Exhibit 99.1

EXCERPTS FROM PROSPECTUS DATED SEPTEMBER 11, 2020

EXPLANATORY NOTE

Except as otherwise indicated, this Exhibit 99.1 speaks as of September 11, 2020, does not reflect events that may have occurred subsequent to such date, and should be read in conjunction with the Company’s other filings with the Securities and Exchange Commission.

Set forth below are certain defined terms used in this Exhibit 99.1:

| · | “BRELF III” refers to BRELF III, LLC, a Washington limited liability company. | |

| · | “Broadmark Realty,” “Broadmark,” “Company,” “we,” “us” and “our” refer to Broadmark Realty Capital Inc., a Maryland corporation, together with its consolidated subsidiaries following the Business Combination and refer to the Predecessor Company Group for periods prior to the Business Combination. | |

| · | “Business Combination” refers to that certain business combination contemplated by that certain Agreement and Plan of Merger dated as of August 9, 2019, by and among Trinity Merger Corp., certain wholly owned subsidiaries thereof and the Predecessor Company Group. | |

| · | “Commission” refers to the Securities and Exchange Commission. | |

| · | “Company Private Placement Warrants” refers to warrants to purchase one share of our common stock at an exercise price of $11.50 per share. | |

| · | “Farallon Entities” refers to Farallon Capital Partners, L.P., Farallon Capital Institutional Partners, L.P., Farallon Capital Institutional Partners II, L.P., Farallon Capital Institutional Partners III, L.P., Four Crossings Institutional Partners V, L.P., and Farallon Capital (AM) Investors, L.P., each an entity affiliated with Farallon Capital Management, L.L.C., and with each of which Broadmark Realty previously entered into a subscription agreement relating to the PIPE Investment. | |

| · | “PIPE Investment” refers to those certain subscription agreements by and between Broadmark Realty and each of the Farallon Entities, whereby Broadmark Realty issued and sold to such investors an aggregate of 7,174,613 shares of common stock immediately prior to the consummation of the mergers that were part of the Business Combination at a price per share equal to the Reference Price, for an aggregate purchase price of approximately $75.0 million. | |

| · | “Predecessor Companies” refers to PBRELF I, LLC, a Washington limited liability company, BRELF II, LLC, a Washington limited liability company, BRELF III, LLC, a Washington limited liability company and BRELF IV, a Washington limited liability company. | |

| · | “Predecessor Company Group” refers to the Predecessor Management Companies and the Predecessor Companies. | |

| · | “Predecessor Management Companies” refers to Pyatt Broadmark Management, LLC, a Washington limited liability company, Broadmark Real Estate Management II, LLC, a Washington limited liability company, Broadmark Real Estate Management III, LLC, a Washington limited liability company and Broadmark Real Estate Management IV, LLC, a Washington limited liability company. | |

| · | “Private REIT” refers to Broadmark Private REIT, LLC, a real estate finance company sponsored by us and organized as a limited liability company under the laws of Delaware. | |

| · | “Private REIT Manager” refers to Broadmark Private REIT Management, LLC, a Delaware limited liability company, which is the manager of the Private REIT and an indirect subsidiary of Broadmark Realty. |

| 1 |

| · | “Public Warrants” refers to warrants to purchase one fourth (1/4th) of one share of our common stock at an exercise price of $2.875 per share. | |

| · | “REIT” refers to a real estate investment trust as such term is defined in the Internal Revenue Code of 1986, as amended. | |

| · | “Reference Price” refers to $10.45, which was the value of the funds held by Trinity Merger Corp. in the account established for the benefit of its stockholders, net of certain taxes and determined as of the close of business on the business day immediately preceding the date of closing of the Business Combination, divided by the outstanding number of shares of Trinity Class A Common Stock that were then outstanding. | |

| · | “Trinity” refers to Trinity Merger Corp., a Delaware corporation. | |

| · | “Trinity Investments” refers to Trinity Real Estate Investments LLC. | |

| · | “Trinity Sponsor” refers to HN Investors LLC, the sponsor of Trinity. | |

| · | “Warrants” refers to warrants to purchase our common stock and includes both the Company Private Placement Warrants and the Public Warrants. |

| 2 |

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This prospectus contains “forward-looking statements” within the meaning of Section 27A of the Securities Act and Section 21E of the Exchange Act. All statements other than statements of historical fact contained in this prospectus, including statements regarding our future results of operations and financial position, strategy and plans, and our expectations of future operations, are forward-looking statements. Forward-looking statements reflect the Company’s current views with respect to, among other things, capital resources, portfolio performance and projected results of operations. Likewise, the Company’s statements regarding anticipated growth in its operations, anticipated market conditions, demographics and results of operations are forward-looking statements. In some cases, you can identify these forward-looking statements by the use of terminology such as “outlook,” “believes,” “expects,” “projects,” “potential,” “continues,” “may,” “will,” “should,” “could,” “seeks,” “approximately,” “predicts,” “intends,” “plans,” “estimates,” “anticipates” or the negative version of these words or other comparable words or phrases.

The forward-looking statements contained in this prospectus are based on the Company’s current expectations and beliefs concerning future developments and their potential effects on the Company. There can be no assurance that future developments affecting the Company will be those that it has anticipated. Actual results may differ materially from those in the forward-looking statements. Some factors that could cause the Company’s actual results to differ include, but are not limited to:

| · | disruptions in our business operations, including construction lending activity, relating to COVID-19; |

| · | adverse impact of COVID-19 on the value of our goodwill established in the Business Combination; |

| · | the magnitude, duration and severity of the COVID-19 pandemic; |

| · | the impact of actions taken by governments, businesses, and individuals in response to the COVID-19 pandemic; |

| · | the current and future health and stability of the economy and residential housing market, including any extended slowdown in the real estate markets as a result of COVID-19; |

| · | changes in laws or regulations applicable to our business, employees, lending activities, including current and future laws, regulations and orders that limit our ability to operate in light of COVID-19; |

| · | defaults by borrowers in paying debt service on outstanding indebtedness; |

| · | impairment in the value of real estate property securing our loans; |

| · | availability of origination and acquisition opportunities acceptable to us; |

| · | potential mismatches in the timing of asset repayments and the maturity of the associated financing agreements; |

| · | general economic uncertainty and the effect of general economic conditions on the real estate and real estate capital markets in particular; |

| · | general and local commercial and residential real estate property conditions; |

| · | changes in federal government policies; |

| · | changes in federal, state and local governmental laws and regulations that impact our business, assets or classification as a real estate investment trust; |

| 3 |

| · | increased competition from entities engaged in construction lending activities; |

| · | changes in interest rates; |

| · | the availability of, and costs associated with, sources of liquidity; |

| · | the ability to manage future growth; |

| · | changes in personnel and availability of qualified personnel; and |

| · | other risks and uncertainties set forth in this prospectus. |

Should one or more of these risks or uncertainties materialize, or should any of the assumptions prove incorrect, actual results may vary in material respects from those projected in these forward-looking statements. The Company undertakes no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws.

| 4 |

BUSINESS

Overview

We are an internally managed commercial real estate finance company that provides secured financing to real estate investors and developers. We intend to elect to be treated as a real estate investment trust for U.S. federal income tax purposes commencing with our taxable year ending December 31, 2019. Based in Seattle, Washington, we specialize in underwriting, funding, servicing and managing a portfolio of short-term, first deed of trust loans to fund the construction and development of, or investment in, residential or commercial properties. Historically, our portfolio of loans has primarily consisted of loans to fund the construction and development of residential properties, but we also make loans on commercial real estate projects. Our objective is to preserve and protect stockholder capital while producing attractive risk-adjusted returns primarily through dividends generated from current income from our loan portfolio. We believe our ability to quickly offer and finalize loan terms and expeditiously fund ongoing construction draws provides us a competitive advantage over traditional funding sources as well as alternative lenders that may involve higher execution risk. We apply a disciplined underwriting approach to our loans, rooted in management’s deep understanding of real estate markets, property construction budgets and timelines and assessing borrower financial strength. We operate in select states that we believe have favorable demographic trends and provide us the ability to efficiently access the underlying collateral in the event of borrower default. As of June 30, 2020, our portfolio of active loans had approximately $1.1 billion of total commitments outstanding across borrowers in eleven states and the District of Columbia, of which approximately $832.3 million was funded by us and $6.9 million by the Private REIT. We refer to loans that have outstanding commitments or principal balances that have not been repaid or retired, including by foreclosure, as “active loans.” Total commitments refers to the aggregate sum of outstanding principal balances, construction holdbacks and committed amounts for future draws and interest reserves on our loans.

Business Combination

On November 14, 2019, we consummated the Business Combination combining the Predecessor Company Group and Trinity. Prior to the Business Combination, Trinity was a special purpose acquisition company listed on the Nasdaq Global Market that was formed for the purpose of effecting a merger, capital stock exchange, asset acquisition, stock purchase, reorganization or similar business combination with one or more businesses. As a result of the Business Combination, our shares of common stock were listed on the New York Stock Exchange on November 15, 2019.

Our Business and Loan Portfolio

Historically, we have funded the growth of our real estate loan portfolio with private capital and have not used debt or leverage to finance our loans. We had no debt outstanding as of December 31, 2019 or June 30, 2020. Going forward, we intend to fund our growth through the issuance of common stock, potential use of cash management tools such as a credit facility and the sale of participation interests in loans we originate to the Private REIT.

Properties securing our loans are generally classified as residential properties, commercial properties or undeveloped land, and are typically not income producing. Each loan is secured by a first deed of trust lien on real estate. Our lending policy limits the committed amount of each loan to a maximum loan-to-value (“LTV”) ratio of up to 65% of the “as-complete” appraised value of the underlying collateral as determined by an independent appraiser at the time of the loan origination. Our lending policy also limits the initial outstanding principal balance of each loan to a maximum LTV of up to 65% of the “as-is” appraised value of the underlying collateral as determined by an independent appraiser at the time of the loan origination. At the time of origination, the difference between the initial outstanding principal and the total commitment is the amount held back for future release subject to property inspections, progress reports and other conditions in accordance with the loan documents. Unless otherwise indicated, LTV is measured by the total commitment amount of the loan at origination divided by the “as-complete” appraisal. LTVs do not reflect interim activity such as construction draws or interest payments capitalized to loans, or partial repayments of the loan. As of June 30, 2020, the weighted average LTV across our active loan portfolio based on “as-complete” appraisals was 59.9%. In addition, each loan is also personally guaranteed on a recourse basis by the principals of the borrower and/or others, at our discretion, to provide further credit support for the loan. The guarantee may be collaterally secured by a pledge of the guarantor’s interest in the borrower or other real estate or assets owned by the guarantor.

| 5 |

Our loans typically range from $0.1 to $35 million in total commitment at origination, generally bear interest at a fixed annual rate of 10% to 13% and have initial terms typically ranging from five to eighteen months in duration, which we often elect to extend for several months based on our evaluation of the project. As of June 30, 2020, the average total commitment of our active loans was $5.2 million and the weighted average remaining term to maturity of our outstanding loans was approximately seven months. We usually receive loan origination fees, or “points,” typically ranging from 4% to 5% of the total commitment at origination, along with loan extension fees, each of which varies in amount based upon the term of the loan and the quality of the borrower and the underlying collateral. In addition to loan origination fees, we receive late fees paid by borrowers and/or are reimbursed by borrowers for costs associated with services provided by us, such as closing costs, collection costs on defaulted loans and construction draw inspection fees.

Our typical borrowers include real estate investors, developers and other commercial borrowers. We do not lend to owner-occupants of residential real estate. Loan proceeds are generally used to fund the vertical construction, horizontal development, investment, land acquisition and refinancing of residential properties and to a lesser extent commercial properties. We also make loans to fund the renovation and rehabilitation of residential and commercial properties. Our loans are generally structured with partial funding at closing and additional loan installments disbursed to the borrower upon satisfactory completion of previously agreed stages of construction.

A principal source of new transactions has been repeat business from our customers and their referral of new business. We also receive leads for new business from real estate brokers and mortgage brokers, a limited amount of advertising and through our website.

We seek to minimize risk of loss through our disciplined underwriting standards. We originate and fund loans secured by first deed of trust liens on residential and commercial real estate located in states that we believe have favorable demographic trends and that provide more efficient and quicker access to collateral in the event of borrower default. We also manage and service our loan portfolio. We believe that the demand/supply imbalance for residential construction-related real estate loans presents significant opportunities for us to selectively originate high-quality first deed of trust loans on attractive terms.

We built our business on a deep knowledge of the residential and commercial real estate market combined with a risk management approach that is designed to protect and preserve capital. We believe our flexibility and ability to structure loans that address the needs of our borrowers without compromising our standards on risk, our expertise in the loan market and our focus on newly originated first deed of trust loans have been the basis for our success.

Markets

At June 30, 2020, we operated in 14 states and the District of Columbia, and our loan portfolio was spread across eleven states and the District of Columbia, with the majority of loans located in Washington, Utah, Colorado, Texas, Oregon and Idaho. We strategically focus on these states as they have exhibited strong population growth. At June 30, 2020, more than 90% of our portfolio was secured by properties located in states ranked in top ten for net population migration between 2010 and 2019 according to the Census Bureau, including Washington, Utah, Colorado, Texas and Idaho. Additionally, each of Washington, Colorado, Utah and Texas are non-judicial foreclosure states, which we believe encourages borrowers to comply with the loan terms and provides us the option to take control of the collateral more quickly in the event of borrower default. We continue to increase our national presence, and in this regard, began operating in the Southeast region in 2018 and the Mid-Atlantic region in 2019.

Industry and Market Opportunity

Real estate investment is a capital-intensive business that typically relies heavily on debt capital to acquire, develop, improve, construct, renovate and maintain properties. We focus on providing construction, development and investment loans for the U.S. housing and real estate industries. Due to structural changes in banking, regulation and monetary policies over the last decade, there has been a reduction in the number of lenders servicing this segment. We believe there is a significant market opportunity to originate real estate loans secured by the underlying real estate as collateral. Our management team further believes that the demand for relatively small real estate loans to construct, develop or invest in residential or, to a lesser extent commercial real estate, located in states with favorable demographic trends presents a compelling opportunity to generate attractive risk-adjusted returns.

| 6 |

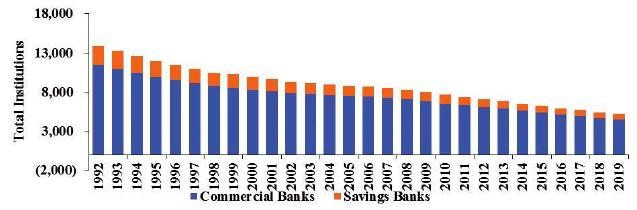

Historically, regional and community banks were the primary providers of construction financing to smaller, private builders. Over the past several decades, there has been significant consolidation within the commercial banking industry, with the number of commercial and savings institutions having decreased by 61% and 72%, respectively, between 1992 and 2019, as reported by the FDIC. In addition, many traditional real estate lenders that competed for loan origination within our target markets have been faced with tighter capital constraints due to changing banking regulations following the 2008 financial crisis. The chart below illustrates the decline in number of commercial and savings banks from 1992 to 2019.

Source: FDIC

While the number of traditional banks and construction loans offered by them has steadily declined, private residential construction spending and housing starts continued to recover from the lows following the 2008 financial crisis through 2019. Current housing starts still remain well below historical averages. In addition, housing starts remain well below the 1.6 million annual housing starts needed to meet current demand, according to Freddie Mac. The chart below illustrates historical housing starts from 1988 to 2019 versus the minimum annual need per Freddie Mac:

Source: Federal Reserve Bank of St. Louis and Freddie Mac

We believe the longer-term outlook for new housing demand remains strong given limited residential housing supply and low interest rate environment for home buyers despite the COVID-19 pandemic and the economic consequences arising from it. In February 2020, Freddie Mac estimated that 2.5 million additional housing units are needed to make up for the shortage.

We believe we are well positioned to capitalize and profit from these industry dynamics. We and our Predecessor Companies have operated in the Pacific Northwest markets since 2010 and in the Mountain West markets since 2014. More recently, through the Predecessor companies we expanded into Southeast markets in 2018 and into Mid-Atlantic markets in 2019.

| 7 |

Business and Growth Strategy

Our objective is to preserve and protect stockholder capital while producing attractive risk-adjusted returns primarily through dividends generated from current income from our loan portfolio. Our business strategy is to directly originate, fund, manage, and service short-term loans secured by first deed of trust liens on real property in order to generate attractive returns. We believe our ability to react quickly to the needs of borrowers, flexibility in terms of structuring loans to meet the needs of borrowers, consistency and expediency in funding future construction draws, intimate knowledge of the relevant markets in which we operate, and focus on newly originated first deed of trust loans positions us to generate attractive returns.

Our strategy to achieve this objective includes the following:

| · | continue to increase market share in existing states to satisfy unmet demand; |

| · | increase geographic footprint by focusing on non-judicial foreclosure states with favorable economic and demographic trends; |

| · | capitalize on opportunities created by the long-term structural changes in the real estate lending market resulting from consolidation and increased regulatory oversight of commercial banks and savings institutions; |

| · | capitalize on the relative strength of our unleveraged balance sheet to grow our customer and asset base while competitors with weaker balance sheets may be capital constrained; |

| · | remain flexible in order to capitalize on changing sets of investment opportunities that may be present in the various points of an economic cycle; |

| · | grow the Private REIT, generating an additional revenue stream by way of management fees to us; and |

| · | operate so as to qualify as a REIT for federal income tax purposes and distribute annually at least 90% of our REIT taxable income. |

Loan Portfolio

The following table highlights certain information regarding Broadmark Realty’s real estate lending activities for the periods indicated:

| For the Six | For the Years Ended, | |||||||||||||||

| Months Ended June 30, | December 31, | |||||||||||||||

| (Dollar amounts in millions) | 2020 | 2019 | 2019 | 2018 | ||||||||||||

| Loans originated | 37 | 72 | 116 | 194 | ||||||||||||

| Loans repaid | 75 | 72 | 140 | 140 | ||||||||||||

| As of June 30, | As of December 31, | |||||||||||||||

| 2020 | 2019 | 2019 | 2018 | |||||||||||||

| Number of loans outstanding | 216 | 264 | 241 | 266 | ||||||||||||

| Unpaid principal balance (end of period balance)(1) | $ | 832.3 | $ | 722.7 | $ | 829.0 | $ | 591.3 | ||||||||

| Total commitment | $ | 1,121.5 | $ | 1,031.3 | $ | 1,101.3 | $ | 898.1 | ||||||||

| Average total commitment | $ | 5.2 | $ | 3.9 | $ | 4.6 | $ | 3.4 | ||||||||

| Weighted average contractual interest rate per annum(2) | 12 | % | 12 | % | 12 | % | 12 | % | ||||||||

(1) June 30, 2020 excludes $6.9 million of Private REIT participation, and construction holdbacks of $7.1 million and interest reserves of $0.7 million on participation interests sold to the Private REIT. The Private REIT was determined to be a voting interest entity for which we, through our wholly owned subsidiary acting as manager with no equity investment, do not hold a controlling interest in and do not consolidate the Private REIT. Furthermore, the Private REIT participation in loans originated by us meets the characteristics of a participating interest in accordance with ASC 860 and therefore, is treated as a sale of mortgage notes receivable and is derecognized from our condensed consolidated financial statements.

(2) Does not include origination fees.

| 8 |

The following table sets forth aggregate number of loans and the total commitment amounts at origination during each of the calendar years set forth below.

| Number of | Total | |||||||

| Year of Origination | Loans | Commitment ($M)(1) | ||||||

| 2020 (through June 30) | 37 | $ | 158.6 | |||||

| 2019 | 116 | $ | 446.6 | |||||

| 2018 | 194 | $ | 647.0 | |||||

| 2017 | 175 | $ | 397.7 | |||||

| 2016 and prior | 565 | $ | 523.6 | |||||

(1) Excludes subsequent loan amendments including amendments that increase the total commitment. Broadmark Realty categorizes its loans into three distinct purposes:

| · | Vertical Construction. Loans which utilize at least 20% of total commitment at origination to fund vertical construction of residential, commercial and mixed-use properties. |

| · | Horizontal Development. Loans which do not fund vertical construction and utilize at least 20% of total commitment at origination to fund horizontal improvements including: initial site preparation, ground clearing, installing utilities, and road, sidewalk and gutter paving. |

| · | Investment. Loans which do not fund vertical or horizontal construction including financings of built real estate properties or raw land. |

The following table sets forth the number of total loans and commitment amount of mortgage loans based on the intended loan purpose, and the percentage of the total commitment by purpose as compared to the total portfolio, in each case at June 30, 2020.

| At June 30, 2020 | ||||||||||||

| Total | ||||||||||||

| Commitment | ||||||||||||

| Loan Purpose | # of Loans | ($M) | % | |||||||||

| Vertical Construction | 153 | $ | 781.3 | 69.7 | % | |||||||

| Horizontal Development | 29 | 194.3 | 17.3 | % | ||||||||

| Investment | 34 | 145.9 | 13.0 | % | ||||||||

| Total | 216 | $ | 1,121.5 | 100.0 | % | |||||||

Broadmark Realty categorizes its loans into five property types:

| · | For Sale Residential. All for sale residential product including single family homes, townhomes, condominiums and other attached product. |

| 9 |

| · | For Rent Residential. All rental residential product including multifamily rental apartments and senior housing. |

| · | Commercial/Other. Non-residential real estate including retail, office, industrial and hotels. |

| · | Horizontal Development. Vertical construction ready sites including finished single-family lots, finished townhome lots and multifamily and commercial development sites. |

| · | Raw Land. Undeveloped land prior to horizontal development. |

The following table sets forth the number of total loans and commitment amount of mortgage loans based on the types of properties securing Broadmark Realty’s mortgage loans, and the percentage of the total commitment by property security of the loan as compared to the total portfolio at June 30, 2020.

| At June 30, 2020 | ||||||||||||

| Total | ||||||||||||

| Commitment | ||||||||||||

| Property Type | # of Loans | ($M) | % | |||||||||

| For Sale Residential | 112 | $ | 397.8 | 35.5 | % | |||||||

| For Rent Residential | 21 | 197.3 | 17.6 | % | ||||||||

| Horizontal Development | 33 | 201.2 | 17.9 | % | ||||||||

| Commercial/Other | 32 | 246.3 | 22.0 | % | ||||||||

| Raw Land | 18 | 78.9 | 7.0 | % | ||||||||

| Total | 216 | $ | 1,121.5 | 100.0 | % | |||||||

At June 30, 2020, we owned one commercial property that we had acquired through foreclosure, which had a carrying value of $3.7 million.

The following table sets forth the number of total loans and total committed amounts of mortgage loans by state, and the percentage of the total committed amount by state as compared to the total portfolio at June 30, 2020.

| June 30, 2020 | ||||||||||||

| Total | ||||||||||||

| # of | Commitment | |||||||||||

| State | Loans | ($M) | % | |||||||||

| WA | 58 | $ | 260.5 | 23.2 | % | |||||||

| CO | 48 | 259.8 | 23.2 | % | ||||||||

| UT | 31 | 241.1 | 21.5 | % | ||||||||

| TX | 17 | 175.2 | 15.6 | % | ||||||||

| OR | 12 | 85.2 | 7.6 | % | ||||||||

| ID | 16 | 54.9 | 4.9 | % | ||||||||

| Other | 34 | 44.8 | 4.0 | % | ||||||||

| Total | 216 | $ | 1,121.5 | 100.0 | % | |||||||

| 10 |

Operations Overview

Loan Origination and Servicing Process

Broadmark Realty is experienced in secured lending, with significant combined real estate and financial services experience of its senior management team. Broadmark Realty’s senior management team spends a significant portion of its time on borrower development as well as on underwriting and structuring the loans in Broadmark Realty’s portfolio. A principal source of new transactions for Broadmark Realty has been repeat business from our customers and their referral of new business. When underwriting a loan, the primary focus of Broadmark Realty’s analysis is the value of a property. Prior to making a final decision on a loan application Broadmark Realty conducts extensive due diligence of the property as well as the borrower and its principals.

The mortgage loans originated by Broadmark Realty generally meet the following criteria:

| · | Collateral. New loans are secured by a first deed of trust lien on real estate. | |

| · | Amount. The amount of Broadmark Realty’s loans range from $0.1 to $35 million in total commitment at origination (average total commitment of $5.2 million for our active loans at June 30, 2020). Our present loan policy limits new loans to an individual size of no greater than 5.0% of the aggregate total commitment of our active loans, and a maximum exposure to any single borrower of 10.0%. | |

| · | Loan to Value. The maximum LTV ratio for a loan at origination is 65.0% of the “as-complete” appraised value of the underlying collateral; and a maximum initial outstanding principal balance of the loan at origination is 65% of the “as-is” appraised value of the underlying collateral, in each case as determined by an independent appraiser at the time of the loan origination. |

| · | Interest rate. Generally, a fixed rate between 10.0% and 13.0% per annum with a late fee of 10.0% of the amount outstanding and a default rate of 24.0% per annum. |

| · | Origination fees. Typically ranges from 4.0% to 5.0% of the total commitment at origination. In addition, if the term of the loan is extended, additional points are payable upon the extension. |

| · | Term. Typically, five to twelve months. Broadmark Realty may agree to extend the maturity date so long as the borrower complies with all loan covenants, financial and non-financial, and the loan otherwise satisfies its then existing underwriting criteria. If Broadmark Realty extends the maturity date to a date that is equal to or greater than twelve months after the initial loan origination, then the loan is registered to go through the underwriting process again, including receipt and review by Broadmark Realty of a new independent appraisal report. |

| · | Covenants. To timely pay all taxes, insurance, assessments, and similar charges with respect to the property; to maintain hazard insurance; and to maintain and protect the property. |

| · | Events of default. Include: (i) failure to make payment when due; and (ii) breach of a covenant. |

| · | Payment terms. Interest only is payable monthly in arrears. Principal is due in a “balloon” payment at the maturity date. Interest earned from an interest holdback is capitalized in the loan principal balance. |

| · | Escrow. Generally, none required. |

| · | Holdbacks. Construction loans typically include a holdback for future construction draws which are funded in arrears following confirmation of work completion. Loans may also include a holdback for interest payments due to a lack of income generated by the real estate. |

| · | Security. Each loan is evidenced by a promissory note, which is secured by a first deed of trust lien on real property owned by the borrower and is personally guaranteed on a recourse basis by the principals of the borrower and/or others, at the discretion of Broadmark Realty, which guarantee may be collaterally secured by a pledge of the guarantor’s interest in the borrower or other real estate owned by the guarantor. |

| · | Fees and Expenses. As is typical in real estate finance transactions, the borrower incurs all expenses in connection with securing the loan, including the cost of a property appraisal, the cost of an environmental assessment report, if any, the cost of a credit report and all title, recording fees and legal fees. |

| 11 |

Upon receipt of a potential borrower’s executed loan application, Broadmark Realty will commence the underwriting process. Before approving and funding a loan, Broadmark Realty undertakes extensive due diligence of the borrower, its principals, the guarantor and the property that will be mortgaged to secure the loan. Such due diligence generally includes:

| · | Borrower and Guarantor Information. Review of a borrower’s credit application, operating agreement or other organizational documents, and review of business and guarantor financial statements and tax returns. |

| · | Confirmatory Collateral Information. Review of an independent appraisal report (customarily including market data and analysis and information regarding comparable properties), preliminary title report, tax records, documentation evidencing proper hazard insurance for improved property, and other property information. Loans secured by existing commercial properties require a Phase I environmental site assessment. |

| · | Project Transaction Information. Review of the property purchase and sale agreement, title insurance, itemized construction budget, building permits, building plans, and specifications and marketing plans and materials. |

| · | Physical Inspection. Broadmark Realty performs a physical inspection of the property, which includes a check of the property’s location, characteristics, qualities, and potential value as represented by the borrower, as well as a review of the comparable properties identified in the independent appraisal report in order to confirm that the properties identified as comparable in the appraisal report are truly comparable. |

Loan Servicing

Broadmark Realty services all of its loans internally, and manages loan payments, draw requests, and loan accounting histories and records. The loan draw process in particular is an important part of Broadmark Realty’s business as it provides borrowers with quick access to capital in order to keep their projects moving, and allows Broadmark Realty to inspect the quality and pace of the borrower’s work. Once a borrower has submitted a draw request, Broadmark Realty will have the project inspected to ensure that the work for which funding is being requested has been completed in a manner satisfactory to Broadmark Realty. In addition, any required county and city inspections are completed and lien releases from all vendors and subcontractors are collected before funds are disbursed. Although the process is thorough, Broadmark Realty makes a point of responding to draw requests as quickly as possible as timing is of paramount importance to a project’s success.

In addition, Broadmark Realty will conduct periodic testing, process loan payoff requests, and collect past due and delinquent payments. In the case of a loan default, Broadmark Realty has broad authority to take such actions as it believes best in working out the defaulted loan, including selling the defaulted loan or foreclosing on the real property serving as collateral for the loan.

Loan Funding

Broadmark Realty’s ability to grow its business is primarily constrained by its ability to raise capital to fund additional real estate loans. Prior to the Business Combination, Broadmark Realty funded loans primarily through the use of private capital. Going forward, Broadmark Realty intends to fund its growth through issuance of common stock, potential use of cash management tools such as a credit facility and the sale of participation interests in loans we originate to the Private REIT.

| 12 |

Private REIT

The Private REIT primarily participates in short-term, first deed of trust loans secured by real estate to fund the construction and development of, or investment in, residential or commercial properties located in the United States that are originated, underwritten and serviced by Broadmark Realty. The Private REIT is managed by the Private REIT Manager. Similar to Broadmark Realty, the Private REIT’s investment objective is to provide attractive risk-adjusted returns primarily through fees and interest income primarily generated from investing in participation interests in Broadmark Realty’s real estate portfolio. The Private REIT initiated operations in 2020 and expects to elect to be taxed as a REIT for U.S. federal income tax purposes at such point in time as the Private REIT satisfies the requirements for making such election and certain other conditions are met. The Private REIT will be classified as a partnership for U.S. federal income tax purposes until such election is made, should the Private REIT not make the election to be taxed as a REIT effective as of its initial tax year.

Broadmark Realty and the Private REIT entered into a Master Loan Participation Agreement (the “Participation Agreement”) pursuant to which a subsidiary of Broadmark Realty expects to offer the Private REIT participation interests in loans that it originates. Broadmark Realty retains sole authority with respect to whether to permit the Private REIT to participate in any particular loan. Broadmark Realty also retains sole authority with respect to the participation percentage of each loan that the Private REIT will receive. While Broadmark Realty generally expects to permit the Private REIT to participate equally in loans that it originates, Broadmark Realty is not required to permit the Private REIT to participate in any particular loan, and the Private REIT will be able to participate in loans only in the amount permitted by Broadmark Realty and will be further limited by the amount of its “Cash Available to Lend.” “Cash Available to Lend” typically will include cash in excess of the Private REIT’s obligations under existing mortgages or participations therein, including contributions of cash from the admission of investors and repayments of mortgages or sales of assets, but excluding cash distributable to investors, cash existing or accrued expenses and liabilities, reserves for estimated construction draws and anticipated redemption payments, or write-downs of defaulted mortgages, if any, in each case as determined by the Private REIT Manager in its discretion. In the event that the Private REIT has Cash Available to Lend in excess of the loan participation interests offered to it by Broadmark Realty, the Private REIT could originate its own mortgages or purchase mortgages from third parties that are comparable to those originated by Broadmark Realty.

The Private REIT Manager is compensated with respect to the mortgages initiated by the Private REIT or participations in Broadmark Realty’s mortgages through the Private REIT Manager’s receipt of 80% of all fee-based income (generally borrower loan fees, including origination points, late fees and extension fees) and 20% of all cash distributable to Private REIT investors in excess of the monthly 0.5% preferred return to investors.

The Private REIT is continuously offering its preferred units to qualified investors in a private placement pursuant to Regulation D promulgated under the Securities Act. The initial sale of Private REIT preferred units occurred in March 2020, and at June 30, 2020, the Private REIT’s assets under management were approximately $12.4 million.

Competition

Real estate lending is a competitive business. Broadmark Realty competes for lending opportunities with a variety of institutional lenders and investors, including other “hard money” lenders, mortgage REITs, specialty finance companies, savings and loan associations, banks, mortgage banks, credit unions, insurance companies, mutual funds, pension funds, private equity real estate funds, hedge funds, institutional investors, investment banking firms, non-bank financial institutions, governmental bodies, family offices, and high net worth individuals. New parties continue to enter the market resulting in increased competition and pricing pressure.

Broadmark Realty competes on the basis of borrower relationships, product offerings, loan structure, terms, and service. Broadmark Realty’s success depends on its ability to maintain and capitalize on relationships with borrowers and their representatives, offer attractive loan terms and provide superior service.

Seasonality

While Broadmark Realty typically originates loans year-round, incremental loan disbursements are made with greater frequency during the spring, summer and fall, when weather is generally more favorable for construction, and borrowers complete previously agreed stages of construction, allowing developers to draw down on additional amounts of capital available under their loan agreements. As a result of these more frequent disbursements, Broadmark Realty generally maintains greater amounts of cash on hand to fund these disbursements during these seasons.

| 13 |

Intellectual Property and Proprietary Data

Broadmark Realty’s business does not depend on exploiting or leveraging any particular intellectual property rights. To the extent that Broadmark Realty owns any rights to intellectual property, it relies on a combination of registered and state, federal, and common law trademarks, service marks, trade names, copyrights, and trade secret protection. Broadmark Realty currently has an application for registration of the trademark “Broadmark” pending with the United States Patent Trademark Office (“USPTO”) and has two applications pending the USPTO for the design of the Broadmark Realty logo.

Properties

Broadmark Realty leases its executive offices in Seattle, Washington and has entered a lease to expand its space to accommodate growth.

Employees

As of June 30, 2020, Broadmark Realty had 42 employees.

Regulation and Compliance

Broadmark Realty’s operations are subject, in certain circumstances, to supervision and regulation by state and U.S. federal government authorities and may be subject to various laws and judicial and administrative decisions imposing various requirements and restrictions. In addition, Broadmark Realty and its subsidiaries may rely on exemptions from various requirements of the Securities Act, the Exchange Act, the Investment Company Act, and the Investment Advisers Act. These exemptions are sometimes highly complex and may, in certain circumstances, depend on compliance by third parties who Broadmark Realty does not control.

Regulation of Commercial Real Estate Lending Activities

In general, commercial real estate lending is a highly regulated industry in the United States and Broadmark Realty is required to comply with, among other statutes and regulations, certain provisions of the Equal Credit Opportunity Act that are applicable to commercial loans, the USA Patriot Act, regulations promulgated by the Office of Foreign Asset Control, and U.S. federal and state securities laws and regulations. In addition, certain states have adopted laws or regulations that may, among other requirements, require licensing of lenders and financiers, prescribe disclosures of certain contractual terms, impose limitations on interest rates and other charges, and limit or prohibit certain collection practices and creditor remedies. Broadmark Realty is required to comply with the applicable laws and regulations in the states in which it does business.

Exemptions from Investment Company Act

Although we reserve the right to modify our business methods at any time, we believe that none of the Company, our subsidiary that issues and holds the mortgages (the “Mortgage Subsidiary”) or the Private REIT is currently required to register as an investment company under the Investment Company Act. However, our business strategies may evolve over time.

Section 3(a)(1)(A) of the Investment Company Act defines an investment company as any issuer that is, or holds itself out as being, engaged primarily, or proposes to engage primarily, in the business of investing, reinvesting or trading in securities. Section 3(a)(1)(C) of the Investment Company Act defines an investment company as any issuer that is engaged or proposes to engage in the business of investing, reinvesting, owning, holding or trading in securities, and owns or proposes to acquire investment securities having a value exceeding 40% of the value of such issuer’s total assets (exclusive of U.S. government securities and cash items) on an unconsolidated basis. Excluded from the term “investment securities” are, among other things, securities issued by majority-owned subsidiaries that are not themselves investment companies and are not relying on the exclusion from the definition of “investment company” set forth in Section 3(c)(1) or Section 3(c)(7) of the Investment Company Act.

| 14 |

The Company believes it will not be considered an investment company under Section 3(a)(1)(A) of the Investment Company Act because it will not engage primarily, or propose to engage primarily, or hold itself out as being engaged primarily, in the business of investing, reinvesting or trading in securities. Rather, the Company is primarily engaged in the non-investment company business of its wholly owned subsidiaries.

The Company believes that it will not be considered an investment company under Section 3(a)(1)(C) of the Investment Company Act. The Company is a holding company that conducts its operations and holds assets primarily through its wholly-owned subsidiaries, including the Mortgage Subsidiary. The Mortgage Subsidiary is excluded from the definition of investment company pursuant to Section 3(c)(5)(C) of the Investment Company Act, which provides an exclusion for companies engaged primarily in investment in mortgages and other liens on or interests in real estate. In order to qualify for this exclusion, the Mortgage Subsidiary must maintain, on the basis of positions taken by the SEC’s Division of Investment Management in interpretive and no-action letters, a minimum of 55% of the value of its total assets in mortgage loans and other related assets that are considered “mortgages and other liens on and interests in real estate” (“Qualifying Interests”), and a minimum of 80% in Qualifying Interests and real estate-related assets. In the absence of SEC guidance that supports the treatment of other investments as Qualifying Interests, the Mortgage Subsidiary will treat those other investments appropriately as real estate-related assets or miscellaneous assets depending on the circumstances. With respect to the Company’s other subsidiaries that maintain this exclusion or another exclusion or exception under the Investment Company Act (other than Section 3(c)(1) or Section 3(c)(7) thereof), or otherwise do not meet the definition of “investment company,” the Company’s interests in these subsidiaries do not and will not constitute “investment securities.”

The Private REIT is not registered, and does not intend to register, as an investment company under the Investment Company Act in reliance upon an exclusion from the definition of investment company provided in Section 3(c)(7) or Section (c)(1) of the Investment Company Act.

Exemption from Investment Advisers Act

The Company does not have a wholly owned subsidiary that would be required to register under the Investment Advisers Act of 1940, as amended (the “Advisers Act”), or under any state securities laws, based on their current activities. The Private REIT Manager relies on the exemption from registration under the Advisers Act registration for certain private fund advisers set forth in Section 203(m)(1) of the Advisers Act and Rule 203(m)-1 promulgated thereunder.

The Private REIT Manager will be required to register with the SEC as an investment adviser under the Investment Advisers Act if the Private REIT’s assets reach $150 million or more, unless another exemption is available. As a registered investment adviser, the Private REIT Manager will become subject to substantial regulation with respect to its compliance policies and procedures, books and record keeping obligations, and to receive client consent to certain transactions, including any change in control of the Private REIT Manager that would result in an “assignment” of voting equity interests (as that term is defined in the Advisers Act).

Exemption from Securities Act of 1933

The Private REIT continuously offers its preferred units to qualified investors in a private placement pursuant to Regulation D promulgated under the Securities Act.

Compliance with Broker-Dealer Regulations

The Private REIT has engaged a registered broker-dealer to act as placement agent, and the Private REIT Manager voluntarily has agreed to pay the placement agent’s annual fee for the first year without reimbursement from the Private REIT. Certain of the Private REIT Manager’s personnel are registered representatives of the placement agent who market the Private REIT preferred units to eligible investors. Although neither the placement agent nor its registered representatives receives any sales commission with respect to the Private REIT preferred units, the Private REIT Manager’s personnel could be eligible to receive a bonus from the Company based on multiple factors, including the growth of the Private REIT Manager. The Private REIT and the Private REIT Manager have engaged third party broker-dealers to refer investors. The Private REIT Manager pays an initial referral fee to third-party broker-dealers equal to 1.0% of a subscriber’s accepted capital contribution to the Private REIT, and, after the first anniversary thereof, an annual fee of 0.50% of the accepted contribution, payable quarterly in arrears for so long as such subscriber continues to hold Private REIT preferred units.

| 15 |

Legal Proceedings

Broadmark Realty is involved in legal proceedings which arise in the ordinary course of business. It believes that the outcome of such matters, individually and in the aggregate, will not have a material adverse effect on its business, financial condition and results of operations.

Policies with Respect to Certain Activities

The following is a discussion of our investment, financing and certain other policies that we have adopted. We intend to conduct our business in a manner such that we are not treated as an investment company under the Investment Company Act. We intend to conduct our business in a manner that is consistent with maintaining our qualification to be taxed as a REIT. These policies may be amended or revised from time to time at the discretion of our board without a vote of our stockholders.

Lending Policies

Real estate lending is our business and our current intention is to continue to focus exclusively on making short-term, first deed of trust loans secured by real estate to fund the construction and development of, or investment in, residential or commercial properties. Our intent is to continue to focus primarily on Washington, Utah, Colorado, Texas, Oregon and Idaho, but also to increase our geographic footprint by focusing on non-judicial foreclosure states with favorable demographic trends. We currently have licenses in Oregon and Idaho. Similarly, we intend to continue to focus only on lending opportunities that will be secured by first deed of trust liens. We have no interest in funding mezzanine, subordinated debt or unsecured debt. Any change in our lending policy would require the approval of our board.

Our executive officers have authority over all lending decisions and wide latitude to set the terms of each particular loan. Our general policy is that (i) each of our loans shall be secured by a first deed of trust lien on real estate, and (ii) the maximum principal amount of a loan shall not exceed 65.0% of the “as-complete” appraised value of the underlying collateral as determined by an independent appraiser at the time of the loan origination. These policies may be waived by our loan committee in appropriate circumstances where there are other indicators of strong credit quality, and may be modified by our board.

Financing and Leverage Policy

Our primary liquidity needs include ongoing commitments to fund our lending activities and future funding obligations for our existing loan portfolio, paying dividends and funding other general business needs. Our primary sources of liquidity and capital resources to date have been derived from the capital contributions from members of the Predecessor Companies, cash flow from operations and payoffs of existing loans. Neither Broadmark Realty nor the Predecessor Company Group has utilized any borrowings since inception. As of June 30, 2020, our cash and cash equivalents totaled $218.0 million.

We seek to meet our long-term liquidity requirements, such as real estate lending needs including future construction draw commitments, through our existing cash resources and return of capital from investments, including loan repayments. Additionally, going forward, we intend to fund our growth through the issuance of common stock, potential use of cash management tools such as a credit facility and the sale of additional participation interests in loans we originate to the Private REIT.

There is no assurance that Broadmark Realty will not issue debt or equity ranking senior to our common stock in the future. For example, we are exploring establishing a revolving credit facility for cash management purposes but have no current plans to incur debt to fund our lending. Those securities will generally have priority upon liquidation. Such securities also may be governed by an indenture or other instrument containing covenants restricting its operating flexibility. Additionally, any convertible or exchangeable securities that Broadmark Realty issues in the future may have rights, preferences and privileges more favorable than those of the shares of our common stock. Because Broadmark Realty’s decision to issue debt or equity in the future will depend on market conditions and other factors beyond Broadmark Realty’s control, it cannot predict or estimate the amount, timing, nature or success of Broadmark Realty’s future capital raising efforts. As a result, future capital raising efforts may reduce the market price of the shares of our common stock and be dilutive to existing stockholders.

| 16 |

Any decision to use leverage and the appropriate level of leverage would be made by our board based on its assessment of a variety of factors, including our historical and projected financial condition, liquidity and results of operations, financing covenants, the cash flow generation capability of assets, the availability of credit on favorable terms, our outlook for borrowing costs relative to the unlevered yields on our assets, REIT qualification, applicable law and other factors. Our decision to use leverage will not be subject to the approval of our stockholders and there are no restrictions in our governing documents in the amount of leverage that we may use.

Investment Policies

Investment in Real Estate or Interests in Real Estate

Our business has been and continues to be one that focuses on originating, servicing and managing a portfolio of funding short-term, first deed of trust loans secured by real estate to fund the construction and development of, or investment in, residential or commercial properties. Direct investment in real estate is not our primary focus. Any decision to invest in real estate or to purchase an interest in real estate outside of our core business, including the acquisition of a portfolio of loans, would only be undertaken with the approval of our board.

Sales of Loans

We do not make loans with the intent of selling them to third parties. However, from time to time, we may determine to do so. Since the commencement of the Predecessor Company Group’s 2017 fiscal year, we have sold seven loans with an aggregate face value of $6.8 million.

Securities of or Interests in Persons Primarily Engaged in Real Estate Activities

We have not purchased, nor do we currently intend to purchase, securities of or interests in entities that are engaged in real estate activities. In any event, because we must comply with various requirements under the Code in order to be taxed as a REIT, including restrictions on the types of assets we may hold, the sources of our income and accumulation of earnings and profits, and because we want to avoid being characterized as an investment company under the Investment Company Act, our ability to engage in these types of transactions, such as acquisitions of “C” corporations, may be limited. Accordingly, any decision to purchase securities of or interests in entities that are engaged in real estate activities would require the approval of our board.

Policies with Respect to Other Activities

We have the authority to issue debt securities, including senior securities, offer shares of common stock, preferred shares or options to purchase shares of common stock in exchange for property and to repurchase or otherwise reacquire our common shares or other securities in the open market or otherwise, and we may engage in such activities in the future. Our board has the authority, without further stockholder approval, to authorize us to issue additional common shares or preferred shares, in one or more series, including senior securities, in any manner, and on the terms and for the consideration, it deems appropriate, subject to applicable laws and regulations. See “Description of Capital Stock and Warrants.” We have not engaged in trading, underwriting or agency distribution or sale of securities of other issuers and do not intend to do so. Any decision to raise capital through the sale of equity or debt securities and any decision to repurchase common shares requires the approval of our board.

| 17 |

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT

The following information table sets forth information known to us regarding the beneficial ownership of our common stock as of August 24, 2020 by:

| · | each of the Company’s directors; |

| · | each of our named executive officers; |

| · | all of the Company’s directors, director nominees and executive officers as a group; and |

| · | each person known to us to be the beneficial owner of more than 5% of outstanding shares of our common stock. |

Beneficial ownership is determined according to the rules of the Commission, which generally provide that a person has beneficial ownership of a security if such person possesses sole or shared voting or investment power over that security, including options and warrants that are currently exercisable or exercisable within 60 days. Common stock issuable upon exercise of options and warrants currently exercisable or exercisable within 60 days, and equity awards vesting within 60 days, are deemed outstanding solely for purposes of calculating the percentage of total voting power of the beneficial owner thereof.

The beneficial ownership of our common stock is based on 132,231,184 shares of our common stock issued and outstanding as of August 24, 2020. As of August 24, 2020, we had 385 holders of record of our common stock.

| Shares | Percentage | |||||||

| Beneficially | of Outstanding Shares | |||||||

| Name of Beneficial Owner(1) | Owned | Beneficially Owned | ||||||

| Joseph L. Schocken(2) | 2,083,657 | 1.6 | % | |||||

| Jeffrey B. Pyatt(3) | 2,500,960 | 1.9 | % | |||||

| Stephen G. Haggerty(4) | 821,184 | * | ||||||

| Daniel J. Hirsch(5) | 30,000 | * | ||||||

| Kevin M. Luebbers(6) | 20,000 | * | ||||||

| Norma J. Lawrence | — | * | ||||||

| David A. Karp | — | * | ||||||

| David Schneider | — | * | ||||||

| Adam Fountain(7) | 607,773 | * | ||||||

| Joanne Van Sickle(8) | 413,288 | * | ||||||

| All current directors and executive officers as a group (10 individuals)(9) | 5,497,106 | 4.2 | % | |||||

| All directors, executive officers and other named executive officers (12 individuals, including former executive officers)(10) | 6,518,167 | 4.9 | % | |||||

| Greater than 5% Stockholders: | ||||||||

| Farallon Capital Management, L.L.C.(11) | 11,355,402 | 8.3 | % | |||||

| Vanguard Group Inc.(12) | 8,851,056 | 6.7 | % | |||||

| Multi-Sector Credit, LLC(13) | 8,090,231 | 6.1 | % | |||||

* Less than 1%.

| (1) | Unless otherwise noted, the business address of each of the following entities or individuals is c/o Broadmark Realty Capital Inc., 1420 Fifth Avenue, Suite 2000, Seattle, Washington 98101. |

| (2) | Includes 140,358 shares held directly by Mr. Schocken, 189,039 shares held by Tranceka, LLC, 229,588 shares held by Tranceka Capital, LLC and 1,524,672 shares held by Tranceka Holdings, LLC. Mr. Schocken is the beneficial owner of the shares held by Tranceka, LLC, Tranceka Capital, LLC and Tranceka Holdings, LLC as he holds voting and dispositive power over such shares. |

| 18 |

| (3) | Includes 13,337 shares held jointly by Mr. Pyatt and his wife, and 2,487,623 shares held by Pyatt Lending Company, LLC. Mr. Pyatt and his spouse are the beneficial owners of the shares held by Pyatt Lending Company, LLC as they share voting and dispositive power over such shares. |

| (4) | Includes 209,521 Company Private Placement Warrants currently exercisable for 209,521 shares of our common stock. Mr. Haggerty has a pecuniary interest in Company Private Placement Warrants owned by Trinity Investments through Mr. Haggerty’s ownership of an interest in Trinity Investments. In the aggregate, taking into account his ownership interests in Trinity Investments, Mr. Haggerty is expected to have a direct or indirect ownership interest in an additional 1,119 Company Private Placement Warrants to acquire 1,119 shares of our common stock, in addition to the securities that he presently owns. The interest in these shares and Company Private Placement Warrants, together with the shares he will receive upon vesting of the restricted stock units (“RSUs”) he has been awarded as part of his compensation as a director, and the shares of our common stock he owned as of August 24, 2020, are expected to represent, a less than 1% beneficial ownership interest by Mr. Haggerty in the Company to the extent these securities were deemed to be beneficially owned by him. |

| (5) | Mr. Hirsch served as a consultant to Trinity Investments pursuant to a consulting agreement, as discussed under “Certain Relationships and Related Party Transactions.” Mr. Hirsch’s consulting agreement provides for a success fee payable by Trinity Investments to Mr. Hirsch in connection with the completion of the Business Combination, pursuant to which Mr. Hirsch will receive 137,305 shares of our common stock and 259 of the Company Private Placement Warrants held by Trinity Investments. These shares of common stock and Company Private Placement Warrants, together with the shares he will receive upon vesting of the RSUs he has been awarded as part of his compensation as a director, and the shares of our common stock he owned as of August 24, 2020, are expected to represent, in the aggregate, a less than 1% beneficial ownership interest by Mr. Hirsch in the Company. Instead of transferring the 137,305 shares of our common stock and 259 of the Company Private Placement Warrants to Mr. Hirsch, Trinity Investments may, at its election, pay the success fee in cash in an amount equal to the value of these securities. |

| (6) | Mr. Luebbers served as a consultant to Trinity Investments pursuant to a consulting agreement, as discussed under “Certain Relationships and Related Party Transactions.” Mr. Luebbers’ consulting agreement provides for a success fee payable by Trinity Investments to Mr. Luebbers in connection with the completion of the Business Combination, pursuant to which Mr. Luebbers will receive 137,305 shares of our common stock and 259 of the Company Private Placement Warrants held by Trinity Investments following the expiration of a lock-up agreement to which Trinity Sponsor is a party. These shares of common stock and Company Private Placement Warrants, together with the shares he will receive upon vesting of the RSUs he has been awarded as part of his compensation as a director, and the shares of our common stock he owned as of August 24, 2020, are expected to represent, in the aggregate, a less than 1% beneficial ownership interest by Mr. Luebbers in the Company. Instead of transferring the 137,305 shares of our common stock and 259 of the Company Private Placement Warrants to Mr. Luebbers, Trinity Investments may, at its election, pay the success fee in cash in an amount equal to the value of these securities. |

| (7) | Mr. Fountain resigned as an executive officer as of March 31, 2020. |

| (8) | Ms. Van Sickle resigned as an executive officer as of February 1, 2020. |

| (9) | The reported amount excludes the Company Private Placement Warrants held by Trinity Investments that Mr. Haggerty has an interest in, and those shares of common stock and Company Private Placement Warrants that may be transferred to Messrs. Hirsch and Luebbers by Trinity Investments. |

| (10) | The reported amount excludes the Company Private Placement Warrants held by Trinity Investments that Mr. Haggerty has an interest in, and those shares of common stock and Company Private Placement Warrants that may be transferred to Messrs. Hirsch and Luebbers by Trinity Investment, but includes shares of our common stock owned by Mr. Fountain and Ms. Van Sickle, each of whom is a former executive officer. |

| 19 |

| (11) | Based on a Schedule 13G/A filed with the SEC on February 14, 2020 and subsequent information provided to us by Farallon Capital Management, L.L.C. Includes (i) 7,170,213 shares of our common stock (including 2,384,159 shares of our common stock directly held by Farallon Capital Partners, L.P. (“FCP”)), 3,101,221 shares of our common stock directly held by Farallon Capital Institutional Partners, L.P. (“FCIP”), 573,569 shares of our common stock directly held by Farallon Capital Institutional Partners II, L.P. (“FCIP II”), 376,367 shares of our common stock directly held by Farallon Capital Institutional Partners III, L.P. (“FCIP III”), 537,696 shares of our common stock directly held by Four Crossings Institutional Partners V, L.P. (“FCIP V”), and 197,201 shares of our common stock directly held by Farallon Capital (AM) Investors, L.P. (“FCAMI”)), (ii) 2,391,536 shares of our common stock, that may be issued pursuant to the option under the PIPE Investment (including 795,186 shares of our common stock that may be issued directly to FCP, 1,034,340 shares of our common stock that may be issued directly to FCIP, 191,323 shares of our common stock that may be issued directly to FCIP II, 125,555 shares of our common stock that may be issued directly to FCIP III, 179,365 shares of our common stock that may be issued directly to FCIP V, and 65,767 shares of our common stock that may be issued directly to FCAMI), and (iii) 1,793,653 shares of our common stock, calculated as one quarter of the 7,174,613 Public Warrants (including 596,390 shares of our common stock calculated based on 2,385,559 Public Warrants directly held by FCP, 775,755 shares of our common stock calculated based on 3,103,021 Public Warrants directly held by FCIP, 143,492 shares of our common stock calculated based on 573,969 Public Warrants directly held by FCIP II, 94,167 shares of our common stock calculated based on 376,667 Public Warrants directly held by FCIP III, 134,524 shares of our common stock calculated based on 538,096 Public Warrants directly held by FCIP V, and 49,325 shares of our common stock calculated based on 197,301 Public Warrants directly held by FCAMI). Farallon Partners, L.L.C. (“FPLLC”), as the general partner of FCP, FCIP, FCIP II, FCIP III, and FCAMI (the “FPLLC Entities”) and the sole member of FCIP V GP (as defined below), may be deemed to beneficially own such shares of our common stock received as part of the PIPE Investment, issued pursuant to the option under the PIPE Investment and Public Warrants received in connection with the PIPE Investment held by or issuable to each of the FPLLC Entities. Farallon Institutional (GP) V, L.L.C. (“FCIP V GP”), as the general partner of FCIP V, may be deemed to beneficially own shares of our common stock received as part of the PIPE Investment, issued pursuant to the option under the PIPE Investment and Public Warrants received in connection with the PIPE Investment held by or issuable to FCIP V. Each of Philip D. Dreyfuss, Michael B. Fisch, Richard B. Fried, David T. Kim, Michael G. Linn, Rajiv A. Patel, Thomas G. Roberts, Jr., William Seybold, Andrew J. M. Spokes, John R. Warren and Mark C. Wehrly (collectively, the “Farallon Managing Members”), as a (i) managing member or senior managing member, as the case may be, of FPLLC or (ii) manager or senior manager, as the case may be, of FCIP V GP, in each case with the power to exercise investment discretion with respect to the shares that may be deemed to be beneficially owned by FPLLC or FCIP V GP, may be deemed to beneficially own such shares of our common stock received as part of the PIPE Investment, issued pursuant to the option under the PIPE Investment and Public Warrants received in connection with the PIPE Investment held by or issuable to the FPLLC Entities or FCIP V. Each of FPLLC, FCIP V GP and the Farallon Managing Members disclaims beneficial ownership of any such shares of our common stock received as part of the PIPE Investment, issued pursuant to the option under the PIPE Investment and Public Warrants received in connection with the PIPE Investment. The address for each of the entities and individuals identified in this footnote is One Maritime Plaza, Suite 2100, San Francisco, California 94111. |

| (12) | Based solely on a Schedule 13G filed with the SEC on February 11, 2020 by Vanguard Group Inc. (“Vanguard Group”). Vanguard Group reported sole voting and dispositive power with respect to 8,851,056 shares of common stock. Vanguard Group’s address is 100 Vanguard Blvd., Malvern, PA 19355. |

| (13) | Based solely on information reported in a Schedule 13G filed with the SEC on November 22, 2019, Multi-Sector Credit, LLC and SCS Capital Management, LLC share voting power and dispositive power over 8,090,231 shares of common stock. The address of Multi-Sector Credit, LLC and SCS Capital Management, LLC is 888 Boylston Street, Suite 1010, Boston, MA 02199. |

| 20 |