UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

(Mark One)

OR

for

the fiscal year ended

OR

For the transition period from ________________ to ________________

OR

Date of event requiring this shell company report

Commission

file number:

(Exact name of Registrant as specified in its charter)

(Jurisdiction of incorporation or organization)

People’s

Republic of

(Address of principal executive offices)

Chief Executive Officer

People’s

Republic of

Tel:

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None

(Title of Class)

Indicate the number of outstanding shares of each of the issuer’s classes of capital stock or common stock as of the close of business covered by the annual report.

An

aggregate of 187,376,337 ordinary shares, representing

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

☐

Yes ☒

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

☐

Yes ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

☒

Indicate by check mark whether the registrant has submitted electronically, every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See definition of “large accelerated filer”, “accelerated filer”, and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ☐ | Accelerated filer ☐ | Emerging

growth company |

If

an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant

has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided

pursuant to Section 13(a) of the Exchange Act.

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate

by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness

of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered

public accounting firm that prepared or issued its audit report.

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| ☒ | International Financial Reporting Standards as issued by the International Accounting Standards Board ☐ | Other ☐ |

If “Other” has been checked in response to the previous question indicate by check mark which financial statement item the registrant has elected to follow.

☐ Item 17 ☐ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

☐

Yes

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court.

☐ Yes ☐ No

EBANG INTERNATIONAL HOLDINGS INC.

TABLE OF CONTENTS

i

ii

FORWARD-LOOKING STATEMENTS

This annual report on Form 20-F contains “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). Many of the forward-looking statements contained in this annual report can be identified by the use of forward-looking words such as “anticipate,” “believe,” “could,” “expect,” “should,” “plan,” “intend,” “will,” “estimate” and “potential,” among others.

Forward-looking statements appear in a number of places in this annual report and include, but are not limited to, statements regarding Ebang International Holdings Inc. and its subsidiaries’ (the “Company,” “we,” “us,” or “our”) intent, belief or current expectations. Forward-looking statements are based on our management’s beliefs and assumptions and on information currently available to our management. Such statements are subject to risks and uncertainties, and actual results may differ materially from those expressed or implied in the forward-looking statements due to various factors, including, but not limited to, those identified under the section “Item 3. Key Information—D. Risk factors” in this annual report. These risks and uncertainties include factors relating to:

| ● | our goals and strategies; |

| ● | our business and operating strategies and plans for the development of existing and new businesses, ability to implement such strategies and plans and expected time; |

| ● | our future business development, financial condition and results of operations; |

| ● | expected changes in our revenues, costs or expenditures; |

| ● | our dividend policy; |

| ● | our expectations regarding demand for and market acceptance of our products and services; |

| ● | our expectations regarding our relationships with customers and business partners; |

| ● | the trends in, expected growth in and market size of the blockchain industry and the telecommunications industry in China and globally; |

| ● | our ability to maintain and enhance our market position; |

| ● | our ability to continue to develop new technologies and/or upgrade our existing technologies; |

| ● | developments in, or changes to, laws, regulations, governmental policies, incentives and taxation affecting our operations, in particular in the blockchain industry and the telecommunications industry; |

| ● | relevant governmental policies and regulations relating to our businesses and industry; |

| ● | competitive environment, competitive landscape and potential competitor behavior in our industry; overall industry outlook in our industry; |

| ● | our ability to attract, train and retain executives and other employees; |

| ● | the development of the global financial and capital markets; |

| ● | fluctuations in inflation, interest rates and exchange rates; |

| ● | general business, political, social and economic conditions in China and the overseas markets we have business; | |

| ● | the length and severity of the recent COVID-19 outbreak and its impact on our business and industry; |

| ● | assumptions underlying or related to any of the foregoing; and | |

| ● | other factors discussed under “Item 3. Key Information—D. Risk factors” in this annual report. |

Forward-looking statements speak only as of the date they are made, and we do not undertake any obligation to update them in light of new information or future developments or to release publicly any revisions to these statements in order to reflect later events or circumstances or to reflect the occurrence of unanticipated events.

iii

PART I

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

| A. | Directors and senior management |

Not applicable.

| B. | Advisers |

Not applicable.

| C. | Auditors |

Not applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

| A. | Offer statistics |

Not applicable.

| B. | Method and expected timetable |

Not applicable.

ITEM 3. KEY INFORMATION

| A. | [Reserved] |

| B. | Capitalization and indebtedness |

Not applicable.

| C. | Reasons for the offer and use of proceeds |

Not applicable.

| D. | Risk factors |

Our business, financial condition and results of operations could be materially and adversely affected if any of the risks described below occur. As a result, the market price of our Class A ordinary shares, par value HK$0.001 per share (the “Class A Ordinary Shares”) could decline, and you could lose all or part of your investment. This annual report also contains forward-looking statements that involve risks and uncertainties. See “Forward-Looking Statements.” The risks below are not the only ones facing the Company. Additional risks not currently known to us or that we currently deem immaterial may also adversely affect us. The following risk factors have been grouped as follows:

| a) | Risks relating to conducting business in China; | |

| b) | Risks relating to our cryptocurrency, blockchain and mining related businesses; | |

| c) | Risks relating to our business operations; |

| d) | Risks relating to our securities; and | |

| e) | General risks. |

1

Summary of Key Risks

Our business is subject to numerous risks and uncertainties, discussed in more detail below. These risks include, among others, the following key risks:

| ● | It is now illegal to engage in digital asset transactions including Bitcoin mining operations in China, the ruling of which may adversely affect us |

| ● | Changes in China’s economic, political or social conditions or government policies could have a material adverse effect on our business, results of operations and financial condition |

| ● | Uncertainties in the interpretation and enforcement of PRC laws and regulations could limit the legal protections available to you and us |

| ● | Our corporate structure may restrict our ability to receive dividends from, and transfer funds to, our PRC operating subsidiaries, which could restrict our ability to act in response to changing market conditions in a timely manner |

| ● | We may be subject to the PRC Enterprise Income Tax Law and dividends payable to our foreign investors and gains on the sale of our Class A ordinary shares by our foreign investors may become subject to PRC tax |

| ● | We are subject to risks associated with legal, political or other conditions or developments regarding holding, using or mining of Bitcoins, which could negatively affect our business, results of operations and financial position |

| ● | The current regulatory environment in foreign markets, and any adverse changes in that environment, could have a material adverse impact on our blockchain products business and our cryptocurrency exchange and financial service platform businesses |

| ● | The future development and growth of cryptocurrency is subject to a variety of factors that are difficult to predict and evaluate. If cryptocurrency does not grow as we expect, our business, operating results, and financial condition could be adversely affected |

| ● | Our results of operations have been and are expected to continue to be significantly impacted by the fluctuation of cryptocurrency prices, especially the price of Bitcoin |

| ● | We have derived and may continue to derive a significant portion of our revenues from our Bitcoin mining machines business. If the market for Bitcoin mining machines ceases to exist or diminishes significantly, our business, results of operations and financial condition would be materially and adversely affected |

| ● | The industries in which we operate and which we intend to operate in the future are characterized by constant changes. If we fail to continuously innovate and to provide products that meet the expectations of our customers, we may be unable to attract new customers or retain existing customers, and hence our business and results of operations may be adversely affected |

| ● | We face risks associated with the expansion of our blockchain products business operations overseas and if we are unable to effectively manage such risks, our business growth and profitability may be negatively affected |

| ● | We may not successfully develop, market or launch any future cryptocurrency exchanges or online brokerages or continue operating our existing cryptocurrency exchanges |

2

| ● | Our intellectual property rights are valuable, and any inability to protect them could adversely impact our business, operating results, and financial condition |

| ● | We rely on a limited number of third parties to fabricate our ASIC chips, and IC packaging and testing services |

| ● | We have been involved, and may continue to be involved, in disputes, claims or proceedings arising from our operations or class actions from time to time, which could result in significant liabilities and reputational harm and could materially and adversely affect our business, financial condition and results of operations |

| ● | We have and may increasingly become a target for public scrutiny, including complaints to regulatory agencies, negative media coverage, and malicious allegations, all of which could severely damage our reputation and materially and adversely affect our business and prospects |

| ● | The audit report included in this annual report is prepared by auditor who might not be fully inspected by the Public Company Accounting Oversight Board, and, as such, you may be deprived of the benefits of such inspection |

| ● | Because we do not expect to pay dividends in the foreseeable future, you must rely on price appreciation of our Class A ordinary shares for return on your investment |

| ● | You may face difficulties in protecting your interests, and your ability to protect your rights through U.S. courts may be limited, because we are incorporated under Cayman Islands law and conduct our operations primarily in emerging markets |

| ● | Our dual-class voting structure will limit your ability to influence corporate matters and could discourage others from pursuing any change of control transactions that holders of our Class A ordinary shares may view as beneficial |

| ● | We are a “controlled company” within the meaning of the Nasdaq Rules, and, as a result, can rely on exemptions from certain corporate governance requirements that provide protection to shareholders of other companies |

| ● | We are an emerging growth company within the meaning of the Securities Act and may take advantage of certain reduced reporting requirements |

| ● | We are a foreign private issuer within the meaning of the rules under the Exchange Act, and as such we are exempt from certain provisions applicable to United States domestic public companies |

| ● | We have in the past incurred and continue to incur losses and negative cash flows from operating activities, and we may not achieve or sustain profitability |

Risks Relating to Conducting Business in China

It is now illegal to engage in digital asset transactions including Bitcoin mining operations in China, the ruling of which may adversely affect us

China has now taken harsh regulatory action to ban cryptocurrency mining operations and to severely restrict the right to acquire, own, hold, sell or use these Bitcoin assets or to exchange them for fiat currency. Such restrictions may adversely affect us as the large-scale use of digital assets as a means of exchange is presently confined to certain regions globally. Ongoing and future regulatory actions may impact our ability to continue to operate, and such actions could affect our ability to continue as a going concern or to pursue our business strategy at all, which could have a material adverse effect on our business, prospects or operations.

3

On May 21, 2021, the Financial Stability and Development Committee of the State Council in China proposed to “crack down on Bitcoin mining and trading.” However, it was not until September 15, 2021, as described below, that all digital asset transactions were banned in China. In May 2021, local governments began to issue corresponding measures in succession to respond to the central government, including Xinjiang Changji Hui Autonomous Prefecture Development and Reform Commission issuing a notice on the immediate shutdown of enterprises engaged in cryptocurrency mining on June 9, 2021. On June 18, 2021, according to the public media report - Sichuan Provincial Development and Reform Commission and Sichuan Energy Bureau issued a notice on the shutdown of cryptocurrency mining projects with the deadline of June 25, 2021. On September 3, 2021, the newly issued Notification of Overhauling the Mining Activity of Cryptocurrency (or the Notification No. 1283) banned all new cryptocurrency operations in China and set forth penalties on a going forward basis for all of the PRC. On September 15, 2021, the People's Bank of China, the Office of the Central Cyberspace Affairs Commission, the Supreme People's Court, the Supreme People's Procuratorate, the Ministry of Industry and Information Technology, the Ministry of Public Security, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the China Securities Regulatory Commission, and the State Administration of Foreign Exchange jointly issued the Circular on Further Preventing and Disposing of Risks in Virtual Currency Trading and Speculation (Yin Fa [2021] No.237), which clarified that virtual currency-related business activities in China and the provision of services by an overseas virtual currency exchange to a Chinese resident via the Internet will be considered as illegal financial activities.

In consideration of the PRC government’s attitude and our intentional business plan, we will not conduct any cryptocurrency mining operations or cryptocurrency trading operations in mainland PRC. We do not have any mining operation in the PRC and have halted all mining machine custody business in China in April 2021. While we do not believe the PRC governmental authorities will seek to impose retroactive fines, penalties or sanctions, there can be no assurance they may not seek to do so. Any such regulations, if implemented, will cause us to incur additional compliance costs and have a material adverse effect on our future business operations.

There are risks to foreign investors in Chinese companies

The Chinese government implements the management systems of pre-establishment national treatment and negative list for foreign investment. Pre-establishment national treatment refers to the treatment given to foreign investors and their investments during the investment access stage, which is not lower than that given to their domestic counterparts; negative list for foreign investment refers to special administrative measures for the restricted or prohibited access of foreign investment in specific fields as stipulated by the Chinese government.

Pursuant to the Special Administrative Measures for Foreign Investment Access (2021 Edition), or the 2021 Edition Negative List, issued by The Ministry of Commerce of the PRC (the “MOFCOM”) and the National Development and Reform Commission (the “NDRC”) on December 27, 2021, which came into effect on January 1, 2022, our business does not fall into the Negative List. However, the 2021 Edition Negative List regulates that “Fields not mentioned in the Negative List for Foreign Investment Access shall be subject to administration under the principle of consistency for domestic and foreign investments. The relevant provisions of the Negative List for Market Access shall apply to domestic and foreign investors on a unified basis.”

In addition, based on the Negative List for Market Access (2022) which became effective on March 12, 2022, “the Catalogue for Guidance on Industrial Restructuring shall be included in the Negative List for Market Access”; plus, according to the Decision of the State Council on Promulgating and Implementing the “Temporary Provisions on Promoting Industrial Structure Adjustment,” valid from December 2, 2005, “In principle, the ‘Guidance Catalogue for the Industrial Structure Adjustment “shall apply to various types of enterprises inside China.” “The industries of the eliminated category under the ‘Guidance Catalogue for the Industrial Structure Adjustment’ shall apply to the foreign investment enterprises.” and “Investments are prohibited from being contributed to projects under the eliminated category.” Furthermore, the NDRC released on December 30, 2021 its No. 49 Decree, announcing that the Decision of the National Development and Reform Commission on Amending the Guiding Catalog for Industrial Restructuring (2019 Version) (the “Amended Catalog”). The Amended Catalog added ‘virtual currency mining activities’ to the eliminated category of ‘1. outdated production processing and equipment’ under the original Catalog. Therefore, the foreign investment enterprises are prohibited from virtual currency activities and our mining machine custody business are banned in China as well.

4

Changes in China’s economic, political or social conditions or government policies could have a material adverse effect on our business, results of operations and financial condition

Substantially all of our revenues were and, in a foreseeable future, are expected to be derived in China, and most of our operations, including all of our manufacturing, is conducted in China. Accordingly, our business, prospects, results of operations and financial condition may be influenced to a significant degree by political, economic and social conditions in China generally and by continued economic growth in China as a whole. The Chinese economy differs from the economies of most developed countries in many respects, including the degree of government involvement, level of development, growth rate, control of foreign exchange and allocation of resources. Although the PRC government has implemented measures emphasizing the utilization of market forces for economic reform, the reduction of state ownership of productive assets and the establishment of improved corporate governance in business enterprises, a substantial portion of productive assets in China is still owned by the government. In addition, the Chinese government continues to play a significant role in regulating industry development by imposing industrial policies. The Chinese government also exercises significant control over China’s economic growth through strategically allocating resources, controlling the payment of foreign currency-denominated obligations, setting monetary policy and providing preferential treatment to particular industries or companies.

While the Chinese economy has experienced significant growth over the past decades, growth has been uneven, both geographically and among various sectors of the economy, and the rate of growth has been slowing since 2012. The Chinese government has implemented various measures to encourage economic growth and guide the allocation of resources. Some of these measures may benefit the overall Chinese economy but may have a negative effect on us. For example, our financial condition and results of operations may be adversely affected by government control over capital investments or changes in tax regulations. In addition, in the past the Chinese government has implemented certain measures, including interest rate increases, to control the pace of economic growth. These measures may cause decreased economic activity in China, and since 2012, and in particular in 2020 as a result of COVID-19, China’s economic growth slowed down. Any prolonged slowdown in the Chinese economy may reduce the demand for our products and services and materially and adversely affect our business and results of operations.

Uncertainties in the interpretation and enforcement of PRC laws and regulations could limit the legal protections available to you and us

The PRC legal system is a civil law system based on written statutes. Unlike the common law system, prior court decisions may be cited for reference but have limited precedential value. Our PRC legal system is evolving rapidly, but its current slate of laws may not be sufficient to cover all aspects of the economic activities in China, including such activities that relate to or have an impact on our business. Implementation and interpretations of laws, regulations and rules are not always undertaken in a uniform matter (some of which can change rapidly with little advance notice) and enforcement of these laws, regulations and rules involves uncertainties.

From time to time, we may have to resort to administrative and court proceedings to enforce our legal rights. However, since PRC administrative and court authorities have significant discretion in interpreting and implementing statutory and contractual terms, it may be more difficult to evaluate the outcome of administrative and court proceedings and the level of protection we enjoy than in more developed legal systems. Furthermore, the PRC legal system is based in part on government policies and internal rules (some of which are not published in a timely manner or at all) that may have a retroactive effect. As a result, we may not always be aware of any potential violation of these policies and rules until sometime after the violation. Such uncertainties, including unpredictability towards the scope and effect of our contractual, property (including intellectual property) and procedural rights, and any failure to respond to changes in the regulatory environment in China could materially and adversely affect our business and impede our ability to continue our operations.

In addition, the PRC governmental authorities may intervene or influence our operations at any time, or may exert more control over offerings conducted overseas and/or foreign investment in China-based issuers, which could significantly limit or completely hinder our ability to offer or continue to offer Class A ordinary shares to investors and cause the value of such shares to significant decline or be worthless.

5

We may be subject to recently announced Measures from the Cyberspace Administration of China concerning the collection of data and required to obtain clearance from the Cybersecurity Administration of China

The Cybersecurity Review Measures (2021) was officially released to the public on December 28, 2021, and became effective on February 15, 2022. According to the Cybersecurity Review Measures (2021) (the “Cybersecurity Measures”), to go public abroad, an online platform operator who possesses the personal information of more than 1 million users shall declare to the Office of Cybersecurity Review for cybersecurity review.

Currently, we have not been involved in any investigations on cybersecurity review initiated by the Cybersecurity Administration of China (the “CAC”) or related governmental regulatory authorities, and we have not received any inquiry, notice, warning, or sanction in such respect. As a result, we currently believe we would not be required to obtain clearance from the CAC regarding our listing in the United States under the Cybersecurity Measures because (i) we have not been involved in any investigations on cybersecurity review initiated by the CAC or related governmental regulatory authorities, and we have not received any inquiry, notice, warning, or sanction in such respect, as well as (ii) we have never set an online platform for any user in China and we have not been an online platform operator in China. However, if the CAC requires us to obtain clearance or permissions pursuant to the Cybersecurity Measures or other applicable laws and regulations promulgated by competent authorities in the future, we would file an application with CAC immediately and seek to obtain the clearance or permissions from the CAC as required since we are not willing to be subject to any inquiry, notice, warning, or sanction in such respect which might make a negative impact on our business operations or financial condition. Therefore, compliance with the Cybersecurity Measures, as well as additional laws, regulations and guidelines that the Chinese government promulgates in the future may entail significant expenses and could materially affect our business.

A severe or prolonged downturn in China’s economy and political tensions between the United States and China could materially and adversely affect our business, financial condition and results of operations

The global macroeconomic environment is facing challenges, including the continuing uncertainty regarding the duration and scope of the COVID-19 pandemic, global supply chain disruptions, the recent inflation in the United States and the foreign and domestic government sanctions imposed on Russia as a result of its recent invasion of Ukraine. The growth of China’s economy has slowed down since 2012 and the outbreak of coronavirus COVID-19 in China has resulted in a severe disruption of social and economic activities in China, which has resulted in a further significant slowdown of China’s economy in 2020 and may continue beyond. See “Item 3. Key Information—D. Risk Factors—Risks Relating to Our Business and Industry—The global coronavirus COVID-19 outbreak has caused significant disruptions in our business, which we expect may continue to materially and adversely affect our results of operations and financial condition.” In addition, there is considerable uncertainty over the long-term effects of the expansionary monetary and fiscal policies adopted by the central banks and financial authorities of some of the world’s leading economies, including the United States and China. There have been concerns over unrest and terrorist threats in the Middle East, Europe and Africa, which have resulted in market volatility.

There have been concerns on the relationship between China and other countries, including the surrounding Asian countries and the United States. In particular, there have been heightened tensions in international economic relations between the United States and China. The U.S. government has recently imposed, and has recently proposed to impose additional, new, or higher tariffs on certain products imported from China to penalize China for what the U.S. government characterizes as unfair trade practices. China has responded by imposing, and proposing to impose additional, new, or higher tariffs on certain products imported from the United States. Following mutual retaliatory actions for months, on January 15, 2020, the United States and China entered into the Economic and Trade Agreement Between the United States of America and the People’s Republic of China as a phase one trade deal, effective on February 14, 2020. It remains unclear what impact these tariff negotiations may have or what further actions the two countries may take. Moreover, political tensions between the United States and China have escalated as a result of the COVID-19 outbreak and the PRC National People’s Congress’ decision on Hong Kong national security legislation. Rising political tensions could reduce levels of trades, investments, technological exchanges and other economic activities between the two major economies, which would have a material adverse effect on global economic conditions and the stability of global financial markets. Any of the circumstances would have a material adverse effect on our business, prospects, financial condition and results of operations. See “Item 3. Key Information—D. Risk Factors— Risks Relating to Our Cryptocurrency, Blockchain and Mining Related Businesses—We plan to increase our export of mining machines to the United States and the European Union in the future, which may be subject to high tariff rates resulting from protectionism trade policies, and as a result, our future sales volumes, profitability and results of operations will be materially and adversely affected.”

6

Furthermore, as part of a continued regulatory focus in the United States on access to audit and other information currently protected by national law, in particular China’s, on December 18, 2020, U.S. President Donald J. Trump signed the Holding Foreign Companies Accountable Act into law, which requires the SEC to propose rules within 90 days after its enactment to prohibit securities of any registrant from being listed on any of the U.S. securities exchanges or traded “over the counter” if the auditor of the registrant’s financial statements is not subject to PCAOB inspection for three consecutive years after the law becomes effective. The Holding Foreign Companies Accountable Act and any proposed SEC rules may have a material and adverse impact on the stock performance of China-based companies listed in the United States. In addition, the recent market panics over the global outbreak of COVID-19 materially and negatively affected the global financial markets in March 2020, which may cause potential slowdown of the global economy. Economic conditions in China are sensitive to global economic conditions, as well as changes in domestic economic and political policies and the expected or perceived overall economic growth rate in China. Any severe or prolonged slowdown in the global or Chinese economy and the political tensions between the United States and China may materially and adversely affect our business, financial condition, results of operations and prospects.

Increases in labor costs and enforcement of stricter labor laws and regulations in the PRC and our additional payments of statutory employee benefits may adversely affect our business and profitability

The average wage in China has increased in recent years and is expected to continue to grow. The average wage level for our employees has also increased in recent years. We expect that our labor costs, including wages and employee benefits, will continue to increase. Unless we are able to pass on these increased labor costs to our customers, our profitability and results of operations may be materially and adversely affected.

In addition, we have been subject to stricter regulatory requirements in terms of entering into labor contracts with our employees and paying various statutory employee benefits, including pensions, housing funds, medical insurance, work-related injury insurance, unemployment insurance and maternity insurance to designated government agencies for the benefit of our employees. Pursuant to the PRC Labor Contract Law and its implementation rules, employers are subject to stricter requirements in terms of signing labor contracts, minimum wages, paying remuneration, determining the term of employee’s probation and unilaterally terminating labor contracts. In the event that we decide to terminate some of our employees or otherwise change our employment or labor practices, the PRC Labor Contract Law and its implementation rules may limit our ability to effect those changes in a desirable or cost-effective manner, which could adversely affect our business and results of operations.

Pursuant to PRC laws and regulations, companies registered and operating in China are required to apply for social insurance registration and housing fund deposit registration within 30 days of their establishment and to pay for their employees different social insurance including pension insurance, medical insurance, work-related injury insurance, unemployment insurance and maternity insurance to the extent required by law. We have not fully paid social insurance and housing provident funds for all of our employees due to inconsistency in implementation or interpretation of the relevant PRC laws and regulations among government authorities in the PRC and, in some cases, voluntary decisions by the relevant employees. Recently, as the PRC government enhanced its enforcement measures relating to social insurance collection, we may be required to make up the contributions for our employees, and may be further subjected to late fees payment and administrative fines, which may materially and adversely affect our financial condition and results of operations. As the interpretation and implementation of labor-related laws and regulations are still evolving, we cannot assure you that our current employment practices do not and will not violate labor-related laws and regulations in China, which may subject us to labor disputes or government investigations. In addition, we may incur additional expenses in order to comply with such laws and regulations, which may adversely affect our business and profitability.

We may be adversely affected by inflation or labor shortage in China

In recent years, the PRC economy has experienced periods of rapid expansion and highly fluctuating rates of inflation. According to the National Bureau of Statistics of China, the year-over-year percent changes in the consumer price index for December 2019, 2020 and 2021 were increases of 4.5%, 0.2% and 1.5%, respectively. Although we have not been materially affected by inflation in the past, we may be affected if PRC experiences higher rates of inflation in the future. It is uncertain when the general price level may increase or decrease sharply in the future. Moreover, the significant economic growth in China has resulted in a general increase in labor costs and shortage of low-cost labor. Inflation may cause our production cost to continue to increase. If we are unable to pass on the increase in production cost to our customers, we may suffer a decrease in profitability and a loss of customers and our results of operations could be materially and adversely affected.

7

Our corporate structure may restrict our ability to receive dividends from, and transfer funds to, our PRC operating subsidiaries, which could restrict our ability to act in response to changing market conditions in a timely manner

We are a Cayman Islands holding company and a certain portion of our operations are conducted through our operating subsidiaries. The ability of our operating subsidiaries to make dividend and other payments to us may be restricted by factors that include changes in applicable foreign exchange and other laws and regulations.

In particular, under the PRC law, each of our PRC operating subsidiaries may only pay dividends after 10% of its net profit has been set aside as reserve funds, unless such reserves have reached at least 50% of its registered capital. In addition, the profit available for distribution from our PRC operating subsidiaries is determined in accordance with generally accepted accounting principles in the PRC. This calculation may differ if it were performed in accordance with U.S. GAAP. As a result, we may not have sufficient distributions from our PRC operating subsidiaries to enable necessary profit distributions to our shareholders in the future, which would be based upon our financial statements prepared under U.S. GAAP.

Distributions by our PRC operating subsidiaries to us other than as dividends may be subject to governmental approval and taxation. Any transfer of funds from our company to our PRC operating subsidiaries, either as a shareholder loan or as an increase in registered capital, is subject to registration or approval of PRC governmental authorities, including the relevant administration of foreign exchange and/or the relevant examining and approval authority. These limitations on the free flow of funds between us and our PRC subsidiaries could restrict our ability to act in response to changing market conditions in a timely manner.

We may be subject to EIT on our worldwide income if our company or any of our subsidiaries were considered a PRC “resident enterprise” under the PRC Enterprise Income Tax Law, or the EIT Law

Under the EIT Law and its implementation rules, enterprises established outside of the PRC with “de facto management bodies” within the PRC are considered a “resident enterprise” and will be subject to EIT at a rate of 25% on their worldwide income. The implementation rules under EIT define the term “de facto management bodies” as “establishments that carry out substantial and overall management and control over the production, operation, personnel, accounting, properties, etc. of an enterprise.” The State Administration of Taxation of the PRC, or the SAT promulgated the Notice Regarding the Determination of Chinese-Controlled Offshore Incorporated Enterprises as PRC Tax Resident Enterprises on the Basis of De Facto Management Bodies, or Circular 82, on April 22, 2009, which provides certain specific criteria for determining whether the “de facto management body” of a Chinese-controlled offshore incorporated enterprise is located in the PRC. On July 27, 2011, the SAT issued the Measures for Administration of Income Tax of Chinese Controlled Resident Enterprises Incorporated Overseas (Trial), or Circular 45, to supplement Circular 82 and other tax laws and regulations. Circular 45 clarifies certain issues relating to resident status determination. Although Circular 82 and Circular 45 apply only to offshore enterprises controlled by PRC enterprises or PRC group companies and not those controlled by PRC individuals or foreigners, the determining criteria set forth in Circular 82 and Circular 45 may reflect the SAT’s general position on how the “de facto management body” test should be applied in determining the tax resident status of offshore enterprises, regardless of whether they are controlled by PRC enterprises or individuals or foreign enterprises. A substantial majority of our senior management team is located in China. If our company or any of our subsidiaries were considered to be a PRC “resident enterprise,” we would be subject to EIT at a rate of 25% on our worldwide income, which could materially reduce our net income.

8

Dividends payable to our foreign investors and gains on the sale of our Class A ordinary shares by our foreign investors may become subject to PRC tax

Under the EIT Law and its implementation regulations issued by the State Council, a 10% PRC withholding tax is applicable to dividends payable to investors that are non-resident enterprises, which do not have an establishment or place of business in the PRC or which have such establishment or place of business but the dividends are not effectively connected with such establishment or place of business, to the extent such dividends are derived from sources within the PRC. Similarly, any gain realized on the transfer of our Class A ordinary shares by such investors is also subject to PRC tax at a current rate of 10%, subject to any reduction or exemption set forth in applicable tax treaties or under applicable tax arrangements between jurisdictions, if such gain is regarded as income derived from sources within the PRC. If we are deemed a PRC resident enterprise, dividends paid on our Class A ordinary shares, and any gain realized from the transfer of our Class A ordinary shares, would be treated as income derived from sources within the PRC and would as a result be subject to PRC taxation. Furthermore, if we are deemed a PRC resident enterprise, dividends payable to individual investors who are non-PRC residents and any gain realized on the transfer of our Class A ordinary shares by such investors may be subject to PRC tax at a current rate of 20%, subject to any reduction or exemption set forth in applicable tax treaties or under applicable tax arrangements between jurisdictions. If we or any of our subsidiaries established outside China are considered a PRC resident enterprise, it is unclear whether holders of our Class A ordinary shares would be able to claim the benefit of income tax treaties or agreements entered into between China and other countries or areas. If dividends payable to our non-PRC investors, or gains from the transfer of our Class A ordinary shares by such investors, are deemed as income derived from sources within the PRC and thus are subject to PRC tax, the value of your investment in our Class A ordinary shares may decline significantly.

PRC regulations relating to investments in offshore companies by PRC residents may subject our PRC-resident beneficial owners or our PRC subsidiaries to liability or penalties, limit our ability to inject capital into our PRC subsidiaries or limit our PRC subsidiaries’ ability to increase their registered capital or distribute profits

In July 2014, the State Administration of Foreign Exchange of the PRC, or SAFE, promulgated the Circular on Relevant Issues Concerning Foreign Exchange Control on Domestic Residents’ Offshore Investment and Financing and Roundtrip Investment through Special Purpose Vehicles, or SAFE Circular 37, which replaces the previous SAFE Circular 75. SAFE Circular 37 requires PRC residents, including PRC individuals and PRC corporate entities, to register with SAFE or its local branches in connection with their direct or indirect offshore investment activities. SAFE Circular 37 is applicable to our shareholders who are PRC residents and may be applicable to any offshore acquisitions that we may make in the future.

Under SAFE Circular 37, PRC residents who make, or have prior to the implementation of SAFE Circular 37 made, direct or indirect investments in offshore special purpose vehicles, or SPVs, are required to register such investments with SAFE or its local branches. In addition, any PRC resident who is a direct or indirect shareholder of an SPV, is required to update its registration with the local branch of SAFE with respect to that SPV, to reflect any material change. Moreover, any subsidiary of such SPV in China is required to urge the PRC resident shareholders to update their registration with the local branch of SAFE to reflect any material change. If any PRC resident shareholder of such SPV fails to make the required registration or to update the registration, the subsidiary of such SPV in China may be prohibited from distributing its profits or the proceeds from any capital reduction, share transfer or liquidation to the SPV, and the SPV may also be prohibited from making additional capital contributions into its subsidiaries in China. In February 2015, SAFE promulgated a Notice on Further Simplifying and Improving Foreign Exchange Administration Policy on Direct Investment, or SAFE Notice 13. Under SAFE Notice 13, applications for foreign exchange registration of inbound foreign direct investments and outbound direct investments, including those required under SAFE Circular 37, must be filed with qualified banks instead of SAFE. Qualified banks should examine the applications and accept registrations under the supervision of SAFE. We have used commercially reasonable efforts to notify PRC residents or entities who directly or indirectly hold shares in our Cayman Islands holding company and who are known to us as being PRC residents to complete the foreign exchange registrations. However, we may not be informed of the identities of all the PRC residents or entities holding direct or indirect interest in our company, nor can we compel our beneficial owners to comply with SAFE registration requirements. We cannot assure you that all other shareholders or beneficial owners of ours who are PRC residents or entities have complied with, and will in the future make, obtain or update any applicable registrations or approvals required by, SAFE regulations. Failure by such shareholders or beneficial owners to comply with SAFE regulations, or failure by us to amend the foreign exchange registrations of our PRC subsidiaries, could subject us to fines or legal sanctions, restrict our overseas or cross-border investment activities, limit our PRC subsidiaries’ ability to make distributions or pay dividends to us or affect our ownership structure, which could adversely affect our business and prospects.

9

Furthermore, as these foreign exchange and outbound investment related regulations are relatively new and their interpretation and implementation has been constantly evolving, it is unclear how these regulations, and any future regulation concerning offshore or cross-border investments and transactions, will be interpreted, amended and implemented by the relevant government authorities. For example, we may be subject to a more stringent review and approval process with respect to our foreign exchange activities, such as remittance of dividends and foreign-currency-denominated borrowings, which may adversely affect our financial condition and results of operations. We cannot assure you that we have complied or will be able to comply with all applicable foreign exchange and outbound investment related regulations. In addition, if we decide to acquire a PRC domestic company, we cannot assure you that we or the owners of such company, as the case may be, will be able to obtain the necessary approvals or complete the necessary filings and registrations required by the foreign exchange regulations. This may restrict our ability to implement our acquisition strategy and could adversely affect our business and prospects.

We and our shareholders face uncertainties with respect to indirect transfers of equity interests in PRC resident enterprises or other assets attributed to a Chinese establishment of a non-Chinese company, or immovable properties located in China owned by non-Chinese companies

In February 2015, SAT issued a Public Notice Regarding Certain Corporate Income Tax Matters on Indirect Transfer of Properties by Non-Tax Resident Enterprises, or SAT Public Notice 7. SAT Public Notice 7 extends its tax jurisdiction to transactions involving transfer of other taxable assets through offshore transfer of a foreign intermediate holding company. In addition, SAT Public Notice 7 provides clear criteria for assessment of reasonable commercial purposes and has introduced safe harbors for internal group restructurings and the purchase and sale of equity through a public securities market. SAT Public Notice 7 also brings challenges to both foreign transferor and transferee (or other person who is obligated to pay for the transfer) of taxable assets. In October 2017, SAT issued the Announcement of the State Administration of Taxation on Issues Concerning the Withholding of Non-resident Enterprise Income Tax at Source, or SAT Bulletin 37, which came into effect on December 1, 2017. The SAT Bulletin 37 further clarifies the practice and procedure of the withholding of non-resident EIT. Where a non-resident enterprise transfers taxable assets indirectly by disposing of the equity interests of an overseas holding company, which is an indirect transfer, the non-resident enterprise as either transferor or transferee, or the PRC entity that directly owns the taxable assets, may report such Indirect Transfer to the relevant tax authority. Using a “substance over form” principle, the PRC tax authority may disregard the existence of the overseas holding company if it lacks a reasonable commercial purpose and was established for the purpose of reducing, avoiding or deferring PRC tax. As a result, gains derived from such indirect transfer other than transfer of shares acquired and sold on public markets may be subject to EIT, and the transferee or other person who is obligated to pay for the transfer is obligated to withhold the applicable taxes, currently at a rate of 10%. Both the transferor and the transferee may be subject to penalties under PRC tax laws if the transferee fails to withhold the taxes and the transferor fails to pay the taxes.

We face uncertainties as to the reporting and other implications of certain past and future transactions that involve PRC taxable assets, such as offshore restructuring, sale of the shares in our offshore subsidiaries and investments. Our company may be subject to filing obligations or taxed if our company is transferor in such transactions and may be subject to withholding obligations if our company is transferee in such transactions, under SAT Public Notice 7 or SAT Bulletin 37, or both.

We are subject to PRC restrictions on currency exchange

Some of our revenues and expenses are denominated in Renminbi. The Renminbi is currently convertible under the “current account,” which includes dividends, trade and service-related foreign exchange transactions, but not under the “capital account,” which includes foreign direct investment and loans, including loans we may secure from our onshore subsidiaries. Currently, certain of our PRC subsidiaries may purchase foreign currency for settlement of “current account transactions,” including payment of dividends to us, without the approval of the SAFE by complying with certain procedural requirements. However, the relevant PRC governmental authorities may limit or eliminate our ability to purchase foreign currencies in the future for current account transactions. Foreign exchange transactions under the capital account remain subject to limitations and require approvals from, or registration with, the SAFE and other relevant PRC governmental authorities. Since a part of our future net income and cash flow will be denominated in Renminbi, any existing and future restrictions on currency exchange may limit our ability to utilize cash generated in Renminbi to fund our business activities outside of the PRC or pay dividends in foreign currencies to our shareholders, including holders of our Class A ordinary shares, and may limit our ability to obtain foreign currency through debt or equity financing for our subsidiaries.

10

If the custodians or authorized users of our controlling non-tangible assets, including chops and seals, fail to fulfill their responsibilities, or misappropriate or misuse these assets, our business and operations may be materially and adversely affected

Under PRC law, legal documents for corporate transactions, including agreements and contracts such as the leases and sales contracts that our business relies on, are executed using the chop or seal of the signing entity or with the signature of a legal representative whose designation is registered and filed with the relevant local branch of the market supervision administration.

In order to maintain the physical security of our chops and the chops of our PRC entities, we generally store these items in secured locations accessible only by the authorized personnel of each of our PRC subsidiary and consolidated entities. Although we monitor such authorized personnel, there is no assurance such procedures will prevent all instances of abuse or negligence. Accordingly, if any of our authorized personnel misuse or misappropriate our corporate chops or seals, we could encounter difficulties in maintaining control over the relevant entities and experience significant disruption to our operations. If a designated legal representative obtains control of the chops in an effort to obtain control over any of our PRC subsidiary or consolidated entities, we, our PRC subsidiaries or consolidated entities would need to pass a new shareholder or board resolution to designate a new legal representative and we would need to take legal action to seek the return of the chops, apply for new chops with the relevant authorities, or otherwise seek legal redress for the violation of the representative’s fiduciary duties to us, which could involve significant time and resources and divert management attention away from our regular business. In addition, the affected entity may not be able to recover corporate assets that are sold or transferred out of our control in the event of such a misappropriation if a transferee relies on the apparent authority of the representative and acts in good faith.

The M&A Rules and certain other PRC regulations establish complex procedures for some acquisitions of Chinese companies by foreign investors, which could make it more difficult for us to pursue growth through acquisitions in China

The Regulations on Mergers and Acquisitions of Domestic Companies by Foreign Investors, or the M&A Rules, adopted by six PRC regulatory agencies in August 2006 and amended in June 2009, and some other regulations and rules concerning mergers and acquisitions established additional procedures and requirements that could make merger and acquisition activities by foreign investors more time consuming and complex, including requirements in some instances that shall obtained an approval from the Ministry of Commerce, or the MOFCOM, in advance of any change-of-control transaction in which a foreign investor takes control of a PRC domestic enterprise. Moreover, the Anti-Monopoly Law requires that the MOFCOM shall be notified in advance of any concentration of undertaking if certain thresholds are triggered. In addition, the Safety Review System for Merger and Acquisition of Domestic Companies by Foreign Investors issued by the MOFCOM that became effective in September 2011 specify that mergers and acquisitions by foreign investors that raise “national defense and security” concerns and mergers and acquisitions through which foreign investors may acquire de facto control over domestic enterprises that raise “national security” concerns are subject to strict review by the MOFCOM, and the rules prohibit any activities attempting to bypass a security review, including by structuring the transaction through a proxy or contractual control arrangement. In the future, we may grow our business by acquiring complementary businesses. Complying with the requirements of the above-mentioned regulations and other relevant rules to complete such transactions could be time consuming, and any required approval processes, including obtaining approval from the MOFCOM or its local counterparts may delay or inhibit our ability to complete such transactions, which could affect our ability to expand our business or maintain our market share.

11

We face regulatory uncertainties in China that could restrict our ability to grant share incentive awards to our employees or consultants who are PRC citizens

Pursuant to the Notices on Issues concerning the Foreign Exchange Administration for Domestic Individuals Participating in a Stock Incentive Plan of an Overseas Publicly-Listed Company issued by SAFE on February 15, 2012, or Circular 7, a qualified PRC agent (which could be the PRC subsidiary of the overseas-listed company) is required to file, on behalf of “domestic individuals” (both PRC residents and non-PRC residents who reside in China for a continuous period of not less than one year, excluding the foreign diplomatic personnel and representatives of international organizations) who are granted shares or share options by the overseas-listed company according to its share incentive plan, an application with SAFE to conduct SAFE registration with respect to such share incentive plan, and obtain approval for an annual allowance with respect to the purchase of foreign exchange in connection with the share purchase or share option exercise. Such PRC individuals’ foreign exchange income received from the sale of shares and dividends distributed by the overseas listed company and any other income shall be fully remitted into a collective foreign currency account in China, which is opened and managed by the PRC domestic agent before distribution to such individuals. In addition, such domestic individuals must also retain an overseas entrusted institution to handle matters in connection with their exercise of share options and their purchase and sale of shares. The PRC domestic agent also needs to update registration with SAFE within three months after the overseas-listed company materially changes its share incentive plan or make any new share incentive plans.

We have adopted our Amended and Restated 2020 Share Incentive Plan (the “2020 Plan”), effective upon the completion of our initial public offering, and our 2021 Share Incentive Plan (the “2021 Plan”), effective upon shareholder approval at the 2021 annual general meeting of shareholders held on December 15, 2021. As of the date of this annual report, we have granted 6,550,000 restricted share awards under the 2020 Plan and we did not grant any awards under the 2021 Plan. We may grant share incentive awards under both or either plan in the future. When we do, from time to time, we need to apply for or update our registration with SAFE or its local branches on behalf of our employees or consultants who receive options or other equity-based incentive grants under the 2020 Plan, 2021 Plan or future share incentive plans we may adopt or material changes in such plan(s). However, we may not always be able to make applications or update our registration on behalf of our employees or consultants who hold any type of share incentive awards in compliance with Circular 7, nor can we ensure you that such applications or update of registration will be successful. If we or the participants of our share incentive plan(s) who are PRC citizens fail to comply with Circular 7, we and/or such participants of our share incentive plan(s) may be subject to fines and legal sanctions, there may be additional restrictions on the ability of such participants to exercise their share options or remit proceeds gained from sale of their shares into China, and we may be prevented from further granting share incentive awards under our share incentive plan(s) to our employees or consultants who are PRC citizens.

Our Hong Kong subsidiaries could become subject to the direct oversight of the PRC government at any time if the National laws of mainland China are applied to Hong Kong

The national laws of the PRC (the “National Laws”), including, but not limited to (i) the Cybersecurity Review Measures which became effective on February 15, 2022; and (ii) approval by the Chinese Securities Regulatory Commission (“CSRC”) or any other Chinese regulatory authority to approve or permit our offering of securities in the U.S., do not currently apply to our Hong Kong subsidiaries, except for those set forth below. However, due to the uncertainty of the PRC legal system and changes in laws, regulations or policies, including how these laws, regulations or policies would be interpreted or implemented, and the national laws applicable in Hong Kong, the Basic Law might be revised in the future.

Pursuant to Article 18 of the Basic Law of the Hong Kong Special Administrative Region of the PRC (the “Basic Law”), “The laws in force in the Hong Kong Special Administrative Region shall be the Basic Law, the laws previously in force in Hong Kong as provided for in Article 8 of this Law, and the laws enacted by the legislature of the Region. National laws shall not be applied in the Hong Kong Special Administrative Region except for those listed in Annex III to the Basic Law. The laws listed therein shall be applied locally by way of promulgation or legislation by the Region. Also, regarding the Annex III and several Instruments of the Basic Law, National Laws, which have applied in Hong Kong until now are as following:

Resolution on the Capital, Calendar, National Anthem and National Flag of the PRC; Resolution on the National Day of the PRC; Declaration of the Government of the PRC on the Territorial Sea; Nationality Law of the PRC; Regulations of the PRC Concerning Diplomatic Privileges and Immunities; Law of the PRC on the National Flag; Regulations of the PRC Concerning Consular Privileges and Immunities; Law of the PRC on the National Emblem; Law of the PRC on the Territorial Sea and the Contiguous Zone; Law of the PRC on Garrisoning the Hong Kong Special Administrative Region; Law of the PRC on the Exclusive Economic Zone and the Continental Shelf; Law of the PRC on Judicial Immunity from Compulsory Measures Concerning the Property of Foreign Central Banks; and Law of the PRC on the National Anthem; Law of the PRC on Safeguarding National Security in the Hong Kong Special Administrative Region.

12

The CSRC released, on December 24, 2021, the Provisions of the State Council on the Administration of Domestic Companies Offering Securities for Overseas Listing (Revision Draft for Comments) (the “Provisions”) and the Administrative Measures for the Filing of Domestic Companies Seeking Overseas Securities Offering and Listing (the “Measures”) for public comment. According to the Provisions and Measures, “Domestic companies that seek to offer and list securities in overseas markets shall fulfill the filing procedure with the securities regulatory agency under the State Council and report relevant information;” and “An overseas offering and listing is prohibited under any of the following circumstances: (1) if the intended securities offering and listing falls under specific clauses in national laws and regulations and relevant provisions prohibiting such financing activities.” Furthermore, the Cybersecurity Review Measures (2021) was officially released to the public on December 28, 2021 and became effective on February 15, 2022. According to the Cybersecurity Review Measures (2021), “To go public abroad, an online platform operator who possesses the personal information of more than 1 million users shall declare to the Office of Cybersecurity Review for cybersecurity review.”

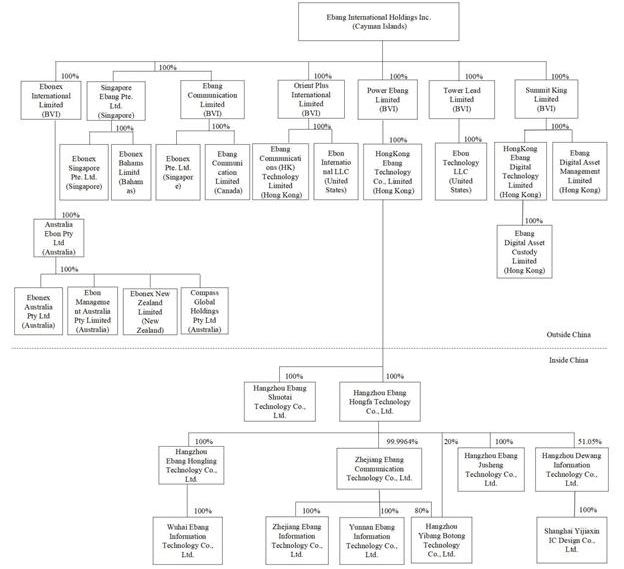

As of the date of this annual report, we have two wholly-owned subsidiaries and operating entities established in Hong Kong, Ebang Communications (HK) Technology Limited, or HK Ebang Communications, principally for the trading of blockchain chips; and HongKong Ebang Digital Technology Limited, or HK Ebang Digital, principally for cryptocurrency exchange businesses. Neither entities have established any subsidiary or branch in PRC or have committed any business operations in PRC. For additional information, see “Item 4. Information of the Company – C. Organizational Structure.”

Based on the aforementioned Basic Law, our Hong Kong subsidiaries are not subject to the Cybersecurity Measures and the Provisions and the Measures. However, due to the uncertainty of the PRC legal system and changes in laws, regulations or policies, including how these laws, regulations or policies would be interpreted or implemented, the national laws applicable in Hong Kong in the Basic Law might be revised in the future. Therefore, we cannot assure you that we will not be affected by the foregoing or relevant laws, regulations or policies in the future. If there are any changes to the foregoing laws, regulations and policies, or if any new laws, regulations, and policies, etc., would be published, we would manage to comply with the changed laws, regulations and policies. However, we could not guarantee that the relevant laws, regulations, or policies would not be applied retroactively, so we might face penalties, and our reputation and results of operations could be materially and adversely affected.

Risks Relating to Our Cryptocurrency, Blockchain and Mining Related Businesses

We are subject to risks associated with legal, political or other conditions or developments regarding holding, using or mining of Bitcoins, which could negatively affect our business, results of operations and financial position

Our customers are based globally. As such, changes in government policies, taxes, general economic and fiscal conditions, as well as political, diplomatic or social events, expose us to financial and business risks. In particular, changes in domestic or overseas policies and laws regarding holding, using and/or mining of Bitcoins could result in an adverse effect on our business operations and results of operations. Moreover, if any domestic or international jurisdiction where we operate or sell our Bitcoin mining machines prohibits or restricts Bitcoin mining activities, we may face legal and other liabilities and will experience a material loss of revenue.

There are significant uncertainties regarding future regulations pertaining to the holding, using or mining of Bitcoins, which may adversely affect our results of operations. While Bitcoin has gradually gained more market acceptance and attention, it is anonymous and may be used for black market transactions, money laundering, illegal activities or tax evasion. As a result, governments may seek to regulate, restrict, control or ban the holding, use mining holding of Bitcoins. In addition, due to compliance risk, cost, government regulation or public pressure, banks and financial institutions may not provide banking services, or may cut off services, to businesses that provide cryptocurrency-related services or that accept cryptocurrencies, including Bitcoins, as payment. Our existing policies and procedures for the detection and prevention of money laundering and terrorism-funding activities through our business activities have only been adopted in recent years and may not completely eliminate instances in which we or our products may be used by other parties to engage in money laundering and other illegal or improper activities. We cannot assure you that there will not be a failure in detecting money laundering or other illegal or improper activities which may adversely affect our reputation, business, financial condition and results of operations.

13

With advances in technology, cryptocurrencies are likely to undergo significant changes in the future. It remains uncertain whether Bitcoin will be able to cope with, or benefit from, those changes. In addition, as Bitcoin mining employs sophisticated and high computing power devices that need to consume large amounts of electricity to operate, future developments in the regulation of energy consumption, including possible restrictions on energy usage in the jurisdictions where we sell our products, may also affect our business operations and the demand for our current Bitcoin mining machines. There has been negative public reaction to the environmental impact of Bitcoin mining, particularly the large consumption of electricity, and governments of various jurisdictions have responded. For example, pursuant to the Notification No. 1283, new virtual currency mining projects are forbidden to apply for electricity facility installation, and the electricity facility installation shall be strictly reviewed. It is not permissible to supply power to virtual currency mining enterprises in any name, and all applications for electricity facility installation projects in progress shall be stopped. In the United States, certain local governments of the state of Washington have discussed measures to address the environmental impacts of Bitcoin-related operations, such as the high electricity consumption of Bitcoin mining activities. Any legislation and increased regulation regarding climate change could impose significant costs on us and our suppliers, including costs related to increased energy requirements, capital equipment, environmental monitoring and reporting, and other costs to comply with such regulations. Specifically, imposition of a carbon tax or other regulatory fee in a jurisdiction where we operate or on electricity that we purchase could result in substantially higher energy costs, and due to the significant amount of electrical power required to operate cryptocurrency mining machines, could in turn put our facilities at a competitive disadvantage. Any future climate change regulations could also negatively impact our ability to compete with companies situated in areas not subject to such limitations. Given the political significance and uncertainty around the impact of climate change and how it should be addressed, we cannot predict how legislation and regulation will affect our financial condition, operating performance and ability to compete. Furthermore, even without such regulation, increased awareness and any adverse publicity in the global marketplace about potential impacts on climate change by us or other companies in our industry could harm our reputation. Any of the foregoing could have a material adverse effect on our financial position, results of operations and cash flows.

The current regulatory environment in foreign markets, and any adverse changes in that environment, could have a material adverse impact on our blockchain products business and our cryptocurrency exchange and financial service platform businesses

We currently export our products to various overseas markets, have established two cryptocurrency trading exchanges, and we intend to further develop our business and operations in overseas jurisdictions in the future to provide cryptocurrency trading related services to cryptocurrency communities, including, but not limited to, Singapore, the Bahamas, Hong Kong, New Zealand and the United States. Our blockchain products business and planned cryptocurrency and financial services platform businesses could therefore be significantly affected by regulatory developments in jurisdictions outside the PRC, including the United States and other jurisdictions.

Certain aspects of business are subject to extensive laws, rules, regulations, policies and legal and regulatory guidance, including those governing securities, commodities, cryptocurrency asset custody, exchange and transfer, data governance, data protection, cybersecurity and tax. Many of these legal and regulatory regimes were adopted prior to the advent of the Internet, mobile technologies, cryptocurrency assets and related technologies. As a result, they do not contemplate or address unique issues associated with the crypto economy, are subject to significant uncertainty, and vary widely across federal, state and local laws, including the PRC and international jurisdictions. These legal and regulatory regimes, including the laws, rules and regulations thereunder, evolve frequently and may be modified, interpreted and applied in an inconsistent manner from one jurisdiction to another, and may conflict with one another. Moreover, the complexity and evolving nature of certain aspects of our business and the significant uncertainty surrounding the regulation of the crypto economy require us to exercise our judgement as to whether certain laws, rules and regulations apply to us, and it is possible that governmental bodies and regulators may disagree with our conclusions. In addition, governmental authorities that oversee certain aspects of the cryptocurrency markets, including those in the United States and other jurisdictions, have taken actions based on current laws and regulations, and are likely to continue to issue new laws, rules and regulations governing the cryptocurrency industry in which we currently operate and may operate in the future. As a result, and as discussed further in “- We are subject to risks associated with legal, political or other conditions or developments regarding holding, using or mining of Bitcoins, which could negatively affect our business, results of operations and financial position,” existing and future regulations affecting the mining, holding, using, or transferring of cryptocurrencies may adversely affect our future business operations and results of operations, could subject us to significant fines and other regulatory consequences, and could result in our or our customers’ liability for activities conducted by our customers.

14

As described under “Item 4. Information on the Company—B. Business Overview—Regulation—Regulatory Overview of United States,” United States federal and state securities laws may specifically limit our ability and the ability of our customers to use our blockchain and telecommunications products where these operations are conducted in connection with cryptocurrencies that are considered “securities” for purposes of United States laws. We have designed new chips for mining cryptocurrencies other than Bitcoin, and the likely status of these cryptocurrencies as securities could limit distributions, transfers, or other actions involving such cryptocurrencies, including mining, in the United States. For example, the distribution of cryptocurrencies to miners through the mining process could be deemed to involve an illegal offering or distribution of securities subject to United States federal or state laws. In addition, miners on cryptocurrency networks could, under certain circumstances, be viewed as statutory underwriters or as “brokers” subject to regulation under the Securities Exchange Act of 1934. This could require us or our customers to change, limit, or cease their mining operations, register as broker-dealers and comply with applicable laws, or be subject to penalties, including fines, or other regulatory consequences. In addition, we could face liability for facilitating their illegal activities.