UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

For the fiscal year ended December 31 , 2022

OR

For the transition period from ___________ to ___________

Commission file number: 001-39392

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||

(Address of principal executive offices and zip code)

(952 ) 974-2200

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||||||||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ☐No ☒

Yes ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes ☐No ☒

Yes ☐

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | ☒ | Non-accelerated filer | ☐ | Smaller reporting company | ||||||||||||||||||||||||||||||

| Emerging growth company | |||||||||||||||||||||||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal controls over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

The aggregate market value, as of June 30, 2022, of voting shares held by non-affiliates of the registrant was approximately $139,680,681 .

As of March 13, 2023, there were 51,238,218 shares of the registrant's common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

TREAN INSURANCE GROUP, INC.

TABLE OF CONTENTS

| Page | ||||||||

2

Forward-Looking Statements

This Annual Report on Form 10-K contains forward‑looking statements within the meaning of the federal securities laws, which statements involve substantial risks and uncertainties. Forward‑looking statements generally relate to future events or our future financial or operating performance. In some cases, you can identify forward‑looking statements because they contain words such as "may," "will," "should," "expects," "plans," "anticipates," "could," "intends," "target," "projects," "contemplates," "believes," "estimates," "predicts," "would," "potential" or "continue" or the negative of these words or other similar terms or expressions that concern our expectations, strategy, plans or intentions. These forward‑looking statements include, among others, statements relating to our future financial performance, our business prospects and strategy, anticipated financial position, liquidity and capital needs and other similar matters. These forward‑looking statements are based on management’s current expectations and assumptions about future events, which are inherently subject to uncertainties, risks and changes in circumstances that are difficult to predict.

Because such statements are based on expectations as to future financial and operating results and are not statements of fact, actual results may differ materially from those projected and are subject to a number of known and unknown risks and uncertainties, including: (i) the risk that the proposed Merger may not be completed in a timely manner or at all, which may adversely affect our business and the price of our common stock, par value $0.01 per share ("Common Stock"); (ii) the failure to satisfy any of the conditions to the consummation of the proposed transaction, including the adoption of the Merger Agreement by our stockholders and the receipt of certain regulatory approvals; (iii) the occurrence of any event, change, or other circumstance or condition that could give rise to the termination of the Merger Agreement, including in circumstances requiring us to pay a termination fee; (iv) the effect of the announcement or pendency of the proposed transaction on our business relationships, operating results, and business generally; (v) risks that the proposed transaction disrupts our current plans and operations; (vi) Our ability to retain and hire key personnel in light of the proposed transaction; (vii) risks related to diverting management’s attention from our ongoing business operations; (viii) unexpected costs, charges, or expenses resulting from the proposed transaction; (ix) potential litigation relating to the Merger that could be instituted against us, Altaris, or respective directors, managers, or officers, including the effects of any outcomes related thereto; (x) certain restrictions during the pendency of the Merger that may impact our ability to pursue certain business opportunities or strategic transactions; and (xi) unpredictability and severity of catastrophic events, including but not limited to acts of terrorism, war or hostilities, or pandemics, including the COVID-19 pandemic, as well as management’s response to any of the aforementioned factors.

The outcome of the events described in these forward‑looking statements is subject to risks, uncertainties, assumptions and other factors, which in many cases are beyond our control, as described in "Item 1A — Risk Factors," and elsewhere in this Annual Report on Form 10-K. Our statements reflecting these risks and uncertainties are not exhaustive, and other risks and uncertainties may currently exist or may arise in the future that could have material effects on our business, operations and financial condition. We cannot assure you that the results, events and circumstances reflected in the forward‑looking statements reflected in this Annual Report on Form 10-K and our other public statements and securities filings will be achieved or occur, and actual results, events or circumstances could differ materially from those described in the forward‑looking statements.

You should read this Annual Report on Form 10-K and the documents that we reference in this Annual Report on Form 10-K and have filed as exhibits to this Annual Report on Form 10-K with the understanding that our actual future results, levels of activity, performance and achievements may be materially different from what we currently expect. We qualify all of our forward‑looking statements by these cautionary statements.

The forward‑looking statements made in this Annual Report on Form 10-K speak only as of the date on which such statements are made. We undertake no obligation, and do not intend, to update any forward‑looking statements after the date of this Annual Report on Form 10-K or to conform such statements to actual results or revised expectations, except as required by applicable securities laws or other rules and regulations of the SEC.

3

Summary Risk Factors

Our actual results may differ materially from those expressed in, or implied by, the forward‑looking statements included in this Annual Report on Form 10-K as a result of various factors. Our business is subject to numerous risks and uncertainties, including those highlighted in "Item 1A — Risk Factors." These risks include the following:

Risks related to the Proposed Merger

•The proposed Merger may not be completed in a timely manner or at all, which may adversely affect our business and the price of our Common Stock;

•The failure to satisfy any of the conditions to the consummation of the proposed Merger, including the adoption of the Merger Agreement by our stockholders and the receipt of certain regulatory approvals;

•The occurrence of any event, change, or other circumstance or condition that could give rise to the termination of the Merger Agreement, including in circumstances requiring us to pay a termination fee;

•The effect of the announcement or pendency of the proposed Merger on our business relationships, operating results, and business generally;

•The proposed Merger may disrupt our current plans and operations;

•Our ability to retain and hire key personnel in light of the proposed Merger;

•Risks related to diverting management’s attention from our ongoing business operations;

•Unexpected costs, charges, or expenses resulting from the proposed Merger;

•Potential litigation relating to the proposed Merger that could be instituted against us, Altaris, or respective directors, managers, or officers, including the effects of any outcomes related thereto;

•Certain restrictions during the pendency of the proposed Merger that may impact our ability to pursue certain business opportunities or strategic transactions;

Risks related to our business and industry:

•Our Program Partners or our Owned MGAs may fail to properly market, underwrite or administer policies;

•We depend on a limited number of Program Partners for a substantial portion of our gross written premiums;

•Our business is subject to significant geographic concentration;

•We may suffer a downgrade in the A.M. Best financial strength ratings of our insurance company subsidiaries;

•We may be unable to accurately underwrite risks and charge competitive yet profitable rates to our clients and policyholders;

•Renewals of our existing contracts may not meet expectations;

•We may change our underwriting guidelines or our strategy without stockholder approval;

•We may act based on inaccurate or incomplete information regarding the accounts we underwrite;

•Our employees could take excessive risks;

•We may be unable to access the capital markets when needed;

•Adverse economic factors, including recession, inflation, periods of high unemployment or lower economic activity could result in the sale of fewer policies than expected or an increase in frequency or severity of claims and premium;

•Adverse developments affecting the financial services industry, such as actual events or concerns involving liquidity, defaults or non-performance by financial institutions or transactional counterparties, could adversely affect our current and projected business operations and its financial condition and results of operations;

•Negative developments in the workers’ compensation insurance industry could adversely affect our results;

•The insurance industry is cyclical in nature;

•Our failure to accurately and timely pay claims could harm our business;

•The effects of emerging claim and coverage issues on our business are uncertain;

•Our risk management policies and procedures may prove to be ineffective;

•If we are unable to obtain reinsurance coverage at reasonable prices or on terms that adequately protect us, we may be required to bear increased risks or reduce the level of our underwriting commitments;

•We are subject to reinsurance counterparty credit risk. Our reinsurers may not pay on losses in a timely fashion, or at all;

•Some of our issuing carrier arrangements contain limits on the reinsurer's obligations to us;

•Retention of business written by our Program Partners could expose us to potential losses;

•Our loss reserves may be inadequate to cover our actual losses;

•We may not be able to manage our growth effectively;

•Our ability to grow our business will depend in part on the addition of new Program Partners, which may be unavailable;

•We could be harmed by the loss of one or more key executives or by an inability to attract and retain qualified personnel;

•Performance of our investment portfolio is subject to a variety of investment risks;

•Any shift in our investment strategy could increase the risk exposure of our investment portfolio;

4

•We could be forced to sell investments to meet our liquidity requirements;

•We may face increased competition in our programs market;

•We compete with a large number of companies in the insurance industry for underwriting premium;

•Our results of operations, liquidity, financial condition and FSRs are subject to the effects of natural and man-made catastrophic events;

•Global climate change may in the future increase the frequency and severity of weather events and resulting losses;

•Because our business depends on insurance brokers, we are exposed to certain risks arising out of our reliance on these distribution channels;

•Our operating results have in the past varied from quarter to quarter and may not be indicative of our long-term prospects;

•Any failure to protect our intellectual property rights could impair our ability to protect our intellectual property, proprietary technology platform and brand, or we may be sued by third parties for alleged infringement of their proprietary rights;

Technology risks:

•Technology breaches, failures or service interruptions of our or our business partners’ systems could harm our business and/or reputation;

•We may be unable to maintain third-party software licenses or errors in their software;

Legal and regulatory risks:

•We are subject to extensive regulation;

•Regulators may challenge our use of fronting arrangements in states in which our Program Partners are not licensed.

•Regulation may become more extensive in the future;

•Increasing regulatory focus on privacy issues and expanding laws may impair our operations;

•Our ability to receive dividends and permitted payments from our subsidiaries is subject to regulatory constraints;

•We may have exposure to losses from acts of terrorism;

•Assessments and premium surcharges may reduce our profitability;

•Changes in federal, state or foreign tax laws could adversely affect our financial results or market conditions;

•The discontinuance of LIBOR may adversely affect the value of certain investments we hold, assets and liabilities;

Risks related to our Common Stock:

•Our stock price may be volatile or may decline regardless of our operating performance;

•Our principal stockholders are able to exert significant influence over us and our corporate decisions;

•Sales or issuances of a substantial amount of shares of our Common Stock may cause the market price of our Common Stock to decline and make it more difficult for investors to sell;

•We will incur significant increased costs as a result of operating as a public company;

•We currently do not anticipate declaring or paying regular dividends on our Common Stock;

•Provisions in our organizational documents, Delaware corporate law, state insurance laws and certain of our contractual agreements and compensation arrangements may prevent or delay an acquisition of us;

•Our principal stockholders have no obligation to offer us corporate opportunities;

Risks related to our status as an emerging growth company:

•We have elected to take advantage of reduced disclosure requirements and other exemptions;

•We have elected to use the extended transition period for complying with new or revised accounting standards;

General risk factors:

•We are subject to certain general risks, including, but not limited to risks related to changes in our accounting practices and future pronouncements, our inability to maintain effective internal controls, the effects of litigation on our business, and the Court of Chancery of the State of Delaware serving as the exclusive forum for certain disputes, that could limit our stockholders' ability to obtain a favorable judicial forum for disputes with us or our directors, officers or employees.

5

PART I

Item 1. Business

Trean Insurance Group, Inc. ("we" or the "Company") is an established, growth-oriented company providing products and services to the specialty insurance market. Historically, we have focused on specialty casualty markets that we believe are underserved and where our expertise allows us to achieve higher rates, such as niche workers’ compensation markets and small- to mid-sized specialty casualty insurance programs. We underwrite specialty casualty insurance products both through our program partners ("Program Partners") and Owned Managing General Agents ("Owned MGAs"). We also provide our Program Partners with a variety of services including issuing carrier services, claims administration and reinsurance brokerage, from which we generate recurring fee-based revenues.

We believe that a number of differentiating factors have contributed to our ability to achieve results and growth that historically have outperformed the broader insurance industry. We believe our multi-service value proposition represents a competitive advantage in our target markets, drives deep integration with our Program Partners and allows us to generate more diversified revenue streams. We seek to carefully identify and select our Program Partners, ensure we have closely aligned interests, and grow and expand these relationships over time. We believe we have a competitive advantage in claims management for longer-tailed lines, specifically workers’ compensation, where our in-house capabilities and differentiated philosophy enable us to have lower claims costs and to settle claims more quickly than many of our competitors. Our business strategy is supported by robust controls surrounding program design and underwriting, ongoing monitoring and reinsurance and collateral management as evidenced by our "A" (Excellent) financial strength rating, with a stable outlook, by A.M. Best Company ("A.M. Best"), a leading rating agency for the insurance industry. This rating is based on matters of concern to policyholders and is not designed or intended for use by investors in evaluating our securities. Our management team has decades of insurance industry experience across underwriting as well as program administration, reinsurance, claims and distribution.

The Company and its subsidiaries are licensed to write business across 49 states and the District of Columbia. We seek to write business in states through select distribution outlets with the potential for attractive underwriting margins, and focus on markets with higher than average premium growth trends. California, Texas and Michigan are our largest markets, representing approximately 25%, 14% and 7%, respectively, of our gross written premiums for the year ended December 31, 2022.

Pending Merger

As previously disclosed, on December 15, 2022, we entered into an Agreement and Plan of Merger (the “Merger Agreement”), by and among the Company, Treadstone Parent Inc., a Delaware corporation (“Parent”), and Treadstone Merger Sub Inc., a Delaware corporation and a direct, wholly-owned subsidiary of Parent (“Merger Sub”), providing for the acquisition of the Company by affiliates of Altaris Capital Partners, LLC, a Delaware limited liability company (“Altaris”), subject to the terms and conditions set forth in the Merger Agreement. Certain investment funds managed by Altaris control Parent and Merger Sub and affiliates of Altaris owned approximately 47% of our outstanding Common Stock as of December 31, 2022. Accordingly, the Merger is considered a “going-private” transaction under the SEC’s rules.

Pursuant to the terms of the Merger Agreement and subject to the satisfaction or waiver of certain conditions set forth in the Merger Agreement, Merger Sub will be merged with and into the Company (the “Merger”) effective as of the effective time of the Merger (the “Effective Time”). As a result of the Merger, Merger Sub will cease to exist, and the Company will survive as a wholly-owned subsidiary of Parent. Further, following the Merger, our Common Stock will no longer be publicly traded. In addition, our Common Stock will be delisted from Nasdaq and deregistered under the Exchange Act, in each case, in accordance with applicable laws, rules and regulations, and we will no longer file periodic reports with the SEC on account of our Common Stock.

As a result of the Merger, at the Effective Time, subject to any applicable withholding taxes, each share of our Common Stock, issued and outstanding immediately prior to the Effective Time, other than Cancelled Shares (as defined in the Merger Agreement) and Dissenting Shares (as defined in the Merger Agreement), will be converted into the right to receive $6.15 in cash, without interest.

The consummation of the Merger is subject to the satisfaction or waiver of various customary conditions set forth in the Merger Agreement, including, but not limited to: (i) the adoption of the Merger Agreement and approval of the Merger and

6

the other transactions by (x) the holders representing a majority of the aggregate voting power of the outstanding shares of Company Common Stock beneficially owned by the Unaffiliated Stockholders (as defined in the Merger Agreement) entitled to vote thereon as well as (y) the holders representing a majority of the aggregate voting power of the outstanding shares of Company Common Stock entitled to vote thereon; (ii) all required insurance regulatory approvals (or the applicable regulatory authorities’ non-objection to requests for exemptions in respect thereof) shall have been obtained; (iii) the expiration or termination of any applicable waiting period (or any extensions thereof) under the Hart-Scott-Rodino Antitrust Improvements Act of 1976, as amended (the “HSR Act”); (iv) the absence of any restraint or law preventing or prohibiting the consummation of the Merger; (v) the accuracy of Parent’s, Merger Sub’s, and the Company’s representations and warranties (subject to certain materiality qualifiers); (vi) Parent’s, Merger Sub’s, and the Company’s compliance in all material respects with their respective obligations under the Merger Agreement; and (vii) the absence of any Company Material Adverse Effect (as defined in the Merger Agreement) since the date of the Merger Agreement.

Merger-related expenses recognized during the year ended December 31, 2022 were approximately $3,081 and are included in other expenses in the consolidated statements of operations.

See “Part I—Item 1A Risk Factors—Risks Related to the Proposed Merger” for a discussion of certain risks related to the Merger.

History

We were founded in 1996 as a reinsurance broker and MGA that targeted smaller, underserved insurance providers writing niche classes of business, predominantly workers’ compensation, accident and health, and medical professional liability.

In 2003, we purchased Benchmark Insurance Company ("Benchmark"), which was licensed in 41 states and the District of Columbia and provided us with an insurance carrier with a financial strength rating of "A-" from A.M. Best. Beginning in 2007, we successfully repositioned Benchmark as a specialty insurance carrier for select, high-performing small- to mid-sized Program Partners. Benchmark is now licensed in 49 states and has an "A" rating from A.M. Best.

In July 2015, we sold an equity stake of 36.4% to certain entities affiliated with Altaris Capital Partners, LLC, a private equity firm (collectively, the "Altaris Funds"). The Altaris Funds subsequently made additional equity investments and owned approximately 47% of our Common Stock as of December 31, 2022.

We have historically made equity investments in or acquired long-term partners where we believe they can add substantial value to our business. In 2013, we acquired S&C Claims Services, which, prior to the acquisition, had been handling our workers’ compensation claims for over 10 years. In 2017, we acquired American Liberty Insurance Company, Inc. ("ALIC"), a Utah-domiciled insurance company that was a former Program Partner and writes workers’ compensation insurance. ALIC is licensed or eligible to conduct insurance business, and therefore subject to regulation and supervision by insurance regulators, in 38 states and the District of Columbia. In 2018, we acquired ownership interests in two additional Program Partners: (i) a 45% common equity ownership in Compstar Holding Company LLC, the parent company of Compstar Insurance Services, LLC, an MGA underwriting workers’ compensation insurance coverage for California contractors; and (ii) a 100% ownership of Westcap, an MGA underwriting general liability insurance coverages for California contractors. In 2020, we acquired: (i) the remaining equity interest in Compstar Holding Company LLC; and (ii) a 100% ownership interest in 7710 Insurance Company ("7710"), a South Carolina-domiciled insurance company that was a former Program Partner and writes workers' compensation insurance, along with its associated program manager and agency. 7710 is licensed or eligible to conduct insurance business, and therefore subject to regulation and supervision by insurance regulators, in 9 states. In 2021, we acquired Western Integrated Care, LLC ("WIC"), a managed care organization that offers services to workers' compensation insurers to enable employees who are injured on the job to access qualified medical treatment.

On July 20, 2020, we closed the sale of 10,714,286 shares of our Common Stock in our Initial Public Offering ("IPO"), comprised of 7,142,857 shares issued and sold by us and 3,571,429 shares sold by selling stockholders pursuant to a registration statement on Form S-1 (File No. 333-239291), which was declared effective by the SEC on July 15, 2020. On July 22, 2020, we closed the sale of an additional 1,207,142 shares by certain selling stockholders in the IPO pursuant to the exercise of the underwriters’ option to purchase additional shares to cover over-allotments. The IPO terminated upon completion of the sale of the above-referenced shares.

On May 19, 2021, we closed the sale of 5,000,000 shares of our Common Stock, comprised entirely of shares sold by selling stockholders. We did not receive any proceeds from the sale of shares of our Common Stock by the selling stockholders in

7

this offering. As a result of this offering, the Altaris Funds no longer beneficially own more than 50% of our Common Stock, and we are no longer a "controlled company" within the meaning of the Nasdaq listing rules.

Our structure

The chart below displays our corporate structure:

| Trean Insurance Group, Inc. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Compstar Insurance Services LLC | Trean Corporation | Benchmark Holding Company | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Trean Reinsurance Services LLC | Benchmark Administrators LLC | Western Integrated Care LLC | Westcap Insurance Services LLC | Benchmark Insurance Company | American Liberty Insurance Company, Inc. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Benchmark Specialty Insurance Company | 7710 Insurance Company | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Our competitive strengths

We believe that our competitive strengths include:

Expertise and focus in underserved specialty casualty insurance markets. We focus on select markets that we believe are underserved and where we can achieve higher rates, including niche workers’ compensation markets and small- to mid-sized specialty casualty insurance programs. Historically, we have had few competitors in our target markets due to the specialized knowledge, broad licensing and filing authority requirements and complex operational systems necessary to profitably manage these traditionally longer-tailed lines of business. We believe that most other companies of our size and smaller do not possess these capabilities to the degree needed to be competitive with us, while most larger companies that do have the required expertise and capabilities in these areas tend not to participate in our target markets because their business models eschew the type of customized solutions that are needed when working with smaller, more entrepreneurial partners.

Multi-service value proposition for our partners. We believe that our focus on the needs of smaller accounts and the breadth of products and services we offer allow us to better serve the needs of our Program Partners and provide us with greater revenue and profit opportunities. We offer our Program Partners reinsurance brokerage, claims administration, underwriting capacity and, in particular, access to our A.M. Best "A" financial strength rating through issuing carrier services. Our ability to leverage our licenses across multiple products in 49 states and the District of Columbia allows us to provide a national multi-service solution for our Program Partners. Our multi-service offering enables us to develop deep relationships with our Program Partners.

Long-term, carefully selected and aligned relationships with Program Partners. We carefully select the Program Partners we choose to do business with, and design our programs to align risks between parties. We select programs with the intention of building long-term relationships, where our business philosophies align and our Program Partners can grow alongside us. Our management team carefully evaluates potential new programs in conjunction with our underwriting and actuarial departments. We only accept programs that meet our stringent underwriting and actuarial requirements. For the year ended December 31, 2022, we declined approximately 94% of the new opportunities that we evaluated. For every Program Partner we select, we work with them to appropriately align interests and to establish rigorous ongoing reporting and auditing requirements upfront.

8

Differentiated in-house claims management. We believe that proactively managing our claims, while also accurately setting reserves, is a key aspect of keeping our losses low. In our workers’ compensation business, our claims philosophy is to provide an injured employee high-quality medical care as quickly as possible in order to reduce pain, accelerate healing and lead to a faster and more complete recovery.

Once an injured employee has healed, we aim to settle the claim and obtain a full and complete release of the claim at the earliest opportunity. In California, for the claim year ended December 31, 2021, valued as of December 31, 2022, our average medical cost for the workers' compensation market was $10,110 per claim compared to the California workers' compensation industry average of $30,691, as reported by the Workers' Compensation Insurance Rating Bureau ("WCIRB") at September 30, 2022. For the claim year ended December 31, 2022, we closed 41% of our workers' compensation claims in California within twelve months, compared with the industry average of 33%, as reported by the WCIRB for the year ended December 31, 2021. To provide our policyholders these processing results, we currently average 84 open claims per claims adjuster. In comparison, the 2020 Workers’ Compensation Benchmarking Study by Rising Medical Solutions found that 61% of third-party administrators ("TPAs") had over 100 open claims per claims adjuster.

Significant fee-based income. Our business model generates significant fee-based income from multiple sources including issuing carrier services, claims administration and reinsurance brokerage. For the years ended December 31, 2022, 2021 and 2020, our fee-based income accounted for approximately 2.7%, 4.7% and 5.9% of total revenue, respectively. All of our fee-based income accrues outside of our regulated insurance companies, which we believe enhances our organization’s financial flexibility and increases the visibility of our earnings. Within our insurance companies, we cede a significant portion of the risk we originate to our reinsurance partners. These agreements enable us to maintain broader relationships with our Program Partners than our current capital base would otherwise enable. We believe that our strategy has allowed us to scale our business and provides a consistent fee-based income stream to complement our underwriting business, thus providing us with greater revenue opportunities from our Program Partners than we would be able to access in a traditional insurance underwriter model.

Disciplined risk management across our organization. Our disciplined approach to risk management begins with the extensive due diligence performed during our Program Partner selection process and continues throughout the relationship. We have rigorous ongoing controls and reporting requirements, including with respect to underwriting and ongoing Program Partner diligence. Similarly, we maintain rigorous controls over our reinsurance exposures by maintaining stringent collateral requirements to limit our credit exposure. As a result of providing multiple services to our Program Partners, we have numerous touch points and are in regular communication regarding underwriting, claims handling, reinsurance placement and collateral management, which we believe enhances our ability to manage risks to our organization.

Entrepreneurial and highly experienced management team. Our management team is highly experienced with decades of experience in specialty insurance markets. In addition to this significant industry experience, our team has a long history of continuity in our business. Our business has been led by our Executive Chairman of the Board and founder Andrew M. O’Brien, who previously served as our Chief Executive Officer from our inception in 1996 through July 2022. Effective in July 2022, the role of Chief Executive Officer was assumed by Julie A. Baron, who served in previous roles as President and Chief Operating Officer, Treasurer and Chief Financial Officer, and Controller of Benchmark since joining the Company in 2007.

Our strategy

We believe that our approach will allow us to continue to achieve our goals of both growing our business and generating attractive returns. Our strategy involves:

Growing within our existing markets. We focus on lines of business that have large markets, including workers' compensation with $51 billion of premiums and all of our other lines of business written with $338 billion in premiums in the United States in 2021 according to S&P Global. By comparison, we generated $651.3 million, $634.2 million and $484.2 million of gross written premiums for the years ended December 31, 2022, 2021 and 2020, respectively. We select Program Partners operating in our target markets with whom we believe we can partner to grow within these significant markets. In addition, Benchmark Specialty Insurance Company ("BSIC"), which was created in 2021, writes specialty/niche products through separate program partners, which will provide the group with expanded geographic diversification, rate flexibility and new product offerings on a non-admitted basis opening the excess and surplus lines market.

9

Given the size of our markets, we believe that we have ample room to continue to grow our business organically for the foreseeable future. Additionally, as we grow our premiums and capital, we expect to continue to optimize our reinsurance program to drive our risk-adjusted returns.

Selectively adding new Program Partners. We have been selective in choosing our current Program Partners, and will continue to ensure that new Program Partners share our business philosophy and meet our underwriting and returns criteria. We focus on specialty lines and will continue to add programs in these markets. However, we also continue to evaluate potential partnerships in additional lines of business that will leverage our core competencies and provide us with new revenue opportunities.

Opportunistically grow and maintain our Owned MGA business through acquisitions. From time to time, we may have the opportunity to deepen our relationships with our existing Program Partners by acquiring equity interests from their management teams. Since 2013, we have successfully completed nine acquisitions of companies with which we have had prior relationships. Seven of these companies write premiums which represented more than 36% of our gross written premiums for the year ended December 31, 2022.

Strengthen and harness our strong and growing capital base. Despite our relatively modest historical balance sheet, we have grown our premiums through the significant use of reinsurance. As our capital base has grown, new opportunities have emerged for us. Of particular note, in 2019, A.M. Best upgraded our insurance companies from an "A-" to an "A" (Excellent) (Outlook Stable) financial strength rating, which we believe differentiates us in the markets in which we operate. As we continue to grow, we believe that we will have the opportunity to access additional business and to retain more profitable business that we have historically ceded to the reinsurance markets.

Maintaining our focus on long-term profitability and growth. Our competitive advantages, including our focus on underserved markets, have enabled us to grow our gross written premiums to $651.3 million for 2022 at a compound annual growth rate of 24.0% since 2015, while maintaining an average return on equity of approximately 14% and an average adjusted return on equity of approximately 15% for the same time period. As we seek to grow our business, we remain disciplined in targeting classes of business and markets where we believe we can generate attractive returns. Rather than make decisions based on where we are in the market cycle, we focus on selecting high-quality programs, only pursuing opportunities that we expect to meet our pricing and risk requirements over the long-term. We will not participate in markets where we do not believe our business model can add incremental risk-adjusted value.

Maintain disciplined controls over our key business risks. In order to maintain our underwriting profitability, we have systematic underwriting and risk monitoring processes across our business. We believe our risk management is enhanced by the fact that we provide multiple services to many of our Program Partners and thus are in regular communication with them regarding underwriting, claims handling, reinsurance placement and collateral management. We seek to swiftly identify, correct and, if necessary, terminate relationships with Program Partners that are not producing targeted underwriting results, writing exposures outside of agreed upon risk tolerances or not meeting their collateral or other commitments to us.

Products and services

We have historically provided products and services to our target markets in the specialty casualty insurance market. We underwrite specialty casualty insurance products both through our Program Partners, programs where we partner with other organizations, and our Owned MGAs. Our insurance product offerings include workers’ compensation, other liability, accident and health, and other lines of business. We also provide our Program Partners with a variety of services from which we generate recurring fee-based revenues, including reinsurance brokerage and, in particular, issuing carrier or "fronting" services.

Owned MGA's and Program Partner Premiums:

The following table shows the total premiums earned on a gross and net basis for Owned MGAs and Program Partners:

10

| The Year Ended December 31, 2022 | The Year Ended December 31, 2021 | ||||||||||||||||||||||||||||||||||

| Owned MGAs | Program Partner | Total | Owned MGAs | Program Partner | Total | ||||||||||||||||||||||||||||||

| Gross written premiums | $ | 239,319 | $ | 411,984 | $ | 651,303 | $ | 268,943 | $ | 365,221 | $ | 634,164 | |||||||||||||||||||||||

| Decrease (Increase) in gross unearned premiums | 9,881 | (18,955) | (9,074) | (25) | (61,886) | (61,911) | |||||||||||||||||||||||||||||

| Gross earned premiums | 249,200 | 393,029 | 642,229 | 268,918 | 303,335 | 572,253 | |||||||||||||||||||||||||||||

| Ceded earned premiums | (79,974) | (277,631) | (357,605) | (144,375) | (229,198) | (373,573) | |||||||||||||||||||||||||||||

| Net earned premiums | $ | 169,226 | $ | 115,398 | $ | 284,624 | $ | 124,543 | $ | 74,137 | $ | 198,680 | |||||||||||||||||||||||

| Direct commissions | 25,002 | 89,864 | 114,866 | 32,351 | 73,614 | 105,965 | |||||||||||||||||||||||||||||

| Ceding commission | (24,265) | (78,494) | (102,759) | (44,168) | (76,520) | (120,688) | |||||||||||||||||||||||||||||

| Net commissions | $ | 737 | $ | 11,370 | $ | 12,107 | $ | (11,817) | $ | (2,906) | $ | (14,723) | |||||||||||||||||||||||

Direct commissions rate(1) | 10.0 | % | 22.9 | % | 17.9 | % | 12.0 | % | 24.3 | % | 18.5 | % | |||||||||||||||||||||||

Ceding commissions rate(2) | 30.3 | % | 28.3 | % | 28.7 | % | 30.6 | % | 33.4 | % | 32.3 | % | |||||||||||||||||||||||

(1) Direct commissions as a percentage of gross earned premiums. | |||||||||||||||||||||||||||||||||||

(2) Ceding commissions as a percentage of ceded earned premiums. | |||||||||||||||||||||||||||||||||||

We utilize both quota share and catastrophe XOL contracts in our reinsurance strategy for our Owned MGAs and Program Partners. Direct commissions for Program Partners include third-party agent commissions and MGA service fees, while Owned MGAs direct commissions includes only third-party agent commissions and the expenses associated with MGA services are included in general and administrative operating expenses. The ceding commission rates vary based on a number of factors including: the line of business, negotiated reinsurance terms, and program cost structures. For the year ended December 31, 2022, the Company retained 67.9% and 29.4% of gross earned premiums for Owned MGAs and Program Partners, respectively. The loss ratios for Owned MGAs and Program Partners for the year ended December 31, 2022 were 79.2% and 60.5%, respectively, resulting in a consolidated loss ratio of 71.6%. For the year ended December 31, 2021, the Company retained 46.3% and 24.4% of gross earned premiums for Owned MGAs and Program Partners, respectively. The loss ratios for Owned MGAs and Program Partners for the year ended December 31, 2021 were 67.6% and 62.9%, respectively, resulting in a consolidated loss ratio of 65.8%.

The following table shows our gross written premiums by insurance product for the years ended December 31, 2022, 2021 and 2020, in thousands.

| Year Ended December 31, | |||||||||||||||||

| 2022 | 2021 | 2020 | |||||||||||||||

| Workers' compensation | $ | 368,408 | $ | 376,819 | $ | 368,949 | |||||||||||

| Commercial auto liability | 62,849 | 53,959 | 25,301 | ||||||||||||||

| Group accident and health | 54,184 | 32,565 | 2,375 | ||||||||||||||

| Other liability - occurrence | 51,334 | 72,306 | 25,531 | ||||||||||||||

| Commercial multiple peril | 49,987 | 37,496 | 24,930 | ||||||||||||||

| Homeowners multiple peril | 32,424 | 38,023 | 17,356 | ||||||||||||||

| Auto physical damage | 19,268 | 13,746 | 7,340 | ||||||||||||||

| Excess workers' compensation | 7,654 | 5,587 | 3,986 | ||||||||||||||

| Inland marine | 3,132 | 1,157 | 25 | ||||||||||||||

| Boiler and machinery | 1,816 | 1,782 | 1,253 | ||||||||||||||

| Fire | 212 | 201 | 129 | ||||||||||||||

| Surety | 35 | 36 | 41 | ||||||||||||||

| Products liability - occurrence | — | 487 | 7,033 | ||||||||||||||

| Total | $ | 651,303 | $ | 634,164 | $ | 484,249 | |||||||||||

11

In total, we are licensed in 49 states and the District of Columbia. The following table shows our gross written premiums by state for the years ended December 31, 2022, 2021 and 2020, in thousands.

| Year Ended December 31, | |||||||||||||||||

| 2022 | 2021 | 2020 | |||||||||||||||

| California | $ | 162,639 | $ | 179,426 | $ | 203,421 | |||||||||||

| Texas | 93,165 | 85,154 | 28,909 | ||||||||||||||

| Michigan | 45,821 | 46,271 | 41,830 | ||||||||||||||

| Tennessee | 16,006 | 15,966 | 12,347 | ||||||||||||||

| Florida | 36,559 | 27,982 | 8,359 | ||||||||||||||

| Georgia | 30,996 | 25,619 | 12,869 | ||||||||||||||

| Arizona | 28,685 | 26,272 | 27,950 | ||||||||||||||

| Alabama | 23,198 | 20,991 | 17,549 | ||||||||||||||

| Pennsylvania | 17,167 | 20,375 | 10,498 | ||||||||||||||

| Indiana | 13,943 | 13,422 | 8,508 | ||||||||||||||

| Other geographical areas | 183,124 | 172,686 | 112,009 | ||||||||||||||

| Total | $ | 651,303 | $ | 634,164 | $ | 484,249 | |||||||||||

Workers’ compensation

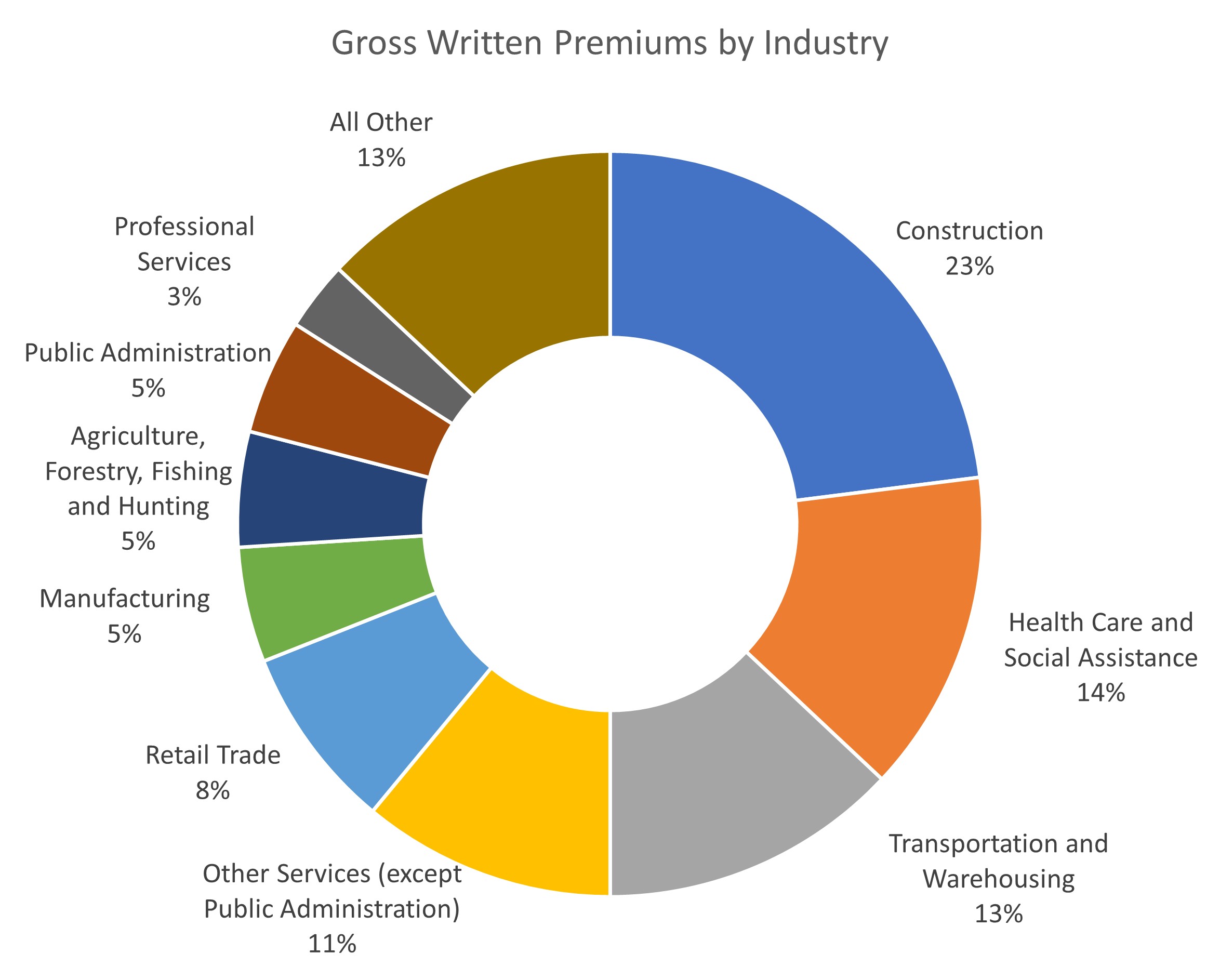

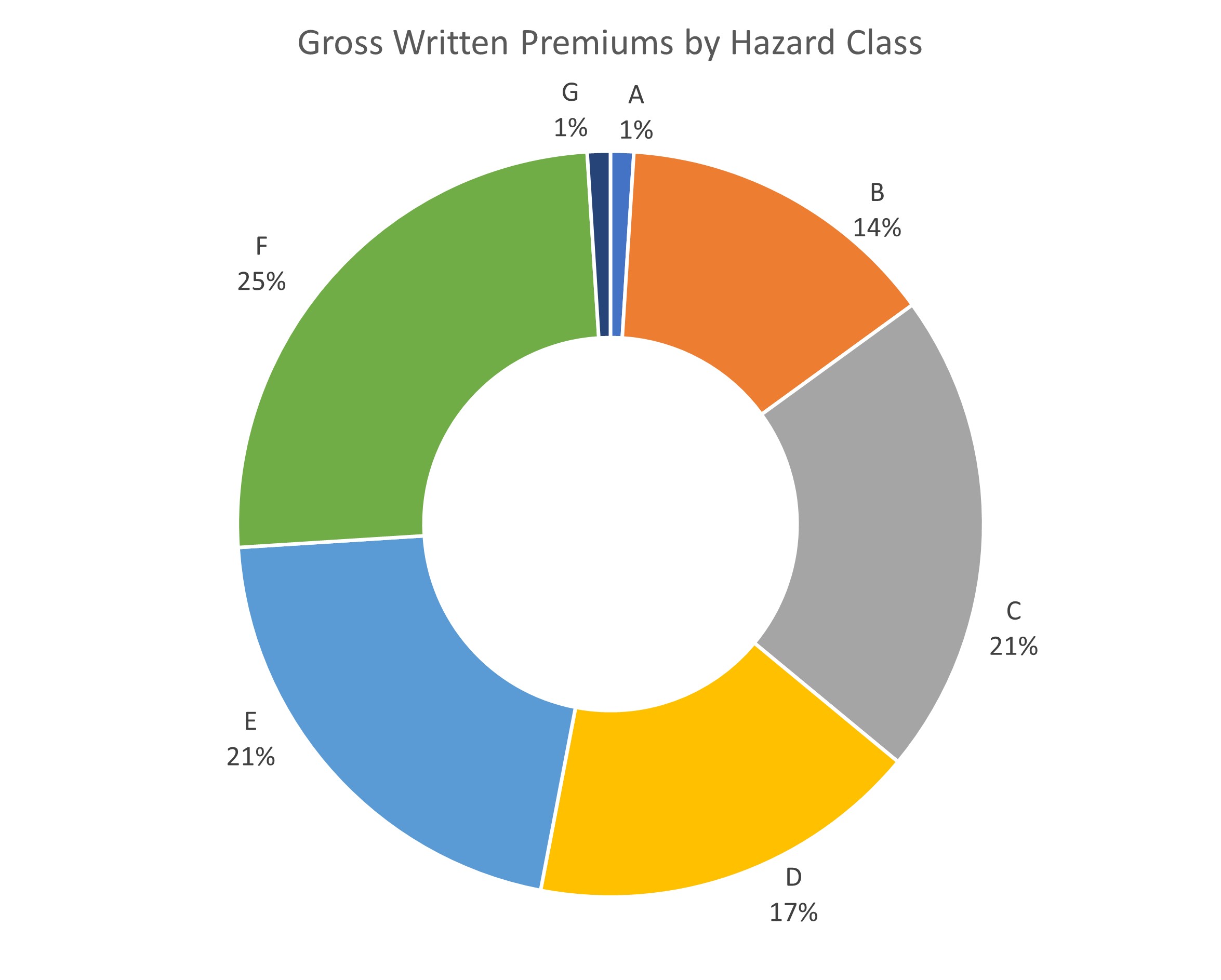

We offer workers’ compensation insurance through both our Owned MGAs and our Program Partners. California, Florida and Arizona represented 35.5%, 7.5% and 7.0%, respectively, of our workers’ compensation gross written premiums for the year ended December 31, 2022 and 41.5%, 5.3% and 6.3%, respectively, for the year ended December 31, 2021. We write business across a variety of industries and hazard classes. The construction industry is our largest industry exposure, representing 23% of premiums written for the year ended December 31, 2022. The workers’ compensation insurance industry classifies risks into hazard groups defined by the National Council on Compensation Insurance, or NCCI, and based on severity, with employers in lower groups having lower cost claims. Our premiums are spread across hazard classes. We target accounts that we believe offer greater risk-adjusted returns, such as small accounts that are less subject to competition, or accounts with high experience modification factors that our underwriters assess to be attractively priced for the potential risk. Experience modification factors are determined by state insurance regulators based on the insured’s historical loss experience.

We do not write accounts that we believe present exposure to catastrophic risk. The average workers’ compensation premium per policy written by us was $15,539 and $14,779 for the years ended December 31, 2022 and 2021, respectively.

We manage workers’ compensation claims administration for all of our Owned MGAs and for several of our Program Partners. We believe that our claims philosophy has been a key differentiating factor allowing us to maintain lower loss ratios and settle claims quickly. Our workers’ compensation programs are supported by various quota share and excess of loss reinsurance facilities, which we utilize to align risk with our Program Partners and optimize our net retention relative to our financial objectives, balance sheet size and ratings requirements. We ceded 39.8% and 57.6% of gross workers’ compensation premiums earned to third-party insurers for the year ended December 31, 2022 and 2021, respectively.

The following exhibits illustrate our business mix of workers’ compensation gross written premiums by industry and hazard class for the year ended December 31, 2022.

12

Other liability

We offer other liability insurance products through both our Owned MGAs and our Program Partners. We target segments of the market that we believe are underserved or mispriced, such as California contractors with an average of five employees.

The other liability products that we offer through our Owned MGAs include admitted general liability and construction defect products offered to small contractors that protect them against claims from third parties. We distribute these products through select wholesale brokers in California. Additionally, through several of our Program Partners, we write 11 other liability insurance products in 49 states and the District of Columbia. Our claims personnel administer claims for our Owned MGA other liability products. We ceded approximately 76.9% and 79.1% of our gross other liability premiums earned to third-party insurers for the years ended December 31, 2022 and 2021, respectively.

Issuing carrier services

We provide issuing carrier services to several of our Program Partners who offer workers' compensation, commercial multi-peril, personal auto and commercial auto and other liability insurance. In these relationships, we act as the policy-issuing insurance carrier for our Program Partner and transfer all or a substantial portion of the underwriting risk to third-party reinsurers. When we enter into issuing carrier relationships, we typically receive reinsurance ceding commissions at rates that include our fronting service from our reinsurers who are both Program Partners and/or third-party reinsurers. Reinsurance ceding commissions vary based on the line of business and premium volume. We provide issuing carrier services across each of our insurance products. For the year ended December 31, 2022, 2021 and 2020, reinsurance ceding commissions from issuing carrier services were $77.6 million, $86.9 million and $71.8 million, respectively, and are recognized as a reduction of direct insurance commission expense within 'General and administrative expenses' in the consolidated statement of operations.

Reinsurance brokerage services

Our reinsurance brokerage services division provides reinsurance placement, servicing and renewal services to small- to mid-sized insurance organizations, including most of our Program Partners and additional third-party insurance organizations. We earn commissions for structuring and placing reinsurance coverage on behalf of our clients. Commissions are based on a percentage of premiums ceded to reinsurers and vary by type or complexity of reinsurance coverage. Our reinsurance brokerage services are a valuable risk management tool in our relationships with our Program Partners, as we typically require the use of our reinsurance brokerage services to place and structure reinsurance prior to the inception of a new program. For the years ended December 31, 2022, 2021 and 2020, reinsurance brokerage generated $5.7 million, $7.0 million and $9.0 million in revenue, which is included in Other revenue.

Other services

We provide a variety of other services to insurance organizations, including claims administration and insurance management services. We provide workers’ compensation insurance claims administration services to some of our Program Partners as well as to third-party insurance organizations with which we do not have additional relationships.

13

Inland marine

Inland marine underwrites coverage for property that may be held in transit or instrumentalities of transportation and communication, such as builders risk, contractors equipment, transportation risk and mobile equipment.

Marketing and distribution

We market and distribute our products through several channels. Our Owned MGAs market through both retail agents and wholesale brokers, and our reinsurance brokerage services division actively markets our services directly to prospective clients. Additionally, we distribute products and services to our Program Partners, which comprise program administrators and insurance carriers. Since we focus on smaller accounts, we do not market our products and services through large insurance brokers. For the year ended December 31, 2022, our Owned MGAs represented 37% of our gross written premiums, Program Partners represented 62% of gross written premiums and national insurance pools represented 1% of gross written premiums. For the year ended December 31, 2021, our Owned MGAs represented 42% of our gross written premiums, Program Partners represented 57% of gross written premiums and national insurance pools represented 1% of gross written premiums. For the year ended December 31, 2020, our Owned MGA's represented 59% of our gross written premiums, Program Partners represented 40% of gross written premiums and national insurance pools represented 1% of gross written premiums.

Retail agents

We distribute our Owned MGA workers’ compensation products through approximately 300 retail agents. We target retail agents with experience and distribution capabilities in our target markets. Retail agents must demonstrate an ability to produce both our desired quality and quantity of business. To assist with this goal, our underwriters regularly visit our retail brokers to market and discuss the products we offer. We terminate retail agents who are unable to produce consistently profitable business or who produce unacceptably low volumes of business.

Wholesale brokers

We distribute our other liability products underwritten by our Owned MGAs through wholesale brokers that have expertise and strong track records in our niche target markets. For these products, we target small contractors in California. We use wholesale brokers to distribute these products because wholesale brokers are an important channel for commercial insurance products where they control much of the premium in these segments. We select our wholesale brokers based on our management’s review of their experience, knowledge, business plan, and track record of delivering us profitable business.

Reinsurance brokerage services

Our reinsurance brokerage services division actively markets our reinsurance services to small- and mid- sized program administrators and other insurance organizations. The primary focus of our reinsurance brokerage services division is to place reinsurance for our program partners, direct business and third parties. We are also able to leverage our reinsurance brokerage relationships to cultivate new Program Partner relationships and market our other services. The majority of our current Program Partner relationships originated as an introduction from our reinsurance brokerage services division.

Program administrators

We partner with select program administrators across each of our target markets to harness the efficiency and scale of these organizations’ marketing and distribution infrastructures. Through these relationships, we are able to access national distribution channels or write specialized risks in our target markets efficiently. Generally, policies bound by our program administrators are underwritten according to strict underwriting guidelines that we establish with each program administrator. We have long relationships with many of our program administrators and, in most cases, we have had an existing relationship with a program administrator before adding it as a new Program Partner. For example, we may have previously provided the program with reinsurance placement or consulting services, or worked with the key principals of the prospective Program Partner at their prior organization. We believe program administrators value our multi-service offering and capabilities and the flexibility with which we can offer these services. In addition to underwriting insurance products through program administrators, we provide these organizations with issuing carrier services and reinsurance brokerage services.

Carrier and other partnerships

Given our unique focus on flexible multi-service offerings, we are a partner of choice for small- to mid-sized insurance carriers seeking a specialty casualty insurance partner to satisfy insurance department requirements, provide comprehensive management solutions or transfer certain classes of risk. We have partnerships with insurance companies, risk retention groups, trusts and state insurance pools.

14

Program selection, underwriting and controls

Program selection

Given our position and reputation in the market, we are presented with more new program opportunities than we choose to write, allowing us to be highly selective with respect to the Program Partners with whom we choose to partner. We decline approximately 94% of the new opportunities we are presented with prior to or through our pre-screening process. We typically source new opportunities through our reinsurance brokerage services business or through referrals from existing Program Partners. For each new opportunity that we choose to evaluate, we conduct a comprehensive pre-screening of the company, including an evaluation of its philosophy, size, past performance, future performance targets and above all, compatibility with our operating model, risk appetite and existing book of business. Our target Program Partners tend to have several, if not all, of the following traits:

•small- to mid-sized books of business (less than $30 million of annual gross premiums at the inception of the relationship);

•presence in markets where we believe we can leverage our distinctive expertise, multi-service offering and market relationships to create a competitive advantage;

•track record of underwriting success supported with credible data;

•proven ability to administer the program pursuant to agreed-upon underwriting and claims guidelines;

•ability and willingness to assume a meaningful quota share risk participation in the program, typically through ownership of an insurance company or captive;

•collaborative, entrepreneurial management team; and

•willingness and ability for us to control the structuring and placement of reinsurance.

Underwriting and program design

For opportunities that are acceptable to us through the pre-screening process, we conduct rigorous underwriting due diligence prior to entering into a partnership. As part of this process, our due diligence team collects and analyzes data relating to the organization’s operating, underwriting, financial and biographical information to prepare an initial due diligence file for our Underwriting Committee. Our Underwriting Committee is led by our CEO and consists of members with expertise in underwriting and finance. In 2022, 7 out of 118 submissions were approved by the Underwriting Committee. If the Underwriting Committee approves the submission on a provisional basis, we then conduct comprehensive underwriting, claims and financial diligence on the potential Program Partner. This includes inviting the potential Program Partner’s management for an on-site meeting at our Wayzata headquarters and on-site diligence of the potential Program Partner.

If we look to enter into a contractual relationship with a potential Program Partner, we work with them to design a program that appropriately aligns interests and establish rigorous underwriting guidelines and ongoing reporting and auditing requirements. At the inception of a new program, we typically act as an issuing carrier where we reinsure a substantial amount of risk to third parties. We also typically require the Program Partner to maintain significant underwriting risk or otherwise align incentives with the Program Partner’s underwriting performance. The amount of risk and premiums ceded to Program Partners is contractually stipulated with each Program Partner. Over time we look to optimize our net retention positions with our Program Partners once we have become comfortable with their performance through our ongoing interactions.

Ongoing monitoring and controls

Throughout the lifetime of a relationship with a Program Partner, we maintain systematic monitoring and control mechanisms to ensure each relationship meets our financial objectives. We closely monitor each Program Partner’s adherence to the agreed upon underwriting and claims guidelines and conduct regular reviews of loss experience, rate levels, reserves and the overall financial health of the Program Partner. We receive underwriting and claims data feeds from each Program Partner at least monthly. We typically conduct two underwriting, claims and accounting audits per program per year. Because we typically provide multiple services to our Program Partners, we are in regular communication with them regarding underwriting, claims handling, reinsurance placement and collateral management. As a result, we have near continuous opportunities to interact with our Program Partners and evaluate their performance.

We maintain the right to terminate relationships with our Program Partners. Reasons for us to terminate a relationship include an inability to produce targeted underwriting results, writing exposures outside of agreed upon risk tolerances, delinquency in

15

meeting reporting requirements, a change of strategic direction, or failure to meet collateral or other commitments to us. Our stringent and extensive due diligence and selection process allows us the flexibility to partner with organizations with which we believe we will have successful relationships.

Claims

We actively manage claims for our Owned MGA businesses, as well as for select Program Partners that underwrite workers’ compensation insurance. Other lines of business are typically managed directly by our Program Partners, or in some cases by TPAs. When our Program Partners or TPAs administer claims, our claims personnel are responsible for overseeing the Program Partner or TPA, including the management of loss reserves, settlement, arbitration and mediation. Claims are reported directly to the applicable Program Partner or TPA, which adheres to agreed-upon service level standards.

For business where we manage the claims, our experienced claims team actively manages the claims. In our largest line of business, workers’ compensation, our philosophy is to provide an injured employee with high-quality medical care as quickly as possible to reduce pain, expedite healing and lead to a faster and more complete recovery. Once an injured employee has healed, we aim to fully settle and achieve a full and complete release of the claim at the earliest opportunity. This approach to claims management enables us to lower our claim costs and settle the ultimate claim reserves more quickly. In order to achieve these outcomes, we manage our claims organization to ensure that each of our claims personnel is responsible for lower than industry average claims files per claims adjuster.

Our claims adjusters have settlement authority that varies by the line of business and the experience of each adjuster. In the case of a catastrophic claim, we may use a third-party administrator that specializes in these types of claims to ease the burden of catastrophic claims on our organization. In addition, our claims examiners work closely with our underwriting staff to keep apprised of claims trends. Vendor management is also an important component of effective claims management and our claims examiners work closely with our vendors to manage expenses and costs.

Reinsurance

We cede a portion of the risk we accept on our balance sheet to third-party reinsurers through a variety of reinsurance arrangements. We manage these arrangements to align risks with our Program Partners, optimize our net retention relative to our financial objectives, balance sheet size and ratings requirements, as well as to limit our maximum loss resulting from a single program or a single event. We utilize both quota share and excess of loss ("XOL") reinsurance as tools in our overall risk management strategy to achieve these goals, usually in conjunction with each other. Quota share reinsurance involves the proportional sharing of premiums and losses of each defined program. We utilize quota share reinsurance for several purposes, including (i) to cede risk to Program Partners, which allows us to share economics and align incentives and (ii) to cede risk to third-party reinsurers in order to manage our net written premiums appropriately based on our financial objectives, capital base, A.M. Best financial strength rating and risk appetite. It is a core pillar of our underwriting philosophy that Program Partners retain a portion of the underwriting risk of their program. We believe this best aligns interests, attracts higher quality programs and leads to better underwriting results. Under XOL reinsurance, losses in excess of a retention level are paid by the reinsurer, subject to a limit, and are customized per program or across multiple programs. We utilize XOL reinsurance to protect against catastrophic or other unforeseen extreme loss activity that could otherwise negatively impact our profitability and capital base. The majority of our exposure to catastrophic risk stems from the workers' compensation premium we retain. Potential catastrophic events include an earthquake, terrorism or another event. We believe we mitigate risk by our focus on small-to mid-sized accounts, which means that we generally do not have concentrated employee counts at a single location that could be exposed to a catastrophic loss. The cost and limits of the reinsurance coverage we purchase vary from year to year based on the availability of quality reinsurance at an acceptable price and our desired level of retention.

Our workers' compensation XOL reinsurance structure consolidates multiple programs under a single XOL reinsurance program comprised of two excess of loss reinsurance agreements with five professional reinsurers. We believe this structure significantly decreases our cost of reinsurance compared with each program maintaining its own XOL reinsurance program. As of December 31, 2022, we had $2 million retention of which is reinsured under various quota share reinsurance agreements at a weighted average rate of 21%, based on 2022 premiums for the applicable programs. These agreements apply to programs that accounted for 87% of workers' compensation premiums for the year ended December 31, 2022. We have the following XOL coverage:

16

•0% of $8 million of losses in excess of $2 million as of December 31, 2022. Gross written premiums for the applicable programs for this layer accounted for 74% of workers' compensation premiums for the year ended December 31, 2022.

•100% of $5 million of losses in excess of $10 million. Gross written premiums for the applicable programs for this layer accounted for 74% of workers' compensation premiums for the year ended December 31, 2022.

•100% of $35 million of losses in excess of $15 million. Gross written premiums for the applicable programs for this layer accounted for 87% of workers' compensation premiums for the year ended December 31, 2022.

Summary workers' compensation reinsurance program

| $50,000,000 | ||||||||||||||||||||

| 7/1/2022 Excess of Loss Reinsurance $35M xs $15M Per Occurrence Risks Attaching | ||||||||||||||||||||

| $15,000,000 | ||||||||||||||||||||

| 7/1/2022 Excess of Loss Reinsurance $5M xs $10M Per Occurrence Risks Attaching | ||||||||||||||||||||

| $10,000,000 | ||||||||||||||||||||

$8M xs $2M Retention: 100% | ||||||||||||||||||||

| $2,000,000 | ||||||||||||||||||||

| Quota Share Reinsurance First $2M Per Occurrence Risks Attaching | Quota Share Reinsurance First $2M Per Occurrence Risks Attaching - Retention: 79%1 | |||||||||||||||||||

| $0 | ||||||||||||||||||||

1 Quota share retention rate reflects a weighted rate based on 2022 gross written premiums for multiple contracts across multiple programs.

Collateral management

As a result of our extensive use of reinsurance in our business model, we effectively convert underwriting risk to credit risk of our Program Partners and other professional reinsurers. Accordingly, it is critical for the success of our business that we actively manage our credit exposures. We achieve this through active collateral management, including: (i) requiring our reinsurance partners who do not have an A.M. Best financial strength rating of "A-" or higher or who are not authorized

17

reinsurers to post collateral equal to at least 100% of reserves for unearned premiums and losses and loss adjustment expense, including incurred but not yet reported ("IBNR") reserves, based on our assessment of expected losses; (ii) securing collateral by trust funds, letters of credit or, more frequently, funds withheld accounts; and (iii) reviewing collateral accounts on a monthly basis and secured with quarterly and annual "true-ups."

As of December 31, 2022, we had reinsurance recoverables on paid and unpaid losses of $408.5 million. Against these recoverables, we maintained $241.3 million of funds withheld and $155.4 million of other forms of collateral, for a total of approximately $396.7 million in credit protection from our reinsurers. As of December 31, 2022, we did not have any balance from reinsurers that was over 90 days old or in dispute, and we held appropriate funding or collateral from all unauthorized reinsurers.

The following table sets forth our ten largest reinsurance recoverables by reinsurer as of December 31, 2022, in thousands:

| Reinsurers: | A.M. Best Rating | Reinsurance Recoverables | Collateral | Net Recoverables | ||||||||||||||||||||||

| Markel Global | A | $ | 68,619 | $ | 10,220 | $ | 58,399 | |||||||||||||||||||

| Greenlight | A- | 49,666 | 85,161 | (35,495) | ||||||||||||||||||||||

| Employers National Insurance Company | NR | 37,471 | 40,811 | (3,340) | ||||||||||||||||||||||

| First Insurance Company of OK (FICO) | NR | 22,828 | 22,855 | (27) | ||||||||||||||||||||||

| Bluefin Risk Partners, Inc. | NR | 20,317 | 38,724 | (18,407) | ||||||||||||||||||||||

| VGM Insurance Companies of America Limited | NR | 17,872 | 31,749 | (13,877) | ||||||||||||||||||||||

| Arch Reinsurance Company (U.S.) | A+ | 17,434 | 3,138 | 14,296 | ||||||||||||||||||||||

| Munich Reinsurance America, Inc | A+ | 17,255 | — | 17,255 | ||||||||||||||||||||||

| Swiss Reinsurance America Corp | A+ | 17,199 | — | 17,199 | ||||||||||||||||||||||

| Provistar Insurance Company, Limited | NR | 16,730 | 25,721 | (8,991) | ||||||||||||||||||||||

| Total | 285,391 | 258,379 | 27,012 | |||||||||||||||||||||||

| All other reinsurers | 123,131 | 138,294 | (15,163) | |||||||||||||||||||||||

| Total recoverables | $ | 408,522 | $ | 396,673 | $ | 11,849 | ||||||||||||||||||||

Technology

We operate on a digital platform with a data warehouse that collects and builds a robust repository of statistical data for our workers’ compensation business and a substantial amount of our other liability business. All of our workers’ compensation business data is automated through the data warehouse. Our platform provides a high degree of efficiency, accuracy and speed across all of our processes. We are able to use the data that we collect through Application Programming Interfaces ("APIs") to quickly analyze trends across all functions in our business. The data warehouse is easily searchable and contains most of the underwriting and claims information we collect at every level. We are able to track rates, monitor historical loss experience and reserve development and measure other relevant metrics at a granular level of detail. Our technology team is continuously enhancing this system to improve its capability and expand its use across our business. We believe our systems and technology allow us to quickly collect and analyze data, thereby improving our ability to manage our business. We have scalable, standardized infrastructure technology systems built for automation, efficiency and security, and are not burdened by legacy technology systems.

Reserves

We record reserves for estimated losses of the policies that we underwrite and for loss adjustment expenses ("LAE") related to the investigation and settlement of policy claims. Our reserves for losses and LAE represent the estimated cost of all reported and unreported losses and loss adjustment expenses incurred and unpaid as of a given point in time. We evaluate the overall adequacy of gross, ceded and net losses and LAE reserves in accordance with established actuarial standards to set our reserves. We establish reserves on a line of business basis at the individual program level. Consistent with our gross and net premium breakdown, reserves for workers’ compensation losses comprise the majority of our carried reserve position.

18

Due to our shorter claims process and ability to close claims faster than competitors, we believe we are able to settle our ultimate reserves more quickly as well.

When a claim is first reported, we establish an initial case reserve for the estimated amount of our loss based on our estimate of the most likely outcome of the claim at that time. Generally, a case reserve is established within 30 days after the claim is reported and consists of anticipated medical costs, indemnity costs and specific adjustment expenses. This case reserve is set to cover the life of the claim based on information available at that point in time. At any point in time, the amount paid on a claim, as well as the reserve for future amounts to be paid, represents the estimated total cost of the claim or the case incurred amount. The estimated amount of loss for a reported claim is based on various factors, including:

•type of loss;

•severity of the injury or damage;

•age and occupation of the injured employee;

•estimated length of temporary disability;

•anticipated permanent disability;

•expected medical procedures, costs and duration;

•our knowledge of the circumstances surrounding the claim;

•insurance policy provisions, including coverage, related to the claim;

•jurisdiction of the occurrence; and

•other benefits defined by applicable statute.

Reserves are estimates involving actuarial projections of the expected ultimate cost to settle and administer claims at a given time but are not expected to precisely represent the ultimate liability. Estimates are based on past loss experience modified for current trends as well as prevailing economic, legal and social conditions. Such estimates are also based on facts and circumstances then known but are subject to significant uncertainty based on the outcome of various factors, such as future events, future trends in claim severity, inflation and changes in the judicial interpretation of policy provisions relating to the determination of coverage.

Reserves are set by our Reserve Committee in consultation with an independent third-party actuarial firm. Our Reserve Committee includes our Chief Executive Officer and President, Chief Financial Officer, Chief Actuary Officer, Senior Vice President of Underwriting, Corporate Controller and Insurance Divisional Controller. The Reserve Committee meets quarterly to review the actuarial reserving recommendations made by the independent actuary. Our independent third-party actuarial firm reviews our net reserves at March 31, June 30 and September 30 of each year and performs a comprehensive review of all programs at each year-end.

As of December 31, 2022 we have had aggregate favorable development of $37.6 million on our reserve estimates since 2015, respectively.

19

| Incurred Claims and Allocated Claim Adjustment Expenses, Net of Reinsurance | As of December 31, 2022 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Years Ended December 31, | Total of IBNR Liabilities Plus Expected Development on Reported Claims | Cumulative Number of Reported Claims | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Accident Year | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2013 | $ | 24,661 | $ | 24,755 | $ | 24,280 | $ | 21,361 | $ | 21,342 | $ | 21,506 | $ | 21,465 | $ | 21,631 | $ | 21,671 | $ | 21,842 | $ | 1,374 | 4,444 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| 2014 | 24,580 | 22,777 | 21,726 | 21,571 | 21,095 | 21,054 | 20,897 | 20,183 | 20,154 | 1,913 | 5,021 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2015 | 25,757 | 26,614 | 26,414 | 25,450 | 25,650 | 22,518 | 22,516 | 22,130 | 2,372 | 6,398 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2016 | 35,281 | 33,672 | 32,554 | 30,165 | 27,340 | 26,550 | 25,858 | 2,880 | 11,427 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2017 | 43,499 | 35,113 | 32,685 | 30,847 | 29,783 | 29,766 | 2,940 | 16,963 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2018 | 47,263 | 41,630 | 39,880 | 38,108 | 37,923 | 4,528 | 14,704 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2019 | 57,778 | 51,598 | 51,824 | 51,211 | 6,724 | 13,008 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2020 | 63,734 | 64,362 | 66,963 | 10,991 | 13,498 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2021 | 127,981 | 132,816 | 27,493 | 14,829 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2022 | 181,164 | 66,546 | 12,597 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| $ | 589,827 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Cumulative Paid Claims and Allocated Claim Adjustment Expenses, Net of Reinsurance | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Years Ended December 31, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||