UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the fiscal year ended December 31 , 2022

OR

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from ________ to ________

Commission file number 001-39395

(Exact name of registrant as specified in its charter)

| 3711 | ||||||||

| (State or other jurisdiction of incorporation or organization) | (Primary standard industrial classification code number) | (I.R.S. Employer Identification Number) | ||||||

| (Address of Principal Executive Offices) | (Zip Code) | |||||||

(424 ) 276-7616

Registrant's telephone number, including area code

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

Securities registered pursuant to section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | o | Accelerated filer | o | ||||||||

x | Smaller reporting company | ||||||||||

| Emerging growth company | |||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. o

If securities are registered pursuant to Section 12 (b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant's executive officers during the relevant recovery period pursuant to §240.10D-1 (b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No x

Based on the closing price as reported on the Nasdaq Stock Market, the aggregate market value of the registrant’s Common Stock held by non-affiliates on June 30, 2022 (the last business day of the registrant’s most recently completed second fiscal quarter) was approximately $240.2 million. Shares of Common Stock held by each executive officer and director and by each stockholder of more than 10% of any class of voting equity securities of the registrant have been excluded from this calculation because such persons may be deemed to be affiliates. This determination of affiliate status is not necessarily a conclusive determination for other purposes.

As of February 27, 2023, there were 692,971,853 shares of Class A Common Stock, $0.0001 par value, and 64,000,588 shares of Class B Common Stock, $0.0001 par value, issued and outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s proxy statement to be filed with the Securities and Exchange Commission pursuant to Regulation 14A in connection with the registrant’s 2023 Annual Meeting of Stockholders, which will be filed subsequent to the date hereof, are incorporated by reference into Part III of this Form 10-K.

Table of Contents

| Page | ||||||||

Item 1. | Business | |||||||

Item 1A. | Risk Factors | |||||||

2

Part I

Item 1. Business

Unless the context indicates otherwise, references in this Annual Report on Form 10-K to “FFIE” refer to Faraday Future Intelligent Electric Inc. (f/k/a Property Solutions Acquisition Corp.), a holding company incorporated in the State of Delaware, and not to its subsidiaries, and references herein to the “Company,” “FF,” “we,” “us,” “our” and similar terms refer to FFIE and its consolidated subsidiaries. We refer to our primary operating subsidiary in the U.S., Faraday&Future Inc., as “FF U.S.” We refer to all our subsidiaries organized in China (including Hong Kong) collectively as the “PRC Subsidiaries,” a complete list of which is set forth in Exhibit 21.1 to this Annual Report on Form 10-K forms a part. As of February 27, 2023, our only operating subsidiaries in mainland China and in Hong Kong are FF Automotive (China) Co. Ltd., Ruiyu Automotive (Beijing) Co., Ltd. and Shanghai Faran Automotive Technology Co., Ltd., each of which was organized in the PRC. The discussion of FF’s business and the electric vehicle industry below is qualified by, and should be read in conjunction with, the discussion of the risks related to FF’s business and industry detailed elsewhere in this Annual Report on Form 10-K.

Company Overview

FF is a California-based global shared intelligent mobility ecosystem company with a vision to disrupt the automotive industry.

With headquarters in Los Angeles, California, the Company designs and engineers next-generation intelligent, connected, electric vehicles. FF intends to start manufacturing vehicles at its production facility in Hanford, California, with additional future production capacity needs addressed through a contract manufacturing partner in South Korea. FF is also exploring other potential contract manufacturing options in addition to the contract manufacturer in South Korea. The Company has additional engineering, sales, and operational capabilities in China and is exploring opportunities for potential manufacturing capabilities in China through a joint venture or other arrangement.

Since its founding, the Company has created major innovations in technology and products, and a user centered business model. We believe these innovations will enable FF to set new standards in luxury and performance that will enhance quality of life and redefine the future of intelligent mobility.

FFIE is a holding company incorporated in the State of Delaware. As a holding company with no material operations of its own, FFIE conducts its operations through its operating subsidiaries. We currently have a majority of our operations in the U.S. conducted through our U.S.-domiciled operating subsidiaries. We also operate our business in the People’s Republic of China and plan to have significant operations in the future in both Mainland China and Hong Kong (together, “PRC” or “China”) through our subsidiaries organized in the PRC (collectively, the “PRC Subsidiaries”). Investors in FFIE’s Class A Common Stock (the “Class A Common Stock,” and with FFIE’s Class B Common Stock, the “Common Stock”) are investors solely of FFIE, a Delaware holding company. There are various risks associated with our current operating presence in China and the potential expansion of our operations in China (including Hong Kong), which is subject to political and economic influence from China. Recently, the Chinese government initiated a series of regulatory actions and made statements to regulate business operations in China with little advance notice, including cracking down on illegal activities in the securities market, enhancing supervision over China-based companies that seek to conduct offshore securities offering or to be listed overseas, adopting new measures to extend the scope of cybersecurity reviews, and expanding the efforts in anti-monopoly enforcement. Since these statements and regulatory actions are new, it is highly uncertain how soon legislative or administrative regulation-making bodies will respond and what existing or new laws or regulations or detailed implementations and interpretations will be modified or promulgated if any, and the potential impact such modified or new laws and regulations will have on our business operations, our ability to accept foreign investments and to maintain FFIE’s listing on a U.S. exchange. The Chinese government may intervene or influence the operations of our PRC Subsidiaries, or at any time exert more control over offerings conducted overseas and foreign investment in China-based issuers in accordance with PRC laws and regulations, which could result in a material change in our operations and/or a material reduction in the value of our Class A Common Stock and warrants. Additionally, the governmental and regulatory interference could significantly limit or completely hinder our and our investors’ ability to offer or continue to offer our shares of Class A Common Stock to investors and cause the value of such securities to significantly decline or be worthless. For a detailed description of risks related to our PRC operations, see “Risk Factors – Risks Related to FF’s Operations in China.”

3

Technology

FF’s technology innovations include its proprietary Variable Platform Architecture (“VPA”), propulsion system, and Internet, Autonomous Driving, and Intelligence (“I.A.I.”) systems.

The VPA is a modular skateboard-like platform which can be sized to accommodate various motor and powertrain configurations, enabling fast and capital efficient product development for both the passenger and commercial vehicle segments. FF’s propulsion system includes an industry-leading inverter design, and a propulsion system that provides a competitive edge in electric drivetrain performance. FF’s advanced I.A.I. technology offers high-performance computing, high speed internet connectivity, Over-the-air (“OTA”) updates, an open ecosystem for third party application integration, and a Level 3 autonomous driving-ready system, in addition to several other proprietary innovations that enable the Company to build a highly personalized user experience.

FF has recently upgraded the FF 91 Futurist vehicle from PT Gen 1.0 to PT Gen 2.0. This generational upgrade consists of 26 significant upgrades to systems and core components of both the EV area (the vehicle) and the I.A.I area (the advanced core of intelligence, autonomous driving and internet). The 13 key upgrades to the EV area include improvements to the powertrain, battery, charging, chassis, and interior, and the 13 key upgrades to I.A.I. include upgrades in computing, sensing, user interaction, and communication, as well as upgrades to the newest technology. Along with other vehicle performance improvements, FF’s technology is designed to deliver superior acceleration of 2.27 seconds from 0 to 60 mph and safety.

Since inception, FF has developed a differentiated portfolio of valuable intellectual property. As of February 27, 2023, the Company has been granted approximately 660 patents (with approximately a third issued in the U.S., and slightly less than two-thirds issued in China, and the remaining issued in other jurisdictions). These patents are issued to various FFIE entities, including Faraday Future, Faraday & Future, FF Automotive (China) Co., Ltd., Leka Automotive Intelligent Technology (Beijing) Co., Ltd., and LeEco Eco-Car (Zhejiang) Co., Ltd. Key patents include FF’s inverter assembly, integrated drive and motor assemblies, methods and apparatus for generating current commands for an interior permanent magnet (“IPM”) motor, and keyless vehicle entry system. These key patents will expire in 2035 and 2036.

Products

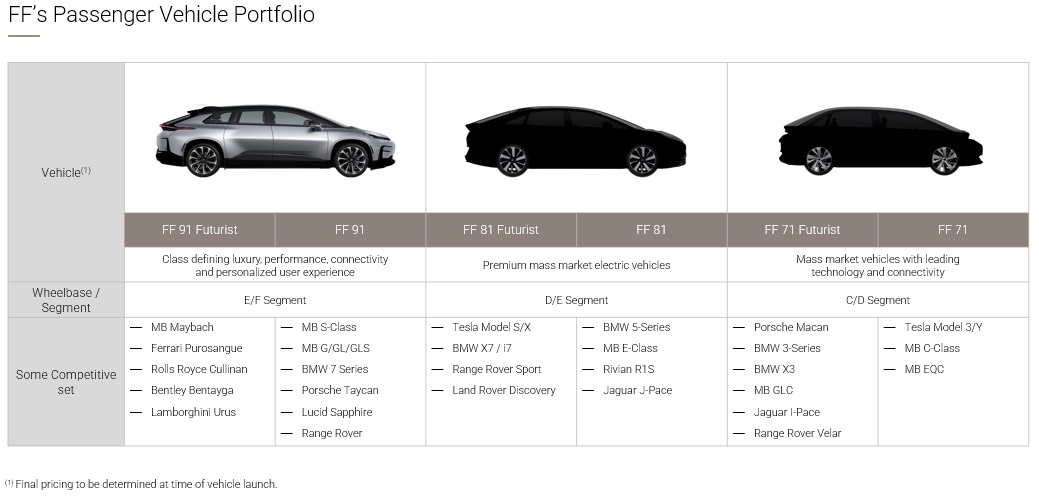

FF’s B2C (business-to-consumer) passenger vehicle pipeline over the next five years includes the FF 91 series, the FF 81 series, and the FF 71 series, each designed to target different passenger vehicle segments. In addition to passenger vehicles, and leveraging its VPA and other proprietary technology, FF plans to produce a Smart Last Mile Delivery (“SLMD”) vehicle to address the high growth last mile delivery market.

Each of the three passenger vehicle series is planned in two different configurations (the FF 91 will also come in a limited edition model). At the top end, the “Futurist” configurations will drive FF’s core brand values (design, superior driving experience, and personalized user experience enabled through FF’s unique I.A.I technologies) to the fullest. Offering multiple configurations allows FF to participate in a wide price range within each vehicle series.

Based on certain management assumptions, including the timely receipt of $38.4 million to $58.4 million of additional funding, which commitments have been secured on February 3, 2023, where the Company entered into an Amendment No. 6 to Securities Purchase Agreement (the “Sixth Amendment”) with FF Simplicity as administrative and collateral agent and Senyun, FF Top, FF Simplicity, FF Prosperity, Acuitas and other purchasers, and approval by stockholders of the proposal to increase FFIE’s authorized shares of Class A Common Stock from 815,000,000 to 1,690,000,000 , increasing the total authorized shares from 900,000,000 to 1,775,000,000 , which approval was obtained during the special meeting of stockholders held on February 28, 2023, timely completion of key equipment installation and commissioning work at the ieFactory California in Hanford, California, suppliers meeting their commitments on program deliverables including parts, the implementation and effectiveness of certain expense reduction and payment delay measures, and timely and successful testing and certification, FF expects start of production of the FF 91 Futurist at the end of March 2023, coming off the line in early April 2023, and deliveries to users anticipated to begin before the end of April 2023. Please refer to “Risk Factors – Risks Related to FF’s Business and Industry – FF’s vehicles are in development and the delivery of FF’s first vehicle has experienced, and may continue to experience, significant delays” for a discussion on risks and uncertainties related to the expected production and delivery. Toward that goal, FF has completed most of its vehicle development milestones, and recently announced Milestone #6, completion of key equipment installation work at the ieFactory California in Hanford, California. The FF 91 series is designed to compete with Maybach, Bentley Bentayga, Lamborghini Urus, Ferrari Purosangue, Mercedes S-Class, Rolls Royce Spectre, Porsche Taycan, BMW 7-Series, etc. In addition to the FF 91 series, FF has planned the following passenger vehicles:

4

| ● | FF 81 series, FF’s second passenger vehicle, is envisioned to be a premium mass market electric connected vehicle positioned to compete against Tesla Model S and Model X, Nio ES8, BMW 5-series, and similar vehicles. | ||||

| ● | FF 71 series, FF’s mass market passenger vehicle, plans to integrate connectivity and advanced technology into a smaller vehicle size and positioned to compete against Tesla Model 3 and Model Y, BMW 3-series, and similar vehicles. | ||||

Product Positioning

All FF passenger vehicles will share common brand “DNA” of:

| ● | Intelligence, Internet and connectivity; | ||||

| ● | modern design: styling; | ||||

| ● | superior driving experience: leading power, performance and driving range; and | ||||

| ● | personalized user experience: space, comfort and internet experience | ||||

The flagship FF 91 series with its recent product and technology upgrade to PT Gen 2.0 will define the FF brand DNA. This DNA will carry over to FF 81 and FF 71 series vehicles at lower price points. With such brand DNA, FF believes its products will be ahead of competition in their respective segments in terms of design, driving experience, interior comfort, connectivity, and user experience.

Robust Hybrid Manufacturing Strategy

To implement a capital light business model, FF has adopted a hybrid global manufacturing strategy consisting of its refurbished manufacturing facility in Hanford, California and a collaboration with Myoung Shin, a contract manufacturing partner in South Korea. FF is also exploring other potential contract manufacturing options in addition to the contract manufacturer agreement in South Korea. The Company is also exploring the possibility of manufacturing capacity in China through a joint venture or other arrangement.

As of the date hereof:

| ● | FFIE leased a 1.1 million square foot manufacturing facility in Hanford, California with an expected production capacity of approximately 10,000 vehicles per year; and | ||||

| ● | FFIE entered into a definitive contract manufacturing and supply agreement with Myoung Shin Co., Ltd. (“Myoung Shin”), a South Korea-based automotive manufacturer and parts supplier, to manufacture the Company’s second vehicle, the FF 81. The agreement has an initial term of nine years from the start of production of the FF 81. Pursuant to the agreement, Myoung Shin shall maintain sufficient manufacturing capabilities and capacity to supply FF 81 vehicles to FF in accordance with the Company’s forecasts and purchase orders. FF and Myoung Shin will each manufacture and supply certain FF 81 parts that Myoung Shin will use in the manufacture and assembly of FF 81 vehicles. | ||||

Distribution Model

FF management anticipates making its first passenger vehicles available in the U.S., followed shortly thereafter by a rollout in China. Expansion of sales to Europe may begin as early as 2024, and additional markets may be added thereafter. FF plans to utilize a direct sales model integrating online and offline sales channels to drive sales and user (including customers, drivers, passengers of FF vehicles) operations to continuously create value. FF’s offline sales are planned through FF’s self-owned stores as well as FF Partner-owned stores and showrooms. The self-owned stores are expected to help establish the FF brand, while the partner-owned stores and showrooms will enable expansion of the sales and distribution network without substantial capital investment by FF.

5

FF’s Competitive Strengths

FF’s products, technology, team and business model provide strong competitive differentiation.

FF’s proprietary VPA

FF’s proprietary VPA is a skateboard-like platform that incorporates the critical components of an electric vehicle, and can be sized to accommodate various motor and powertrain configurations. This flexible modular design supports a range of consumer and commercial vehicles and facilitates rapid development of multiple vehicle programs to reduce cost and time to market.

Projected product performance with industry-leading propulsion technology

FF’s propulsion system includes an industry-leading inverter design and proprietary drive propulsion system. FF’s proprietary FF Echelon Inverter has the technological advantage of driving a large amount of current in a small space using proprietary parallel Insulated Gate Bipolar Transistors (“IGBTs”), achieving low inverter losses and high efficiency. The propulsion system has high torque accuracy with fast transient response. The electric motor drive units are fully integrated with the inverter, transmission and control unit to create industry-leading volume and design efficiency. Propelled by an integrated FF designed powertrain, FF’s vehicles can achieve leading horsepower, efficiency, and acceleration performance as recently attested by the U.S. Environmental Protection Agency (“EPA”) and California’s Air Resources Board (“CARB”) by confirming a range of 381 miles on a single charge and internally measured acceleration of 2.27 seconds from 0 to 60 mph for the FF 91.

Internet, Autonomous Driving, and Intelligence (“I.A.I”) Technology

FF’s advanced I.A.I. technology offers high-performance computing, high speed internet connectivity, OTA updates, an open ecosystem for third party application integration, and a Level 3 autonomous driving-ready system, in addition to several other proprietary innovations that enable the Company to build an advanced highly personalized user experience. The FF 91 series will feature a high-performance dual systems-on-a-chip (“SoC”) computing platform for in-vehicle infotainment, a NVIDIA based autonomous driving system, and a high-speed connectivity system that will be capable of up to three simultaneous 5G connections. Together, these systems will deliver a highly intelligent voice-first user experience, and seamless cloud connectivity and a vehicle that is Level 3 highway autonomous driving ready.

FF’s I.A.I system is built on an enhanced Android Automotive code base and is upgraded with each release of Google’s platform.

All FF vehicles use FF’s proprietary FFID unique identifier to deliver personalized content, apps and experiences. FFID provides a unique FF user profile that ensures a consistent experience across the FF Ecosystem, as the user goes from one seat to another or even from one vehicle to another.

Strong intellectual property portfolio

FF has significant capabilities in the areas of vehicle engineering, vehicle design and development, as well as software, internet, and AI. The Company has also developed a number of proprietary processes, systems and technologies across these areas. FF’s research and development efforts have resulted in a strong intellectual property portfolio across battery, powertrain, software, user interface design and user experience design (“UI/UX”), and advanced driver-assistance systems, among other areas. FF’s proprietary inverter design provides high current and is integrated into the electric drive unit, creating a high power-to-weight ratio. The patented keyless entry technology recognizes the user from a distance, opens (rather than simply unlocking) doors and customizes the user’s seating area using facial-recognition-prompted download of FFID data. Patented autonomous driving technology will allow users to find empty space in a parking lot and autonomously park using cameras, radars, LIDARs (Light Detection and Ranging), ultrasound and an inertial measurement unit (“IMU”) (available after production and delivery via a software upgrade). FF believes its strong intellectual property portfolio will allow continued differentiation from its competitors and shorten time to market for future products.

6

Visionary management with a strong record of success

FF is led by a visionary management team with a unique combination of automotive, communication, and internet experience. FF’s Global CEO, Mr. Xuefeng Chen, is an automotive veteran with international and extensive operational experience with luxury automotive brands, Mr. Xuefeng Chen has spent nearly 20 years in the automotive industry, having worked for Changan Ford, Changan Mazda, Ford Asia Pacific Design Center and Chery Jaguar Land Rover prior to joining FF. FF’s founder and Chief Product and User Ecosystem Officer, Mr. Yueting Jia, focuses on product and mobility ecosystem; internet and AI; and advanced R&D technology. Mr. Jia founded Leshi Information Technology Co., Ltd., a video streaming website in 2004. He also founded Le Holdings Co. Ltd. (“LeEco”), an internet ecosystem and technology company with businesses including smart phones, smart TVs, smart cars, internet sports, video content, internet finance and cloud computing. FF’s other management team members have significant product, industry and leadership experience in areas such as vehicle engineering, battery, powertrain, software, internet, AI, and consumer electronics.

Speed to market

FF has achieved several commercial milestones as it works to bring the FF 91 Futurist to the market. When FF delivers the FF 91 Futurist, the Company expects to be the first entrant in the ultra-luxury EV segment, particularly in light of the recently announced product and technology upgrade to PT Gen 2.0. Please refer to “Risk Factors – Risks Related to FF’s Business and Industry – FF’s vehicles are in development and the delivery of FF’s first vehicle has experienced, and may continue to experience, significant delays” for a discussion on risks and uncertainties related to the expected commercial production and delivery.

Electric Vehicle Industry Overview and Market Opportunity

The electric vehicle industry is poised for explosive growth. Based on the Electric Vehicle Outlook 2022 report, a long-term forecast published by Bloomberg New Energy Finance (“BNEF Report”), which forecasts that passenger electric vehicle sales in the U.S., Europe, China and other regions in the world could grow to a total of approximately 20.6 million vehicles in 2025, from 6.6 million vehicles in 2021, and then continue to grow rapidly.

Driven by China’s new energy vehicle (“NEV”) credit and European CO2 regulations as well as city policies restricting new internal combustion engine (“ICE”) vehicle sales, electric vehicle sales in China and Europe are estimated to exceed 65% of all passenger electric vehicle sales by 2030, according to the BNEF Report. In addition, since many U.S. households have the infrastructure to install home charging, they are ideal adopters of electric vehicles. According to the BNEF Report, by 2040, over three-quarters of all new passenger vehicles sold will be electric, with markets in China and parts of Europe achieving even higher penetration. For commercial electric vehicles, demand for electric small vans, and trucks are expected to rise quickly, with the U. S., Europe, and China markets expanding faster than the overall market, according to the BNEF Report. In addition, the report notes that light-duty commercial vehicles will see the greatest surge in demand for electric drivetrains among all commercial vehicles. FF believes its U.S. and China dual-home market strategy, as well as its innovative DNA, strong technology portfolio, and emphasis on design, driving experience and personalized user experience will position it well in the passenger electric vehicle segments in these markets. By leveraging the scalable design and modularity of FF’s variable platform architecture, FF is well-positioned to capitalize on growing demands for light, commercial electric vehicles. Additionally, FF’s robust vehicle engineering capabilities and extensive portfolio of technologies offer significant future licensing and strategic partnership opportunities.

Key Drivers for Electric Vehicle Market Growth

Several important factors are contributing to the popularity of electric vehicles, in both the passenger electric vehicle and light-duty commercial vehicle segments. FF believes the following factors will continue to drive growth in these markets:

Increasing Environmental Awareness and Tightening Emission Regulations

Environmental concerns have resulted in tightening emission regulations globally, and there is a broad consensus that further emission reductions will require increased electrification in the automotive industry. The cost of regulatory compliance for ICE powertrains is rising sharply due to the natural limitations of traditional ICE technologies. In response, global original equipment manufacturers (“OEMs”) are aggressively shifting their strategies toward electric vehicles. At the same time, consumers are more concerned about the impact of goods they purchase, both on their personal health and the environment. As consumer awareness increases, zero emission transportation has become a popular and widely advocated urban lifestyle which has accelerated further development of the electric vehicle market. Consumer pressure can also be seen in the commercial

7

electric vehicle market. Being encouraged by their customers to reduce their carbon footprints, retailers, logistics companies, and other corporations are highly incentivized to transition their existing fleets or new vehicle purchases toward electric vehicles.

Decreasing Battery and Electric Vehicle Ownership Costs

Battery and battery-related costs generally represent the most expensive components of an electric vehicle. The falling price of lithium-ion batteries is expected to be among the most important factors affecting electric vehicle penetration in the future. Additionally, the average battery energy density is expected to increase with continuous improvements in battery chemistries, improved materials, advanced engineering, and manufacturing efficiencies. With improvements in battery technology and economies of scale, battery production costs (translated to electric vehicle ownership costs) should continue to decrease. The BNEF Report states that the average lithium-ion battery price has fallen by 89% from 2010 to 2021 to $131/kWh. They project the cost of lithium-ion batteries will fall below $100/kWh by 2024 and continue to decline as advancements in manufacturing and technology continue. According to the BNEF Report, price parity between electric vehicles and ICE is expected to be reached by the mid-2020s in most vehicle segments, subject to variation between geographies.

Strong Regulatory Push

An increasing number of countries are encouraging the adoption of electric vehicles or a shift away from fossil-fuel-powered vehicles. For example, in the U.S., both states and municipalities have begun to roll out legislation banning combustion engines, with California mandating that every new passenger car and truck sold to be zero-emission by 2035, and every new medium and heavy-duty truck sold be zero-emission by 2045. Fifteen additional U.S. states and Washington, D.C. have announced they intend to follow California’s lead in transitioning all sales of heavy-duty trucks, vans and buses to zero-emission, with potentially more to follow in coming years. In China, the focused regulatory push has been one of the strongest drivers of NEV penetration. In recent years, the Chinese government implemented a series of favorable policies encouraging the purchase of electric vehicles and construction of electric vehicle charging infrastructure. Since 2015, the Chinese regulatory authorities have provided subsidies to purchasers of electric vehicles. Although previous purchase subsidies were reduced in China by approximately half in 2019, the Chinese government has continued to provide subsidies for charging infrastructure construction. Since 2016, the Chinese central finance department has been incentivizing certain local governments with funds and subsidies for the construction and operation of charging facilities and other relevant charging infrastructure, such as charging stations and battery swap stations. Europe, UK, Denmark, Iceland, Ireland, the Netherlands, Slovenia, and Sweden have all announced plans to phase out combustion engines in some form or fashion by 2030. These legislative tailwinds have already begun to force some legacy OEMs toward electrification, creating a strong need for a modular, flexible, and cost-efficient electric vehicle solution, which will increase competition in the alternative energy vehicle industry.

Growth of Electric “Shared Mobility”

According to the BNEF Report, despite the significant near-term impact from COVID-19, the global shared mobility fleet (i.e., ride-hailing and car-sharing) is expected to represent more than 15% of the total kilometers traveled by passenger vehicles by 2040, up from less than 5% in 2019. Bloomberg data also predicted that due to electric vehicles’ lower operating costs, they are anticipated to account for over 75% of shared mobility vehicles by 2040, representing a dramatic increase from current low single digit penetration. At the same time, as vehicle consumers move to rely upon shared mobility fleets, and view ride-hailing and car-sharing as a service, such trends may partially offset passenger vehicle demand growth.

Corporate History and Milestones

FF U.S., the Company’s primary U.S. operating subsidiary, was incorporated and founded in the State of California in May 2014. In July 2014, LeSee Automotive (Beijing) Co., Ltd. (“LeSee Beijing”), which was previously the Company’s primary Chinese operating entity, was formed in China.

To facilitate global investment of FF’s business and operations in different jurisdictions, FF established a Cayman Islands holding company structure for the entities within the group. As part of these efforts, Smart Technology Holdings Ltd. (formerly known as FF Global Holdings Ltd.) was incorporated on May 23, 2014 in the Cayman Islands, which directly or indirectly owned and/or controlled 100% of the shareholding of all operating subsidiaries in the group. In March 2017, FF established FF Automotive (China) Co., Ltd., as a Chinese wholly-foreign-owned entity (“WFOE”). As part of a broader corporate reorganization, and to facilitate third-party investment, FF incorporated its top-level holding company, FF Intelligent Mobility Global Holdings Ltd. (formerly known as Smart King Ltd.), in the Cayman Islands in November 2017, as the parent company of Smart Technology Holdings Ltd. To enable effective control over FF’s Chinese operating entity and its subsidiaries

8

without direct equity ownership, in November 2017, the WFOE entered into a series of contractual arrangements (“VIE contractual arrangements”) with LeSee Beijing and LeSee Zhile Technology Co., Ltd., which previously held 100% of LeSee Beijing. The VIE contractual arrangement enabled FF to exercise effective control over LeSee Beijing and its subsidiaries, to receive substantially all of the economic benefits of such entities, and to have an exclusive option to purchase all or part of the equity interests in LeSee Beijing. The VIE contractual arrangements were adjusted in the past three years and were terminated on August 5, 2020. LeSee Beijing is currently owned 99% by the WFOE.

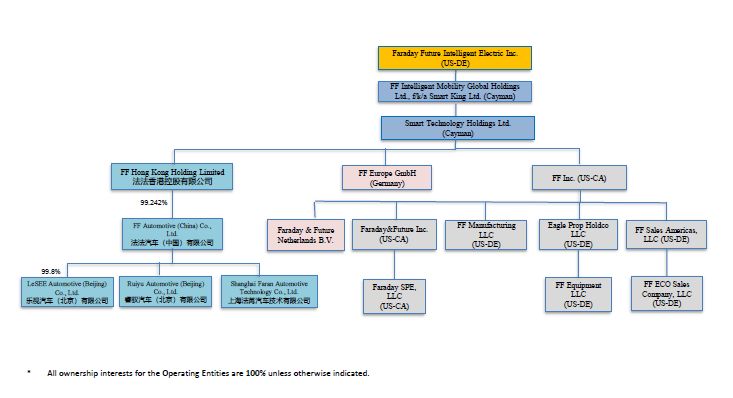

The organizational chart below shows FFIE’s operating subsidiaries* as of the date hereof:

| * | Excludes subsidiaries with immaterial operations. FF Hong Kong Holding Limited is a holding company subsidiary organized in Hong Kong. As of the date hereof, LeSEE Automotive (Beijing) Co. Ltd., a subsidiary organized in China, has immaterial operations. | |||||||

PRC Subsidiaries

FFIE is a holding company incorporated in the State of Delaware. “FF U.S.”, FF’s primary U.S. operating subsidiary, was incorporated and founded in the State of California in May 2014. We refer to all our subsidiaries organized in China (including Hong Kong) collectively as the “PRC Subsidiaries.” A complete list of our subsidiaries is set forth in Exhibit 21.1 to this Annual Report on Form 10-K. As of February 27, 2023, our only operating subsidiaries in China (including Hong Kong) are FF Automotive (China) Co. Ltd., Ruiyu Automotive (Beijing) Co., Ltd. and Shanghai Faran Automotive Technology Co., Ltd., each of which was organized in the PRC.

How Cash is Transferred Through Our Corporate Organization

The PRC has currency and capital transfer regulations that require us to comply with certain requirements for the movement of capital in and out of the PRC. FFIE is able to transfer cash (U.S. Dollars) to the PRC Subsidiaries through capital contributions (increasing FFIE’s capital investment in the PRC Subsidiaries). FFIE may receive cash or assets declared as dividends from the PRC Subsidiaries. The PRC Subsidiaries can transfer funds to each other when necessary, by way of intercompany loans in the following manners:

•FF Hong Kong Holding Limited, as the holding company of all the other PRC Subsidiaries, can transfer cash to any PRC Subsidiary through capital contribution. We note Hong Kong’s banking system is outside PRC mainland’s banking system. As a result, when FF Hong Kong Holding Limited transfers cash to a PRC Subsidiary, it is required to follow the SAFE (as defined below) process and regulation.

9

•FF Hong Kong Holding Limited, as the holding company of all the other PRC Subsidiaries, may receive cash or assets declared as dividends from the other PRC Subsidiaries.

•Among PRC Subsidiaries other than FF Hong Kong Holding Limited, one PRC Subsidiary can provide funds through intercompany loan to another PRC Subsidiary and each such PRC Subsidiary is required to follow the rules of China Banking Regulatory Commission and other relevant Chinese authorities. Additionally, one PRC Subsidiary can transfer cash to its subsidiary through capital contribution, and any PRC Subsidiary may receive cash or assets declared as dividends from any of its subsidiaries.

During 2019, FF Inc., a U.S.-based subsidiary incorporated in California, issued a loan to FF Hong Kong Holding Limited, a holding company subsidiary established in Hong Kong, in the aggregate amount of $1.2 million, which was the only transaction that involved the transfer of cash or assets throughout our corporate structure during 2019. During 2020, LeSee Automotive (Beijing) Co. Ltd., a PRC Subsidiary, assigned to Legacy FF its obligation to pay certain notes issued by a third party in the aggregate principal and accrued interest amount of $26.5 million. Also during 2020, Smart Technology Holdings Ltd., a subsidiary incorporated in the Cayman Islands, transferred to FF Hong Kong Holding Limited $1.7 million in cash, in the aggregate, by way of capital contributions to fund the PRC Subsidiaries’ operations. During 2021, Smart Technology Holdings Ltd. transferred to FF Hong Kong Holding Limited $32.1 million, in the aggregate, by way of capital contributions to fund the operations of the PRC Subsidiaries, including $10.0 million proceeds from the sale of PIPE Shares. In August 2021, Legacy FF extended a loan of $50.0 million to FF Automotive (Zhuhai) Co. Ltd., a PRC Subsidiary, for the purpose of acquiring a technology license agreement with a third party. We transferred cash or assets of $9.1 million from Smart Technology Holdings Ltd. to FF Hong Kong Holding Limited during the fourth quarter of 2021. In 2022 and 2023 to date, FF U.S. extended loans in an aggregated amount of $8.0 million and $3.0 million, respectively, to FF Hong Kong Holding Limited to fund the operations of the PRC Subsidiaries. We will continue to assess the PRC Subsidiaries’ requirements to fund their operations and intend to effect additional contributions as appropriate. As of February 27, 2023, our only operating subsidiaries in China (including Hong Kong) are FF Automotive (China) Co. Ltd., Ruiyu Automotive (Beijing) Co., Ltd. and Shanghai Faran Automotive Technology Co., Ltd., each of which was organized in the PRC. The PRC Subsidiaries have not transferred cash or other assets to FFIE, including by way of dividends. FFIE does not currently plan or anticipate transferring cash or other assets from our operations in China to any non-Chinese entity.

Capital contributions to PRC companies are mainly governed by the Company Law and Foreign Investment Law of the People’s Republic of China, and the dividends and distributions from the PRC Subsidiaries are subject to regulations and restrictions of the PRC on dividends and payment to parties outside of the PRC. Applicable PRC law permits payment of dividends to FFIE by our PRC Subsidiaries only out of their net income, if any, determined in accordance with PRC accounting standards and regulations. Our operating PRC Subsidiaries are required to set aside a portion of their net income, if any, each year to fund general reserves for appropriations until such reserves have reached 50% of the relevant entity’s registered capital. These reserves are not distributable as cash dividends. A PRC company is not permitted to distribute any profits until any losses from prior fiscal years have been offset. Profits retained from prior fiscal years may be distributed together with distributable profits from the current fiscal year. In addition, registered share capital and capital reserve accounts are also restricted from withdrawal in the PRC, up to the amount of net assets held in each operating subsidiary.

PRC Restrictions on Foreign Exchange and Transfer of Cash

Under PRC laws, if certain procedural requirements are satisfied, the payment of current account items, including profit distributions and trade and service related foreign exchange transactions, can be made in foreign currencies between entities, across borders, and to U.S. investors without prior approval from State Administration of Foreign Exchange (the “SAFE”) or its local branches. However, where Chinese Yuan (“CNY”) is to be converted into foreign currency and remitted out of China to pay capital expenses, such as the repayment of loans denominated in foreign currencies, approval from or registration with SAFE or its authorized banks is required. The PRC government may take measures at its discretion from time to time to restrict access to foreign currencies for current account or capital account transactions. If the foreign exchange control system prevents our PRC Subsidiaries from obtaining sufficient foreign currencies to satisfy their foreign currency demands, our PRC Subsidiaries may not be able to pay dividends in foreign currencies to FFIE. Further, we cannot assure you that new regulations or policies will not be promulgated in the future that would have the effect of further restricting the remittance of CNY into or out of the PRC. We cannot assure you, in light of the restrictions in place, or any amendment thereof, that the PRC Subsidiaries will be able to fund their future activities which are conducted in foreign currencies, including the payment of dividends.

10

Furthermore, under PRC laws, dividends may be paid only out of distributable profits. Distributable profits are the net profit as determined under PRC GAAP, less any recovery of accumulated losses and appropriations to statutory and other reserves required to be made. Our PRC Subsidiaries shall appropriate 10% of the net profits as reported in their statutory financial statements (after offsetting any prior year’s losses) to the statutory surplus reserves until the reserves have reached 50% of their registered capital. As a result, our PRC Subsidiaries may not have sufficient, or any, distributable profits to pay dividends to us. See “Risk Factors–Risks Related to FF’s Operations in China–FFIE is a holding company and, in the future, may rely on dividends and other distributions on equity paid by the PRC Subsidiaries to fund any cash and financing requirements that FFIE may have, and the restrictions on PRC Subsidiaries’ ability to pay dividends or make other payments to FFIE could restrict FFIE’s ability to satisfy its liquidity requirements and have a material adverse effect on FFIE’s ability to conduct its business” for a more detailed discussion of the relevant risks relating to restrictions on foreign exchange and transfer of cash.

Requirements Under PRC Laws and Regulations

Under current PRC laws and regulations, each of our PRC Subsidiaries is required to obtain a business license to operate in the PRC. Our PRC Subsidiaries have all received the requisite business license to operate, and no application for business license had been denied.

As our operations in the PRC expand, our PRC Subsidiaries will be required to obtain approvals, licenses, permits and registrations from PRC regulatory authorities, such as the State Administration for Market Regulation, the National Development and Reform Commission, Ministry of Commerce (“MOFCOM”), and the Ministry of Industry and Information Technology (“MIIT”), which oversee different aspects of the electric vehicle business. As of February 27, 2023, no application by our PRC Subsidiaries for any such approvals, licenses, permits and registrations that are currently applicable to them had been denied, but there can be no assurance that the PRC Subsidiaries will be able to maintain their existing licenses or obtain new ones. See “Risk Factors–Risks Related to FF’s Operations in China–FF may be adversely affected by the complexity, uncertainties and changes in PRC regulations on internet-related business, automotive businesses and other business carried out by FF’s PRC Subsidiaries.” for a more detailed discussion of the risks relevant to the regulations relating to the operations of the PRC Subsidiaries.

We do not believe any permission is required from any Chinese authorities (including the China Securities Regulatory Commission (the “CSRC”) and the Cyberspace Administration of China (the “CAC”)) in connection with our previous offerings or listing. We do not and immediately prior to the filing of this Annual Report on Form 10-K, will not possess over one million of PRC-based individual’s personal information. After consulting our PRC counsel, Fangda Partners, we believe we are currently not subject to the requirement under the Cybersecurity Review Measures that a network platform operator which possesses more than one million users’ personal information must apply for a cybersecurity review with CAC before listing abroad. In addition, as of February 27, 2023, after consulting our PRC counsel, we are not aware of any other laws or regulations currently effective in the PRC which explicitly require us to obtain any permission from the CSRC or other Chinese authorities for our previous offering or listing, nor had we received any inquiry, notice, or warning from the CSRC or any other Chinese authorities in such respects. The PRC authorities have promulgated new or proposed laws and regulations recently to further regulate securities offerings that are conducted overseas and/or foreign investment in China-based issuers. According to these new laws and regulations and the draft laws and regulations if enacted in their current forms, in connection with our future securities offering activities, we may be required to fulfill filing, reporting procedures with the CSRC, and may be required to go through cybersecurity review by the PRC authorities. However, there are uncertainties with respect to whether we will be able to fully comply with requirements to obtain such permissions and approvals from, or complete such reporting or filing procedures with PRC authorities. For more detailed information, see “Risk Factors–Risks Related to FF’s Operations in China–The approval of, or filing or other administrative procedures with, the CSRC or other PRC governmental authorities may be required in connection with certain of our financing activities, and, if required, we cannot predict if we will be able to obtain such approval or complete such filing or other administrative procedures” and “Risk Factors–Risks Related to FF’s Operations in China–We face challenges from the evolving regulatory environment regarding cybersecurity, information security, privacy and data protection. Many of these laws and regulations are subject to change and uncertain interpretation, and any actual or alleged failure to comply with related laws and regulations regarding cybersecurity, information security, data privacy and protection could materially and adversely affect our business and results of operations” for a more detailed discussion of the relevant risks relating to the applicable of PRC laws and Regulations.

11

Risks Related to FF’s Operations in China

FF operates in China, and plans to have significant operations in the future in China (including Hong Kong) through its PRC Subsidiaries, and faces various legal and operational risks associated with doing business in China, which could result in a material change in the operations of our PRC Subsidiaries, cause the value of FFIE’s securities to significantly decline or become worthless, and significantly limit or completely hinder FF’s ability to accept foreign investments, and FFIE’s and our investors’ ability to offer or continue to offer our shares of Class A Common Stock to investors. FF also faces similar risks related to its expansion plans in Hong Kong, which is subject to political and economic influence from China. These risks, each discussed in detail in the section “Risk Factors–Risks Related to FF’s Operations in China” include:

•Changes in the political and economic policies of the PRC government may materially and adversely affect FF.

•Uncertainties with respect to the Chinese legal system, regulations and enforcement policies could have a material adverse effect on FF.

•Foreign currency fluctuations could reduce the value of our Common Stock and dividends paid on our Common Stock.

•Changes in the laws and regulations of China or noncompliance with them could adversely affect FF.

•Restrictions on PRC Subsidiaries’ ability to pay dividends or make other payments to FFIE in the future could restrict FFIE’s ability to satisfy its liquidity requirements and have a material adverse effect on FFIE’s business.

•FFIE may be classified as a PRC “resident enterprise,” which would likely result in unfavorable tax consequences to FFIE and its non-PRC enterprise stockholders.

•FFIE and its stockholders face uncertainty with respect to indirect transfers of equity interests in China resident enterprises through transfer of non-Chinese-holding companies.

•PRC regulation of loans to and direct investments in PRC entities may delay or prevent us from making loans or additional capital contributions to our PRC Subsidiaries.

•The PRC government can take regulatory actions and make statements to regulate business operations in China with little advance notice, so our assertions and beliefs of the risks imposed by the Chinese legal and regulatory system cannot be certain, and actions related to oversight and control over offerings that are conducted overseas and/or foreign investment in issuers with substantial operations in China could significantly limit or completely hinder our and our investors’ ability to offer or continue to offer shares of Class A Common Stock $0.0001 par value, and warrants to purchase shares of Class A Common Stock to investors and cause the value of our securities to significantly decline or be worthless.

•The approval of, or filing or other administrative procedures with, the CSRC or other PRC governmental authorities may be required in connection with certain of our financing activities, and, if required, we cannot predict if we will be able to obtain such approval or complete such filing or other administrative procedures.

•Certain PRC rules and regulations establish complex procedures for some acquisitions by foreign investors, which could make it more difficult for us to grow in China.

•FF may be adversely affected by the complexity, uncertainties and changes in PRC regulations on internet-related business, automotive businesses and other business carried out by FF’s PRC Subsidiaries.

12

•We face challenges from the evolving regulatory environment regarding cybersecurity, information security, privacy and data protection.

•In the event that the independent auditor operating in China that FF engages for its operations in China is not permitted to be subject to inspection by the Public Company Accounting Oversight Board (“PCAOB”), then investors may be deprived of the benefits of such inspection.

•U.S. regulatory bodies may be limited in their ability to conduct investigations or inspections of our operations in China.

•There may be difficulties in effecting service of legal process, conducting investigations, collecting evidence, enforcing foreign judgments or bringing actions in China against us and our management.

Milestones

Significant milestones in FF’s historical development and commercialization of FF’s electric vehicles include the following:

| ● | In 2015, FF completed its first test mule car, and a fully developed electric vehicle Beta prototype was completed in August 2016. | ||||

| ● | In January 2016, FF debuted the FF Zero 1 at the 2016 Consumer Electronics Show (“CES”) and obtained a U.S. patent for FF’s proprietary power inverter, the “FF Echelon Inverter.” In November 2016, FF obtained an autonomous vehicle testing permit issued by the State of California, which allowed FF to test self-driving vehicles on public roads with the presence of a safety driver. | ||||

| ● | In January 2017, FF revealed FF 91, its luxury electric crossover vehicle, at CES 2017. FF 91’s beta prototype set the fastest production-electric vehicle record at the Pikes Peak International Hill Climb in 2017, with a time of 11 minutes and 25.083 seconds. | ||||

| ● | In November 2017, FF entered into agreements with its Series A investor in connection with its Series A financing and received gross proceeds of $800.0 million through June 2018. | ||||

| ● | In August 2018, FF completed its first pre-production build of FF 91 in its Hanford, California manufacturing facility. FF also began designing the FF 81 project in January 2018. | ||||

| ● | In January 2021, Legacy FF, FF Automotive (Zhuhai) Co., Ltd. and FF Hong Kong Holding Limited entered into a cooperation framework agreement with Zhejiang Geely Holding Group Co., Ltd. pursuant to which Geely Holding agreed to explore the possibility of joint investment in the technology licensing, contract manufacturing and joint venture with FF and the city, as well as to pursue the possibility of further business cooperation with the joint venture. The joint venture and contract manufacturing projects with Geely Holding are on hold. | ||||

| ● | In January 2021, FF announced that it entered into a definitive agreement for a business combination with PSAC, with the combined company to be listed on The Nasdaq Stock Market under the ticker symbol “FFIE”. | ||||

| ● | In July 2021, FF announced that it completed its previously announced merger with PSAC, which resulted in the combined company being renamed Faraday Future Intelligent Electric. The Class A Common Stock and Public Warrants of the Company began trading on The Nasdaq Stock Market on July 22, 2021 as “FFIE” and “FFIEW,” respectively. | ||||

| ● | In September 2021, FF completed the installation of pilot equipment in the pre-production build area of its Hanford, California facility. | ||||

13

| ● | In October 2021, FF received its final Certificate of Occupancy (“CO”) for a dedicated area for pre-production manufacturing at the facility in Hanford, California. | ||||

| ● | In December 2021, FF started foundation construction for all remaining production areas in the Hanford facility, including body, propulsion, warehouse and vehicle assembly. Interior foundation work in the production area is complete, major mechanical systems, including electrical and plumbing, have been installed and equipment installation is underway. | ||||

| ● | In February 2022, FF announced that Myoung Shin had been contracted to manufacture FF’s second vehicle, the FF 81, with SOP scheduled for as early as 2024. | ||||

| ● | In February 2022, FF unveiled the first production-intent FF 91 EV manufactured at its Hanford, California plant. | ||||

| ● | In April 2022, FF signed a sourcing agreement for battery packs for the FF 91 with a leading global battery supplier and innovator in lithium-ion technology. The FF 91 battery pack will feature state-of-the-art technology designed to deliver superior power, energy, and charging speeds. | ||||

| ● | In May 2022, FF marked Production Milestone #5 at its Hanford, California manufacturing facility, with the start of installation of all mechanical, electrical and plumbing systems to support equipment installation. | ||||

| ● | In May 2022, FF announced its Flagship brand experience center, to be located in Beverly Hills, California where visitors can experience the brand’s advanced technology, distinctive luxury, and futuristic design. | ||||

| ● | In August 2022, FF announced its sponsorship and attendance at the 2022 Pebble Beach Concours d’Elegance taking place from August 18-21, 2022. FF’s flagship FF 91 EV was available for demo rides and made a special appearance on the Concept Lawn on August 21, 2022. | ||||

| ● | In September 2022, FF announced the FF 91 Futurist, the Ultimate Intelligent TechLuxury EV, was officially certified to have a robust rating of 381 miles of EV range from the U.S. Environmental Protection Agency. | ||||

| ● | In November, 2022, FF announced the CARB has certified the FF 91 Futurist as a zero-emissions vehicle (ZEV). The ZEV program is part of CARB’s Advanced Clean Cars package of coordinated standards that control smog-causing pollutants and greenhouse gas emissions of passenger vehicles in California. | ||||

| ● | In November 2022, FF announced Production Milestone #6, completion of key equipment installation work at its Hanford, California manufacturing Facility. | ||||

| ● | On December 15, 2022, FF hosted a Global Investor Business Update meeting, announcing plans to start production of FF 91 Futurist in March 2023 (subject to various management assumptions disclosed elsewhere in this Annual Report on Form 10-K), financing progress and completion of product upgrades. On February 20, 2023, FF announced that March 30, 2023 as its target start of production date, assuming timely receipt of funds from investors. | ||||

| ● | On January 17, 2023, FF announced that, in the third quarter of fiscal year 2022, it had reached a non-binding Cooperation Framework Agreement with the government of the City of Huanggang in Hubei Province, China (“Huanggang”), for promoting FF’s U.S.-China dual-home market strategy. According to the Cooperation Framework Agreement, FF intends to relocate its FF China headquarters to Huanggang, while maintaining its global headquarters in Los Angeles, California. | ||||

14

Partnership Program

Acting through FF Global Partners LLC (“FF Global”), a major shareholder of the Company, in July 2019 certain current and former executives of the Company established an arrangement which they refer to as the “Partnership Program.” FF Global beneficially owns approximately 15.4% of the voting power of the Company’s fully diluted Common Stock. As described below, the Partnership Program provides financial benefits to certain Company directors, management and employees, which they are required to report to the Company pursuant to the Company’s Investment Reporting Policy. The Partnership Program is administered by FF Global and is not under the Company’s supervision.

Purpose of Partnership Program

The purpose of the Partnership Program is to help the Company and FF Global succeed, including by helping key Company employees remain aligned with the Company’s mission, interests and economic success, by awarding units representing membership interests in FF Global to such individuals. We have been advised by FF Global that the secretary of FF Global provides recommendations to the FF Global Board of Managers regarding proposed awards based on, among other things:

| ● | the individual’s position in the Company and/or FF Global, | ||||

| ● | the importance of the individual’s role in the Company and/or FF Global, | ||||

| ● | the individual’s historical contributions to the Company and/or FF Global, | ||||

| ● | the importance of the individual to the achievement of the Company’s and FF Global’s strategic objectives, | ||||

| ● | the individual’s awards under the Company’s employee stock option plan, and | ||||

| ● | the individual’s existing holdings of FF Global units. | ||||

The awards under the Partnership Program have in the past been granted exclusively to current or former employees of the Company or its affiliates, FF Global may in the future determine to grant awards to individuals who are not affiliated with the Company.

Pursuant to our Investment Reporting Policy, members of our management and other employees are required to report information relating to their investments, including their interests in FF Global. However, since the Company’s board of directors (the “Board”) does not have oversight over the Partnership Program, the Company is not able to assess whether awards made by FF Global under the Partnership Program incentivize management and employee behavior and activities that the Company intends to incentivize, or indeed, whether the Partnership Program effectively works against efforts by the Company to manage its workforce. For example, as part of the special committee of independent directors established by the Board to investigate allegations of inaccurate Company disclosures (“Special Committee”), as further discussed below, it was determined that a Company employee who is also a beneficiary under the Partnership Program deliberately interfered with the Special Committee’s investigation. Although the Company disciplined this employee, the effectiveness of the Company’s disciplinary efforts may have been counteracted by awards this employee has received or expects to receive under the Partnership Program.

Terms of Awards

FF Global units awarded under the Partnership Program are purchased by the recipient from FF Global. The recipient pays the purchase price for their common units in 10 annual installments. The units entitle the recipient to receive distributions from FF Global when and if declared by the FF Global Board of Managers on a pro rata basis based on their paid-in capital (after their contributions are all returned). FF Global units are subject to redemption in certain cases, including upon termination of employment with FF Global or the Company or any of their affiliates, at a redemption price that generally is no lower than the unreturned capital contributions.

15

Scope of Partnership Program

FF Global has informed us that to date a total of 34 individuals have received awards under the Partnership Program, that 19 individuals continue to hold such awards, and that all recipients of such awards are current or former directors or employees of the Company or its affiliates. Some of these individuals are or were members of the FF Global Board of Managers. In particular, we understand that (amounts below in single dollars):

| ● | Dr. Carsten Breitfeld, FF’s former Global CEO and a former director of FFIE, was a non-voting member of the FF Global Board of Managers until May 2022, and previously held FF Global units. In connection with Dr. Breitfeld’s voluntary resignation from FF Global in May 2022 to avoid any potential conflicts of interest, Dr. Breitfeld forfeited his 13,000,000 FF Global units. On November 26, 2022, the Board voted to remove Dr. Breitfeld as Global CEO and, on December 26, 2022, Dr. Breitfeld tendered his resignation from the Board, which was effective immediately. | ||||

| ● | Matthias Aydt, our Senior Vice President, Product Execution and a director of FFIE, was a member of the FF Global Board of Managers until June 2022, and previously held FF Global units. According to information provided by Mr. Ruokun Jia, a nephew of Mr. Jia who was formerly an Assistant Treasurer of FFIE but who was terminated for conduct during the Special Committee’s investigation, Dream Sunrise is owned by an associate of him. On June 26, 2019, to finance his acquisition of the FF Global units and his then concurrent loan to FF Global in the original principal amount of $4,257,791.97, Mr. Aydt issued a note in the original principal amount of $4,624,391.97 to Dream Sunrise LLC (“Dream Sunrise”). On August 2, 2021, FF Global paid down its loan obligations to Mr. Aydt by $2,071,721.72, by paying down Mr. Aydt’s loan obligations to Dream Sunrise by the same amount, evidenced by that certain Repayment Agreement, dated as of March 7, 2022, by and among Dream Sunrise, FF Global and Mr. Aydt, an amended and restated note dated as of March 7, 2022 from FF Global to Mr. Aydt in the principal amount of $2,186,070.25 (the “Aydt-FF Global Note”), replacing the prior note issued by FF Global to Mr. Aydt on June 26, 2019 in its entirety, and an amended and restated note dated as of March 7, 2022 from Mr. Aydt to Dream Sunrise in the principal amount of $2,552,670.25 (the “Dream Sunrise-Aydt Note”), replacing the prior note issued by Mr. Aydt to Dream Sunrise on June 26, 2019 in its entirety. In order to avoid any potential conflicts of interest that his ownership of FF Global units presents toward his role as a director of FFIE, in June 2022, Mr. Aydt requested that FF Global redeem in full all of his FF Global units. On July 8, 2022, FF Global, Dream Sunrise and Mr. Aydt entered into an Redemption Agreement, pursuant to which in exchange for FF Global’s redemption in full of all of Mr. Aydt’s FF Global units and in satisfaction of all of FF Global’s then outstanding loan obligations to Mr. Aydt under the Aydt-FF Global Note, other than $87,742.95, which represents interests accrued on $366,600 of the principal amount under the Dream Sunrise-Aydt Note, FF Global assumed all of Mr. Aydt’s then outstanding loan obligations under the Dream Sunrise-Aydt Note. As of February 27, 2023, the $87,742.95 that Mr. Aydt owes to Dream Sunrise remains outstanding. | ||||

16

| ● | Qing Ye, former director of FFIE and former Vice President of Business Development and FF PAR, previously held FF Global units. On June 26, 2019, to finance his acquisition of the FF Global units and his then concurrent loan to FF Global in the original principal amount of $1,993,009.01, Mr. Ye issued a note in the original principal amount of $2,164,609.01 to Dream Sunrise. On June 13, 2022, FF Global paid down its loan obligations to Mr. Ye by $969,742.08, by paying down Mr. Ye’s loan obligations to Dream Sunrise by the same amount, evidenced by an amended and restated note dated as of June 13, 2022 from FF Global to Mr. Ye in the principal amount of $1,023,266.93 (the “Ye-FF Global Note”), replacing the prior note issued by FF Global to Mr. Ye on June 26, 2019 in its entirety, and an amended and restated note dated as of June 13, 2022 from Mr. Ye to Dream Sunrise in the principal amount of $1,194,866.93 (the “Dream Sunrise-Ye Note”), replacing the prior note issued by Mr. Ye to Dream Sunrise on June 26, 2019 in its entirety. In order to avoid any potential conflicts of interest that his ownership of FF Global units presents towards his role as a director of FFIE, in June 2022, Mr. Ye requested that FF Global redeem in full all of his FF Global units. On June 24, 2022, FF Global, Dream Sunrise and Mr. Ye entered into an Redemption Agreement, pursuant to which in exchange for FF Global’s redemption in full of all of Mr. Ye’s FF Global units and in satisfaction of all of FF Global’s then outstanding loan obligations to Mr. Ye under the Ye-FF Global Note, other than $41,071.17, which represents interests accrued on $171,600 of the principal amount under the Dream Sunrise-Ye Note, FF Global assumed all of Mr. Ye’s then outstanding loan obligations under the Dream Sunrise-Ye Note. As of February 27, 2023, the $41,071.17 that Mr. Ye owes to Dream Sunrise remains outstanding. On January 25, 2023, Mr. Ye resigned as a member of the Board. Mr. Ye remains a consultant of the Company as an independent contractor until November 18, 2023, at which time both parties will mutually reassess the relationship. | ||||

| ● | Robert Kruse, FF’s former Senior Vice President, Product Execution, previously held 1,500,000 FF Global units. On November 29, 2022, Mr. Kruse resigned from the Company. | ||||

| ● | Chui Tin Mok, our Global Executive Vice President and the Global Head of User Ecosystem and a director of FFIE (effective January 25, 2023), currently holds 780,000 FF Global units. On June 26, 2019, to finance his acquisition of the FF Global units and his then concurrent loan to FF Global in the original principal amount of $2,264,782.96, Mr. Mok issued a note in the original principal amount of $2,459,782.96 to Dream Sunrise. In May 2022, Mr. Mok returned 3,120,000 of his FF Global units to FF Global pursuant to amendments to the governance documents of FF Global. On March 7, 2022, FF Global paid down its loan obligations to Mr. Mok by $1,101,979.63, by paying down Mr. Mok’s loan obligations to Dream Sunrise by the same amount, evidenced by an amended and restated note dated as of March 7, 2022 from FF Global to Mr. Mok in the principal amount of $1,162,803.33, replacing the prior note issued by FF Global to Mr. Mok on June 26, 2019 in its entirety, and an amended and restated note dated as of March 7, 2022 from Mr. Mok to Dream Sunrise in the principal amount of $1,357,803.33, replacing the prior note issued by Mr. Mok to Dream Sunrise on June 26, 2019 in its entirety. | ||||

| ● | Hong Rao, our Vice President of I.A.I. (Internet, Autonomous Driving, Intelligence), currently holds 100,000 FF Global units. | ||||

| ● | In addition to the loans described above with respect to Mr. Aydt and Mr. Ye, a number of our other current and former employees have used funds loaned by Dream Sunrise to fund the purchase of their FF Global units and their concurrent loans to FF Global, including Chui Tin Mok and Jerry Wang. | ||||

Moreover, based on information provided by Mr. Xuefeng Chen and FF Global, pursuant to an offer letter between them dated January 20, 2021, Mr. Xuefeng Chen will become an FF Global partner if he subscribes and pays for 5,000,000 FF Global units and 2,500,000 performance-based units at a subscription price currently set at $0.50 per unit (which could be subject to adjustment based on FFIE’s stock price).

17

FF Technology

Variable Platform Architecture

FF believes one of its core technology competencies is its proprietary Variable Platform Architecture (“VPA”). FF’s VPA is a flexible and adaptable skateboard-like platform featuring a monocoque vehicle structure with integrated chassis and body. The platform directly houses the critical components of an electric vehicle, including all-wheel steering, suspension system, brakes, wheels, electric propulsion system, electronic control units and high voltage battery, among others. Each of these component systems has been engineered in-house or in collaboration with suppliers and has been integrated into the FF vehicle design with a view to strive for optimizing performance, efficient packaging, and functional integration.

As an integrated structure, the skateboard-like platform can be shortened or lengthened to allow various wheelbases and battery pack sizes along with other options to fit into the platform. It is designed to accommodate up to three motors and support single or dual rear motors and a single front motor. The VPA can be configured in front-wheel-drive (“FWD”), rear-wheel-drive (“RWD”) or all-wheel-drive (“AWD”) configurations. The platform enables scalable vehicle design and improves manufacturing flexibility as well as capital efficiency and allows continuous improvement across product generations. It is also designed to reduce development time for future models leveraging the platform, as most of research and development and a significant portion of the crash structure is integrated into the platform and enables five star and equivalent safety performance. The modular design of the VPA is adaptable to support a wide range of FF vehicles for both consumer and commercial vehicle markets.

Propulsion Technology

FF has designed an integrated set of powertrain systems ideally suited for FF’s modular VPA, which has been recently upgraded to PT Gen 2.0 to further enhance performance. FF believes its proprietary and patented designed electric powertrain provides a competitive edge in horsepower, efficiency, and acceleration performance.

FF Echelon Inverter

The inverter in FF’s electric vehicle powertrain governs the flow of high-voltage electrical current throughout the vehicle and serves to power the electric motor, generating torque while driving and delivering energy into the battery pack while braking. The inverter converts direct current from the battery pack into alternating current to drive the permanent magnet motors and provides “regenerative braking” functionality, which captures energy from braking to charge the battery pack. The primary technological advantages of FF’s designs include the ability to drive large amounts of current in a small, physical package with high efficiency and low cost (low inverter losses to provide 98% of inverter efficiency) utilizing patented parallel IGBT technology and can achieve high torque accuracy with fast transient response. The inverter can achieve high reliability due to tab bonds in the high current path. The monitoring system is integrated into the inverter to provide enhanced safety. The patented FF Echelon Inverter is designed to have high power in a compact light weight package with high reliability and durability and can support multiple motor configurations.

Integrated Electric Motor Drive Units

FF designed its electric motor drive units (including gearbox). The electric drive units are fully integrated with the inverter, transmission, and control unit to create a compact and efficient design. The FF designed drive units have low noise and vibration that can greatly improve driving experience. Depending on the power requirements of each model, the motors can be utilized individually or in two or three motor configurations. The FF 91 Futurist, equipped with three integrated electric drive units (each is designed to deliver up to 350 horsepower), is expected to deliver 1,050 horsepower and 12,510 Newton meters (“Nm”) of torque. FF believes its electric drive unit design is ahead of many of its competitors in terms of performance because of its proprietary, advanced packaging, stator-rotor design, and unique inverter layout.

Internet, Autonomous Driving, and Intelligence (“I.A.I.”)

FF utilizes an industry-leading automotive grade dual-chip computing system running the Android Automotive operating system. FF’s I.A.I system is built on an enhanced Android Automotive code base and is upgraded with each release of Google’s platform. FF’s vehicles are designed with software OTA capabilities, which allow software and applications in the vehicle to be updated and upgraded wirelessly to deliver continuous enhancements. The vehicle is designed to be connected to FF’s information cloud at all times. When there is a firmware or software update available, FF’s cloud will push an update message to the vehicle to notify the driver to schedule an update. Upgrades will be wirelessly downloaded to the vehicle, installed, and

18

enabled, including updates for firmware, operating systems, middleware, and applications. FF’s patented Future OS operating system allows multiple users to login through FF 91, preparing user’s preferences per their cloud based FFID profiles.

For autonomous driving, FF’s Level 3 autonomous driving-ready system (“ADAS”) will deliver multiple ADAS features through a combination of FF’s own as well as industry partners’ applications. FF plans to devote resources to autonomous driving research and development and plans to work with partners to deliver full autonomous-driving capabilities in highway and urban driving, as well as parking, across its vehicle lines in the future.

FF’s Artificial Intelligence system can actively learn preferences, habits, entertainment, and navigation routines of a user, and associates them with the user’s unique FFID (FF proprietary user ID). FFID provides a unique FF user profile that ensures a consistent experience across the FF Ecosystem, as the user goes from one seat to another or even from one vehicle to another. The seamless design and interface of the in-vehicle infotainment system planned in FF vehicles will offer multiple human-machine interface (“HMI”) options and facilitate a personalized user experience for each seat in the vehicle. The enhanced user experience platform powered by Android enables seamless access to third party applications. FF’s patented Intelligent Aggregation Engine can pull content from multiple video applications and displays content in a single area, removing the need to access multiple applications. The Intelligent Recommendation Engine that may be integrated in certain FF series learns each passenger or driver’s digital media preferences across multiple video applications and provide personalized recommendations. The User Recognition function is embedded in each seat through facial or voice recognition, to deliver a suite of personalized content and preferences.

Electrical/ Electronic (“E/E”) Architecture

FF has designed the first generation of FF vehicle series (FF 91) with a domain-centralized E/E architecture, which enables architecture flexibility and maximizes performance efficiency while meaningfully reducing the overall system complexity and weight. The domain-centralized E/E architecture will consolidate the domain functions across five core high-performance domain control units (“DCU”) that manage, compute, and process controls for propulsion, chassis, self-driving, body, and IoV (Internet of Vehicle-connected infotainment system). The E/E architecture of FF’s variable platform architecture is designed with the capacity to support the power and communication requirements necessary for seamless integration with advanced autonomous systems as they evolve. All of FF’s DCUs will support OTA updates and data collection.

FF Products

FF has developed an extensive portfolio of proprietary technologies that will be embedded and integrated in FF vehicles. FF’s B2C passenger vehicle pipeline over the next five years includes FF 91 series, FF 81 series and FF 71 series. In addition to

19

passenger vehicles, leveraging its VPA, FF plans to produce a Smart Last Mile Delivery (“SLMD”) vehicle to address the high growth last mile delivery opportunity.

Passenger Vehicles

Each of the three passenger vehicle series is planned in two different configurations. All passenger vehicles will share common brand “DNA” of:

| ● | Intelligence, Internet and connectivity; | ||||