Exhibit 99.1

BITFARMS LTD.

ANNUAL INFORMATION FORM

FOR THE FISCAL YEAR ENDED DECEMBER 31, 2022

March 20, 2023

TABLE OF CONTENTS

| GLOSSARY OF DEFINED TERMS | 2 |

| GENERAL | 7 |

| STATEMENT REGARDING FORWARD-LOOKING STATEMENTS | 7 |

| CURRENCY | 8 |

| CORPORATE STRUCTURE | 9 |

| GENERAL DEVELOPMENT OF THE BUSINESS | 9 |

| DESCRIPTION OF BUSINESS | 18 |

| RISK FACTORS | 32 |

| PRIOR SALES | 49 |

| DIVIDENDS | 50 |

| DESCRIPTION OF CAPITAL STRUCTURE | 50 |

| MARKET FOR SECURITIES | 50 |

| ESCROWED SECURITIES AND SECURITIES SUBJECT TO CONTRACTUAL RESTRICTION ON TRANSFER | 51 |

| DIRECTORS AND OFFICERS | 52 |

| INTEREST OF MANAGEMENT AND OTHERS IN MATERIAL TRANSACTIONS | 60 |

| LEGAL PROCEEDINGS | 60 |

| TRANSFER AGENT AND REGISTRAR | 61 |

| MATERIAL CONTRACTS | 61 |

| EXPERTS | 62 |

| ADDITIONAL INFORMATION | 62 |

| SCHEDULE A – AUDIT COMMITTEE CHARTER | 63 |

GLOSSARY OF DEFINED TERMS

In this Annual Information Form, the following capitalized words and terms shall have the following meanings:

“Additional Server Farms” means the additional server farms that the Company had planned for and that started operating on or before December 31, 2022, namely the Sherbrooke Expansion, Argentina Expansion, Paraguay Expansion and Washington Expansion;

“AIF” means this annual information form dated March 20, 2023;

“ANDE” means the National Electricity Administration of Paraguay;

“Argentina Expansion” means the existing and planned construction of a server farm facility in stages in Argentina;

“ASIC” means application specific integrated circuit;

“ATM Agreement” means the at-the-market offering agreement dated August 16, 2021, between the Company and H.C. Wainwright & Co.;

“August SFBS Prospectus” means the final base shelf short form prospectus filed by the Company on August 12, 2021;

“Backbone” means Backbone Hosting Solutions Inc.;

“Backbone Argentina” means Backbone Hosting Solutions S.A.U. (Argentina);

“Backbone Paraguay” means Backbone Hosting Solutions Paraguay S.A.;

“Bitcoin Halving” has the meaning ascribed thereto in RISK FACTORS – BTC Halving Event;

“Bitfarms” means the operating business name and trademarked name of Backbone;

“Bitfarms Canada” or the “Company” means Bitfarms Ltd., a corporation incorporated pursuant to the laws of Canada and continued under the Ontario Business Corporation Act listed on the TSX and NASDAQ under the symbol BITF, including all subsidiaries thereof;

“Bitfarms Canada Board” or the “Board” means the board of directors of Bitfarms Canada;

“Bitfarms Shares” or “Common Shares” means the common shares in the capital of Bitfarms Canada;

“Bitfarms Israel” means Bitfarms Ltd., a corporation incorporated pursuant to the laws of Israel;

“BMS” means Backbone Mining Solutions, Inc.;

“Botnet” means a number of Internet-connected devices, each of which is running one or more bots (a computer program that does automated tasks). Botnets can be used to perform distributed denial-of-service attack, steal data, send spam, and allows the attacker to access the device and its connection;

“BTC” or “Bitcoin” means Bitcoin, a decentralized digital currency that can be sent from user to user on the BTC network without the need for intermediaries to clear transactions;

“Bunker” means the property leased by the Company in Sherbrooke in 2021 with the expansion project completed in 2022, as described in DESCRIPTION OF BUSINESS - Recently Completed Development and Future Growth Plans – The Bunker;

| 2 | Page |

“CEO” means Chief Executive Officer;

“CFO” means Chief Financial Officer;

“CLYFSA” means Compañía Luz y Fuerza S.A., an electricity distribution company located in the city of Villarrica, Paraguay;

“Coinbase Custody” means Coinbase Trust Company, LLC;

“Compensation Committee” has the meaning as provided in DIRECTORS AND OFFICERS – Committees of the Board of Directors – Compensation Committee;

“CORE IR Agreement” means the agreement between the Company and CORE IR for investor relations, public relations and shareholder communications services entered into on March 12, 2021, and terminated in September 2021;

“Cryptocurrency” means a form of encrypted and decentralized digital currency, transferred directly between peers across the Internet, with transactions being settled, confirmed and recorded in a distributed public ledger through Mining. Cryptocurrency is either newly “minted” through an initial coin/token offering or Mined, which results in a new coin generated as a reward to incentivize miners for verifying transactions on the blockchain;

“Current Facilities” means the ten operational Mining facilities operated by the Company in the Province of Québec, Washington State, Paraguay and Argentina as of March 20, 2023, namely the facilities at Farnham, Saint-Hyacinthe, Cowansville, Magog, Sherbrooke (Bunker, Leger, and Garlock), Villarrica, Washington State and Rio Cuarto;

“December 2021 Debt Facility” means the US$100 million credit facility between the Company and Galaxy Digital entered into on December 30, 2021 and repaid and retired on December 2022;

“De la Pointe Property” means the Company’s former 78,000 square foot facility located in Sherbrooke, Quebec, which ceased production and was sold on December 2022;

“Digital Asset Management Program” means the Company’s BTC holding strategy implemented in January 2021 as described in DESCRIPTION OF BUSINESS - Business and Strategy - Digital Asset Management Program;

“Dominion” means Dominion Capital;

“Dominion Facility” has the meaning as provided for in GENERAL DEVELOPMENT OF THE BUSINESS - Three-year History - Fiscal 2020 – Debt Financing;

“Environmental and Social Responsibility Committee” has the meaning as provided in DIRECTORS AND OFFICERS – Committees of the Board of Directors – Environmental and Social Responsibility Committee;

“February 2021 Offering” means the February 2021 private placement of 11,560,695 Common Shares and associated warrants;

“February 2022 BlockFi Loan Facility” means the US$32 million credit facility between the Company and BlockFi Lending LLC., a private lender entered into on February 24, 2022 and repaid and retired on February 2023;

“Fiscal 2020” means the fiscal year ended December 31, 2020;

“Fiscal 2021” means the fiscal year ended December 31, 2021;

| 3 | Page |

“Fiscal 2022” means the fiscal year ended December 31, 2022;

“Fiscal 2023” means the fiscal year ended December 31, 2023;

“Foundry Loans #1, #2, #3 and #4” which are fully repaid, has the meaning as provided for in GENERAL DEVELOPMENT OF THE BUSINESS - Three-year History - Fiscal 2021 – Debt Financing;

“FPPS” means Full Pay Per Share, the formula-driven rate at which the Company sells computational power to Mining Pools;

“Garlock” means the building acquired by the Company on March 11, 2022 located in Sherbrooke, Quebec;

“GMSA” means Generacion Mediterranea S.A., one of the subsidiaries of Grupo Albanesi, an Argentine private corporate group focused on the energy market which provides natural gas and electrical energy to its clients.

“Governance and Nominating Committee” has the meanings as provided in DIRECTORS AND OFFICERS – Committees of the Board of Directors – Governance and Nominating Committee;

“Grant PUD” means the Grant County Power Utility District in Washington State;

“Hash” means the output of a hash function, i.e., the output of the fundamental mathematical computation of a particular cryptocurrency’s computer code which Miners execute, and “Petahash” or “PH” and “Exahash” or “EH” mean, respectively, 1x1015 and 1x1018 Hashes;

“Hosting Agreement” has the meaning as provided for in GENERAL DEVELOPMENT OF THE BUSINESS - Three-year History - Fiscal 2021 – Development of Operations;

“Hydro-Magog” means the regional public utility company that manages the generation and distribution of electricity in the region of Magog, Québec;

“Hydro-Québec” means “Commission hydroélectrique du Québec”, the provincial public utility company that manages the generation and distribution of electricity in the Province of Québec;

“Hydro-Sherbrooke” means the regional public utility company that manages the generation and distribution of electricity in the region of Sherbrooke, Québec;

“Ingenia” means Ingenia Grupo Consultor and Gieco S.A., as described in DESCRIPTION OF BUSINESS - Argentina Expansion.;

“Initial Draw” means the initial US$60 million draw on the December 2021 Debt Facility;

“Israel” means the State of Israel;

“January 7, 2021 Offering” means the January 2021 private placement offering of 8,888,889 Common Shares and associated warrants;

“January 13, 2021 Offering” means the January 2021 private placement offering of 5,586,593 Common Shares and associated warrants;

“July 2021 Hosting Agreement” means the hosting agreement entered into by the Company for 12 MW in Washington State, US entered into on November 11, 2021 and terminated upon the closing of the November 2021 Washington Acquisition;

“June 2022 NYDIG Financing” means the equipment financing agreement dated June 17, 2022 between the Company and NYDIG for initial funding of US$37,000,000;

| 4 | Page |

“Leger” means the Company’s 36,000 square foot facility in Sherbrooke, Quebec;

“Lender Warrants” has the meaning as provided for in GENERAL DEVELOPMENT OF THE BUSINESS - Three-year History - Fiscal 2020 – Debt Financing;

“LHA IR Agreement” has the meaning as provided for in GENERAL DEVELOPMENT OF THE BUSINESS - Fiscal 2021;

“LPZ” means LPZ Hosting S.A.S, as described in DESCRIPTION OF BUSINESS - Argentina Expansion.;

“May 2021 Offering” means the May 2021 private placement of 14,150,940 Common Shares and associated warrants;

“MD&A” means management’s discussion and analysis;

“MOU” means the nonbinding memorandum of understanding entered into by the Company on October 26, 2020, to secure 200 MW of electricity in South America;

“Miner” means a computer configured for the purpose of performing blockchain computer operations. See DESCRIPTION OF BUSINESS;

“Mine” or “Mining” means the process of using Miners to provide the service of verifying and validating cryptographic blockchain transactions and being rewarded with cryptocurrency in return for such service. See DESCRIPTION OF BUSINESS;

“Mining Pool” refers to when cryptocurrency Miners aggregate their processing power over a network and Mine transactions together. See DESCRIPTION OF BUSINESS - Principal Market Overview;

“Nasdaq” means the Nasdaq Stock Market;

“NI 52-110” means National Instrument 52-110 – Audit Committees;

“NEO” or “Named Executive Officer” has the meaning ascribed to that term in Form 51-102F6 Statement of Executive Compensation;

“November 2021 Washington Acquisition” means the Company’s acquisition of a bitcoin mining production facility in Washington State, US on November 11, 2021;

“NYDIG” means NYDIG ABL LLC;

“OBCA” means the Ontario Business Corporations Act;

“Power Producer” has the meaning ascribed to that term in DESCRIPTION OF BUSINESS - Recently Completed Development and Future Growth Plans - Argentina Expansion;

“PROA” means Proyectos y Obras Americanas S.A.

“PSU” means power supply unit;

“Régie”, “Municipal Electrical Networks”, “Preferential Rate”, “Phase 1”, “Phase 2” and “Phase 3” have the meanings as provided in DESCRIPTION OF BUSINESS - Supply of Electrical Power, Electricity Rates, Terms of Service and the Régie de l’Énergie;

| 5 | Page |

“Rio Cuarto Facility” means the facility located in the Province of Córdoba, Argentina, for which the Company entered into an eight-year lease agreement in July 2021;

“Server farms” means specialized computers often held in large warehouses where the computers, also known as Miners, validate and verify transactions on a public blockchain. Digital coins or tokens are issued by the applicable cryptocurrency network when miners solve hash functions;

“Sherbrooke Expansion” means the planned and completed construction of server farm facilities in stages in Sherbrooke, Québec;

“Stage” has the meaning as provided for in DESCRIPTION OF BUSINESS – Recently Completed Development and Future Growth Plans – Sherbrooke Expansion;

“Tranche #2 Restructuring” has the meaning as provided for in GENERAL DEVELOPMENT OF THE BUSINESS - Three-year History - Fiscal 2020 – Debt Financing;

“Tranche #3 Restructuring” has the meaning as provided for in GENERAL DEVELOPMENT OF THE BUSINESS - Three-year History - Fiscal 2020 – Debt Financing”;

“TSX” or the “Exchange” means the Toronto Stock Exchange;

“TSXV” means the TSX Venture Exchange;

“Villarrica Facility” means the Company’s 10 MW facility located in Villarrica, Paraguay;

“Volta” means 9159-9290 Québec Inc., a wholly owned subsidiary of the Company, which also operates under the name Volta Électrique Inc.; and

“Warrants” has the meaning ascribed thereto in “PRIOR SALES”.

| 6 | Page |

GENERAL

In this annual information form (“AIF”), Bitfarms Ltd., together with its subsidiaries, as the context requires, is referred to as the “Company” and “Bitfarms Canada”. All information contained in this AIF is as of March 20, 2023, unless otherwise stated.

Reference is made in this AIF to the Financial Statements, together with the auditor’s report thereon, and MD&A for Bitfarms Canada for Fiscal 2022. The Financial Statements and MD&A are available for review on the SEDAR website located at www.sedar.com.

STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This AIF contains forward-looking statements about the Company’s objectives, plans, goals, aspirations, strategies, financial condition, results of operations, cash flows, performance, prospects, opportunities, and legal and regulatory matters. Specific forward-looking statements in this AIF include, but are not limited to, statements with respect to the Company’s anticipated future results, events and plans, strategic initiatives, future liquidity, and planned capital investments. Forward-looking statements are typically identified by words such as “expect”, “anticipate”, “believe”, “foresee”, “could”, “estimate”, “goal”, “intend”, “plan”, “seek”, “strive”, “will”, “may”, “maintain”, “achieve”, “grow”, “should” and similar expressions, as they relate to the Company and its management.

Forward-looking statements reflect the Company’s current estimates, beliefs and assumptions, which are based on management’s perception of historical trends, current conditions and expected future developments, as well as other factors it believes are appropriate under the circumstances. The Company’s expectation of operating and financial performance is based on certain assumptions including assumptions about operational growth, anticipated cost savings, operating efficiencies, anticipated benefits from strategic initiatives, future liquidity, and planned capital investments. The Company’s estimates, beliefs and assumptions are inherently subject to significant business, economic, competitive and other uncertainties and contingencies regarding future events and as such, are subject to change. The Company can give no assurance that such estimates, beliefs and assumptions will prove to be correct.

Numerous risks and uncertainties could cause the Company’s actual results to differ materially from those expressed, implied or projected in the forward-looking statements. Such risks and uncertainties include:

| ● | BTC Halving events; | |

| ● | Counterparty risk; | |

| ● | the availability of financing opportunities and risks associated with economic conditions, including BTC price and BTC network difficulty; | |

| ● | the speculative and competitive nature of the technology sector; | |

| ● | dependency on continued growth in blockchain and cryptocurrency usage; | |

| ● | limited operating history and share price fluctuations; | |

| ● | cybersecurity threats and hacking; | |

| ● | controlling shareholder risk; | |

| ● | risk related to technological obsolescence and difficulty in obtaining hardware; | |

| ● | economic dependence on regulated terms of service and electricity rates; |

| 7 | Page |

| ● | increases in commodity prices or reductions in the availability of such commodities could adversely impact the Company’s results of operations; | |

| ● | permits and licenses; | |

| ● | server failures; | |

| ● | global financial conditions; | |

| ● | tax consequences; | |

| ● | environmental regulations and liability; | |

| ● | erroneous transactions and human error; | |

| ● | facility developments; | |

| ● | non-availability of insurance; | |

| ● | loss of key employees; | |

| ● | lawsuits and other legal proceedings and challenges; | |

| ● | conflict of interests with directors and management; | |

| ● | political and regulatory risk; | |

| ● | Corruption; | |

| ● | Foreign corrupt practices; | |

| ● | Political instability; | |

| ● | adoption of ESG practices and the impacts of climate change; | |

| ● | third-party supplier risks; | |

| ● | COVID-19 pandemic, and other endemic and pandemics which could occur such as SARS, Avian flu, etc.; and | |

| ● | other factors beyond the Company’s control. |

The above is not an exhaustive list of the factors that may affect the Company’s forward-looking statements. For a more comprehensive discussion of the factors that could affect the Company, refer to the risks discussed above and those contained in the section RISK FACTORS. Other risks and uncertainties not presently known to the Company or that the Company presently believes are not material could also cause actual results or events to differ materially from those expressed, implied or projected in its forward-looking statements. Readers are cautioned not to place undue reliance on these forward-looking statements, which reflect the Company’s expectations only as of the date of this AIF. Except as required by law, the Company does not undertake to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

CURRENCY

Unless otherwise indicated, all references to “$”, “US$” or “dollars” refer to United States dollars and references to CAD$ refer to Canadian dollars.

| 8 | Page |

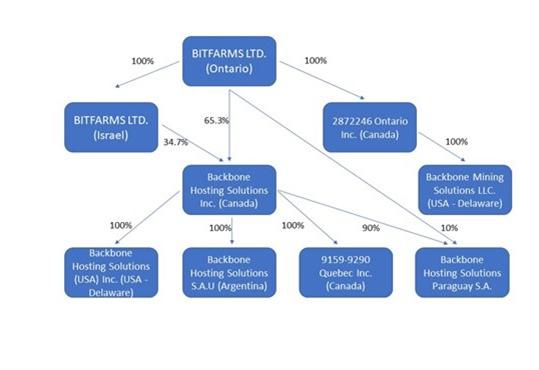

CORPORATE STRUCTURE

Name, Address and Incorporation

Bitfarms Canada was incorporated under the Canada Business Corporations Act on October 11, 2018, and continued under the Business Corporations Act (Ontario) (“OBCA”) on August 27, 2021. Bitfarms Canada has its registered and head office located at 18 King St. E, Suite 902, Toronto, ON M5C 1C4. The Company’s common shares are listed under the symbol “BITF” on the Toronto Stock Exchange (the “TSX”) and on the Nasdaq Stock Market (the “Nasdaq”) in the United States.

Intercorporate Relationships

Bitfarms Canada has the following main controlled subsidiaries:

GENERAL DEVELOPMENT OF THE BUSINESS

Three-year History

Fiscal 2020

Board and Management Changes

In Fiscal 2020, the following changes to the Company’s board of directors (the “Board”) and Management were made:

| ● | On March 11, 2020, Wes Fulford resigned as CEO and as a director of the Company and was issued 500,000 common shares in consideration for past services rendered and to satisfy certain historical entitlements. These common shares have a deemed value of $0.54 per share. |

| 9 | Page |

| ● | On April 17, 2020, Brian Howlett was appointed as a director of the Company. |

| ● | Effective May 15, 2020, Wendi Locke and Sophie Galper-Komet resigned as directors of the Company. |

| ● | On May 19, 2020, Geoffrey Morphy was appointed as a director of the Company. |

| ● | On June 1, 2020, the Company expanded the responsibility of John Rim by appointing him as Chief Operating Officer in addition to Chief Financial Officer and expanded the responsibility of Nicolas Bonta by appointing him as Chief Development Officer and Chairman. Ryan Hornby resigned as Executive Vice President and General Counsel of the Company effective June 1, 2020. |

| ● | On August 31, 2020, Geoffrey Morphy was appointed Executive Vice-President – Finance, Administration & Corporate Development. Mr. Morphy resigned his position as a director of the Company to facilitate his role as a senior officer. John Rim gave notice of his resignation as Chief Operating Officer and CFO of the Company effective September 30, 2020. In addition, Andres Finkielsztain was appointed as a director of the Company. |

| ● | On October 28, 2020, Mauro Ferrara was appointed Interim Chief Financial Officer and Corporate Secretary. |

| ● | On December 29, 2020, Nicolas Bonta was appointed Executive Chairman, Brian Howlett was appointed Lead Director, Emiliano Grodzki was appointed Chief Executive Officer, Mathieu Vachon was appointed Chief Information Officer and Geoffrey Morphy was appointed President. |

Debt Financing

The Company had previously entered into a secured debt financing facility with Dominion Capital (“Dominion”) for up to $20 million (the “Dominion Facility”) on March 14, 2019. The Dominion Facility was structured into four separate loans in tranches of $5.0 Million, with each such tranche bearing interest at 10% per annum on the initial principal balance of each tranche. The Company also agreed to issue 1,666,667 warrants (“Lender Warrants”) to purchase Bitfarms’ common shares at US$0.40 for each loan tranche drawn. In September 2020, the Company entered into an agreement with Dominion to amend its second loan tranche and third loan tranche. The amendment in respect of the second loan tranche of $5.0 Million resulted in the extension of the maturity date from the original due date of April 17, 2021, to November 1, 2021 (the “Tranche #2 Restructuring”). As consideration for the Tranche #2 Restructuring, the Company issued 1,000,000 common shares to Dominion, and reduced the term of the 1,666,667 warrants exercisable at US$0.40 from April 16, 2024, to November 1, 2021.

The amendment in respect of the third loan tranche of $5.0 Million, due June 20, 2021, resulted in this tranche being made convertible, at the option of Dominion, into common shares at a fixed conversion of US$0.59 per share, representing a premium of approximately 100% to the then current market price of the common shares (the “Tranche #3 Restructuring”). Further, pursuant to the Tranche #3 Restructuring, the previously issued 1,666,667 warrants exercisable at US$0.40 per common share, expiring on June 20, 2024, were cancelled and 1,666,667 new warrants were issued at an exercise price of US$0.304 per share with an expiry date of June 20, 2021.

| 10 | Page |

As of February 2021, the Dominion Facility has been repaid in its entirety and all Lender Warrants have been exercised.

Development of Operations

A summary of the development of computing power in Fiscal 2020 is as follows:

| Installed: | Equipment: | |

| June 2020 | Purchased: 1,847 MicroBT’s WhatsMiner M20S adding 133 PH of computing power | |

| September 2020 | Leased: 1,000 MicroBT’s WhatsMiner M31S+ adding 82 PH of computing power | |

| November 2020 | Leased: 2,000 MicroBT’s WhatsMiner M31S adding 144 PH of computing power | |

| December 2020 | Leased: 1,000 MicroBT’s WhatsMiner M31S units adding 74 PH of computing power |

On October 26, 2020, the Company announced that it signed a nonbinding memorandum of understanding (“MOU”) with a private energy producer to secure exclusive use of up to 210 MW of electricity in South America.

Fiscal 2021

Board and Management Changes

In Fiscal 2021, the following changes to the Board and Management were made:

| ● | Mathieu Vachon resigned as the Chief Information Officer and director of the Company on January 14, 2021. |

| ● | On March 31, 2021, Darcy Donelle was appointed as Vice-President of Corporate Development. |

| ● | On June 3, 2021, the Company announced Jeffrey Lucas was appointed as Chief Financial Officer of the Company effective June 14, 2021, and was issued 364,050 incentive stock options exercisable into one common share at a price of CAD$5.45 for a period of five years, pursuant to the Company’s stock option plan. |

| ● | On June 3, 2021, the Company announced Ben Gagnon was appointed Chief Mining Officer and Nathaniel Port, Director of Finance, was appointed Senior Vice President of Finance and Accounting, both effective June 1, 2021. |

| ● | On September 6, 2021, Darcy Donelle resigned as the Vice-President of Corporate Development. |

| ● | On November 1, 2021, Patricia Osorio was appointed as Vice-President of Corporate Affairs. |

| ● | On November 1, 2021, Benoit Gobeil was appointed as Senior Vice President of Operations and Infrastructure. |

| ● | On December 9, 2021, Geoff Morphy was appointed as Chief Operating Officer in addition to his role as President of the Company. |

Private Placements

On January 7, 2021, the Company closed a private placement (the “January 7, 2021 Offering”) for gross proceeds of approximately CAD$20.0 million, comprised of 8,888,889 common shares along with warrants to purchase an aggregate of up to 8,888,889 common shares at a purchase price of CAD$2.25 per common share and associated warrant. The warrants have an exercise price of CAD$2.75 per common share and an exercise period of three years. The net proceeds of the private placement were used by the Company principally to acquire additional miners, expand infrastructure, and improve its working capital position. H.C. Wainwright & Co. acted as the agent and received (i) a cash commission equal to 8.0% of the gross proceeds of the January 7, 2021 Offering and (ii) 711,111 broker warrants, with each broker warrant exercisable for one common share of the Company at a price of CAD$2.81 at any time on or before January 8, 2024.

| 11 | Page |

On January 11, 2021 the Company received notice from Dominion of its election to convert $5.0 Million, the principal amount of the third loan tranche, into an aggregate of 8,474,577 common shares at a conversion price of U.S.$0.59 per common share.. The conversion to equity took place in January 2021.

On January 13, 2021, the Company closed a private placement (the “January 13, 2021 Offering”) for gross proceeds of approximately CAD$20.0 million, comprised of 5,586,593 common shares along with warrants to purchase an aggregate of up to 5,586,593 common shares at a purchase price of CAD$3.58 per common share and associated warrant. The warrants have an exercise price of US$3.10 per common share and exercise period of three and a half years. The net proceeds of the private placement were used by the Company principally to acquire additional miners, expand infrastructure, and improve its working capital position. H.C. Wainwright & Co. acted as the agent and received (i) a cash commission equal to 8.0% of the gross proceeds of the January 13, 2021 Offering and (ii) 446,927 broker warrants, with each such broker warrant exercisable for one common share of the Company at a price of US$3.53 at any time on or before July 15, 2024.

Ten percent of the gross proceeds of the January 7, 2021 Offering and January 13, 2021 Offering were utilized to reduce the amount of the respective outstanding Loans due in March and November 2021.

On February 10, 2021, the Company closed a private placement (the “February 2021 Offering”) for gross proceeds of approximately CAD$40.0 million, comprised of 11,560,695 common shares along with warrants to purchase an aggregate of up to 11,560,695 common shares at a purchase price of CAD$3.46 per common share and associated warrant. The warrants have an exercise price of US$3.01 per common share and exercise period of three and one-half years. The net proceeds of the private placement were used by the Company principally to acquire additional miners, expand infrastructure, and improve its working capital position. H.C. Wainwright & Co. acted as the agent and received (i) a cash commission equal to 8.0% of the gross proceeds of the February 2021 Offering and (ii) 924,856 broker warrants, with each broker warrant exercisable for one common share of the Company at a price of US$3.39 at any time on or before August 12, 2024.

On May 20, 2021, the Company closed a private placement (the “May 2021 Offering”) for gross proceeds of approximately CAD$75.0 million, comprised of 14,150,940 common shares along with warrants to purchase an aggregate of up to 10,613,208 common shares at a purchase price of CAD$5.30 per common share and associated warrant. The warrants have an exercise price of US$4.87 per common share and an exercise period of three years (through May 20, 2024). The net proceeds were used by the Company principally to acquire additional miners, expand infrastructure and improve its working capital position. H.C. Wainwright & Co. acted as the agent and received (i) a cash commission equal to 8.0% of the gross proceeds of the May 2021 Offering, and (ii) 1,132,076 non-transferrable broker warrants each exercisable for one common share at a price of US$5.49 at any time on or before May 20, 2024.

Debt Financing

In April and May 2021, the Company entered into four loan agreements for the acquisition of 2,465 WhatsMiner Miners, referred to herein as “Foundry Loans #1, #2, #3 and #4”, respectively.

On December 30, 2021, the Company secured a US$100 million credit facility with Galaxy Digital LLC (the “December 2021 Debt Facility”). The December 2021 Debt Facility is a revolving, multi-draw credit facility that renews annually. The Company made an initial US$60 million draw with a six-month term at an interest rate of 10.75% per annum (the “Initial Draw”). The credit facility is secured by Bitcoin, with the minimum value of Bitcoin pledged as collateral calculated as 143% of the amount borrowed. The Initial Draw and the December 2021 Debt Facility were used for general corporate purposes and for the Company’s global growth initiatives. The December 2021 Debt Facility was fully repaid in December 2022.

Nasdaq Listing

On May 7, 2021, the Company announced that its application to list its common stock on the Nasdaq Global Market was approved by the Nasdaq.

On June 17, 2021, in connection with the Company’s listing on the Nasdaq, the Company received “Depository Trust Company” (also known as “DTC”) eligibility for the common shares.

On June 21, 2021, trading of the common shares on the Nasdaq commenced under the symbol “BITF”.

| 12 | Page |

Prospectus Filings

On March 12, 2021, the Company filed a preliminary base shelf short form prospectus.

On August 12, 2021, the Company filed a final base shelf short form prospectus (the “August SFBS Prospectus”) relating to the offering for sale of such number of securities of the Company as would result in aggregate gross proceeds of up to US$500 million, over a 25-month period.

On August 16, 2021, the Company filed a prospectus supplement to the August SFBS Prospectus qualifying the distribution of up to US$500 million Common Shares pursuant to an at-the-market offering agreement (the “ATM Agreement”) dated August 16, 2021, between the Company and H.C. Wainwright & Co.

IR Agreement

On March 12th, 2021, the Company entered into an agreement to retain the services of CORE IR, an investor relations, public relations and shareholder communications firm (the “CORE IR Agreement”). Under the Core IR Agreement, the Company agreed to pay US$15,000 per month for an initial term of twelve months and made a one-time grant to CORE IR of 15,000 incentive stock options exercisable at a price of CAD$6.35 per share for a period of two years. The CORE IR Agreement was terminated as of October 2021. See GENERAL DEVELOPMENT OF THE BUSINESS - Three-year History - Fiscal 2022 – Development of Operations.

On September 17, 2021, the Company announced the entering into of an agreement, subject to TSX Venture Exchange (“TSXV”) approval, to retain the services of LHA Investor Relations, to handle the Company’s public relations and shareholder communications (the “LHA IR Agreement”). Under the LHA IR Agreement, the Company agreed to pay US$20,000 per month for an initial term of six months.

Digital Asset Management Program

In early January 2021, the Company implemented a program (the “Digital Asset Management Program”), pursuant to which the Company added approximately 3,201 BTC to its balance sheet during the year ended December 31, 2021. See DESCRIPTION OF BUSINESS - Business and Strategy - Digital Asset Management Program .

Development of Operations

A summary of the development of computing power in Fiscal 2021 is as follows:

| Installed: | Equipment: | |

| Q1 2021 | Leased: 3,000 MicroBT’s WhatsMiner M31S+ machines, adding approximately 240 PH of computing power | |

| Q1 2021 | Acquired: 1,500 MicroBT’s WhatsMiner M31S machines, adding approximately 120 PH of computing power | |

| January 2022 – December 2022 | Entered into agreements to acquire 48,000 MicroBT’s WhatsMiner machines, adding what was expected to be approximately 5.0 EH of computing power. In December 2022, the Company negotiated its miner purchasing agreements by extinguishing the remaining 24,000 MicroBT commitment, without penalty. | |

| June 2021 | Acquired: 1,500 MicroBT M31S+ and 700 Bitmain S19j machines, adding 183 PH of computing power | |

| Q2 – Q4 2021 | Acquired: 2,465 WhatsMiner M30S Bitcoin mining machines, adding 133 PH of production | |

| Q2 – Q3 2021 | Acquired: 1,996 MicroBT’s WhatsMiner M31S machines, adding approximately 120 PH of computing power | |

| Q3 – Q4 2021 | Acquired: 6,600 Bitmain S19j Pro Antminer machines, adding approximately 660 PH of computing power |

On March 2, 2021, the Company entered into a hosting agreement in the United States (the “Hosting Agreement”). Pursuant to the Hosting Agreement, the Company delivered older generation equipment already owned and used by the Company, for hosting at one of the host’s facilities located in the United States in order to free up capacity at the facilities (namely, the facilities at Farnham, Saint-Hyacinthe, Cowansville, Magog, and De la Pointe as each is described herein) for more efficient and profitable mining equipment. The Hosting Agreement was replaced by the July 2021 Hosting Agreement, as defined herein.

On July 3, 2021, the Company entered into 3 purchase agreements for miners with affiliated companies of MicroBT, pursuant to which, the Company purchased 48,000 Miners to be delivered throughout Fiscal 2022 (the “2021 Miner Purchase Agreements”) – see Material Agreements.

On September 17, 2021, the Company announced entering into an agreement, subject to Exchange approval, to retain the services of LHA Investor Relations, to handle the Company’s public relations and shareholder communications (the “LHA IR Agreement”). Under the LHA IR Agreement, the Company agreed to pay US$20,000 per month for an initial term of six months.

| 13 | Page |

Quebec Operations

On September 7, 2021, the Company entered into an agreement with the City of Sherbrooke by which the Company’s operations at the De la Pointe Property were to be replaced by new, higher efficiency facilities with next-generation mining equipment optimized for higher output levels and lower power consumptions. On October 27, 2021, the Company announced the construction of two new high power production facilities in Sherbrooke with a combined capacity of 78 MW, expected to be completed in the second quarter of 2022 – see Sherbrooke Expansion.

In September and October 2021, the Company entered into lease agreements for two new facilities in Sherbrooke: “Leger” and “The Bunker”, respectively. See DESCRIPTION OF BUSINESS - Sherbrooke Expansion.

On October 4, 2021, the Company announced that it had completed its planned expansion in Cowansville, Quebec, consisting of the replacement of the original 4 MW facility that was operational since 2017 with an entirely newly constructed 17 MW facility. The Company also announced that it had installed 450 new Bitmain S19j Pro miners at the Cowansville facility, in addition to other used miners, adding approximately 100 PH/s of production.

Washington Expansion

On November 9, 2021, the Company acquired a bitcoin mining production facility used for providing hosting services in Washington State, US (the “November 2021 Washington Acquisition”). The Company entered into a hosting agreement for 12 MW with the seller in July 2021 (the “July 2021 Hosting Agreement”), replacing its previous hosting agreements in the United States under which 4,000 Bitmain S19j Pro miners with a capacity of 400 PH/s were installed at the facility. The July 2021 Hosting Agreement terminated upon the closing of the November 2021 Washington Acquisition.

South America Expansion

On April 19, 2021, the Company entered into an eight-year power purchase agreement with a private power producer in Argentina to secure up to 210 MW of electricity with various rate mechanisms, further to the Company’s plan to pursue the development of a Bitcoin Mining facility in Argentina. See DESCRIPTION OF BUSINESS - Argentina Expansion.

On October 7, 2021, the Company announced that it had entered into engineering, procurement and construction contracts with Proyectos y Obras Americanas S.A.(“PROA”) and Dreicon, as the owner’s engineer to commence construction of a 210 MW production facility in Argentina.

On September 8, 2021, the Company announced that it had signed a 5-year lease and an annually renewable power purchase agreement to secure up to 10 MW of green hydro electrical capacity at approximately US$3.6 cents per kilowatt hour in Paraguay In December 2021, the Company completed the construction of a 10 MW facility in Paraguay (the “Villarrica Facility”). See DESCRIPTION OF BUSINESS - Paraguay Expansion.

Fiscal 2022

Board and Management Changes

In Fiscal 2022, the following changes to the Board and Management were made:

| ● | On February 14, 2022, the Company announced the addition of three executives for newly created positions. Philippe Fortier was appointed Vice President – Special Projects, Andrea Keen Souza was appointed Vice President – Human Resources, and Stephanie Wargo was appointed Vice President – Marketing & Communications. |

| ● | On May 15, 2022, Nathaniel Port resigned as Senior Vice President of Finance and Accounting. |

| 14 | Page |

| ● | On May 16, 2022, Marc-André Ammann was appointed as Vice President – Finance & Accounting and on May 24, 2024, Paul Magrath was appointed as Vice President – Taxation. |

| ● | On November 17, 2022, the Company announced the addition of Edie Hofmeister to the Board, bringing the total number of directors to six. |

| ● | On December 29, 2022, the Company announced the promotion of Geoffrey Morphy from President and Chief Operating Officer to the position of President and Chief Executive Officer. Emiliano Grodzki, the Company’s previous CEO, resigned as CEO and remained a member of the board of directors. The Company also announced that Nicolas Bonta shifted from the position of Executive Chairman to the role of Chairman of the Board of Directors. |

At-the-market equity

For the Fiscal year 2022, the Company issued a total of 29,324,000 common shares, in exchange for US$54.1 million of net proceeds through the at-the-market equity program.

Debt Financing

On February 24, 2022, the Company secured a US$32 million credit facility with a private lender (the “February 2022 BlockFi Loan Facility”). The February 2022 BlockFi Loan Facility has a 24-month term at an interest rate of 14.5 % per annum and is secured by approximately 6,100 Bitmain S19j Pro miners. The February 2022 BlockFi Loan Facility was used for general corporate purposes and for the Company’s global growth initiatives.

On March 31, 2022, the Company made an additional draw of US$40 million from its December 2021 Debt Facility.

On June 17, 2022, the Company entered into an equipment financing agreement with NYDIG ABL LLC (“NYDIG”) which provided for initial funding of US$37 million at an interest rate of 12% per annum (the “June 2022 NYDIG Financing”). The June 2022 NYDIG Financing is collateralized by miners 10,395 WhatsMiner M30S Miners at Leger and the Bunker, funded as the assets are installed and become operational.

On June 17, 2022, the Company announced that it reduced the December 2021 Debt Facility from US$100 million to US$66 million, funded through the sale of 1,500 bitcoin.

On June 30, 2022, the Company amended its December 2021 Debt Facility and extended its maturity date to October 1, 2022.

On September 29, 2022, the Company amended its December 2021 Debt Facility and extended its maturity date from October 1, 2022, to December 29, 2022, and reduced the collateral requirement from 143% to 135%, for a maximum of US$40 million at an interest rate of 11.25%. The December 2021 Debt Facility was fully repaid in December 2022.

As of December 31, 2022, the Foundry Loan #1 entered into on April 2021 matured and was fully repaid.

TSX Listing

On April 7, 2022, the Company announced that it had received final approval for the up listing of its common shares on the TSX. The Common Shares commenced trading on the TSX under the symbol “BITF” effective market open on April 8, 2022, and were concurrently delisted from the TSXV.

| 15 | Page |

NASDAQ Listing

On December 14, 2022, the Company announced that it has received a written notice from Nasdaq indicating that, for the prior thirty days, the bid price for the Common Shares had closed below the minimum US$1.00 per share requirement for continued listing on the Nasdaq under Nasdaq Listing Rule 5550(a)(2). In accordance with Nasdaq Listing Rule 5810(c)(3)(A), the Company was provided an initial period of 180 calendar days (until June 12, 2023) to regain compliance.

IR Agreement

In March 2022, the Company extended the agreement LHA IR Agreement for an indefinite period, under the same terms.

Digital Asset Management Program

In January 2022, the Board authorized management to purchase 1,000 BTC for US$43.2 million, increasing the Company’s Bitcoin holdings by approximately 30%.

On June 21, 2022, the Company announced that it had adjusted its Digital Asset Management Program to improve liquidity and strengthen its balance sheet. During the second and third quarter of 2022, the Company sold 3,670 in collateral to partially pay the December 2021 Credit Facility. During the same period the Company also sold 2,275 BTC in treasury to manage liquidity levels. Since August 2022, the Company has been selling almost all of its daily Bitcoin mining production, and holds 405 BTC as of December 31, 2022, valued at approximately US$6.7 million based on a BTC price of approximately US$16,500 as of December 31, 2022.

Development of Operations

A summary of the development of computing power in Fiscal 2022 is as follows:

| Installed: | Equipment: | |

| Q1 2022 | 4,800 MicroBT WhatsMiners | |

| Q2 2022 | 11,600 MicroBT WhatsMiners | |

| Q3 2022 | 7,800 MicroBT WhatsMiners | |

| Q4 2022 | 1,600 MicroBT WhatsMiners |

In August 2022, to better align the number of Miners on hand with the infrastructure capacity available to utilize the Miners, the Company amended the Miner Purchase Agreements, signed in July 2021, with deliveries originally expected to be completed during Fiscal Year 2022, to postpone into 2023, without penalty, the remaining delivery of and payment for certain remaining equipment purchases. In December 2022, the Company made a second amendment of this agreement for which 28,000 miner deliveries had already arrived in 2022. Following the amendment, the obligation to acquire the remaining 20,000 miner was cancelled without penalty.

Quebec Operations

On March 17, 2022, the Company began operations in Phase one of the Bunker (as defined herein). See DESCRIPTION OF BUSINESS - Recently Completed Development and Future Growth Plans - Sherbrooke Expansion - The Bunker.

On March 11, 2022, the Company acquired a building in Sherbrooke Quebec expected to accommodate 18 MW of electrical infrastructure (“Garlock”) as described in DESCRIPTION OF BUSINESS - Recently Completed Development and Future Growth Plans - Sherbrooke Expansion - Garlock.

On April 6, 2022, the Company began operations at Leger (as defined herein) in Sherbrooke, Quebec, bringing the total operational hashrate to 3 EH/s. See DESCRIPTION OF BUSINESS – Recently Completed Development and Future Growth Plans - Sherbrooke Expansion - Leger.

| 16 | Page |

On July 28, 2022, the Company announced that it had completed the second phase of its expansion of the Bunker, bringing the total operational hashrate to 3.8 EH/s.

During December 2022, the remaining portions of the Bunker (6 MW) and Garlock (12 MW) farms in Sherbrooke, Quebec had been energized, reaching their full capacity of 48 MW and 18 MW, respectively, which represented the completion of the Sherbrooke Expansion (as herein defined).

On December 16, 2022, the Company announced that it had completed the sale of the De la Pointe Property, receiving US$3.6 million in net proceeds.

Washington Expansion

During the second quarter of 2022, the Company added 3 MW of electrical infrastructure and is currently operating approximately 20 MW of electrical infrastructure with the majority of the Company’s Antminer S19j Pro Miners generating approximately 600 PH/s in this facility. The Company’s power supplier has provided a preliminary indication that the next 6 MW of in-process applications are expected to be energized in the first half of 2023 with the remaining 3 MW of in-process applications estimated to be energized after 2027 due to the nearby substation being at capacity.

South America Expansion

In January 2022, the Villarrica Facility became operational with the installation of 2,900 of the Company’s older generation Miners relocated from Quebec and generating approximately 125 PH/s. On February 1, 2022, the Company announced commencement of operations at its 10 MW farm in Paraguay, increasing the total farms operated by the Company from six to seven, and total mining capacity to 116 MW. See GENERAL DEVELOPMENT OF THE BUSINESS – Three-year History - Fiscal 2023 - South America Expansion.

On September 19, 2022, the Company announced commencement of operations at the first 50 MW warehouse in Argentina, increasing the total number of farms operated by the Company to ten and the total operational hashrate to 4.1 EH/s.

Fiscal 2023

Board and Management Changes

In Fiscal 2023, until March 20, 2023, the following changes to the Board and Management have been made:

| ● | On January 1, 2023, Jeff Gao was appointed as Vice President - Risk management. |

Debt Financing

In January 2023, the principal amount of the remaining Foundry Loans #2, #3 and #4, entered into on May 2021, were fully repaid before their maturity date without prepayment penalty for $0.8 million.

During February 2023, the Company negotiated a settlement of its February 2022 BlockFi Loan Facility with an outstanding debt balance of $20.3 million for a payment of $7.8 million in cash. Upon settlement, the 6,100 Bitmain S19j Pro miners that secured the February 2022 BlockFi Loan Facility are unencumbered.

General

During February 2023, the Company modified a lease agreement previously entered on September 18, 2020 with Reliz Ltd. in order to settle an outstanding lease liability of $0.4 million for a payment of $0.1 million.

South America Expansion

In January 2023, all the older generation Miners in the Villarrica Facility were replaced with approximately 2,900 new M30S WhatsMiner Miners generating approximately 290 PH/s, a 165 PH/s increase compared to the hashrate that was being produced by the older generation Miners. The Company has reached an agreement to sell the older generation Miners to a third party for approximately $0.2 million.

Current Computing Power

The Company’s total operating hashrate is approximately 4.7 EH/s as of the March 20, 2023.

| 17 | Page |

DESCRIPTION OF BUSINESS

Description of the Business

The Company’s primary business is the mining of cryptocurrency. Through its subsidiaries, the Company owns and operates server farms, comprised of computers (referred to as “Miners”) designed for the purpose of validating transactions on the Bitcoin (“BTC”) Blockchain (referred to as “Mining”). Bitfarms Canada generally operates Miners 24 hours a day producing computational power (measured by hashrate) which it sells to Mining Pools (as defined herein), for a formula-driven rate commonly known in the industry as Full Pay Per Share (“FPPS”). Under FPPS, pools compensate Mining Companies for their hashrate based on what the pool would be expected to generate in revenue for a given time period if there was no randomness involved. The fee paid by a Mining Pool to Bitfarms Canada for its hashrate may be in cryptocurrency, U.S. dollars, or other currency. Bitfarms Canada accumulates the cryptocurrency fees it receives or exchanges them for U.S. dollars, as determined to be needed, through reputable and established cryptocurrency trading platforms. Mining Pools generate revenue by Mining with purchased hashrate through the accumulation of block rewards and transaction fees issued by the BTC network. Mining Pools are purchasing hashrate and take on risk with the aim to mine more blocks than they should in a given time period in pursuit of profit.

Prior to January 2021, the Company routinely exchanged cryptocurrencies mined into U.S. dollars through reputable cryptocurrency trading platforms. At the beginning of Fiscal 2021, the Company implemented the Digital Asset Management Program under which the Company decided how many mined Bitcoin would be held by the Company through its custodians. See DESCRIPTION OF BUSINESS - Principal Market Overview - Digital Asset Management Program.

As of March 20, 2023, Bitfarms Canada operates ten total server farms around the world. Seven server farm facilities are located in Québec, Canada, with electrical infrastructure capacity of 148 MW for Mining Bitcoin; one server farm facility is located in Washington State, United States, with operational electrical infrastructure capacity of 20 MW and expansion opportunities up to 24 MW; one server farm facility is located in Villarrica, Paraguay, with electrical infrastructure capacity of 10 MW; and one server farm facility is located in Argentina, with current operational electrical infrastructure capacity of 50 MW, of which 10 MW are currently operating. The Company has contracts securing an aggregate of 160 MW, 10 MW and 24 MW of hydro-electric green energy in Quebec, Paraguay, and Washington, respectively, and up to 210 MW of natural gas energy in Argentina. In addition, Bitfarms Canada owns proprietary software, known as the MGMT System, that is used to control, manage, report and secure mining operations. The MGMT System scans and reports the location, status, computing power and temperature of all Miners at regular intervals to allows the Company to monitor performance and maximize up-time. The MGMT System was substantially upgraded during 2022 and is continually getting updated to enhance its features and improve its functionality. The revised system is referred to as MGMT-2.

Volta provides electrician services to both commercial and residential customers in Québec, while assisting Bitfarms Canada in building and maintaining its server farms in Quebec.

Cryptocurrency Background

Bitcoin Blockchain technology was developed around 2009 by a pseudonymous person or organization known as Satoshi Nakamoto. It is often defined as a distributed ledger, or database, with decentralized control. The types of databases that could be implemented using blockchain technology are broad and include, among others, databases similar to a bank ledger that record statements of accounts or transactions, or any other digital record of asset ownership, such as an identity system, land registry or even the rights and obligations defined in a contract. In the traditional centralized ledger models, a master version of such ledgers is controlled by a bank, government or a trusted third party. Disputes are resolved by checking the master version, through a manual and often redundant reconciliation process. In the decentralized blockchain model, a master ledger is not stored in one place or controlled by one entity. Every counterparty on the network receives an identical real-time copy of the ledger; the data in the ledger is tamper-proof using cryptography; new states of the ledger are agreed upon by consensus among all parties.

The shared ledger is made tamper-proof using a cryptographic technique called hashing. A hashing algorithm is a mathematical transformation function with two key properties. First, it accepts any alphanumeric dataset as an input and produces a unique 256-bit code as an output. Second, the smallest change in the dataset results in a significant change in the unique code. Any tampering of the dataset can be detected by re-hashing the data and checking for a change in the unique code. Any user that runs the hash algorithm on the same strings will derive the same unique code. Consequently, the data on the distributed ledger can be run through a series of hash algorithms to create a unique code which ensures the entire ledger is immutable. Whenever a new set or block of transactions is added to the ledger, it is appended with the code from the prior state of the ledger before it is hashed. This chain links both states of the ledger by combining them into a single unique code. Tampering of any historical state of the ledger can be automatically detected by the blockchain network. The historical state of the ledger can be changed if control of more than 50% of the network is obtained; however, in the case of widely held cryptocurrencies with non-trivial valuations, it is likely economically prohibitive for any actor or group of actors acting in concert to obtain the requisite control of more than 50% of the network.

| 18 | Page |

Mining

The process by which cryptocurrency coins or tokens are created and transactions are verified is called mining. A user or Miner operates a publicly distributed mining client, which turns the user’s computer into a “node” on the network that validates blocks. In order to add blocks to the Bitcoin blockchain, a miner must map an input data set (i.e., the blockchain, plus a block of the most recent transactions and an arbitrary number called a “nonce”) to a desired output data set of a predetermined length using the SHA256 cryptographic hash algorithm. Each unique block can only be solved and added to the blockchain by one miner. As more miners join the network and its processing power increases, the network adjusts the complexity of the block solving equation to maintain a predetermined pace of adding a new block to the blockchain approximately every ten minutes. The prevailing level of complexity in the context of cryptocurrency mining is often referred to as the “difficulty”. See DESCRIPTION OF BUSINESS - Principal Market Overview - RISK FACTORS - Cryptocurrency Network Difficulty and Impact of Increased Global Computing Power.

A Miner’s proposed block is added to the blockchain once a majority of the nodes on the network confirms the Miner’s work which is targeted to occur every ten minutes. Miners that are successful in adding a block to the blockchain are automatically awarded coins or tokens (referred to as block rewards) for their effort plus any transaction fees paid by transferors whose transactions are recorded in the block. This reward system is the method by which new coins enter into circulation to the public.

Principal Market Overview

Business and Strategy

The Company’s strategy consists of mainly constructing and operating server farms using a geographically diversified portfolio of low-cost energy sources. In support of the strategy, the Company has sourced electrical power from Hydro-Québec, Hydro-Sherbrooke, Hydro-Magog and predominantly power grid operators in Washington state and Paraguay. Power from these sources is derived from clean hydroelectricity as opposed to, for instance, coal-fired or gas-fired plants. Hydro-electric power is generated through exploitation of the natural water cycle, which is renewable, sustainable, and abundant owing to the natural geography of the Province of Québec, Washington State and Paraguay. The Company has also entered into an agreement with a private energy producer to secure exclusive use of up to 210 MW of natural gas-powered electricity in Argentina. As a result of these efforts, the management of the Company has developed a business model utilizing low-cost power capacity and a supply of computer hardware from leading manufacturers.

The Company’s server farms are operated by the MGMT-2 System, a proprietary software suite comprised of three operating programs that control, manage, report and secure the operation. One program in the suite of software is the central point of the infrastructure, and saves the status of the Company’s Miners into a database at 30 second intervals. A second program in the suite connects directly to the first program to do the scanning of all the Company’s Miners and return the data for analysis and storage. A third program in the suite displays the data retrieved by the other programs in readable and digestible format that assists operators in identifying machines issues. The software is configured to notify operators of profitability conditions, enabling operators to manually optimize margins under different economic conditions through optimizing the hashing performance and energy consumption of the Miners. Additionally, the Company has an automated cooling management system which autonomously controls exhaust fans to maintain the optimal temperature of the Miners at the locations in which they are operated, based on prevailing ambient conditions. See DESCRIPTION OF BUSINESS - Hardware and Software.

Digital Asset Management Program

The Company’s Digital Asset Management Program commenced in early January 2021 following the implementation of internal controls, counter-party risk assessments and custody arrangement reviews. Rather than selling all Bitcoin mined at then-prevailing market rates, the Company decided to retain Bitcoin through its custodial arrangements.

Retaining Bitcoin allowed the Company flexibility in deciding when or whether to sell the assets based on prevailing market conditions. With the decrease in Bitcoin prices during late 2021 and 2022, coupled with the high price of mining hardware, the Company converted a portion of its cash position into Bitcoin with a purchase of 1,000 Bitcoin during the first week of 2022. In August 2022, attending to market conditions, the Board approved the sale of the Company’s daily Bitcoin production to reduce indebtedness and increase financial flexibility.

Bitfarms Canada has implemented internal controls and custody arrangements to minimize the risk of loss or theft of the retained Bitcoin. The Company retains Coinbase Trust Company LLC as its third-party custodian. Coinbase Trust Company LLC is a US-based fiduciary and qualified custodian under New York Banking Law and is licensed by the State of New York to custody digital assets. See DESCRIPTION OF BUSINESS - Custody of Crypto Assets.

| 19 | Page |

Current Mining Operations

The following table sets out summary information regarding the Current Facilities as at March 20, 2023.

| Location | Power Capacity (Megawatts) | Hash-power per second | Property Information | Primary

Energy Source | ||||

| Farnham, Québec, Canada | 10 | 200 Petahash | Leased | Hydroelectric | ||||

| Saint-Hyacinthe, Québec, Canada | 15 | 380 Petahash | Leased | Hydroelectric | ||||

| Cowansville, Québec, Canada | 17 | 400 Petahash | Leased | Hydroelectric | ||||

| Magog, Québec, Canada | 10 | 210 Petahash | Leased | Hydroelectric | ||||

| The Bunker, Sherbrooke, Québec, Canada | 48 | 1300 Petahash | Leased | Hydroelectric | ||||

| Leger, Sherbrooke, Quebec, Canada | 30 | 750 Petahash | Leased | Hydroelectric | ||||

| Garlock – Sherbrooke, Québec, Canada | 18 | 410 Petahash | Owned | Hydroelectric | ||||

| Washington, United States | 20 | 600 Petahash | Owned & Leased | Hydroelectric | ||||

| Villarrica, Paraguay | 10 | 290 Petahash | Leased | Hydroelectric | ||||

| Rio Cuarto, Argentina – Warehouse #1 | 50 | 230 Petahash | Leased | Natural Gas |

Recently Completed Development and Future Growth Plans

The Company has described its recently completed and future expansion plans below under the sections, “Sherbrooke Expansion”, “Argentina Expansion”, “Paraguay Expansion”, and “Washington Expansion”.

The estimated costs and timelines to achieve Future Growth plans may change based on, among other factors, the prevailing price of Bitcoin, network difficulty, supply of cryptocurrency mining equipment, supply of electrical and other supporting infrastructure equipment, construction materials, currency exchange rates, the impact of COVID-19 on the supply chains described above and the Company’s ability to fund the initiatives. The Company’s future growth plans are reliant on a consistent supply of electricity at cost-effective rates, see the Economic Dependence on Regulated Terms of Service and Electricity Rates Risks of this AIF for further details.

Sherbrooke Expansion

On March 8, 2018, the Company announced a 96-megawatt power contract in the municipality of Sherbrooke, Québec, for two new server farm facilities (herein referred to as the “Sherbrooke Expansion”). The facilities in Sherbrooke consisted of a 78,000 sq. foot facility (the “De la Pointe Property”), and a 36,000 sq. foot facility (“Leger”). On February 11, 2019, the land where Leger was going to be built was sold for CAD$1,750,000 and as part of the agreement reached with the buyer, a real estate developer, the buyer agreed to construct a purpose-built addition to the building for crypto-mining that would be leased to Bitfarms Canada and allow it to realize net savings in its overall future buildout costs for the Sherbrooke Expansion while also providing immediate working capital from the proceeds of the building sale.

De la Pointe Property

The Company successfully completed Stages 1 and 2 of the Sherbrooke Expansion at the De la Pointe Property representing 30 MW of electrical infrastructure, which was operational from 2019 to 2022. In response to complaints concerning noise at the De la Pointe Property and indications from Sherbrooke municipal officials that they were reviewing applicable regulations, the Company met with community residents and city officials on several occasions during 2020 and 2021. In an effort to address community concerns, the Company constructed a sound barrier wall at a cost of approximately $0.3 million in 2020 and invested $0.7 million to install quieter exhaust structures and fans as well as other sound mitigating measures including real-time sound monitoring equipment and feedback channels for residents to communicate directly with the Company.

In September 2021, the Company reached an agreement with the City of Sherbrooke to gradually retire the De la Pointe Property. Under the agreement, the Company agreed to reduce its consumption at the De la Pointe Property to 18 MW at the earlier of the completion of 66 MW of new electrical infrastructure elsewhere in the City of Sherbrooke, or May 31, 2022. The Company engaged to entirely relocate its operations from the De la Pointe Property at the earlier of the completion of 80 MW of new electrical infrastructure in the City of Sherbrooke, or February 28, 2023. In addition, the Company retained the option to sell the land and building housing the De la Pointe Property to the City of Sherbrooke for approximately US$2.3 million (CAD$3.0 million). Subject to a first right of refusal, the agreement did not restrict the ability of the Company to sell the building to a third party other than the City of Sherbrooke. In December 2022, the Company finished the decommissioning of the De la Pointe Property and sold the De la Pointe Property to Société de transport de Sherbrooke US$3.6 million in net proceeds.

Leger

In September 2021, the Company entered into a lease agreement for the purpose of building Leger. Leger, representing 30 MW of capacity, located in an industrial area of the city of Sherbrooke, and including modern and effective sound mitigation mechanisms, was completed in June 2022 and became fully operational in August 2022. Leger accommodates approximately 7,500 new generation Miners and produces 750 PH/s.

| 20 | Page |

The Bunker

In 2021, the Company entered into a lease agreement for the Bunker, an existing building in Sherbrooke capable of housing up to 48 MW of electrical infrastructure, which was completed in three Stages:

| ● | Phase one, representing 18 MW, was constructed in a pre-existing building. Internal infrastructure work began in Q4 2021 with the first 12 MW becoming operational in March 2022, and the remaining 6 MW started operating by June 2022. |

| ● | Phase two, representing 18 MW, is in a portion of the building that was originally under construction. Internal infrastructure work began in Q1 2022 and on July 28, 2022, the Company announced that it had completed the second phase of its expansion of the Bunker, providing an additional 18 MW of capacity. |

| ● | Phase three, representing the remaining 12 MW, is in a portion of the building that was originally under construction. It was completed in November 2022 and fully energized in December 2022. |

Garlock

In March 2022, the Company acquired an existing building in Sherbrooke (“Garlock”) at a cost of approximately $1.8 million and the issuance of 25,000 common share purchase warrants to the seller. Garlock was completed in two phases and began operations during November and December 2022, representing 18 MW of electrical infrastructure at a cost of $3.4 million, excluding the cost of the property. Garlock, combined with the Bunker, replaced the De la Pointe Property and, along with Leger, fully utilizes the Company’s power contracts totaling 96 MW in the municipality, in accordance with the Company’s agreement with the City of Sherbrooke reached in September 2021.

As of December 31, 2022, the Company employed 77 team members in Canada.

Argentina Expansion

In April 2021, the Company entered into an eight-year power purchase agreement for up to 210 MW with a private Argentinian power producer in the city of Rio Cuarto, Province of Cordoba (the “Power Producer”), with an electricity cost of US$0.022 per kilowatt-hour for the first four years, up to a maximum amount of 1,103,760 megawatt hours per year (on a pro-rata basis for a consumption of 210 MW), and is subject to certain adjustments, variable pricing components and consumption limitations. The pricing on the remaining four years of the eight-year energy contract will be determined by a formula that is largely dependent on natural gas prices. The agreement also allows for the Power Producer to renegotiate the rate if the ratio of the exchange rate under the blue-chip mechanism used in Argentina to the official exchange rate is less than 1.50. For further details, refer to DESCRIPTION OF BUSINESS - Supply of Electrical Power, Electricity Rates, Terms of Service and the Régie de l’Énergie and RISK FACTORS - Economic Dependence on Regulated Terms of Service and Electricity Rates Risks.

In July 2021, the Company entered into an eight-year lease agreement, comprising annual payments of approximately $0.1 million, with the Power Producer to lease land within the Power Producer’s property for the mining facility’s construction and operation in the Province of Cordoba, Argentina (the “Rio Cuarto Facility”).

In September 2021, the Company entered into a contract with PROA, to provide engineering, procurement, and construction services for the Argentina facility. PROA specializes in utility-grade electrical infrastructure and civil construction with relevant expertise in the design and construction of electrical interconnections, high voltage electrical lines, and transformers needed for operations of the size of the planned Argentina facility. Pursuant to an agreement signed with LPZ Hosting S.A.S (“LPZ”), LPZ is responsible for the detail engineering, purchasing management and execution of louvers, sound and noise system, electric installation, data network installation, air conditioning system, air extraction and filter systems, racks, closed-circuit television “(CCTV)”, fire detection and extinguisher system as well as installation of all low voltage works. Ingenia Grupo Consultor and Gieco S.A. (“Ingenia”) were retained as a consortium group responsible for the construction of provisional high voltage powerline and transformer station as well as the expansion of the 132 KW public bars of the power plant. Ingenia, under the supervision of LPZ, was also selected to carry out electrical data and CCTV assembly work for the first warehouse. The Company has also engaged Dreicon S.A. as an independent engineering firm to oversee construction, quality control and project milestones for the Company’s projected buildout schedule.

The Rio Cuarto Facility, if fully developed, is expected to be built as four separate warehouse style buildings with a capacity to accommodate over 55,000 new generation Miners and be capable of producing approximately 5.5. EH/s. The first warehouse, which was included in the capacity needed to reach the corporate 5.0 EH/s target for 2022, represents approximately 50 MW of incremental infrastructure capacity.

On September 19, 2022, the Company announced it has initiated production in the first 10 MW module of the First Warehouse at the Rio Cuarto Facility, increasing the total number of farms operated by the Company to ten, and the total operational hashrate to 4.1 EH/s.

| 21 | Page |

On November 1, 2022, the Company reported that Argentina was wrestling with high inflation, currency devaluation and a significant debt burden. To alleviate concerns about a drain on the Argentina Central Bank’s foreign currency reserves, trade approval for the importation of most goods, including Mining and IT equipment, had been imposed in the Country, adversely affecting the Company’s ability to import in Argentina the additional Miners needed to operate the first warehouse at its full capacity of 50 MW. Additionally, it was also announced that the Power Producer was awaiting approval of its final operation permit. In the meantime, the Rio Cuarto Facility is drawing power during the start-up and commissioning phase from the provincial electrical utility at a higher cost than the expected contracted cost of power under the agreement with the Power Producer. The adverse impact of recent geopolitical events on natural gas prices, as well as new importation restrictions, as detailed below, are leading the Company to revise the timing to fully utilize the infrastructure built in the first 50 MW warehouse and to reassess the timing of its build-out and deployment of further production facilities at the Rio Cuarto location.

The Company planned to deploy a significant portion of its order of 48,000 Miners at this facility, with pending deliveries currently expected to arrive during the first six months of 2023.

On January 3, 2023, the Company announced that it had completed construction of the first 50-MW warehouse in the Rio Cuarto Facility and is expected to be fully commissioned during the first six months of 2023.

In February 2023, Management approved a temporary cessation of the development of the second warehouse until the power permit is obtained, the importation limitations are resolved, and natural gas prices stabilize at an acceptable level. In light of these circumstances, the Company is not in a position to determine when or if construction of warehouse 2 will resume and construction of warehouses 3 and 4 will commence.

As of December 31, 2022, the Company has placed deposits of $8.8 million and $4.3 million with suppliers for existing and additional construction costs and for Blockchain Verification and Validation Equipment and electrical components, respectively. The Company has also acquired $51.6 million of property, plant and equipment, incurred 0.3 million of expenditures relating to design and feasibility studies and recorded cumulative gains on disposition of marketable securities of $57.8 million associated with the mechanism to convert funds into Argentine Pesos for disbursements.

As of December 31, 2022, the Company employed 31 team members in Argentina.

Paraguay Expansion

During the year ended December 31, 2021, the Company entered into an annually renewable 10 MW power purchase agreement with the city of Villarrica electricity distribution company, Compañía Luz y Fuerza S.A. (“CLYFSA”), at an effective electricity cost of $0.036 per kilowatt hour. The Company also entered into a five-year lease agreement with a third party, consisting of monthly payments of $20,000, beginning August 1, 2021, to lease land where the Villarrica Facility was constructed. The construction of the facility, at a cost of $1.1 million, was completed in December 2021.

| 22 | Page |

In January 2022 2,900 of the Company’s older generation Miners were installed at the Villarrica Facility, capable of producing approximately 125 PH/s.

On July 18, 2022, the Paraguayan Congress approved a bill regulating the mining, trading, intermediation, exchange, transfer, custody and administration of crypto-assets and instruments that would allow control of crypto-assets. The proposed legislation aimed to create an attractive regulatory environment within the country through the establishment of a straightforward licensing regime that clearly establishes the requirements to operate crypto-assets activities in the Country. Approved by both chambers, the law has been submitted to the executive branch, where the President has the power to approve or veto it. On August 30, 2022, the law was vetoed by the President and was returned to the congress to be discussed again. It is unknown if a new law will be approved and when. The absence of specific law regarding crypto assets has not impacted the Company’s current operations in the country.

On September 16, 2022, the executive branch issued decree No. 7824/22 by which the National Electricity Administration (“ANDE”) was requested to adopt complementary and temporary regulatory measures to adjust the variables corresponding to the electricity rates aimed at special intensive consumption sectors. In this context, ANDE, through resolution No. 7824/22, dated October 4, 2022, created the Special Intensive Consumption Group, which includes supplies at very high voltage (220 kV), high voltage (66 kV), medium voltage (23 kV) at the substation and at the line, and set up the tariffs until December 2027. This Special Intensive Consumption group applies, among others, to crypto asset mining activities. While the new ANDE tariffs have no impact in our current activities in Paraguay as our contract is with the local supplier CLYFSA as detailed above, the impact, if any, on the Company’s future operations cannot be determined at this time.

During December 2022, ANDE, as part of a local development plan, installed a new transformer in the city of Villarrica which is expected to be operational in the first half of 2023. The new transformer will help ensure fewer energy curtailments to the Company’s facility as well as to nearby residents.

In January 2023, all of the older generation miners in the Villarrica Facility were replaced with approximately 2,900 new M30S WhatsMiner Miners generating approximately 290 PH/s, a 165 PH/s increase compared to the hashrate that was being produced by the older generation Miners. The Company has reached an agreement to sell the older generation Miners to a third party for approximately $0.2 million.

Washington Expansion

On November 9, 2021, the Company completed the acquisition of a facility in Washington State, consisting of 12 MW of hydro-electric power purchase agreements, an additional 9 MW of in-process applications for expanded power-purchase agreements, transformers with 17 MW of capacity, land, buildings, electrical distribution equipment and a below market lease for a 5 MW facility, expiring on November 8, 2022. In October 2022, the Company renewed the lease for a period of 23 months with similar terms.

For consideration of the purchase of the Washington State facility, the Company transferred approximately $23.0 million in cash and 414,508 common shares with a value of $3.7 million on the closing date, being November 9, 2021. The net identifiable assets acquired include: electrical distribution equipment valued at $6.0 million, buildings valued at $0.7 million, land valued at $0.1 million and a favourable lease valued at $2.0 million. The acquisition resulted in the Company recording goodwill of $17.9 million, which was determined as of June 30, 2022 to be fully impaired as a result of the decrease in the price of BTC.

On July 28, 2022, the Company announced the addition of 3 MW of low-cost hydropower that went online at the Washington State facility. The added 3 MW facility brought the total production from the Washington State farms to 20 MW. The Company is currently operating the majority of its Antminer S19j Pro Miners generating approximately 600 PH/s in this facility. The Company’s power supplier has provided preliminary indication that the first 6 MW of in-process applications are expected to be energized in the first half of 2023, while another 3 MW of in-process applications are estimated to be energized in the next five (5) years due to transmission being at capacity in relation to the nearby substation.

As of December 31, 2022, the Company employed 16 team members in the United States of America.

| 23 | Page |

Cautionary Statements