UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark one)

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the fiscal year ended: December 31 , 2021

or

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from to

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation) | (Commission File Number) | (IRS Employer Identification No.) | ||||||||||||

(Address of principal executive offices, including zip code)

Registrant’s telephone number, including area code: (732 ) 225-8400

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||||||||

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer a smaller reporting company or an emerging growth company. See the definitions of the “large accelerated filer,” “accelerated filer,” “non-accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

☒ | Accelerated filer | ☐ | |||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | |||||||||

| Emerging growth company | |||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. Yes ☒ No ☐

Indicate by check mark whether registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

The aggregate market value of the voting stock held by non-affiliates of the registrant as of the last business day of the registrant’s most recently completed second fiscal quarter, June 30, 2021, was approximately $715 million based upon the closing sale price of our common stock of $17.96 on that date. As of February 16, 2022, there were 53,958,013 shares of the registrant’s common stock issued and outstanding.

| Page | |||||

Item 15. Exhibits and Financial Statement Schedules | |||||

Frequently Used Terms

Unless otherwise stated or unless the context otherwise requires, the terms “Company,” “we,” “us,” “our,” and “Eos” refer to Eos Energy Enterprises, Inc., a Delaware corporation, and the term “BMRG” refers to the Company prior to the consummation of the business combination. In this Form 10-K:

• “Charter” means the third amended and restated certificate of incorporation of the Company.

• “EES ” means Eos Energy Storage LLC.

• “Exchange Act” means the Securities Exchange Act of 1934, as amended.

• “Founder shares” means the shares of common stock, which were formerly shares of Class B common stock purchased, by BMRG’s initial stockholders.

•“GAAP” means United States generally accepted accounting principles, consistently applied, as in effect from time to time.

•“IPO” means the Company’s initial public offering, consummated on May 22, 2020, through the sale of 17,500,000 units at $10.00 per unit.

•“Nasdaq” means The Nasdaq Capital Market.

•“Private Placement” means the private sale of the private placement units simultaneously with the closing of the IPO.

1

•“Private Placement Shares” means the shares of common stock included in the private placement units.

•“Private Placement Units” means the 650,000 units at $10.00 per private placement unit purchased by the Sponsor in the private placement, each of which consists of one share of common stock and one-half of one private placement warrant. The private placement units were separated into their component parts upon the consummation of the business combination.

• “Private Placement Warrants” means the warrants underlying the private placement units issued in the Private Placement, each of which is exercisable for one share of common stock at $11.50 per share.

• “Public Warrants” means the 8,750,000 redeemable warrants sold as part of the units in the IPO.

•“SEC” means the U.S. Securities and Exchange Commission.

•“Securities Act” means the Securities Act of 1933, as amended.

•“Sponsor” means B. Riley Principal Sponsor Co. II, LLC.

•“Trust account” means the trust account established in connection with the IPO.

•“Warrants” means the Private Placement Warrants and Public Warrants.

Our website address is www.eosenergystorage.com, and our board committee charters and other corporate governance documentation is available at https://investors.eose.com. Information contained on, or that can be accessed through, our website does not constitute part of this Annual Report on Form 10-K.

Forward-Looking Statements

All statements included in this Annual Report on Form 10-K ("Annual Report"), other than statements or characterizations of historical fact, are forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. The words "anticipate," "believe," "estimate," "project," "expect," "intend," "plan," "should," and similar expressions, as they relate to us, are intended to identify forward-looking statements. These statements appear in a number of places in this Annual Report and include statements regarding the intent, belief or current expectations of Eos Energy Enterprises, Inc. Forward-looking statements are based on our management’s beliefs, as well as assumptions made by, and information currently available to, them. Because such statements are based on expectations as to future financial and operating results and are not statements of fact, actual results may differ materially from those projected. Factors which may cause actual results to differ materially from current expectations include, but are not limited to:

•changes adversely affecting the business in which we are engaged;

•our ability to forecast trends accurately; our ability to generate cash, service indebtedness and incur additional indebtedness;

•our ability to raise financing in the future;

•our ability to develop efficient manufacturing processes to scale and to forecast related costs and efficiencies accurately;

•fluctuations in our revenue and operating results;

•competition from existing or new competitors;

•the failure to convert firm order backlog to revenue;

•risks associated with security breaches in our information technology systems;

•risks related to legal proceedings or claims;

•risks associated with evolving energy policies in the United States and other countries and the potential costs of regulatory compliance;

•risks associated with changes to U.S. trade environment;

•risks resulting from the impact of global pandemics, including the novel coronavirus, Covid-19;

2

•risks related to adverse changes in general economic conditions;

•other factors detailed under the section entitled “Risk Factors” herein.

Should one or more of these risks or uncertainties materialize, or should any of our assumptions prove incorrect, actual results may vary in material respects from those projected in these forward-looking statements. Forward-looking statements speak only as of the date they are made. Readers are cautioned not to put undue reliance on forward-looking statements, and, except as required by law, the Company assumes no obligation and does not intend to update or revise these forward-looking statements, whether as a result of new information, future events, or otherwise.

PART I

ITEM. 1 BUSINESS

Business Combination

Eos Energy Enterprises, Inc. (the “Company” or "Eos"), a Delaware corporation, was incorporated under its prior name B. Riley Merger Corp. II as a blank check company on June 3, 2019. On September 7, 2020, the Company entered into an Agreement and Plan of Merger (the “Merger Agreement”) with BMRG Merger Sub, LLC, our wholly-owned subsidiary and a Delaware limited liability company (“Merger Sub I”), BMRG Merger Sub II, LLC, our wholly-owned subsidiary and a Delaware limited liability company (“Merger Sub II”), Eos Energy Storage LLC, a Delaware limited liability company (“EES”), New Eos Energy LLC, a wholly-owned subsidiary of EES and a Delaware limited liability company (“Newco”) and AltEnergy Storage VI, LLC, a Delaware limited liability company (“AltEnergy”).

On November 16, 2020, the transactions described above were consummated. In connection with the business combination (the “Business Combination”): (1) Merger Sub I merged with and into Newco (the “First Merger”), and Newco continued as the surviving company (sometimes referred to as the “First Surviving Company”) and became our wholly owned subsidiary; and (2) immediately following the First Merger and as part of the same overall transaction as the First Merger, the First Surviving Company merged with and into Merger Sub II and Merger Sub II continued as the surviving company and our wholly owned subsidiary.

Upon the closing of the business combination (the “Closing”), the Company changed its name to “Eos Energy Enterprises, Inc.” The business combination is accounted for as a reverse recapitalization. EES is deemed the accounting predecessor and the combined entity is the successor SEC registrant. The historical financial statements of EES became the historical financial statements of the combined entities that are disclosed in the registrant’s future periodic reports filed with the SEC.

Business Overview

We design, manufacture, and deploy safe, scalable, and sustainable, low total cost of ownership battery storage solutions for the electricity industry. Our flagship technology is the proprietary Eos Znyth aqueous zinc battery, the core of the Eos DC energy storage system (the “Eos Znyth™ system”), with both front-of-the-meter and behind-the-meter applications, particularly applications with three to twelve- hour use cases. The flexibility of the Znyth™ battery allows the battery to support use cases such as frequency regulation's one-second response time. The Eos Znyth™ system is the first non lithium-ion ("Li-ion") stationary battery energy storage system (“BESS”) that is competitive in price and performance with Li-ion and is more flexible, safe and sustainable. The Znyth™ battery is fully recyclable, does not require any rare earth or conflict materials, is manufactured in the United States with a primarily domestic supply chain, and is scalable to multi-GWh sites or can be sized for small commercial sites.

3

Stationary BESS are used to store energy for many purposes, including stabilizing and reducing congestion of the power grid, reducing peak energy usage, and time-shifting of renewable energy sources. When coupled with renewable energy sources such as solar photovoltaic (“PV”) and wind generation, the Eos Znyth™ system can store energy that the renewable source produces and discharge energy when the source is not producing energy, thus reducing the intermittency and increasing the value and reliability of the renewable energy source. Additionally, storage is used by commercial and industrial (“C&I”) customers to save energy costs by reducing their peak usage, thus reducing demand charges and avoiding peak energy pricing from utilities. We believe that scalable energy storage serves as a central catalyst for modernizing and creating a more reliable and resilient, efficient, sustainable, and affordable grid. The significant market demand for battery storage is driven by independent power producers (“IPP”), renewable developers, utilities and C&I customers who are especially eager for a reliable, sustainable, safe, low-cost and scalable battery storage solution to complement their other energy resources.

EES was founded in 2008 under the name Grid Storage Technologies, initially focusing on developing the chemistry of its proprietary electrolyte-based battery technology and improving mechanical design and system performance. Our products, which are developed and manufactured in the United States, have the ability to play a pivotal role in the transition to a more sustainable, resilient and low carbon energy future. We have transformed from an organization that focused primarily on research and development to one focused on commercialization of our energy storage solution and, more recently, to scaling our manufacturing platform. We produced our first proof of concept with generation 1 of the Eos Znyth™ system in 2015 (“Gen 1”) and began commercial shipments of our generation 2 Eos Znyth™ system in 2018 (“Gen 2”). During 2020, we completed the development of our Generation 2.3 Eos Znyth™ systems (“Gen 2.3”) and shipped our first Gen 2.3 system in December 2020. As of December 31, 2021, we have delivered 22 Eos Znyth™ systems comprised of over 9,300 Znyth™ batteries or approximately 28 megawatt hours ("MWh"). Each Gen 2.3 20 foot battery container (“Eos Cube”) is comprised of 144 batteries, which are connected to, and monitored through, our proprietary battery management system. Each system is individually designed with the appropriate number of Eos Cube to achieve the end user’s desired energy needs. We also offer a larger battery systems in the form of our prefabricated building system (“Eos Hangar”) which provides 40MWh of storage per Eos Hangar and an indoor racking solution (“Eos Stack”) that leverages the safe and modular characteristics of the Znyth™ battery in providing indoor energy solutions for C&I buildings.

Our competitive advantage is our Znyth™ battery technology, which employs a unique zinc-halide oxidation/reduction cycle packaged in a sealed, flooded, bipolar battery. Our patented aqueous zinc-powered battery technology offers a safe, scalable, fully recyclable and sustainable alternative to Li-ion battery power. The Znyth™ technology requires just five core commodity materials derived from non-rare earth and non-conflict minerals that are abundantly available and fully recyclable. The Eos Znyth™ system is also non-flammable and does not require any moving parts or pumps, allowing for simple maintenance and low-cost operation.

The Eos Znyth™ system offers an alternative to Li-ion at a price per kilowatt hour (“kWh”) that is competitive. Unlike Li-ion, and due to Znyth™'s wide operating temperature range, our commodity-based aqueous zinc chemistry does not require high-cost heating, ventilation, air conditioning ("HVAC"), or fire suppression equipment. Where Li-ion batteries have a history of explosions and fires, our systems do not face this issue due to the stable, non-combustible chemistry used in our battery. Our raw materials and components are readily available commodities with fewer supply constraints than competing technologies. Li-ion batteries use scarce, toxic rare earth materials that can be in short supply due to their use in electric vehicles, mobile phones and an array of other electronics. Li-ion batteries can themselves be, and in recent months have been, in short supply. Our technology is highly scalable, easily installed and integrated into new or existing electric infrastructure. Our systems also include our proprietary battery management system, which optimizes our battery performance and protects the health and longevity of the battery. Our products are currently manufactured in the United States and require a fraction of the capital expenditure of equivalent Li-ion manufacturing processes. Our scalable manufacturing platform can be localized anywhere in the world in fewer than 12 months. Our technology is protected by a robust patent portfolio. As of December 31, 2021, we had over 220 patent applications filed, and we have more than 140 patents pending, issued or published in 33 countries.

4

We sell our products through our direct sales force and through sales channels to developers, power producers, large utilities and commercial and industrial companies. Our sales focus is primarily on use cases that require three (3) to twelve (12) hours of battery storage, although our battery can be used for shorter durations as well. We are establishing a global sales presence by leveraging our sales channels and direct sales team. We work with customers to understand the use case for each battery storage project and propose the best solution to maximize the economics for the end user. Examples of customers and use cases for our systems include:

•Solar developers that combine battery storage with solar fields to time-shift energy by charging the battery during the day and then discharging the battery during peak hours.

•Industrial customers that use battery storage to improve power quality, reduce peak usage, and improve the efficiency of other energy sources.

•C&I customers that utilize battery storage to safely reduce demand charges from their utility and participate in utility programs to improve grid operations. In the event of a loss of electricity from the grid, our battery provides resilience, such as running emergency systems in the building including elevators and fire alarms.

•Utilities that use battery storage systems to offset or postpone transmission and distribution capital expenditures and to provide congestion relief, which improves the reliability of the power grid.

On April 9, 2021, we acquired the remaining 51% ownership stake in HI-POWER, LLC ("HI-POWER"), which was initially established as joint venture in August 2019. The acquisition allows us to enhance our operational and financial flexibility through the vertical integration of our supply chain. We assumed full control over the supply chain, back-office functions, HI-POWER personnel, and day-to-day management. We continue to manufacture our non-toxic, non-flammable energy storage systems at the Turtle Creek, Pennsylvania location, where we employ more than 150 technicians.

Industry Overview

We believe that energy storage is on the verge of global wide-scale deployment. Specifically, we believe we are on the cusp of what could be a rebirth of American manufacturing and innovation in energy resilience as governments, communities and corporations race to reduce emissions and meet climate change goals. The number of companies that set targets and report progress increased nearly 300% from 2019 to 2020, and this figure is likely to grow with the United States and other countries as they set more aggressive targets for carbon mitigation.

As batteries increasingly become economical on a levelized cost of storage basis, we believe that utility-scale battery technology will be increasingly beneficial for a variety of solutions, including solar-plus-storage, peaking capacity, grid congestion and wind-plus-storage. We anticipate rapid increases in utility scale, co-located renewable energy-plus-storage projects, especially in the United States, with most near and medium-term installations qualifying as utility scale. By combining a battery with an intermittent renewable energy source, such as wind or solar, the energy stored in the battery can be used when the intermittent source is not available, for example if the wind is not blowing or the sun is not shining.

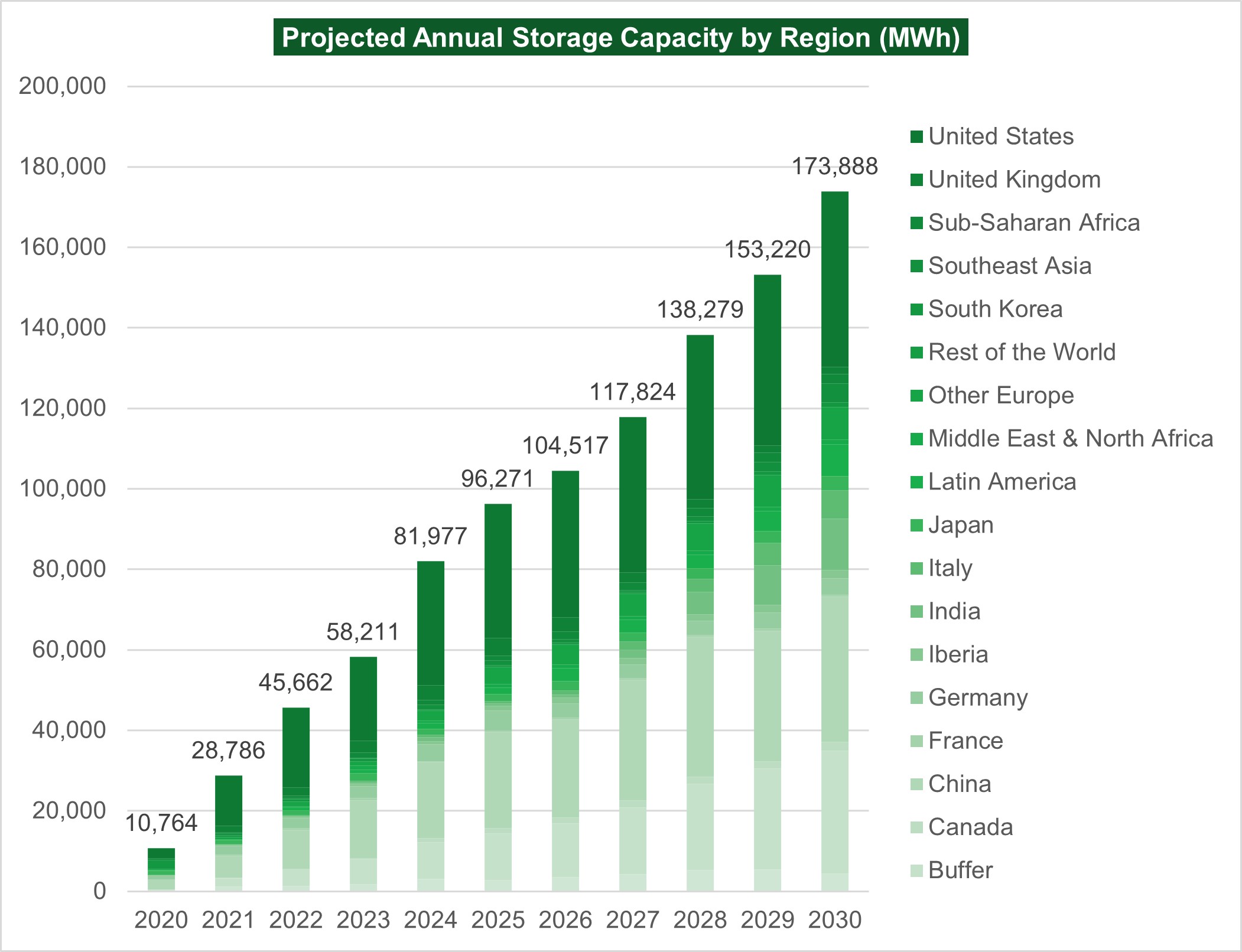

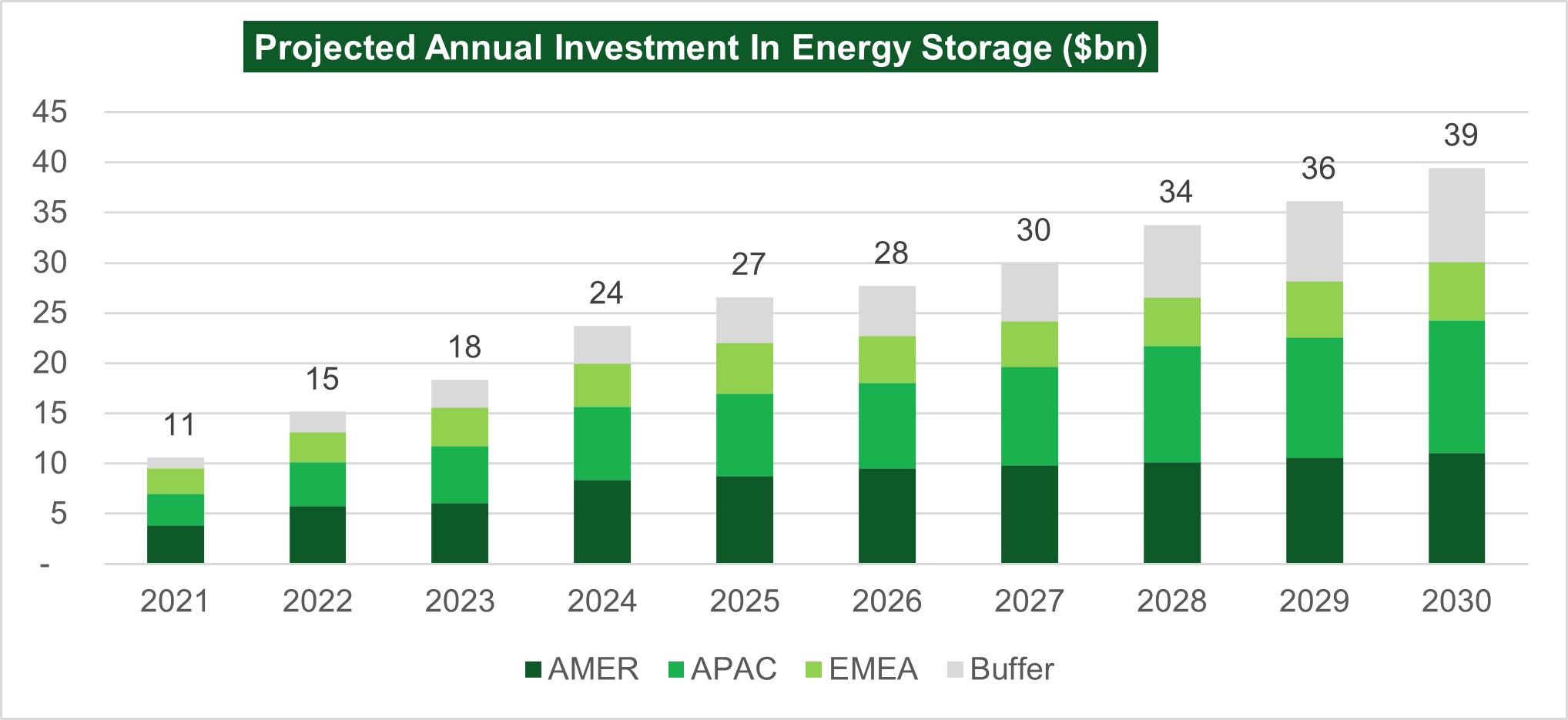

According to Bloomberg New Energy Finance (“BNEF”), the global energy storage market is expected to grow to a cumulative 350 gigawatts (“GW”), attracting an estimated $262 billion in future investment by 2030. With approximately 5.5 GW of energy storage commissioned globally in 2020, BNEF anticipated an increase to 11.9 GW in 2021. It is expected the global energy storage market will grow at a 33% compound annual growth rate from 10,764 MWh annually in 2020 to approximately 174,000 MWh annually by 2030.

Based on BNEF, the United States would represent over 28% of this global cumulative market through 2030. According to the U.S. Energy Information Association, the percentage of renewable energy in total electricity generation in the United States will change from 20% in 2020 to 33% or more by 2030. Favorable regulatory conditions such as the court decision validating Federal Energy Regulatory Commission (FERC) Order 841, along with state sponsored incentives in New York, California, Massachusetts and other states coupled with the rapid growth of solar PV plus storage applications throughout the United States are expected to grow the energy storage market from 2,473 MWh deployed in 2020 to 43,586 MWh deployed in 2030. Below is a demonstration of the projected energy storage global market and the projected annual investment in the energy storage global market by region:

5

Source: BNEF

(1) Buffer represents markets where we lack visibility.

6

Limitations of Other Existing Technologies

Li-ion is the most prevalent incumbent energy storage technology, historically used in consumer electronics, electric vehicles and select transportation industries, and is the primary alternative to our systems. According to the U.S. Energy Information Administration, Li-ion accounted for 93% of all new energy storage capacity in the United States since 2012, growing at an annual rate of 55%. According to the Lazard Levelized Cost of Storage Version 4.0 Final report (“Lazard LCOS 4.0 Report”), Li-ion has an optimal power capacity of between 5 kilowatts (“kW”) — 100 Megawatts ("MW") and an anticipated useful life of twelve (12) years. Key primary ingredients for Li-ion batteries are lithium and cobalt or nickel, with companies now relying more on nickel. In addition, the Lazard Levelized Cost of Storage Version 7.0 (“Lazard LCOS 7.0 Report”) highlights increased concerns regarding the availability of Li-ion battery modules given ongoing supply constraints as the demand for storage solutions increases across several markets.

Due to the factors described below, we believe that even though lithium supplies are generally forecasted to accommodate the global increase in demand in the near term, supply chains will likely become strained over time. Additionally, lithium faces significant supply chain uncertainty that may constrain Li-ion battery growth.

•Lithium Supply. The lithium supply chain is highly concentrated, and according to an article by McKinsey & Company titled “Lithium and Cobalt: A tale of two commodities” (“McKinsey Article”) only eight (8) countries are producing lithium globally, of which Chile, Australia and China accounted for 85% of production in 2017. Only four companies — Talison Lithium Pty Ltd, Sociedad Química y Minera de Chile S.A., Albemarle Corporation and FMC Corporation — control the majority of the global mining output. Without the addition of new lithium mining projects and with growing lithium demand, especially in the electric vehicle space, demand is on pace to exceed supply soon, which would hinder the growth of lithium-based products.

•Cobalt Supply. According to the McKinsey Article, while the top three producers of cobalt comprise only 40% of the global cobalt supply, regional suppliers are more monopolistic. The Democratic Republic of the Congo (“DRC”) represented approximately 70% of global output in 2019, a share that is projected to increase further. The DRC historically experienced supply disruptions and is currently revising mining laws, with additional concerns regarding child labor, potentially threatening the market’s overall growth. Additionally, approximately 90% of the global cobalt supply is produced as a by-product from either copper or nickel mining, making cobalt expansion projects closely tied to the economics of these markets. Global forecasts for cobalt production show supply shortages arising as early as 2022, which would likely slow Li-ion battery growth.

•Nickel Supply. According to Rystad Energy, global demand for nickel used in battery production is projected to increase by 22% from 2021 to 2026. The supply crunch is driven by mining companies not finding enough new high-grade nickel to keep up with the current demand. Most of the higher energy cathodes of the future will need high nickel content.

•Electric Vehicle (“EV”) Demand. The lithium, nickel and cobalt markets have been largely driven by battery demand, primarily from consumer electronics, representing 40% and 25% of demand in 2017, respectively. Lithium, nickel and cobalt could face supply constraints due to the demand for these materials in batteries for the EV industry. As the global EV market expands, we expect global demand for both materials to increase. EVs represented 1.3% of global vehicle sales in 2017, but BNEF forecasted that EVs will hit 10% of global passenger vehicle sales in 2025, with that number rising to 28% in 2030 and 58% in 2040. The proportion of Li-ion batteries consumed by the EV industry was 64% in 2019 and is forecasted to grow to 80% by 2030. The Lazard LCOS 7.0 Report reaffirms this perspective by stressing that battery module demand from EVs is expected to increase to ~90% from ~75% of end-market demand by 2030. Stationary storage currently represents <5% of end market demand and is not expected to exceed 10% of the market by 2030.

7

Li-ion also suffers from inherent technological limitations. Performance under extreme ambient temperature can significantly impact the life cycle of Li-ion batteries. This makes Li-ion difficult to pair with solar, or wind, in areas where the operating temperature window ranges widely. In cases where extreme ambient conditions are expected, energy storage systems have implemented HVAC systems to maintain a narrower operating temperature to offset temperature limitations. While ensuring lower degradation through the life of the battery, the use of such systems impact overall system efficiency performance, as some of the energy must be used for thermal management.

Li-ion is also susceptible to thermal runaway conditions. This condition can lead to overheating, explosions, and related safety issues, as the April 2019 lithium battery explosion near Phoenix, Arizona demonstrated. With the increased need of energy storage for multiple applications, this safety concern is front and center in the minds of regulators and authorities as they draft guidelines and requirements for properly installing storage systems. Many urban areas restrict the use of commercial size Li-ion batteries in buildings and some standards organizations, such as UL, are modifying their standards to accommodate for proper examination of such systems. UL9540A, is a widely accepted test method set to evaluate thermal runaway propagation on energy storage systems. Under the test conditions laid out by UL9540, no single Li-ion based cell is able to meet the minimum requirements for thermal stability and flammable outgassing, since Li-ion electrolytes are inherently flammable. Lithium cell manufacturers avoid some of these issues by designing cell cooling systems, fire suppression systems, and battery pack designs which minimize propagation of fires, at the expense of added system cost and complexity. Finally, Li-ion technology is difficult to recycle and dispose because it contains toxic materials, the cells are difficult to disassemble, and the metals in the electrodes are difficult to separate, making the complete life-cycle management of the product significantly more complex.

There are a number of additional battery technologies utilized in the energy storage industry, such as:

•Flow Battery. Flow batteries store energy electrochemically by pumping electrolyte from storage tanks through a series of cells at high pressure. According to the Lazard LCOS 4.0 Report, flow batteries have an optimal power capacity of between 25 kW — 100 MW and an anticipated useful life of twenty (20) years. Further assessment on this technology using the Lazar LCOS 7.0 Report, generally supports that flow batteries typically have minimal storage capacity degradation and limited potential for fire, while requiring expensive components such as membranes and catalysts and have a comparatively high balance of system, operations and maintenance cost compared to static batteries. Specifically, the raw materials are expensive, and the cost of operation and maintenance are very high. Flow batteries also have reduced efficiency due to high mechanical losses, and high maintenance requirements. They require massive scale to reach competitive cost points which, along with the above, limits applications to niche markets.

•Lead-Acid. Lead-acid batteries are the most commonly utilized battery storage technology, and are the primary battery utilized in automotive vehicles. The Lazard LCOS 4.0 Report notes that they have an optimal power capacity of 1 — 100+ MW and an anticipated useful life of between three and five years. Furthermore, while lead-acid batteries are relatively low cost and can be utilized for multiple purposes, they have a poor depth of discharge, short lifespan, low energy density and a large environmental footprint as compared to other technologies.

Our Solution

Our Znyth™ battery storage systems offer a safe, sustainable and scalable alternative to Li-ion at a lower Levelized Cost of Storage (“LCOS”) for key use cases for our customers.

The key benefits of our solution include:

8

•Peak Shifting and Demand Management. Our multi-cycle DC Znyth™ system shifts power to peak hours, with repeated constant power performance using 100% depth of discharge without increased degradation. Li-ion typically limits the depth of discharge to 80-90% due to the impact on accelerating the lithium battery degradation. Additionally, based on our research estimates, even at 80% depth of discharge of a Li-ion battery is expected to lose 2.5% of energy storage capacity per year over its lifetime, compared with 1-2% for our product, resulting in a more favorable degradation curve with estimated operating expense savings at $3/kWh per year. Utilities and end customers can use our batteries to efficiently store excess base-load generation and renewable energy produced during off peak hours. By discharging during peak hours, we eliminate the need for new fossil-based fuel and inefficient peaking generation, thereby reducing carbon emissions drastically. Boundless Impact Research & Analytics performed a climate impact study in November 2020 comparing Eos batteries to traditional battery chemistries such as Li-ion, Lead-Acid, Sodium Sulfur and Vanadium Redox. Eos’s technology achieved the lowest GHG emissions compared to all of the other technologies, notably showing an 84% lower GHG emissions footprint compared to Li-ion from a life-cycle assessment perspective. Additionally, utilities can use the peak shifted energy to postpone or eliminate capital investment, and the end user can reduce their demand charges from the utility.

•Low Maintenance and Minimal Auxiliary Load. Our battery system does not require an HVAC or fire suppression system, resulting in significantly lower expenses associated with operation and maintenance of the battery. This in turn brings significant cost savings to our customers, resulting in a meaningfully improved return on investment for our storage product and up to an approximately 30% reduction in levelized cost of storage. HVAC systems usually represent 9% of delivered energy for Li-ion storage systems to run the cooling fans for the batteries, compared with 2% for our product, resulting in operating expense savings from cooling the batteries of $2/kWh per year, based on our estimates. Additionally, given that our battery does not require an auxiliary electricity load to support HVAC and fire suppression systems, it is able to ride through grid outages, resulting in more reliable energy storage. Comparatively, Li-ion often cannot operate without grid power due to its large auxiliary load needed for HVAC systems.

•Solar/Wind Integration and Shifting. Renewable energy sources such as wind and solar are intermittent, potentially introducing instability into the electric grid and limiting their viability as a firm, consistently dispatchable power source. Our batteries allow utilities and consumers to moderate production and time-shift the produced energy. Our batteries enable solar electricity produced at noon to be stored and deployed as a stable power source during peak demand later in the afternoon. Similarly, wind energy produced overnight can be used to level out peaks in the morning.

•Ancillary Services. Our batteries can be used to bring revenue to our commercial and industrial customers through their participation in the demand response and ancillary markets. The demand response markets are used by utilities to offset grid congestion at certain locations by paying end users for reducing their energy use during congested periods. The ancillary markets are used to stabilize and keep the grid in balance, and end users are paid to either inject energy into the grid or receive power from the grid, thus providing the balance. Our batteries are eligible for entry into demand response and ancillary electricity markets that provide stability to the power grid.

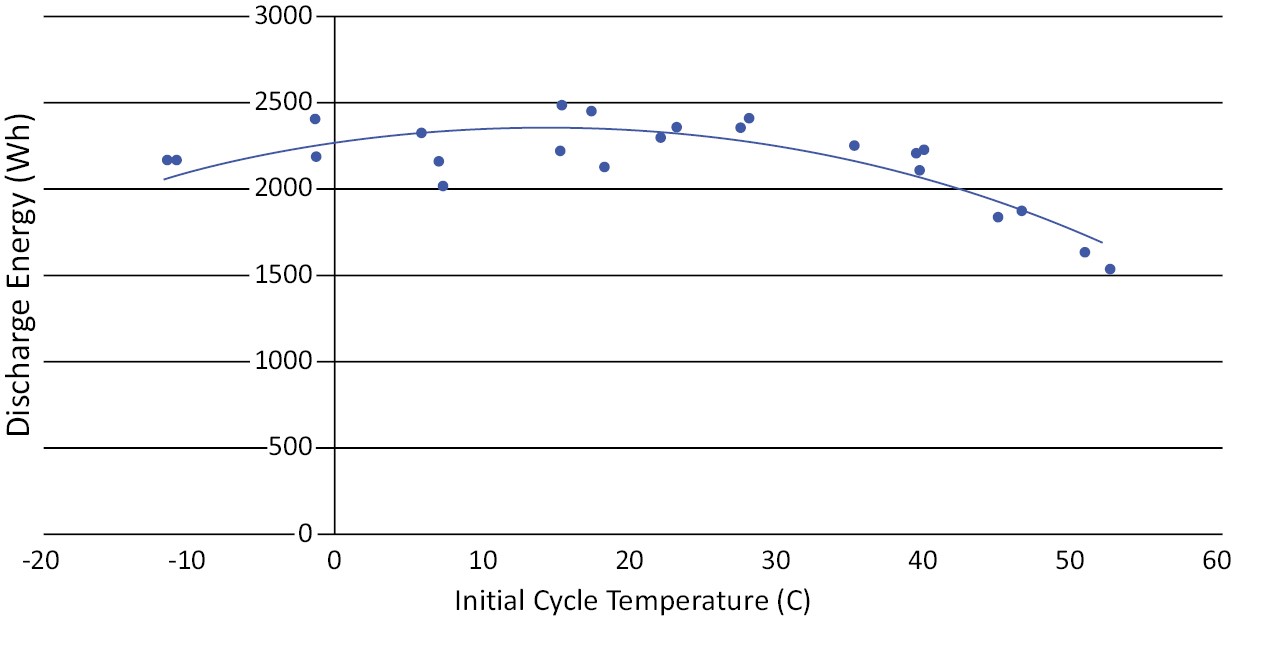

•Performs Across Wide Temperature Range. Our system’s performance is stable from -20º to 50ºC without HVAC and has a unique ability to recover from temperatures as high as 70º to 90ºC, which might cause other battery technologies such as Li-ion to experience thermal runaway and potential fire or explosion. Data from our cell, battery and system testing shows that round trip efficiency (“RTE”) is stable within 75%+/- 3% across -11º to 41ºC. (round-trip efficiency is the ratio of energy put in (in kWh) to energy retrieved from storage (in kWh)). Below is a demonstration of the wide temperature operating range of our battery technology based on data from deployed systems:

9

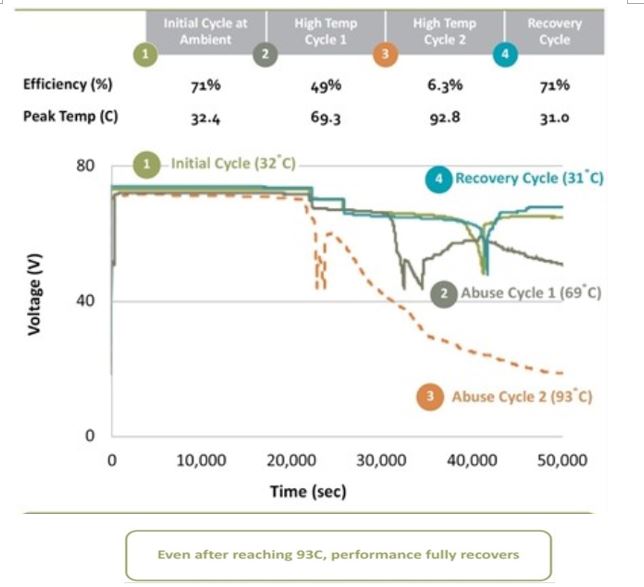

•Resilient system recovering after extreme temperature abuse as high as 90ºC. The Znyth™ battery displays resilience after exposure to extreme temperatures, a significant differentiator to Li-ion which requires HVAC and fire suppression, increasing both capital expenditures required for maintenance and the risk of thermal runaway, fire or explosion. Based on our estimates, our low maintenance capabilities result in approximately $1/kWh per year operating expense savings. Below is a demonstration of our battery that was subjected to temperatures exceeding 90ºC while being operated. After the battery was allowed to cool to room temperature, the battery returned to its pre-abuse performance.

10

•Upside Opportunities. Given that raw materials represent a high percentage of the Eos Znyth™ system’s total cost, we expect the salvage value of the raw materials could offset the cost of system removal and decommissioning at the end of life for our customers. We continue to evaluate and refine recycling cost and estimate that our battery system may have 50% of its original capacity after thirty (30) years of use. We anticipate development of a secondary, after-life market for our batteries in approximately 10 years, which may generate additional revenue for customers or offset other costs.

•Discharge Duration Flexibility. The Eos Znyth™ product is designed to be used as a flexible energy storage product capable of discharge durations ranging from 3 to 12 hours with minimal impact on degradation rate across this operating window. Additionally, the Eos product yields higher discharge energy and round-trip energy efficiency as duration is increased, meaning the chemistry and module design is well suited for applications where discharge duration reaches over 8 hours.

Our Competitive Strengths

Our key competitors are traditional Li-ion battery manufacturers, such as Samsung Electronics Co., Ltd, LG Chem, Ltd., Tesla, Inc, BYD Co. Ltd, Sungrow and Contemporary Amperex Technology Co. Limited. Longer duration competitors include ESS Tech Inc., Lockheed Martin Corporation, Redflow, Gelion, Energy Vault, and Malta.

We believe the following strengths of our business distinguish us from our competitors and position us to capitalize on the expected continued growth in the energy storage market:

11

•Differentiated Product. Lithium cells must be kept within a narrow temperature range (25 °C +/- 5 °C), otherwise they are at risk of thermal runaway, potentially leading to fire or explosion. The Eos Znyth™ system has a significantly wider thermal operating range (-20°C to 50°C), which eliminates the need for costly thermal management measures such as HVAC and fire suppression systems. Additionally, the Eos product is a static modular battery design, which eliminates the need for pumps or compressors, both maintenance prone equipment required for flow batteries. Our battery system can charge and discharge at different durations, covering a wide range of use cases. The charge and discharge rates are fixed for Li-ion, and the life of a Li-ion battery can degrade if it is not charged or discharged at the rate for which it was designed.

•Minimal Supply Chain Constraints. All materials for producing our Eos Znyth™ system are widely available commodities with fewer supply chain constraints and minimal competition with EVs. No rare earths or conflict materials are used in the production of our batteries. Additionally, all materials are fully recyclable at end of product life and the recycled material can be sold, which results in net present value savings of $4/kWh versus lithium.

•Proven Technology Solution in the Growing and Evolving Energy Storage Market. We have delivered over 28,000 kWh worth of our systems to customers since inception. As we launched the Znyth™ Gen 2.3 product and are ramping manufacturing up to gigawatt-hours (“GWh”) scale, we believe that we will benefit from the overall growth of the energy storage market, which is expected to reach 1,095 GWh by 2040, as projected by BNEF. From an application perspective, the market is evolving to a long-duration storage market. Our technology is tailored to address such a need. While Li-ion has been optimized for shorter duration, the performance of our batteries improves as it moves towards longer duration (lower c-rates), making us the prime technology for the long-duration storage market.

•Experienced Technology Team Focused on Continuous Innovation. We have successfully introduced three generations of energy storage systems in six years (Gen 1, Gen 2, and Gen 2.3) and plan to release a new generation in early 2023. Gen 1 and Gen 2 were pilot systems that provided us with the field data and experience to optimize the performance and design of Gen 2.3. Our research and development team is responsible for our portfolio of fourteen (14) patent families with over 220 patent applications filed, more than 140 pending, issued or published in thirty-three (33) countries, protecting our technology and system architecture. We believe that our continued investment in Research and Development will enable us to improve efficiency, energy density, functionality, and reliability while reducing the cost of our battery solution. We are also focused on leveraging our technology know-how to improve our battery management system, expanding the operation of our batteries and increasing our overall performance. This same leverage will allow us to optimize our energy management solution to contextualize the operation of the battery based on the application, expanding our customer's ability to use our Znyth™ battery system in a wider set of use-cases.

•Established Global Sales Channels Anchored with Top-Tier Customers. We sell products directly to the electric utility industry and through sales channels to the commercial and industrial market. As we are building our pipeline, during fiscal year 2021, we built relationships with new customers and entered into agreements to provide battery solutions to multiple customers within and outside of the United States. Our average project size also increased, and we booked our first 50+ MWh project with Blue Ridge Power.

•Strong management team. We have assembled an executive team focused on accelerating the commercialization of the next-generation Eos Znyth™ solution. With decades of combined, diverse experience in the energy industry and deep expertise in manufacturing, battery storage and executing complex power and energy projects around the world, our management team is able to develop, manufacture and deliver systems at scale to meet the growing demands of the global storage market.

12

Our Products

The Eos Znyth™ system is designed to meet a wide range of requirements in the battery storage industry, including large grid-scale energy storage projects, large and small solar storage projects, commercial or industrial projects, in-building urban projects and eventually the residential market. With a three (3) to twelve (12) hour discharge capability, immediate response time, and modular construction, the Eos Znyth™ system can be scaled and configured to reduce cost and maximize profitability in a wide range of battery storage projects. While the Eos Znyth™ system can be implemented in any configuration required, we offer three standardized configurations: the Eos Cube, which consists of a plug-and-play 20 foot shipping container, the Eos Hangar, a prefabricated building for larger battery storage systems; and the Eos Stack, which is a modular racking system for indoor solutions.

Our innovative Eos Cube packaging comprises a plug-and-play twenty (20) foot standard International Organization for Standardization shipping container which enables flexible options for system installation while significantly lowering the installation cost and accelerating permitting and installation time. The Eos Cube is shipped with batteries and Battery Management System ("BMS") and is factory tested into a standard twenty (20) foot intermodal shipping container allowing for simpler and lower cost installation. Each sub-system includes pre-integrated strings of Eos Znyth™ batteries with DC wiring, DC system protection, support structure, enclosure and Eos BMS. The Eos Cube system integrates Eos Znyth™ batteries in a modular, outdoor-rated enclosure capable of delivering three (3) to twelve (12) hours of continuous discharge at specified power. Each DC system is made up of a containerized Energy Block integrating one hundred and forty-four (144) Znyth™ Batteries and a DC control section. Our proprietary BMS actively monitors the voltage and temperature of each battery in the system, isolates faulty battery strings and provides real-time visibility of battery operating limits.

The Eos Hangar, our large-scale system is designed for large battery storage projects by allowing for what we believe to be the highest "power density to footprint" on the market. The Eos Hangar system is a standard, open span structure with a racking system that allows the modular Znyth™ batteries to be stacked in a tall multilevel configuration, providing increased power density. Because the Znyth™ battery does not require HVAC or special fire suppression systems and is simpler to install, operate and maintain as compared to Li-ion, we believe the Eos Hangar system provides a cost-effective way to implement large Znyth™ battery storage systems. Furthermore, the Eos Hangar system is designed to be used by utilities, independent power producers, solar and wind developers, and is an ideal solution for larger systems above 40MWh.

Our Eos Stack configuration, a modular racking solution is offered primarily for indoor battery storage projects but could be used in a wide range of projects. The safety and modular nature of the Znyth™ battery allows for implementations in basements, on rooftops, or any number of other locations in a building. Customized racks are designed for commercial and industrial customers, as well as system integrators, and would be used for indoor systems that require a modular configuration.

Our Strategy

Since our founding in 2008, we have been on a mission to accelerate the shift to clean energy with positively ingenious solutions that transform how the world stores power. Key elements of our strategy include:

13

•Continue to innovate and advance our solutions. We intend to continue to innovate our energy storage systems by developing new and enhanced technologies and solutions. Our innovative spirit extends to our manufacturing ability, which includes a proprietary equipment and process design. We continue to improve our manufacturing process and equipment and to optimize our supply chain and material costs. We believe that our future technology will continue to reduce cost and improve the efficiency and competitiveness of our offerings. We plan to continue to introduce new generations of our technology to increase the adoption of our energy storage systems worldwide.

•Further expand our products and services. We offer remote asset monitoring and optimization services to track the performance and health of our batteries and to proactively identify future system performance. We intend to continue to expand the software functionality by including an onsite controller that integrates with the power control system (inverter), which can be remotely controlled and managed to ensure that the battery system is optimized to the use case for performance and the best economic return. Specifically, we plan on incorporating machine learning, artificial intelligence, data science and optimization algorithms in an Energy Management Software system to enable use cases and create the greatest value to the end user.

•Further expand project related services. We offer to customers the following project related services:

1.Project management. We offer customers project management services to ensure the process of implementing our battery system is managed in conjunction with the overall project plans. We offer each customer project management services for portions of the project and can oversee the entire project from beginning to end. We charge the customer depending on the scope of our involvement.

2.Commissioning of the battery system. We commission our battery system and charge the customer for the commissioning services. The commissioning service ensures that our battery is providing the performance and operations that were committed to the customer.

3.Operations and Maintenance ("O&M"). We offer our customers operational and maintenance plans to keep our battery in top performance. These consist of both remote monitoring of the battery health and performance as well as periodic onsite visits to perform routine maintenance. We intend to continue to expand our O&M services to include 24x7 proactive monitoring and fault detection, not only for the Znyth™ battery system, but also for the inverter and balance of plant at the project site.

We plan to expand our O&M resources and capabilities to meet our customers’ needs. This expansion will include adding employees to perform the work, as well as contracting and certifying qualified third parties to perform the commissioning, operations and maintenance services.

•Implement near-term cost reduction. We intend to optimize manufacturing for our Znyth™ battery system by insourcing selected services and implementing further automation of the manufacturing process. Through our continued research and development efforts, we also believe we can continue to reduce the amount and cost of material required to manufacture the batteries. We further plan to substitute new materials to reduce cost. We aim to achieve lower prices for certain materials through volume purchasing.

Our Customers

Our customers include renewable power producers and developers like EnerSmart Storage LLC ("EnerSmart"), Renew Akshay Urja PVT. LTD ("ReNew Power"), Carson Hybrid Energy Storage ("CHES") and International Electric Power, LLC ("IEP"), industrial companies such as Motor Oil Corinth Refineries S.A. ("Motor Oil"), utilities companies such as Duke Energy Corporation ("Duke") and San Diego Gas & Electric Company ("SDG&E") as well as microgrid developers like Verdant Microgrid LLC ("Verdant"), Nayo Tropical Technology LTD ("Nayo") and Charge Bliss, Inc. ("Charge Bliss").

During fiscal year 2021, our largest customers were Charge Bliss and Motor Oil, who accounted for 37% and 21% of our revenues, respectively. None of our other customers accounted for more than ten percent of our revenues for the year ended December 31, 2021.

14

Intellectual Property

The success of our business depends, in part, on our ability to maintain and protect our proprietary technology, information, processes and know-how. We rely primarily on patent, trademark, copyright and trade secrets laws in the United States and similar laws in other countries, confidentiality agreements and procedures and other contractual arrangements. We have recently filed patents relating to our Gen 2.3 product that are subject to United States Patent and Trademark Office ("USPTO") approval. In 2021, Eos filed two utility applications, two provisional applications, and had seven patents granted. A majority of our patents relate to cell chemistry, architecture and battery mechanical design, system packaging and battery management systems. We continually assess opportunities to seek patent protection for those aspects of our technology, design, methodologies and processes that we believe provide significant competitive advantages. As of December 31, 2021, we had fourteen (14) patent families with over 220 patent applications filed, more than 140 patent pending, issued, or published in thirty-three (33) countries, protecting our technology and system architecture. Our key currently issued patents are scheduled to expire between years 2035 and 2036.

We rely on trade secret protection and confidentiality agreements to safeguard our interests with respect to proprietary know-how that is not patentable and processes for which patents are difficult to enforce. We believe that many key elements of our manufacturing processes involve proprietary know-how, technology or data that are not covered by patents or patent applications, including technical processes, test equipment designs, algorithms and procedures.

All of our research and development personnel have entered into confidentiality and proprietary information agreements with us. These agreements address intellectual property protection issues and require our employees to assign to us all of the inventions, designs and technologies that our personnel develop during the course of their employment.

We also require our customers and business partners to enter into confidentiality agreements before we disclose any sensitive aspects of our technology or business plans.

Competition

The markets for our products are competitive, and we compete with manufacturers of traditional Li-ion and other battery storage systems. Factors affecting customers when choosing from different battery storage systems in the market include:

•product performance and features;

•safety and sustainability;

•total lifetime cost of ownership;

•total product lifespan;

•power and energy efficiency;

•duration of the batteries storage;

•customer service and support; and

•U.S.-based manufacturing and sourced materials.

Our Znyth™ system competes with products from traditional Li-ion battery manufacturers and solution providers such as Samsung Electronics Co., Ltd, LG Chem, Ltd., Tesla, BYD, Sungrow, and Contemporary Amperex Technology Co. Limited. Our longer duration competitors include ESS Inc. and Lockheed Martin. We believe that our Znyth™ battery system offers significant technology, safety and cost advantages that reflect a competitive differentiation over lithium energy storage technologies.

15

Regulatory Policy

The United States is one of almost 200 nations that, in December 2015, agreed to an international climate change agreement in Paris, France, that calls for countries to set non-binding greenhouse gas ("GHG") emissions targets and be transparent about the measures each country will use to achieve these targets ("Paris Agreement"). The Paris Agreement was signed by the United States in April 2016 and came into force on November 4, 2016. In August 2017, the U.S. Department of State informed the United Nations of the United States' intent to withdraw from the Paris Agreement, effective November 2020. On January 20, 2021, in one of his first post-inauguration actions, President Biden notified the United Nations of the United States’ intention to rejoin the Paris Agreement, which became effective on February 19, 2021.

Legislation or regulations adopted to address climate change could make lower GHG emitting energy sources, such as solar and wind, more desirable than higher GHG emitting energy sources, such as coal and fuel oil. As a result, climate change regulatory and legislative initiatives that impose more stringent limitations on GHG emissions would potentially increase the demand for energy storage systems.

In the United States and Puerto Rico, geographic distribution of energy storage deployment has been driven by regulatory policy with both federal and state level programs contributing to stable revenue streams for energy storage. Such policies include:

•Federal Energy Regulatory Commission. FERC Order 841 requires eligibility for energy storage in wholesale, capacity and ancillary services markets. FERC Order 841 allows each regional transmission organization and independent system operator to establish its own rules and guidelines for integrating energy storage resources, but does specify that the guidelines must allow storage resources to provide and be compensated for all the services it is technically capable of providing. According to BNEF, markets being enabled by FERC Order 841 may spur the United States back to the top of global storage deployments.

•California. California is expected to lead front-of-the-meter energy storage deployments through 2023, mainly driven by Assembly Bill 2514 procurement targets and investor-owned utilities procuring storage for capacity applications. The California Public Utilities Commission mandated utilities to procure up to 500 MW of behind the meter (“BTM”) storage. Further, growth in California is driven by the Demand Response Auction Mechanism, which creates economic incentives for distributed energy resources to offer their services to utilities and grid energy markets. The California independent systems operator allows wholesale market participation for BTM storage assets which can earn capacity payments and provide ancillary services.

•Massachusetts. Massachusetts set an energy storage procurement target of 1,000 MWh by 2025. The Solar Massachusetts Renewable Target program calls for 1,600 MW of PV, and includes significant incentives paid to solar system owners if paired with storage. The Peak Demand Reduction Grant Program is a $4.7 million Massachusetts Department of Energy Resources initiative designed to test strategies for reducing Massachusetts’ energy usage at times of peak demand. The Massachusetts Department of Energy Resources also published the Clean Peak Energy Standard which is designed to provide incentives to clean energy technologies that can supply electricity or reduce demand during seasonal peak demand periods established by the Department of Energy Resources.

•New York. New York set an energy storage target of 1,500 MW by 2025 (3,000 MW by 2030), 500 MW of which will be commercial and industrial. $400 million in state funding was made available for energy storage projects. The New York State Energy Research and Development Authority must distribute $350 million in market acceleration incentives for energy storage, including for solar-plus-storage projects to jump-start activity and allow projects to access federal tax credits in the near term. NY Green Bank announced $200 million in financing support for energy storage. The Value of Distributed Energy Resources (“VDER”) program also benefits storage, offering greater compensation to resources that can provide capacity during specific hours of the year when the grid has greatest needs.

16

•Other. The Midwest, New England, Pacific Northwest states and Puerto Rico have taken the early charge on front-of-the-meter energy storage adoption in the “all others” market category, although we anticipate that states such as Minnesota and Florida, as well as areas in the Southwest Power Pool and the Midcontinent Independent System Operator, will emerge further over the next five years. Puerto Rico issued two tranches of request for proposals for renewables and storage capacity in 2021, with Tranche 1 seeking 2 GWh of storage and Tranche 2 seeking 1 GWh of storage in order to support the island's integrated resource plan; a total of six tranches are planned through the mid-2020s. Under Executive Order 28, the New Jersey Energy Master Plan calls for 17,000 MW of solar energy, 2,500 MW of energy storage by 2035 and 100 percent clean energy by 2050. In Nevada, Senate Bill 204 requires the public utilities commission of Nevada to investigate and establish targets for certain electric utilities to procure energy storage systems while Senate Bill 145 establishes an incentive program for behind-the-meter energy storage within the state’s solar program. In Hawaii, Hawaiian Electric Company, Inc. announced 262 MW of storage across three islands several years back, further establishing its position as a leading market. Illinois passed a clean energy policy in late 2021, which targets 100% carbon-free electricity by 2045 and includes $280.5 million to support the deployment of storage systems at retiring coal plant sites.

Government Incentives

U.S. federal, state, and local government entities, as well as non-U.S. government entities, provide incentives, subsidies, and other support programs for infrastructure improvement and energy transition programs. For example, the U.S. Congress is considering a variety of proposals for tax incentives that will benefit the renewable energy and energy storage industry, including in the form of tax credits. IRS private letter ruling 201809003 clarified that energy storage is eligible for federal tax credits if charged primarily by qualifying renewable resources. In December 2020, the U.S. Congress passed a spending bill that includes $35 billion in energy research and development programs, a two-year extension of the Investment Tax Credit for solar power, a one-year extension of the Production Tax Credit for wind power projects, and an extension through 2025 for offshore wind tax credits.

In the latest Build Back Better Plan under consideration in Congress, several potential tax incentives are designed to promote and reward sourcing materials and manufacturing batteries in the United States. Proposals under consideration include: i) Investment Tax Credits (“ITC”) for purchasers of stationary, stand-alone energy storage systems including: a 6% (six percent) base ITC for energy storage; a 24% (twenty-four percent) ITC if prevailing wage and apprenticeship standards are met; a 10% (ten percent) ITC if domestic content standards are met for projects started before 2025; a 10% (ten percent) ITC for projects in an area where carbon workers are being displaced; and a 10% (ten percent) ITC if the energy storage is a nascent technology, which Eos would qualify under; (ii) extension of the federal solar energy investment tax credit for ten (10) more years; (iii) the consolidation of forty-four (44) federal energy tax incentives into three provisions to award credits for clean electricity, lower emitting transportation fuels and energy efficient offices and homes; and (iv) the allowance of renewable electricity production and investment tax credits to be transferred on a limited basis to any entity involved in a renewable energy project, regardless of whether they have taxable income. There can be no assurance that all or any of the above proposals will be adopted by the U.S. Congress.

Environmental, Social and Governance ("ESG")

Since our founding, Eos has been on a mission to accelerate the shift to clean energy by transforming how the world stores power in a safe, scalable, efficient, and sustainable way. We are committed to advancing global sustainable development through our products, working to systematically grow our business to meet the challenges of the global energy transition and combat the global climate crisis.

Our approach to ESG is tied to our four product themes: safety, scalability, sustainability, and efficiency. As we continue to scale, we remain committed to driving progress across these themes. Our Nominating & Corporate Governance Committee of our Board of Directors oversees ESG matters and our internal ESG Steering Committee drives progress on our ESG strategy and reporting efforts.

Human Capital

17

As of December 31, 2021, we had two hundred fifty-one (251) full-time employees. Of these full-time employees, two hundred forty-eight (248) are located in the United States, two (2) in Italy and one (1) in India; fifty (50) were engaged in research and development, one hundred forty-seven (147) in operations and support and fifty-four (54) in selling, general and administrative capacities.

None of our employees are represented by a labor union. We have not experienced any employment-related work stoppages, and we consider relations with our employees to be good.

Our success is based on the focused passion and dedication of our people. We are committed to providing a positive and engaging work environment for our employees and taking an active role in the betterment of the communities in which our employees live and work. Our full-time employees are provided a competitive benefits program, including comprehensive healthcare benefits and a 3% non-elective employer contribution 401(k) plan, equity awards, bonus and incentive pay opportunities, unlimited paid time-off benefits and paid parental leave, wellness programs, and periodic surveys.

Facilities

Our corporate headquarters are located in Edison, New Jersey, in an office consisting of approximately 63,000 square feet of office, testing and product design space. We have a ten (10) year lease on our corporate headquarters, which expires on September 14, 2026.

Our manufacturing facility is located in the Turtle Creek, Pittsburgh area in Pennsylvania. In January 2022, the Company entered into a new lease agreement for a building next to our existing manufacture site. We expect to expand our annual manufacturing capacity from approximately 260 MWh to approximately 800+ MWh in 2022. The leases of the facility expire on December 31, 2026.

We believe that our existing properties are in good condition and are sufficient and suitable for the conduct of our business for the foreseeable future. To the extent we need to increase our footprint as our business grows, we expect that additional space and facilities will be available.

Available Information

Our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and all amendments to these reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 are available free of charge on our investor website, located at https://investors.eose.com/, as soon as reasonably practicable after they are filed with or furnished to the Securities and Exchange Commission. Our reports are also available on the Securities and Exchange Commission's website at https://www.sec.gov/. The information on our website is not, and shall not be deemed to be, a part hereof or incorporated into this or any of our other filings with the SEC.

ITEM 1A. RISK FACTORS

In addition to the factors discussed elsewhere in this Report, the following risks and uncertainties could materially and adversely affect the Company’s business, financial condition, results of operations, and cash flows.

Risk Factors Summary

The following is a summary of the principal risks that could adversely affect our business, operations and financial results.

Risks Related to Our Business and Industry

•We have a history of losses that casts substantial doubt as to our ability to continue as a going concern. We have to deliver on our potential for significant business growth and improved manufacturing processes to achieve sustained, long-term profitability and long-term commercial success.

18

•We identified material weaknesses in our internal controls over financial reporting at December 31, 2021 and 2020, and we may identify additional material weaknesses in the future that may cause us to fail to meet our reporting obligations or result in material misstatements of our financial statements. If we fail to remediate these material weaknesses or if we otherwise fail to establish and maintain effective control over financial reporting, our ability to accurately and timely report our financial results could be adversely affected.

•The relatively recent commercialization of our products makes it difficult to evaluate our future prospects.

•If demand for energy storage solutions does not continue to grow or grows at a slower rate than we anticipate, our business and results of operations may be impacted.

•Failure to deliver the benefits offered by our technologies, or the emergence of improvements to competing technologies, could reduce demand for our products and harm our business.

•As we endeavor to expand our business, we will incur significant costs and expenses, which could outpace our cash reserves. Unfavorable conditions or disruptions in the capital and credit markets may adversely impact business conditions and the availability of credit.

•The failure or breach of our IT systems could affect our sales and operations.

•The nature of our business exposes us to potential legal proceedings or claims that could adversely affect our operating results. These claims could conceivably exceed the level of our liability insurance coverage.

Risks Related to Our Products and Manufacturing

•We must obtain Underwriters Laboratories ("UL") and other related certifications for our future generations of product.

•We have limited manufacturing experience and could experience difficulty in producing commercial volumes of the battery storage system.

•We may experience difficulties in establishing manufacturing capacity to scale and in meeting potential cost savings and efficiencies from anticipated improvements to our manufacturing capabilities.

•We may experience delays, disruptions, or quality control problems in our manufacturing operations.

•Defects or performance problems in our products could result in loss of customers, and decreased revenue, as well as warranty, indemnity, and product liability claims.

•We are heavily dependent on third-party suppliers and contractors. Supply chain issues could adversely affect our operations and financial results.

•If we elect to expand our production capacity by constructing one or more new manufacturing facilities, we may encounter challenges relating to the construction, management and operation of such facilities.

•Failure to meet our goals and disclosures related to ESG matters or to keep up with evolving trends, regulations and shareholder expectations relating to ESG issues or reporting could adversely impact our reputation, share price, access to and cost of capital and financial results.

Risks Related to Our Future Growth

•If we fail to manage our recent and future growth effectively, we may be unable to execute our business plan, maintain high levels of customer service, or adequately address competitive challenges.

•We will require additional financing to achieve our long-term goals and a failure to obtain this capital on acceptable terms may adversely impact our ability to support our business growth strategy.

•Our planned expansion into new geographic markets or new product lines or services could subject us to additional business, financial, and competitive risks.

•Our results of operations may fluctuate from quarter to quarter, which could make our future performance difficult to predict and could cause our results of operations for a particular period to fall below expectations, resulting in a decline in the price of our common stock.

•Forecasts of market growth in this Form 10-K may not be accurate.

Risks Related to Our United States and Foreign Operations

•The reduction, elimination or expiration of government subsidies and economic incentives related to renewable energy solutions could reduce demand for our technologies and harm our business.

•Changes in the U.S. trade environment, including the imposition of import tariffs, could adversely affect the amount or timing of our revenues, results of operations or cash flows.

•Supply chain constraints due to the Covid-19 pandemic could affect our ability to deliver product to customers on time.

19

•Changes in applicable law, regulations or requirements, or our material failure to comply with any of them, can increase our costs and have other negative impacts on our business.

•We could be adversely affected by any violations of the FCPA, the U.K. Bribery Act, and other foreign anti-bribery laws, as well as violations against export controls and economic embargo regulations.

Risks Related to Intellectual Property

•If we fail to protect, or incur significant costs in defending, our intellectual property and other proprietary rights, then our business and results of operations could be materially harmed.

•Third parties may assert that we are infringing upon their intellectual property rights, which could divert management’s attention, cause us to incur significant costs, and prevent us from selling or using the technology to which such rights relate.

Risk Related to Our Securities

•Provisions in our Charter may inhibit a takeover of us, which could limit the price investors might be willing to pay in the future for our common stock and could entrench management.

•Future resales of common stock may cause the market price of our securities to drop significantly, even if our business is doing well.

•We may redeem the public warrants prior to their exercise at a time that is disadvantageous to such warrant holders, thereby making your public warrants worthless.

•Our stock price may be volatile and may decline regardless of our operating performance.

•There can be no assurance that the warrants will be in the money at the time they become exercisable, and they may expire worthless.

•There can be no assurance that our common stock will be able to comply with the continued listing standards of Nasdaq.

Risk Related to Our Status as a Public Company

•Effective December 31, 2021, we no longer qualify as an “an emerging growth company” and the reduced disclosure requirements applicable to emerging growth companies no longer apply, which has increased our costs and demands on management.

Risk Factors

An investment in our securities involves a high degree of risk. You should carefully consider the risks described below before making an investment decision. Our business, prospects, financial condition, or operating results could be harmed by any of these risks, as well as other risks not known to us or that we consider immaterial as of the date of this Form 10-K. The trading price of our securities could decline due to any of these risks, and, as a result, you may lose all or part of your investment.

Risks Related to Our Business and Industry

We have a history of losses that casts substantial doubt as to our ability to continue as a going concern. We have to deliver on our potential for significant business growth and improved manufacturing processes to achieve sustained, long-term profitability and long-term commercial success.

We have had net losses and negative operating cash flows each fiscal quarter since inception of our business. For the years ended December 31, 2021, 2020, and 2019, we had $124.2 million, $70.6 million and $79.5 million in net losses, respectively. We expect to continue to incur losses and experience negative operating cash flows for the foreseeable future, as we anticipate continued investment in the development and launch of product with outside capital at the expense of short-term profitability. For the fiscal year ended December 31, 2021, the Company concluded that there was substantial doubt about its ability to continue to operate as a going concern for the 12 months following the issuance of these consolidated financial statements.

20

Although our available capital has increased substantially with our Merger with BMRG and issuance of convertible notes, we continue to have limited resources relative to certain of our competitors, especially certain Li-ion manufacturers that have a longer history, are part of large multinational corporations and are already operating at a profit. To achieve profitability as well as long-term commercial success, we must continue to execute our plan to expand our business, which will require us to deliver on our existing global sales pipeline in a timely manner, increase our production capacity, improve our cost profile, grow demand for our products, and seize new market opportunities by leveraging our proprietary technology and its manufacturing processes for novel solutions. Failure to do one or more of these things could prevent us from achieving sustained, long-term commercial success.

As we transition from our research and development to early commercialization phase, we expect, based on our sales pipeline, to grow revenues. However, our revenue may not grow as expected for a number of reasons, many of which are outside of our control, including a decline in global demand for battery storage products, increased competition, or our failure to continue to capitalize on growth opportunities. In addition, although we have achieved sales of our products to potential customers, it is not clear to what extent, if any, the products will be profitable and when. The costs of goods associated with production of our battery storage system are significant. While we are working to optimize our supply chain, improve the speed and efficiency of our manufacturing processes, and lower the cost of other input costs such as raw material and conversion costs, there can be no assurance that we will be successful in these efforts. If we are not able to sustain revenue growth, reduce cost and continue to raise the capital necessary to support operations, our failure to achieve or maintain profitability could negatively impact the value of our common stock.

We identified material weaknesses in our internal controls over financial reporting at December 31, 2021 and 2020, and we may identify additional material weaknesses in the future that may cause us to fail to meet our reporting obligations or result in material misstatements of our financial statements. If we fail to remediate these material weaknesses or if we otherwise fail to establish and maintain effective control over financial reporting, our ability to accurately and timely report our financial results could be adversely affected.

Our management is responsible for establishing and maintaining adequate internal control over financial reporting designed to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with GAAP. Our management is likewise required, on a quarterly basis, to evaluate the effectiveness of our internal controls and to disclose any changes and material weaknesses identified through such evaluation in those internal controls. A material weakness is a deficiency, or a combination of deficiencies, in internal control over financial reporting, such that there is a reasonable possibility that a material misstatement of our annual or interim financial statements will not be prevented or detected on a timely basis.

As described in Item 9A in this Annual Report on Form 10-K, we have identified a material weakness in our internal control over financial reporting. As a result of this material weakness, our management has concluded that our internal control over financial reporting was not effective as of December 31, 2021. The Company intends to take steps to remediate this material weakness, including increasing the depth and experience within its accounting and finance organization, as well as designing and implementing improved processes and internal controls. However, our efforts to remediate this material weakness may not be effective in preventing a future material weakness or significant deficiency in the Company’s internal control over financial reporting. If the Company’s efforts are not successful or other material weaknesses or control deficiencies occur in the future, the Company may be unable to report its financial results accurately and/or on a timely basis, which could cause the Company’s reported financial results to be materially misstated, result in the loss of investor confidence and cause the market price of the Company’s common stock to decline.

We can give no assurance that the measures we have taken or that the Company plans to take in the future will remediate the material weakness identified or that any additional material weaknesses or restatements of financial results will not arise in the future due to a failure to implement and maintain adequate internal control over financial reporting or circumvention of these controls.