UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM

AMENDMENT NO. 1

FOR

THE FISCAL YEAR ENDED

OR

| [ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

COMMISSION FILE NUMBER:

(Exact name of registrant as specified in its charter)

(State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) | ||

3F K’s Minamiaoyama 6-6-20 Minamiaoyama, Minato-ku, Tokyo 107-0062, Japan |

107-0062 | ||

| (Address of Principal Executive Offices) | (Zip Code) |

Securities to be registered under Section 12(b) of the Act: None

Securities to be registered under Section 12(g) of the Exchange Act:

| Title of each class | Name of each exchange on which registered |

|||

| Common Stock, $0.0001 | N/A |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

[ ] Yes [X]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

[ ] Yes [X]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

[ ] Yes [X]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

[ ] Yes [X]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.

[ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act:

Large accelerated filer [ ] Accelerated filer

[ ]

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. [ ]

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

[ ] Yes [X]

As of January 31, 2022, the last business day of the

registrant’s most recently completed second fiscal quarter, the aggregate market value of the voting common stock held by

non-affiliates of the registrant was approximately $

As of June 2, 2023, there were shares of the Registrant’s Common Stock and shares of the Registrant’s Series A Preferred Stock issued and outstanding.

Explanatory Note: We are filing this Amendment No. 1 to our Form 10-K, originally filed on June 2, 2023, to revise a clerical error in the audit report previously provided by our PCAOB. In the previous audit report, the incorrect periods were mentioned. The audit report included herein has been revised accordingly. No other revisions have been made to our previous 10-K filed on June 2, 2023, and this copy should be read as of the date the original Form 10-K was filed, June 2, 2023.

- 1 -

TABLE OF CONTENTS

WB Burgers Asia, INC.

- 2 -

CAUTIONARY STATEMENT REGARDING FORWARD LOOKING STATEMENTS

This Current Report on Form 10-K contains forward-looking statements which involve risks and uncertainties, principally in the sections entitled “Business”, and “Management’s Discussion and Analysis of Financial Condition and Results of Operations”. All statements other than statements of historical fact contained in this Current Report on Form 10-K, including statements regarding future events, our future financial performance, business strategy and plans and objectives of management for future operations, are forward-looking statements. We have attempted to identify forward-looking statements by terminology including “anticipates”, “believes”, “can”, “continue”, “could”, “estimates”, “expects”, “intends”, “may”, “plans”, “potential”, “predicts”, or “should”, or the negative of these terms or other comparable terminology. Although we do not make forward-looking statements unless we believe we have a reasonable basis for doing so, we cannot guarantee their accuracy. These statements are only predictions and involve known and unknown risks, uncertainties and other factors that may appear in this Current Report on Form 10-K, which may cause our or our industry’s actual results, levels of activity, performance or achievements expressed or implied by these forward-looking statements to vary. Moreover, we operate in a very competitive and rapidly changing environment. New risks emerge from time to time and it is not possible for us to predict all risk factors, nor can we address the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause our actual results to differ materially from those contained in any forward-looking statements. All forward-looking statements included in this document are based on information available to us on the date hereof, and we assume no obligation to update any such forward-looking statements, except as expressly required by law.

You should not place undue reliance on any forward-looking statement, each of which applies only as of the date of this Current Report on Form 10-K. Except as required by law, we undertake no obligation to update or revise publicly any of the forward-looking statements after the date of this Current Report on Form 10-K to conform our statements to actual results or changed expectations.

All dollar amounts used throughout this Report are in US Dollars, unless otherwise stated. All amounts in Japanese Yen used throughout this Report are preceded by JPY, for example JPY 500, is referring to 500 Japanese Yen.

Restatement of Previously Issued Consolidated Financial Statements

We have restated herein our audited consolidated financial statements at July 31, 2021 for the fiscal year ended July 31, 2021. We have also restated impacted amounts within the accompanying footnotes to the consolidated financial statements.

Restatement Background

In August of 2022, the sole director of WB Burgers Asia, Inc.(the “Company”) was advised by M&K CPAs PLLC (“M&K”), its registered independent public accounting firm, that the Company’s previously issued financial statements included in its Annual Reports on Form 10-K for the year ended July 31, 2021, should be restated to correct historical errors related to the recognition of cash received for the sale of shares, the calculation of the fair market value of shares issued, and classifications due to the recapitalization of the Company. The restated financials also show the differences between this current Form 10-K and the previously filed report due to the consolidation of financial reporting to include all activity of the Company’s wholly owned subsidiary, WB Burgers, Japan Co., Ltd (“WBBJ”). WBBJ became a wholly owned subsidiary of the Company in September of 2021, after the preparation of the previous Form 10-K for the year ended July 31, 2021. As a result, we determined that we would restate such financial statements to correct the accounting errors and also highlight the restatement differences resulting from the financial consolidation of the Company and its subsidiary.

Description of misstatements

(1) Recognition of cash received for the sale of shares and recording of the related issuance of shares

We recorded adjustments for cash received for the sale of common shares that was incorrectly recognized. On July 1, 2021, cash for the purchase of 9,090,909 shares of common stock was received by related party, White Knight Co., Ltd. and was not held by the Company, via its subsidiary, until September 2021. Additionally, these shares were not issued to the purchaser on July 1, 2021 as previously reported but were issued after the fiscal year end, in October 2021.

(2) Recognition of financial activity of wholly owned subsidiary

We recorded adjustments made to the financial statements due to the consolidation of financial information with our wholly owned subsidiary.

(3) Adjustment to the fair market value of shares issued as compensation

We recorded an adjustment to the value of 1,000,000 shares of Series A preferred shares issued as compensation due to the adoption of a third party evaluation of those shares, which differed from our previous valuation.

(4) Retroactive restatements of shares cancelled and returned and shares exchanged in merger and reorganization

We recorded adjustments to the statement of owners’ equity to account for the revision, by the Company’s transfer agent, of the dates of shares cancelled and returned, and also shares exchanged pursuant to a reorganization. These retroactive date changes were due to the recapitalization of the Company pursuant to its reorganization, legally effective March 31, 2021 and when control of the Company passed from our previous controlling shareholder to our current controlling shareholder, who is our CEO and sole director, Koichi Ishizuka.

(5) Reclassification of additional paid-in capital

We reclassed the amount of expenses paid on behalf of the Company on the Statement of Cash Flows to properly report those payments as cash provided by operating activities rather than cash provided by financing activities.

- 3 -

PART I

Item 1. Business

Corporate History

We were originally incorporated in the state of Nevada on August 30, 2019, under the name Business Solutions Plus, Inc.

On August 30, 2019, Paul Moody was appointed Chief Executive Officer, Chief Financial Officer, President, Secretary, Treasurer, and Director.

On February 9, 2021, the Company filed, with the Secretary of State of Nevada (“NSOS”), Restated Articles of Incorporation.

On March 4, 2021, Business Solutions Plus, Inc., (the “Company” or “Successor”) announced on Form 8-K plans to participate in a holding company reorganization (“the Reorganization” or “Merger”) with InterActive Leisure Systems, Inc. (“IALS” or “Predecessor”), the Company and Business Solutions Merger Sub, Inc. (“Merger Sub”), collectively (the “Constituent Corporations”) pursuant to NRS 92A.180, NRS A.200, NRS 92A.230 and NRS 92A.250.

Immediately prior to the Reorganization, the Company was a direct and wholly owned subsidiary of Interactive Leisure Systems, Inc. and Business Solutions Merger Sub, Inc. was a direct and wholly owned subsidiary of the Company.

As disclosed in our 8-K filed on March 26, 2021, the above-mentioned Reorganization was legally effective as of March 31, 2021.

Each share of Predecessor’s common stock issued and outstanding immediately prior to the Effective Time was converted into one validly issued, fully paid and non-assessable share of Successor common stock. The control shareholder, (at the time) of the Predecessor, Flint Consulting Services, LLC, (“Flint”) a Wyoming limited liability company became the same control shareholder of the Successor. Jeffrey DeNunzio, as sole member of Flint was deemed to be the indirect and beneficial holder of 405,516,868 shares of Common Stock and 1,000,000 shares of Series A Preferred Stock of the Company representing, at the time, approximately 93.70% voting control of the Company. Paul Moody, (our now former sole officer/director), was the same officer/director of the Predecessor. There are/were no other shareholders or any officer/director holding at least 5% of the outstanding voting shares of the Company.

Immediately prior to the Effective Time, and under the respective articles of incorporation of Predecessor and Successor, the Successor Capital Stock had the same designations, rights, and powers and preferences, and the qualifications, limitations, and restrictions thereof, as the Predecessor Capital Stock which was automatically converted pursuant to the reorganization.

Immediately prior to the Effective Time, the articles of incorporation and bylaws of Successor, as the holding company, contain provisions identical to the Articles of Incorporation and Bylaws of Predecessor immediately prior to the merger, other than as permitted by NRS 92A.200.

Immediately prior to the Effective Time, the articles of incorporation of Predecessor stated that any act or transaction by or involving the Predecessor, other than the election or removal of directors of the Predecessor, that requires for its adoption under the NRS or the Articles of Incorporation of Predecessor the approval of the stockholders of the Predecessor, shall require in addition the approval of the stockholders of Successor (or any successor thereto by merger), by the same vote as is required by the articles of Incorporation and/or the bylaws of the Predecessor.

Immediately prior to the Effective Time, the articles of incorporation and bylaws of Successor and Merger Sub were identical to the articles of incorporation and bylaws of Predecessor immediately prior to the merger, other than as permitted by NRS 92A.200;

The Boards of Directors of Predecessor, Successor, and Merger Sub approved the Reorganization, shareholder approval not being required pursuant to NRS 92A.180;

The Reorganization constituted a tax-free organization pursuant to Section 368(a)(1) of the Internal Revenue Code;

Successor common stock traded in the OTC Markets under the Predecessor ticker symbol “IALS” under which the common stock of Predecessor previously listed and traded until the new ticker symbol “BSPI” was announced April 14, 2021, on the Financial Industry Regulatory Authority’s daily list with a market effective date of April 15, 2021. The CUSIP Number 45841W107 for IALS’s common stock was suspended upon market effectiveness. The Company received a new CUSIP Number 12330M107.

After completion of the Holding Company Reorganization, the Company cancelled all of its stock held in Predecessor resulting in the Company as a stand-alone and separate entity with no subsidiaries, no assets and negligible liabilities. The Company abandoned the business plan of its Predecessor and resumed its former business plan of a blank check company after completion of the Merger.

On May 4, 2021, Business Solutions Plus, Inc., a Nevada Corporation (the “Company”), entered into a Share Purchase Agreement (the “Agreement”) by and among Flint Consulting Services, LLC, a Wyoming Limited Liability Company (“FLINT”), and White Knight Co., Ltd., a Japan Company (“WKC”), pursuant to which, on May 7, 2021, (“Closing Date”), FLINT sold 405,516,868 shares of the Company’s Restricted Common Stock and 1,000,000 Shares of Series A Preferred Stock, representing approximately 93.70% voting control of the Company. The consummation of the transactions contemplated by the Agreement resulted in a change in control of the Company, with WKC becoming the Company’s largest controlling stockholder.

The sole shareholder of White Knight Co., Ltd., a Japanese Company, is Koichi Ishizuka.

On May 7, 2021, Mr. Paul Moody resigned as the Company’s Chief Executive Officer, Chief Financial Officer, President, Secretary, Treasurer, and Director.

On May 7, 2021, Mr. Koichi Ishizuka was appointed as the Company’s Chief Executive Officer, Chief Financial Officer, President, Secretary, Treasurer, and Director.

- 4 -

A Certificate of Amendment to change our name, from Business Solutions Plus, Inc., to WB Burgers Asia, Inc. was filed with the Nevada Secretary of State on June 18, 2021, with a legal effective date of July 2, 2021. The name change to WB Burgers Asia, Inc., as well as a change of our ticker symbol from BSPI to WBBA, was announced by FINRA, via their “daily list”, on July 7, 2021, with a market effective date of both on July 8, 2021. The new CUSIP number associated with our common stock, as of the market effective date of July 8, 2021, is 94684P100.

On July 1, 2021, we filed an amendment to our Articles of Incorporation with the Nevada Secretary of State, resulting in an increase to our authorized shares of common stock from 500,000,000 to 1,500,000,000.

Subsequent to the above action, on or about July 1, 2021, we sold 9,090,909 shares of restricted common stock to SJ Capital Co., Ltd., a Japanese Company, at a price of $0.20 per share of common stock. The total subscription amount paid by SJ Capital Co., Ltd. was approximately $1,818,181.80 or approximately 200,000,000 Japanese Yen.

SJ Capital Co., Ltd., is owned and controlled by Senju Pharmaceutical Co., Ltd., a Japanese Company.

Mr. Takeshi Sugisawa, the President of SJ Capital Co., Ltd., authorized the above transaction on behalf of SJ Capital Co., Ltd. Both SJ Capital Co., Ltd., and Senju Pharmaceutical Co., Ltd. are considered non-related parties to the Company.

The proceeds from the above sale of shares went to the Company to be used for working capital.

On August 24, 2021, we sold 1,363,636 shares of restricted common stock to Yasuhiko Miyazaki, a Japanese Citizen, at a price of $0.20 per share of common stock. The total subscription amount paid by Yasuhiko Miyazaki was approximately $272,727 or approximately 30,000,000 Japanese Yen. Mr. Yasuhiko Miyazaki is not a related party to the Company. The proceeds from the above sale of shares went to the Company to be used for working capital.

In regards to all of the above transactions, the Company claims an exemption from registration afforded by Section Regulation S of the Securities Act of 1933, as amended ("Regulation S") for the above sales/issuances of the stock since the sales/issuances of the stock were made to non-U.S. persons (as defined under Rule 902 section (k)(2)(i) of Regulation S), pursuant to offshore transactions, and no directed selling efforts were made in the United States by the issuer, a distributor, any of their respective affiliates, or any person acting on behalf of any of the foregoing.

On August 30, 2021, our largest controlling shareholder, White Knight Co., Ltd., a Japanese Company, owned and controlled by our sole officer and Director, Koichi Ishizuka, sold a total of 353,181,818 shares of restricted common stock of the Company to the following parties in the respective quantities:

| Name of Purchaser | Common Shares Purchased | Price Paid Per Share | Total Amount Paid ($) | |

|---|---|---|---|---|

| Koichi Ishizuka | 101,363,636 | $0.0001 | 10,136.00 | |

| Rei Ishizuka 1 | 50,000,000 | $0.0001 | 5,000.00 | |

| Kiyoshi Noda | 100,909,091 | $0.0001 | 10,091.00 | |

| Yuma Muranushi | 100,909,091 | $0.0001 | 10,091.00 |

1 Rei Ishizuka is the wife of our sole officer and Director, Mr. Koichi Ishizuka.

In regards to all of the above transactions White Knight Co., Ltd. claims an exemption from registration afforded by Section Regulation S of the Securities Act of 1933, as amended ("Regulation S") for the above sales of the stock since the sales of the stock were made to non-U.S. persons (as defined under Rule 902 section (k)(2)(i) of Regulation S), pursuant to offshore transactions, and no directed selling efforts were made in the United States by the issuer, a distributor, any of their respective affiliates, or any person acting on behalf of any of the foregoing.

On September 14, 2021, we entered into an “Acquisition Agreement” with White Knight Co., Ltd., a Japan Company, whereas we issued 500,000,000 shares of restricted common stock to White Knight Co., Ltd., in exchange for 100% of the equity interests of WB Burgers Japan Co., Ltd., a Japan Company. Following this transaction, WB Burgers Japan Co., Ltd. became our wholly owned subsidiary which we now operate through.

In regards to the above transaction, the Company claims an exemption from registration afforded by Section Regulation S of the Securities Act of 1933, as amended ("Regulation S") for the above sales/issuances of the stock since the sales/issuances of the stock were made to non-U.S. persons (as defined under Rule 902 section (k)(2)(i) of Regulation S), pursuant to offshore transactions, and no directed selling efforts were made in the United States by the issuer, a distributor, any of their respective affiliates, or any person acting on behalf of any of the foregoing.

- 5 -

The aforementioned Acquisition Agreement is attached as Exhibit 10.1 to our Form 8-K filed with the Securities and Exchange Commission on September 14, 2021. All references to the Acquisition Agreement are qualified, in their entirety, by the text of such exhibit.

White Knight Co., Ltd., is owned entirely by our sole officer and Director, Koichi Ishizuka. White Knight Co., Ltd. is our largest controlling shareholder.

WB Burgers Japan Co., Ltd., referred to herein as “WBJ”, which we now operate through and share the same business plan of, holds the rights to the “Master Franchise Agreement” with Jakes’ Franchising LLC, a Delaware Limited Liability Company, as it pertains to the establishment and operation of Wayback Burger Restaurants within the country of Japan.

The Master Franchise Agreement provides WBJ the right to establish and operate Wayback Burgers restaurants in the country of Japan, and also license affiliated and unaffiliated third parties (“Franchisees”) to establish and operate Wayback Burgers restaurants in the Country of Japan. The Master Franchise Agreement, amongst other things, also provides WBJ the right of first refusal to enter into a subsequent Master Franchise Agreement with Jake’s Franchising, LLC to establish and operate Wayback Burgers restaurants in the Countries of Indonesia, Malaysia (Eastern Malaysia only, Western Malaysia if it becomes available as it is currently licensed to another party), the Philippines, Vietnam, China, India, Korea, Thailand, Singapore, and Taiwan.

WB Burgers Japan Co., Ltd. seeks to make “Wayback Burgers” a nationally recognized brand, if not a household name, within the country of Japan through the promotion and opening of various Wayback Burgers Restaurants.

Following the acquisition of our now wholly owned subsidiary, WB Burgers Japan Co., Ltd., on September 14, 2021, we ceased to be a shell company. Immediately upon our acquisition of WB Burgers Japan Co., Ltd. we adopted the same business plan as WB Burgers Japan Co., Ltd.

On October 22, 2021, we sold 2,252,252 shares of restricted common stock to Shokafulin LLP, a Japan Company, which is controlled by Takuya Watanabe, a Japanese Citizen, at a price of $0.20 per share of common stock. The total subscription amount paid by Shokafulin LLP was approximately $450,450 or approximately 50,000,000 Japanese Yen. Shokafulin LLP and Mr. Watanabe are not related parties to the Company. The proceeds from the above sale of shares went to the Company to be used for working capital.

The aforementioned sale of shares was conducted pursuant to Regulation S of the Securities Act of 1933, as amended ("Regulation S"). The sale of shares was made only to non-U.S. persons (as defined under Rule 902 section (k)(2)(i) of Regulation S), pursuant to offshore transactions, and no directed selling efforts were made in the United States by the issuer, a distributor, any of their respective affiliates, or any person acting on behalf of any of the foregoing.

On November 6, 2021, our largest controlling shareholder, White Knight Co., Ltd., a Japanese Company, owned and controlled by our sole officer and Director, Koichi Ishizuka, sold a total of 14,347,826 shares of restricted common stock to the following parties in the respective quantities:

| Name of Purchaser | Common Shares Purchased | Price Paid Per Share ($) | Total Approximate Amount Paid ($) | |

|---|---|---|---|---|

| M&A Company 1 | 1,304,348 | 0.20 | 260,870 | |

| Michinari Yamamoto | 1,304,348 | 0.20 | 260,870 | |

| Atsushi Morikawa | 1,304,348 | 0.20 | 260,870 | |

| Motoki Hirai | 1,304,348 | 0.20 | 260,870 | |

| Tomonori Yoshinaga | 1,739,130 | 0.20 | 347,826 | |

| Go Watanabe | 3,043,478 | 0.20 | 608,696 | |

| Okakichi Co., Ltd 2 | 4,347,826 | 0.20 | 869,565 | |

| Total | 14,347,826 | 0.20 | 2,869,567 |

1 The authorized party of M&A Company, a Japan entity, is Akihiro Ando.

2 The authorized party of Okakichi Co., Ltd, a Japan entity, is Shigeru Okada.

In regards to all of the above transactions White Knight Co., Ltd. claims an exemption from registration afforded by Section Regulation S of the Securities Act of 1933, as amended ("Regulation S") for the above sales of the stock since the sales of the stock were made to non-U.S. persons (as defined under Rule 902 section (k)(2)(i) of Regulation S), pursuant to offshore transactions, and no directed selling efforts were made in the United States by the issuer, a distributor, any of their respective affiliates, or any person acting on behalf of any of the foregoing.

On November 9, 2021, our wholly owned subsidiary, WB Burgers Japan Co., Ltd., consummated a lease agreement with Arai Co., Ltd., a Japanese realty group, for the location of our first Wayback Burgers restaurant. The property is located in the popular shopping plaza of Omotesando, located in the Tokyo prefecture.

On December 27, 2021, we sold 1,315,789 shares of restricted Common Stock to Takahiro Fujiwara, Japanese Citizen, at a price of $0.20 per share of Common Stock. The total subscription amount paid by Takahiro Fujiwara was approximately $263,158. Takahiro Fujiwara is not a related party to the Company.

The aforementioned sale of shares was conducted pursuant to Regulation S of the Securities Act of 1933, as amended ("Regulation S"). The sale of shares was made only to non-U.S. persons (as defined under Rule 902 section (k)(2)(i) of Regulation S), pursuant to offshore transactions, and no directed selling efforts were made in the United States by the issuer, a distributor, any of their respective affiliates, or any person acting on behalf of any of the foregoing.

On or about February 8, 2022, we incorporated Store Foods Co., Ltd., a Japan Company. Store Foods Co., Ltd. is now a wholly owned subsidiary of the Company. Currently, Koichi Ishizuka is the sole Officer and Director of Store Foods Co., Ltd.

To date, Store Foods Co., Ltd. has yet to commence material operations. While our future plans for Store Foods Co., Ltd. are not definitive and may change, our intended business purpose for this company are as follows:

1. Food sales;

2. Food wholesale and retail;

3. Chain organizations consisting of food retailers as members;

4. Restaurants;

5. Manufacturing and sales of boxed lunches for catering;

6. Alcohol sales;

7. Health supplement and health drink sales;

8. Manufacturing and sales of functional foods;

9. Lease of goods related to restaurant management;

10. System development;

11. Delivery;

12. Application development and sales;

13. Advertising;

14. Management consulting;

15. All businesses incidental to any of the above.

- 6 -

On March 11, 2022 we opened our first flagship Wayback Burgers location to the public in the Omotesando shopping plaza. At this location, we offer an array of quick bites, including but not limited to traditional hamburgers, fries, shakes, and other alternatives.

On March 29, 2022, 869,565 shares of restricted Common Stock were sold to Hidemi Arasaki, Japanese Citizen, by our controlling shareholder, White Knight Co., Ltd., at a price of $0.20 per share of Common Stock. This was a private sale, not a sale made by the Company. The total amount paid by Hidemi Arasaki was approximately $173,913. Hidemi Arasaki is not a related party to the Company.

The aforementioned sale of shares was conducted pursuant to Regulation S of the Securities Act of 1933, as amended ("Regulation S"). The sale of shares was made only to non-U.S. persons (as defined under Rule 902 section (k)(2)(i) of Regulation S), pursuant to offshore transactions, and no directed selling efforts were made in the United States by the issuer, a distributor, any of their respective affiliates, or any person acting on behalf of any of the foregoing.

On May 20, 2022, we dismissed our independent registered public accounting firm, BF Borgers CPA PC (“BFG”) effective immediately. This decision was approved by the Company’s Board of Directors, comprised solely of Koichi Ishizuka.

On May 20, 2022, we engaged M&K CPAS, PLLC (“M&K”) as our new independent registered public accounting firm. This decision was approved by the Company’s Board of Directors, comprised solely of Koichi Ishizuka.

On August 8, 2022, we sold 1,586,538 shares of restricted Common Stock to Takahiro Fujiwara, a Japanese Citizen, at a price of $0.032 per share of Common Stock. The total subscription amount paid by Takahiro Fujiwara was approximately $50,769. Takahiro Fujiwara is not a related party to the Company.

On August 8, 2022, we sold 2,403,846 shares of restricted Common Stock to Shokafulin LLP, a Japanese Company, at a price of $0.032 per share of Common Stock. The total subscription amount paid by Shokafulin LLP was approximately $76,923. Shokafulin LLP is not a related party to the Company.

On August 12, 2022, we sold 32,065,458 shares of restricted Common Stock to Asset Acceleration Axis, LLC, a Japanese Company, at a price of $0.032 per share of Common Stock. The total subscription amount paid by Asset Acceleration Axis, LLC was approximately $1,026,094. Asset Acceleration Axis, LLC is not a related party to the Company.

The proceeds from these sales went to the Company to be used as working capital.

The aforementioned sale of shares was conducted pursuant to Regulation S of the Securities Act of 1933, as amended ("Regulation S"). The sale of shares was made only to non-U.S. persons (as defined under Rule 902 section (k)(2)(i) of Regulation S), pursuant to offshore transactions, and no directed selling efforts were made in the United States by the issuer, a distributor, any of their respective affiliates, or any person acting on behalf of any of the foregoing.

In August of 2022, we, through our wholly owned subsidiary, WB Burgers Japan Co., Ltd., entered into and consummated a rental agreement with “Kitchen Depot” for a ghost kitchen in the Tamachi neighborhood of Minato, Tokyo, Japan. Kitchen Depot is an unrelated third party, and the rental agreement is for a period of two years, with the option to renew at the conclusion. From this location, as of August 27, 2022, the Company has begun to offer delivery of Wayback Burgers menu items, such as those offered at the Company’s physical “dine in” restaurant location in the Omotesando shopping plaza, located in Tokyo, Japan. This new location only offers a delivery option with no option to dine in.

On September 13, 2022, we sold 7,262,324 shares of restricted Common Stock to Asset Acceleration Axis, LLC, a Japanese Company, at a price of $0.032 per share of Common Stock. The total subscription amount paid by Asset Acceleration Axis, LLC was approximately $232,395. Asset Acceleration Axis, LLC is not a related party to the Company.

The proceeds from these sales went to the Company to be used as working capital.

The aforementioned sale of shares was conducted pursuant to Regulation S of the Securities Act of 1933, as amended ("Regulation S"). The sale of shares was made only to non-U.S. persons (as defined under Rule 902 section (k)(2)(i) of Regulation S), pursuant to offshore transactions, and no directed selling efforts were made in the United States by the issuer, a distributor, any of their respective affiliates, or any person acting on behalf of any of the foregoing.

On October 4, 2022, 3,472,222 shares of restricted Common Stock of the Issuer were sold to Mitsuru Ueno, a Japanese Citizen, by White Knight Co., Ltd., at a price of $0.001 per share of Common Stock. This was a private sale. The total amount paid by Mitsuru Ueno was approximately $3,472.

On October 4, 2022, 3,472,222 shares of restricted Common Stock of the Issuer were sold to Motoki Hirai, a Japanese Citizen, by White Knight Co., Ltd., at a price of $0.001 per share of Common Stock. This was a private sale. The total amount paid by Motoki Hirai was approximately $3,472.

The aforementioned sales of shares, on October 4, 2022, were conducted pursuant to Regulation S of the Securities Act of 1933, as amended ("Regulation S"). The sale of shares was made only to non-U.S. persons (as defined under Rule 902 section (k)(2)(i) of Regulation S), pursuant to offshore transactions, and no directed selling efforts were made in the United States by the issuer, a distributor, any of their respective affiliates, or any person acting on behalf of any of the foregoing.

On February 6, 2023, we sold 10,033,445 shares of restricted Common Stock to Kazuya Iwasaki, a Japanese Citizen, at a price of $0.023 per share of Common Stock. The total subscription amount paid by Kazuya Iwasaki was approximately $230,769. Kazuya Iwasaki is not a related party to the Company.

On February 6, 2023, we sold 3,344,482 shares of restricted Common Stock to Shokafulin LLP, a Japanese Company, at a price of $0.023 per share of Common Stock. The total subscription amount paid by Shokafulin LLP was approximately $76,923. Shokafulin LLP is not a related party to the Company.

The proceeds from these sales went to the Company to be used as working capital.

The aforementioned sales of shares were conducted pursuant to Regulation S of the Securities Act of 1933, as amended ("Regulation S"). The sales of shares were made only to non-U.S. persons (as defined under Rule 902 section (k)(2)(i) of Regulation S), pursuant to offshore transactions, and no directed selling efforts were made in the United States by the issuer, a distributor, any of their respective affiliates, or any person acting on behalf of any of the foregoing.

- 7 -

Japanese Food-Service Market

The Japanese Food-Service Market is Segmented by Type (Full-service Restaurants, Quick Service Restaurants, Cafes, Bars, 100% Home Delivery Restaurants, Street Stalls and Kiosks) and Structure (Independent Consumer Food Service and Chained Consumer Food Service). We believe Japanese consumers, in general, tend to be highly demanding, putting great emphasis on quality and branding and are willing to spend more resources on value-added products. (1)

The Japanese food service market was valued at USD 142.84 billion in 2020, and it is projected to witness a CAGR of 0.84% during the forecast period, 2021 - 2026. The coronavirus pandemic has made short-term projections hard to predict, with sales in March 2020 down almost 40% for some food companies. Japanese food service operators, which rely on lunch and dinner demand from business workers, are also suffering as more companies have employees working from home at the government’s request. (1)

According to a report released by TableCheck Inc., the percentage of reservations (dining reservations) being canceled increased about 3.6 times before the pandemic for groups of 10 or more. A French restaurant and bar named Scene near Hachioji Station on the Keio Line, earlier in June 2020, launched take-out and delivery services which we believe many others will begin offering if not already, due in part to the changing attitudes of dining out as a result of the ongoing pandemic. We believe take-out and delivery services, along with menu options that are quick to prepare, increasing in consumer demand. (1)

The variety of restaurants and menu items available in the Japanese food service industry continues to expand in the country, as Japanese consumers are interested in trying a new and vast variety of cuisines, which are available at their convenience in Japan. Food from Europe, Asia, Australia, and the Americas are becoming increasingly popular, partly due to a large number of Japanese traveling abroad every year.

The Japanese food service market is highly competitive, with a major market share held by prominent companies, such as McDonald’s Corporation, Yum! Brands Inc., Zensho Holdings Co. Ltd, Skylark Group, MOS Food Services Inc., and Yoshinoya Holdings Co. Ltd. Zensho Holdings Co. Ltd, with the largest market share of 2.76% in 2020, emerging as the market leader, and Skylark Group holding the second-largest share with 1.66%. (1)

Currently, in the Japanese market, hamburgers and related fast-food options have been prevalent, with high-end gourmet hamburgers being in the most expensive category consisting usually of single restaurant locations, followed by lesser expensive hamburger options via chain restaurants such as Shake Shack and MOS Premiums. The size of the current market for hamburgers in Japan is approximately $6.6 Billion (2020), and has been steadily increasing ever since 2015. It is also projected to grow by approximately 5% over the next few years. Hamburgers are considered to be one of the few food categories that were not affected by COVID-19 in Japan and were able to take advantage of home deliveries and to-go orders during the pandemic. (Source: Fuji Keizai Group 2020.)

Source:

1.https://www.reportlinker.com/p06036755/Japan-Foodservice-Market-Growth-Trends-COVID-19-Impact-and-Forecasts.html?utm_source=GNW

- 8 -

Business Information

WB Burgers Japan Co., Ltd., referred to herein as “WBJ”, which we now operate through and share the same business plan of, holds the rights to the “Master Franchise Agreement” with Jakes’ Franchising LLC, a Delaware Limited Liability Company, as it pertains to the establishment and operation of Wayback Burger Restaurants within the country of Japan.

The Master Franchise Agreement provides WBJ the right to establish and operate Wayback Burgers restaurants in the country of Japan, and also license affiliated and unaffiliated third parties (“Franchisees”) to establish and operate Wayback Burgers restaurants in the Country of Japan, this agreement lasts for a term of twenty years, unless it is terminated sooner in accordance with terms outlined in the Master Franchise Agreement, and may be extended one additional, consecutive term of ten years. In exchange for such rights, we paid Jake’s Franchising $2,700,000 USD, and we must pay an additional $10,000 for each additional company operated Wayback Burgers restaurant and for each sub-franchised location the fee is either $10,000 or 28.57% of the initial franchise fee collected for such Restaurant, whichever is greater. Additionally, there is also a royalty fee in the amount of three percent (3%) of the Gross Sales of all Company-Operated Wayback Burgers Restaurants in the Country and the greater of two percent (2%) of the Gross Sales of all Franchised Wayback Burgers Restaurants in the Country or forty percent (40%) of the royalty fees collected for all Franchised Wayback Burgers Restaurants in the Country. The Master Franchise Agreement, amongst other things, also provides WBJ the right of first refusal to enter into a subsequent Master Franchise Agreement with Jake’s Franchising, LLC to establish and operate Wayback Burgers restaurants in the Countries of Indonesia, Malaysia (Eastern Malaysia only, Western Malaysia if it becomes available as it is currently licensed to another party), the Philippines, Vietnam, China, India, Korea, Thailand, Singapore, and Taiwan.

The Master Franchise Agreement dictates specific duties we must perform which include, but are not limited to, providing Jake’s Franchising with plans and specifications for restaurant locations, provide employees with Wayback Burgers mandated training, present Jake’s Franchising with copies of all potential advertising and promotional material, etc. Furthermore, we are required to open one Wayback Burgers restaurant by the end of the 2022 calendar year, three restaurants by the end of the 2023 calendar year, and an additional three restaurants must open, and remain in operation, every following year until December 31, 2041, at which time we must have sixty Wayback Burgers restaurants open and in operation. If we fail to meet these targets, then we would need to renegotiate terms with Jake’s Franchising, or we could potentially lose our master franchise rights in their entirety. For full terms and details of the Master Franchise Agreement, one can view a complete copy which has been filed as an exhibit to the Form 8-K filed with the Securities and Exchange Commission on September 16, 2021. The Master Franchise Agreement is included herein by reference, please refer to the exhibits.

WB Burgers Japan Co., Ltd. seeks to make “Wayback Burgers” a nationally recognized brand, if not a household name, within the country of Japan through the promotion and opening of various Wayback Burgers Restaurants.

Following the acquisition of our now wholly owned subsidiary, WB Burgers Japan Co., Ltd., on September 14, 2021, we ceased to be a shell company. Immediately upon our acquisition of WB Burgers Japan Co., Ltd. we adopted the same business plan as WB Burgers Japan Co., Ltd.

Background

The first Wayback Burgers, previously known as Jake’s Wayback Burgers, began with a single location in Newark, Delaware approximately thirty-one years ago in 1991, offering a combination of burgers, hot dogs, fries, milkshakes, and other similar menu options. Since then, it has reached a global scale with a presence in the US, Europe, Africa, and Asia with hundreds of corporate owned restaurants and over five hundred franchise locations worldwide offering much of the same comfort items many have grown accustomed to, with the addition of a few menu items specifically geared toward the pallets of those in various demographics.

The products we seek to offer in our anticipated location(s), and those we seek to franchise to within Japan, will also offer many of the same product offerings many are accustomed to elsewhere such as hamburgers, hot dogs chicken sandwiches, hand-dipped milkshakes, various side dishes, fresh salad, kid’s meals, refreshing drinks and alcoholic beverages. We intend to source our ingredients in any of our current or future location(s) from highly regarded local Japanese suppliers in order to satisfy the food quality standards as set by Wayback Burgers Inc., within the United States.

Our First Location

On November 9, 2021, our wholly owned subsidiary, WB Burgers Japan Co., Ltd., consummated a lease agreement with Arai Co., Ltd., a Japanese realty group, for the location in which we now operate our first Wayback Burgers restaurant. The property is located in the popular shopping plaza of Omotesando, located in the Tokyo prefecture, in the country of Japan. We believe the high volume of foot traffic and shopping will yield a large group of patrons seeking to try our product offerings.

On March 11, 2022 we opened our first flagship Wayback Burgers location to the public in the Omotesando shopping plaza in Japan. We offer an array of quick bites, including, but not limited to, traditional hamburgers, fries, shakes, and other alternatives.

Other Current Locations

In August of 2022, we, through our wholly owned subsidiary, WB Burgers Japan Co., Ltd., entered into and consummated a rental agreement with “Kitchen Depot” for a ghost kitchen in the Tamachi neighborhood of Minato, Tokyo, Japan. Kitchen Depot is an unrelated third party, and the rental agreement is for a period of two years, with the option to renew at the conclusion. From this location, as of August 27, 2022, the Company has begun to offer delivery of Wayback Burgers menu items, such as those offered at the Company’s physical “dine in” restaurant location in the Omotesando shopping plaza, located in Tokyo, Japan. This new location only offers a delivery option with no option to dine in.

At this time, orders can be placed exclusively through UberEats, although we have plans to expand the range of our delivery options in the future. Additionally, delivery is only available within a 2-3 kilometer radius of our Tamachi location. The Company believes that its new Wayback Burgers delivery-only location, with convenient online ordering, will serve to not only attract additional customers, but will also expand awareness of our menu items and Wayback Burgers as a whole.

Mobile Application

The Company has begun to develop its own mobile application for food delivery services. This application is in its early stages of development, and cannot, at this time, be discussed in greater detail as developments are ongoing. As mentioned previously, the Company is currently relying exclusively on Uber Eats for ordering and delivering as it relates to its new location in Tamachi.

- 9 -

Marketing Strategy

In order to grow an initial customer base, from which we intend to launch future expansion efforts, our marketing strategy begins with the physical location of our flagship restaurant. Our current location in Omotesando is in a shopping center with high foot-traffic that can serve to attract not only customers, but also future franchisee prospects throughout Japan. For future franchisee locations, we intend to identify areas where competitors are not already located, such as road-side in the outskirts of major cities, and open our restaurants in these areas.

However, we do not intend to rely solely on our physical location in order to attract customers, we also are in the development stages of a robust marketing stratagem comprised, in part, of SNS (social networking service) marketing through collaboration with influencers and celebrities, magazine advertisements, and expansive television and media appearances. The specifics of these marketing initiatives are in the planning stages and have not yet been determined in sufficient detail to disclose in their entirety.

Wayback Burgers in Japan intends to position itself as a newly entered and authentic American hamburger brand, comparable to our competitor Shack Shake, while contrasting ourselves through offering higher quality foods at competitive price points. We plan to achieve this by focusing on the ingredients, such as the option of vegetables in our hamburgers, the increased diameter of our meat patties, and the overall volume of our menu items. Additionally, we intend to offer original Japanese breakfast and dinner menu options, as well as forming a special collaboration focused on all-plant based alternative foods with Next Meats, Co., Ltd., a Japanese alternative meat company.

Expansion Plans

We have forecasted our expansion plans over the next few years, however, as we have just recently commenced operations, we may find that our plans may be materially altered, expanded, or curtailed as dictated by market forces at the time. As such, our expansion plans should be read as a framework for our future goals, but not a guarantee that we will carry out any or all such operations in the indicated timeline.

At present, our expansion plans, which we cannot state with certainty will be realized, are as follows:

- Over the course of 2023, we are aiming to open five Wayback Burgers restaurants throughout Japan, with one of these restaurants directly managed by us while the remaining four would ideally be franchise locations. This number may increase or decrease depending on the results of our operations.

- Additionally, during 2023, we intend to execute another master franchise agreement in Asia for the right to open Wayback Burgers restaurants in another Asian country or territory. We have not yet identified which country or territory we will seek to acquire these rights for first. As noted previously, we have the right of first refusal to enter into a subsequent Master Franchise Agreement with Jake’s Franchising, LLC to establish and operate Wayback Burgers restaurants in the Countries of Indonesia, Malaysia (Eastern Malaysia only, Western Malaysia if it becomes available as it is currently licensed to another party), the Philippines, Vietnam, China, India, Korea, Thailand, Singapore, and Taiwan.

- By the year 2024, we intend for there to be ten Wayback Burgers Franchise locations open throughout Japan. We also intend, during 2024, to execute two additional Master Franchise Agreements in Asia to establish and operate Wayback Burgers restaurant locations in additional Asian countries or territories.

Partnerships

The company believes partnerships are a vital means to expansion and that partnerships with other food institutions or distributors may allow the Company to provide menu items that might appeal to a larger demographic within the Japanese market.

Our current Officer and Director, Koichi Ishizuka has existing ties and relationships with Next Meats Co., Ltd. a Japanese plant based alternative meat company, that produces and sells plant-based foods (predominantly meat alternatives) to consumers. As a result of the collaboration with Next Meats Co., Ltd., at our flagship Wayback Burgers restaurant we have been able to add alternative meat options into its menu, and in the future we may create customized menu options as provided by Next Meats Co., Ltd. Menu alterations are subject to approval by Jake’s Franchising, LLC. It is the belief of management that such offerings can gain a larger market share in the country of Japan allowing for greater growth potential. However, such plans are speculative and may not materialize. It is also possible that if such plans do materialize, they may not result in the expected level of growth the Company forecasts as a result of the partnership or partnerships it enters into. Additionally, we may explore the possibility of entering into an agreement with Dr. Foods, Inc., a company in the “alternative meat” industry which has common management with the Company.

It should be noted that Koichi ishizuka has an equity interest in Next Meats Holdings, Inc., a Nevada Company. He also currently serves as Chief Executive Officer, Chief Financial Officer, and Director of Next Meats Holdings, Inc. Next Meats Co., Ltd. is a wholly owned subsidiary of Next Meats Holdings, Inc. Koichi Ishizuka is also the Sole Officer, Director, and controlling shareholder of Dr. Foods, Inc.

- 10 -

Government Regulations

The below does not extensively detail every single law and regulation to which the Company may be subject to, but rather provides an overview of the kind of food safety standards to which our restaurant(s) will be held.

The main law that governs food quality and integrity in Japan is the Food Sanitation Act ("FSA") and the law that comprehensively governs food labelling regulation is the Food Labelling Act.

The FSA regulates food quality and integrity by:

- Establishing standards and specifications for food, additives, apparatus, and food containers and packaging;

- Providing for inspection to see whether the established standards are met;

- Providing for hygiene management in the manufacture and sale of food; and

- Requiring food businesses to be licensed.

Under the FSA, additives and foods containing additives must not be sold, or be produced, imported, processed, used, stored, or displayed for marketing purposes unless the Minister of Health, Labour and Welfare ("MHLW") has declared them as having no risk to human health after seeking the views of the Pharmaceutical Affairs and Food Sanitation Council ("PAFSC"). In addition, it is not permissible to add any processing aids, vitamins, minerals, novel foods or nutritive substances to food unless they have been expressly declared by the MHLW as having no risk to human health.

The MHLW may establish specifications for methods of producing, processing, using, cooking, or preserving food or additives to be served to the public for marketing purposes ("Specifications"), or may establish standards for food ingredients or additives to be served to the public for marketing purposes ("Standards") pursuant to the FSA. Accordingly, where substances are allowed to be added to food, they may only be used within the limits expressly set by the Specifications and Standards.

In order to operate a restaurant in Japan, we were required to obtain, and have obtained, a restaurant business license from a local health center. The requirement to obtain this license is that we must have, and we currently do have, an employee to act as a director of food sanitation, and a fire protection manager. Additionally, we must pay consumption tax, corporate tax, social insurance for our employees, as well as welfare pension for our employees. We follow all related guidelines and the company directly pays all such fees in order to remain in compliance.

Employees

Currently, we, “WB Burgers Asia, Inc.”, have only one employee, our sole officer and Director Koichi Ishizuka, who is not compensated at present for his services. Our wholly subsidiary, WB Burgers Japan Co., Ltd. has three officers, Koichi Ishizuka, Chief Executive Officer, Mitsuru Anthony, Co-Chief Operating Officer, and Motoko Hirai, Co-Chief Operating Officer. The biographical information for Mr. Koichi Ishizuka is detailed herein on page 16 and the biographical information for Mr. Mitsuru Anthony and Mr. Motoki Hirai are directly below:

Mitsuru Anthony Ueno

Mitsuru Anthony Ueno, age 48, graduated from UCLA in 2000 with a BA in Italian and Special Fields. In 2010, he obtained his MAFED (Master in Fashion, Experience & Design) from SDA Bocconi School of Management in Milan, Italy. Mr. Ueno is an international marketing, branding and cross border business management specialist and has nearly 20 years of foreign study and working experience. In 2017, Mr. Ueno founded, and remains the owner of, Artigiappone, a Japanese Company offering a handmade bespoke suit brand. Also in 2017, he became an Executive Producer at Photozou Co., Ltd. (Japan), a Company operating an online photo sharing website. In 2019, he became Chief Executive Officer of Forcellon Holding, Inc. Pte. Ltd., a Singapore Company providing international business management and consulting services.

Mitoki Hirai

Mitoki Hirai, age 40, became the Chief Executive Officer of Three Ways Co, Ltd., a company specialized in the production and sale of electric fans, in 2015. In 2017 he opened Yakiniku Mistuboshi, a barbecue restaurant in Nagoya City, and also began to work as a restaurant consultant. In 2019, he opened Tonto, a pork dish restaurant in Nagoya City. In 2020, he became the Chief Executive Officer of Tosapo Co., Ltd. In 2021, Mr. Hirai acquired the Empire Stake House restaurant in Roppongi and he also opened Yakiniku Fujisan, a barbecue restaurant in Ama city.

Aside from the three officers of WB Burgers Japan Co., Ltd., the Company has also hired twenty seven salaried staff members. Two employees are full time, and twenty five employees are part time.

Item 1A. Risk Factors.

As a smaller reporting company, as defined in Rule 12b-2 of the Exchange Act, we are not required to provide the information called for by this Item.

Item 1B. Unresolved Staff Comments.

None.

Item 2. Properties.

At present, we do not own any properties. However, we do lease our two restaurant locations.

Our first location is currently leased from Arai Co., Ltd., a Japanese realty group,

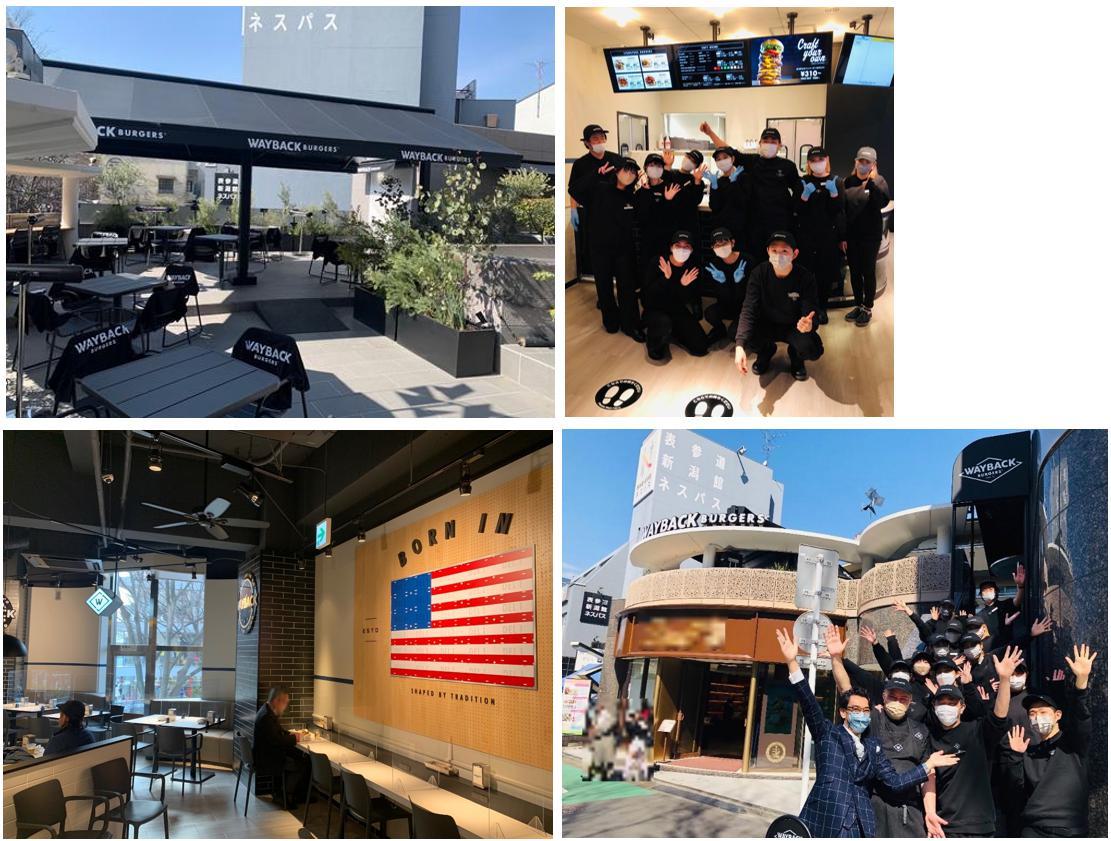

Details of the Leased Property: The property is located at 6-19-20 No.15 Arai Bldg Jingumae Shibuya-Ku, Tokyo, Japan, which is in a popular shopping location that is only a minute walk from the Omotesando Station. The deposit is 35,000,000 JPY ($304,000) and the monthly rent is 3,850,000 JPY (including tax) ($33,475). The term of the lease extends from November 9, 2021 to January 8, 2024, and has the option to be extended indefinitely for additional two-year periods. The interior space is 157.82 ㎡ (1698.760 square ft), and the terrace space is 145.06 ㎡ (1561.413 square ft), which accounts for a total usable space of 302.88 ㎡ (3260.173 square ft).

Below are a few photographs of this physical restaurant location. Logos and branding of neighboring businesses have been blurred out in the image below.

In August of 2022, we, through our wholly owned subsidiary, WB Burgers Japan Co., Ltd., entered into and consummated a rental agreement with “Kitchen Depot” for a ghost kitchen in the Tamachi neighborhood of Minato, Tokyo, Japan. We consider this our second location. Kitchen Depot is an unrelated third party, and the rental agreement is for a period of two years, with the option to renew at the conclusion. Pursuant to our agreement with Kitchen Depot, we are to pay Kitchen Depot approximately 187,000 JPY per month, or approximately $1,316. The floor space of this location is approximately 5.92 ㎡ (63.5 square feet).

From this location, as of August 27, 2022, the Company has begun to offer delivery of Wayback Burgers menu items, such as those offered at the Company’s physical “dine in” restaurant location in the Omotesando shopping plaza, located in Tokyo, Japan. This new location only offers a delivery option with no option to dine in.

The address of the Tamachi location is 5-23-16 Shiba, Minato-ku, Tokyo 2F depo3, Japan.

In addition to our two restaurant locations, we also utilize office space provided by our sole officer and director, Koichi Ishizuka, at no cost. This office space is located at 3F K’s Minamiaoyama 6-6-20 Minamiaoyama, Minato-ku,Tokyo, Japan 107-0062. Management estimates such amounts to be immaterial.

Item 3. Legal Proceedings.

From time to time, we may become party to litigation or other legal proceedings that we consider to be a part of the ordinary course of our business. We are not currently involved in legal proceedings that could reasonably be expected to have a material adverse effect on our business, prospects, financial condition or results of operations. We may become involved in material legal proceedings in the future.

Item 4. Mine Safety Disclosures.

Not applicable.

- 11 -

PART II

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

Market Information

Our common stock was quoted on the over-the-counter market (the “OTC Markets”) in the Pink Open® Market (the “Pink Market”) under the symbol “WBBA”. Given our delinquent SEC Reporting status, we have recently been demoted by the OTC Markets to the “Expert Market” tier under the same symbol.

Quotations in Expert Market securities are restricted from public viewing. We anticipate that we will resume trading on the Pink Open® Market when we are current in our SEC reporting obligations once again. Currently, we are delinquent in filing our Form 10-Q for the quarterly period ended October 31, 2022, and January 31, 2023. We intend to file these reports subsequent to the filing of this Form 10-K, however we cannot state with any level of specificity exactly when each delinquent report will be filed as we remain active in preparing each report.

There is currently a limited trading market in the Company’s shares of common stock. Generally speaking, our shares of common stock are, and have been thinly traded, meaning our shares cannot be easily purchased or sold and have a low volume of shares trading per day which can lead to volatile changes in price per share.

Over-the-counter market quotations reflect inter-dealer prices, without retail mark-up, mark-down or commission and may not necessarily represent actual transactions.

| Quarter Ended | High Bid | Low Bid |

| April 30, 2023 | $0.034 | $0.0002 |

| January 31, 2023 | $0.0445 | $0.01 |

| October 31, 2022 | $0.0472 | $0.0169 |

| July 31, 2022 | $0.0672 | $0.0185 |

| April 30, 2022 | $0.247 | $0.021 |

| January, 31, 2022 | $0.3455 | $0.1101 |

| October 31, 2021 | $0.46 | $0.162 |

| July 31, 2021 | $0.799 | $0.18 |

| April 30, 2021 1 | $0.475 | $0.20 |

1 We were a party to a corporate reorganization, legally effective as of March 31, 2021. Information regarding this reorganization is detailed herein on page 2 and elsewhere herein. Prior to this reorganization, we have no information to report pursuant to the above table. The quarter ending April 30, 2021, only includes data stemming back to March 31, 2021.

Holders

As of June 2, 2023, we have 1,070,718,679 shares of common stock, $0.0001 par value, issued and outstanding and 1,000,000 shares of Series A preferred stock, $0.0001 par value, issued and outstanding. Every one share of Series A Preferred Stock has voting rights equal to 1,000 shares of Common Stock.

As of June 2, 2023, we also have approximately 224 shareholders of record. This is inclusive of Cede and Co., which is deemed to be one shareholder of record. For further clarification, Cede & Co. is currently defined by the “NASDAQ”, as “a Nominee name for The Depository Trust Company, a large clearing house that holds shares in its name for banks, brokers and institutions in order to expedite the sale and transfer of stock.”

Dividends

We have not paid any cash dividends to date and do not anticipate or contemplate paying dividends in the foreseeable future. It is the present intention of our management to utilize all available funds for the development of our business.

Issuer Purchases of Equity Securities

None.

Equity Compensation Plan Information

Not applicable.

Recent Sales of Unregistered Securities; Uses of Proceeds from Registered Securities

On or about about July 1, 2021, we sold 9,090,909 shares of restricted common stock to SJ Capital Co., Ltd., a Japanese Company, at a price of $0.20 per share of common stock. The total subscription amount paid by SJ Capital Co., Ltd. was approximately $1,818,181.80 or approximately 200,000,000 Japanese Yen.

SJ Capital Co., Ltd., is owned and controlled by Senju Pharmaceutical Co., Ltd., a Japanese Company.

Mr. Takeshi Sugisawa, the President of SJ Capital Co., Ltd., authorized the above transaction on behalf of SJ Capital Co., Ltd. Both SJ Capital Co., Ltd., and Senju Pharmaceutical Co., Ltd. are considered non-related parties to the Company. The proceeds from the above sale of shares went to the Company to be used for working capital.

On August 24, 2021, we sold 1,363,636 shares of restricted common stock to Yasuhiko Miyazaki, a Japanese Citizen, at a price of $0.20 per share of common stock. The total subscription amount paid by Yasuhiko Miyazaki was approximately $272,727 or approximately 30,000,000 Japanese Yen. Mr. Yasuhiko Miyazaki is not a related party to the Company. The proceeds from the above sale of shares went to the Company to be used for working capital.

On September 14, 2021, we entered into an “Acquisition Agreement” with White Knight Co., Ltd., a Japan Company, whereas we issued 500,000,000 shares of restricted common stock to White Knight Co., Ltd., in exchange for 100% of the equity interests of WB Burgers Japan Co., Ltd., a Japan Company. Following this transaction, WB Burgers Japan Co., Ltd. became our wholly owned subsidiary which we now operate through.

The aforementioned Acquisition Agreement is attached as Exhibit 10.1 to our Form 8-K filed with the Securities and Exchange Commission on September 14, 2021. All references to the Acquisition Agreement are qualified, in their entirety, by the text of such exhibit. White Knight Co., Ltd., is owned entirely by our sole officer and Director, Koichi Ishizuka. White Knight Co., Ltd. is our largest controlling shareholder.

On October 22, 2021, we sold 2,252,252 shares of restricted common stock to Shokafulin LLP, a Japan Company, which is controlled by Takuya Watanabe, a Japanese Citizen, at a price of $0.20 per share of common stock. The total subscription amount paid by Shokafulin LLP was approximately $450,450 or approximately 50,000,000 Japanese Yen. Shokafulin LLP and Mr. Watanabe are not related parties to the Company. The proceeds from the above sale of shares went to the Company to be used for working capital.

- 12 -

On December 27, 2021, we sold 1,315,789 shares of restricted Common Stock to Takahiro Fujiwara, Japanese Citizen, at a price of $0.20 per share of Common Stock. The total subscription amount paid by Takahiro Fujiwara was approximately $263,158. Takahiro Fujiwara is not a related party to the Company. The proceeds from the above sale of shares went to the Company to be used for working capital.

On August 8, 2022, we sold 1,586,538 shares of restricted Common Stock to Takahiro Fujiwara, a Japanese Citizen, at a price of $0.032 per share of Common Stock. The total subscription amount paid by Takahiro Fujiwara was approximately $50,769. Takahiro Fujiwara is not a related party to the Company.

On August 8, 2022, we sold 2,403,846 shares of restricted Common Stock to Shokafulin LLP, a Japanese Company, at a price of $0.032 per share of Common Stock. The total subscription amount paid by Shokafulin LLP was approximately $76,923. Shokafulin LLP is not a related party to the Company.

On August 12, 2022, we sold 32,065,458 shares of restricted Common Stock to Asset Acceleration Axis, LLC, a Japanese Company, at a price of $0.032 per share of Common Stock. The total subscription amount paid by Asset Acceleration Axis, LLC was approximately $1,026,094. Asset Acceleration Axis, LLC is not a related party to the Company.

The Company intends to use the proceeds from the aforementioned sales of shares for working capital.

On September 13, 2022, we sold 7,262,324 shares of restricted Common Stock to Asset Acceleration Axis, LLC, a Japanese Company, at a price of $0.032 per share of Common Stock. The total subscription amount paid by Asset Acceleration Axis, LLC was approximately $232,395. Asset Acceleration Axis, LLC is not a related party to the Company.

The Company intends to use the proceeds from the aforementioned sales of shares for working capital.

On February 6, 2023, we sold 10,033,445 shares of restricted Common Stock to Kazuya Iwasaki, a Japanese Citizen, at a price of $0.023 per share of Common Stock. The total subscription amount paid by Kazuya Iwasaki was approximately $230,769. Kazuya Iwasaki is not a related party to the Company.

On February 6, 2023, we sold 3,344,482 shares of restricted Common Stock to Shokafulin LLP, a Japanese Company, at a price of $0.023 per share of Common Stock. The total subscription amount paid by Shokafulin LLP was approximately $76,923. Shokafulin LLP is not a related party to the Company.

The proceeds from these sales went to the Company to be used as working capital.

In regards to all of the above transactions, the Company claims an exemption from registration afforded by Section Regulation S of the Securities Act of 1933, as amended ("Regulation S") for the above sales/issuances of the stock since the sales/issuances of the stock were made to non-U.S. persons (as defined under Rule 902 section (k)(2)(i) of Regulation S), pursuant to offshore transactions, and no directed selling efforts were made in the United States by the issuer, a distributor, any of their respective affiliates, or any person acting on behalf of any of the foregoing.

- 13 -

Item 6. Selected Financial Data.

Not applicable because the Company is a smaller reporting company.

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

Management’s Discussion and Analysis of Financial Condition and Results of Operations is designed to provide a reader of the financial statements with a narrative report on our financial condition, results of operations, and liquidity. This discussion and analysis should be read in conjunction with the audited Financial Statements and notes thereto for the year ended July 31, 2022 and 2021, included under Item 8 “Financial Statements and Supplementary Data” in this Report. The following discussion contains forward-looking statements that involve risks and uncertainties, such as statements of our plans, objectives, expectations, and intentions. Our actual results could differ materially from those discussed in the forward-looking statements. Please also see the cautionary language at the beginning of this Report regarding forward-looking statements.

Restatement of Previously Issued Consolidated Financial Statements

We have restated herein our audited consolidated financial statements at July 31, 2021 for the fiscal year ended July 31, 2021. We have also restated impacted amounts within the accompanying footnotes to the consolidated financial statements.

Restatement Background

In August of 2022, the sole director of WB Burgers Asia, Inc.(the “Company”) was advised by M&K CPAs PLLC (“M&K”), its registered independent public accounting firm, that the Company’s previously issued financial statements included in its Annual Reports on Form 10-K for the year ended July 31, 2021, should be restated to correct historical errors related to the recognition of cash received for the sale of shares, the calculation of the fair market value of shares issued, and classifications due to the recapitalization of the Company. The restated financials also show the differences between this current Form 10-K and the previously filed report due to the consolidation of financial reporting to include all activity of the Company’s wholly owned subsidiary, WB Burgers, Japan Co., Ltd (“WBBJ”). WBBJ became a wholly owned subsidiary of the Company in September of 2021, after the preparation of the previous Form 10-K for the year ended July 31, 2021. As a result, we determined that we would restate such financial statements to correct the accounting errors and also highlight the restatement differences resulting from the financial consolidation of the Company and its subsidiary.

Description of misstatements

(1) Recognition of cash received for the sale of shares and recording of the related issuance of shares

We recorded adjustments for cash received for the sale of common shares that was incorrectly recognized. On July 1, 2021, cash for the purchase of 9,090,909 shares of common stock was received by related party, White Knight Co., Ltd. and was not held by the Company, via its subsidiary, until September 2021. Additionally, these shares were not issued to the purchaser on July 1, 2021 as previously reported but were issued after the fiscal year end, in October 2021.

(2) Recognition of financial activity of wholly owned subsidiary

We recorded adjustments made to the financial statements due to the consolidation of financial information with our wholly owned subsidiary.

(3) Adjustment to the fair market value of shares issued as compensation

We recorded an adjustment to the value of 1,000,000 shares of Series A preferred shares issued as compensation due to the adoption of a third party evaluation of those shares, which differed from our previous valuation.

(4) Retroactive restatements of shares cancelled and returned and shares exchanged in merger and reorganization

We recorded adjustments to the statement of owners’ equity to account for the revision, by the Company’s transfer agent, of the dates of shares cancelled and returned, and also shares exchanged pursuant to a reorganization. These retroactive date changes were due to the recapitalization of the Company pursuant to its reorganization, legally effective March 31, 2021 and when control of the Company passed from our previous controlling shareholder to our current controlling shareholder, who is our CEO and sole director, Koichi Ishizuka.

(5) Reclassification of additional paid-in capital

We reclassed the amount of expenses paid on behalf of the Company on the Statement of Cash Flows to properly report those payments as cash provided by operating activities rather than cash provided by financing activities.

Cash and Cash Equivalents

As of July 31, 2022, and 2021, we had cash and cash equivalents in the amount of $126,669 and $30,021, respectively. The variance in our cash balance from July 31, 2021 to July 31, 2022 is the result of the Company having increased operations, namely our primary dine in and dine out restaurant location in the Omotesando Shopping Plaza, located in Tokyo, Japan. It should be noted that as of July 31, 2022 we had only one restaurant location fully operational. Our second location, our ghost kitchen that provides delivery only, was opened August of 2022.

Assets

Our total assets for July 31, 2022 and July 31, 2021 were $3,760,615 and $2,688,692 respectively. For both periods, our total assets were predominantly from the franchise rights we have acquired from Jakes’ Franchising LLC, a Delaware Limited Liability Company, to operate Wayback Burgers’ Franchise locations.

The Master Franchise Agreement provides our wholly owned subsidiary WB Burgers Japan Co., Ltd., “WBJ”, the right to establish and operate Wayback Burgers restaurants in the country of Japan, and also license affiliated and unaffiliated third parties (“Franchisees”) to establish and operate Wayback Burgers restaurants in the Country of Japan. The Master Franchise Agreement, amongst other things, also provides WBJ the right of first refusal to enter into a subsequent Master Franchise Agreement with Jake’s Franchising, LLC to establish and operate Wayback Burgers restaurants in the Countries of Indonesia, Malaysia (Eastern Malaysia only, Western Malaysia if it becomes available as it is currently licensed to another party), the Philippines, Vietnam, China, India, Korea, Thailand, Singapore, and Taiwan.

From July 31, 2021 to July 31, 2022 our total assets have increased in part due to equipment acquired, inventories acquired, accounts receivable, right of use asset(s), and deposits.

Revenues

For the year ended July 31, 2022, and 2021, we generated revenues of $180,821 and $0 respectively. The variance in revenue year over year is due to the fact that we began generating revenue from our restaurant location in the Omotesando Shopping Plaza, Tokyo Japan. Our cost of revenue was $716,083 for the year ended July 31, 2022 and $0 for the year ended July 31, 2021. The variance, is attributable to the fact that we did not operate a restaurant location in our 2021 fiscal year. Our cost of revenue exceed our cost of revenues for our fiscal year ended July 31, 2022. We believe our gross loss of $535,262 to be attributable, primarily to what we believe to be initial start up costs. In order to remediate our gross loss we believe we will need to increase our revenue. We do not believe that our cost of revenues will proportionally increase with our revenues, and thus, we believe generating more revenue will alleviate our losses we have experienced for the year ended July 31, 2022.

Net Loss

Our general and administrative expenses were $733,744 for the year ended July 31, 2022 and $49,598 for the year ended July 31, 2021. Our Net loss for the year ended July 31, 2022 was $1,567,583 and $196,079. For July 31, 2022, we believe most of these general and administrative expenses were due to initial startup costs incurred, including but not limited to professional fees, franchise rights amortization, and advertising costs. As mentioned above, we believe that in order to remedy our net loss we will require additional revenue. We are currently exploring a means in which to gain more foot traffic into our dine in location. It is the company’s belief that the COVID-19 pandemic has largely contributed to our inability to experience more revenue for the year ended July 31, 2022. It is our believe that easing COVID-19 restrictions in Japan will have a positive impact upon our financial performance moving forward, however we cannot state with any level of specificity what this impact will be given we have not operated prior to the COVID-19 pandemic to compare our results to.

Additional Paid-In Capital

During the period ended July 31, 2022, White Knight forgave a loan to the Company of approximately $2,317,272, which is recorded as additional paid-in capital.

The Company’s sole officer and director, Koichi Ishizuka, paid expenses on behalf of the Company totaling $55,030 during the period ended July 31, 2022. These payments are considered contributions to the company with no expectation of repayment and are posted as additional paid-in capital.

The Company’s sole officer and director, Koichi Ishizuka, paid expenses on behalf of the Company totaling $6,400 during the year ended July 31, 2021. The Company’s former sole officer and director, Paul Moody, paid expenses on behalf of the company totaling $4,013 during the year ended July 31, 2021. Former related party, Jeffrey DeNunzio, paid expenses on behalf of the company totaling $6,500 during the period ended July 31, 2021.

The $16,913 in total payments are considered contributions to the company with no expectation of repayment and are posted as additional paid-in capital.

During the year ended July 31, 2022, the Company recognized the capital value of its wholly owned subsidiary, Store Foods, as additional paid-in capital in the amount of $8,673.

During the year ended July 31, 2021, the Company recognized the capital value of its wholly owned subsidiary, WB Burgers Japan, as additional paid-in capital in the amount of $91,980.

During the year ended July 31, 2021, the Company issued 1,000,000 shares of preferred stock after a merger and reorganization, which resulted in approximately $53,008 of additional paid-in capital (see Note 11).

At July 31, 2021, the Company recognized $24,399 of imputed interest related to the above payments which was recorded as additional paid-in capital.

Item 7A. Quantitative and Qualitative Disclosures about Market Risk.

We qualify as a smaller reporting company, as defined by Item 10 of Regulation S-K and, thus, are not required to provide the information required by this Item.

- 14 -

Item 8. Financial Statements and Supplementary Data.

Index to Financial Statements - WB Burgers Asia, Inc.

(Audited)

| Page | ||

| Report