UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 20-F/A

Amendment No. 1

(Mark One)

☐ REGISTRATION STATEMENT PURSUANT

TO SECTION 12(B) OR 12(G)

OF THE SECURITIES EXCHANGE ACT OF 1934

OR

☒ ANNUAL REPORT PURSUANT TO SECTION

13 OR 15(D)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2019

OR

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934

OR

☐ SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934

Commission File Number: 001-39171

BROOGE ENERGY LIMITED

(Exact name of Registrant as specified in its charter)

| Not applicable | Cayman Islands | |

| (Translation of Registrant’s name into English) | (Jurisdiction of incorporation or organization) |

c/o Brooge Petroleum and Gas Investment Company FZE

P.O. Box 50170

Fujairah, United Arab Emirates

+971 9 201 6666

(Address of Principal Executive Offices)

Nicolaas L. Paardenkooper

P.O. Box 50170

Fujairah, United Arab Emirates

+971 9 201 6666

nico.paardenkooper@bpgic.com

(Name, Telephone, Email and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

| Ordinary shares, $0.0001 par value per share | BROG | The Nasdaq Stock Market LLC | ||

| Warrants to purchase ordinary shares | BROGW | The Nasdaq Stock Market LLC |

Securities registered or to be registered pursuant to Section 12(g) of the Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report: 109,587,754 ordinary shares

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. Yes ☐ No ☒

Note – Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or an emerging growth company. See definition of “accelerated filer, large accelerated filer and emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ☐ Accelerated filer ☐ Non-accelerated filer ☒ Emerging growth company ☒

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| US GAAP ☐ | International Financial Reporting Standards as issued by the International Accounting Standards Board ☒ | Other ☐ |

If “Other” has been checked in response to the previous question indicate by check mark which financial statement item the registrant has elected to follow. Item 17 ☐ Item 18 ☐

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

BROOGE ENERGY LIMITED

TABLE OF CONTENTS

-i-

EXPLANATORY NOTE TO AMENDMENT NO. 1

Restatement of Audited Consolidated Financial Statements

On November 16, 2020, the Audit Committee (the “Audit Committee”) of the Board of Directors of Brooge Energy Limited (the “Company”), in consultation with the Company’s management, concluded that the Company’s previously issued audited consolidated financial statements as of and for the period ended December 31, 2019 should no longer be relied upon because the Company has concluded that the warrants issued by it should have been accounted for as a derivative liability rather than equity.

On November 18, 2020, the Company announced that the adjustments required to correct this error would reduce equity by $15,709,460 and increase current liabilities by $15,709,460 after taking into account non-cash income of $1,273,740 related to changes in the estimated fair value of derivative warrant liability. The Company also announced that it would restate its previously issued audited consolidated financial statements as of and for the period ended December 31, 2019.

This amendment (the “Amendment”) to the annual report on Form 20-F of the Company for the fiscal year ended December 31, 2019 filed on June 30, 2020 (the “Original Form 20-F”) is being filed to reflect the following changes:

(i) the inclusion of restated audited consolidated financial statements of the Company as of and for the period ended December 31, 2019, which have been restated to reflect the reclassification as derivative liability of the warrants that were previously classified as equity as more fully described in Note 2.4 to the accompanying consolidated financial statements;

(ii) the update of Note 26 to the accompanying consolidated financial statements to describe certain subsequent events that occurred after the filing of the Original Form 20-F; and

(iii) the amendment of Items 3A “Key information¾Selected Financial Data”, 3D “Key Information¾Risk Factors”, 5 “Operating and Financial Review and Prospects”, 8 “Financial Information”, 10A “Additional Information¾Share capital”, 11 “Quantitative and Qualitative Disclosures About Market Risks”, 15(a) “Controls and Procedures¾Disclosure Controls and Procedures” 18 “Financial Statements” and 19 “Exhibits”, in each case, solely to make appropriate changes to reflect the reclassification described in clause (i), the update described in clause (ii), the effects of each and related matters.

Other than as expressly set forth above and minor wording changes necessary to properly refer to the Original Form 20-F, the Company has not modified or updated any other disclosures and has made no changes to the items or sections in the Company’s Original Form 20-F. Other than as expressly set forth above, this Amendment does not, and does not purport to, amend, update or restate the information in any part of the Company’s Original Form 20-F or reflect any events that have occurred after the Original Form 20-F was filed on June 30, 2020. Except as set forth above, information not affected by the restatement is unchanged and reflects the disclosures made at the time of the Original Form 20-F. The Company’s Chief Executive Officer and Chief Financial Officer are providing currently dated revised certifications in connection with this Form 20-F/A; the certifications are filed as Exhibits 12.1, 12.2, 13.1 and 13.2. The Company’s Original Form 20-F, as modified by this Amendment, are referred to herein as this “Report”).

-ii-

RELIANCE ON CONDITIONAL EXEMPTION FROM FILING DEADLINE

On June 30, 2020, the Company filed the Original Form 20-F for the fiscal year ended December 31, 2019, after the April 30, 2020 deadline applicable to the Company for the filing of its Original Form 20-F in reliance on the Order of the Securities and Exchange Commission (the “SEC”), issued on March 25, 2020, pursuant to Section 36 of the Securities Exchange Act of 1934 (the “Exchange Act”), granting conditional exemptions from specified provisions of the Exchange Act and certain rules thereunder (Release No. 34-88465) (the “Order”), which permitted a delay in filing of up to forty-five days due to circumstances related to the COVID-19 outbreak.

As previously disclosed on Form 6-K furnished by the Company on April 29, 2020, although the COVID-19 global pandemic caused little interruption to the operation of the Company’s oil storage facilities due to its highly automated and high-tech designs, it disrupted the operations of its management and corporate staff. In addition to voluntary measures the Company has taken to protect its staff, government authorities have at various recent times implemented lockdown or other measures restricting the movement of people, including staff, vendors and professionals. This impacted the Company’s ability to efficiently perform work related to the financial statements and related materials necessary for the audit and, as a result, delayed the completion of the audited consolidated financial statements and other information required to be included in the Company’s Annual Report on Form 20-F.

On June 15, 2020, the Company filed a “Notification of Late Filing” on Form 12b-25 pursuant to Rule 12b-25 of the Exchange Act to further delay by 15 days the filing of the Company’s Annual Report for the year ended December 31, 2019. As previously disclosed on a Form 12b-25, the Annual Report for the year ended December 31, 2019 could not be filed without unreasonable effort and expense. The Company required additional time to compile, review and prepare certain information in its financial statements following delays resulting from the COVID-19 pandemic. As required by Form 12b-25, the Company filed the Original Form 20-F on or prior to June 30, 2020.

-iii-

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Report (including information incorporated by reference herein) contains or may contain forward-looking statements as defined in Section 27A of the Securities Act, and Section 21E of the Exchange Act that involve significant risks and uncertainties. All statements other than statements of historical facts are forward-looking statements. These forward-looking statements include information about our possible or assumed future results of operations or our performance. Words such as “expects,” “intends,” “plans,” “believes,” “anticipates,” “estimates,” and variations of such words and similar expressions are intended to identify the forward-looking statements. The risk factors and cautionary language referred to or incorporated by reference in this Report provide examples of risks, uncertainties and events that may cause actual results to differ materially from the expectations described in our forward-looking statements, including among other things, the items identified in the Risk Factors section of this Report.

Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this Report. Although we believe that the expectations reflected in such forward-looking statements are reasonable, there can be no assurance that such expectations will prove to be correct. These statements involve known and unknown risks and are based upon a number of assumptions and estimates which are inherently subject to significant uncertainties and contingencies, many of which are beyond our control. Actual results may differ materially from those expressed or implied by such forward-looking statements. We undertake no obligation to publicly update or revise any forward-looking statements contained in this Report, or the documents to which we refer readers in this Report, to reflect any change in our expectations with respect to such statements or any change in events, conditions or circumstances upon which any statement is based.

-iv-

EXPLANATORY NOTES TO INITIAL FILING

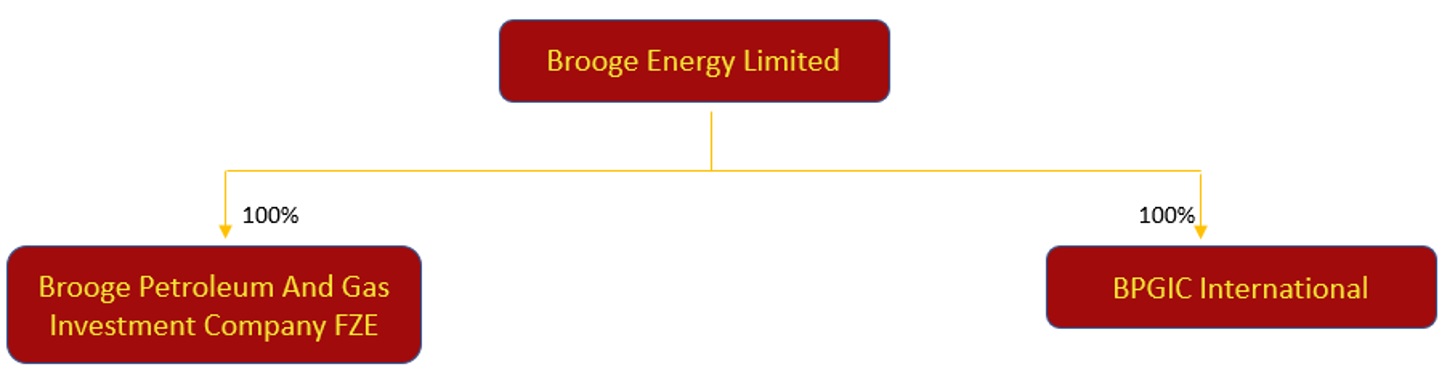

On April 15, 2019, (i) Twelve Seas Investment Company (now known as BPGIC International), a Cayman Islands exempted company (“Twelve Seas”), (ii) Brooge Energy Limited (f/k/a Brooge Holdings Limited), a Cayman Islands exempted company (the “Company”), (iii) Brooge Merger Sub Limited, a Cayman Islands exempted company, and a wholly-owned subsidiary of the Company (”Merger Sub”), and (iv) Brooge Petroleum And Gas Investment Company FZE, a company formed under the laws of the Fujairah Free Zone, United Arab Emirates (“BPGIC”), entered into that certain Business Combination Agreement, pursuant to which BPGIC Holdings Limited (“BPGIC Holdings”), a Cayman Islands exempted company also become a party thereafter pursuant to the Assignment and Joinder to Business Combination Agreement dated as of November 19, 2019 (as assignee of Brooge Petroleum and Gas Investment Company (BPGIC) PLC, a company formed under the laws of England and Wales, which became a party to the Business Combination Agreement pursuant to a Joinder to Business Combination Agreement dated as of May 10, 2019) (as amended prior to the date of Closing, including by the foregoing joinders and by the First Amendment to Business Combination Agreement, dated as of September 16, 2019, the “Business Combination Agreement”), pursuant to which, subject to the terms and conditions thereof, upon the consummation of the transactions contemplated thereby on December 20, 2019 (the “Closing”), among other matters, (a) Twelve Seas merged with and into Merger Sub, with Twelve Seas continuing as the surviving entity with the name BPGIC International (“BPGIC International”), and as a wholly-owned subsidiary of the Company and with holders of the Twelve Seas’ securities receiving substantially equivalent securities of the Company, and (b) the Company acquired all of the issued and outstanding ordinary shares of BPGIC from BPGIC Holdings in exchange for Ordinary Shares of the Company, subject to the withholding of the escrow shares being deposited in the escrow account in accordance with the terms and conditions of the Business Combination Agreement and the escrow agreement, and with BPGIC becoming a wholly-owned subsidiary of the Company (such transactions contemplated by the Business Combination Agreement, collectively, the “Business Combination”).

Upon consummation of the Business Combination pursuant to the terms of the Business Combination Agreement, the Company’s Ordinary Shares and warrants to purchase Ordinary Shares became listed on The Nasdaq Stock Market.

Unless otherwise indicated, “we,” “us,” “our,” “the Company,” “the Group” and similar terminology refers to Brooge Energy Limited, a company organized under the laws of the Cayman Islands, and its subsidiaries subsequent to the Business Combination.

-v-

IMPLICATIONS OF BEING AN EMERGING GROWTH COMPANY

As a company with less than $1.07 billion in revenue during our last fiscal year, we qualify as an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012 (the “JOBS Act”). An emerging growth company may avail itself of certain exemptions from various reporting requirements that are applicable to other public companies that are not emerging growth companies. For example, we have elected to rely on an exemption from the auditor attestation requirements of Section 404 of the Sarbanes Oxley Act of 2002 (the “Sarbanes Oxley Act”) relating to internal control over financial reporting, and we will not provide such an attestation from our auditors.

We will remain an emerging growth company until the earliest of the following:

| ● | the end of the first fiscal year in which the market value of our Ordinary Shares that are held by non- affiliates is at least $700 million as of the end of the second quarter of such fiscal year; |

| ● | the end of the first fiscal year in which we have total annual gross revenues of at least $1.07 billion; |

| ● | the date on which we have issued more than $1 billion in non-convertible debt securities in any rolling three year period; or |

| ● | December 31, 2024. |

Once we cease to be an emerging growth company, we will not be entitled to the exemptions provided for by the JOBS Act emptions provided for by the JOBS Act.

-vi-

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not Applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not Applicable.

A. Selected Financial Data

The Company was formed solely to effectuate the Business Combination and to hold BPGIC. Following and as a result of the Business Combination, all of the Company’s business is conducted through BPGIC. The financial statements of the Company, BPGIC and BPGIC International have been prepared in United States Dollars (“$”).

Selected Financial Information

Consolidated Statements of Comprehensive Income for the years ended December 31, 2019, 2018 and 2017.

| 2019 | 2018 | 2017 | ||||||||||

| (Restated) | ||||||||||||

| $ | $ | $ | ||||||||||

| Revenue | 44,085,374 | 35,839,268 | 89,593 | |||||||||

| Direct costs | (10,202,465 | ) | (9,607,360 | ) | (2,295,809 | ) | ||||||

| GROSS PROFIT | 33,882,909 | 26,231,908 | (2,206,216 | ) | ||||||||

| Listing expenses | (101,773,877 | ) | - | - | ||||||||

| General and administrative expenses | (2,608,984 | ) | (2,029,260 | ) | (574,266 | ) | ||||||

| Finance costs | (5,730,535 | ) | (6,951,923 | ) | (966,926 | ) | ||||||

| Change in estimated fair value of derivative warrant liabilities | 1,273,740 | - | - | |||||||||

| Changes in fair value of derivative financial instruments | (328,176 | ) | (1,190,073 | ) | - | |||||||

| (LOSS) PROFIT AND TOTAL COMPREHENSIVE INCOME FOR THE YEAR | (75,284,923 | ) | 16,060,652 | (3,747,408 | ) | |||||||

| (Loss) / Earnings per share | ||||||||||||

| -Basic and diluted | (0.94 | ) | 0.20 | (0.05 | ) | |||||||

| Selected Non-IFRS Financial Data | ||||||||||||

| Adjusted EBITDA* | 37,059,670 | 29,918,711 | (2,087,954 | ) | ||||||||

| Adjusted EBITDA Margin | 84.06 | 83.48 | - | |||||||||

| * | Adjusted EBITDA is defined as profit (loss) before finance costs, income tax expense (currently not applicable in the UAE but included here for reference purposes), depreciation, listing expenses and net change in the value of derivative financial instruments |

1

Consolidated statements of financial position as of December 31, 2019 and 2018

| 2019 | 2018 | |||||||

| (Restated) | ||||||||

| $ | $ | |||||||

| ASSETS | ||||||||

| Non-current assets | 284,893,352 | 197,629,114 | ||||||

| Current assets | 22,359,108 | 2,307,518 | ||||||

| TOTAL ASSETS | 307,252,460 | 199,936,632 | ||||||

| Equity | 109,416,415 | 60,977,933 | ||||||

| Non-current liabilities | 102,799,150 | 28,115,068 | ||||||

| Current liabilities | 95,036,895 | 110,843,631 | ||||||

| TOTAL EQUITY AND LIABILITIES | 307,252,460 | 199,936,632 | ||||||

See Note 2.4 to the notes to the consolidated financial statements included in this Amendment.

B. Capitalization and Indebtedness

Not applicable.

C. Reasons for the Offer and Use of Proceeds

Not applicable.

D. Risk Factors

Risks Related to BPGIC

BPGIC is currently reliant on Al Brooge International Advisory LLC for the majority of its revenues and any material non-payment or non-performance by Al Brooge International Advisory LLC would have a material adverse effect on BPGIC’s business, financial condition and results of operations.

Phase I of the BPGIC Terminal consists of 14 oil storage tanks with an aggregate geometric oil storage capacity of approximately 0.399 million m3 and related infrastructure (“Phase I”). On December 12, 2017, BPGIC entered into a five-year lease and service agreement (the “Phase I End User Agreement”) with an international energy trading company (the “Initial Phase I End User”). BPGIC’s revenues historically depended solely on the fees it received pursuant to the Phase I End User Agreement which were comprised of (i) a monthly fixed fee to lease BPGIC’s Phase I storage capacity (regardless of whether the Initial Phase I End User used any storage capacity) and (ii) monthly variable fees based on the Initial Phase I End User’s usage of the following ancillary services: throughput, blending, heating and inter-tank transfers.

2

In August 2019, with the approval of the Initial Phase I End User, BPGIC restructured its relationship with the Initial Phase I End User by entering into a four-year lease and offtake agreement (the “Phase I Customer Agreement”) with Al Brooge International Advisory LLC (“BIA”), for the Phase I facility. After entering the Phase I Customer Agreement, BIA assumed BPGIC’s rights and obligations under the Phase I End User Agreement. Subsequently, in May 2020, BIA agreed to release 129,000 m3 of the Phase I capacity, amounting to approximately one third of the total Phase I capacity, back to BPGIC. BPGIC leased this capacity to, Totsa Total Oil Trading SA (the “Super Major”), for a 6 month period (the “Super Major Agreement”) subject to renewal for an additional 6 month period with the mutual agreement of the parties.

Accordingly, a majority of BPGIC’s revenues for the immediate future are expected to consist of the fees it receives pursuant to the Phase I Customer Agreement which are comprised of (i) a monthly fixed fee to lease approximately two thirds of BPGIC’s Phase I storage capacity (regardless of whether BIA uses any storage capacity) and (ii) monthly variable fees based on BIA’s, or its sublessees’, usage of the following ancillary services: throughput, blending, heating and inter-tank transfers.

The terms of the Phase I Customer Agreement allow BIA to sublease, subject to BPGIC’s prior approval, the use of Phase I’s facilities. In 2020, BIA subleased the use of the Phase I facility to multiple international and regional end users. Under the Phase I Customer Agreement, BIA still retains the obligation to pay any outstanding amounts due, including if a sublessee were to fail to make any payments owed to it. There can be no assurance that in the event of a non-payment by one or more of the Phase I end users, of amounts owed to BIA, that BIA would honor its obligation to pay any outstanding amounts due to BPGIC.

We are susceptible to general economic conditions, natural catastrophic events and public health crises, which could adversely affect our operating results.

Our results of operations could be adversely affected by general conditions in the global economy, including conditions that are outside of our control, such as the impact of health and safety concerns from the current outbreak of COVID-19. Governments in affected countries, including the United Arab Emirates, have imposed travel bans, quarantines and other emergency public health measures. Those measures, though temporary in nature, may continue and increase depending on developments in the COVID-19’s outbreak. Though our oil storage and services operations have not been significantly impacted by the COVID-19 pandemic, the activities of our executives and corporate staff have been, and may continue to be, disrupted and delayed. Many of the vendors and professionals with whom we work have also experienced disruptions. Our executives and corporate staff have been, and may continue to be, focused on mitigating the effects of COVID-19, which may delay other value-add initiatives.

In particular, COVID-19 has resulted, and may continue to result in, delay in negotiations with counterparties, including BIA with respect to the BIA Refinery, that could be material to our business. Further, we and our contractors have been, and may continue to be, delayed or unable to procure essential equipment, supplies or materials for the construction of Phase II in adequate quantities and at acceptable prices.

In addition, the COVID-19 pandemic has significantly increased economic uncertainty. It is likely that the current outbreak or continued spread of COVID-19 will cause an economic slowdown, and it is possible that it could cause a global recession. Such adverse impact on the global economy may negatively impact the availability of debt and equity financing on commercially reasonable terms, which, in turn, may adversely affect our ability to successfully execute our business strategies and initiatives, such as the funding of capital expenditures.

The extent, if any, to which the coronavirus impacts our results will depend on future developments, which are highly uncertain and will include emerging information concerning the severity of the coronavirus and the actions taken by governments and private businesses to attempt to contain the coronavirus.

3

The Phase I users’ usage of BPGIC’s ancillary services has an impact on BPGIC’s profitability. The demand for such ancillary services can be influenced by a number of factors including current or expected prices and market demand for refined petroleum products, each of which can be volatile.

With respect to the Phase I Customer Agreement and the Super Major Agreement, the total monthly storage fees are fixed and the total monthly fees for BPGIC’s ancillary services are subject to variation based on BIA’s or its sublessees’ and the Super Major’s, usage of BPGIC’s ancillary services. BPGIC expects its revenue from the ancillary services offered in Phase I to vary based on the orders received from the Super Major and the orders BIA receives from its end users, which in turn, vary based on the orders the Super Major and the Phase I end users receive from their customers. The needs of the Super Major’s and the Phase I end users’ customers, and consequently, the Super Major’s and BIA’s usage of BPGIC’s ancillary services, tend to vary based on a number of factors including current or expected refined petroleum product prices and trading activity. Factors that could lead to a decrease in the demand for BPGIC’s ancillary services include:

| ● | changes in expectations for future prices of refined petroleum products; |

| ● | the level of worldwide oil and gas production and any disruption of those supplies; |

| ● | a decline in global trade volumes, economic growth, or access to markets; |

| ● | higher fuel taxes or other governmental or regulatory actions that increase, directly or indirectly, the cost of gasoline and diesel; and |

| ● | changes to applicable regulations or new regulations affecting the refined petroleum products serviced by BPGIC. |

Any of the factors referred to above, either alone or in combination, may result in the Super Major’s and/or the Phase I end users’ reduced usage of BPGIC’s ancillary services, which would ultimately have a material adverse effect on BPGIC’s business, financial condition and results of operations.

In the event that the Super Major Agreement or the Phase I Customer Agreement expire or otherwise terminate, BPGIC may have difficulty locating a replacement for the Super Major or BIA due to competition with other oil storage companies in the Port of Fujairah and at other ports.

BPGIC may have to compete with other oil storage companies in the Port of Fujairah (the “Port of Fujairah” or the “Port”) to secure a third party to contract for BPGIC’s services in the event that the Super Major Agreement or the Phase I Customer Agreement expire or otherwise terminate. Such third parties may not only consider competitors in the Port of Fujairah but may also consider companies located at other ports. Although BPGIC believes that it has a best-in-class technically designed terminal in Fujairah and there is a scarcity of land in Fujairah available for expansion by competitors, BPGIC’s ability to compete could be harmed by factors it cannot control, including:

| ● | BPGIC’s competitors’ construction of new assets or conversion of existing terminals in a manner that would result in more intense competition in the Port of Fujairah; |

| ● | BPGIC’s competitors, which currently provide services to their own businesses, seeking to provide their services to third parties, including third-party oil companies and oil traders; |

| ● | BPGIC’s competitors making significant investments to upgrade or convert their facilities in a manner that, while limiting their capacity in the short term, would eventually enable them to meet or exceed BPGIC’s capabilities; |

| ● | the perception that another company or port may provide better service; and |

| ● | the availability of alternative heating and blending facilities located closer to users’ operations. |

Any combination of these factors could result in third parties entering into long-term contracts to utilize the services of BPGIC’s competitors instead of BPGIC’s services, or BPGIC being required to lower its prices or increase its costs to attract such parties, either of which could adversely affect BPGIC’s business, financial condition and results of operations.

In addition, in the event that BIA’s agreements with its sublessees expire or otherwise terminate, BIA would have similar risks and may face similar difficulties locating replacements for its sublessees due to competition with other oil storage companies in the Port of Fujairah and at other ports. If BIA is unable to contract with new end users, or the new end users do not use ancillary services to the same extent as the existing sublessees, the ancillary services used by BIA would be reduced and BIA’s ability to satisfy its payment obligations to BPGIC under the Phase I Customer Agreement would be impaired, each of which could adversely affect BPGIC’s business, financial condition and results of operations.

4

BPGIC may be subject to significant risks and expenses when constructing Phase II, which could adversely affect BPGIC’s business, financial condition and results of operations.

The construction of the second phase of the terminal that BPGIC is developing on land located in close proximity to the Port of Fujairah’s berth connection points (such land, the “Phase I & II Land”) which is expected to consist of 8 oil storage tanks with an aggregate geometric oil storage capacity of approximately 0.601 million m3 and related infrastructure (“Phase II”) is subject to a number of risks, including:

| ● | delays by the Phase II contractor, Audex Fujairah LL FZC (“Audex”), in constructing Phase II; |

| ● | a shortage of building materials, equipment or labor; |

| ● | poor performance in project execution on the part of Audex; |

| ● | difficulty procuring supplies and arranging global shipping due to the COVID-19 lockdowns; |

| ● | COVID-19 cases amongst construction labor; |

| ● | default by or financial difficulties faced by Audex or other third-party service and goods providers or failure by Audex or other providers to meet their contractual obligations; |

| ● | BPGIC’s inability to find a suitable replacement contractor in the event of a default by Audex; and |

| ● | cost overruns that require BPGIC to obtain additional financing because there can be no assurance such additional financing would be available at all or upon acceptable terms by BPGIC. |

Any of the factors referred to above, either alone or in combination, could materially delay the completion of Phase II or materially increase the costs associated with the construction of Phase II, and therefore materially adversely affect BPGIC’s future financial condition. Any failure to complete construction according to specifications may also result in liabilities, reduced efficiency and lower financial returns than anticipated which may result in BPGIC having to enter into restructuring negotiations with its creditors. Delays in one part of Phase II may cause delays to other parts and to the overall Phase II completion timetable.

BPGIC will become reliant on BIA for all of its BIA Refinery revenues, and the termination of the Refinery Agreement would have a material adverse effect on BPGIC’s business, financial condition and results of operations.

In February 2020, BPGIC and Sahara Energy Resources DMCC (“Sahara”) mutually agreed to discontinue their joint development discussions to install a modular oil refinery at BPGIC’s terminal. Shortly thereafter, BPGIC entered into a new agreement with BIA (the “Refinery Agreement”) which provides that the parties will use their best efforts to finalize the technical and design feasibility studies for a refinery with a capacity of 25,000 bpd (the “BIA Refinery”). The parties further agreed to negotiate, within 30 days, a sublease agreement and a joint venture agreement (such sublease agreement and joint venture agreement, collectively, the “Refinery Operations Agreement”) to govern the terms on which (i) BPGIC will sublease land to BIA to locate, (ii) BIA will construct, and (iii) BPGIC will operate the BIA Refinery. Due to the COVID-19 pandemic, the parties agreed to extend the period for their negotiations until August 4, 2020. As illustrated by the discontinuance of the prior agreement with Sahara, there can be no assurance that BPGIC and BIA will be able to reach agreement on the terms of a sublease and a joint venture agreement to govern the location, construction and operation of the BIA Refinery.

Upon completion of the BIA Refinery, BPGIC will become reliant on BIA for another significant portion of its revenues. If the Refinery Agreement is terminated, there can be no assurance that BPGIC will be able to find a new partner to install a modular refinery at the terminal that BPGIC is developing on two plots of land located in close proximity to the Port of Fujairah’s berth connection points (the “BPGIC Terminal”), or enter into a comparable agreement to provide refinery, storage and ancillary services at comparable or more favorable pricing and/or terms. Additionally, BPGIC may incur substantial cost if it suffers delays in locating a third party or if modifications or installation of a new refinery are required by a new agreement. The occurrence of any one or more of these events could have a material adverse effect on BPGIC’s business, financial condition and results of operations.

BPGIC will become reliant on BIA for all of its Phase II revenues, and the termination of the Phase II Customer Agreement and the failure to find a replacement for BIA would have a material adverse effect on BPGIC’s business, financial condition and results of operations.

In connection with Phase II, BPGIC entered into a five-year lease and service agreement (the “Phase II End User Agreement”) with an international commodities trading company (the “Phase II End User”), which extends automatically for an additional five years. Pursuant to the Phase II End User Agreement, the Phase II End User has agreed to lease all eight oil storage tanks in Phase II once Phase II becomes operational, which is expected to occur during 2020.

5

In September 2019, with the approval of the Phase II End User, BPGIC restructured its relationship with the Phase II End User by entering into a five-year lease and offtake agreement (the “Phase II Customer Agreement”) for the Phase II facility with BIA. In connection with the Phase II Customer Agreement, BIA assumed BPGIC’s rights and obligations under the Phase II End User Agreement.

When Phase II becomes operational, BPGIC will become reliant on BIA for another significant portion of its revenues. In the event that insolvency proceedings are commenced against BIA, BPGIC would have the option to terminate the Phase II Customer Agreement. Upon the termination of the Phase II Customer Agreement, BPGIC would be able to enter into lease and service agreements with one or more third parties. However, in that event, there can be no assurance that BPGIC would be able to locate one or more third parties to enter into lease and service agreements with BPGIC and/or that BPGIC would be able to obtain agreements for a comparable amount of utilization of Phase II’s oil storage and ancillary services at comparable or more favorable pricing and/or terms. Additionally, BPGIC may incur substantial costs if it suffers delays in locating a third party or if modifications to Phase II are required by a new agreement. The occurrence of any one or more of these events would have a material adverse effect on BPGIC’s business, financial condition and results of operations.

The terms of the Phase II Customer Agreement allow BIA to sublease, subject to BPGIC’s prior approval, the use of Phase II’s facilities, and by assuming the Phase II End User Agreement, BIA subleased the use of the Phase II facility to the Phase II End User. Under the Phase II Customer Agreement, BIA still retains the obligation to pay any outstanding amounts due, including if a sublessee were to fail to make any payments owed to BIA. There can be no assurance that in the event of a non-payment by the Phase II End User, or another sublessee, of amounts owed to BIA, that BIA would honor its obligation to pay any outstanding amounts due to BPGIC in the event of a non-payment by a sublessee.

BPGIC will become further reliant on BIA for a substantial majority of its revenues, and any material non-payment or non-performance by BIA would have a material adverse effect on BPGIC’s business, financial condition and results of operations.

Upon completion of Phase II and the BIA Refinery, BIA will be BPGIC’s customer with respect to a substantial majority of the capacity of the Phase I facility, and will be BPGIC’s sole customer with respect to the Phase II facility and the BIA Refinery.

The terms of both the Phase I Customer Agreement and the Phase II Customer Agreement allow BIA to sublease the corresponding facilities, subject to BPGIC’s prior approval. BIA has subleased the Phase I capacity that it still leases to certain end users. By assuming the Phase II End User Agreement, BIA has subleased the Phase II facility to the Phase II End User. Under both the Phase I Customer Agreement, and the Phase II Customer Agreement, BIA remains obligated to pay any outstanding amounts due to BPGIC, even if a sublessee fails to make any payment owed to BIA as sublessor. There can be no assurance that BIA would honor its obligation to pay any outstanding amounts due to BPGIC.

BIA’s inability or failure to meet its obligations under the Phase I Customer Agreement, the Phase II Customer Agreement, or both, would have a material adverse effect on BPGIC’s business, financial condition and results of operations. If BIA fails to honor its obligations under either agreement, BPGIC is entitled to terminate such agreement and BIA remains liable to pay certain termination fees. However, in that event, there can be no assurance that BPGIC would be able to locate one or more third parties to enter into lease and service agreements with BPGIC and/or that BPGIC would be able to obtain agreements for a comparable amount of utilization of such facility and ancillary services at comparable or more favorable pricing and/or terms. Additionally, BPGIC may incur substantial costs if it suffers delays in locating a third party or if modifications to such facility are required by a new agreement. The occurrence of any one or more of these events would have a material adverse effect on BPGIC’s business, financial condition and results of operations.

6

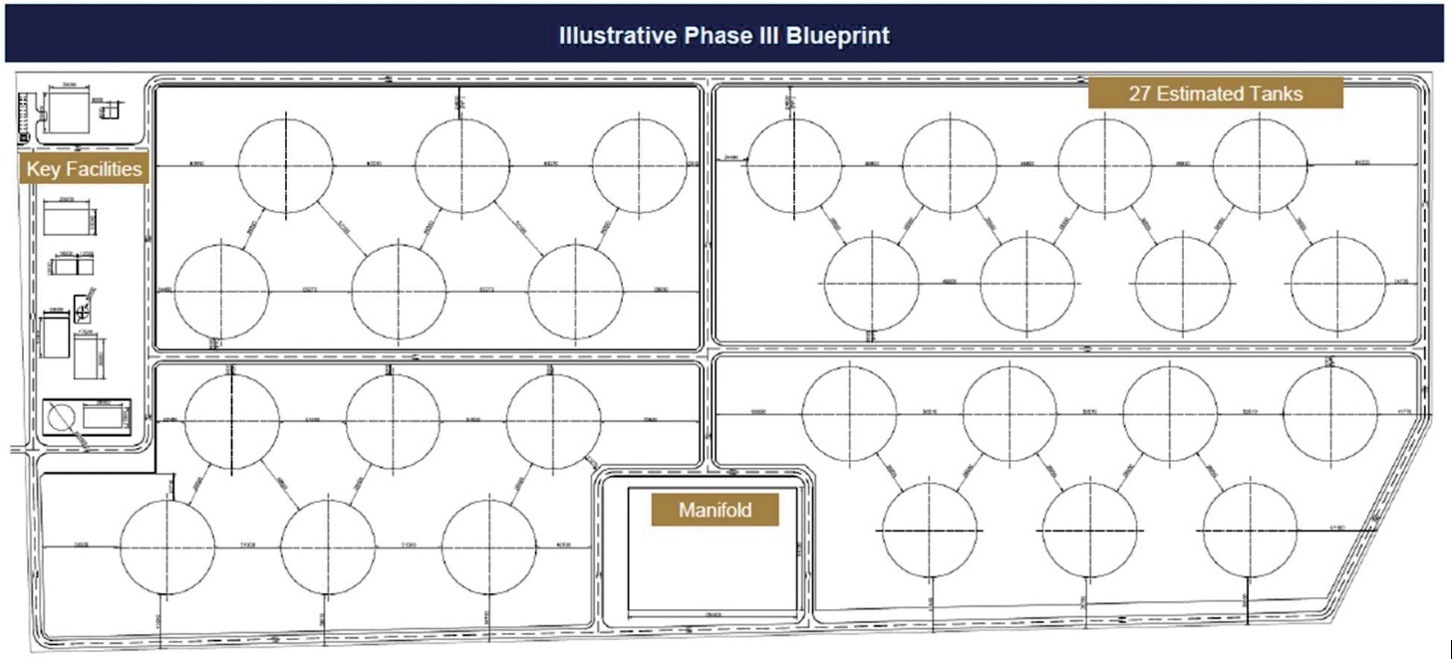

The scarcity of available land in the Fujairah oil zone region could subject BPGIC to competition for additional land, unfavorable lease terms for that land and limit BPGIC’s ability to expand its facilities in Fujairah beyond Phase III.

As discussed further in “Item 4.B Information on the Company ¾ Business Overview — Strategy” and “Item 4.A History and Development of the Company — Proposed Phase III”, BPGIC has entered into a land lease agreement, dated as of February 2, 2020 (the “Phase III Land Lease Agreement”), by and between BPGIC and the Fujairah Oil Industry Zone (“FOIZ”) to lease an additional plot of land that has a total area of approximately 450,000 m2 (the “Phase III Land”). BPGIC intends to use the relevant land to expand its crude oil storage and service and refinery capacity (“Phase III”).

However, all land in the Fujairah oil zone region is owned and controlled by FOIZ. The Fujairah oil zone region currently has limited available land to lease. As a result, BPGIC’s ability to further expand its facilities if it wishes to expand in Fujairah beyond Phase III is limited. This could subject BPGIC to enhanced competition both in terms of price and lease terms for any land that becomes available to lease.

If BPGIC is able to lease additional land, there can be no assurance that it would be able to do so on terms that are as favorable or more favorable than the terms of the land lease that BPGIC entered into in connection with Phases I and II, dated as of March 10, 2013, by and between Fujairah Municipality and BPGIC, as amended by the novation agreement, dated September 1, 2014, by and among Fujairah Municipality, BPGIC and FOIZ (the “Phase I & II Land Lease” and together with the Phase III Land Lease Agreement, the “Land Leases”) or the Phase III Land Lease Agreement, or that would allow BPGIC to use the land as intended. BPGIC’s inability to secure new land from FOIZ in the Fujairah oil zone region could substantially impair BPGIC’s regional growth prospects in Fujairah beyond Phase III, leading to fewer remaining options for its expansion in Fujairah, other than the acquisition of an existing third-party owned oil storage terminal in Fujairah.

Accidents involving the handling of oil products at the BPGIC Terminal could disrupt BPGIC’s business operations and/or subject it to environmental and other liabilities.

Accidents in the handling of oil products (hazardous or otherwise) at the BPGIC Terminal could disrupt BPGIC’s business operations during any repair or clean-up period, which could negatively affect its business operations. The BPGIC Terminal, which has received multiple international awards since it began operations, was designed to minimize the risk of oil leakage and has state-of-the-art control facilities. In addition, pursuant to the Fujairah Municipality environmental regulations, BPGIC installed impermeable lining over the ground soil throughout its tank farm area and any other area where oil leakage could occur and potentially reach the ground soil. BPGIC intends to take similar steps to minimize the risk of oil leakage in connection with Phase III. Nevertheless, there is a risk that oil leakages or fires could occur at the terminal and, in the event of an oil leakage, there can be no assurance that the installed lining will prevent any oil products from reaching the ground soil. Although BPGIC believes that it has adequate insurance in place to insure against the occurrence of any of the foregoing events, any such leakages or fires could disrupt terminal operations and result in material remediation costs. Any such damage or contamination could reduce gross throughput and/or subject BPGIC to liability in connection with environmental damage, any or all of which could have a material adverse effect on its business, financial condition and results of operations.

The BIA Refinery, once completed, will face operating hazards, and the potential limits on insurance coverage could expose us to potentially significant liability costs.

Once completed, the BIA Refinery will be subject to certain operating hazards, and our cash flow from its operations could decline if it experiences a major accident, pipeline rupture or spill, explosion or fire, is damaged by severe weather or other natural disaster, or otherwise is forced to curtail its operations or shut down. These operating hazards could result in substantial losses due to personal injury and/or loss of life, severe damage to and destruction of property and equipment and pollution or other environmental damage and may result in significant curtailment or suspension of our related operations.

Although we intend to maintain insurance policies, including personal and property damage and business interruption insurance for each of our facilities, we cannot ensure that this insurance will be adequate to protect us from all material expenses related to potential future claims for personal and property damage or significant interruption of operations.

Furthermore, we may be unable to maintain or obtain insurance of the type and amount we desire at reasonable rates. If we were to incur a significant liability for which we were not fully insured, it could affect our financial condition and diminish our ability to make distributions to our shareholders.

7

When the BIA Refinery is completed, our financial results will be affected by volatile refining margins, which are dependent upon factors beyond our control, including the price of crude oil, to the extent such volatility reduces customer demand of ancillary services.

When the BIA Refinery is operational, our financial results will be affected by the relationship, or margin, between refined petroleum product prices and the prices for crude oil and other feedstocks to the extent decreases in refining margins reduce BIA ‘s use of the BIA Refinery and our ancillary services. Historically, refining margins have been volatile, and we believe they will continue to be volatile in the future. BIA’s costs to acquire feedstocks and the price at which it can ultimately sell refined petroleum products depend upon several factors beyond its, and our, control, including regional and global supply of and demand for crude oil, gasoline, diesel, and other feedstocks and refined petroleum products. These in turn depend on, among other things, the availability and quantity of imports, production levels, levels of refined petroleum product inventories, productivity and growth (or the lack thereof) of global economies, international relations, political affairs, and the extent of governmental regulation. Some of these factors can vary by region and may change quickly, adding to market volatility, while others may have longer-term effects. The longer-term effects of these and other factors on refining and marketing margins are uncertain. Decreased refining margins could have a significant effect on the extent to which BIA uses the BIA Refinery and our ancillary services which, in turn, could have a significant effect on our financial results.

BPGIC’s competitive position and prospects depend on the expertise and experience of senior management and BPGIC’s ability to continue to attract, retain and motivate qualified personnel.

BPGIC’s business is dependent on retaining the services of, or in due course promptly obtaining equally qualified replacements for senior management, those persons named as senior managers in Item 6. Directors, Senior Management and Employees. Directors and Senior Management. Competition in the UAE for personnel with relevant expertise is intense and it could lead to challenges in locating qualified individuals with suitable practical experience in the oil storage industry. Although BPGIC has employment agreements with all of the members of senior management, the retention of their services cannot be guaranteed. Should they decide to leave BPGIC, it may be difficult to replace them promptly with other managers of sufficient expertise and experience or at all. To mitigate this risk, BPGIC intends to enter into long term incentive plans with members of senior management in due course. In the event of any increase in the levels of competition in the oil storage industry or general price levels in the Fujairah region, BPGIC may experience challenges in retaining members of the senior management team or recruiting replacements with the appropriate skills. Should BPGIC lose any of the members of senior management without prompt and equivalent replacement or if BPGIC is otherwise unable to attract or retain such qualified personnel for BPGIC’s requirements, this could have a material adverse effect on its business, financial condition and results of operations. For more information regarding senior management, see Item 6. Directors, Senior Management and Employees. Directors and Senior Management.

In connection with the preparation of the Company’s consolidated financial statements as of and for the years ended December 31, 2017, 2018 and 2019, the Company and its independent registered public accounting firm identified two material weaknesses in the Company’s internal control over financial reporting, one related to lack of sufficient skilled personnel and one related to lack of sufficient entity level and financial reporting policies and procedures.

Prior to the consummation of the Business Combination, the Company was neither a publicly listed company, nor an affiliate or a consolidated subsidiary of, a publicly listed company, and it has had limited accounting personnel and other resources with which to address its internal controls and procedures. Effective internal control over financial reporting is necessary for it to provide reliable financial reports and, together with adequate disclosure controls and procedures, are designed to prevent fraud.

In connection with the preparation and external audit of the Company’s financial statements as of and for the years ended December 31, 2017 and December 31, 2018, the Company and our auditors, noted material weaknesses in the Company’s internal control over financial reporting. The Public Company Accounting Oversight Board has defined a material weakness as a deficiency, or a combination of deficiencies, in internal control over financial reporting, such that there is a reasonable possibility that a material misstatement of the Company’s financial statements will not be prevented or detected on a timely basis.

8

The material weaknesses identified were (1) a lack of sufficient skilled personnel with requisite IFRS and SEC reporting knowledge and experience and (2) a lack of sufficient entity level and financial reporting policies and procedures that are commensurate with IFRS and SEC reporting requirements. These material weaknesses remain as of December 31, 2019.

The Company was not required to perform an evaluation of internal control over financial reporting as of December 31, 2019, December 31, 2018 or December 31, 2017 in accordance with the provisions of the Sarbanes-Oxley Act. Had such an evaluation been performed, additional control deficiencies may have been identified by the Company’s management, and those control deficiencies could have also represented one or more material weaknesses.

The Company’s auditors did not undertake an audit of the effectiveness of its internal controls over financial reporting. The Company’s independent registered public accounting firm will not be required to report on the effectiveness of their respective internal controls over financial reporting pursuant to Section 404(b) of the Sarbanes-Oxley Act of 2002 until the Company’s first annual report on Form 20-F following the date on which it ceases to qualify as an “emerging growth company,” which may be up to five full fiscal years following the date of the Closing. The process of assessing the effectiveness of the Company’s internal control over financial reporting may require the investment of substantial time and resources, including by members of the Company’s senior management. As a result, this process may divert internal resources and take a significant amount of time and effort to complete. In addition, the Company cannot predict the outcome of this determination and whether the Company will need to implement remedial actions in order to implement effective control over financial reporting. If in subsequent years the Company is unable to assert that the Company’s internal control over financial reporting is effective, or if the Company’s auditors express an opinion that the Company’s internal control over financial reporting is ineffective, the Company could lose investor confidence in the accuracy and completeness of their financial reports, which could have a material adverse effect on the price of the Company’s securities. Since the date of the Original Form 20-F, the Company has implemented measures to address the material weaknesses, including (i) hiring personnel with relevant public reporting experience, (ii) conducting training for Company personnel with respect to IFRS and SEC financial reporting requirements and (iii) engaging a third party to prepare standard operating procedures for the Company. In this regard, the Company has, and will need to continue to, dedicate internal resources, recruit personnel with public reporting experience, potentially engage additional outside consultants and adopt a detailed work plan to assess and document the adequacy of their internal control over financial reporting. This has, and may continue to, include taking steps to improve control processes as appropriate, validating that controls are functioning as documented and implementing a continuous reporting and improvement process for internal control over financial reporting.

9

Our auditor’s report includes a going concern paragraph.

As of 31 December 2018, the Group had not paid USD 3.7 million of principal and accrued interest that was due under the Group’s Phase I Financing Facilities. Also, as of 31 December 2018, the Group was not in compliance with its debt covenants, including the debt service coverage ratio contained in the Group’s Phase I Financing Facilities. Even though the lender did not declare an event of default under the loan agreements, these breaches constituted events of default and could have resulted in the lender requiring immediate repayment of the loans. Accordingly, as of 31 December 2018, the Group has classified its debt balance of USD 94.8 million as a current liability.

On 10 September 2019 and again on 30 December 2019 the Group entered into agreements with its lender to amend the Phase 1 Financing Facility such that on 31 December 2019 the Group was in compliance with the amended facility agreement. At 31 December 2019, the Group’s current liabilities exceeded its current assets by USD 72 million.

Subsequent to the year end, the Group defaulted on its commitments under its term loans and the Group was not in compliance with its debt covenants, including the debt service coverage ratio contained in the Group’s loan agreement. Even though the lender did not declare an event of default under the loan agreements, these breaches constituted events of default and could have resulted in the lender requiring immediate repayment of the loans.

On 15 June 2020, the Group entered into an agreement with its lender to amend its Phase I Financing Facilities (note15). The Group will have to pay principal and accrued interest of USD 8.8 million in 2020 which represents the cumulative instalments including interest outstanding from periods prior to this amended agreement and an amendment fee of USD 136,000. Term loan (1) and Term loan (2) is now payable in 46 and 16 instalments respectively starting 30 June 2020 with final maturity on 31 July 2030 and 31 July 2023, respectively.

During 2018, the Group signed a sales agreement for phase 2 to provide storage and ancillary services to an international commodity trading company, which was novated to a new party during the year. Phase 2 operations are scheduled to start in fourth quarter of 2020 and management expects this will generate significant operating cash flows. The Group is in receipt of a loan facility letter date 15 October 2018 from a lender. The Group intends to draw down from this facility to finance the payments due to the contractor in respect of Phase 2 construction in the third quarter of 2020. The ability of the Group to draw down on this facility is contingent upon a number of conditions agreed in the facility letter which will need to be assessed and approved by the bank prior to the disbursement of funds.

Based on the above noted, management has considered the going concern status of the Group and believes there to be a material uncertainty that casts significant doubt upon the Group’s ability to continue as a going concern. Based on management’s forecasts the capital expenditure requirements for phase 2 and debt servicing as described above will be funded by cash generated through the ongoing operations and further drawdowns from approved loan facilities. The Group’s management acknowledge that there is a risk that the quantum and timing of cash flows may not be achievable in line with the twelve months forecasts from the date of approval of the Group’s financial statements. Accordingly, there is significant doubt that the Group will be able to pay its obligations as they fall due and this significant doubt is not alleviated by management’s plans.

The financial statements have been prepared assuming that the Group will continue as a going concern. Accordingly, the consolidated financial statements do not include any adjustments relating to the recoverability and classification of recorded asset amounts, the amounts and classification of liabilities, or any other adjustments that might result in the event the Group is unable to continue as a going concern.

10

BPGIC has a limited operating history and the Report contains limited financial information, which makes it particularly difficult for a potential investor to evaluate BPGIC’s financial performance and predict its future prospects.

BPGIC commenced operations of Phase I in late Fourth Quarter 2017 and began operating it at full capacity on April 1, 2018. As a result, although BPGIC’s senior management and site teams have up to thirty years of relevant international and industry experience, BPGIC has only limited operating results to demonstrate its ability to operate its business on which a potential investor may rely to evaluate BPGIC’s business and prospects. Accordingly, the financial information included in the Report may be of limited use in assessing the business. BPGIC is also subject to the business risks and uncertainties associated with any new business, including the risk that it will not achieve its operating objectives and business strategy. BPGIC’s limited operating history increases the risks and uncertainties that potential investors face in making an investment in the Ordinary Shares and warrants and the lack of historic information may make it particularly difficult for a potential investor to evaluate BPGIC’s financial performance and forecast reliable long-term trends.

If BPGIC is unable to make acquisitions on economically acceptable terms, its future growth would be limited, and any acquisitions it makes could adversely affect its business, financial condition and results of operations.

As discussed further in “Item 4.B Information on the Company ¾ Business Overview ¾ Strategy”, one of BPGIC’s medium to long term strategies is to potentially grow its business through the acquisition and development of oil storage terminals globally. BPGIC’s strategy to grow its business is dependent on its ability to make acquisitions that improve its financial condition. If BPGIC is unable to make acquisitions from third parties because it is unable to identify attractive acquisition candidates or negotiate acceptable purchase contracts, it is unable to obtain financing for these acquisitions on economically acceptable terms or it is outbid by competitors, its future growth will be limited. Furthermore, even if BPGIC does consummate acquisitions that it believes will be accretive, they may in fact harm its business, financial condition and results of operations. Any acquisition involves potential risks, some of which are beyond BPGIC’s control, including, among other things:

| ● | inaccurate assumptions about revenues and costs, including synergies; |

| ● | an inability to successfully integrate the various business functions of the businesses BPGIC acquires; |

| ● | an inability to hire, train or retain qualified personnel to manage and operate BPGIC’s business and newly acquired assets; |

| ● | an inability to comply with current or future applicable regulatory requirements; |

| ● | the assumption of unknown liabilities; |

| ● | limitations on rights to indemnity from the seller; |

| ● | inaccurate assumptions about the overall costs of equity or debt; |

| ● | the diversion of management’s attention from other business concerns; |

| ● | unforeseen difficulties operating in new product areas or new geographic areas; and |

| ● | customer or key employee losses at the acquired businesses. |

If BPGIC consummates any future acquisitions, its business, financial condition and results of operations may change significantly, and holders of Ordinary Shares will not have the opportunity to evaluate the economic, financial and other relevant information that BPGIC will consider in determining the application of these funds and other resources.

11

BPGIC is subject to a wide variety of regulations and may face substantial liability if it fails to comply with existing or future regulations applicable to its businesses or obtain necessary permits and licenses pursuant to such regulations.

BPGIC’s operations are subject to extensive international, national and local laws and regulations governing, amongst other things, the loading, unloading and storage of hazardous materials, environmental protection and health and safety. BPGIC’s ability to operate its business is contingent on its ability to comply with these laws and regulations and to obtain, maintain and renew as necessary related approvals, permits and licenses from governmental agencies and authorities in Fujairah and the UAE. Because of the complexities involved in ensuring compliance with different and sometimes inconsistent national and international regulatory regimes, BPGIC cannot assure investors that it will remain in compliance with all of the regulatory and licensing requirements imposed on it by each relevant jurisdiction. BPGIC’s failure to comply with all applicable regulations and obtain and maintain requisite certifications, approvals, permits and licenses, whether intentional or unintentional, could lead to substantial penalties, including criminal or administrative penalties or other punitive measures, result in revocation of its licenses and/or increased regulatory scrutiny, impair its reputation, subject it to liability for damages, or invalidate or increase the cost of the insurance that it maintains for its business. Additionally, BPGIC’s failure to comply with regulations that affect its staff, such as health and safety regulations, could affect its ability to attract and retain staff. BPGIC could also incur civil liabilities such as abatement and compensation for loss in amounts in excess of, or that are not covered by, its insurance. For the most serious violations, BPGIC could also be forced to suspend operations until it obtains such approvals, certifications, permits or licenses or otherwise brings its operations into compliance.

In addition, changes to existing regulations or tariffs or the introduction of new regulations or licensing requirements are beyond BPGIC’s control and may be influenced by political or commercial considerations not aligned with its interests. Any such changes to regulations, tariffs or licensing requirements could adversely affect BPGIC’s business by reducing its revenue, increasing its operating costs or both and BPGIC may be unable to mitigate the impact of such changes.

Finally, any expansion of the scope of the regulations governing BPGIC’s environmental obligations, in particular, would likely involve substantial additional costs, including costs relating to maintenance and inspection, development and implementation of emergency procedures and insurance coverage or other financial assurance of BPGIC’s ability to address environmental incidents or external threats. If BPGIC is unable to control the costs involved in complying with these and other laws and regulations, or pass the impact of these costs on to users through pricing, BPGIC’s business, financial condition and results of operations could be adversely affected.

Any material reduction in the quality or availability of the Port of Fujairah’s facilities could have a material adverse effect on BPGIC’s business, financial condition and results of operations.

BPGIC is dependent on the Port of Fujairah to operate and maintain the Port’s facilities at an appropriate standard and BPGIC is dependent on such facilities, including the berths, the very large crude carrier (“VLCC”) jetty and the associated pipelines, to operate its business. Any interruptions or reduction in the capabilities or availability of these facilities would result in reduced volumes being transported through the BPGIC Terminal. Reductions of this nature are beyond BPGIC’s control. If the utilization or the costs to BPGIC or users to deliver oil products through these facilities were to significantly increase, BPGIC’s profitability could be reduced. The Port of Fujairah’s facilities are subject to deterioration or damage, due to potential declines in the physical condition of its facilities and ship collisions, among other things. Any failure of the Port of Fujairah to carry out necessary repairs, maintenance and expansions of its facilities and any resulting interruptions for access to its facilities could adversely affect BPGIC’s business volumes, cause delays in the arrival and departure of oil tankers or disruptions to BPGIC’s operations, in part or in whole, may subject BPGIC to liability or impact its brand and reputation and may otherwise hinder the normal operation of the BPGIC Terminal, which could have a material adverse effect on its business, financial condition and results of operations.

BPGIC is subject to restrictive covenants in its Financing Facilities that may limit its operating flexibility and, if it defaults under its covenants, it may not be able to meet its payment obligations.

BPGIC entered into secured Shari’a compliant Istisna’ and Murabaha financing arrangements of $84.6 million (the “Phase I Construction Facility”) and of $11.1 million (the “Phase I Admin Building Facility” and together with the Phase I Construction Facility, the “Phase I Construction Facilities”) to fund a portion of the construction costs of Phase I, of $3.5 million (the “Phase I Short Term Financing Facility” and together with the Phase I Construction Facilities, the “Phase I Financing Facilities”) to settle certain amounts due under the Phase I Construction Facilities and of $95.3 million (the “Phase II Financing Facility” and together with the Phase I Financing Facilities, the “Financing Facilities”) to fund a portion of the capital expenditure in respect of Phase II. The Financing Facilities contain covenants limiting BPGIC’s ability to incur indebtedness, grant liens, engage in transactions with affiliates and make distributions on or redeem or repurchase ordinary shares. The Phase I Financing Facilities contain covenants requiring BPGIC to maintain certain financial ratios, including a facility service coverage ratio of greater than 1.50:1. Similarly, the Phase II Financing Facility also contains restrictive financial covenants, including, (i) a minimum facility service coverage ratio of 1.25:1, (ii) a participations to value ratio not exceeding 1.50:1 at all times, (iii) a participations to cost ratio not exceeding 57% at any date, and (iv) an amount equivalent to one instalment including interest in a facility service reserve account at all times or in the event of an initial public offering, an amount equivalent to the next two instalments including interest.

12

On December 30, 2019, BPGIC and FAB agreed to amend the Phase I Construction Facility to defer the installments due thereunder to later dates. The key changes resulting from the amendment were as follows:

| 1. | an amount of $5,729,417.50 which was due on November 30, 2019 will now be repayable on February 28, 2020; |

| 2. | an amount of $1,765,553.50 which was due on January 31, 2020 will now be payable in two installments: $882,776.75 on January 31, 2020 and $882,776.75 on February 28, 2020; and |

| 3. | the Debt Service Reserve Account to be created by February 28, 2020; and |

| 4. | testing of the Debt Service Coverage Ratio covenant to start on February 28, 2020 and to be conducted on each subsequent due date. |

BPGIC did not comply with the terms of the Phase I Construction Facilities as amended on December 30, 2019. A payment of principal and interest of $6.6 Million for the Phase I Construction Facility due on February 28, 2020 was not paid. Payments of principal and interest totaling $2.2 Million for the Phase I Construction Facility and the Phase I Admin Building Facility due on April 30, 2020 were not made. The Debt Service Reserve Account did not maintain a balance in an amount equivalent to one quarterly instalment including interest by February 28, 2020. BPGIC did not maintain a minimum Debt Service Coverage Ratio of 150% beginning on February 28, 2020. These non-payments and failures to comply with covenants were events of default, but, as in the past, the lender did not declare an event of default.

On June 15, 2020, BPGIC entered into an agreement with its lender to amend the Phase I Construction Facilities (the “June 15 Phase I Construction Facilities Amendment”).

Pursuant to the June 15 Phase I Construction Facilities Amendment, BPGIC and the lender agreed to a revised payment schedule for the Phase I Construction Facility that requires BPGIC to make the following payments from June 30, 2020 through December 31, 2020:

| Date | Amount | |

| June 30, 2020 | $2.99 Million | |

| July 31, 2020 | $3.62 Million | |

| August 31, 2020 | $0.14 Million | |

| September 30, 2020 | $0.14 Million | |

| October 31, 2020 | $1.01 Million | |

| November 30, 2020 | $0.14 Million | |

| December 31, 2020 | $3.87 Million | |

| Total | $11.9 Million by end of 2020 |

13

Thereafter, beginning on January 31, 2021 and ending on July 30, 2030, BPGIC will make quarterly payments of approximately $1.77 Million

Pursuant to the June 15 Phase I Construction Facilities Amendment, BPGIC and the lender also agreed to a revised payment schedule for the Phase I Admin Building Facility that requires BPGIC to make the following payments from August 31, 2020 through December 21, 2020:

| Date | Amount | |

| August 31, 2020 | $0.14 Million | |

| September 30, 2020 | $0.14 Million | |

| October 31, 2020 | $0.41 Million | |

| November 30, 2020 | $0.14 Million | |

| December 31, 2020 | $0.80 Million | |

| Total | $1.63 Million by end of 2020 |

Thereafter, beginning on January 31, 2021 and ending on July 31, 2023, BPGIC will make quarterly payments of approximately $0.54 Million.

Testing of the Debt Service Ratio Covenant will start on December 31, 2020 and will be conducted on each subsequent payment date. A Debt Service Reserve Account containing at least 1 quarter of debt service amounts must be maintained with the lender by October 31, 2020 and at all times thereafter through the term of the Phase I Construction Facility or until BPGIC repays all liabilities owed under the Phase I Construction Facilities. BPGIC pledged the account to the lender as security for the Phase I Construction Facilities. BPGIC, The Company and BPGIC Holdings undertook to have no other bank accounts except for the one that is the Debt Service Reserve Account until the Phase I Construction Facilities are repaid and to route all funds through the Debt Service Reserve Account. BPGIC further granted the lender a non-possessory mortgage over the Phase I Customer Agreement as security for the Phase I Construction Facilities.

Also pursuant to the June 15 Phase I Construction Facilities Amendment, BPGIC negotiated revised pricing terms as follows:

| o | Phase I Construction Facility: Enhanced to 6M EIBOR + 4% per annum [Minimum 5%] and to be further enhanced to 6M EIBOR + 4.5% per annum [Minimum 5%] beginning on January 1, 2021; and |

| o | Phase I Admin Building Facility: Enhanced to 3M EIBOR + 4% per annum [Minimum 5%] and to be further enhanced to 3M EIBOR + 4.5% per annum [Minimum 5%] beginning on January 1, 2021. |

There is no change in the final maturity of Phase I Construction Facility which is July 30, 2030 and Phase I Admin Building Facility which is July 31, 2023. BPGIC will pay FAB a transaction service fee of $0.14 million in connection with the June 15, 2020 amendment.

BPGIC’s ability to comply with these restrictions and covenants may be affected by events beyond its control, including prevailing economic, financial and industry conditions. If BPGIC is unable to comply with these restrictions and covenants, a significant portion of the indebtedness under the Financing Facilities may become immediately due and payable. BPGIC might not have, or be able to obtain, sufficient funds to make these accelerated payments. In addition, BPGIC’s obligations under the Financing Facilities are secured by substantially all of BPGIC’s assets, and if BPGIC is unable to repay the indebtedness under the Financing Facilities, the lenders could seek to foreclose on such assets, which would adversely affect BPGIC’s business, financial condition and results of operations. The Financing Facilities also have cross-default provisions that apply to any other material indebtedness that BPGIC may have. For more information regarding the Financing Facilities, see the section entitled “Item 5. Operating and Financial Review and Prospects— Liquidity and Capital Resources — Debt Sources of Liquidity.”

The Company and BPGIC have and will hire, new management personnel and have implemented a number of corporate governance and financial reporting procedures and other policies, processes, systems and controls which have a limited operating history.

The Company and BPGIC has hired new management personnel, including a new chief financial officer, and implemented a number of corporate governance and financial reporting procedures and other policies, processes, systems and controls to comply with the requirements for a foreign private issuer on The Nasdaq Capital Market (“Nasdaq”). While the Company believes it is in full compliance with these requirements, it does not have a long track record on which it can assess the performance and effectiveness of these policies, processes, systems and controls or the analysis of their outputs. Any material inadequacies, weaknesses or failures in BPGIC’s policies, processes, systems and controls could have a material adverse effect on BPGIC’s business, financial condition and results of operations.

14

The fixed cost nature of BPGIC’s operations could result in lower profit margins if certain costs were to increase and BPGIC were not able to offset such costs with sufficient increases in its storage or ancillary service fees or its customers’ utilization of BPGIC’s ancillary services.

BPGIC’s fixed costs for Phase I, Phase II and the BIA Refinery are paid for with the fixed storage fees it receives or will receive, as the case may be, from BIA and the Super Major. BPGIC expects that a large portion of its future expenses related to the operation of the BPGIC Terminal will be relatively fixed because the costs for full-time employees, rent in connection with the Land Leases, maintenance, depreciation, utilities and insurance generally do not vary significantly with changes in users’ needs. However, BPGIC expects that its profit margins could change if its costs change.

In particular, if wages in the region’s oil storage industry were to increase, BPGIC may need to increase the levels of its employee compensation more rapidly than in the past to remain competitive or keep up with increases in general price levels or inflation in the UAE and in Fujairah. If wage costs were to increase at a greater rate than our customers’ utilization of BPGIC’s ancillary services, then such increased wage costs may reduce BPGIC’s profit margins.

The Phase I Customer Agreement provides that every two years, BPGIC may elect to review and seek to amend its storage and ancillary services fees with BIA. The Phase I Customer Agreement provides that the outcome of this review can result only in either an increase in rates or no change. As such, if wages were to increase, BPGIC may yield lower margins for a period of time before it is able to review and amend its storage and ancillary service fees. Furthermore, if BIA does not agree to increase the storage and ancillary service fees, or if the increase is insufficient, then BPGIC may not be able to maintain its profit margins.

The pricing terms for the Refinery Operations Agreement remain subject to negotiation with BIA. If BPGIC is unable to negotiate for periodic price review and increases or if any such increase is insufficient, then BPGIC may not be able to maintain its profit margins.

The Phase II Customer Agreement provides that every two years, BPGIC may elect to seek to amend its storage fee to the applicable market price. The Phase II Customer Agreement provides that the outcome of this amendment can result only in either an increase in rate or no change from the contracted floor price. As such, if wages were to increase, BPGIC may yield lower margins for a period of time before it is able to amend its storage fees. Furthermore, if the increase is insufficient, or BIA does not agree to increase the fees, then BPGIC may not be able to maintain its profit margins.

BPGIC expects that its fixed costs for Phase III will be paid for with the fixed storage fees it will receive from the Phase III customer(s). BPGIC expects that a large portion of its future expenses related to the operation of Phase III will be relatively fixed because the costs for full-time employees, rent in connection with the Phase III Land Lease Agreement, maintenance, depreciation, utilities and insurance generally do not vary significantly with changes in users’ needs. However, as with its fixed costs for Phase I and Phase II, BPGIC expects that its profit margins could change if its costs, in particular wage costs, change.