UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

For the quarterly period ended

or

For the transition period from to

Commission File Number

(Exact Name of Registrant as Specified in Its Charter)

| (State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) |

(Address of Principal Executive Offices) (Zip Code)

(

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act: None

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

Securities registered pursuant to Section 12(g) of the Act: Osprey Bitcoin Trust Units

Indicate by check mark whether the registrant (1) has filed

all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months

(or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing

requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically

every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or

for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |

| ☒ | Smaller reporting company | |||

| Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant

has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided

pursuant to Section 13(a) of the Exchange Act.

Indicate by check mark whether the registrant is a shell company

(as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No

Number Units of the registrant outstanding as of October 28th, 2022:

OSPREY BITCOIN TRUST

TABLE OF CONTENTS

STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This Quarterly Report on Form 10-Q contains “forward-looking statements” with respect to the financial conditions, results of operations, plans, objectives, future performance and business of Osprey Bitcoin Trust (the “Trust”). Statements preceded by, followed by or that include words such as “may,” “might,” “will,” “should,” “expect,” “plan,” “anticipate,” “believe,” “estimate,” “predict,” “potential” or “continue,” the negative of these terms and other similar expressions are intended to identify some of the forward-looking statements. All statements (other than statements of historical fact) included in this Quarterly Report that address activities, events or developments that will or may occur in the future, including such matters as changes in market prices and conditions, the Trust’s operations, the plans of Osprey Funds, LLC, the sponsor of the Trust (the “Sponsor”), references to the Trust’s future success and other similar matters are forward-looking statements. These statements are only predictions. Actual events or results may differ materially from such statements. These statements are based upon certain assumptions and analyses the Sponsor made based on its perception of historical trends, current conditions and expected future developments, as well as other factors appropriate in the circumstances. You should specifically consider the numerous risks outlined under “Risk Factors.” Whether or not actual results and developments will conform to the Sponsor’s expectations and predictions, however, is subject to a number of risks and uncertainties, including:

| ● | the risk factors discussed in this Quarterly Report and in “Item 1A. Risk Factors” of the Trust’s Annual Report on Form 10-K for the year ended December 31, 2021, including the particular risks associated with new technologies such as Bitcoin and blockchain technology; |

| ● | the inability to redeem Units; |

| ● | the economic conditions in the Bitcoin industry and market, including any prolonged substantial reduction in Bitcoin prices; |

| ● | general economic, market and business conditions; |

| ● | the use of technology by us and our vendors, including the Custodian (as defined herein), in conducting our business, including disruptions in our computer systems and data centers and our transition to, and quality of, new technology platforms; |

| ● | changes in laws or regulations, including those concerning taxes, made by governmental authorities or regulatory bodies; |

| ● | the costs and effect of any litigation or regulatory investigations; |

| ● | our ability to maintain a positive reputation; and |

| ● | other world economic and political developments, such as the ongoing conflict in Ukraine. |

Consequently, all the forward-looking statements made in this Quarterly Report are qualified by these cautionary statements, and there can be no assurance that the actual results or developments the Sponsor anticipates will be realized or, even if substantially realized, that they will result in the expected consequences to, or have the expected effects on, the Trust’s operations or the value of the Units. Should one or more of the risks discussed under “Item 1A. Risk Factors” in this Quarterly Report or “Item 1A. Risk Factors” of the Trust’s Annual Report on Form 10-K for the year ended December 31, 2021, or other uncertainties materialize, or should underlying assumptions prove incorrect, actual outcomes may vary materially from those described in forward-looking statements. Forward-looking statements are made based on the Sponsor’s beliefs, estimates and opinions on the date the statements are made and neither the Trust nor the Sponsor is under a duty or undertakes an obligation to update forward-looking statements if these beliefs, estimates and opinions or other circumstances should change, other than as required by applicable laws. Moreover, neither the Trust, the Sponsor, nor any other person assumes responsibility for the accuracy and completeness of any of these forward-looking statements.

| 2 |

INDUSTRY AND MARKET DATA

Although we are responsible for all disclosure contained in this Quarterly Report on Form 10-Q, in some cases we have relied on certain market and industry data obtained from third-party sources that we believe to be reliable. Market estimates are calculated by using independent industry publications in conjunction with our assumptions regarding the Bitcoin industry and market. While we are not aware of any misstatements regarding any market, industry or similar data presented herein, such data involves risks and uncertainties and is subject to change based on various factors, including those discussed under the headings “Statement Regarding Forward-Looking Statements.”

| 3 |

PART I – FINANCIAL INFORMATION

Item 1. Financial Statements (Unaudited)

Osprey Bitcoin Trust

Statements of Assets and Liabilities

September 30, 2022 and December 31, 2021

(Amounts in U.S. dollars, except units issued and outstanding)

| September 30, 2022 (Unaudited) | December 31, 2021 | |||||||

| Assets | ||||||||

| Investment in Bitcoin, at fair value (cost $ | $ | $ | ||||||

| Cash | ||||||||

| Total assets | $ | $ | ||||||

| Liabilities | ||||||||

| Management Fee payable | $ | $ | ||||||

| Other payable | ||||||||

| Total liabilities | ||||||||

| Net assets | $ | $ | ||||||

| Net assets | ||||||||

| Paid-in capital | $ | $ | ||||||

| Accumulated net investment loss | ( | ) | ( | ) | ||||

| Accumulated net realized gain on investment in Bitcoin | ||||||||

| Accumulated net change in unrealized appreciation

(depreciation) on investment in Bitcoin | ( | ) | ||||||

| $ | $ | |||||||

| Units issued and outstanding, no par value (unlimited Units authorized) | ||||||||

| Net asset value per Unit | $ | $ | ||||||

The accompanying notes are an integral part of these financial statements.

| 4 |

Osprey Bitcoin Trust

Schedules of Investment

September 30, 2022 and December 31, 2021

(Amounts in U.S. dollars, except units)

| September 30, 2022 (Unaudited) | Units | Fair Value | Percentage of Net Assets | |||||||||

| Investment in Bitcoin, at fair value (cost $ | $ | % | ||||||||||

| Liabilities, less cash | $ | ( | ) | ( | )% | |||||||

| $ | % | |||||||||||

| December 31, 2021 | Units | Fair Value | Percentage of Net Assets | |||||||||

| Investment in Bitcoin, at fair value (cost $ | $ | % | ||||||||||

| Liabilities, less cash | $ | ( | ) | ( | )% | |||||||

| $ | % | |||||||||||

The accompanying notes are an integral part of these financial statements.

| 5 |

Osprey Bitcoin Trust

Statements of Operations

For the three months and nine months ended September 30, 2022 and 2021

(Amounts in U.S. dollars)

| Three months ended September 30, 2022 (Unaudited) | Three months ended September 30, 2021 (Unaudited) | Nine months ended September 30, 2022 (Unaudited) | Nine months ended September 30, 2021 (Unaudited) | |||||||||||||

| Expenses | ||||||||||||||||

| Management Fee | $ | $ | $ | $ | ||||||||||||

| Other | ||||||||||||||||

| Total expenses | ||||||||||||||||

| Other expenses waived by the Sponsor | — | ( | ) | — | ( | ) | ||||||||||

| Net expenses | ||||||||||||||||

| Net investment loss | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||

| Net realized gain (loss) and net change in unrealized appreciation (depreciation) on investment in Bitcoin | ||||||||||||||||

| Net realized gain (loss) on investment in Bitcoin | ( | ) | ( | ) | ||||||||||||

| Net change in unrealized appreciation (depreciation) on investment in Bitcoin | ( | ) | ||||||||||||||

| Total net realized gain (loss) and net change in unrealized appreciation (depreciation) on investment in Bitcoin | ( | ) | ||||||||||||||

| Net increase (decrease) in net assets resulting from operations | $ | $ | $ | ( | ) | $ | ||||||||||

The accompanying notes are an integral part of these financial statements.

| 6 |

Osprey Bitcoin Trust

Statements of Changes in Net Assets

For the three months and nine months ended September 30, 2022 and 2021

(Amounts in U.S. dollars, except units issued and outstanding)

| Three months ended September 30, 2022 (Unaudited) | Three months ended September 30, 2021 (Unaudited) | Nine months ended September 30, 2022 (Unaudited) | Nine months ended September 30, 2021 (Unaudited) | ||||||||||||||

| Increase (decrease) in net assets from operations | |||||||||||||||||

| Net investment loss | $ | ( | ) | $ | ( | ) | $ | ( | ) | $ | ( | ) | |||||

| Net realized gain (loss) on investment in Bitcoin | ( | ) | ( | ) | |||||||||||||

| Net change in unrealized appreciation (depreciation) on investment in Bitcoin | ( | ) | |||||||||||||||

| Net increase (decrease) in net assets resulting from operations | ( | ) | |||||||||||||||

| Increase in net assets from capital transactions | |||||||||||||||||

| Subscriptions | — | — | |||||||||||||||

| Net Increase (decrease) in net assets | ( | ) | |||||||||||||||

| Net assets at the beginning of the period | |||||||||||||||||

| Net assets at the end of the period | $ | $ | $ | $ | |||||||||||||

| Change in units issued and outstanding | |||||||||||||||||

| Units issued and outstanding at the beginning of the period | * | ||||||||||||||||

| Subscriptions | — | — | |||||||||||||||

| Units issued and outstanding at the end of the period | |||||||||||||||||

| * | ||||||||||||||||

The accompanying notes are an integral part of these financial statements.

| 7 |

Osprey Bitcoin Trust

Notes to the Financial Statements (unaudited)

As of September 30, 2022

1. Organization

Osprey Bitcoin Trust (the “Trust”) is a Delaware Statutory Trust, formed on January 3, 2019, which commenced operations on January 22, 2019 and is governed by the Second Amended and Restated Declaration of Trust and Trust Agreement dated November 1, 2020, as amended by the Amendment to Trust Agreement dated April 15, 2022 (the “Trust Agreement”). In general, the Trust holds Bitcoin and, from time to time, issues common units of fractional undivided beneficial interest (“Units”) in exchange for Bitcoin. The investment objective of the Trust is for the Units to track the price of Bitcoin, less liabilities and expenses of the Trust. The Units are designed as a convenient and cost-effective method for investors to gain investment exposure to Bitcoin, similar to a direct investment in Bitcoin.

Osprey Funds, LLC (the “Sponsor”) acts as the sponsor of the Trust. Other funds under the Osprey name are also managed by the Sponsor. The Sponsor is responsible for the day-to-day administration of the Trust pursuant to the provisions of the Trust Agreement. The Sponsor is responsible for preparing and providing annual reports on behalf of the Trust to investors and is also responsible for selecting and monitoring the Trust’s service providers. As consideration for the Sponsor’s services, the Trust pays the Sponsor a Management Fee (as defined herein) as discussed in Notes 2 and 5.

Fidelity Digital Asset Services, LLC was the custodian for the Trust as of and for the year ended December 31, 2021. During March 2022, the Trust changed custodians to Coinbase Custody Trust Company, LLC (the “Custodian”). The Custodian is responsible for safeguarding the Bitcoin held by the Trust.

The transfer agent for the Trust (the “Transfer Agent”) is Continental Stock Transfer & Trust Company. The Transfer Agent is responsible the issuance and redemption of Units, the payment, if any, of distributions with respect to the Units, the recording of the issuance of the Units and the maintaining of certain records therewith.

2. Summary of Significant Accounting Policies

Basis of Presentation

The financial statements are expressed in US dollars and have been prepared in accordance with generally accepted accounting principles in the United States (“GAAP”). The Trust qualifies as an investment company for accounting purposes pursuant to the accounting and reporting guidance under Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) Topic 946, Financial Services – Investment Companies. The Trust is not registered with U.S. Securities and Exchange Commission (“SEC”) under the Investment Company Act of 1940. The results for the nine months ended September 30, 2022 and 2021 are not necessarily indicative of the results for the entire year or any subsequent interim period. These financial statements should be read in conjunction with the audited financial statements and notes thereto included in the Company’s Annual Report on Form 10-K for the year ended December 31, 2021.

Use of Estimates

GAAP requires management to make estimates and assumptions that affect the reported amounts in the financial statements and accompanying notes. The most significant estimate in the financial statements is the fair value of investments in Bitcoin. Actual results could differ from those estimates and these differences could be material.

Cash

Cash is received by the Trust from investors and converted into Bitcoin for investment. Cash held by the Trust represents deposits maintained with Signature Bank (New York). At times, bank deposits may be in excess of federally insured limits. In accordance with ASC 230 “Statement of Cash Flows”, the Trust qualifies for an exemption from the requirement

| 8 |

to provide a statement of cash flows and has elected not to provide a statement of cash flows.

Subscriptions and Redemptions of Units

Proceeds received by the Trust from the issuance and sale of Units consist of Bitcoin deposits and forked or airdropped cryptocurrency coins from the Bitcoin Network, or their respective U.S. dollar cash equivalents. Such Bitcoins (or cash equivalent) will only be (1) owned by the Trust and held by the Custodian (or, if cash, used by the Sponsor to purchase Bitcoins to be held by the Custodian), (2) disbursed (or converted to U.S. dollars, if necessary) to pay the Trust’s expenses, (3) distributed to Accredited Investors (subject to obtaining regulatory approval from the SEC described below) in connection with the redemption of Units, (4) distributed (or converted to U.S. dollars, prior to distribution, to Unitholders as dividends, and (5) liquidated in the event that the Trust terminates or as otherwise required by law or regulation.

The Trust conducts its transactions in Bitcoin, including receiving Bitcoin for the creation of Units and delivering Bitcoin for the redemption of Units (if a redemption program were to be established) and for the payment of the Management Fee.

During June 2020, the Trust began a continuous

offering of up to $5,000,000 of Units with no par value, each Unit representing a fractional undivided beneficial interest in the

Trust.

On November 12, 2020, the Trust began an

offering of an unlimited number of Units pursuant to Rule 506(c) under the Securities Act (“November 2020 Offering”).

On December 30, 2020, the Sponsor of the Trust announced that it has declared a four to one split of the Trust’s issued and outstanding Units of fractional undivided beneficial interest. With the Unit split, Unitholders of record on December 31, 2020 received four additional Units of the Trust for each Unit held. The effective date of the split was January 5, 2021. The Units that were issued in the Rule 504 Offering and the November 2020 Offering were adjusted retroactively to reflect the 4:1 Unit split effective January 5, 2021.

On January 14, 2021, the Financial Industry Regulatory Authority (“FINRA”) determined that the Trust’s Units met the criteria for trading on the over-the-counter market (“OTC Market”). On February 16, 2021, the Trust’s Units began trading in the OTC Market, operated by OTC Markets Group, Inc., under the ticker symbol “OBTC”. On March 3, 2021, the Trust’s Units began trading in the OTCQX tier of the OTC Market, under the ticker symbol “OBTC.”

Effective November 1, 2021, the Trust suspended the November 2020 Offering under Rule 506(c) under the Securities Act.

As of September 30, 2022, there were

The Trust is currently unable to redeem Units. At some date in the future, the Trust may seek approval from the SEC to operate an ongoing redemption program.

Investment Transactions and Revenue Recognition

The Trust identifies Bitcoin as an “other investment” in accordance with ASC 946. The Trust records its investment transactions on a trade date basis and changes in fair value are reflected as the net change in unrealized appreciation or depreciation on investments. Realized gains and losses are calculated using a first in first out method. Realized gains and losses are recognized in connection with transactions including settling obligations for the Management Fee and other expenses in Bitcoin.

| 9 |

Management Fee

The Trust is expected to pay the remuneration

due to the Sponsor (the “Management Fee” or “Sponsor Fee”). The Management Fee is charged by the Sponsor

to the Trust at an annual rate of

Trust Expenses

In accordance with the Trust Agreement, the Sponsor bears the routine operational, administrative and other ordinary administrative operating expenses of the Trust (the “Assumed Expenses”) other than audit fees, index license fees, aggregate legal fees in excess of $50,000 per annum and the fees of the Custodian ( “Excluded Expenses”) and certain extraordinary expenses of the Trust, including but not limited to taxes and governmental charges, expenses and costs, expenses and indemnities related to any extraordinary services performed by the Sponsor (or any other service provider, including the Trustee) on behalf of the Trust to protect the Trust or the interest of Unitholders, indemnification expenses, fees and expenses related to public trading on OTCQX (“Extraordinary Expenses”). Other expenses reported on the accompanying statements of operations is comprised of Excluded Expenses.

Fair Value Measurements

The Trust’s investment in Bitcoin is stated at fair value in accordance with ASC 820-10 “Fair Value Measurements”, which outlines the application of fair value accounting. Fair value is defined as the price that would be received to sell an asset or paid to transfer a liability (i.e., the “exit price”) in an orderly transaction between market participants at the measurement date. ASC 820-10 requires the Trust to assume that Bitcoin is sold in its principal market to market participants or, in the absence of a principal market, the most advantageous market. Principal market is the market with the greatest volume and level of activity for Bitcoin, and the most advantageous market is defined as the market that maximizes the amount that would be received to sell the asset or minimizes the amount that would be paid to transfer the liability, after taking into account transaction costs. The principal market is generally selected based on the most liquid and reliable exchange (including consideration of the ability for the Trust to access the specific market, either directly or through an intermediary, at the end of each period). The Sponsor has identified Coinbase Pro as the principal market for Bitcoin.

GAAP utilizes a fair value hierarchy for inputs used in measuring fair value that maximizes the use of observable inputs and minimizes the use of unobservable inputs by requiring that the most observable inputs be used when available. Observable inputs are those that market participants would use in pricing the asset or liability based on market data obtained from sources independent of the Trust. Unobservable inputs reflect the Trust’s assumptions about the inputs market participants would use in pricing the asset or liability developed based on the best information available in the circumstances.

The fair value hierarchy is categorized into three levels based on the inputs as follows:

Level 1 – Valuations based on unadjusted quoted prices in active markets for identical assets or liabilities that the Trust has the ability to access. Since valuations are based on quoted prices that are readily and regularly available in an active market, these valuations do not entail a significant degree of judgment.

Level 2 – Valuations based on quoted prices in markets that are not active or for which significant inputs are observable, either directly or indirectly.

Level 3 – Valuations based on inputs that are unobservable and significant to the overall fair value measurement.

The availability of valuation techniques and observable inputs can vary by investment. To the extent that valuations are based on sources that are less observable or unobservable in the market, the determination of fair value requires more judgment. Fair value estimates do not necessarily represent the amounts that may be ultimately realized by the Trust.

Definition of Net Asset Value

The net asset value (“NAV”) of the Trust is used by the Trust in its day-to-day operations to measure the net value of the Trust’s assets. The NAV is calculated on each business day and is equal to the aggregate value of the Trust’s assets

| 10 |

less its liabilities (which include accrued but unpaid fees and expenses, both estimated and finally determined), based on the Bitcoin Market Price. In calculating the value of the Bitcoin held by the Trust on any business day, the Trust will use the market price as of 4:00 p.m. New York time. The Trust will also calculate the NAV per Unit of the Trust daily, which equals the NAV of the Trust divided by the number of outstanding Units (the “NAV per Unit”). The Trust considers 4:00 p.m. New York time as a cut off for the end of day reporting.

3. Fair Value of Bitcoin

The investment measured at fair value on a recurring basis and categorized using the three levels of fair value hierarchy consisted of the following as of September 30, 2022 and December 31, 2021:

| Number | Per Bitcoin | Amount at | Fair Value Measurement Category | |||||||||||||||

| September 30, 2022 | of Bitcoin | Fair Value | Fair Value | Level 1 | Level 2 | Level 3 | ||||||||||||

| Investment in Bitcoin | $ | $ | $ | $ | $ | |||||||||||||

| Number | Per Bitcoin | Amount at | Fair Value Measurement Category | |||||||||||||||

| December 31, 2021 | of Bitcoin | Fair Value | Fair Value | Level 1 | Level 2 | Level 3 | ||||||||||||

| Investment in Bitcoin | $ | $ | $ | $ | $ | |||||||||||||

The Trust determined the fair value per Bitcoin using the price provided at 4:00 p.m., New York time, by Coinbase Pro, the Trust’s principal market.

The Management Fee payable accrued in Bitcoin is converted into United States dollar amount at the period-end Bitcoin Market Price. The fluctuations arising from the effect of changes in liability denominated in Bitcoin are included with the net realized or unrealized appreciation or depreciation on investment in Bitcoin in the statements of operations.

The following represents the changes in quantity and the respective fair value of Bitcoin for the nine months ended September 30, 2022:

| Bitcoin | Fair Value | |||||||

| Balance at January 1, 2022 | $ | |||||||

| Bitcoin distributed for Management Fee, related party | ( | ) | ( | ) | ||||

| Bitcoin distributed for other fees | ( | ) | ( | ) | ||||

| Net realized gain on investment in Bitcoin | — | |||||||

| Net change in unrealized depreciation on investment in Bitcoin | — | ( | ) | |||||

| Balance at September 30, 2022 | $ | |||||||

Net realized gain on the transfer of Bitcoins

to pay the Management Fee and other expenses for the nine months ended September 30, 2022, was $

The following represents the changes in quantity and the respective fair value of Bitcoin for the year ended December 31, 2021:

| 11 |

| Bitcoin | Fair Value | |||||||

| Balance at January 1, 2021 | $ | |||||||

| Bitcoin distributed for Management Fee, related party | ( | ) | ( | ) | ||||

| Bitcoin distributed for other fees | ( | ) | ( | ) | ||||

| Subscriptions | ||||||||

| Net realized gain on investment in Bitcoin | — | |||||||

| Net change in unrealized appreciation on investment in Bitcoin | — | |||||||

| Balance at December 31, 2021 | $ | |||||||

Net realized gain on the transfer of Bitcoins

to pay the Management Fee and other expenses for the year ended December 31, 2021, was $

4. Income Taxes

The Trust is a grantor trust for U.S. federal income tax purposes. Accordingly, the Trust will not be subject to U.S. federal income tax. Rather, each beneficial owner of Units will be treated as directly owning its pro rata share of the Trust’s assets and a pro rata portion of the Trust’s income, gain, losses and deductions will “flow through” to each beneficial owner of Units.

In accordance with GAAP, the Trust has defined the threshold for recognizing the benefits of tax return positions in the financial statements as “more-likely-than-not” to be sustained by the applicable taxing authority and requires measurement of a tax position meeting the “more-likely-than-not” threshold, based on the largest benefit that is more than 50% likely to be realized. As of September 30, 2022, the Trust did not have a liability for any unrecognized tax amounts for uncertain tax positions related to federal, state, and local income taxes.

However, the conclusions concerning the determination of “more-likely-than-not” tax positions may be subject to review and adjustment at a later date based on factors including, but not limited to, further implementation guidance, and on-going analyses of and changes to tax laws, regulations and interpretations thereof.

The Sponsor of the Trust has evaluated whether or not there are uncertain tax positions that require financial statement recognition and has determined that no reserves for uncertain tax positions related to federal, state and local income taxes existed as of September 30, 2022 and December 31, 2021. The Trust’s 2019, 2020, and 2021 tax returns are subject to audit by federal, state and local tax authorities.

5. Related Parties

The Trust is responsible for custody, audit,

legal fees in excess of $

The Sponsor in its discretion, may elect

to reduce, or waive, the Trust’s expenses. For the three months ended September 30, 2022, and 2021, the Sponsor irrevocably

waived

For the three months ended September 30,

2022, and 2021, the Trust incurred Management Fees of $

| 12 |

were unpaid Management Fees of $

The Trust’s Management Fee is accrued daily in Bitcoins and will be payable, at the Sponsor’s sole discretion, in U.S. dollars or in Bitcoins at the Bitcoin market price in effect at the time of such payment. From inception through September 30, 2022, all Management Fees have been made in Bitcoin to the Sponsor.

6. Risks and Uncertainties

Investment in Bitcoin

The Trust is subject to various risks including market risk, liquidity risk, and other risks related to its concentration in a single asset, Bitcoin. Investing in Bitcoin is currently unregulated, highly speculative, and volatile.

The net asset value of the Trust relates primarily to the value of Bitcoin held by the Trust, and fluctuations in the price of Bitcoin could materially and adversely affect an investment in the Units of the Trust. The price of Bitcoin has a limited history. During such history, Bitcoin prices have been volatile and subject to influence by many factors including the levels of liquidity.

If Bitcoin exchanges continue to experience significant price fluctuations, the Trust may experience losses. Several factors may affect the price of Bitcoin, including, but not limited to, global Bitcoin supply and demand, theft of Bitcoin from global exchanges or vaults, and competition from other forms of digital currency or payment services. The Bitcoin held by the Trust are commingled and the Trust’s Unitholders have no specific rights to any specific Bitcoin. In the event of the insolvency of the Trust, its assets may be inadequate to satisfy a claim by its Unitholders.

There is currently no clearing house for Bitcoin, nor is there a central or major depository for the custody of Bitcoin. There is a risk that some or all of the Trust’s Bitcoin could be lost or stolen. The Trust does not have insurance protection on its Bitcoin which exposes the Trust and its Unitholders to the risk of loss of the Trust’s Bitcoin. Further, Bitcoin transactions are irrevocable. Stolen or incorrectly transferred Bitcoin may be irretrievable. As a result, any incorrectly executed Bitcoin transactions could adversely affect an investment in the Trust.

To the extent private keys for Bitcoin addresses are lost, destroyed or otherwise compromised and no backup of the private keys are accessible, the Trust may be unable to access the Bitcoin held in the associated addresses and the private keys will not be capable of being restored. The processes by which Bitcoin transactions are settled are dependent on the Bitcoin peer-to-peer network, and as such, the Trust is subject to operational risk. A risk also exists with respect to previously unknown technical vulnerabilities, which may adversely affect the value of Bitcoin.

7. Indemnifications

In the normal course of business, the Trust enters into contracts with service providers that contain a variety of representations and warranties and which provide general indemnifications. It is not possible to determine the maximum potential exposure or amount under these agreements due to the Trust having no prior claims. Based on experience, the Trust would expect the risk of loss to be remote.

| 13 |

8. Financial Highlights

| Three months ended September 30, 2022 | Three months ended September 30, 2021 |

Nine months ended September 30, 2022 | Nine months ended September 30, 2021 |

|||||||||||||||

| Per Unit Performance | ||||||||||||||||||

| (for a unit outstanding throughout the period) | ||||||||||||||||||

| Net asset value per unit at beginning of period | $ | $ | $ | $ | * | |||||||||||||

| Net increase (decrease) in net assets resulting from operations | ||||||||||||||||||

| Net realized gain (loss) and change in unrealized appreciation (depreciation) on investment in Bitcoin | ( | ) | ||||||||||||||||

| Net investment loss | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||||

| Net increase (decrease) in net assets resulting from operations | ( | ) | ||||||||||||||||

| Net asset value per unit at end of period | $ | $ | $ | $ | ||||||||||||||

| Total return | % | % | ( | % | % | |||||||||||||

| Supplemental Data | ||||||||||||||||||

| Ratios to average net asset value Expenses | % | % | ** | % | % | ** | ||||||||||||

| Net investment loss | ( | % | ( | % | ( | % | ( | % | ||||||||||

*

**

An individual Unitholder’s return, ratios, and per Unit performance may vary from those presented above based on the timing of Unit transactions. Total return and ratios to average net asset value are calculated for the Unitholders taken as a whole. Ratios have been annualized for the partial periods ended September 30, 2022 and September 30, 2021.

9. Subsequent Events

There are no events that have occurred that require disclosure other than that which has already been disclosed in these notes to the financial statements.

| 14 |

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

The following discussion and analysis of our financial condition and results of operations should be read together with our unaudited financial statements and related notes included elsewhere in this Quarterly Report, which have been prepared in accordance with GAAP. The following discussion may contain forward-looking statements based on assumptions we believe to be reasonable. Our actual results could differ materially from those discussed in these forward-looking statements. Factors that could cause or contribute to these differences include, but are not limited to, those set forth under Part II, Item 1A. Risk Factors in this Quarterly Report.

Trust Overview

The Trust is a passive investment vehicle and its assets will not be actively managed. As a result, it will not engage in any activities designed to obtain a profit from, or to ameliorate losses caused by, changes in the market prices of Bitcoins. The investment objective of the Trust is for the Units to reflect the performance of Bitcoin as measured by reference to Coin Metrics CMBI Bitcoin Index (the “Index”), less the aggregate Trust expenses and other liabilities. To date, the Trust has not met its investment objective.

The Units are intended to constitute a cost-effective and convenient means of gaining investment exposure to Bitcoin. However, an investment in the Units may operate and perform differently over time, and at any given time, than an investment directly in Bitcoin due to such factors as Trust fees and expenses, the quantity of Units available for trading, and the relative liquidity, and differences in the markets trading Bitcoin from the markets trading the Units (e.g., hours of operation, marketplace rules, clearance and settlement, market participants). Although the Units will not be the exact equivalent of a direct investment in Bitcoin, they provide investors with an alternative that constitutes a relatively cost-effective way to participate in Bitcoin markets through the securities market. The Units have been quoted on OTC Markets since February 12, 2021, and on OTCQX under the symbol “OBTC” since February 26, 2021, and to date have not met their investment objective.

Critical Accounting Policies and Estimates

Investment Transactions and Revenue Recognition

The Trust considers investment transactions to be the receipt of Bitcoin for Units creations and the delivery of Bitcoin for Units redemptions or for payment of expenses in Bitcoin. At this time, the Trust is not accepting redemption requests from unitholders. The Trust records its investment transactions on a trade date basis and changes in fair value are reflected as the net change in unrealized appreciation or depreciation on investments. Realized gains and losses are calculated using a first in, first out method. Realized gains and losses are recognized in connection with transactions including settling obligations for the Management Fee and other expenses in Bitcoin.

Principal Market and Fair Value Determination

To determine which Bitcoin market will serve as the Trust’s principal market (or in the absence of a principal market, the most advantageous market) for purposes of calculating the Trust’s NAV, the Trust follows FASB ASC 820-10, which outlines the application of fair value accounting. ASC 820-10 determines fair value to be the price that would be received for Bitcoin in a current sale, which assumes an orderly transaction between market participants on the measurement date. ASC 820-10 requires the Trust to assume that Bitcoin is sold in its principal market to market participants or, in the absence of a principal market, the most advantageous market. Market participants are defined as buyers and sellers in the principal or most advantageous market that are independent, knowledgeable, and willing and able to transact.

The Trust purchases Bitcoin directly from various counterparties, such as Galaxy Digital, Jane Street, and Cumberland DRW LLC, and does not itself transact in any Bitcoin markets. The purchase price of Bitcoin from our counterparties may vary significantly. The Trust looks to these counterparties when assessing entity-specific and market-based volume and the level of activity in the Bitcoin markets. The Trust determines the value of Bitcoin at any given time by reference to the market price of Bitcoin traded on Coinbase Pro, the Trust’s principal market, as determined at 4:00 p.m., New York time on each business day (the “Bitcoin Market Price”). The Trust evaluates its principal market selection (or in the absence of a principal market the most advantageous market) at least annually and conducts a quarterly analysis to determine (i) if there have been recent changes to each Bitcoin market’s trading volume and level of activity in the trailing twelve months, (ii) if any Bitcoin markets have developed that the Trust has access to, or (iii) if recent changes to a Bitcoin market’s price stability have occurred that would materially impact the selection of the principal market and necessitate a change in the Trust’s determination of its principal market. The Trust does not anticipate changing its principal market more frequently than annually, in connection with its annual evaluation of its principal market selection and annual financial audit. Each annual evaluation will take into account the findings from the Trust’s quarterly reviews.

| 15 |

The cost basis of a Trust investment in Bitcoin recorded by the Trust for financial reporting purposes is the fair value of the Bitcoin at the time of contribution to the Trust. The Bitcoin cost basis recorded by the Trust may differ from the value of the proceeds collected by the Sponsor from the sale of the corresponding Units to investors.

Investment Company Considerations

The Trust is an investment company for GAAP purposes and follows accounting and reporting guidance in accordance with the FASB ASC Topic 946, Financial Services – Investment Companies. The Trust uses fair value as its method of accounting for Bitcoin in accordance with its classification as an investment company for accounting purposes. The Trust is not a registered investment company under the Investment Company Act of 1940. GAAP requires management to make estimates and assumptions that affect the reported amounts in the financial statements and accompanying notes. Actual results could differ from those estimates and these differences could be material.

Review of Financial Results (unaudited)

Financial Highlights for the Three and Nine Months Ended September 30, 2022 and 2021

| Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||||

| 2022 | 2021 | 2022 | 2021 | |||||||||||||

| Net realized gain (loss) and net change in unrealized appreciation (depreciation) on investment in Bitcoin | $ | 1,673,140 | $ | 24,809,981 | $ | (74,368,046) | $ | 10,194,503 | ||||||||

| Net increase (decrease) in net assets resulting from operations | $ | 1,474,257 | $ | 24,577,170 | $ | (75,148,019) | $ | 9,557,239 | ||||||||

| Net assets | $ | 54,525,149 | $ | 123,291,217 | $ | 54,525,149 | $ | 123,291,217 | ||||||||

Net realized and unrealized gain on investment in Bitcoin for the three months ended September 30, 2022 was $1,673,140 which includes a realized gain of $195,373 on the transfer of Bitcoins to pay the Management Fee and other expenses and net change in unrealized appreciation on investment in Bitcoin of $1,477,767. Net realized and unrealized gain on investment in Bitcoin for the period was driven by Bitcoin price appreciation from $18,895.01 per Bitcoin as of June 30, 2022 to $19,480.51 per Bitcoin as of September 30, 2022. Net increase in net assets resulting from operations was $1,474,257 for the three months ended September 30, 2022, which consisted of the net realized and unrealized gain on investment in Bitcoin, less the Management Fee of $73,637 and other expenses of $125,246. Net assets increased to $54,525,149 at September 30, 2022, a 3% increase for the period. The increase in net assets resulted from the aforementioned Bitcoin price appreciation which was partially offset by the Trust’s expenses of $198,883 for the period.

Net realized and unrealized gain on investment in Bitcoin for the three months ended September 30, 2021 was $24,809,981, which includes a realized loss of $11,480 on the transfer of Bitcoins to pay the Management Fee and other expenses and net change in unrealized appreciation on investment in Bitcoin of $24,821,461. Net realized and unrealized gain on investment in Bitcoin for the period was driven by Bitcoin price appreciation from $34,764.81 per Bitcoin as of June 30, 2021 to $43,529.16 per Bitcoin as of September 30, 2021. Net increase in net assets resulting from operations was $24,577,170 for the three months ended September 30, 2021, which consisted of the net realized and unrealized gain on investment in Bitcoin, less the Management Fee of $146,014 and other expenses of $86,797, net of waivers. Net assets increased to $123,291,217 at September 30, 2021, a 25% increase for the period. The increase in net assets resulted from the aforementioned Bitcoin price appreciation and the capital contribution of approximately 9.55 Bitcoin with a value of $384,982 to the Trust in connection with Units issuance during the period, which was partially offset by the Trust’s Net expenses of $232,811 for the period.

Net realized and unrealized loss on investment in Bitcoin for the nine months ended September 30, 2022 was $74,368,046, which includes a realized gain of $648,250 on the transfer of Bitcoins to pay the Management Fee and other expenses and net change in unrealized depreciation on investment in Bitcoin of $75,016,296. Net realized and unrealized loss on investment in Bitcoin for the period was driven by Bitcoin price depreciation from $45,867.86 per Bitcoin as of December 31, 2021, to $19,480.51 per Bitcoin as of September 30, 2022. Net decrease in net assets resulting from operations was $75,148,019 for the nine months ended September 30, 2022, which consisted of the net realized and unrealized loss on investment in Bitcoin, less the Management Fee of $326,553 and other expenses of $453,420. Net assets decreased to $54,525,149 at September 30, 2022, a 58% decrease for the period. The decrease in net assets resulted from the aforementioned Bitcoin price depreciation and the Trust’s expenses of $779,973 for the period.

| 16 |

Net realized and unrealized gain on investment in Bitcoin for the nine months ended September 30, 2021 was $10,194,503 which includes a realized loss of $72,220 on the transfer of Bitcoins to pay the Management Fee and other expenses and net change in unrealized appreciation on investment in Bitcoin of $10,266,723. Net realized and unrealized gain on investment in Bitcoin for the period was driven by Bitcoin price appreciation from $29,026.66 per Bitcoin as of December 31, 2020, to $43,529.16 per Bitcoin as of September 30, 2021. Net increase in net assets resulting from operations was $9,557,239 for the nine months ended September 30, 2021, which consisted of the net realized and unrealized gain on investment in Bitcoin, less the Management Fee of $410,107 and other expenses of $227,157, net of waivers. Net assets increased to $123,291,217 at September 30, 2021, a 175% increase for the period. The increase in net assets resulted from the aforementioned Bitcoin price appreciation and the contribution of approximately 1,299.49 Bitcoin with a value of $68,827,296 to the Trust in connection with Units issuance during the period, which was partially offset by the Trust’s Net expenses of $637,264 for the period.

Cash Resources and Liquidity

When selling Bitcoins to pay expenses, the Sponsor endeavors to sell the exact number of Bitcoins needed to pay expenses in order to minimize the Trust’s holdings of assets other than Bitcoin. As a consequence, the Sponsor expects that the Trust will not record any cash flow from its operations and that its cash balance will be zero at the end of each reporting period. The prices of digital assets, specifically Bitcoin, have experienced substantial volatility, which may reflect “bubble” type volatility, meaning that high or low prices may have little or no relationship to identifiable market forces, may be subject to rapidly changing investor sentiment, and may be influenced by factors such as technology, regulatory void or changes, fraudulent actors, manipulation, and media reporting. Bitcoin may have value based on various factors, including their acceptance as a means of exchange by consumers and others, scarcity, and market demand.

In exchange for the Management Fee, the Sponsor has agreed to bear the routine operational, administrative and other ordinary fees and expenses incurred by the Trust. The Trust is not aware of any trends, demands, conditions or events that are reasonably likely to result in material changes to its liquidity needs.

Selected Operating Data

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||||

| 2022 | 2021 | 2022 | 2021 | ||||||||||||||

| Bitcoins: | |||||||||||||||||

| Opening balance | 2,816.07 | 2,829.85 | 2,828.93 | 1,548.46 | |||||||||||||

| Purchases | — | 9.55 | — | 1,299.49 | |||||||||||||

| Management Fee, related party | (3.46 | ) | (3.70 | ) | (10.36 | ) | (8.66 | ) | |||||||||

| Other Expenses | (6.92 | ) | (0.88 | ) | (12.88 | ) | (4.47 | ) | |||||||||

| Closing balance | 2,805.69 | 2,834.82 | 2,805.69 | 2,834.82 | |||||||||||||

| Accrued but unpaid Management Fee, related party | (1.13 | ) | (1.14 | ) | (1.13 | ) | (1.14 | ) | |||||||||

| Accrued but unpaid Other Expenses | — | (1.30 | ) | — | (1.30 | ) | |||||||||||

| Net closing balance | 2,804.56 | 2,832.38 | 2,804.56 | 2,832.38 | |||||||||||||

| Number of Units: | |||||||||||||||||

| Opening balance | 8,340,536 | 8,312,486 | 8,340,536 | 4,529,312 | * | ||||||||||||

| Issuance | — | 28,050 | — | 3,811,224 | |||||||||||||

| Closing balance | 8,340,536 | 8,340,536 | 8,340,536 | 8,340,536 | |||||||||||||

*Units have been adjusted retroactively to reflect the 4:1 Unit split effective January 5, 2021.

| As of September 30, | ||||||||

| 2022 | 2021 | |||||||

| NAV per Unit | $ | 6.54 | $ | 14.78 | ||||

| Bitcoin Market Price | $ | 19,480.51 | $ | 43,529.16 | ||||

| Bitcoin Holdings per Unit | 0.00034 | 0.00034 | ||||||

Historical Digital Asset Holdings and Bitcoin Prices

As movements in the price of Bitcoins will directly affect the price of the Units, investors should understand recent movements in the price of Bitcoin. Investors, however, should also be aware that past movements in the Bitcoin price are

| 17 |

not indicators of future movements. Movements may be influenced by various factors, including, but not limited to, government regulation, security breaches experienced by service providers, as well as political and economic uncertainties around the world.

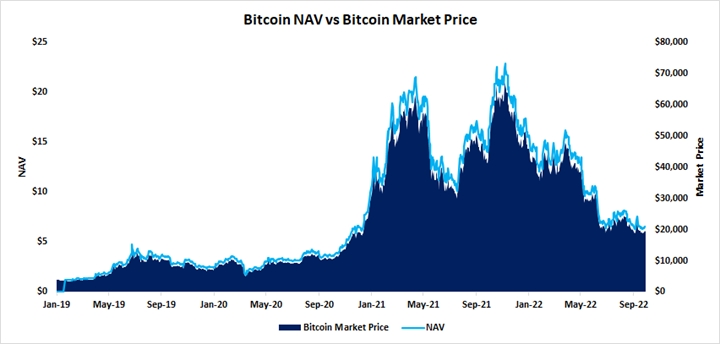

The following chart illustrates the movements in the NAV and the Bitcoin Market Price (referred to in the chart as “Market Price”) from the beginning of the Trust’s operations on January 3, 2019 to September 30, 2022.

The table below illustrates the movements in the Bitcoin Market Price since the beginning of the Trust’s operations on January 3, 2019. Since the beginning of the Trust’s operations to September 30, 2022 the Bitcoin Market Price has ranged from $3,358.67 to $67,371.70, with the straight average being $23,924.12. The Sponsor has not observed a material difference between the Bitcoin Market Price and average prices from the constituent Bitcoin exchanges individually or as a group.

| Period | Average | High | Date | Low | Date | End of period | ||||||||||||||

| From January 3, 2019 to December 31, 2019 | $ | 7,379.15 | $ | 13,724.33 | 6/26/2019 | $ | 3,358.67 | 2/7/2019 | $ | 7,153.38 | ||||||||||

| Year ended December 31, 2020 | $ | 11,131.27 | $ | 29,026.66 | 12/31/2020 | $ | 4,956.92 | 3/16/2020 | $ | 29,026.66 | ||||||||||

| Year ended December 31, 2021 | $ | 47,524.08 | $ | 67,371.70 | 11/9/2021 | $ | 29,785.71 | 7/20/2021 | $ | 45,867.86 | ||||||||||

| Nine months ended September 30, 2022 | $ | 31,595.35 | $ | 47,982.33 | 3/28/2022 | $ | 18,808.23 | 9/23/2022 | $ | 19,480.51 | ||||||||||

| January 3, 2019 (the inception of the Trust’s operations) to September 30, 2022 | $ | 23,924.12 | $ | 67,371.70 | 11/9/2021 | $ | 3,358.67 | 2/7/2019 | $ | 19,480.51 | ||||||||||

Secondary Market Trading

The Trust’s Units have been quoted on OTC Markets since February 12, 2021, and on OTCQX since February 26, 2021 under the symbol “OBTC.” The price of the Units as quoted on OTCQX (and OTC Markets) has varied significantly from the NAV per Unit. From February 12, 2021 to September 30, 2022, the maximum premium of the closing price of the Units quoted on OTCQX (and OTC Markets) over the value of the Trust’s NAV per Unit was approximately 240% and the average daily discount since the Units were first traded on OTC Markets on February 12, 2021 was approximately 4%. As of September 30, 2022, the Trust’s Units were quoted on OTCQX at a discount of approximately 24% to the Trust’s NAV per Unit.

The historical premium of the closing price of the Units quoted on OTCQX and OTC Markets as compared with the NAV per Unit has varied, from a high of 240% on February 16, 2021 (closing price $56.39 per Unit on OTCQX (and OTC Markets) and NAV per Unit $16.58) to a low (i.e., discount) of -30% on June 7, 2022 (closing price $7.28 per Unit on OTCQX (and OTC Markets) and NAV per Unit $10.47). The historical premiums and discounts at times reflect a material deviation from the Bitcoin Market Price.

| 18 |

The following table sets out the range of high and low closing prices for the Units as reported by OTCQX (or OTC Markets) and the Trust’s NAV per Unit for the period from February 12, 2021 to September 30, 2022. The Trust’s Bitcoin Holdings per Unit for the period was 0.00034.

| High | Low | |||||||||||||

| OTC

Markets | NAV per Unit | OTC

Markets | NAV per Unit | |||||||||||

| 2/16/2021 | 11/9/2021 | 9/27/2022 | 9/23/2022 | |||||||||||

| $ | 56.39 | $ | 22.86 | $ | 4.85 | $ | 6.31 | |||||||

Item 3. Quantitative and Qualitative Disclosures about Market Risk

Not applicable.

Item 4. Controls and Procedures

Evaluation of Disclosure Controls and Procedures

Disclosure controls and procedures are controls and other procedures that are designed to ensure that information required to be disclosed in our reports filed or submitted under the Securities Exchange Act of 1934, as amended (the “Exchange Act”), is recorded, processed, summarized and reported within the time periods specified in the SEC’s rules and forms. Disclosure controls and procedures include, without limitation, controls and procedures designed to ensure that information required to be disclosed in company reports filed or submitted under the Exchange Act is accumulated and communicated to management, including our Chief Executive Officer (who serves as our principal executive officer) and Chief Financial Officer (who serves as our principal financial and accounting officer), to allow timely decisions regarding required disclosure.

As previously described in Part I, Item 4 of our Quarterly Report on Form 10-Q for the fiscal quarter ended September 30, 2021, Part II, Item 9A of our Annual Report on Form 10-K for the fiscal year ended December 31, 2021 and Part I, Item 4 of our Quarterly Reports on Form 10-Q for the fiscal quarters ended March 31, 2022 and June 30, 2022, management made enhancements to remediate the previously reported material weakness in our internal controls and procedures. The ongoing remediation efforts include hiring additional qualified accounting and financial reporting personnel, providing greater access to accounting literature, research materials and documents and increased communication among our personnel and third-party professionals with whom we consult regarding financial statements presentation.

As required by Rules 13a-15 and 15d-15 under the Exchange Act, our Chief Executive Officer and Chief Financial Officer carried out an evaluation of the effectiveness of the design and operation of our disclosure controls and procedures as of September 30, 2022. Based upon their evaluation, our Chief Executive Officer and Chief Financial Officer concluded that our disclosure controls and procedures (as defined in Rules 13a-15(e) and 15d-15(e) under the Exchange Act) were ineffective.

Changes in Internal Control over Financial Reporting

There was no change in our internal control over financial reporting that occurred during the fiscal quarter ended September 30, 2022, that has materially affected, or is reasonably likely to materially affect, our internal control over financial reporting.

| 19 |

PART II – OTHER INFORMATION

Item 1. Legal Proceedings

None.

Item 1A. Risk Factors

Except as noted below, there have been no material changes to the risk factors previously disclosed under “Item 1A. Risk Factors” of the Trust’s Annual Report on Form 10-K for the year ended December 31, 2021.

Failure of funds that hold digital assets or that have exposure to digital assets through derivatives to receive SEC approval to list their shares on exchanges could adversely affect the value of the Shares.

There have been a growing a number of attempts to list on national securities exchanges the shares of funds that hold digital assets or that have exposures to digital assets through derivatives. These investment vehicles attempt to provide institutional and retail investors exposure to markets for digital assets and related products. The SEC has repeatedly denied such requests. In January 2018, the SEC’s Division of Investment Management outlined several questions that sponsors would be expected to address before the SEC will consider granting approval for funds holding “substantial amounts” of cryptocurrencies or “cryptocurrency-related products.” The questions, which focus on specific requirements of the Investment Company Act of 1940, generally fall into one of five key areas: valuation, liquidity, custody, arbitrage and potential manipulation. The SEC has not explicitly stated whether each of the questions set forth would also need to be addressed by entities with similar products and investment strategies that instead pursue registered offerings under the Securities Act, although such entities would need to comply with the registration and prospectus disclosure requirements of the Securities Act. Requests to list the shares of other funds on national securities exchanges have also been submitted to the SEC. Although the SEC approved several futures-based Bitcoin ETFs in October 2021, it has not approved any requests to list the shares of digital asset funds like the Trust to date. The requests to list the shares of digital asset funds submitted by the Chicago Board Options Exchange (“CBOE”) and the NYSE Arca in 2019 were withdrawn or received disapprovals. Subsequently, NYSE Arca and CBOE filed several new requests to list shares of various digital asset funds in 2021. Several of those requests were recently denied by the SEC in 2021 and to date in 2022. The exchange listing of shares of digital asset funds would create more opportunities for institutional and retail investors to invest in the digital asset market. If exchange-listing requests are not approved by the SEC and further requests are ultimately denied by the SEC, increased investment interest by institutional or retail investors could fail to materialize, which could reduce the demand for digital assets generally and therefore adversely affect the value of the Shares.

Substantial sales or dispositions by a large Unitholder could negatively impact the price of our Units in the secondary market.

The market price of our Units could decline as a result of substantial sales or dispositions of our Units by large Unitholders. A large disposition of Units may cause a negative perception of our Units in the market and could result in other Unitholders deciding to sell and further disrupt the market price of our Units.

Unitholders are bound by the fee-shifting provision contained in the subscription agreement, which may discourage actions against us.

The subscription agreement also provides that if any legal action or any arbitration or other proceeding is brought for the enforcement of the subscription agreement or because of an alleged dispute, breach, default or misrepresentation in connection with any of the provisions in the subscription agreement, the successful or prevailing party or parties shall be entitled to recover reasonable attorneys’ fees and their costs incurred in that action nor proceedings, in addition to any other relief to which they may be entitled; provided, however, that the foregoing shall not apply to any claim, suit, action or proceeding brought to enforce any duty or liability created by the federal securities laws. In the event a Unitholder initiates or asserts a claim against us, including the Trust, our Sponsor and its officers, in accordance with the dispute resolution provisions contained in the subscription agreement and the Unitholder does not prevail, the Unitholder will be obligated to reimburse us for all reasonable costs and expenses incurred in connection with such claim, including, but not limited to, reasonable attorney’s fees and expenses and costs of appeal, if any. The subscription agreement does not define what constitutes a successful or prevailing party, though we intend to apply a broad interpretation to such provision to apply the fee shifting provision broadly. Whether a specific judgment satisfies the applicable criteria and the extent of recovery for applicable fees and expenses will be subject to judicial interpretation. The enforceability of fee shifting provisions have been challenged in legal proceedings, and it is possible that a court could find this type of provision to be inapplicable to, or unenforceable in respect of, one or more of the specified types of actions or proceedings. The provision could discourage Unitholder lawsuits that might otherwise benefit the Trust or its Unitholders.

| 20 |

The Trust does not maintain audit or inspection rights under the Custodial Services Agreement, and as such our Bitcoin Holdings held in the custodial account cannot be independently verified.

The Trust does not enjoy audit or inspection rights under the Custodial Services Agreement and cannot independently verify the Bitcoin Holdings held in the custodial account. The Sponsor relies on the Custodian’s System and Organization Controls (“SOC”) reports to provide assurances as to the existence of the Trust’s Bitcoin at the Custodian. SOC reports are internal control evaluations conducted by independent auditors. SOC 1 reports broadly comment on controls and processes that impact financial statements and reporting. SOC 2 reports comment on controls and processes that address the security, availability, processing integrity, confidentiality and privacy. SOC 1 and 2 reports can be subcategorized into Type I, which is an attestation of controls at a service organization at specific point in time, and Type II, which is an attestation of controls as a service organization over a period of time. The Custodian engages an independent auditor to conduct both a SOC 1, Type II audit and a SOC 2, Type II audit. Such reports cannot specifically identify the existence of the Trust’s Bitcoin Holdings at the Custodian. The Trust can use such reports to demonstrate the existence of effective controls in place by the Custodian providing assurance and confidence in the Custodian’s service delivery processes and controls for digital assets.

The Trust’s Bitcoin Holdings may be considered property of a bankruptcy estate should our Custodian initiate bankruptcy proceedings and the Trust could be considered an unsecured creditor, and the Custodian’s assets may not be adequate to satisfy a claim by the Trust.

Due to the uncertainty of the treatment of digital assets in a bankruptcy proceeding, the Trust’s Bitcoin Holdings may be considered property of a bankruptcy estate should our Custodian initiate bankruptcy proceedings, and the Trust could potentially be considered an unsecured creditor. Generally, creditors in a bankruptcy case and the priority of payment for their claims are distinguished by the type of claims they hold and creditors whose claims are secured by assets of the estate are in a superior position, and an unsecured creditor is generally in the lowest priority position. In the event that our Custodian initiates bankruptcy proceedings and the Trust is considered an unsecured creditor, there can be no assurance that we will be able to recover our Bitcoin Holdings or that there will be sufficient assets to satisfy our claim, which would have a material adverse effect on the Trust.

Item 2. Unregistered Sales of Equity Securities and Use of Proceeds

None.

Item 3. Defaults Upon Senior Securities

None.

Item 4. Mine Safety Disclosures

Not applicable.

Item 5. Other Information

None.

| 21 |

Item 6. Exhibits

| 22 |

SIGNATURES

Pursuant to the requirements of Section 13 or 15(d) of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned in the capacities* indicated, thereunto duly authorized.

| Osprey Funds, LLC as Sponsor of Osprey Bitcoin Trust | |||

| By: | /s/ Gregory D. King | ||

| Name: | Gregory D. King | ||

| Title: | Chief Executive Officer* | ||

| By: | /s/ Robert J. Rokose | ||

| Name: | Robert J. Rokose | ||

| Title: | Chief Financial Officer* | ||

Date: November 9, 2022

| * | The Registrant is a trust and the persons are signing in their capacities as officers or directors of Osprey Funds, LLC, the Sponsor of the Registrant. |

| 23 |