UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

(Mark one)

OR

For the fiscal year ended

OR

For the transition period from __________ to _________

OR

Date of event requiring this shell company report __________

Commission file number

(Exact name of the Registrant as specified in its charter)

(Jurisdiction of incorporation or organization)

(Address of principal executive offices)

Tel:

Email:

(Name, Telephone, E-mail and/or

Facsimile number and Address

of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol | Name of each exchange on which registered | ||

| The |

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None

(Title of Class)

Indicate the number of outstanding shares of each of the issuer’s

classes of capital or common stock as of the close of the period covered by the annual report:

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

| ☐ Yes | ☒ |

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

| ☐ Yes | ☒ |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

| ☒ | ☐ No |

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

| ☒ | ☐ No |

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

| ☐ Large Accelerated filer | ☐ Accelerated filer | ☒ |

If an emerging

growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected

not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section

13(a) of the Exchange Act.

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark

whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal

control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting

firm that prepared or issued its audit report.

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| ☐ US GAAP | International Financial Reporting | ☐ Other |

| Standards as issued by the International | ||

| Accounting Standards Board |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

| ☐ Item 17 | ☐ Item 18 |

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

| ☐ Yes |

Annual Report on Form 20-F

Year Ended June 30, 2022

TABLE OF CONTENTS

i

ii

CERTAIN INFORMATION

As used in this Annual Report on Form 20-F (the “Annual Report”), unless otherwise indicated or the context otherwise requires, references to

| ● | “we,” “Snow Lake,” “us,” “our,” “the Company,” or “our company” are to Snow Lake Resources Ltd., including its subsidiaries; |

| ● | “common shares” are to our common shares, no par value; and |

| ● | “NASDAQ” are to the Nasdaq Capital Market. |

In this Annual Report on Form 20-F, references to “Canada” are to Canada and its provinces and territories and references to “$,” “USD,” “dollars,” “USD$” or “U.S. dollars” are to the legal currency of the United States and references to “C$,” or “Canadian dollar” are to the legal currency of Canada.

Solely for the convenience of the reader, this Annual Report on Form 20-F contains translations of certain Canadian dollar amounts into U.S. dollars at specified rates. Except as otherwise stated in this Annual Report on Form 20-F, all translations from Canadian dollar to U.S. dollars are based on the closing rate of C$1.2886 per $1.00 for cable transfers of Canadian dollars, as certified by Bank of Canada on June 30, 2022. On October 28, 2022, the noon buying rate for Canadian dollar was 1.3615 per US$1.00. No representation is made that such Canadian dollar amounts referred to in this Annual Report on Form 20-F could have been or could be converted into U.S. dollars at such rates or any other rates. Any discrepancies in any table between totals and sums of the amounts listed are due to rounding.

The audited consolidated financial statements and notes thereto as of and for fiscal 2022, 2021 and 2020 included elsewhere in this Annual Report on Form 20-F have been prepared in accordance with International Financial Reporting Standards, or IFRS. Our fiscal year end is June 30.

Share Consolidation (“Reverse Split”)

On October 7, 2021, we effectuated a one-for-five reverse stock split of our common shares, or the Reverse Split. The Reverse Split combined each five of our common shares into one common share. Fractional shares will not be issued to any existing shareholder in connection with the Reverse Split, but the Company purchased from each existing shareholder the right to such fractional share that would have been issued, at a price based on our initial public offering price. The right to fractional shares which the Company purchased resulting from the Reverse Split, in the aggregate, was less than ten (10) common shares. The historical audited financial statements included elsewhere in this Annual Report on Form 20-F have been adjusted for the Reverse Split. Unless otherwise indicated, all other share and per share data in this Annual Report on Form 20-F have been retroactively adjusted, where applicable, to reflect the Reverse Split as if it had occurred as at the June 30, 2019 fiscal year end. References to “post-consolidation” below are references to the number of our common shares after giving effect to this share consolidation.

FORWARD-LOOKING STATEMENTS

This Annual Report contains many statements that are “forward-looking” and uses forward-looking terminology such as “anticipate,” “believe,” “could,” “estimate,” “expect,” “future,” “intend,” “may,” “ought to,” “plan,” “possible,” “potentially,” “predicts,” “project,” “should,” “will,” “would,” negatives of such terms or other similar statements. You should not place undue reliance on any forward-looking statement due to its inherent risk and uncertainties, both general and specific. Although we believe the assumptions on which the forward-looking statements are based are reasonable and within the bounds of our knowledge of our business and operations as of the date of this Annual Report, any or all of those assumptions could prove to be inaccurate. As a result, the forward-looking statements based on those assumptions could also be incorrect. The forward-looking statements in this Annual Report include, without limitation, statements relating to:

| ● | our goals and strategies; |

| ● | expectations regarding revenue, expenses and operations; |

| ● | our having sufficient working capital and be able to secure additional funding necessary for the continued exploration of our property interests; |

| ● | expectations regarding the potential mineralization, geological merit and economic feasibility of our projects; |

| ● | expectations regarding exploration results at the Snow Lake Lithium™ Project; |

iii

| ● | mineral exploration and exploration program cost estimates; |

| ● | expectations regarding any environmental issues that may affect planned or future exploration programs and the potential impact of complying with existing and proposed environmental laws and regulations; |

| ● | receipt and timing of exploration permits and other third-party approvals; |

| ● | government regulation of mineral exploration and development operations; |

| ● | expectations regarding any social or local community issues that may affected planned or future exploration and development programs; and |

| ● | key personnel continuing their employment with us. |

The forward-looking statements included in this Annual Report are subject to known and unknown risks, uncertainties and assumptions about our businesses and business environments. These statements reflect our current views with respect to future events and are not a guarantee of future performance. Actual results of our operations may differ materially from information contained in the forward-looking statements as a result of risk factors, some of which are described under the headings “Risk Factors”, “Operating and Financial Review and Prospects,” “Information on our Company” and elsewhere in this Annual Report. Such risks and uncertainties are not exhaustive. Other sections of this Annual Report include additional factors which could adversely impact our business and financial performance. The forward-looking statements contained in this Annual Report speak only as of the date of this Annual Report or, if obtained from third-party studies or reports, the date of the corresponding study or report, and are expressly qualified in their entirety by the cautionary statements in this Annual Report. Since we operate in an emerging and evolving environment and new risk factors and uncertainties emerge from time to time, you should not rely upon forward-looking statements as predictions of future events. Except as otherwise required by the securities laws of the United States, we undertake no obligation to update or revise any forward-looking statements to reflect events or circumstances after the date of this Annual Report or to reflect the occurrence of unanticipated events.

iv

PART I

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable.

ITEM 3. KEY INFORMATION

3.A. [Reserved]

3.B. Capitalization and Indebtedness

Not applicable.

3.C. Reasons for the Offer and Use of Proceeds

Not applicable.

3.D. Risk factors

You should carefully consider all of the information in this report, including various changing regulatory, competitive, economic, political and social risks and conditions described below, before making an investment in our common shares. One or more of a combination of these risks could materially impact our business, results of operations and financial condition. In any such case, the market price of our common shares could decline, and you may lose all or part of your investment.

Summary Risk Factors

Risks Related to Our Business and Industry

Risks and uncertainties related to our business and industry include, but are not limited to, the following:

| ● | We have a limited operating history and have not yet generated any revenues; | |

| ● | Our financial statements have been prepared on a going concern basis and our financial status creates a doubt whether we will continue as a going concern; | |

| ● | If we do not obtain additional financing, our business may be at risk or execution of our business plan may be delayed; | |

| ● | The coronavirus pandemic may cause a material adverse effect on our business; | |

| ● | All of our business activities are now in the exploration stage and there can be no assurance that our exploration efforts will result in the commercial development of lithium hydroxide; | |

| ● | Our mineral resources described in our most recent S-K 1300 compliant indicated and inferred mineral resource report are only estimates and no assurance can be given that the anticipated tonnages and grades will be achieved, or that the indicated level of recovery will be realized. Although S-K 1300 compliant, there has been insufficient drilling on the Snow Lake Lithium™ property to qualify our inferred resource under the SEC’s new Mining Modernization Rules. Further drilling will be required to determine whether the Snow Lake Lithium™ property contains proven or probable mineral reserves and there can be no assurance that we will be successful in our efforts to prove our resource; |

| ● | Mineral exploration and development are subject to extraordinary operating risks. We currently do not insure against these risks. In the event of a cave-in or similar occurrence, our liability may exceed our resources, which could have an adverse impact on us; | |

| ● | Our business operations are exposed to a high degree of risk associated with the mining industry; | |

| ● | We may not be able to obtain or renew licenses or permits that are necessary to our operations; |

1

| ● | Our Snow Lake Lithium™ property may face indigenous land claims; | |

| ● | Volatility in lithium prices and lithium demand may make it commercially unfeasible for us to develop our Snow Lake Lithium™ Project; | |

| ● | There can be no guarantee that our interest in the Snow Lake Lithium™ property is free from any title defects; | |

| ● | Our mining operations are dependent on the adequate and timely supply of water, electricity or other power supply, chemicals and other critical supplies; | |

| ● | We currently report our financial results under International Financial Reporting Standards, or IFRS, which differs in certain significant respect from U.S. generally accepted accounting principles; | |

| ● | Our directors and officers are engaged in other business activities and accordingly may not devote sufficient time to our business affairs, which may affect our ability to conduct operations and generate revenue; and | |

| ● | In the event that key personnel leave our company, we would be harmed since we are heavily dependent upon them for all aspects of our activities. | |

| ● | Adverse outcomes in our new litigation matters that arise in the future, could negatively affect our business, results of operations, financial condition and cash flows. |

Risks Related to the Ownership of Our Common Shares

Risks and uncertainties related to our Common Shares include, but are not limited to, the following:

| ● | If through additional drilling we are not able to prove our resource according to the SEC’s new Mining Modernization Rules, your investment in our common shares could become worthless; | |

| ● | You may experience difficulties in effecting service of legal process, enforcing foreign judgments or bringing actions against us or our management named in the report based on foreign laws; | |

| ● | We are a foreign private issuer within the meaning of the rules under the Exchange Act, and as such we are exempt from certain provisions applicable to U.S. domestic public companies; | |

| ● | As a foreign private issuer, we are permitted to rely on exemptions from certain Nasdaq corporate governance standards applicable to domestic U.S. issuers. This may afford less protection to holders of our shares; | |

| ● | A major shareholder, Nova Minerals Ltd., or Nova, owns a significant interest in our outstanding common shares. As a result, it will have the ability to influence all matters submitted to our shareholders for approval; and | |

| ● | Future issuances of debt securities, which would rank senior to our common shares upon our bankruptcy or liquidation, and future issuances of preferred shares, which could rank senior to our common shares for the purposes of dividends and liquidating distributions, may adversely affect the level of return you may be able to achieve from an investment in our common shares. |

Risks Related to Our Business and Industry

We have a limited operating history and have not yet generated any revenues.

Our limited operating history makes evaluating our business and future prospects difficult and may increase the risk of your investment. We were formed in May 2018 and we have not yet begun commercial production of lithium hydroxide. To date, we have no revenues. We are in the exploration stage of our development with the potential to establish commercial operations still an unknown. We intend to proceed with the development of the Snow Lake Lithium™ property through to economic studies such as a PFS and provided the results are positive, through to mine development. We intend in the longer term to derive substantial revenues from becoming a strategic supplier of battery-grade lithium hydroxide to the growing electric vehicle and battery storage markets. Our company is in the exploration stage, and we do not expect to start generating revenues until the fourth quarter of 2024, at the earliest. Our planned exploration and development of mineral resources, primarily lithium, will require significant investment prior to commercial introduction and may never be successfully developed or commercially successful.

2

Our financial statements have been prepared on a going concern basis and our financial status creates a doubt whether we will continue as a going concern.

Our financial statements have been prepared on a going concern basis under which an entity is considered to be able to realize its assets and satisfy its liabilities in the ordinary course of business. Our future operations are dependent upon the identification and successful completion of equity or debt financing and the achievement of profitable operations at an indeterminate time in the future. There can be no assurances that we will be successful in completing an equity or debt financing or in achieving or maintaining profitability. The financial statements do not give effect to any adjustments relating to the carrying values and classification of assets and liabilities that would be necessary should we be unable to continue as a going concern.

If we do not obtain additional financing, our business may be at risk or execution of our business plan may be delayed.

We have limited assets upon which to commence our business operations and to rely otherwise. As of June 30, 2022, we had cash of C$23,792,408 (approximately US$18,463,765) and during the fiscal years ended June 30, 2022, June 30, 2021, and 2020, we had a net loss of C$9,446,454 (approximately US$7,330,788), C$552,436 (approximately US$428,710) and C$182,116 (approximately US$141,329), respectively. On November 18, 2021, we completed our initial public offering of common shares on the Nasdaq resulting in net proceeds of US$25.29 million. Additional funding will be needed to implement our business plan that includes various expenses such as continuing our mining exploration program, legal, operational set-up, general and administrative, marketing, employee salaries and other related start-up expenses. Obtaining additional funding will be subject to various factors, including general market conditions, investor acceptance of our business plan and ongoing results from our exploration efforts. These financings could result in substantial dilution to the holders of our common shares, or require contractual or other restrictions on our operations or on alternatives that may be available to us. If we raise additional funds by issuing debt securities, these debt securities could impose significant restrictions on our operations. Any such required financing may not be available in amounts or on terms acceptable to us, and the failure to procure such required financing could have a material and adverse effect on our business, financial condition and results of operations, or threaten our ability to continue as a going concern.

We may not be able to acquire additional funds on acceptable terms, or at all. If we are unable to raise adequate funds, we may have to delay, reduce the scope of or eliminate some or all of our planned exploration programs. If we do not have, or are not able to obtain, sufficient funds, we may be required to delay further exploration, development or commercialization of our expected mineral resources, if and when verified. We also may have to reduce the resources devoted to our mining efforts or cease operations. Any of these factors could harm our operating results.

The coronavirus pandemic may cause a material adverse effect on our business.

The COVID-19 outbreak has led governments across the globe to impose a series of measures intended to contain its spread, including border closures, travel bans, quarantine measures, social distancing, and restrictions on business operations and large gatherings. On March 11, 2020, the federal government of Canada announced a $1 billion package to help Canadians through the health crisis. To date, there have been a large number of temporary business closures, quarantines and a general reduction in consumer activity in Canada.

As a result of the measures adopted by the Province of Manitoba and the federal government of Canada, certain of our mining exploration activities have been delayed. The access to investor capital as well as the potential for a 14-day quarantine when travelling into the Province of Manitoba have discouraged us from engaging in certain exploration activities in the near term. As a result of these unexpected delays, we had placed our focus on completing lab work and technical report writing using the field data that we have previously compiled. In August 2021, members of our team made a site visit to Manitoba and conducted mapping and prospecting and in October 2021 additional members of our team visited the site. In February 2022, a drilling program began at the site that is ongoing as of the date of filing.

The spread of the virus in many countries continues to adversely impact global economic activity and has contributed to significant volatility and negative pressure in financial markets and supply chains. The pandemic has had, and could have a significantly greater, material adverse effect on the Canadian economy as a whole, as well as the local economy where we conduct our operations. The pandemic has resulted, and may continue to result for an extended period, in significant disruption of global financial markets, which may reduce our ability to access capital in the future, which could negatively affect our liquidity.

3

If the current pace of the pandemic does not continue to slow and the spread of the virus is not contained, our business operations could be further delayed or interrupted. We expect that government and health authorities may announce new or extend existing restrictions, which could require us to make further adjustments to our operations in order to comply with any such restrictions. We may also experience limitations in employee resources. In addition, our operations could be disrupted if any of our employees were suspected of having the virus, which could require quarantine of some or all such employees or closure of our facilities for disinfection. We may also delay or reduce certain capital spending and related projects until the travel and logistical impacts of the pandemic are lifted, which will delay the completion of such projects. The duration of any business disruption cannot be reasonably estimated at this time but may materially affect our ability to operate our business and result in additional costs.

The extent to which the pandemic may impact our results will depend on future developments, which are highly uncertain and cannot be predicted as of the date of this report, including the effectiveness of vaccines and other treatments and other new information that may emerge concerning the severity of the pandemic and steps taken to contain the pandemic or treat its impact, among others. Nevertheless, the pandemic and the current financial, economic and capital markets environment, and future developments in the global lithium mining and other areas present material uncertainty and risk with respect to our performance, financial condition, results of operations and cash flows.

To the extent the pandemic adversely affects our business and financial results, it may also have the effect of heightening many of the other risks described in this “Risk Factors” section.

Our business is subject to operational risks that are generally outside of our control and could adversely affect our business.

Mineral mining sites, like the sites where our Snow Lake Lithium™ property is located, by their nature are subject to many operational risks and factors that are generally outside of our control and could adversely affect our business, operating results and cash flows. These operational risks and factors include the following:

| ● | unanticipated ground and water conditions; |

| ● | adverse claims to water rights and shortages of water to which we have rights; |

| ● | adjacent land ownership that results in constraints on current or future operations; |

| ● | geological problems, including earthquakes and other natural disasters; |

| ● | metallurgical and other processing problems; |

| ● | the occurrence of unusual weather or operating conditions and other force majeure events; |

| ● | lower than expected ore grades or recovery rates; |

| ● | accidents; |

| ● | delays in the receipt of or failure to receive necessary government permits; |

| ● | the results of litigation, including appeals of agency decisions; |

| ● | uncertainty of exploration and development; |

| ● | delays in transportation; |

| ● | interruption of energy supply; |

| ● | labor disputes; |

| ● | inability to obtain satisfactory insurance coverage; and |

| ● | the failure of equipment or processes to operate in accordance with specifications or expectations. |

Any one or more of these factors or other risks could cause us not to realize the anticipated benefits of an acquisition of properties or companies and could have a material adverse effect on our financial condition.

4

All of our business activities are now in the exploration stage and there can be no assurance that our exploration efforts will result in the commercial development of lithium hydroxide.

All of our operations are at the exploration stage and there is no guarantee that any such activity will result in commercial production of lithium mineral deposits. Very limited drilling has been conducted on our Snow Lake Lithium™ property to date, which makes the extrapolation of an S-K 1300 compliant indicated or inferred resource to an S-K 1300 probable or proven reserve and to commercial viability impossible without further drilling. We intend to engage in that additional exploratory drilling with proceeds from our initial public offering but we can provide no assurance of future success from our planned additional drilling program. The exploration for lithium deposits involves significant risks which even a combination of careful evaluation, experience and knowledge may not eliminate. While the discovery of an ore body may result in substantial rewards, few properties which are explored are ultimately developed into producing mines. Major expenses may be required to locate and establish proven mineral reserves, to develop metallurgical processes and to construct mining and processing facilities at a particular site. It is impossible to ensure that the exploration programs planned by us or any future development programs will result in a profitable commercial mining operation. There is no assurance that our mineral exploration activities will result in any discoveries of commercial quantities of lithium. There is also no assurance that, even if commercial quantities of ore are discovered, a mineral property will be brought into commercial production. Whether a mineral deposit will be commercially viable depends on a number of factors, some of which are: the particular attributes of the deposit, such as size, grade and proximity to infrastructure, metal prices which are highly cyclical; and government regulations, including regulations relating to prices, taxes, royalties, land tenure, land use, importing and exporting of minerals and environmental protection. The exact effect of these factors cannot be accurately predicted. Our long-term profitability will be in part directly related to the cost and success of our exploration programs and any subsequent development programs.

Our mineral resources or reserves may be significantly lower than expected.

We are in the exploration stage and our planned principal operations have not commenced. There is currently no commercial production on the Snow Lake Lithium™ property and we have not yet completed a preliminary feasibility study. As such, our estimated proven or probable mineral reserves, expected mine life and lithium pricing cannot be determined as the exploration program, drilling, feasibility studies and pit (or mine) design optimizations have not yet been undertaken, and the actual mineral reserves may be significantly lower than expected. You should not rely on the S-K 1300 compliant technical report, or PFS, if and when completed and published, as indications that we will have successful commercial operations in the future. Even if we prove reserves on the Snow Lake Lithium™ property, we cannot guarantee that we will be able to develop and market them, or that such production will be profitable.

The estimation of lithium reserves is not an exact science and depends upon a number of subjective factors. Any indicated or inferred resource figures presented in this report are estimates from the written reports of technical personnel and mining consultants who were contracted to assess the mining prospects. Resource estimates are a function of geological and engineering analyses that require us to forecast production costs, recoveries, and metals prices. The accuracy of such estimates depends on the quality of available data and of engineering and geological interpretation, judgment, and experience. Estimated indicated or inferred lithium resources may not be upgraded to indicated or measured or to probable or proved reserves, and any reserves may not be realized in actual production and our operating results may be negatively affected by inaccurate estimates. Additionally, resource estimates do not determine the economics of a mining project and, although we have begun to prepare a preliminary feasibility study, even once the PFS is produced we cannot guarantee that it will reflect positive economics for our mining resources or that we will be able to execute our plans to create an economically viable mining operation.

Our mineral resources described in our most recent S-K 1300 compliant indicated and inferred mineral resource report are only estimates and no assurance can be given that the anticipated tonnages and grades will be achieved, or that the indicated level of recovery will be realized.

We intend to continue exploration on our Snow Lake Lithium™ property and we may or may not acquire additional interests in other mineral properties. The search for mineral deposits as a business is extremely risky. We can provide investors with no assurance that exploration on our current properties, or any other property that we may acquire, will establish that any commercially exploitable quantities of mineral deposits exist. Additional potential problems may prevent us from discovering any mineral deposits. These potential problems include unanticipated problems relating to exploration and additional costs and expenses that may exceed current estimates. If we are unable to establish the presence of viable lithium mineral deposits on our properties, our ability to fund future exploration activities will be impeded, we will not be able to operate profitably and investors may lose all of their investment in our company.

We have no history of mineral production.

We are an exploration stage company and we have no history of mining or refining mineral products from our properties. As such, any future revenues and profits are uncertain. There can be no assurance that our Snow Lake Lithium™ Project will be successfully placed into production, produce minerals in commercial quantities or otherwise generate operating earnings. Advancing projects from the exploration stage into development and commercial production requires significant capital and time and will be subject to further technical studies, permitting requirements and construction of mines, processing plants, roads and related works and infrastructure. We will continue to incur losses until mining-related operations successfully reach commercial production levels and generate sufficient revenue to fund continuing operations. There is no certainty that we will generate revenue from any source, operate profitably or provide a return on investment in the future.

5

Lithium mining and production is relatively new to the Province of Manitoba and the Snow Lake area.

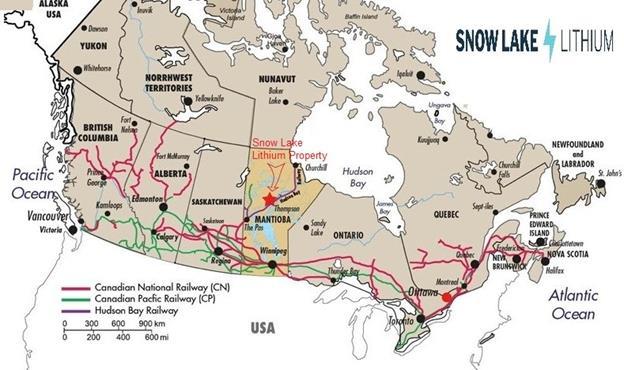

If and when our lithium resources on the Snow Lake Lithium™ property are proven, we intend to work towards entering the production stage of our operations. We intend not to use diesel or gasoline fuel for any of our mining, sorting and concentrating activities. This means that the sorting and concentrating of, and the production of our spodumene lithium into a lithium hydroxide will be conducted through a fully electrified process, potentially not using any fossil fuels to generate the electrical power needed to run our operations. Lithium mining has occurred at the Tanco mine located north east of Winnipeg, but the mining and processing of lithium ore has not previously been undertaken in or near the Snow Lake region of Manitoba. Locating the necessary experts and work force that are familiar with and trained in this particular mining process may be a challenge and our success may be hindered by the lack of historical familiarity with the processes and challenges faced in lithium mining and production.

Mineral exploration and development are subject to extraordinary operating risks. We currently do not insure against these risks. In the event of a cave-in or similar occurrence, our liability may exceed our resources, which could have an adverse impact on us.

Exploration and mining operations generally involve a degree of risk. Our operations are subject to all of the hazards and risks normally encountered in the exploration, development and production of rare earth metals, including, without limitation, unusual and unexpected geologic formations, seismic activity, rock bursts, cave-ins, flooding and other conditions involved in the drilling and removal of material, any of which could result in damage to, or destruction of, mines and other producing facilities, personal injury or loss of life and damage to property and environmental damage, all of which may result in possible legal liability. Although we expect that adequate precautions to minimize risk will be taken, mining operations are subject to hazards such as fire, rock falls, geo-mechanical issues, equipment failure or failure of retaining dams around tailings disposal areas which may result in environmental pollution and consequent liability. The occurrence of any of these events could result in a prolonged interruption of our operations that would have a material adverse effect on our business, financial condition, results of operations and prospects.

The exploration for and development of mineral deposits involves significant risks, which even a combination of careful evaluation, experience and knowledge may not eliminate. While the discovery of a mineral deposit may result in substantial rewards, few properties that are explored are ultimately developed into producing mines. Major expenses may be required to locate and establish mineral resources and reserves, to develop metallurgical processes and to construct mining and processing facilities and infrastructure at a particular site. It is impossible to ensure that the exploration or development programs planned by us will result in a profitable commercial mining operation. Whether a mineral deposit will be commercially viable depends on a number of factors, some of which are: the particular attributes of the deposit, such as size, grade and proximity to infrastructure, metal prices that are highly cyclical, and government regulations, including regulations relating to prices, taxes, royalties, land tenure, land use, importing and exporting of minerals and environmental protection. The exact effect of these factors cannot be accurately predicted, but the combination of these factors may result in our company not receiving an adequate return on invested capital. There is no certainty that the expenditures made towards the search and evaluation of mineral deposits will result in the discovery of mineral resources or the development of commercial quantities of mineral reserves.

Our development projects have no operating history upon which to base estimates of future capital and operating costs. Mineral resource and reserve estimates and estimates of operating costs are, to a large extent, based upon the interpretation of geologic data obtained from drill holes and other sampling techniques, and feasibility studies, which derive estimates of capital and operating costs based upon anticipated tonnage and grades to be mined and processed, ground conditions, the configuration of the deposit, expected recovery rates of minerals from ore, estimated operating costs, and other factors. As a result, actual production, cash operating costs and economic returns could differ significantly from those estimated.

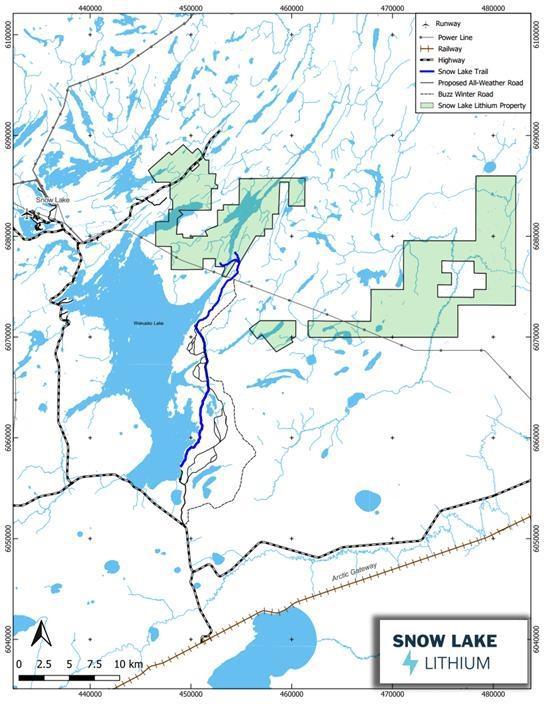

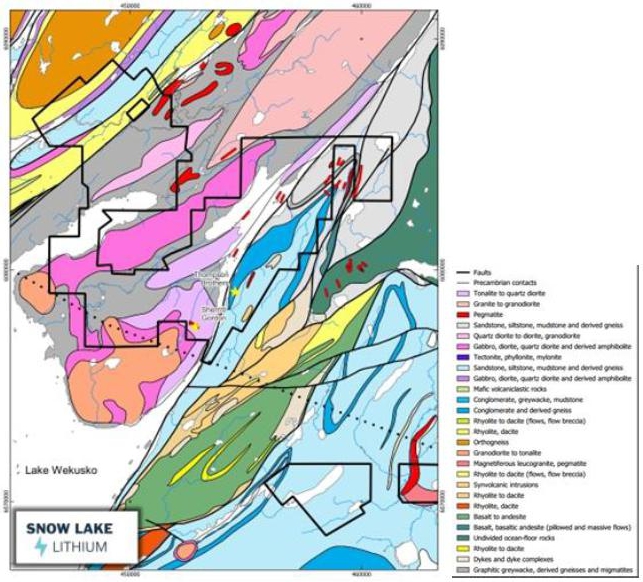

There are numerous risks associated with the development of the Snow Lake Lithium™ property.

Our future success will largely depend upon our ability to successfully explore, develop and manage the Snow Lake Lithium™ property. In particular, our success is dependent upon management’s ability to implement our strategy, to develop the project and to maintain ongoing lithium production from the mines that we expect to develop.

Development of the Snow Lake Lithium™ property could be delayed, experience interruptions, incur increased costs or be unable to complete due to a number of factors, including but not limited to:

| ● | changes in the regulatory environment including environmental compliance requirements; |

| ● | non-performance by third party consultants and contractors; |

6

| ● | inability to attract and retain a sufficient number of qualified workers; |

| ● | unforeseen escalation in anticipated costs of exploration and development, or delays in construction, or adverse currency movements resulting in insufficient funds being available to complete planned exploration and development; |

| ● | increases in extraction costs including energy, material and labor costs; |

| ● | lack of availability of mining equipment and other exploration services; |

| ● | shortages or delays in obtaining critical mining and processing equipment; |

| ● | catastrophic events such as fires, storms or explosions; |

| ● | the breakdown or failure of equipment or processes; |

| ● | construction, procurement and/or performance of the processing plant and ancillary operations falling below expected levels of output or efficiency; |

| ● | civil unrest in and/or around the mine site and supply routes, which would adversely affect the community support of our operations; |

| ● | changes to anticipated levels of taxes and imposed royalties; and/or |

| ● | a material and prolonged deterioration in lithium market conditions, resulting in material price erosion. |

It is not uncommon for new mining developments to experience these factors during their exploration or development stages or during construction, commissioning and production start-up, or indeed for such projects to fail as a result of one or more of these factors occurring to a material extent. There can be no assurance that we will complete the various stages of exploration and development necessary in order to achieve our strategy in the timeframe pre-determined by us or at all. Any of these factors may have a material adverse effect on our business, results of operations and activities, financial condition and prospects.

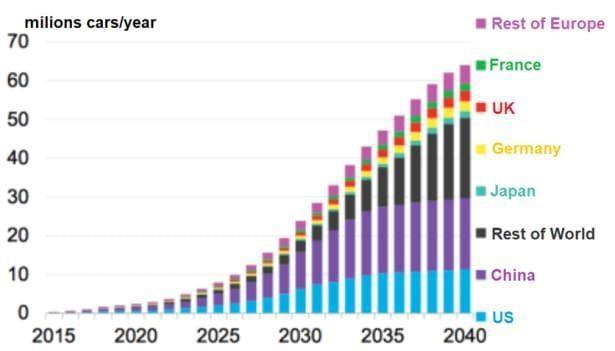

Changes in technology and future demand may result in an adverse effect on our results of operation.

Currently lithium is a key metal used in batteries, including those used in electric vehicles. However, the technology pertaining to batteries, electric vehicles and energy creation and storage is changing rapidly and there is no assurance lithium will continue to be used to the same degree as it is now, or that it will be used at all. Any decline in the use of lithium ion batteries or technologies utilizing such batteries may result in a material and adverse effect on our future profitability, results of operation and financial condition.

Our business operations are exposed to a high degree of risk associated with the mining industry.

Our business operations are exposed to a high degree of risk inherent in the mining sector. Risks which may occur during the exploration and development of mineral resources include environmental hazards, industrial accidents, equipment failure, import/customs delays, shortage or delays in installing and commissioning plant and equipment, metallurgical and other processing problems, seismic activity, unusual or unexpected formations, formation pressures, rock bursts, wall failure, cave ins or slides, burst dam banks, flooding, fires, explosions, power outages, opposition with respect to mining activities from individuals, communities, governmental agencies and non-governmental organizations, interruption to or the increase in costs of services, cave-ins and interruption due to inclement or hazardous weather conditions.

Commencement of mining can also reveal mineralization or geologic formations, including higher than expected content of other minerals that can be difficult to separate from rare earth metals, which can result in unexpectedly low recovery rates.

Such occurrences could cause damage to, or destruction of properties, personal injury or death, environmental damage, pollution, delays, increased production costs, monetary losses and potential legal liabilities. Moreover, these factors may result in a mineral deposit, which has been mined profitably in the past to become unprofitable. They are also applicable to sites not yet in production and to expanded operations. Successful mining operations will be reliant upon the availability of processing and refining facilities and secure transportation infrastructure at the rate of duty over which we may have limited or no control. Any liabilities that we incur for these risks and hazards could be significant and the costs of rectifying the hazard may exceed our asset value.

7

Infrastructure required to carry on our business may be affected by unusual or infrequent weather phenomena, sabotage, government or other interference in the maintenance or provision of such infrastructure.

Exploitation of the Snow Lake Lithium™ property will depend to a significant degree on adequate infrastructure. In the course of developing our expected operations, assuming our exploration efforts will be successful, we may need to construct and support the construction of infrastructure, which includes permanent gas pipelines, water supplies, power, transport and logistics services which affect capital and operating costs. Unusual or infrequent weather phenomena, sabotage, government or other interference in the maintenance or provision of such infrastructure or any failure or unavailability in such infrastructure could materially adversely affect our operations, financial condition and results of operations.

We may not be able to obtain or renew licenses or permits that are necessary to our operations.

In the ordinary course of business, we will be required to obtain and renew governmental licenses or permits for exploration, development, construction and commencement of mining at the Snow Lake Lithium™ property. Obtaining or renewing the necessary governmental licenses or permits is a complex and time-consuming process involving public hearings and costly undertakings on the part of our company. The duration and success of our efforts to obtain and renew licenses or permits are contingent upon many variables not within our control, including the interpretation of applicable requirements implemented by the licensing and/or permitting authorities. We may not be able to obtain or renew licenses or permits that are necessary to our operations, including, without limitation, an exploitation license, or the cost to obtain or renew licenses or permits may exceed what we believe we can recover from the Snow Lake Lithium™ property. Any unexpected delays or costs associated with the licensing or permitting process could delay the development or impede the operation of a mine, which could adversely impact our operations and profitability.

The Snow Lake Lithium™ property may face indigenous land claims

The Snow Lake Lithium™ property may now or in the future be the subject of indigenous land claims. The legal nature of land claims is a matter of considerable complexity. The impact of any such claim on our ownership interest in the Snow Lake Lithium™ property cannot be predicted with any degree of certainty and no assurance can be given that a broad recognition of indigenous rights in the area in which the Snow Lake Lithium™ property is located, by way of a negotiated settlement or judicial pronouncement, would not have an adverse effect on our operations. Even in the absence of such recognition, we may at some point be required to negotiate with, and seek the approval of holders of, such interests in order to facilitate exploration and development work on the Snow Lake Lithium™ property. There is no assurance that we will be able to establish a practical working relationship with the indigenous groups in the area which would allow us to ultimately develop the Snow Lake Lithium™ property.

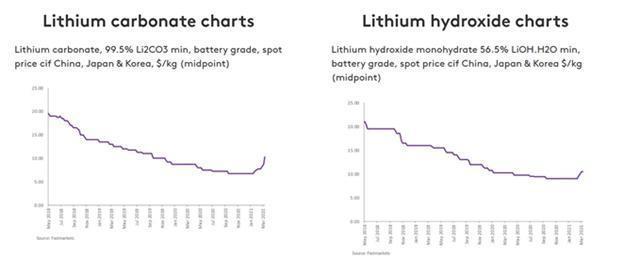

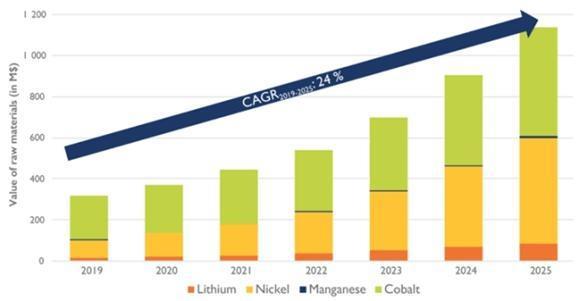

Volatility in lithium prices and lithium demand may make it commercially unfeasible for us to develop our Snow Lake Lithium™ Project.

The development of our Snow Lake Lithium™ Project is dependent on the continued growth of the lithium market, and the continued increased demand for lithium chemicals by emerging producers of electric vehicles and other users of lithium-ion batteries. These producers and the related technologies are still under development and a continued sustained increase in demand is not certain. To the extent that such demand does not manifest itself, and the lithium market does not continue to grow, or existing producers increase supply to satisfy this demand, then our ability to develop our Snow Lake Lithium™ Project will be adversely affected. Our lithium exploration and development activities may be significantly adversely affected by volatility in the price of lithium. Mineral prices fluctuate widely and are affected by numerous factors beyond our control such as global and regional supply and demand, interest rates, exchange rates, inflation or deflation, fluctuation in the value of the United States dollar and foreign currencies, and the political and economic conditions of mineral-producing countries throughout the world. The exact effect of these factors cannot be accurately predicted, but the combination of these factors may result in our lithium activities not producing an adequate return on invested capital to be profitable or viable.

There can be no guarantee that our interest in the Snow Lake Lithium™ property is free from any title defects.

We have taken all reasonable steps to ensure it has proper title to the Snow Lake Lithium™ property. However, there can be no guarantee that our interest in the Snow Lake Lithium™ property is free from any title defects, as title to mineral rights involves certain intrinsic risks due to the potential problems arising from the unclear conveyance history characteristic of many mining projects. There is also the risk that material contracts between us and relevant government authorities will be substantially modified to the detriment of us or be revoked. There can be no assurance that our rights and title interests will not be challenged or impugned by third parties.

Our mining operations are dependent on the adequate and timely supply of water, electricity or other power supply, chemicals and other critical supplies.

Our exploration programs are dependent on the adequate and timely supply of water, electricity or other power supply, chemicals and other critical supplies. If we are unable to obtain the requisite critical supplies in time and at commercially acceptable prices or if there are significant disruptions in the supply of electricity, water or other inputs to the mine site, our business performance and results of operations may experience material adverse effects.

8

We may experience an inability to attract or retain qualified personnel.

Our success depends to a large degree upon our ability to attract, retain and train key management personnel, as well as other technical personnel. If we are not successful in retaining or attracting such personnel, our business may be adversely affected. Furthermore, the loss of our key management personnel could materially and adversely affect our business and operations.

As our business becomes more established, it will also be required to recruit additional qualified key financial, administrative, operations and marketing personnel. There will be no guarantee that we will be able to attract and keep such qualified personnel and if we are not successful, it could have a material and adverse effect on our business and results from operations.

Failure to comply with federal, provincial and/or local laws and regulations could adversely affect our business.

Our mining operations are subject to various laws and regulations governing exploration, development, production, taxes, labor standards and occupational health, mine safety, protection of endangered and protected species, toxic substances and explosives use, reclamation, exports, price controls, waste disposal and use, water use, forestry, land claims of local people, and other matters. This includes periodic review and inspection of the Snow Lake Lithium™ property that may be conducted by applicable regulatory authorities.

Although the exploration activities on the Snow Lake Lithium™ property have been and, we expect, will continue to be carried out in accordance with all applicable laws and regulations, there is no guarantee that new laws and regulations will not be enacted or that existing laws and regulations will not be applied in a way which could limit or curtail exploration or in the future, production. New laws and regulations or amendments to current laws and regulations governing the operations and activities of mining or more stringent implementation of existing laws and regulations could have a material adverse effect on us and cause increases in capital expenditures costs, or reduction in levels of exploration, development and/or production.

Failure to comply with applicable laws and regulations, even if inadvertent, may result in enforcement actions thereunder, including orders issued by regulatory or judicial authorities causing operations to cease or be curtailed, and may include corrective measures requiring capital expenditures, installation of additional equipment or remedial actions. We may also be required to reimburse any parties affected by loss or damage caused by our mining activities and may have civil or criminal fines and/or penalties imposed against us for infringement of applicable laws or regulations.

Failure to comply with environmental regulation could adversely affect our business.

All phases of our operations with respect to the Snow Lake Lithium™ property will be subject to environmental regulation. Environmental legislation involves strict standards and may entail increased scrutiny, fines and penalties for non-compliance, stringent environmental assessments of proposed projects and a high degree of responsibility for companies and their officers, directors and employees. Changes in environmental regulation, if any, may adversely impact our operations and future potential profitability. In addition, environmental hazards may exist on the Snow Lake Lithium™ property that are currently unknown. We may be liable for losses associated with such hazards, or may be forced to undertake extensive remedial cleanup action or to pay for governmental remedial cleanup actions, even in cases where such hazards have been caused by previous or existing owners or operators of the properties, or by the past or present owners of adjacent properties or by natural conditions. The costs of such cleanup actions may have a material adverse impact on our operations and future potential profitability.

Failure to comply with applicable laws, regulations, and permitting requirements may result in enforcement actions thereunder, including orders issued by regulatory or judicial authorities causing operations to cease or be curtailed, and may include corrective measures requiring capital expenditures, installation of additional equipment, or remedial actions. Parties engaged in mining operations may be required to compensate those suffering loss or damage by reason of the mining activities and may have civil or criminal fines or penalties imposed for violations of applicable laws or regulations and, in particular, environmental laws.

We currently report our financial results under IFRS, which differs in certain significant respect from U.S. generally accepted accounting principles.

We report our financial statements under IFRS. There have been and there may in the future be certain significant differences between IFRS and United States generally accepted accounting principles, or U.S. GAAP, including differences related to revenue recognition, intangible assets, share-based compensation expense, income tax and earnings per share. As a result, our financial information and reported earnings for historical or future periods could be significantly different if they were prepared in accordance with U.S. GAAP. In addition, we do not intend to provide a reconciliation between IFRS and U.S. GAAP unless it is required under applicable law. As a result, you may not be able to meaningfully compare our financial statements under IFRS with those companies that prepare financial statements under U.S. GAAP.

9

Our assets and operations are subject to economic, geopolitical and other uncertainties.

Economic, geopolitical and other uncertainties may negatively affect our business. Economic conditions globally are beyond our control. In addition, the outbreak of hostilities and armed conflicts between countries can create geopolitical uncertainties that may affect both local and global economies. Downturns in the economy or geopolitical uncertainties may cause future customers to delay or cancel projects, reduce their overall capital or operating budgets or reduce or cancel orders which could have a material adverse effect on our business, results of operations and financial condition.

Our operations may be affected in varying degrees by government regulations with respect to, but not limited to, restrictions on production, price controls, export controls, currency remittance, income taxes, foreign investment, maintenance of claims, environmental legislation, land use, land claims of local people, water use and mine safety. Failure to comply strictly with applicable laws, regulations and local practices relating to mineral rights, could result in loss, reduction or expropriation of entitlements.

In addition, the financial markets can experience significant price and value fluctuations that can affect the market prices of equity securities and other companies in ways that are unrelated to the operating performance of these companies. Broad market fluctuations, as well as economic conditions generally, may adversely affect the market price of our common shares.

As we face intense competition in the mineral exploration and exploitation industry, there can be no assurance that we will be able to compete effectively with other companies.

The mining industry, and the lithium mining sector in particular, is very competitive. Our competition is from larger, established mining companies with greater liquidity, greater access to credit and other financial resources, newer or more efficient equipment, lower cost structures, more effective risk management policies and procedures and/or a greater ability than us to withstand losses. Our competitors may be able to respond more quickly to new laws or regulations or emerging technologies, or devote greater resources to the expansion or efficiency of their operations than we can. In addition, current and potential competitors may make strategic acquisitions or establish cooperative relationships among themselves or with third parties. Accordingly, it is possible that new competitors or alliances among current and new competitors may emerge and gain significant market share to our detriment.

As a result of this competition, we may have to compete for financing and be unable to acquire financing on terms we consider acceptable. we may also have to compete with the other mining companies for the recruitment and retention of qualified managerial and technical employees. If we are unable to successfully compete for financing or for qualified employees or we may not be able to compete successfully against current and future competitors, and any failure to do so could have a material adverse effect on our business, financial condition, results of operations and future prospects as well as our exploration programs may be slowed down or suspended, which may cause us to cease operations as a company.

Our executive officers are engaged in other business activities and, accordingly, may not devote sufficient time to our business affairs, which may affect our ability to conduct operations.

Our executive officers are engaged as consultants under independent contractor agreements rather than as employees and, as such, they have been and are involved in other business activities. Our VP of Resource Development may also be engaged in the exploration program of our majority shareholder, Nova, and our Chief Executive Officer and our Chief Operating Officer each have consulting clients in addition to working for us. Although we expect that as our business operations ramp up our executive officers will devote substantially all of their time to our business, as a result of the other business endeavors that they are currently engaged in, our executive officers may not be able to devote sufficient time to our business affairs, which may negatively affect our ability to conduct our ongoing operations. In addition, management of our company may be periodically interrupted or delayed as a result of these officers’ other business interests.

We may be subject to potential conflicts of interest.

We may be subject to potential conflicts of interests, as certain directors of our company are, and may continue to be, engaged in the mining industry through their participation in corporations, partnerships or joint ventures, which are potential competitors of our company. Situations may arise in connection with potential acquisitions in investments where the other interests of these directors and officers may conflict with the interests of our company. Our directors and officers with conflicts of interest will be subject to the procedures set out in the related Canadian law and regulations.

10

We may not meet cost estimates.

A change in the timing of any projected cash flows due to capital funding or, once in production, production shortfalls or labor disruptions would result in delays in receipt of such cash flows and in using such cash to fund operating activities and, as applicable, reduce debt levels. This could result in additional loans to finance capital expenditures in the future.

The level of capital and operating cost estimates which are used for determining and obtaining financing and other purposes are based on certain assumptions and are fundamentally subject to considerable uncertainties. It is very likely that actual results for the Snow Lake Lithium™ property will differ from our current projections, estimates and assumptions, and these differences may be significant. Moreover, experience from actual mining may identify new or unexpected conditions that could decrease operational activities, and/or increase capital and/or operating costs above, the current estimates. If actual results are less favorable than we currently estimate, our business, results from operations, financial condition and liquidity could be materially adversely affected.

We may pursue opportunities to acquire complementary businesses, which could dilute our shareholders’ ownership interests, incur expenditure and have uncertain returns.

We may seek to expand through future acquisitions of either companies or properties, however, there can be no assurance that we will locate attractive acquisition candidates, or that we will be able to acquire such candidates on economically acceptable terms, if at all, or that we will not be restricted from completing acquisitions pursuant to contractual arrangements. Future acquisitions may require us to expend significant amounts of cash, resulting in our inability to use these funds for other business or may involve significant issuances of equity. Future acquisitions may also require substantial management time commitments, and the negotiation of potential acquisitions and the integration of acquired operations could disrupt our business by diverting management and employees’ attention away from day-to-day operations. The difficulties of integration may be increased by the necessity of coordinating geographically diverse organizations, integrating personnel with disparate backgrounds and combining different corporate cultures.

Any future acquisition involves potential risks, including, among other things: (i) mistaken assumptions and incorrect expectations about mineral properties, mineral resources and costs; (ii) an inability to successfully integrate any operation our company acquires; (iii) an inability to recruit, hire, train or retain qualified personnel to manage and operate the operations acquired; (iv) the assumption of unknown liabilities; (v) limitations on rights to indemnity from the seller; (vi) mistaken assumptions about the overall cost of equity or debt; (vii) unforeseen difficulties operating acquired projects, which may be in geographic areas new to us; and (viii) the loss of key employees and/or key relationships at the acquired project.

At times, future acquisition candidates may have liabilities or adverse operating issues that we may fail to discover through due diligence prior to the acquisition. If we consummate any future acquisitions with unanticipated liabilities or that fails to meet expectations, our business, results of operations, cash flows or financial condition may be materially adversely affected. The potential impairment or complete write-off of goodwill and other intangible assets related to any such acquisition may reduce our overall earnings and could negatively affect our balance sheet.

Legal proceedings may arise from time to time in the course of our business.

Legal proceedings may arise from time to time in the course of our business. Such litigation may be brought from time to time in the future against us. Defense and settlement costs of legal claims can be substantial, even with respect to claims that have no merit. Other than as disclosed elsewhere in this report, we are not currently subject to material litigation nor have we received an indication that any material claims are forthcoming. However, due to the inherent uncertainty of the litigation process, we could become involved in material legal claims or other proceedings with other parties in the future. The results of litigation or any other proceedings cannot be predicted with certainty. The cost of defending such claims may take away from management’s time and effort and if we are incapable of resolving such disputes favorably, the resultant litigation could have a material adverse impact on our financial condition, cash flow and results from operation.

11

Adverse outcomes in our new litigation matters that arise in the future, could negatively affect our business, results of operations, financial condition and cash flows.

Our Company is the respondent in two Motions for injunction. See “Item 4. Information On The Company - B. Business Overview - Legal Proceedings” for further details. Snow Lake Lithium filed a Withdrawal of the Registration Statement on Form F-1 (File No. 333-267600) in response to the Court of King’s Bench (Manitoba) (the “Court”) issuing an order enjoining the Company from issuing any securities prior to October 27, 2022, the record date for the determination of shareholders entitled to vote at the Company’s annual general meeting (“AGM”) set for December 15, 2022. The court order was issued at the request of a group of concerned shareholders on Thursday, September 29, 2022. The outcome of litigation and other legal proceedings that the Company may be involved in the future, is difficult to assess or quantify. Defense and settlement costs can be substantial, even with respect to claims that have no merit. Due to the inherent uncertainty of the litigation process, the litigation process could take away from the time and effort of the Company’s management and could force the Company to pay substantial legal fees. Any conclusion of these matters in a manner adverse to us could have a material adverse effect on our business, results of operation, financial condition and cash flows. For example, we may be required to pay substantial damages, incur payments of fines and penalties, suffer a significant adverse impact on our reputation, and management’s attention and resources may be diverted from other priorities, including the execution of business plans and strategies that are important to our ability to grow our business, any of which could have a material adverse effect on our business. If we do not have sufficient funds to settle or pay any damages and costs with respect to any lawsuits, this would have a material adverse effect on our business, financial condition and results of operation.

Land reclamation requirements may be burdensome.

Land reclamation requirements are generally imposed on companies with mining operations or mineral exploration companies in order to minimize long term effects of land disturbance. Reclamation may include requirements to control dispersion of potentially deleterious effluents or reasonably re-establish pre-disturbance landforms and vegetation. In order to carry out reclamation obligations imposed on us in connection with exploration, potential development and production activities, we must allocate financial resources that might otherwise be spent on exploration and development programs. If we are required to carry out unanticipated reclamation work, our financial position could be adversely affected.

In the event that key personnel leave our company, we would be harmed since we are heavily dependent upon them for all aspects of our activities.

We are heavily dependent on our officers and directors, the loss of whom could have, in the short-term, a negative impact on our ability to conduct our activities and could cause additional costs from a delay in the exploration and development of our Snow Lake Lithium™ property.

The obligations associated with being a public company require significant resources and management attention, and we incur significant costs as a result of being a public company.

As a public company, we face increased legal, accounting, administrative and other costs and expenses that we did not incur as a private company. We are subject to the reporting requirements of the Exchange Act, which requires that we file annual and other reports with respect to our business and financial condition, as well as the rules and regulations implemented by the SEC, the Sarbanes-Oxley Act, the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010, the Public Company Accounting Oversight Board, and the continued listing requirements of Nasdaq, each of which imposes additional reporting and other obligations on public companies. As a public company, we are required to, among other things:

| ● | prepare and file annual and other reports in compliance with the federal securities laws; |

| ● | expand the roles and duties of our board of directors and committees thereof and management; |

| ● | hire additional financial and accounting personnel and other experienced accounting and finance staff with the expertise to address complex accounting matters applicable to public companies; |

| ● | institute more comprehensive financial reporting and disclosure compliance procedures; |

| ● | involve and retain, outside counsel and accountants to assist us with the activities listed above; |

| ● | build and maintain an investor relations function; |

| ● | establish new internal policies, including those relating to trading in our securities and disclosure controls and procedures; |

| ● | comply with the initial listing and maintenance requirements of Nasdaq; and |

| ● | comply with the Sarbanes-Oxley Act. |

12

We expect these rules and regulations, and any future changes in laws, regulations and standards relating to corporate governance and public disclosure, which have created uncertainty for public companies, to continue to incur legal and financial compliance costs and make some activities more time consuming and costly than for private companies. These laws, regulations and standards are subject to varying interpretations, in many cases, due to their lack of specificity, and, as a result, their application in practice may evolve over time as new guidance is provided by regulatory and governing bodies. This could result in continuing uncertainty regarding compliance matters and higher costs necessitated by ongoing revisions to disclosure and governance practices. Our investment in compliance with existing and evolving regulatory requirements will result in increased administrative expenses and a diversion of management’s time and attention from revenue-generating activities to compliance activities, which could have a material adverse effect on our business, financial condition and results of operations.

Risks Related to the Ownership of Our Common Shares

An active market in which investors can resell their common shares may not be available.

Our common shares were listed and began trading on the Nasdaq Capital Market on November 19, 2021 under the symbol “LTIM.” Prior to the listing, there was no public market for our common shares. A liquid public market for our common shares may not sufficiently develop. The prices at which our securities are traded may decline, meaning that you may experience a decrease in the value of your common shares regardless of our operating performance or prospects.

The market price of our common shares may fluctuate, and you could lose all or part of your investment.

The market price for our common shares has been volatile, in part because our shares do not have a substantial history of trading publicly. In addition, the market price of our common shares may fluctuate significantly in response to several factors, most of which we cannot control, including:

| ● | actual or anticipated variations in our operating results; |

| ● | increases in market interest rates that lead investors of our common shares to demand a higher investment return; |

| ● | changes in earnings estimates; |

| ● | changes in market valuations of similar companies; |

| ● | actions or announcements by our competitors; |

| ● | adverse market reaction to any increased indebtedness we may incur in the future; |

| ● | additions or departures of key personnel; |

| ● | actions by shareholders; |

| ● | announcement’s by Government, or general market confidence; and |

| ● | our ability to maintain the listing of our common shares on Nasdaq. |

| ● | speculation in the media, online forums, or investment community; |

Volatility in the market prices of our securities may prevent investors from being able to sell their securities at or above their purchase price. As a result, you may suffer a loss on your investment.

We may not be able to maintain a listing of our common shares on Nasdaq.

Although our common shares are listed on Nasdaq, we must meet certain financial and liquidity criteria to maintain such listing. If we violate Nasdaq’s listing requirements, or if we fail to meet any of Nasdaq’s listing standards, our common shares may be delisted. In addition, our board of directors may determine that the cost of maintaining our listing on a national securities exchange outweighs the benefits of such listing. A delisting of our common shares from Nasdaq may materially impair our shareholders’ ability to buy and sell our common shares and could have an adverse effect on the market price of, and the efficiency of the trading market for, our common shares. The delisting of our common shares could significantly impair our ability to raise capital and the value of your investment.

On September 19, 2022, we received a letter from the staff of the Listing Qualifications Department of the Nasdaq Stock Market LLC stating the Company is no longer in compliance with Nasdaq’s audit committee requirement as set forth in Listing Rule 5605 due to the removal of Mr. Nachum Labkowski from the Company’s audit committee on September 7, 2022. Mr. Labkowski was also removed as member of the nominating and corporate governance committee. He remains as an independent director of our board of directors.

The letter also states that Nasdaq will provide the Company a cure period in accordance with Listing Rule 5605(c)(4). Pursuant to Nasdaq Listing Rule 5605(c)(4), the Company is entitled to a cure period to regain compliance, such cure period to expire on the earlier of the Company’s next annual shareholders’ meeting or September 7, 2023; provided, however, that if the Company’s next annual shareholders’ meeting is held before March 6, 2023, then the Company must evidence compliance no later than March 6, 2023.

13

The receipt of the Notification Letter has no immediate effect on the listing of the Company’s common shares, which will continue to trade uninterrupted on Nasdaq under the ticker “LITM”. We are working with the relevant authorities to remedy this issue and is conducting a search for a new director who meets the requirements of Nasdaq and is available for appointment to the Company’s board of directors and audit committee within the cure period. The Company must also submit to Nasdaq documentation, including biographies of any new directors, evidencing compliance with the listing rule within the cure period.

We do not expect to declare or pay dividends in the foreseeable future.

We do not expect to declare or pay dividends in the foreseeable future, as we anticipate that we will invest future earnings in the development and growth of our business. Therefore, holders of our common shares will not receive any return on their investment unless they sell their securities, and holders may be unable to sell their securities on favorable terms or at all.

If securities industry analysts do not publish research reports on us, or publish unfavorable reports on us, then the market price and market trading volume of our common shares could be negatively affected.

Any trading market for our common shares may be influenced in part by any research reports that securities industry analysts publish about us. We may not obtain further research coverage by securities industry analysts. If no further securities industry analysts commence coverage of us, the market price and market trading volume of our common shares could be negatively affected. In the event we are covered by more analysts, and one or more of such analysts downgrade our shares, or otherwise reports on us unfavorably, or discontinues coverage of us, the market price and market trading volume of our common shares could be negatively affected.

You may experience difficulties in effecting service of legal process, enforcing foreign judgments or bringing actions against us or our management named in the report based on foreign laws.