As filed with the U.S. Securities and Exchange Commission on November 17, 2022

Registration No. 333-257530

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 12 TO

FORM F-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Huake Holding Biology Co., LTD

(Exact name of registrant as specified in its charter)

| Cayman Islands | 2075 | Not Applicable | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

Shuhe Road, Tangchi Town

Shucheng County, Lu’an City, Anhui Province

People’s Republic of China 231343

+86 564 8242 222

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Puglisi& Associates

850 Library Avenue

Suite 204

Newark, Delaware 19711

(Name, address, including zip code, and telephone number, including area code, of agent for service)

With a Copy to:

Joan Wu, Esq. Ying Li, Esq. New York, NY 10005 (212) 530-2208 |

William S. Rosenstadt, Esq. Jason “Mengyi” Ye, Esq. Ortoli Rosenstadt LLP |

Approximate date of commencement of proposed sale to the public: Promptly after the effective date of this registration statement.

| If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box. | ☐ | |

| If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. | ☐ | |

| If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering | ☐ | |

| If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering | ☐ | |

| Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 | ||

| Emerging growth company | ☒ | |

| If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act | ☐ |

The Registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the registration statement shall become effective on such date as the U.S. Securities and Exchange Commission, acting pursuant to such Section 8(a), may determine.

| The information in this prospectus is not complete and may be changed. We may not sell the securities until the registration statement filed with the U.S. Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and it is not soliciting any offer to buy these securities in any jurisdiction where such offer or sale is not permitted. |

SUBJECT TO COMPLETION

PRELIMINARY PROSPECTUS DATED NOVEMBER 17, 2022

1,250,000 Class A Ordinary Shares

Huake Holding Biology Co., LTD

This is an initial public offering of Huake Holding Biology Co., LTD’s Class A ordinary shares. We are offering on a firm commitment basis our Class A ordinary shares, par value $0.002 per share (the “Class A Ordinary Shares”). Prior to this offering, there has been no public market for our Class A Ordinary Shares. We expect that the initial public offering price will be in the range of $4 to $6 per Class A Ordinary Share. We have reserved the symbol “HUAK” for purposes of listing our Class A Ordinary Shares on the Nasdaq Capital Market (“Nasdaq”) and have applied to list our Class A Ordinary Shares on Nasdaq. At this time, Nasdaq has not yet approved our application to list our Class A Ordinary Shares. The closing of this offering is conditioned upon Nasdaq’s final approval of our listing application. We cannot assure you that our application will be approved, and if it is not approved by Nasdaq, we will not proceed with this offering.

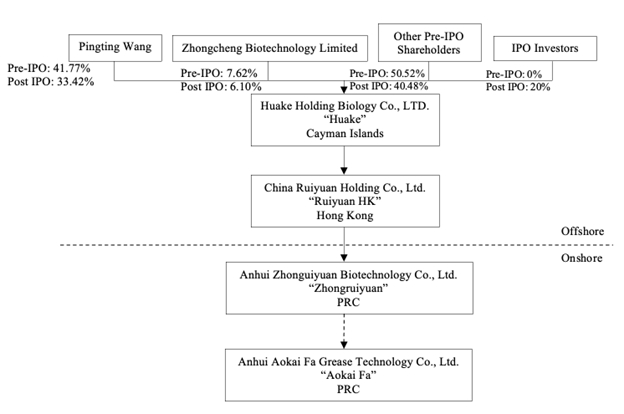

On November 3, 2022, we filed an amended and restated memorandum and articles of association with the Cayman Islands Registrar of Companies to effectuate a share combination at a ratio of one-for-four (the “Share Combination”). After the Share Combination, our authorized share capital is $US 50,000 divided into (i) 2,500,000 preferred shares of par value of US$0.002 each, (ii) 17,500,000 Class A Ordinary Shares, par value of US$0.002 each, and (iii) 5,000,000 Class B ordinary shares, par value of US$0.002 each, (the “Class B Ordinary Shares”). Each Class A Ordinary Share is entitled to one (1) vote and each Class B Ordinary Share is entitled to twenty (20) votes on all matters subject to vote at our general meetings. Future transfers by holders of Class B Ordinary Shares will generally result in those shares converting to Class A Ordinary Shares, subject to limited exceptions, such as certain transfers effected for estate planning purposes. The conversion of Class B Ordinary Shares to Class A Ordinary Shares will have the effect, over time, of increasing the relative voting power of those holders of Class B Ordinary Shares who retain their shares in the long term. See “Description of Share Capital and Articles of Association—Ordinary Shares” starting on page 109 of this prospectus for more information. All of our issued and outstanding Class B Ordinary Shares are beneficially held by Ms. Pingting Wang, our Chief Executive Officer and Chairperson of the Board, and Mr. Tingyin Zhang, our former Chairman of the Board. Ms. Wang holds 2,088,500 Class B Ordinary Shares, representing 80.45% of the voting power of our capital stock and Mr. Zhang holds 381,000 Class B Ordinary Shares through Zhongcheng Biotechnology Limited, representing 14.68% of the voting power of our capital stock. After this offering, Ms. Wang and Mr. Zhang together, or Ms. Wang alone, will control shares representing more than 50% of the total voting power of our shares. As a result, this concentrated control may limit or preclude your ability to influence corporate matters for the foreseeable future, including the election of directors, amendments of our organizational documents, and any merger, consolidation, sale of all or substantially all of our assets, or other major corporate transaction requiring shareholder approval. In addition, this may prevent or discourage unsolicited acquisition proposals or offers for our capital stock that you may feel are in your best interest as one of our shareholders.

We are incorporated in the Cayman Islands. As a holding company with no material operations of our own, we conduct our operations in China through the variable interest entity, Anhui Aokai Fa Grease Technology Co., Ltd. (“Aokai Fa” or the “VIE”). This is an offering of the Class A Ordinary Shares of Huake Holding Biology Co., LTD, our Cayman Islands holding company. You are not directly investing in and may never hold equity interests of Aokai Fa, the consolidated VIE of Huake in China.

As a holding company, we may rely on dividends and other distributions on equity paid by our subsidiary in Hong Kong, Anhui Zhongruiyuan Biotechnology Co., Ltd. (“Zhongruiyuan” or the “WFOE”) and the VIE in China for our cash and financing requirements. If the WFOE or the VIE incur debt on their own behalf in the future, the instruments governing such debt may restrict their ability to pay dividends to us. In addition, the VIE is required to set aside at least 10% of its after-tax profits each year, if any, to fund a statutory reserve until such reserve reaches 50% of its registered capital. The VIE is also required to further set aside a portion of its after-tax profits to fund the employee welfare fund, although the amount to be set aside, if any, is determined at the discretion of its board of directors. Although the statutory reserves can be used, among other ways, to increase the registered capital and eliminate future losses in excess of retained earnings of the respective companies, the reserve funds are not distributable as cash dividends except in the event of liquidation. As of the date of this prospectus, the VIE has not remitted any services fees to WFOE. However, the VIE is obligated to pay a service fee equivalent to 100% of VIE’s net income after deduction of certain tax and operational expenses. As of the date of this prospectus, none of our subsidiaries or the VIE have made any dividends or distributions to us and we have not made any dividends or distributions to our shareholders. We currently intend to retain all available funds and future earnings, if any, for the operation and expansion of our business and do not anticipate declaring or paying any dividends in the foreseeable future. In the future, cash proceeds raised from overseas financing activities, including this offering, may be transferred by us to the VIE via capital contribution or shareholder loans, as the case may be. For more information, please see “Prospectus Summary - Dividend Distributions or Assets Transfer among the Holding Company, its Subsidiaries and the Consolidated VIE” starting on page 18 of this prospectus for more information.

We engage in the production and sales of camellia seed oil (“Camellia Oil”) products through the VIE in China. The research, farming, production and sales of Camellia Oil are categorized as “restricted” or “prohibited” from foreign investment under the “negative list” issued in 2020 by the National Development and Reform Commission and the Ministry of Commerce in China. The VIE, WFOE, and the VIE’s shareholders entered into the VIE Agreements; as a result of which, we are regarded as the primary beneficiary of Aokai Fa for accounting purposes, and, therefore, we are able to consolidate the financial results of Aokai Fa in our consolidated financial statements in accordance with U.S. GAAP. However, neither we nor our subsidiaries own any share in Aokai Fa, and the investors will not and may never directly hold equity interests in the VIE either. The VIE structure cannot completely replicate a foreign investment in China-based companies. Instead, the VIE structure provides contractual exposure to foreign investment in us. Because of our corporate structure, we are subject to risks due to uncertainty of the interpretation and the application of the PRC laws and regulations, including but not limited to limitation on foreign ownership of internet technology companies, and regulatory review of oversea listing of PRC companies through a special purpose vehicle, and the validity and enforcement of the VIE Agreements because they have not been tested in a court of law. We are also subject to the risks of uncertainty about any future actions of the PRC government in this regard. The VIE Agreements may not be effective in providing control over Aokai Fa. We may also subject to sanctions imposed by PRC regulatory agencies including Chinese Securities Regulatory Commission if we fail to comply with their rules and regulations.

Additionally, we are subject to certain legal and operational risks associated with the VIE’s operations in China. PRC laws and regulations governing our current business operations are sometimes vague and uncertain, and we are subject to the risks of uncertainty about any future actions of the PRC government in this regard that could disallow the VIE structure, which may result in a material change in the VIE’s operations, significant depreciation of the value of our Class A Ordinary Shares, or a complete hindrance of our ability to offer or continue to offer our securities to investors and cause the value of such securities to significantly decline or be worthless. Recently, the PRC government initiated a series of regulatory actions and statements to regulate business operations in China with little advance notice, including cracking down on illegal activities in the securities market, enhancing supervision over China-based companies listed overseas using variable interest entity structure, adopting new measures to extend the scope of cybersecurity reviews, and expanding the efforts in anti-monopoly enforcement. We, through the VIE in China, engages in the production and sale of Camellia Oil, which do not involve operation of critical information infrastructure.

On December 24, 2021, the CSRC, issued Provisions of the State Council on the Administration of Overseas Securities Offering and Listing by Domestic Companies (Draft for Comments) (the “Administration Provisions”), and the Provisions of the State Council on the Administration of Overseas Securities Offering and Listing by Domestic Companies (Draft for Comments) (the “Measures”), both of which have a comment period that expired on January 23, 2022. The Administration Provisions and Measures for overseas listings lay out specific requirements for filing documents and include unified regulation management, strengthening regulatory coordination, and cross-border regulatory cooperation. Domestic companies seeking to list abroad must carry out relevant security screening procedures if their businesses involve such supervision. Companies endangering national security are among those off-limits for overseas listings. According to Relevant Officials of the CSRC Answered Reporter Questions (“CSRC Answers”), after the Administration Provisions and Measures are implemented upon completion of public consultation and due legislative procedures, the CSRC will formulate and issue guidance for filing procedures to further specify the details of filing administration and ensure that market entities could refer to clear guidelines for filing, which means it still takes time to make the Administration Provisions and Measures into effect. As the Administration Provisions and Measures have not yet come into effect, we are currently unaffected. However, according to CSRC Answers, new initial public offerings and refinancing by existent overseas listed Chinese companies will be required to go through the filing process; other existent overseas listed companies will be allowed sufficient transition period to complete their filing procedure, which means we will certainly go through the filing process for this Offering.

Pursuant to the PRC Cybersecurity Law, which was promulgated by the Standing Committee of the National People’s Congress on November 7, 2016 and took effect on June 1, 2017, personal information and important data collected and generated by a critical information infrastructure operator in the course of its operations in China must be stored in China, and if a critical information infrastructure operator purchases internet products and services that affects or may affect national security, it should be subject to cybersecurity review by the Cyberspace Administration of China (“CAC”). Due to the lack of further interpretations, the exact scope of “critical information infrastructure operator” remains unclear. On December 28, 2021, the CAC and other relevant PRC governmental authorities jointly promulgated the Cybersecurity Review Measures (the “new Cybersecurity Review Measures”) to replace the original Cybersecurity Review Measures. The new Cybersecurity Review Measures took effect on February 15, 2022. Pursuant to the new Cybersecurity Review Measures, if critical information infrastructure operators purchase network products and services, or network platform operators conduct data processing activities that affect or may affect national security, they will be subject to cybersecurity review. On November 14, 2021, CAC published the Administration Measures for Cyber Data Security (Draft for Public Comments), or the “Cyber Data Security Measures (Draft)”, which require cyberspace operators with personal information of more than 1 million users who want to list abroad to file a cybersecurity review with the Office of Cybersecurity Review. The cybersecurity review will evaluate, among others, the risk of critical information infrastructure, core data, important data, or a large amount of personal information being influenced, controlled or maliciously used by foreign governments and risk of network data security after going public overseas. As advised by our PRC counsel, Beijing Docvit Law Firm, we do not expect to be subject to cybersecurity review, because: (i) our products are offered not directly to individual consumers but through our distributors; (ii) we do not possess a large amount of personal information in our business operations; and (iii) data processed in our business does not have a bearing on national security and thus may not be classified as core or important data by the authorities. Since these statements and regulatory actions are new, it is highly uncertain how soon legislative or administrative regulation making bodies will respond and what existing or new laws or regulations or detailed implementations and interpretations will be modified or promulgated, if any, and the potential impact such modified or new laws and regulations will have on our daily business operation, the ability to accept foreign investments and list on an U.S. exchange. See “Risk Factors – Risks Related to Doing Business in the PRC” starting on page 29 of this prospectus and “Risk Factors – Risks Related to Our Corporate Structure” starting on page 47 of this prospectus for more information.

Furthermore, as an auditor of companies that are registered with the SEC and publicly traded in the United States and a firm registered with the PCAOB, our auditor is located in Hackensack, New Jersey and is required under the laws of the United States to undergo regular inspections by the U.S. Public Company Accounting Oversight Board (“PCAOB”) to assess their compliance with the laws of the United States and professional standards. Although we operate through Aokai Fa in mainland China, a jurisdiction where the PCAOB is currently unable to conduct inspections without the approval of the Chinese government authorities, our auditor is currently inspected fully by the PCAOB. Inspections of other auditors conducted by the PCAOB outside mainland China have at times identified deficiencies in those auditors’ audit procedures and quality control procedures, which may be addressed as part of the inspection process to improve future audit quality.

Even though our auditor is based in Hackensack, New Jersey and under full inspection by the PCAOB and it is not currently subject to the determinations announced by the PCAOB on December 16, 2021, if any PRC law relating to the access of the PCAOB to auditor files were to apply to a company such as Aokai Fa or its auditor, the PCAOB may be unable to fully inspect our auditor, which may result in our securities being delisted or prohibited from being traded “over-the-counter” pursuant to the Holding Foreign Companies Accountable Act (the “HFCA Act”) and materially and adversely affect the value and/or liquidity of your investment. The Accelerating Holding Foreign Companies Accountable Act (the “AHFCA Act”), passed by the U.S. Senate and if enacted, would require foreign companies to comply with the PCAOB audits within two consecutive years instead of three consecutive years, which would reduce the time before our securities may be prohibited from trading or be delisted. Furthermore, our auditor is not among the auditor firms listed on an HFCAA Determination List, which includes all of the auditor firms that the PCAOB is not able to inspect. There are risks and uncertainties which we cannot foresee for the time being, and rules and regulations in the PRC can change quickly with little or no advance notice. The PRC government may intervene or influence Aokai Fa’s future operations in the PRC at any time, or may exert more control over offerings conducted overseas and/or foreign investment in companies like us. In the event it is later determined that the PCAOB is unable to inspect or investigate completely our auditor, then such lack of inspection could cause trading in our securities to be prohibited under the HFCA Act, and ultimately result in a determination by a securities exchange to delist our securities.

On August 26, 2022, the PCAOB signed SOP Agreements with the CSRC and China’s Ministry of Finance. The SOP Agreements established a specific, accountable framework to make possible complete inspections and investigations by the PCAOB of audit firms based in mainland China and Hong Kong, as required under U.S. law. However, if the PCAOB continues to be prohibited from conducting complete inspections and investigations of PCAOB-registered public accounting firms in mainland China and Hong Kong, the PCAOB is likely to determine by the end of 2022 that positions taken by authorities in the PRC obstructed the its ability to inspect and investigate registered public accounting firms in mainland China and Hong Kong completely, then the companies audited by those registered public accounting firms would be subject to a trading prohibition on U.S. markets pursuant to the HFCA Act. A termination in the trading of our securities or any restriction on the trading in our securities would be expected to have a negative impact on us as well as on the value of our securities. See “Risk Factors—Risks Related to Doing Business in the PRC” for a detailed description of risks related to the PRC starting on page 29 of this prospectus for more information.

Ms. Pingting Wang, our Chairperson of the Board of Directors and Chief Executive Officer, is currently the beneficial owner of 2,088,500 Class B Ordinary Shares, representing 80.45% of the total voting power, and has the controlling interest of our Company. Upon the closing of this offering, Ms. Wang will own approximately 78.56% of our total voting power and we will continue to be a “controlled company” under the corporate governance standards for NASDAQ listed companies and for so long as we remain a controlled company under this definition, we are eligible to utilize certain exemptions from the corporate governance requirements of the NASDAQ Stock Market.

We are an “emerging growth company” as defined under the federal securities laws and will be subject to reduced public company reporting requirements. Please read the disclosures beginning on page 21 of this prospectus for more information.

Investing in our Class A Ordinary Shares involves a high degree of risk, including the risk of losing your entire investment. See “Risk Factors” beginning on page 29 to read about factors you should consider before buying our Class A Ordinary Shares.

| Per Share | Total Without Exercise of Over-Allotment Option | |||||||

| Public offering price | $ | 5.000 | $ | 6,250,000 | ||||

| Underwriting discounts | $ | 0.375 | $ | 468,750 | ||||

| Net proceeds to us | $ | 4.625 | $ | 5,781,250 | ||||

| (1) | We have agreed to pay EF Hutton, division of Benchmark Investments, LLC (the “Representative”), the representative on behalf of the underwriters, a fee equal to seven point five (7.5%) of the gross proceeds of the offering. We have agreed to grant to the Representative a 45-day option to purchase up to 15% of the aggregate number of Class A Ordinary Shares sold in the offering. See “Underwriting” starting on page 134 of this prospectus for more information regarding our arrangements with the underwriters. |

| (2) | We expect our total cash expenses for this offering (including cash expenses payable to our underwriters for their out-of-pocket expenses) to be approximately $1.41 million, exclusive of the above discounts. In addition, we will pay additional items of value in connection of this offering that are viewed by the Financial Industry Regulatory, or FINRA, as underwriting compensation. These payments will further reduce proceeds available to us before expenses. See “Underwriting” starting on page 134 of this prospectus for more information. |

| (3) | Assumes that the Representative does not exercise any portion of its over-allotment option. |

This offering is being conducted on a firm commitment basis. The underwriters are obligated to take and pay for all of the shares if any such shares are taken. We have granted the underwriters an option for a period of 45 days after the closing of this offering to purchase up to 15% of the total number of our Class A Ordinary Shares to be offered by us pursuant to this offering (excluding shares subject to this option), solely for the purpose of covering overallotments, at the initial public offering price less the underwriting discount. If the over-allotment option is exercised in full, the total underwriting discounts payable will be $539,063, and the total proceeds to us, after underwriting discounts and expenses but before offering expenses, will be $6,648,437. If we complete this offering, net proceeds will be delivered to our company on the closing date. Except as otherwise noted, all information in this prospectus reflects and assumes no exercise of the over-allotment option.

One of the conditions to our obligation to sell any securities through the underwriters is that, upon the closing of the offering, the Class A Ordinary Shares would qualify for listing on Nasdaq.

As used in this prospectus, “we”, “us”, or the “Company” refers to Huake Holding Biology Co., LTD, the Cayman Islands holding company, its direct and indirect subsidiaries and the VIE in China, as the case may be, and, in the context of describing our operations and consolidated financial information, the VIE in China.

Neither the U.S. Securities and Exchange Commission nor any state securities commission nor any other regulatory body has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

Sole Book-Running Manager

EF HUTTON

division of Benchmark Investments, LLC

Prospectus dated , 2022

TABLE OF CONTENTS

You should rely only on the information contained in this prospectus or in any related free-writing prospectus. We have not authorized anyone to provide you with information different from that contained in this prospectus. We are offering to sell, and seeking offers to buy, the ordinary shares only in jurisdictions where offers and sales are permitted. The information contained in this prospectus is current only as of the date of this prospectus, regardless of the time of delivery of this prospectus or of any sale of the ordinary shares.

Until , 2022 (the 25th day after the date of this prospectus), all dealers that buy, sell or trade ordinary shares, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to the obligation of dealers to deliver a prospectus when acting as an underwriter and with respect to their unsold allotments or subscriptions.

i

About this Prospectus

We and the underwriters have not authorized anyone to provide any information or to make any representations other than those contained in this prospectus or in any free writing prospectuses prepared by us or on our behalf or to which we have referred you. We take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. This prospectus is an offer to sell only the Class A Ordinary Shares offered hereby, but only under circumstances and in jurisdictions where it is lawful to do so. We are not making an offer to sell these securities in any jurisdiction where the offer or sale is not permitted or where the person making the offer or sale is not qualified to do so or to any person to whom it is not permitted to make such offer or sale. For the avoidance of doubt, no offer or invitation to subscribe for Class A Ordinary Shares is made to the public in the Cayman Islands. The information contained in this prospectus is current only as of the date on the front cover of the prospectus. Our business, financial condition, results of operations and prospects may have changed since that date.

Other Pertinent Information

Unless otherwise indicated or the context requires otherwise, references in this prospectus to:

| ● | “Aokai Fa” and “VIE” are to Anhui Aokai Fa Grease Technology Co., Ltd., a limited liability company organized under the laws of the PRC and a VIE that entered into via a series of contractual arrangement with its shareholders and Zhongruiyuan; | |

| ● | “Affiliate Entities” are to our subsidiaries and Aokai Fa and its subsidiaries, if any; | |

| ● | “Articles of Association” are to the amended and restated memorandum and articles of association of Huake; | |

| “China” or the “PRC” are to the People’s Republic of China, excluding Taiwan and the special administrative regions of Hong Kong and Macau for the purposes of this prospectus only; | ||

| ● | “Class A Ordinary Shares” are to the Class A ordinary shares of the Company, par value US$0.002 per share; | |

| ● | “Class B Ordinary Shares” are to the Class B ordinary shares of the Company, par value US$0.002 per share; | |

| ● | “Companies Act” is to the Cayman Islands Companies Act (As Revised); | |

| ● | “Huake” are to Huake Holding Biology Co., LTD, an exempted company with limited liability incorporated under the laws of Cayman Islands; | |

| ● | “Ruiyuan HK” are to Huake’s wholly owned subsidiary, China Ruiyuan Holding Co., Ltd., a Hong Kong corporation; | |

| ● | “VIE Agreements” are to a series of contractual arrangements, including the Exclusive Option Agreement, Exclusive Business Cooperation Agreement, Supplementary Agreement to the Exclusive Business Cooperation Agreement, Equity Interest Pledge Agreement, and Powers of Attorney Agreement between WFOE, the VIE, and the shareholders of the VIE; | |

| ● | “we,” “us,” or the “Company” in this prospectus are to Huake, Ruiyuan HK, Zhongruiyuan, and Aokai Fa, unless otherwise indicated or the context requires otherwise, in the context of describing our business, operations and consolidated financial information, “we,” “us,” or the “Company” are to Aokai Fa | |

| ● | “Zhongruiyuan” and “WFOE” are to Anhui Zhongruiyuan Biotechnology Co., Ltd., a limited liability company organized under the laws of the PRC, which is wholly owned by Ruiyuan HK. |

Our business is conducted by Aokai Fa, the VIE in the PRC, using RMB, the currency of China. Our consolidated financial statements are presented in United States dollars. In this prospectus, we refer to assets, obligations, commitments, and liabilities in our consolidated financial statements in United States dollars. These dollar references are based on the exchange rate of RMB to United States dollars, determined as of a specific date or for a specific period. Changes in the exchange rate will affect the amount of our obligations and the value of our assets in terms of United States dollars which may result in an increase or decrease in the amount of our obligations (expressed in dollars) and the value of our assets, including accounts receivable (expressed in dollars).

ii

The following summary is qualified in its entirety by, and should be read in conjunction with, the more detailed information and financial statements included elsewhere in this prospectus. In addition to this summary, we urge you to read the entire prospectus carefully, especially the risks of investing in our Class A Ordinary Shares, discussed under “Risk Factors,” before deciding whether to buy our Class A Ordinary Shares.

Overview

We are incorporated in the Cayman Islands. As a holding company with no material operations of our own, we conduct our operations in China through our subsidiaries, and the consolidated variable interest entity, Aokai Fa.

This is an offering of the Class A Ordinary Shares of the Cayman Islands holding company. You are not directly investing in and may never hold equity interests of Aokai Fa, the VIE, in China. The VIE, WFOE, and the VIE’s shareholders entered into the VIE Agreements; as a result of which we are regarded as the primary beneficiary of Aokai Fa for accounting purpose, and, therefore, we are able to consolidate the financial results of Aokai Fa in our consolidated financial statements in accordance with U.S. GAAP. However, neither we nor our subsidiaries own any share in Aokai Fa, and the investors will not and may never directly hold equity interests in the VIE either. The VIE structure cannot completely replicate a foreign investment in China-based companies. Instead, the VIE structure provides contractual exposure to foreign investment in us.

We engage in the production and sales of Camellia Oil products in China through the VIE. Aokai Fa was founded in 2011 in Tangchi town, Shucheng county of the Anhui province in China. Aokai Fa is a large-scale producer of Camellia Oil in the Anhui province, and it is now one of the leading enterprises of forestry and agricultural industrialization in Anhui province. We integrate scientific research, farming, production, and sales. Our goal is to become a leading Camellia Oil producer in the PRC and to develop “Aokai Fa” into a leading brand in the Camellia Oil industry in the PRC.

Aokai Fa guarantees the quality of its Camellia Oil through a vertically integrated system which starts from the farms and moves all the way through production and sales. Aokai Fa has established a standard laboratory with professional laboratory personnel. In the production process, sampling and testing are carried out in accordance with the industry standards. Each batch of the finished products is tested in strict accordance with GB11765 National Standard for Camellia Seed Oil. The products are also sent to a qualified third-party testing agency for testing from time to time. Applying the multiple patents Aokai Fa holds in its production, Aokai Fa has perfected its production process. The products are produced in a sterile environment where Aokai Fa maintains strict control over its products’ quality at a much higher level than the national testing standards.

We maintain a strong and growing customer base through different channels of merchandising, including direct selling, sales exhibition, and franchising, etc. As of date of this prospectus, the Company has over 20 sales agents nationwide covering provinces including Beijing, Guangxi, and Fujian. We also export our goods to areas like Taiwan, Hong Kong, and Southeast Asia.

Over the years, we have maintained stable revenues and net income. For the years ended September 30, 2021 and 2020, the Company had revenue of $18,540,385 and $14,636,348, respectively, and had net income of $2,362,859 and $1,703,903, respectively. For the six months ended March 31, 2022 and 2021, the Company had revenue of $10,017,587 and $7,448,147, respectively, and had net income of $1,545,206 and $1,007,290, respectively.

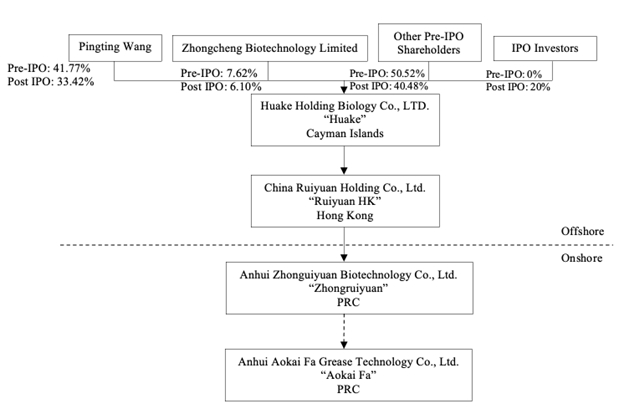

Corporate History and Holding Company Structure

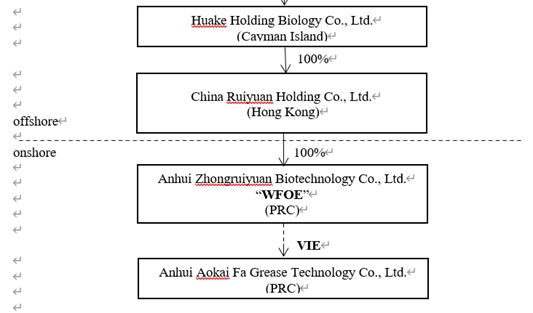

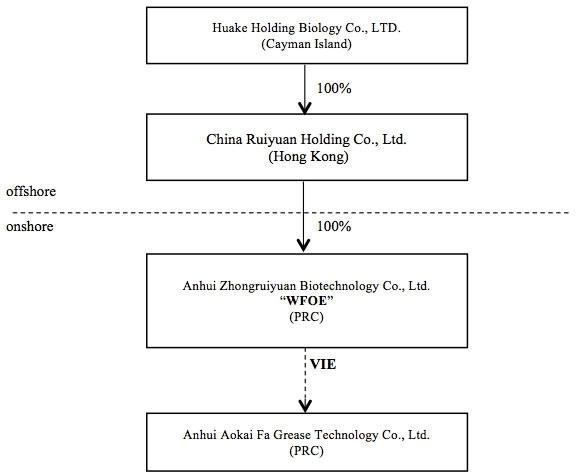

Huake Holding Biology Co., LTD is an exempted company incorporated with limited liability under the laws of the Cayman Islands on February 15, 2019. Huake wholly owns Ruiyuan HK, a company incorporated under the laws of the Hong Kong S.A.R. of the PRC on March 19, 2019. Ruiyuan HK is the sole shareholder of Zhonguiyuan, a limited liability company formed under the laws of the PRC on May 24, 2019. Zhonguiyuan has entered into a series of VIE Agreements with Aokai Fa, a company established under the laws of the PRC on December 26, 2011, and Aokai Fa’s shareholders. Because of the VIE Agreements, we are regarded as the primary beneficiary of Aokai Fa for accounting purpose, and, therefore, we are able to consolidate the financial results of Aokai Fa in our consolidated financial statements in accordance with U.S. GAAP. However, neither we nor our subsidiaries own any share in Aokai Fa, and the investors will not and may never directly hold equity interests in the VIE either. The VIE structure cannot completely replicate a foreign investment in China-based companies. Instead, the VIE structure provides contractual exposure to foreign investment in us. Because of our corporate structure, we are subject to risks due to uncertainty of the interpretation and the application of the PRC laws and regulations, including but not limited to limitation on foreign ownership of internet technology companies, and regulatory review of oversea listing of PRC companies through a special purpose vehicle, and the validity and enforcement of the VIE Agreements because they have not been tested in a court of law.

On February 15, 2019, 20,000,000 ordinary shares were issued to our founder shareholders in connection with their entering into the VIE Agreements.

On September 17, 2021, our shareholders and the Board of Directors adopted and approved an amendment to our amended and restated memorandum and articles of association, pursuant to which, among other matters, 10,122,000 ordinary shares were re-designated as Class A Ordinary Shares and 9,878,000 ordinary shares, of which 1,524,000 ordinary shares were beneficially owned by Mr. Tingyin Zhang, our former Chairman of the Board, and 8,354,000 were beneficially owned by Ms. Pingting Wang, our Chief Executive Officer and Chairperson, were re-designated as Class B Ordinary Shares on an one-for-one basis on the same date.

On November 3, 2022, our shareholders and the Board of Directors adopted and approved an amendment to our amended and restated memorandum and articles of association to effectuate the Share Combination. As of the date of this prospectus, there are 2,530,500 Class A Ordinary Shares issued and outstanding and 2,469,500 Class B Ordinary Shares issued and outstanding, of which 381,000 Class B Ordinary Shares were beneficially owned by Mr. Tingyin Zhang, our former Chairman of the Board, and 2,088,500 Class B Ordinary Shares were beneficially owned by Ms. Pingting Wang, our Chief Executive Officer and Chairperson.

1

VIE Agreements among WFOE, Aokai Fa and its shareholders

Huake Holding Biology Co., LTD is an exempted company incorporated with limited liability under the laws of the Cayman Islands on February 15, 2019. Huake wholly owns Ruiyuan HK, a company incorporated under the laws of the Hong Kong S.A.R. of the PRC on March 19, 2019. Ruiyuan HK is the sole shareholder of Zhonguiyuan, the wholly foreign owned entity, or the “WFOE”, a limited liability company formed under the laws of the PRC on May 24, 2019. The WFOE has entered into a series of VIE Agreements with Aokai Fa, a company established under the laws of the PRC on December 26, 2011, and Aokai Fa’s shareholders.

The Class A Ordinary Shares offered in this prospectus are those of the Cayman Islands holding company. You are not directly investing in and may never hold equity interests of Aokai Fa, the VIE in China.

As a holding company with no material operations of our own, we conduct our operations of the production and sales of Camellia Oil products in China through the variable interest entity, Aokai Fa. The research, farming, production and sales of Camellia Oil are categorized as “restricted” or “prohibited” from foreign investment under the “negative list” issued in 2020 by the National Development and Reform Commission and the Ministry of Commerce in China. As a result, neither we nor our subsidiaries own any equity interest in Aokai Fa. Instead, WFOE, Aokai Fa and its shareholders entered into a series of VIE Agreements, pursuant to which, we are regarded as the primary beneficiary of Aokai Fa for accounting purpose, and, therefore, we are able to consolidate the financial results of Aokai Fa in our consolidated financial statements in accordance with U.S. GAAP. However, neither we nor our subsidiaries own any share in Aokai Fa, and the investors will not and may never directly hold equity interests in the VIE either. The VIE structure cannot completely replicate a foreign investment in China-based companies. Instead, the VIE structure provides contractual exposure to foreign investment in us. Because of our corporate structure, we are subject to risks due to uncertainty of the interpretation and the application of the PRC laws and regulations, including but not limited to limitation on foreign ownership of internet technology companies, and regulatory review of oversea listing of PRC companies through a special purpose vehicle, and the validity and enforcement of the VIE Agreements because they have not been tested in a court of law.

Although we took every precaution available to effectively enforce the contractual and corporate relationship with the VIE, these VIE Agreements may still be less effective than direct ownership and that the Company may incur substantial costs to enforce the VIE Agreements. For example, the VIE and their shareholders could breach the VIE Agreements with us by, among other things, failing to conduct their operations in an acceptable manner or taking other actions that are detrimental to our interests. If we had direct ownership of the VIE, we would be able to exercise our rights as a shareholder to effect changes in the board of directors of the VIE, which in turn could implement changes, subject to any applicable fiduciary obligations, at the management and operational level. However, under the VIE Agreements, we rely on the performance by the VIE and their shareholders of their obligations under the contracts to exercise control over the VIE. The shareholders of our consolidated VIE may not act in the best interests of the Company or may not perform their obligations under the VIE Agreements. In addition, failure of the VIE shareholders to perform certain obligations could compel the Company to rely on legal remedies available under PRC laws, including seeking specific performance or injunctive relief, and claiming damages, which may not be effective.

The VIE Agreements are governed by PRC law and provide for the resolution of disputes through arbitration in the PRC. The legal environment in the PRC is not as developed as in some other jurisdictions, such as the United States. As a result, uncertainties in the PRC legal system could limit our ability to enforce the VIE Agreements. In the event we are unable to enforce the VIE Agreements, we may not be able to exert effective control over our operating entities and we may be precluded from operating our business, which would have a material adverse effect on our financial condition and results of operations. In addition, there is uncertainty as to whether the courts of the Cayman Islands or the PRC would recognize or enforce judgments of U.S. courts against us or such persons predicated upon the civil liability provisions of the securities laws of the United States or any state. See “Risk Factors – Risks Related to Our Corporate Structure” starting on page 47 of this prospectus for more information.

Because we do not directly hold equity interests in the VIE, we are subject to risks due to uncertainty of the interpretation and the application of the PRC laws and regulations, including, but not limited to, regulatory review of overseas listing of PRC companies through a special purpose vehicle, and the validity and enforcement of the VIE Agreements. We are also subject to the risks of uncertainty about any future actions of the PRC government in this regard that could disallow the VIE structure, which would likely result in a material change in our operations and the value of our Class A Ordinary Shares may depreciate significantly or become worthless.

2

Each of the VIE Agreements is described in detail below:

Exclusive Business Cooperation Agreement

On August 18, 2019, WFOE and Aokai Fa executed the exclusive business cooperation agreement pursuant to which WFOE has agreed to provide Aokai Fa with technical support, consulting and other services. The parties agree that during the term of this agreement, where necessary, Aokai Fa may enter into further service agreements with WFOE or any other party designated by WFOE, which shall provide the specific contents, manner, personnel, and fees for the specific services. Aokai Fa has agreed to pay a monthly service fee to WFOE. The service fee for each month consists of a management fee and a fee for services provided, which is mutually determined by the parties based on: (i) complexity and difficulty of the services provided by WFOE; (ii) title of and time consumed by employees of WFOE providing the services; (iii) contents and value of the services provided by WFOE; (iv) market price of the same type of services; and (v) operational conditions of the Aokai Fa. In addition, if WFOE transfers technology to Aokai Fa or develops software or other technology as requested by Aokai Fa or leases equipment or properties to Aokai Fa, the technology transfer price, development fees or rent shall be determined by the parties based on the actual situation on a case by case basis.

On April 8, 2022, WFOE and Aokai Fa executed a supplementary agreement to the exclusive business cooperation agreement, which amended the “services fee” to be 100% of the VIE’s net income, which is the Aokai Fa’s before corporate income tax, being the monthly revenues after deduction of operating costs, expenses and other taxes.

If Aokai Fa materially breaches any term of this agreement or the supplementary agreement, WFOE has a right to terminate this agreement and the supplementary agreement, and/or require Aokai Fa to indemnify it for all damages. Unless otherwise required by applicable laws, Aokai Fa does not have any right to terminate the agreement or the supplementary agreement. The agreement and the supplementary agreement became effective upon execution by the parties. Unless terminated in accordance with the terms of this agreement and the supplementary agreement, the agreement and the supplementary agreement remain in full force and effect.

Exclusive Option Agreement

On May 25, 2019, the shareholders of Aokai Fa, Aokai Fa and WFOE executed the Exclusive Option Agreement pursuant to which the shareholders of Aokai Fa irrevocably granted WFOE or its designee an exclusive purchase option to acquire, at any time, in whole or in part Aokai Fa’s equity interest held by each shareholder of Aokai Fa, or any portion thereof, to the extent permitted by the PRC law. The purchase price for the shareholders’ equity interests in Aokai Fa is RMB 108,687,728, unless PRC Law requires a minimum price that is higher at the time of the exercise of the option.

The shareholders of Aokai Fa and Aokai Fa further agree that, without obtaining prior written consent of WFOE, they may not (1) supplement, change or amend the articles of association of Aokai Fa, increase or decrease its registered capital, or change its structure of registered capital in other manner; (2) sell, transfer, mortgage or dispose of in any manner any material assets of Aokai Fa or legal or any other beneficial interest in the material business or revenues of Aokai Fa of more than RMB 10,000,000, or allow the encumbrance thereon of any security interest; (3) incur, inherit, guarantee or suffer the existence of any debt, except for payables incurred in the ordinary course of business other than through loans, or cause Aokai Fa to provide any person with any loan or credit; (4) cause Aokai Fa to execute any major contract with a price greater than RMB 500,000, except for the contracts in the ordinary course of business; (5) cause or permit Aokai Fa to merge, consolidate with, acquire or invest in any person; (6) in any manner distribute dividends to its shareholders, provided that upon WFOE’s written request, Aokai Fa shall immediately distribute all distributable profits to its shareholders; (7) engage in any business in competition with WFOE or its affiliates; or (8) be dissolved or liquated without prior written consent by WFOE.

The shareholders of Aokai Fa have agreed that, without obtaining the prior written consent of WFOE, among other things, (1) they may not sell, transfer, mortgage or dispose of, in any other manner, any legal or beneficial interest in the equity interests in Aokai Fa held by them, or allow the encumbrance thereon, except for the interest placed in accordance with the shareholders’ Equity Interest Pledge Agreement and their Powers of Attorney, (2) they shall cause the shareholders and/or directors (or the executive director) of Aokai Fa not to approve any sale, transfer, mortgage or disposition in any other manner of any legal or beneficial interest in the equity interests in Aokai Fa held by them as the shareholders, or allow the encumbrance thereon of any security interest, except for the interest placed in accordance with shareholders’ Equity Interest Pledge Agreement and the shareholders’ Powers of Attorney, and (3) they shall cause the shareholders and/or directors (or the executive director) of Aokai Fa not to approve the merger or consolidation with any person, or the acquisition of or investment in any person.

3

The shareholders of Aokai Fa shall (1) cause the shareholders’ and/or the directors (or the executive director) of Aokai Fa to vote their approval of the transfer of the optioned interests as set forth in this agreement and to take any and all other actions that may be requested by WFOE; (2) appoint any designee of WFOE as the director or the executive director of Aokai Fa, at the request of WFOE; (3) waive any right of first of refusal with respect to transferring of equity interest, and give consent to execution by each other shareholder of Aokai Fa with WFOE any agreements similar to the contractual arrangements and undertakes not to take any action in conflict with such agreements; and (4) promptly assign any profit, interest, dividend or proceeds of liquidation to WFOE or any other person designated by WFOE to the extent permitted under the applicable PRC laws;

The agreement became effective upon execution by the parties, and remains effective until all equity interests held by the shareholders of Aokai Fa have been transferred or assigned to WFOE and/or any other person designated by WFOE in accordance with the agreement.

Equity Interest Pledge Agreement

On May 25, 2019, the shareholders of Aokai Fa, Aokai Fa and WFOE executed the Equity Interest Pledge Agreement, pursuant to which the shareholders of Aokai Fa have agreed that without the prior written consent of WFOE, the shareholders of Aokai Fa may not directly or indirectly assign, sell, donate, pledge, encumber or otherwise dispose of, any interest in the equity interest of Aokai Fa which they hold. Pursuant to the terms of the agreement, in the event that either Aokai Fa or its shareholders are in breach of their obligations under the Exclusive Business Cooperation Agreement, Exclusive Option Agreement and/or the Powers of Attorney (the “Transaction Documents”) and/or the Equity Interest Pledge Agreement, then WFOE has a right to request the shareholders of Aokai Fa to transfer all or part of the equity interest they hold to any other person designated by WFOE at a minimum price allowed by the applicable PRC laws and regulations.

Upon the fulfillment of all obligations under the Transaction Documents, this agreement will be deemed completed and terminated.

Powers of Attorney

On May 25, 2019, each shareholder of Aokai Fa has executed an irrevocable power of attorney to appoint WFOE the or the authorized personnel of WFOE as its attorney-in-fact to exercise all of its rights as an equity owner of Aokai Fa, including (1) the right to attend shareholders and employees’ meetings of Aokai Fa; (2) the voting rights and any other rights that a shareholder of Aokai Fa is entitled to under the laws of China and Aokai Fa’s Articles of Association, including but not limited to the right to sell, transfer, pledge or dispose of shareholder’s equity interest in part or in whole; and (3) the designation and appointment of a legal representative, directors, supervisors, a chief executive officer and other senior management members of Aokai Fa.

Spousal Consent Letters

The spouse of each married shareholder of Aokai Fa executed a Spousal Consent Letter on May 25, 2019. Pursuant to the Spousal Consent Letter, the shareholder’s spouse has agreed to the execution of the Exclusive Option Agreement, Equity Interest Pledge Agreement, Power of Attorney and the disposal of the equity interests held by the shareholder in Aokai Fa pursuant to those agreements. The spouse of the shareholder agreed that he/she shall not assert any interests in such equity interests in Aokai Fa held by the shareholder, and if he/she obtains any such equity interests, he/she shall be bound by the Exclusive Option Agreement, Equity Interest Pledge Agreement, Power of Attorney and the Exclusive Business Cooperation Agreement.

4

The following diagram illustrates our corporate structure as of the date of this prospectus and after giving effect to this offering (assuming no exercise of the over-allotment option):

Organizational chart

Consolidation

We conduct substantially all of our business in China via Aokai Fa, the VIE, due to PRC legal restrictions of foreign ownership in certain sectors. Substantially all of Huake Holding Biology Co., LTD’s revenues, costs and net income in China are directly or indirectly generated through Aokai Fa. Huake Holding Biology Co., LTD through its indirect subsidiary, Zhongruiyuan, has signed various agreements with Aokai Fa and shareholders of Aokai Fa to allow the transfer of economic benefits from Aokai Fa to Zhongruiyuan and to direct the activities of Aokai Fa. However, Zhongruiyuan does not have any direct or indirect ownership of Aokai Fa. As a result, our shareholders are not investing in Aokai Fa, but instead are investing in Huake Holding Biology Co., LTD.

The following is a selected condensed consolidating schedule depicting the financial position as of September 30, 2021 and 2020, cash flows and results of operations for the year ended September 30, 2021 and 2020, and a selected condensed consolidating schedule depicting the financial position as of March 31, 2022, cash flows and results of operations for the six months ended March 31, 2022 and 2021 for Huake Holding Biology Co., LTD, our subsidiaries, the VIE and corresponding eliminating adjustments.

5

Selected Condensed Consolidation Schedule of Balance Sheet

As of September 30, 2021 (Restated)

| Parent and Hong Kong | WFOE | VIE | Elimination Entries and Reclassification Entries | Consolidated | ||||||||||||||||

| (As Restated) | (As Restated) | (As Restated) | (As Restated) | (As Restated) | ||||||||||||||||

| Cash | $ | - | $ | - | $ | 108,383 | $ | - | $ | 108,383 | ||||||||||

| Intercompany receivable from VIE | - | 4,868,297 | - | (4,868,297 | ) | - | ||||||||||||||

| Total Current Assets | - | 4,868,297 | 20,243,861 | (4,868,297 | ) | 20,243,861 | ||||||||||||||

| Investment in Subsidiaries | 4,868,297 | - | - | (4,868,297 | ) | - | ||||||||||||||

| Total Non-current Assets | - | - | 5,450,757 | - | 5,450,757 | |||||||||||||||

| Intercompany payable to WFOE | - | - | 4,868,297 | (4,868,297 | ) | - | ||||||||||||||

| Total Liabilities | - | - | 11,611,343 | (4,868,297 | ) | 6,743,046 | ||||||||||||||

| Total Shareholders’ Equity | 4,868,297 | 4,868,297 | 14,083,275 | (4,868,297 | ) | 18,951,572 | ||||||||||||||

| * | Intercompany receivable from VIE and intercompany payable to WFOE represented the service fee payable to WFOE based on Exclusive Business Cooperation Agreement and its supplementary agreement. There has been no cash transaction between VIE and other entities. |

6

Selected Condensed Consolidation Schedule of Comprehensive Income

For the year ended September 30, 2021 (Restated)

| Parent and Hong Kong | WFOE | VIE | Elimination Entries | Consolidated | ||||||||||||||||

| (As Restated) | (As Restated) | (As Restated) | (As Restated) | (As Restated) | ||||||||||||||||

| Revenue | $ | - | $ | - | $ | 18,540,385 | $ | - | $ | 18,540,385 | ||||||||||

| Cost of Goods Sold | - | - | 15,146,691 | - | 15,146,691 | |||||||||||||||

| Gross Profit | - | - | 3,393,694 | - | 3,393,694 | |||||||||||||||

| Service fee expense from VIE to WFOE | 2,603,446 | (2,603,446 | ) | - | ||||||||||||||||

| Total operating expenses | - | - | 3,450,242 | (2,603,446 | ) | 846,796 | ||||||||||||||

| Operating Income | - | - | (56,548 | ) | 2,603,446 | 2,546,898 | ||||||||||||||

| Income from VIE | - | 2,603,446 | - | (2,603,446 | ) | - | ||||||||||||||

| Income from Equity Method Investment | 2,603,446 | - | - | (2,603,446 | ) | - | ||||||||||||||

| Net Income | 2,603,446 | 2,603,446 | (240,587 | ) | (2,603,446 | ) | 2,362,859 | |||||||||||||

| Total Comprehensive Income | $ | 2,603,446 | $ | 2,603,446 | $ | 627,471 | $ | (2,603,446 | ) | $ | 3,230,917 | |||||||||

7

Selected Condensed Consolidation Schedule of Cash Flows

For the year ended September 30, 2021 (Restated)

| Parent and Hong Kong | WFOE | VIE | Elimination Entries | Consolidated | ||||||||||||||||

| (As Restated) | (As Restated) | (As Restated) | (As Restated) | (As Restated) | ||||||||||||||||

| OPERATING ACTIVITIES | ||||||||||||||||||||

| Net income | $ | 2,603,446 | $ | 2,603,446 | $ | (240,587 | ) | $ | (2,603,446 | ) | $ | 2,362,859 | ||||||||

| Equity in earnings of subsidiaries | (2,603,446 | ) | - | 2,603,446 | - | |||||||||||||||

| Intercompany receivable / payable between WFOE and VIE | (2,603,446 | ) | 2,603,446 | - | - | |||||||||||||||

| Net cash provided by operating activities | - | - | 2,321,156 | - | 2,321,156 | |||||||||||||||

| Net cash used in investing activities | - | - | (2,422,394 | ) | - | (2,422,394 | ) | |||||||||||||

| Net cash provided by financing activities | - | - | 53,513 | - | 53,513 | |||||||||||||||

8

Selected Condensed Consolidation Schedule of Balance Sheet

As of September 30, 2020

| Parent and Hong Kong | WFOE | VIE | Elimination Entries and Reclassification Entries | Consolidated | ||||||||||||||||

| Cash | $ | - | $ | - | $ | 148,596 | $ | - | $ | 148,596 | ||||||||||

| Intercompany receivable from VIE | - | 2,264,851 | - | (2,264,851 | ) | - | ||||||||||||||

| Total Current Assets | 2,264,851 | 18,021,453 | (2,264,851 | ) | 18,021,453 | |||||||||||||||

| Investment in subsidiaries | 2,264,851 | - | - | (2,264,851 | ) | - | ||||||||||||||

| Total Non-current Assets | - | - | 3,225,608 | - | 3,225,608 | |||||||||||||||

| Intercompany payable to WFOE | 2,264,851 | (2,264,851 | ) | - | ||||||||||||||||

| Total Liabilities | - | - | 7,791,257 | (2,264,851 | ) | 5,526,406 | ||||||||||||||

| Total Shareholders’ Equity | 2,264,851 | 2,264,851 | 13,455,804 | (2,264,851 | ) | 15,720,655 | ||||||||||||||

| * | Intercompany receivable from VIE and intercompany payable to WFOE represented the service fee payable to WFOE based on Exclusive Business Cooperation Agreement and its supplementary agreement. There has been no cash transaction between VIE and other entities. |

9

Selected Condensed Consolidation Schedule of Comprehensive Income

For the year ended September 30, 2020

| Parent and Hong Kong | WFOE | VIE | Elimination Entries | Consolidated | ||||||||||||||||

| Revenue | $ | - | $ | - | $ | 14,636,348 | $ | - | $ | 14,636,348 | ||||||||||

| Cost of Goods Sold | - | - | 11,650,058 | - | 11,650,058 | |||||||||||||||

| Gross Profit | - | - | 2,986,290 | - | 2,986,290 | |||||||||||||||

| Service fee expense from VIE to WFOE | 2,264,851 | (2,264,851 | ) | - | ||||||||||||||||

| Total operating expenses | - | - | 3,088,494 | (2,264,851 | ) | 823,643 | ||||||||||||||

| Operating Income | - | - | (102,204 | ) | 2,264,851 | 2,162,647 | ||||||||||||||

| Income from VIE | - | 2,264,851 | - | (2,264,851 | ) | - | ||||||||||||||

| Income from Equity Method Investment | 2,264,851 | - | - | (2,264,851 | ) | - | ||||||||||||||

| Net Income | 2,264,851 | 2,264,851 | (560,948 | ) | (2,264,851 | ) | 1,703,903 | |||||||||||||

| Total Comprehensive Income | $ | 2,264,851 | $ | 2,264,851 | $ | 192,782 | $ | (2,264,851 | ) | $ | 2,457,633 | |||||||||

10

Selected Condensed Consolidation Schedule of Cash Flows

For the year ended September 30, 2020

| Parent and Hong Kong | WFOE | VIE | Elimination Entries | Consolidated | ||||||||||||||||

| OPERATING ACTIVITIES | ||||||||||||||||||||

| Net income | $ | 2,264,851 | $ | 2,264,851 | $ | (560,948 | ) | $ | (2,264,851 | ) | $ | 1,703,903 | ||||||||

| Equity in earnings of subsidiaries | (2,264,851 | ) | - | - | 2,264,851 | - | ||||||||||||||

| Intercompany receivable / payable between WFOE and VIE | (2,264,851 | ) | 2,264,851 | - | - | |||||||||||||||

| Net cash provided by operating activities | - | - | 1,485,793 | - | 1,485,793 | |||||||||||||||

| Net cash used in investing activities | - | - | (1,349,337 | ) | - | (1,349,337 | ) | |||||||||||||

| Net cash used in financing activities | - | - | (63,758 | ) | - | (63,758 | ) | |||||||||||||

11

Selected Condensed Consolidation Schedule of Balance Sheet

As of March 31, 2022

| Parent and Hong Kong | WFOE | VIE | Elimination Entries and Reclassification Entries | Consolidated | ||||||||||||||||

| Cash | $ | - | $ | - | $ | 149,029 | $ | - | $ | 149,029 | ||||||||||

| Intercompany receivable from VIE | - | 6,686,187 | - | (6,686,187 | ) | - | ||||||||||||||

| Total Current Assets | - | 6,686,187 | 22,819,312 | (6,686,187 | ) | 22,819,312 | ||||||||||||||

| Investment in Subsidiaries | 6,686,187 | - | - | (6,686,187 | ) | - | ||||||||||||||

| Total Non-current Assets | - | - | 5,907,389 | - | 5,907,389 | |||||||||||||||

| Intercompany payable to WFOE | - | - | 6,686,187 | (6,686,187 | ) | - | ||||||||||||||

| Total Liabilities | - | - | 14,597,563 | (6,686,187 | ) | 7,911,376 | ||||||||||||||

| Total Shareholders’ Equity | 6,686,187 | 6,686,187 | 14,129,138 | (6,686,187 | ) | 20,815,325 | ||||||||||||||

| * | Intercompany receivable from VIE and intercompany payable to WFOE represented the service fee payable to WFOE based on Exclusive Business Cooperation Agreement and its supplementary agreement. There has been no cash transaction between VIE and other entities. |

12

Selected Condensed Consolidation Schedule of Comprehensive Income

For the six months ended March 31, 2022

| Parent and Hong Kong | WFOE | VIE | Elimination Entries | Consolidated | ||||||||||||||||

| Revenue | $ | - | $ | - | $ | 10,017,587 | $ | - | $ | 10,017,587 | ||||||||||

| Cost of Goods Sold | - | - | 7,838,994 | - | 7,838,994 | |||||||||||||||

| Gross Profit | - | - | 2,178,593 | - | 2,178,593 | |||||||||||||||

| Service fee expense from VIE to WFOE | - | - | 1,817,890 | (1,817,890 | ) | - | ||||||||||||||

| Total operating expenses | - | - | 2,209,993 | (1,817,890 | ) | 392,103 | ||||||||||||||

| Operating Income | - | - | (31,400 | ) | 1,817,890 | 1,786,490 | ||||||||||||||

| Income from VIE | - | 1,817,890 | - | (1,817,890 | ) | - | ||||||||||||||

| Income from Equity Method Investment | 1,817,890 | - | - | (1,817,890 | ) | - | ||||||||||||||

| Net Income | 1,817,890 | 1,817,890 | (272,684 | ) | (1,817,890 | ) | 1,545,206 | |||||||||||||

| Total Comprehensive Income | $ | 1,817,890 | $ | 1,817,890 | $ | 45,863 | $ | (1,817,890 | ) | $ | 1,863,753 | |||||||||

13

Selected Condensed Consolidation Schedule of Cash Flows

For the six months ended March 31, 2022

| Parent and Hong Kong | WFOE | VIE | Elimination Entries | Consolidated | ||||||||||||||||

| OPERATING ACTIVITIES | ||||||||||||||||||||

| Net income | $ | 1,817,890 | $ | 1,817,890 | $ | (272,684 | ) | $ | (1,817,890 | ) | $ | 1,545,206 | ||||||||

| Equity in earnings of subsidiaries | (1,817,890 | ) | - | - | 1,817,890 | - | ||||||||||||||

| Intercompany receivable / payable between WFOE and VIE | (1,817,890 | ) | 1,817,890 | - | - | |||||||||||||||

| Net cash provided by operating activities | - | - | 477,812 | - | 477,812 | |||||||||||||||

| Net cash used in investing activities | - | - | (439,131 | ) | - | (439,131 | ) | |||||||||||||

| Net cash provided by financing activities | - | - | - | - | - | |||||||||||||||

14

Selected Condensed Consolidation Schedule of Comprehensive Income

For the six months ended March 31, 2021

| Parent and Hong Kong | WFOE | VIE | Elimination Entries | Consolidated | ||||||||||||||||

| Revenue | $ | - | $ | - | $ | 7,448,147 | $ | - | $ | 7,448,147 | ||||||||||

| Cost of Goods Sold | - | - | 5,959,641 | - | 5,959,641 | |||||||||||||||

| Gross Profit | - | - | 1,488,506 | - | 1,488,506 | |||||||||||||||

| Service fee expense from VIE to WFOE | 1,000,456 | (1,000,456 | ) | - | ||||||||||||||||

| Total operating expenses | - | - | 1,543,600 | (1,000,456 | ) | 543,144 | ||||||||||||||

| Operating Income | - | - | (55,094 | ) | 1,000,456 | 945,362 | ||||||||||||||

| Income from VIE | - | 1,000,456 | - | (1,000,456 | ) | - | ||||||||||||||

| Income from Equity Method Investment | 1,000,456 | - | - | (1,000,456 | ) | - | ||||||||||||||

| Net Income | 1,000,456 | 1,000,456 | 6,834 | (1,000,456 | ) | 1,007,290 | ||||||||||||||

| Total Comprehensive Income | $ | 1,000,456 | $ | 1,000,456 | $ | 577,544 | $ | (1,000,456 | ) | $ | 1,578,000 | |||||||||

15

Selected Condensed Consolidation Schedule of Cash Flows

For the six months ended March 31, 2021

| Parent and Hong Kong | WFOE | VIE | Elimination Entries | Consolidated | ||||||||||||||||

| OPERATING ACTIVITIES | ||||||||||||||||||||

| Net income | $ | 1,000,456 | $ | 1,000,456 | $ | 6,834 | $ | (1,000,456 | ) | $ | 1,007,290 | |||||||||

| Equity in earnings of subsidiaries | (1,000,456 | ) | - | 1,000,456 | - | |||||||||||||||

| Intercompany receivable / payable between WFOE and VIE | (1,000,456 | ) | 1,000,456 | - | - | |||||||||||||||

| Net cash provided by operating activities | - | - | 2,111,172 | - | 2,111,172 | |||||||||||||||

| Net cash used in investing activities | - | - | (2,255,288 | ) | - | (2,255,288 | ) | |||||||||||||

| Net cash used in financing activities | - | - | (961 | ) | - | (961 | ) | |||||||||||||

16

Permission or Approval Required from the PRC Authorities for the VIE’s Operation and Our Offering

To operate our general business activities currently conducted in China, the consolidated VIE has obtained a business license from the State Administration for Market Regulation (“SAMR”), which allows it to conduct specific business within the government’s geographical jurisdiction. As of the date of this prospectus, the business license is the only permission that the VIE is required to obtain for its operations. The VIE does not need specific licenses for the Camellia Oil business nor is it covered by permissions requirements from the China Securities Regulatory Commission (“CSRC”) or CAC.

However, applicable laws and regulations may become stricter, and new laws or regulations may be introduced to impose additional government approval, license and permit requirements. If we inadvertently conclude that such approval is not required, fail to obtain and maintain such approvals, licenses or permits required for our business or respond to changes in the regulatory environment, we could be subject to liabilities, penalties and operational disruption, which may materially and adversely affect our business, operating results, financial condition and the value of our securities, significantly limit or completely hinder our ability to offer or continue to offer securities to investors, or cause such securities to significantly decline in value or become worthless.

As of the date of this prospectus, none of our Company, our subsidiaries, or the VIE has applied for, received or been denied approval from any PRC authorities to list on the Nasdaq Stock Market, nor received any inquiry, notice, warning or sanctions regarding our planned overseas listing from the CSRC, the CAC, or any other PRC governmental authorities. As advised by our PRC counsel, Beijing Docvit Law Firm, we, our subsidiaries and the VIE are not required to obtain permission from the CSRC, the CAC, or any other Chinese authorities to issue these securities to foreign investors based on the PRC laws, regulations and rules currently in effect. However, if we are subsequently advised by any Chinese authorities that permission for this offering and/or listing on the Nasdaq Stock Market was required, we may not be able to obtain such permission in a timely manner, if at all. If this risk occurs, our ability to offer securities to investors could be significantly limited or completely hindered and the securities currently being offered may substantially decline in value and be worthless.

We are aware, however, that recently the PRC government initiated a series of regulatory actions and statements to regulate business operations in China with little advance notice, including cracking down on illegal activities in the securities market, enhancing supervision over China-based companies listed overseas using variable interest entity structure, adopting new measures to extend the scope of cybersecurity reviews, and expanding the efforts in anti-monopoly enforcement.

On December 24, 2021, the China Securities Regulatory Commission issued Provisions of the State Council on the Administration of Overseas Securities Offering and Listing by Domestic Companies (Draft for Comments) (the “Administration Provisions”), and the Provisions of the State Council on the Administration of Overseas Securities Offering and Listing by Domestic Companies (Draft for Comments) (the “Measures”), both of which have a comment period that expired on January 23, 2022. The Administration Provisions and Measures for overseas listings lay out specific requirements for filing documents and include unified regulation management, strengthening regulatory coordination, and cross-border regulatory cooperation. Domestic companies seeking to list abroad must carry out relevant security screening procedures if their businesses involve such supervision. Companies endangering national security are among those off-limits for overseas listings. According to Relevant Officials of the CSRC Answered Reporter Questions (“CSRC Answers”), after the Administration Provisions and Measures are implemented upon completion of public consultation and due legislative procedures, the CSRC will formulate and issue guidance for filing procedures to further specify the details of filing administration and ensure that market entities could refer to clear guidelines for filing, which means it still takes time to make the Administration Provisions and Measures into effect. As the Administration Provisions and Measures have not yet come into effect, we are currently unaffected. However, according to CSRC Answers, new initial public offerings and refinancing by existent overseas listed Chinese companies will be required to go through the filing process; other existent overseas listed companies will be allowed sufficient transition period to complete their filing procedure, which means we will certainly go through the filing process in the future.

Pursuant to the PRC Cybersecurity Law, which was promulgated by the Standing Committee of the National People’s Congress on November 7, 2016 and took effect on June 1, 2017, personal information and important data collected and generated by a critical information infrastructure operator in the course of its operations in China must be stored in China, and if a critical information infrastructure operator purchases internet products and services that affects or may affect national security, it should be subject to cybersecurity review by the CAC. Due to the lack of further interpretations, the exact scope of “critical information infrastructure operator” remains unclear. On December 28, 2021, the CAC and other relevant PRC governmental authorities jointly promulgated the new Cybersecurity Review Measures to replace the original Cybersecurity Review Measures. The new Cybersecurity Review Measures took effect on February 15, 2022. Pursuant to the new Cybersecurity Review Measures, if critical information infrastructure operators purchase network products and services, or network platform operators conduct data processing activities that affect or may affect national security, they will be subject to cybersecurity review. On November 14, 2021, CAC published the Administration Measures for Cyber Data Security (Draft for Public Comments), or the “Cyber Data Security Measure (Draft)”, which requires cyberspace operators with personal information of more than 1 million users who want to list abroad to file a cybersecurity review with the Office of Cybersecurity Review. The cybersecurity review will evaluate, among others, the risk of critical information infrastructure, core data, important data, or a large amount of personal information being influenced, controlled or maliciously used by foreign governments and risk of network data security after going public overseas. As advised by our PRC counsel, Beijing Docvit Law Firm, we do not expect to be subject to cybersecurity review, because: (i) our products are offered not directly to individual consumers but through our distributors; (ii) we do not possess a large amount of personal information in our business operations; and (iii) data processed in our business does not have a bearing on national security and thus may not be classified as core or important data by the authorities. Since these statements and regulatory actions are new, it is highly uncertain how soon legislative or administrative regulation making bodies will respond and what existing or new laws or regulations or detailed implementations and interpretations will be modified or promulgated, if any, and the potential impact such modified or new laws and regulations will have on our daily business operation, the ability to accept foreign investments and list on an U.S. exchange. If applicable laws, regulations, or interpretations change, and we are required to obtain permission or approval from the PRC authority for the offering of our Class A Ordinary Shares in the U.S. in the future, and if any of such permission or approval were not received maintained, or subsequently rescinded, it may significantly limit or completely hinder our ability to complete this offering or cause the value of our Ordinary Shares to significantly decline or become worthless. See “Risk Factors – Risks Related to Doing Business in the PRC” starting on page 29 of this prospectus and “Risk Factors – Risks Related to Our Corporate Structure” starting on page 47 of this prospectus for more information.

17

Dividend Distributions or Assets Transfer among the Holding Company, its Subsidiaries and the Consolidated VIE

We intend to keep any future earnings to re-invest in and finance the expansion of our business, and we do not anticipate that any cash dividends will be paid or any assets will be transferred in the foreseeable future. As of the date of this prospectus, the VIE has not remitted any services fees to WFOE. However, the VIE is obligated to pay a service fee equivalent to 100% of VIE’s net income after deduction of certain tax and operational expenses. As of the date of this prospectus, none of our subsidiaries or VIE have made any dividends or distributions to us and we has not made any dividends or distributions to our shareholders.

Under Cayman Islands law, a Cayman Islands company may pay a dividend on its shares out of either profit or share premium amount, provided that in no circumstances may a dividend be paid if this would result in the company being unable to pay its debts due in the ordinary course of business. If we determine to pay dividends on any of our Class A Ordinary Shares in the future, as a holding company, we will be dependent on receipt of funds from our Hong Kong subsidiary, Ruiyuan HK.

Current PRC regulations permit our indirect PRC subsidiary to pay dividends to the Company only out of their accumulated profits, if any, determined in accordance with Chinese accounting standards and regulations. In addition, each of our subsidiaries in China is required to set aside at least 10% of its after-tax profits each year, if any, to fund a statutory reserve until such reserve reaches 50% of its registered capital. Each of such entity in China is also required to further set aside a portion of its after-tax profits to fund the employee welfare fund, although the amount to be set aside, if any, is determined at the discretion of its board of directors. Although the statutory reserves can be used, among other ways, to increase the registered capital and eliminate future losses in excess of retained earnings of the respective companies, the reserve funds are not distributable as cash dividends except in the event of liquidation.

The PRC government also imposes controls on the conversion of RMB into foreign currencies and the remittance of currencies out of the PRC. Therefore, we may experience difficulties in completing the administrative procedures necessary to obtain and remit foreign currency for the payment of dividends from our profits, if any. Furthermore, if our subsidiaries in the PRC incur debt on their own in the future, the instruments governing the debt may restrict their ability to pay dividends or make other payments. If we or our subsidiaries are unable to receive all of the revenues from our operations through the current VIE Agreements, we may be unable to pay dividends on our Class A Ordinary Shares.