Table of Contents

As filed with the Securities and Exchange Commission on July 12, 2021

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

CHARGEPOINT HOLDINGS, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 6770 | 84-1747686 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial 240 East Hacienda Avenue Campbell, CA 95008 (408) 841-4500 |

(I.R.S. Employer Identification No.) |

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Rex Jackson

Chief Financial Officer

240 East Hacienda Avenue

Campbell, CA 95008

Tel: (408) 841-4500

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

| Frank R. Adams, Esq. Weil, Gotshal & Manges LLP 767 Fifth Avenue New York, NY 10153 Tel: (212) 310-8000 |

Rebecca Chavez, General Counsel ChargePoint, Inc. 240 East Hacienda Avenue Campbell, CA 95008 Tel: (408) 841-4500 |

Alan F. Denenberg, Esq. Davis Polk & Wardwell LLP 1600 El Camino Real Menlo Park, CA 94025 Tel: (650) 752-2000 |

Approximate date of commencement of proposed sale to the public:

As soon as practicable after the effective date of this registration statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box: ☐

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |||

| Non-accelerated filer | ☒ | Smaller reporting company | ☒ | |||

| Emerging growth company | ☒ | |||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act ☐

CALCULATION OF REGISTRATION FEE

|

| ||||||||

| Title of Securities to be Registered |

Amount to be Registered(1) |

Proposed Maximum Aggregate Offering Price Per Share |

Proposed Maximum Aggregate Offering Price(1)(2) |

Amount of Registration Fee | ||||

| Common Stock, par value $0.0001 per share |

13,800,000 |

$27.73 | $382,674,000 | $41,749.73 | ||||

|

| ||||||||

|

| ||||||||

| (1) | Includes 1,800,000 shares that the underwriters have the option to purchase. See “Underwriting.” |

| (2) | Estimated solely for the purpose of computing the amount of the registration fee. In accordance with Rule 457(c) under the Securities Act of 1933, as amended, the maximum price per share and maximum aggregate offering price are based on the average of the $28.36 (high) and $27.09 (low) sale price of the registrant’s Common Stock as reported on The New York Stock Exchange on July 8, 2021, which date is within five business days prior to filing this Registration Statement. Estimated solely for purposes of calculating the registration fee in accordance with Rule 457(o) under the Securities Act of 1933, as amended. |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until this registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject To Completion, Dated July 12, 2021

12,000,000 Shares

ChargePoint Holdings, Inc.

Common Stock

The selling securityholders named in this prospectus are offering 12,000,000 shares of our common stock, par value $0.0001 per share (“Common Stock”). We will not receive any proceeds from the sale of the shares by the selling securityholders, but we have agreed to pay certain registration expenses, other than commissions or discounts of underwriters.

Our Common Stock is listed on the New York Stock Exchange (“NYSE”) under the symbol “CHPT.” On July 9, 2021, the last reported sale price of our Common Stock was $27.90 per share.

We are an “emerging growth company” and a “smaller reporting company” under applicable federal securities laws and will be subject to reduced public company reporting requirements.

Investing in our securities involves risks that are described in the “Risk Factors” section beginning on page 12.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of the securities to be issued under this prospectus or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| Per Share | Total | |||||||

| Public offering price |

$ | $ | ||||||

| Underwriting discounts and commissions(1) |

$ | $ | ||||||

| Proceeds, before expenses, to the selling securityholders |

$ | $ | ||||||

| (1) | See the section titled “Underwriting” for a description of the compensation payable to the underwriters. |

The selling securityholders have granted the underwriters an option to purchase up to 1,800,000 additional shares of Common Stock at the public offering price less the underwriting discount for a period of 30 days from the date of this prospectus. The underwriters expect to deliver the shares against payment in New York, New York on , 2021.

| BofA Securities |

Goldman Sachs & Co. LLC | Oppenheimer & Co. | ||

| Morgan Stanley | ||||

Prospectus dated , 2021.

Table of Contents

| ii | ||||

| iii | ||||

| vi | ||||

| 1 | ||||

| 10 | ||||

| 12 | ||||

| 42 | ||||

| 43 | ||||

| Management’s Discussion and Analysis of Financial Condition and Results of Operations |

44 | |||

| 69 | ||||

| 82 | ||||

| 89 | ||||

| 101 | ||||

| 104 | ||||

| 107 | ||||

| 114 | ||||

| Material U.S. Federal Income Tax Considerations for Non-U.S. Holders |

126 | |||

| 130 | ||||

| 139 | ||||

| 139 | ||||

| 140 | ||||

| 140 | ||||

| F-1 |

i

Table of Contents

We have not, nor have any of the selling securityholders or the underwriters, authorized anyone to provide any information or to make any representations other than those contained in this prospectus or in any free writing prospectuses prepared by or on behalf of us or to which we have referred you. None of us, the selling securityholders or the underwriters take responsibility for, or can provide assurance as to the reliability of, any other information that others may give you. This prospectus is an offer to sell only the shares offered hereby, but only under circumstances and in jurisdictions where it is lawful to do so. The information contained in this prospectus or in any applicable free writing prospectus is current only as of its date, regardless of its time of delivery or any sale of shares of our Common Stock. Our business, financial condition, results of operations and prospects may have changed since that date.

For investors outside the United States: We have not, nor have any of the selling securityholders or the underwriters done anything that would permit this offering or possession or distribution of this prospectus or any free writing prospectus we may provide to you in connection with this offering in any jurisdiction where action for that purpose is required, other than in the United States. You are required to inform yourselves about and to observe any restrictions relating to this offering and the distribution of this prospectus and any such free writing prospectus outside the United States.

ii

Table of Contents

Unless otherwise stated or unless the context otherwise requires, the terms “we,” “us,” “our,” “Company” and “ChargePoint” refer to ChargePoint Holdings, Inc., a Delaware corporation:

| • | “Board” or “Board of Directors” means the board of directors of ChargePoint. |

| • | “ChargePoint” means ChargePoint Holdings, Inc., a Delaware corporation. |

| • | “Code” means the Internal Revenue Code of 1986, as amended. |

| • | “Common Stock” means the shares of our common stock, par value $0.0001 per share. |

| • | “DGCL” means the General Corporation Law of the State of Delaware. |

| • | “ESPP” means the ChargePoint Holdings, Inc. 2021 Employee Stock Purchase Plan. |

| • | “Exchange Act” means the Securities Exchange Act of 1934, as amended. |

| • | “Founder Shares” means 6,868,235 shares of Common Stock that currently are owned by the Initial Stockholders. The Founder Shares were shares of Class B Common Stock, par value $0.0001 per share, of Switchback that automatically converted into shares of Common Stock upon the closing of the Merger. |

| • | “Founders Stock Letter” means the stock letter the Sponsor and Initial Stockholders entered into with Switchback in connection with the execution of the Merger Agreement. |

| • | “Initial Stockholders” means the Sponsor together with Joseph Armes, Zane Arrott and Ray Kubis. |

| • | “IPO” means Switchback’s initial public offering, consummated on July 30, 2019, of 31,411,763 units (including 1,411,763 units that were subsequently issued to the underwriters in connection with their partial exercise of their overallotment option) at $10.00 per unit. |

| • | “leader,” “leading,” “industry leadership,” “industry leading,” and other similar statements included in this prospectus regarding ChargePoint and its services are based on ChargePoint’s beliefs regarding its market position in its sector. ChargePoint bases its beliefs regarding these matters, including its estimates of its market share in its sector, on its collective institutional knowledge and expertise regarding its industries, markets and technology, requests for proposal which are based on, among other things, publicly available information, reports of government agencies, and the results of contract bids and awards, and industry research firms, as well as ChargePoint’s internal research, calculations and assumptions based on its analysis of such information and data. ChargePoint believes these assertions to be reasonable and accurate as of the date of this prospectus. |

| • | “JOBS Act” means the Jumpstart Our Business Startups Act of 2012. |

| • | “Legacy ChargePoint” means ChargePoint, Inc., a Delaware corporation. |

| • | “Legacy ChargePoint Common Stock” means the Common Stock, par value $0.0001 per share, of Legacy ChargePoint. |

| • | “Legacy ChargePoint Options” means all incentive stock options or nonqualified stock options to purchase outstanding shares of Legacy ChargePoint Common Stock, whether or not exercisable and whether or not vested, under the Legacy ChargePoint Stock Plans. |

| • | “Legacy ChargePoint Preferred Stock” means the preferred stock, par value $0.0001 per share, of Legacy ChargePoint. |

| • | “Legacy ChargePoint Stock Plans” means Legacy ChargePoint’s 2007 Stock Incentive Plan and Legacy ChargePoint’s 2017 Stock Plan, in each case, as such may have been amended, supplemented or modified from time to time. |

iii

Table of Contents

| • | “Legacy ChargePoint Restricted Stock” means the unvested restricted shares of Legacy ChargePoint Common Stock granted pursuant to the Legacy ChargePoint Stock Plans upon the “early exercise” of Legacy ChargePoint Options. |

| • | “Legacy ChargePoint Warrants” means warrants issued by Legacy ChargePoint that were converted into warrants of ChargePoint in the Merger. |

| • | “Merger” means the transactions described in the Merger Agreement. |

| • | “Merger Agreement” means that certain Merger Agreement and Plan of Reorganization, dated as of September 23, 2020, by and among Switchback, Merger Sub and Legacy ChargePoint. |

| • | “Merger Sub” means Lightning Merger Sub Inc., a Delaware corporation and a wholly owned subsidiary of Switchback. |

| • | “Non-Reliance Periods” mean those financial statements which ChargePoint’s audit committee concluded on May 4, 2021 could no longer be relied upon, based on the following facts: (i) the audited consolidated financial statements of Switchback as of December 31, 2020 and 2019, for the year ended December 31, 2020 and for the period from May 10, 2019 (inception) through December 31, 2019 included in the Original Filing, (ii) certain items on the Company’s previously issued audited balance sheet dated as of July 30, 2019, which was included in the Company’s Current Report on Form 8-K filed with the SEC on August 5, 2019 (the “IPO Closing 8-K”), and (iii) the condensed consolidated unaudited financial statements of Switchback included in Switchback’s Quarterly Reports on Form 10-Q for (a) the three months ended September 30, 2019 and for the period from May 10, 2019 (inception) through September 30, 2019 (b) the three months ended March 31, 2020, (c) the three and six months ended June 30, 2020, and (d) the three and nine months ended September 30, 2020. |

| • | “NYSE” means the New York Stock Exchange. |

| • | “public shares” means shares of Common Stock included in the public units. |

| • | “public stockholders” means holders of public shares, including the Initial Stockholders to the extent the Initial Stockholders hold public shares; provided, that the Initial Stockholders are considered “public stockholders” only with respect to any public shares held by them. |

| • | “public units” means the units sold in the IPO, consisting of one share of Common Stock and one-third of one Public Warrant. |

| • | “Public Warrants” means the warrants sold as part of the public units in the IPO (whether they were purchased in the IPO or thereafter in the open market). |

| • | “Private Warrants” means the warrants issued to the Sponsor in a private placement simultaneously with the closing of our IPO. |

| • | “Registration Rights Holders” refers to the undersigned parties listed under Holder on the signature page of the Registration Rights Agreement. |

| • | “Sarbanes-Oxley” means the Sarbanes-Oxley Act of 2002. |

| • | “SEC” means the U.S. Securities and Exchange Commission. |

| • | “Second A&R Bylaws” means our second amended and restated bylaws, dated February 26, 2021. |

| • | “Second A&R Charter” means our second amended and restated certificate of incorporation, dated February 26, 2021. |

| • | “Securities Act” means the Securities Act of 1933, as amended. |

| • | “selling securityholders” means those identified as the selling securityholders in the “Selling Securityholders” section. |

| • | “Sponsor” means NGP Switchback, LLC, a Delaware limited liability company. |

iv

Table of Contents

| • | “Switchback” means Switchback Energy Acquisition Corporation, a Delaware corporation, prior to the completion of the Merger. |

| • | “Transfer Agent” means Continental Stock Transfer & Trust Company. |

| • | “Triggering Events” means any time period between the Closing and the five-year anniversary of the Closing Date when eligible former equity holders may receive the Earnout Shares in three equal tranches if the volume-weighted average closing sale price of ChargePoint’s Common Stock is greater than or equal to $15.00, $20.00 and $30.00 for any 10 trading days within any 20 consecutive trading day period. |

| • | “U.S. GAAP” means U.S. generally accepted accounting principles. |

| • | “Warrants” means the Public Warrants, Private Warrants and Legacy ChargePoint Warrants. |

v

Table of Contents

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

The Company makes forward-looking statements within the meaning of Section 27A of the Securities Act and Section 21E of the Exchange Act in this prospectus. All statements, other than statements of present or historical fact included in this prospectus, regarding the Company’s future financial performance, as well as the Company’s strategy, future operations, future operating results, financial position, estimated revenues, and losses, projected costs, prospects, plans and objectives of management are forward-looking statements. In some cases, you can identify forward-looking statements by terminology such as “may,” “should,” “could,” “would,” “expect,” “plan,” “anticipate,” “intend,” “believe,” “estimate,” “continue,” “project” or the negative of such terms and other similar expressions that predict or indicate future events or trends or that are not statements of historical matters. These statements are based on various assumptions, whether or not identified herein, and on the current expectations of the Company’s management and are not predictions of actual performance. These forward-looking statements are provided for illustrative purposes only and are not intended to serve as, and must not be relied on by any investor as a guarantee, an assurance, a prediction or a definitive statement of, fact or probability. Actual events and circumstances are difficult or impossible to predict and may differ from assumptions, and such differences may be material. Many actual events and circumstances are beyond the control of the Company. These forward-looking statements are subject to known and unknown risks, uncertainties and assumptions about the Company that may cause the actual results, level of activity, performance or achievements to be materially different from any future results, levels of activity, performance or achievements expressed or implied by such forward-looking statements. If any of these risks materialize or the Company’s assumptions prove incorrect, actual results could differ materially from the results implied by these forward-looking statements. There may be additional risks that the Company does not presently know or that the Company currently believes are immaterial that could also cause actual results to differ from those contained in the forward-looking statements. In addition, forward-looking statements reflect the Company’s expectations, plans or forecasts of future events and views as of the date hereof. The Company anticipates that subsequent events and developments will cause the Company’s assessments to change. However, while the Company may elect to update these forward-looking statements at some point in the future, except as otherwise required by applicable law, the Company specifically disclaims any duty to update any forward-looking statements, all of which are expressly qualified by the statements in this section, to reflect events or circumstances after the date of this prospectus. These forward-looking statements should not be relied upon as representing the Company’s assessments as of any date subsequent to the date hereof. Accordingly, undue reliance should not be placed upon the forward-looking statements. The Company cautions you that these forward-looking statements are subject to numerous risk and uncertainties, most of which are all difficult to predict and many of which are beyond the control of the Company.

The following factors, among others, could cause actual results to differ materially from forward-looking statements:

| • | ChargePoint’s success in retaining or recruiting, or changes in, its officers, key employees or directors; |

| • | changes in applicable laws or regulations; |

| • | the possibility that the coronavirus (“COVID-19”) pandemic and its effects on the overall economy may adversely affect the results of operations, financial position and cash flows of ChargePoint; |

| • | ChargePoint’s ability to expand its business in Europe; |

| • | the Electric Vehicle (“EV”) market may not continue to grow as expected; |

| • | ChargePoint may not attract a sufficient number of fleet owners as customers; |

| • | incentives from governments or utilities may be reduced, which could reduce demand for EVs; |

| • | the impact of competing technologies that could reduce the demand for EVs; |

| • | technological changes; |

| • | data security breaches or other network outages; |

vi

Table of Contents

| • | ChargePoint’s ability to remediate its material weaknesses in internal control over financial reporting; |

| • | the possibility that ChargePoint may be adversely affected by other economic, business or competitive factors; and |

| • | any further changes to our financial statements that may be required due to SEC comments, including to the Form 10-K/A or Form 10-Q or further guidance regarding the accounting treatment of the Warrants, and the quantitative effects of the restatement of our financial statements. |

The foregoing review of important factors should not be construed as exhaustive and should be read in conjunction with the other risk factors included herein. Forward-looking statements reflect current views about ChargePoint’s plans, strategies and prospects, which are based on information available as of the date of this prospectus. Except to the extent required by applicable law, ChargePoint undertakes no obligation (and expressly disclaims any such obligation) to update or revise the forward-looking statements whether as a result of new information, future events or otherwise.

Forward-looking statements are subject to risks and uncertainties, many of which are outside our control, which could cause actual results to differ materially from these statements. Therefore, you should not place undue reliance on those statements.

vii

Table of Contents

This summary highlights selected information from this prospectus and does not contain all of the information that is important to you in making an investment decision. This summary is qualified in its entirety by the more detailed information included in this prospectus. Before making your investment decision with respect to our securities, you should carefully read this entire prospectus, including the information under “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the financial statements included elsewhere in this prospectus.

Unless otherwise indicated or the context otherwise requires, references in this prospectus to “we,” “our,” “us” and other similar terms refer to ChargePoint.

ChargePoint

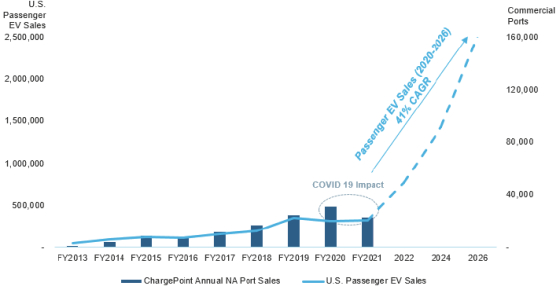

ChargePoint is a leading EV charging network provider committed to enabling the electrification of mobility for all people and goods. Years before EVs were widely available, ChargePoint envisioned a new way of fueling, conveniently located where drivers live, work and play. By pioneering networked EV charging, ChargePoint has helped make electrified mobility a reality with consumers and fleets rapidly adopting EVs. With 13 years of focused development, over 5,000 existing commercial customers and over $1.1 billion of capital raised from a diversified set of high-profile investors from automotive, energy, manufacturing and venture funding, ChargePoint is driving the shift to electric mobility by providing charging solutions in North America and Europe for all segments, including commercial (e.g., retail, workplace, parking, recreation, education and highway fast charge), fleet (e.g., delivery, logistics, motorpool, transit and shared mobility) and residential (e.g., homes, apartments and condos). As of April 30, 2021, over 112,000 ports have been installed and activated on our network of which over 3,500 ports use DC charging. We also provide access to over 175,000 ports through roaming integrations. In addition, we have been focusing on building a sustainable future. Since 2007, we estimate that we have powered 2.9 billion electric miles driven, resulting in 116 million gallons of gasoline and 682,000 metric tons of greenhouse gas emissions avoided as of April 30, 2021. The avoided amount of greenhouse gas emissions equate to planting 11.3 million tree seedlings, capturing carbon from 836,000 acres of U.S. forests and recycling 29 million bags of waste, according to the United States Environmental Protection Agency’s Greenhouse Gas Equivalencies Calculator.

Major auto manufacturers have committed to electrification and large battery EVs are winning the day across vehicle categories. ChargePoint’s networked solutions can charge EV passenger cars or fleet vehicles regardless of manufacturer. ChargePoint believes it should benefit from the broader electrification trend without needing to identify which vehicle brands, traditional or more recent “born electric” entrants, will be successful. ChargePoint believes it will continue to grow proportionally to EV market growth due to the fact that for almost a decade ChargePoint’s charging port (electrified parking space) growth in North America has correlated closely with new passenger EV sales in North America. Passenger EV sales are expected to increase from 2.7% of new vehicles sold in 2019 to 43.1% in 2030 in the United States and Europe according to the Bloomberg New Energy Finance Electric Vehicle Outlook 2021 (the “BNEF Report”). Additional factors propelling this shift to electrification include proposed fossil fuel bans or restrictions, transit electrification mandates and utility incentive programs. Accordingly, the BNEF Report projects that the cumulative EV charging infrastructure investment in North America and Europe is expected to be approximately $121 billion by 2030 and increase to approximately $307 billion by 2040.

The mailing address of ChargePoint’s principal executive office is 240 East Hacienda Avenue, Campbell, CA 95008, and its telephone number is (408)-841-4500.

The ChargePoint Model for EV Fueling

Because vehicles spend most of their time parked and electricity is pervasively and safely distributed, fueling can shift to a model where vehicles charge while their drivers are doing something else and the locations

1

Table of Contents

where the vehicle is parked will offer fueling with charging speeds matched to the natural parking duration of vehicles at the site. With the exception of occasional drives beyond a vehicle’s battery range, EV charging is primarily a top-up model and fueling is transitioning from being a chore commonly performed by having to make a dedicated stop to being conveniently located where drivers live, work and play. ChargePoint offers a platform of products, cloud software subscriptions, support, warranty coverage and professional services enabling turn-key development of charging at any location.

ChargePoint’s founders understood that the widespread adoption of electric mobility required a more sustainable, efficient and convenient fueling infrastructure. Fueling with electricity is expected to be less expensive, more sustainable and more convenient than traditional liquid fueling. Further, EV charging does not present all of the same environmental risks of liquid fueling, as it does not involve the storage and potential release of hydrocarbons at the fueling site. ChargePoint believes the development and expanding capacity of renewable energy sources, including wind and solar, can play an increasing and complementary role in electric mobility as the world becomes more electrified and continues to shift to clean energy.

ChargePoint is tackling this growing addressable market one parking lot at a time with a business model it believes is unique in the industry in that it (a) encourages businesses and fleets to directly invest in charging infrastructure, therefore crowdsourcing the buildout of charging infrastructure, (b) is designed to deliver consistent revenue aligned closely to EV sales growth and (c) provides a quality experience for businesses and drivers that yields significant network effects. ChargePoint sells charging solutions in the form of networked hardware and recurring software subscriptions and services primarily sold to commercial and fleet customers. With rare exceptions, ChargePoint does not own charging sites or stations, monetize driver access to stations or monetize the sale of energy. In other words, ChargePoint does not depend on utilization rates and site selections; hence, ChargePoint believes there is limited direct competition with other charging players such as EVgo Services LLC (“Evgo”), Electrify America, Volta and Blink Charging Co. (“Blink”) in the United States. Because customers own the charging infrastructure, ChargePoint can focus its resources on product development, customer acquisition and public policy to drive innovation, competition and customer choice in the market.

For 13 years, ChargePoint has been optimizing its operating model, combining high quality charging hardware and software subscriptions with turn-key support and parts and labor warranty services that are among the most comprehensive on the market. ChargePoint believes this approach is unique in the industry, creates significant network effects and, when combined with ChargePoint’s first mover advantage, provides the potential for recurring revenue. ChargePoint’s user experience is designed to generate high driver satisfaction and awareness and to keep site hosts engaged and loyal. This creates a virtuous cycle of brand awareness, recurring software revenue and meaningful charging footprint growth with existing customers (with the opportunity for high land and expand rates), all supported by mass market EV adoption.

The Portfolio

ChargePoint primarily generates revenue through the sale of networked charging hardware, combined with its cloud-based services which enable consumers the ability to locate, reserve, authenticate and transact EV charging sessions (“Cloud” or “Cloud Services”). Cloud Services are billed as an annual subscription. Access to the Cloud Services is available through each charging port. An extended parts and labor warranty (“Assure”) is also offered as an annual subscription. We expect that the revenue contribution for recurring Cloud or Assure sales will equal the revenue contribution from one-time CT4000 Dual-Port Station hardware sales after approximately seven years. ChargePoint offers both an upfront sale of the charging stations with subsequent payment for Cloud Services and Assure or ChargePoint as a Service (“CPaaS”) in which charging station hardware, Cloud Services and Assure are bundled into an annual subscription payment.

Hardware Portfolio Powered by Software. While software is at the center of a scaled EV fueling network, ChargePoint believes it offers among the industry’s best in hardware for both Level 2 Alternating Current (“AC”)

2

Table of Contents

and Level 3 Direct Current (“DC”) Fast charging. It does not sell these solutions without a Cloud Services subscription. The ChargePoint portfolio includes solutions for many use cases and was designed from the ground up with the software in mind.

Advanced Cloud Services to Scale Charging Infrastructure. ChargePoint’s network, sold as a Cloud Services subscription, enables commercial and fleet customers to manage charging in their parking lots and depots. Cloud Services capabilities include the following:

| • | Host pricing and payment remittance capabilities. |

| • | Energy management. |

| • | Driver management tools. |

| • | Integration with route planning systems for fleets. |

ChargePoint believes that as EV penetration rises, so does the importance of Cloud Services to help manage charging complexity. Some examples include:

| • | The ability for commercial customers to adjust the rate at which vehicles charge to match the natural parking duration at the site and to avoid peak or demand charges. |

| • | Charging infrastructure made available to the public during the day can be reserved for private fleets at night. |

| • | Ecosystem integrations enable drivers to access charging functionality via in-vehicle infotainment systems, consumer mobile applications, payment systems, mapping tools, home automation assistants, fleet fuel cards, wearables and residential utility programs. |

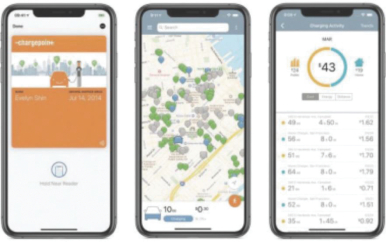

All ChargePoint commercial ports are integrated into one network available to drivers who can use the ChargePoint mobile application to find charging locations, check availability, start sessions, pay for charging, use their ChargePoint account to roam across networks, access preferential pricing and loyalty offers and track the estimated avoidance of CO2 emissions in comparison to the use of liquid fuel, though this does not account for any emissions associated with the generation of the electricity used to charge the EV at the commercial ports.

Parts and Labor Warranty Subscriptions and Customer Support Foster Loyalty. ChargePoint offers Assure services which include proactive monitoring, fast response times, parts and labor warranty, expert advice and robust reporting. ChargePoint also provides phone support in nine languages to both site hosts and drivers. Rising EV adoption creates more awareness and utilization. ChargePoint believes the quality of the ChargePoint experience generates driver satisfaction and therefore encourages customers to purchase additional networked chargers and software, creating a virtuous cycle of growth from customers expanding their charging capacity.

Go to Market Strategy

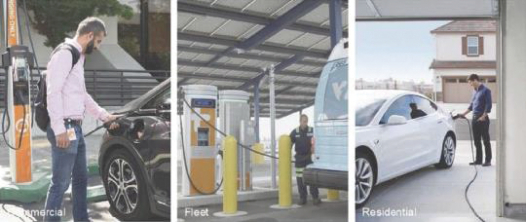

ChargePoint sells networked charging solutions in North America and Europe and has over 5,000 existing commercial customers including 72% of the 2021 Fortune 50 companies. It is focused on three key markets: commercial, fleet and residential.

| • | Commercial: Commercial businesses already own or lease parking and many wish to electrify some or all of these parking spaces. ChargePoint believes commercial businesses view charging as essential and invest to attract tenants, employees, customers and visitors, generate direct and indirect income, reduce expenses and achieve sustainability goals. ChargePoint believes commercial businesses choose ChargePoint based on solution completeness (they are not responsible for being the integrator or support agent for drivers) and the quality that comes from designing hardware, software and services |

3

Table of Contents

| together. Customers benefit from drivers typically being familiar with ChargePoint including access to a free, top-rated application, around-the-clock support, integration to popular mapping platforms, payment systems and wearables. Brand awareness, education and demand marketing programs generate sales opportunities. The commercial market is accessed via a direct sales force (inside and field teams) and by channel partners. |

| • | Fleet: Fleet customers are organizations that operate vehicle fleets in delivery/logistics, sales/service, motorpool shared transit and ridesharing service operators. ChargePoint believes these customers choose to electrify their fleets for economic reasons, as the comparative total cost of ownership compellingly favors electrification. EV charging solutions can help them design and fuel operations, manage operating costs and achieve sustainability goals. ChargePoint provides a flexible architecture of networked charging stations, software subscriptions, professional services, support, monitoring and parts and labor warranties needed to run electrified depots at scale. The fleet market is accessed via a direct sales force and a curated set of channel partners. |

| • | Residential: ChargePoint offers residential EV charging solutions for drivers in single family residences who want the convenience of fueling at home with the ability to optimize energy costs and full integration with the same mobile application they use for charging away from home. Residential charging solutions include the capability to manage grid load in conjunction with utility programs and EV fueling rate programs. Single family residential opportunities are accessed by direct marketing to the consumer using proprietary and third-party e-commerce platforms. For apartments and condominium settings, ChargePoint offers landlords and owner associations the ability to offer charging billed directly to the tenant. ChargePoint also offers customer support around-the-clock and in nine languages. This residential aspect is accessed via marketing and direct and channel partners. |

With its capital light business model, ChargePoint is able to allocate its capital strategically in research and development, marketing and sales and public policy.

| • | Research and Development. With a singular focus on EV charging for 13 years, ChargePoint now offers a complete set of solutions for most EV charging use cases in North America and Europe. |

| • | Go to Market. ChargePoint has built a global marketing and sales engine, with an established sales channel, digital marketing capability and substantial direct sales. ChargePoint has focused on category awareness, consistent branding and customer acquisition. ChargePoint also has nationwide and local partners who sell, install and maintain ChargePoint solutions. |

| • | Public Policy. ChargePoint has also supported early and sustained investments in policy and utility relationships. ChargePoint advocates for policies that advance electric mobility and ensure a healthy industry with a focus on competition, innovation and customer choice, including: |

| • | Support for vehicle policy and climate action, such as zero emission vehicle requirements, fossil fuel bans and transit electrification directives; |

| • | Partnership with North America’s leading utilities to scale the new electric fueling network, including enabling the resale of electricity, securing fast charging-friendly tariffs, protecting site host choice, developing make-ready programs, creating rebate programs and informing utility commission decisions and legislation; and |

| • | Reduction in barriers to infrastructure deployment including construction costs, permitting, building codes and right to charge policies for renters and tenants. |

ChargePoint operates in all segments of EV charging stations in North America and Europe, and offers a broad set of solutions for EV applications, including home, multi-family, residential, hospitality, workplace, commercial, fast-charging and fleet. ChargePoint does not compete with charging asset owners and operators and

4

Table of Contents

in many cases the asset owners and operators are our actual or potential customers. In addition, ChargePoint does not directly compete with charging asset owners or charging networks that monetize the driver. Rather, it makes solutions available to them for purchase as a platform to enable their services.

Growth Strategies

ChargePoint estimates it had over a 70% market share in publicly available networked Level 2 AC charging in North America as of April 30, 2021. ChargePoint began European operations in late 2017 and currently operates in 16 European countries. It expects significant market opportunities for fleet solutions as fleet EVs begin to arrive in more meaningful volume in coming years. ChargePoint believes that the breadth and quality of its networked EV charging solutions, market share and driver awareness typically leads to customer loyalty, whereby they typically choose to expand their charging footprint with ChargePoint as EV penetration rises and/or charging utilization at their location increases. Over the years, ChargePoint’s customers typically renew their cloud subscriptions and expand the number of charging ports they purchase from ChargePoint. Additional growth results from the breadth of ecosystem integrations ChargePoint has enabled that keep the brand top of mind with drivers, including in-vehicle infotainment systems, consumer mobile applications, payment systems, mapping tools, home automation assistants, fleet fuel cards, wearables and residential utility programs.

ChargePoint’s growth strategies to continue to scale networked EV charging are as follows:

| • | Accelerate new product offerings. ChargePoint intends to maintain its leadership position with continued efficient investment in product development. |

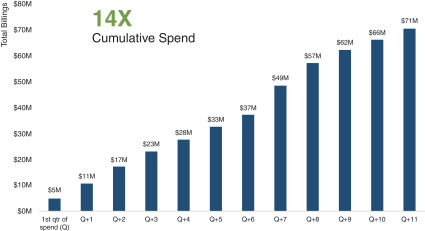

| • | Invest incrementally in marketing and sales. In both North America and Europe, ChargePoint intends to continue to attract new customers and pursue a “land-and-expand” model which encourages existing customers to increase their charging footprint over time as EV penetration increases. ChargePoint will also fund more CPaaS opportunities for commercial and fleet customers. Our “land-and-expand” approach resulted in our top 25 customers to increase their quarterly spending 14x over their first 12 quarters from the initial sale. One Fortune 50 customer’s spend of $2.6 million during fiscal year 2017 was followed by a total cumulative spend of $12.6 million during the five year period through 2021. Another Fortune 50 company’s spend increased from $334,000 in fiscal year 2017 to a cumulative $6.6 million over the five year period from fiscal 2017 to 2021. One major U.S. city’s spend increased from $76,000 in fiscal year 2017 to a cumulative $5.3 million over the five year period from fiscal 2017 to 2021. |

| • | Pursue strategic acquisitions. ChargePoint will continue to explore potential high-quality acquisition opportunities. |

The Merger and Recent Developments

On February 26, 2021 (the “Closing Date”), ChargePoint consummated the previously announced Merger pursuant to the Merger Agreement. As a result of the Merger, Legacy ChargePoint became a wholly-owned subsidiary of the Company.

Pursuant to the terms of the Merger Agreement, each stockholder of Legacy ChargePoint received 0.9966 shares of Common Stock and the contingent right to receive certain Earnout Shares (as defined below), for each share of Legacy ChargePoint Common Stock, par value $0.0001 per share, owned by such Legacy ChargePoint stockholder that was outstanding immediately prior to the closing of the Merger (other than any shares of Legacy ChargePoint Restricted Stock). In addition, certain investors purchased an aggregate of 22,500,000 shares of Common Stock (such investors, the “PIPE Investors”) concurrently with the closing of the Merger for an aggregate purchase price of $225 million. Additionally, at the closing of the Merger, after giving effect to the forfeiture contemplated by the Founders Stock Letter, each outstanding Founder Share was converted into a share of Common Stock on a one-for-one basis and the Founder Shares ceased to exist.

5

Table of Contents

Also at the closing of the Merger, the Sponsor exercised its right to convert a portion of the working capital loans made by the Sponsor to ChargePoint into an additional 1,000,000 Private Warrants at a price of $1.50 per warrant in satisfaction of $1.5 million principal amount of such loans.

In addition, pursuant to the terms of the Merger Agreement, at the effective time of the Merger (the “Effective Time”), (1) warrants to purchase shares of capital stock of Legacy ChargePoint were converted into warrants to purchase an aggregate of 38,761,031 shares of Common Stock and the contingent right to receive certain Earnout Shares, (2) options to purchase shares of Common Stock of Legacy ChargePoint were converted into options to purchase an aggregate of 30,135,695 shares of Common Stock and, with respect to vested options, the contingent right to receive certain Earnout Shares and (3) unvested shares of Legacy ChargePoint Restricted Stock that were outstanding pursuant to the “early exercise” of Legacy ChargePoint Options were converted into an aggregate of 345,689 restricted shares of ChargePoint Common Stock.

During the time period between the Closing Date and the five-year anniversary of the Closing Date, eligible former equityholders of Legacy ChargePoint could receive up to 27,000,000 additional shares of Common Stock (the “Earnout Shares”) in the aggregate in three equal tranches if certain earnout conditions (as further described in the Merger Agreement) are fully satisfied. The first two Triggering Events for up to 18,000,000 of the Earnout Shares occurred on March 12, 2021 and, after the withholding of some of these Earnout Shares for tax withholding, 17,539,657 Earnout Shares were issued on March 19, 2021. The third Triggering Event occurred on June 29, 2021 and, after the withholding of some of these Earnout Shares for tax withholding, 8,773,596 Earnout Shares were issued on July 1, 2021.

On July 6, 2021, ChargePoint redeemed all of its remaining outstanding Public Warrants that had not been exercised as of that date following our issuance of a notice of redemption on June 4, 2021, which resulted in the exercise of 3,517,192 warrants for proceeds to us of $40,447,708 and the redemption of 244,481 Public Warrants at a redemption price of $0.01 per warrant. The Private Warrants were not subject to redemption and, to the extent not exercised, remain outstanding and exercisable through February 26, 2026 or until terminated pursuant to the warrant agreement. As of July 9, 2021, we had no Public Warrants outstanding; Private Warrants were exercisable for 2,173,856 shares of our Common Stock at an exercise price of $11.50 per share outstanding, and Legacy ChargePoint Warrants were exercisable for 37,075,846 shares of our Common Stock with a weighted average exercise price of $7.00 per share outstanding.

Risk Factors

Investing in our securities involves risks. You should carefully consider the risks described in “Risk Factors” beginning on page 12 before making a decision to invest in our Common Stock. If any of these risks actually occurs, our business, financial condition and results of operations would likely be materially adversely affected. In such case, the trading price of our securities would likely decline, and you may lose all or part of your investment. Set forth below is a summary of some of the principal risks we face:

| • | ChargePoint is an early stage company with a history of losses, and expects to incur significant expenses and continuing losses for the near term. |

| • | ChargePoint has experienced rapid growth and expects to invest in growth for the foreseeable future. If it fails to manage growth effectively, its business, operating results and financial condition could be adversely affected. |

| • | ChargePoint currently faces competition from a number of companies, particularly in Europe, and expects to face significant competition in the future as the market for EV charging develops. |

| • | Failure to effectively expand ChargePoint’s sales and marketing capabilities could harm its ability to increase its customer base and achieve broader market acceptance of its solutions. |

6

Table of Contents

| • | ChargePoint faces risks related to health pandemics, including the COVID-19 pandemic, which could materially and adversely affect its business and results of operations. |

| • | ChargePoint relies on a limited number of suppliers and manufacturers for its charging stations. A loss of any of these partners could negatively affect its business. |

| • | ChargePoint’s business is subject to risks associated with construction, cost overruns and delays, and other contingencies that may arise in the course of completing installations, and such risks may increase in the future as ChargePoint expands the scope of such services with other parties. |

| • | Future acquisitions or strategic investments could be difficult to identify and integrate, divert the attention of key management personnel, disrupt ChargePoint’s business, dilute stockholder value and adversely affect its results of operations and financial condition. |

| • | If ChargePoint is unable to attract and retain key employees and hire qualified management, technical, engineering and sales personnel, its ability to compete and successfully grow its business would be harmed. |

| • | ChargePoint is expanding operations internationally, which will expose it to additional tax, compliance, market and other risks. |

| • | Some members of ChargePoint’s management have limited experience in operating a public company. |

| • | ChargePoint may need to raise additional funds and these funds may not be available when needed. |

| • | ChargePoint’s future revenue growth will depend in significant part on its ability to increase sales of its products and services to fleet operators. |

| • | Computer malware, viruses, ransomware, hacking, phishing attacks and similar disruptions could result in security and privacy breaches and interruption in service, which could harm ChargePoint’s business. |

| • | ChargePoint’s headquarters and other facilities are located in an active earthquake zone; an earthquake or other types of natural disasters or resource shortages, including public safety power shut-offs that have occurred and will continue to occur in California, could disrupt and harm its operations and those of ChargePoint’s customers. |

| • | Seasonality may cause fluctuations in ChargePoint’s revenue. |

| • | ChargePoint’s future growth and success is highly correlated with and thus dependent upon the continuing rapid adoption of EVs for passenger and fleet applications. |

| • | The EV market currently benefits from the availability of rebates, tax credits and other financial incentives from governments, utilities and others to offset the purchase or operating cost of EVs and EV charging stations. |

| • | ChargePoint’s business may be adversely affected if it is unable to protect its technology and intellectual property from unauthorized use by third-parties. |

| • | Some of ChargePoint’s products contain open-source software, which may pose particular risks to its proprietary software, products and services in a manner that could harm its business. |

| • | If ChargePoint is unable to remediate the material weaknesses in its internal control over financial reporting, or if ChargePoint identifies additional material weaknesses in the future or otherwise fails to maintain the effective system of internal control over financial reporting, this may result in material misstatements of ChargePoint’s consolidated financial statements or failure to meet its periodic reporting obligations. |

| • | Concentration of ownership among ChargePoint’s existing executive officers, directors and their affiliates may prevent new investors from influencing significant corporate decisions. |

7

Table of Contents

| • | ChargePoint has never paid cash dividends on its capital stock, and does not anticipate paying dividends in the foreseeable future. |

| • | The price of ChargePoint’s Common Stock may be subject to wide fluctuations. |

| • | The coverage of ChargePoint’s business or its securities by securities or industry analysts or the absence thereof could adversely affect the trading price and volume of ChargePoint’s Common Stock, Warrants and other securities. |

| • | Sales of a substantial number of shares of Common Stock by ChargePoint’s existing stockholders could cause the price of the Common Stock to decline. |

| • | ChargePoint’s Warrants are being accounted for as a warrant liability and are being recorded at fair value upon issuance with changes in fair value each period reported in earnings, which may have an adverse effect on the market price of its Common Stock. |

Implications of Being an Emerging Growth Company and Smaller Reporting Company

As a company with less than $1.07 billion in revenue during our last fiscal year, we qualify as an “emerging growth company” as defined in the JOBS Act. An emerging growth company may take advantage of reduced reporting requirements that are not otherwise applicable to public companies. These provisions include, but are not limited to:

| • | being permitted to present only two years of audited financial statements and only two years of related Management’s Discussion and Analysis of Financial Condition and Results of Operations; |

| • | not being required to comply with the auditor attestation requirements on the effectiveness of our internal control over financial reporting; |

| • | not being required to comply with any requirement that may be adopted by the Public Company Accounting Oversight Board regarding mandatory audit firm rotation or a supplement to the auditor’s report providing additional information about the audit and the financial statements (auditor discussion and analysis); |

| • | reduced disclosure obligations regarding executive compensation arrangements; and |

| • | exemptions from the requirements of holding a nonbinding advisory vote on executive compensation and stockholder approval of any golden parachute payments not previously approved. |

We may use these provisions until the last day of our fiscal year following the fifth anniversary of our initial public offering. However, if certain events occur prior to the end of such five-year period, including if we become a “large accelerated filer,” our annual gross revenues exceed $1.07 billion or we issue more than $1.0 billion of non-convertible debt in any three-year period, we will cease to be an emerging growth company prior to the end of such five-year period.

We have elected to take advantage of certain of the reduced disclosure obligations in the registration statement of which this prospectus is a part and may elect to take advantage of other reduced reporting requirements in future filings. As a result, the information that we provide to our stockholders may be different than you might receive from other public reporting companies in which you hold equity interests.

The JOBS Act provides that an emerging growth company can take advantage of an extended transition period for complying with new or revised accounting standards, until those standards apply to private companies. We have elected to take advantage of the benefits of this extended transition period and, therefore, we are not subject to the same new or revised accounting standards as other public companies that are not emerging growth companies; however, we may adopt certain new or revised accounting standards early. Our financial statements may therefore not be comparable to those of companies that comply with such new or revised accounting standards during the period in which we remain an emerging growth company. It is possible that some investors

8

Table of Contents

will find our Common Stock less attractive as a result, which may result in a less active trading market for our Common Stock and higher volatility in our stock price.

We are also a “smaller reporting company,” and we will continue to be a “smaller reporting company” if either (i) the market value of our stock held by non-affiliates is less than $250.0 million as of the last business day of our second fiscal quarter or (ii) our annual revenue is less than $100.0 million during the most recently completed fiscal year and the market value of our stock held by non-affiliates is less than $700.0 million as of the last business day of our second fiscal quarter. If we are a smaller reporting company at the time we cease to be an emerging growth company, we may continue to rely on exemptions from certain disclosure requirements that are available to smaller reporting companies. Specifically, as a smaller reporting company, we may choose to present only the two most recent fiscal years of audited financial statements and only two years of management’s discussion and analysis of financial condition and results of operations disclosures and, similar to emerging growth companies, smaller reporting companies have reduced disclosure obligations regarding executive compensation.

9

Table of Contents

| Common Stock to be offered by the selling securityholders |

12,000,000 shares |

| Option to purchase additional shares |

The underwriters have a 30-day option to purchase up to 1,800,000 additional shares of Common Stock from the selling securityholders. |

| Use of proceeds |

The selling securityholders will receive all of the net proceeds from the sale of Common Stock to be sold in this offering, and we will not receive any proceeds. See the sections entitled “Use of Proceeds,” “Selling Securityholders” and “Underwriting.” We will be paying certain costs associated with the sale of shares by the selling securityholders, other than underwriting discounts and commissions. |

| Risk Factors |

You should read the section of this prospectus titled “Risk Factors” and other information included in this prospectus for a discussion of factors you should carefully consider before investing in our Common Stock. |

| NYSE symbol |

“CHPT” |

As of April 30, 2021, we had 305,073,200 shares of Common Stock outstanding, and after giving effect to (i) 8,773,596 shares of our Common Stock issued as Earnout Shares related to the occurrence of the third Triggering Event, net of 226,397 shares withheld in connection with the related tax withholdings obligation and (ii) 3,517,192 shares of our Common Stock issued in connection with the exercise of Public Warrants that were outstanding on April 30, 2021 following our notice of redemption of the Public Warrants issued on June 4, 2021, we would have had 317,363,988 shares of Common Stock outstanding on a pro forma basis. The exercise of Public Warrants which were outstanding as of April 30, 2021 at an exercise price of $11.50 per share resulted in proceeds to us of $40,447,708. On July 6, 2021 we redeemed all remaining Public Warrants that had not been exercised as of that date at a redemption price of $0.01 per warrant.

The number of shares of our Common Stock to be outstanding after this offering excludes:

| • | 37,663,726 shares of our Common Stock issuable upon exercise of the Legacy ChargePoint Warrants as of April 30, 2021 with a weighted-average exercise price of $6.91 per share; |

| • | 2,173,856 shares of our Common Stock issuable upon exercise of outstanding Private Warrants as of April 30, 2021 at an exercise price of $11.50 per share; |

| • | 29,795,964 shares of our Common Stock issuable upon the exercise of stock options outstanding as of April 30, 2021 with a weighted-average exercise price of $0.67 per share; |

| • | 41,429,526 shares of our Common Stock reserved for future issuance under our 2021 Equity Incentive Plan as of April 30, 2021, plus (i) up to 39,000,000 shares subject to awards that are outstanding under our Predecessor Plans and that are subsequently forfeited, expire or lapse unexercised or unsettled or are reacquired by ChargePoint, plus (ii) the annual increase in shares described below; and |

| • | 8,177,683 shares of our Common Stock that may be issued under the ESPP as of April 30, 2021, plus the annual increase in shares that may be issued under the ESPP described below. |

2021 Equity Incentive Plan annual increase. On the first day of each March during the term of the 2021 Equity Incentive Plan, beginning on March 1, 2021 and ending on (and including) March 1, 2030, the number of shares of Common Stock that may be issued under the 2021 Equity Incentive Plan will increase by a number of

10

Table of Contents

shares equal to the lesser of (a) 5% of the outstanding shares on the last day of the immediately preceding month or (b) such lesser number of shares (including zero) that the 2021 Plan Administrator (as defined below), determines for purposes of the annual increase for that fiscal year. On March 1, 2021, the number of shares of Common Stock that may be issued under the 2021 Equity Incentive Plan increased by 13,888,417 shares (which shares are included in the reserved shares described in the bullet above).

2021 Employee Stock Purchase Plan. On the first day of each March during the term of the ESPP, beginning on March 1, 2021 and ending on (and including) March 1, 2040, the number of shares of Common Stock that may be issued under the ESPP will increase by a number of shares equal to the least of (a) 1% of the outstanding shares on the last day of the immediately preceding month, (b) 5,400,000 shares or (c) such lesser number of shares (including zero) that the ESPP Administrator determines for purposes of the annual increase for that fiscal year. On March 1, 2021, the number of shares of Common Stock that may be issued under the ESPP increased by 2,777,683 shares (which shares are included in the shares that may be issued described in the bullet above).

11

Table of Contents

An investment in our securities involves a high degree of risk. You should carefully consider the risks described below before making an investment decision. Our business, prospects, financial condition, or operating results could be harmed by any of these risks, as well as other risks not known to us or that we consider immaterial as of the date of this prospectus. The trading price of our securities could decline due to any of these risks, and, as a result, you may lose all or part of your investment.

Risks Related to ChargePoint’s Business

ChargePoint is an early-stage company with a history of losses, and expects to incur significant expenses and continuing losses for the near term.

ChargePoint incurred a net loss of $197.0 million for the fiscal year ended January 31, 2021 and had net income of $82.3 million for the three months ended April 30, 2021. As of April 30, 2021, ChargePoint had an accumulated deficit of $597.1 million. ChargePoint believes it will continue to incur operating and net losses each quarter for the near term. There can be no assurance that it will be able to maintain profitability in the future. ChargePoint’s potential profitability is particularly dependent upon the continued adoption of EVs by consumers and fleet operators, the widespread adoption of electric trucks and other vehicles and other electric transportation modalities, which may not occur.

ChargePoint has experienced rapid growth and expects to invest in growth for the foreseeable future. If it fails to manage growth effectively, its business, operating results and financial condition could be adversely affected

ChargePoint has experienced rapid growth in recent periods. For example, the number of employees has grown from 743 as of January 31, 2020 to 834 as of January 31, 2021 and to 917 as of April 30, 2021, including 77 employees in Europe as of January 31, 2020 to 101 as of January 31, 2021 and to 133 as of April 30, 2021. The growth and expansion of its business has placed and continues to place a significant strain on management, operations, financial infrastructure and corporate culture. In the event of further growth, ChargePoint’s information technology systems and ChargePoint’s internal control over financial reporting and procedures may not be adequate to support its operations and may introduce opportunities for data security incidents that may interrupt business operations and permit bad actors to obtain unauthorized access to business information or misappropriate funds. ChargePoint may also face risks to the extent such bad actors infiltrate the information technology infrastructure of its contractors.

To manage growth in operations and personnel, ChargePoint will need to continue to improve its operational, financial and management controls and reporting systems and procedures. Failure to manage growth effectively could result in difficulty or delays in attracting new customers, declines in quality or customer satisfaction, increases in costs, difficulties in introducing new products and services or enhancing existing products and services, loss of customers, information security vulnerabilities or other operational difficulties, any of which could adversely affect its business performance and operating results.

ChargePoint currently faces competition from a number of companies, particularly in Europe, and expects to face significant competition in the future as the market for EV charging develops.

The EV charging market is relatively new and competition is still developing. ChargePoint primarily competes with smaller providers of EV charging station networks for installations, particularly in Europe. Large early-stage markets, such as Europe, require early engagement across verticals and customers to gain market share, and ongoing effort to scale channels, installers, teams and processes. Some European customers require solutions not yet available and ChargePoint’s recent entrance into Europe requires establishing itself against existing competitors. In addition, there are multiple competitors in Europe with limited funding, which could cause poor experiences, hampering overall EV adoption or trust in any particular provider.

12

Table of Contents

In addition, there are other means for charging EVs, which could affect the level of demand for onsite charging capabilities at businesses. For example, Tesla Inc. (“Tesla”) continues to build out its supercharger network across the United States for its vehicles, which could reduce overall demand for EV charging at other sites. Also, third-party contractors can provide basic electric charging capabilities to potential customers seeking to have on premise EV charging capability as well as for home charging. In addition, many EV charging manufacturers, including ChargePoint, are offering home charging equipment, which could reduce demand for on premise charging capabilities of potential customers and reduce the demand for onsite charging capabilities if EV owners find charging at home to be sufficient.

Further, ChargePoint’s current or potential competitors may be acquired by third-parties with greater available resources. In addition, certain of ChargePoint’s competitors are engaging in a process similar to the Merger and may have ready access to the capital markets for additional funding. As a result, competitors may be able to respond more quickly and effectively than ChargePoint to new or changing opportunities, technologies, standards or customer requirements and may have the ability to initiate or withstand substantial price competition. In addition, competitors may in the future establish cooperative relationships with vendors of complementary products, technologies or services to increase the availability of their solutions in the marketplace. This competition may also materialize in the form of costly intellectual property disputes or litigation.

New competitors or alliances may emerge in the future that have greater market share, more widely adopted proprietary technologies, greater marketing expertise and greater financial resources, which could put ChargePoint at a competitive disadvantage. Future competitors could also be better positioned to serve certain segments of ChargePoint’s current or future target markets, which could create price pressure. In light of these factors, even if ChargePoint’s offerings are more effective and higher quality than those of its competitors, current or potential customers may accept competitive solutions. If ChargePoint fails to adapt to changing market conditions or continue to compete successfully with current charging providers or new competitors, its growth will be limited which would adversely affect its business and results of operations.

Failure to effectively expand ChargePoint’s sales and marketing capabilities could harm its ability to increase its customer base and achieve broader market acceptance of its solutions.

ChargePoint’s ability to grow its customer base, achieve broader market acceptance, grow revenue, and achieve and sustain profitability will depend, to a significant extent, on its ability to effectively expand its sales and marketing operations and activities. Sales and marketing expenses represent a significant percentage of its total revenue, and its operating results will suffer if sales and marketing expenditures do not contribute significantly to increasing revenue.

ChargePoint is substantially dependent on its direct sales force to obtain new customers. ChargePoint plans to continue to expand its direct sales force both domestically and internationally but it may not be able to recruit and hire a sufficient number of sales personnel, which may adversely affect its ability to expand its sales capabilities. New hires require significant training and time before they achieve full productivity, particularly in new sales territories. Recent hires and planned hires may not become as productive as quickly as anticipated, and ChargePoint may be unable to hire or retain sufficient numbers of qualified individuals. Furthermore, hiring sales personnel in new countries can be costly, complex and time-consuming, and requires additional set up and upfront costs that may be disproportionate to the initial revenue expected from those countries. There is significant competition for direct sales personnel with strong sales skills and technical knowledge. ChargePoint’s ability to achieve significant revenue growth in the future will depend, in large part, on its success in recruiting, training, incentivizing and retaining a sufficient number of qualified direct sales personnel and on such personnel attaining desired productivity levels within a reasonable amount of time. ChargePoint’s business will be harmed if continuing investment in its sales and marketing capabilities does not generate a significant increase in revenue.

13

Table of Contents

ChargePoint faces risks related to health pandemics, including the recent COVID-19 pandemic, which could have a material and adverse effect on its business and results of operations.

The impact of COVID-19, including changes in consumer and business behavior, pandemic fears and market downturns, and restrictions on business and individual activities, has created significant volatility in the global economy and has led to reduced economic activity. The spread of COVID-19 has also created a disruption in the manufacturing, delivery and overall supply chain of vehicle manufacturers and suppliers, and has led to a decrease in EV sales in markets around the world. Any sustained downturn in demand for EVs would harm ChargePoint’s business.

The pandemic has resulted in government authorities implementing numerous measures to try to contain the virus, such as travel bans and restrictions, quarantines, stay-at-home or shelter-in-place orders and business shutdowns. These measures may adversely impact ChargePoint’s employees and operations and the operations of its customers, suppliers, vendors and business partners, and may negatively impact demand for EV charging stations, particularly at workplaces. These measures by government authorities may remain in place for a significant period of time and may adversely affect manufacturing and building plans, sales and marketing activities, business and results of operations.

ChargePoint had initially modified its business practices by recommending that all non-essential personnel work from home and cancelling or reducing physical participation in sales activities, meetings, events and conferences. ChargePoint has also implemented additional safety protocols for essential workers, has implemented cost cutting measures in order to reduce its operating costs, some of which it recently reversed, and may take further actions as may be required by government authorities or that it determines are in the best interests of its employees, customers, suppliers, vendors and business partners. There is no certainty that such actions will be sufficient to mitigate the risks posed by the virus or otherwise be satisfactory to government authorities. If significant portions of ChargePoint’s workforce are unable to work effectively, including due to illness, quarantines, social distancing, government actions or other restrictions in connection with the COVID-19 pandemic, its operations will be negatively impacted. Furthermore, if significant portions of its customers’ or potential customers’ workforces are subject to stay-at-home orders or otherwise have substantial numbers of their employees working remotely for sustained periods of time, user demand for charging stations and services will decline.

The extent to which the COVID-19 pandemic impacts ChargePoint’s business, prospects and results of operations will depend on future developments, which are highly uncertain and cannot be predicted, including, but not limited to, the duration and spread of the pandemic, its severity, the actions to contain the virus or treat its impact, and when and to what extent normal economic and operating activities can resume. The COVID-19 pandemic could limit the ability of customers, suppliers, vendors and business partners to perform, including third-party suppliers’ ability to provide components and materials used in charging stations or in providing installation or maintenance services. Even after the COVID-19 pandemic has subsided, ChargePoint may continue to experience an adverse impact to its business as a result of its global economic impact, including any recession that has occurred or may occur in the future.

Specifically, difficult macroeconomic conditions, such as decreases in per capita income and level of disposable income, increased and prolonged unemployment or a decline in consumer confidence as a result of the COVID-19 pandemic, as well as reduced spending by businesses, could have a material adverse effect on the demand for ChargePoint’s products and services.

ChargePoint relies on a limited number of suppliers and manufacturers for its charging stations. A loss of any of these partners could negatively affect its business.

ChargePoint relies on a limited number of suppliers to manufacture its charging stations, including in some cases only a single supplier for some products and components. This reliance on a limited number of

14

Table of Contents

manufacturers increases ChargePoint’s risks, since it does not currently have proven reliable alternatives or replacement manufacturers beyond these key parties. In the event of interruption, it may not be able to increase capacity from other sources or develop alternate or secondary sources without incurring material additional costs and substantial delays. Thus, ChargePoint’s business could be adversely affected if one or more of its suppliers is impacted by any interruption at a particular location.

If ChargePoint experiences a significant increase in demand for its charging stations, or if it needs to replace an existing supplier, it may not be possible to supplement or replace them on acceptable terms, which may undermine its ability to deliver products to customers in a timely manner. For example, it may take a significant amount of time to identify a manufacturer that has the capability and resources to build charging stations in sufficient volume. Identifying suitable suppliers and manufacturers could be an extensive process that requires ChargePoint to become satisfied with their quality control, technical capabilities, responsiveness and service, financial stability, regulatory compliance, and labor and other ethical practices. Accordingly, a loss of any significant suppliers or manufacturers could have an adverse effect on ChargePoint’s business, financial condition and operating results. In addition, ChargePoint’s suppliers may face supply chain risks and constraints of their own, which may impact the availability and pricing of its products. For example, supply chain challenges related to global chip shortages have impacted companies worldwide both within and outside of ChargePoint’s industry, and may have adverse effects on ChargePoint’s suppliers and, as a result, ChargePoint.

In addition, as a result of the Merger, ChargePoint became subject to requirements under the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 (the “Dodd-Frank Act”) to diligence, disclose, and report whether or not its products contain minerals originating from the Democratic Republic of the Congo and adjoining countries, or conflict minerals. ChargePoint will incur additional costs to comply with these disclosure requirements, including costs related to determining the source of any of the relevant minerals and metals used in ChargePoint’s products. These requirements could adversely affect the sourcing, availability, and pricing of minerals used in the components used in its products. It is also possible that ChargePoint’s reputation may be adversely affected if it determines that certain of its products contain minerals not determined to be conflict-free or if it is unable to alter its products, processes or sources of supply to avoid use of such materials. ChargePoint may also encounter end-customers who require that all of the components of the products be certified as conflict free. If ChargePoint is not able to meet this requirement, such end-customers may choose to purchase products from a different company.