UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

(Mark One)

For

the Fiscal Year Ended

Or

For the transition period from _____ to _____

Commission

File Number:

(Exact name of registrant as specified in its charter)

(State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

(

(Address, including zip code, of registrant's principal executive offices and

telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class | Trading Symbol | Name of each exchange on which registered | ||

| The

|

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes

☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes

☐

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically, every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company, in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ☐ | Accelerated filer ☐ |

| Smaller reporting company

|

|

| Emerging

Growth Company |

If

an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying

with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

Indicate

by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness

of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C.7262(b)) by the registered

public accounting firm that prepared or issued its audit report.

Indicate

by check mark whether the registrant is a shell company (as defined in Rule12b-2 of the Act). Yes: ☐

The Registrant was not a public company as of the last business day of its most recently completed second fiscal quarter and, therefore, cannot calculate the aggregate market value of its voting and non-voting common equity held by non-affiliates as of such date.

The number of shares outstanding of the Registrant's common stock, par value $0.0001 per share, on March 30, 2022 was .

| 1 |

Table of Contents

| 2 |

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

Statements made in this report that are not statements of historical fact, including statements about our beliefs and expectations, are forward-looking statements, and should be evaluated as such. Forward-looking statements include information concerning possible or assumed future results of operations, including descriptions of our business plan and strategies. These statements often include words such as “anticipate,” “expect,” “suggest,” “plan,” “believe,” intend,” “project,” “forecast,” “estimates,” “targets,” “projections,” “should,” “could,” “would,” “may,” “might,” “will,” and other similar expressions. These forward-looking statements are contained throughout this Annual Report, including the sections entitled “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “Business. ”

We base these forward-looking statements or projections on our current expectations, plans, and assumptions, which we have made in light of our experience in the industry, as well as our perceptions of historical trends, current conditions, expected future developments, and other factors we believe, are appropriate under the circumstances and at this time. As you read and consider this Annual Report, you should understand that these statements are not guarantees of performance or results. The forward-looking statements and projections contained herein are subject to and involve risks, uncertainties, and assumptions, and therefore you should not place undue reliance on these forward-looking statements or projections. Although we believe that these forward-looking statements and projections are based on reasonable assumptions at the time they are made, you should be aware that many factors could affect our actual financial results, and therefore actual results might differ materially from those expressed in the forward-looking statements and projections. Factors that might materially affect such forward-looking statements and projections include

| • | Our ability to effectively operate our business segments; |

| • | Our ability to manage our research, development, expansion, growth, and operating expenses; |

| • | Changes or delays in government regulation relating to the healthcare and Life Sciences industries; |

| • | Changes or delays in government regulation relating to the healthcare and Life Sciences industries; |

| • | Our ability to compete, directly and indirectly, and succeed in the highly competitive and evolving ridesharing industry; |

| • | Our ability to compete, directly and indirectly, and succeed in the highly competitive and evolving ridesharing industry; |

| • | Our ability to protect our intellectual property and to develop, maintain and enhance a strong brand; and |

| • | Other factors (including the risks contained in the section of this Annual Report entitled “Item 1A :Risk Factors”) relating to our industry, our operations, and results of operations. |

The preceding list is not intended to be an exhaustive list of all of our forward-looking statements. The forward-looking statements are based on our beliefs, assumptions, and expectations of future performance, taking into account the information currently available to us. These statements are only predictions based upon our current expectations and projections about future events. There are important factors that could cause our actual results, level of activity, performance, or achievements to differ materially from the results, level of activity, performance, or achievements expressed or implied by the forward-looking statements. Other sections of this Annual Report may include additional factors that could adversely impact our business and financial performance. Moreover, we operate in a very competitive and rapidly changing environment. New risks emerge from time to time and it is not possible for our management to predict all risks, nor can we assess the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements we may make. Factors or events that could cause our actual results to differ may emerge from time to time, and it is not possible for us to predict all of them. We cannot guarantee future results, levels of activity, performance, or achievements. Except as required by applicable law, including the securities laws of the United States, we do not intend to update any of the forward-looking statements to conform these statements to actual results.

SUMMARY OF RISK FACTORS

Our business is subject to a number of risks. You should be aware of these risks before making an investment decision. These risks are discussed more fully in “Item 1A : Risk Factors” in this Annual Report. These risks include, among others, that:

• We have a limited operating history in an evolving industry, which makes it difficult to evaluate our future prospects and may increase the risk that we will not be successful;

• If we fail to raise capital when needed it will have a material adverse effect on the Company's business, financial condition and results of operations;

• We rely on internet search engines and application marketplaces to drive traffic to our Platform, certain providers of which offer products and services that compete directly with our products. If links to our applications and website are not displayed prominently, traffic to our Platform could decline and our business would be adversely affected;

• The ecommerce market is highly competitive and if the Company does not have sufficient resources to maintain research and development, marketing, sales and client support efforts on a competitive basis our business could be adversely affected;

• Delays in the implementation of or lack of consumer acceptance of Society Points could have a material adverse effect on our business;

• If the Company is unable to expand its systems or develop or acquire technologies to accommodate increased volume its Platform could be impaired;

• The Company’s failure to successfully market its brands could result in adverse financial consequences;

• A decline in the demand for goods and services of the merchants included in the Platform could result in adverse financial consequences;

• We may be required to expend resources to protect Platform information or we may be unable to launch our services;

• The Company may engage in acquisition activity, which could have adverse effects on its business;

• We rely on the performance of highly skilled personnel, and if we are unable to attract, retain and motivate well-qualified employees, our business could be harmed;

• All of our operations are overseas;

• We are subject to changes in the economic, political, or legal environment of the Asia Pacific region;

• Many of the economies in SEA are experiencing substantial inflationary pressures which may prompt the governments to take action to control the growth of the economy and inflation that could lead to a significant decrease in our profitability;

• Our business will be exposed to foreign exchange risk;

• If inflation increases significantly in SEA or South Asia countries it could adversely affect our profitability;

• Geopolitical unrest in the regions in which we operate could adversely affect our business;

• Our business may be materially adversely affected by the recent coronavirus (COVID-19) outbreak;

• The payment processing regulatory regimes of the countries in which we operate could have adverse consequences on our business;

• Regulation of the internet generally could have adverse consequences on our business;

• We may be exposed to liabilities under the Foreign Corrupt Practices Act, and any determination that we violated the Foreign Corrupt Practices Act could have a material adverse effect on our business;

• Our financial statements have been prepared on a going-concern basis and our continued operations are in doubt;

• There is no active public trading market for our common stock and we cannot assure you that an active trading market will develop in the near future;

• We may not be able to maintain a listing of our common stock;

• As a “controlled company” under the rules of the Nasdaq Capital Market, we may choose to exempt our company from certain corporate governance requirements that could have an adverse effect on our public shareholders;

• Our financial controls and procedures may not be sufficient to ensure timely and reliable reporting of financial information, which, as a public company, could materially harm our stock price; and

• We are an “emerging growth company” under the JOBS Act of 2012 and we cannot be certain if the reduced disclosure requirements applicable to emerging growth companies will make our common stock less attractive to investors.

PART I

Item 1. Business

Our Mission

Our mission statement is: Loyalty and Data…that’s what we do.

We are an acquisitions-focused, e-commerce holding company. Since 2018, we developed our unique SoPa branded ecosystem and acquired our #HOTTAB, Leflair, Pushkart and Handycart platforms to facilitate e-commerce transactions between our consumers and our merchants in Southeast Asia (“SEA”) (including Vietnam, Philippines, Indonesia, Singapore, Malaysia, Thailand, Cambodia, Laos, Myanmar, and Brunei). Our marketing platform empowers small and medium enterprises (“SMEs”) to benefit from e-commerce opportunities in developing and frontier markets across SEA, driving job-creation and economic growth in one of the world’s most dynamic regions. We intend to continue to opportunistically acquire regional e-commerce companies and applications to drive revenues and increase the number of registered consumers and merchants in our SoPa ecosystem. As more merchants and consumers in SEA register on our Society Pass platform, more transaction data is generated. With more data generation, there are more opportunities for creating loyalty from consumers to merchants.

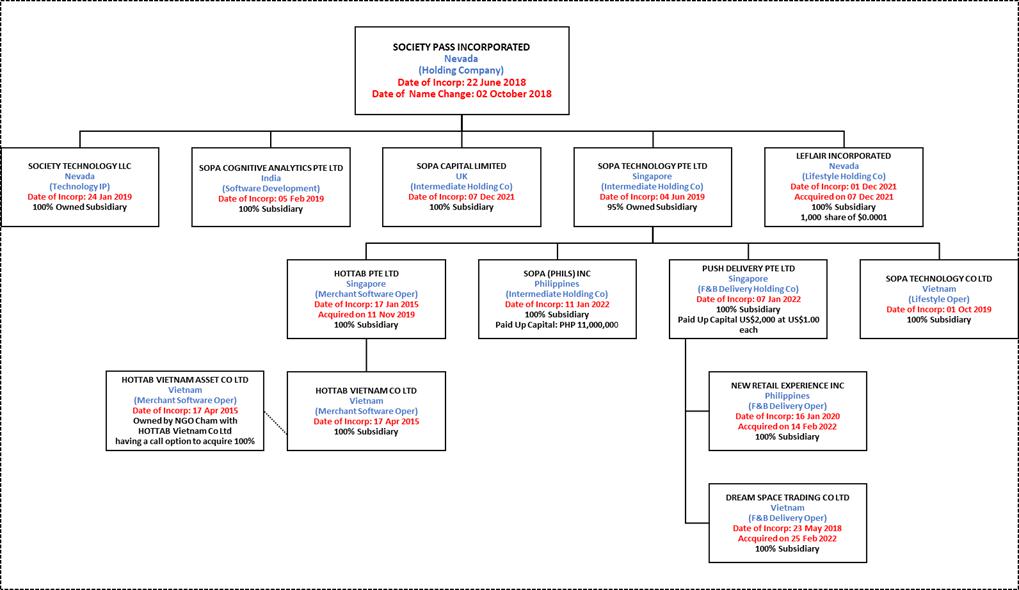

Our Company

We acquire and operate e-commerce platforms and mobile applications through our direct and indirect wholly or majority-owned subsidiaries, including but not limited to Society Technology LLC, SOPA Technology Pte Ltd, SOPA Cognitive Analytics Pte Ltd, SOPA Technology Co Ltd, HOTTAB Pte Ltd and HOTTAB Vietnam Co Ltd. Along with HOTTAB Asset Vietnam Co Ltd (currently wholly-owned by one employee of HOTTAB Vietnam Co Ltd and contractually operated by HOTTAB Vietnam Co Ltd), Leflair Incorporated, Push Delivery Pte Ltd, New Retail Experience Incorporated (“NREI”), and Dream Space Co., Ltd (“Dream Space”), these twelve companies form the Society Pass Group (the “Group”). The Group currently markets to both consumers and merchants in Vietnam and Philippines while maintaining an administrative headquarters in Singapore and a software development center, which was located in India but is transitioning to a location in SEA. In February 2022, we acquired an online lifestyle platform of Leflair branded assets (the “Leflair Assets”). We recently acquired NREI and Dream Space in February 2022 and have integrated the Leflair Assets, NREI and Dream Space onto the Society Pass corporate structure and ecosystem. We plan to continue to expand our e-commerce ecosystem throughout the rest of SEA by making selective acquisitions of leading e-commerce companies and applications with particular focuses on the VIP countries (Vietnam, Indonesia and Philippines) of SEA.

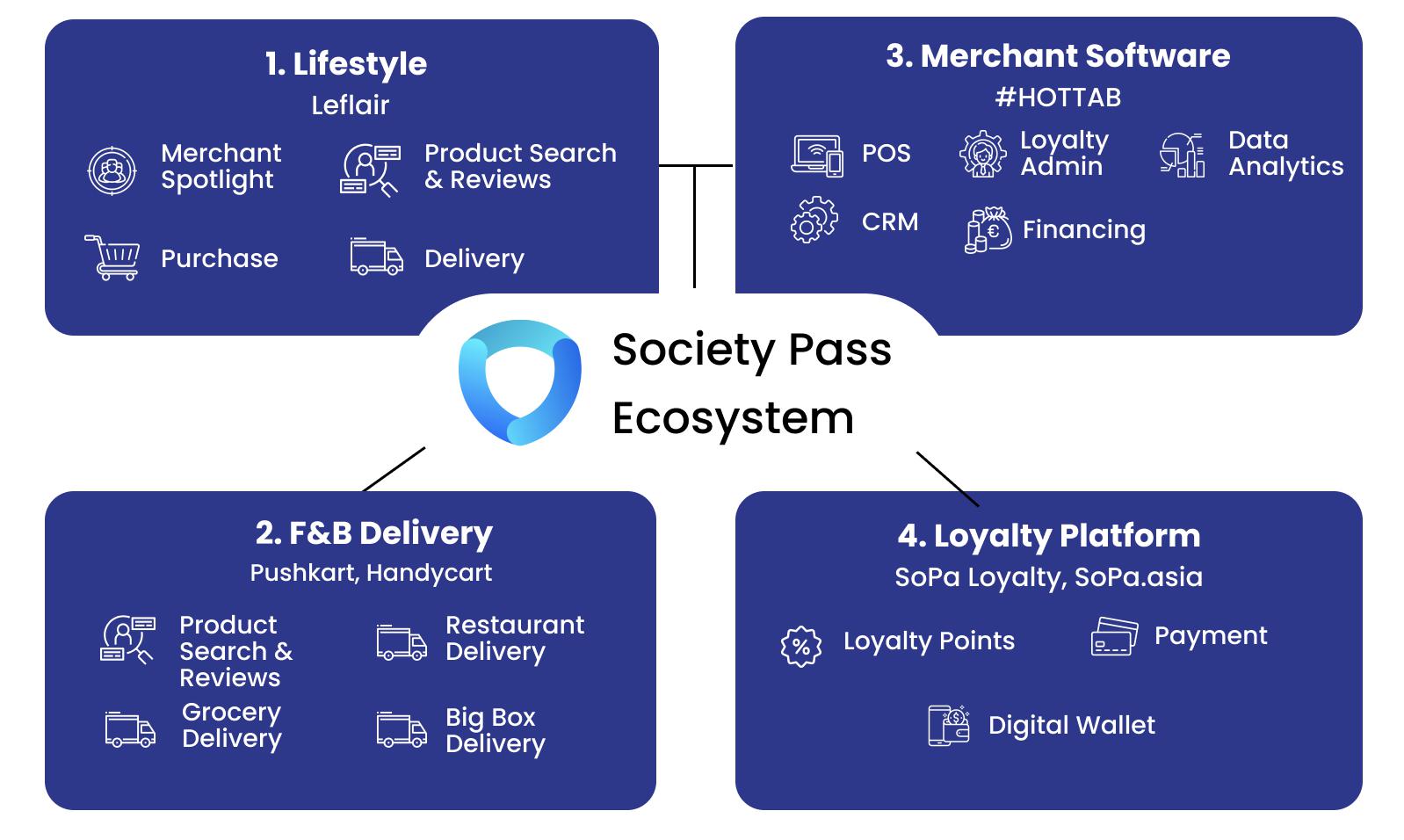

Our business currently comprises of the following four verticals: lifestyle, food and beverage (“F&B”) delivery, merchant software and loyalty. Lifestyle includes Leflair App and Leflair.com website; F&B Delivery includes Pushkart App, Pushkart.ph website, Handycart App, and Handycart.vn website. The merchant software segment includes #HOTTAB Biz App, #HOTTAB POS App and Hottab.net website, while the loyalty vertical includes Society Pass App and SoPa.asia website. In addition, we are looking at acquiring companies in the travel and digital media verticals. These current four and prospective e-commerce interfaces are collectively referred to in this Annual Report as the “Platform”.

Our loyalty-focused and data-driven e-commerce marketing platform interfaces connect consumers with merchants in the F&B and lifestyle sectors, assisting local brick-and-mortar businesses to access new customers and markets to thrive in an increasingly convenience-driven economy. Our Platform integrates with both global and country-specific search engines and applications and accepts international address and phone number data, providing a consumer experience that respects local languages, address formats and customs. Our Strategic Partners (as defined below) work with us to penetrate local markets, while our Platform allows effortless integration with existing technological applications and websites.

Leflair.com website and Leflair App are marketed in Vietnam and feature the following:

| • | Premium brand access. Provides access to more than 2,500 premium Vietnamese and international brands in the fashion and accessories, beauty, personal care, home and lifestyle markets. |

| • | Flash sales events. Highlight daily flash sales events with a curated selection of premium brands, all with guaranteed authenticity. |

| • | Premium packaging. Sold with premium packaging and brand specific content. |

| • | Customized searches. Filter and search program designed to optimize user experience. |

Pushkart.ph website and Pushkart App are marketed in Philippines and feature the following:

| • | Grocery store access. Provides access to more than 20 Philippines based grocery stores. |

| • | Customized technology solutions for smaller grocers and restaurants. Easy to onboard technology setup allows smaller grocers and restaurants to increase market coverage to potential consumers without having to pay for expensive B2C technology platform. |

| • | Quick delivery time. Even in crowded and congested Manila, our shoppers and drivers provide quick delivery time of less than 6 hours from time of order. |

| • | Growing selection of products. Our filter and search program is designed to allow users to select available products on the Pushkart platform. |

Handycart.vn website and Handycart App are marketed in Vietnam and feature the following:

| • | Restaurant focus. Focuses on providing delivery services for Korean, Japanese, Chinese and non-Vietnamese food restaurants in Hanoi. |

| • | Customized technology solutions for smaller grocers and restaurants. Easy to onboard technology setup allows smaller grocers and restaurants to increase market coverage to potential consumers without having to pay for expensive B2C technology platform. |

| • | Quick delivery time. Even in crowded and congested Manila, our shoppers and drivers provide quick delivery time of less than 6 hours from time of order. |

| • | Growing selection of products. Our filter and search program is designed to allow users to select available products on the Handycart platform. |

Branded as “#HOTTAB”, our merchant software business helps merchants increase revenues and streamline costs with an online and multilingual store front, fully integrated POS software solution, joint marketing program, payment infrastructure, loyalty administration, customer profile analytics, and SME financing packages. Through #HOTTAB Biz App, #HOTTAB POS and Hottab.net merchant administration website interfaces, #HOTTAB functions both online and offline and facilitates transactions, orders, voucher redemption, and rewards. Merchants only need a smart device in order to quickly access our #HOTTAB product ecosystem. In addition, our Customer Care department provides attentive after-sales service.

The Hottab.net admin website and #HOTTAB Biz App are marketed in both Vietnam and Indonesia and features the following services for merchants:

| • | Ordering/Payment. Merchants track their order history and accept all forms of payment methods, including Society Points, as well as review their payment history. |

| • | Offers and Promotions. Merchants easily create bundle offers or any kind of promotion. By awarding Society Points, merchants incent purchases without sacrificing margins. |

| • | Merchant Partnership Program. This value-added program is designed to optimize costs and increase revenues for our Merchants through a combination of personalized branding tools, joint marketing campaigns, and special vendor financing program. |

| • | Vendor Financing. Buy directly from featured suppliers with built-in financing, payment, and delivery management. Financing up to 100 million VND. |

| • | Connect with consumers. Merchants receive order details the instant consumers place an order on SoPa Loyalty application and SoPa.asia Marketplace. Merchants can also communicate with consumers via the integrated chat box function. |

| • | Menu and Loyalty Management. Merchants upload dish description, pictures, detailed menus directly from their smartphone. Multilingual option available for all of #HOTTAB merchants. Merchants can also create any kind of promotion and have full control to allocate Society Points at all levels. |

#HOTTAB POS APP are marketed in both Vietnam and Indonesia and feature the following products and services for merchants:

| • | Remote Management. Though our software, business owners, shareholders and managers can choose a time to receive daily report about their business including number of orders, daily and monthly revenue, revenue by cash/card, discounted amount, etc. |

| • | Operation Management. Through our POS software, managers can assign tier to staff and what they can access on the system. They can track orders, inventory, while also manage daily operation, table reservations. We bundle and sell our POS software solutions together with devices such as POS machines and remote receipt printers that are manufactured by others and for which we receive a commission on sales. We do not currently manufacture any products. |

SoPa.asia website and Society Pass App are marketed in Vietnam and feature the following:

| • | Location-based homepage. Based on consumers’ location, nearby SMEs and exclusive offers are selected and displayed on the Homepage for a smooth, user-friendly interaction. |

| • | Search/review. Our smart search engine, which allows consumers to search/review their favorite restaurants and cafes among tens of thousands of choices. Our ratings improve merchant customer service and product quality. |

| • | Merchant spotlight. Featured restaurants, cafes and bars get customized banners on SoPa.asia homepage, making it easier for consumers to discover and purchase from these merchants. |

| • | Cash/cashless payments. Consumers can decide on either cash or cashless payments. Payment integration partners (Momo, VNT, VTC, Zalo and Paytec), allow for fast and secure payments anytime and anywhere. Or users can pay by cash or with Society Points. Also, consumers can review purchase history. |

| • | Society Points (expected to be launched in Q2 2022). Beginning in the second quarter of 2022, we expect to launch our unique merchant agnostic and universal loyalty points, branded as “Society Points.” We expect that Society Points will create permanent customer loyalty for merchants through the issuance and redemption of Society Points with unique and personalized deals. After its launch, consumers will be able to use Society Points at merchant locations initially throughout Vietnam and then we expect to expand availability of Society Points throughout SEA. |

As of March 30, 2022, we have onboarded over 1.6 million registered consumers and over 5,500 registered merchants/brands on our Platform.

Our Competitive Strengths

Powerful and Integrated Ecosystem. Our ecosystem serves both consumers and merchants in ways that are designed to maximize value creation and enhance shopping experience. Our four unique verticals (lifestyle, F&B, merchant software, and loyalty) and five separate business units create a highly synergistic ecosystem, generating additional sales channels, and onboarding increasingly greater numbers of consumers and merchants. We leverage our verticals within our ecosystem to create multiple touch points for consumers and merchants and service them more efficiently. Our integrated technology platform and operational efficiencies drives value creation for SoPa ecosystem through our multi-faceted revenue model comprises of e-commerce revenues, delivery fees, brokerage fees, and SaaS revenues.

Unique Loyalty Program. Beginning in the second quarter of 2022, we expect to launch our foundational core product, Society Points, to create permanent loyalty between consumers and merchants as well as to our Platform. Merchant and location agnostic, we believe that Society Points replace cash discounting and create permanent customer stickiness. As Society Points are merchant/location agnostic, they can be earned and redeemed across different business units within SoPa ecosystem. Society Pass and Society Points are additional marketing channels for merchants on SoPa ecosystem to onboard more customers and generate more revenues in a cost efficient manner for their individual businesses.

Attractive Markets. We currently operate predominantly in Vietnam and Philippines, which are two of the fastest growing economies in the world. As we continue to opportunistically acquire market leading e-commerce platforms and scale up our operations, we intend to expand to other countries in SEA, especially Indonesia. Because they are attractively valued, regional acquisition opportunities allow Society Pass to quickly and more efficiently build consumer/merchant scale and expand service offerings. The VIP countries boast some of the fastest growing economies in the world, possess 500 million of SEA’s 720 million people, fast growing middle class, favorable demographics and quick adoption of mobile technology.

Experienced Management Team. Senior executives and directors possess +150 years of on-the-ground, operational, marketing, software development, legal and financial experience in local Asia markets and intimate knowledge of international capital markets. We are female managed with +60% of SoPa employees are female. Our CEO, CFO, CMO, COO and CTO all possess solid track records of building companies and creating value for shareholders and other stakeholders.

Recent Acquisitions

Pushkart Acquisition. On February 14, 2022, Push Delivery PTE Ltd., a Republic of Singapore corporation (“Push Delivery”), a wholly owned subsidiary of SOPA Technology PTE LTD, a Singapore company, which in turn is a 95% owned subsidiary of the Company acquired all of the outstanding capital stock of New Retail Experience, Incorporated, a Philippines company d/b/a Pushkart (“Pushkart”) pursuant to a Share Purchase Agreement (the “Pushkart Agreement”) dated February 14, 2022 among Push Delivery and all of the shareholders of Pushkart (the “Pushkart Sellers”). Pursuant to the Pushkart Agreement, the Pushkart Sellers were paid (i) $200,000 in cash upon the execution of the Agreement; and (ii) $800,000 in common stock of the Company, based on a share price of $3.53. Pushkart is a leading online grocery delivery service in the Philippines.

Handycart Acquisition. On February 25, 2022, Push Delivery acquired all of the outstanding capital stock of Dream Space Trading Co. Ltd, d/b/a Handycart, a Vietnam company (“Dream Space”), a leading online grocery delivery service based in Hanoi, Vietnam pursuant to a Transfer of Capital Contribution Agreement (the “Handycart Agreement”) dated February 25, 2022 among Push Delivery and the shareholder of Dream Space (the “Handycart Seller”). Pursuant to the Handycart Agreement, the Handycart Seller was paid 2,300,000 Vietnamese Dong (approximately $100). In connection with the Handycart acquisition, Push Delivery entered into an employment agreement with Seo Jun Ho, the former Director of Handycart, employing him as Handycart’s Head of Business Unit for one year or until terminated. Mr. Ho was issued $25,000 in common stock of the Company, based on a share price of $2.61. Pushkart is a leading online grocery delivery service in Hanoi, Vietnam.

Corporate Structure

Society Pass Incorporated (formerly named Food Society, Inc.) is a Nevada corporation that was incorporated on June 22, 2018. We operate solely through the Group. Summaries of each Group member are provided below.

Society Technology, LLC, a Nevada limited liability company formed on January 24, 2019, is owned by 100% by Society Pass Incorporated. Society Technology, LLC owns all intellectual property rights to copyrightable, patentable, and other protectable matter in our business, including trademarks.

SOPA Technology Pte Ltd, a company limited by shares incorporated under the laws of Singapore on June 6, 2019, is owned by 85% by Society Pass Incorporated. Society Technology Pte Ltd manages the Group’s operating activities in SEA. As of December 31, 2021, Society Pass Incorporated has increased its shareholding on SOPA Technology Pte Ltd to 95%

SOPA Cognitive Analytics Private Limited, a company limited by shares incorporated under the laws of India on February 05, 2019, is owned by 100% by Society Technology Pte Ltd. SOPA Cognitive Analytics Private Limited operated the Group’s technology and software development in India, which is now being transitioned to SEA.

SOPA Technology Co Ltd, a company limited by shares incorporated under the laws of Vietnam on October 1, 2019, is owned 100% by Society Technology Pte Ltd. SOPA Technology Co Ltd operates the Group’s consumer facing business in Vietnam.

Leflair Incorporated, a Nevada corporation formed on December 1, 2021, is a wholly owned subsidiary of the Company.

SOPA Capital Limited, a United Kingdom corporation formed on December 7, 2021, is a wholly owned subsidiary of the Company.

HOTTAB Pte Ltd, a company limited by shares incorporated under the laws of Singapore on January 17, 2015, is owned 100% by Society Technology Pte Ltd. HOTTAB Pte Ltd manages the Group’s regional merchant facing business in SEA.

HOTTAB Vietnam Co Ltd, a company limited by shares incorporated under the laws of Vietnam on April 17, 2015, is owned 100% by HOTTAB Pte Ltd. HOTTAB Vietnam Co Ltd manages the Group’s merchant facing business in Vietnam.

HOTTAB Asset Vietnam Co Ltd, a company limited by shares incorporated under the laws of Vietnam on July 25, 2019, is currently wholly-owned by one employee of HOTTAB Vietnam Co Ltd. HOTTAB Asset Vietnam Co Ltd manages the Group’s website and apps in Vietnam via a contractual relationship. HOTTAB Vietnam Co Ltd has an irrevocable call option to acquire 100% of the equity of HOTTAB Asset Vietnam Co Ltd.

SOPA (Philps) INC, a company limited by shares incorporated under the laws of Philippines on January 11, 2022 is owned 100% by SOPA Technology Pte Ltd.

Push Delivery PTE Ltd, a company limited by shares incorporated under the laws of Singapore on January 7, 2022 is a wholly owned subsidiary of SOPA Technology PTE Ltd.

Dream Space Trading Co. Ltd, d/b/a Handycart, a company limited by shares incorporated under the laws of Vietnam on May 23, 2018, is a wholly-owned subsidiary of Push Delivery.

New Retail Experience, Incorporated, a Philippines company d/b/a Pushkart formed on January 16, 2020, is a wholly-owned subsidiary of Push Delivery.

The following chart represents the structure of Society Pass and its operating subsidiaries.

Follow-on Public Offering

On February 11, 2022 we closed a public offering of 3,484,845 shares of our common and warrants to purchase 3,484,845 shares of our common stock (including the full exercise of the underwriter’s over-allotment option) at a public offering price of $3.30 per share and warrant to purchase one share of common stock. We received aggregate proceeds from the public offering of $11.5 million before deducting underwriting fees and commission and other offering expenses.

Our Market Opportunity

We expect that continued strong economic expansion, robust population growth, rising level of urbanization, the emergence of the middle class and the increasing rate of adoption of mobile technology provide market opportunities for our Company in SEA. As of 2020, SEA gross domestic product (“GDP”) totaled US$3.1 trillion. In comparison, the respective GDP for both the European Union (“EU”) and the United States (“US”) totaled US$15 trillion and US$20.8 trillion in 2020. SEA has experienced rapid economic growth rates in recent years, far exceeding growth in major world economies such as Japan, the EU and the US. According to the International Monetary Fund (“IMF”) since 2010, SEA has averaged 4.6% GDP growth, compared to 0.7% for Japan, 0.8% for the EU and 1.7% for the US. Vietnam’s GDP growth averaged 6.1% from 2011 to 2020 and is expected to average 7% for the next five years. The size of Vietnam’s economy grew from US$39 billion in 2000 to US$340 billion in 2020 and is projected to reach US$530 billion by 2025. SMEs are a dynamic, driving force in Vietnam’s economy, contributing 40% to its GDP last year.

SEA continues to enjoy robust population growth. The United Nations Population Division estimates that the population of the SEA countries in 2000 was approximately 525 million people growing to 668 million in 2020. Vietnam has a population of approximately 98 million people today compared to 80 million people in 2000.

This population growth is driving rising levels of urbanization. Mirroring the demographic trends in China more than 25 years ago, Vietnamese are moving to cities in greater numbers. In the past two decades, Vietnam’s urbanization rate has increased steadily at approximately 3% per year since 2000, with 36% of the population now living in cities. This urbanization trend is highly correlated with the growth of the middle class. Simply put, urbanization drives middle class consumption demand. According to the World Bank, Vietnam’s middle class currently accounts for 13% of the population and is expected to reach 26% by 2026. Fitch Solutions predicts that Vietnam’s real household spending will expand at an annual average annual growth rate of 7.5% year-on-year from 2021 to 2024.

And despite the ongoing effects from the Covid-19 pandemic, the Internet economy continues to boom in SEA. According to Google Temasek e-Conomy SEA 2020 Report, Internet usage in the region increased with 40 million new users added in 2020 for a total of 400 million compared to 360 million in 2019. Seventy percent of SEA’s population is now online, compared to approximately twenty percent in 2009. In addition, SEA mobile Internet penetration now reaches more than 67%. E-commerce, online media and food delivery adoption and usage surged with the total value of goods and services sold via the Internet, or gross merchandise value (“GMV”), in SEA, expected to reach more than US$100 billion by year end 2020 according to Google, Temasek, Bain SEA Report 2020. In fact, the SEA Internet sector GMV is forecast to grow to over US$300 billion by 2025.

Vietnam’s mobile penetration rate has reached 95% in city areas and among SEA countries, Vietnamese consumers spend the most time online for personal purposes, just after Singaporean users. According to Google Temasek e-Conomy SEA 2020 Report, total GMV of e-Commerce spending in Vietnam is currently US$ 14 billion and is forecast to grow to over US$ 50 billion by 2025.

We believe that these ongoing positive economic and demographic trends in SEA propelled demand for our Platform.

During the fiscal years ended December 31, 2021 and 2020, we recorded revenues of $34,830 and $40,719, respectively, from Aryaduta Hospitality & Leisure Group, which in fiscal years ended December 31, 2021 and 2020 accounted for approximately 5% and 75% of our revenues, respectively.

We incurred net losses of $34,760,640 and $3,864,740 in fiscal years ended December 31, 2021 and 2020, respectively.

Our Business Model

Our four inter-connected verticals (lifestyle, F&B, merchant software and loyalty) and 5 unique business units connect millions of registered consumers and thousands of merchants in SEA. For our consumers, we offer personalized promotions on our Leflair, Pushkart and Handycart platforms. For our merchants, we sell POS software, vendor finance and customized merchant marketing programs. And we expect to offer Society Points in the second quarter of 2022. Our business model incents both consumers and merchants to transact with one another to receive personalized offers, Society Points (when launched) and generate revenues.

Our Platform consists of seven interconnected interfaces:

| 1) | Society Pass Loyalty App; |

| 2) | SoPa.asia Loyalty Marketplace Website; |

| 3) | #HOTTAB Biz App; |

| 4) | Hottab.net Merchant Admin Website; |

| 5) | #HOTTAB POS App; |

| 6) | Leflair Lifestyle App; |

| 7) | Leflair.com Lifestyle Website; |

| 8) | Pushkart F&B Delivery App; |

| 9) | Pushkart F&B Delivery Website; |

| 10) | Handycart F&B Delivery App; and |

| 11) | Handycart F&B Delivery Website. |

The diagram below is a representation of our Society Pass Platform:

Our Growth Strategy

Simply put, our growth strategy is to onboard as many consumers and merchants as possible onto our Platform. Our virtuous cycle of consumer and merchant engagement is as follows: As more consumers and more merchants in SEA register on our Society Pass platform, more transaction data is generated. With more data generation, there are more opportunities for creating loyalty from consumers to merchants. SoPa’s ecosystem allows for:

| • | More revenue generation for merchants leads to creation of customer loyalty; |

| • | More customer loyalty creation leads to more consumers for merchants; |

| • | More consumers for merchants leads to greater revenues for merchants; which results in and |

| • | virtuous cycle of revenue generation and loyalty creation. |

Our goal is to make Society Pass the preferred e-commerce ecosystem for both consumers and merchants in SEA. Our Society Pass loyalty product allows merchants to create sticky interactions with their consumers. Our Leflair e-commerce platform allows premium international and domestic brands to reach a wider consumer base. We aim to make our #HOTTAB merchants successful by connecting them to a large consumer base along with the technology and marketing tools to maximize their sales. Our Pushkart and Handycart F&B delivery platforms provides consumers with convenient grocery and restaurant delivery options which alleviate time constraints on their busy lifestyles. In doing so, we engage our registered consumers with a reliable and user-friendly e-commerce ecosystem that serves all of their needs in the F&B and lifestyle verticals. This virtuous marketing cycle creates permanent customer loyalty to our Platform, which continuously drives consumer traffic, merchant participation and revenues.

The key elements of our growth strategy are as follows:

Acquiring other e-Commerce companies and applications in SEA

To complement our organic growth strategy, we will continue to opportunistically acquire regional e-commerce companies and applications to drive revenues and increase the number of registered consumers and merchants in our SoPa ecosystem throughout SEA with particular focuses on Vietnam, Philippines and Indonesia. Our anticipated investments and acquisitions of other e-commerce platforms and applications in different verticals are expected to expand our service offerings and attract new consumers and merchants. Our acquisition of #HOTTAB in November 2019, for example, allowed us to start marketing and selling to merchants in Vietnam. Our acquisition of the Leflair Assets in February 2021 allowed us to market and sell lifestyle products to consumers in Vietnam. Our acquisitions of NREI and Dream Space in February 2022 allowed us to deliver F&B products to consumers in Philippines and Vietnam, respectively. The Company is currently negotiating with acquisition targets in the lifestyle, F&B and travel verticals in SEA.

Launching our Loyalty System

Beginning in second quarter of 2022, we intend to market our unique merchant agnostic and universal Society Points to generate additional revenues for merchants and create permanent customer loyalty in SEA. Our Society Points are expected to play a pivotal role in attracting merchants to our Platform as they allow merchants to build permanent customer loyalty and more cost effectively market to new consumers and retain existing consumers. For consumers, Society Points will offer them both a cashless payment option and the ability to spend bonus points accumulated from one consumer vertical such as lifestyle to a separate one such as F&B.

Entering into Strategic Partnerships

The Company has entered into agreements with the following Vietnamese companies to provide essential services to the Platform:

Lala Move Vietnam Co. Ltd (“Lala Move”) and Tikinow Smart Logistics Co. Ltd (“Tikinow”) provides food delivery services for the Platform; VTC Technology and Digital Content Company (“VTC Pay”), Media Corporation (Vietnam Post Telecommunication Media) (“VNPT Pay”), Zion Joint DStock Company (“Zalo Pay”), and Online Mobile Service Joint Stock Co. (“Momo”) provide payment integration services to the Platform which allows merchants to process consumer transactions; SHBank Finance Co. Ltd (“SHB”) provides vendor financing to merchants on the Platform; Triip Pte. Ltd (“Triip”) provides travel agency services to the Platform; Paytech Company Limited (“Paytec”) provides payment integration and loyalty services to the Platform that allows merchants to process transactions with consumers; and Rainbow Loyalty Company Limited (“Rainbow”) provides loyalty services for merchants on the Platform. The aforementioned companies are collectively referred to in this Annual Report as “Strategic Partners”.

Strategic partnerships are vital to the strategy and operations of Society Pass ecosystem as they enable our Platform to offer more value-added services to both our consumers and merchants. We are constructing a regional loyalty alliance comprising of synergistic merchant partners. Through our partnerships, we gain access to our partners’ clients and users at minimal cost where possible and to proliferate the usage of Society Points (when available). From our partnerships, we also enhance our offerings like reliable delivery services through our relationships with delivery service providers and vendor financing options through our partnerships with financial institutions. Our marketing approach to acquire strategic partners focuses on the benefits of joining our Loyalty Alliance, stressing the ability to access a larger pool of consumers and clients while reducing marketing expenses via joint marketing efforts like press interviews, brochures and co-branding initiatives with merchants.

Maximizing the value of consumer transactions

Growing our consumer base, converting registered consumers into active ones, increasing transaction frequency, and maximizing basket sizes are key growth drivers for our lifestyle and F&B verticals. We are growing our base of registered consumers through a multi-pronged marketing approach across social media, emails, SMS, QR codes, tailored promotional campaigns and public relations engagement. Through these marketing approaches, we promote features of the SoPa branded interfaces as well as end-to-end capabilities from searches to orders to payments and finally to delivery. We believe that by serving consumers in all aspects of their daily lives, we create more opportunities to cross-sell and thus maximize our consumer wallet share.

Developing our data and analytics capabilities

We will further investing in identifying and mentoring female executives, acquiring entrepreneurial talent and hiring gifted software developers and marketing professionals to build the next generation digital ecosystem in Southeast Asia.

Expanding service offerings to merchants

Merchants are a critical component of our business, thus growing our registered merchant base and serving them with desirable technology and marketing solutions to improve sales, cut costs, and realize operational efficiencies. We onboard merchants through marketing outreach tools such as our websites, public relations, social media and focused sales efforts. In our marketing messages, we attract merchants to our ecosystem by offering them access to our growing consumer base as well as numerous opportunities to optimize their sales, including enhanced customer loyalty through the expected launch of our Society Points in the second quarter of 2022.

Expectation of Competition

We operate a loyalty-focused e-commerce ecosystem that connects consumers with merchants in the F&B delivery and lifestyle sectors. Across these verticals, we compete with other online platforms for merchants, who can sell their products on other food ordering platforms or online lifestyle retail marketplaces. We also compete with companies that sell software and services such as Software-as-a-Service providers and point-of-sale module vendors, enabling a merchant to run its business independently of our platform. We expect to be able to compete for merchants based on our unique Society Points feature once launched, which we expect will build lasting customer loyalty for our merchants, as well as our personalized, data-driven approach to customer engagement, both of which ensure that our success is aligned with that of our merchants’.

We also compete with other e-commerce platforms, fashion retailers and restaurants for the attention of the consumer. Consumers have the choice of shopping with any online or offline retailers, large marketplaces or restaurant chains that may also have the ability to build their own independent online platforms. We are able to compete for consumers based on our ability to deliver a personalized e-commerce experience with easy-to-use mobile apps, well-integrated payments and a reliable platform.

Intellectual Property Matters

The Company technology and platform comprise of various copyrightable and/or patentable subject matter owned and/or licensed by the Company’s wholly-owned subsidiary, Society Technology LLC (“Society Technology”), a Nevada limited liability company. Our intellectual property assets additionally include trade secrets associated with the software platform. We successfully carried out development of our multilayer cloud-based software platform from reliance on third parties for payment and loyalty points deployment. As a result, we can monetize our software by making its available in Apple Store and Google Play and compatible with existing payment systems depending on the country’s regulatory requirements.

The Company is currently focusing on using its intellectual property in SEA.

With regard to exclusive and non-exclusive licenses, there is a risk that these licenses could be construed in a manner that imposes unanticipated conditions or restrictions on the Company’s platform. Additionally, if portions of our proprietary software are determined to be subject to an open-source license, or if we do not correctly comply with the terms of the open-source software licenses applicable to our open-source software and technology, it could result in costly litigation or lead to negative public relations.

Occasionally, the Company may be targeted with patent infringement lawsuits or copyright infringement lawsuits. These cases may be brought by non-practicing entities that sustain themselves by suing other companies. Currently, the Company is not aware of any patent or copyright infringement suits against it, or contemplated to be brought against it.

The Company signed a Software Setup, Development and Use License Agreement (the “WF Agreement”) with Wallet Factory International Limited (“WF”) on November 15, 2018. Subject to the terms and conditions of the WF Agreement, WF granted a non-exclusive, sublicensable, transferable, perpetual, and irrevocable license to the Company to use the Licensed Technology in any manner allowed by use, to reproduce, to distribute, to make derivative works based on the Licensed Technology in the following countries: Vietnam, India, Indonesia, the Philippines, Thailand, Malaysia, Cambodia, Laos, Singapore and Brunei.

Trademarks

The Company is the owner of multiple registered and common law trademarks in connection with its technology and its services. The names and marks “Society Pass”, “SOPA”, “Leflair”, “#HOTTAB” and other trademarks, trade names, and service marks of Society Pass in this Annual Report are the property of Society Pass or its subsidiaries.

The Company arranges the registration of trademarks, trade names, and service marks in the name of Society Technology LLC, its wholly-owned subsidiary created for the purposes of managing all intellectual property matters of the Company. It is not the intent of this Annual Report to delineate each and every trademarkable matter of the Company owned through Society Technology. Without prejudice to the generality of foregoing, Society Technology is, inter alia, the owner of the registered trademarks “Society Pass”, “SOPA”, “Leflair” and “#HOTTAB”” in connection with artificial intelligence software, electronic payment services, loyalty programs, SaaS platforms, and other subsets of the Company’s business. Society Technology has 12 trademarks currently registered with the United States Patents and Trademark Office (the “USPTO”) and has two applications with the USPTO pending. Further, Society Technology filed and registered numerous trademarks with the trademark offices of Vietnam, India, Singapore, the Philippines, Malaysia, Indonesia, and Thailand. The complete list of the Company’s trademarks as of the date of this Annual Report is filed with the Company’s registration statement related to this Annual Report as Exhibit 21.1.

Item 1a. Risk Factors.

Investing in our common stock is highly speculative and involves a significant degree of risk. Before you invest in our securities, you should give careful consideration to the following risk factors, in addition to the other information included in this Annual Report on Form 10-K, including our financial statements and related notes, before deciding whether to invest in our securities. The occurrence of any of the adverse developments described in the following risk factors could materially and adversely harm our business, financial condition, results of operations or prospects. In that case, the trading price of our common stock could decline, and you may lose all or part of your investment.

Risks Related to Our Business

We have a limited operating history in an evolving industry, which makes it difficult to evaluate our future prospects and may increase the risk that we will not be successful.

The Company has a limited operating history on which to base an evaluation of its business and prospects. The Company is subject to all the risks inherent in a small company seeking to develop, market and distribute new services, particularly companies in evolving markets such as the internet, technology, and payment systems. The likelihood of the Company’s success must be considered, in light of the problems, expenses, difficulties, complications and delays frequently encountered in connection with the development, introduction, marketing and distribution of new products and services in a competitive environment.

Such risks for the Company include, but are not limited to, dependence on the success and acceptance of the Company’s services, the ability to attract and retain a suitable client base, and the management of growth. To address these risks, the Company must, among other things, generate increased demand, attract a sufficient clientele base, respond to competitive developments, increase the “SoPa” and “#HOTTAB” brand names’ visibility, successfully introduce new services, attract, retain and motivate qualified personnel and upgrade and enhance the Company’s technologies to accommodate expanded service offerings. In view of the rapidly evolving nature of the Company’s business and its limited operating history, the Company believes that period-to-period comparisons of its operating results are not necessarily meaningful and should not be relied upon as an indication of future performance.

The Company is therefore subject to many of the risks common to early-stage enterprises, including under-capitalization, cash shortages, limitations with respect to personnel, financial, and other resources and lack of revenues.

If we fail to raise capital when needed it will have a material adverse effect on the Company’s business, financial condition and results of operations.

The Company has limited revenue-producing operations and will require the proceeds from future offering to execute its full business plan. The Company believes the proceeds from its future offering will be sufficient to develop its intermediate plans. However, the Company can give no assurance that all, or even a significant portion of these shares will be sold or, that the moneys raised will be sufficient to execute the entire business plan of the Company. Further, no assurance can be given if additional capital is needed as to how much additional capital will be required or that additional financing can be obtained, or if obtainable, that the terms will be satisfactory to the Company, or that such financing would not result in a substantial dilution of shareholder’s interest. A failure to raise capital when needed would have a material adverse effect on the Company’s business, financial condition and results of operations. In addition, debt and other debt financing may involve a pledge of assets and may be senior to interests of equity holders. Any debt

financing secured in the future could involve restrictive covenants relating to capital raising activities and other financial and operational matters, which may make it more difficult for the Company to obtain additional capital or to pursue business opportunities, including potential acquisitions. If adequate funds are not obtained, the Company may be required to reduce, curtail, or discontinue operations.

We rely on internet search engines and application marketplaces to drive traffic to our Platform, certain providers of which offer products and services that compete directly with our products. If links to our applications and website are not displayed prominently, traffic to our Platform could decline and our business would be adversely affected.

We rely heavily on Internet search engines, such as Google, to drive traffic to our Platform through their unpaid search results and on application marketplaces, such as Apple’s App Store and Google’s Play, to drive downloads of our applications. Although search results and application marketplaces have allowed us to attract a large audience with low organic traffic acquisition costs to date, if they fail to drive sufficient traffic to our Platform, we may need to increase our marketing spend to acquire additional traffic. We cannot assure you that the value we ultimately derive from any such additional traffic would exceed the cost of acquisition, and any increase in marketing expense may in turn harm our operating results.

The amount of traffic we attract from search engines is due in large part to how and where information from and links to our website are displayed on search engine result pages. The display, including rankings, of unpaid search results can be affected by a number of factors, many of which are not in our direct control, and may change frequently. Search engines have made changes in the past to their ranking algorithms, methodologies and design layouts that have reduced the prominence of links to our Platform and negatively impacted our traffic, and we expect they will continue to make such changes from time to time in the future. Similarly, Apple, Google or other marketplace operators may make changes to their marketplaces that make access to our products more difficult. For example, our applications may receive unfavorable treatment compared to the promotion and placement of competing applications, such as the order in which they appear within marketplaces.

We may not know how or otherwise be in a position to influence search results or our treatment in application marketplaces. With respect to search results in particular, even when search engines announce the details of their methodologies, their parameters may change from time to time, be poorly defined or be inconsistently interpreted. For example, Google previously announced that the rankings of sites showing certain types of app install interstitials could be penalized on its mobile search results pages. While we believe the type of interstitial we currently use is not being penalized, we cannot guarantee that Google will not unexpectedly penalize our app install interstitials, causing links to our mobile website to be featured less prominently in Google’s mobile search results and harming traffic to our Platform as a result.

In some instances, search engine companies and application marketplaces may change their displays or rankings in order to promote their own competing products or services or the products or services of one or more of our competitors. For example, Google has integrated its local product offering with certain of its products, including search and maps. The resulting promotion of Google’s own competing products in its web search results has negatively impacted the search ranking of our website. Because Google in particular is the most significant source of traffic to our website, accounting for a substantial portion of the visits to our website, our success depends on our ability to maintain a prominent presence in search results for queries regarding local businesses on Google. As a result, Google’s promotion of its own competing products, or similar actions by Google in the future that have the effect of reducing our prominence or ranking on its search results, could have a substantial negative effect on our business and results of operations.

The ecommerce market is highly competitive and if the Company does not have sufficient resources to maintain research and development, marketing, sales and client support efforts on a competitive basis our business could be adversely affected.

The internet-based ecommerce business is highly competitive and the Company competes with several different types of companies that offer some form of user-vendor connection experience, payment processing and/or funds transfer content, as well as marketing data companies. Certain of these competitors may have greater industry experience or financial and other resources than the Company.

To become and remain competitive, the Company will require research and development, marketing, sales, and client support. The Company may not have sufficient resources to maintain research and development, marketing, sales and client support efforts on a competitive basis which could materially and adversely affect the business, financial condition and results of operations of the Company. The Company intends to differentiate itself from competitors by developing a payments platform that allows consumers and merchants to accept and use bonus points.

The market for consumer’s lifestyle is rapidly evolving and intensely competitive, and the Company expects competition to intensify further in the future. There is no guarantee that any factors that differentiate the Company from its competitors will give the Company a market advantage or continue to be a differentiating factor for the Company in the foreseeable future. Competitive pressures created by any one of the above-mentioned companies (and other direct or indirect competitors), or by the Company’s competitors collectively, could have a material adverse effect on the Company’s business, results of operations and financial condition.

The market for our Platform is new and unproven.

We were founded in 2018 and since our inception have been creating products for the developing and rapidly evolving market for API-based software platforms, a market that is largely unproven and is subject to a number of inherent risks and uncertainties. We believe that our future success will depend in large part on the growth, if any, in the market for software platforms that provide features and functionality to create the entire lifestyle ecosystem. It is difficult to predict customer adoption and renewal rates, customer demand for our solutions, the size and growth rate of the overall market that our Platform addresses, the entry of competitive products or the success of existing competitive products. Any expansion of the market our Platform addresses depends upon a number of factors, including the cost, performance, and perceived value associated with such solutions. If the market our Platform addresses does not achieve significant additional growth or there is a reduction in demand for such solutions caused by a lack of customer acceptance, technological challenges, competing technologies and products or decreases in corporate spending, it could have a material adverse effect on the Company’s business, results of operations and financial condition.

Delays in the implementation of or lack of consumer acceptance of Society Points could have a material adverse effect on our business.

We expect to launch Society Points in the second quarter of 2022 which will be a significant component to our SoPa consumer facing platform. However, if such launch is delayed or there is not the expected consumer acceptance of Society Points by consumers, our business and financial prospects could be materially and adversely affected.

If we are unable to expand our systems or develop or acquire technologies to accommodate increased volume our Platform could be impaired.

We seek to generate a high volume of traffic and transactions through its technologies. Accordingly, the satisfactory performance, reliability and availability of the Company’s website and platform, processing systems and network infrastructure are critical to our reputation and its ability to attract and retain large numbers of users who transact sales on its platform while maintaining adequate customer service levels. The Company’s revenues depend, in substantial way, on the volume of user transactions that are successfully completed. Any system interruptions that result in the unavailability of our service or reduced customer activity would ultimately reduce the volume of transactions completed. Interruptions of service may also diminish the attractiveness of our company and its services. Any substantial increase in the volume of traffic on our website or Platform or in the number of transactions being conducted by customers will require us to expand and upgrade our technology, transaction processing systems and network infrastructure. There can be no assurance that we will be able to accurately project the rate or timing of increases, if any, in the use of the Platform or timely expand and upgrade our systems and infrastructure to accommodate such increases in a timely manner. Any failure to expand or upgrade its systems could have a material adverse effect on the Company’s business, results of operations and financial condition.

The Company’s uses internally developed systems to operate its service and for transaction processing, including collections processing. The Company must continually enhance and improve these systems in order to accommodate the level of use of its products and services and increase its security. Furthermore, in the future, the Company may add new features and functionality to its services that would result in the need to develop or license additional technologies. The Company’s inability to add new software and hardware to develop and further upgrade its existing technology, transaction processing systems or network infrastructure to accommodate increased traffic on its platforms or increased transaction volume through its processing systems or to provide new features or functionality may cause unanticipated system disruptions, slower response times, degradation in levels of customer service, impaired quality of the user’s experience on the Company’s service, and delays in reporting accurate financial information. There can be no assurance that the Company will be able in a timely manner to effectively upgrade and expand its systems or to integrate smoothly any newly developed or purchased technologies with its existing systems. Any inability to do so would have a material adverse effect on the Company’s business, results of operations and financial condition.

The Company’s failure to successfully market its brands could result in adverse financial consequences.

The Company believes that continuing to strengthen its brands is critical to achieving widespread acceptance of the Company, particularly in light of the competitive nature of the Company’s market. Promoting and positioning its brands will depend largely on the success of the Company’s marketing efforts and the ability of the Company to provide high quality services. In order to promote its brand, the Company will need to increase its marketing budget and otherwise increase its financial commitment to creating and maintaining brand loyalty among users. There can be no assurance that brand promotion activities will yield increased revenues or that any such revenues would offset the expenses incurred by the Company in building its brand. Further, there can be no assurance that any new users attracted to the Company will conduct transactions over the Company on a regular basis. If the Company fails to promote and maintain its brand or incurs substantial expenses in an attempt to promote and maintain its brand or if the Company’s existing or future strategic relationships fail to promote the Company’s brand or increase brand awareness, the Company’s business, results of operations and financial condition would be materially adversely affected.

The Company may not be able to successfully develop and promote new products or services which could result in adverse financial consequences.

The Company plans to expand its operations by developing and promoting new or complementary services, products or transaction formats or expanding the breadth and depth of services. There can be no assurance that the Company will be able to expand its operations in a cost-effective or timely manner or that any such efforts will maintain or increase overall market acceptance. Furthermore, any new business or service launched by the Company that is not favorably received by consumers could damage the Company’s reputation and diminish the value of its brand. Expansion of the Company’s operations in this manner would also require significant additional expenses and development, operations and other resources and would strain the Company’s management, financial and operational resources. The lack of market acceptance of such services or the Company’s inability to generate satisfactory revenues from such expanded services to offset their cost could have a material adverse effect on the Company’s business, results of operations and financial condition.

In addition, if we are unable to keep up with changes in technology and new hardware, software and services offerings, for example, by providing the appropriate training to out account managers, sales technology specialists, engineers and consultants to enable them to effectively sell and deliver such new offerings to customers, our business, results of operations, or financial condition could be adversely affected.

A decline in the demand for goods and services of the merchants included in the Platform could result in adverse financial consequences.

The Company expects to derive most of its revenues from fees from successfully completed transactions on its consumer facing platforms. The Company’s future revenues will depend upon continued demand for the types of goods and services that are offered by the merchants that are included on such platforms. Any decline in demand for the goods offered through the Company’s services as a result of changes in consumer trends could have a material adverse effect on the Company’s business, results of operations and financial condition.

The effective operation of the Company’s platform is dependent on technical infrastructure and certain third-party service providers.

Our ability to attract, retain, and serve customers is dependent upon the reliable performance of our Platform and the underlying technical infrastructure. We may fail to effectively scale and grow our technical infrastructure to accommodate these increased demands. In addition, our business will be reliant upon third party partners such as financial service providers and cash-out providers, payment terminals and equipment providers. Any disruption or failure in the services from third party partners used to facilitate our business could harm our business. Any financial or other difficulties these partners face may adversely affect our business, and we exercise little control over these partners, which increases vulnerability to problems with the services they provide.

There is no assurance that the Company will be profitable.

There is no assurance that we will earn profits in the future, or that profitability will be sustained. There is no assurance that future revenues will be sufficient to generate the funds required to continue our business development and marketing activities. If we do not have sufficient capital to fund our operations, we may be required to reduce our sales and marketing efforts or forego certain business opportunities.

We could lose the right to the use of our domain names.

We have registered domain names for our website that we use in our business. If we lose the ability to use a domain name, whether due to trademark claims, failure to renew the applicable registration, or any other cause, we may be forced to market our products under a new domain name, which could cause us substantial harm, or to incur significant expense in order to purchase rights to the domain name in question. In addition, our competitors and others could attempt to capitalize on our brand recognition by using domain names similar to ours, especially in the light of our expected expansion in SEA. Domain names similar to ours may be registered in the United States and elsewhere. We may be unable to prevent third parties from acquiring and using domain names that infringe on, are similar to, or otherwise decrease the value of our brand or our trademarks or service marks. Protecting and enforcing our rights in our domain names may require litigation, which could result in substantial costs and diversion of management’s attention.

We may be required to expend resources to protect Platform information or we may be unable to launch our services.

From time to time, other companies may copy information from our Platform, through website scraping, robots or other means, and publish or aggregate it with other information for their own benefit. We have no assurance other companies will not copy, publish or aggregate content from our Platform in the future. When third parties copy, publish, or aggregate content from our Platform, it makes them more competitive, and decreases the likelihood that

consumers will visit our website or use our mobile app to find the information they seek, which could negatively affect our business, results of operations and financial condition. We may not be able to detect such third-party conduct in a timely manner and, even if we could, we may not be able to prevent it. In some cases, particularly in the case of websites operating outside of the United States, our available remedies may be inadequate to protect us against such practices. In addition, we may be required to expend significant financial or other resources to successfully enforce our rights.

Breaches of our online commerce security could occur and could have an adverse effect on our reputation.

A significant barrier to online commerce and communications is the secure transmission of confidential information over public networks. There can be no assurance that advances in computer capabilities, new discoveries in the field of cryptography and cybersecurity, or other events or developments will not result in a compromise or breach of the technology used by the Company to protect customer transaction data. If any such compromise of the Company’s security were to occur, it could have a material adverse effect on the Company’s reputation and, therefore, on its business, results of operations and financial condition. Furthermore, a party who is able to circumvent the Company’s security measures could misappropriate proprietary information or cause interruptions in the Company’s operations. The Company may be required to expend significant capital and other resources to protect against such security breaches or to alleviate problems caused by such breaches. Concerns over the security of transactions conducted on the Internet and other online services and the privacy of users may also inhibit the growth of the Internet and other online services generally, and the Web in particular, especially as a means of conducting commercial transactions. To the extent that activities of the Company involve the storage and transmission of proprietary information, security breaches could damage the Company’s reputation and expose the Company to a risk of loss or litigation and possible liability. There can be no assurance that the Company’s security measures will prevent security breaches or that failure to prevent such security breaches will not have a material adverse effect on the Company’s business, results of operations and financial condition.

The Company may not have the ability to manage its growth.

The Company anticipates that significant expansion will be required to address potential growth in its customer base and market opportunities. The Company’s anticipated expansion is expected to place a significant strain on the Company’s management, operational and financial resources. To manage any material growth of its operations and personnel, the Company may be required to improve existing operational and financial systems, procedures and controls and to expand, train and manage its employee base. There can be no assurance that the Company’s planned personnel, systems, procedures and controls will be adequate to support the Company’s future operations, that management will be able to hire, train, retain, motivate and manage required personnel or that the Company’s management will be able to successfully identify, manage and exploit existing and potential market opportunities. If the Company is unable to manage growth effectively, its business, prospects, financial condition and results of operations may be materially adversely affected.

The Company may engage in acquisition activity, which could have adverse effects on its business.

If appropriate opportunities present themselves, the Company intends to acquire businesses, technologies, platforms, services, or products that the Company believes are strategic. The Company currently has no binding commitments or agreements with respect to any material acquisition. There can be no assurance that the Company will be able to successfully negotiate currently contemplated acquisitions or successfully negotiate or finance future contemplated acquisitions, or to integrate such acquisitions with its current business. The process of integrating an acquired business, technology, service or product into the Company may result in unforeseen operating difficulties and expenditures and may absorb significant management attention that would otherwise be available for ongoing development of the Company’s business. Future contemplated acquisitions could result in potentially dilutive issuances of equity securities, the incurrence of debt, contingent liabilities and/or amortization expenses related to goodwill and other intangible assets, which could materially adversely affect the Company’s business, results of operations and financial condition. Any future contemplated acquisitions of other businesses, technologies, services or products might require the Company to obtain additional equity or debt financing, which might not be available on terms favorable to the Company, or at all, and such financing, if available, might be dilutive.

We rely on the performance of highly skilled personnel, and if we are unable to attract, retain and motivate well-qualified employees, our business could be harmed.

The Company is, and will be, heavily dependent on the skill, acumen and services of the management and other employees of the Company. Our future success depends on our continuing ability to attract, develop, motivate and retain highly qualified and skilled employees. Qualified individuals are in high demand, and we may incur significant costs to attract them. In addition, the loss of any of our senior management or key employees could materially adversely affect our ability to execute our business plan, and we may not be able to find adequate replacements. All of our officers and. employees are at-will employees, which means they may terminate their employment relationship with us at any time, and their knowledge of our business and industry would be extremely difficult to replace. We cannot ensure that we will be able to retain the services of any members of our senior management or other key employees. If we do not succeed in attracting well-qualified employees or retaining and motivating existing employees, our business could be harmed.

Illegal use of our Platform by could result in adverse consequences to the Company.

Despite measures the Company will implement to detect and prevent identify theft or other fraud our Platform remains susceptible to potentially illegal or improper uses. Despite measures the Company will take to detect and lessen the risk of this kind of conduct, the Company cannot assure that these measures will succeed. The Company’s business could suffer if customers use the Platform for illegal or improper purposes.

If merchants on our Platform are operating illegally, the Company could be subject to civil and criminal lawsuits, administrative action, and prosecution for, among other things, money laundering or for aiding and abetting violations of law. The Company would lose the revenues associated with these accounts and could be subject to material penalties and fines, both of which would seriously harm its business.

We are subject to certain risks by virtue of our international operations.