Table of Contents

As filed with the Securities and Exchange Commission on July 6, 2020.

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM F-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Vasta Platform Limited

(Exact Name of Registrant as Specified in its Charter)

| The Cayman Islands | 8200 | N/A | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

Av. Paulista, 901, 5th Floor

Bela Vista

São Paulo – SP, 01310-100

Brazil

+55 11 3133-7311

(Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant’s Principal Executive Offices)

Cogency Global Inc. 10 East 40th Street, 10th Floor New York, NY 10016 (212) 947-7200

(Name, address, including zip code, and telephone number, including area code, of agent for service)

| Copies to: | ||

| Manuel Garciadiaz (212) 450-4000 |

Grenfel Calheiros Simpson Thacher & Bartlett LLP Av. Presidente Juscelino Kubitschek, 1455 12th Floor, Suite 121 São Paulo, SP 04543-011 Brazil +55-11-3546-1011 | |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this registration statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ☐

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933.

Emerging growth company ☒

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

CALCULATION OF REGISTRATION FEE

|

| ||||

| Title of Each Class of Securities to be Registered |

Proposed Maximum Aggregate Offering Price(1)(2) |

Amount of Registration Fee(3) | ||

| Class A common shares, par value US$0.00005 per share |

US$100,000,000 | US$12,980 | ||

|

| ||||

|

| ||||

| (1) | Estimated solely for the purpose of computing the amount of the registration fee pursuant to Rule 457(o) under the Securities Act of 1933, as amended. |

| (2) | Includes Class A common shares to be sold upon the exercise of the underwriters’ option to purchase additional shares. See “Underwriting.” |

| (3) | Calculated pursuant to Rule 457(o) based on an estimate of the proposed maximum aggregate offering price. |

The Registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the registration statement shall become effective on such date as the Commission, acting pursuant to such Section 8(a), may determine.

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED , 2020

PRELIMINARY PROSPECTUS

Class A Common Shares

Vasta Platform Limited

(incorporated in the Cayman Islands)

This is an initial public offering of the Class A common shares, US$0.00005 par value per share of Vasta Platform Limited, or Vasta. Vasta is offering of the Class A common shares to be sold in this offering.

Prior to this offering, there has been no public market for our Class A common shares. It is currently estimated that the initial public offering price per Class A common share will be between US$ and US$ . We have applied to list our Class A common shares on the Nasdaq Global Market, or Nasdaq, under the symbol “ .”

Following this offering, our existing shareholder, Cogna Educação S.A., or Cogna, will beneficially own % of our outstanding share capital, assuming no exercise of the underwriters’ option to purchase additional shares referred to below. The shares held by Cogna are Class B common shares, which carry rights that are identical to the Class A common shares being sold in this offering, except that (1) holders of Class B common shares are entitled to 10 votes per share, whereas holders of our Class A common shares are entitled to one vote per share, (2) Class B common shares have certain conversion rights and (3) holders of Class B common shares are entitled to preemptive rights in the event that additional Class A common shares are issued in order to maintain their proportional ownership interest. For further information, see “Description of Share Capital.” As a result, Cogna will control approximately % of the voting power of our outstanding share capital and % of our total equity ownership following this offering, assuming no exercise of the underwriters’ option to purchase additional shares.

We are an “emerging growth company” under the U.S. federal securities laws as that term is used in the Jumpstart Our Business Startups Act of 2012 and will be subject to reduced public company reporting requirements for as long as we remain an emerging growth company. In addition, following the offering, we will be a “controlled company” within the meaning of the Nasdaq corporate governance standards and as such plan to rely on available exemptions from certain Nasdaq corporate governance requirements. Investing in our Class A common shares involves risks. See “Risk Factors” beginning on page 31 of this prospectus.

| Per Class A common share |

Total | |||||||

| Initial public offering price |

US$ | US$ | ||||||

| Underwriting discounts and commissions |

US$ | US$ | ||||||

| Proceeds, before expenses, to us(1)(2) |

US$ | US$ | ||||||

| (1) | See “Underwriting” for a description of all compensation payable to the underwriters. |

| (2) | Assumes no exercise of the underwriters’ option to purchase additional Class A common shares. |

We have granted the underwriters an option for a period of 30 days from the date of this prospectus to purchase up to additional Class A common shares at the initial public offering price, less underwriting discounts and commissions.

Neither the U.S. Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the Class A common shares against payment in New York, New York on or about , 2020.

Global Coordinators

| Goldman Sachs & Co. LLC | BofA Securities | Morgan Stanley | Itaú BBA |

Joint Bookrunners

| UBS Investment Bank | Bradesco BBI |

The date of this prospectus is , 2020.

Table of Contents

Table of Contents

We have not authorized anyone to provide any information or make any representation about this offering that is different from, or in addition to, that contained in this prospectus or in any free writing prospectus prepared by or on behalf of us or to which we may have referred you. We and the underwriters take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. We, the underwriters and any of our or their affiliates have not authorized any other person to provide you with different or additional information. Neither we, the underwriters nor any of our or their affiliates are making an offer to sell, or seeking an offer to buy, the Class A common shares in any jurisdiction where the offer or sale is not permitted.

This prospectus is being used in connection with the offering of the Class A common shares in the United States and, to the extent described below, elsewhere. This offering is being made in the United States and elsewhere solely based on the information contained in this prospectus. You should assume that the information appearing in this prospectus is accurate only as of the date on the front cover of this prospectus, regardless of the time of delivery of this prospectus or any sale of the Class A common shares. Our business, financial condition, results of operations and prospects may have changed since the date on the front cover of this prospectus.

For investors outside the United States: Neither we, any of the underwriters nor any of our or their affiliates have done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction, other than the United States, where action for that purpose is required. Persons outside the United States who come into possession of this prospectus must inform themselves about, and observe any restrictions relating to, the offering of our Class A common shares and the distribution of this prospectus outside the United States.

Notice to EEA Investors. In any European Economic Area, or EEA, Member State that has implemented the Prospectus Regulation, this communication is only addressed to and is only directed at qualified investors in that Member State within the meaning of the Prospectus Regulation.

i

Table of Contents

This prospectus has been prepared on the basis that any offer of our Class A common shares in any Member State of the EEA (each, a “Relevant Member State”), will be made pursuant to an exemption under the Prospectus Regulation from the requirement to publish a prospectus for offers of shares. Accordingly, any person making or intending to make any offer within the EEA of our Class A common shares which are the subject of this offering may only do so in circumstances in which no obligation arises for us or any of the underwriters to publish a prospectus pursuant to Article 3 of the Prospectus Regulation in relation to such offer. Neither we nor the underwriters have authorized, nor do they authorize, the making of any offer of our Class A common shares in circumstances in which an obligation arises for us or the underwriters to publish a prospectus for such offer.

For the purposes of this provision, the expression “Prospectus Regulation” means Regulation (EU) 2017/1129 and includes any relevant implementing measure in each Relevant Member State.

Notice to UK Investors. In the United Kingdom, this prospectus is only addressed to and directed at qualified investors who are (1) investment professionals falling within Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (the “Order”); or (2) high net worth entities and other persons to whom it may lawfully be communicated, falling within Article 49(2)(a) to (d) of the Order (all such persons together being referred to as “relevant persons”). Any investment or investment activity to which this prospectus relates is available only to relevant persons and will only be engaged with relevant persons. Any person who is not a relevant person should not act or rely on this prospectus or any of its contents.

We own or have rights to trademarks, service marks and trade names that we use in connection with the operation of our business, including our corporate name, logos and website names. Other trademarks, service marks and trade names appearing in this prospectus are the property of their respective owners. Solely for convenience, some of the trademarks, service marks and trade names referred to in this prospectus are listed without the ® and ™ symbols, but we will assert, to the fullest extent under applicable law, our rights to our trademarks, service marks and trade names.

Unless otherwise indicated or the context otherwise requires, as used in this prospectus, (i) the terms “we,” “our,” “us,” “Vasta” or the “Company,” when used in the context of (a) the period up to October 11, 2018, the date of the acquisition by Saber Serviços Educacionais S.A., or Saber, a subsidiary of Cogna (formerly known as Kroton Educacional S.A., and together with its subsidiaries, the Cogna Group) of Somos Educação S.A., or Somos, and together with its subsidiaries, the Somos Group, which we refer to herein as the “Acquisition,” refer to the Combined Carve-out K-12 curriculum businesses held by each of Somos (which we refer to as “Somos – Anglo”) and the Cave-out K-12 curriculum business already held by Cogna, known as “Pitágoras” (and together with Somos – Anglo, which we refer to as the “Predecessors”); and (b) the period after the Acquisition, refer to the Predecessors’ Combined Carve-out K-12 curriculum business under the Vasta brand (which we refer to in this prospectus alternatively as “Vasta” or the “Successor”); and (ii) the term “issuer” refers to Vasta exclusive of its subsidiaries.

Due to the change in the basis of accounting resulting from the acquisition by Cogna of the K-12 curriculum businesses held by the Somos Group, and because the K-12 business held by Cogna (Predecessor – Pitágoras) came into common control with such K-12 curriculum business previously held by the Somos Group only upon completion of the Acquisition, we are required to present separately (1) the financial information for the period beginning on October 11, 2018, and through and including December 31, 2019, which we refer to as the “Post-Acquisition Period,” and (2) the financial information for the periods prior to, and including, October 10, 2018, which we refer to as the “Pre-Acquisition Period.” Certain financial information of the Post-Acquisition Period is not comparable to that of the Pre-Acquisition Period. For a discussion of our Post-Acquisition and Pre-Acquisition Periods, see “Presentation of Financial and Other Information—Financial Statements.”

The term “Brazil” refers to the Federative Republic of Brazil and the phrase “Brazilian government” refers to the federal government of Brazil. “Central Bank” refers to the Brazilian Central Bank (Banco Central do Brasil). References in the prospectus to “real,” “reais” or “R$” refer to the Brazilian real, the official currency of Brazil and references to “U.S. dollar,” “U.S. dollars” or “US$” refer to U.S. dollars, the official currency of the United States.

ii

Table of Contents

This summary highlights information contained elsewhere in this prospectus. This summary may not contain all the information that may be important to you, and we urge you to read this entire prospectus carefully, including the “Risk Factors,” “Business” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” sections and our combined carve-out financial statements and notes to those statements, included elsewhere in this prospectus, before deciding to invest in our Class A common shares.

Overview

We are a leading, high-growth education company in Brazil powered by technology, providing end-to-end educational and digital solutions that cater to all needs of private schools operating in the K-12 educational segment, ultimately benefiting all of our stakeholders, including students, parents, educators, administrators and private school owners.

We have built a “Platform as a Service,” or PaaS, with two main modules. Our Content & EdTech Platform combines a multi-brand and tech-enabled array of high-quality core and complementary education solutions with digital and printed content through long-term contracts with partner schools. We characterize revenue associated with these arrangements as subscription revenue given the renewable and predictable nature of the revenue associated with these contracts. Our emerging Digital Platform will unify our partner schools’ entire administrative ecosystem, enabling them to aggregate multiple learning strategies, helping them to focus on education, and promoting client and revenue growth to allow them to become more profitable institutions.

We believe our experience, high-quality education system and life-long learning solutions have helped us establish market-leading brands that are well-known both locally and nationally. This expertise has enabled continuous growth within the private K-12 market through long-term relationships and we believe it will be translated into a LTV/CAC ratio (as defined below) for the solutions that we characterize as subscription arrangements equal to 6.4x based on 2020 sales cycle (from October 1, 2019 to September 30, 2020). This is an important metric as it compares the estimated value of the customer relationship over its lifetime, Lifetime Value or LTV (measured as a function of the gross margin we expect to derive from the additional Annual Contract Value Bookings, or ACV Bookings, related to the contracts with our customers, divided by Weighted Average Cost of Capital, or WACC, plus the customer churn rate, which is the expected turnover rate), divided by the cost of acquiring the customer, Customer Acquisition Cost, or CAC (which consists of sales and marketing costs for the revenue for the solutions we characterize as subscription arrangements). We consider only subscription arrangements in our calculation of our LTV/CAC ratio because such arrangements have recurring, generally predictable revenue, while the revenue that is not based on subscription arrangements may be non-recurring and less predictable in nature. We believe the LTV/CAC ratio is an important metric for measuring how our sales efforts and costs related to acquiring subscription-based customers will provide value to us over time.

As of March 31, 2020, our network of business-to-business, or B2B, customers consisted of 4,167 partner schools. As of December 31, 2019, our network of B2B customers consisted of 3,400 partner schools, compared to 2,945 schools as of December 31, 2018, and 2,581 schools as of December 31, 2017, representing annual growth rates of 15.4% and 14.1%, respectively. As of March 31, 2020, we had 1,311 thousand enrolled students, defined as students contracted through our partner schools, using our platform in Brazil. As of December 31, 2019, we had 1,186 thousand enrolled students compared to 1,011 thousand enrolled students as of December 31, in 2018 and 891 thousand as of December 31, 2017, representing annual growth rates of 17.3% and 13.5%, respectively.

Our revenue derived from the solutions we characterize as subscription arrangements is driven by the number of enrolled students in each partner school that adopts our solutions. The net revenue from sales and

1

Table of Contents

services for the solutions we characterize as subscription arrangements represented 67.7% of the total net revenue from sales and services of the Successor in the three months ended March 31, 2020, 67.2% of the total net revenue from sales and services of the Successor in the year ended December 31, 2019, 65.4% of the sum of the total net revenue from sales and services of the Successor and Predecessors in 2018 and 58.7% of the sum of the total net revenue from sales and services of the Predecessors in 2017.

Revenue from solutions other than the ones we characterize as subscription arrangements includes stand-alone textbook sales, university admission preparatory exam courses and sales from our Livro Fácil business, an e-commerce for the sale of educational content (textbooks, school materials, stationery, among others) directly to schools, parents and students. Net revenue from sales and services deriving from these solutions represented 32.4% of the total net revenue from sales and services of the Successor for the three months ended March 31, 2020, 32.8% of the total net revenue from sales and services of the Successor in the year ended December 31, 2019, 34.5% of the sum of the total net revenue from sales and services of the Successor and Predecessors in 2018 and 41.3% of the sum of the total net revenue from sales and services of the Predecessors in 2017.

Our Mission

Our mission is to revolutionize the private primary and secondary educational ecosystem, offering educational content and technology services that allow schools to deliver high-quality education to their students, as well as digital services that support their growth and efficiency, supporting the digital transformation in schools. We believe we are uniquely positioned to help schools in Brazil undergo the process of digital transformation and bring their education skill-set to the 21st century. We promote the unified use of technology in K-12 education with enhanced data and actionable insight for educators, increased collaboration among support staff and improvements in production, efficiency and quality.

We provide the following solutions for the empowerment of our stakeholders:

For students

Our pedagogical approach and educational solutions are designed to equip students with abilities that go beyond learning core and complementary knowledge. We encourage them to think critically and creatively, solve complex problems, make evidence-based decisions, and work collaboratively at their own individualized pace.

For parents

Through our solutions, parents can access real-time student performance data and have a direct communication channel with educators and optimize parents’ time by addressing all of their children’s developmental needs, including core education and complementary activities through a single location—the school.

For educators

We help educators discover the pedagogical approach best suited to an individual student through immediate access to student data, which generates insight and analytics on student progress in order to target growth areas and develop teaching plans aimed at delivering personalized learning.

For private school owners and administrators

We are working on expanding our digital administrative platform to allow private school owners and administrators to maximize time, access a broader set of information more intelligently, develop new action

2

Table of Contents

plans, promote leadership and motivate their teams. As a result, this will allow private school owners to better manage their schools, focusing on improving educational content, solutions and services, while enhancing the school’s reputation and growing revenue.

For society

As part of our social responsibility initiatives, we seek to make education available to all segments of society. We share many of the best practices in education that we acquire through our experience in the private K-12 with public schools and teachers in Brazil for free.

We believe that our reputation, excellent track record in education, brand awareness, personalization, flexibility, customer service, academic outcomes and innovation are attributes valued by all of our stakeholders. We believe we are the only player in the market to integrate a wide array of content formats from different brands in a unified, technology-powered platform that allows for the continuous tracking of their academic performance during the whole education cycle.

In addition, we aim at adopting a neuroscience-first approach in evolving our understanding of what directly impacts teaching and learning, which includes acquiring new knowledge and nurturing attention, concentration, memory and motivation.

Our Results

Financial and Operating Information

We believe our business model includes highly predictable, contracted revenue and a unique product offering. The following is a brief summary of our principal results of operations and financial condition for the first quarter of 2020 and the most recently completed fiscal year.

| • | Our total net revenue from sales and services amounted to R$392.4 million and R$353.1 million for the three months ended March 31, 2020 and 2019, respectively, and R$989.7 million for the year ended December 31, 2019; |

| • | Net revenue derived from the solutions we characterize as subscription arrangements represented 67.7% and 65.0% of our total net revenue from sales and services for the three months ended March 31, 2020 and 2019, respectively, and 67.2% for the year ended December 31, 2019; |

| • | Our net profit amounted to R$27.6 million and R$14.9 million for the three months ended March 31, 2020 and 2019, respectively, and our net loss amounted to R$60.7 million for the year ended December 31, 2019; |

| • | Our Adjusted EBITDA amounted to R$121.5 million and R$105.7 million for the three months ended March 31, 2020 and 2019, respectively, and R$254.0 million for the year ended December 31, 2019 (see Presentation of Financial and Other Information—Special Note Regarding Non-GAAP Financial Measures—Adjusted EBITDA, Free Cash Flow and Adjusted Cash Conversion Ratio); |

| • | As of March 31, 2020, we had total outstanding bonds and financing of R$1,647.0 million, mostly comprised of private debentures issued by Somos Sistemas to Saber and Cogna (as creditors) at annual interest rate of the Interbank Deposit Certificate (Certificado de Depósito Interbancário), or CDI, plus 1.15%, with semi-annual coupon payments and a bullet repayment at maturity in August 2023. |

Please see “Management’s Discussion and Analysis of Financial Condition and Results of Operations” for a more detailed discussion of our results of operations and financial condition.

3

Table of Contents

Our level of indebtedness may require that we use a substantial portion of our cash flows to service our debt, which will reduce funds available for working capital, capital expenditures and other corporate purposes, and which may limit our ability to operate our business. In addition, the terms of the debentures and our other indebtedness contain covenants that may restrict our ability to operate our business. The terms of the debentures that we owe to our parent require that (1) we will allocate at least 50% of the use of proceeds from any liquidity event (including the proceeds from this offering) to repay such debentures; (2) we will not obtain any new loans unless the proceeds of any such loan are directed to repay our debentures with Cogna; and (3) we will not pledge shares and/or dividends. We expect to use two-thirds of the net proceeds from this offering to repay these debentures. See “Use of Proceeds.” See also “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources—Indebtedness” for a summary of the covenants of our indebtedness.

Our Addressable Market and Opportunity for Growth

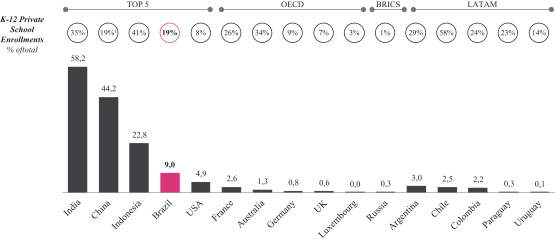

According to a report by Oliver Wyman that was commissioned by us, the total addressable market, or TAM, for our Content & EdTech Platform and Digital Platform for private schools in Brazil was R$25.3 billion as of 2018 and segregated between: (1) R$6.0 billion for core content; (2) R$6.4 billion for complementary education solutions; and (3) R$12.9 billion for digital platform. Oliver Wyman expects that our TAM will more than double by 2030, reaching R$54.0 billion, segregated between: (1) R$13.4 billion for core content; (2) R$14.0 billion for complementary education solutions; and (3) R$26.6 billion for digital platform. As of 2018, we estimate we captured approximately 12.1% of the TAM for core content and 0.4% of the TAM for complementary education solutions (which is included in our Content & EdTech Platform segment) and 0.5% of the TAM for our Digital Platform segment, which we believe represents significant growth opportunity.

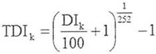

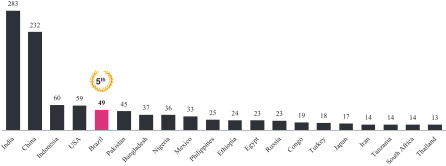

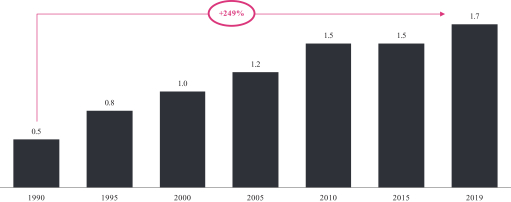

With 48.5 million students enrolled in private and public schools in 2018 according to Censo Escolar 2018, Brazil’s K-12 education segment is significantly larger in relative terms compared to other world markets; Brazil’s K-12 students account for 23% of the total population, while in the United States this representation falls behind at 17% (considering an estimate of 56.6 million students attending school in fall 2019), according to the National Center for Education Statistics, or NCES. The Brazilian private K-12 market is also large and, despite being larger than the U.S. market in relative size, there is a strong potential to increase the penetration of private K-12 education in Brazil when compared to China, Indonesia and India, for instance, as presented in the graph below. Private K-12 education is very valued by Brazilian families given the quality gap between private and public K-12 schools, as discussed in more detail in the “Industry” section.

| (1) | Including Hong Kong and Macao. |

Source: BMI, INEP and UNESCO

4

Table of Contents

We believe our opportunities to capture market growth will continue to expand as we incorporate new solutions into our existing platform, including, for example, by expanding our offering of STEAM-based content (science, technology, engineering, arts and math) and by increasing our offerings within our Digital Platform, to include online enrollment tools, a scholarship marketplace, academic and financial ERP and digital marketing services.

Private K-12 Industry Market Trends

We believe that our addressable market is characterized by the following trends:

Digital transformation is reshaping private K-12 industry

Technology has enabled improvements in core content, complementary education and digital platform solutions. The internet and digital technology are changing the way people learn, expanding beyond the classroom, increasing learning through gamification, immersion and virtual reality tools, and making the learning process adaptive and personalized. Moreover, technology has supported the development of management systems for schools to manage their costs and expenses and increase their efficiency and profitability.

Limited internal management and administrative solutions for schools

According to Censo Escolar 2018, there were approximately 40,000 private schools in Brazil as of December 2018, which are mainly small-scale units dedicating significant working hours to administrative activities, such as intake, retention, financial management and communication with parents, for which they are currently interacting with multiple and unintegrated providers. We believe there is strong demand for an integrated platform like ours that consolidates multiple school management services that allow for more actionable data reports, optimization of administrators’ time and increased efficiency in schools.

Need for modernized content distribution models

We believe the modern student is easily distracted, yet intellectually curious and demanding for high-quality, efficiently-delivered content. At the same time, schools and families are ready for the benefits available from the combined use of science and technology in education. This data-driven approach can aid in delivering superior and more responsive learning outcomes through products based on personalization and adaptive learning.

We believe we can lead the imminent transition of the underlying learning methods in Brazilian education, by offering assertive content in multiple formats alongside more effective high-impact learning techniques, with support from our constantly evolving neuro-pedagogical and science in learning approaches. Furthermore, integrated technological solutions customarily allow parents and educators to engage and track more closely student development.

New student skill set and importance of socio-emotional solutions

The increased labor market competitiveness and social demands in the 21st century require new skill sets, driving demand for a broader learning experience. Schools at the forefront of this movement teach socio-emotional learning and collaboration skills, foster individual participation, autonomy and critical thinking, and include new areas of broad student development such as STEAM-based curriculum and language instruction. We are uniquely positioned to capture this market with our English instruction and socio-emotional skills solutions, and plan to add even more solutions to our integrated platform.

5

Table of Contents

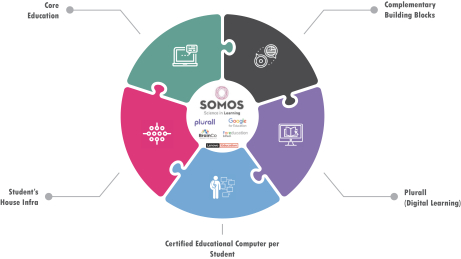

Our Products and Services

Our Ecosystem

We believe each school is unique. Understanding each school’s specific needs is crucial to providing differentiated solutions and services, thereby building and deepening long-standing relationships with our partner schools. We believe we are building the most complete and integrated platform of K-12 products and services to deliver end-to-end solutions that cater to each school’s entire ecosystem.

The chart below details the variety of products and services we currently provide through our Content & EdTech Platform and our Digital Platform along with other areas in which we plan to operate, establishing ourselves as a one-stop partner for private schools:

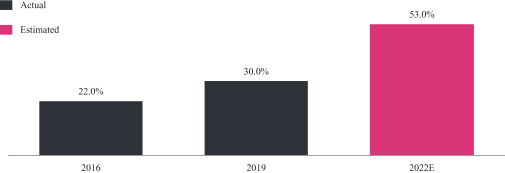

In the three months ended March 31, 2020 and for the comparative period of 2019, total net revenue from sales and services from our Content & EdTech Platform and our Digital Platform accounted for 81.0% and 19.0%, respectively, of the net revenue from sales and services of the Successor.

In 2019, total net revenue from sales and services from our Content & EdTech Platform and our Digital Platform accounted for 89% and 11%, respectively, of the net revenue from sales and services of the Successor, compared to 92% and 8%, respectively for the sum of the total net revenue from sales and services of the Successor for the period from October 11 to December 31, 2018 and Predecessors for the period from January 1 to October 10, 2018 and 100% and 0%, respectively for the total net revenue from sales and services of the Predecessors in 2017.

6

Table of Contents

Content & EdTech Platform

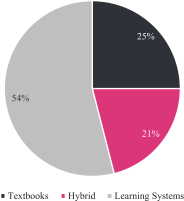

Core Content (learning systems, textbooks and other services)

We provide core educational content for Brazilian primary and secondary education through a multi-brand, tech-enabled platform, with the flexibility and quality required to satisfy customer needs through a multitude of pedagogical approaches, made available primarily through a model that we characterize as subscription arrangements. In the three months ended March 31, 2020, total net revenue from sales and services from subscription arrangements accounted for 83.6% of net revenue from sales and services of our Content & EdTech Platform, compared to 80.1% in the comparative period of 2019. In 2019, total net revenue from sales and services derived from subscription arrangements accounted for 75.4% of net revenue from sales and services of our Content & EdTech Platform, compared to 71.1% in 2018 and 58.7% in 2017.

The core content solutions we characterize as subscription arrangements include traditional learning systems (with main brands including Anglo, pH, Maxi, Pitágoras, Ético and Rede Cristã de Educação) and PAR, our proprietary product designed as an educational platform based on textbooks. All of our solutions include digital and printed content covering all disciplines for students, educators’ orientation manuals, exercise books, books for the study of multidisciplinary subjects and workbooks, as well as other features such as continuous assessment, ongoing training for educators, pedagogical support, marketing support, education-related events and gatherings, proprietary and differentiated student assessment tools and digital learning tools, available digitally and non-digitally. We offer a large range of brands targeting a wide spectrum of schools and students of varying academic preferences, backgrounds and demographics, allowing us to maximize outreach, awareness, penetration and customer satisfaction. We also derive revenue from other sources, such as (1) one-off textbook sales, which despite not being part of our core strategy, can be an important first step to start a relationship with a school, which can eventually subscribe to PAR or one of our learning systems in the future; and (2) a preparatory course for university admissions exam, which acts as a reputation enhancer for our Anglo brand.

Sold as a bundle with our core content, we offer digital learning and continuous teacher training, as follows.

| • | Digital Learning |

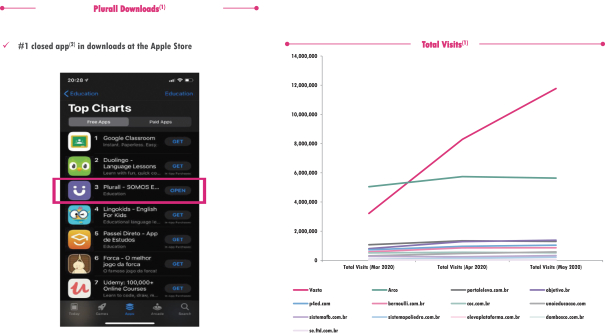

Plurall and Plurall Maestro are one of the only mobile-friendly and fully-integrated digital platforms for students, educators, coordinators and administrators currently available in the Brazilian market. For students, Plurall allows interaction with educational content inside and outside the classroom, as well as the opportunity to ask questions online through a student discussion forum, access tutors and review mock exams from ENEM and Brazil’s main university entrance applications. For parents and guardians, Plurall provides summarized reports with individual performance and serves as a communication tool with the school. For educators, coordinators and administrators of private schools, Plurall Maestro also allows for the creation of individualized content and data generation and evaluation reports to support in-class enhancements.

| • | Continuous Teacher Training |

PROFS is our fully digital teacher training program, also offered as a bundle with our core content solutions and aimed at enhancing in-class work through mentoring so that teaching professionals can reflect on their practice and skill-set and continue to pursue excellence in performance.

Complementary education solutions

We offer diversified solutions, both as part of core curricula and as after-school content. The complementary education solutions we characterize as subscription arrangements include:

| • | English Stars: an English educational platform designed to develop fluency in the English language with an emphasis on 21st century skills; |

7

Table of Contents

| • | O Líder em Mim: a program with content, methodology, teaching material and training to develop leadership and other socio-emotional skills; |

| • | Matific: In partnership with the international online learning company Matific, we provide engaging and entertaining mathematics instruction based on a strong pedagogical background and presented through playful interactions; |

| • | MindMakers: MindMakers uses children’s curiosity and energy as fuel to create rational minds with powerful computational thinking skills. MindMakers is designed to teach students how to develop leadership, collaboration and persistence through multidisciplinary problem-solving exercises; and |

| • | Plurall Olímpico: an academic platform of preparatory content for scientific competitions. |

We are constantly looking to incorporate new solutions into our existing platform. We are currently working on expanding our complementary offerings to include STEAM-based curriculum.

Digital Platform

Our Digital Platform is being developed to cater to all other school needs aside from education, aiming at increasing efficiency and quality of service. It is also an excellent tool to reduce the churn of our partner schools, greatly improving user experience for school owners and families through the seamless integration of educational and administrative services. Currently, we offer Livro Fácil, an e-commerce for the sale of educational content for schools, which also functions as a hub for distribution materials from other suppliers that are chosen by our partner schools, reinforcing our partner of choice positioning. We plan to increase our portfolio of solutions offered through our Digital Platform, either by developing additional solutions in-house, through partnerships or through merger and acquisition opportunities, including academic and financial ERP, digital marketing, scholarship marketplace and online enrollment services. See “—Our Growth Strategy—Increase the quantity of products and services we offer.”

Our Competitive Strengths

True partner of choice for private K-12 schools in Brazil

We believe tradition, reputation, experience and innovation are imperative for success in K-12 education. We have been present in the lives of Brazilian students over the last five decades though our parent company, or Cogna. As of March 31, 2020, we served 6,939 schools in the K-12 private market, with almost 2.6 million enrolled students. We believe we are best positioned to cover all of our total addressable market as we cater to each private K-12 school’s unique profile and preferences. We believe our track record in Brazil is unique, as demonstrated by the following:

| • | pioneer in education subscription arrangements; |

| • | large, well-recognized portfolio of private K-12 brands; |

| • | first to implement socio-emotional curricula in Brazil and first Brazilian educational platform with online tutoring for one-on-one personalized learning; |

| • | we believe we have one of the largest groups of educators, authors and tutors entirely dedicated to K-12 in Brazil and one of the largest databases of K-12 educational content in Brazilian Portuguese; |

| • | only company in Brazil to provide an educational platform based on textbooks (PAR) and supported by an e-commerce platform for the sale of educational content; |

| • | we believe we are at the forefront in integrating different content formats (text, video, audio, images, quizzes, among others) in a unified platform; |

8

Table of Contents

| • | we are pioneering the incorporation of neuroscience elements into our educational platform and emphasizing science in learning and promoting student success through personalized learning; and |

| • | we are developing our Digital platform to cater to the entire school ecosystem, delivering core and complementary content education, and promoting improved school management to promote efficiency gains. |

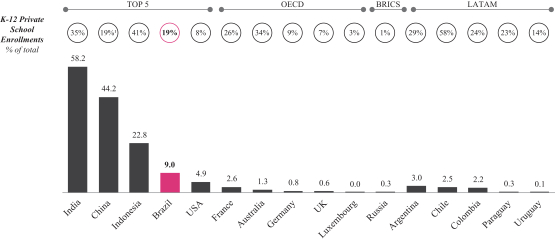

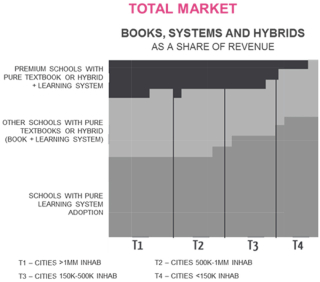

By becoming the schools’ partner of choice through our end-to-end offering of core and complementary content and the ramp-up of the solutions we will offer through our Digital Platform, we expect to continue to significantly increase our TAM while increasing school retention. The following chart shows the size and potential growth in TAM from 2018 to 2030 for Core Content and Complementary Solutions, comprising our Content & EdTech Platform (area shaded in gray) and for school administrative and management solutions, which will be served by our Digital Platform (area shaded in pink).

Private K-12 TAM

(in R$ billion, 2018)

Source: Oliver Wyman

Strong combination of content and technology teams dedicated to enhancing our value proposition

We value intellectual agility and structure ourselves in small multidisciplinary groups that are focused on building product functionality. We believe we have the most resourceful division of business intelligence and analytics in content adoption in the Brazilian K-12 market. Our digital team consists of 235 product, technology, digital operations and content specialists. Our product and technology specialists are organized in 11 teams, each being responsible for end-to-end implementation of projects aimed at accomplishing long-term goals.

Our content production is deeply linked to technology, allowing us to update content dynamically based on student and teacher feedback. To improve student engagement, we overlay content production with social media consumption (interactive video, podcasts and quizzes), aimed at promoting a pleasing aesthetic that captures the conceptual rigor essential for educational content. Our partner schools benefit from the unique combination of our Plurall products, a single platform that enables the delivery of a richer learning experience to both educators and students in an integrated and uniformed matter and combines in our content solutions in a 100% digital interface.

Our data science team employs a science in learning approach by leveraging our streaming data pipeline, allowing for rapid evolution of our solutions and services. Our data analytics educational team is focused on (1) tracking user behavior and creating dashboards to improve student and teacher engagement with Plurall and

9

Table of Contents

its many features; (2) allowing educators to take advantage of engagement and learning dashboards to improve student participation in the learning experience both inside and outside the classroom; (3) providing seamless integration of the Plurall platform with external products; and (4) gathering feedback and improving content generation in real time.

We also have a forward-leaning approach to applying neuroscience in education. We have been developing the Learning Science Lab, by partnering with highly regarded scientists in Brazil through Rede Nacional de Ciência para Educação and BrainCo, a startup born out of the Harvard Innovation Lab, to develop neuroscience technology products, and collaborate with scientists from the MIT Media Lab to test the effectiveness of their technology and develop new applications for brainwave technology.

Robust salesforce, business intelligence team and customer-centric mindset lead to differentiated go-to-market strategy

Our relentless focus on understanding our customers has led us to assemble a robust salesforce and client support team. Our team is comprised of 219 educational specialists (divided among commercial teams and inside sales teams, responsible for general marketing strategy and targeted client sales, respectively) and 181 customer support experts, who cover all Brazilian states through a differentiated go-to-market strategy where we target customers through multiple channels including online advertising, marketing research tools, on-site visits, social media, among others. We also have what we believe to be the largest business intelligence database and business intelligence team in the market. Our business intelligence team collects data from over 17,400 schools every year in order to have a comprehensive view of the total private K-12 market and to determine exactly what kind of products and services our salesforce should offer to each and every school. We offer our staff over 80 hours per year of training activities, on average, and 70% of our staff has been with us for over 3 years.

Our sales strategy allows educational specialists and customer support experts to establish themselves as trusted advisors for our partner schools and nurture relationships in order to keep on adding value through higher revenue streams, penetration, retention and awareness.

We seek to motivate our salesforce through financially aligned incentives based on new sales and client and revenue retention rates, among others. We also provide ongoing training, shadowing opportunities and participation in sales conferences.

Strong academic outcomes and recognition

The established tradition of our brands in the education sector, some of which have been developed over a period of more than 100 years, and our pioneering efforts in rolling out one of the first education subscription arrangement models in Brazil have contributed to our reputation for excellence. We believe our complete educational platform has translated into strong brand awareness, as demonstrated by the following:

| • | Anglo is the top of mind brand among learning systems considering premium schools choices and, alongside pH, is among the top four most preferred brands among school administrators and educators according to Hello Research; |

| • | 90% of premium schools know Pitágoras according to Hello Research; and |

| • | Publishers in our K-12 business have been honored with 102 Jabuti prizes since 1959, a widely recognized award as the most prestigious literary honor in Brazil. |

10

Table of Contents

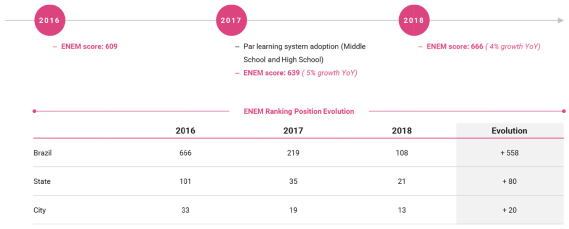

Quality perception is key for parents, and the quality of our pedagogical system and digital platform delivery is demonstrated by the following metrics:

| • | As of December 31, 2018 (most recent public data), we had 504 partner schools ranked among the top three schools in their respective municipalities based on their scores in ENEM, of which 263 partner schools were ranked as the best school in their municipality; and |

| • | As of December 31, 2018 (most recent public data), we had 44 partner schools ranked among the top 250 schools in the country based on their scores on the ENEM. |

Finally, the satisfaction of our customers (including students, parents, educators and administrators of private schools operating in the K-12 educational segment) and their positive experience with our platform is evidenced by our high net promoter score, or NPS, among core learning systems and digital learning brands. As of August 30, 2019, we scored 93 out of 100 possible points for both Anglo and pH learning systems, in a survey carried out by us with our partner schools, and 63 out of 100 possible points for our digital learning platform (Plurall), in a survey carried out by us with school coordinators.

The nature of our business model

Business model backed by solid fundamentals: we employ an asset-light business model centered on innovative and personalized content and user experience and focus on creating and maintaining long-standing relationships with partner schools. We are powered by technology and highly scalable, which allows for consistent high revenue growth.

End-to-end solutions provide meaningful unit economic gains: as we continue to strengthen our portfolio of full-service solutions, our potential to deepen relationships with schools increases through cross-sell and up-sell opportunities, generally at low incremental costs to us and to schools. We believe this leads to lifetime value at low customer acquisition cost while simultaneously increasing customer switching costs.

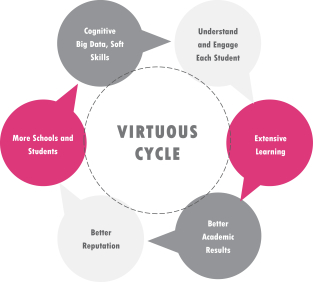

Self-reinforcing network effects of our virtuous cycle: we have created and have been nurturing an education cycle that entails scale, science in learning, high-quality and retainable learning, differentiated academic outcomes and recognition. Our company is based on information, using a robust team of business intelligence and analytics and source of big data with respect to the K-12 Brazilian industry, which is the start of a virtuous cycle for our partner schools. We help start the cycle by providing important data and key tools for schools to engage their students in a way that is meaningful for each student, providing enhancing learning, which we believe leads to better academic results and therefore improves schools’ reputations, which attracts more students

11

Table of Contents

to more schools. The cycle is reinforced as more students lead to more big data, which is the start of the cycle to provide the data needed to continue to engage our partner schools’ students.

Experienced and focused management, with an innovation mindset

Our senior management is recognized in the industry for its experience, reputation, working knowledge and close relationship with our partner schools, and strong track record in terms of the educational business and innovation. We share the same operational culture as our parent company, and our senior management team has over 100 years of combined experience dedicated to education. As one of the largest education groups in the world, we believe our parent company brings expertise in school operations, a long track record of carrying out mergers and acquisitions and integrating new businesses and technologies, a history of constant evolution and high total shareholder return, effective and transparent communication with shareholders and the market in general, with high levels of corporate governance and a strong drive for innovation.

Our Growth Strategy

Increase shift towards solutions we characterize as subscription arrangements within our current customer base

We will continue focusing on increasing the percentage of our partner schools (and related stakeholders) adopting the solutions we characterize as subscription arrangements instead of purchasing content without a long-term contract. We believe there is a significant potential to increase the number of total students enrolled in solutions we characterize as subscription arrangements from 1.3 million as of March 31, 2020, to 2.6 million total students, by converting part of our current base of partner schools adopting core content without a long-term contract into clients of solutions we characterize as subscription arrangements, including through the execution of new PAR and learning system contracts. In 2019, 2018 and 2017, the subscription agreements represented 37.0%, 20.4% and 8.3%, respectively, of the total revenue from the sales of textbooks. In 2019, we sold products (including textbooks without subscription) to approximately 3.0 million students from private schools, of which 1.2 million were from schools that had a contractual relationship with us, which 1.2 million students out of 3.0 million represents 40% of potential students from schools that use our products. From December 31, 2018 to December 31, 2019 and from December 31, 2017 to December 31, 2018, we successfully signed up 7.8% (6.3% to PAR and 1.5% to learning systems) and 5.7% (4.0% to PAR and 1.7% to learning systems), respectively, of our existing partner schools as compared to the respective year-end date for the prior year without a long-term contract to long-term subscription arrangements.

12

Table of Contents

Increase penetration of our current services in existing capacity with our current partner school base

We utilize a land-and-expand strategy with our partner schools, beginning with certain products from our portfolio of solutions contained in our Content & EdTech Platform and Digital Platform and gradually increasing the amount of services offered to each partner school. We focus on deepening relationships with our partner schools by leveraging our salesforce expertise to up-sell and cross-sell other products and services within our wide portfolio of current offers and future product and service developments and acquisitions. Our ultimate goal is to replace our partner schools’ collection of scattered educational vendors with our integrated platform of educational and digital solutions.

| • | As of March 31, 2020, only 11.1% of our student base used both our core and socio-emotional solutions; and |

| • | As of March 31, 2020, only 2.6% of our student base used both our core and languages solutions. |

We believe there is significant potential to increase the total number of students enrolled in our solutions, considering our current base of partner schools and the fact that one student can be enrolled in more than one solution at the same time. As of March 31, 2020, we had 1.5 million enrollments in our solutions (1.31 million in core content and 0.18 million in complementary solutions), considering each student at each solution as an enrollment. Through cross-selling and up-selling across both our Content & EdTech Platform and Digital Platform, we believe we are able to capture up to 5.1 million new enrollments, totaling a potential of 6.6 million students enrolled in our ecosystem (including core content, socioemotional content, languages, STEAM and other academic content).

Grow our base of partner schools

We have significantly expanded our sales force and will continue doing so in new regions across Brazil, while pursuing greater market share in regions where we have strong brand awareness and price attractiveness, which has helped us establish a presence in 12.1% of the TAM for core education as of 2018. We intend to reinvest a portion of our operational leverage in marketing activities that are aligned with our objective to continue increasing our base of partner schools through our superior value offering and extensive and integrated offering of products and services.

Increase the quantity of products and services we offer, including through in-house development, partnerships and acquisitions

We believe there is significant room to expand our value proposition to our partner schools and their stakeholders by adding new complementary education solution and digital platform to our ecosystem and, therefore, also significantly increasing our TAM potential. For instance, STEAM and academics are becoming “must-have” skills given increasing competition in the labor market. In addition, schools have been increasingly adopting management systems so they can focus on what they do best: educating.

We believe we can expand our current product offering, enhance our content and technology platforms and improve students’ learning, educators’ teaching and schools’ management experience by either developing innovative digital content in-house, engaging in strategic partnerships or carrying out mergers and acquisitions of companies and/or products that will contribute additional content or technologies to our portfolio. For example, we have identified a wide range of potential target acquisitions in Brazil that we believe will complement our business, in particular with respect to the delivery of digital solutions. With the expansion of our scope and product and service offerings through our platform, our TAM could increase even further. See “Presentation of Financial and Other Information—Corporate Events” for our recent acquisitions.

13

Table of Contents

Expand internationally

We believe schools, students, educators and families in Latin America are facing the same problems as in Brazil and demand the same solutions we are currently offering. Despite Spanish and Portuguese being different languages, the stakeholders’ needs are the same and we are able to fulfill many of those since we are already producing educational content in Spanish.

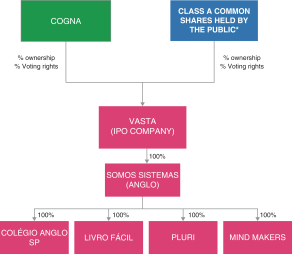

Our Corporate Structure

Our Incorporation and Corporate Reorganization

We are a Cayman Islands exempted company incorporated with limited liability on October 16, 2019 for purposes of undertaking our initial public offering, fully owned by Cogna on the date hereof.

Prior to this offering, our parent company, Cogna, reorganized its K-12 business under its wholly-owned subsidiary, Somos Sistemas de Ensino S.A., or Somos Sistemas, as described under “Presentation of Financial and Other Information—Corporate Events—Our Incorporation and Corporate Reorganization.” Prior to the consummation of this offering, Cogna will consummate the contribution of the entirety of the shares of Somos Sistemas held by Cogna to Vasta, or the Contribution. The Contribution will be accounted for at historical book value, in return for new Class B common shares issued by Vasta in a one-to- exchange. Until the Contribution of Somos Sistemas’ shares to us, we will not have commenced operations and will have only nominal assets and liabilities and no material contingent liabilities or commitments. Following the Contribution, Saber will continue to own and operate, directly or through other subsidiaries, certain K-12 businesses as a subsidiary of Cogna, including the operation of its own K-12 private schools and the sales of textbooks under the National Textbook Program (Programa Nacional do Livro e do Material Didático), or PNLD, which are separate from Vasta’s business.

After accounting for the new Class A common shares that will be issued and sold by us in this offering, we will have a total of common shares issued and outstanding immediately following this offering, of these shares will be Class B common shares beneficially owned by Cogna (which will hold % of the combined voting power of our outstanding Class A and Class B common shares), and of these shares will be Class A common shares beneficially owned by investors purchasing in this offering (which will hold % of the combined voting power of our outstanding Class A and Class B common shares). As a result, following this offering, our parent company will continue to control the outcome of all decisions at our shareholders’ meetings and will be able to elect a majority of the members of our board of directors. Our parent company will also be able to direct our actions in areas such as business strategy, financing, distributions, acquisitions and dispositions of assets or businesses. In addition, following the offering, we will be a “controlled company” within the meaning of the Nasdaq corporate governance standards and as such plan to rely on available exemptions from certain Nasdaq corporate governance requirements. See “Risk Factor—Our parent company, our sole shareholder prior to this offering, will own 100% of our outstanding Class B common shares, which represent approximately % of the voting power of our issued share capital and % of our total equity ownership following the offering, and will control all matters requiring shareholder approval. Our parent company’s ownership and voting power limits your ability to influence corporate matters.”

14

Table of Contents

The following chart shows our corporate structure after giving effect to this offering*:

| * | Investors in this offering will not have any interest in Cogna or its subsidiaries other than Vasta or its subsidiaries. |

Recent Developments

COVID-19

As a result of the global outbreak of a novel strain of coronavirus, or COVID-19, unprecedented economic uncertainties have arisen that continue to have an adverse impact on global economic and market conditions, including in Brazil. In March 2020, the World Health Organization declared the COVID-19 outbreak a pandemic, and the Brazilian federal government declared a national emergency with respect to COVID-19. In addition, state and municipal authorities in Brazil ordered suspensions of a variety of economic activities as part of measures taken to mitigate the dissemination of the virus.

The global impact of the outbreak has been rapidly evolving and the outbreak presents material uncertainty and risk with respect to our future performance and financial results. In response to the outbreak, we have implemented several measures aimed at safeguarding the health of our employees and the stability of our operations, including: (1) the implementation of a work from home policy; (2) the reduction in the work hours and wages by 25% of our administrative and corporate employees for the months of May, June and July; (3) on-line campaigns to promote our products to potential new customers; and (4) the implementation in our distribution centers of health and safety measures recommended by government authorities. In addition, we have accelerated the expansion of our digital education solutions to help keep the private school system operating during the COVID-19 pandemic, seeking to maintain the continuity in our operations and minimize the impacts of the pandemic on students enrolled at our partner schools. Through the integration of our Plurall and Plurall Maestro platforms with Google Hangouts, we have allowed students to access live classroom instruction remotely along with the instructional content already available through Plurall, such as ongoing homework and learning exercises, access to tutors, and an online library with a variety of content in different formats. We continue to monitor the availability and use of these solutions and engaged students for their feedback, which has been very positive during the pandemic. As of the date of this prospectus, we had more than 2.3 million students using our platforms, participating in more than 50,000 classes daily during week days.

We cannot predict the extent the extent of the impact of COVID-19 on our business or that any of the measures we have taken in response to the pandemic will be effective in mitigating the impact of COVID-19 on our business.

15

Table of Contents

In connection with social distancing and social isolation measures implemented by state and local governments in Brazil in response to the COVID-19 pandemic, and considering the effect of such measures on the education sector, certain of our partner schools experienced a decline in enrollment during the first half of the year, particularly in respect of early childhood education. Certain of our partner schools requested to decrease their level of purchases of educational materials and solutions we characterize as subscription arrangements for the second half of our 2020 sales cycle (which comprises the period between October 1, 2019 and September 30, 2020). On January 23, 2020 we had announced the result of ACV Bookings for the 2020 cycle (from October 2019 to September 2020), which reached R$716.0 million based on contracted amounts as of such date. This volume represented growth of 25% over the amount registered in the 2019 sales cycle. Notwithstanding such an increase, we believe that the revenue in the year 2020 to be derived from solutions we characterize as subscription arrangements will be adversely affected by such effects of declining enrollment at our partner schools. Such assessment on revenues derived from solutions we characterize as subscription arrangements is not a guarantee of future performance or outcomes and should not be relied on as guidance. Moreover, ACV Bookings is a non accounting managerial metric designed to show amounts that we expect to be recognized as revenue from subscription services during our commercial sales cycle and not for the fiscal year, ACV Bookings is only one metric in measuring the components of our revenues, and ACV Bookings in isolation is not indicative of our total revenues. ACV Bookings amounts refer only to amounts contracted by us and should not be considered as a forecast or estimate of our revenues. See “Presentation of Financial and Other Information—Special Note Regarding ACV Bookings” and “Cautionary Statement Regarding Forward-Looking Statements.”

For further information, please see “Risk Factors—Risks Relating to Our Business and Industry—Our operations and results may be negatively impacted by the COVID-19 pandemic” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Trend Information.”

Summary of Risk Factors

An investment in our Class A common shares is subject to a number of risks, including risks relating to our business and industry, risks related to Brazil and risks related to the offering and our Class A common shares. The following list summarizes some, but not all, of these risks. Please read the information in the section entitled “Risk Factors” for a more thorough description of these and other risks.

Certain Factors Relating to Our Business and Industry

| • | Our operations and results may be negatively impacted by the COVID-19 pandemic. |

| • | We face significant competition and the possibility of new competitors and potential substitutes for every product or service we offer and in each geographic region in which we operate. If we fail to compete efficiently, we may lose market share and our profitability may be adversely affected. |

| • | We depend significantly on information technology, or IT, systems, and are subject to risks related to technological change. Any failure to maintain and support customer facing services, systems, and platforms, including addressing quality issues and executing timely release of new products and enhancements, could negatively impact our revenue and reputation. |

| • | Our revenue depends on sales of educational content, products and services to our customers, and any setback in customer relations could cause us significant harm. |

| • | Our growth may have a negative effect on the successful expansion of our business, on our people management, and on the increase in complexity of our software and platforms. In addition, if our growth rate decelerates significantly, our future prospects and financial results would be adversely affected, preventing us from achieving profitability. |

16

Table of Contents

| • | Our business depends on the success of our brands and our ability to attract and retain customers could be adversely affected due to events or conditions that damage our reputation or the image of our brands. |

| • | Misuse of our brands or other actions carried out by other companies controlled by our parent company may damage our business and our reputation due to certain of our brands being shared with other businesses controlled by our parent company. |

| • | Failure to protect or enforce our intellectual property and other proprietary rights could adversely affect our business and financial condition and results of operations. In addition, we may in the future be subject to intellectual property claims, which are costly to defend and could harm our business, financial condition and operating results. |

| • | The quality of the teaching content we deliver to our customers depends to a significant degree on the quality of our publishers and of the content we purchase. Any issues related to obtaining this content or regarding the quality of this content may have an adverse effect on our business. |

| • | We may not be able to implement our business strategy as intended, including relating to our PAR product, cross-selling and up-selling to our existent base, entering new markets and business, especially regarding our Digital Platform, expanding our complementary education portfolio, carrying out new or integrating existing acquisitions and increasing our base of partner schools, which could have an adverse effect on our results. |

| • | If we are unable to retain or replace our key personnel or are unable to attract, retain and develop other qualified employees, our business, financial situation and operating results may be adversely affected. |

Certain Factors Relating to Brazil

| • | The Brazilian federal government has exercised, and continues to exercise, significant influence over the Brazilian economy. This involvement as well as Brazil’s political, regulatory, legal and economic conditions could harm us and the price of our Class A common shares. |

| • | The ongoing economic uncertainty and political instability in Brazil may harm us and the price of our Class A common shares. |

| • | Exchange rate instability may have adverse effects on the Brazilian economy, us and the price of our Class A common shares. |

| • | Developments and the perceptions of risks in other countries, including other emerging markets, the United States and Europe, may harm the Brazilian economy and the price of our Class A common shares. |

Certain Factors Relating to the Offering and our Class A Common Shares

| • | Our Class A common shares have not previously been traded on any stock exchange and, therefore, an active and liquid trading market for such securities may not develop, which could potentially depress the trading price of our Class A common shares after this offering. |

| • | Upon our corporate reorganization and prior to the completion of this offering, Cogna, will own 100% of our Class B common shares, which represent approximately % of the voting power of our issued share capital and % of our total equity ownership following the offering (assuming no exercise of the underwriters option to purchase additional shares), and will control all matters requiring shareholder approval. This concentration of ownership and voting power limits your ability to influence corporate matters. |

17

Table of Contents

| • | The market price of our shares may be volatile or may decline sharply or suddenly, regardless of our operating performance, and we may not be able to meet investors’ or analysts’ expectations. You may not be able to resell your shares for the initial offer price or above it and you may lose all or part of your investment. In addition, the price of our Class A common shares may be subject to changes in the price of the shares of our parent company. |

| • | Our dual class capital structure means our shares will not be included in certain indices. We cannot predict the impact this may have on our share price. The dual class structure also has the effect of concentrating voting control with our parent company; this will limit or preclude your ability to influence corporate matters. |

| • | We are a Cayman Islands exempted company with limited liability. The rights of our shareholders, including with respect to fiduciary duties and corporate opportunities, may be different from the rights of shareholders governed by the laws of U.S. jurisdictions. |

Corporate Information

Our principal executive offices are located at Av. Paulista, 901, 5th Floor, Bela Vista, São Paulo—SP, CEP 01310-100, Brazil. Our telephone number at this address is +55-11-3133-7311. Our email address is ri@somoseducacao.com.br.

Investors should contact us for any inquiries through the address, telephone number and email listed above. Our principal website is http://www.vastaedu.com.br. The information contained in, or accessible through, our website is not incorporated into this prospectus or the registration statement of which it forms a part. You should not consider information contained on our website to be part of this prospectus or in deciding whether to invest in our Class A common shares.

Implications of Being an Emerging Growth Company

As a company with less than US$1.07 billion in revenue during our last fiscal year, we qualify as an “emerging growth company” as defined in the Jumpstart our Business Startups Act of 2012, or the JOBS Act. An emerging growth company may take advantage of specified reduced reporting and other burdens that are otherwise applicable generally to public companies. These provisions include:

| • | a requirement to have only two years of audited financial statements and only two years of related Management’s Discussion and Analysis of Financial Condition and Results of Operations disclosure; |

| • | an exemption from the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act of 2002, as amended, or the Sarbanes-Oxley Act, in the assessment of our internal control over financial reporting; |

| • | reduced disclosure about our executive compensation arrangements in our periodic reports, proxy statements and registration statements; and |

| • | exemptions from the requirements of holding non-binding advisory votes on executive compensation and golden parachute arrangements. |

We will remain an emerging growth company until the earlier of (1) the last day of the fiscal year (a) following the fifth anniversary of the completion of this offering, (b) in which we have total annual revenue of at least US$1.07 billion, or (c) in which we are deemed to be a large accelerated filer, which means the market value of our shares that is held by non-affiliates exceeds US$700.0 million as of the prior June 30, and (2) the date on which we have issued more than US$1.07 billion in non-convertible debt during the prior three-year period. As an emerging growth company, we are eligible to take advantage of certain exemptions from various

18

Table of Contents

reporting requirements that are applicable to other public companies in the United States that are not emerging growth companies. Accordingly, the information about us available to you will not be the same as, and may be more limited than, the information available to shareholders of a non-emerging growth company.

In addition, under the JOBS Act, emerging growth companies can delay adopting new or revised accounting standards until such time as those standards apply to private companies. Given that we currently report and expect to continue to report under IFRS as issued by the IASB, we will not be able to avail ourselves of this extended transition period and, as a result, we will adopt new or revised accounting standards on the relevant dates on which adoption of such standards is required by the IASB.

19

Table of Contents

This summary highlights information presented in greater detail elsewhere in this prospectus. This summary is not complete and does not contain all the information you should consider before investing in our Class A common shares. You should carefully read this entire prospectus before investing in our Class A common shares including “Risk Factors” and our combined carve-out financial statements.

| Issuer |

Vasta Platform Limited. |

| Class A common shares offered by us |

Class A common shares (or Class A common shares if the underwriters exercise in full their option to purchase additional Class A common shares from us). |

| Offering price range |

Between US$ and US$ per Class A common share. |

| Voting rights |

The Class A common shares will be entitled to one vote per share, whereas the Class B common shares (which are not being sold in this offering) will be entitled to 10 votes per share. |

| Each Class B common share may be converted into one Class A common share at the option of the holder. |

| If, at any time, the total number of the issued and outstanding Class B common shares is less than 10% of the total number of shares outstanding, then each Class B common share will convert automatically into one Class A common share. |

| In addition, each Class B common share will convert automatically into one Class A common share upon any transfer, except for certain transfers to other holders of Class B common shares or their affiliates or to certain unrelated third parties as described under “Description of Share Capital—Conversion.” |