United States

Securities and Exchange Commission

Washington, D.C. 20549

FORM

(Amendment No. 1)

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES

EXCHANGE ACT OF 1934

For the fiscal year ended

Commission file number

(Exact name of Registrant as specified in its charter)

Province of Ontario

(Jurisdiction of incorporation or organization)

(Address of principal executive offices)

General Counsel

Tel: (

Facsimile: (954) 212-0808

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

Title of each class |

| Trading symbol |

| Name of each exchange on which registered |

|

|

Securities registered or to be registered pursuant to Section 12(g) of the Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ☐

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

Yes ☐

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b))by the registered public accounting firm that prepared or issued its audit report.

Yes

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | ☐ | Accelerated filer | ☐ |

☒ | Emerging growth company |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act.

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

U.S. GAAP | ☐ | ☒ | Other | ☐ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

Item 17 ☐ Item 18 ☐

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act) Yes

EXPLANATORY NOTE

On May 9, 2022, Flora Growth Corp. (the “Company”) filed its Annual Report on Form 20-F for the fiscal year ended December 31, 2021 (the “Original Form 20-F”). This Amendment No. 1 (the “Amendment”) amends the Original Form 20-F solely (i) to modify Item 6.C—Board Practices—Corporate Governance Policies to disclose certain inadvertently omitted home country practices the Company follows in lieu of their respective rules and standards under the Nasdaq Stock Market rules, and (ii) to file a new consent of the Company’s Independent Registered Public Accounting Firm, Davidson & Company LLP, as Exhibit 15.1.

This Amendment speaks as of the original filing date and does not reflect events occurring after the filing of the Original Form 20-F. No revisions are being made to the other portions of the Original Form 20-F.

In addition, as required by Rule 12b-15 under the Securities Exchange Act of 1934, as amended (the “Exchange Act”), new certifications by the Company’s principal executive officer and principal financial officer are filed herewith as exhibits to this Amendment pursuant to Rule 13a-14(a) of the Exchange Act and Section 1350 of Chapter 63 of Title 18 of the United States Code (18 U.S.C. 1350).

TABLE OF CONTENTS

|

|

| 1 |

| |

|

|

|

| 1 |

|

|

| 1 |

| ||

|

|

|

| ||

|

|

|

| ||

|

| 18 |

| ||

|

| 38 |

| ||

|

| 38 |

| ||

|

| 49 |

| ||

|

| 57 |

| ||

|

| 59 |

| ||

|

| 59 |

| ||

|

| 60 |

| ||

|

| 69 |

| ||

|

| 70 |

| ||

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

| 71 |

| ||

Material modifications to the rights of security holders and use of proceeds |

|

| 71 |

| |

|

| 71 |

| ||

|

| 72 |

| ||

|

| 72 |

| ||

|

| 73 |

| ||

|

| 73 |

| ||

Purchases of equity securities by the issuer and affiliated purchasers |

|

| 73 |

| |

|

| 73 |

| ||

|

| 73 |

| ||

|

| 73 |

| ||

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

| 74 |

| ||

|

| 74 |

| ||

|

| 75 |

|

| i |

| Table of Contents |

INTRODUCTION

As used in this Annual Report on Form 20-F (this “Annual Report”), unless the context otherwise requires or otherwise states, references to the “Company,” “Flora,” “we,” “us,” “our,” and similar references refer to Flora Growth Corp., a corporation formed under the laws of the Province of Ontario, and its subsidiaries.

Our functional currency and reporting currency is the U.S. dollar, the legal currency of the United States (which we refer to as “USD”, “US$” or “$”).

INTERNATIONAL FINANCIAL REPORTING STANDARDS

Our financial statements are prepared in accordance with International Financial Reporting Standards (IFRS) as issued by the International Accounting Standards Board (IASB). Our fiscal year ends on December 31 of each year as does our reporting year. Our most recent fiscal year ended on December 31, 2021. See Notes 2 and 3 to our audited consolidated financial statements as of and for the year ended December 31, 2021 for a discussion of the basis of presentation, functional currency, and translation of financial statements.

We have made rounding adjustments to some of the figures included in this Annual Report. Accordingly, numerical figures shown as totals in some tables may not be an arithmetic aggregation of the figures that precede them.

TRADEMARKS AND SERVICE MARKS

We rely on a combination of trademark, patent, copyright and trade secret protection laws in Colombia, the United States and other jurisdictions to protect our intellectual property and our brands. We have applied for, and we have received approvals from the Superintendency of Industry and Commerce and the Instituto Nacional de Vigilancia de Medicamentos y Alimentos, for our beauty and skincare, pharmaceutical, loungewear, and food and beverage products.

| ii |

| Table of Contents |

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report contains “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995 and other U.S. Federal securities laws. These forward-looking statements may include projections and estimates concerning our possible or assumed future results of operations, financial condition, business strategies and plans, market opportunity, competitive position, industry environment, and potential growth opportunities. In some cases, you can identify forward- looking statements by terms such as “may”, “will”, “should”, “believe”, “expect”, “could”, “intend”, “plan”, “anticipate”, “estimate”, “continue”, “predict”, “project”, “potential”, “target,” “goal” or other words that convey the uncertainty of future events or outcomes. You can also identify forward-looking statements by discussions of strategy, plans or intentions. We have based these forward-looking statements on our current expectations and assumptions about future events. While our management considers these expectations and assumptions to be reasonable, because forward-looking statements relate to matters that have not yet occurred, they are inherently subject to significant business, competitive, economic, regulatory and other risks, contingencies and uncertainties, most of which are difficult to predict and many of which are beyond our control. These and other important factors, including, among others, those discussed in this Annual Report, may cause our actual results, performance or achievements to differ materially from any future results, performance or achievements expressed or implied by the forward-looking statements in this Annual Report. Some of the factors that could cause actual results to differ materially from those expressed or implied by the forward-looking statements in this Annual Report include:

| · | Our limited operating history and net losses; |

| · | unpredictable events, such as the COVID-19 outbreak, and associated business disruptions; |

| · | changes in cannabis laws, regulations and guidelines; |

| · | decrease in demand for cannabis and derivative products due to certain research findings, proceedings, or negative media attention; |

| · | damage to our reputation as a result of negative publicity; |

| · | exposure to product liability claims, actions and litigation; |

| · | risks associated with product recalls; |

| · | product viability; |

| · | continuing research and development efforts to respond to technological and regulatory changes; |

| · | shelf life of inventory; |

| · | our ability to successfully integrate businesses that we acquire; |

| · | maintenance of effective quality control systems; |

| · | changes to energy prices and supply; |

| · | risks associated with expansion into new jurisdictions; |

| · | regulatory compliance risks; |

| · | opposition to the cannabinoid industry; |

| · | risks related to our operations in Colombia; and |

| · | potential delisting resulting in reduced liquidity of our Common Shares. |

Given the foregoing risks and uncertainties, you are cautioned not to place undue reliance on the forward-looking statements in this Annual Report. The forward-looking statements contained in this Annual Report are not guarantees of future performance and our actual results of operations and financial condition may differ materially from such forward- looking statements. In addition, even if our results of operations and financial condition are consistent with the forward-looking statements in this Annual Report, they may not be predictive of results or developments in future periods.

Any forward-looking statement that we make in this Annual Report speaks only as of the date of this Annual Report. Except as required by law, we do not undertake any obligation to update or revise, or to publicly announce any update or revision to, any of the forward-looking statements in this Annual Report, whether as a result of new information, future events or otherwise, after the date of this Annual Report.

| iii |

| Table of Contents |

PART ONE

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable.

ITEM 3. KEY INFORMATION

3.A. [Reserved].

3.B. Capitalization and indebtedness

Not applicable.

3.C. Reasons for the offer and use of proceeds

Not applicable.

3.D. Risk factors

Summary of Risk Factors

There are a number of risks that you should carefully consider before making an investment in our business. These risks are discussed more fully in the sections below. If any of these risks actually occur, our business, financial condition, operating results and cash flows could be materially adversely affected. These risk factors include, but are not limited to:

| · | limited operating history and net losses; |

| · | unpredictable events, such as the COVID-19 outbreak, and associated business disruptions; |

| · | changes in cannabis laws, regulations and guidelines; |

| · | decrease in demand for cannabis and derivative products due to certain research findings, proceedings, or negative media attention; |

| · | damage to reputation as a result of negative publicity; |

| · | exposure to product liability claims, actions and litigation; |

| · | risks associated with product recalls; |

| · | product viability; |

| · | continuing research and development efforts to respond to technological and regulatory changes; |

| · | shelf life of inventory; |

| · | our ability to successfully integrate businesses that we acquire; |

| · | maintenance of effective quality control systems; |

| · | changes to energy prices and supply; |

| · | risks associated with expansion into new jurisdictions; |

| · | regulatory compliance risks; |

| · | opposition to the cannabinoid industry; |

| · | risks related to our operations in Colombia; and |

| · | potential delisting resulting in reduced liquidity of our Common Shares. |

There are a number of risks and uncertainties that could affect our business and cause our actual results to differ from past performance or expected results. We consider the following risks and uncertainties to be those material to our business. If any of these risks actually occur, our business, financial condition and results of operations could suffer, and the trading price of our Common Shares could decline. We urge investors to consider carefully the risk factors described below in evaluating any investment in our Common Shares and the information contained in this Annual Report.

Risks Related to our Business and Industry

We are an early-stage company with limited operating history and may never become profitable.

We are an early-stage company focused on cultivating, processing and supplying natural, medicinal-grade cannabis oil and high-quality cannabis derived medical and wellness products to large channel distributors and retailers globally. Newly-formed in March 2019, we have limited operating history. Flora has only started full commercial cannabis cultivation with the passage of the latest Colombian cannabis resolution after two successful years cultivating and harvesting cannabidiol (“CBD”) and Tetrahydrocannabinol (“THC”) for derivatives, while investigating cultivars with the Instituto Colombiano Agropecuario (“ICA”). We have produced oil extracts, however only on a smaller scale, and we will require time to maximize production and refine operating procedures. We are currently in discussions with distributors with whom we intend to engage although no definitive agreements have been signed until the import requirements are met with local jurisdictions. We have limited financial resources and minimal operating cash flow. For the year ended December 31, 2021, we had losses of $21.4 million and as of December 31, 2021 an accumulated deficit of $38.5 million.

| 1 |

| Table of Contents |

Additionally, there can be no assurance that additional funding will be available to us for the development of our business, which will require the commitment of substantial resources. Accordingly, you should consider our prospects in light of the costs, uncertainties, delays and difficulties frequently encountered by companies in the early stages of development. Potential investors should carefully consider the risks and uncertainties that a company with a limited operating history will face. In particular, potential investors should consider that we may be unable to:

· | successfully implement or execute our business plan, or that our business plan is sound; |

· | adjust to changing conditions or keep pace with increased demand; |

· | attract and retain an experienced management team; or |

· | raise sufficient funds in the capital markets to effectuate our business plan, including product development, licensing and approvals. |

The Coronavirus (“COVID-19”) outbreak or similar pandemics could adversely affect our operations.

The Company’s operations could be significantly adversely affected by the effects of a widespread global outbreak of a contagious disease and other unforeseen events, including the outbreak of respiratory illness caused by COVID-19 and the related economic repercussions. We cannot accurately predict the effects COVID-19 will have on our operations and the ability of others to meet their obligations with the Company, including uncertainties relating to the ultimate geographic spread of the virus, the severity of the disease, the duration of the outbreak, and the length of travel and quarantine restrictions imposed by governments of affected countries. In addition, a significant outbreak of contagious diseases in the human population could result in a widespread health crisis that could adversely affect the economies and financial markets of many countries, resulting in an economic downturn that could further affect the Company’s operations and ability to finance its operations.

Agricultural activity has been declared as an essential activity in Colombia. Our cultivation and processing facility in Colombia is operating under a protocol authorized by the Colombian government. At the site, all employees receive a new mask and a new set of surgical gloves daily. Hand sanitizer is provided and hand washing protocols are in place. The employees are also provided a transparent face protection mask, which is replaced every 30 days. Our employees frequently have their temperature taken and must report to the Health and Safety office if they are experiencing any symptoms, including diarrhea, cough, runny nose, or headache. If an employee reports any of these symptoms, the employee is sent home to isolate for 10 days and, if the symptoms persist for 72 hours, the employee is required to go to a hospital.

Recent and future acquisitions and strategic investments could be difficult to integrate, divert the attention of key management personnel, disrupt our business, dilute shareholder value, may subject us to liability, and harm our results of operations and financial condition.

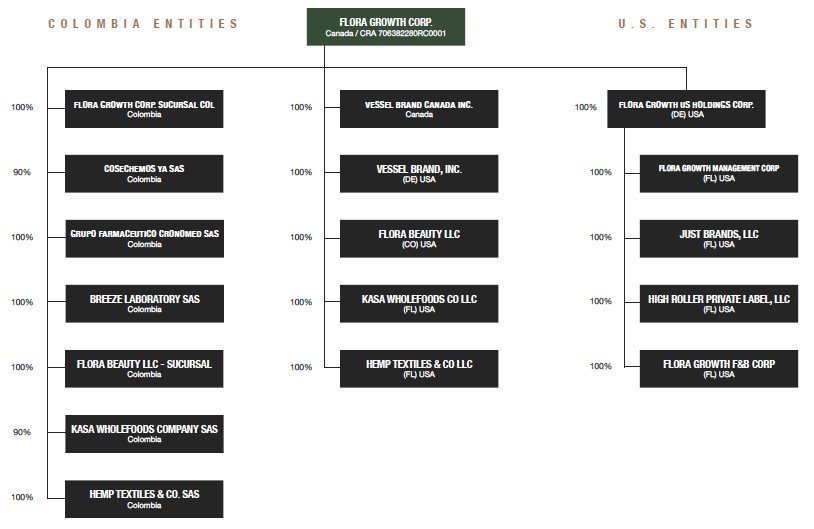

We have recently acquired the businesses of Vessel Brand, Inc. (“VBI”), Just Brands LLC (“JBL”) and High Roller Private Label LLC (“HRPL”), and we may in the future seek to acquire or invest in businesses, products, or technologies that we believe could complement our operations or expand our breadth, enhance our capabilities, or otherwise offer growth opportunities. Our diversity of product offerings may not be successful. While our growth strategy includes broadening our service and product offerings, implementing an aggressive marketing plan and employing product diversification, there can be no assurance that our systems, procedures and controls will be adequate to support our operations as they expand. We cannot assure you that our existing personnel, systems, procedures or controls will be adequate to support our operations in the future or that we will be able to successfully implement appropriate measures consistent with our growth strategy. As part of our planned growth and diversified product offerings, we may have to implement new operational and financial systems, procedures and controls to expand, train and manage our employee base, and maintain close coordination among our staff. We cannot guarantee that we will be able to do so, or that if we are able to do so, we will be able to effectively integrate them into our existing staff and systems. Additionally, the integration of our acquisitions and pursuit of potential future acquisitions may divert the attention of management and cause us to incur various expenses in identifying, investigating, and pursuing suitable acquisitions, whether or not they are consummated. Any acquisition, investment or business relationship may result in unforeseen operating difficulties and expenditures. In addition, we have limited experience in acquiring other businesses. Specifically, we may not successfully evaluate or utilize the acquired products, assets or personnel, or accurately forecast the financial impact of an acquisition transaction, including accounting charges.

We may not be able to find and identify desirable acquisition targets or we may not be successful in entering into an agreement with any one target. Acquisitions could also result in dilutive issuances of equity securities or the incurrence of debt, which could harm our results of operations. In addition, if an acquired business fails to meet our expectations, our business, results of operations, and financial condition may suffer. In some cases, minority shareholders may exist in certain of our non-wholly-owned acquisitions (for businesses we do not purchase as an 100% owned subsidiary) and may retain minority shareholder rights which could make a future change of control or corporate approvals for actions more difficult to achieve and/or more costly.

We also make strategic investments in early-stage companies developing products or technologies that we believe could complement our business or expand our breadth, enhance our technical capabilities, or otherwise offer growth opportunities. These investments may be in early-stage private companies for restricted stock. Such investments are generally illiquid and may never generate value. Further, the companies in which we invest may not succeed, and our investments would lose their value.

| 2 |

| Table of Contents |

Moreover, the anticipated benefits of any acquisition, investment, or business relationship may not be realized, or we may be exposed to unknown risks or liabilities of our acquisitions. Furthermore, we may be subject to unknown liabilities of the businesses we acquire. In addition, we may become subject to legal proceedings in connection with the businesses of, or resulting from, our acquisitions. For example, we received a letter from an attorney representing an undisclosed group of former pre-acquisition shareholders of VBI seeking to engage in settlement discussions on the basis of certain allegations. While no formal litigation has been initiated, we believe that any potential claims as alleged in the letter are without merit and we intend to defend vigorously against them in connection with any future potential legal proceedings. For more information, see Item 4.B. “Business overview—Legal Proceedings.”

Certain conditions or events could disrupt the Company’s supply chains, disrupt operations, and increase operating expenses.

Conditions or events including, but not limited to, the following could disrupt the Company’s supply chains and in particular its ability to deliver its products, interrupt operations at its facilities, increase operating expenses, resulting in loss of sales, delayed performance of contractual obligations or require additional expenditures to be incurred: (i) extraordinary weather conditions or natural disasters such as hurricanes, tornadoes, floods, fires, extreme heat, earthquakes, etc.; (ii) a local, regional, national or international outbreak of a contagious disease, including the COVID-19 coronavirus, Middle East Respiratory Syndrome, Severe Acute Respiratory Syndrome, H1N1 influenza virus, avian flu, or any other similar illness could result in a general or acute decline in economic activity; (iii) political instability, social and labor unrest, war or terrorism, including the current conflict between Russia and Ukraine; or (iv) interruptions in the availability of basic commercial and social services and infrastructure including power and water shortages, and shipping and freight forwarding services including via air, sea, rail and road.

Cannabis laws, regulations, and guidelines are dynamic and subject to changes.

Cannabis laws and regulations are dynamic and subject to evolving interpretations which could require us to incur substantial costs associated with compliance or alter certain aspects of our business plan. It is also possible that regulations may be enacted in the future that will be directly applicable to certain aspects of our businesses. We cannot predict the nature of any future laws, regulations, interpretations or applications, nor can we determine what effect additional governmental regulations or administrative policies and procedures, when and if promulgated, could have on our business. Management expects that the legislative and regulatory environment in the cannabis industry in Colombia and internationally will continue to be dynamic and will require innovative solutions to try to comply with this changing legal landscape in this nascent industry for the foreseeable future. Compliance with any such legislation may have a material adverse effect on our business, financial condition and results of operations.

Public opinion can also exert a significant influence over the regulation of the cannabis industry. A negative shift in the public’s perception of the cannabis industry could affect future legislation or regulation in different jurisdictions.

Demand for cannabis and derivative products could be adversely affected and significantly influenced by scientific research or findings, regulatory proceedings, litigation, media attention or other research findings.

The legal cannabis industry is at an early stage of its development. Consumer perceptions regarding legality, morality, consumption, safety, efficacy and quality of medicinal cannabis are mixed and evolving and can be significantly influenced by scientific research or findings, regulatory investigations, litigation, media attention and other publicity regarding the consumption of medicinal cannabis products. There can be no assurance that future scientific research, findings, regulatory proceedings, litigation, media attention or other research findings or publicity will be favorable to the medicinal cannabis market or any particular product, or consistent with earlier publicity. Future research reports, findings, regulatory proceedings, litigation, media attention or other publicity that are perceived as less favorable than, or that question, earlier research reports, findings or publicity, could have a material adverse effect on the demand for medicinal cannabis and on our business, results of operations, financial condition and cash flows. Further, adverse publicity reports or other media attention regarding cannabis in general or associating the consumption of medicinal cannabis with illness or other negative effects or events, could have such a material adverse effect. Public opinion and support for medicinal cannabis use has traditionally been inconsistent and varies from jurisdiction to jurisdiction. Our ability to gain and increase market acceptance of our business may require substantial expenditures on investor relations, strategic relationships and marketing initiatives. There can be no assurance that such initiatives will be successful and their failure to materialize into significant demand may have an adverse effect on our financial condition.

Damage to the Company’s reputation can be the result of the actual or perceived occurrence of any number of events, and could include any negative publicity, whether such publicity is accurate or not.

The increased usage of social media and other web-based tools used to generate, publish and discuss user-generated content and to connect with other users has made it increasingly easier for individuals and groups to communicate and share opinions and views regarding the Company and its activities, whether true or not. Although the Company believes that it operates in a manner that is respectful to all stakeholders and that it takes pride in protecting its image and reputation, it does not ultimately have direct control over how it is perceived by others. Reputational loss may result in decreased ability to enter into new customer, distributor or supplier relationships, retain existing customers, distributors or suppliers, reduced investor confidence and access to capital, increased challenges in developing and maintaining community relations and an impediment to our overall ability to advance our projects, thereby having a material adverse effect on our financial performance, financial condition, cash flows and growth prospects.

| 3 |

| Table of Contents |

We are subject to the inherent risk of exposure to product liability claims, actions and litigation.

As a distributor of products designed to be ingested by humans, we face an inherent risk of exposure to product liability claims, regulatory action and litigation if our products are alleged to have caused bodily harm or injury. In addition, the sale of our products involves the risk of injury to consumers due to tampering by unauthorized third parties or product contamination. Adverse reactions resulting from human consumption of our products alone or in combination with other medications or substances could occur. We may be subject to various product liability claims, including, among others, that our products caused injury or illness, include inadequate instructions for use or include inadequate warnings concerning health risks, possible side effects or interactions with other substances. Product liability claims or regulatory actions against us could result in increased costs, could adversely affect our reputation with our clients and consumers generally, and could have a material adverse effect on our results of operations and financial condition. There can be no assurances that we will be able to obtain or maintain product liability insurance on acceptable terms or with adequate coverage against potential liabilities. Such insurance is expensive and may not be available in the future on acceptable terms, or at all. The inability to obtain sufficient insurance coverage on reasonable terms or to otherwise protect against potential product liability claims could prevent or inhibit the commercialization of our potential products.

We are subject to the inherent risks involved with product recalls.

Manufacturers and distributors of products are sometimes subject to the recall or return of their products for a variety of reasons, including product defects, such as contamination, unintended harmful side effects or interactions with other substances, packaging safety and inadequate or inaccurate labeling disclosure. If any of our products are recalled due to an alleged product defect or for any other reason, we could be required to incur the unexpected expense of the recall and any legal proceedings that might arise in connection with the recall. We may lose a significant amount of sales and may not be able to replace those sales at an acceptable margin, or at all. In addition, a product recall may require significant management attention. There can be no assurance that any quality, potency or contamination problems will be detected in time to avoid unforeseen product recalls, regulatory action or lawsuits. Additionally, if our products are subject to recall, our reputation could be harmed. A recall for any of the foregoing reasons could lead to decreased demand for our products and could have a material adverse effect on our results of operations and financial condition. Additionally, product recalls may lead to increased scrutiny of our operations by regulatory agencies, requiring further management attention, potential loss of applicable licenses, and potential legal fees and other expenses.

The Company’s products could have unknown side effects.

If the products the Company sells are not perceived to have the effects intended by the end user, its business may suffer and the business may be subject to products liability or other legal actions. Many of the Company’s products contain innovative ingredients or combinations of ingredients. There is little long-term data available with respect to efficacy, unknown side effects and/or interaction with individual human biochemistry, or interaction with other drugs. Moreover, there is little long-term data available with respect to efficacy, unknown side effects and/or its interaction with individual animal biochemistry. As a result, the Company’s products could have certain side effects if not taken as directed or if taken by an end user that has certain known or unknown medical conditions.

The Company may be unable to anticipate changes in its potential client requirements that could make the Company’s existing products and services obsolete. The Company’s success will depend, in part, on its ability to continue to enhance its product and service offerings so as to address the increasing sophistication and varied needs of the market and respond to technological and regulatory changes and emerging industry standards and practices on a timely and cost-effective basis.

Research regarding the medical benefits, viability, safety, efficacy, use and social acceptance of cannabis or isolated cannabinoids (such as CBD and tetrahydrocannabinol (“THC”)) remains in early stages.

There have been relatively few clinical trials on the benefits of cannabis or isolated cannabinoids (such as CBD and THC). Although the Company believes that the articles, reports and studies support its beliefs regarding the medical benefits, viability, safety, efficacy, dosing and social acceptance of cannabis, future research and clinical trials may prove such statements to be incorrect, or could raise concerns regarding, and perceptions relating to, cannabis. Given these risks, uncertainties and assumptions, investors should not place undue reliance on such articles and reports. Future research studies and clinical trials may draw opposing conclusions to those stated herein or reach negative conclusions related to medical cannabis, which could have a material adverse effect on the demand for the Company’s products, which could result in a material adverse effect on our business, financial condition and results of operations or prospects.

Our growth depends, in part, on expanding into additional consumer markets, and we may not be successful in doing so.

We believe that our future growth depends not only on continuing to provide our current customers with new products, but also continuing to enlarge our customer base. The growth of our business will depend, in part, on our ability to continue to expand in the United States, as well as into international markets. We are investing significant resources in these areas, and although we hope that our products will gain popularity, we may face challenges that are different from those we currently encounter, including competitive merchandising, distribution, hiring, and other difficulties. We may also encounter difficulties in attracting customers due to a lack of consumer familiarity with or acceptance of our brand, or a resistance to paying for premium products, particularly in international markets. In addition, although we are investing in sales and marketing activities to further penetrate newer regions, including expansion of our dedicated sales force, we may not be successful. If we are not successful, our business and results of operations may be harmed.

| 4 |

| Table of Contents |

Fluctuations in the cost and availability of raw materials, equipment, labor, and transportation could cause manufacturing delays or increase our costs.

The price and availability of key components used to manufacture our products has been increasing and may continue to fluctuate significantly. In addition, the cost of labor within our company or at our third-party manufacturers could increase significantly due to regulation or inflationary pressures. Additionally, the cost of logistics and transportation fluctuates in large part due to the price of oil, and availability can be limited due to political and economic issues. Any fluctuations in the cost and availability of any of our raw materials, packaging, or other sourcing or transportation costs could harm our gross margins and our ability to meet customer demand. If we are unable to successfully mitigate a significant portion of these product cost increases or fluctuations, our results of operations could be harmed.

We rely on third-parties for raw materials and to manufacture and compound some of our products. We have no control over these third parties and if these relationships are disrupted our results of operations in future periods will be adversely impacted.

We currently hold short term supply contracts with unaffiliated third-party vendors for our critical raw materials. In addition, some of our products are manufactured or compounded by unaffiliated third parties and the use of these third-party co-packers changes from time to time due to customer demand and the composition of our product mix and product portfolio. We do not have any long-term contracts with any of these third parties, and we expect to compete with other companies for raw materials, production and imported packaging material capacity. If we experience significant increased demand or need to replace an existing raw material supplier or third-party manufacturer, there can be no assurances that replacements for these third-party vendors will be available when required on terms that are acceptable to us, or at all, or that any manufacturer or compounder would allocate sufficient capacity to us in order to meet our requirements. In addition, even if we are able to expand existing or find new sources, we may encounter delays in production and added costs as a result of the time it takes to engage third parties. Any delays, interruption or increased costs in raw materials and/or the manufacturing or compounding of our products could have an adverse effect on our ability to meet retail customer and consumer demand for our products and result in lower revenues and net income both in the short and long-term.

The Company’s inventory has a shelf life and may reach its expiration and not be sold.

The Company holds finished goods in inventory and its inventory has a shelf life. Finished goods in the Company’s inventory may include cannabis flower, cannabis oil products and cosmeceuticals. The Company’s inventory may reach its expiration and not be sold. Although management regularly reviews the quantity and remaining shelf life of inventory on hand, and estimates manufacturing and sales lead times in order to manage its inventory, write-downs of inventory may still be required. Any such write-down of inventory could have a material adverse effect on the Company’s business, financial condition, and results of operations.

The Company may not be able to maintain effective quality control systems.

The Company may not be able to maintain an effective quality control system. The Company ascribes its early successes, in part, on its commitment to product quality and its effective quality control system. The effectiveness of the Company’s quality control system and its ability to obtain or maintain good manufacturing practice (“GMP”) certification with respect to its manufacturing, processing and testing facilities depend on a number of factors, including the design of its quality control procedures, training programs, and its ability to ensure that its employees adhere to the Company’s policies and procedures. The Company also depends on service providers such as toll manufacturers and contract laboratories to manufacture, process or test its products that are subject to GMP certification requirements.

We expect that regulatory agencies will periodically inspect our and our service providers’ facilities to evaluate compliance with applicable GMP requirements. Failure to comply with these requirements may subject us or our service providers to possible regulatory enforcement actions. Any failure or deterioration of the Company’s or its service providers’ quality control systems, including loss of GMP certification, may have a material adverse effect on the Company’s business, results of operations and financial condition.

Energy prices and supply may be subject to change or curtailment due to new laws or regulations, imposition of new taxes or tariffs, interruptions in production by suppliers, imposition of restrictions on energy supply by government, worldwide price levels and market conditions.

The Company requires diesel and electric energy and other resources for its cultivation and harvest activities and for transportation of cannabis. The Company relies upon third parties for its supply of energy resources used in its operations. The prices for and availability of energy resources may be subject to change or curtailment, respectively, due to, among other things, new laws or regulations, imposition of new taxes or tariffs, interruptions in production by suppliers, imposition of restrictions on energy supply by government, worldwide price levels and market conditions. Although the Company attempts to mitigate the effects of fuel shortages, electricity outages and cost increases, the Company’s operations will continue to depend on external suppliers of fuel and electricity. If energy supply is cut for an extended period and the Company is unable to find replacement sources at comparable prices, or at all, the Company’s business, financial condition and results of operations could be materially and adversely affected.

The cannabinoid industry faces strong opposition and may face similar opposition in other jurisdictions in which we operate.

Many political and social organizations oppose hemp and cannabis and their legalization, and many people, even those who support legalization, oppose the sale of hemp and cannabis in their geographies. Our business will need support from local governments, industry participants, consumers and residents to be successful. Additionally, there are large, well-funded businesses that may have a strong opposition to the cannabis industry. For example, the pharmaceutical and alcohol industries have traditionally opposed cannabis legalization. Any efforts by these or other industries to halt or impede the cannabis industry could have detrimental effects on our business.

| 5 |

| Table of Contents |

We are subject to the risks inherent in an agricultural business.

Our business involves the growing of cannabis, which is an agricultural product. The occurrence of severe adverse weather conditions, especially droughts, fires, storms or floods is unpredictable and may have a potentially devastating impact on agricultural production and may otherwise adversely affect the supply of cannabis. Adverse weather conditions may be exacerbated by the effects of climate change and may result in the introduction and increased frequency of pests and diseases. The effects of severe adverse weather conditions may reduce our yields or require us to increase our level of investment to maintain yields. Additionally, higher than average temperatures and rainfall can contribute to an increased presence of insects and pests, which could negatively affect cannabis crops. Future droughts might reduce the yield and quality of our cannabis production, which could materially and adversely affect our business, financial condition and results of operations.

The occurrence and effects of plant disease, insects and pests can be unpredictable and devastating to agricultural production, potentially rendering all or a substantial portion of the affected harvests unsuitable for sale. Even when only a portion of the production is damaged, our results of operations could be adversely affected because all or a substantial portion of the production costs may have been incurred. Although some plant diseases are treatable, the cost of treatment can be high and such events could adversely affect our operating results and financial condition. Furthermore, if we fail to control a given plant disease and the production is threatened, we may be unable to adequately supply our customers, which could adversely affect our business, financial condition and results of operations. There can be no assurance that natural elements will not have a material adverse effect on production.

Our operations could be materially and adversely affected if the supply of cannabis seeds is ceased or delayed and we do not find replacement suppliers and obtain all necessary authorizations.

If for any reason the supply of cannabis seeds is ceased or delayed, we would have to seek alternate suppliers for a number of our current cultivars and obtain all necessary authorization for the new seeds. If replacement seeds cannot be obtained at comparable prices, or at all, or if the necessary authorizations are not obtained, our business, financial condition and results of operations would be materially and adversely affected.

Many of our competitors have greater resources that may enable them to compete more effectively than us in the cannabis industry.

The industry in which we operate is subject to intense and increasing competition. Some of our competitors have a longer operating history and greater capital resources and facilities, which may enable them to compete more effectively in this market. We expect to face additional competition from existing licensees and new market entrants who are granted licenses in Colombia, who are not yet active in the industry. If a significant number of new licenses are granted in the near term, we may experience increased competition for market share and may experience downward pricing pressure on our products as new entrants increase production. Such competition may cause us to encounter difficulties in generating revenues and market share, and in positioning our products in the market. If we are unable to successfully compete with existing companies and new entrants to the market, our lack of competitive advantage will have a negative effect on our business and financial condition.

The Company could face competitive risks from the development and distribution of synthetic cannabis.

The pharmaceutical industry and others may attempt to enter the cannabis industry and, in particular, the medical cannabis industry through the development and distribution of synthetic products that emulate the effects of and treatment provided by naturally occurring cannabis. If synthetic cannabis products are widely adopted, the widespread popularity of such synthetic cannabis products could change the demand, volume and profitability of the botanical cannabinoid industry. This could adversely affect our ability to secure long-term profitability and success through the sustainable and profitable operation of our business.

The Company is reliant on third party transportation services and importation services to deliver its products to customers.

The Company relies on third party transportation services and importation services to deliver its products to its customers. The Company is exposed to the inherent risks associated with relying on third party transportation service-providers, including logistical problems, delays, loss or theft of product and increased shipping and insurance costs. Any delay in transporting the product, breach of security or loss of product, could have a material adverse effect on the Company’s business, financial performance and results of operations. Further, any breach of security and loss of product during transport could affect the Company’s status as a licensed producer in Colombia.

The Company is dependent on suppliers to supply equipment, parts and components for the operation of its business.

The Company’s ability to compete and grow will be dependent upon having access, at a reasonable cost and in a timely manner, to equipment, parts and components. No assurances can be given that the Company will be successful in maintaining the required supply of equipment, parts and components. It is also possible that the final costs of the major equipment contemplated by capital expenditure programs may be significantly greater than anticipated or available, in which circumstance there could be a materially adverse effect on the Company’s financial results.

| 6 |

| Table of Contents |

We may not be able to establish and maintain bank accounts in certain countries.

There is a risk that banking institutions in countries where we operate will not open accounts for us or will not accept payments or deposits from proceeds related to the cannabis industry. Such risks could increase our costs or prevent us from expanding into certain jurisdictions.

The Company may be subject to cyber-security and privacy risks that could disrupt its operations and expose the Company to financial losses, contractual losses, liability, reputational damage and additional expense.

The Company may be subject to risks related to our information technology systems, including cyber-attacks, malware, ransomware and phishing attacks that could target our intellectual property, trade secrets, financial information, personal information of our employees, customers and patients, including sensitive personal health information. The occurrence of such an attack could disrupt our operations and expose the Company to financial losses, contractual damages, liability under labor and privacy laws, reputational damage and additional expenses. We have implemented security measures to protect our data and information technology systems; however, such measures may not be effective in preventing cyber-attacks. We may be required to allocate additional resources to implement additional preventative measures including significant investments in information technology systems. A serious cyber-security breach could have a material adverse effect on our business, financial condition and results of operations.

The Company may collect and store certain personal information about customers and is responsible for protecting such information from privacy breaches. A privacy breach may occur through procedural or process failure, information technology malfunction, or deliberate unauthorized intrusions. In addition, theft of data is an ongoing risk whether perpetrated via employee collusion or negligence or through deliberate cyber-attack. Any such privacy breach or theft could have a material adverse effect on the Company’s business, financial condition and results of operations. If the Company were found to be in violation of privacy or security rules or other laws protecting the confidentiality of information, the Company could be subject to sanctions and civil or criminal penalties, which could increase its liabilities, harm its reputation and have a material adverse effect on the Company’s business, financial condition and results of operations.

The Company may incur significant costs to defend its intellectual property and other proprietary rights.

The ownership and protection of trademarks, patents, trade secrets and intellectual property rights are significant aspects of the Company's future success. Unauthorized parties may attempt to replicate or otherwise obtain and use the Company's products and technology. Policing the unauthorized use of the Company's current or future trademarks, patents, trade secrets or intellectual property rights could be difficult, expensive, time-consuming and unpredictable, as may be enforcing these rights against unauthorized use by others.

In addition, other parties may claim that the Company's products infringe on their proprietary and perhaps patent protected rights. Such claims, regardless of their merit, may result in the expenditure of significant financial and managerial resources, legal fees, injunctions, temporary restraining orders and/or require the payment of damages. As well, the Company may need to obtain licenses from third parties who allege that the Company has infringed on their lawful rights. Such licenses may not be available on terms acceptable to the Company or at all. In addition, the Company may not be able to obtain or utilize on terms that are favorable to it, or at all, licenses or other rights with respect to intellectual property that it does not own.

Risks Related to Operations in Colombia

We are reliant on certain licenses and authorizations to operate in Colombia.

Our ability to grow, store and sell cannabis in Colombia is dependent on our ability to sustain and/or obtain the necessary licenses and authorizations by certain authorities in Colombia. To date, we have received the Non-Psychoactive Cannabis Cultivation License, the Cannabis Derivatives Manufacturing License and the Psychoactive Cannabis Cultivation License including a quota for export of 43,500 kilograms in 2022. The effects of the compliance regime, any delays in obtaining, or failure to obtain or keep the regulatory approvals may significantly delay or impair the development of markets, products and sales initiatives and could have a material adverse effect on our business, results of operations and financial condition. In addition, the medical cannabis compliance process requires research phases to ensure both the cultivation process and subsequent derivatives are standardized and express the same or similar cannabinoid and terpene profiles while remaining free of pesticides, heavy metals and other microbial or external containments. Therefore any delay or changes in these conditions may significantly delay or impair products and sales initiatives and could have an adverse effect on our business.

The licenses and authorizations are subject to ongoing compliance and reporting requirements and our ability to obtain, sustain or renew any such licenses and authorizations on acceptable terms is subject to changes in regulations and policies and to the discretion of the applicable authorities or other governmental agencies in Colombia and potentially in other foreign jurisdictions. Failure to comply with the requirements of the licenses or authorizations or any failure to maintain the licenses or authorizations would have a material adverse effect on our business, financial condition and operating results. Specifically, the validity of the licenses for the cultivation of psychoactive cannabis, non-psychoactive and the manufacture of cannabis derivatives is ten (10) years pursuant to Article 8 of resolution 227 of 2022, in accordance with the provisions of article 2.8. 11 .2 .1.8. replacement by Decree 811 of 2021 and the Law 1787 of 2016 in relation to the medical and scientific use of cannabis. Such licenses may be renewed for an equal period as many times as requested by the licensee. The license will remain valid as long as it complies with the requirements established by law.

Although we believe that we will meet the requirements to obtain, sustain or renew the necessary licenses and authorizations, there can be no guarantee that the applicable authorities will issue these licenses or authorizations. Should the authorities fail to issue the necessary licenses or authorizations, we may be curtailed or prohibited from the production and/or distribution of cannabis or from proceeding with the development of our operations as currently proposed and our business, results of operations and financial condition may be materially adversely affected.

| 7 |

| Table of Contents |

Restrictions or regulations concerning changes in corporate structure may discourage transactions that otherwise could involve payment of a premium over prevailing market processes for our securities.

Colombian cannabis licenses are granted on a non-transferable, non-exchangeable and non-assignable basis. Any breach of this restriction may result in the revocation of the license. While there are no specific regulations or restrictions regarding the effects of a change in control, modification of the corporate structure, issuance of shares, or any changes in holders or final beneficiaries on the cannabis licenses, these restrictions may discourage transactions that otherwise could involve payment of a premium over prevailing market prices for our securities.

While we do not currently operate in protected areas established by the National System of Protected Areas, we cannot provide assurances that areas in which we operate will not be subject to risks associated therewith in the future.

Under Colombian laws, competent governmental authorities are not allowed to grant any type of cannabis licenses on properties that are located within areas registered as national parks or protected areas in the National System of Protected Areas (“SINAP”). Additionally, the Colombian government is entitled to create new protected areas based on their environmental relevance, which might result in the prohibition to conduct any type of activities on those areas or the need to obtain specific environmental authorizations or permits.

We do not operate in a protected area and we believe that we are not currently at risk of expropriation pursuant to the SINAP, but we cannot assure you that the areas in which we operate will not be subject to such risks in the future.

Economic and political conditions in Colombia may have an adverse effect on our financial condition and results of operations.

Many of our operations are located in Colombia. Consequently, a portion of our financial condition and results of operations depend significantly on macroeconomic and political conditions prevailing in Colombia. Decreases in the growth rate, periods of negative growth, increases in inflation, changes in law, regulation, policy, or future judicial rulings and interpretations of policies involving exchange controls and other matters such as (but not limited to) currency depreciation, inflation, interest rates, taxation, banking laws and regulations and other political or economic developments in or affecting Colombia may affect the overall business environment and may, in turn, adversely affect our financial condition and results of operations in the future. The Colombian government frequently intervenes in Colombia’s economy and from time to time makes significant changes in monetary, fiscal and regulatory policy. Our business and results of operations or financial condition may be adversely affected by changes in government or fiscal policies, and other political, diplomatic, social and economic developments that may affect Colombia. We cannot predict what policies the Colombian government will adopt and whether those policies would have a negative effect on the Colombian economy or on our business and financial performance in the future.

We cannot assure you whether current stability in the Colombian economy will be sustained. If the condition of the Colombian economy were to deteriorate, we would likely be adversely affected.

Certain of the Company’s key documents are in Spanish, and translations may not exist or be readily available.

As a result of the Company conducting its operations in Colombia, certain of the Company’s subsidiaries’ books and records, including key documents such as material contracts and financial documentation are principally negotiated and entered into in the Spanish language and English translations may not exist or be readily available. The Company relies on the use of professional translators for in person meetings with non-Spanish speakers where required, and for document translation. The Company does not foresee that significant additional accommodations will be required. The Company does not have a formal communication plan that sets out measures that will be taken to mitigate any potential communication-related issues as it does not consider one necessary. All material documents provided to the directors are in the English language. If any material documents are in an original language other than English, the documents are translated by certified translators. All members of the Company’s Board of Directors and its executive officers are fluent in English. Additionally, Luis Merchan, our Chairman and CEO and Juan Carlos Gomez Roa, a director, are fluent in the Spanish language.

The Colombian government and the Central Bank exercise significant influence on Colombia’s economy.

Although the Colombian government has not imposed foreign exchange restrictions since 1990, Colombia’s foreign currency markets have historically been extremely regulated. Colombian law permits the Central Bank of Colombia (the “Central Bank”) to impose foreign exchange controls to regulate the remittance of dividends and/or foreign investments in the event that the foreign currency reserves of the Central Bank fall below a level equal to the value of three months of imports of goods and services into Colombia. An intervention that precludes our Colombian subsidiary from possessing, utilizing or remitting U.S. Dollars would impair our financial condition and results of operations, and would impair the Colombian subsidiary’s ability to convert any dividend payments to U.S. dollars.

The Colombian government and the Central Bank may also seek to implement new policies aimed at controlling further fluctuation of the Colombian peso against the U.S. dollar and fostering domestic price stability. The Central Bank may impose certain mandatory deposit requirements in connection with foreign-currency denominated loans obtained by Colombian residents. We cannot predict or control future actions by the Central Bank in respect of such deposit requirements, which may involve the establishment of a different mandatory deposit percentage. The U.S. dollar/Colombian peso exchange rate has shown some instability in recent years.

| 8 |

| Table of Contents |

Colombia has experienced several periods of violence and instability that could affect the economy and our Company.

Colombia has experienced periods of criminal violence over the past four decades, primarily due to the activities of guerilla groups and drug cartels. Despite the peace treaty between the Colombian government and the Revolutionary Armed Forces of Colombia (Fuerzas Armadas Revolucionarias de Colombia or FARC), a lasting decrease in violence or drug-related crime in Colombia or the successful integration of former guerilla members into Colombian society may not be achieved. In 2018, the Colombian government suspended the peace negotiations with the National Liberation Army (Ejército de Liberación Nacional or ELN) and, in 2019, a minority group of dissidents of the peace process with FARC announced their return to illegal activities. Violence incidents could create a security risk for our key employees in Colombia and require them to leave the country.

Allegations of corruption against the Colombian government, at the national or local level, politicians and private industry could create economic and political uncertainty should the investigations triggered by these cases reach conclusions or result in further allegations or findings of illicit conduct committed by the accused parties. Furthermore, proven or alleged wrongdoings could have adverse effects on the political stability in Colombia and the Colombian economy.

An escalation of violence, drug-related crime, or political instability may have a negative impact on the Colombian economy and on our business, financial condition and results of operations.

The Company is subject to risks from its construction projects.

The Company is subject to a number of risks in connection with the construction of facilities in Colombia and the United States, including the availability and performance of engineers and contractors, suppliers and consultants and the receipt of required governmental approvals, licenses and permits. Any delay in the performance of any one or more of the contractors, suppliers, consultants or other persons on which the Company is dependent in connection with its construction activities, a delay in or failure to receive the required governmental approvals, licenses and permits in a timely manner or on reasonable terms, or a delay in or failure in connection with the completion and successful operation of the operational elements in connection with any capital or construction project.

Any additional taxes resulting from changes to tax regulations or the interpretation thereof in Colombia or other countries where we operate, could adversely affect our consolidated results.

Uncertainty relating to tax legislation poses a constant risk to us. Colombian national authorities have levied new taxes in recent years. Changes in legislation, regulation and jurisprudence can affect tax burdens by increasing tax rates and fees, creating new taxes, limiting stated expenses and deductions, and eliminating incentives and non-taxed income.

Additional tax regulations could be implemented that could require us to make additional tax payments, negatively affecting our financial condition, results of operation, and cash flow. In addition, either national or local taxing authorities may not interpret tax regulations in the same way that we do. Differing interpretations could result in future tax litigation and associated costs.

Risks Related to Our Regulatory Framework

Marijuana remains illegal under U.S. federal law, and the enforcement of U.S. cannabis laws could change.

There are significant legal restrictions and regulations that govern the cannabis industry in the United States. Marijuana remains a Schedule I drug under the Controlled Substances Act, making it illegal under federal law in the United States to, among other things, cultivate, distribute or possess cannabis in the United States. In those states in which the use of marijuana has been legalized, its use remains a violation of federal law pursuant to the Controlled Substances Act. The Controlled Substances Act classifies marijuana as a Schedule I controlled substance, and as such, medical and adult cannabis use is illegal under U.S. federal law. Unless and until the U.S. Congress amends the Controlled Substances Act with respect to marijuana (and the President approves such amendment), there is a risk that federal authorities may enforce current federal law. Financial transactions involving proceeds generated by, or intended to promote, cannabis-related business activities in the United States may form the basis for prosecution under applicable U.S. federal money laundering legislation. While the approach to enforcement of such laws by the federal government in the United States has trended toward non-enforcement against individuals and businesses that comply with medical or adult-use cannabis regulatory programs in states where such programs are legal, strict compliance with state laws with respect to cannabis will neither absolve us of liability under U.S. federal law, nor will it provide a defense to any federal proceeding which may be brought against us. Since U.S. federal law criminalizing the use of marijuana preempts state laws that legalize its use, enforcement of federal law regarding marijuana is a significant risk and would greatly harm our business, prospects, revenue, results of operation and financial condition. The enforcement of federal laws in the United States is a risk to our business and any proceedings brought against us thereunder may materially, adversely affect our operations and financial performance.

Our activities are, and will continue to be, subject to evolving regulation by governmental authorities. The legality of the production, cultivation, extraction, distribution, retail sales, transportation and use of cannabis differs among states in the United States. Due to the current regulatory environment in the United States, new risks may emerge; management may not be able to predict all such risks.

| 9 |

| Table of Contents |

Due to the conflicting views between state legislatures and the federal government regarding cannabis, cannabis businesses are subject to inconsistent laws and regulations. There can be no assurance that the federal government will not enforce federal laws relating to marijuana and seek to prosecute cases involving marijuana businesses that are otherwise compliant with state laws in the future. The prior U.S. administration attempted to address the inconsistent treatment of cannabis under state and federal law in the Cole Memorandum that Deputy Attorney General James Cole sent to all U.S. Attorneys in August 2013, which outlined certain priorities for the U.S. Department of Justice (the “DOJ”) relating to the prosecution of cannabis offenses. The Cole Memorandum noted that, in jurisdictions that have enacted laws legalizing cannabis in some form and that have also implemented strong and effective regulatory and enforcement systems to control the cultivation, production, distribution, sale and possession of cannabis, conduct in compliance with such laws and regulations was not a priority for the DOJ. However, the DOJ did not provide (and has not provided since) specific guidelines for what regulatory and enforcement systems would be deemed sufficient under the Cole Memorandum.

There can be no assurance that the federal government will not enforce federal laws relating to cannabis and seek to prosecute cases involving cannabis businesses that are otherwise compliant with state laws in the future. Most states that have legalized cannabis continue to craft their regulations pursuant to the Cole Memorandum. Federal enforcement agencies have taken little or no action against state-compliant cannabis businesses. However, the DOJ may change its enforcement policies at any time, with or without advance notice.

The uncertainty of U.S. federal enforcement practices going forward and the inconsistency between U.S. federal and state laws and regulations present major risks for the Company.

Changes to federal or state laws pertaining to industrial hemp could slow the use of industrial hemp which would materially impact our revenues in future periods.

As of the date hereof, approximately 46 states have authorized industrial hemp programs pursuant to the United States of the Agricultural Improvement Act of 2018, commonly known as the “Farm Bill,” or under prior programs authorized under the 2014 Farm Bill or have plans under review by the United States Department of Agriculture (“USDA”). Effective January 1, 2022, several states without an approved plan under the Farm Bill, or a plan under review, will default to the USDA Hemp Producer License. Continued development of the industrial hemp industry will be dependent upon new legislative authorization of industrial hemp at the state level, and further amendment or supplementation of legislation at the federal level. Any number of events or occurrences could slow or halt progress all together in this space. While progress within the industrial hemp industry is currently encouraging, growth is not assured. While there appears to be ample public support for favorable legislative action, numerous factors may impact or negatively affect the legislative process(es) within the various states where we have business interests. Any one of these factors could slow or halt use of industrial hemp, which could negatively impact the business up to possibly causing us to discontinue operations as a whole. In addition, changes in Federal or state laws could require us to alter the way we conduct our business in order to remain compliant with applicable state laws in ways we are presently unable to foresee. These possible changes, if necessary, could be costly and may adversely impact our results of operations in future periods.

Uncertainty caused by potential changes to legal regulations could impact the use of CBD products.

There is substantial uncertainty and different interpretations among federal, state and local regulatory agencies, legislators, academics and businesses as to the scope of operation of Farm Bill-compliant hemp programs relative to the emerging regulation of cannabinoids. These different opinions include, but are not limited to, the regulation of cannabinoids by the U.S. Drug Enforcement Administration and/or the Food and Drug Administration (“FDA”) and the extent to which manufacturers of products containing Farm Bill-compliant cultivators and processors may engage in interstate commerce. The uncertainties cannot be resolved without further federal, and perhaps even state-level, legislation, regulation or a definitive judicial interpretation of existing legislation and rules. If these uncertainties continue, they may have an adverse effect upon the introduction of our products in different markets.

Any failure on our part to comply with applicable regulations could prevent us from being able to carry on our business, and there may be additional costs associated with any such failure.

Our business activities are heavily regulated in all jurisdictions where we do business. Our operations are subject to various laws, regulations and guidelines by governmental authorities relating to the cultivation, processing, manufacture, marketing, management, distribution, transportation, storage, sale, packaging, labeling, pricing and disposal of cannabis and cannabis products. In addition, we are subject to laws and regulations relating to employee health and safety, insurance coverage and the environment. Laws and regulations, applied generally, grant government agencies and self-regulatory bodies broad administrative discretion over our activities, including the power to limit or restrict business activities as well as impose additional disclosure requirements on our products and services.

Any failure by us to comply with the applicable regulatory requirements could

· | require extensive changes to our operations; |

|

|

· | result in regulatory or agency proceedings or investigations; |

|

|

· | result in the revocation of our licenses and permits, increased compliance costs; |

|

|

· | result in damage awards, civil or criminal fines or penalties; |

|

|

· | result in restrictions on our operations; |

|

|

· | harm our reputation; or |

|

|

· | give rise to material liabilities. |

| 10 |

| Table of Contents |

There can be no assurance that any future regulatory or agency proceedings, investigations or audits will not result in substantial costs, a diversion of management’s attention and resources or other adverse consequences to our business.

Achievement of our business objectives is contingent, in part, upon compliance with regulatory requirements enacted by governmental authorities and obtaining all necessary regulatory approvals for the cultivation, processing, production, storage, distribution, transportation, sale, import and export, as applicable, of our products. Any failure to comply with the regulatory requirements applicable to our operations may lead to possible sanctions, including:

· | the revocation or imposition of additional conditions on licenses to operate our business; |

|

|

· | the suspension or expulsion from a particular market or jurisdiction or of our key personnel; |

|

|

· | the imposition of additional or more stringent inspection, testing and reporting requirements; |

|

|

· | product recalls or seizures; and |

|

|

· | the imposition of fines and censures. |

In addition, changes in regulations, government or judicial interpretation of regulations, or more vigorous enforcement thereof or other unanticipated events could require extensive changes to our operations, increase compliance costs or give rise to material liabilities or a revocation of our licenses and other permits. Furthermore, governmental authorities may change their administration, application or enforcement procedures at any time, which may adversely affect our ongoing regulatory compliance costs. There is no assurance that we will be able to comply or continue to comply with applicable regulations.

The FDA limits the ability to discuss the medical benefits of CBD.

Under FDA rules it is illegal for companies to make “health claims” or claim that a product has a specific medical benefit. The FDA has not recognized any medical benefits derived from CBD, which means that we are not legally permitted to advertise any potential health claims related to our CBD products. Because of the perception among many consumers that CBD is a health/medicinal product, the inability to make such health claims about its CBD products may limit our ability to market and sell products to consumers, which would negatively affect our revenues and profits.

The legal cannabis market is a relatively new industry. As a result, the size of our target market is difficult to quantify, and investors will be reliant on their own estimates on the accuracy of market data.

Because the cannabis industry is in a nascent stage, there is a lack of information about comparable companies available for potential investors to review and to decide whether to invest in us and, few, if any, established companies whose business model we can follow or upon whose success we can build. Accordingly, investors should rely on their own estimates regarding the potential size, economics and risks of the cannabis market in deciding whether to invest in our Common Shares. We are an early-stage company that has not generated net income. There can be no assurance that our growth estimates are accurate or that the cannabis market will be large enough for our business to grow as projected.