UNITED STATES SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

(Mark One)

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||||||||

For the Fiscal Year Ended December 31, 2021

OR

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||||||||

Commission file number 1-39361

(Exact name of registrant as specified in its charter)

| (State of incorporation) | (I.R.S. Employer Identification No.) | |||||||

| (Address of principal executive offices) | (Zip Code) | |||||||

(904 ) 648-6350

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class | Trading Symbol | Name of Each Exchange on Which Registered | ||||||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| ☒ | Accelerated filer | ☐ | Non-accelerated filer | ☐ | |||||||||||||

| Smaller reporting company | Emerging growth company | ||||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

The aggregate market value of the shares of Dun & Bradstreet Holdings, Inc. common stock held by non-affiliates of the registrant as of June 30, 2021 was $3,665,506,111 based on the closing price of $21.37 as reported by the New York Stock Exchange.

There were 431,165,887 shares outstanding of the Registrant's common stock as of February 18, 2022.

The information in Part III hereof is incorporated by reference to certain information from the registrant's definitive proxy statement for the 2022 annual meeting of shareholders. The registrant intends to file the proxy statement within 120 days after the close of the fiscal year that is the subject of this Report.

DUN & BRADSTREET HOLDINGS, INC.

FORM 10-K

TABLE OF CONTENTS

| Page | ||||||||

| Item 1. | ||||||||

| Item 1A. | ||||||||

| Item 2. | ||||||||

| Item 3. | ||||||||

| Item 4. | ||||||||

| Item 5. | ||||||||

| Item 6. | ||||||||

| Item 7. | ||||||||

| Item 7A. | ||||||||

| Item 8. | ||||||||

| Item 9. | ||||||||

| Item 9A. | ||||||||

| Item 9B. | ||||||||

| Item 10. | ||||||||

| Item 11. | ||||||||

| Item 12. | ||||||||

| Item 13. | ||||||||

| Item 14. | ||||||||

| Item 15. | ||||||||

| Item 16. | ||||||||

2

Forward-Looking Statements

Forward-looking statements included in this Annual Report on Form 10-K (this "Annual Report"), including, without limitation, statements concerning the conditions of our industry and our operations, performance and financial condition, including in particular, statements relating to our business, growth strategies, product development efforts and future expenses, can be identified by words such as “anticipates,” “intends,” “plans,” “seeks,” “believes,” “estimates,” “expects” and similar references to future periods, or by the inclusion of forecasts or projections. Examples of forward‑looking statements include, but are not limited to, statements we make regarding the outlook for our future business and financial performance, such as those contained in “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

Forward‑looking statements are based on our current expectations and assumptions regarding our business, the economy and other future conditions. Because forward‑looking statements relate to the future, by their nature, they are subject to inherent uncertainties, risks and changes in circumstances that are difficult to predict. As a result, our actual results may differ materially from those contemplated by the forward‑looking statements. Important factors that could cause actual results to differ materially from those in the forward‑looking statements include the following:

•our ability to implement and execute our strategic plans to transform the business;

•our ability to develop or sell solutions in a timely manner or maintain client relationships;

•competition for our solutions;

•harm to our brand and reputation;

•unfavorable global economic conditions;

•risks associated with operating and expanding internationally;

•failure to prevent cybersecurity incidents or the perception that confidential information is not secure;

•failure in the integrity of our data or systems;

•system failures and personnel disruptions, which could delay the delivery of our solutions to our clients;

•loss of access to data sources or ability to transfer data across the data sources in markets we operate;

•failure of our software vendors and network and cloud providers to perform as expected or if our relationship is terminated;

•loss or diminution of one or more of our key clients, business partners or government contracts;

•dependence on strategic alliances, joint ventures and acquisitions to grow our business;

•our ability to protect our intellectual property adequately or cost-effectively;

•claims for intellectual property infringement;

•interruptions, delays or outages to subscription or payment processing platforms;

•risks related to acquiring and integrating businesses and divestitures of existing businesses;

•our ability to retain members of the senior leadership team and attract and retain skilled employees;

•compliance with governmental laws and regulations;

•risks related to the voting letter agreement among and registration and other rights held by certain of our largest shareholders;

•an outbreak of disease, global or localized health pandemic or epidemic, or the fear of such an event (such as the COVID-19 global pandemic), including the global economic uncertainty and measures taken in response; and

•the short- and long-term effects of the COVID-19 global pandemic, including the pace of recovery or any future resurgence.

See "Item 1A.—Risk Factors" for a further description of these and other factors. For the reasons described above, we caution you against relying on any forward-looking statements, which should also be read in conjunction with the other cautionary statements that are included elsewhere in this Annual Report on Form 10-K. Any forward-looking statement made by us in this Annual Report on Form 10-K speaks only as of the date on which we make it. Factors or events that could cause our actual results to differ may emerge from time to time, and it is not possible for us to predict all of them. We are not under any obligation (and expressly disclaim any such obligation) to update or alter our forward-looking statements, whether as a result of new information, future events or otherwise. You should carefully consider the possibility that actual results may differ materially from our forward-looking statements.

3

Part I

Item 1. Business

Our Company

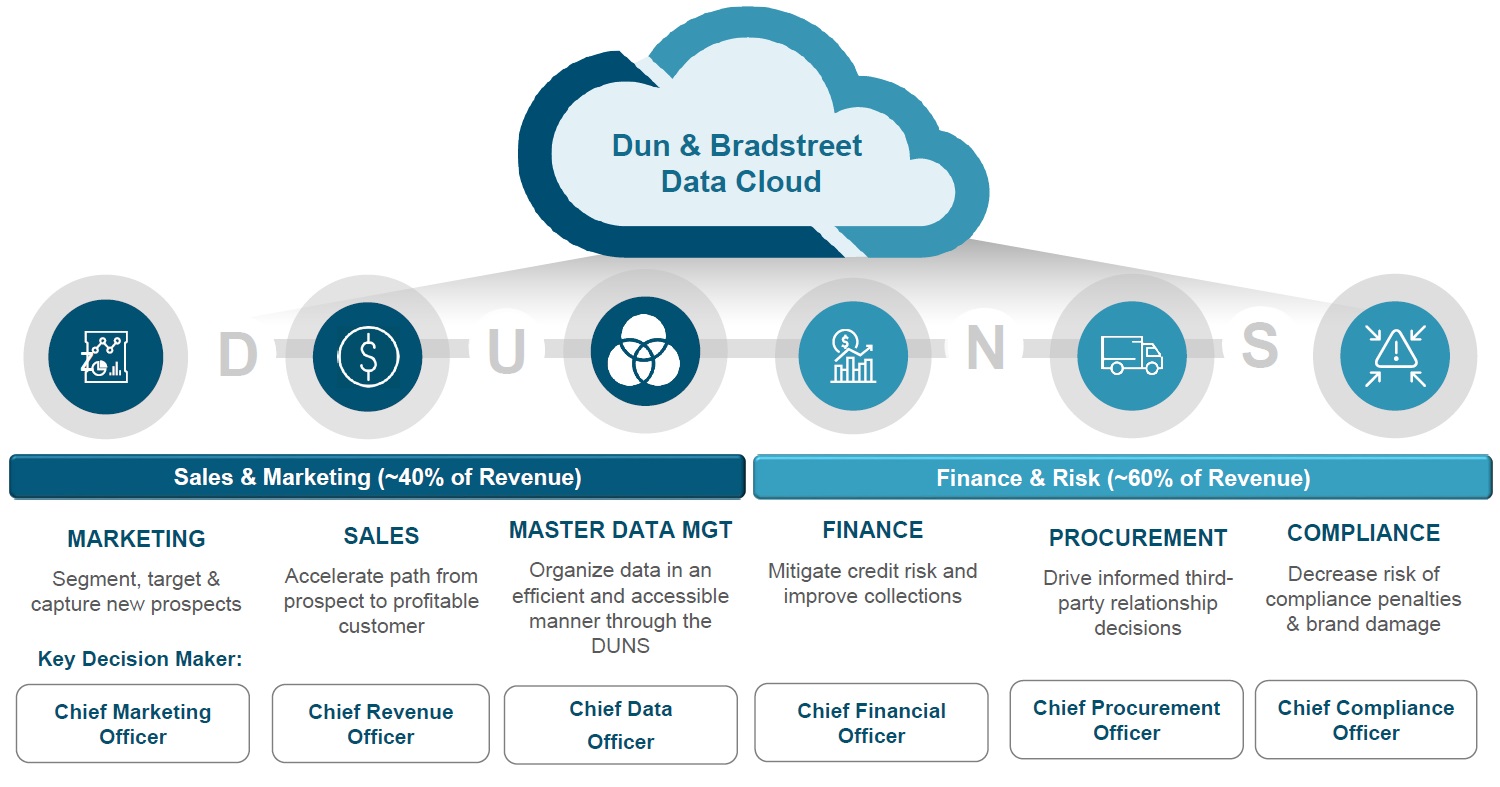

Dun & Bradstreet is a leading global provider of business decisioning data and analytics. Our mission is to deliver a global network of trust, enabling clients to transform uncertainty into confidence, risk into opportunity and potential into prosperity. Clients embed our trusted, end-to-end solutions into their daily workflows to inform commercial credit decisions, confirm suppliers and other third parties are financially viable and compliant with laws and regulations, enhance salesforce productivity and gain visibility into key markets. Our solutions support our clients’ mission critical business operations by providing proprietary and curated data and analytics to help drive informed decisions and improved outcomes.

We are differentiated by the scale, depth, diversity and accuracy of our constantly expanding business database, known as our "Data Cloud," that contains comprehensive information on more than 460 million total organizations as of December 31, 2021. Access to longitudinal curated data is critical for global commerce, and with only a small percentage of the world’s businesses filing public financial statements, our data is a trusted source for reliable information about both public and private businesses. By building such a set of data over time, we were able to establish a unique identifier that creates a single thread connecting related corporate entities allowing our clients to form a holistic view of an enterprise. This unique identifier, which we refer to as the D-U-N-S Number, is an organization's "fingerprint" or "Social Security Number" of businesses. We believe that we are the only scale provider to possess both worldwide commercial credit data and comprehensive public records data that are linked together by a unique identifier allowing for an accurate assessment of public and private businesses globally.

Leveraging our commercial credit data and analytics, our Finance & Risk solutions are used in the critical decisioning processes of finance, risk, compliance and procurement departments worldwide. We are a market leader in commercial credit decisioning, with many of the top businesses in the world utilizing our solutions to make informed decisions when considering extending business loans and trade credit. We are also a leading provider of data and analytics to businesses looking to analyze supplier relationships and more effectively collect outstanding receivables. We believe our proprietary Paydex score is widely relied upon as an important measure of credit health for businesses. We are well positioned to provide accessible and actionable insights and analytics that mitigate risk and uncertainty, and ultimately protect and drive increased profitability for our clients.

Our Sales & Marketing solutions combine firmographic, personal contact, intent and non-traditional, or alternative data, such as foot traffic, website usage, social media posts, online browsing activity and shipping trackers, to assist clients in optimizing their sales and marketing strategy by cleansing customer relationship management ("CRM") data and narrowing their focus and efforts on the highest probability prospects. As global competition continues to intensify, businesses need assistance with focusing their sales pipelines on the people most likely to buy so that they can have their best sellers target the highest probability return accounts. We provide invaluable insights into businesses that can help our clients grow their businesses in a more efficient and effective manner.

We leverage these differentiated capabilities to serve a broad set of clients across multiple industries and geographies. As of December 31, 2021, we have a global client base of more than 200,000, including some of the largest companies in the world. Our data and analytics support a wide range of use cases covering nearly all industry verticals, including financial services, technology, communications, government, retail, transportation and manufacturing. On January 8, 2021, we acquired Bisnode Business Information Group AB (“Bisnode”) which has increased our client base across Europe, and expanded and enhanced our Data Cloud. In terms of our geographic footprint, we have an industry-leading presence in North America, an established presence in the United Kingdom, Ireland, Nordics (Sweden, Norway, Denmark and Finland), DACH (Germany, Austria and Switzerland), Central and Eastern Europe ("CEE"), Greater China and India through our majority or wholly-owned subsidiaries and a broader global presence through our Worldwide Network alliances ("WWN alliances").

We believe that we have an attractive business model that is underpinned by highly recurring, diversified revenues, significant operating leverage, low capital requirements and strong free cash flow. The proprietary and embedded nature of our data and analytics solutions and the integral role that we play in our clients’ decision-making processes have translated into high client retention and revenue visibility. We also benefit from strong operating leverage given our centralized Data Cloud and solutions, which allow us to generate strong contribution margins and free cash flow.

Our Transformation

Over the course of our history, we have earned the privileged position of leadership and trust within the industries we serve. However, operational and execution issues led to stagnant revenue growth and declining profitability. Identifying an opportunity to unlock Dun & Bradstreet's potential, an investor consortium led by William P. Foley II at Bilcar, LLC ("Bilcar"), Thomas H. Lee Partners, L.P. ("THL"), Cannae Holdings, Inc. ("Cannae"), Black Knight, Inc. ("Black Knight") and CC Capital Partners, LLC ("CC Capital" and together with Bilcar, THL, Cannae and Black Knight, the "Investor Consortium"), acquired Dun & Bradstreet in the Take-Private Transaction (the "Take-Private Transaction"), as described below, in February 2019.

4

The Investor Consortium brought in a new senior leadership team with extensive experience and a proven track record of driving long-term shareholder value creation through transformation and growth initiatives. The senior leadership team immediately commenced a comprehensive transformation of our organization and platform with new business unit leaders, enhanced technology and data, solution innovation and a client-centric go-to-market strategy.

To capitalize on the opportunities identified, we have invested in and continue to invest in strategic initiatives that we believe will allow Dun & Bradstreet to achieve its fullest potential, including:

•Realigning Management and Organization: We immediately reorganized our management and operating infrastructure into vertically aligned business units to increase focus and accountability. Within each business unit, we then allocated shared corporate functions, such as analytics, data, finance, legal, marketing and communications, operations, people, sales, strategy and technology, to help better understand and drive accountability for the specific revenues and costs associated with each function.

•Optimizing Go-to-Market and Client Service: We reorganized our salesforce and go-to-market strategy. Our sales team separates clients into three primary tiers, Enterprise, National and small- and medium-sized businesses ("SMBs"). Enterprise clients are each managed by a designated team, many of whom work on clients’ premises given the importance of strategic relationships, while National and SMB clients are managed by teams focused on specific solutions and geographies. Our sales commission plans are structured to incentivize sales of long-term contracts and the cross-selling of additional solutions rather than focusing on the annual renewal of existing contracts. From a client service perspective, we systematically track and monitor service metrics and key service performance indicators to more effectively assist our clients.

•Simplifying and Scaling Technology: We continue to make investments in modernizing our infrastructure and optimizing our architecture to increase control, create efficiencies and greatly enhance the ability of our platforms to scale. As part of our simplification initiative, we are rationalizing and reducing our overall physical data center footprint and are continuing to transition to a cloud-based solution. We also rationalize our legacy solutions and decommission those that are either not profitable or can be consolidated into our core solutions. We continue to re-architect our technology platform to enhance our ability to organize and process high volumes of disparate data, increase system availability and improve delivery, while lowering our overall cost structure and ensuring information security. As part of this effort, we are in the process of reorienting the delivery of all of our solutions via our centralized Prime platform, which collects the cleansed and curated data from our local and global data supply chains and is designed to feed all of our delivery mechanisms with consistent data.

•Expanding and Enhancing Data: We have significantly increased our investment in the breadth and depth of our data, with a focus on better utilization of available data, automation of business data research, improvement of identity resolution, expansion of our individual contact database and implementation of tools to monitor and streamline our data supply chain so that we can generate better, more actionable business insights and outcomes for our clients. We are also expanding our coverage of SMBs and incorporating new, alternative data sets to expand the breadth of companies covered and depth of information we are able to provide clients. We have implemented a data watch program to proactively monitor and repair issues before clients experience them.

•Strengthening Analytics and Insights: We have strengthened our analytics by leveraging our artificial intelligence ("AI") capabilities and expanded data sets and growing our analytics team. Enhanced analytics enable us to provide easy to implement end-to-end solutions that can be used by a wide range of clients, including SMBs that do not have the resources to support a full data analytics staff. By creating configurable, rather than customizable, analytics solutions, we believe that we can increase the adoption of solutions by our clients and expand the size of our client base.

On July 6, 2020, we completed an initial public offering ("IPO") of 90,047,612 shares of our common stock, par value $0.0001 per share at a public offering price of $22.00 per share. Immediately subsequent to the closing of the IPO, we also completed a private placement of 18,458,700 shares of common stock at a price per share equal to 98.5% of the IPO price, or $21.67 per share. See Note 1 to Consolidated Financial Statements in Item 8 for a more detailed discussion of the IPO and concurrent private placement.

Our Market Opportunity

Businesses rely on business-to-business ("B2B") data and analytics providers to extract data-driven insights and make better decisions. For example, in commercial lending and trade credit, the scarcity of readily available credit history makes the extension of credit a time-consuming and imprecise process. In procurement, and business development, businesses face increasingly complex and global supply chains, making the assessment of compliance, risk, and viability of all suppliers and third parties prohibitively difficult and expensive if not conducted effectively. In sales and marketing, businesses have benefited from the proliferation of CRM, Marketing Automation and Sales Acceleration tools designed to help identify, track and improve both customer management and prospecting growth activities. While these tools help to fill sales funnels and improve the progression of opportunities, key challenges remain in salesforce productivity, effective client segmentation and marketing

5

campaign activation. Common stumbling blocks include incorrect, or outdated, contact information, duplicated or inaccurate firmographic data and a lack of synchronization between the various platforms in the marketing technology ecosystem.

We help our clients solve these mission critical business problems. We believe the total addressable market ("TAM") in which we operate is large, growing and significantly under penetrated. We participate in the big data and analytics software market, as defined by Interactive Data Corporation ("IDC"), which represents a collection of software markets that functionally address decision support and decision automation. This market includes business intelligence and analytics tools, analytic data management and integration platforms and analytics and performance management applications. Within the broader market of data and analytics solutions, we serve a number of different markets, including the commercial credit data, sales and marketing data and Governance, Risk and Compliance ("GRC") markets to provide clients with decisioning support and automation. As we continue to drive innovation in our solutions, we expect to address a greater portion of this TAM as new use cases for our data assets and analytical capabilities are introduced.

We believe there are several key trends in the global macroeconomic environment generating additional growth in our TAM and increasing the potential demand for our solutions:

•Growing Recognition of Analytics and Data-Informed Business Decisioning. Due to the pervasive digital transformation that nearly all industries are experiencing, businesses are increasingly recognizing the value of incorporating data-driven insights into their organizations. Businesses are leveraging the advancements of technology in data creation and interpretation to analyze business practices with the aim of improving efficiency, reducing risk and driving growth. We expect companies will continue to recognize the value in relying on insightful and accurate B2B data in their finance and credit decisioning, regulatory and compliance and sales and marketing workflows.

•Growth in Data Creation and Applications. As a result of the increasing recognition of data’s value, the volume of data sets being collected and assembled continues to increase. Not only is the size of these data sets larger than ever, but the data being collected covers a wider range of topics and subjects. Driven in large part by the global trend of an "Internet of Things," the proliferation of mobile phones and connected devices has created a "digital exhaust" of data that can be captured and tracked. This alternative data can be incorporated in predictive models alongside traditional data to provide more sophisticated and accurate business insights. Businesses now have a massive amount of data at their fingertips but often have to rely on large scale providers to help them curate, match, append and create insights in order to convert that data into improved outcomes.

•Advances in Analytical Capabilities Unlocking the Value of Data. The combination of increasingly available data sets with effective artificial intelligence and machine learning capabilities allows for the generation of mission critical insights integrated into clients’ workflows. Businesses that lack the resources for developing these complex tools and solutions internally turn to data and analytics providers, creating market demand. The availability of more insightful analytical tools, in turn, drives growing recognition of the power of analytics in everyday business processes.

•Heightened Compliance Requirements in an Evolving Regulatory Environment for Business. Businesses today are under intense scrutiny to comply with an ever-expanding and evolving set of data regulatory requirements, which often vary by geography and industry served. Performing adequate diligence on clients and suppliers can be cumbersome and dampen the pace of business expansion, or worse, leave a business exposed to expensive fines and penalties. Regulations such as the U.S. Bank Secrecy Act and the recently announced Sixth EU Anti-Money Laundering Directive, the U.S. Department of the Treasury’s Office of Foreign Assets Control's ("OFAC’s") Specially Designated Nationals and Blocked Persons List and other export controls and economic sanctions requirements, the U.S. Foreign Corrupt Practices Act ("FCPA") the UK Bribery Act, and similar laws in other countries, evolving enforcement under competition and antitrust laws. as well as the U.S. Federal Sentencing Guidelines Elements of an Effective Ethics and Compliance Program and environmental, social, and governance ("ESG") disclosure rules, such as the Sustainable Finance Disclosure Regulation (“SFDR”) require businesses to take the necessary steps to comply in an efficient manner. Recently, regulations such as the EU General Data Protection Regulation ("GDPR"), the California Consumer Privacy Act of 2018 ("CCPA") and the California Privacy Rights Act (“CPRA”) and similar laws in other U.S. states such as Virginia and Colorado, the Brazil General Data Protection Act (“LGPD”), and the recently enacted China Personal Information Protection Law (“PIPL”) and the China Data Security Law (“DSL”), and judicial decisions such as the European Court of Justice Case C-311/18 (Schrems II”) have also introduced complexity into the collection, use, sharing, and transfer of data by businesses. Manual processes are burdensome and prone to human error, and therefore demand for data and analytics as a solution continues to increase.

We believe that due to our differentiated capabilities and our long-term client relationships, we are well positioned to capture this market opportunity and benefit from these long-term trends.

Our Solutions

The defining characteristic of our solutions is the breadth and depth of our combined proprietary and curated public data and actionable analytics that help drive informed decisions for our clients. As of December 31, 2021, our Data Cloud is

6

compiled from approximately 28,000 sources, as well as from data collected by our 13 WWN alliances, resulting in data sourced from 256 countries and territories worldwide. We believe that we are uniquely able to match data to its corresponding entity, and have extensive related intellectual property dedicated to this function. Since 1963, we have tracked these businesses by assigning unique identifiers (known as a D-U-N-S Number) to all organizations in our data set. The D-U-N-S Number is recommended and, in many cases required, by over 240 commercial, trade and government organizations. This privileged position in the market has allowed us to commercialize the creation and monitoring of D-U-N-S Numbers by suppliers, which in turn feeds additional proprietary data into our platform.

Data is only valuable when it drives action that moves an organization towards its goals. Underpinned by an integrated technology platform, our solutions derive data-driven insights that help clients target, grow, collect, procure and comply. We provide clients with both curated bulk data to incorporate into their internal workflows and end-to-end solutions that generate insights from this data through configurable analytics. The chart below illustrates the comprehensive, end-to-end nature of our solutions, which are organized into two primary areas: Finance & Risk and Sales & Marketing.

Finance & Risk

Our Finance & Risk solutions are mission critical to our clients as they seek to leverage the data sets and analytics from our platform to manage risk, minimize fraud and monitor their supply chain. Top commercial enterprises across the globe utilize our configurable solutions to make better decisions when considering small business loans, extending trade credit, analyzing supplier relationships and collecting outstanding receivables. Our Finance & Risk solutions help clients increase cash flow and profitability while mitigating credit, operational and regulatory risks.

Our principal Finance & Risk solutions include:

D&B Finance Analytics, which includes D&B Credit Intelligence and D&B Receivables Intelligence, is a subscription-based online application that offers clients real time access to our most complete and up-to-date global information, comprehensive monitoring and portfolio analysis.

D&B Direct is an application programming interface ("API") that delivers risk and financial data directly into enterprise applications such as enterprise resource planning applications ("ERPs") and CRM for real-time credit decision making. The API format allows users to configure their own solutions for their organization’s needs.

D&B Small Business is a suite of powerful tools that allows SMBs to monitor and potentially build their business credit file. SMBs can review detailed reporting on all D&B scores and ratings as well as access triggered alerts for any changes in scores and custom reports with key scores and risk indicators.

D&B Enterprise Risk Assessment Manager ("eRAM") is a global solution for managing and automating credit decisioning and reporting for complex account portfolios, regardless of geography. This solution provides globally consistent data and

7

integrates with in-house ERPs and CRMs. eRAM allows clients to access all of Dun & Bradstreet’s global scores and risk indicators for customized scoring, reporting and analytics.

InfoTorg is a subscription based online SaaS application that provides clients with detailed information on people, companies, vehicles, real estate, laws and regulations as well as court judgments. InfoTorg helps our clients solve their core everyday tasks based on verified and easy to find information. The versatility of the product enables many different use cases, e.g. Anti-Money Laundering ("AML")/Know Your Customer ("KYC") - controls in the financial industry, verification and control of individuals in the public sector as well as vehicle transactions for car dealers and workshops.

Within Finance & Risk, Risk & Compliance offers the tools and expertise to help certify, monitor, analyze and mitigate risk for clients. These solutions provide clients with supplier intelligence, enable ethical and responsible sourcing and facilitate anti-bribery, anti-corruption, and sanction management required by the FCPA, United Kingdom Bribery Act and the OFAC regulations. In addition, these solutions provide KYC and AML insights.

Our principal Risk & Compliance solutions include:

D&B Beneficial Ownership offers risk intelligence on Ultimate Beneficial Ownership from what we believe to be the world’s largest commercial database. Clients are able to view, update and monitor an organization’s hierarchy and beneficial ownership to provide clarity, efficiency and accuracy around beneficial owners. The database includes key shareholders, both individuals and corporate entities, globally.

D&B Supplier Risk Manager provides focused and predictive insights to help certify, monitor, analyze and mitigate risk across the supply chain to avoid costly disruptions. This solution offers predictive scores and government indicators to provide strategic advantage and visibility into risk management.

D&B Onboard leverages the Data Cloud to provide comprehensive insights into businesses to facilitate global KYC/AML compliance and to minimize financial, legal and reputational risk exposure. Onboard automates compliance and onboarding activities by validating identities of businesses against a global Data Cloud of over 460 million organizations to confirm accurate representation.

Sales & Marketing

Our Sales & Marketing solutions help businesses discover new revenue opportunities and accelerate growth by extending the use cases of our data and analytics platform. By adding our proprietary business data set to our personal contact, intent and non-traditional data, we are able to provide a single view of the prospective customer. Our Sales & Marketing solutions extend beyond simple contact data to enable modern marketers and sellers to automate data management and cleansing, leverage AI-powered models to build segments of high-propensity prospects, activate those segments across email, digital ads, paid media and sales plays, unmask and track website visitors and measure campaign performance. We help our clients optimize their sales and marketing functions and narrow their focus on the highest probability businesses.

Our principal Sales & Marketing solutions include:

D&B Connect is a self-service data management platform built using our proprietary AI-powered matching algorithm that provides an easy-to-use portal for managing sales and marketing data. Connect enables clients to reduce time spent on data management from weeks to hours and greatly reduces process complexity by integrating with existing workflows.

D&B Optimizer is an integrated data management solution that links clients’ first party business records in their CRMs, marketing automation and other marketing applications directly with the D&B Data Cloud and ensures continuous data hygiene and management to drive actionable commercial insights and a single client view across multiple systems and touchpoints.

D&B Direct is an API-enabled data management solutions that delivers valuable customer insights into CRMs, marketing automation and other marketing applications for on-demand business intelligence. This configurable format allows users to tailor their own solutions for their organization’s needs.

D&B Rev.Up ABX is an open and agnostic platform that aligns marketing and sales teams to deliver an optimal and coordinated buying journey for accelerated pipeline creation and progression. D&B Rev.Up ABX consolidates first and third party data, allows teams to build high-propensity targets from that data for account-based campaigns, activate target segments across leading email, advertising, and sales automation tools, engage prospects with personalized content, and measure resulting campaign performance.

D&B Audience Targeting helps clients reach the right audiences with the right messages by leveraging our digital IDs and curated pre-defined B2B audience targeting segments that span digital display, mobile, social and connected TV advertising channels. In November 2021, we acquired Eyeota Holdings Pte Ltd. (“Eyeota”), a global online and offline data onboarding and transformation company, and NetWise Data, LLC (“NetWise”), a provider of B2B and business-to-consumer identity graph and

8

audience targeting data. We expect these acquisitions to extend our position in the B2B online marketing value chain and will build upon our Audience Solutions business by adding global scale and the online data to power omni-channel marketing around the world.

D&B Visitor Intelligence turns web visitors into leads by leveraging D&B’s rich B2B data set and digital identity resolution capabilities to unmask anonymous web traffic and identify which companies and potential buyers are visiting client websites. This critical real-time visitor intelligence drives personalized web experiences, increased conversion rates with prefill web registrations and retargeting capabilities to quickly engage these new leads and accelerate the sales process.

D&B Hoovers is a sales intelligence solution that allows clients to research companies, quickly build pipelines, engage in informed conversations and enhance sales productivity. Clients are able to target companies and contacts through search filters that continually refresh based on developed criteria. Hoovers populates leading tools such as Salesforce, Microsoft Dynamics, HubSpot and Marketo records to allow clients to reduce time spent on administrative tasks and improve sales productivity.

Our Competitive Strengths

Market Leadership with the Most Comprehensive Business-to-Business Database

We are uniquely qualified to address the commercial data-driven decisioning needs of our clients due to the breadth and depth of our proprietary Data Cloud and the extensive intellectual property driving insights. Our Data Cloud includes more than 460 million organizations globally and extends far beyond those for which data is publicly available. The D-U-N-S Number is a widely recognized identifier and is a policy-driven requirement for the process of supplying trade credit for many businesses and governments. In addition to the data ingested, D&B has been awarded 243 patents, 140 of which are focused on the complex problem of mapping disparate data sources to a business entity. Our owned, proprietary data sets include commercial credit and firmographic data, professional contact data, third party regulatory compliance, receivables, payment history and other data. Our strategic relationships with our global WWN alliances provide us with international data in our global Data Cloud, which we view as a key competitive strength in serving both U.S. and international businesses. The contributory nature of our Data Cloud, where we typically obtain updated information at little or no cost and own most of the data, creates a strong network effect that we believe gives us an expanding competitive advantage over other market participants or potential entrants. Our Data Cloud is also differentiated in our ability to track corporate linkages of child-to-parent organization relationships and define universal beneficial ownership across entities to help clients better understand commercial relationships and make better informed decisions with a more holistic view of the business.

Innovative Analytics and Decisioning Capabilities Driving End-to-End Solutions

In a world of increasing data access, the value proposition for companies like ours is shifting from the provision of core data to the generation of analytical insights to inform decisioning processes and optimize workflows, across interrelated business activities. Our end-to-end solutions cover a comprehensive spectrum of use cases across the lifecycle of our clients’ businesses. These use cases continue to evolve as we find additional ways to derive insights from our data. We believe our configurable solutions, in combination with our proprietary Data Cloud, are a key competitive advantage for us and allow us to effectively compete across the entire commercial data and analytics landscape.

Deep Relationships with Blue Chip Clients

With our leading data and analytical insights, we serve many of the largest enterprises in the world. Our client base is diversified across size, industry and geography and features minimal concentration. In 2021, 2020 and 2019, no client accounted for more than 5% of our revenue, and our top 50 clients accounted for approximately 25% of our revenue. We have held relationships with 21 of our top 25 clients by size of revenue for the year ended December 31, 2021, 2020 and 2019 for more than 20 years, which reflects how deeply embedded we are in their daily workflows and decisioning processes. For 2021, 2020 and 2019, our annual revenue retention rate was 96%.

Scalable and Highly Attractive Financial Profile

We have an attractive business model underpinned by stable and highly recurring revenues, significant operating leverage and low capital requirements that contribute to strong free cash flow. Our high levels of client retention and shift toward multi-year subscription contracts result in a high degree of revenue visibility. The vast majority of our revenues are either recurring or re-occurring in nature. Additionally, we benefit from natural operating leverage given the high contribution margins associated with incremental revenue generated from our centralized Data Cloud and solutions. Despite the investments being made to enhance our technology, analytics and data, our capital requirements remain minimal with capital expenditures (including

capitalized software development costs) of approximately 8% of our revenues in 2021, excluding the one-time purchase of our new headquarters location in Jacksonville Florida. All of these factors contribute to strong free cash flow generation, allowing us the financial flexibility to invest in the business and pursue growth through acquisitions.

World Class Management Team with Depth of Experience and Track Record of Success

9

Our senior management team has a track record of strong performance and significant expertise in both the markets we serve and in transforming similar businesses by delivering consistent growth both organically and through acquiring and integrating businesses. Our management team operates under the leadership of Mr. Foley, who has a long, successful history of acquiring, reorganizing and transforming companies by rationalizing cost structures, investing in growth and onboarding and mentoring senior management. Beyond our senior management team, we are focused on attracting and retaining the strongest talent at all levels throughout the organization.

Our Growth Strategy

Enhance Existing Client Relationships

We believe our current client base presents a large opportunity for growth through enhanced cross selling in order to capture more of our clients’ data and analytics spend. As an end-to-end provider of commercial data and analytics, we believe that there are significant opportunities to have clients buy from a consistent, single-source provider and to increase their interaction with our platform. Our go-to-market strategy enables us to increase the number of touchpoints with key decision makers within any given client and allows us to identify and sell the right solutions to each decision maker’s respective department. By focusing on enhancing the quality of our data and analytics, we will be able to produce more valuable insights, increasing client engagement across our existing solutions and driving clients towards new, innovative solutions.

Win New Clients in Targeted Markets

We believe that there is substantial opportunity to grow our client base. While we have significant market share in the enterprise and mid-market, there continues to be opportunity to win new clients. There are several instances where we have built a successful long-term enterprise client relationship with a particular company, but its competitors are not our clients. Our focus is to leverage our best practices from serving one company and articulate the value to similar companies that may benefit from our solutions and experience.

We also believe there is significant opportunity to expand our presence in the SMB market. We currently serve approximately 90,000 SMB clients out of the millions of businesses within the global marketplace. In addition, we are servicing over 1,000 businesses a day on average that seek our solutions and D-U-N-S Number and have over 1,500,000 businesses leveraging our business credit and insights. We have existing relationships with many SMBs through solutions enabling the proactive monitoring of their D-U-N-S Number. However, we have not historically capitalized on the opportunity to cross-sell them into our solutions. In 2021 we launched our D&B Marketplace, an integrated web platform that provides businesses with an introduction to Dun & Bradstreet’s capabilities and solutions for their potential use, and digital advertising solutions that enable enterprises to target their offers to our SMB audiences. By leveraging this go-to-market channel and offering more simplified solutions that are easily integrated into client workflows, we can continue to expand our reach among SMBs.

Develop Innovative Solutions

Given the depth and coverage of information contained in our proprietary Data Cloud, we believe we can continue to develop differentiated solutions to serve our clients in an increasing number of use cases. As we continue to gather and incorporate additional sources of data, we believe the resulting analytics and insights we are able to provide within our solutions will be increasingly impactful to our clients and their decisioning processes. By improving the quality and breadth of our Data Cloud, we will be able to expand into adjacent use cases and leverage our data insights in new functional areas such as collections, fraud and capital markets. We will also be able to identify and further penetrate attractive addressable markets, as demonstrated by the development of our Risk & Compliance solutions, a high growth area within our Finance & Risk solutions, in order to better address the GRC market. These additional solutions utilize existing data architecture to generate high contribution incremental revenue streams.

The most recent example of innovative application of the D&B Data Cloud was the rapid development of our AI-driven D&B ESG Intelligence capability using patent-pending technology. Our ESG scores are derived by applying established sustainability standards ("SASB") to companies using our Data Cloud. Given the breadth and depth of the Data Cloud, this deployment immediately moved D&B into a leader role within the ESG score provider industry, making available approximately 20 million ESG scores derived directly from an objective data set. This comprehensive source of ESG data enables compliance and procurement teams to protect company reputation, benchmark against industry trends, identify ESG risks and goals, monitor shifting ESG risks through automated approaches, and streamline ESG assessment processes.

Expand Our Presence in Attractive International Markets

Despite our global presence and industry leading position in the North American market, we remain relatively under-penetrated in international markets, with International revenue accounting for approximately a third of our business in 2021. We believe that expanding our presence in owned international markets can be a significant growth driver for us in the coming years. Our international growth strategy begins with localizing current solutions to meet global demand and, similar to our domestic strategy, includes a focus on cross-selling and upselling, winning new clients and developing innovative solutions. On

10

January 8, 2021, we acquired Bisnode, a leading European data and analytics firm, which positioned us to rapidly expand our client base across the Nordics, DACH and CEE markets.

Selectively Pursue Strategic Acquisitions

While the core focus of our strategy is to grow organically, we believe there are strategic acquisition opportunities that may allow us to expand our footprint, broaden our client base, increase the breadth and depth of our data sets and further strengthen our solutions. We believe there are attractive synergies that result from acquiring small companies that provide innovative solutions and integrating these solutions into our existing offerings to generate cross-selling and upselling opportunities across our existing client base. Our leadership team has a proven track record of identifying, acquiring and integrating companies to drive long-term value creation, and we will continue to maintain a disciplined approach to pursuing acquisitions.

The most recent example of expanding our solution set inorganically is our simultaneous acquisitions of Eyeota and NetWise. D&B’s Sales and Marketing Solutions have been providing off-line data to enrich and enable digital marketing campaigns for many years. Through these acquisitions D&B simplifies the process our clients execute to segment, target and activate ad campaigns. Importantly, these acquisitions position D&B for the post-cookie world as expanding privacy regulations impose greater restrictions on the use of third-party data as well as third-party data sharing.

Our Clients

We have a diversified client base with more than 200,000 clients worldwide during 2021.

Our client base is diversified across size, industry and geography, and features minimal concentration; with no client accounting for more than 5% of revenue and our top 50 clients accounting for approximately 25% of revenue. Our clients include enterprises across nearly all industry verticals, including financial services, technology, communications, retail, transportation and manufacturing, and our data and analytics support use cases of all types. A substantial portion of our revenue is derived from companies in the financial services industry. We have held relationships with 21 of our top 25 clients by size of revenue for the year ended December 31, 2021 for more than 20 years, which reflects how deeply embedded we are in their daily workflows and decisioning processes. For 2021, our annual revenue retention rate, reflecting the percentage of prior year revenue from clients who were retained in the current year, was 96%.

In addition to our blue chip corporate client base, we serve a number of government organizations. Through the development of our analytics, we continue to move into mission critical functions with higher applicability across federal, state and local government organizations.

We have a presence in 256 countries and territories, including the United States, Canada, the United Kingdom, Ireland, Nordics, DACH, CEE, Greater China and India as of December 31, 2021. Our international presence is organized through the WWN alliances and owned markets. The following table presents the contribution by geography to revenue, which excludes Corporate and other:

| Year Ended December 31, | |||||||||||||||||

| 2021 | 2020 | 2019 | |||||||||||||||

| Revenue by geography | |||||||||||||||||

| North America | 69 | % | 83 | % | 83 | % | |||||||||||

| International | 31 | % | 17 | % | 17 | % | |||||||||||

Go-to-Market Organization

Our sales and marketing efforts are focused on both generating new clients as well as cross-selling and upselling our end-to-end solutions to existing clients. Our salesforce is segmented into three distinct categories: strategic sales, field sales and inside sales. To more effectively align our salesforce with our clients, we have also organized these distribution channels into geographic territories supported by specialized sales support and centralized sales development teams.

Our strategic sales team covers our largest and most sophisticated clients who typically use multiple D&B solutions across a variety of use cases. These strategic clients are each independently managed by directors who own the client relationship and are equipped to sell all solutions. In many instances, we deploy our employees on-site to assist our clients in implementing and configuring our analytics for various use cases, acting as a "one-stop shop" for our clients’ data and analytics needs.

11

Our field sales team is geographically distributed and promotes both our Finance & Risk solutions and Sales & Marketing solutions, largely targeting clients with revenues in excess of $250 million. Clients in this grouping typically buy only one of our solutions, and there is ample opportunity to expand the depth of our relationships as we continue to educate and train our sales professionals on selling our full suite of solutions.

Lastly, our inside sales team is focused on all other businesses that are not covered by our other direct sales channels in the emerging and micro business segments. Our specialized sales support and subject matter experts are consolidated in a shared services organization and support all channels as needed. In addition, we are building a sales development representative organization that supports lead generation of our sales teams.

In addition to our direct go-to-market efforts, we also sell through our network of strategic alliances to jointly deliver our data and analytics to our mutual clients. This indirect channel is centrally managed collaboratively within the sales organization and also has responsibility for coordinating all global WWN and owned markets to ensure consistency of approach and account management for our global clients.

Given the breadth of our end-to-end solutions and increased focus on cross-selling, we have spent considerable time training and upskilling our salesforce in a formal sales training program. We now require sales certifications from our salesforce and have instituted talent assessments and mid-year performance check-ins to ensure we continue to shape our culture to winning and accountability.

We have also redesigned our sales compensation plans to incentivize multi-year contracting and cross-selling rather than one-year deals that are renewed each year.

International Presence

We have operated internationally for over 160 years and benefit from an extensive network and strong global brand recognition. We have an operating framework of owned, majority-controlled and partnered markets that serve international clients and secure critical global data to support both our United States and international clients. Across all international markets, we leverage our unique data sets and solutions to serve our clients’ Finance & Risk and Sales & Marketing needs.

There are certain key international markets in which we operate independently or through joint ventures, including the United Kingdom, Ireland, Nordics, DACH, CEE, Greater China and India. As we continue to provide international companies with our best-in-class data on U.S. companies, suppliers and prospects, our solutions have also increasingly become localized in recent years to better serve foreign markets. Our local presence ensures the complete, timely and accurate collection of commercial information.

In addition, as of December 31, 2021, we also operated through 13 WWN alliances. Our partners license our data as well as our trademarks and brand, to serve local markets that Dun & Bradstreet does not have direct ownership. Our extensive international network enables millions of executives around the world to make confident business decisions with reliable and accessible information. Our strategic relationships with our global WWN alliances provide us with best-in-class breadth of international data in our Data Cloud, which we view as a key competitive strength in serving international enterprises. This approach has improved the applicability of our data to local clients, while enlarging and strengthening the data sets for clients in all geographies.

Competition

We primarily compete on the basis of differentiated data sets, analytical capabilities, solutions, client relationships, innovation and price. We believe that we compete favorably in each of these categories across both our Finance & Risk and Sales & Marketing solutions. Our competitors vary based on the client size and geographical market that our solutions cover.

For our Finance & Risk solutions, our competition generally varies by client size between enterprise, mid-market and SMBs. Dun & Bradstreet has a leading presence in the enterprise market as clients place a high degree of value on our best-in-class commercial credit database to inform their critical decisions around the extension of credit. Dun & Bradstreet’s main competitors in the enterprise and mid-market include Bureau van Dijk (owned by Moody’s Corporation), Experian and Creditsafe in Europe and Experian and Equifax in North America. In the SMB market, commercial credit health becomes increasingly tied to consumer credit health. Our competition in this market generally includes Equifax, Experian and other consumer credit providers that offer commercial data. Additionally, there is a fragmented tail of low cost, vertical and regionally focused point solutions in this market that may be attractive to certain clients but lack the scale and coverage breadth to compete holistically.

For our Sales & Marketing solutions, our competition has historically been very fragmented with many players offering varying levels of data quantity and quality, and with data being collected in ways that may cross ethical and privacy boundaries. Dun & Bradstreet strives to protect the data and privacy of clients and other constituents and to maintain high standards of integrity and accountability in the ethical acquisition, aggregation, curation and delivery of data. Our direct competitors vary depending on use cases, such as market segmentation, digital marketing lead generation, lead enrichment, sales effectiveness

12

and data management. In the market for professional contact data, our competition generally includes ZoomInfo and a few consultancies building bespoke solutions. For other sales and marketing solutions such as customer data platform, visitor intelligence, audience targeting and intent data, we face a number of smaller competitors.

Overall, outside North America, the competitive environment varies by region and country, and can be significantly impacted by the legislative actions of local governments, availability of data and local business preferences.

In the United Kingdom and Ireland, our direct competition for our Finance & Risk solutions is primarily from Bureau van Dijk, Creditsafe and Experian. Additionally, the Sales & Marketing solutions landscape in these markets is both localized and fragmented, where numerous local players of varying sizes compete for business.

In the Nordics, we primarily compete with Enento and Experian and in Central and Eastern European markets we compete with several regional and local players.

In Asia Pacific, we face competition in our Finance & Risk solutions from a mix of local and global providers. In China we primarily compete with global providers such as Experian and Bureau van Dijk, as well as technology driven local players focusing on domestic data. In India we compete with local competitors. In addition, as in the United Kingdom, the Sales & Marketing solutions landscape throughout Asia is localized and fragmented.

We believe that the solutions we provide to our clients in all geographies reflect our deep understanding of our clients’ businesses, the differentiated nature of our data and the quality of our analytics and decisioning capabilities. The integration of our solutions into our clients’ mission critical workflows helps to ensure long-lasting relationships, efficiency and continuous improvement.

Technology

Technology is key to how we efficiently collect, curate and ultimately deliver our data, actionable analytics and business insights to make investments in modernizing our infrastructure and optimizing our architecture to increase control, create efficiencies and greatly enhance the ability of our platforms to scale. We make investments in the re-architecture of our technology platform to enhance our ability to organize and process high volumes of disparate data, increase system availability and improve delivery, while lowering our overall cost structure and ensuring information security. We continue to work towards evolving Dun & Bradstreet into a platform with the ability to seamlessly add and integrate new data sets and analytical capabilities into our simplified and scaled technology infrastructure.

Intellectual Property

We own and control various intellectual property rights, such as trade secrets, confidential information, trademarks, service marks, trade names, copyrights, patents and applications to the foregoing. These rights, in the aggregate, are of material importance to our business. We also believe that the Dun & Bradstreet name and related trade names, marks and logos are of material importance to our business. We are licensed to use certain technology and other intellectual property rights owned and controlled by others, and other companies are licensed to use certain technology and other intellectual property rights owned and controlled by us. We consider our trademarks, service marks, databases, software, analytics, algorithms, inventions and other intellectual property to be proprietary, and we rely on a combination of statutory (e.g., copyright, trademark, trade secret, patent, etc.) and contractual safeguards for protecting them throughout the world.

We own patents and have filed for patent applications both in the United States and in other selected countries of importance to us. The patents and patent applications include claims which pertain to certain technologies and inventions which we have determined are proprietary and warrant patent protection. We believe that the protection of our innovative technology and inventions, such as our proprietary methods for data curation and identity resolution, through the filing of patent applications, is a prudent business strategy. Filing of these patent applications may or may not provide us with a dominant position in the fields of technology. However, these patents and/or patent applications may provide us with legal defenses should subsequent patents in these fields be issued to third-parties and later asserted against us. An important aspect of our intellectual property strategy is to file for patents in innovative and modern technology spaces. For example, our application for a “System and Method for Identity Resolution across Disparate Distributed Immutable Ledger Networks” in the blockchain space was granted in December 2021 in Canada. In the United States, our patent detailing a “System and Method for Assessing and Optimizing Master Data Maturity” was granted in May 2021. Where appropriate, we may also consider asserting, or cross-licensing, our patents.

Corporate Social Responsibility

We firmly believe a defining quality of successful companies is that they demonstrate a consistent commitment to empowering the people and communities where they operate. We believe in having a positive impact through responsible engagement on environmental, social, and governance issues.

13

Our company culture provides a foundation that lets us commit to fostering social and economic development and contributing to the sustainability of the communities in which we all live and operate. We look at responsibility from several dimensions— how we support and empower our employees, the way we focus on helping our clients and the way we manage our corporation—all aligned with our core value of inherent generosity.

We are committed to fostering a workplace where everyone’s voice is valuable and diversity in all its forms is welcomed. In 2021, Dun & Bradstreet received a 100% score on the Human Rights Campaign Corporate Equality Index for LGBTQ Equality, an award the company has earned consecutively since 2017. We also earned a 100% score on the Disability Equality Index Best Places to Work for Disability Inclusion in 2021.

We seek to be a steward of the global environment and actively shape sustainable futures in the communities where we work and live. We use our data and analytics to help companies grow their business and become better global corporate citizens.

Workforce and Human Capital Resources

As of December 31, 2021, we had 6,296 employees worldwide, of whom 2,731 were in our North America segment and Corporate, and 3,565 were in our International segment. Our workforce also engages third-party consultants as an ongoing part of our business where appropriate. There are no unions in our U.S. or Canadian operations, and work councils and trade unions represent a portion of our employees in a few European markets. We have not experienced any work stoppages and we believe we maintain strong relations with our employees.

We are committed to creating a passionate, outside-in, forward-leaning culture. We want Dun & Bradstreet to be the best place to work and one that attracts and retains the very best talent. We strive to make our company a diverse, inclusive and safe workplace that will drive personal growth for each of our employees. We design our human resources programs to support these critical objectives. We provide a comprehensive compensation and benefits package designed to support our employees, both at home and at work. We provide learning and development programs for our people to prepare them for their roles and facilitate internal career mobility aiming at creating a high-performing workforce. Our diversity and inclusion programs further enhance our culture with the goal of making our workplace more engaging and inclusive. Our “Corporate Citizenship / Do Good” program is designed to give back to our communities where we live and work, and to support worthy causes around the world. This program further enhances the interaction of our employees at all levels.

In our continued response to the COVID-19 pandemic, we implemented operational changes with the primary objective of safety for our employees, as well as the communities in which we operate, and to comply with government regulations. We have adopted a distributed workforce model, including a long-term, full-time work from home arrangement for some employees, while implementing additional safety measures for employees and contractors continuing essential and critical on-site work.

Financial Information by Segment

In addition to our two reportable segments, we have a corporate organization that consists primarily of general and administrative expenses that are not included in the other segments. For financial information by reporting segment, see Note 18 to the Consolidated Financial Statements.

Regulatory Matters

Compliance with legal and regulatory requirements is a top priority for us. This includes compliance, to the extent applicable, with national and local anti-bribery and anti-corruption laws, information privacy, communications privacy, and data protection laws and regulations, data security and cybersecurity laws, unfair and deceptive trade practices laws, export control and economic sanctions laws, antitrust/competition laws national laws regulating enterprise credit reporting agencies and, in a few cases internationally, consumer reporting agencies, and digital accessibility and advertising laws. These laws are enforced by national and local regulatory agencies, and in some instances also through private civil litigation.

We proactively manage our compliance with laws and regulations through a dedicated legal and compliance and ethics team situated in the United States, the United Kingdom, Nordics, Central Europe, Greater China and India all reporting to the Chief Legal Officer and Chief Compliance Officer in the United States. Through the legal and compliance and ethics functions, we operate a comprehensive compliance and ethics program aligned with the U.S. Federal Sentencing Guidelines Elements of an Effective Compliance and Ethics Program, the OECD Good Practices Guidance on Internal Controls, Ethics, and Compliance, the OECD Guidelines Governing the Protection of Privacy and Transborder Flows of Personal Data, and the accountability principle of the GDPR. Based on an holistic program model integrating these frameworks, we undertake compliance risk assessments, promulgate compliance policies and procedures, provide awareness and training to our teams and associates, maintain and strive to continually improve upon compliance program operations, monitor all material laws and regulations applicable to our business, oversee, monitor and audit the efficacy of our internal compliance-related controls, evaluate the compliance and regulatory risks of the suppliers and other third parties we engage, advise on and assist in the

14

development of new products and services, and meet as necessary and appropriate with regulators and legislators to establish transparency of our operations and create a means to understand and respond should any issues arise.

Data and Privacy Protection and Regulation

Our operations are subject to applicable national and local laws that regulate privacy, data and cyber security, broader data collection, use and sharing, cross-border data transfers and/or business, and in certain cases internationally, consumer credit reporting. These laws impact, among other things. data collection, usage, storage, transparency, security and breach, dissemination (including transfer to third parties and cross-border), individual rights management, retention and destruction. Certain of these laws provide for civil and criminal penalties for violations. Expansion into new use cases for personal information and growth through acquisitions, such as Bisnode and Eyeota, adds a further layer of complexity to our overall obligations under these laws, including new obligations relating to certain categories of consumer data. The laws and regulations that affect our business include, but are not limited to:

•the GDPR, the ePrivacy Directive and implementing national legislation, and judicial and regulatory developments on the EU and national level, including the recent Schrems II decision and EDPB guidance;

•U.S. federal, state and local data protections laws such as the Federal Trade Commission Act ("FTC Act") and similar state laws, state data breach laws and state privacy laws, such as the CCPA, the recently adopted Virginia Consumer Data Protection Act ("CDPA") and the Colorado Privacy Act ("CPA");

•China’s Cybersecurity Law and the newly passed China Personal Information Protection Law ("PIPL") and Data Security Law ("DSL"), as well as other civil and criminal laws relating to data protection;

•other international data protection, data localization, and state secret laws impacting us or our data suppliers;

•oversight by regulatory authorities for engaging in business credit reporting such as the U.K. Financial Conduct Authority and People’s Bank of China; and

•Canadian Federal and provincial privacy laws, such as PIPEDA and CASL.

We are also subject to federal and state laws impacting marketing such as the Americans with Disabilities Act, the Telephone Consumer Protection Act of 1991 and state unfair or deceptive practices acts and telemarketing laws.

These laws and regulations, which generally are designed to protect the privacy of the public and to prevent the misuse of personal information available in the marketplace, are complex, change frequently and have consistently trended towards becoming more stringent over time. We already incur significant expenses in our attempt to ensure compliance with these laws. Currently, public concern is high with regard to the operation of credit reporting agencies in the United States, as well as the collection, use, accuracy, correction. sharing and cross border transfers of personal information, especially any personal information that may be deemed as sensitive, such as U.S. Social Security numbers, dates of birth, financial information, medical information, department of motor vehicle data, behavioral data, and data related to ethnicity, political, religious or philosophical beliefs, sexual orientation and genetic, biometric and health data. In addition, many consumer advocates, privacy advocates, legislatures and government regulators believe that existing laws and regulations do not adequately protect privacy and personal data in light of evolving technologies and data uses and have become increasingly concerned about the need for expanded oversight for the processing, generation, handling, and security of such data. As a result, they are lobbying and advocating for further restrictions, transparency, and accountability for the dissemination or commercial use of personal information to the public and private sectors. Additional legislative or regulatory efforts in the United States and other jurisdictions globally could further regulate the collection, use, communication, access, accuracy, obsolescence, sharing, cross border transfer, correction, security and rights of individuals and entities related to this personal information. In addition, any perception that our practices or products are an invasion of privacy, whether or not consistent with current or future regulations and industry practices, may subject us to public criticism, private class actions, reputational harm, or claims by regulators, which could disrupt our business and expose us to increased liability. Further developments in the area of data subject rights, including broad rights around data access, correction, deletion and erasure, portability, restriction, and objection may incur additional costs to the Company as we continue to refine operational and technical controls to meet our expanding legal obligations.

Additional Information

Our website address is www.dnb.com. We make available free of charge on or through our website our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and all amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act as soon as reasonably practicable after such material is electronically filed with or furnished to the Securities and Exchange Commission ("SEC"). Information regarding our ESG, corporate responsibility and sustainability initiatives is also available on our website at https://investor.dnb.com/governance/Corporate-Social-Sustainability-Report/default.aspx. However, the information found on our website is not part of this or any other report.

15

Item 1A. Risk Factors

You should carefully consider the following risk factors and all of the information contained in this Annual Report on Form 10-K. If any of the following risks occur, our business, financial condition and results of operations could be materially and adversely affected.

Our operations and financial results are subject to various risks and uncertainties, including but not limited to those described below, which could harm our business, reputation, financial condition, and operating results. Below is a summary of these risk factors followed by the detailed risk factors:

Operational Risks

•Our ability to implement and execute our strategic plans to transform the business may not be successful and, accordingly, we may not be successful in achieving our goals to transform our business, which could have a material adverse effect on our business, financial condition and results of operations.

•If we are unable to develop or sell solutions in a timely manner or maintain and enhance our existing client relationships, our ability to maintain or increase our revenue could be adversely affected.

•We face significant competition for our solutions, which may increase as we expand our business.

•Our brand and reputation are key assets and a competitive advantage, and our business may be affected by how we are perceived in the marketplace.

•Our international operations and our ability to expand our operations outside the United States are subject to economic, political and other inherent risks.

•Data security and integrity are critically important to our business, and cybersecurity incidents, including cyberattacks, breaches of security, unauthorized access to or disclosure of confidential information, business disruption, or the perception that confidential information is not secure, could result in a material loss of business, regulatory enforcement, substantial legal liability and/or significant harm to our reputation.

•A failure in the integrity of our data or the systems upon which we rely could harm our brand and result in a loss of sales and an increase in legal claims.

•If we experience system failures, personnel disruptions or capacity constraints, the delivery of our solutions to our clients could be delayed or interrupted, which could harm our business and reputation and result in the loss of revenues or clients.

•We could lose our access to data sources or ability to transfer data across the data sources in markets we operate, which could prevent us from providing our solutions.

•We use software vendors and network and cloud providers in our business and if they cannot deliver or perform as expected or if our relationships with them are terminated or otherwise change it could have a material adverse effect on our business, financial condition and results of operations.

•We rely on our relationships with key long-term clients, business partners and government contracts for a substantial part of our revenue, the diminution or termination of which could have a material adverse effect on our business, financial condition and results of operations.

•We depend, in part, on strategic alliances, joint ventures and acquisitions to grow our business. If we are unable to make strategic acquisitions and develop and maintain these strategic alliances and joint ventures, our growth may be adversely affected.

•We are subject to subscription and payment processing risk from our third-party vendors and any disruption to such processing systems could have a material adverse effect on our business, financial condition and results of operations.

Legal and Regulatory Risks

•We may be unable to protect our intellectual property adequately or cost-effectively, which may cause us to lose market share or force us to reduce our prices. We also rely on trade secrets and other forms of unpatented intellectual property that may be difficult to protect.

•We may face claims for intellectual property infringement, which could subject us to monetary damages or limit us in using some of our technologies or providing certain solutions.

•We are subject to various governmental regulations, laws and orders, compliance with which may cause us to incur significant expenses or reduce the availability or effectiveness of our solutions, and the failure to comply with which could subject us to civil or criminal penalties or other liabilities.

•Current and future litigation, investigations or other actions against us could be costly and time consuming to defend.

•If we experience changes in tax laws or adverse outcomes resulting from examination of our tax returns, it could have a material adverse effect on our business, financial condition and results of operations.

Financial Risks