UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

(Mark One)

For the fiscal year ended

or

For the transition period from ______ to ______

Commission file number

(Exact name of registrant as specified in its charter)

| Not Applicable | ||

|

(State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

|

|

||

|

(Address of principal executive offices) |

(Zip Code) |

| (Registrant’s telephone number, including area code) |

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

| The |

Securities registered pursuant to section 12(g) of the Act: NONE

Ordinary share, $0.001 par value

(Title of class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

☐ Yes ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

☐ Yes ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

☒

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| ☒ | Smaller reporting company | ||

| Emerging growth company | |||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). ☐ Yes ☒

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the Registrant, based on the closing price of $10.22 for shares of the Registrant’s ordinary share on the Nasdaq Capital Market on June 30, 2022, the last business day of its most recently completed second fiscal quarter, was $

As of the date of this report, the Company had shares of ordinary share issued and outstanding.

TABLE OF CONTENTS

i

FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, or the Securities Act, and Section 21E of the Securities Exchange Act of 1934, as amended, or the Exchange Act. Such forward-looking statements reflect, among other things, our business plans and strategy, market trends, beliefs regarding our competitive strengths, current expectations, future capital expenditures, and anticipated results of operations, all of which are subject to known and unknown risks, uncertainties and other factors that may cause our actual results, performance or achievements, market trends, or industry results to differ materially from those expressed or implied by such forward-looking statements. Therefore, any statements contained herein that are not statements of historical fact may be forward-looking statements and should be evaluated as such, including statements regarding future financial and operational results, our business strategy, the future impact of macroeconomic trends, such as inflation and increased interest rates, and the ongoing COVID-19 pandemic on our business, financial results, and financial condition, benefits of acquisitions, and planned capital expenditures. Without limiting the foregoing, the words “anticipates,” “believes,” “can,” “continue,” “could,” “estimates,” “expects,” “intends,” “may,” “might,” “plans,” “projects,” “should,” “would,” “targets,” “will” and the negative thereof and similar words and expressions are intended to identify forward-looking statements. These forward-looking statements are subject to a number of risks, uncertainties and assumptions, including those described in Part I, Item 1A, “Risk Factors” in this Annual Report on Form 10-K. Unless legally required, we assume no obligation to update any such forward-looking information to reflect actual results or changes in the factors affecting such forward-looking information.

As used in this report, the terms “MicroAlgo Inc.,” “Company,” “we,” “us,” and “our” mean MicroAlgo Inc. and its subsidiaries unless the context indicates otherwise.

Summary of Principal Risk Factors

Our business operations are subject to numerous risks and uncertainties, including the risks described in the section titled “Risk Factors” included under Part I, Item 1A of this Annual Report, which could cause our business, financial condition or operating results to be harmed, including risks regarding the following:

| ● | expectations regarding our strategies and future financial performance, including our future business plans or objectives, prospective performance and opportunities and competitors, revenues, customer acquisition and retention, products and services, pricing, marketing plans, operating expenses, market trends, liquidity, cash flows and uses of cash, capital expenditures, and our ability to invest in growth initiatives and pursue acquisition opportunities; |

| ● | the ability to list our securities on the Nasdaq Capital Market; |

| ● | limited liquidity and trading of our securities; |

| ● | geopolitical risk and changes in applicable laws or regulations; |

| ● | the possibility that we may be adversely affected by other economic, business, and/or competitive factors; |

| ● | operational risks; |

| ● | legal and other changes or actions by the PRC government to exert more oversight and control over offerings that are conducted overseas and / or foreign investment in China-based issuers which may significantly limit or completely hinder our ability to offer or continue to offer securities to investors and cause the value of our securities to significantly decline or be worthless; |

| ● | litigation and regulatory enforcement risks, which may result in the diversion of management time and attention and the additional costs and demands on our resources; |

ii

| ● | fluctuations in exchange rates between the foreign currencies in which we typically do business and the United States dollar; |

| ● | We may be materially and adversely affected by the complexity, uncertainties and changes in PRC regulation of the Internet industry and companies. |

| ● | Our business generates and processes a large amount of data, and we are required to comply with PRC laws and regulations relating to cyber security. These laws and regulations could create unexpected costs, subject us to enforcement actions for compliance failures, or restrict portions of our business or cause us to change its data practices or business model. |

| ● | Sudden or unexpected changes with little advance notice in China’s economic, political, or social conditions or government policies could have a material adverse effect on our business and operations. |

| ● | The PRC government may intervene or influence our operations at any time or may exert more control over offerings conducted overseas and/or foreign investment in China-based issuers, which could result in a material change in our operation and/or the value of our ordinary shares. |

| ● | Any actions by the PRC government to exert more oversight and control over offerings that are conducted overseas and/or foreign investment in China-based issuers could significantly limit or completely hinder our ability to offer or continue to offer securities to investors and cause the value of such securities to significantly decline or be worthless. We are currently not required to obtain approval from Chinese authorities to list on U.S. exchanges, however, if we are required to obtain approval in the future and were denied permission from Chinese authorities to list on U.S. exchanges, we will not be able to continue listing on U.S. exchange, which would materially affect the interest of the investors. |

| ● | You may experience difficulties in effecting service of legal process, enforcing foreign judgments, or bringing actions in China against us or our management named in the report based on foreign laws. It may also be difficult for you or overseas regulators to conduct investigations or collect evidence within China. |

iii

PART I

Item 1. Business.

Unless the context indicates otherwise, references in this Annual Report to the “Company,” “MicroAlgo,” “we,” “us,” “our” and similar terms refer to MicroAlgo Inc. and its consolidated subsidiaries. References to “Venus” refer to the predecessor company prior to the consummation of the Business Combination.

Background and Business Combination

MicroAlgo Inc. (“MicroAlgo” or the “Company”) (f/k/a Venus Acquisition Corporation (“Venus”)), a Cayman Islands exempted company, entered into the Business Combination and Merger Agreement dated June 10, 2021 (as amended on January 24, 2022, August 2, 2022, August 3, 2022 and August 10, 2022, the “Merger Agreement”), by and among WiMi Hologram Cloud Inc. (“WiMi” or the “Majority Shareholder”), Venus, Venus Merger Sub Corporation (“Venus Merger Sub”), a Cayman Islands exempted company incorporated for the purpose of effectuating the Business Combination (as defined herein), and VIYI Algorithm Inc. (“VIYI”), a Cayman Islands exempted company.

Pursuant to the terms of the Merger Agreement, the Company effected a business combination with VIYI through the merger of Merger Sub with and into VIYI, with VIYI surviving as the surviving company and as our wholly-owned subsidiary. In connection with the closing of the Business Combination, the Company changed its name to MicroAlgo Inc.

Mission

Our mission is to transform the digital economy by making the way our customers do business more efficiently.

Overview

We are dedicated to the development and application of bespoke central processing algorithms. We provide comprehensive solutions to customers by integrating central processing algorithms with software or hardware, or both, thereby helping them increase the number of customers, improve end-user satisfaction, achieve direct cost savings, reduce power consumption, and achieve technical goals. The range of our services include algorithm optimization, accelerating computing power without the need for hardware upgrades, lightweight data processing, and data intelligence services. Our ability to efficiently deliver software and hardware optimization to customers through bespoke central processing algorithms serves as a driving force for our long-term development.

Central processing algorithms refer to a range of computing algorithms, including analytical algorithms, recommendation algorithms, and acceleration algorithms. The businesses engaged in internet advertisement, game development, intelligent chip design, finance, retail, and logistics depend on the ability to efficiently process and analyze data with optimized computing software and hardware capable of handling the data workload. Bespoke central processing algorithms suitable to each customer’s distinct needs help them achieve this purpose.

In the mid-to-long term, we will continue to adhere to our strategic mindset. By improving upon each iteration of our one-stop intelligent data management solutions made possible by our proprietary central processing algorithm services, we can help customers to enhance their service efficiency and make model innovations in business, and actively enhance the industry value of the central processing algorithm services in the general field of data intelligent processing industry.

1

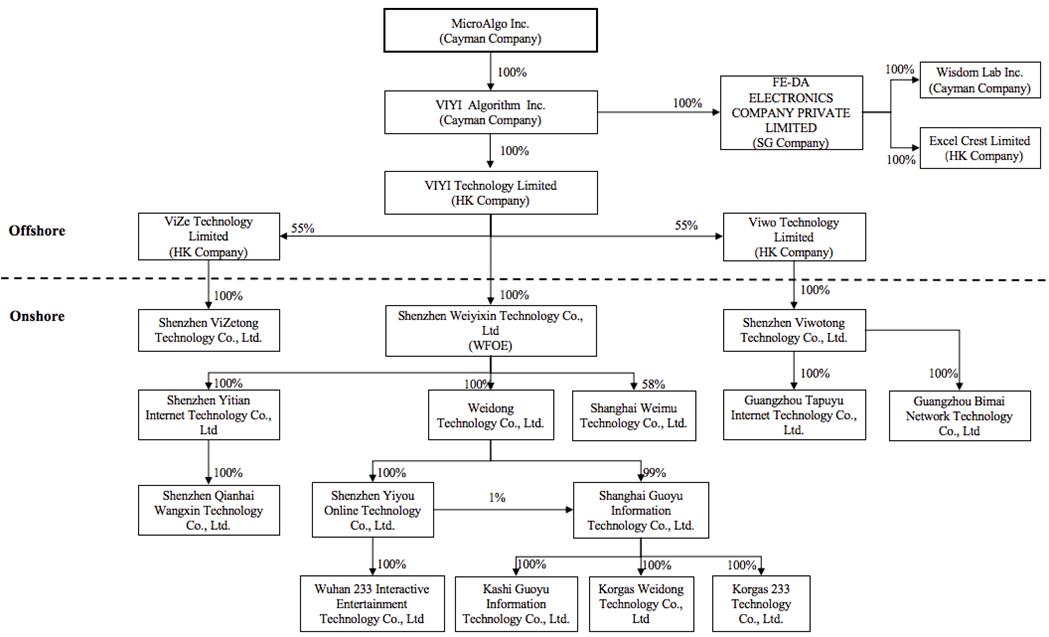

Our Organization

Our corporate structure as of December 31, 2022 is set forth below:

Competitive Strengths

We stand out as compared with our competitors in the following ways:

Leading bespoke central processing algorithm service provider in China enjoying first-mover advantages and rapid revenue growth

We are China’s leading central processing service provider and one of the earliest service providers to enter this field. In recent years, our business has grown rapidly and the growth rate of revenue has been increasing.

Customized central processing algorithm solutions in a diverse range of scenarios, serving customers in a diverse and growing range of industry verticals

Our diverse range of customers from multiple industries is evidence that our central processing algorithm technology is highly versatile, which allows us to ensure a constant stream of revenue from various sources. We primarily provide central processing algorithm solutions to enterprise customers in three industry verticals: internet advertisement, gaming, and intelligent chips, which translate to a range of customers including advertisement integration agencies, game developers and distributors, electronics manufacturers, internet information infrastructure service providers, and intelligent chip designers and integrators. Having the capability to service customers from a range of industries works to our advantage because we can derive business from multiple industry sources to ensure a stream of revenue even when one industry faces downturns.

2

Generally, the central processing algorithm services of our achieves computing power acceleration, digital lightweight processing, and intelligent data management and processing. These improvements help our customers grow and enhance their businesses’ operational quality and overall efficiency. Currently, our central processing algorithm solutions have the following applications to our existing core customers:

| ● | For customers in the internet advertisement industry, our proprietary central processing algorithms allow them to effectively optimize advertisement content, match internet traffic, and deliver targeted advertisements to increase conversion rate; |

| ● | For customers in the gaming industry, we provide a platform for distributing games augmented by cloud-based software and hardware optimization and acceleration, dynamic games marketing based on gamer preference, and lightweight data processing solutions to increase our customers’ revenue; |

| ● | For customers in the intelligent chip industry, we provide value-added data processing solutions and optimized hardware for more efficient data services, promoting our customers’ efficiency in developing new technologies. |

For more information on how we provide services to our customers, please see “Business—Our Business Model.”

In addition, due to the versatility of our central processing algorithm solutions and our proven commitment to research and development, we are well-positioned to continue growing our customer base to reach customers from a broader range of industries that are reforming the way they do business as a result of the rapidly developing information technology, prevalence of smartphones and 5G connectivity, AI, big data, IoT and cloud computing. The industry verticals such as government, finance, healthcare, manufacturing, education, and cultural media demand better data processing and management capabilities from an internet advertisement perspective. We believe that our highly versatile central processing algorithm solutions will be ideally suited to meet those demands. For more information on our expansion plans, please also see “Business—Our Strategies—We plan to expand our central processing algorithm solutions to cover more applications and different industries.”

Long-term and stable strategic cooperation relationships

We enjoy stable and long-term strategic alliances with many of our customers in the internet advertisement, gaming, and intelligent chip design and development. Our customers are internet advertising integration agencies, online game developers and distributors, electronics manufacturers, and internet information infrastructure service providers who have entered into a master agreement with us and used our services according to such agreement during the relevant contact period. Our customers typically enter into a master agreement with us for a fixed term, which means we are constantly communicating with our customers to help them explore needs or applications which may be optimized. Once that need is identified, our customers send in a separate request for service engagements or products, or both. Our involvement in our customers’ process of identifying needs means they count on us as trusted advisors to introduce them to industry trends and our latest technological developments. This close collaboration creates a synergistic effect between us and our customers, which results in high customer loyalty.

Market leader in cutting edge technology protected by intellectual property rights

We are the market leader in terms of the quantity of intellectual property. As of December 31, 2022, we own 548 proprietary intellectual property rights, which include 400 copyrights of which 396 are software copyrights, 83 patents, 27 registered trademarks, 20 exclusive rights for the layout design of integrated circuit, and 18 domain names. The large quantity of intellectual property at our disposal as compared to our competitors exemplifies our commitment to research and development and long-term development.

We leverage our fixation on staying in the forefront of technological development to help customers explore solutions and needs that are yet to be identified. We then provide proprietary central processing algorithm solutions to meet those needs.

To maintain our market leader position, we are seizing opportunities arising from the increasing global application of emerging technologies such as cloud computing, AI, and 5G, by focusing on applications stemming from these technologies that are ripe for optimization via central processing algorithms. In the year ended December 31, 2022, we expended $13,928,428 in research and development; we intend to commit more investments in the future to improve upon our research and development platform, retain talented individuals in the field of central processing algorithm technology, and strengthen the research and development for core technologies and products. Our efforts for research and development have, and will continue to secure our market leader position through technical barriers, which has allowed us to stay afront and be the first choice of our customers.

3

Visionary and experienced management team in the central processing algorithm industry and exceptional research and development team

We believe that our success is attributable in part to our experienced and visionary senior management team with extensive experience in China’s information technology industry. Our management team, led by Min Shu, our CEO and executive director, has delivered proven financial results since the company’s inception. Mr. Shu has accumulated over 22 years of experience in the information technology industry since he began his career as a software development engineer. Since entering the industry, he has also developed leadership and management skills in various management roles prior to joining us in 2018 as the deputy general manager of technology. Mr. Shu is supported by our senior management team with over 50 years of collective industry experience, including our Chairman of the Board, Jie Zhao, Chief Financial Officer, Li He, Chief Operating Officer, Shiwen Liu, and Chief Technical Officer, Chengwei Yi.

Our goal to stay at the forefront of technological development and fixation on research and development has driven us to build an exceptional research and development team staffed by 77 full-time research and development team members. Our research and development team is well versed in early-stage technological development to implement central processing algorithm solutions in a range of use cases. Our core technical staff have an average of 5 to 8 years of working experience in computer, software, computer graphic processing, data algorithm and neural networks. Our talented technical staff are responsible for the design and development of central processing algorithm solutions in, for example, algorithm design and development, digital graphic lightweight processing, image synthesis and data intelligence.

Excellent corporate culture and values attracting talents

Our management principals are best described as efficient and quick, open and innovative, and customer-dedicated:

| ● | Efficient and Quick—We pursues an efficient management model and follows the “craftsman’s spirit” to provide the most suitable solutions for our customers. In the face of the ever-changing internet industry, we are capable of responding quickly to industry changes. |

| ● | Open and Innovative—We maintains an open mind receptive to new business ideas. We value inclusion, embraces change, and pursues innovation and reform. Our team members enjoy their working environment and feel a sense of belonging. |

| ● | Customer-Dedicated—We are customer-dedicated. This means we aligns the interests of our customers with our own; thus, we are driven to meet the changing needs of our customers with quality services and products. |

Driven by our management principles, we have kept both of our team members and customers happy and satisfied, which has attributed to our success to date.

Our Strategies

To achieve our mission and further grow our market position, we plan to implement the following strategies:

We will continue to strengthen our central processing algorithm solutions for our core customers in internet advertisement, gaming, and intelligent chip businesses to ensure a steady revenue stream.

Our core customers in internet advertisement, gaming, and intelligent chip businesses represent industries experiencing significant growth in recent years and are expected to continue growing. We will continue to strengthen and market our central processing algorithm solutions applicable to our core industry customers to deliver measurable results and ensure a constant stream of revenue.

4

In terms of the digital marketing industry, we understand our customers are increasingly focusing on measurable advertising results, with performance-based advertising solutions experiencing rapid growth. Our scalable central processing algorithm solutions are well suited to meet this increasing demand and customers’ need for measurable results, i. e., measurable conversion rate. For details of our range of services for internet advertisement customers, please see “Business—Our Business Model—Application of our central processing algorithm service in internet advertisement.”

In terms of the gaming industry, our game distribution platform coupled with the capability to provide central processing algorithm solutions to upstream developers and gamers alike is uniquely positioned to capture this growing market opportunity. For details of our range of services for gaming industry customers, please see “Business—our Business Model—Application of our central processing algorithm service in internet gaming entertainment industry.”

In terms of the intelligent chip industry, technologies that are critical to the intelligent chip industry have become increasingly mature since the beginning of the 21st century. Intelligent chips have also been entering into consumers’ daily lives at an increasing rate as components to mobile phones, personal computers, and smart TVs. The development of AI will be a significant driving force behind the monetization market for central processing algorithm solutions intended to optimize intelligent chip performance.

From the perspective of applications of our central processing algorithms in relation to intelligent chips, we understand that AI—from cloud to edge or down to terminals—is inseparable from the ability for intelligent chips to efficiently execute “training” and “inference” computing tasks, which cannot occur unless the baseline software and hardware are optimized correctly. Moreover, industrial applications of intelligent chips are wide-ranging and include information infrastructure services, electronic products manufacturing, image recognition, voice recognition, machine translation, smart IoT, and other smart applications. These demands create a distinct market for our central processing algorithms solutions, while giving off better energy efficiency ratios during such data processing exercises.

We will continue to strengthen our research and development capabilities in central processing algorithms to establish more technical barriers to enhance our competitiveness.

Technological innovation coupled with research and development sets the foundation for us to maintain competitiveness. We endeavor to increase investments in research and development to improve upon our research and development platform, retain talented individuals in the field of central processing algorithm technology, and strengthen the research and development for core technologies and products, intelligent chips algorithms and AI algorithms. In so doing, we aim to seize first-mover opportunities created by an increasing global application of emerging technologies such as cloud computing, artificial intelligence, and 5G, and focus on the development of central processing algorithm services capable of enhancing the research and development capabilities for these emerging technologies.

Meanwhile, we are continuously working on expanding our range of intellectual property, including software copyright and utility model patents. Currently, we have utility model patents also under application, including “overheating detection device of central processing unit” and “fault and power failure device of central processing unit.”

Through research and development, we will continue to improve the applications and platform upon which we provide our central processing algorithm service. By taking advantage of cloud computing, we plan on integrating AI chip technology, big data management, analytics, and other emerging technologies to provide a comprehensive service platform that combines both hardware and software to explore all potential value of data by way of data intelligence analysis. Our ultimate goal is to integrate central processing algorithm technology, big data, and artificial intelligence via the cloud infrastructure and provide even more versatile software and hardware integration service for smart application for industrial purposes, creating an ecosystem where individuals, enterprises and various applications are interconnected, so as to enable our customers and other industry participants to accelerate the process of digital transformation in alignment with our mission.

5

We plan to expand our central processing algorithm solutions to cover more applications and increase marketing efforts aimed at different industries.

We plan to expand the range of our central processing algorithms’ application for use in mobile internet, finance, government, manufacturing, and other industries where there is an increasing demand for data management and processing efficiency. While focusing on our customers in internet advertisement, gaming, and intelligent chips to generate revenue, we intend to branch out in accordance with market trends and continue to expand the application and platform of our central processing algorithm solutions consistently with this development strategy. In so doing, we intend to expand our integrated services built upon our proprietary central processing algorithms to penetrate industries including:

| ● | Government cloud computing; |

| ● | Manufacturing industry; |

| ● | Financial technology; |

| ● | Medical cloud computing; |

| ● | Smart transportation; |

| ● | PaaS 3D; and |

| ● | Central processing algorithm cloud service for enterprise (SAAS) marketing. |

Below is a brief industry overview for each of these industries and our value-added:

Government cloud central processing algorithm services

The government is committed to breaking down data silos and sharing urban resources to provide better civil services and security to the general population, which means the “market” for the government’s services is by far the largest in any industry. In the process of a government’s self-transformation, it would be required to undertake massive data management and analysis, massive data connectivity and massive city terminal perception exercises.

In general, the government cloud is a platform that serves as the “engine room,” coordinating the technological hardware and software resources used by the government. The cloud provides the government with a platform to engage in comprehensive services such as infrastructure, supporting software, application system, information resources, operation guarantee, and information security. By using cloud technology, the government significantly reduces IT costs, promotes the sharing of information between departments, and improves the speed of launching applications and service quality. The government is also able to accelerate the establishment of smart cities and satisfy the high threshold of data sharing by efficiently processing and managing data.

The government cloud algorithm solutions we intend to provide enable the government to improve the efficiency and quality of service of the government cloud platform’s operational efficiency and quality of service, and have exhibited strong market potential.

Central processing algorithm services for the manufacturing industry

As information technology is ever-increasing intertwined with traditional manufacturing industries, the industrial internet is constantly required to upgrade ICT infrastructure platform, which is a platform for unified communications, to support the application digitalization, networking, and intelligent upgrading of the manufacturing industry and the entire real economy. The integration of information technology and manufacturing also gave rise to new business models such as network collaboration, personalized customization, and service-oriented manufacturing. A variety of machines, devices, and equipment must be embedded with a large number of energy-efficient chips and connected to the network through sensors, embedded controllers, and application systems to form a new complex architecture based on “terminal-cloud” collaboration.

6

With the integration of AI, these new business models promote the centralization and intelligent development of the manufacturing industry. As a result of network inter connectivity between machines, raw materials, control systems, information systems, products, and people, efficient business decisions can be made through the combination of comprehensive and in-depth perception of data and big data analysis to achieve intelligent control, operation optimization and production organization reform, effectively unleashing the potential of machines and enhancing productivity. As a transit station for data localization and transmission, central processing algorithms serve a crucial role in the overall development of the industrial internet.

Financial technology central processing algorithm services

Financial technology is reshaping the way the financial industry work. The transformation of channel and real-time trading scenarios from a centralized system to a fully distributed system demands higher computing power and better energy efficiency ratios. In the next few years, operation analysis scenario will complete the switch from all-in-one to an open architecture, requiring high distributed concurrency. The new smart finance business is the fastest-growing scenario in the future, which requires high concurrency and mobile collaboration. The traditional business scenario is transforming to the cloud, which requires low energy consumption and costs to improve the price-performance ratio of big data comprehensive analysis.

Big data finance focuses on the acquisition, storage, processing analysis, and visualization of financial big data. In general, the core technologies of financial big data include the infrastructure layer, the data storage and management layer, the computing processing layer, the data analysis and visualization layer. The data analysis and visualization layer are mainly responsible for simple data analysis, advanced data analysis, and visualization of the relevant analysis results. Big data finance is also committed to the research and development of new financial business models of financing, payment, investment, and information intermediary services by adopting internet technology and information and communications technology. The application scenarios above would benefit from bespoke centralized processing algorithms to improve business efficiency and reduce costs.

Medical cloud central processing algorithm services

Big data and AI technologies will drive the way consumers access health care. Applications include intelligent healthcare such as disease prediction, personalized precision healthcare, personalized medicine, and medical graph and image analysis. Distinct features of the medical cloud include data diversity (such as voice, text, and medical images) and massive data volume (such as high-quality data training). Our central processing algorithms solutions can meet the diversified computing needs for green and low power consumption and intensive computing power.

The medical cloud essentially serves as the holder of electronic health records. With the development of the medical cloud, functions such as remote consultation, remote medical treatment, and information sharing are becoming a reality. Moreover, medical cloud will promote public health and achieve cross-system and cross-department business information sharing, allowing medical and health service institutions to share medical resources and carry out remote diagnosis and treatment services to individuals or families to reduce repeated examination expenditures. It will also make patient transfers between hospitals more efficient, and patients can enjoy higher quality services through remote medical treatment and establish an information-sharing platform.

Intelligent transportation central processing algorithm services

Terminal-edge-cloud is crucial to the future of how people travel. On the terminal side, it is necessary to have a comprehensive view of the surrounding situation and detailed information and to make changes in a timely manner. On the edge side, it is essential to timely provide intelligent and accurate information on decision-making for efficient deployment. On the cloud side, a sustainable and iterative “brain” is needed to empower the edge and terminal sides. Collection of traffic information through efficient technologies enables transportation industry players to engage in more efficient traffic management, public travel, and the industry vertical pertaining to transportation construction management. Through the terminal-edge-cloud, and interconnected transportation system can efficiently perceive, analyze, predict and control regional traffic to ensure safety and efficiency.

7

To achieve such a level of interconnectivity, terminal-edge cloud servers and data centers perform intensive arithmetic processing for large amounts of raw data, which demands excellent computing capacity, speed, data storage, and bandwidth of basic hardware such as chips. As traditional data centers face various development bottlenecks such as high energy consumption and low computing efficiency, terminal-edge cloud servers will prove to be the answer to the industry’s current problem.

With the continuous popularization of these new technologies, the realization of an intelligent society must first undergo comprehensive digitalization, and the central processing algorithm application field is the core driver of such digitalization.

PaaS 3D central processing algorithm cloud services

Based on the 3DPaaS vertical cloud service platform, we provide internet industry applications with support in areas including scenario intelligence, scenario visualization, and lightweight processing for 3D interactive procedures. One of our goals is to construct the best intelligent 3D data platform in China to provide more efficient and intelligent information services for people’s work and life.

Through the implementation of hybrid cloud deployment solutions, 3D computing system architecture, and interactive stream transmission, we have solved many industry pain points, such as excessive data usage on 3D Internet online applications and cross-platform deployment. Our self-developed 3D acceleration algorithm, intelligent interaction, and stream transmission technologies are the first in the PRC and have already achieved commercialization.

We provide enterprises with a one-stop lightweight launching cloud platform for 3D applications, which is featured with scenario-based intelligent interaction. We will charge fees on a project-by-project basis (B2B) or based on various factors such as space usage and traffic volume, annual fees, and technology licensing to cater to different industries such as VR, AR, games, 3D interactive programs, and scenario-based e-commerce. We will facilitate the promotion and application of central processing algorithm technology in the future.

Central processing algorithm cloud service for enterprise (SAAS) marketing

Leveraging our technologies on 3D online display, VR tours, data algorithm analysis, and precise traffic algorithm matching, we will provide enterprise owners with a one-stop product display system, real-time VR product tour and interactive communication, VR live professional broadcast promotion, and sales platform, decision-making system for customer acquisition and data optimization, and consumer analysis and accurate user matching algorithm system.

This technology provides a new form of display and interactive communication for products and integrates the functions, features, and highlights of product introduction. Through intuitive interaction, customers can quickly switch and select different materials and colors of the same product.

| ● | SAAS marketing helps customers to craft a compelling story about products with professional sales presentations and flexible operation and interaction methods. |

| ● | Helping customers to understand the advantages of the products in the shortest time immediately establishes efficient communication between customers and corporate personnel, improves consumer decision-making efficiency, and enhances user acquisition efficiency by increasing the scope of live streaming. |

| ● | Data optimization algorithms can help customers to accurately match consumers and traffic users, and thereby increasing the conversion rate of product sales; and |

| ● | Efficient transactions can be achieved by attracting and stimulating consumers’ desire with highly innovative presentation and integrated algorithms. |

8

Leveraging the current development of the central processing algorithm technology and our technical reserve capability, the platform is ready for use under the existing environment. We will receive relevant service fees from content production, annual fees for the SAAS system, algorithm technology service fees, and streaming platform licensing fees. We are currently liaising with some small and medium-sized brand owners in relation to the provision of our competitive product (SAAS) marketing cloud services. Our next step is to provide global online product (SAAS) marketing cloud services both domestically and internationally to export companies and factories.

We will selectively seek strategic acquisitions to enhance market position, integrate industrial chain resources, and maximize capital efficiency.

We intend to pursue investment opportunities or acquire businesses that complement or enhance our existing businesses that are strategically beneficial to our long-term goals. We aim to target companies that have competitive strengths in algorithm development and research, and AI capabilities to enhance our research and development abilities.

In addition, we plan to pursue business collaborations to enhance our operational efficiency by collaborating with resource-based partners that generate significant user traffic. Our ideal partners are internet traffic wholesalers, game developers, and advertisement integration agencies.

We will continue our focus on brand building to enhance our brand value.

Concurrent to improving our innovative technologies, we are attaching ever greater importance to brand building and strategic positioning, especially in view of becoming a public company. We carry out brand value communication through multiple channels, including through media and investor relations. We believe that building a good reputation in the industry is essential to building up brand value. We strive to maximize brand value by providing customers with high-quality products and services, operates our business with integrity, and builds an excellent corporate image through good value output.

Our Business Model

We provide central processing algorithm solutions primarily to the internet advertisement, gaming, and intelligent chip industry. Our customers are internet advertising integration agencies, online game developers and distributors, electronics manufacturers, and internet information infrastructure service providers who have entered into contracts with us and used our services pursuant to such contracts during the relevant period. Customers typically enter into a master agreement with us for a fixed term and submit separate requests for each service engagement or product, or for both. For more information on how We enter into business arrangements with our customers, please see “Business—Our Strengths—Long-term and stable strategic cooperation relationships.”

Application of our central processing algorithm service in internet advertisement

Generally, for customers in the field of internet advertisement, like internet advertising integration agencies, our central processing algorithm solutions helps them engage in more efficient data processing and management, which culminates in more effective programmed advertising and dynamic content optimization with the goal to improve consumer conversion rate, which means the rate at which individuals who have seen an advertisement turn into a user or purchaser of the service or items contemplated by the advertisement.

Our proprietary central processing algorithm solutions improve upon the processes by which our customers are able to make one of their most crucial business decisions—the effective placement of advertisements. In sum, our customers provide advertisement materials in the form of 3D models or images, which we process in our back servers into more detailed data such as color key and fusion image; we then purchas advertisement placement opportunities from ad traffic wholesalers and begins analyzing multimedia sources hosted on such traffic wholesalers with our image recognition software to extract scenario data from such videos to determine data points such as the location, time, space and other useful information. At the same time, we are also processing internet users’ data to achieve effective and precise placement of advertisements.

9

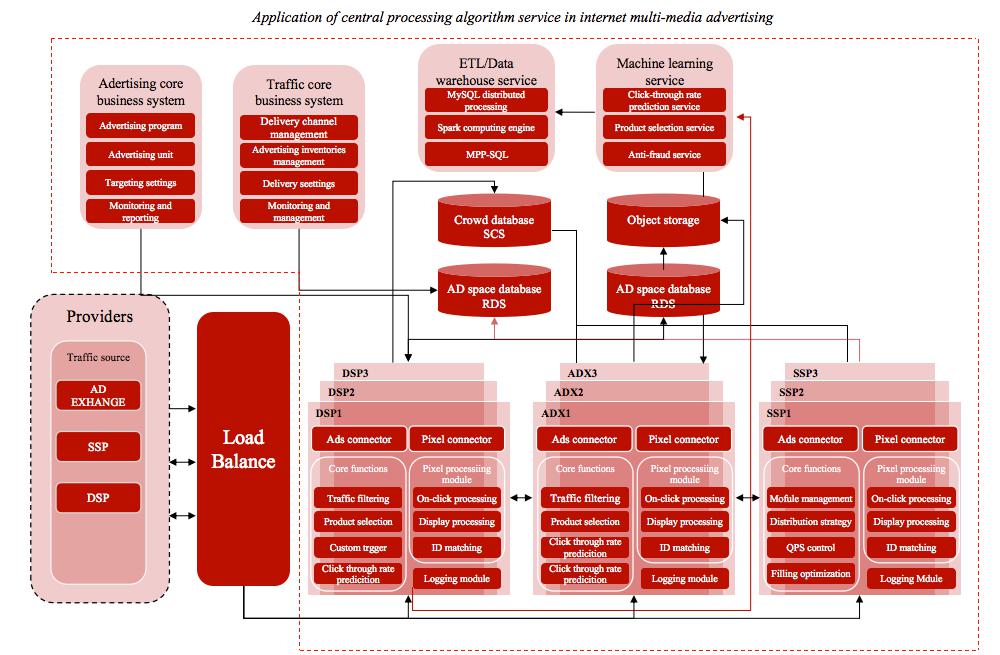

The diagram below illustrates the key steps of providing solutions to our digital marketing customers:

We first obtain advertisement placement opportunities from internet traffic wholesalers. We then use our image recognition software to perform scenario-based classification of such videos to determine their location, time, space, and other relevant information to identify the most appropriate places to insert our customers’ advertisements. With such data, we establish dynamic information databases in relation to these multimedia sources with technology such as Relational Database Service (RDS) to be further processed at our disposal. At the same time, our back servers are communicating with these traffic wholesaler’s servers to collect user data, which we then processes with our crowd-based socio-cognitive systems (SCS) for the purpose of effectively placing our customer’s advertisement through a process of dynamic content optimization (DCO), with the aim of improving our customers’ consumer conversion rate.

In sum, we provide effective advertising solutions for digital marketers by optimizing advertising content and precisely matching content with suitable consumers by processing a massive amount of data through efficient automation. Eligible consumers are selected in accordance with their demographics and personal preferences, which our central processing algorithm service is able to analyze for the purpose of maximizing the internet advertisement effect.

We ensure high-quality engineering architecture for our proprietary central processing algorithms, which means our services are being provided at low latencies while being highly scalable. We are capable of powerful real-time transcoding with stable, smooth, and low latency, which provides our customers valuable insights into consumer behavior.

10

Application of our central processing algorithm service in the internet gaming entertainment industry

With respect to customers in the gaming and entertainment industry, we provide game developers with lightweight data processing solutions through customized central processing algorithms. We also maintain a proprietary game distribution platform hosted “on the cloud,” where we interact with gamers directly, publishes our customers’ games and provides software and hardware performance acceleration and optimization through customized central processing algorithms. Our game distribution platform also uses accurate traffic targeting algorithms to match gamers with suitable games. Our upstream solutions aim to help our customers in the gaming industry to improve the gamer experience and increase conversion rate since our solutions tend to reduce the initial cost for buying such games, which tends to increase the willingness for gamers to pay for in-game items or subscriptions.

Our games distribution platform uses an architecture design that is part terminal and part cloud— “terminal+cloud” —this helps our customers to obtain lightweight terminals and low-latency, high-response results. Through the central processing algorithm service, we optimize algorithms (computing process performed on computers) and computing power (computing capacity of computers) of software algorithms so that end-users game files are small, and the game content is gradually loaded as it is being used, as opposed to loading a large chunk of data at the beginning to maintain smooth operation. Combining with hardware algorithm optimization, we accelerate the computing power and the loading of games at the gamer’s end to improve user experience. We also engage in practical data collection exercises with our proprietary algorithms through the game distribution platform; we then analyze such data for the benefit of our customers to improve conversion rates and achieve cost reduction. All of this can be acquired and scaled with our bespoke centralized processing algorithms.

Our platform also provides payment services for gamers to access high-quality and diversified game content. From payment patterns, our centralized processing algorithms engage in machine learning to increase the accuracy and efficiency of our central processing algorithm service, which results in referrals and more customers while increasing our revenue. Our games distribution platform is essentially a self-sufficient ecosystem providing support to both our upstream customers to downstream gamers.

Notably, our online application acceleration solutions made possible by our central processing algorithms can continuously monitor and optimize the data transmission path of the whole network. These solutions reduce latency and packet loss and provide high-quality real-time participation for millions of concurrent users, which is a solution for not only our customers engaged in the games industry but also those in social and online education industries.

Our gaming platform powered by our proprietary central processing algorithm improves the marketing conversion rate of games by 20% through personalized recommendation, acceleration, and convenient distribution, it also significantly improves gamer experience, reduces the cost to our customers and improves the retention rate and payment rate of gamers.

From an industry demand perspective, game developers, their corporate customers, and marketing agents have been demanding more effective online game licensing solutions in recent years.

We have mature technology and customer resources in the field of entertainment and game central processing algorithms. With the development of the market, we will continue to grow on the basis of existing customers and strive for a larger market share.

Application of our central processing algorithm service in intelligent chip optimization solutions business

Our intelligent chip industry customers depend on us to provide them with solutions for data processing and optimizing hardware. Our centralized processing algorithm solution manifests in the form of reducing our customer’s energy efficiency ratio through more efficient data services under optimization of algorithm software as well as through equipping instruction chip CPU with intelligent chips such as GPU, FPGA, and ASIC that have incredible computing power. Different CPU and intelligent chip combinations are fitted in accordance with the diverse requirements of data processing and various data type of other industries. We also provide CPUs coupled with integrated smart application solutions. By delivering our products directly to customers, we act as the bridge between upstream and downstream businesses in the CPU industry chain.

11

Currently, the chips applied in the AI field are primarily designed for specific applications and are unable to adapt to the needs of multiple scenarios flexibly. In order to achieve progress in the field of artificial intelligence, an intelligent chip must adapt to the requirements of various algorithms in different scenarios, provide powerful computing power support, and meet the application of terminal scenarios with high energy consumption ratios.

We apply central processing algorithm to intelligent chip optimization. Our central processing algorithm service has mature technology in chip performance improvement and software application, providing chip products based on solution services and technology development services for customers. Usually, we provide customers with online technical services and support, and we also provide customers with on-site technical solution implementation and technical support. Intelligent chips must be able to change the function dynamically in real-time to meet the changing needs of the software. Software defines hardware, hardware feedback software. Through the central processing algorithm to explore the specific architecture of machine learning, architecture feedback to the central processing algorithm to optimize, to achieve two-way optimization. If a chip is to be deemed practical, it must have robust scalability so that it can be used in more scenarios. The central processing algorithm can make more efficient use of the chip architecture, guide the design of the chip architecture, and transform the computing power into intelligence.

We use the central processing algorithm, the instruction chip CPU is equipped with GPU, FPGA, ASIC, and other intelligent chips with more outstanding computing power. In order to improve the overall energy efficiency ratio of data service, according to the different data of different industries and their various data processing methods, we use the CPU to carry different combinations of intelligent chips to realize more efficient data service under the optimization of algorithm software.

By using our powerful central processing algorithm technology, we can provide chip optimization solutions for customers’ personalized needs. We provide our customers with the application scheme of the combination of CPU and central processing algorithm. Through more effective use of central processing algorithms, artificial intelligence, cloud computing, and other technologies for chip resources and data scheduling, we can meet the diversified needs of customers. We use the central processing algorithm service to realize the computing acceleration, data lightweight, and efficiency in the cloud computing application field.

Leveraging our central processing algorithm services, we have achieved accelerated computing in cloud computing applications, data lightweight efficiency enhancement, and traffic monetization. Our strength in intelligent chip optimization solutions business in satisfying the development requirements of mobile and data business has accelerated the transformation of the computing architecture of cloud service providers from a single to a diversified one. Under the multiplier effect generated by the combination of 5G and central processing algorithm service technologies, we will facilitate the effective collaboration of and build an ecosystem for the “terminal-edge-cloud” application scenarios of our customers.

Benefiting from the development of IoT, cloud computing technology, and the increasing government investment, China’s artificial intelligence market size is in the process of speedy expansion, the development of the artificial intelligence market will drive the growth of the central processing algorithm intelligent chip optimization solution industry.

In the future, IoT will provide more data collection terminals, which dramatically enhances the data volume. Big data provides information sources for AI, cloud computing offers a physical carrier for AI, and 5G reduces the delay of data transmission and processing. 5G, IoT, cloud computing all put forward higher data processing, analysis, and other needs and requirements. The central processing algorithm intelligent chip solutions combined with hardware performance optimization, software algorithm optimization, and other vital technologies will make breakthrough progress in the future under the background of the increasingly mature emerging technologies such as 5G, IoT, cloud computing, and big data.

12

Our Ecosystem and our Participants

We have effectively established an ecosystem centered around internet advertisement, games, and intelligent chip optimization. We connect with market participants representing every stage in these core industry verticals. They include advertisers, internet advertising integration agencies, internet traffic wholesalers, online platforms, online game developers and distributors, cloud service providers, electronics manufacturers, internet information infrastructure service providers, and internet users, as illustrated in the diagram below:

Our revenue from digital marketing is derived based on the effectiveness of our ad placement. Our one-stop-shop service solutions enable internet advertising integration agencies to complete cost-effective advertising placements, which allows them to acquire, transform and retain advertisers efficiently.

As cost outlays, we purchase advertisement placement opportunities from internet traffic wholesalers. We also pay corresponding fees to internet traffic wholesalers based on the CPM charging model.

13

To ensure a continuous stream of revenue, we are constantly updating the inventory of advertisements ready for placement to internet traffic wholesalers with whom our partners. They include short video platforms, video platforms for drama series and films, as well as news and information platforms. We are constantly updating internet traffic wholesalers’ advertisement inventories in real-time for maximum effectiveness. The central processing algorithm services we provide are able to meet these real-time requirements. Therefore, we believe that our services are critical to helping our customers to achieve high conversion rates.

Our revenue from the gaming industry is mainly derived from sales commissions. We collaborated with numerous online game developers and game distributors in operating online games, which are made available on our online game platform. We provide online game developers and game distributors with value-added services through customized central processing algorithm processing services, including lightweight data processing, computing power, and algorithm optimizations as well as game acceleration.

We also use cloud services to ensure that our central processing algorithm services are maintained in a safe and reliable environment.

Our revenue from the intelligent chip industry is derived from service fees and sales revenue. Electronics manufacturers and internet information infrastructure service providers rely on our intelligent chip optimization solutions; We provide them with hardware and software integrated intelligent chip optimization solution services that combine chip hardware and smart application software.

Sales and Marketing

For the years ended December 31, 2021, and 2022, we had 248 and 173 customers who engaged us to provide central processing algorithm services and intelligent chips and services business, respectively. We focus our efforts to deepen our relationships with existing customers, develop relationships with new and potential customers, and on exploring untapped business opportunities. Our company has mature business development capabilities and oftentimes rely on customer referrals. As such, we do not require intensive investments in sales modeling. This results in direct cost savings in terms of project travel, public relations, and business entertainment.

In addition, while optimizing the service of central processing algorithm, we are also adjusting our sales strategy with the change of market environment, taking advantage of good service, seeking potential clients in the industry so as to increase our revenue and market share rapidly. We have built deep relationships with our major customers from whom we generate a significant amount of our revenue.

14

Research and Development

As of December 31, 2022, our research and development team consisted of 77 full-time staff. The professional background of our team members include computer, software, computer graphic processing, data algorithm, and neural networks. Our research and development team has extensive experience, averaging 5 – 8 years of working experience, and is responsible for the design and development of solutions for our central processing algorithms services such as digital graphic lightweight, algorithm, data intelligence, and image synthesis.

We are committed to continuously strengthening and updating our information technology infrastructure and other technologies according to our annual development plan and based on our assessment of market demand. The process of our self-development research and development is as follows: (1) research and development personnel raises new ideas for research and development based on the market situation and customers’ needs to complete the investigation report and decision analysis; (2) project approval and formulate product research and development plan; (3) development of product technology; (4) product testing and review; (5) launching of new product; (6) promotion and application of the new product.

Intellectual Property

Intellectual property rights are critical to our success and competitiveness. We rely on a combination of trademarks, patents, domain names, copyrights, and employee confidentiality agreements to protect our intellectual property rights. As of December 31, 2022, we owned:

| ● | Trademarks: 27 registered trademarks in the PRC; |

| ● | Patents: 83 patents in the PRC; |

| ● | Layout design of integrated circuit: 20 items in the PRC; |

| ● | Domain names: 18 domain names in the PRC; |

| ● | Copyrights: 4 works of copyrights in the PRC; |

| ● | Software copyrights: 396 works of software copyrights in the PRC; |

All of which are material to our business.

Competition

There are other companies addressing various aspects/verticals of the central processing algorithm service market in the PRC. The central processing algorithm service market is highly fragmented and evolving. With respect to our central processing algorithm services, we compete against other companies engaged in similar services like us.

We believe the principal competitive factors in our market are:

| ● | service and products feature and functionality; |

| ● | capability for customization, configurability, integration, security, scalability, and reliability; |

| ● | quality of technologies and research and development capabilities; |

| ● | ability to innovate and rapidly respond to customer needs; |

| ● | the breadth of use cases supported; |

| ● | diversified customer base; |

15

| ● | relationships with key participants in our customers’ industry verticals; |

| ● | sufficient capital support; |

| ● | platform extensibility and ability to integrate with emerging technologies such as AI and cloud computing; and |

| ● | brand awareness and reputation. |

We believe we compete favorably on the basis of the above factors; however, we expect competition to intensify in the future. Our ability to remain competitive will largely depend on the quality of our applications, the effectiveness of our sales and marketing efforts, the quality of our customer service, and our ability to acquire or develop complementary technologies, products, and businesses to enhance the features and functionality of our applications.

Employees

We had 125 full-time employees, respectively, as of December 31, 2022. As of the date of this report, all of our employees are based in China.

The following table sets forth the number of our employees as of December 31, 2022:

| Function | full-time employees |

|||

| Research and Development | 77 | |||

| Business and Marketing | 26 | |||

| Administrative, Human Resources and Finance | 22 | |||

| Total | 125 | |||

Under PRC law, we participate in various employee social security plans that are organized by municipal and provincial governments for our PRC-based full-time employees, including pension, unemployment insurance, childbirth insurance, work-related injury insurance, medical insurance, and housing fund. We are required under PRC law to make contributions monthly to employee benefit plans for our PRC-based full-time employees at specified percentages of the salaries, bonuses, and certain allowances of such employees, up to a maximum amount determined by the local governments in China.

We enter into labor contracts and standard confidentiality and non-compete agreements with our key employees. We believe that we maintain a good working relationship with our employees, and we have not experienced any labor disputes. None of our employees are represented by labor unions.

Facilities

Our headquarters are located in Shenzhen, China, and our maintain office in Unit 507, Building C, Taoyuan Street, Long Jing High and New Technology Jingu Pioneer Park, Nanshan District, Shenzhen, 518052. We believe that our existing facilities are adequate for our current requirements and that additional space can be obtained on commercially reasonable terms to meet our future needs.

Insurance

We do not maintain insurance policies covering damages to our Information Technology systems. Neither do we carry business interruption insurance or general third-party liability insurance or have product liability insurance or key-man insurance. We consider our insurance coverage to be in line with that of other companies in the same industry of similar size in China.

Legal Proceedings

We may be subject to legal proceedings, investigations, and claims incidental to the conduct of our business from time to time. We are not currently a party to, nor are we aware of, any legal proceedings, investigations, or claims which, in the opinion of our management, are likely to have a material adverse effect on our business, financial condition, or results of operations.

16

Item 1A. Risk Factors.

The following risk factors apply to our business and operations. These risk factors are not exhaustive, and investors are encouraged to perform their own investigation with respect to our business, financial condition and prospects. We may face additional risks and uncertainties that are not presently known to us, or that we currently deem immaterial, which may also impair our business. The following discussion should be read in conjunction with the financial statements and notes to such financial statements included elsewhere in this Annual Report and the “Management’s Discussion and Analysis of Financial Condition and Results of Operations” section of this Annual Report.

Risk Factors Relating to our Business and Industry

We operate in a relatively new and rapidly evolving market.

We provide customers with comprehensive solutions integrating central processing algorithms with software or hardware to streamline their digital services to end users, thereby helping our customers to improve end user satisfaction, achieve direct cost savings, and reduce power consumption. Our services include algorithm optimization, accelerating computing power without the need for hardware upgrades, lightweight data processing and data intelligence services. Our business and prospects mainly depend on the continuous development and growth of the central processing algorithm service industry in the PRC. The development of this industry is affected by numerous factors, including but not limited to technological innovation, user experience, the development of the Internet and Internet-based services, regulatory environment, and macro-economic environment. The markets for our products and services are relatively new and rapidly developing and are subject to significant challenges. In addition, our continued growth depends, in part, on our ability to respond to changes in the central processing algorithm service industry, including rapid technological evolution, continued shifts in customer demands, introductions of new products and services and emergence of new industry standards and practices. Developing and integrating new solutions, products, services or infrastructure could be expensive and time-consuming, and these efforts may not yield the benefits we expect to achieve.

In addition, as the central processing algorithm service industry in China is relatively young, there are few proven methods of projecting customer demand or available industry standards on which we can rely. Some of our current monetization methods are also in a relatively preliminary stage. We cannot assure you that our attempts to monetize current applications will continue to be successful, profitable or accepted, and therefore the profit potential of our business is difficult to gauge. Our growth prospects should be considered in light of the risks and uncertainties that fast-growing early-stage companies with limited operating history in an evolving industry may encounter, including, among others, risks and uncertainties regarding our ability to:

| ● | continue to develop new software and related solutions that are appealing to customers; |

| ● | maintain stable relationships with other key participants in the value chain; |

| ● | expand products and services into more scenarios and customer bases; and |

| ● | expand into new geographic markets with high growth potential. |

Addressing these risks and uncertainties will require significant capital expenditures and allocation of valuable management and employee resources. We cannot assure you that it will succeed in any of these aspects or that the central processing algorithm service industry in the PRC will continue to grow at a rapid pace. If we fail to successfully address any of the above risks and uncertainties, then the size of our customer base, our revenue and profits may decline.

17

Our competitive position and results of operations could be harmed if we do not compete effectively.

The markets for our products and services are characterized by intense competition, new industry standards, limited barriers to entry, disruptive technology developments, short product life cycles, customer price sensitivity and frequent product introductions (including alternatives with limited functionality available at lower costs or free of charge). Any of these factors could create downward pressure on pricing and profitability and could adversely affect our ability to retain current customers or attract new customers. Our future success will depend on a continued ability to enhance and integrate our existing products and services, introduce new products and services in a timely and cost-effective manner, meet changing customer expectations and needs, extend our core technology into new applications, and anticipate emerging standards, business models, software delivery methods and other technological developments. Furthermore, some of our current and potential competitors enjoy competitive advantages such as greater financial, technical, sales, marketing and other resources, broader brand awareness, and access to larger customer bases. As a result of these advantages, potential and current customers might select the products and services of our competitors, causing a loss of market share to us.

We have a limited operating history, and it may not be able to sustain rapid growth, effectively manage growth or implement business strategies.

We have a limited operating history. Although we have experienced significant growth since launching our business, our historical performance results and growth rate may not be indicative of our future performance. We may not be able to achieve similar results or grow at the same rate as it has in the past. To keep pace with the development of the central processing algorithm service industry in the PRC, we may need to adjust and upgrade our product and service offerings or modify our business model. These adjustments may not achieve expected results and may have a material and adverse impact on our financial conditions and results of operations.

In addition, our rapid growth and expansion have placed, and is expected to continue to place, a significant strain on our management and resources. There is no assurance that the future growth of us will be sustained at a similar rate or at all. We believe that our revenue, expenses and operating results may vary from period to period in response to a variety of factors beyond our control, which primarily include general economic conditions, emergencies and changes in policies, laws and regulations that may affect our business operations and our ability to monitor costs. In addition, our ability to develop new sources of revenues, diversify monetization methods, attract and retain customers, continue developing innovative technologies, increase brand awareness, expand into new market segments, and adjust to the rapidly changing regulatory environment in the PRC, will also affect our future growth to a great extent. Therefore, you should not rely on our historical results in predict our future financial performance.

Recent acquisitions could prove difficult to integrate, disrupt the business, dilute shareholder value and strain the resources.

On September 28, 2020, we acquired 100% equity interests of Fe-da Electronics. Integrating the operations of acquired businesses successfully or otherwise realizing any of the anticipated benefits of acquisitions, including anticipated cost savings and additional revenue opportunities, involves a number of potential challenges. The failure to meet these integration challenges could seriously harm the financial condition and results of operations of us. Realizing the benefits of acquisitions depends in part on the integration of operations and personnel. These integration activities are complex and time-consuming, and we may encounter unexpected difficulties or incur unexpected costs, including:

| ● | the inability to achieve the operating synergies anticipated in the acquisitions; |

| ● | diversion of management attention from ongoing business concerns to integration matters; |

| ● | consolidating and rationalizing information technology platforms and administrative infrastructures; |

18

| ● | complexities associated with managing the geographic separation of the combined businesses and consolidating multiple physical locations; |

| ● | retaining professionals and other key employees and achieving minimal unplanned attrition; |

| ● | integrating personnel from different corporate cultures while maintaining focus on providing consistent and high quality service; |

| ● | demonstrating to the clients and to clients of acquired businesses that the acquisition will not result in adverse changes in client service standards or business focus; |

| ● | possible cash flow interruption or loss of revenue as a result of transitional matters; and |

| ● | inability to generate sufficient revenue to offset acquisition costs. |

Acquired businesses may have liabilities or adverse operating issues that we failed to discover through due diligence prior to the acquisition. In particular, to the extent that prior owners of any acquired businesses or properties failed to comply with or otherwise violated applicable laws or regulations, or failed to fulfill their contractual obligations to clients, us, as the successor owner, may be financially responsible for these violations and failures and may suffer financial or reputational harm or otherwise be adversely affected. Similarly, the acquisition targets may not have as robust internal controls over financial reporting as would be expected of a public company. Acquisitions also frequently result in the recording of goodwill and other intangible assets which are subject to potential impairment in the future that could harm our financial results. We may also become subject to new regulations as a result of an acquisition, including if we acquire a business serving clients in a regulated industry or acquires a business with clients or operations in a country in which we do not already operate. In addition, if we finance acquisitions by issuing equity securities, the interests of existing shareholders may be diluted, which could affect the market price of the shares of us. As a result, if we fail to evaluate properly acquisitions or investments, we may not achieve the anticipated benefits of any such acquisitions, and we may incur costs in excess of what we anticipate. Acquisitions frequently involve benefits related to the integration of operations of the acquired business. The failure to successfully integrate the operations or otherwise to realize any of the anticipated benefits of the acquisition could seriously harm the results of operations of us.

Failure to maintain adequate financial, information technology and management processes and controls could result in material weaknesses which could lead to errors in our financial reporting, which could adversely affect our business.

As a subsidiary of WiMi, a public company, we are subject to the reporting requirements of the Exchange Act, the Sarbanes-Oxley Act and of the rules and regulations of the Nasdaq Global Market. However, failure to maintain adequate financial, information technology and management processes and controls of us could result in material weaknesses which could lead to errors in our financial reporting, which could adversely affect our business. Similarly, as an “emerging growth company,” we would be exempted from the SEC’s internal control reporting requirements. We may lose our emerging growth company status and become subject to the SEC’s internal control over financial reporting management and auditor attestation requirements in the year in which it is deemed to be a large accelerated filer, which would occur once the market value of our common equity held by non-affiliates exceeds $700 million as of the end of the prior fiscal year’s second fiscal quarter. In addition, our current controls and any new controls that it develops may become inadequate because of poor design and changes in our business. Any failure to implement and maintain effective internal controls over financial reporting could adversely affect the results of assessments by our independent registered public accounting firm and their attestation reports.