UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

For the fiscal year ended December 31 , 2023

or

For the transition period from ______ to ______

Commission File Number: 1-39804

Exact name of registrant as specified in its charter:

| State or other jurisdiction of incorporation or organization: | IRS Employer Identification No.: | |||||||

Address of principal executive offices:

Registrant’s telephone number, including area code:

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

(par value $.01 per share) | ||||||||

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes þ No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No þ

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check One)

| þ | Accelerated filer | ¨ | |||||||||

| Non-accelerated filer | ¨ | Smaller reporting company | |||||||||

| Emerging growth company | |||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. þ

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ¨

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No þ

The aggregate market value of the common stock held by non-affiliates of the registrant as of the last business day of the registrant’s most recently completed second fiscal quarter (June 30, 2023) was approximately $7.5 billion.

As of February 14, 2024, there were 7,668,422 shares of Common Stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE:

None

TEXAS PACIFIC LAND CORPORATION

TABLE OF CONTENTS

| Page | ||||||||

PART I

Statements in this Annual Report on Form 10-K that are not purely historical are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934, including statements regarding management’s expectations, hopes, intentions or strategies regarding the future. Words or phrases such as “expects” and “believes,” or similar expressions, when used in this Annual Report on Form 10-K or other filings with the Securities and Exchange Commission (the “SEC”), are intended to identify “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements include statements regarding the Company’s future operations and prospects, the markets for real estate in the areas in which the Company owns real estate, applicable zoning regulations, the markets for oil and gas including actions of other oil and gas producers or consortiums worldwide such as the Organization of Petroleum Exporting Countries (“OPEC”) and Russia (collectively referred to as “OPEC+”), expected competition, management’s intent, beliefs or current expectations with respect to the Company’s future financial performance and other matters. All forward-looking statements in this Report are based on information available to us as of the date this Report is filed with the SEC, and we assume no responsibility to update any such forward-looking statements, except as required by law. All forward-looking statements are subject to a number of risks, uncertainties and other factors that could cause our actual results, performance, prospects or opportunities to differ materially from those expressed in, or implied by, these forward-looking statements. These risks, uncertainties and other factors include, but are not limited to, the factors discussed in Item 1A. “Risk Factors” and Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

Item 1. Business.

General

Texas Pacific Land Corporation (which, together with its subsidiaries as the context requires, may be referred to as “TPL”, the “Company”, “our”, “we” or “us”) is a Delaware Corporation and one of the largest landowners in the State of Texas with approximately 868,000 surface acres of land in West Texas, principally concentrated in the Permian Basin. Additionally, we own a 1/128th nonparticipating perpetual oil and gas royalty interest (“NPRI”) under approximately 85,000 acres of land, a 1/16th NPRI under approximately 371,000 acres of land, and approximately 4,000 additional net royalty acres (normalized to 1/8th) (“NRA”), for a collective total of approximately 195,000 NRA all located in the western part of Texas.

The Company was originally organized as Texas Pacific Land Trust (the “Trust”) under a Declaration of Trust, dated February 1, 1888 (the “Declaration of Trust”), to receive and hold title to extensive tracts of land in the State of Texas, previously the property of the Texas and Pacific Railway Company. The Declaration of Trust provided for the appointment of trustees (the “Trustees”) to manage the assets of the Trust with all of the powers of an absolute owner. On January 11, 2021, the Trust completed its reorganization from a business trust, Texas Pacific Land Trust, into Texas Pacific Land Corporation (“TPL Corporation”), a corporation formed and existing under the laws of the State of Delaware. TPL Corporation is an independent public company and its common stock, par value of $0.01 per share (“Common Stock”) is listed under the symbol “TPL” on the New York Stock Exchange (the “NYSE”). See further discussion under “Corporate Reorganization” below. Any references in this Annual Report on Form 10-K to the Company, TPL, our, we or us with respect to periods prior to January 11, 2021, will be in reference to the Trust, and references to periods on that date and thereafter will be in reference to Texas Pacific Land Corporation or TPL Corporation.

Our surface and royalty ownership provide revenue opportunities throughout the oil and gas development value chain. While we are not an oil and gas producer, we benefit from various revenue sources throughout the life cycle of a well. During the initial development phase where infrastructure for oil and gas development is constructed, we receive fixed fee payments for use of our land and revenue for sales of materials (caliche) used in the construction of the infrastructure. During the drilling and completion phase, we generate revenue for providing sourced and/or treated produced water in addition to fixed fee payments for use of our land. During the production phase, we receive revenue from our oil and gas royalty interests and also revenues related to saltwater disposal on our land. In addition, we generate revenue from pipeline, power line and utility easements, commercial leases and temporary permits principally related to a variety of land uses, including, but not limited to, midstream infrastructure projects and processing facilities as hydrocarbons are processed and transported to market.

TPL’s mission is to pursue a thoughtful, long-term approach towards optimizing and building upon the commercial and environmental virtues of our extensive lands and resources. TPL has a long history of responsible management of its legacy assets, and in recent years, the Company has expanded its business strategy to generate incremental revenue streams that take advantage of the Company’s vast surface and royalty footprint, such as its investments in the Water Services and Operations business segment. Beyond TPL’s current businesses, the Company continues to explore new opportunities related

to renewable energy, environmental sustainability, and technology, among others, that can leverage the already existing legacy surface and royalty assets. The Company’s business model emphasizes high cash flow margins and relatively low ongoing capital expenditure requirements, and new opportunities would generally be expected to align with these priorities. The Company remains focused on optimizing long-term value creation and profitability, fostering responsible stewardship of our assets, providing quality customer service, and engaging with and advocating for employee and stakeholder interests.

Corporate Reorganization

On January 11, 2021, TPL completed its reorganization from a trust into a corporation (the “Corporate Reorganization”).

As part of the Corporate Reorganization, on January 11, 2021, shares of TPL Corporation’s Common Stock were distributed to holders of sub-share certificates of proprietary interest, par value $0.03-1/3 of the Trust (“Sub-shares”) on the basis of one share of Common Stock for every Sub-share (the “Distribution”).

Prior to the Corporate Reorganization, as a result of a proxy contest mounted by certain holders of Sub-shares, the Trust entered into a stockholders’ agreement dated as of June 11, 2020 and amended as of December 14, 2020 (the “Stockholders’ Agreement”), with Horizon Kinetics LLC, Horizon Kinetics Asset Management LLC (together with Horizon Kinetics LLC and its affiliates, “Horizon”), SoftVest Advisors, LLC, SoftVest, L.P. (together with SoftVest Advisors, LLC and its affiliates, “SoftVest,” and together with Horizon, the “Investor Group”), and Mission Advisors, LP, (“Mission” and together with the Investor Group, collectively, the “stockholder parties”). The Stockholders’ Agreement provided for, among other things, the appointment of Dana F. McGinnis, Eric L. Oliver and Murray Stahl as directors of TPL’s board of directors (the “Board”) in connection with the Corporate Reorganization. Mr. McGinnis resigned from the Board in March 2022.

Pursuant to the Stockholders’ Agreement, the stockholder parties agreed to vote all of the shares of Common Stock they beneficially owned at each annual or special meeting of stockholders of the Company in accordance with the Board’s recommendations, subject to certain exceptions. The termination date of the Stockholders’ Agreement was to occur immediately following the completion of the 2022 annual meeting of stockholders, except that the respective obligations of the Investor Group were to survive until such time as neither Investor Group designee is serving on the Board.

A dispute arose relating to the voting by the Investor Group on a proposal at the 2022 annual meeting of stockholders. The dispute was eventually resolved by the Delaware Court of Chancery, which ruling is now being appealed, but prior to such resolution, on July 28, 2023, the Company and the Investor Group entered into a Cooperation Agreement (the “Cooperation Agreement”) pursuant to which (i) Mr. Stahl, Marguerite Woung-Chapman and Robert Roosa would be nominated by the Company for election at the 2023 annual meeting of stockholders, (ii) the pre-signed conditional resignation letters submitted by Messrs. Stahl and Oliver pursuant to the Stockholders’ Agreement were considered withdrawn and no longer effective, and (iii) the Investor Group agreed to vote or cause to be voted all of the shares of Common Stock over which the Investor Group has direct or indirect voting control for the election of the three nominees named above and against any director nominee not recommended by the Board, for proposals regarding approval of executive compensation and ratification of the Company’s independent registered public accounting firm, and in accordance with the recommendation of the majority of the Board in respect of any proposals submitted by stockholders. The Cooperation Agreement also provided for mutual non-disparagement covenants and certain standstill obligations for the Investor Group as long as one of Mr. Stahl or Mr. Oliver remain on the Board. In addition, the termination date of the Stockholders’ Agreement was changed to occur following the completion of the 2023 annual meeting, which occurred on November 10, 2023.

Historical Operating Performance

The table below reflects our historical operating results for the last five years (in thousands, except per share amounts):

| Years Ended December 31, | |||||||||||||||||||||||||||||

| 2023 | 2022 | 2021 | 2020 | 2019 | |||||||||||||||||||||||||

| Revenues | $ | 631,595 | $ | 667,422 | $ | 450,958 | $ | 302,564 | $ | 490,496 | |||||||||||||||||||

| Net income | $ | 405,645 | $ | 446,362 | $ | 269,980 | $ | 176,049 | $ | 318,728 | |||||||||||||||||||

| Net income per share: | |||||||||||||||||||||||||||||

| Basic | $ | 52.81 | $ | 57.80 | $ | 34.83 | $ | 22.70 | $ | 41.09 | |||||||||||||||||||

| Diluted | $ | 52.77 | $ | 57.77 | $ | 34.83 | $ | 22.70 | $ | 41.09 | |||||||||||||||||||

2

Business Segments

We operate our business in two reportable segments: Land and Resource Management and Water Services and Operations. Our segments provide management with a comprehensive financial view of our key businesses. The segments enable the alignment of strategies and objectives of the Company and provide a framework for timely and rational allocation of resources within businesses. See Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and Note 14, “Business Segment Reporting” in Item 8. “Financial Statements and Supplementary Data” in this Annual Report on Form 10-K.

Land and Resource Management

Our Land and Resource Management segment encompasses the business of managing our approximately 868,000 surface acres of land and our oil and gas royalty interests in West Texas, principally concentrated in the Permian Basin. The revenue streams of this segment consist primarily of royalties from oil and gas, revenues from easements, commercial leases and renewables, and land and material sales.

We are not an oil and gas producer. Rather, our oil and gas revenue is derived from our oil and gas royalty interests. Thus, in addition to being subject to fluctuations in response to the market prices for oil and gas, our oil and gas royalties are also subject to decisions made by the owners and operators of the oil and gas wells to which our royalty interests relate as to investments in and production from those wells. Our oil and gas royalty interests require no capital expenditures or operating expense burden from us for well development.

Our revenue from easements is primarily generated from pipelines transporting oil, gas and related hydrocarbons, power line and utility easements, and subsurface wellbore easements. Easements typically have a thirty-plus year term but subsequently renew every ten years with an additional payment. In addition to easements, we also receive revenues from other surface-related operations on our land, including but not limited to, commercial leases, well development and material sales. Commercial lease revenue is derived primarily from processing, storage and compression facilities, and roads. Material sales include caliche, sand, and other material sales to operators. Caliche is used in the construction of oil and gas-related infrastructure, and sand is utilized for completion operations.

In recent years, we entered into agreements with third parties related to renewables and various “next generation” opportunities that will potentially utilize TPL’s surface assets. These agreements include the evaluation of grid-connected batteries, studies on carbon capture and sequestration, and development of bitcoin mining facilities, among other opportunities. Generally, these projects are structured with multi-year terms that allow for feasibility and/or commercial suitability and revenue arrangements that provide royalty, fee, profit sharing, lease and/or rental payments, though contractual terms and timing for commercial operations will vary by project. We do not anticipate these agreements will have a significant impact on our revenues in the short-term but do have the potential to contribute meaningfully to our revenues in the longer term.

As a significant landowner, we also generate revenue from land sales. From time to time, we receive offers from third parties to acquire tracts of our land. Sales demand and related sale prices of particular tracts of land are influenced by many factors, including general economic conditions, the rate of development in nearby areas and the suitability of the particular tract for commercial uses prevalent in West Texas.

3

Operations

Revenues from the Land and Resource Management segment for the last three years were as follows (dollars presented in thousands):

| Years Ended December 31, | |||||||||||||||||||||||||||||||||||

| 2023 | 2022 | 2021 | |||||||||||||||||||||||||||||||||

| Segment Revenue | % of Total Consolidated Revenue | Segment Revenue | % of Total Consolidated Revenue | Segment Revenue | % of Total Consolidated Revenue | ||||||||||||||||||||||||||||||

| Oil and gas royalties | $ | 357,394 | 57 | % | $ | 452,434 | 68 | % | $ | 286,468 | 64 | % | |||||||||||||||||||||||

| Easements and other surface-related income | 67,905 | 11 | % | 44,569 | 7 | % | 32,892 | 7 | % | ||||||||||||||||||||||||||

| Land sales and other operating revenue | 6,806 | 1 | % | 9,972 | 1 | % | 1,027 | — | % | ||||||||||||||||||||||||||

| Total Revenue - Land and Resource Management segment | $ | 432,105 | 69 | % | $ | 506,975 | 76 | % | $ | 320,387 | 71 | % | |||||||||||||||||||||||

Please see discussion of our financial results at Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations — Segment Results of Operations.”

Oil and Gas Activity for the Year Ended December 31, 2023

For the year ended December 31, 2023, our share of crude oil, natural gas and natural gas liquid (“NGL”) production was 23.5 thousand barrels of oil equivalent (“Boe”) per day compared to 21.3 thousand Boe per day for the same period of 2022. The total equivalent price was $42.58 per Boe for the year ended December 31, 2023, a decrease of 30.0% compared to the total equivalent price of $60.81 per Boe for the same period of 2022.

For the year ended December 31, 2023, the number of oil and gas wells that had been drilled but are not yet completed (“DUC”) subject to our royalty interest was 675 compared to 584 for the same period of 2022. The number of DUC wells is determined using uniform drilling spacing units with pooled interests for all wells awaiting completion.

Competition

Our Land and Resource Management segment does not have direct peers, as such, in that it sells, leases and generally manages land owned by the Company and, to that extent, any owner of property located in areas comparable to the Company is a potential competitor.

Water Services and Operations

Our Water Services and Operations segment encompasses the business of providing full-service water offerings to operators in the Permian Basin through Texas Pacific Water Resources LLC (“TPWR”), a single member Texas limited liability company owned by the Company.

These full-service water offerings include, but are not limited to, water sourcing, produced-water treatment, infrastructure development, and disposal solutions. We are committed to sustainable water development. Our significant surface ownership in the Permian Basin provides TPWR with a unique opportunity to provide multiple full-service water offerings to operators.

The revenue streams of this segment principally consist of revenue generated from sales of sourced and treated water as well as revenue from produced water royalties. Energy businesses use water for their oil and gas projects while service businesses (i.e., water management service companies) operate water facilities to produce and sell water to energy businesses.

4

Operations

Revenues from our Water Services and Operations segment for the last three years were as follows (dollars presented in thousands):

| Years Ended December 31, | |||||||||||||||||||||||||||||||||||

| 2023 | 2022 | 2021 | |||||||||||||||||||||||||||||||||

| Segment Revenue | % of Total Consolidated Revenue | Segment Revenue | % of Total Consolidated Revenue | Segment Revenue | % of Total Consolidated Revenue | ||||||||||||||||||||||||||||||

| Water sales | $ | 112,203 | 18 | % | $ | 84,725 | 13 | % | $ | 67,766 | 15 | % | |||||||||||||||||||||||

| Produced water royalties | 84,260 | 13 | % | 72,234 | 11 | % | 58,081 | 13 | % | ||||||||||||||||||||||||||

| Easements and other surface-related income | 3,027 | — | % | 3,488 | — | % | 4,724 | 1 | % | ||||||||||||||||||||||||||

| Total Revenue – Water Services and Operations segment | $ | 199,490 | 31 | % | $ | 160,447 | 24 | % | $ | 130,571 | 29 | % | |||||||||||||||||||||||

Please see discussion of our financial results at Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations — Segment Results of Operations.”

Activity for the year ended December 31, 2023

The increase in water sales during 2023 compared to 2022 is principally due to a 21.8% increase in water sales volumes over the same time period.

During 2023, we invested $15.2 million in TPWR projects to maintain and/or enhance water sourcing assets and acquired groundwater rights for $3.8 million to provide us access to additional water volumes outside of our existing surface footprint to assist in managing fluctuations in customer demand. We also acquired a saltwater disposal (“SWD”) easement for $17.6 million. The SWD easement covers approximately 49,000 acres and provides us future disposal opportunities to service injection customers seeking disposal solutions located outside of core basins.

Competition

While there is competition in the water service business in the Permian Basin, we believe our position as a significant landowner of approximately 868,000 surface acres in West Texas gives us a unique advantage over our competitors who must negotiate with existing landowners to source water and then for the right of way to deliver the water to the end user.

5

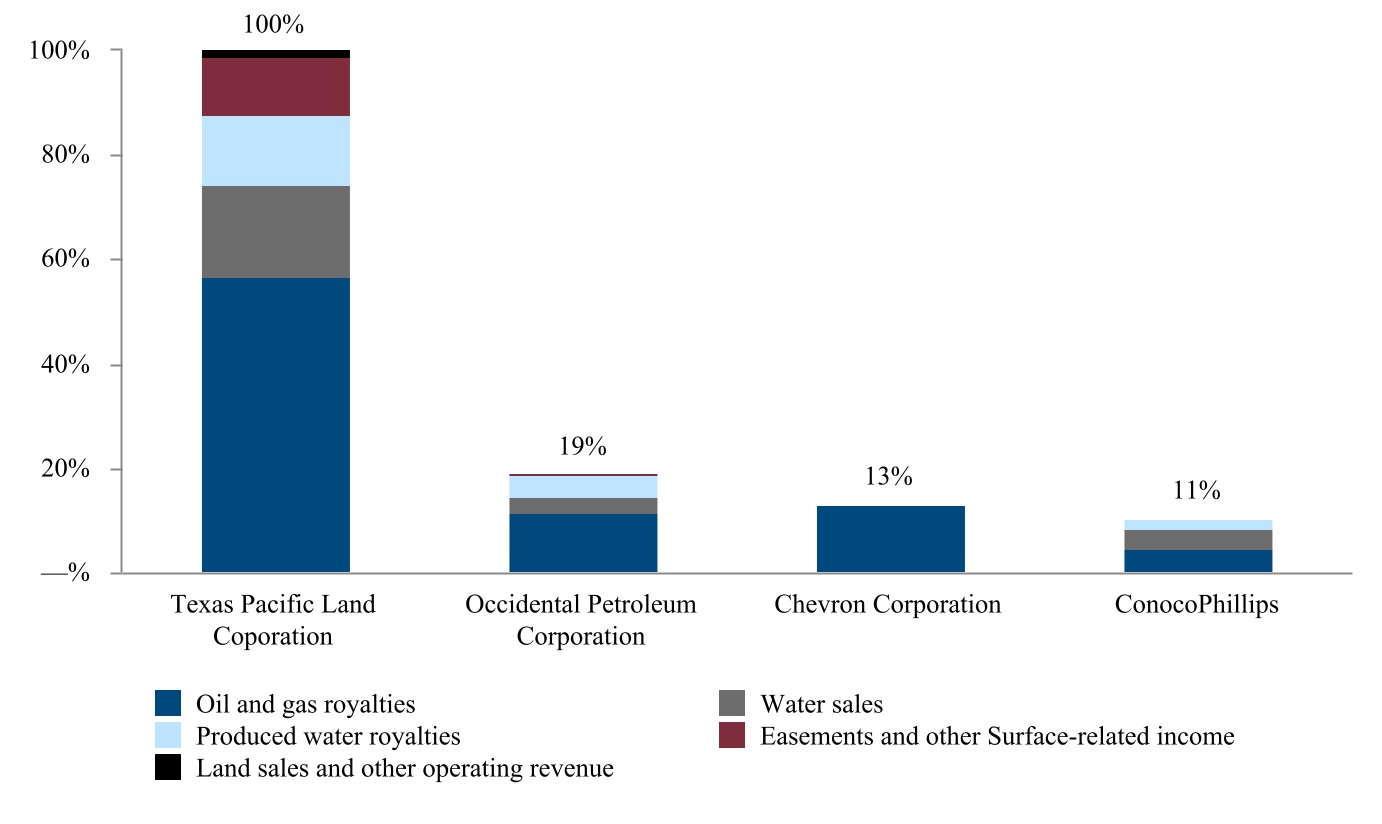

Major Customers

The chart below depicts our total revenues and revenues from customers representing more than 10% of our 2023 consolidated revenues:

While approximately 43% of our 2023 revenue is derived from only three customers, two of these customers are in the top 10, and the remaining customer is in the top 35, energy companies in the world based on market capitalization, and we believe each of them is a strong and reliable operator. Given their major presence in the Permian Basin and our significant surface lands in the same area, the high concentration of business with these three customers is expected. Further, the choice of whom we do business with largely depends on location of mineral royalties and surface rights on or near our assets and consists of a limited universe of oil and gas companies who operate in the Permian Basin.

Seasonality

While the business of TPL is not seasonal in nature, as that term is generally understood, revenues from oil and gas royalties may fluctuate from period to period based upon market prices for oil and gas and production decisions made by the operators. Our other revenue streams, which include, but are not limited to, water sales and royalties, easements and other surface related income and sales of land, may also fluctuate from period to period. In addition, our results generally rely on the decisions and actions of third parties out of our ultimate control. As a consequence, the results of our operations for any particular period are not necessarily indicative of the results of operations for a full year.

Regulations

We are subject to various federal, state and local laws. Management believes that our operations comply in all material respects with applicable laws and regulations and that the existence and enforcement of such laws and regulations have no more restrictive effect on our method of operations than on other companies similar to TPL.

We cannot determine the extent to which new legislation, new regulations or changes in existing laws or regulations may affect our future operations.

6

Environmental Considerations

Compliance with Federal, State and local provisions that have been enacted or adopted regulating the discharge of materials into the environment, or otherwise relating to the protection of the environment, have had no material effect upon our business generally, including the capital expenditures, earnings and competitive position of the Company. To date, the Company has not been called upon to expend any funds for these purposes.

Environmental, Social and Governance (“ESG”)

In August 2021, the Company published its inaugural Environmental, Social, Governance (“ESG”) disclosure highlighting data and processes that began in 2020. The Company’s current ESG disclosure is available at the Company’s website at www.TexasPacific.com. The ESG disclosure has been prepared in accordance with the frameworks of the Sustainable Accounting Standards Board, the Global Reporting Initiative, and the Task Force on Climate Related Disclosures.

Integrating sustainability and ESG objectives is a priority for our Company. The Company’s ESG strategy reflects its dedication to meeting tactical business priorities while managing the environmental impacts of its operations, maintaining principles for social responsibility, and upholding a commitment to strong corporate governance. Our ESG strategy is focused on the overarching priorities of environmental management, employee health and safety, workforce management and equality, community and landowner engagement, and strong corporate governance and ethics. We are committed to sustainability and responsible stewardship across all of our operations and land management activities.

As the Company does not produce oil or gas from the land from which its royalties’ revenue stream is derived, it developed its sustainability goals and partnership opportunities in consultation with the entities operating on its land. On the water solutions side of its business, the Company developed a tailored ESG program that addresses the ethical and responsible buildout of water assets and management of water as a natural resource. The Company’s continued goal is an integrated and iterative approach to sustainable and responsible resource management.

TPL’s ESG accomplishments and goals include but are not limited to:

•Converted from a business trust to a Delaware corporation in January 2021, providing enhanced governance to the Company’s stockholders.

•Increased the electrification of the Company’s water assets in an effort to reduce costs and mitigate the overall emission profile of the Company by reducing reliance on diesel generators. Cumulatively through December 31, 2023, TPL has spent $15.8 million of capital on electric infrastructure.

•Initiated energy tracking in 2020 to monitor and identify trends in energy consumption and sourcing.

•Prioritizing the health and welfare of TPL’s workforce.

•Employed practices for the tracking and monitoring of all spills, regardless if they are within or outside of regulatory reporting requirements. We had zero spills of produced water in 2023 and 2022.

•Partnered with oil & gas operators on the Company’s surface estate to collectively discuss and manage ESG risks. Partnership opportunities included: developing renewable energy infrastructure across the Company’s land, developing water infrastructure to support the reuse and recycling of produced water—a critical response to climate change, partnering to develop innovative technologies that support emissions management, and more.

•Instituted a governance framework that includes oversight and stewardship of the Company’s ESG strategies. The Nominating and Corporate Governance Committee reviews the Company’s policies and programs concerning corporate social responsibility, including ESG matters, with the support of the Audit Committee and the Compensation Committee, where appropriate. The committees provide guidance to the Board and management with respect to trends and developments regarding environmental, social, governance, and political matters that could significantly impact the Company.

The disclosure denotes that the Company’s ESG strategy, including metrics and targets, will be continuously reviewed and assessed annually to determine if updates or process improvements are needed.

Our full ESG disclosure is available at www.TexasPacific.com/esg.

7

Human Capital Resources

We believe we have a talented, motivated and dedicated team and we are committed to supporting the development of our team members and continuously building on our strong culture. As of December 31, 2023, the Company had 100 full-time employees, of which 30 were employees of TPWR.

Our business strategy and ability to serve customers relies on employing talented professionals and attracting, training, developing and retaining a knowledgeable skilled workforce. We maintain a good working relationship with our employees. We value our employees and their experience in providing value through land, mineral and water resource management and water solutions. Maintaining a robust pipeline of talent is crucial to our ongoing success and is a key aspect of succession planning efforts across the organization. Our leadership and human resources teams are responsible for attracting and retaining top talent by facilitating an environment where employees feel supported and encouraged in their professional and personal development. We are committed to enhancing gender, racial and ethnic diversity throughout our organization. We believe that diversity is an important factor in bringing people together, encouraging shared commitment and fostering new ideas.

We strive to be a great place for our employees to work. Accordingly, we offer industry competitive pay and benefits, tuition reimbursement and continuing education classes and are committed to maintaining a workplace environment that promotes employee productivity and satisfaction.

Employee safety is also among our top priorities. Accordingly, we have developed and administer company-wide policies to ensure a safe and fair workplace free of discrimination or harassment for each team member and compliance with Occupational Safety and Health Administration (“OSHA”) standards, as further discussed in our Code of Business Conduct and Ethics. This commitment applies to recruiting, hiring, compensation, benefits, training, termination, promotions or any other terms and conditions of employment. We maintain our strong focus on safety and have taken measures to protect our employees and maintain safe, reliable operations.

We strive for a goal of zero occupational injuries, illnesses and incidents in our workplace. To ensure that we protect our safety culture, we have in place a dedicated HS&E team with substantial combined years of experience and have in-house authorized trainers for OSHA-required certified training, powered equipment training and PCE-safe land certificated training.

Available Information on our Website

The Company makes available on our website at www.TexasPacific.com, free of charge, its Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to those reports as soon as reasonably practicable after they are electronically filed with, or furnished to, the SEC pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 (the “Exchange Act”). Such reports are also available at www.sec.gov. The information contained on our website is not part of this Report.

8

Item 1A. Risk Factors.

An investment in our securities involves a degree of risk. The risks described below are not the only ones facing us. Additional risks not presently known to us or that we currently deem immaterial may also have a material adverse effect on us. If any of the following risks actually occur, our financial condition, results of operations, cash flows or business could be harmed. In that case, the market price of our stock could decline and you could lose part or all of your investment in our stock.

Risks Related to our Business

Our oil and gas royalties are dependent upon the market prices of oil and gas which fluctuate.

The oil and gas royalties that we receive are dependent upon the market prices for oil and gas. When lower market prices for oil and gas occur, they will have an adverse effect on our oil and gas royalties. The market prices for oil and gas are subject to US and global macroeconomic and geopolitical conditions and infrastructure and logistical constraints, amongst others, and, in the past, have been subject to significant price fluctuations. Price fluctuations for oil and gas have been particularly volatile in recent years due to supply and demand fundamentals, Organization of the Petroleum Exporting Countries (“OPEC”) and Russia (collectively referred to as “OPEC+”) actions, the prolonged Ukraine/Russia conflict and general economic cycles, among other factors. These measures have at times resulted in a reduction of global economic activity and volatility in the global financial markets. The scale and duration of the impact of these factors remain unknowable but could lead to a decrease in our revenues and have a material impact on our business segments and earnings, cash flow and financial condition.

We are not an oil and gas producer. Our revenues from oil and gas royalties are subject to the actions of others.

We are not an oil and gas producer. Our oil and gas income is derived primarily from perpetual non-participating oil and gas royalty interests that we have retained. As oil and gas wells age, their production capacity may decline absent additional investment. However, the owners and operators of the oil and gas wells make all decisions as to investments in, and production from, those wells and our royalties are dependent upon decisions made by those operators, among other factors. Accordingly, a significant portion of our revenues is reliant on the management and actions of third parties, over whom we have no control. There can be no assurance that such third parties will take actions or make decisions that will be beneficial to us, which could result in adverse effects on our financial results and performance.

Our revenues from the sale of land are subject to substantial fluctuation. Land sales are subject to many factors that are beyond our control.

Our land sales vary widely from year to year and quarter to quarter. The total price obtained, the average price per acre, and the number of acres sold in any one year or quarter should not be assumed to be indicative of future land sales. Our desire to sell and the demand and pricing for any particular tract of our land is influenced by many factors, including but not limited to: (i) access and location, (ii) the national and local economies, (iii) the rate of oil and gas well development by operators, (iv) the rate of development in nearby areas, (v) the livestock carrying capacity, and (vi) the condition of the local industries, which itself is influenced by a range of conditions. Our ability to sell land can be, therefore, largely dependent on the actions of adjoining landowners.

Demand for TPWR’s products and services is substantially dependent on the levels of expenditures by our customers.

Demand for TPWR’s products and services depends substantially on demand and expenditures by our customers for the exploration, development and production of oil and natural gas reserves. These expenditures are generally dependent on our customers’ overall financial position, capital allocation priorities, and views of future oil and natural gas prices. Declines, as well as anticipated declines, in oil and gas prices have in the past resulted in, and may in the future result in, lower capital expenditures, project modifications, delays or cancellations, general business disruptions, and delays in payment of, or nonpayment of, amounts that are owed to us, which would adversely affect our earnings, cash flow and financial condition. The results of operations for the Water Services and Operations segment have been impacted from time to time by reduced development pacing and declines in expenditures by our customers in response to varying industry or global circumstances. Our results may continue to be impacted by producer discretion on development pacing and capital expenditures.

9

We face the risks of doing business in a new and rapidly evolving market for TPWR and may not be able to successfully address such risks and achieve acceptable levels of success or profits.

We have encountered and may continue to encounter the challenges, uncertainties and difficulties frequently experienced in new and rapidly evolving markets with respect to the business of TPWR, including:

•pricing pressure driven by new competition;

•volatile and/or unexpected operating and maintenance costs;

•lack of sufficient customers or loss of significant customers for the new line of business;

•increased regulation, including with respect to environmental and geological uses and impacts on industry operations; and

•uncertainty with outsourced 3rd party provider(s) providing water treatment services.

The impact of government regulation on TPWR could adversely affect our business.

The business of TPWR is subject to applicable state and federal laws and regulations, including laws and regulations on water use, environmental and safety matters. These laws and regulations may increase the costs and timing of planning, designing, drilling, installing, operating and abandoning water wells, source water and treatment facilities and impact our customers’ ability to transport, store and/or dispose of produced water in certain locations. Due to increased seismicity in the Delaware and Midland Basins, the Texas Railroad Commission recently began implementing Seismic Response Areas (“SRAs”) limiting the permitted capacity and use of certain Saltwater Disposal Wells (“SWDs”) for the injection of produced water. The implementation of SRAs could limit the volume of produced water disposed on the Company’s surface within the SRAs or, in certain cases, could direct additional volumes of produced water to SWDs on the Company’s surface outside of SRAs. These limitations and/or redirections may cause TPWR to adapt its business plans and could affect TPWR’s financial performance. The Company continues to actively engage with the Texas Railroad Commission and evaluate the potential effect of SRAs on the Company’s produced water royalties.

Our business and financial results could be disrupted by natural or human causes beyond our control.

Our revenues depend on natural and environmental conditions with respect to operations that result in royalties to us, or that use our water services. Our business and financial results are therefore subject to disruption from natural or human causes beyond our control, including physical risks from severe storms, floods, droughts resulting in aquifer declines and other forms of severe weather, war, accidents, civil unrest, political events, fires, earthquakes, system failures, pipeline disruptions, environmental hazards such as oil and produced water spills, terrorist acts and epidemic or pandemic diseases, any of which could result in a material adverse effect on oil and natural gas production and, therefore, our results of operations.

Our business and financial results are subject to major trends in our industry, such as decarbonization, and may be adversely affected by future developments out of our control.

Much of the value of the land we own and upon which we receive royalties is based on the oil and natural gas reserves located there. Our revenues may be negatively affected by changes driven by trends such as decarbonization efforts. Such changes may relate to the types or sources of energy in demand, such as a shift to renewable sources of power generation (for example, wind and solar), along with ongoing changes in regulatory, investor, customer and consumer policies and preferences. The evolution of global energy sources is affected by factors out of our control, such as the pace of technological developments and related cost considerations, the levels of economic growth in different markets around the world and the adoption of climate change-related policies. In addition, the possibility of taxes on energy sources, including oil and gas, may affect the demand for crude oil and natural gas and the operating costs for third party operators on our royalty properties.

Cyber incidents or attacks targeting systems and infrastructure used by the oil and gas industry may adversely impact our operations, and if we are unable to obtain and maintain adequate protection of our data, our business may be adversely impacted.

We and our operators increasingly rely on information technology systems to operate our respective businesses, and the oil and gas industry depends on digital technologies in exploration, development, production, and processing activities. Threats to information technology systems associated with cybersecurity risks and cyber incidents or attacks continue to grow. Our technologies, systems, networks, and those of the operators on our properties, vendors, suppliers, and other business

10

partners, may become the target of cyberattacks or information security breaches that could result in the unauthorized release, gathering, monitoring, misuse, loss or destruction of proprietary, personal and other information, or other disruption of business activities. In addition, certain cyber incidents, such as surveillance, may remain undetected for some period of time. While we utilize various systems, procedures and controls to mitigate exposure to such risk, cyber incidents and attacks are continually evolving and unpredictable. Our information technology systems and any insurance coverage for protecting against cybersecurity risks may not be sufficient. As cyber security threats continue to evolve, we may be required to expend additional resources to continue to modify or enhance our protective measures or to investigate and remediate any vulnerability to cyber incidents. There can be no assurance that our business, finances, systems and assets will not be compromised in a cyber attack.

The loss of key members of our management team or difficulty attracting and retaining experienced technical personnel could reduce our competitiveness and prospects for future success.

The successful implementation of our strategies and handling of other issues integral to our future success will depend, in part, on our experienced management team, including with respect to the business of TPWR. The loss of key members of our management team could have an adverse effect on our business. If we cannot retain our experienced personnel or attract additional experienced personnel, our ability to compete could be harmed.

Global health threats may adversely affect our business.

Our business could be adversely affected by the effects of a widespread outbreak of contagious disease, such as the outbreak of COVID-19. A significant outbreak of contagious diseases in the human population and resulting widespread health crisis could adversely affect the economies and financial markets of many countries, resulting in an economic downturn, reduced demand for oil and gas and interruption to supply chains related to oil and gas. The reduction of economic activity and reduced global demand for oil and gas related to such outbreaks and actions taken by governments to mitigate the spread of a virus or other infectious agent could lead to an increase in our operating costs and have a material impact on our business segments and earnings, cash flow and financial condition.

We face direct and indirect supply chain risks that may adversely affect our business.

Our business could be negatively affected by supply shortages and/or price increases driven by the increased costs of materials and logistics as a result of macroeconomic conditions, including the prolonged Ukraine/Russia conflict, general inflationary pressures, labor shortages, part or equipment availability, manufacturing capacity, tariffs, trade disputes and barriers, natural disasters or pandemics and the effects of climate change. Supply shortages and/or price increases could lead to a reduction in revenues and an increase in our operating costs and could have a material impact on our business segments and earnings, cash flow and financial condition.

Supply chain issues may disrupt the operations and development activities of operators on our land, upon whom much of our revenue relies, which could negatively affect our revenues from oil and gas royalties, easements and our water offerings. Supply chain issues could also lead to an increase in TPWR’s operating costs and disrupt its water sourcing and treatment operations, which could further negatively affect our revenues from our water offerings. TPWR has adapted lead times for ordering parts and equipment to mitigate supply chain issues, but given the uncertainty surrounding the macroeconomic factors and geopolitical situation, there can be no assurance that we will not suffer adverse effects on our business operations in the future.

Risks Related to the Corporate Reorganization

The completion of the Corporate Reorganization may implicate conditions and covenants contained in certain agreements to which the Trust was a party and thereby may cause us to lose certain benefits that the Trust historically received. If the Company is unable to obtain consents to, or approval or waiver of, any such conditions or covenants, or is unable to obtain an acknowledgement that any such benefits shall continue for the benefit of TPL Corporation, we may not be entitled to all benefits and other rights under such agreements, which may have an adverse impact on the business and results of operations.

The completion of the Corporate Reorganization may implicate conditions and covenants, contained in certain agreements to which the Trust was, and now TPL Corporation is, a party and thereby may cause us to lose certain benefits that the Trust historically received. Certain counterparties may withhold consent to, or approval or waiver of, certain conditions or covenants in order to obtain more favorable terms from us. If the Company is unable to obtain consents to, or approval or waiver of, any such conditions or covenants, or if the Company is unable to obtain acknowledgement from any counterparties

11

that any such benefits shall continue for the benefit of TPL Corporation, then we may decide to enforce our rights and interests by initiating legal action. In the meantime, and pending the outcome of any such legal proceeding to enforce our rights, we may be unable to continue to obtain all benefits and other rights under such agreements that would otherwise be transferred to us as part of the Corporate Reorganization. This may have an adverse impact on TPL’s business and results of operations.

For example, the obligation to pay ad valorem taxes with respect to certain of our royalty interests was assumed by a third party and is now the obligation of the successors in interest to such third party (the “obligors”), so long as such royalty interests are held by the Trustees or their successors in office under the Declaration of Trust. The amount of such taxes depends on the valuations determined by various county taxing authorities with respect to our royalty interests and the tax rates used in assessing such ad valorem taxes. Consequently, the amount of ad valorem taxes that may be assessed against our royalty interests may vary from year to year, and we are unable to reliably predict the amount of any such increases or decreases in future years. We have received an indication from one such obligor that it does not intend to continue to make the ad valorem tax payments that it has been making to date. We have accrued an estimate of such taxes and are making payments on a current basis in order to protect the royalty interests from any potential tax liens for nonpayment of future ad valorem taxes. While we intend to seek reimbursement from the third party following payment of such taxes, there can be no assurance that we will be successful in getting reimbursed. Taking on the cost of such payments will have an adverse impact on our business and results of operations.

The Corporate Reorganization may have adverse tax consequences.

We have obtained an opinion from counsel that the Corporate Reorganization and the Distribution qualified as a tax-free reorganization within the meaning of Section 368(a)(1)(F) of the Code. The opinion of counsel does not address any U.S. state or local or non-U.S. tax consequences of the Corporate Reorganization and the Distribution. The opinion assumed that the Corporate Reorganization and the Distribution was completed according to the terms of certain of the operative agreements and required regulatory filings, and relied on the facts as stated therein and in other ancillary agreements and documents. In addition, the opinion was based on certain representations as to factual matters from, and certain covenants by, us and the Trust. The opinion cannot be relied on if any of the assumptions, representations or covenants were incorrect, incomplete or inaccurate or were violated in any material respect.

The opinion of counsel is not binding on the IRS or the courts, and no assurance can be given that contrary positions will not be taken by the IRS or a court. We have not sought and will not seek a ruling from the IRS regarding the federal income tax consequences of the Corporate Reorganization and the Distribution.

If the Corporate Reorganization and the Distribution were to fail to qualify as a reorganization or for tax-free treatment either under Section 368(a)(1)(F) or any other provision of the Code, then U.S. Holders of Sub-shares would recognize gain or loss, as applicable, equal to the difference between (a) the sum of the fair market value of the shares of TPL Corporation Common Stock received by such holder and (b) its adjusted tax basis in the Sub-shares surrendered in exchange therefor. Further, the Trust would recognize taxable gain as if it sold all of its assets, subject to its liabilities, at fair market value. The consequences of the Corporate Reorganization and the Distribution to any holder will depend on that holder’s particular situation.

Risks Related to Our Common Stock

We cannot be certain that an active trading market for our Common Stock will be sustained, and our stock price may fluctuate significantly.

A public market for our Common Stock did not exist until the Corporate Reorganization was effected on January 11, 2021. We cannot guarantee that the active trading market that has developed will be sustained for our Common Stock, nor can we predict the prices at which shares of our Common Stock may trade.

Until the market has fully evaluated our business as a corporation, the prices at which shares of our Common Stock trade may fluctuate more significantly than might otherwise be typical, even with other market conditions, including general volatility, held constant. The increased volatility of our stock price following the Corporate Reorganization may have a material adverse effect on our business, financial condition and results of operations. The market price of our Common Stock may fluctuate significantly due to a number of factors, some of which may be beyond our control, including:

•actual or anticipated fluctuations in our results of operations due to factors related to our business;

•our quarterly or annual earnings, or those of other companies in our industry;

12

•changes to the regulatory and legal environment under which we operate;

•changes in accounting standards, policies, guidance, interpretations or principles;

•the failure of securities analysts to cover, or positively cover, our Common Stock;

•changes in earnings estimates by securities analysts or our ability to meet those estimates;

•the operating and stock price performance of other comparable companies;

•investor perception of our Company and our industry;

•actual or anticipated fluctuations in commodities prices; and

•domestic and worldwide economic and geopolitical conditions.

There may be substantial changes in our stockholder base.

Investors in the Trust may have held Sub-shares because of a decision to invest in an organization with the Trust’s governance profile or operating track record. Since the Corporate Reorganization, the shares of our Common Stock held by those investors represent an investment in a company with a different governance profile, in particular a board of directors at TPL Corporation subject to changes from year to year at annual elections of directors. More frequent changes in the leadership of the organization, particularly on the Board, could lead to changes in the operating policies of TPL Corporation over time. Such changes may not match some stockholders’ investment strategies, which could cause them to sell our Common Stock. These changes may also attract new investors who previously did not invest in the Trust because of its structure, governance profile or operating track record. As a result of such changes, our stock price may decline or experience volatility as our stockholder base changes. Additionally, new investors or leadership at TPL Corporation could advocate for business or corporate initiatives that would not be desired by or beneficial for all stockholders, such as an untimely sale of the business.

Our business could be negatively affected as a result of the actions of activists.

Our business could be negatively affected as a result of stockholder activism, which could cause us to incur significant expense, hinder execution of our business strategy, and impact the trading value of our securities. In the past, the Company has been the subject of stockholder activism, and we are subject to the risks associated with any ongoing or future such activism. Stockholder activism, including potential proxy contests, requires significant time and attention by management and our Board, potentially interfering with our ability to execute our strategic plan. We may be required to incur significant legal fees and other expenses related to activist stockholder matters, and the attention of our management may be diverted by such activism. While we welcome our stockholders’ constructive input, there can be no assurance that stockholder actions would not result in negative impacts to the Company. Any of these impacts could materially and adversely affect our business and operating results, and the market price of our Common Stock could be subject to significant fluctuation or otherwise be adversely affected by stockholder activism.

If our amended and restated certificate of incorporation is amended to allow for the issuance of additional Common Stock, holders of our Common Stock could experience dilution in the future.

If our amended and restated certificate of incorporation is amended to allow for the issuance of additional Common Stock, holders of our Common Stock could be diluted because of equity issuances for proposed acquisitions or capital market transactions or equity awards proposed to be granted to our directors, officers and employees subject to any required vote of holders of our Common Stock under our amended and restated certificate of incorporation and amended and restated bylaws. We may issue stock-based awards, including annual awards, new hire awards and periodic retention awards, as applicable, to our directors, officers and other employees under any employee benefits plans we have adopted or may adopt, using newly issued shares rather than treasury shares as is currently our practice.

At our 2022 annual meeting of stockholders, our stockholders voted on a proposal to increase the number of shares of Common Stock authorized under our amended and restated certificate of incorporation. A dispute relating to the voting on this proposal was resolved by the Delaware Court of Chancery, which determined that the proposal was approved by stockholders. The decision is currently subject to an appeal, and, therefore, we have not yet taken any action to amend the amended and restated certificate of incorporation.

13

In addition, our amended and restated certificate of incorporation authorizes us to issue, without the approval of our stockholders, one or more series of preferred stock having such designations, powers, preferences, privileges and relative, participating, optional and special rights, and qualifications, limitations and restrictions as the Board may generally determine in its sole discretion. The terms of one or more classes or series of preferred stock could dilute the voting power or reduce the value of our Common Stock. For example, we could grant the holders of preferred stock the right to elect some number of the members of the Board in all events or upon the happening of specified events, or the right to veto specified transactions. Similarly, the repurchase or redemption rights or liquidation preferences that we could assign to holders of preferred stock could affect the residual value of our Common Stock.

We may not continue the Trust’s historical practice of declaring cash dividends. We will evaluate whether to pay cash dividends on our Common Stock in the future and we cannot guarantee the timing, amount or payment of dividends, if any.

The timing, declaration, amount of, and payment of any cash dividends to our stockholders is within the discretion of our Board and will depend upon many factors, including our financial condition, earnings, capital requirements of our operating subsidiaries, covenants associated with any debt service obligations or other contractual obligations, legal requirements, regulatory constraints, industry practice, ability to access capital markets and other factors deemed relevant by the Board. Moreover, should our Board determine to pay any dividend in the future, there can be no assurance that we will continue to pay such dividends or the amount of such dividends.

We may not continue the Trust’s historical practice of repurchasing outstanding equity of its holders. We will evaluate whether to repurchase our outstanding Common Stock in the future and we cannot guarantee the timing, amount or payment of share repurchases, if any.

During the year ended December 31, 2023, the Company repurchased 27,619 outstanding shares of Common Stock which repurchased shares were placed in treasury. We expect that we will from time to time offer to repurchase a portion of our outstanding Common Stock. However, any repurchase will be within the discretion of our Board and will depend upon many factors, including market and business conditions, the trading price of our Common Stock, available cash and cash flow, capital requirements and the nature of other investment opportunities.

State law and anti-takeover provisions could enable our Board to resist a takeover attempt by a third party and limit the power of our stockholders.

Our amended and restated certificate of incorporation and amended and restated bylaws contain, and Delaware law contains, provisions that are intended to deter coercive takeover practices and inadequate takeover bids by making such practices or bids unacceptably expensive to the bidder and to encourage prospective acquirers to negotiate with our Board rather than to attempt a hostile takeover. These provisions include, among others: (a) the ability of our remaining directors to fill vacancies on our Board (except in an instance where a director is removed by stockholders and the resulting vacancy is filled by stockholders); (b) the inability of stockholders to call a special meeting of stockholders; (c) rules regarding how stockholders may present proposals or nominate directors for election at stockholder meetings; and (d) the right of our Board to issue preferred stock without stockholder approval.

In addition, we are subject to Section 203 of the Delaware General Corporation Law (“DGCL”), which could have the effect of delaying or preventing a change of control that you may favor. Section 203 provides that, subject to limited exceptions, persons that acquire, or are affiliated with persons that acquire, more than 15% of the outstanding voting stock of a Delaware corporation may not engage in a business combination with that corporation, including by merger, consolidation or acquisitions of additional shares, for a three-year period following the date on which that person or any of its affiliates becomes the holder of more than 15% of the corporation’s outstanding voting stock.

We believe these provisions protect our stockholders from coercive or otherwise unfair takeover tactics by requiring potential acquirers to negotiate with our Board and by providing our Board with more time to assess any acquisition proposal. These provisions are not intended to make the Company immune from takeovers; however, these provisions apply even if the offer may be considered beneficial by some stockholders and could delay or prevent an acquisition that our Board determines is not in the best interests of the Company and its stockholders. These provisions may also prevent or discourage attempts to remove and replace incumbent directors.

Our amended and restated certificate of incorporation designates the Court of Chancery of the State of Delaware or the U.S. District Court for the Northern District of Texas as the sole and exclusive forums for certain types of actions and proceedings that may be initiated by our stockholders, which could discourage lawsuits against the Company and our directors and officers.

14

Our amended and restated certificate of incorporation provides that unless the Company otherwise determines, the Court of Chancery of the State of Delaware (or, if such court does not have jurisdiction, the U.S. District Court for the District of Delaware) or the U.S. District Court for the Northern District of Texas (or, if such court does not have jurisdiction, any district court in Dallas County in the State of Texas) will be the sole and exclusive forums for any derivative action brought on our behalf, any action asserting a claim of breach of a fiduciary duty owed by any of our current or former directors, officers, employees or stockholders, any action or proceeding asserting a claim against us or any of our directors, officers, employees or agents arising pursuant to, or seeking to enforce any right, obligation or remedy under any provision of the DGCL, the laws of the State of Texas, our amended and restated certificate of incorporation or our amended and restated bylaws or any action asserting a claim against us or any of our directors, officers, employees or agents governed by the internal affairs doctrine, in each such case, subject to the applicable court having personal jurisdiction over the indispensable parties named as defendants. Our amended and restated certificate of incorporation also provides that unless our Board otherwise determines, the federal district courts of the United States will be the sole and exclusive forum for the resolution of any complaint asserting a cause of action arising under the Securities Act of 1933, as amended (the “Securities Act”).

To the fullest extent permitted by law, this exclusive forum provision will apply to state and federal law claims, including claims under the federal securities laws, including the Securities Act and the Exchange Act, although our stockholders will not be deemed to have waived our compliance with the federal securities laws and the rules and regulations thereunder. The enforceability of similar exclusive forum provisions in other companies’ certificates of incorporation has been challenged in legal proceedings, and it is possible that, in connection with one or more actions or proceedings described above, a court could rule that one or more parts of the exclusive forum provision in our amended and restated certificate of incorporation is inapplicable or unenforceable.

This exclusive forum provision may limit the ability of our stockholders to bring a claim in a judicial forum that such stockholders find favorable for disputes with the Company or our directors or officers, which may discourage such lawsuits against the Company and our directors and officers. Alternatively, if a court were to find this exclusive forum provision inapplicable to, or unenforceable in respect of, one or more of the specified types of actions or proceedings described above, we may incur additional costs associated with resolving such matters in other jurisdictions, which could negatively affect our business, results of operations and financial condition.

Item 1B. Unresolved Staff Comments.

Not Applicable.

15

Item 1C. Cybersecurity Risk Management, Strategy, Governance, and Incident Disclosure.

We have established policies, standards, processes and practices for assessing, identifying, and managing material risks from cybersecurity threats. We have devoted substantial financial and personnel resources to implement and maintain security measures to meet regulatory requirements, and we intend to continue to make significant investments to maintain the security of our data and cybersecurity infrastructure. There can be no guarantee that our policies and procedures will be properly followed in every instance or that those policies and procedures will be effective. Our risk factors, which can found be found in Item 1A. “Risk Factors,” include further detail about the material cybersecurity risks we face. We have had no cybersecurity incidents to date, and can provide no assurance that there will not be incidents in the future or that they will not materially affect us, including our business strategy, results of operations, or financial condition.

Cyber Risk Management and Strategy

Overview

We employ a risk-based approach to cybersecurity which aligns with corporate strategy, risk management and governance, and adaptable information technology (“IT”) infrastructure. Our cybersecurity program consists of policies, procedures, systems, controls and technology designed to help prevent, identify, detect and mitigate cybersecurity risk and is based on the National Institute of Standards and Technology (“NIST”) Cybersecurity framework.

Collaboration

We have integrated cybersecurity risk management into our overall risk management framework by (i) maintaining disaster recovery, business continuity and security incident recovery plans, (ii) conducting annual enterprise and IT risk assessments, (iii) implementing periodic key risk indicator tracking, and (iv) holding regular cross-departmental meetings to address cybersecurity risks.

Risk Assessment

Our risk management activities and cybersecurity strategy include IT policies, standards, procedures and systems to address and mitigate risks for critical system availability, network integrity, information protection, and operational continuity.

We perform vulnerability and threat monitoring mitigation activities on a regular basis and perform a cybersecurity risk assessment at least annually. Our cybersecurity risk assessment program includes the following assessments and activities:

•ensure program alignment with the NIST Cybersecurity framework; and,

•prioritize, remediate and ensure effectiveness of critical applications, infrastructure, and information.

We regularly collaborate with the Company’s internal audit department and third parties with security and infrastructure expertise for review and evaluation of the Company’s cybersecurity risk program and the associated IT control environment. We engage third-party service providers to perform annual external penetration testing, disaster recovery testing, and security incident simulations.

Infrastructure; Network and Physical Security

Our IT infrastructure is secured and continually monitored using a number of tools to effect physical and logical security. We strictly regulate and limit access to servers and networks. Network access is controlled by the network firewall and restricted by stringent access control lists. We also employ (i) network and endpoint intrusion prevention and detection throughout our infrastructure, (ii) systems that monitor our infrastructure and alert our management of potential cybersecurity issues and vulnerabilities, and (iii) a seasoned process for managing and installing patches for third-party applications.

We have also implemented the following protective and preventative measures:

•identity management and access control safeguards;

•encryption of data in transit and at rest;

16

•system and network security and monitoring;

•information protection and governance; and,

•ongoing systems and equipment maintenance.

Incident Response and Recovery Planning

We have instituted cybersecurity event detection systems, methods, and supporting processes to perform continuous monitoring, identify and classify events and anomalies, take appropriate actions when necessary and report incidents to the appropriate parties. Our response and recovery capabilities are designed to, among other things, contain any impacts, analyze and mitigate events, track events to resolution, provide effective stakeholder communication, recover and resume operations, and evaluate and improve systems and methods.

Third-Party Risk Management

We have implemented and continue to maintain the Company’s IT policies, standards, procedures, and controls to oversee, identify and manage cybersecurity risks associated with all third-party service providers. These include, but are not limited to, an IT acceptable use policy, a records and information management policy, change control procedures, risk and control registry, attestation report reviews, and configuration standards.

Education and Awareness

Our policies require each of our employees to complete annual information security training, in addition to other training requirements. The result is an educated, informed, and prepared workforce, with an awareness of potential cybersecurity threats, how they may occur, and how to report and escalate such matters. These training efforts are supplemented with regular corporate-led communications and outreach initiatives to facilitate cybersecurity awareness and ensure employees remain vigilant and informed about cybersecurity threats and trends.

Governance

Both management and the Board are actively involved in the oversight of risks from cybersecurity threats. TPL’s information security program is designed to ensure that management and the Board are adequately informed about, and provided with the tools necessary to monitor, (i) material risks from cybersecurity threats and (ii) the Company’s efforts related to the prevention, detection, mitigation, and remediation of cybersecurity incidents.

Role of the Board

The Board has delegated to the Audit Committee of the Board (the “Audit Committee”) primary responsibility for overseeing enterprise risk management, including oversight of risks from cybersecurity threats. The Audit Committee periodically reviews TPL’s policies and practices, including incident response plans, for managing cybersecurity risks to ensure that such policies and practices are appropriately tailored to TPL’s risk framework. Throughout the year, the Audit Committee receives quarterly IT and cybersecurity updates unless there is a notable event that requires immediate communication. These quarterly updates include cybersecurity risk assessment updates from TPL’s Director of Information Technology, including key risk indicators, the steps management has taken to monitor and control such cybersecurity risk exposure, and continuous improvement efforts. In addition to the risk management experience of the Audit Committee members, Ms. Duganier holds the CERT Cybersecurity Oversight Certification from Carnegie Mellon University.

Role of Management

TPL’s cybersecurity risk is managed utilizing a multi-tiered approach by the Company’s Director of Information Technology. In addition to the Director of Information Technology, the Company also engages the services of a third party chief information security officer (“CISO”). The qualifications of the Director of Information Technology include over 30 years of IT management, cybersecurity, and information governance experience. The CISO, who reports to the Director of Information Technology, has 21 years of cybersecurity, IT management, and infrastructure consulting experience and is a certified CISO. The Director of Information Technology is regularly informed about the latest developments in cybersecurity,

17

including potential threats, vulnerabilities, and innovative risk management techniques. This ongoing knowledge acquisition is crucial for the effective prevention, detection, mitigation, and remediation of cybersecurity incidents.

The Director of Information Technology oversees risk management and strategy through (i) an IT operating committee (“the IT Operating Committee”) made up of the Director of Information Technology, the CISO, and the Company’s department heads, which is responsible for the establishment and review of the Company’s IT governance, risk management and compliance, and (ii) an IT steering committee (the “IT Steering Committee”) made up of the Company’s executives, which provides guidance and oversight to support and achieve TPL’s IT objectives, including cybersecurity. Both the IT Operating Committee and the IT Steering Committee meet on a quarterly basis. The IT Operating Committee reviews monthly reports on cybersecurity incident prevention, mitigation, detection, and remediation and reviews the Company’s plans and policies related to IT processes on an annual basis. The Director of Information Technology also coordinates with the Company’s internal audit department and the Audit Committee to ensure cybersecurity is represented and addressed within the Company’s enterprise risk management strategy.

18

Item 2. Properties.

As of December 31, 2023, TPL owned the surface estate in 868,446 acres of land, comprised of numerous separate tracts, located in the western part of Texas. There were no material liens or encumbrances on the Company’s title to the surface estate in those tracts. Additionally, the Company also owns a 1/128th NPRI under 84,934 acres of land (5,308 NRA) and a 1/16th NPRI under 370,737 acres of land (185,369 NRA) in the western part of Texas. The following table shows our surface ownership and NPRI ownership by county as of December 31, 2023:

| Number of Acres | ||||||||||||||||||||

| County | Surface | 1/128th Royalty | 1/16th Royalty | |||||||||||||||||

| Andrews | 12,121 | — | — | |||||||||||||||||

| Callahan | — | — | 80 | |||||||||||||||||

| Coke | — | — | 1,183 | |||||||||||||||||

| Concho | 2,592 | — | — | |||||||||||||||||

| Crane | 3,622 | 265 | 5,198 | |||||||||||||||||

| Culberson | 270,893 | — | 111,513 | |||||||||||||||||

| Ector | 19,888 | 33,633 | 11,793 | |||||||||||||||||

| El Paso | 16,613 | — | — | |||||||||||||||||

| Fisher | — | — | 320 | |||||||||||||||||

| Glasscock | 27,227 | 3,600 | 11,111 | |||||||||||||||||

| Howard | 4,788 | 3,099 | 1,840 | |||||||||||||||||

| Hudspeth | 154,247 | — | 1,008 | |||||||||||||||||

| Jeff Davis | 8,293 | — | 7,555 | |||||||||||||||||

| Loving | 63,284 | 6,107 | 48,066 | |||||||||||||||||

| Midland | 28,372 | 12,945 | 13,120 | |||||||||||||||||

| Mitchell | 3,842 | 1,760 | 586 | |||||||||||||||||

| Nolan | 1,600 | 2,488 | 3,157 | |||||||||||||||||

| Palo Pinto | — | — | 800 | |||||||||||||||||

| Pecos | 43,377 | 320 | 16,895 | |||||||||||||||||

| Presidio | — | — | 3,200 | |||||||||||||||||

| Reagan | — | 6,162 | 1,274 | |||||||||||||||||

| Reeves | 187,320 | 3,013 | 116,691 | |||||||||||||||||

| Stephens | — | 2,817 | 160 | |||||||||||||||||

| Sterling | 5,212 | 640 | 2,080 | |||||||||||||||||

| Taylor | 690 | — | 966 | |||||||||||||||||

| Upton | 6,661 | 6,903 | 9,101 | |||||||||||||||||

| Winkler | 7,804 | 1,182 | 3,040 | |||||||||||||||||

| Total | 868,446 | 84,934 | 370,737 | |||||||||||||||||

19

As of December 31, 2023, the Company owned additional royalty interests in the following counties:

| County | Number of Net Royalty Acres(1) | |||||||

| Culberson | 810 | |||||||

| Glasscock | 1,062 | |||||||