |

Risks Related to Our Relationships with Franchisees

Risks and uncertainties relating to our relationships with franchisees include, but are not limited to, the following:

| ● | The financial performance of our franchisees can negatively impact our business. |

| ● | We have limited control with respect to the operations of our franchisees, which could have a negative impact on our business. |

Risks Related to Ownership of the ADSs

Risks and uncertainties relating to ownership of the ADSs include, but are not limited to, the following:

| ● | Our Chief Executive Officer owns a “golden share” with key veto rights, thereby limiting a shareholder’s ability to influence our business and affairs. |

Risks Related to Japan

Risks and uncertainties relating to Japan include, but are not limited to, the following:

| ● | We are incorporated in Japan, and it may be more difficult to enforce judgments against us that are obtained in courts outside of Japan. |

| ● | Substantially all of our revenues are generated in Japan, but an increase of our international presence could expose us to fluctuations in foreign currency exchange rates, or a change in monetary policy may harm our financial results. |

9

See “Risk Factors” and other information included in this prospectus for a discussion of these and other risks and uncertainties that we face.

Recent Developments

On January 18, 2022, we received a written notification (the “Notification Letter”) from NASDAQ, notifying us that we are not in compliance with the minimum market value requirement set forth in Nasdaq Listing Rules for continued listing on The Nasdaq Capital Market. Nasdaq Listing Rule 5550(b)(2) requires companies to maintain a minimum market value of $35 million and Nasdaq Listing Rule 5810(c)(3)(C) provides that a failure to meet the minimum market value requirement exists if the deficiency continues for a period of 30 consecutive business days. Based on our market value from November 23, 2021 to January 14, 2022, we no longer meet the minimum market value requirement. Pursuant to the Notification Letter, we have been provided 180 calendar days, or until July 18, 2022, to regain compliance. Although we expect to regain compliance during this period, adverse market events and other circumstances beyond our control may impact our ability to do so. If we are unable to regain compliance in the initial 180 day-period, we may become eligible for additional time to regain compliance or, alternatively, our ADSs may be delisted.

Implications of Being an Emerging Growth Company and a Foreign Private Issuer

We are an “emerging growth company”, as defined in Section 2(a) of the Securities Act of 1933, as amended (which we refer to as the “Securities Act”), as modified by the Jumpstart Our Business Startups Act of 2012 (which we refer to as the “JOBS Act”). As such, we are eligible to take advantage of specified reduced reporting and other requirements that are otherwise applicable generally to reporting companies that make filings with the U.S. Securities and Exchange Commission (which we refer to as the “SEC”). For so long as we remain an emerging growth company, we will not be required to, among other things:

| ● | present more than two years of audited financial statements and two years of related selected financial data and management’s discussion and analysis of financial condition and results of operations disclosure in our registration statement of which this prospectus forms a part; |

| ● | have an auditor report on our internal control over financial reporting pursuant to Section 404(b) of the Sarbanes-Oxley Act of 2002 (which we refer to as the “Sarbanes-Oxley Act”); |

| ● | disclose certain executive compensation related items; and |

| ● | seek shareholder non-binding advisory votes on certain executive compensation matters and golden parachute arrangements, to the extent applicable to our Company as a foreign private issuer. |

The JOBS Act also permits emerging growth companies to take advantage of an extended transition period to comply with new or revised accounting standards applicable to public companies. We have elected to use the extended transition period for complying with new or revised accounting standards under Section 102(b)(2) of the JOBS Act. This election allows us to delay the adoption of new or revised accounting standards that have different effective dates for public and private companies until those standards apply to private companies. As a result, our financial statements may not be comparable to companies that comply with public company effective dates.

We will remain an emerging growth company until the earlier of (i) the last day of the fiscal year following the fifth anniversary of the completion of this offering, (ii) the last day of the fiscal year during which we have total annual gross revenue of at least $1.07 billion, (iii) the date on which we are deemed to be a “large accelerated filer” under the Securities Exchange Act of 1934, as amended (which we refer to as the “Exchange Act”), which means the market value of our common shares that are held by non-affiliates exceeds $700.0 million as of the last business day of our most recently completed second fiscal quarter, and (iv) the date on which we have issued more than $1.0 billion in non-convertible debt during the prior three-year period.

In addition, we report in accordance with SEC rules and regulations applicable to a “foreign private issuer.” As a foreign private issuer, we will take advantage of certain provisions under the rules that allow us to follow the laws of Japan for certain corporate governance matters. Even when we no longer qualify as an emerging growth company, as long as we continue to qualify as a foreign private issuer under the Exchange Act, we will be exempt from certain provisions of the Exchange Act that are applicable to U.S. domestic public companies, including:

| ● | the sections of the Exchange Act regulating the solicitation of proxies, consents or authorizations with respect to a security registered under the Exchange Act; |

10

| ● | the rules under the Exchange Act requiring the filing with the SEC of quarterly reports on Form 10-Q containing unaudited financial and other specified information, and current reports on Form 8-K upon the occurrence of specified significant events; and |

| ● | Regulation Fair Disclosure (which we refer to as “Regulation FD”), which regulates selective disclosures of material information by issuers. |

As a foreign private issuer, we have four months after the end of each fiscal year to file our annual report on Form 20-F with the SEC. In addition, our executive officers, directors, and principal shareholders are exempt from the requirements to report transactions in our equity securities and from the short-swing profit liability provisions contained in Section 16 of the Exchange Act.

Foreign private issuers, like emerging growth companies, are exempt from certain more stringent executive compensation disclosure rules. As such, even when we no longer qualify as an emerging growth company, as long as we continue to qualify as a foreign private issuer under the Exchange Act, we will continue to be exempt from the more stringent compensation disclosures required of public companies that are not a foreign private issuer.

We may take advantage of these exemptions until such time as we are no longer a foreign private issuer. We are required to determine our status as a foreign private issuer on an annual basis at the end of our second fiscal quarter. We would cease to be a foreign private issuer at such time as more than 50% of our outstanding voting securities are held by U.S. residents and any of the following three circumstances applies:

| (i) | the majority of our executive officers or directors are U.S. citizens or residents; |

| (ii) | more than 50% of our assets are located in the United States; or |

| (iii) | our business is administered principally in the United States. |

In this prospectus, we have taken advantage of certain of the reduced reporting requirements as a result of being an emerging growth company and a foreign private issuer. Accordingly, the information that we provide in this prospectus may be different than the information you may receive from other public companies in which you hold equity interests. If some investors find our securities less attractive as a result, there may be a less active trading market for our securities and the prices of our securities may be more volatile.

Corporate Information

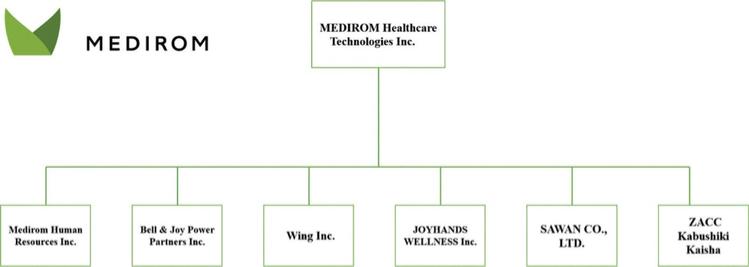

We are a joint-stock corporation incorporated in Japan under the Companies Act. Our Company was originally incorporated in Japan on July 13, 2000 under the name “Kabushiki Kaisha Young Leaves.” In January 2017, we changed our name to “MEDIROM Inc.” In April 2018, we established three wholly- owned subsidiaries, Bell Epoc Wellness Inc., JOYHANDS WELLNESS Inc., and Medirom Human Resources Inc. In October 2018, we acquired our fourth wholly-owned subsidiary, Decollte Wellness Corporation. In March 2020, our Company’s English name was changed to “MEDIROM Healthcare Technologies Inc.” In December 2020, we listed the ADSs representing our common shares on The Nasdaq Capital Market (which we refer to as “NASDAQ”). In May 2021, we acquired SAWAN, our fifth wholly-owned subsidiary. In July 2021, in order to speed up decision-making process, improve business efficiency and maximize business value, we reorganized and re-designated certain of our wholly-owned subsidiaries by business functions. In January 2022, we completed the acquisition of ZACC Kabushiki Kaisha, a high-end hair salon company. Please refer to “Business — The Roots of our Business” for details.

Our agent for service of process in the United States is Cogency Global Inc., located at 122 East 42nd Street, 18th Floor, New York, NY 10168. Our principal executive offices are located in 2-3-1 Daiba, Minato- ku, Tokyo 135-0091, Japan, and our main telephone number is +81(0)3-6721-7364. Our website is https://medirom.co.jp/en/. The information contained in, or that can be accessed through, our website is not incorporated by reference into, and is not a part of, this prospectus. You should not consider any information on our website to be a part of this prospectus. We have included our website address in this prospectus solely for informational purposes.

11

Trademarks

The names and marks, Re.Ra.Ku® and Lav®, appearing in this prospectus are the property of Medirom. CLP CARE LIFE PLANNER® is licensed by the Company from the CEO. Our standard character trademark application for MOTHER Bracelet™ was approved by the Japan Patent Office in February 2022. The use of the symbol ® in this prospectus denotes registration of the Company’s names and marks in Japan only, and Lav® denotes a registration of a combined trademark, including both letters and design marks. None of the Company’s names and marks appearing in this prospectus are currently registered in the United States. Solely for convenience, trademarks, trade names and service marks referred to in this prospectus may appear without the ®, ™ or SM symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights or the right of the applicable licensor to these trademarks, trade names and service marks. We do not intend any use or display by us of other parties’ trademarks, trade names or service marks to imply, and such use or display should not be construed to imply, a relationship with, or endorsement or sponsorship of us by, these other parties.

12

THE OFFERING

Issuer | MEDIROM Healthcare Technologies Inc. |

ADSs offered by us | 800,000 ADSs. |

Common Shares Outstanding Immediately prior to this Offering(1) | 4,882,500 common shares. |

Common Shares expected to be Outstanding Immediately After this Offering(1) | 5,682,500 common shares (or 5,802,500 common shares if the underwriters exercise in full their option to purchase additional ADSs representing our common shares). |

Option to Purchase Additional ADSs | We have granted to the underwriters an option to purchase up to additional 120,000 ADSs from us at the offering price less the underwriting discounts and commissions, to cover over-allotments, if any, for a period of 45 days from the date of this prospectus. |

The ADSs | Each ADS represents one common share. |

The depositary will be the holder of the common shares underlying the ADSs, and you will have the rights of an ADS holder as provided in the deposit agreement among us, the depositary, and owners and beneficial owners of ADSs from time to time. | |

You may surrender your ADSs to the depositary to withdraw the common shares underlying your ADSs. The depositary will charge you a fee for such an exchange. | |

We may amend or terminate the deposit agreement for any reason without your consent. If an amendment becomes effective, you will be bound by the deposit agreement, as amended, if you continue to hold your ADSs. | |

To better understand the terms of the ADSs, you should carefully read the section in this prospectus entitled “Description of American Depositary Shares.” We also encourage you to read the deposit agreement, a form of which is an exhibit to the registration statement to which this prospectus forms a part. | |

Depositary | The Bank of New York Mellon |

Use of Proceeds | We estimate that the net proceeds to us from this offering will be approximately $4.7 million (or $5.5 million if the underwriters exercise in full their option to purchase additional ADSs), based on an assumed public offering price of $7.02 per ADS, which was the last reported sale price of the ADSs on The Nasdaq Capital Market on February 10, 2022, after deducting the underwriting discounts and commissions and estimated offering expenses payable by us. |

We currently intend to use the net proceeds from this offering for working capital and general corporate purposes, which may include investments, acquisitions, or strategic collaborations to expand our customer base, as well as the development and marketing of new services. In addition, we intend to use a portion of the net proceeds to replace our current IT systems with or install new IT systems to strengthen our operating efficiency, internal control over financial reporting, general IT functions and protection of customer data. See “Use of Proceeds.” | |

Lock-ups | We, our directors, executive officers and holders of three percent (3%) or more of our outstanding common shares will enter into agreements with the underwriters |

13

pursuant to which they will not offer to sell, sell, pledge, contract to sell, purchase any option to sell, grant any option for the purchase of, lend, or otherwise dispose of, any of our securities for a period of 180 days following the closing of this offering, subject to certain exceptions. See “Underwriting — No Sales of Similar Securities” for more information. | |

Listing | The ADSs representing our common shares are listed on The Nasdaq Capital Market under the symbol “MRM.” |

Risk Factors | Investing in the ADSs is highly speculative and involves a high degree of risk. You should carefully read and consider the information set forth under the heading “Risk Factors” beginning on page 18, and all other information contained in this prospectus, before deciding to invest in the ADSs. |

| (1) | The number of common shares to be outstanding immediately prior to and after this offering does not include up to an aggregate of 608,500 common shares issuable upon the exercise of stock options outstanding as of June 30, 2021. |

Except as otherwise indicated, all information in this prospectus assumes no exercise by the underwriters of their option to purchase additional ADSs from us.

14

SUMMARY CONSOLIDATED FINANCIAL INFORMATION AND OPERATING DATA

The following tables set forth our summary consolidated financial information and operating data as of and for the years ended December 31, 2020 and 2019 and the six months ended June 30, 2021 and 2020. You should read the following summary consolidated financial information and operating data in conjunction with, and it is qualified in its entirety by reference to, our audited consolidated financial statements and the related notes thereto, our unaudited condensed consolidated financial statements and the related notes thereto, and the sections entitled “Capitalization”, “Selected Consolidated Financial Information and Operating Data” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations”, each of which are included elsewhere in this prospectus.

Our summary consolidated statement of income information and operating data for the years ended December 31, 2020 and 2019, and our related summary consolidated balance sheet information as of December 31, 2020 and 2019, have been derived from our audited consolidated financial statements as of and for the years ended December 31, 2020 and 2019, prepared in accordance with U.S. GAAP, which are included elsewhere in this prospectus.

Our summary consolidated statement of income information and operating data for the six months ended June 30, 2021 and 2020, and our related summary consolidated balance sheet information as of June 30, 2021 and 2020, have been derived from our unaudited condensed consolidated financial statements as of and for the six months ended June 30, 2021 and 2020, prepared in accordance with U.S. GAAP, which are included elsewhere in this prospectus.

Our historical results for the periods presented below are not necessarily indicative of the results to be expected for any future periods.

Six months ended June 30, | Year ended December 31, | ||||||||||||||||||||||||||||||

(in thousands, except Adjusted | |||||||||||||||||||||||||||||||

EBITDA margin) |

| 2021($) |

| 2021(¥) |

| 2020(¥) |

| 2020($) |

| 2020(¥) |

| 2019(¥) | |||||||||||||||||||

(unaudited) | |||||||||||||||||||||||||||||||

Consolidated Statement of Income Information: | |||||||||||||||||||||||||||||||

Revenues: | |||||||||||||||||||||||||||||||

Relaxation Salons | $ | 19,006 | ¥ | 2,110,561 | ¥ | 1,344,503 | $ | 29,860 | ¥ | 3,315,947 | ¥ | 3,864,656 | |||||||||||||||||||

Digital Preventative Healthcare | 152 | 16,918 | 11,774 | 231 | 25,670 | 43,608 | |||||||||||||||||||||||||

Total revenue | 19,158 | 2,127,479 | 1,356,277 | 30,091 | 3,341,617 | 3,908,264 | |||||||||||||||||||||||||

Cost of revenues and operating expenses: | |||||||||||||||||||||||||||||||

Cost of revenues | 15,929 | 1,768,907 | 1,269,220 | 26,228 | 2,912,667 | 2,957,506 | |||||||||||||||||||||||||

Selling, general and administrative expenses | 7,571 | 840,760 | 521,364 | 9,622 | 1,068,537 | 871,862 | |||||||||||||||||||||||||

Impairment loss on long- lived assets | — | — | — | 959 | 106,501 | 44,546 | |||||||||||||||||||||||||

Total cost of revenues and operating expenses | 23,500 | 2,609,667 | 1,790,584 | 36,809 | 4,087,705 | 3,873,914 | |||||||||||||||||||||||||

Operating (loss) income | $ | (4,342) | ¥ | (482,188) | ¥ | (434,307) | $ | (6,718) | ¥ | (746,088) | ¥ | 34,350 | |||||||||||||||||||

Other income (expenses): | |||||||||||||||||||||||||||||||

Dividend income | — | 2 | 2 | — | 2 | 2 | |||||||||||||||||||||||||

Interest income | 4 | 506 | 674 | 12 | 1,332 | 1,336 | |||||||||||||||||||||||||

Interest expense | (60) | (6,683) | (6,076) | (119) | (13,234) | (13,591) | |||||||||||||||||||||||||

Gain from bargain purchases | 9 | 1,014 | 1,624 | — | — | 6,487 | |||||||||||||||||||||||||

Government subsidies and other, net | 187 | 20,798 | 14,142 | 1,182 | 131,299 | 4,153 | |||||||||||||||||||||||||

Total other income (expenses) | 140 | 15,637 | 10,366 | 1,075 | 119,399 | (1,613) | |||||||||||||||||||||||||

Income tax expense (benefit) | 497 | 55,219 | 19,030 | (788) | (87,519) | 15,961 | |||||||||||||||||||||||||

Equity in earnings of investment | — | — | — | — | — | 559 | |||||||||||||||||||||||||

Net (loss) income | $ | (4,699) | ¥ | (521,770) | ¥ | (442,971) | $ | (4,855) | ¥ | (539,170) | ¥ | 17,335 | |||||||||||||||||||

Adjusted EBITDA(1) | $ | (2,626) | ¥ | (291,601) | ¥ | (374,224) | $ | (4,894) | ¥ | (543,456) | ¥ | 139,301 | |||||||||||||||||||

Adjusted EBITDA margin(2) | (13.7) | % | (13.7) | % | (27.6) | % | (16.3) | % | (16.3) | % | 3.6 | % | |||||||||||||||||||

| (1) | For a reconciliation of Adjusted EBITDA to net income (loss), the most comparable U.S. GAAP measure, see the following table. |

| (2) | Adjusted EBITDA margin is calculated by dividing Adjusted EBITDA for a period by total revenue for the same period. |

15

Six months ended June 30, | Year ended December 31, | ||||||||||||||||||

(in thousands, except | |||||||||||||||||||

Adjusted EBITDA margin) |

| 2021($) |

| 2021(¥) |

| 2020(¥) |

| 2020($) |

| 2020(¥) |

| 2019(¥) |

| ||||||

Reconciliation of non-GAAP measures: | |||||||||||||||||||

Net (loss) income | $ | (4,699) | ¥ | (521,770) | ¥ | (442,971) | $ | (4,855) | ¥ | (539,170) | ¥ | 17,335 | |||||||

Dividend income and interest income | (4) | (508) | (676) | (12) | (1,334) | (1,338) | |||||||||||||

Interest expense | 60 | 6,683 | 6,076 | 119 | 13,234 | 13,591 | |||||||||||||

Gain from bargain purchases | (9) | (1,014) | (1,624) | — | — | (6,487) | |||||||||||||

Government subsidies and other, net | (187) | (20,798) | (14,142) | (1,182) | (131,299) | (4,153) | |||||||||||||

Income tax expense | 497 | 55,219 | 19,030 | (788) | (87,519) | 15,961 | |||||||||||||

Equity in earnings of investment | — | — | — | — | — | (559) | |||||||||||||

Operating (loss) income | $ | (4,342) | ¥ | (482,188) | ¥ | (434,307) | $ | (6,718) | ¥ | (746,088) | ¥ | 34,350 | |||||||

Depreciation and amortization | 357 | 39,631 | 33,105 | 561 | 62,290 | 46,174 | |||||||||||||

Losses on sales of directly- operated salons to franchises | — | 49 | 65 | — | — | 9,600 | |||||||||||||

Losses on disposal of property and equipment, net and other intangible assets, net | 18 | 1,967 | 26,913 | 304 | 33,841 | 4,631 | |||||||||||||

Stock compensation expense* | 1,341 | 148,940 | — | — | — | — | |||||||||||||

Impairment loss on long-lived assets | — | — | — | 959 | 106,501 | 44,546 | |||||||||||||

Adjusted EBITDA | $ | (2,626) | ¥ | (291,601) | ¥ | (374,224) | $ | (4,894) | ¥ | (543,456) | ¥ | 139,301 | |||||||

Adjusted EBITDA margin | (13.7) | % | (13.7) | % | (27.6) | % | (16.3) | % | (16.3) | % | 3.6 | % | |||||||

* | The Company did not recognize stock compensation expense in the six months ended June 30, 2020 or the years ended December 31, 2020 and 2019. |

| Six months ended June 30, |

| Year ended December 31, |

| |||||||||

| 2021 |

| 2020 |

| 2020 |

| 2019 | ||||||

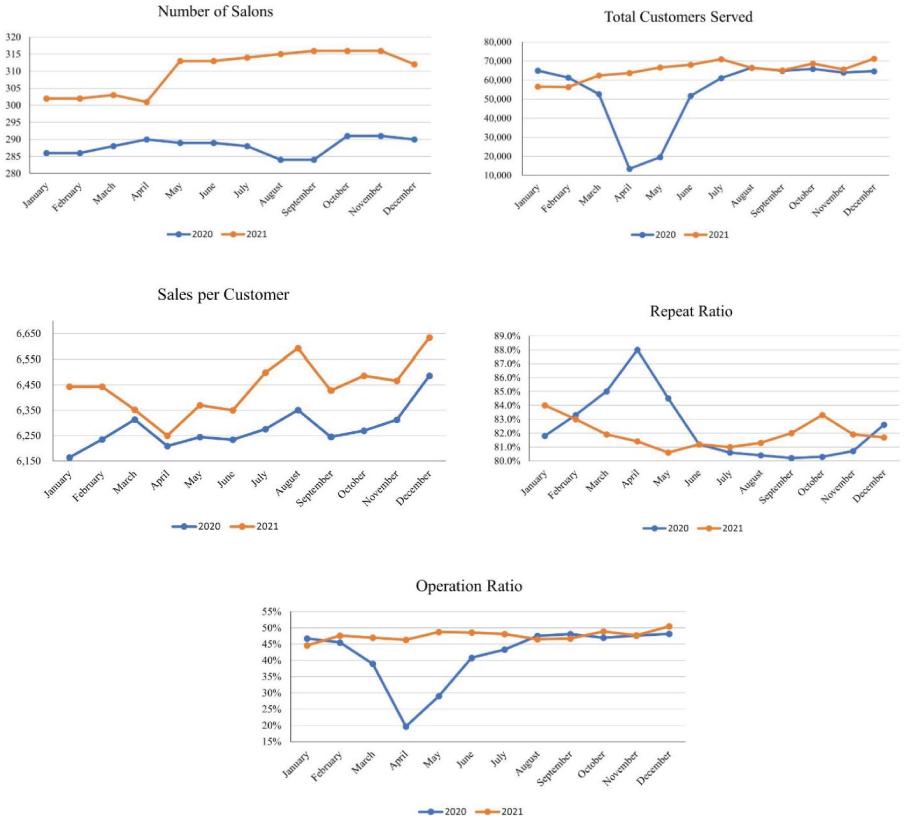

Other Operating Data: | |||||||||||||

Number of Salons | 313 | 289 | 290 | 283 | |||||||||

Sales per Customer(3) | ¥ | 6,350 | ¥ | 6,234 | ¥ | 6,486 | ¥ | 6,064 | |||||

Repeat Ratio(4) | 81.2 | % | 81.2 | % | 82.6 | % | 81.7 | % | |||||

Operation Ratio(5) | 48.6 | % | 40.8 | % | 48.2 | % | 50.4 | % | |||||

| (3) | We define sales per customer as the ratio of total salon sales to number of treated customers at salons (other than JOYHANDS WELLNESS, SAWAN, and a few other salons for which comparative financial and customer data is not available). |

| (4) | We define the repeat ratio as the ratio of repeat customer visits to total customer visits in the applicable month or other stated period for all salons for which comparable financial and customer data is available. |

| (5) | We define the operation ratio as the ratio of therapists’ in-service time to total therapists’ working hours (including stand-by time) for the applicable month or other stated period for all salons for which comparable financial and customer data is available. |

16

As of June 30, | As of December 31, |

| |||||||||||

(in thousands) |

| 2021(¥) |

| 2020(¥) |

| 2020(¥) |

| 2019(¥) | |||||

(unaudited) | |||||||||||||

Consolidated Balance Sheet Information: | |||||||||||||

Total assets | ¥ | 5,200,016 | ¥ | 4,097,971 | ¥ | 5,713,466 | ¥ | 4,757,465 | |||||

Total liabilities | 4,993,947 | 3,940,884 | 5,222,209 | 4,157,407 | |||||||||

Equity | |||||||||||||

Common stock, no par value; 19,899,999 shares authorized; 4,975,000 shares issued and 4,882,500 shares outstanding at June 30, 2021; 9,999,999 shares authorized; 4,915,000 shares issued and 4,822,500 shares outstanding at December 31, 2020 | 1,223,134 | 595,000 | 1,179,313 | 595,000 | |||||||||

Class A common stock, no par value | 100 | 100 | 100 | 100 | |||||||||

Treasury stock, at cost — 92,500 common shares | (3,000) | (3,000) | (3,000) | (3,000) | |||||||||

Additional paid-in capital | 1,210,907 | 713,267 | 1,018,146 | 713,267 | |||||||||

Accumulated deficit | (2,225,072) | (1,148,280) | (1,703,302) | (705,309) | |||||||||

Total equity | 206,069 | 157,087 | 491,257 | 600,058 | |||||||||

Total Liabilities and Equity | ¥ | 5,200,016 | ¥ | 4,097,971 | ¥ | 5,713,466 | ¥ | 4,757,465 | |||||

17

RISK FACTORS

An investment in the ADSs is highly speculative and involves a high degree of risk. We operate in a dynamic and rapidly changing industry that involves numerous risks and uncertainties. You should carefully consider the factors described below, together with all of the other information contained in this prospectus, including the audited and unaudited financial statements and the related notes included in this prospectus. These risk factors are not presented in the order of importance or probability of occurrence. If any of the following risks actually occurs, our business, financial condition and results of operations could be materially and adversely affected. Some statements in this prospectus, including statements in the following risk factors, constitute forward-looking statements. Please refer to the section entitled “Cautionary Note Regarding Forward-Looking Statements.”

Risks Related to Our Company and Our Business

We may not achieve our development goals, which could adversely affect our operations and financial results.

Our number of salons has increased from 290 as of December 31, 2020 to 312 as of December 31, 2021. We intend to continue our growth either through developing additional directly-operated salons or through new salon development by acquisition, both in existing markets and in new markets, particularly in Japan. Such rapid development involves substantial risks, including the risk of:

| ● | the inability to identify suitable franchisees; |

| ● | limited availability of financing for our Company and for franchisees at acceptable rates and terms; |

| ● | development costs exceeding budgeted or contracted amounts; |

| ● | delays in completion of construction; |

| ● | the inability to identify, or the unavailability of, suitable sites at acceptable cost and other leasing or purchase terms; |

| ● | developed properties not achieving desired revenue or cash flow levels once opened; |

| ● | the negative impact of a new salon upon sales at nearby existing salons; |

| ● | the challenge of developing in areas where competitors are more established or have greater penetration or access to suitable development sites; |

| ● | incurring substantial unrecoverable costs in the event a development project is abandoned prior to completion; |

| ● | impairment charges resulting from underperforming salons or decisions to curtail or cease investment in certain locations or markets; |

| ● | in new geographic markets where we have limited or no existing locations, the inability to successfully expand or acquire critical market presence for our brands, acquire name recognition, successfully market our products or attract new customers; |

| ● | operating cost levels that reduce the demand for, or raise the cost of, developing new salons; |

| ● | the challenge of identifying, recruiting and training qualified salon management; |

| ● | the inability to obtain all required permits; |

| ● | changes in laws, regulations and interpretations; and |

| ● | general economic and business conditions. |

Although we manage our growth and development activities to help reduce such risks, we cannot provide assurance that our present or future growth and development activities will perform in accordance with our expectations. Our inability to expand in

18

accordance with our plans or to manage the risks associated with our growth could have a material adverse effect on our results of operations and financial condition.

We are implementing new growth strategy, priorities and initiatives and any inability to execute and evolve our strategy over time could adversely impact our financial condition and results of operations.

We seek to accelerate the growth of our acquisition model while at the same time improve the performance of directly-operated salons. Our success also depends, in part, on our ability to grow our franchise model, including attracting and retaining qualified franchisees. Our ability to open new relaxation salons is dependent upon a number of factors, many of which are beyond our control, including our and our franchisees’ ability to:

| ● | identify available and suitable relaxation salon sites; |

| ● | successfully compete for relaxation salon sites; |

| ● | reach acceptable agreements regarding the lease or purchase of locations; |

| ● | obtain or have available the financing required to acquire and operate a relaxation salon, including construction and opening costs, which includes access to build-to-suit leases at favorable interest and capitalization rates; |

| ● | respond to unforeseen engineering or environmental problems with leased premises; |

| ● | avoid the impact of inclement weather, natural disasters and other calamities; |

| ● | hire, train and retain the skilled management and other employees necessary to meet staffing needs; |

| ● | obtain, in a timely manner and for an acceptable cost, required licenses, permits and regulatory approvals and respond effectively to any changes in law and regulations that adversely affect our and our franchisees’ costs or ability to open new relaxation salons; and |

| ● | control construction cost increases for new relaxation salons. |

The growth of our acquisition model will take time to execute and may create additional costs, expose us to additional legal and compliance risks, cause disruption to our current business and impact our short-term operating results. Further, in order to enhance services to its franchisees, we may need to invest in certain new capabilities and/or services.

Our success also depends, in part, on our ability to improve sales, as well as both cost of service and product and operating margins at our directly-operated salons. Same-store sales are affected by average ticket and same-store guest visits. A variety of factors affect same-store guest visits, including the guest experience, salon locations, staffing and retention of therapists and salon leaders, price competition, current economic conditions, marketing programs and weather conditions. These factors may cause our same- store sales to differ materially from prior periods and from our expectations.

As part of our new growth strategy, we may in the future sell certain of our directly-operated salons to investors and charge management fees from such sold salons. Our revenue from salon sales will depend on a number of factors including the interest of potential investors, financial market conditions, available interest rates, and expected return of other comparable types of investments, none of which we will have control over. In addition, our management fees from the sold salons will depend on the actual contractual terms subject to our negotiation with potential investors in the future.

As part of our longer-term growth strategy, we plan to enter new geographical markets primarily in Asia where we have little or no prior operating or franchising experience. The challenges of entering new markets include: difficulties in hiring experienced personnel; unfamiliarity with local real estate markets and demographics; consumer unfamiliarity with our brand; and different competitive and economic conditions, consumer tastes and discretionary spending patterns that are more difficult to predict or satisfy than in our existing markets. Consumer recognition of our brand has been important in the success of both directly- operated and franchised relaxation salons in our existing markets. Relaxation salons that we open in new markets may take longer to reach expected sales and profit levels and may have higher construction, occupancy and operating costs than existing relaxation salons, thereby

19

negatively affecting our operating results. Any failure on our part to recognize or respond to these challenges may adversely affect the success of any new relaxation salons. Expanding our franchise system could require the implementation, expense and management of enhanced business support systems, management information systems and financial controls as well as additional staffing, franchise support and capital expenditures and working capital.

We are actively expanding in Japan and overseas markets, and we may be adversely affected if Japanese and global economic conditions and financial markets deteriorate.

We seek to proactively expand our business overseas in the future including into new regions for us, particularly Asia. We also intend to explore growth opportunities in other markets where we assess primarily on low cost of entry, friendly franchising or partnership relationships and believe there is an economic staying power of our relaxation salon brand locally. As a result, our financial condition and results of operations may be materially affected by general economic conditions and financial markets in Japan and foreign countries, which would be influenced by the changes of various factors. These factors include fiscal and monetary policies, and laws, regulations and policies on financial markets. In the event of an economic downturn in Japan, consumer spending habits could be adversely affected, and we could experience lower than expected net sales, which could force us to delay or slow our growth strategy and have a material adverse effect on our business, financial condition, profitability and cash flows. In addition, we could be impacted by labor shortages in Japan or other markets. The deterioration of Japanese and global economic conditions, or financial market turmoil, could result in a worsening of our liquidity and capital conditions, an increase in our credit costs, and, as a result, adversely affect our business, financial condition and results of operations.