UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the fiscal year ended December 31 , 2020

OR

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from to

Commission file number 001-39329

(Exact name of registrant as specified in its charter)

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | ||||||||||

(Address of principal executive offices and Zip Code)

(212 ) 883-0200

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark whether the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark whether the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports); and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ | ||||||||

☒ | Smaller reporting company | ||||||||||

Emerging growth company | |||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

The aggregate market value of the voting and non-voting ordinary shares held by non-affiliates of the registrant as of June 30, 2020, the last business day of the registrant's most recently completed second fiscal quarter, was approximately $4.2 billion based upon the closing price reported for such date on the Nasdaq Global Select Market. This determination of affiliate status is not necessarily a conclusive determination for any other purposes.

As of February 19, 2021, Royalty Pharma plc had 388,134,040 Class A ordinary shares outstanding and 218,976,830 Class B ordinary shares outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

ROYALTY PHARMA PLC

| PART I | ||||||||

| Item 1. | ||||||||

| Item 1A. | ||||||||

| Item 1B. | ||||||||

| Item 2. | ||||||||

| Item 3. | ||||||||

| Item 4. | ||||||||

| PART II | ||||||||

| Item 5. | ||||||||

| Item 6. | ||||||||

| Item 7. | ||||||||

| Item 7A. | ||||||||

| Item 8. | ||||||||

| Item 9. | ||||||||

| Item 9A. | ||||||||

| Item 9B. | ||||||||

| PART III | ||||||||

| Item 10. | ||||||||

| Item 11. | ||||||||

| Item 12. | ||||||||

| Item 13. | ||||||||

| Item 14. | ||||||||

| PART IV | ||||||||

| Item 15. | ||||||||

| Item 16. | ||||||||

Special Note Regarding Forward-Looking Statements

This Annual Report on Form 10-K contains statements reflecting our views about our future performance that constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. In some cases, you can identify these statements by forward-looking words such as “may,” “might,” “will,” “should,” “expects,” “plans,” “anticipates,” “believes,” “estimates,” “predicts,” “potential” or “continue,” the negative of these terms and other comparable terminology. These forward-looking statements are not historical facts, but rather are based on current expectations, estimates and projections about us, our current and prospective assets, our industry, our beliefs and our assumptions. These statements are not guarantees of future performance and are subject to risks, uncertainties and other factors, some of which are beyond our control and difficult to predict and could cause actual results to differ materially from those expressed or forecasted in the forward-looking statements. There are important factors that could cause our actual results, level of activity, performance or achievements to differ materially from the results, level of activity, performance or achievements expressed or implied by the forward-looking statements, including those factors discussed in Part I under Item 1A. “Risk Factors” in this Annual Report on Form 10-K.

These risks and uncertainties include factors related to:

•sales risks of biopharmaceutical products on which we receive royalties;

•the ability of RP Management, LLC (the “Manager”) to locate suitable assets for us to acquire;

•uncertainties related to the acquisition of interests in development-stage biopharmaceutical product candidates and our strategy to add development-stage product candidates and late stage funding opportunities to our product portfolio;

•the assumptions underlying our business model;

•our ability to successfully execute our royalty acquisition strategy;

•our ability to leverage our competitive strengths;

•actual and potential conflicts of interest with the Manager and its affiliates;

•the ability of the Manager or its affiliates to attract and retain highly talented professionals;

•the effect of changes to tax legislation and our tax position; and

•the risks, uncertainties and other factors we identify elsewhere in this Annual Report on Form 10-K and in our other filings with the SEC.

Although we believe the expectations reflected in the forward-looking statements are reasonable, any of those expectations could prove to be inaccurate, and as a result, the forward-looking statements based on those expectations also could be inaccurate. In light of these and other uncertainties, the inclusion of a projection or forward-looking statement in this Annual Report on Form 10-K should not be regarded as a representation by us that our plans and business objectives will be achieved. Moreover, neither we nor any other person assumes responsibility for the accuracy and completeness of any of these forward-looking statements. We are under no duty to update any of these forward-looking statements after the date of this Annual Report on Form 10-K to conform our prior statements to actual results or revised expectations.

PART I

Item 1. BUSINESS

Overview

We are the largest buyer of biopharmaceutical royalties and a leading funder of innovation across the biopharmaceutical industry. Since our founding in 1996, we have been pioneers in the royalty market, collaborating with innovators from academic institutions, research hospitals and not-for-profits through small and mid-cap biotechnology companies to leading global pharmaceutical companies. We have assembled a portfolio of royalties which entitles us to payments based directly on the top-line sales of many of the industry’s leading therapies, which includes royalties on more than 45 commercial products, including AbbVie and J&J’s Imbruvica, Astellas and Pfizer’s Xtandi, Biogen’s Tysabri, Gilead’s HIV franchise, Merck’s Januvia, Novartis’ Promacta, Vertex’s Kalydeco, Orkambi, Symdeko and Trikafta, and five development-stage product candidates. We fund innovation in the biopharmaceutical industry both directly and indirectly - directly when we partner with companies to co-fund late-stage clinical trials and new product launches in exchange for future royalties, and indirectly when we acquire existing royalties from the original innovators.

Our capital-efficient business model enables us to benefit from many of the most attractive characteristics of the biopharmaceutical industry, including long product life cycles, significant barriers to entry and non-cyclical revenues, but with substantially reduced exposure to many common industry challenges such as early stage development risk, therapeutic area constraints, high research and development costs, and high fixed manufacturing and marketing costs. We have a highly flexible approach that is agnostic to both therapeutic area and treatment modality, allowing us to acquire royalties on the most attractive therapies across the biopharmaceutical industry.

The success of our business has been the result of a focused strategy of actively identifying and tracking the development and commercialization of key new therapies, allowing us to move quickly to make acquisitions when opportunities arise. We acquire royalties on approved products, often in the early stages of their commercial launches, and development-stage product candidates with strong proof of concept data, mitigating development risk and expanding our opportunity set. From 1996 through 2020, we have deployed more than $20 billion of cash to acquire biopharmaceutical royalties, representing approximately 50% of all royalty transactions during this period. From 2012, when we began acquiring royalties on development-stage product candidates, through 2020, we have deployed more than $15 billion of cash to acquire biopharmaceutical royalties, representing approximately 60% of all royalty transactions during this period.

In 2020, we generated cash from operating activities of $2.03 billion, Adjusted Cash Receipts (as defined in “—Non-GAAP Financial Results”) of $1.80 billion and Adjusted Cash Flow (as defined in “—Non-GAAP Financial Results”) of $1.48 billion. We deployed $2.3 billion of cash in 2020 for royalties and related assets.

Portfolio Overview

Our current portfolio includes royalties on more than 45 commercial products and five development-stage product candidates. Growth Products are defined as royalties with a duration beyond December 31, 2020. We define all other royalties on approved products as Mature Products. We believe that end market sales of the therapies in our portfolio are important drivers of our financial performance as a substantial portion of our royalties are based on end market sales. In addition, end market sales are a strong indicator of the importance of the therapies to both patients and the marketers. The following table provides an overview of our current portfolio of royalties:

1

| Product(s) | Marketer(s) | Product Detail | 2020 Royalty Receipts (in millions) | 2020 End Market Sales (in millions)(1) | ||||||||||

| Growth Portfolio (Approved Products) | ||||||||||||||

Cystic fibrosis franchise (2) | Vertex | Portfolio of therapies for the treatment of cystic fibrosis | $ | 551.3 | $ | 6,203 | ||||||||

| Tysabri | Biogen | Therapy for the treatment of relapsing forms of multiple sclerosis | 345.8 | 1,946 | ||||||||||

| Imbruvica | AbbVie, Johnson & Johnson | Therapy for the treatment of hematological malignancies and chronic GVHD | 322.1 | 6,612 | ||||||||||

HIV franchise (3) | Gilead, others | Portfolio of therapies for the treatment and prevention of HIV | 293.8 | 16,890 | ||||||||||

| Xtandi | Pfizer, Astellas | Therapy for the treatment of prostate cancer | 146.4 | 4,170 | ||||||||||

| Januvia, Janumet, Other DPP-IVs | Merck, others | Portfolio of therapies for the treatment of diabetes | 143.8 | 9,007 | ||||||||||

| Promacta | Novartis | Therapy for the treatment of chronic ITP and aplastic anemia | 143.7 | 1,738 | ||||||||||

| Farxiga/Onglyza | AstraZeneca | Therapies for the treatment of diabetes | 25.0 | 2,434 | ||||||||||

| Prevymis | Merck | Therapy for prophylaxis of CMV in adult recipients of stem cell transplant | 21.5 | 281 | ||||||||||

| Emgality | Eli Lilly | Therapy for the treatment of migraine prevention & episodic cluster headache | 9.5 | 363 | ||||||||||

| Crysvita | Ultragenyx, Kyowa Kirin | Therapy for the treatment of X-linked hypophosphatemia | 9.5 | 398 | ||||||||||

| Erleada | Johnson & Johnson | Therapy for the treatment of prostate cancer | 7.9 | 760 | ||||||||||

| IDHIFA | Bristol Myers Squibb | Therapy for the treatment of relapsed/refractory AML with an IDH2 mutation | 6.1 | Not Disclosed | ||||||||||

| Trodelvy | Gilead | Therapy for the treatment of metastatic triple-negative breast cancer | 3.0 | 137 | ||||||||||

| Nurtec ODT | Biohaven | Therapy for the treatment of migraine | 0.7 | 64 | ||||||||||

| Tazverik | Epizyme | Therapy for the treatment for epithelioid sarcoma and follicular lymphoma | 0.5 | 12 | ||||||||||

| Evrysdi | Roche | Therapy for the treatment of spinal muscular atrophy | 0.3 | 61 | ||||||||||

| Orladeyo | BioCryst | Therapy for the treatment of hereditary angioedema prophylaxis | Approved Dec 2020 | |||||||||||

Other Growth Products (4)(5) | 246.5 | 9,848 | ||||||||||||

| Total Royalty Receipts - Growth Products | $ | 2,277.4 | $ | 60,924 | ||||||||||

| Mature Portfolio (Approved Products) | ||||||||||||||

| Letairis | Gilead, GlaxoSmithKline | Therapy for the treatment of pulmonary arterial hypertension | $ | 40.2 | $ | 493 | ||||||||

| Lyrica | Pfizer | Therapy for the treatment of neuropathic pain | 22.9 | 1,425 | ||||||||||

Other Mature Products (6) | 3.9 | 65 | ||||||||||||

| Total Mature Portfolio (Approved Products) | $ | 67.0 | $ | 1,983 | ||||||||||

| Development Stage Product Candidates | ||||||||||||||

| Zavegepant | Biohaven | Potential therapy for the treatment and prevention of migraine (Phase III) | — | — | ||||||||||

| PT027 | Astrazeneca | Potential therapy for the treatment of asthma (Phase III) | — | — | ||||||||||

Seltorexant (7) | Johnson & Johnson | Potential therapy for the treatment of MDD with insomnia symptoms (Phase III) | — | — | ||||||||||

Omecamtiv mercarbil (8) | Cytokinetics | Potential therapy for the treatment of heart failure (Phase III) | — | — | ||||||||||

| BCX9930 | BioCryst | Potential therapy for the treatment of PNH (Phase I) | — | — | ||||||||||

GVHD is Graft Versus Host Disease, ITP is Immune Thrombocytopenic Purpura, CMV is Cytomegalovirus, AML is Acute Myelogenous Leukemia, MDD is Major Depressive Disorder and PNH is Paroxysmal Nocturnal Hemoglobinuria.

Notes:

(1) Represents end market sales for calendar year 2020 as reported by respective product marketers or based on EvaluatePharma projections where marketers have not reported. Sales shown for Crysvita represent EMEA only. Royalty receipts lag product performance by one quarter and can be estimated by applying our publicly disclosed royalty rate to the preceding quarter’s marketer-announced net revenues on a product-by-product basis.

(2) The cystic fibrosis franchise includes the following approved products: Kalydeco, Orkambi, Symdeko/Symkevi and Trikafta/Kaftrio.

(3) The HIV franchise includes the following approved products: Atripla, Truvada, Emtriva, Complera, Stribild, Genvoya, Descovy, Odefsey, Symtuza and Biktarvy; royalties are received on the emtricitabine portion of sales only.

(4) Excludes duplicate end-market sales where we have multiple royalties on the same product: Kombiglyze, Nesina, Onglyza and Soliqua.

(5) Other Growth Products include royalties on the following products: Bosulif, Cimzia, Conbriza/Fablyn/Viviant, Entyvio, Lexiscan, Mircera, Myozyme, Nesina, Priligy and Soliqua. Other Growth Products also include contributions from the Legacy SLP Interest, a distribution from Avillion in respect of the Merck KGaA’s anti-IL 17 nanobody M1095 (the “Merck KGaA Asset”), for which development ceased in 2020 and a payment from Biohaven in respect of an expired option to exercise additional funding of the Biohaven Series A Preferred Shares.

(6) Other Mature Products primarily include royalties on the following products: Prezista and Thalomid.

(7) Royalty was acquired in January 2021.

(8) The financial royalty asset associated with omecamtiv mercarbil was written off in the three months ended December 31, 2020 given the uncertainty around the future of omecamtiv.

2

Biopharmaceutical Industry and the Role of Royalties

Our business is supported by significant growth and unprecedented innovation within the biopharmaceutical industry. Global prescription pharmaceutical sales are expected to grow from approximately $0.9 trillion in 2020 to approximately $1.3 trillion in 2025, representing a CAGR of 7% according to EvaluatePharma despite nearly $125 billion in cumulative sales being lost to expected patent expiries during the same period. The growth of the biopharmaceutical industry is driven by global secular trends, including population growth, increasing life expectancy and growth of the middle classes in emerging markets. In addition, a dramatic acceleration of medical research in recent years has led to a better understanding of the molecular origins of disease and identification of potential targets for therapeutic intervention. This has created research and development opportunities for new drugs. The significant pace of biopharmaceutical innovation coupled with the proliferation of new biotechnology companies and the increasing cost of drug development has created a significant capital need over recent years that we believe will provide a sustainable tailwind for our business.

Royalties play a fundamental and growing role in the biopharmaceutical industry. As a result of the increasing cost and complexity of drug development, the creation of a new drug today typically involves a number of industry participants. Academia and other research institutions conduct basic research and license new technologies to industry for further development. Biotechnology companies typically in-license these new technologies, add value through applied research and early-stage clinical development, and then either out-license the resulting development-stage product candidates to large biopharmaceutical companies for late-stage clinical development and commercialization, or commercialize the products themselves. As new drugs are transferred along this value chain, royalties are created as compensation for the licensing or selling institutions. Biotechnology companies are also increasingly creating royalties on existing products within their portfolios, known as synthetic royalties, in order to provide a source of non-dilutive capital to fund their businesses. As a result of this industry paradigm, the development of a single new drug can lead to the creation of multiple royalties. Given our leadership position within the biopharmaceutical royalty sector, we are able to capitalize on the growing volumes of royalties that are created as new therapies are developed to address unmet medical needs.

Our Business Model

We believe that the following elements of our business and product portfolio provide a unique and compelling proposition to investors seeking exposure to the biopharmaceutical sector.

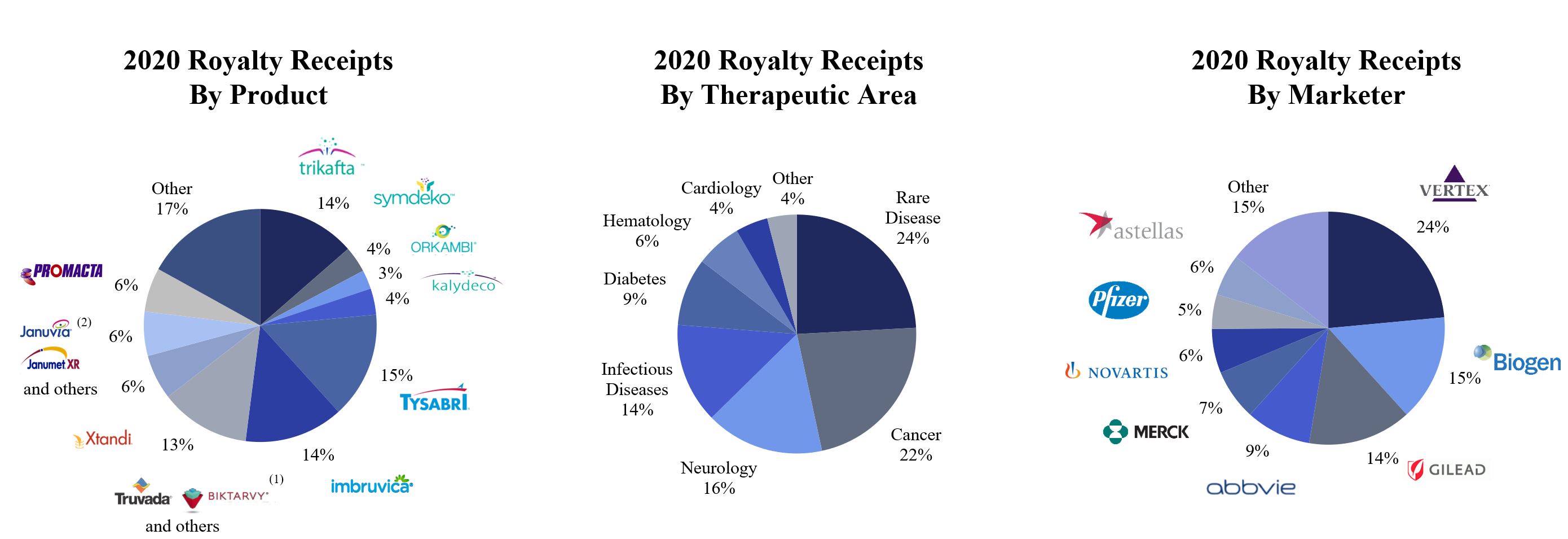

Our portfolio provides direct exposure to a broad array of blockbuster therapies. In 2020, our portfolio included royalties on 20 therapies that each generated end-market sales of more than $1 billion, including seven therapies that each generated end-market sales of more than $3 billion. The therapies within our royalty portfolio are marketed by leading global biopharmaceutical companies for whom these products are important sources of revenue. Given the marketers’ significant focus on and investment in these products, they are motivated to invest substantial resources in driving continued sales growth.

Our portfolio is highly diversified across products, therapeutic areas and marketers. Our portfolio consists of royalties on more than 45 marketed biopharmaceutical therapies which address a wide range of therapeutic areas, including rare diseases, cancer, neurology, HIV, cardiology and diabetes. In the year ended December 31, 2020, no individual therapy accounted for more than 15% of our royalty receipts, no therapeutic area accounted for more than 24% of our royalty receipts and no marketer represented more than 24% of our royalty receipts. The royalties in our portfolio entitle us to payments based directly on the top-line sales of the associated therapies, rather than the profits of these therapies. As such, the diversification of our profits directly reflects the diversification of our royalty receipts, rather than varying levels of product-level profitability, as would typically be expected within a biopharmaceutical company. The graphic below shows the diversification within our 2020 royalty receipts by product, therapeutic area and marketer.

3

Notes:

(1) Comprised of royalty receipts from Truvada, Genvoya, Biktarvy and several other emtricitabine products.

(2) Comprised of royalty receipts from Januvia, Janumet and several other DPP-IVs.

The key growth-driving royalties in our portfolio are protected by long patent lives. The estimated weighted average royalty duration of our portfolio is approximately 15 years based on projected cumulative cash royalty receipts. Our largest marketed royalty in 2020 was on Vertex’s cystic fibrosis franchise, and existing patent applications covering Trikafta, the most significant product in that franchise, are expected to provide exclusivity through 2037. Our right to receive royalties is perpetual, but we expect that the 2037 patent expiration for Trikafta may result in potential sales declines based on potential generic entry. Several of our marketed royalties have unlimited durations and could provide cash flows for many years after key patents have expired.

Simple and efficient operating model generates substantial cash flow for reinvestment in new biopharmaceutical royalties. Our capital-efficient operating model requires limited operating expenses and no material capital investment in fixed assets or infrastructure in order to support the ongoing growth of our business. As a result, we generate high Adjusted Cash Flow relative to our Adjusted Cash Receipts and we convert the vast majority of our Adjusted Cash Flow into operating cash flow. In 2020, we generated cash from operating activities of $2.0 billion, Adjusted Cash Receipts of $1.8 billion and Adjusted Cash Flow of $1.5 billion. We deployed $2.3 billion of cash in 2020 for new royalties and related assets. Our high cash flow conversion provides us with significant capital that we can deploy for new royalty acquisitions, while also growing our dividend to shareholders.

Our business model captures many of the most attractive aspects of the biopharmaceutical industry, but with reduced exposure to many common industry challenges. The biopharmaceutical industry benefits from a number of highly attractive characteristics, including long product life cycles, significant barriers to entry and non-cyclical revenues. We have a highly flexible approach that is agnostic to both therapeutic area and treatment modality, allowing us to acquire royalties on the most attractive therapies from across the biopharmaceutical industry. We focus on the acquisition of royalties on approved products or development-stage product candidates that have generated strong proof of concept data, avoiding the risks associated with early stage research and development. By acquiring royalties, we are able to realize payments based directly on the top-line sales of leading biopharmaceutical therapies, without the costs associated with fixed research and development, manufacturing and commercial infrastructure.

Our unique role in the biopharmaceutical ecosystem positions us to benefit from multiple compounding growth drivers. As a result of our significant scale and highly flexible business model, we believe that we are uniquely positioned to capitalize on multiple compounding growth drivers: an accelerating understanding of the molecular origins of disease, technological innovation leading to the creation of new treatment modalities, increasing number of biopharmaceutical industry participants with significant capital needs, competitive industry dynamics which reward companies that can rapidly execute broad clinical development programs, increasing FDA drug approvals which reached an all-time high in 2018 and the potential for multiple royalties to be created from each new drug that reaches the market.

4

We have the ability to access innovation from across the biopharmaceutical ecosystem. Our approach is to first assess innovative science in areas of significant unmet medical need and then evaluate how to acquire royalties on therapies that we believe are attractive. We closely follow a broad range of therapeutic areas and treatment modalities and are therefore able to move quickly when we identify compelling opportunities to acquire new royalties.

We have deep access to attractively priced investment grade debt that provides a significant cost of capital advantage. We believe that we have an attractive cost of capital that enables us to acquire high-quality biopharmaceutical royalties at competitive prices while still creating value for our shareholders. As of December 31, 2020, we had an aggregate principal amount of $6.0 billion of senior unsecured notes outstanding with a weighted average coupon of 2.125% and a weighted-average maturity of approximately 12 years. In addition, we have an undrawn $1.5 billion five-year unsecured revolving credit facility (the “Revolving Credit Facility”) that we entered into on September 18, 2020.

We have a talented, long-tenured team with extensive experience and deep industry relationships. Our team has significant experience identifying, evaluating and acquiring royalties on biopharmaceutical therapies. Together they have been responsible for $20 billion of acquisitions of biopharmaceutical royalties and related assets. Our acquisitions have included many of the industry’s leading therapies across the past three decades, such as Humira, Imbruvica, Trikafta, Lyrica, Tecfidera, Xtandi, Neupogen and Rituxan, among others. Our long history of collaboration has resulted in deep relationships with a broad range of participants across the biopharmaceutical industry.

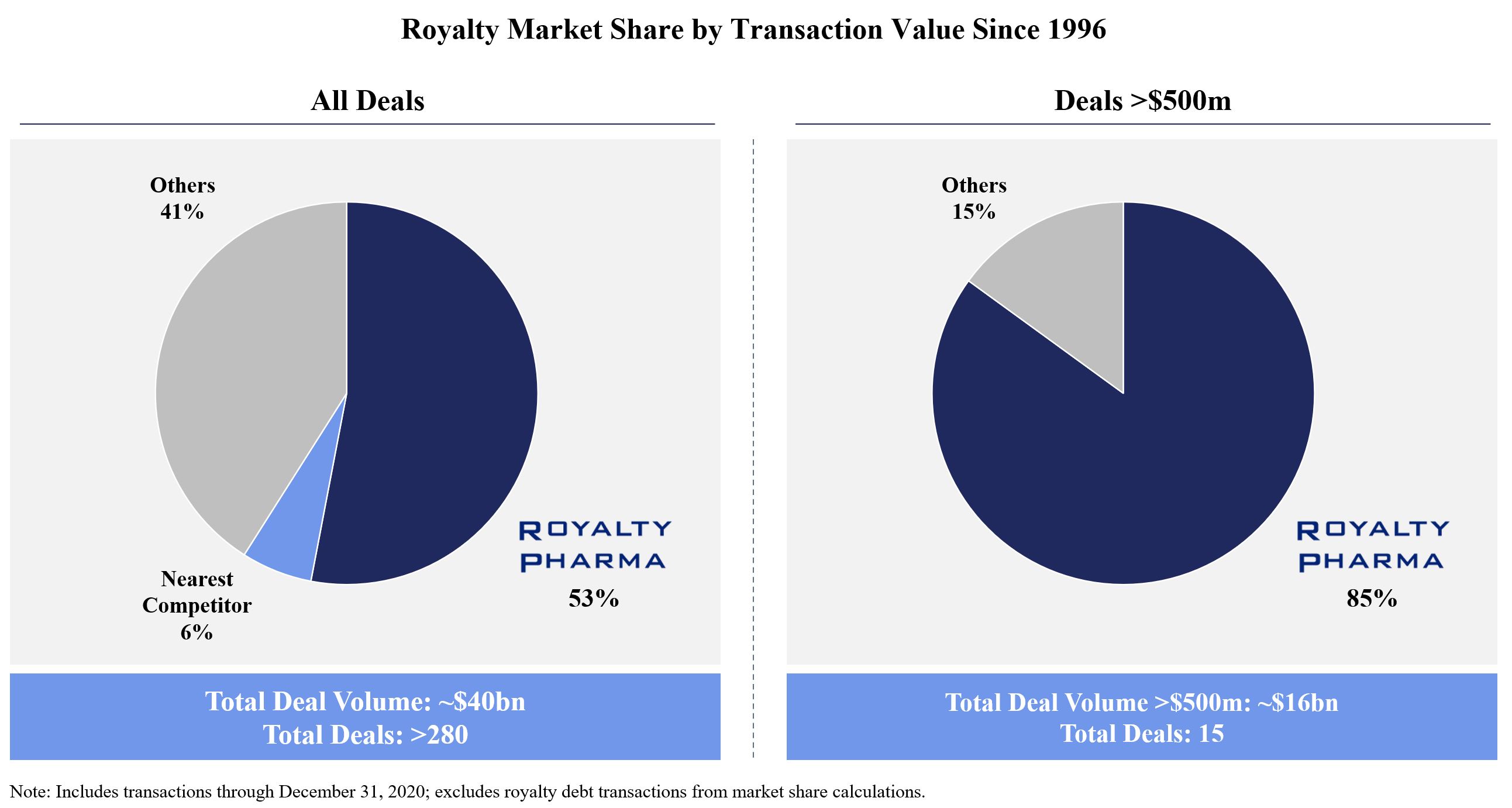

We are the leader in acquiring biopharmaceutical royalties. We are the leader within the space, having executed transactions with an aggregate transaction value of $20 billion of cash. We estimate this to represent an estimated market share of more than 50% by value. This compares to our next nearest competitor, which we believe has executed $2.4 billion of transactions, which we estimate to represent market share of 6%. Given the scale of our business relative to our competitors, we have a particularly strong leadership position within large royalty transactions. Since 1996, there have been 15 transactions with an aggregate value of more than $500 million each. From 1996 through December 31, 2020, we executed 13 of the 15 royalty transactions, for a total aggregate transaction value of $13.5 billion of cash and estimated market share of more than 80%, in this transaction size range. The charts below show our market share since 1996 across all transaction sizes and in royalty transactions with an aggregate value of more than $500 million.

5

Our Strategic Plan to Grow the Portfolio

We intend to grow our business by continuing to partner with constituents across the biopharmaceutical value chain to fund innovation. The three key pillars of our growth strategy are summarized below.

• Acquisition of royalties on approved products which provide dependable cash flows. We intend to continue capturing a leading share of royalties on approved products, particularly those that are early in their life cycles, so that we can participate in the growth that is generated as they penetrate their markets, and enter new indications or geographies.

• Acquisition of royalties on attractive development-stage product candidates. We intend to supplement our diverse portfolio of royalties on approved products with acquisitions of royalties on development-stage product candidates that have generated strong clinical proof of concept data, we can minimize risk while providing attractive upside potential.

• Acquisition of royalties in connection with merger and acquisition (M&A) transactions. We acquire royalties in connection with M&A transactions in a number of ways: by purchasing non-strategic assets following the closing of acquisitions, by partnering with biopharmaceutical companies to acquire other biopharmaceutical companies that own significant royalties, or in select circumstances, by seeking to acquire biopharmaceutical companies on our own that have significant royalties or products that could be out-licensed to create royalties.

We acquire royalties in a number of ways including by acquiring existing royalties, acquiring new synthetic royalties and by funding R&D in exchange for future royalties. During the early years of our business, we focused our acquisitions on royalties on approved biopharmaceutical products. However, as we grew and diversified our business, we began acquiring royalties on development-stage product candidates that had demonstrated strong clinical proof of concept. These development-stage transactions have broadened our landscape of potential opportunities where we are able to leverage our scientific expertise and financial strength.

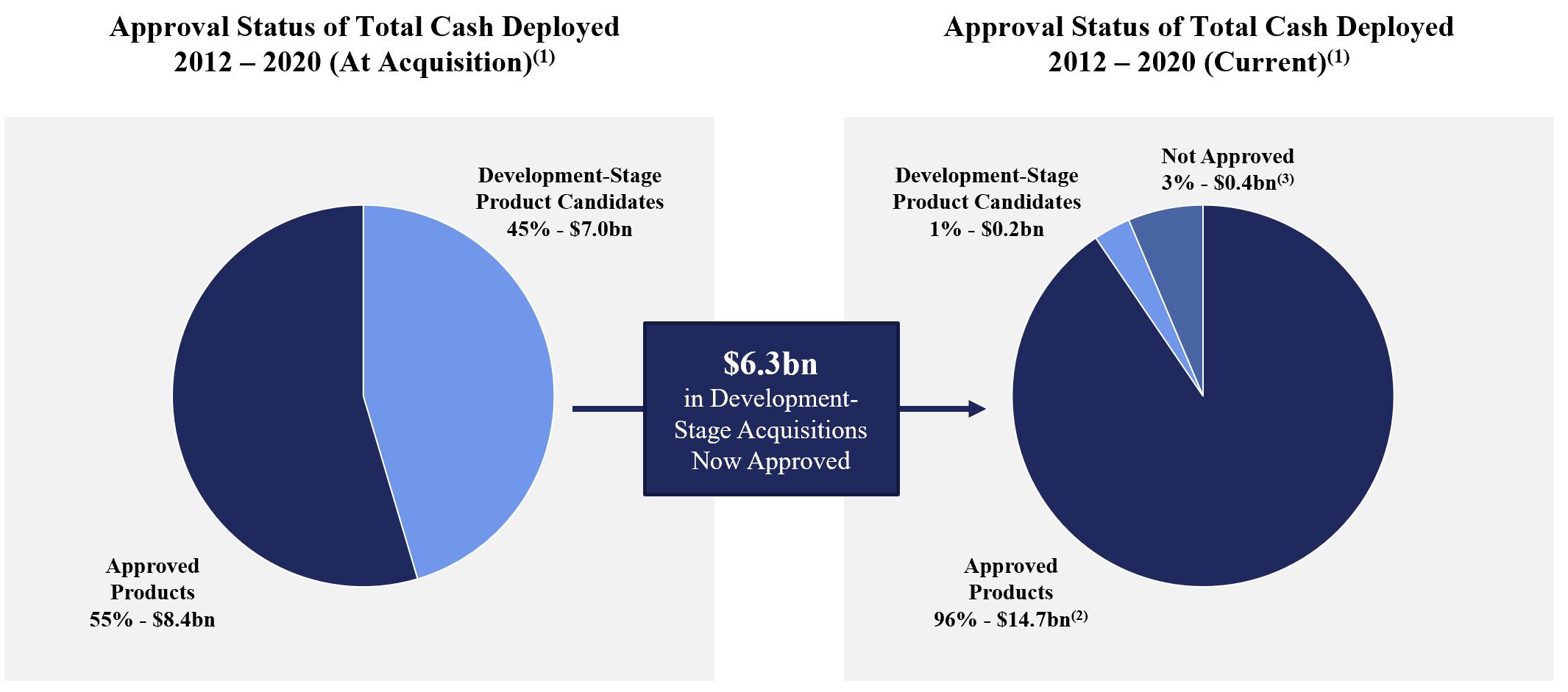

From 2012 through December 31, 2020, we deployed $7.0 billion of cash to acquire royalties on development-stage product candidates. Products underlying $6.3 billion of these acquisitions have already been approved, representing a success rate of 90%, while products underlying $0.4 billion were not approved and products underlying $0.2 billion are still in development.

Notes:

(1) Reflects cash deployed for royalty acquisitions from 2012 through 2020.

(2) Includes Epizyme equity investment; Tazverik not yet approved in Japan.

(3) Includes $100 million Cytokinetics/omecamtiv investment; includes $16 million in R&D funding for Merck KGaA’s anti-IL 17 nanobody M1095, for which we received a cash payment of 1.25 times upon termination of development.

6

In recent years, we have increased the scope of our investments beyond royalties to include additional assets such as equity investments and the acquisition of businesses with significant royalty assets. Our broad scope maximizes our total addressable market and has allowed us to provide a broad range of solutions to our partners across the biopharmaceutical ecosystem.

Our approach is to first assess innovative science in areas of significant unmet medical need and then evaluate how to acquire royalties on therapies that we believe are attractive. We have a strong base of institutional knowledge of important therapeutic areas and key industry trends. Our team of scientific experts actively monitors the evolving treatment landscape across many therapeutic areas and treatment modalities in order to identify new opportunities. We analyze a wide range of scientific data and stay in constant communication with leading physicians, scientists, biopharmaceutical executives and venture capital firms. This allows us to quickly assess and gain conviction in the value of assets when acquisition opportunities arise.

We take a disciplined approach in assessing opportunities and seek to acquire exposure to therapies based on the following key product characteristics:

• Clinically validated: therapies that have received regulatory approval or have strong clinical proof-of-concept data that gives us confidence in the clinical and commercial profile.

• High unmet need: therapies that address areas of significant unmet medical need that also represent large commercial opportunities.

• Significant benefits to patients: therapies that have potential to disrupt or significantly enhance the treatment paradigm for patients and physicians based on compelling clinical data.

• Unique competitive positioning: therapies that are well-positioned to be leaders in their respective categories and are expected to maintain a competitive advantage in the long-term.

• Growth potential: therapies where we see strong long-term potential, based on our in-depth evaluation and in-house expertise.

• Strong marketer: therapies marketed by biopharmaceutical companies that have the resources, capabilities and commitment to successfully develop them and maximize their commercial potential.

• IP: therapies that have strong patent portfolios and offer durable, long-term cash flows.

• Attractive value proposition: therapies that we believe provide value-add to the healthcare system.

Our focus is to create significant long-term value for our shareholders by acquiring both approved and development-stage product candidates through a variety of structures. In evaluating these acquisition opportunities, we focus on the following financial characteristics:

• Long duration cash flows: we prioritize long-duration assets over short-duration assets that may boost near-term financial performance. The durability of our cash flows also allows us to add leverage to our portfolio, enhancing returns and providing capital that we can use to acquire additional assets.

• Attractive risk-adjusted returns: we focus on generating attractive returns on our investments on a risk-adjusted basis. We do not target the same return for all assets and evaluate opportunities across the risk spectrum.

• Growth and scale: we seek assets that are accretive to our long-term growth profile and additive to our overall scale.

7

We conduct extensive due diligence when evaluating potential new opportunities. We have end-to-end capabilities that span clinical and commercial analysis, valuation and transaction structuring. We have a highly focused and experienced team that conducts proprietary primary market research, forms its own views on the clinical and commercial outlook for the product, and builds its own financial models, allowing us to generate direct insights and allowing us to take significant accountability and ownership for our investments. We invest significant time and resources across all levels of the organization, including senior leadership, in the evaluation of potential opportunities.

Our Portfolio

Commercial Products

The key royalties in our marketed portfolio related to approved products include the ones listed below. Descriptions of estimated royalty expiration dates are based on our estimates of patent expiry dates (which may include estimated patent term extensions) or estimates of the dates on which the royalties otherwise expire and are based on each product’s key geographies; duration may differ in other geographies. Royalty expiration dates can change due to patent, regulatory, commercial or other developments. In addition, the royalties in our portfolio are subject to the underlying contractual agreements from which they arise and may be subject to reductions or other adjustments in accordance with the terms of such agreements.

Cystic fibrosis franchise

Our cystic fibrosis franchise consists of our right to receive royalty payments on the sale of various products marketed by Vertex for use in the treatment of cystic fibrosis, including Kalydeco (ivacaftor), Orkambi (lumacaftor and ivacaftor), Symdeko/Symkevi (tezacaftor and ivacaftor) and Trikafta/Kaftrio (elexacaftor, tezacaftor and ivacaftor). Vertex’s cystic fibrosis franchise represents the leading treatments for cystic fibrosis, providing treatment options for approximately 90% of cystic fibrosis patients.

We added the cystic fibrosis franchise to our portfolio in November 2014 and purchased an additional residual royalty interest in November 2020. Our right to receive royalties is perpetual, but we expect that the 2037 patent expiration for Trikafta may result in potential sales declines based on potential generic entry. Total global end market sales for the cystic fibrosis franchise during 2020 were $6.2 billion and we collected $551 million in related royalty receipts over the same period. Global end market sales of the cystic fibrosis franchise are projected to grow to approximately $10.1 billion in 2026, according to EvaluatePharma.

Tysabri

Tysabri (natalizumab) is a monoclonal antibody marketed by Biogen for the treatment of relapsing forms of multiple sclerosis (RMS), including clinically isolated syndrome, relapsing-remitting disease and active secondary progressive disease. Tysabri competes in the high efficacy segment of the multiple sclerosis market, often reserved for patients with aggressive disease at onset and patients who have failed front-line therapies.

We added Tysabri to our portfolio in February 2017. Our right to receive royalties is perpetual. Total global end market sales for Tysabri during 2020 were $1.9 billion and we collected $346 million in related royalty receipts over the same period. Global end market sales of Tysabri are projected to be approximately $1.5 billion in 2026, according to EvaluatePharma.

Imbruvica

Imbruvica (ibrutinib) is a first-in-class small molecule Bruton’s tyrosine kinase inhibitor marketed by AbbVie and Janssen, a subsidiary of Johnson & Johnson, that is the leading therapy in chronic lymphocytic leukemia, relapsed/refractory mantle cell lymphoma and other blood cancers. A robust clinical program supports Imbruvica's use across a wide range of patient populations and cancer types, including 11 FDA approvals in six distinct indications with more than 200,000 patients treated globally.

We added Imbruvica to our portfolio in July 2013. We estimate that our royalties will substantially end from 2027-2029. Total global end market sales for Imbruvica during 2020 were $6.6 billion and we collected $322 million in related royalty receipts over the same period. Global end market sales of Imbruvica are projected to grow to approximately $10.0 billion in 2026, according to EvaluatePharma.

8

HIV franchise

Our HIV franchise consists of our right to receive royalty payments on the sale of various products, including Atripla, Biktarvy, Complera, Descovy, Emtriva, Genvoya, Odefsey, Stribild, Symtuza and Truvada, which have been approved for the treatment and prevention of human immunodeficiency virus infection and acquired immune deficiency syndrome (HIV). Gilead is the primary marketer for the products in our HIV franchise.

We added the HIV franchise to our portfolio starting in July 2005. We estimate that our royalties will substantially end in 2021. Total global end market sales for the products in the HIV franchise during 2020 were $16.9 billion and we collected $294 million in related royalty receipts over the same period.

Xtandi

Xtandi (enzalutamide) is an oral, small molecule androgen receptor inhibitor marketed by Pfizer and Astellas for the treatment of non-metastatic and metastatic castration-resistant prostate cancer as well as metastatic castration sensitive prostate cancer.

We added Xtandi to our portfolio in March 2016. We estimate that our royalties will substantially end from 2027-2028. Total global end market sales for Xtandi during 2020 were approximately $4.2 billion and we collected $146 million in related royalty receipts over the same period. Global end market sales of Xtandi are projected to grow to approximately $6.2 billion in 2026, according to EvaluatePharma.

Januvia, Janumet, other DPP-IVs

We hold patents covering the DPP-IV inhibitors which entitle us to royalty payments on the sale of various products, including Januvia (sitagliptin) / Janumet (sitagliptin and metformin) marketed by Merck; Onglyza (saxagliptin) / Kombiglyze (saxagliptin and metformin) and Qtern (dapagliflozin and saxagliptin), which are marketed by AstraZeneca; Novartis’ Galvus (vildagliptin) / Eucreas (vildagliptin and metformin); Tradjenta (linagliptin) / Jentadueto (linagliptin and metformin) marketed by Boehringer Ingelheim and Eli Lilly; and Nesina (alogliptin) marketed by Takeda, which have been approved for the treatment of Type 2 diabetics in substitution of, or in addition to, insulin therapy.

We added the DPP-IV inhibitors to our portfolio in June 2011. Our royalties on Januvia and Janumet will expire in 2022 and royalties on the other DPP IVs have substantially ended. Total global end market sales for the DPP-IV inhibitors during 2020 were $9.0 billion and we collected $144 million in related royalty receipts over the same period.

Promacta

Promacta (eltrombopag) is an oral, small molecule activator of the thrombopoietin receptor used to increase the number of platelets in the blood, marketed by Novartis for the treatment of chronic immune thrombocytopenia and aplastic anemia.

We added Promacta to our portfolio in March 2019. We estimate that our royalties will substantially end from 2025-2027. Total global end market sales for Promacta during 2020 were $1.7 billion and we collected $144 million in related royalty receipts over the same period. Global end market sales of Promacta are projected to be approximately $0.6 billion in 2026, according to EvaluatePharma.

Prevymis

Prevymis (letermovir) is a first-in-class prophylactic marketed by Merck for the prophylaxis of cytomegalovirus infection and disease in adults who have received an allogeneic hematopoietic stem cell transplant.

We added Prevymis to our portfolio in the second quarter of 2020. We estimate that our royalties will substantially end in 2029. Total global end market sales for Prevymis during 2020 were $281 million and we collected $21 million in related royalty receipts over the same period. Global end market sales of Prevymis are projected to grow to approximately $0.9 billion in 2026, according to EvaluatePharma.

9

Emgality

Emgality (galcanezumab-gnlm) is a monoclonal antibody calcitonin gene-related peptide (CGRP) receptor antagonist indicated for the preventive treatment of migraine and for the treatment of episodic cluster headache.

We added Emgality to our portfolio in March 2019. We estimate that our royalties will substantially end in 2033. Total global end market sales for Emgality during 2020 were $363 million and we collected $10 million in related royalty receipts over the same period. Global end market sales of Emgality are projected to grow to approximately $1.1 billion in 2026, according to EvaluatePharma.

Crysvita

Crysvita (burosumab) is a monoclonal antibody against fibroblast growth factor 23 that has received European conditional marketing authorization for the treatment of X-linked hypophosphatemia (XLH) with radiographic evidence of bone disease in children one year of age and older and adolescents with growing skeletons. In October 2020, this authorization was expanded to include older adolescents and adults.

We added a royalty on Crysvita sales in Europe to our portfolio in December 2019. Our royalties expire when we receive aggregate royalties equal to $608 million if that happens prior to December 31, 2030, and otherwise when we receive aggregate royalties of $800 million. We estimate that our royalties will substantially end from 2033-2038. Total global end market sales for Crysvita during 2020 were approximately $398 million and we collected approximately $9 million in related royalty receipts over the same period. Global end market sales of Crysvita are projected to grow to approximately $2.0 billion in 2026, according to EvaluatePharma.

Erleada

Erleada (apalutamide) is an oral, small molecule androgen receptor inhibitor indicated for the treatment of patients with non-metastatic castration-resistant prostate cancer and for the treatment of patients with metastatic castration sensitive prostate cancer.

We added Erleada to our portfolio in February 2019. We estimate that our royalties will substantially end in 2032. Total global end market sales for Erleada during 2020 were $760 million and we collected approximately $8 million in related royalty receipts over the same period. Global end market sales of Erleada are expected to grow to approximately $2.2 billion in 2026, according to EvaluatePharma.

IDHIFA

IDHIFA (enasidenib) is an oral, targeted therapy approved by the FDA for the treatment of adult patients with relapsed or refractory acute myeloid leukemia with an isocitrate dehydrogenase-2 (IDH2) mutation. It is marketed by Bristol Myers Squibb.

We added IDHIFA to our portfolio in June 2020. We estimate that our royalties will substantially end from 2033-2037. End market sales for IDHIFA are not disclosed by Bristol Myers Squibb, but we collected approximately $6 million in related royalty receipts in 2020. We also hold rights to receive up to $55 million in outstanding regulatory milestone payments from Bristol Myers Squibb.

Trodelvy

Trodelvy (sacituzumab govitecan-hziy) is an antibody-drug conjugate approved by the FDA for the treatment of adult patients with metastatic triple-negative breast cancer. Trodelvy was initially developed by Immunomedics and is now marketed by Gilead following the acquisition of Immunomedics in 2020. Gilead is exploring monotherapy and combinations of Trodelvy across numerous cancer indications and lines of therapy.

10

We added Trodelvy to our portfolio in January 2018. Our right to receive royalties is perpetual. Total global end market sales for Trodelvy during 2020 were $137 million and we collected approximately $3 million in related royalty receipts over the same period. Global end market sales of sacituzumab govitecan are expected to grow to approximately $2.4 billion in 2026, according to EvaluatePharma.

Nurtec ODT

Nurtec ODT (rimegepant) is an oral, small molecule CGRP receptor antagonist marketed by Biohaven Pharmaceuticals for the acute treatment of migraine.

We added Nurtec ODT to our portfolio in June 2018 and purchased an additional interest as part of our expanded funding agreement with Biohaven in August 2020. We estimate that our royalties will substantially end from 2034-2036. Total global end market sales for Nurtec ODT during 2020 were approximately $64 million and we collected less than $1 million in related royalty receipts over the same period. Global end market sales of Nurtec ODT are projected to grow to approximately $1.6 billion in 2026, according to EvaluatePharma.

Tazverik

Tazverik (tazemetostat) is a first-in-class, oral EZH2 inhibitor marketed by Epizyme that was granted accelerated approval for the treatment of epithelioid sarcoma and follicular lymphoma.

We added Tazverik to our portfolio in November 2019. We estimate that our royalties will substantially end in 2034. Total global end market sales for Tazverik during 2020 were $12 million and we collected less than $1 million in related royalty receipts over the same period. Global end market sales of Tazverik are projected to grow to approximately $1.0 billion in 2026, according to EvaluatePharma.

Evrysdi

Evrysdi (risdiplam) is a survival motor neuron 2 (SMN2) splicing modifier marketed by Roche, and is the first oral treatment approved for infants, children and adults with all types of spinal muscular atrophy.

We added Evrysdi to our portfolio in July 2020. Key patents on Evrysdi in the United States expire in 2035, but our royalty will cease when aggregate royalties paid to us equal $1.3 billion. Total global end market sales for Evrysdi during 2020 were approximately $61 million and we collected less than $1 million in related royalty receipts over the same period. Global end market sales of Evrysdi are expected to grow to approximately $2.0 billion in 2026, according to EvaluatePharma.

Orladeyo

Orladeyo (berotralstat) is a first-in-class oral inhibitor of plasma kallikrein marketed by BioCryst for the prevention of hereditary angioedema attacks.

We added Orladeyo to our portfolio in December 2020. Our right to receive royalties is perpetual, but we expect that the 2035-2039 patent expirations for Orladeyo may result in potential sales declines based on potential generic entry. Global end market sales of Orladeyo are expected to grow to approximately $0.4 billion in 2026, according to EvaluatePharma.

Development-Stage Product Candidates

Our current portfolio includes five development-stage product candidates. These development-stage product candidates have not yet been approved, and therefore have not generated any royalties (and we have not collected any related royalty receipts) to date.

Zavegepant

Zavegepant is a small molecule CGRP receptor antagonist in clinical development by Biohaven Pharmaceuticals for the acute treatment and prevention of migraines.

11

We added zavegepant to our portfolio in June 2018. We estimate that our royalties will substantially end from 2034-2036. As a result of an additional transaction in 2020, we are also entitled to success-based milestone payments that range from 0.6 times to 2.95 times of the funded amount, depending on the number of regulatory approvals achieved for zavegepant (including 1.9 times for the first zavegepant migraine regulatory approval) that would be paid over a ten-year period.

PT027

PT027 is an investigational fixed dose combination of the inhaled corticosteroid, budesonide and albuterol, a short-acting beta-2 agonist for the treatment of asthma.

In 2018, we agreed to fund up to approximately $105 million over multiple years to fund a portion of the costs for Phase III clinical trials of Avillion II, who simultaneously entered into a co-development agreement with AstraZeneca to advance PT027 through a global clinical development program in exchange for a series of deferred payments and success-based milestones. We estimate that our royalties will substantially end in 2030.

Seltorexant

Seltorexant is a selective orexin 2 receptor antagonist currently in Phase III development for the treatment of major depressive disorder (MDD) with insomnia symptoms by Janssen, a subsidiary of Johnson & Johnson.

We added seltorexant to our portfolio in January 2021.

Omecamtiv mecarbil

Omecamtiv mecarbil is an oral, small molecule cardiac myosin activator in Phase III clinical development by Amgen and Cytokinetics for the treatment of heart failure with reduced ejection fraction.

We added omecamtiv mecarbil to our portfolio in 2017. In November 2020, results from the Phase III GALACTIC-HF trial of omecamtiv mecarbil in patients with heart failure showed that the trial met the primary composite endpoint of reduction in cardiovascular death or heart failure events, but did not meet the secondary endpoint of reduction in cardiovascular death. Cytokinetics subsequently regained global rights to develop and commercialize omecamtiv mercarbil when Amgen and Servier elected to terminate their collaboration agreement effective, May 2021. Following the Phase III results and termination of the collaboration announced in 2020, we recognized an impairment charge of $65 million related to the write-off of the associated financial royalty asset of $90 million and its associated provision of $25 million, given the uncertainty around the future of omecamtiv.

BCX9930

BCX9930 is an oral Factor D inhibitor in Phase I clinical development by BioCryst Pharmaceuticals as monotherapy for paroxysmal nocturnal hemoglobinuria and other complement-mediated diseases.

We added BCX9930 to our portfolio in December 2020. Our right to receive royalties is perpetual.

Our Portfolio Products and Product Candidates

The table below provides a summary of the estimated royalty expiration and the royalty rates for our key products:

12

| Product | Therapeutic Area | Estimated Royalty Expiration(1) | Royalty Rate(5) | ||||||||

| Cystic fibrosis franchise | Rare disease | 2037(3) | For combination therapies, sales are allocated equally to each of the active pharmaceutical ingredients; tiered royalties ranging from single digit to subteen percentages on annual worldwide net sales of ivacaftor, lumacaftor and tezacaftor, and mid-single digit percentages on annual worldwide net sales of elexacaftor | ||||||||

| Tysabri | Neurology | Perpetual | Contingent payments of 18% on annual worldwide net sales up to $2.0 billion and 25% on annual worldwide net sales above $2.0 billion | ||||||||

| Imbruvica | Cancer | 2027-2029 | Tiered royalties in the mid-single digits on annual worldwide net sales | ||||||||

| HIV franchise | Infectious disease | 2021(4) | Royalties in the single digit percentages on annual worldwide net sales varying by product depending on contribution of emtricitabine to the total | ||||||||

| Januvia and Janumet | Diabetes | 2022 | Royalties in the low single digit percentages on annual worldwide net sales | ||||||||

| Xtandi | Cancer | 2027-2028 | Royalties slightly less than 4% on annual worldwide net sales | ||||||||

| Promacta | Hematology | 2025-2027 | Tiered royalty ranging from 4.7% to 9.4% on annual worldwide net sales | ||||||||

| Prevymis | Infectious disease | 2029 | Low double-digit royalty on annual worldwide net sales up to $300 million | ||||||||

| Emgality | Neurology | 2033 | Low single-digit royalties on annual worldwide net sales | ||||||||

| Crysvita | Rare disease | 2033-2038(5) | 10% royalty on annual EU, U.K. and Switzerland net sales | ||||||||

| Erleada | Cancer | 2032 | Low single-digit royalties on annual worldwide net sales | ||||||||

| IDHIFA | Cancer | 2033-2037(6) | Tiered royalties in the low double-digits to mid-teens based on annual worldwide sales | ||||||||

| Trodelvy | Cancer | Perpetual | 4.15% royalty on annual worldwide net sales up to $2 billion, declining stepwise based on sales tiers to 1.75% on annual worldwide net sales above $6 billion | ||||||||

| Nurtec ODT and Zavegepant | Neurology | 2034-2036 | 2.1% royalty on annual combined worldwide net sales up to $1.5 billion and 1.5% on annual combined worldwide net sales above $1.5 billion. 0.4% incremental royalty on all Nurtec ODT worldwide net sales and up to a 3.0% incremental royalty on zavegepant worldwide net sales | ||||||||

| Tazverik | Cancer | 2034(7) | Royalties in the mid-teen percentages on annual worldwide net sales, stepping down on annual worldwide net sales above certain sales thresholds | ||||||||

| Evrysdi | Neurology | 2030-2035(8) | Total royalties are tiered at 8% on worldwide net sales up to $500 million, 11% on net sales between $500 million and $1 billion, 14% on net sales between $1 billion and $2 billion, 16% on net sales over $2 billion; Royalty Pharma is entitled to approximately 43% of total royalties | ||||||||

| Orladeyo | Rare disease | 2035-2039(9) | 8.75% on direct annual net sales of up to $350 million, 2.75% on sales between $350 million and $550 million, no royalty on sales over $550 million; tiered percentage of sublicense revenue in certain territories | ||||||||

| PT027 | Respiratory | 2030(10) | Tiered royalties in the low-single digits on annual worldwide net sales(11) | ||||||||

| Seltorexant | Neurology | — | Mid single-digit royalty on worldwide net sales | ||||||||

| Omecamtiv mecarbil | Cardiology | 2032-2033 | 4.5% royalty on annual worldwide net sales | ||||||||

| BCX9930 | Rare disease | Perpetual | 1.0% royalty on annual worldwide net sales | ||||||||

Notes:

(1) Dates shown represent our estimates of when a royalty will substantially end, which may depend on patent expiration dates (which may include patent term extensions) or other factors and may vary by geography. Royalty expiration dates can change due to patent, regulatory, commercial or other developments. There can be no assurances that our royalties will expire when expected.

(2) The royalties in our portfolio are subject to the underlying contractual agreements from which they arise and may be subject to reductions or other adjustments in accordance with the terms of such agreements.

(3) Royalty is perpetual; year shown represents Trikafta expected patent expiration and potential sales decline based on generic entry.

(4) Represents patent expiration date in the United States as patents in major jurisdictions outside the United States have expired.

(5) Royalties expire when we receive aggregate royalties equal to $608 million if that happens prior to December 31, 2030, and otherwise when we receive aggregate royalties of $800 million.

(6) Represents estimated patent expiration dates in the United States and Europe, respectively.

(7) Represents the estimated patent expiration date in the United States.

(8) Key patents on Evrysdi in the United States expire in 2035, but our royalty will cease when aggregate royalties paid to us equal $1.3 billion.

(9) Royalty is perpetual; years shown represent estimated United States patent expiration for Orladeyo and potential sales decline based on generic entry.

(10) AstraZeneca is entitled to certain buyout rights which, if exercised, would result in earlier expiration.

(11) Represents the portion of the royalties owed to Avillion II attributable to our minority ownership stake in Avillion II.

There can be no assurance that patents covering the products generating our royalties will expire when expected. Any reduction in the expected patent term or any other expected period in which we are entitled to receive royalties may adversely affect our financial condition and results of operation. See “Risk Factors” in Item 1A, Risk Factors for further information.

13

Competition

We face competition from other entities that acquire biopharmaceutical royalties, including competitors to the Manager that are in the similar business of acquiring biopharmaceutical royalties. There are a limited number of suitable and attractive acquisition opportunities available in the market. Therefore, competition to acquire such assets is intense. The Manager is subject to competition from other potential royalty buyers, including from the companies that market the products on which royalties are paid, financial institutions and other entities. These potential royalty buyers may be larger and better capitalized than us. The Manager may not be able to identify and obtain a sufficient number of asset acquisition opportunities to invest the full amount of capital that may be available to us. There can be no assurance that we will continue to acquire biopharmaceutical products and companies that hold biopharmaceutical royalties that are acceptable to us.

The products that provide the basis for the cash flows of the biopharmaceutical products in which we invest are also subject to intense competition. The biopharmaceutical industry is a highly competitive and rapidly evolving industry. The length of any product’s commercial life cannot be predicted. There can be no assurance that one or more products will not be rendered obsolete or non-competitive by new products or improvements made to existing products, either by the current marketer of such products or by another marketer. Adverse competition, obsolescence or governmental and regulatory action or healthcare policy changes could significantly affect the revenues, including royalty-related revenues, of the products which serve as the security or other support for the payments due under the biopharmaceutical products that we hold.

Competitive factors affecting the market position and success of each product include:

• effectiveness;

• safety and side effect profile;

• price, including third-party insurance reimbursement policies;

• timing and introduction of the product;

• efficacy of marketing strategy;

• governmental regulation;

• availability of lower-cost generics and/or biosimilars;

• treatment innovations that eliminate or minimize the need for a product; and

• product liability claims.

If a product for which we have a royalty receivable or other interest is rendered obsolete or non-competitive by new products, including generics and/or biosimilars, or improvements on existing therapies or governmental or regulatory action, such developments could have a material adverse effect on the ability of the payor with respect to a biopharmaceutical asset to make payments to us, and consequently could materially adversely affect our business, financial condition and results of operations. If additional side effects or complications are discovered with respect to a product, and such product’s market acceptance is impaired or it is withdrawn from the market, continuing payments with respect to biopharmaceutical products, including royalty payments and payments of interest on and repayment of the principal, relating to such product may not be made on time or at all.

Corporate Responsibility

We are the largest buyer of biopharmaceutical royalties and a leading funder of innovation across the biopharma industry. We play an important role in providing capital to the biopharma ecosystem and thereby positively impact human health. Our responsibility to stakeholders is based around three key areas: integrity (maintaining the highest ethical standards), culture (promoting an inclusive and diverse workforce) and taking responsibility (being a responsible citizen). We do not directly conduct biopharma R&D or manufacture or market the biopharmaceutical assets in which we participate, and thus our environmental impact is minimal. Despite the passive nature of our business, we strive to invest in novel therapies that address unmet patient needs and to support ethical business practices that drive innovation, competition and patient choice.

Integrity

We maintain the highest standards of integrity and trust in our role as investors and partners to the biopharma industry. This is recognized in our market-leading position and the high esteem with which we believe we are held in the industry. We conduct thorough diligence and monitoring with all of our investment positions. The biopharmaceutical companies and academic and non-profit institutions with which we work typically have well-developed and transparent environmental, social and governance (ESG) policies, which seek to benefit wider society through sustainable and ethical business practices.

14

Culture

A diverse, talented and motivated workforce is essential to maintain our competitive advantages and to successfully execute our business strategy. We consider it highly important to strive for an appropriate gender balance: currently approximately 51% of our workforce are women. We take employee engagement and retention very seriously and are proud that on average our workforce has been employed with us for approximately 4.5 years. We are committed to our employees’ health, well-being and job satisfaction and to ensuring that people find purpose in their careers. Opportunities for career enhancement and progression are regularly reviewed.

Responsibility

We are committed to good corporate citizenship and actively supports the work of a number of patient advocacy groups and medical research foundations, including the American Heart Association, the Alliance for Lupus Research, Children of Bellevue, the Melanoma Research Alliance, the National Multiple Sclerosis Society and the Prostate Cancer Foundation. Over one-third (by value) of the transactions we have completed since our founding have been with leading academic and non-profit institutions. By partnering with these institutions, we have provided capital which has been used to further scientific research (for example with the Cystic Fibrosis Foundation) or to help fund capital projects. Our commitment to responsibility starts with our Chief Executive Officer who is a founding member of Boston Children’s Hospital Medical Research Council and serves on the Board of Governors of the New York Academy of Sciences, as well as the Boards of Trustees of Rockefeller University, the Hospital for Special Surgery, the Pasteur Foundation (the U.S. affiliate of the French Institute Pasteur) and the Open Medical Institute. Mr. Legorreta was the founder and is currently Honorary Chairman of Alianza Médica para la Salud, a non-profit dedicated to enhancing the quality of health care in Latin America by providing doctors and healthcare providers with continued education opportunities. Since its foundation in 2010, AMSA has provided over 500 scholarships to Mexican and Latin American doctors and healthcare providers to study abroad. Mr. Legorreta is also a founding member of Mount Sinai’s Institute for Health Equity Research, created in part as a response to the health inequities made apparent by COVID-19. These diverse organizations are united in their quest to advance science, the careers of scientists and human health around the globe.

Employees

Our directors and executive officers will manage our operations and activities. However, we do not currently have any employees or any officers other than our executive officers. Pursuant to the management agreement entered into in connection with our initial public offering (the “Management Agreement”) with the Manager, the Manager will perform corporate and administration services for us.

As of December 31, 2020, the Manager had 51 employees. None of these employees are represented by labor unions or covered by any collective bargaining agreement. We believe that the Manager’s relations with its employees are satisfactory.

Human Capital Resources

Because we are “externally managed,” we do not employ our own personnel, but instead depend upon the Manager and its executive officers and employees for virtually all of the services we require. Under the Management Agreement, the Manager manages the assets of our business and sources and evaluates royalty acquisitions. Accordingly, our success is largely dependent upon the expertise and services of the executive officers and other personnel provided to us through the Manager. The Manager is responsible for the selection of these executive officers and other personnel, and our Board of Directors reviews personnel with the Manager with the objective of evaluating the Manager’s internal capabilities. The Management Agreement requires the Manager’s executives to devote substantially all of their time to managing us and any legacy vehicles related to Royalty Pharma Investments, an Irish Unit Trust (“Old RPI”) or Royalty Pharma Investments 2019 ICAV (“RPI”) unless otherwise approved by our Board of Directors. The Management Agreement also provides for the development of succession plans for the senior management of the Manager by the Management Development and Compensation Committee of our Board of Directors in consultation with the Manager.

15

Governmental Regulation and Environmental Matters

Our business has been and will continue to be subject to numerous laws and regulations. Failure to comply with these laws and regulations could subject us to administrative and legal proceedings and actions by various governmental bodies. See “Risk Factors” in Item 1A, Risk Factors for further information. Our compliance with these laws and regulations has not had a material impact on our capital expenditures, earnings, financial condition or competitive position in excess of those affecting

others in our industry.

We believe that there are no compliance issues with laws and regulations that have been enacted or adopted regulating the discharge of materials into the environment, or otherwise relating to the protection of the environment, that have adversely affected, or are reasonably expected to adversely affect, our business, financial condition and results of operations, and we do

not currently anticipate material capital expenditures arising from environmental regulation. We believe that climate change could present risks to our business. Some of the potential impacts of climate change to our business include increased operating costs due to additional regulatory requirements and the risk of disruptions to our business. We do not believe these risks are material to our business at this time.

U.S. Investment Company Act Status

We intend to conduct our business so as not to become regulated as an investment company under the U.S. Investment Company Act. An entity generally will be determined to be an investment company for purposes of the U.S. Investment Company Act if, absent an applicable exemption, (i) it is or holds itself out as being engaged primarily, or proposes to engage primarily, in the business of investing, reinvesting or trading in securities or (ii) it owns or proposes to acquire investment securities having a value exceeding 40% of the value of its total assets (exclusive of U.S. government securities and cash items) on an unconsolidated basis, which we refer to as the ICA 40% Test.

We do not hold ourselves out as being engaged primarily, or propose to engage primarily, in the business of investing, reinvesting or trading in securities, and believe that we are not engaged primarily in the business of investing, reinvesting or trading in securities. We believe that, for U.S. Investment Company Act purposes, we are engaged primarily, through one or more of our subsidiaries, in the business of purchasing or otherwise acquiring certain obligations that represent part or all of the sales price of merchandise. Our subsidiaries that are so engaged rely on Section 3(c)(5)(A) of the U.S. Investment Company Act, which, according to certain SEC staff interpretations, generally may be available to an issuer who invests at least 55% of its assets in “notes, drafts, acceptances, open accounts receivable, and other obligations representing part or all of the sales price of merchandise, insurance, and services,” which we refer to as ICA Exception Qualifying Assets and not to issue any redeemable securities, face-amount certificates of the installment type or periodic payment plan certificates.

In a no-action letter, dated August 13, 2010, to our predecessor, the SEC staff promulgated an interpretation that royalties that entitle an issuer to collect royalty receivables that are directly based on the sales price of specific biopharmaceutical assets that use intellectual property covered by specific license agreements are ICA Exception Qualifying Assets under Section 3(c)(5)(A). We rely on this no-action letter for the position that royalty receivables relating to biopharmaceutical assets that we hold are ICA Exception Qualifying Assets under Section 3(c)(5)(A) and Section 3(c)(6), which is described below.

As the parent of one or more subsidiaries that rely on Section 3(c)(5)(A), we currently are excepted from registration as an investment company based on Section 3(a)(1)(C) and/or Section 3(c)(6) of the U.S. Investment Company Act. To ensure that we are not obligated to register as an investment company, we must not exceed the thresholds provided by the ICA 40% Test. For purposes of the ICA 40% Test, the term “investment securities” does not include U.S. government securities or securities issued by majority-owned subsidiaries that are not themselves investment companies and are not relying on Section 3(c)(1) or Section 3(c)(7) of the U.S. Investment Company Act, such as majority-owned subsidiaries that rely on Section 3(c)(5)(A). We also may rely on Section 3(c)(6), which, based on SEC staff interpretations, requires us to invest, either directly or through majority-owned subsidiaries, at least 55% of our assets in, as relevant here, businesses relying on Section 3(c)(5)(A). For a subsidiary to be “majority-owned,” a parent entity must own a majority of the voting securities of the applicable security. Therefore, the assets that we and our subsidiaries hold and acquire are limited by the provisions of the U.S. Investment Company Act and the rules and regulations promulgated thereunder.

16

If the SEC or its staff in the future adopts a contrary interpretation to that provided in the no-action letter to Royalty Pharma or otherwise restricts the conclusions in the SEC staff’s no-action letter such that royalties are no longer treated as ICA Exception Qualifying Assets for purposes of Section 3(c)(5)(A) and Section 3(c)(6), or the SEC or its staff in the future determines that the no-action letter does not apply to some or all types of royalty receivables relating to biopharmaceutical assets, our business will be materially and adversely affected. In particular, we would be required either to convert to a corporation formed under the laws of the United States or a state thereof (which would likely result in our being subject to U.S. federal corporate income taxation) and to register as an investment company, or to stop all business activities in the United States until such time as the SEC grants an application to register us as an investment company formed under non-U.S. law. It is unlikely that such an application would be granted and, even if it were, requirements imposed by the Investment Company Act, including limitations on our capital structure, our ability to transact business with affiliates and our ability to compensate key employees, could make it impractical for us to continue our business as currently conducted. Our no longer qualifying for an exemption from registration as an investment company would materially and adversely affect the value of your Class A ordinary shares and our ability to pay dividends in respect of our Class A ordinary shares.

Corporate Information

Our predecessor was founded in 1996 and we were incorporated under the laws of England and Wales on February 6, 2020. We are a holding company, and our principal asset is a controlling equity interest in Royalty Pharma Holdings Ltd. (“RP Holdings”). Our principal executive offices are located at 110 East 59th Street, New York, NY 10022, and our telephone number is (212) 883-0200. Our Internet site is www.royaltypharma.com. Our website and the information contained therein or connected thereto is not incorporated into this Annual Report on Form 10-K. Our agent for service in the United States is CSC North America located at 251 Little Falls Drive, Wilmington, Delaware, 19808.

Available Information

Our reports filed with or furnished to the SEC pursuant to Sections 13(a) and 15(d) of the Securities Exchange Act of 1934, as amended, or the Exchange Act, are available, free of charge, on the Investors section of our website at https://royaltypharma.com as soon as reasonably practicable after we electronically file such material with, or furnish it to, the SEC. The SEC maintains a website at http://www.sec.gov that contains reports, and other information regarding us and other companies that file materials with the SEC electronically. We use the Investor section of our website as a means of disclosing material information. Accordingly, investors should monitor our website, in addition to following our press releases, SEC filings, and public conference calls and webcasts.

Item 1A. RISK FACTORS

Described below are certain risks that we believe apply to our business. You should carefully consider the following information about these risks, together with the other information contained in this Annual Report on Form 10-K, including the section titled “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and related notes. Additional risks and uncertainties not presently known to us or that we currently deem immaterial also may impair our business.

Summary of Risk Factors

Our business is subject to a number of risks, including risks that may adversely affect our business, financial condition and results of operations. These risks are discussed more fully below and include, but are not limited to, risks related to:

Risks Relating to Our Business

•sales risks of biopharmaceutical products on which we receive royalties;

•the growth of the royalty market;

•the ability of the Manager to identify suitable assets for us to acquire;

•uncertainties related to the acquisition of interests in development-stage biopharmaceutical product candidates and our strategy to add development-stage product candidates and late-stage funding opportunities to our product portfolio;

•potential strategic acquisitions of biopharmaceutical companies;

17

•our use of leverage in connection with our capital deployment;

•our reliance on the Manager for all services we require;

•our reliance on key members of the Manager’s senior advisory team;

•our ability to successfully execute our royalty acquisition strategy;

•our ability to leverage our competitive strengths;

•actual and potential conflicts of interest with the Manager and its affiliates;

•interest rate and foreign exchange fluctuations;

•the assumptions underlying our business model;

•our reliance on a limited number of products;

•the ability of the Manager or its affiliates to attract and retain highly talented professionals;

•the competitive nature of the biopharmaceutical industry;

Risks Relating to Our Organization and Structure

•our organizational structure, including our status as a holding company;

Risks Relating to Our Class A Ordinary Shares

•volatility of the market price of our Class A ordinary shares;

•our incorporation under English law;

Risks Relating to Taxation

•the effect of changes to tax legislation and our tax position; and

General Risk Factors

•the impact of COVID-19 on our operations.