UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the fiscal year ended December 31 , 2022

OR

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from to

Commission file number 001-38858

(Exact name of registrant as specified in its charter)

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||||||||

(Address of Principal Executive Offices) | (Zip Code) | |||||||||||||

Registrant's telephone number, including area code: (210 ) 678-3700

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Trading Symbol | Name of each exchange on which registered | ||||||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the Registrant is a well-known seasoned issuer, as identified in Rule 405 of the Securities Act. Yes x No ☐

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ☐ No x

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ☐

Indicate by check mark whether the Registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit such files). Yes x No ☐

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

☒ | Accelerated filer | ☐ | |||||||||

Non-accelerated filer | ☐ | Smaller reporting company | |||||||||

Emerging growth company | |||||||||||

If an emerging growth company, indicate by check mark if the Registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the Registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the Registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the Registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

The aggregate market value of the common stock held by non-affiliates of the Registrant, as of June 30, 2022, the last business day of the Registrant’s most recently completed second fiscal quarter, was approximately $1,006,381,554 .

The Registrant had 27,616,064 shares of common stock outstanding as of February 28, 2023.

DOCUMENTS INCORPORATED BY REFERENCE

| Document | Parts into which Incorporated | ||||

| Portions of the registrant’s Proxy Statement relating to the 2023 Annual Meeting of Stockholders to be held on May 24, 2023. | Part III | ||||

TABLE OF CONTENTS

| Page | ||||||||

CAUTIONARY NOTICE REGARDING FORWARD-LOOKING STATEMENTS

Certain statements made in this Annual Report on Form 10-K (“Annual Report”) include forward-looking statements, which reflect our current expectations and projections about future events and financial trends that we believe may affect our business, financial condition and results of operations. These forward-looking statements speak only as of the date of this Annual Report and are subject to a number of risks, uncertainties and assumptions described under the sections entitled “Business,” “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “Financial Statements and Supplementary Data” and elsewhere in this Annual Report.

Forward-looking statements include, but are not limited to, statements with respect to the nature of our strategy and capabilities, the vertical and regional expansion of our market and business opportunities, and the expansion of our product offerings in the future. Statements that include words like “believe,” “expect,” “anticipate,” “intend,” “plan,” “seek,” “estimate,” “could,” “potentially” or similar expressions are forward-looking statements and reflect future predictions that may not be correct, even though we believe they are reasonable. These statements are not guarantees of future performance and involve risks and uncertainties that are difficult to predict or are beyond our control. A number of important factors could cause actual outcomes and results to differ materially from those expressed in these forward-looking statements. Consequently, readers should not place undue reliance on such forward-looking statements. In addition, these forward-looking statements relate to the date on which they are made.

The forward-looking statements reflect our current expectations and are based on information currently available to us and on assumptions we believe to be reasonable. Forward-looking information is subject to known and unknown risks, uncertainties and other factors that may cause our actual results, activities, performance or achievements to be materially different from that expressed or implied by such forward-looking statements.

Factors to consider when evaluating these forward-looking statements include, but are not limited to:

•Our business is highly dependent on automotive sales and production volumes.

•We currently rely on one distributor for sales of our products in China.

•A material portion of our business is in China, which may be an unpredictable market and is currently suffering trade tensions with the U.S.

•We must continue to attract, retain and develop key personnel.

•We could be impacted by disruptions in supply.

•Our accounting estimates and risk management processes rely on assumptions or models that may prove inaccurate.

•We must maintain an effective system of internal control over financial reporting to keep stockholder confidence.

•Our industry is highly competitive.

•Our North American market is currently designed for the public’s use of car dealerships to purchase automobiles which may dramatically change.

•Our revenue could be impacted by growing use of ride-sharing or other alternate forms of car ownership.

•We must be effective in developing new lines of business and new products to maintain growth.

•Any disruptions in our relationships with independent installers and new car dealerships could harm our sales.

•Our strategy related to acquisitions and investments could be unsuccessful or consume significant resources.

•We must maintain and grow our network of sales, distribution channels and customer base to be successful.

•We are exposed to a wide range of risks due to the multinational nature of our business.

•We must continue to manage our rapid growth effectively.

•We are subject to claims and litigation in the ordinary course of our business, including product liability and warranty claims.

1

•We must comply with a broad and complicated regime of domestic and international trade compliance, anti-corruption, economic, intellectual property, cybersecurity, data protection and other regulatory regimes.

•We may seek to incur substantial indebtedness in the future.

•Our growth may be dependent on the availability of capital and funding.

•Our Common Stock could decline or be downgraded at any time.

•Our stock price has been, and may continue to be, volatile.

•We may issue additional equity securities that may affect the priority of our Common Stock.

•We do not currently pay dividends on our Common Stock.

•Shares eligible for future sale may depress our stock price.

•Anti-takeover provisions could make a third party acquisition of our Company difficult.

•Our directors and officers have substantial control over us.

•Our bylaws may limit investors’ ability to obtain a favorable judicial forum for disputes.

•The COVID-19 pandemic could materially affect our business.

•Our business faces unpredictable global, economic and business conditions, including the risk of inflation in various markets.

Although we have attempted to identify important factors that could cause actual actions, events or results to differ materially from those described in forward-looking information, there may be other factors that cause actions, events or results to differ from those anticipated, estimated or intended. The forward-looking information contained herein is made as of the date of this Annual Report and, other than as required by law, we do not assume any obligation to update any forward-looking information, whether as a result of new information, future events or results or otherwise.

You should also read the matters described in “Risk Factors” and the other cautionary statements made in this Annual Report as being applicable to all related forward-looking statements wherever they appear in this Annual Report. The forward-looking statements in this Annual Report may not prove to be accurate and therefore you are encouraged not to place undue reliance on forward-looking statements. You should read this Annual Report completely.

EXPLANATORY NOTE

This Annual Report includes estimates and other statistical data made by independent parties and by us relating to market size and growth and other data about our industry. This data involves a number of assumptions and limitations, and you are cautioned not to give undue weight to such estimates. In addition, projections, assumptions and estimates of our future performance and the future performance of the markets in which we operate are necessarily subject to a high degree of uncertainty and risk.

We own or have rights to trademarks or trade names that we use in connection with the operation of our business, including our corporate names, logos and website names. In addition, we own or have the rights to copyrights, trade secrets and other proprietary rights that protect the content of our products and the formulations for such products. Solely for convenience, some of the trademarks, trade names and copyrights referred to in this report are listed without the ©, ® and ™ symbols, but we will assert, to the fullest extent under applicable law, our rights to our trademarks, trade names and copyrights. Please see “Business -Intellectual Property and Brand Protection” for more information.

Other trademarks and trade names in this Annual Report are the property of their respective owners.

Unless the context indicates otherwise, all references in this Annual Report to “XPEL,” the “Company,” “we,” “us,” and “our” refer to XPEL, Inc. and its subsidiaries.

SUMMARY OF RISK FACTORS

The following is a summary of the most significant risks and uncertainties that we believe could adversely affect our business, financial condition or results of operations. In addition to the following summary, you

2

should consider the other information set forth in the “Risk Factors” section and the other information contained in this Annual Report.

Operational Risks

•We currently rely on one distributor for our products in China. The loss of this relationship, or a material disruption in sales by this distributor, could severely harm our business.

•A significant percentage of our revenue is generated from our business in China, a market that is associated with certain risks.

•The loss of one or more of our key personnel or our failure to attract and retain other highly qualified personnel in the future, could harm our business.

•A material disruption from our contract manufacturers or suppliers or our inability to obtain a sufficient supply from alternate suppliers, could cause us to be unable to meet customer demands or increase our costs.

•The preparation of our financial statements involves the use of estimates, judgments and assumptions, and our financial statements may be materially affected if such estimates, judgments or assumptions prove to be inaccurate.

Risks Related to Our Business and Industry

•We are highly dependent on the automotive industry. A prolonged or material contraction in automotive sales and production volumes could adversely affect our business, results of operations and financial condition.

•Fluctuations in the cost and availability of raw materials, equipment, labor and transportation could cause manufacturing delays, increase our costs and/or impact our ability to meet customer demand.

•The after-market automotive product supply business is highly competitive. Competition presents an ongoing threat to the success of our Company.

•Harm to our reputation or the reputation of one or more of our products could have an adverse effect on our business.

•Our revenue and operating results may fluctuate, which may make our results difficult to predict and could cause our results to fall short of expectations.

Strategic Risks

•If changes to our existing products or introduction of new products or services do not meet our customers’ expectations or fail to generate revenue, we could lose our customers or fail to generate any revenue from such products or services and our business may be harmed.

•We depend on our relationships with independent installers and new car dealerships and their ability to sell and service our products. Any disruption in these relationships could harm our sales.

•We may not be able to identify, finance and complete suitable acquisitions and investments, and any completed acquisitions and investments could be unsuccessful or consume significant resources.

•If we are unable to maintain our network of sales and distribution channels, it could adversely affect our net sales, profitability and implementation of our growth strategy.

•If we are unable to retain and acquire new customers, our financial performance may be materially and adversely affected.

•We are exposed to political, regulatory, economic and other risks that arise from operating a multinational business.

Legal, Regulatory and Compliance Risks

•We may incur material losses and costs as a result of product liability and warranty claims.

3

•Violations of the U.S. Foreign Corrupt Practices Act and similar anti-corruption laws outside the U.S. could have a material adverse effect on us.

Liquidity Risks

•We may seek to incur substantial indebtedness in the future.

•We cannot be certain that additional financing will be available on reasonable terms when required, or at all.

•Our variable rate indebtedness exposes us to interest rate volatility, which could cause our debt service obligations to increase significantly.

Risks Relating to Common Stock

•If research analysts issue unfavorable commentary or downgrade our Common Stock, the price of our Common Stock and its trading volume could decline.

•Our stock price has been, and may continue to be, volatile.

•We may issue additional equity securities, or engage in other transactions that could dilute our book value or affect the priority of our Common Stock, which may adversely affect the market price of our Common Stock.

•We may issue shares of preferred stock with greater rights than our Common Stock.

•We have not paid any cash dividends in the past and have no plans to pay cash dividends in the future, which could cause our Common Stock to have a lower value than that of similar companies which do not pay cash dividends.

•Shares eligible for future sale may depress our stock price.

General Risk Factors

•Pandemics have in the past and may in the future have a significant negative impact on our financial condition and operations.

•General global and economic business conditions affect demand for our products.

4

Part I

Item 1. Business

Company Overview

Founded in 1997 and incorporated in Nevada in 2003, XPEL has grown from an automotive product design software company to a global provider of after-market automotive products, including automotive surface and paint protection, headlight protection, and automotive window films, as well as a provider of complementary proprietary software. In 2018, we expanded our product offerings to include architectural window film (both commercial and residential) and security film protection for commercial and residential uses, and in 2019 we further expanded our product line to include automotive ceramic coatings.

XPEL began as a software company designing vehicle patterns used to produce cut-to-fit protective film for the painted surfaces of automobiles. In 2007, we began selling automotive surface and paint protection film products to complement our software business. In 2011, we introduced our ULTIMATE protective film product line which, at the time, was the industry’s first protective film with self-healing properties. The ULTIMATE technology allows the protective film to better absorb the impacts from rocks or other road debris, thereby fully protecting the painted surface of a vehicle. The film is described as “self-healing” due to its ability to return to its original state after damage from surface scratches. The launch of the ULTIMATE product catapulted XPEL into several years of strong revenue growth.

Our over-arching strategic philosophy stems from our view that being closer to the end customer in terms of our channel strategy affords us a better opportunity to efficiently introduce new products and deliver tremendous value which, in turn, drives more revenue growth for the Company. Consistent with this philosophy, we have executed on several strategic initiatives including:

2014

•We began our international expansion by establishing an office in the United Kingdom.

2015

•We acquired Parasol Canada, a distributor of our products in Canada.

2016

•We opened our XPEL Netherlands office and established our European headquarters

2017

•We continued our international expansion with the acquisition of Protex Canada Corp., or Protex Canada, a leading franchisor of automotive protective film franchises serving Canada, and

•We opened our XPEL Mexico office.

2018

•We launched our first product offering outside of the automotive industry, a window and security film protection for commercial and residential uses.

5

•We introduced the next generation of our highly successful ULTIMATE line, ULTIMATE PLUS.

•We acquired Apogee Corporation which led to formation of XPEL Asia based in Taiwan.

2019

•We were approved for the listing of our stock on Nasdaq trading under the symbol “XPEL”.

2020

•We acquired Protex Centre, a wholesale-focused paint protection installation business based in Montreal, Canada.

•We expanded our presence in France with the acquisition of certain assets of France Auto Racing.

•We expanded our architectural window film presence with the acquisition of Houston-based Veloce Innovation, a leading provider of architectural films for use in residential, commercial, marine and industrial settings.

2021

•We expanded our presence into numerous automotive dealerships throughout the United States with the acquisition of PermaPlate Film, LLC, a wholesale-focused automotive window film installation and distribution business based in Salt Lake City, Utah.

•We acquired five businesses in the United States and Canada from two sellers as a continuation of our acquisition strategy. These acquisitions allowed us to continue to increase our penetration into mid-range dealerships in the US and solidify our presence in Western Canada.

•We acquired invisiFRAME, Ltd, a designer and manufacturer of paint protection film patterns for bicycles, thus further expanding our non-automotive offerings.

2022

•We expanded our presence in Australia with the purchase of the paint protection film business of our Australian distributor.

Products and Services

Surface and Paint Protection Film Rolls: Our primary products are paint and surface protection films. Most of the products sold are for automotive application which principally protect painted surfaces from rock chips, damage from bug acids and other road debris. Some of the products sold are used for non-automotive applications, such as industrial protection, screen protection or architectural protection. We sell a variety of product lines each with their own unique characteristics, warranty and intended use.

Automotive Surface and Paint Protection

XPEL ULTIMATE PLUS: ULTIMATE PLUS is our flagship clear, thermoplastic polyurethane, or TPU, based product which is a self-healing, stain-resistant film with exceptional clarity and durability.

6

XPEL ULTIMATE FUSION: ULTIMATE FUSION is our newest paint protection film product providing the same benefits as ULTIMATE PLUS but also contains a hydrophobic top-coat which creates a naturally slick surface to repel water and road grime

XPEL STEALTH: STEALTH is a satin-finished paint protection film, made with the same construction as ULTIMATE PLUS. STEALTH is designed to protect surfaces that already have a matte finish or to give otherwise glossy surfaces a matte finish.

TRACWRAP: TRACWRAP is a temporary TPU-based paint protection film, for both do-it-yourself, or DIY, and professional applications, that is designed to be used for a short period of time, including during road trips, vehicle transport or vehicles pending a full installation of our other products such as XPEL ULTIMATE PLUS.

LUX PLUS: LUX PLUS is our flagship clear, TPU-based paint protection film for the Chinese market. Designed and formulated specifically for the demands of China, with excellent self-healing and stain-resistance, it is offered for sale exclusively in that market.

XPEL RX: RX Protection Film provides protection for a variety of surfaces including screens and other electronics and contains silver ions which inhibit the growth of microbes on the film’s surface.

XPEL ARMOR: ARMOR is a thick PVC-based protection film that looks and performs like a spray-on bedliner. It is designed to resist abrasions and punctures from aggressive terrains.

OTHER FILMS: We sell a variety of other specialty films in smaller quantities for select customers or in certain markets, including: LUX-M, MPD and ARES in the Chinese Market and F Series Film in various international markets.

Most of our Surface and Paint Protection films are applied wet and can be installed in bulk or pre-cut using our pattern database accessible by DAP, our SAAS platform. While we sell some pre-cut and Do-It-Yourself products made from these rolls directly to consumers, the vast majority of the products are professionally installed.

Surface and Paint Protection film sales represented approximately 62% of our consolidated revenue for the year ended December 31, 2022.

Automotive Window Film Rolls: We sell several lines of automotive window films, primarily under the XPEL PRIME brand name, which exhibit a range of performance characteristics and appearances, including:

XPEL PRIME XR PLUS: PRIME XR PLUS offers 98% infrared heat rejection developed with multi-layer nano-particle technology. This is our most expensive flagship product with our best specifications and characteristics. It is available in a variety of visible light transmission, or VLT, levels.

XPEL PRIME XR: PRIME XR utilizes a nano-ceramic construction, blocking 88% of infrared heat and does not interfere with radio, cellular or Bluetooth signals like a metallized film.

XPEL PRIME CS: PRIME CS blocks solar heat radiation to keep vehicles at comfortable temperatures and blocks 99% of harmful UV rays. Available in both a black and neutral charcoal color, PRIME CS is designed to remain the same over the years and never fades or turns purple.

OTHER FILMS: We also sell a variety of other automotive window films both under the PRIME brand and on a private-label basis, including: PRIME X-SERIES and PRIME AP in China, PRIME HP, PRIME GL, PRIME SD and more. Generally, these products are lower cost and are sold only in certain markets.

7

Automotive window film sales represented approximately 15% of our consolidated revenue for the year ended December 31, 2022.

Architectural Window Film Rolls: We sell architectural glass solutions for commercial and residential buildings under the VISION brand name, representing our first product set with a fully non-automotive use. Architectural window films come in several broad categories, including:

SOLAR: Solar films are designed to provide solar energy rejection. We offer a variety of films with varying colors, VLTs and price points.

SAFETY & SECURITY: Safety and Security films are clear, thick polyethylene terephthalate, or PET, films to secure glass in the event of a breakage. We offer a variety of thicknesses and offer films with varying adhesive characteristics for different types of installations.

OTHER: In addition to the main categories of SOLAR and SAFETY & SECURITY films, we also offer anti-graffiti, exterior applied and decorative films.

Architectural window film sales represented approximately 2% of our consolidated revenue for the year ended December 31, 2022.

DAP: A key component of our product offering is our DAP platform. DAP is a proprietary SAAS platform and database consisting of over 80,000 vehicle applications used by the Company and its customers to cut automotive protection film into vehicle panel shapes for both paint protection film and window film products.

We commit significant resources to keep the pattern database updated with a goal toward having a pattern for every panel of every vehicle. When new vehicle models are introduced to the market, we strive to create the pattern as soon as possible. Our patterns and software increase installer efficiency and reduce waste.

Our DAP customers pay a monthly access fee to access our proprietary database. Monthly DAP subscriptions represented less than 2% of our consolidated revenue for the year ended December 31, 2022.

Installation and Dealership Services: We offer installation services of our various products directly to retail and wholesale customers through our Company-owned installation facilities in their respective markets and through our dealership services business which provides on-site services to automobile dealerships. Our installation services are primarily automotive film installation but have grown to include architectural film installation in certain markets. Installation services (including product and labor revenue) represented approximately 16% of our consolidated revenue for the year ended December 31, 2022.

Miscellaneous Products, Tools and Pre-Cut Films: We sell a variety of other miscellaneous product sets which include:

PRE-CUT FILM PRODUCTS: While most of our surface protection films, automotive window films and architectural window films are sold as rolls, we also offer to pre-cut them into vehicle specific shapes (if applicable) or cut them into smaller pieces or shapes to aide in the installation or to increase affordability or efficiency for our customers.

XPEL FUSION PLUS CERAMIC COATING: XPEL FUSION PLUS is a hydrophobic, self-cleaning coating that can be applied to paint and paint protection film, wheels and calipers, plastic and trim, upholstery and glass. XPEL FUSION PLUS provides additional protection to these surfaces to enhance their appearance and protect from minor scratches.

8

TOOLS AND ACCESSORIES: We sell a variety of tools and accessories which are used in the installation of our products, including squeegees and microfiber towels, application fluids, plotter cutters, knives and more. Generally, these are offered as a service to our customers to provide one-stop shopping.

MERCHANDISE AND APPAREL: We sell a variety of XPEL-branded merchandise and apparel which helps represent and build our brand.

Strategic Overview

XPEL continues to pursue several key strategic initiatives to drive continued growth. Our global expansion strategy includes establishing a local presence where possible, allowing us to better control the delivery of our products and services. We also add locally based regional sales personnel, leveraging local knowledge and relationships to expand the markets in which we operate.

We seek to increase global brand awareness in strategically important areas, including pursuing high visibility at premium events such as major car shows and high value placement in advertising media consumed by car enthusiasts, to help further expand the Company’s premium brand.

XPEL also continues to expand its delivery channels by acquiring select installation facilities in key markets and acquiring international partners to enhance our global reach. As we expand globally, we strive to tailor our distribution model to adapt to target markets. We believe this flexibility allows us to penetrate and grow market share more efficiently. Our acquisition strategy centers on our belief that the closer the Company is to its end customers, the greater its ability to drive increased product sales. During 2022, we acquired the paint protection film business of our Australian distributor in furtherance of this objective.

We also continue to drive expansion of our non-automotive product portfolio. Our architectural window film segment continues to gain traction. We believe there are multiple uses for protective films and we continue to explore those adjacent market opportunities.

Sales and Distribution

We sell and distribute our products through independent installers, new car dealerships, third-party distributors, Company-owned installation centers, Automobile Original Equipment Manufacturers, Protex Canada’s franchisees, and online.

Independent Installers/New Car Dealerships

We primarily operate by selling a complete turn-key solution directly to independent installers and new car dealerships, which includes XPEL protection films, installation training, access to our proprietary DAP software, marketing support and lead generation. For the year ended December 31, 2022, approximately 65% of the Company’s consolidated revenue was through this channel.

We offer a suite of services to complement our products for our dealers and strive to create value for being an XPEL dealer. We provide access to our proprietary DAP software which, in turn, provides access to pattern libraries that enable cutting our films into specific shapes to aid in their installation. We believe that this software greatly enhances installation efficiency and reduces film waste – a valuable feature to our customers, as their highest cost tends to be labor. Increasingly, DAP is used to manage operations for our dealers, including job management, scheduling and inventory tracking. We also provide marketing and lead generation for our customers by featuring them in our dealer locator on our website. To be considered an Authorized Dealer (and thereby have end customers referred to them), independent installers must employ certified installers and meet other requirements including purchase minimums and more.

9

Our products are primarily utilized for new cars. As such, new car dealerships will likely be involved in the ultimate sale of our products and services. New car dealerships have multiple options to sell our products: 1) outsourcing the installation of film to the after-market which is the most common option; 2) developing an in-house program where they hire and train their own employees to install the product; and, 3) utilizing third party labor to install the product in the dealership facility either on a pre-load basis or after the sale. We are agnostic as to who applies our products to new vehicles. We support all of these options for new car dealerships through the sales and support to our after-market customers, training and support to dealerships who want to build an in-house program and through our Dealership Services business which provides third party installation services at dealership locations primarily on a pre-load basis.

XPEL also offers 24/7 customer service for independent installers and new car dealerships where we provide installation, software and training support via our website and telephone technical support services.

Distributors

In various parts of the world, XPEL operates primarily through third-party distributors under written agreements with the Company to develop a market or a region under our supervision and direction. These distributors may sell to other distributors or customers who ultimately install the product on an end customer’s vehicle. Due to the nature of this channel, product margins are generally less than other channels. For the year ended December 31, 2022, approximately 17% of the Company’s consolidated revenue was through this channel.

In China, we operate through a sole distributor under a distribution agreement, Shanghai Xing Ting Trading Co., Ltd., which we refer to as the China Distributor. Approximately 10% of our consolidated revenue for the year ended December 31, 2022, was derived from sales to the China Distributor.

Through our distribution agreement with the China Distributor entered into on May 31, 2018, the China Distributor has rights to promote, market, distribute, sell and install our products in China. Additionally, we have granted the non-exclusive right to the China Distributor to use our software in connection with customers’ purchases of our products. The China Distributor places orders with us on a prepaid basis at a price set by us, which we may change with 30 days’ notice. Certain of our products have minimum purchase requirements that increase annually.

We have also granted the China Distributor a non-exclusive license to use our brands to promote sales of our products to end-users. The distribution agreement applies to separate product categories, distinguished by their exclusive or non-exclusive relationship with the China Distributor, each for a term of five years, each of which will automatically renew for up to three additional five-year periods unless otherwise terminated by either party with 60 days’ notice.

We consider our relations with the China Distributor to be good, but the loss of our relationship could result in the delay of the distribution and a decrease in marketing of our products in China. For more information, see Risk Factors—We currently rely on one distributor of our products and services in China. The loss of this relationship, or a material disruption in sales by this distributor, could severely harm our business” and “A significant percentage of our revenue is generated from our business in China, a market that is associated with certain risks.”

Company-Owned Installation Centers/Dealership Services

XPEL operates 13 Company-owned installation centers: seven in the United States, three in Canada and one in the United Kingdom. These locations serve wholesale and retail customers in their respective markets. The Company also provides on-site installation services to automobile dealerships throughout

10

the United States and Canada through its dealership services business. This channel represented approximately 15% of the Company’s consolidated revenue for the year ended December 31, 2022.

Some of our Company-owned installation centers are located in geographic areas where we also serve customers in our independent installer/dealership channel, which could be perceived to generate channel conflict. However, we believe these channels have a synergistic relationship with our Company-owned centers supporting independent installers and dealerships by allowing us to implement local marketing, making inventory available locally for fast delivery, offering overflow installation capacity and assisting with training needs. We believe this channel strategy benefits our goal of generating the most revenue possible.

Automobile Original Equipment Manufacturers (“OEMs”)

XPEL sells products, including paint protection film, and provides services, including the installation of paint protection film and pre-delivery inspection to various OEMs. These services are provided in-plant at the OEMs’ facilities or in one of our facilities that is typically adjacent to the OEM’s facility. This channel represented approximately 3% of the Company’s consolidated revenue for the year ended December 31, 2022.

Online and Catalog Sales

XPEL offers certain products such as paint protection kits, car wash products, after-care products and installation tools via its website. Revenues from this channel are negligible but we believe that by offering these products on our website, we increase brand awareness. The revenue from this channel represented less than 1% of the Company’s consolidated revenue for the year ended December 31, 2022.

Competition

The Company principally competes with other manufacturers and distributors of automotive protective film products. While the Company considers itself a product company competing with other product companies, the Company believes its suite of services which accompany the Company’s product offerings including its software, marketing and lead generation to its customers and customer service provide for substantial differentiation from its competitors. Within the market for surface and paint protection film, our principal competitors include Eastman Chemical Company (under the LLumar and Suntek brands) and several other smaller companies. For more information, see Risk Factors—The after-market automotive product supply business is highly competitive. Competition presents an ongoing threat to the success of our Company.

Suppliers

The Company’s products are sourced from a number of suppliers or manufactured by various third-party contract manufacturers. The Company has currently opted to pursue an “asset-light” manufacturing model whereby third-party suppliers and manufacturers are used to supply the Company with the majority of its products. We routinely evaluate building or buying manufacturing assets for some of our products, but we believe that our asset-light model best suits the Company at the present time. The Company’s film products (including paint protection film and automotive and architectural window films) are produced using various roll-to-roll manufacturing processes performed entirely by third parties. The Company internalizes many conversion operations including quality assurance, inspection, rewinding, boxing and packaging for many of its products at its facilities around the world.

The Company’s product lines continue to grow and include both film and non-film products. The products fall into three categories:

11

•Products where we own or license the intellectual property or, “IP” – the Company owns or licenses the underlying IP for product construction or for one or more components of the product and could seek to have the products made at a variety of manufacturing locations. The Company has a perpetual license to United States Patent No. 8,765,263 “Multilayer Polyurethane Protective Films”.

•Products that are made for us on an exclusive basis – the Company does not own all the underlying IP, but has products made by a third party solely for the Company on an exclusive basis.

•Products that we source from suppliers on a non-exclusive basis – the Company does not own the underlying IP but sources products on commercial terms from a third party.

The Company either owns or licenses the relevant IP or has alternative substitutes to continue to operate for the material portion of products sold.

The loss of our relationship with any of our suppliers or contract manufacturers, could result in the delay of the manufacture and delivery of some of our automotive film products. For more information, see Risk Factor—A material disruption from our contract manufacturers or suppliers, or our inability to obtain a sufficient supply of product from alternate suppliers, could cause us to be unable to meet customer demands or increase our costs.

Government Regulation and Legislation

The manufacturing, packaging, storage, distribution, advertising and labeling of our products and our business operations all must comply with extensive federal, state and foreign laws and regulations and consumer protection laws. Governmental regulations also affect taxes and levies, capital markets, healthcare costs, energy usage, international trade, immigration and other labor issues, all of which may have a direct or indirect negative effect on our business and our customers’ and suppliers’ businesses. We are also required to comply with certain federal, state and local laws and regulations and industry self-regulatory codes concerning privacy and data security. These laws and regulations require us to provide customers with our policies on sharing information with third parties, and advance notice of any changes to these policies. Related laws may govern the manner in which we store or transfer sensitive information, or impose obligations on us in the event of a security breach or inadvertent disclosure of such information. International jurisdictions impose different, and sometimes more stringent, consumer and privacy protections.

Our products are subject to export controls, including the U.S. Department of Commerce’s Export Administration Regulations and economic and trade sanctions regulations administered by the U.S. Treasury Department’s Office of Foreign Asset Controls, and similar laws that apply in other jurisdictions in which we distribute or sell our products. Export control and economic sanctions laws include prohibitions on the sale or supply of certain products and services to certain embargoed or sanctioned countries, regions, governments, persons and entities. In addition, various countries regulate the import of certain products, through import permitting and licensing requirements, as well as customs, duties and similar charges, and have enacted laws that could limit our ability to distribute our products. The exportation, re-exportation, and importation of our products, including by our distributors, must comply with these laws or else we may be adversely affected, through reputational harm, government investigations, penalties, and a denial or curtailment of our ability to export our products. Complying with export control and sanctions laws for a particular sale may be time consuming and may result in the delay or loss of sales opportunities. If we are found to be in violation of U.S. sanctions or export control laws, it could result in substantial fines and penalties for us and for the individuals working for us. Changes in export, sanctions or import laws, may delay the introduction and sale of our product in international markets, or, in some cases, prevent the export or import of our products to certain countries, regions,

12

governments, persons or entities altogether, which could adversely affect our business, financial condition and operating results.

We are also subject to various domestic and international anti-corruption laws, such as the U.S. Foreign Corrupt Practices Act and the U.K. Bribery Act, as well as other similar anti-bribery and anti-kickback laws and regulations. These laws and regulations generally prohibit companies and their intermediaries from making improper payments to non-U.S. officials for the purpose of obtaining or retaining business. Our exposure for violating these laws would increase to the extent our international presence expands and as we increase sales and operations in foreign jurisdictions.

Proposed or new legislation and regulations could also significantly affect our business. For example, the European General Data Protection Regulation, or “GDPR”, took effect in May 2018 and applies to all of our products and services used by people in Europe. The GDPR includes operational requirements for companies that receive or process personal data of residents of the European Union that are different from those previously in place in the European Union. In addition, the GDPR requires submission of breach notifications to our designated European privacy regulator and includes significant penalties for non-compliance with the notification obligation as well as other requirements of the regulation. The California Consumer Privacy Act, or AB 375, or CCPA, created new data privacy rights for users, beginning in 2020. Similarly, there are a number of legislative proposals in the European Union, the United States, at both the federal and state level, as well as other jurisdictions that could impose new obligations in areas affecting our business. In addition, some countries are considering or have passed legislation implementing data protection requirements or requiring local storage and processing of data or similar requirements that could increase the cost and complexity of delivering our services.

Environmental Matters

General

We are subject to a variety of federal, state, local and foreign environmental, health and safety laws and regulations governing, among other things, the generation, storage, handling, use and transportation of hazardous materials; the emission and discharge of hazardous materials into the environment; and the health and safety of our employees. The Company is ISO 14001:2015 registered and accredited. We have incurred and expect to continue to incur costs to maintain or achieve compliance with environmental, health and safety laws and regulations. To date, these costs have not been material to the Company.

Recycling

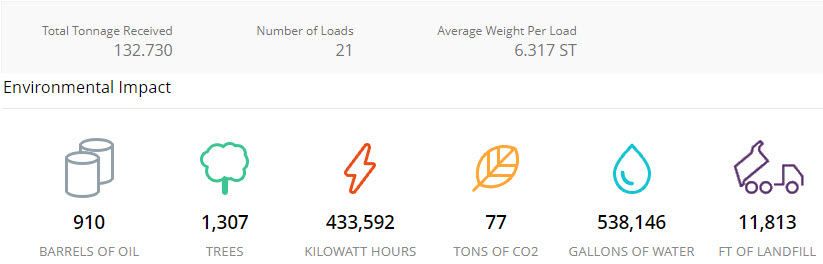

The Company strives to be a good steward of the environment. The Company recycles plastic cores, film waste, corrugated boxes and other material related to our conversion operations. We utilize third party software to monitor our progress on this objective. The following represents a summary of our recycling results and impact to the environment in 2022:

13

Intellectual Property and Brand Protection

We own intellectual property rights, including numerous patents, copyrights and trademarks, that support key aspects of our brand and products. We believe these intellectual property rights, combined with our brand name and reputation, provide us with a competitive advantage. We protect our intellectual property rights in the United States and many international jurisdictions.

We aggressively pursue and defend our intellectual property rights to protect our distinctive brand and products. We have processes and procedures in place to identify and protect our intellectual property assets on a global basis. We utilize legal and brand protection resources to initiate claims and litigation to protect our intellectual property assets. In the future, we intend to continue to seek intellectual property protection for our products and enforce our rights against those who infringe on these valuable assets.

Human Capital Resources

On December 31, 2022, the Company employed approximately 818 people (full-time equivalents), with approximately 567 employed in the United States and 251 employed internationally. We believe that the ability to recruit, retain, develop, protect and fairly compensate our global workforce greatly contributes to the Company’s success.

In addition to a professional work environment that promotes innovation and rewards performance, the Company’s total compensation for employees includes a variety of components that support sustainable employment and the ability to build a strong financial future, including competitive market-based pay and comprehensive benefits. In addition to earning a base salary, eligible employees are compensated for their contributions to the Company’s goals with short-term cash incentives. Through its global pay philosophy, principles and consistent implementation, the Company is committed to providing fair and equitable pay for employees. Eligible full-time employees in the United States also have access to medical, dental and vision plans, savings plans and other resources. Programs and benefits differ internationally for a variety of reasons, such as local legal requirements, market practices and negotiations with work councils, trade unions and other employee representative bodies.

Available Information

XPEL was incorporated in Nevada in 2003. Our street address is 711 Broadway, Suite 320, San Antonio, Texas 78219 and our phone number is (210) 678-3700. The address of our website is www.xpel.com. The inclusion of the Company’s website address in this Annual Report does not include or incorporate by reference the information on or accessible through the Company’s website, and the information contained on or accessible through the website should not be considered as part of this Annual Report.

The Company will make its Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and other reports (and amendments to those reports) filed or furnished pursuant to Section 13(a) of the Securities Exchange Act of 1934, as amended, or the Securities Exchange Act, available on the Company’s website as soon as reasonably practicable after the Company electronically files or furnishes such materials with the Securities and Exchange Commission or, “SEC”. Interested persons can view such materials without charge under the “Investor Relations” section and then by clicking “Corporate Filings / Financial Results” on the Company’s web site. The SEC also maintains a website at www.sec.gov that contains reports, proxy statements and other information about SEC registrants, including XPEL.

Item 1A. Risk Factors

This Annual Report contains forward-looking statements that involve risks and uncertainties. Our actual results could differ materially from those anticipated in these forward-looking statements as a result

14

of certain factors, including the risks we face as described below and elsewhere in this Annual Report. See “Cautionary Notice Regarding Forward-Looking Statements.”

Operational Risks

We currently rely on one distributor of our products and services in China. The loss of this relationship, or a material disruption in sales by this distributor, could severely harm our business.

The Company distributes all of its products in China through one distributor, with sales to such distributor representing approximately 10.5% of our consolidated revenue for the year ended December 31, 2022. The China Distributor places orders with us on a prepaid basis at a price set by us, which we may change with 30 days’ notice. The China Distributor then generates orders, sells and distributes our products to its end customers in China.

Any failure by the China Distributor to perform its obligations, including a failure to procure sufficient orders of our products to satisfy customer demand or a failure to adequately market our products, could have a material adverse effect on our business, financial condition, results of operations and cash flows.

Because of our dependence on the China Distributor, any loss of our relationship or any adverse change in the financial health of such distributor that would affect its ability to distribute our products may have a material adverse effect on our business, financial condition, results of operations and cash flows.

A significant percentage of our revenue is generated from our business in China, a market that is associated with certain risks.

Maintaining a strong position in the Chinese market is a key component of our global growth strategy. During the year ended December 31, 2022, approximately 10.5% of our consolidated revenue was generated in China, more than any other country outside of the U.S. and Canada in which we operate, and we expect to continue to expand our business in China. However, there are risks generally associated with doing business in China, including:

Significant political and economic uncertainties

Historically, the Chinese government has exerted substantial influence over the business activities of private companies. Under its current leadership, the Chinese government has been pursuing economic reform policies that encourage private economic activity and greater economic decentralization. There is no assurance, however, that the Chinese government will continue to pursue these policies, or that it will not significantly alter these policies from time to time without notice. Furthermore, the Chinese government continues to exercise significant control over the Chinese economy through regulation and state ownership. Changes in China’s laws, regulations or policies, including those affecting taxation, currency, imports, or the nationalization of private enterprises could have a material adverse effect on our business, results of operations and financial condition. Furthermore, government actions in the future could have a significant effect on economic conditions in China or particular regions thereof, and could require us to divest ourselves of any interest we then hold in Chinese properties.

Trade policy

In 2018, the U.S. government took the stance that China was engaged in unfair trade practices, and instituted a series of tariffs and other trade barriers on China in response. Though the U.S. and China reached a phase one agreement in January 2020, tension persists between the two countries. The current administration instituted additional export controls in October 2022. Although the current U.S. administration has continued to enforce the phase one agreement, the future of U.S. and Chinese trade relations is uncertain. If the current agreement is abandoned, changed or violated by either party, we

15

could be forced to increase the sales price of our products, reduce margins, or otherwise suffer from trade restrictions or changes in policy levied by the U.S. or Chinese governments, any of which may have a material adverse effect on our business.

Limited recourse in China

While the Chinese government has enacted a legal regime surrounding corporate governance and trade, its history of implementing such laws and regulations is limited. It is unclear how successful any attempt to enforce commercial claims or resolve commercial disputes will be. The resolution of any such dispute may be subject to the exercise of considerable discretion by the Chinese government and its agencies and forces unrelated to the legal merits of a particular matter or dispute may influence their determination.

Additionally, any rights we may have to specific performance, or to seek an injunction under China law are severely limited, and without a means of recourse by virtue of the Chinese legal system, we may be unable to prevent these situations from occurring. The occurrence of any such events could have a material adverse effect on our business, financial condition and results of operations.

Uncertain interpretation of law

There are substantial uncertainties regarding the interpretation and application of the laws and regulations in the greater China area, including, but not limited to, the laws and regulations governing our business. China’s laws and regulations are frequently subject to change due to rapid economic and social development and many of them were newly enacted within the last ten years. The effectiveness of newly enacted laws, regulations or amendments may be delayed, resulting in detrimental reliance by foreign investors. New laws and regulations that affect existing and proposed future businesses may also be applied retroactively.

The Chinese government has broad discretion in dealing with violations of laws and regulations, including levying fines, revoking business permits and other licenses and requiring actions necessary for compliance. In particular, licenses and permits issued or granted to our Company by relevant governmental bodies may be revoked at a later time by higher regulatory bodies. We cannot predict the effect of the interpretation of existing or new Chinese laws or regulations on our businesses. We cannot assure you that our current ownership and operating structure would not be found to be in violation of any current or future Chinese laws or regulations. As a result, we may be subject to sanctions, including fines, and could be required to restructure our operations or cease to provide certain services. In addition, any litigation in China may be protracted and result in substantial costs and diversion of resources and management attention. Any of these or similar actions could significantly disrupt our business operations or restrict us from conducting a substantial portion of our business operations, which could materially and adversely affect our business, financial condition and results of operations.

Management of COVID-19

The Chinese government continues to grapple with COVID-19 in country. Throughout much of 2022, the government enforced a total lockdown in most parts of the country which negatively impacted the Company’s revenue from China. Recently, the lockdowns were lifted resulting in rampant infections across China. We cannot predict the impact of the continuing spread of COVID-19 in China. If COVID-19 persists over the long-term, it could negatively impact our China sales which, in turn, could have a material adverse effect on our business, financial condition, results of operations and cash flows.

16

The loss of one or more of our key personnel, or our failure to attract and retain other highly qualified personnel in the future, could harm our business.

We currently depend on the continued services and performance of our executive officers, Ryan L. Pape, our President and Chief Executive Officer, Barry R. Wood, our Senior Vice President and Chief Financial Officer and Mathieu Moreau, our Senior Vice President, Sales and Product, none of whom has an employment agreement. Loss of key personnel, including members of management as well as key product development, marketing, and sales personnel, could disrupt our operations and have an adverse effect on our business. As we continue to grow, we cannot guarantee that we will continue to attract the personnel we need to maintain our competitive position. As we grow, the incentives to attract, retain, and motivate employees may not be as effective as in the past. If we do not succeed in attracting, hiring, and integrating effective personnel, or retaining and motivating existing personnel, our business could be adversely affected.

A material disruption from our contract manufacturers or suppliers, or our inability to obtain a sufficient supply of product from alternate suppliers, could cause us to be unable to meet customer demands or increase our costs.

If any of our sources of supply were to deteriorate or operations were to be disrupted as a result of disagreements with one or more of our contract manufacturers or suppliers, COVID-19, significant equipment failures, natural disasters, earthquakes, power outages, fires, explosions, terrorism, adverse weather conditions, labor disputes or other reasons, we may be unable to fill customer orders or otherwise meet customer demand for our products. Any such disruption or failure by us to obtain a sufficient supply of our products to satisfy customer demand could increase our costs and reduce our sales, either of which could have a material adverse effect on our business, financial condition, results of operations and cash flows.

Our contract manufacturers and suppliers have been subject to various supply chain disruptions. While these supply chain disruptions have not yet slowed the delivery of products, any such disruption could cause us to not be able to meet demand due to a lack of inventory and/or cause a significant increase in costs of raw materials and shipping costs. Our ability to produce and timely deliver our products may be materially impacted in the future if these supply chain disruptions continue or worsen. In addition, because of rising costs, we may be forced to increase the price of our products to our customers, or we may have to reduce our gross margins on the products that we sell.

Our ability to meet the demand of our customers on a timely basis is dependent upon the quality of film we receive from our contract manufacturers and suppliers. If we are unable to successfully manage the production of quality film produced by our contract manufacturers on a timely basis, our ability to meet the demand of our customers may be severely impacted.

Our asset-light business model exposes us to product quality and variable cost risks

We rely on the ability of contract manufacturers and suppliers to deliver adequate supplies of quality film. If contract manufacturers and suppliers are unable to deliver products that meet quality standards, we may lack recourse or the ability to make the quality improvements ourselves.

Our asset-light model for manufacturing trades lower fixed costs for higher variable costs. If existing or new competitors have lower variable costs, our ability to effectively compete could be impacted.

If we choose to transition away from our asset-light model approach, our capital requirements and capital allocation decisions may fundamentally change which may introduce additional operational, environmental and other risks. In addition, the Company may lack the experience to manage this transition effectively or may lack the appropriate personnel to successfully accomplish this transition.

17

The preparation of our financial statements involves the use of estimates, judgments and assumptions, and our financial statements may be materially affected if such estimates, judgments and assumptions prove to be inaccurate.

Financial statements prepared in accordance with United States Generally Accepted Accounting Principles (“U.S. GAAP” or “GAAP”) require the use of estimates, judgments and assumptions that affect the reported amounts. Different estimates, judgments and assumptions reasonably could be used that would have a material effect on the consolidated financial statements, and changes in these estimates, judgments and assumptions are likely to occur from period to period in the future. Significant areas of accounting requiring the application of management’s judgment include, but are not limited to, determining the fair value of our assets and the timing and amount of cash flows from our assets. These estimates, judgments and assumptions are inherently uncertain and, if they prove to be wrong, we face the risk that charges to income will be required. Any such charges could significantly harm our business, financial condition, results of operations and the price of our securities. Estimates and assumptions are made on an ongoing basis for the following: revenue recognition, capitalization of software development costs, impairment of long-lived assets, inventory reserves, allowances for doubtful accounts, fair value for business combinations, and impairment of goodwill.

If we fail to maintain an effective system of internal control over financial reporting, we may not be able to accurately report our financial results or prevent fraud. As a result, stockholders could lose confidence in our financial and other public reporting, which would likely negatively affect our business and the market price of our Common Stock.

Effective internal control over financial reporting is necessary for us to provide reliable financial reports and prevent fraud. Any failure to implement required new or improved controls, or difficulties encountered in their implementation could cause us to fail to meet our reporting obligations. In addition, any testing conducted by us, or any testing conducted by our independent registered public accounting firm may reveal deficiencies in our internal control over financial reporting that are deemed to be material weaknesses or that may require prospective or retroactive changes to our consolidated financial statements or identify other areas for further attention or improvement. Inferior internal controls could also cause investors to lose confidence in our reported financial information, which is likely to negatively affect our business and the market price of our Common Stock.

Risks Related to Our Business and Industry

We are highly dependent on the automotive industry. A prolonged or material contraction in automotive sales and production volumes could adversely affect our business, results of operations and financial condition.

Automotive sales and production are cyclical and depend on, among other things, general economic conditions, consumer spending, vehicle demand and preferences (which can be affected by a number of factors, including fuel costs, employment levels and the availability of consumer financing). As the volume of automotive production and the mix of vehicles produced fluctuate, the demand for our products may also fluctuate. Prolonged or material contraction in automotive sales and production volumes, or significant changes in the mix of vehicles produced, could cause our customers to reduce purchases of our products and services, which could adversely affect our business, results of operations and financial condition.

Automobile manufacturers continue to experience a global semiconductor shortage which has affected production of vehicles and, in turn, the inventory of vehicles at new car dealerships. To the extent that this shortage persists, it could have a material adverse effect on our business, financial condition, results of operations and cash flows.

18

Fluctuations in the cost and availability of raw materials, equipment, labor and transportation could cause manufacturing delays, increase our costs and/or impact our ability to meet customer demand.

The price and availability of key components used to manufacture our products may fluctuate significantly. Any fluctuations in the cost and availability of any of our products and/or any interruptions in the delivery of our products could harm our gross margins and our ability to meet customer demand. If we are unable to successfully mitigate these cost increases, supply interruptions and/or labor shortages, our results of operations could be affected.

The after-market automotive product supply business is highly competitive. Competition presents an ongoing threat to the success of our Company.

We face significant competition from a number of companies, many of whom have greater financial, marketing and technical resources than us, as well as regional and local companies and lower-cost manufacturers of automotive and other products. Such competition may result in pressure on our profit margins and limit our ability to maintain or increase the market share of our products.

Additionally, as we introduce new products and as our existing products evolve, or as other companies introduce new products and services, we may become subject to additional competition. Our principal competitors have significantly greater resources than we do. This may allow our competitors to respond more effectively than we can to new or emerging technologies and changes in market requirements. Our competitors may also develop products, features, or services that are similar to ours or that achieve greater market acceptance, may undertake more far-reaching and successful product development efforts or marketing campaigns, or may adopt more aggressive pricing policies. Certain competitors could use strong or dominant positions in one or more markets to gain a competitive advantage against us.

We believe that our ability to compete effectively depends upon many factors both within and beyond our control, including:

•the usefulness, ease of use, performance, and reliability of our products compared to our competitors;

•the timing and market acceptance of products, including developments and enhancements to our products or our competitors’ products;

•customer service and support efforts;

•marketing and selling efforts;

•our financial condition and results of operations;

•acquisitions or consolidation within our industry, which may result in more formidable competitors;

•our ability to attract, retain, and motivate talented employees;

•our ability to cost-effectively manage and grow our operations;

•our ability to meet the demands of local markets in high-growth emerging markets, including some in which we have limited experience; and

•our reputation and brand strength relative to that of our competitors.

If we are unable to differentiate or successfully adapt our products, services and solutions from competitors, or if we decide to cut prices or to incur additional costs to remain competitive, it could have a material adverse effect on our business, financial condition, results of operations and cash flows.

19

Harm to our reputation or the reputation of one or more of our products could have an adverse effect on our business.

We believe that maintaining and developing the reputation of our products is critical to our success and that the importance of brand recognition for our products increases as competitors offer products similar to our products. We devote significant time and incur substantial marketing and promotional expenditures to create and maintain brand loyalty as well as increase brand awareness of our products. Adverse publicity about us or our brands, including product safety or quality or similar concerns, whether real or perceived, could harm our image or that of our brands and result in an adverse effect on our business, as well as require resources to rebuild our reputation.

Our revenue and operating results may fluctuate, which may make our results difficult to predict and could cause our results to fall short of expectations.

As a result of the rapidly changing nature of the markets in which we compete, our quarterly and annual revenue and operating results may fluctuate from period to period. These fluctuations may be caused by a number of factors, many of which are beyond our control. For example, changes in industry or third-party specifications may alter our development timelines and consequently our ability to deliver and monetize new or updated products and services. Other factors that may cause fluctuations in our revenue and operating results include:

•any failure to maintain strong customer relationships;

•any failure of significant customers, including distributors, to renew their agreements with us;

•variations in the demand for our services and products and the use cycles of our services and products by our customers;

•changes in our pricing policies or those of our competitors; and

•general economic, industry and market conditions and those conditions specific to our business.

For these reasons and because the market for our services and products is relatively new and rapidly changing, it is difficult to predict our future financial results.

If the model of selling vehicles through dealerships in North America changes dramatically, our revenue could be impacted.

Generally, most vehicles in North America are sold through franchised new car dealerships. These dealerships have a strong profit motive and are historically very good at selling accessories and other products. Going forward, if the dealership model were to change in the form of fewer franchised dealerships, or the possibility of manufacturer owned distribution, the prospects in this channel may diminish. Manufacturer-owned sales of new cars might become harder to penetrate or more streamlined with fewer opportunities to sell accessories. This would make us more reliant on our independent installer, retail-oriented channel, which would require more internal efforts and financial resources to create consumer awareness.

If ride-sharing or alternate forms of vehicle ownership gain in popularity, our revenue could be impacted.

If ride-sharing or alternate forms of vehicle ownership including rental, ride-sharing, or peer-to-peer car sharing gain in popularity, consumers may own fewer vehicles per household, which would reduce our revenue. More vehicles entering a ride-sharing or car-sharing fleet could have an uncertain impact on our revenue as consumers could be less interested in accessorizing vehicles they own that are in the ride-sharing fleet.

20

Technology could render the need for some of our products obsolete.

We derive the majority of our revenue from surface and paint protection films, with the majority of products applied on painted surfaces of vehicles. If automotive paint technology were to improve substantially, such that newer paint did not chip, scratch and was generally not as susceptible to damage, or vehicles were manufactured in a way that no longer required painted surfaces, our revenue could be impacted.

If paint were replaced with other technologies such as film-based products at the point of manufacture, or if machined-based application of paint protection film was developed, the need for paint protection film or the labor services provided by our sales and distribution channels could be reduced.

We create patterns for our DAP platform through a combination of technology and skilled labor. If technology for pattern creation were improved or if paint protection film properties fundamentally changed, our proprietary patterns could become more widely available and our business could be negatively impacted.

Similarly, our automotive and architectural window films could be impacted by changes or enhancements from automotive manufacturers or window manufacturers that would reduce the need for our products.

Infringement of our intellectual property could impact our ability to compete effectively

Our intellectual property, particularly our patterns, are susceptible to being copied without our authorization. We maintain an aggressive approach to defending our intellectual property. If we are unable to adequately protect our intellectual property or if our patterns become widely available without our permission, our revenue could be impacted.

Strategic Risks

If changes to our existing products or introduction of new products or services do not meet our customers’ expectations or fail to generate revenue, we could lose our customers or fail to generate any revenue from such products or services and our business may be harmed.

We may introduce significant changes to our existing products or develop and introduce new and unproven products or services, including using products with which we have little or no prior development or operating experience. The trend of the automotive industry towards autonomous vehicles and car- and ride-sharing services may result in a rapid increase of new and untested products in the aftermarket automotive industry. If new or enhanced products fail to attract or retain customers or to generate sufficient revenue, operating margin, or other value to justify certain investments, our business may be adversely affected. If we are not successful with new approaches to monetization, we may not be able to maintain or grow our revenue as anticipated or recover any associated development costs.

We depend on our relationships with independent installers and new car dealerships and their ability to sell and service our products. Any disruption in these relationships could harm our sales.

The largest portion of our products are distributed through independent installers and new car dealerships. We do not have direct control over the management or the business of these independent installers and new car dealerships, except indirectly through terms as negotiated with us. Should the

21

terms of doing business with them change, our business may be disrupted, which could have an adverse effect on our business, financial condition, results of operations and cash flows.

Because some of our independent installer and new car dealership customers also may offer our competitors’ products, our competitors may incent such customers to favor their products. We do not have long-term contracts with a majority of these independent installers and new car dealerships, and these customers are not obligated to purchase specified amounts of our products but instead buy from us on a purchase order basis. Consequently, the independent installers and new car dealerships may terminate their relationships with us or materially reduce their purchases of our products with little or no notice. If we were to lose any significant independent installers or new car dealerships, for any reason, including if an independent installer and new car dealership acquired or were acquired by a competitor such that they became a direct competitor, then we would need to obtain one or more new independent installers or new car dealerships to cover the particular location or product line, which may not be possible on favorable terms or at all.

We may not be able to identify, finance and complete suitable acquisitions and investments, and any completed acquisitions and investments could be unsuccessful or consume significant resources.