UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM

(Mark One)

OR

For the fiscal year ended

OR

OR

Date of event requiring this shell company report

For the transition period from to

Commission file number

(Exact name of Registrant as specified in its charter)

N/A

(Translation of Registrant’s name into English)

(Jurisdiction of incorporation or organization)

(Address of principal executive offices)

Telephone: +

Email:

Address:

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

Title of each class |

|

Trading Symbol |

|

Name of each exchange on which registered |

|

|

|||

|

|

|

|

|

|

|

* Not for trading, but only in connection with the listing on the New York Stock Exchange of American depositary shares.

Securities registered or to be registered pursuant to Section 12(g)

None

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

None

(Title of Class)

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ☐ Yes ☒

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. ☐ Yes ☒

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ☒

Indicate by check mark whether the registrant has submitted every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). ☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer |

|

☐ |

|

|

☒ |

|

Non-accelerated filer |

|

☐ |

|

Emerging growth company |

|

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ☐

† |

The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012. |

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark which basis of accounting the registration has used to prepare the financial statements included in this filing:

|

International Financial Reporting Standards as issued by the International Accounting Standards Board |

☐ |

Other ☐ |

If “Other” has been checked in response to the previous question, indicate by check mark which consolidated financial statement item the registrant has elected to follow. ☐ Item 17 ☐ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Securities Exchange Act of 1934). ☐ Yes

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. ☐ Yes ☐ No

Table of Contents

|

Page |

|||

3 |

||||

|

ITEM 1. |

|

3 |

|

|

ITEM 2. |

|

3 |

|

|

ITEM 3. |

|

3 |

|

|

ITEM 4. |

|

37 |

|

|

ITEM 4A. |

|

71 |

|

|

ITEM 5. |

|

71 |

|

|

ITEM 6. |

|

82 |

|

|

ITEM 7. |

|

93 |

|

|

ITEM 8. |

|

94 |

|

|

ITEM 9. |

|

95 |

|

|

ITEM 10. |

|

96 |

|

|

ITEM 11. |

|

104 |

|

|

ITEM 12. |

|

106 |

|

|

|

109 |

||

|

ITEM 13. |

|

109 |

|

|

ITEM 14. |

|

MATERIAL MODIFICATIONS TO THE RIGHTS OF SECURITY HOLDERS AND USE OF PROCEEDS |

109 |

|

ITEM 15. |

|

109 |

|

|

ITEM 16A. |

|

110 |

|

|

ITEM 16B. |

|

110 |

|

|

ITEM 16C. |

|

110 |

|

|

ITEM 16D. |

|

110 |

|

|

ITEM 16E. |

|

PURCHASES OF EQUITY SECURITIES BY THE ISSUER AND AFFILIATED PURCHASERS |

111 |

|

ITEM 16F. |

|

111 |

|

|

ITEM 16G. |

|

111 |

|

|

ITEM 16H. |

|

112 |

|

|

ITEM 16I. |

|

DISCLOSURE REGARDING FOREIGN JURISDICTIONS THAT PREVENT INSPECTIONS |

112 |

|

ITEM 16J. |

|

112 |

|

|

ITEM 16K. |

|

112 |

|

|

|

116 |

||

|

ITEM 17. |

|

116 |

|

|

ITEM 18. |

|

116 |

|

|

ITEM 19. |

|

116 |

|

i

CONVENTIONS THAT APPLY TO THIS ANNUAL REPORT ON FORM 20-F

Except where the context otherwise requires, references in this annual report to:

Unless specifically indicated otherwise or unless the context otherwise requires, all references to our ordinary shares exclude ordinary shares issuable upon the exercise of outstanding options with respect to our ordinary shares under our share incentive plans.

The translations from AED to U.S. dollars in this annual report were made at a rate of AED3.6725 to US$1.00, the exchange rate at which AED has been pegged to U.S. dollars since November 1997. We make no representation that AED amounts referred to in this annual report could have been or could be converted into U.S. dollars at any particular rate or at all.

We listed our ADSs on the New York Stock Exchange under the symbol “YALA” on September 30, 2020.

1

FORWARD-LOOKING INFORMATION

This annual report on Form 20-F contains statements of a forward-looking nature. All statements other than statements of historical facts are forward-looking statements. These forward-looking statements are made under the “safe harbor” provision under Section 21E of the Securities Exchange Act of 1934, as amended, or the Exchange Act, and as defined in the Private Securities Litigation Reform Act of 1995. These statements involve known and unknown risks, uncertainties and other factors that may cause our actual results, performance or achievements to be materially different from those expressed or implied by the forward-looking statements. In some cases, these forward-looking statements can be identified by words or phrases such as “may,” “will,” “expect,” “anticipate,” “aim,” “estimate,” “intend,” “plan,” “believe,” “potential,” “continue,” “is/are likely to” or other similar expressions. These forward-looking statements relate to, among others:

We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends that we believe may affect our financial condition, results of operations, business strategy and financial needs.

You should read these statements in conjunction with the risks disclosed in “Item 3. Key Information—D. Risk Factors” of this annual report and other risks outlined in our other filings with the Securities and Exchange Commission, or the SEC. Moreover, we operate in an emerging and evolving environment. New risks may emerge from time to time, and it is not possible for our management to predict all risks, nor can we assess the impact of such risks on our business or the extent to which any risk, or combination of risks, may cause actual results to differ materially from those contained in any forward-looking statements. The forward-looking statements made in this annual report relate only to events or information as of the date on which the statements are made in this annual report. Except as required by law, we undertake no obligation to update any forward-looking statements to reflect events or circumstances after the date on which the statements are made or to reflect the occurrence of unanticipated events. You should read this annual report and the documents that we have referred to in this annual report, completely and with the understanding that our actual future results may be materially different from what we expect.

2

PART I.

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not Applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not Applicable.

ITEM 3. KEY INFORMATION

Our Operations in China

We are a leading social networking and gaming platform in MENA, and we primarily generate revenue through our subsidiaries in the UAE. We have our headquarters in Dubai, and at the same time, our technology and product development team and certain members of our management, among others, are located in China, and we have operating subsidiaries incorporated under the laws of the PRC. Therefore, we face various risks and uncertainties related to operating in China. PRC government’s significant authority in regulating our operations and its oversight and control over offerings conducted overseas by, and foreign investment in, issuers with operations in China could significantly limit or completely hinder our ability to offer or continue to offer securities to investors. Implementation of industry-wide regulations, including those affecting the Internet industry, may cause the value of our ADSs to significantly decline. Risks and uncertainties arising from the legal system in China, including risks and uncertainties regarding the enforcement of laws and quickly evolving rules and regulations in China, could result in a material adverse change in our operations and the value of our ADSs. See “—D. Risks Factors—Risks Relating to Doing Business in Certain Countries and Regions—The economic, political and social conditions in MENA and China, as well as government policies, laws and regulations, could affect our business, financial condition and results of operations.”

Holding Foreign Companies Accountable Act

The Holding Foreign Companies Accountable Act, as amended, or the HFCA Act, was signed into law on December 18, 2020 and amended pursuant to the Consolidated Appropriations Act, 2023 on December 29, 2022. Under the HFCA Act and the rules issued by the SEC and the U.S. Public Company Accounting Oversight Board, or the PCAOB, thereunder, if we have retained a registered public accounting firm to issue an audit report where the registered public accounting firm has a branch or office that is located in a foreign jurisdiction and the PCAOB has determined that it is unable to inspect or investigate completely because of a position taken by an authority in the foreign jurisdiction, the SEC will identify us as a “covered issuer”, or SEC-identified issuer, shortly after we file with the SEC a report required under the Securities Exchange Act of 1934, or the Exchange Act (such as our annual report on Form 20-F), that includes an audit report issued by such accounting firm; and if we were to be identified as an SEC-identified issuer for two consecutive years, the SEC would prohibit our securities (including our shares or ADSs) from being traded on a national securities exchange or in the over-the-counter trading market in the United States.

In December 2021, the PCAOB made its determinations, or the 2021 determinations, pursuant to the HFCA Act that it was unable to inspect or investigate completely registered public accounting firms headquartered in mainland China or Hong Kong including our auditor, KPMG Huazhen LLP. After we filed our annual report on Form 20-F for the fiscal year ended December 31, 2021 that included an audit report issued by KPMG Huazhen LLP on April 25, 2022, the SEC conclusively identified us as an SEC-identified issuer on May 26, 2022.

3

Following the Statement of Protocol signed between the PCAOB and the China Securities Regulatory Commission and the Ministry of Finance of the PRC in August 2022 and the on-site inspections and investigations conducted by the PCAOB staff in Hong Kong from September to November 2022, the PCAOB Board voted in December 2022 to vacate the previous 2021 determinations, and as a result, our auditor, KPMG Huazhen LLP, was no longer a registered public accounting firm that the PCAOB was unable to inspect or investigate completely as of the date of our annual report for the fiscal year ended December 31, 2022 and we were not identified as an SEC-identified issuer in 2023. On November 30, 2023, the PCAOB announced that it had completed its inspections on registered public accounting firms headquartered in mainland China and Hong Kong for 2023 with the complete access required under the HFCA Act. As such, we do not expect to be identified as an SEC-identified issuer in 2024 either. However, the PCAOB may change its determinations under the HFCA Act at any point in the future. See “D. Risks Factors—Risks Relating to Doing Business in Certain Countries and Regions—If the PCAOB determines that it is unable to inspect or investigate completely our auditor at any point in the future, our ADSs may be prohibited from trading in the United States under the Holding Foreign Companies Accountable Act, as amended, or the HFCA Act, and any such trading prohibition on our ADSs or threat thereof may materially and adversely affect the price of our ADSs and value of your investment.”

Not Applicable.

Not Applicable.

Summary of Risk Factors

Investing in our ADSs involves significant risks. You should carefully consider all of the information in this annual report before making an investment in the ADSs. Below please find a summary of the principal risks we face, organized under relevant headings:

Risks Relating to Our Business and Industry

Risks and uncertainties relating to our business and industry include, but are not limited to, the following:

4

Risks Relating to Doing Business in Certain Countries and Regions

We are subject to risks and uncertainties relating to doing business in certain countries and regions in general, including, but are not limited to, the following:

Risks Relating to the American Depositary Shares

Risks relating to our ADSs, include, but not limited to, the following:

Risks Relating to Our Business and Industry

If we fail to retain our existing users, keep them engaged or further grow our user base, our business, operation, profitability and prospects may be materially and adversely affected.

The size of our user base and the level of our user engagement are critical to our success. Our social networking and gaming platform depends on our ability to maintain and increase the size of our user base and user engagement level. We may be unable to attract and retain users or convert non-paying users into paying users. A decline in our user base may also adversely affect the engagement level of our users and vibrancy of the Yalla community, which may in turn reduce attractiveness of our platform and reduce our monetization opportunities. Any of these factors could have a material and adverse effect on our business, financial condition and results of operations.

Maintaining and improving the size of our user base and level of user engagement is critical to our continued success. To maintain and improve the size of our user base and high level of user engagement, we would have to ensure that we adequately and timely respond to changes in user preferences, adapt to cultural differences in our target markets, and offer new features that may attract new users, among others. There is no guarantee that we could meet any or all of these goals. A number of factors could negatively affect user retention, growth and engagement, including if:

5

If we cannot retain our existing users and expand our user base, the network effect provided by the social nature of our platform will diminish and the popularity of our platform and its profitability may be materially and adversely affected. As a result, our results of operations and financial conditions may be material and adversely affected.

We face risks and uncertainties regarding the growth of the social networking and gaming industry and market acceptance of our platform and services.

The social networking and gaming industry is a relatively new and evolving industry. The growth of the social networking and gaming industry and the level of demand and market acceptance of our platform and services are subject to a high degree of uncertainty. Our future operating results will depend on a number of factors, some of which are beyond our control. These factors include:

If we fail to anticipate and effectively manage these risks and uncertainties, our market share may decrease, and our business, financial condition and results of operations may be materially and adversely affected.

If we fail to effectively manage our growth and control our spending to maintain such growth, our brand, business and results of operations may be materially and adversely affected.

We have experienced a period of rapid growth and expansion that has placed, and continues to place, significant strain on our management and resources. However, given our limited operating history and the rapidly evolving markets in which we compete, we may encounter difficulties as we expand our operations, technology and product development, selling and marketing, and general and administrative capabilities. We cannot assure you that this level of growth will be sustainable in the future. We believe that our continued growth will depend on our ability to attract and retain users, develop an infrastructure to serve and support an expanding user base, increase user engagement levels, explore new monetization avenues, and convert non-paying users to paying users, among others. We cannot assure you that we will be successful with any of the above.

6

To manage our growth and maintain profitability, we expect our costs and expenses to continue to increase in the future as we anticipate that we will need to continue to implement, from time to time, a variety of new and upgraded operational and technology systems. We will also need to expand, train, manage and motivate our workforce and manage our relationships with users. All of these endeavors involve risks and will require substantial management efforts, skills and significant additional expenditures. We expect to continue to invest in our infrastructure in order to enable us to provide our services rapidly and reliably to users. Continued growth would put strains on our ability to maintain reliable service levels for all of our users. Managing our growth will require significant expenditures and involve the allocation of valuable management resources. If we fail to achieve the necessary level of efficiency in our organization as we grow, our business, operating results and financial condition could be harmed.

Our revenue model for social networking and gaming community may not remain effective and we cannot guarantee that our future monetization strategies will be successfully implemented or generate sustainable revenues and profit.

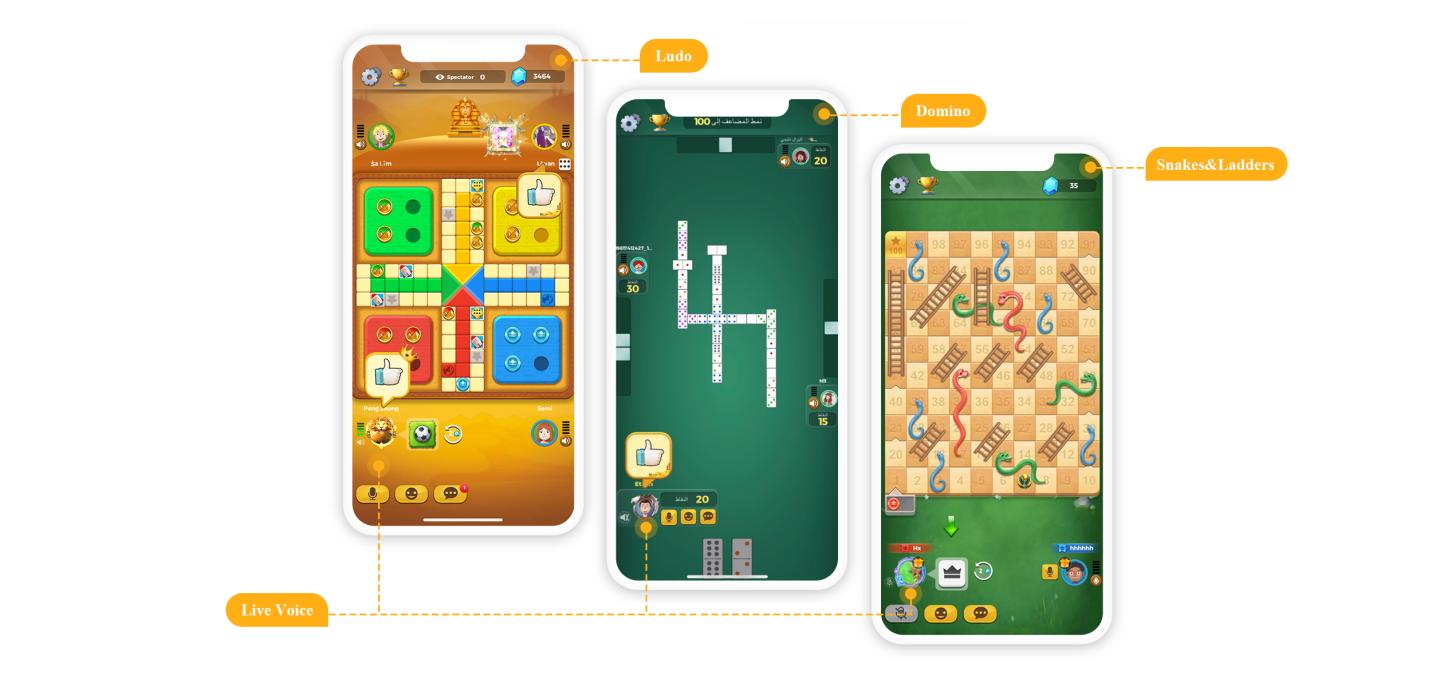

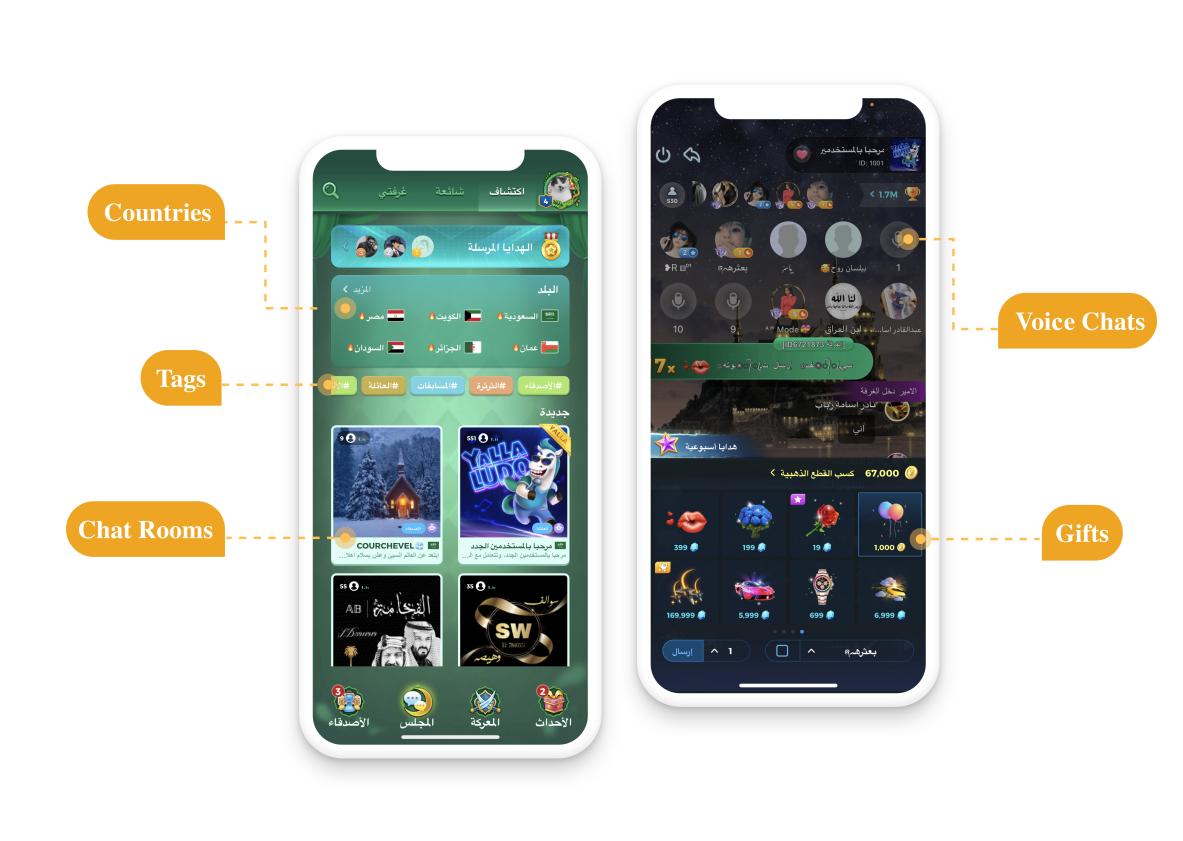

We primarily generate our revenue by providing group chatting and games services. We operate our social networking and gaming platform using a revenue model whereby users can get free access to the basic functions on our platform for our group chatting service but have the options to purchase virtual currencies. Individual users consume virtual currencies to purchase virtual items and upgrade services or play games on our platform. Virtual items primarily consist of various virtual gifts and privileges in chat rooms or games. Upgrade services primarily consist of VIP rights or premium membership on our platform. Although our social networking and gaming business has experienced significant growth in recent years, we may not achieve a similar growth rate in the future, as the user demand for this service may change, decrease substantially or dissipate, or we may fail to anticipate and serve user demands effectively.

Although we design the virtual currency systems on our platform based on our knowledge about users’ preferences and behavior, there can be no assurance that users will continue to purchase and spend our virtual currencies. If users’ spending habits change and they choose to only access our platform for free without additional purchases, we may not be able to continue to successfully implement the virtual currency-based revenue model for our platform, in which case we may have to develop other value-added services or products to monetize our user base. We cannot guarantee that our attempts to monetize our user base will continue to be successful, profitable or widely accepted, and therefore the future revenue and income potential of our business are difficult to evaluate.

If we fail to maintain and enhance our brand or if we incur excessive expenses in this effort, our business, results of operations and prospects may be materially and adversely affected.

We believe that maintaining and enhancing our brand is of significant importance to the success of our business. A well-recognized brand is important to increasing the number of users and the level of engagement of our users. Since we operate in a highly competitive market, brand maintenance and enhancement directly affect our ability to maintain our market position.

We have developed our Yalla brand mostly through word of mouth referrals and advertisement on search engines, app stores and other social media platforms. As we expand, we may conduct various additional marketing and brand promotion activities using more methods and channels to continue promoting our brand. We cannot assure you, however, that these activities will be successful or that we will be able to achieve the brand promotion effect we expect.

In addition, any negative publicity in relation to our platform, services or operations, regardless of its veracity, could harm our brands and reputation. We have sometimes received, and expect to continue to receive, complaints from users regarding the quality of the services we offer. Negative publicity or public complaints may harm our reputation, and if complaints against us are not addressed to users’ satisfaction, our reputation and our market position could be significantly harmed, which may materially and adversely affect our business, results of operations and prospects.

We plan to continue expanding into additional markets where we have limited operating experience and may be subject to increased business, economic and other risks that could affect our operating results.

We are headquartered in the UAE, and MENA is our key market. As of December 31, 2023, our mobile platform was available in over 160 countries, with Yalla in eight languages and Yalla Ludo in two languages. We believe the sustainable growth of our business depends on our ability to increase the penetration of our products in both our existing and new markets. Our continued international operations and global expansion may result in increased costs and expose us to a number of challenges and risks, including:

7

In particular, we face significant challenges to ensure the content presented on our platform is in compliance with the different regulatory frameworks in the jurisdictions in which our platform is available. These jurisdictions may impose stringent restrictions on the content generated by users and onerous requirements for online platforms to monitor content, and our expansion into new markets could cause substantial increases in our compliance costs. Our experience in existing markets may be of limited value in new markets. The different and potentially more stringent regulatory environments in the new markets may increase our risk exposure in our operations. Any incidents related to our failure to comply with applicable laws and regulations or remove inappropriate content could materially and adversely affect our business operations and our reputation.

Our business, financial condition and results of operations may be materially and adversely affected by these challenges and risks associated with our global operations.

We face competition in several major aspects of our business. If we fail to compete effectively, we may lose users, which could in turn materially and adversely affect our business, financial condition and results of operations.

We face competition in several major aspects of our business. We directly compete with other social networking and gaming platforms for users. In addition, we compete with other social networking and gaming platforms. Some of our competitors may have longer operating histories and significantly greater financial, technical and marketing resources than we do, and in turn may have an advantage in attracting and retaining users and potential business partners. In addition, our competitors may have significantly larger user bases and more established brand names and user stickiness than we do and therefore are able to more effectively leverage their user bases and brand names to provide online social network and other products and services, and thereby increase their respective market shares. In addition, as user preferences evolve, new forms of mobile entertainment may emerge in the future and compete with our platform.

If we are not able to compete effectively, our overall user base and level of user engagement may decrease, which could reduce the number of our paying users or make us less attractive to potential users and potential business partners. We may be required to devote additional resources to further increasing our brand recognition and promoting our platform and services, and such additional spending may adversely affect our profitability and may not generate the expected results cost-effectively, or at all. Furthermore, if we are involved in disputes with any of our competitors that result in negative publicity to us, such disputes, regardless of their veracity or outcome, may harm our reputation or brand image and in turn lead to a reduced number of users for our platform. Any legal proceedings or measures we take in response to such disputes may be expensive, time-consuming and disruptive to our operations and divert our management’s attention.

8

Our limited operating history with a relatively new business model in a relatively new market makes it difficult to evaluate our business and growth prospects.

Our business operations commenced in April 2016, with commercialization beginning in the same year. We have experienced growth in the number of active users and total revenues in recent years. Our average MAUs increased from 28.1 million in the three months ended December 31, 2021 to 32.0 million in the same period of 2022, and further increased to 36.2 million in the same period of 2023. Our revenues increased by 11.2% from US$273.1 million in 2021 to US$303.6 million in 2022, and further increased by 5.0% to US$318.9 million in 2023. However, our operational and financial growth in 2021, 2022 and 2023 may not be indicative of our future performance, as our operating results represent a limited history and sample size and may be hard to repeat in the future. We also face fierce competition from new and existing competitors in our target markets, including MENA. As a result, we cannot assure you that we will be able to maintain our growth in such a competitive environment.

Furthermore, many elements of our business are evolving. The markets for our social networking and gaming platform and the related services are relatively new and rapidly developing and are subject to significant challenges, especially in terms of converting non-paying users to paying users, maintaining a stable paying user base and attracting new paying users. Our business plan relies heavily upon an expanding user base and the resulting increased revenues from group chatting and games services, as well as our ability to capitalize on growth opportunities in the social networking and gaming industry and explore other monetization avenues. We may not succeed in any of these aspects.

As the social networking and gaming industry in our target markets is relatively young, there are few proven methods of projecting user demand or available industry standards on which we can rely. Our current monetization method is also at a relatively preliminary stage. For example, if we fail to properly manage the volume and price of our virtual items or upgrade services, our users may be less likely to purchase them. We cannot assure you that our monetization attempts will be successful, profitable or accepted by users, and therefore it may be difficult to gauge the income potential of our business.

Addressing these risks and uncertainties will require significant capital expenditures and allocation of valuable management and employee resources. If we fail to successfully address any of the above risks and uncertainties, the size of our user base, our revenues and our operating margin may decline.

Our community culture is vital to our success. Our operations may be materially and adversely affected if we fail to maintain the culture of the Yalla community.

We have cultivated an interactive and vibrant online community centered on our social networking and gaming platform. We strive to provide premium user experience by continuously improving user interfaces and features of our platform to adapt to the relevant local cultures and by encouraging social interactions among users. We believe that maintaining and promoting such a vibrant community culture is critical to retaining and expanding our user base. We have taken multiple initiatives to preserve our community culture and values. Leveraging our insights into MENA culture and local user preferences, we infuse our user interfaces with local cultural elements. For non-English versions of Yalla, we update the user interface with color themes and logos related to specific local holidays to celebrate with our users, and virtual gifts are typically designed based on local customs. However, there can be no assurance that we will be able to maintain our community culture and remain as the preferred platform for our target users. For example, frictions among our users and inflammatory comments posted by Internet trolls and any inappropriate handling of these frictions may damage our community culture and brand image. Any failure to timely screen out and remove illegal or inappropriate content posted on our platform or to identify and close fake accounts of Internet trolls could also adversely affect users’ perception of and experience on our platform. Any damage to our community culture could materially and adversely affect our business prospects and results of operations.

Our business is highly dependent on the proper functioning and improvement of our information technology systems and infrastructure. Our business and operating results may be harmed by service disruptions, or by our failure to timely and effectively scale up and adjust our existing technology and infrastructure.

The popularity of our platform and services and our ability to further monetize our user base depend on our ability to adapt to rapidly changing technologies as well as our ability to continually innovate in response to evolving consumer demands and expectations and market competition. Our ability to provide a superior user experience on our platform depends on the continuous and reliable operation of our IT systems.

9

We may not be able to procure sufficient bandwidth in a timely manner or on acceptable terms or at all. Failure to do so may significantly impair user experience on our platform and decrease the overall effectiveness of our platform to users. Our IT systems are vulnerable to damage or interruption as a result of fires, floods, earthquakes, power losses, telecommunications failures, undetected errors in software, computer viruses, hacking and other attempts to harm our IT systems. Disruptions, failures, unscheduled service interruptions or a decrease in connection speeds could damage our reputation and cause our users to migrate to our competitors’ platforms. If we experience frequent or constant service disruptions, whether caused by failures of our own IT systems or those of third-party service providers, our user experience may be negatively affected, which in turn may have a material and adverse effect on our reputation and business. We may not be successful in minimizing the frequency or duration of service interruptions. As the number of our users increases and our users generate more content on our platform, we may be required to expand and adjust our technology and infrastructure to continue to reliably store and monitor content generated by users on our platform. It may become increasingly difficult to maintain and improve the performance of our platform, particularly during peak usage times, as our services become more complex and as our user base increases.

We use third-party services and technologies in connection with our business, and any disruption to the provision of these services and technologies to us could result in negative publicity and a slowdown in the growth of our user base, which could materially and adversely affect our business, financial condition and results of operations.

Our business partially depends on services provided by, and relationships with, various third parties. For example, we source audio processing and multi-party real-time communication solutions from third parties to support all of our Yalla rooms and we use servers of third parties for data storage and processing. We also rely on third parties to provide software and other IT services to us. If such third parties terminate their services to us or if they encounter technological or other difficulties, we may not be able to find alternative solutions in a timely manner or on terms satisfactory to us. In particular, there are only a limited number of providers of high quality audio processing solutions in the market. In addition, certain third-party software we use in our operations is currently publicly available free of charge. If the provider of any such software decides to charge users or no longer makes the software publicly available, we may need to incur significant costs to obtain licensing, find replacement software or develop it on our own. If we are unable to obtain licensing, find or develop replacement software at a reasonable cost, or at all, our business and operations may be adversely affected.

In addition, we process purchases of our virtual currencies through third-party payment platforms. If any of these third-party payment platforms suffer from security breaches or leakage of user information, users may lose confidence in such payment systems or channels and refrain from purchasing our virtual currencies, in which case our results of operations would be negatively impacted. See “—The security of operations of, and fees charged by, third-party payment platforms may have a material adverse effect on our business and results of operations.”

Certain of our customer service staff are employees of third-party service providers incorporated in Egypt and the UAE. If the third parties’ employees fail to provide satisfactory services to our users, we may not be able to rectify the deficiency in a timely manner, and our business could be adversely affected. Labor or contractual disputes could also arise among us, the third-party service providers and/or the relevant customer service staff, which could cause disturbance of services to our users.

We exercise no control over the third parties with whom we have business arrangements. If such third parties increase their prices, fail to provide their services effectively, terminate their services or agreements or discontinue their relationships with us, we could suffer service interruptions, reduced revenues or increased costs, any of which may have a material adverse effect on our business, financial condition and results of operations.

10

We face risks related to health epidemics, pandemics, natural disasters and other outbreaks, which could significantly disrupt our operations.

Our business could be adversely affected by the effects of epidemics or pandemics. In recent years, there have been outbreaks of epidemics in MENA, China and globally. Our business operations could be disrupted if any of our employees are suspected of having COVID-19, H1N1 flu, avian flu or another epidemic or pandemic, since it could require our employees to be quarantined and/or our offices to be disinfected. In addition, our results of operations could be adversely affected to the extent that the outbreak harms the economy in our target markets in general and the mobile Internet industry in particular. For example, as a result of the COVID-19 outbreak, government measures designed to control the spread of the virus, such as restrictions on travel and the closing-down of businesses to the public, resulted in a decline of economic activities in our target markets. In addition, we implemented working from home arrangements for our employees as a result of the outbreak. If the pandemic resurges, we may be subject to further negative impact on our business operations. To the extent the COVID-19 pandemic adversely affects our business and financial results, it may also have the effect of heightening many of the other risks described in this “Item 3. Key Information—D. Risk Factors” section, such as those relating to our ability to grow our user base and implement our monetization strategies.

We are also vulnerable to natural disasters and other calamities. It is possible that we may be unable to recover certain data in the event of a server failure. We cannot assure you that any backup systems will be adequate to protect us from the effects of fire, floods, typhoons, earthquakes, power loss, telecommunications failures, break-ins, war, riots, terrorist attacks or similar events. Any of the foregoing events may give rise to server interruptions, breakdowns, system failures, technology platform failures or Internet failures, which could cause the loss or corruption of data or malfunctions of software or hardware as well as adversely affect our ability to provide services on our platform.

Our business is sensitive to global political and economic conditions. A severe or prolonged downturn in the global economy could materially and adversely affect our business, financial condition and results of operations.

The global macroeconomic environment is facing challenges. There is considerable uncertainty over the long-term effects of the expansionary monetary and fiscal policies adopted by the central banks and financial authorities of some of the world’s leading economies, including the United States. There have been concerns over unrest and terrorist threats in MENA, Europe and Africa, which have resulted in volatility in oil and other markets, and concerns over the conflicts involving Ukraine, Syria and North Korea.

We are headquartered in the UAE. MENA is our key market. While the UAE is seen to have a relatively stable political environment, certain other jurisdictions in MENA are not. In particular, since early 2011 there have been increased political risks in several countries in the region, including Algeria, Bahrain, Egypt, Libya, Morocco, Oman, Saudi Arabia, Tunisia and Syria. These risks have ranged from public demonstrations to, in extreme cases, armed conflicts and civil war and have given rise to a number of regime changes and increased political uncertainty across the region. In particular, the armed conflicts in Syria, Iraq and Yemen have the potential to further destabilize the region, further increase uncertainty and have a material negative impact on the regional economy. In January 2020, the United States conducted a drone strike that killed the Iranian general Qasem Soleimani, which escalated tensions between the United States and Iran and heightened the risk for a military conflict between the two countries. The fluctuations in oil price may materially and adversely affect the economic conditions in MENA. Further, the MENA region is currently subject to a number of active and potential armed conflicts, including the Israel-Gaza conflict and the Red Sea crisis. Unrest in the region has implications for the wider global economy and may negatively affect market sentiment towards other countries in the region, including the UAE. Although the UAE continues to exercise de-escalation diplomacy and self-restraint, any continuation of, or increase in, international or regional tensions or any military action may have a destabilizing impact on the MENA region. There can be no assurance that tensions will not continue to escalate in the region, or that further unrest will not happen. The financial, political and general economic conditions prevailing from time to time across MENA may affect mobile users’ willingness and ability to spend on the mobile Internet and have a material adverse impact on our performance and operating results. It is not possible to predict the occurrence of events or circumstances such as war or hostilities, or the impact of such occurrences, and no assurance can be given that we would be able to sustain our current profit levels if adverse political events or circumstances were to occur, particularly in MENA. A general downturn or instability in certain sectors of MENA’s economies could have an adverse effect on our business. In addition, we may be affected by unexpected changes in regulations and enforcement, nationalization of assets and other governmental actions by the host countries, government regulations that favor local competitors, changing taxation policies, restrictions on converting foreign currencies into U.S. dollars, most of which are beyond our control. Investors should also note that our business could be adversely affected by political, economic or related developments both within and outside MENA because of inter-relationships within the global financial markets.

11

Significant political, social and economic instability in one or more of our markets could have a material adverse effect on our business, financial condition and results of operations. Any severe or prolonged slowdown in the global economy may also materially and adversely affect our business, results of operations and financial condition. In addition, continued turbulence in the international markets may adversely affect our ability to access capital markets to meet liquidity needs.

We have incurred and may incur substantial share-based compensation expenses.

On June 22, 2018, we adopted a share incentive plan, which was amended and restated on November 19, 2019 and was further amended in June 2020, or the 2018 Plan. See “Item 6. Directors, Senior Management and Employees—B. Compensation—Share Incentive Plans” for a detailed discussion. As of December 31, 2023, 23,460,740 Class A ordinary shares were issuable upon the exercise of outstanding share options under the 2018 Plan. On August 31, 2020, we adopted the 2020 Plan. See “Item 6. Directors, Senior Management and Employees—B. Compensation—Share Incentive Plans” for a detailed discussion. As of December 31, 2023, 6,989,288 Class A ordinary shares were issuable upon the exercise of outstanding share options under the 2020 Plan. We are required to recognize compensation expense for an equity award over the period in which the recipient is required to provide service in exchange for the equity award. We recognized share-based compensation expenses in the amount of US$17.9 million in 2023. As of December 31, 2023, the total unrecognized compensation expense associated with share options amounted to US$22.3 million. If additional share options or other equity incentives are granted to our employees, directors or consultants in the future, we will incur additional share-based compensation expense and our results of operations will be further adversely affected.

Our corporate actions are substantially controlled by our Chairman and Chief Executive Officer, Mr. Tao Yang, who has the ability to control or exert significant influence over important corporate matters that require approval of shareholders, which may deprive you of an opportunity to receive a premium for your ADSs and materially reduce the value of your investment.

Our third amended and restated memorandum and articles of association provides that in respect of all matters subject to a shareholders’ vote, each Class A ordinary share is entitled to one vote and each Class B ordinary share is entitled to 20 votes. Mr. Tao Yang, our Chairman and Chief Executive Officer, beneficially owns all the Class B ordinary shares issued and outstanding and exercises 84.5% of the aggregate voting power of our total issued and outstanding shares as of March 31, 2024. As a result, Mr. Tao Yang has the ability to control or exert significant influence over important corporate matters; investors may be prevented from affecting important corporate matters involving our company that require approval of shareholders, including:

These actions may be taken even if they are opposed by our other shareholders, including the holders of the ADSs. Furthermore, this concentration of ownership may also discourage, delay or prevent a change in control of our company, which could have the dual effect of depriving our shareholders of an opportunity to receive a premium for their shares as part of a sale of our company and reducing the price of the ADSs. As a result of the foregoing, the value of your investment could be materially reduced.

12

User growth and engagement depend upon effective interoperation with mobile operating systems, networks, devices and standards that we do not control.

We make our mobile applications available across a variety of mobile operating systems and devices. We are dependent on the effective interoperation of our mobile applications with mobile operating systems, such as Android and iOS, networks, devices and standards, which we do not control. Any changes in such mobile operating systems, networks, devices or standards that degrade the functionality of our mobile applications or give preferential treatment to competitive products could adversely affect usage of our mobile applications and our ability to deliver high quality user experience. We may not be successful in developing relationships with key participants in the mobile industry or in developing mobile applications that operate effectively with these mobile operating systems, networks, devices and standards. In the event that it is difficult for our users to access and use our mobile applications, particularly on their mobile devices, our user growth and user engagement could be harmed, and our business and operating results could be adversely affected.

User misconduct and misuse of our platform may adversely impact our brand image, and we may be held liable for information or content displayed on, retrieved from or linked to our platform, or distributed to our users, and the relevant local authorities may impose restrictions on access to our platform.

Our social networking and gaming platform enables users to chat, play games and engage in various forms of other online communications in real time. We also allow users to share texts, images and other content with each other through our platform. However, our platform does not require real-name registration and identity verification of our users. In addition, because all of the audio and text communications on our platform are conducted in real time, we are unable to examine the content generated by our users on air before they are streamed on our platform. We require all users to agree to our terms of service upon account registration. Our terms of service set out types of content strictly prohibited on our platform, and we have also developed a content monitoring system that utilizes primarily automation, as well as manual screening, to filter inappropriate content. We also encourage users to report any non-compliance of our terms of service. However, due to the immense quantity of user-generated content on our platform, we may not be able to detect all violations of our terms of service or inappropriate or illegal content streamed, displayed or exchanged over our platform, or determine the type of content or actions that may result in liability to us. Our automated screening system may fail to timely screen out and remove inappropriate or illegal content. As such, relevant government authorities could identify inappropriate or illegal content on our platform, which could lead to restrictions on access to our platform in the relevant jurisdictions. Even if we manage to identify and remove offensive content, we may still be held liable. Negative publicity of incidents related to inappropriate or illegal content on our platform or any misuse of our platform by users could also adversely affect our brand image. As a result, our ability to retain or increase our user base and user engagement may be adversely affected, we may not be able to maintain or grow our revenues as anticipated, and our business prospects and financial results could be adversely affected.

13

Additionally, it is possible that our users may engage in illegal, obscene or incendiary conversations or activities on or through our platform that may be deemed illegal under the relevant local laws and regulations or inappropriate under local cultures or customs, for which we may be subject to potential liability. Content generated, including text and images posted, by our users may infringe on rights of others. In addition, because we offer our mobile applications in a large number of jurisdictions, and we have not implemented any user screening procedures, we cannot ensure that our provision of online social networking and gaming services to all users is in compliance with all applicable laws. The jurisdictions in which our mobile applications are available may have regulations governing the distribution of information over the Internet. These regulations may prohibit the display of content that, among other things, impairs the public interest, or is obscene, superstitious, fraudulent or defamatory. For example, the regulations in some countries in MENA and Southeast Asia prohibit online social networking platforms from being used for dating, pornographic or gambling purposes. While we do not believe our mobile applications are provided to users for any of these purposes, we cannot control how users interact online or offline other than through content monitoring on our mobile applications. We may be subject to fines or other disciplinary actions as prescribed under the relevant local laws and regulations. We may also face claims for defamation, libel, negligence, aiding-and-abetting liability, infringement of copyright, patent, trademark or other intellectual property or third-party rights, other unlawful activities or other theories and claims based on the nature and content of the information delivered on or otherwise accessed through our platform. For example, if any of our users suffers or alleges to have suffered physical, financial or emotional harm as a result of content posted on or conduct initiated from our platform, we may face legal actions initiated by the affected user. In response to such lawsuits, government authorities may take regulatory actions against us based on alleged non-compliance with applicable laws and regulations, such as prohibitions of illegal or inappropriate content on mobile platforms. Defending any such actions could be costly and involve significant time and attention of our management and other resources, which would materially and adversely affect our business and operations. Moreover, the costs of compliance with these regulations may increase as a result of the expansion of our platform, which may adversely affect our results of operations. We may also be required to restrict, discontinue or make other changes to certain features and services provided on our mobile applications, and we may even be prohibited from providing our mobile applications to users in certain jurisdictions. As a result, our business may suffer, our user base, revenue growth and profitability may be materially and adversely affected, and the price of our ADSs may decline.

Malicious software and applications may affect user experience, which could reduce our ability to attract users and materially and adversely affect our business, financial condition and results of operations.

Malicious software and applications may interrupt the operations of our platform and pass on such malware to our users which could adversely hinder user experience. We cannot guarantee that we will be able to successfully block these attacks. If users experience a malware attack by using our platform, our users may associate the malware with our platform. As a result, our reputation, business, and results of operations could be materially and adversely affected.

The security of operations of, and fees charged by, third-party payment platforms may have a material adverse effect on our business and results of operations.

Currently, we process purchases of our virtual currencies through third-party payment platforms. In all of these payment transactions, secured transmission of confidential information such as the users’ credit card numbers and personal information over public networks and through the payment platforms is essential to maintaining consumer confidence.

We do not have control over the security measures of our third-party payment platforms. Any security breaches of a payment platform that we use could expose us to litigation and possible liability for failing to secure confidential customer information and could, among other things, damage our reputation and the perceived security of the other payment platforms that we use. If a well-publicized Internet or mobile network security breach were to occur, users may become reluctant to purchase our virtual currencies, even if such breach did not involve payment systems or methods used by us. In addition, there may be billing software errors that would damage customer confidence in these payment platforms. If any of the above were to occur and damage our reputation or the perceived security of the payment platforms we use, we may lose paying users and users may be discouraged from spending on our platform, which may have a material adverse effect on our business.

14

In addition, there are currently only a limited number of reputable third-party payment systems in our target markets. If any of these major payment systems decides to cease to provide services to us, or significantly increases the fee rates it charges us for using its payment systems for our virtual currencies, our results of operations may be materially and adversely affected.

Users’ payments to purchase and use of virtual currencies on our mobile applications could expose us to additional regulatory requirements and other risks that could be costly or difficult to comply with.

We may be subject to a variety of laws and regulations in the various jurisdictions where our users are located in respect of the users’ payments to purchase virtual currencies on our applications through third-party payment platforms, including those governing money transmission, gift cards and other prepaid access instruments, electronic funds transfers, anti-money laundering, counter-terrorist financing, gambling, banking and lending. In some jurisdictions, the application or interpretation of these laws and regulations may be unclear. Our efforts to comply with these laws and regulations could be costly and result in diversion of management time and effort and may still not guarantee compliance. In the event that we are found to be in violation of any such legal or regulatory requirements, we may be subject to monetary fines or other penalties, or we may be required to make product or marketing practice changes, any of which could have an adverse effect on our business and financial results. In addition, we may be subject to a variety of additional risks as a result of these payments by users, including potential fraudulent or otherwise illegal activity by users, employees, or third parties.

Changes in laws and regulations related to the Internet and mobile Internet, perceptions toward the use of social media and changes in Internet infrastructure itself may diminish the demand for our platform or products and could adversely affect our business and results of operations.

The success of our business depends upon the continued use of the Internet or mobile Internet and social media. Relevant government regulatory authorities, including those in MENA, may adopt laws or regulations that restrict the use of the Internet, mobile Internet or social media in the future. In addition, government agencies or private organizations may impose additional taxes, fees or other charges for accessing the Internet. These laws, taxes, fees or charges could limit the use of the Internet or mobile Internet or decrease the demand for online social media.

In addition, the performance of our platform could be adversely affected due to delays in the development or adoption of new standards and protocols to handle increased demands of Internet activity, security, reliability, cost, ease-of-use, accessibility and quality of services. The performance of the Internet and mobile Internet has been adversely affected by “viruses,” “worms” and similar malicious programs, as well as the risks associated with other types of security breaches. If the use of the Internet or mobile Internet is reduced as a result of these or other issues, then demand for our platform could decline, which could adversely affect our revenue, business, results of operations and financial condition.

Concerns about collection, use, retention, transfer, disclosure, processing and security of personal data could damage our reputation and deter current and potential users from using our platform and services, or subject us to significant compliance costs or penalties, which could materially and adversely affect our business, financial condition and results of operations.

Concerns about our practices with regard to the collection, use, retention, transfer, disclosure, processing and security of personal information or other privacy-related matters, such as cybersecurity breaches, misuse of personal data and data sharing without necessary safeguards, even if unfounded, could damage our reputation and operating results. MENA is our key market, and we have data centers with servers that collect and process our user data mainly in Germany and the United States. In addition, we also store data locally in Oman, Qatar and UAE. As of December 31, 2023, our platform was available in over 160 countries. The United Arab Emirates issued Federal Decree-Law No. 45 of 2021 regarding the Protection of Personal Data which came into effect on January 2, 2022. See “Item 4. Information on the Company—B. Business Overview—Regulation—United Arab Emirates—Regulations Relating to Technology Media and Telecommunications—Data protection laws” for details. Furthermore, the regulatory frameworks regarding privacy issues in many jurisdictions are constantly evolving and can be subject to significant changes from time to time, and therefore we may not be able to comprehensively assess the scope and extent of our compliance responsibility at a global level. For example, the PRC regulatory frameworks with regard to data security and data protection is evolving. The PRC Civil Code, the PRC Cyber Security Law, the Personal Information Protection Law, the Provisions on the Cyber Protection of Children’s Personal Information, the Regulation on the Protection of Minors in Cyberspace and the PRC Data Security Law set forth the regime to protect individual privacy and personal data security in general by requiring internet service providers to collect data in accordance with the laws and in proper manner, and obtain consents from internet users prior to the collection, use or disclosure of internet users’ personal data, and the PRC Cyber Security Law sets high requirements for the operational

15

security of facilities deemed to be part of China’s “critical information infrastructure.” Furthermore, the Cybersecurity Review Measures, the Measures for the Security Assessment of Data Cross-border Transfer and the Provisions on Promoting and Regulating Cross-border Data Flow require that a “network platform operator” that possesses personal information of more than one million users apply for a cybersecurity review when seeking overseas listing, and that a data processor apply for security assessment for its cross-border data transfer based on the importance and amount of the data transferred. See “Item 4. Information on the Company—B. Business Overview—Others—Regulations Relating to Personal Privacy and Data Protection.” The developing requirements relating to clear and prominent privacy notices (including in the context of obtaining informed and specific consents to the collection and processing of personal data, where applicable) may potentially deter users from consenting to certain uses of their personal information. In general, negative publicity of us or our industry regarding actual or perceived violations of our users’ privacy-related rights, including fines and enforcement actions against us or other similarly placed businesses, may also impair users’ trust in our privacy practices and make them reluctant to give their consent to share their data with us.

This risk is enhanced in certain jurisdictions with stringent, extra-territorial data protection laws, and the three regulations that have significant impacts on our industry are the General Data Protection Regulation (EU) 2016/679 that became applicable on May 25, 2018, or the GDPR, the California Consumer Privacy Act that became effective on January 1, 2020, or the CCPA, and the California Privacy Right Act that became effective on January 1, 2023, or the CPRA. The GDPR places stringent obligations and operational requirements on processors and controllers of personal data, including, for example, requiring expanded disclosures to data subjects about how their personal data is to be used, limitations on retention of information, mandatory data breach notification requirements, and higher standards for data controllers to demonstrate that they have obtained either valid consent or have another legal basis in place to justify their data processing activities. The GDPR also enhances the rights of data subjects, who may, for example, request access to their personal data, the deletion and amendment of their personal data, or to have their personal data transferred to another service provider. Data subjects also have the right to be compensated for any material or non-material damage suffered as a result of a controller or processor’s non-compliance with the GDPR. Under the GDPR, data protection supervisory authorities are also given various enforcement powers, including that they can levy fines of up to EUR20 million or up to 4% of an organization’s total worldwide annual turnover for the preceding financial year, whichever is higher, for non-compliance, which significantly increases our potential financial exposure for non-compliance. While the GDPR provides a more harmonized approach to data protection regulation across the EU member states, it also gives EU member states certain areas of discretion and therefore laws and regulations in relation to certain data processing activities may differ on a member state by member state basis, which could further limit our ability to use and share personal data and could require localized changes to our operating model. The EU has also released a proposed Regulation on Privacy and Electronic Communications 2002, or the ePrivacy Regulation, to replace the EU’s current Privacy and Electronic Communications Directive, or the ePrivacy Directive, to, among other things, achieve a greater harmonization among EU member states and better align the rules governing online tracking technologies and electronic communications (for example, in relation to the use of cookies and similar technologies and protection against email spam) with the requirements of the GDPR. While the ePrivacy Regulation was originally intended to be adopted on May 25, 2018 (alongside the GDPR), it is currently going through the European legislative process. The current draft of the ePrivacy Regulation significantly increases fining powers to the same levels as GDPR and may lead to broader restrictions on our online activities, including efforts to understand followers’ Internet usage and promote ourselves to them.

Outside of the EU, many jurisdictions have adopted or are adopting new data privacy and data protection laws, which may result in additional expenses to us and increase the risk of non-compliance. For example, the CCPA creates new data privacy rights for users and new operational requirements for businesses. The CCPA gives California residents rights to access and delete their personal information, opt out of sales of personal information and receive detailed information about how their personal information is used. The CCPA provides for civil penalties for violations, as well as a private right of action for data breaches that is expected to increase data breach litigation. The CPRA builds on the CCPA and further supplements and strengthens the compliance requirements within CCPA in many aspects. For example, the CPRA expands the scope of information that consumers can request from companies, further allows California residents to opt out of both personal data sales and data sharing, supplements a 12-month waiting period to re-obtain the consent for the right of opt-in of minors, and entitles California residents to correct their personal information, restrict the processing of, access to, and opt-out of automated decision making for sensitive personal information, and request the company to transfer their personal information to another service provider. The CPRA also imposes greater penalties for violations involving the personal information of minors. Fines for such violations can be up to three times the amount of the standard penalties under the law. Furthermore, we may need to comply with regulations in other territories that may impose further onerous compliance requirements, such as data localization, which prohibits companies from storing data relating to resident individuals in data centers outside the jurisdiction. The proliferation of such laws within jurisdictions and countries in which we operate may result in conflicting and contradictory requirements.

16

While we strive to comply with our data privacy guidelines as well as all applicable data protection laws and regulations or contract obligations, any failure or perceived failure to comply, including in relation to lawful basis of data processing and providing users with sufficient information with respect to our use of their personal data, may result in proceedings or actions against us, including fines and penalties on us, by government entities or proceedings or actions against us by our business partners or others (including enforcement orders requiring us to cease collecting or processing data in a certain way), and could damage our reputation and discourage current and future users from using our mobile applications. In addition, compliance with applicable laws on data privacy requires substantial expenditure and resources, including to continually evaluate our policies and processes and adapt to new requirements that are or become applicable to us on a jurisdiction-by-jurisdiction basis, which would impose significant burdens and costs on our operations or may require us to alter our business practices. Concerns about the security of personal data could also lead to a decline in general Internet usage, which could lead to lower registered, active or paying user numbers on our platform. Furthermore, if the local government authorities in our target markets require real-name registration for users of our platform, the growth of our user numbers may slow down and our business, financial condition and results of operations may be adversely affected. A significant reduction in registered, active or paying user numbers could lead to lower revenues, which could have a material and adverse effect on our business, financial condition and results of operations.

If we fail to prevent security breaches, cyber-attacks or other unauthorized access to our systems or our users’ data, we may be exposed to significant consequences, including legal and financial exposure and loss of users, and our reputation, business and operating results may be materially and adversely affected.

We collect, store, transmit and process personal and other sensitive data generated by our users through their interactions with our apps. We may be exposed to risks of security breaches or unauthorized access to or cyber-attacks on our systems or the data we store. Our efforts to protect our data may be unsuccessful due to software “bugs,” system errors or other technical deficiencies, mistakes or malfeasance of our employees or contractors, vulnerabilities of our vendors and service providers, or other cybersecurity-related vulnerabilities. Although we have developed systems and processes that are designed to prevent and detect security breaches and protect our users’ data, we cannot guarantee that such measures will be sufficient defenses against the evolving techniques used to obtain unauthorized access, disable or degrade services or sabotage systems. Any failure to prevent, detect, or mitigate security breaches, cyber-attacks or other unauthorized access to our systems, theft of users’ accounts or disclosure of our users’ data, including personal information, could result in loss or misuse of such data, interruptions to the services we provide, diminished user experience, loss of user confidence and trust in our products, impairment of our network and technological infrastructure, and harm to our reputation and business, significant legal and financial exposure and potential lawsuits brought by private individuals or regulators. In addition, as we have servers mainly in data centers in Germany and the United States, and we also store data locally in Oman, Qatar and UAE, we may incur significant costs in protecting them against, or remediating, security breaches and cyber-attacks.

We may be required to obtain and maintain licenses and approvals relating to Internet or telecommunications services in certain jurisdictions.

Our platform is available in over 160 countries, and some of these countries may require us to obtain certain licenses, permits or approvals or conduct certain registrations or filings with local authorities in relation to our mobile applications. Considerable uncertainties exist in the interpretation and implementation of laws and regulations governing our business activities in certain jurisdictions, including MENA.

Our mobile applications enable voice-based, real-time communications on the Internet. As a result, we may be deemed to offer regulated Internet or telecommunications services that require licenses in certain jurisdictions. For example, the law of Saudi Arabia is unclear about whether we are required or eligible to obtain licenses for our provision of audio social media services, including the Voice Over Internet Protocol, or VoIP, license. It is also unclear whether our mobile applications fall into regulated telecommunications services or violate any other local telecommunication requirements in the jurisdictions in which our mobile applications are available.

In addition, we may be found by regulators and/or licensed telecommunications service providers in the UAE to be providing VoIP services without the requisite licenses. VoIP services are specifically regulated under Voice over Internet Protocol Policy, or VoIP Policy, issued by the UAE Telecommunications and Digital Government Regulatory Authority, or the TDRA, on December 30, 2009. “VoIP Services” are defined for the purposes of the VoIP Policy as “all of the services and technologies that allow transmitting, receiving, delivering and routing of voice telecommunications by means of Internet Protocol (IP).” Yalla apps’ free voice chat function may be deemed VoIP services, as such chat function delivers voice communications and multimedia content over the Internet.

17

Based on a strict interpretation of laws and regulations, VoIP services can only be used in the UAE in limited circumstances where:

Under the Telecoms Law, it is a criminal offense that may be penalized by a fine between AED50,000 (US$13,615) and AED1,000,000 (US$272,294) and/or imprisonment of up to two years to provide regulated telecommunication services without being licensed to do so. It is the supplier, rather than the user, that commits this offense. In practice, the main enforcement action taken against unlicensed VoIP service providers is for the licensed service providers to block the VoIP service in the UAE.

There are uncertainties in the UAE market regarding the use of VoIP services, as despite the apparently strict legal position concerning the use of VoIP services and the blocking of certain well-known international VoIP service brands in the UAE, many users in the UAE can in fact use various other VoIP applications, such as certain online gaming platforms. Due to such uncertainties around the use of VoIP, there is no guarantee that the chat room features of our platform will remain available in the UAE in the future.

As of March 31, 2024, we had not obtained any VoIP or other telecommunications license and we have not received any notification from regulators or licensed telecommunications service providers alleging that we provide unlicensed VoIP or telecommunications services. We are nonetheless subject to uncertainties in laws and regulations, including those in MENA. We cannot assure you that we are exempt from the licensing requirements relating to Internet or telecommunications services in the relevant jurisdictions. If our mobile applications were found by a regulatory authority to be in violation of any applicable laws or regulations, such as the lack of requisite approvals or licenses, we may no longer be able to offer our mobile applications in the relevant jurisdiction, and we may also be subject to other penalties. Any such penalties or enforcement actions may disrupt our business operations and materially and adversely affect our business, financial condition and results of operations.

Third parties may register trademarks or domain names or purchase Internet search engine keywords that are similar to our trademarks, brands or mobile applications, or misappropriate our data and copy our platform, all of which could cause confusion to our users, divert users away from our platform and services or harm our reputation.

Competitors and other third parties may (i) register trademarks or domain names or (ii) in Internet search engine advertising programs and in the header and text of the resulting sponsored links or advertisements, purchase keywords, which are confusingly similar to our trademarks, brands or mobile applications in order to divert potential customers from us to their websites or mobile applications. Preventing such infringing, inappropriate or damaging practices is inherently difficult. If we are unable to prevent such practices, competitors and other third parties may continue to drive potential online customers away from our platform to competing, irrelevant or potentially offensive platforms, which could harm our reputation and cause us to lose revenue.