UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

For

the fiscal year ended

or

For the transition period from _____ to _____

Commission

file number:

(Exact name of registrant as specified in its charter)

(State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

| (Address of principal executive offices) | (Zip Code) |

Registrant’s

telephone number, including area code:

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

| The

| ||||

Securities registered pursuant to section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes

☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes

☐

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company, in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ☐ | Accelerated filer ☐ |

| Smaller

reporting company | |

| Emerging

growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate

by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness

of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered

public accounting firm that prepared or issued its audit report.

If

securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant

included in the filing reflect the correction of an error to previously issued financial statements.

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act).

Yes

☐ No

The

aggregate market value of the common stock, $0.086 par value per share, held by non-affiliates of the registrant, based on the closing

sale price of registrant’s common stock ($4.71) as quoted on the NASDAQ on June 30, 2023 (the last business day of the registrant’s

most recently completed second fiscal quarter), was approximately $

At April 4, 2024, the registrant had shares of common stock, par value $0.086 per share, outstanding.

DOCUMENTS

INCORPORATED BY REFERENCE:

TABLE OF CONTENTS

Industry and Market Data

Unless otherwise indicated, information contained in this Annual Report on Form 10-K concerning our industry and the markets in which we operate, including our general expectations and market opportunity and market size, is based on information from various sources, including independent industry publications. In presenting this information, we have also made assumptions based on such data and other similar sources, and on our knowledge of, and our experience to date in the relevant industries and markets. This information involves a number of assumptions and limitations, and you are cautioned not to give undue weight to such estimates. We believe that the information from these industry publications that is included in this Annual Report on Form 10-K is reliable. The industry in which we operate is subject to a high degree of uncertainty and risk due to a variety of factors, including those described in “Risk Factors.” These and other factors could cause results to differ materially from those expressed in the estimates made by the independent parties and by us.

PART I

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains forward-looking statements (within the meaning of the federal securities law) that involve substantial risks and uncertainties. All statements, other than statements of historical facts, included in this Annual Report on Form 10-K regarding our strategy, future operations, future financial position, future net sales, gross margin expectations, projected costs, projected expenses, prospects and plans and objectives of management are forward-looking statements. The words “anticipates,” “believes,” “estimates,” “expects,” “intends,” “may,” “plans,” “projects,” “will,” “would,” and similar expressions are intended to identify forward-looking statements, although not all forward-looking statements contain these identifying words. We have based these forward-looking statements on our current expectations and projections about future events. Although we believe that the expectations underlying any of our forward-looking statements are reasonable, these expectations may prove to be incorrect, and all of these statements are subject to risks and uncertainties. Should one or more of these risks and uncertainties materialize, or should underlying assumptions, projections, or expectations prove incorrect, our actual results, performance, or financial condition may vary materially and adversely from those anticipated, estimated, or expected. We have included important factors in the cautionary statements included in this Annual Report on Form 10-K, particularly in the section entitled “Risk Factors,” that we believe could cause actual results or events to differ materially from the forward-looking statements that we make. Our forward-looking statements do not reflect the potential impact of any future acquisitions, mergers, dispositions, joint ventures, investments or terminations of distribution arrangements that we may make. We do not assume any obligation to update any forward-looking statements, whether as a result of new information, future events, or otherwise, except as required by law.

Unless the context requires otherwise, references to “Reliance Global Group,” the “Company,” “we,” “our,” and “us” in this Annual Report on Form 10-K refer to Reliance Global Group, Inc.

Item 1. BUSINESS

About Reliance Global Group, Inc.

Reliance Global Group, Inc. (formerly known as Ethos Media Network, Inc.) was incorporated in Florida on August 2, 2013. In September 2018, Reliance Global Holdings, LLC, a related party (“Reliance Holdings”), purchased a controlling interest in the Company. Ethos Media Network, Inc. was renamed Reliance Global Group, Inc. on October 18, 2018.

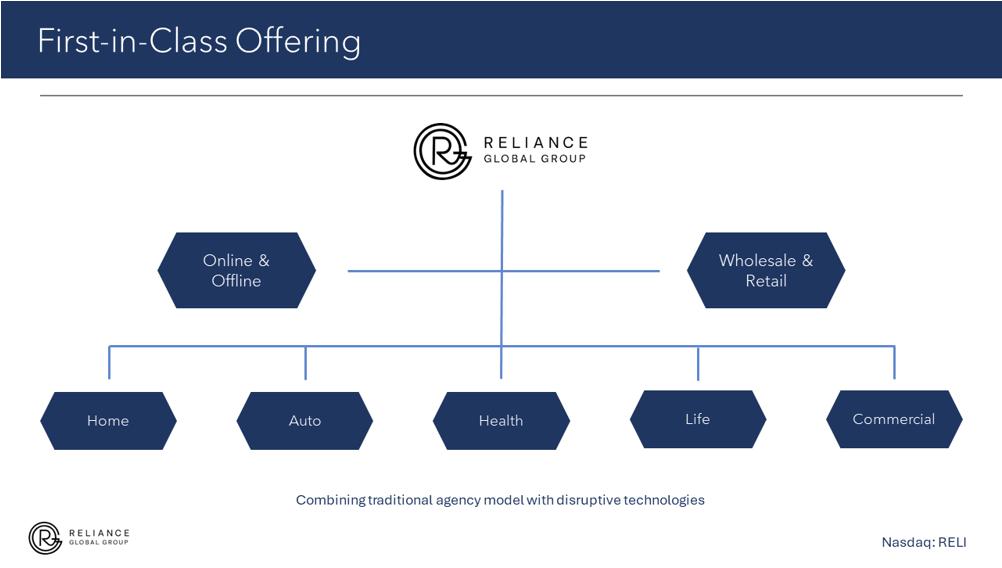

We operate as a company managing assets in the insurance markets, as well as other related sectors. Our focus is to grow the Company by pursuing an aggressive acquisition strategy, initially and primarily focused upon wholesale and retail insurance agencies. We are led and advised by a management team that offers over 100 years of combined business expertise in insurance, real estate and the financial service industry.

| 1 |

In the insurance sector, our management has extensive experience acquiring and managing insurance portfolios in several states, as well as developing specialized programs targeting niche markets. Our primary strategy is to identify specific risk to reward arbitrage opportunities and develop these on a national platform, thereby increasing revenues and returns, and then identify and acquire undervalued wholesale and retail insurance agencies with operations in growing or underserved segments, expand and optimize their operations, and achieve asset value appreciation while generating interim cash flows.

As part of our growth and acquisition strategy, we remain active in M&A markets and anticipate completing insurance agency/brokerage transactions throughout the course of 2024 and beyond. As of December 31, 2023, we have acquired nine insurance agencies. During 2022, the Company acquired Barra & Associates, LLC., an unaffiliated full-service insurance agency, which we rebranded to RELI Exchange and expanded its footprint nationally.

The Company also developed and launched 5MinuteInsure.com (“5MI”), a proprietary direct to consumer InsurTech platform which went live during the summer of 2021. 5MI is a business to consumer website which enables consumers to compare and purchase car and home insurance in a time efficient and effective manner. The platform is currently live in 44 states and offers coverage with more than thirty carriers.

Over the next 12 months, we plan to expand and grow our footprint and market share both through organic growth, and by expansion through additional acquisitions in various insurance markets.

Our competitive advantage includes the ability to:

| ● | Scale to compete at a national level. | |

| ● | Capitalize on the consumer shift to ‘online’ with the personal touch of an agent, as the only InsurTech company with this combination. | |

| ● | Leverage proprietary agency software & automation to compare carrier prices, for competitive renewal pricing. | |

| ● | Employ an empowered and scalable insurance agency model. | |

| ● | Leverage technology that facilitates comparing carriers for the best prices. |

The RELI Exchange Business to Business (“B2B”) InsurTech platform and partner network for insurance agents and agencies also:

| ● | Boast being the only white label insurance brokerage agency – New agents can have a multimillion-dollar agency look on day one, with a full suite of back-office support (business resources, licensing, compliance, etc.). | |

| ● | Combines the low barriers to entry of an agency network, with state-of-the-art tech. | |

| ● | Builds on the artificial intelligence and data mining backbone of 5MinuteInsure.com | |

| ● | Is designed to provide instant and competitive insurance quotes from more than thirty insurance carriers nationwide. | |

| ● | Reduces back-office burden and expenses by reducing the need for paperwork and redundant tasks. | |

| ● | Provides agents more time to focus on revenue driving activities, such as selling policies. |

In addition, we have a vast mentorship program behind the scenes, to upskill our sales teams. Once people are registered, we enroll them in our mentorship program, and coach them to bring new business.

RELI Exchange is a complete, private label system where agents have more flexibility in how they choose to brand themselves, compared to competitor platforms that require agents to work under the platform’s brand name. In effect, agents have a greater sense of ownership on our platform, and the feeling that comes with a well-financed agency.

| 2 |

Insurance Market Overview

There are three main insurance sectors: (1) property/casualty (P/C), which consists mainly of auto, home, and commercial insurance; (2) life/health (L/H), which consists mainly of life insurance and annuity products; and (3) accident and health, which is normally written by insurers whose main business is health insurance. The insurance industry plays a huge role in the U.S. economy (Source: OECD Insurance Statistics).

The U.S. remained the world’s largest insurance market, with a 40% market share of global direct premiums written in 2023, with premiums of $2.8 trillion, and Swiss Re forecasts that premiums will grow by an average 9% per annum over the next decade, stronger than the 7.5% annual average of 2015–2023 (Source: beinsure, Top Ranking the World’s Largest Insurance Markets 2024).

Insurance Agency Industry Overview

Insurance agencies act as intermediaries between insurance carriers and consumers. Unlike carriers, agencies do not bear insurance risk. The market has grown steadily including a sharp increase in 2019 due to macroeconomic growth, beneficial legislation, COVID treatments, and positive trends within the insurance sector. While inflation and other factors have impacted the industry, it has continued to grow through 2021. The market flattened in 2022 (12.15% of US GDP in 2022 vs. 12.20% in 2021), with a positive outlook due to the increased use of AI. Results may be impacted by changes to federal interest rates, with the federal funds rate skyrocketing from about 0% in early 2022 to 5.33% in February 2024, the highest rate in over 20 years (Source: St. Louis Federal Reserve, Federal Funds Effective Rate).

An insurance agency or broker solicits, writes, and binds policies through many different insurance companies, as they are not directly employed by any insurance carrier. Thus, insurance agencies can decide which insurance carriers they would like to represent and which products they would like to sell. They are like a retail shop that sells insurance services and products created by the insurance carrier. The main difference between a broker and an agent has to do with who they represent. An agent represents one or more insurance companies, acting as an extension of the insurer. A broker represents the insurance buyer.

An insurance carrier, on the other hand, is a manufacturer of insurance services and products that the insurance agencies sell. They control the underwriting process, claims process, pricing, and the overall management of the insurance products. Insurance carriers do not sell their products through direct agents, but only through independent agencies. Insurance policies are created and administered by the insurance carrier.

A key operating difference between agencies and carriers is the risk profile. The potential financial risks to the insurance industry caused by unforeseen events such as natural disasters are the responsibility of the carriers (and their re-insurers). Agencies and brokers bear no insurance risk. Furthermore, increased damage caused by natural disasters generally boosts demand for insurance and results in possible premium increases. Since insurance brokers and agents are a central part of the distribution of these products, they normally benefit from this increase in demand and premiums despite damaged profit margins among these upstream underwriters and carriers. (Source: IBISWorld Insurance Brokers & Agencies Industry in the US, January 2023). Natural disasters are inherently difficult to forecast, but any increase in the frequency of these events has the potential to boost insurance policy volumes, particularly for property and casualty products.

| 3 |

This risk difference is key, especially considering volatile weather patterns and an increased rate of natural disasters. The economic costs of 2023’s natural disaster events was $380 billion, up from $313 billion in 2022 (Source: Statista, Cost of natural disaster losses worldwide from 2000 to 2023, by type of loss). Insurance only covered 42% of the total damages from 421 natural disaster events in 2022 (Source: AON, Testimony of Eric Anderson, President of Aon, before the United States Senate Committee on Budget, Wednesday, March 22, 2023).

Key external drivers for insurance industry performance include factors such as motor vehicle registrations, the homeowner rate, and per capita disposable income. The industry is in a hardening cycle, which leads to growth. There are still effects from the COVID-19 measures, with shifting sales trends expected to boost profitability while lowering marginal costs. Additionally, businesses rebounding from COVID-19 are reported to translate to a consistent stream of new insurance customers (Source: IBISWorld, Insurance Brokers & Agencies Industry in the US, January 2023).

In 2023, the global insurance brokerage & agency market had an estimated value of $436 billion, and is forecasted to grow 7.2% to $468 billion in 2024 and to $613 billion by 2028 (Source: Research and Markets, Insurance Brokers & Agents Global Market Report 2024). The insurance distribution industry continues to prove its resiliency and the growth is reflected in continued robust mergers and acquisition (M&A) activity within the sector, despite decreases as compared to recent prior years. Total deal volume in 2023 was $78 billion, 41% lower than in 2022, with a 15% drop in total deals to 1,062 M&A deals in 2023. That said, there were 22 mega-deals of over $1 billion in 2023, a 38% increase over 2022 (Source: GlobalData, Insurance M&A Deals 2023 – Top Themes – Thematic Intelligence). The drop in deal volume was due to a 40-year high in inflation, rising capital costs and tightening budgets. As rate increases have already peaked, companies may allocate more capital to acquisitions. In 2024, there is an expected influx of private equity money into insurance M&A. (Source: Deloitte, 2024 insurance M&A outlook: Climbing the leaderboard).

The global InsurTech market size was valued at $16.6 billion in 2023 and is expected to grow to $336.5 billion by 2032, including the highest CAGR of 41.0% between 2023 and 2032 (Market.us, Global Insurtech Market By Type (Auto, Business, Health, and Other Types), By Deployment (On-Premise, and Cloud Based), By Technology, By Services, By End-User, By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, and Forecast 2023-2032). The increasing need for digitization of insurance services is expected to propel the market growth. Insurtech is the usage of technology innovations particularly designed to make the existing insurance model more efficient. By using technologies such as AI and data analytics, InsurTech solutions allow products to be priced more competitively. Insurance companies are widely adopting these solutions to drive cheaper, better, and faster operational results. Hence, the insurance industry is witnessing increased investment in technology. The outbreak of COVID-19 had a positive impact on the market. Numerous insurance companies are reconsidering their long-term strategies and short-term needs. COVID-19 and its impacts have accelerated the implementation of online platforms and new mobile applications to meet consumer needs. (Sources: Grand View Research, Insurtech Market Size, Share & Growth Report, 2021-2028 and 2022 - 2030).

The Company therefore has strategically invested in its RELI Exchange and 5MinuteInsure.com online digital platforms as additional steps in expanding its national footprint which now also includes a client referral portal. As discussed above, RELI Exchange and 5MI are high-tech proprietary tools developed by the Company as business to business or business to consumer portals which enables agents/consumers to compare and purchase car home and life insurance in a time efficient and effective manner. These platforms tap into the growing number of online users and utilize advanced artificial intelligence and data mining techniques, to provide competitive insurance quotes in around 1-5 minutes, with minimal data input needed from the agent/consumer.

| 4 |

General Industry Outlook

Insurance brokers and agencies play a critical role within the insurance market by distributing policies and consulting insurance underwriters and consumers. This industry is a vital component to the larger insurance sector as industry operators act as intermediaries between insurance providers and downstream consumers. Operators generate income via commissions earned on policies sold. Given the transaction-based nature of the industry, revenue primarily depends on three factors: (1) policy (premium) pricing; (2) demand for insurance; and (3) the popularity of using agents and brokers in the distribution process.

As mentioned, the insurance broker and agency industry has grown steadily over the five years due to macroeconomic growth, beneficial legislation that has been passed, and positive trends in the insurance sector, achieving approximately $436 billion in revenues in 2023. As macroeconomic conditions improve over the next few years, revenue generated by industry operators is expected to increase to $613 billion in 2028 as businesses regain confidence in their financial stability, despite increased external competition from online insurance marketplace platforms.

Insurance carriers should not continue to depend on the positive (though uncertain) fundamental economic strength of years past to maintain positive balance sheet momentum. To succeed, carriers must address foundational challenges, which include remaining relevant despite systemic economic changes combined with expanding consumer preferences. Some of the issues that insurers must address will fall within the areas of mergers and acquisitions (M&A), technology, product development, talent, regulation, as well as tax reform, as described below.

| ● | M&A. The convergence of market pressures to attain sustainable growth, a persistent wealth of capital and capacity, combined with the upturn in interest rates may demonstrate that insurers should be prepared for an uptick in M&A activity in 2024. As it stands now, fairly rich valuations could dampen activity, however, M&A could offer opportunities to scale and obtain new capabilities, primarily as it relates to technology. | |

| ● | Proprietary Technology. Advancements in AI, mobile and digital technology are forcing insurers to innovate, which is expected to continue and intensify, where every insurance agency will need to focus on what makes their customer experiences and products unique. They will also need to integrate with technology enablers to bring to their customers a value proposition via a connected ecosystem. Furthermore, to better compete within the industry, those within the distribution system would benefit tremendously by improving the ability to share critical data and analytics between systems. Insurers are seeking to employ the cloud to power advanced analytics, improve data gathering, and grow cognitive applications. To keep pace with the industry and prepare for a cloud-enabled future, insurance carriers should prioritize migrating their existing systems to the cloud and launch new applications off-site. | |

| ● | Product Development. Economic and technological changes create the need for new types of coverage, revamped policies, and alternative distribution platforms; adaptation of this, however, has been slow within the insurance industry. Siloed business lines, legacy processes, and regulatory considerations hinder the rapid and agile product development needed within this highly competitive landscape. Accordingly, insurers would benefit by focusing on creating hybrid policies that cover both commercial and personal risks. They could also supply on-demand coverage options, which provide greater control to customers for their policy terms and time frames. Furthermore, novel and unique micro-experiences could become the foundation for digital expansion as agencies are distinguished by the niche markets they sell to and can better service versus their peers. Digital content campaigns and user interfaces targeting specialized prospects and customer segments are expected to continue to expand. These micro-experiences could allow agencies to have access to a market that can quote, bind, and service insurance online, and where they are focused on commercial lines and specialty insurance for niche markets. In such a scenario, they may be able to offer new opportunities for agencies to expand quickly via digital building blocks that can be easily integrated into existing business and/or workflows. |

| 5 |

| ● | Regulation. Regulation will continue to play a significant role in the operations and development of the insurance industry, with three high-priority compliance issues (each with global and domestic implications) facing insurers: |

| ○ | Market conduct. “Best interest” standards have been implemented and more are being considered at both the federal and state levels to protect consumers who purchase annuities and life insurance. In 2020, the NAIC required producers to put the consumer’s interests ahead of their own. Currently, the NAIC’s Suitability in Annuity Transactions Model Regulation (#275) has been adopted by 41 states. It aims to protect consumers from potentially abusive and predatory practices among life insurance and annuity producers (Source: NAIC, The NAIC Annuity Suitability “Best Interest” Model Regulation). Additionally, similar standards were adopted in New York (Source: Debevoise & Plimpton, New York’s “Best Interest” Rule for Life and Annuities Found Constitutional). Due to these standards, insurers should seek to review and adjust their compliance structures to accommodate what could turn into a patchwork oversight system. One possibility could be to integrate new technologies that would allow for continual oversight and management of the sales process. | |

| ○ | Cyber risk. With New York State’s latest cybersecurity regulations, insurers are facing compliance deadlines, which have formed the basis of a nationwide model law developed by the National Association of Insurance Commissioners. Going forward, the spotlight is likely to be on how insurers plan to manage third-party risks, given so much importance has been placed on migrating policyholder data and software systems to external hosts. | |

| ○ | Privacy oversight. Privacy is both a data-security and reputational risk issue given the European Union’s General Data Protection Regulation (GDPR) having been implemented along with similar standards set to be imposed in California. Equally as important is how data can be used moving forward, specifically when it comes to disclosure and consumer signoff. In addition to legal and IT experts, insurers should include multiple stakeholders in its compliance efforts. Over the longer term, carriers may reexamine how the vast amounts of alternative data at their disposal may be leveraged for the mutual benefit not only for the carriers but their policyholders, while simultaneously remaining compliant with domestic and global regulations. |

| ● | Taxes. The global trend has been to lower corporate income tax rates, with a recent report from the Organization for Economic Co-operation and Development citing significant tax reform packages enacted in Argentina, France, Latvia, and the U.S., with other countries introducing more disjointed reforms. U.S. insurers continue to focus on adapting to the changes introduced in the Tax Cuts and Jobs Act of 2017. The U.S. Department of the Treasury and the Internal Revenue Service (IRS) have issued final and proposed guidance on certain important, newly enacted provisions, such as the application of the base erosion and anti-abuse tax to reinsurance, as well as the taxation of foreign operations owned by U.S. taxpayers. Additional guidance could be imminent on many other important provisions, including how the new loss carryover rules will fit with the old rules in the context of consolidated returns. |

Further complexity may come from several areas in 2024, including (Source: Accenture, 5 predictions for the insurance industry in 2024):

| ● | Monetizing AI, including generative AI such as ChatGPT. | |

| ● | Alternative human capital strategies which include the use of generative AI acting as “supplementary talent.” | |

| ● | Cost pressures driving operational model change including allocation methodologies and centralized costs. | |

| ● | Risk portfolio shifts and capital reallocation, including shifts into the retirement space as Millennials and GenZ become beneficiaries. | |

| ● | Service revenue increases alongside risk capital decreases, to raise RoE, and to expand product offerings in advice and services including tele-health, care navigation, and risk mitigation. |

While the industry may need to address internal and external pressures, the impact from these issues will continue to fall within the individual insurer. Thus, since insurers have choice in their decision making process, potentially the most significant factor is likely to be how committed and prepared insurers are to quickly adjust to changes in the economy, society, and technology, and respond accordingly.

Insurance Options

Single-product platforms limit buyers’ choices and often lead to high costs or insufficient coverage. We’ve partnered with an extensive list of carriers and filter results for buyers according to their needs. This gets them the right coverage at a fair price. From there, they’re connected to an agent who onboards them with minimal friction.

Insurance Buyers

Insurance buyers want coverage that fits their needs at a fair price. They also want good customer service. We believe the independent insurance agents, combined with the RELI Exchange platform can serve these needs best. Our platform makes it easy to weigh the options and connect with a knowledgeable agent with the buyer’s interests in mind.

| 6 |

Expert Agents

We train our agents to evaluate coverages based on buyers’ needs, and to explain options in simple terms. Furthermore, service doesn’t stop there. People’s needs change during different life events, and we facilitate adjustments to their coverage when it matters most.

Agents can revolutionize their insurance businesses—or start a new one on RELI Exchange. They have the freedom to offer coverage from a variety of carriers, utilizing our cutting-edge technology, and proven sales system. This is particularly beneficial to captive insurance agents who previously found themselves limited to one carrier and pricing model. By offering more choices, agents now have more chances of closing business with interested buyers. By partnering with us, agents gain access to a variety of carriers, yet are able to streamline their workflows to focus on business development with support from our team and lower marketing costs.

Top Carriers

Insurance carriers want to maximize profits without detracting from the customer experience. The challenge is that it’s costly to distribute coverage through independent agents with varying levels of expertise. Some carriers choose the Captive Agent route to save on cost, but RELI Exchange offers a better alternative. We reduce overhead and scale distribution for carriers while maintaining good standards with our technology and back office support team.

The performance improvements and lower costs lead to higher customer retention and a better customer experience, which translates to a higher customer lifetime value and more profits for the carrier and the agent.

Leadership Team

Our leadership team has over 100 years of combined industry experience.

Ezra Beyman, Chairman & Chief Executive Officer, brings nearly three decades of entrepreneurial experience in real estate and fifteen years in insurance. His portfolio of commercial and residential properties at one point consisted of more than 40,000 residential units, as well as several insurance companies. In 1985, he founded his first mortgage brokerage, which rapidly grew into the third largest licensed mortgage brokerage in the United States of America by 2008. He also expanded to real estate acquisition, having grown his portfolio to over three billion dollars.

Scott Korman, Director, serves as President of Nashone, Inc., a private equity firm, which he founded in 1984. In this role, Mr. Korman is involved in financial advisory, M&A, and general management assignments. He is a founder and Managing Member and CEO of Illumina Radiopharmaceuticals LLC, CEO of Red Mountain Medical Holdings, Inc. Mr. Korman previously served as Chairman of Da-Tech Corporation, a Pennsylvania based contract electronics manufacturer and as Chairman and CEO of Best Manufacturing Group LLC, a leading manufacturer and distributor of uniforms, napery, service apparel, and hospitality and healthcare textiles. Mr. Korman also served as President and CEO of Welsh Farms Inc., a full-service dairy processor and distributor of milk, ice cream mix and ice cream products.

Ben Fruchtzweig, Director, brings decades of executive experience in accounting and financial services. He has served as Chief Comptroller/Financial Analyst at national financial services and investment companies. He received his NYS C.P.A. license in 1987 and has worked at Deloitte Haskins and Sells and other leading accounting firms. Currently, Mr. Fruchtzweig lectures on a variety of topics including business ethics. He also serves on a voluntary basis as a trustee of a non-profit private foundation, which serves to provide the needed financial support, services and guidance to qualifying individuals and families.

Sheldon Brickman, Director, brings over 25 years of M&A advisory and business development experience with more than $40 billion in deals value. He has worked for numerous multibillion-dollar insurance carriers, including assignments for such companies as AIG, Aetna and National General. Sheldon has assisted international companies (UAE, UK, Asia and Latin America), start-up operations, and regional insurance carriers. Mr. Brickman’s experience covers the property casualty and life/health markets, including working with insurance carriers, managing general agencies, wholesalers, retailers and third-party administrators.

Alex Blumenfrucht, Director, previously served as CFO of Reliance, and prior to that, served as an Audit & Assurance Professional at Deloitte & Touche, LLP where he successfully led audit teams on both public and privately held corporations. He brings extensive experience in internal controls, financial analysis and reporting for both private and publicly traded companies. Currently Alex serves as the CFO of a Private Equity backed company in the healthcare space. Additionally, he has served as a Board Member of an ESOP structured entity.

| 7 |

Joel Markovits, CPA, Chief Financial Officer, Joel joined Reliance Global Group in June 2021, bringing over 12 years of financial and accounting experience in both the public and private sectors. Prior to joining Reliance Global Group, Joel was a senior manager at KPMG LLP from April 2015 through May 2021, where he led some of the larger and more complex audit engagements, including serving as lead audit senior manager on a global $16 billion (annual revenues) enterprise reporting on both US GAAP and IFRS standards. He was also a data & analytics specialist and technology innovation leader at KPMG for its largest US Business Unit, overseeing the development and deployment of technological capabilities that enhance data analyses. Joel has been a Certified Public Accountant in the State of New Jersey since November 2013.

Yaakov Beyman - Executive Vice President, Insurance Division, oversees the overall insurance operations of Reliance, including strategy and developing/implementing operational tools. He holds insurance licenses in most of the continental United States, and is involved heavily in marketing, maintaining state of the art technological models, financial management and distributions, and entity creation and maintenance.

Grant Barra - Senior Vice President of Operations, Mr. Barra brings extensive insurance experience scaling businesses by employing innovative tactics to increase revenue and overall profitability. He founded Barra & Associates in 2008 and served as its CEO until it was acquired by Reliance in 2022 and subsequently rebranded as RELI Exchange. Concurrent with the acquisition, Mr. Barra was appointed as Reliance’s senior vice president of operations, where he’s responsible to oversee operations, innovation, and growth, amongst other senior responsibilities.

Moshe Fishman, Director of Insurtech and Operations, brings a unique perspective to the insurance sales process. Prior to starting his own insurance agency, Mr. Fishman was a recognized guru in the travel industry leveraging the technology in the travel sector. This tech savviness has been applied into the insurance and financial services industries with the founding of Fishman Insurance Agency as well as Tekeno Financial. Mr. Fishman is one of the driving talents of the RELI Exchange & 5MinuteInsure.com InsurTech platforms.

Agency Partner network and proprietary InsurTech platform at ReliExchange.com

Our Go-to-Market Strategy

Our Go-to-Market high level goals include:

| ● | Brand awareness |

| ● | Targeted Market Segmentation and Positioning |

| ● | Content Marketing and Thought Leadership |

| ● | Best in class recruitment team |

Target #1: Captive

| ● | When an agent represents one insurance company, they have limited offerings for clients, assuming the same activity they’ll close more business, earning multiples of what they make currently due to our partnerships with many of the largest carriers in the industry. |

| ● | Key target for Agency Partners |

| ● | Eliminate many of the biggest expenses running an independent agency as an Agency Partner with RELI Exchange. |

| 8 |

Target #2: Agency Producers/CSRs

| ● | Agents that want their own agency. |

Target #3: New Agency Startups

| ● | Our platform makes it easy for those with little to no experience that want to start their own agency business. This is a significant market with manty potential participants. |

Promotion

To meet our agency registration objectives, we have engaged in both inbound and outbound marketing. Outbound sales and marketing includes outreach on social media through posts and direct messages using tools on LinkedIn and other platforms, phone, email, and other methods of communication. Inbound marketing is primarily through driving traffic to our website through search engines, social media, and digital publicity campaigns. These combined tactics give us a constant influx of marketing qualified leads (MQL) and sales qualified leads (SQL) to predictably hit our target metrics each month.

Email Marketing

As we continue to build our database of customers and prospects, we will implement an effective email marketing campaign. This includes newsletters as well as content flows that drip out over time to keep people engaged. This content is pre-programmed to automatically fire at set intervals whenever someone registers for a list. Through automation, we continue to build rapport with people who eventually sign up for the service.

Public Relations

The digital marketing tactics that we use have the following benefits:

| ● | Increase brand credibility | |

| ● | Generate leads | |

| ● | Attract investors and partners | |

| ● | Make other marketing more effective | |

| ● | Attract talent | |

| ● | Improve reputation on Google | |

| ● | Drive domain authority for SEO | |

| ● | Differentiate from competitors | |

| ● | Increase perceived value | |

| ● | Convert leads faster |

| 9 |

Social Media

As part of our content creation process, we’ve implemented a system for ongoing posts to social media channels such as LinkedIn. Tactics include:

| ● | Daily social listening – eye-on competitor + industry news + influencer | |

| ● | Creative design and content planning | |

| ● | Daily posting schedule | |

| ● | Real-time events support and live posting | |

| ● | Daily monitoring comments and discussions | |

| ● | A content coordinator with approving capabilities to approve/direct. | |

| ● | Monitoring data, providing monthly reports | |

| ● | Weekly meetings with updates on new content, industry news approval etc.… | |

| ● | Daily outreach, engagement, and growth of LinkedIn profile. | |

| ● | Weekly: 2 posts that demonstrate expertise, experience and thought leadership. | |

| ● | Monthly: Strategic growth and visibility |

Using platforms like LinkedIn, Facebook, and Twitter, we post regular content with the aim of growing our visibility and credibility through social media storytelling. Our goal is to maintain a consistent brand story for customers, prospects, stakeholders, and industry experts.

Planning, writing, creating, and posting a mixture of our available assets, plus curated topics on industry trends and influencer thought leadership to provide validation and exposure outside of our existing followers, to develop the company story.

Our initial focus is on LinkedIn, with expansion to other platforms as it makes sense.

Podcasts

We have appeared on several podcasts as subject matter experts, and will continue with outreach to increase exposure, visibility, brand awareness, and sales.

Website Search Engine Optimization

Our goal is to improve the website to drive more organic traffic through Google and other search engines. The two primary objectives are to create engaging content, and to improve the technical SEO of the website.

SEO growth opportunities include:

| ● | SEO Audit and Execution to improve HTML, structured data and other technical issues | |

| ● | SEO review of any future site migration and platform upgrade plans as part of the M&A process | |

| ● | Information architecture & internal linking for SEO | |

| ● | Content topic and structural improvements | |

| ● | Keyword Tracking | |

| ● | Competitive analysis |

Product

Our best-in-class product offerings include the following:

| 1) | An agency partner contract | |

| 2) | An agent / pro contract |

| 10 |

Our value proposition is that we’re giving people a complete, white label business. Agents have a fast and easy website presence, get contracts with carriers they wouldn’t normally access, and they can get paid for referrals.

Price

Costs are very low. Access is approximately $90/month for agents, and $190/month for agency partners. This is a singular solution that gives people an all-in-one insurance agency.

For comparison, people used to pay about $50,000 to build out an insurance agency. Additionally, licensing can be around $750, with $100-200 in monthly expenditures. RELI Exchange removes these costly barriers to entry through technology.

With the RELI Exchange platform, our vision is to remove all barriers and activate contracted agents at scale. Being cost efficient for these agencies is key to our success. Unlike the franchise model, RELI Exchange is designed with low barriers to entry and a compelling value proposition. In addition, RELI Exchange significantly enhances competitive advantages through provided agency partners.

People (Target Audience)

We have identified several highly receptive target audiences, including:

| ● | Existing insurance agents & agency leadership/owners | |

| ● | People looking for a career change (GenX, older Millennials) | |

| ● | Experienced salespeople | |

| ● | Younger “quiet quitters” and “Great Resigners” who want more purposeful, lucrative work & flexibility | |

| ● | Recent college graduates with debt & unmarketable degrees with few career options | |

| ● | Captive Agents who feel trapped |

The RELI Exchange Platform

The RELI Exchange platform is a revolutionary way to get insurance quotes without requiring users to undergo a complicated process of manually completing lengthy forms. With basic contact information, our proprietary tool can generate accurate home auto and life insurance quotes from credible providers in under 5 minutes, for free. Then, our platform connects each user with a fully trained and knowledgeable agent who guides them through the rest of the process to deliver the best coverage at the best price.

| 11 |

RELI Exchange is at the forefront of the digital transformation of the insurance industry. Our platform leverages unique technology, a proprietary database, and expert methodologies from experienced insurance agents to deliver a quality experience to agents and people looking to get insured.

In addition to providing customers with a great experience, RELI Exchange automates many processes for agents to free up their time to sell to new customers. The result is higher profitability with less work. Most importantly, mentorship is part of the RELI Exchange model, so that agents always receive the support they need to be successful.

System for Agent and Agency Partner Success

RELI Exchange agents have a distinct advantage over their captive counterparts when it comes to serving clients. They have access to multiple carriers in their markets, to provide more choices and solutions that fit their customers’ needs. Additionally, our automations and back-office support eliminate time spent on service requests and renewals, so agents can focus on sales growth.

We spent years developing our proprietary sales processes, backed up by an engaging mentorship program to maximize agent success. We provide every agent with comprehensive training, product and carrier knowledge, and cutting-edge technology. Plus, our back-office support team is readily available to train and assist agents at every step.

We actively recruit agents who are passionate about owning their own business and have a proven track record in business development. Our revenues are tied directly to their success, creating an environment that delivers consistent results.

Agents benefit from low startup costs and minimal overhead—no employees or physical location is required. In contrast, captive agents are often burdened with immediate hiring requirements, storefront leases, and advertising budgets. Moreover, our software platform delivers economies of scale so that fixed and variable costs are reduced for greater profitability.

Online Insurance and 5MinuteInsure.com

In August 2021, we launched 5MinuteInsure.com, which is a licensed online insurance agency that utilizes state of the art digital technology and seek to use this platform to develop business in the online insurance business which we believe represents an underutilized opportunity.

While 90% of customers are open to purchasing insurance online, 75% of the people who attempt to make online purchases report problems (Source: J.D. Power, Direct-to-Consumer Auto Insurers Take Top Honors in Shopping Study as New Normal Arrives for P&C Industry, J.D. Power Finds; Invoca, 36 Insurance Marketing Statistics You Need to Know in 2023). Moreover, the current insurance purchasing processes is time consuming and lacks transparency. There are over 96 insurance companies paying thousands of affiliates to generate leads, paying as much as $120 per lead (Source: The Insurance Marketer, Best Life Insurance Affiliate Programs: How Much Can You Earn?; Lasso, The 96 Best Insurance Affiliate Programs of 2023). Consequently, most of the current online sites are simply lead generators, which result in false insurance quotes, constant spam and aggressive sales pitches. We believe consumers are looking for an online platform that will replicate the services they could obtain from a traditional brick and mortar insurance agency, thus driving business toward the online site as we all migrate to online in this post COVID world.

Another key benefit to online insurance is the ability to combine seamlessly with electronic capabilities in processing, such as 5MinuteInsure.com’s proprietary backend processing technology to support our traditional agency business. 5MinuteInsure.com will be used internally by all the Reliance Global Group affiliated agencies to offer more products to our existing client base. By implementing artificial intelligence, robotic process automation and automatic shopping for best rates at renewals, we believe we can dramatically reduce costs, and allow our agents to focus on selling new policies, creating a digitally empowered and scalable insurance agency model.

| 12 |

Specific benefits of the 5MinuteInsure.com platform include:

| ● | First, a simplified application process | |

| ● | Second, 5MinuteInsure.com has real-time connections with over 15 top-rated insurance companies, which allows consumers to transparently compare real live quotes from multiple insurers side-by-side. | |

| ● | Third, 5MinuteInsure.com provides instant accurate coverage recommendations for home, auto and life insurance, providing consumers confidence they are not under or over-insured. | |

| ● | Fourth, 5MinuteInsure.com provides in-house insurance buying and policy binding capabilities, meaning no redirection to other websites and the ability to finalize purchases on 5MinuteInsure.com in as little as five minutes. | |

| ● | Fifth, coming soon is 5MinuteInsure’s free and secure account enables 24/7 access to previous quotes, policies and other documents. | |

| ● | Finally, when it’s time for a policy renewal, 5MinuteInsure.com can populate the best offers in the market before their policy expires. |

Thus, we believe in the specific benefits of the online insurance business, and we believe that 5MinuteInsure.com provides the platform to transform this segment of the industry.

Business Operations (OneFirm)

Reliance Global Group has adopted a ‘One-Firm’ approach, whereby the Reliance owned and operated agencies come together to operate as one cohesive unit which allows for efficient and effective cross-selling, cross-collaboration, and the effective deployment of the Company’s human capital. This strategy also aims to enhance the Company’s overall market presence across the U.S., with all business lines operating under the RELI Exchange brand. It’s expected to benefit agents and clients by improving relationships with carriers, leading to better commission and bonus contracts due to higher business volumes. The approach also strengthens the capability of RELI Exchange agency partners in securing diverse insurance policies and fosters increased cross-selling opportunities. This unified strategy positions the company for rapid scaling and integration of accretive acquisitions, expanding its industry reach.

Insurance M&A Overview

As noted above, M&A deal volume in the insurance agency market remains robust with $78 billion in deals during 2023, despite drops as compared prior recent years and 2024 is expected to bring more acquisition opportunities.

| 13 |

The COVID-19 crisis may have an impact on the insurance industry for quite some time. Some factors to consider:

| ● | Strain on investment portfolios – Insurance companies rely on their investment portfolios to generate returns. Markets have been in turmoil and, as a result, insurers’ investment portfolios may be significantly impacted. | |

| ● | Delayed payments – Regulators are urging insurance companies to accept late premium payments with no penalty, putting a strain on cash flow. Despite liquidity being impacted, insurance companies are still being expected to pay out claims. | |

| ● | Decreased premium volume – Full or partial closing of businesses coupled with social distancing has led to decreased demand for insurance. Lower payroll levels lead to lower payroll-based premiums, such as those in workers’ compensation, and an uptick in layoffs results in fewer people buying houses, cars, and other insurable purchases. A decrease in premium volume means a decrease in income for insurers. | |

| ● | Coverage disputes – Pandemics are generally excluded from insurance policy coverage and therefore policy premium has not included the necessary charges to provide such coverage. A number of states are attempting to legislate to force insurance companies to provide insurance coverage for business interruption and other losses for claims resulting from the COVID-19 pandemic. There is uncertainty regarding which party will ultimately incur the additional cost for these adjustments. |

We cannot presently estimate the full financial impact of the unprecedented COVID-19 pandemic on our business or predict the related federal, state and local civil authority actions, which are highly dependent on the severity and duration of the pandemic; however, we see opportunities which may arise as to changes in the markets. Due to the uncertainties associated with the COVID-19 pandemic and the indeterminate length of time it will affect, we have taken proactive measures to secure our liquidity position to be able to meet our obligations for the foreseeable future.

Reliance Insurance Agency Brand Acquisitions:

| ● | RELI Exchange | |

| ● | Altruis Benefits | |

| ● | J.P. Kush & Associates | |

| ● | US Benefits Alliance | |

| ● | Employee Benefits Solutions | |

| ● | Fortman Insurance Solutions | |

| ● | Southwestern Montana Insurance Center | |

| ● | UIS Agency | |

| ● | Commercial Coverage Solutions |

Acquisition History

| ● | In October 2018, announced first two acquisitions: Employee Benefits Solutions and U.S. Benefits Alliance; Michigan-based agencies specializing in the sale of health insurance products in the wholesale and retail industry | |

| ● | In December 2018, acquired Commercial Coverage Solutions, LLC, a commercial property and casualty insurance company specializing in commercial trucking and transportation insurance |

| 14 |

| ● | In September 2019, two agencies transferred ownership from Reliance Global Holdings, LLC, a private company affiliated with Reliance Global Group: |

| Ø | Southwestern Montana Insurance, a group health insurance agency providing personal and commercial lines of insurance |

| Ø | Fortman Insurance Agency, LLC, an agency providing multiple lines of insurance in the property/casualty and life/health insurance sectors |

| ● | In September 2019, acquired Altruis Benefit Consulting; serves customers throughout the entire State of Michigan, specializing in providing individual and group health insurance |

| ● | In September 2020, acquired the assets of UIS Agency, LLC (UIS), a premier regional insurance agency serving the commercial transportation industry |

| ● | In May 2021, acquired J.P. Kush and Associates, Inc., a premier healthcare insurance agency with operations in 10 states, headquartered in Troy, Michigan |

| ● | In April 2022, acquired Barra & Associates, (changed to RELI Exchange following acquisition) a recognized provider of both personal and commercial insurance products, including P&C insurance, life insurance, health insurance and other insurance products. |

Insurance Agency Acquisition Strategy

| ● | Numerous acquisition targets within a highly fragmented market |

| Ø | Reliance’s access to capital supports the growth of the acquired companies |

| ● | Ownership and management remain engaged |

| ● | Focus on acquiring growing and profitable businesses, for below-market prices |

| Ø | Ability to leverage cash flow of acquiree through low-cost debt financing and provide earnouts as part of consideration |

| ● | Economies of scale through first class technology infrastructure and national sales/marketing platform |

| Ø | Few insurance agencies have the size and scale to compete at a national level |

| ● | Management expertise in acquisitions, operations, and financial management |

Digitizing Bricks & Mortar Agencies

| ● | Capitalizing on consumer shift to ‘online’ |

| Ø | More and more customers search for insurance online, but consumers prefer the personal touch of an agent |

| ● | Proprietary backend processing technology to support Reliance’s agency business |

| ● | Strategy to acquire traditional ‘offline’ home, auto and life agencies, and utilize technology to more cost effectively service the acquired policies |

| ● | By implementing artificial intelligence, robotic process automation (RPA) and automatic shopping for best rates at renewals, Reliance can: |

| Ø | Dramatically reduce cost |

| Ø | Allow agents to focus on selling new policies, |

| Ø | Create a digitally empowered and scalable insurance agency model |

| ● | Ability to rapidly expand Reliance’s agency network nationwide and drive margin expansion through the combination of digital backend and continued M&A of cash flow positive and accretive acquisitions |

Employees

As of December 31, 2023, we employed 67 employees across all Company subsidiaries.

We believe that a diverse workforce is important to our success. We will continue to focus on the hiring, retention, and advancement of underrepresented populations, and to cultivate an inclusive and diverse corporate culture. In the future, we intend to continue to evaluate our use of human capital measures or objectives in managing our business such as the factors we employ or seek to employ in the development, attraction and retention of personnel and maintenance of diversity in our workforce.

| 15 |

The success of our business is fundamentally connected to the well-being of our people. Accordingly, we are committed to the health, safety and wellness of our employees. We provide our employees and their families with access to a variety of innovative, flexible and convenient health and wellness programs, including benefits that provide protection and security so they can have peace of mind concerning events that may require time away from work or that impact their financial well-being; that support their physical and mental health by providing tools and resources to help them improve or maintain their health status and encourage engagement in healthy behaviors; and that offer choice where possible so they can customize their benefits to meet their needs and the needs of their families.

We also provide robust compensation and benefits programs to help meet the needs of our employees. We believe that we maintain a satisfactory working relationship with our employees and have not experienced any labor disputes.

Competition

The insurance brokerage business is highly competitive, and numerous firms actively compete with us for customers and insurance markets. Competition is largely based upon innovation, knowledge, terms and conditions of coverage, quality of service and price. We believe that we’re well positioned to be highly competitive and continuously gain market share. Additionally, our focus on InsurTech is a game-changer in the industry and helps us stand-out vs. the competition.

The Merger and Acquisition of Insurance Agencies is a highly competitive industry, as well. Competition is due to many well-established companies having extensive experience in identifying and effecting business combinations who possess great technical, human, and financial resources. Several firms and banks with substantially greater resources and market presence compete with us. While we believe that there are numerous potential target businesses that we could acquire, our ability to compete in acquiring certain sizable target businesses might be limited.

Government Regulation

The business practices and compensation arrangements of the insurance intermediary industry, including our practices and arrangements, are regulated by various governmental authorities. Certain of our offices are parties to profit-sharing contingent commission agreements with certain insurance companies, including agreements providing for potential payment of revenue-sharing commissions by insurance companies based primarily on the overall profitability of the aggregate business written with those insurance companies and/or additional factors such as retention ratios and the overall volume of business that an office or offices place with those insurance companies. The legislatures of various states may adopt new laws addressing contingent commission arrangements, including laws prohibiting such arrangements, and addressing disclosure of such arrangements to insureds.

We and our employees must be licensed to act as brokers, intermediaries, or third-party administrators by state regulatory authorities in the locations in which we conduct business. Regulations and licensing laws vary by individual state and are often complex. The applicable licensing laws and regulations in all states are subject to amendment or reinterpretation by regulatory authorities, and such authorities are vested in most cases with relatively broad discretion as to the granting, revocation, suspension, and renewal of licenses. We believe that we are in compliance with the applicable licensing laws and regulations of all states in which we currently operate. However, the possibility still exists that we or our employees could be excluded or temporarily suspended from carrying on some or all of our activities in, or could otherwise be subjected to penalties by, a particular jurisdiction.

Nearly all states have insurance laws requiring personal property and casualty insurers to file rating plans, policy or coverage forms, and other information with the state’s regulatory authority. In many cases, such rating plans, policy, or coverage forms, must be approved prior to use and the regulator has the authority to disapprove a rate filing. While we are not an insurer, and thus not required to comply with state laws and regulations regarding insurance rates, our commissions are derived from a percentage of the premium rates set by insurers in conjunction with state law.

| 16 |

Item 1a. RISK FACTORS

The following important factors, among others, could cause our actual operating results to differ materially from those indicated or suggested by forward-looking statements made in this Annual Report on Form 10-K or presented elsewhere by management from time to time. Investors should carefully consider the risks described below before making an investment decision. The risks described below are not the only ones we face. Additional risks not presently known to us or that we currently believe are not material may also significantly impair our business operations. Our business could be harmed by any of these risks. The trading price of our common stock could decline due to any of these risks, and investors may lose all or part of their investment.

Risks Related to Our Business

We may experience significant fluctuations in our quarterly and annual results.

Fluctuations in our quarterly and annual financial results have resulted and will continue to result from numerous factors, including:

| ● | The Company having a limited operating history | |

| ● | The Company has limited resources and there is significant competition for business combination opportunities. Therefore, the Company may not be able to acquire other assets or businesses | |

| ● | The Company may be unable to obtain additional financing, if required, to complete an acquisition, or to complement the operations and growth of existing and target business, which could compel the Company to restructure a potential business transaction or abandon a particular business combination | |

| ● | We hold our cash and cash equivalents that we use to meet our working capital and operating expense needs in deposit accounts that could be adversely affected if the financial institution holding such funds fail. | |

| ● | Our inability to retain or hire qualified employees, as well as the loss of any of our executive officers, could negatively impact our ability to retain existing business and generate new business | |

| ● | Our growth strategy depends, in part, on the acquisition of other insurance intermediaries, which may not be available on acceptable terms in the future or which, if consummated, may not be advantageous to us | |

| ● | A cybersecurity attack, or any other interruption in information technology and/or data security and/or outsourcing relationships, could adversely affect our business, financial condition and reputation | |

| ● | Rapid technological change may require additional resources and time to adequately respond to dynamics, which may adversely affect our business and operating results | |

| ● | Changes in data privacy and protection laws and regulations, or any failure to comply with such laws and regulations, could adversely affect our business and financial results | |

| ● | Because our insurance business is highly concentrated in Michigan, New York, Montana, New Jersey, Ohio, and Illinois adverse economic conditions, natural disasters, or regulatory changes in these regions could adversely affect our financial condition | |

| ● | If we fail to comply with the covenants contained in certain of our agreements, our liquidity, results of operations and financial condition may be adversely affected | |

| ● | Certain of our agreements contain various covenants that limit the discretion of our management in operating our business and could prevent us from engaging in certain potentially beneficial activities | |

| ● | There are inherent uncertainties involved in estimates, judgments and assumptions used in the preparation of financial statements in accordance with United States Generally Accepted Accounting Principles (U.S. GAAP). Any changes in estimates, judgments and assumptions could have a material adverse effect on our financial position and results of operations and therefore our business | |

| ● | Improper disclosure of confidential information could negatively impact our business | |

| ● | Our business could be adversely impacted by inflation. |

These factors, some of which are not within our control, may cause the price of our common stock to fluctuate substantially. If our operating results fail to meet or exceed the expectations of securities analysts or investors, our stock price could drop suddenly and significantly. Due to the Company’s limited operating history, we believe period to period comparisons of our financial results are not always meaningful and should not be relied upon as an indication of future performance.

| 17 |

The Company has limited resources and there is significant competition for business combination opportunities. Therefore, the Company may not be able to acquire other assets or businesses.

The Company expects to encounter intense competition from other entities having a business objective similar to ours, which are also competing for acquisitions. Many of these entities are well established and have extensive experience in identifying and effecting business combinations directly or through affiliates. Many of these competitors possess greater technical, human, financial and other resources. While the Company believes that there are numerous potential target businesses that it could acquire, the Company’s ability to compete in acquiring certain sizable target businesses might be limited if the Company’s limited financial resources are less than that of its competitors. This inherent competitive limitation gives others an advantage in pursuing the acquisition of certain target businesses.

The Company may be unable to obtain additional financing, if required, to complete an acquisition, or to Company the operations and growth of existing and target business, which could compel the Company to restructure a potential business transaction or abandon a particular business combination.

To date, much of our capital for acquiring and operating insurance agencies comes from loans from unaffiliated lenders, from direct market capital raises or funds provided by Reliance Global Holdings our affiliate. We may be required to seek additional financing. We cannot assure you that such financing would be available on acceptable terms, if at all. If additional financing proves to be unavailable, we would be compelled to restructure or existing business, or abandon a proposed acquisition or acquisitions. In addition, if we consummate additional acquisitions, we may require additional financing to complement the operations or growth of that business. The failure to secure additional financing could have a material adverse effect on the continued development or growth of our business.

We hold our cash and cash equivalents that we use to meet our working capital and operating expense needs in deposit accounts that could be adversely affected if the financial institution holding such funds fail.

We hold our cash and cash equivalents that we use to meet our working capital and operating expense needs in deposit accounts at one financial institution. The balance held in these accounts exceeds the Federal Deposit Insurance Corporation, or FDIC, standard deposit insurance limit of $250,000. If the financial institution in which we hold such funds fails or is subject to significant adverse conditions in the financial or credit markets, we could be subject to a risk of loss of all or a portion of such uninsured funds or be subject to a delay in accessing all or a portion of such uninsured funds. Any such loss or lack of access to these funds could adversely impact our short-term liquidity and ability to meet our operating expense obligations, including payroll obligations.

For example, on March 10, 2023, Silicon Valley Bank, or SVB, and Signature Bank, were closed by state regulators and the FDIC was appointed receiver for each bank. The FDIC created successor bridge banks and all deposits of SVB and Signature Bank were transferred to the bridge banks under a systemic risk exception approved by the United States Department of the Treasury, the Federal Reserve and the FDIC. If the financial institution in which we hold funds for working capital and operating expenses were to fail, we cannot provide any assurances that such governmental agencies would take action to protect our uninsured deposits or investments in a similar manner.

Our inability to retain or hire qualified employees, as well as the loss of any of our executive officers, could negatively impact our ability to retain existing business and generate new business.

Our success depends on our ability to attract and retain skilled and experienced personnel. There is significant competition from within the insurance industry and from businesses outside the industries for exceptional employees, especially in key positions. If we are not able to successfully attract, retain and motivate our employees, our business, financial results and reputation could be materially and adversely affected.

| 18 |

Losing employees who manage or support substantial customer relationships or possess substantial experience or expertise could adversely affect our ability to secure and complete customer engagements, which would adversely affect our results of operations. Also, if any of our key personnel were to join an existing competitor or form a competing company, some of our customers could choose to use the services of that competitor instead of our services. While our key personnel are generally prohibited by contract from soliciting our employees and customers for a two-year period following separation from employment with us, they are not prohibited from competing with us.

In addition, we could be adversely affected if we fail to adequately plan for the succession of our senior leaders and key executives. We cannot guarantee that the services of these executives will continue to be available to us. The loss of our senior leaders or other key personnel, or our inability to continue to identify, recruit and retain such personnel, or to do so at reasonable compensation levels, could materially and adversely affect our business, results of operations, cash flows and financial condition.

Our growth strategy depends, in part, on the acquisition of other insurance intermediaries, which may not be available on acceptable terms in the future or which, if consummated, may not be advantageous to us.

Our growth strategy partially includes the acquisition of other insurance intermediaries. Our ability to successfully identify suitable acquisition candidates, complete acquisitions, integrate acquired businesses into our operations, and expand into new markets requires us to implement and continuously improve our operations and our financial and management information systems. Integrated, acquired businesses may not achieve levels of revenues or profitability comparable to our existing operations, or otherwise perform as expected. In addition, we compete for acquisition and expansion opportunities with firms and banks that may have substantially greater resources than we do. Acquisitions also involve a number of special risks, such as diversion of management’s attention; difficulties in the integration of acquired operations and retention of personnel; increase in expenses and working capital requirements, which could reduce our return on invested capital; entry into unfamiliar markets or lines of business; unanticipated problems or legal liabilities; estimation of the acquisition earn-out payables; and tax and accounting issues, some or all of which could have a material adverse effect on our results of operations, financial condition and cash flows. Post-acquisition deterioration of operating performance could also result in lower or negative earnings contribution and/or goodwill impairment charges.

A cybersecurity attack, or any other interruption in information technology and/or data security and/or outsourcing relationships, could adversely affect our business, financial condition, and reputation.

We rely on information technology and third-party vendors to provide effective and efficient service to our customers, process claims, and timely and accurately report information to carriers and which often involves secure processing of confidential sensitive, proprietary, and other types of information. Cybersecurity breaches of any of the systems we rely on may result from circumvention of security systems, denial-of-service attacks or other cyber-attacks, hacking, “phishing” attacks, computer viruses, ransomware, malware, employee or insider error, malfeasance, social engineering, physical breaches, or other actions, any of which could expose us to data loss, monetary and reputational damages and significant increases in compliance costs. An interruption of our access to, or an inability to access, our information technology, telecommunications or other systems could significantly impair our ability to perform such functions on a timely basis. If sustained or repeated, such a business interruption, system failure or service denial could result in a deterioration of our ability to write and process new and renewal business, provide customer service, pay claims in a timely manner or perform other necessary business functions. We have from time-to-time experienced cybersecurity breaches, such as computer viruses, unauthorized parties gaining access to our information technology systems and similar incidents, which to date have not had a material impact on our business.

Additionally, we are an acquisitive organization and the process of integrating the information systems of the businesses we acquire is complex and exposes us to additional risk as we might not adequately identify weaknesses in the targets’ information systems, which could expose us to unexpected liabilities or make our own systems more vulnerable to attack. In the future, any material breaches of cybersecurity, or media reports of the same, even if untrue, could cause us to experience reputational harm, loss of clients and revenue, loss of proprietary data, regulatory actions and scrutiny, sanctions or other statutory penalties, litigation, liability for failure to safeguard clients’ information or financial losses. Such losses may not be insured against or not fully covered through insurance we maintain.

| 19 |

Rapid technological change may require additional resources and time to adequately respond to dynamics, which may adversely affect our business and operating results.

Frequent technological changes, new products and services and evolving industry standards are influencing the insurance businesses. The Internet, for example, is increasingly used to securely transmit benefits, property and personal information, and related information to customers and to facilitate business-to-business information exchange and transactions.

We are continuously taking steps to upgrade and expand our information systems capabilities. Maintaining, protecting, and enhancing these capabilities to keep pace with evolving industry and regulatory standards, and changing customer preferences, requires an ongoing commitment of significant resources. If the information we rely upon to run our businesses was found to be inaccurate or unreliable or if we fail to effectively maintain our information systems and data integrity, we could experience operational disruptions, regulatory or other legal problems, increases in operating expenses, loss of existing customers, difficulty in attracting new customers, or suffer other adverse consequences.

Changes in data privacy and protection laws and regulations, or any failure to comply with such laws and regulations, could adversely affect our business and financial results.