Table of Contents

As filed with the Securities and Exchange Commission on June 30, 2021.

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Endeavor Group Holdings, Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 7900 | 83-3340169 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

9601 Wilshire Boulevard, 3rd Floor

Beverly Hills, CA 90210

(310) 285-9000

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Jason Lublin

Chief Financial Officer

9601 Wilshire Boulevard, 3rd Floor

Beverly Hills, CA 90210

(310) 285-9000

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

| Justin G. Hamill, Esq. Marc D. Jaffe, Esq. Benjamin J. Cohen, Esq. Latham & Watkins LLP 885 Third Avenue |

Seth Krauss, Esq. Chief Legal Officer Robert Hilton, Esq. Senior Vice President, Associate General Counsel & Corporate Secretary Endeavor Group Holdings, Inc. |

Approximate date of commencement of proposed sale to the public: As soon as practicable after this Registration Statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box: ☐

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |||

| Non-accelerated filer | ☒ | Smaller reporting company | ☐ | |||

| Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

CALCULATION OF REGISTRATION FEE

|

| ||||||||

| Title of Each Class of Securities to be Registered |

Amount to be |

Proposed Maximum Offering Price Per Share(2) |

Proposed Maximum Offering Price |

Amount of Registration Fee | ||||

| Class A common stock, par value $0.00001 per share |

76,806,172 |

$26.91 | $2,066,854,089 | $225,494 | ||||

|

| ||||||||

|

| ||||||||

| (1) | In accordance with Rule 416 under the Securities Act of 1933, as amended, this registration statement shall be deemed to cover an indeterminate number of additional shares to be offered or issued from stock splits, stock dividends or similar transactions with respect to the shares being registered. |

| (2) | In accordance with Rule 457(c) under the Securities Act of 1933, as amended, the proposed maximum aggregate offering price per share of these shares of Class A common stock is estimated solely for the calculation of the registration fees due for this filing. The calculation of the proposed aggregate offering price of these shares of Class A common stock is based on the average of the high and low selling price of the Class A common stock as quoted on the New York Stock Exchange on June 29, 2021. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell nor does it seek an offer to buy these securities in any state or jurisdiction where the offer or sale is not permitted.

Subject to Completion. Dated June 30, 2021.

Prospectus

| Class A Common Stock | 76,806,172 Shares |

This prospectus relates to the resale of up to 76,806,172 shares of our Class A common stock by the selling stockholders named in this prospectus or their permitted transferees. We are registering the shares for resale pursuant to such stockholders’ registration rights under a subscription agreement between us and such stockholders. Subject to any contractual restrictions on them selling the shares of our Class A common stock they hold, the selling stockholders may offer, sell or distribute all or a portion of their shares of our Class A common stock publicly or through private transactions at prevailing market prices or at negotiated prices. We will not receive any of the proceeds from the sale of the shares of our Class A common stock owned by the selling stockholders. We will bear all costs, expenses and fees in connection with the registration of these shares of our Class A common stock, including with regard to compliance with state securities or “blue sky” laws. The selling stockholders will bear all commissions and discounts, if any, attributable to their sale of shares of our Class A common stock.

See “Plan of Distribution” beginning on page 186 of this prospectus.

INVESTING IN OUR SECURITIES INVOLVES RISKS. SEE “RISK FACTORS” BEGINNING ON PAGE 9 OF THIS PROSPECTUS AND ANY SIMILAR SECTION CONTAINED IN ANY APPLICABLE PROSPECTUS SUPPLEMENT TO READ ABOUT CERTAIN FACTORS YOU SHOULD CONSIDER BEFORE INVESTING IN OUR SECURITIES.

We currently conduct our business through Endeavor Operating Company and its subsidiaries. Endeavor Group Holdings manages and operates the business and controls the strategic decisions and day-to-day operations of Endeavor Operating Company through Endeavor Manager and includes the operations of Endeavor Operating Company in our consolidated financial statements.

Endeavor Group Holdings, Inc. has five classes of authorized common stock: Class A common stock, Class B common stock, Class C common stock, Class X common stock, and Class Y common stock. The Class A common stock and the Class X common stock have one vote per share. The Class Y common stock has 20 votes per share. The Class B and Class C common stock is non-voting. Our Chief Executive Officer, Ariel Emanuel, and our Executive Chairman, Patrick Whitesell, and their affiliates, together with affiliates of Silver Lake, hold a majority of our issued and outstanding Class Y common stock and Class X common stock and, as a group, control more than a majority of the combined voting power of our common stock. As a result, they are able to control any action requiring the general approval of our stockholders, including the election of our board of directors, the adoption of amendments to our certificate of incorporation and by-laws, and the approval of any merger or sale of substantially all of our assets.

We are a “controlled company” under the corporate governance rules of the Exchange applicable to listed companies, and therefore we are permitted to, and we intend to, elect not to comply with certain corporate governance requirements thereunder. See “Management—Controlled Company.”

Our Class A common stock is listed on the New York Stock Exchange (the “NYSE”) under the symbol “EDR”. On June 24, 2021, the last reported sale price of our Class A common stock was $27.32 per share.

Neither the Securities and Exchange Commission nor any other regulatory body has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

Prospectus dated , 2021.

Table of Contents

| 3 | ||||

| 8 | ||||

| 9 | ||||

| 43 | ||||

| 45 | ||||

| 46 | ||||

| 47 | ||||

| 48 | ||||

| 59 | ||||

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

62 | |||

| 105 | ||||

| 120 | ||||

| 126 | ||||

| 161 | ||||

| 167 | ||||

| 180 | ||||

| 186 | ||||

| 189 | ||||

| 190 | ||||

| 191 | ||||

| F-1 |

Table of Contents

ABOUT THIS PROSPECTUS

Neither we nor the selling stockholders have authorized anyone to provide you with any information or to make any representations other than those contained in this prospectus, any applicable prospectus supplement or any free writing prospectuses prepared by or on behalf of us or to which we have referred you. Neither we nor the selling stockholders take any responsibility for, nor provide any assurance as to the reliability of, any other information that others may give you. Neither we nor the selling stockholders will make an offer to sell these securities in any jurisdiction where the offer or sale is not permitted.

ii

Table of Contents

INDUSTRY AND MARKET DATA

Industry and market data used throughout this prospectus were obtained through Company research, surveys and studies conducted by third parties and industry and general publications. Certain information contained under the heading “Business” is based on studies, analyses, and surveys prepared by AdAge, ActionNetwork, Activate, Inc., the American Gaming Association, Ampere Analysis, Billboard, The Business Research Company, the Bureau of Economic Analysis, The Center for Generational Kinetics, LLC, Expedia, Forbes, H2 Global, License Global, Licensing International, the Organization for Economic Co-operation and Development (the “OECD”), Technavio, and the University of Texas at Austin. While we are not aware of any misstatements regarding the industry data presented herein, estimates involve risks and uncertainties and are subject to change based on various factors, including those discussed under the headings “Risk Factors” and “Forward-Looking Statements.”

TRADEMARKS

This prospectus contains references to our trademarks and service marks and to those belonging to other entities. Solely for convenience, trademarks and trade names referred to in this prospectus may appear without the ® or ™ symbols, but such references are not intended to indicate, in any way, that their respective owners will not assert, to the fullest extent under applicable law, their rights thereto. We do not intend our use or display of other companies’ trade names, trademarks, or service marks to imply a relationship with, or endorsement or sponsorship of us by, any other companies.

DEFINITIONS

As used in this prospectus, unless we state otherwise or the context otherwise requires:

| • | “we,” “us,” “our,” “Endeavor,” the “Company,” and similar references refer (a) after giving effect to the Reorganization Transactions, to Endeavor Group Holdings and its consolidated subsidiaries, and (b) prior to giving effect to the Reorganization Transactions, to Endeavor Operating Company and its consolidated subsidiaries. |

| • | “Endeavor Catch-Up Profits Units” refer to the Endeavor Full Catch-Up Profits Units and the Endeavor Partial Catch-Up Profits Units. |

| • | “Endeavor Full Catch-Up Profits Units” refer to the Endeavor Profits Units that were designated as “catchup” units. Endeavor Full Catch-Up Profits Units had a per unit hurdle price and were entitled to receive a preference on distributions once the hurdle price applicable to such unit was met. Since our May 2021 IPO, we have achieved a price per share that would have fully satisfied such preference on distributions, and the Endeavor Full Catch-Up Profits Units were converted into Endeavor Operating Company Units. |

| • | “Endeavor Group Holdings” refers to Endeavor Group Holdings, Inc. (“EGH”). |

| • | “Endeavor Manager” refers to Endeavor Manager, LLC, a Delaware limited liability company and a direct subsidiary of Endeavor Group Holdings following the Reorganization Transactions. |

| • | “Endeavor Manager Units” refers to the common interest units in Endeavor Manager. |

| • | “Endeavor Operating Company” refers to Endeavor Operating Company, LLC, a Delaware limited liability company (“EOC”) and a direct subsidiary of Endeavor Manager’s and indirect subsidiary of ours following the Reorganization Transactions. |

| • | “Endeavor Operating Company Units” refers to all of the existing equity interests in Endeavor Operating Company (other than the Endeavor Profits Units) that were reclassified into Endeavor Operating Company’s non-voting common interest units upon the consummation of the Reorganization Transactions. |

1

Table of Contents

| • | “Endeavor Partial Catch-Up Profits Units” refer to the Endeavor Profits Units that were designated as “catchup” units. Endeavor Partial Catch-Up Profits Units had a per unit hurdle price and were entitled to receive a preference on distributions once the hurdle price applicable to such unit was met. Since our May 2021 IPO, we have achieved a price per share that would have fully satisfied such preference on distributions, and the Endeavor Partial Catch-Up Profits Units were converted into Endeavor Profits Units (without any such preference) with a reduced per unit hurdle price to take into account such prior preference. |

| • | “Endeavor Phantom Units” refers to the phantom units outstanding, which, subject to certain conditions and limitations, entitle the holder to cash equal to the value of a number of Endeavor Manager Units, Endeavor Operating Company Units, or Endeavor Profits Units, or of equity settled to the equivalent number of Endeavor Manager Units, Endeavor Operating Company Units, or Endeavor Profits Units. |

| • | “Endeavor Profits Units” refers to the profits units of Endeavor Operating Company and that are economically similar to stock options. Each outstanding Endeavor Profits Unit has a per unit hurdle price, which is economically similar to the exercise price of a stock option. |

| • | “Executive Holdcos” refers to Endeavor Executive Holdco, LLC, Endeavor Executive PIU Holdco, LLC, and Endeavor Executive II Holdco, LLC, each a management holding company, the equity owners of which include current and former senior officers, employees, or other service providers of Endeavor Operating Company, and which are controlled by Messrs. Emanuel and Whitesell. |

| • | “Reorganization Transactions” refers to the internal reorganization completed in connection with our May 2021 initial public offering, following which Endeavor Group Holdings manages and operates the business and control the strategic decisions and day-to-day operations of Endeavor Operating Company through Endeavor Manager and includes the operations of Endeavor Operating Company in its consolidated financial statements. |

Presentation of Financial Information

Endeavor Operating Company, LLC is the predecessor of the issuer, Endeavor Group Holdings, Inc., for financial reporting purposes. Endeavor Group Holdings, Inc. became the financial reporting entity following our May 2021 initial public offering. Accordingly, this prospectus contains the following historical financial statements:

| • | Endeavor Group Holdings, Inc. Other than the audited balance sheets as of December 31, 2020 and 2019 and the unaudited balance sheet as of March 31, 2021, the historical financial information of Endeavor Group Holdings, Inc. has not been included in this prospectus as it has no business transactions or activities until the closing of our initial public offering in May 2021 other than those incidental to its formation and preparation for our initial public offering. Endeavor Group Holdings, Inc. had no other assets or liabilities during the periods presented in this prospectus prior to the consummation of our May 2021 initial public offering. |

| • | Endeavor Operating Company, LLC. As we have no other interest in any operations other than those of Endeavor Operating Company, LLC and its subsidiaries, the historical consolidated financial information included in this prospectus is that of Endeavor Operating Company, LLC and its subsidiaries. |

The unaudited pro forma financial information of Endeavor Group Holdings, Inc. presented in this prospectus has been derived by the application of pro forma adjustments to the historical consolidated financial statements of Endeavor Operating Company, LLC and its subsidiaries included elsewhere in this prospectus. See “Unaudited Pro Forma Financial Information” for a complete description of the adjustments and assumptions underlying the pro forma financial information included in this prospectus.

2

Table of Contents

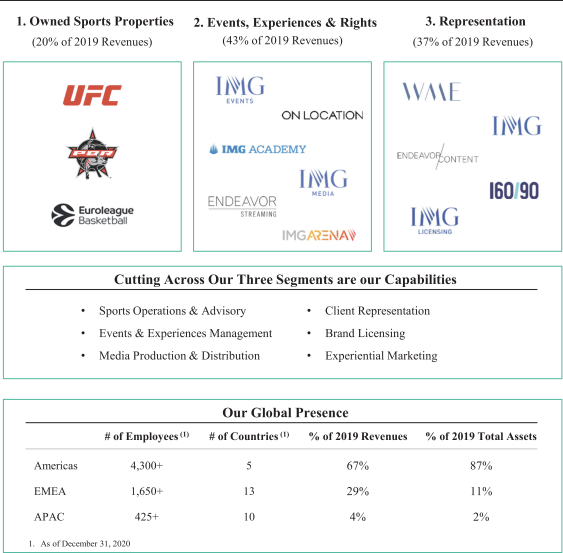

Our Company

Endeavor is a premium intellectual property, content, events, and experiences company. We own and operate premium sports properties, including the UFC, produce and distribute sports and entertainment content, own and manage exclusive live events and experiences, and represent top sports and entertainment talent, as well as blue chip corporate clients. Founded as a client representation business, we expanded organically and through strategic mergers and acquisitions, investing in new capabilities, including sports operations and advisory, events and experiences management, media production and distribution, brand licensing, and experiential marketing. The addition of these new capabilities and insights transformed our business into an integrated global platform anchored by owned and managed premium intellectual property.

We believe that our unique business model gives us a competitive advantage in the industries in which we operate. Our direct ownership of scarce sports properties positions us to directly benefit from the generally rising value of sports assets, while giving us direct control to make decisions that sustain the long-term value of our properties. Our dual role as an intellectual property owner and as a trusted advisor to clients and rights holders allows us to make connections across our platform, increasing the earnings of our clients and the value of our sports and entertainment properties. We possess category leading capabilities in various industries, each of which contributes to our financial success. The integration of our broad range of capabilities, along with our owned and managed premium sports and entertainment properties, drives network effects across our platform. We measure these effects by evaluating the impact that activity in one business segment has on growth in another. Our management team has successfully executed a mergers and acquisitions and organic-driven growth strategy that has transformed our business from a pure representation model to an integrated global platform. After we founded Endeavor in 1995, we gained scale in representation by merging with the venerable William Morris Agency to form WME in 2009, which was followed by our acquisition of IMG in 2014, adding marketing and licensing, events, media production and distribution, and the sports training institution, IMG Academy. The acquisition of a controlling interest in the UFC in 2016 served as a major step forward in the transformation of our business. We have also built businesses primarily organically that take advantage of our unique role within the sports and entertainment ecosystem.

Recent Developments

Acquisitions

On April 1, 2021, we entered into a Share Purchase Agreement (the “FlightScope Purchase Agreement”), to acquire all of the issued and outstanding equity interests of EDH Tennis Limited, the holding company of FlightScope Services sp. z o.o., comprising the services business of FlightScope (collectively, the “FlightScope Services Business”) and simultaneously closed the acquisition. Pursuant to the FlightScope Purchase Agreement, we acquired the FlightScope Services Business for an aggregate cash purchase price of approximately $60 million (approximately $35 million was paid upfront as initial consideration, and the remainder will be paid as deferred consideration in two installments in 2022 and 2024). The FlightScope Services Business is a data collection, audio-visual production and tracking technology specialist for golf and tennis events.

On January 14, 2021, we entered into a Membership Interests Purchase Agreement (the “Reigning Champs Purchase Agreement”), to acquire the path-to-college business of Reigning Champs, LLC (“Reigning Champs”), which acquisition closed on June 1, 2021. Pursuant to the Reigning Champs Purchase Agreement, we acquired all of the issued and outstanding membership interests or other equity securities of all of the subsidiaries within the path-to-college business of Reigning Champs (collectively, the “Reigning Champs PTC Business”) for an aggregate cash purchase price of approximately $200 million. We refer to this acquisition of the Reigning Champs PTC Business as the “Reigning Champs Acquisition.” The Reigning Champs PTC Business consists of companies that offer recruiting and admissions services and related software products to high school student athletes, as well as college athletic departments and admissions officers.

3

Table of Contents

Senior Credit Facilities

On April 19, 2021, the Company entered into an amendment to the credit agreement governing the Credit Facilities (as defined below) to, among other things, waive the financial covenant for the test periods ending June 30, 2021, September 30, 2021 and December 31, 2021. In addition, the amendment also extended the maturity date of the Revolving Credit Facility to May 18, 2024.

On June 29, 2021, we reduced our debt under our Senior Credit Facilities (as defined below) by $600 million, consisting of repayment of (i) approximately $180 million first lien term loans under the UFC Credit Facilities (as defined below), (ii) approximately $163 million under the Revolving Credit Facility and (iii) approximately $257 million incremental term loans issued in May 2020 under the Credit Facilities.

Learfield Investment

On June 17, 2021, we acquired additional common units in A-L Tier 1 LLC (“Learfield IMG College”) for aggregate consideration having a value equal to $109.1 million. We will continue to account for our Learfield IMG College investment under the equity method of accounting.

IPO, Private Placement and UFC Buyout

On May 3, 2021, Endeavor Group Holdings, Inc. (“EGH”) closed an initial public offering (“IPO”) of 24,495,000 shares of Class A common stock at a public offering price of $24.00 per share, which included 3,195,000 shares of Class A common stock issued pursuant to the underwriters’ option to purchase additional shares of Class A common stock. This option to purchase additional shares of Class A common stock was closed on May 12, 2021.

Prior to the closing of the IPO, a series of Reorganization Transactions (the “Reorganization Transactions”) was completed:

| • | EGH’s certificate of incorporation was amended and restated to, among other things, provide for the following common stock: |

| Class of Common Stock |

Par Value | Votes | Economic Rights | |||||

| Class A common stock |

$ | 0.00001 | 1 | Yes | ||||

| Class B common stock |

$ | 0.00001 | None | Yes | ||||

| Class C common stock |

$ | 0.00001 | None | Yes | ||||

| Class X common stock |

$ | 0.00001 | 1 | None | ||||

| Class Y common stock |

$ | 0.00001 | 20 | None | ||||

| • | Voting shares of EGH’s common stock will generally vote together as a single class on all matters submitted to a vote of our stockholders; |

| • | Endeavor Manager became the sole managing member of EOC and EGH became the sole managing member of Endeavor Manager; |

| • | Endeavor Manager issued to equityholders of certain management holding companies common interest units in Endeavor Manager Units in Endeavor Manager along with paired shares of its Class X common stock as consideration for the acquisition of Endeavor Operating Company Units held by such management holding companies; |

| • | For certain pre-IPO investors, EGH issued shares of its Class A common stock, Class Y common stock and rights to receive payments under a tax receivable agreement and for certain other pre-IPO investors, EGH issued shares of its Class A common stock as consideration for the acquisition of Endeavor Operating Company Units held by such pre-IPO investors; |

4

Table of Contents

| • | For holders of Endeavor Operating Company Units which remained outstanding following the IPO, EGH issued paired shares of its Class X common stock and, in certain instances, Class Y common stock, in each case equal to the number of Endeavor Operating Company Units held and in exchange for the payment of the aggregate par value of the Class X common stock and Class Y common stock received; and |

| • | Certain Endeavor Profits Units, Endeavor Full Catch-Up Profits Units and Endeavor Partial Catch-Up Profits Units remained outstanding. |

Concurrent to the closing of the IPO, several new and current investors purchased in the aggregate 75,584,747 shares of Class A common stock at a price per share of $24.00 (the “Private Placement”). Of these shares, 57,378,497 were purchased from EGH and 18,206,250 were purchased from an existing investor. Net proceeds received by EGH from the IPO and the Private Placement, after deducting underwriting discounts and commissions but before deducting offering expenses was approximately $1,901.5 million.

Subsequent to the closing of the IPO and the Private Placement, through a series of transactions, EOC acquired the equity interests of the minority unitholders of Zuffa, which owns and operates the Ultimate Fighting Championship (the “UFC Buyout”). This resulted in EOC directly or indirectly owning 100% of the equity interests of Zuffa.

In connection with the acquisition of the minority unitholders’ equity interests of Zuffa, (a) EGH issued to certain of such unitholders (or their affiliates) shares of Class A common stock, Endeavor Operating Company Units, Endeavor Manager Units, shares of Class X common stock and/or shares of Class Y common stock, and (b) EGH used $835.7 million of the net proceeds from the IPO and the concurrent Private Placements to purchase Endeavor Operating Company Units from certain of such holders. In addition, some affiliates of those minority unitholders sold Class A Common Stock they received to the Private Placement Investors (as defined below) in the concurrent Private Placement.

Remaining net proceeds after the UFC Buyout were contributed to Endeavor Manager in exchange for Endeavor Manager Units. Endeavor Manager then in turn contributed such net proceeds to Endeavor Operating Company in exchange for Endeavor Operating Company Units.

Upon the IPO, the 2021 Incentive Award Plan became effective with an initial reserve of 21,700,000 shares of Class A common stock. In addition, the following significant equity-based compensation items occurred: (i) 9,400,353 restricted stock units and stock options of EGH were granted to certain directors, employees and other service providers under the 2021 Incentive Award Plan; (ii) modification of certain pre-IPO equity-based awards were made primarily to remove certain forfeiture and discretionary call terms; (iii) the third Zuffa equity value threshold was achieved under the Zuffa future incentive award and EGH granted 520,834 restricted stock units to our Chief Executive Office (“CEO”); (iv) our CEO was granted 2,333,334 time-vesting restricted stock units as well as a performance-based award with a metric based on the increase in our share price; and (v) our Executive Chairman was granted a performance-based award with a metric based on the increase in our share price. The Company is currently assessing the accounting treatment for these items and will record the necessary equity-based compensation charges in the three months ended June 30, 2021, which in the aggregate is expected to be material.

Risks Associated with Our Business

An investment in our Class A common stock involves a high degree of risk. You should carefully consider the risks summarized in the “Risk Factors” section of this prospectus immediately following this prospectus summary, including:

| • | the COVID-19 pandemic’s significant adverse impact on our business; |

5

Table of Contents

| • | changes in public and consumer tastes and preferences and industry trends could reduce demand for our services and content offerings and adversely affect our business; |

| • | our ability to generate revenue from discretionary and corporate spending on entertainment and sports events, such as corporate sponsorships and advertising, is subject to many factors, including many that are beyond our control, such as general macroeconomic conditions; |

| • | we may not be able to adapt to or manage new content distribution platforms or changes in consumer behavior resulting from new technologies; |

| • | because our success depends substantially on our ability to maintain a professional reputation, adverse publicity concerning us, one of our businesses, our clients, or our key personnel could adversely affect our business; |

| • | we depend on the relationships of our agents, managers, and other key personnel with clients across many categories, including television, film, professional sports, fashion, music, literature, theater, digital, sponsorship and licensing; |

| • | our success depends, in part, on our continuing ability to identify, recruit, and retain qualified and experienced agents and managers. If we fail to recruit and retain suitable agents or if our relationships with our agents change or deteriorate, it could adversely affect our business; |

| • | our failure to identify, sign, and retain clients could adversely affect our business; |

| • | the markets in which we operate are highly competitive, both within the United States and internationally; |

| • | we depend on the continued service of the members of our executive management and other key employees, as well as management of acquired businesses, the loss or diminished performance of whom could adversely affect our business |

| • | we depend on key relationships with television and cable networks, satellite providers, digital streaming partners and other distribution partners, as well as corporate sponsors; |

| • | we may be unable to protect our trademarks and other intellectual property rights, and others may allege that we infringe upon their intellectual property rights; |

| • | we are subject to extensive U.S. and foreign governmental regulations, and our failure to comply with these regulations could adversely affect our business; |

| • | we are signatory to certain franchise agreements of unions and guilds and are subject to certain licensing requirements of the states in which we operate. We are also signatories to certain collective bargaining agreements and depend upon unionized labor for the provision of some of our services. Our clients are also members of certain unions and guilds that are signatories to collective bargaining agreements. Any expiration, termination, revocation or non-renewal of these franchises, collective bargaining agreements, or licenses and any work stoppages or labor disturbances could adversely affect our business; |

| • | we have a substantial amount of indebtedness, which could adversely affect our business; |

| • | we are a holding company and our principal asset is our indirect equity interests in Endeavor Operating Company and, accordingly, we are dependent upon distributions from Endeavor Operating Company to pay taxes and other expenses; |

| • | we are required to pay certain of our pre-IPO investors, including certain Other UFC Holders, for certain tax benefits we may claim (or are deemed to realize) in the future, and the amounts we may pay could be significant; and |

6

Table of Contents

| • | we are controlled by Messrs. Emanuel and Whitesell, Executive Holdcos, and the Silver Lake Equityholders, whose interests in our business may be different than yours, and our board of directors has delegated significant authority to an Executive Committee and to Messrs. Emanuel and Whitesell. |

Corporate Information

We were formed as a Delaware corporation in January 2019. We are a holding company whose principal assets are the Endeavor Manager Units we hold in Endeavor Manager, and have not engaged in any business or other activities except in connection with the Reorganization Transactions and the IPO. Our corporate headquarters are located at 9601 Wilshire Boulevard, 3rd Floor, Beverly Hills, CA 90210, and our telephone number is (310) 285-9000. Our website address is www.endeavorco.com. Information contained on, or that can be accessed through, our website does not constitute a part of this prospectus.

7

Table of Contents

| Issuer |

Endeavor Group Holdings, Inc. |

| Shares of Class A Common Stock Offered by the Selling Stockholders |

Up to 76,806,172 shares of Class A common stock |

| Use of Proceeds |

We will not receive any proceeds from the sale of shares of Class A common stock by the selling stockholders. |

| Market for Class A Common Stock |

Our Class A common stock is listed on the NYSE under the symbol “EDR”. |

| Risk Factors |

Investing in our Class A common stock involves a high degree of risk. See “Risk Factors” beginning on page 9 of this prospectus for a discussion of factors you should carefully consider before investing in our Class A common stock. |

8

Table of Contents

Investing in our Class A common stock involves substantial risks. You should carefully consider the following factors, together with all of the other information included in this prospectus, including under the heading “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the consolidated financial statements and the related notes included elsewhere in this prospectus, before investing in our Class A common stock. Any of the risk factors we describe below could adversely affect our business, financial condition or results of operations. The market price of our Class A common stock could decline if one or more of these risks or uncertainties develop into actual events, causing you to lose all or part of your investment. We cannot assure you that any of the events discussed below will not occur. While we believe these risks and uncertainties are especially important for you to consider, we may face other risks and uncertainties that could adversely affect our business. Please also see “Forward-Looking Statements” for more information.

Risks Related to Our Business

The impact of the COVID-19 global pandemic could continue to materially and adversely affect our business, financial condition and results of operations.

In March 2020, the World Health Organization declared COVID-19 a global pandemic, and governmental authorities around the world implemented measures to reduce the spread of COVID-19. Numerous state and local jurisdictions, including in markets where we operate, imposed “shelter-in-place” orders, quarantines, travel restrictions, executive orders and similar government orders and restrictions for their residents to control the spread of COVID-19. Such orders or restrictions resulted in work stoppages, slowdowns and delays, travel restrictions and cancellation of events, among other effects.

These measures began to have a significant adverse impact on our business and operations beginning in March 2020, including in the following ways: the inability to hold live ticketed PBR and UFC events and the early cancellation of the 2019-2020 Euroleague season adversely impacted our Owned Sports Properties segment; the postponement or cancellation of live sporting events and other in-person events adversely impacted our Events, Experiences & Rights segment; stoppages of entertainment productions, including film, television shows, and music events, as well as reduced corporate spending on marketing, experiential and activation, adversely impacted our Representation segment.

While activity has resumed in certain of our businesses and restrictions have been lessened or lifted in some cases, restrictions impacting certain of our businesses remain in effect in locations where we are operating and could in the future be reduced or increased, or removed or reinstated. As a result of this and numerous other uncertainties, including the duration of the pandemic, the effectiveness of mass vaccinations and other public health efforts to mitigate the impact of the pandemic, additional postponements or cancellations of live sporting events and other in-person events, and changes in consumer preferences towards our business and the industries in which we operate, we are unable to accurately predict the full impact of COVID-19 on our business, results of operations, financial position and cash flows; however, its impact may be significant. The ongoing pandemic has had a significant impact on our cash flows from operations. We expect that any recovery will continue to be gradual and that the wider impact on revenue and cash flows will vary, but will generally depend on the factors listed above and the general uncertainty surrounding COVID-19.

As an example, for those live events that resume, attendance may continue at significantly reduced levels throughout 2021, and any resumption may bring increased costs to comply with new health and safety guidelines. Given the ongoing uncertainty, we have taken several steps to preserve capital and increase liquidity. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Impact of the COVID-19 Pandemic.” We cannot assure you that such measures and our cash flows from operations, cash and cash equivalents, or cash available under our Senior Credit Facilities (as defined below) will be sufficient to meet our working capital requirements and commitments, including long-term debt service, in the foreseeable future.

9

Table of Contents

We will continue to assess the situation, including abiding by any government-imposed restrictions, market by market. We are unable to accurately predict the ultimate impact that COVID-19 will have on our operations going forward due to the aforementioned uncertainties. We may be unable to accurately predict the impact, operating costs and effectiveness of continuing to adapt certain aspects of our business or restarting certain of our businesses that have not been fully operational during this period, or the future ways in which we will need to adapt our businesses to further changes or consumer behaviors arising out of the pandemic. In addition, any broader global deterioration in economic conditions, which may have an adverse impact on discretionary consumer spending, could also impact our business. For instance, consumer spending may be negatively impacted by general macroeconomic conditions, including a rise in unemployment and decreased consumer confidence resulting from the pandemic. Changing consumer behaviors as a result of COVID-19 may also have a material impact on our revenue for the foreseeable future.

In the past, governments have taken unprecedented actions in an attempt to address and rectify these extreme market and economic conditions by providing liquidity and stability to financial markets. If these actions are not successful, the return of adverse economic conditions may cause a material impact on our ability to raise additional capital, if needed, on a timely basis and on acceptable terms, or at all.

To the extent the COVID-19 pandemic adversely affects our business and financial results, it may also have the effect of heightening many of the other risks described in this “Risk Factors” section, such as those relating to our liquidity, indebtedness, and our ability to comply with the covenants contained in the agreements that govern our indebtedness.

Changes in public and consumer tastes and preferences and industry trends could reduce demand for our services and content offerings and adversely affect our business.

Our ability to generate revenues is highly sensitive to rapidly changing consumer preferences and industry trends, as well as the popularity of the talent, brands, and owners of IP we represent, and the assets we own. Our success depends on our ability to offer premium content through popular channels of distribution that meet the changing preferences of the broad consumer market and respond to competition from an expanding array of choices facilitated by technological developments in the delivery of content. Our operations and revenues are affected by consumer tastes and entertainment trends, including the market demand for the distribution rights to live sports events, which are unpredictable and may be affected by changes in the social and political climate, or global issues such as the COVID-19 pandemic. Changes in consumers’ tastes or a change in the perceptions of our brands and business partners, whether as a result of the social and political climate or otherwise, could adversely affect our operating results. Our failure to avoid a negative perception among consumers or anticipate and respond to changes in consumer preferences, including in the form of content creation or distribution, could result in reduced demand for our services and content offerings or those of our clients and owned assets across our platform, which could have an adverse effect on our business, financial condition and results of operations.

Consumer tastes change frequently and it is a challenge to anticipate what offerings will be successful at any point in time. We may invest in our content and owned assets, including in the creation of original content, before learning the extent to which it will achieve popularity with consumers. For example, as of December 31, 2020 we have committed to spending approximately $2.2 billion in guaranteed payments for media, event, or other representation rights and similar expenses, regardless of our ability to profit from these rights. Subsequent to December 31, 2020, we have entered into certain new arrangements increasing our purchase/guarantee agreements by $1.3 billion, which will be due in 2021 through 2028. Specifically, our results of operations have been negatively impacted due to the costs associated with acquired media rights to major soccer events in excess of revenue, which will continue to adversely impact our results of operations for the term of certain of these contracts, two of which expired in 2021 and the last expires in 2027. A lack of popularity of these, our other content offerings, or our owned assets, as well as labor disputes, unavailability of a star performer, equipment shortages, cost overruns, disputes with production teams, or adverse weather conditions, could have an adverse effect on our business, financial condition and results of operations.

10

Table of Contents

Our ability to generate revenue from discretionary and corporate spending on entertainment and sports events, such as corporate sponsorships and advertising, is subject to many factors, including many that are beyond our control, such as general macroeconomic conditions.

Our business depends on discretionary consumer and corporate spending. Many factors related to corporate spending and discretionary consumer spending, including economic conditions affecting disposable consumer income such as unemployment levels, fuel prices, interest rates, changes in tax rates, and tax laws that impact companies or individuals and inflation can significantly impact our operating results. While consumer and corporate spending may decline at any time for reasons beyond our control, the risks associated with our businesses become more acute in periods of a slowing economy or recession, which may be accompanied by reductions in corporate sponsorship and advertising and decreases in attendance at live entertainment and sports events, among other things. There can be no assurance that consumer and corporate spending will not be adversely impacted by current economic conditions, or by any future deterioration in economic conditions, thereby possibly impacting our operating results and growth. A prolonged period of reduced consumer or corporate spending, such as those during the COVID-19 pandemic, could have an adverse effect on our business, financial condition, and results of operations.

We may not be able to adapt to or manage new content distribution platforms or changes in consumer behavior resulting from new technologies.

We must successfully adapt to and manage technological advances in our industry, including the emergence of alternative distribution platforms. If we are unable to adopt or are late in adopting technological changes and innovations that other entertainment providers offer, it may lead to a loss of consumers viewing our content, a reduction in revenues from attendance at our live events, a loss of ticket sales, or lower ticket fees. It may also lead to a reduction in our clients’ ability to monetize new platforms. Our ability to effectively generate revenue from new distribution platforms and viewing technologies will affect our ability to maintain and grow our business. Emerging forms of content distribution may provide different economic models and compete with current distribution methods (such as television, film, and pay-per-view (“PPV”)) in ways that are not entirely predictable, which could reduce consumer demand for our content offerings. We must also adapt to changing consumer behavior driven by advances that allow for time shifting and on-demand viewing, such as digital video recorders and video-on-demand, as well as internet-based and broadband content delivery and mobile devices. If we fail to adapt our distribution methods and content to emerging technologies and new distribution platforms, while also effectively preventing digital piracy, our ability to generate revenue from our targeted audiences may decline and could result in an adverse effect on our business, financial condition, and results of operations.

Because our success depends substantially on our ability to maintain a professional reputation, adverse publicity concerning us, one of our businesses, our clients, or our key personnel could adversely affect our business.

Our professional reputation is essential to our continued success and any decrease in the quality of our reputation could impair our ability to, among other things, recruit and retain qualified and experienced agents, managers, and other key personnel, retain or attract agency clients or customers, or enter into multimedia, licensing, and sponsorship engagements. Our overall reputation may be negatively impacted by a number of factors, including negative publicity concerning us, members of our management or our agents, managers, and other key personnel. In addition, we are dependent for a portion of our revenues on the relationships between content providers and the clients and key brands, such as sports leagues and federations, that we represent, many of whom are significant public personalities with large social media followings whose actions generate significant publicity and public interest. Any adverse publicity relating to such individuals or entities that we employ or represent, or to our company, including from reported or actual incidents or allegations of illegal or improper conduct, such as harassment, discrimination, or other misconduct, could result in significant media attention, even if not directly relating to or involving Endeavor, and could have a negative impact on our professional reputation. This could result in termination of licensing or other contractual relationships, or our

11

Table of Contents

employees’ ability to attract new customer or client relationships, or the loss or termination of such employees’ services, all of which could adversely affect our business, financial condition, and results of operations. Our professional reputation could also be impacted by adverse publicity relating to one or more of our owned or majority owned brands, events, or businesses.

We depend on the relationships of our agents, managers, and other key personnel with clients across many categories, including television, film, professional sports, fashion, music, literature, theater, digital, sponsorship and licensing.

We depend upon relationships that our agents, managers, and other key personnel have developed with clients across many content categories, including, among others, television, film, professional sports, fashion, music, literature, theater, digital, sponsorship, and licensing. The relationships that our agents, managers, and other key personnel have developed with studios, brands, and other key business contacts help us to secure access to sponsorships, endorsements, professional contracts, productions, events, and other opportunities for our clients. Due to the importance of those industry contacts to us, a substantial deterioration in these relationships, or substantial loss of agents, managers, or other key personnel who maintain these relationships, could adversely affect our business. In particular, our client management business is dependent upon the highly personalized relationships between our agent and manager teams and their respective clients. A substantial deterioration in the team managing a client may result in a deterioration in our relationship with, or the loss of, the clients represented by that agent or manager. The substantial loss of multiple agents or managers and their associated clients could have an adverse effect on our business, financial condition, and results of operations. Most of our agents, managers, and other key personnel are not party to long-term contracts and, in any event, can leave our employment with little or no notice. We can give no assurance that all or any of these individuals will remain with us or will retain their associations with key business contacts.

Our success depends, in part, on our continuing ability to identify, recruit, and retain qualified and experienced agents and managers. If we fail to recruit and retain suitable agents or if our relationships with our agents change or deteriorate, it could adversely affect our business.

Our success depends, in part, upon our continuing ability to identify, recruit, and retain qualified and experienced agents and managers. There is great competition for qualified and experienced agents and managers in the entertainment and sports industry, and we cannot assure you that we will be able to continue to hire or retain a sufficient number of qualified persons to meet our requirements, or that we will be able to do so under terms that are economically attractive to us. Any failure to retain certain agents and managers could lead to the loss of sponsorship, multimedia, and licensing agreements, and other engagements and have an adverse effect on our business, financial condition, and results of operations.

Our failure to identify, sign, and retain clients could adversely affect our business.

We derive substantial revenue from the engagements, sponsorships, licensing rights, and distribution agreements entered into by the clients with whom we work. We depend on identifying, signing, and retaining as clients those artists, athletes, models, and businesses whose identities or brands are in high demand by the public and, as a result, are deemed to be favorable candidates for engagements. Our competitive position is dependent on our continuing ability to attract, develop, and retain clients whose work is likely to achieve a high degree of value and recognition as well as our ability to provide such clients with sponsorships, endorsements, professional contracts, productions, events, and other opportunities. Our failure to attract and retain these clients, an increase in the costs required to attract and retain such clients, or an untimely loss or retirement of these clients could adversely affect our financial results and growth prospects. We have not entered into written agreements with many of the clients we represent. These clients may decide to discontinue their relationship with us at any time and without notice. In addition, the clients with whom we have entered into written contracts may choose not to renew their contracts with us on reasonable terms or at all or they may breach or seek to terminate these contracts. If any of our clients decide to discontinue their relationships with us, whether they are under a contract

12

Table of Contents

or not, we may be unable to recoup costs expended to develop and promote them and our financial results may be adversely affected. Further, the loss of such clients could lead other of our clients to terminate their relationships with us.

We derive substantial revenue from the sale of multimedia rights, licensing rights, and sponsorships. A significant proportion of this revenue is dependent on our commercial agreements with entertainment and sports events. Our failure to renew or replace these key commercial agreements on similar or better terms could have an adverse effect on our business, financial condition and results of operations.

Our business involves potential internal conflicts of interest and includes our client representation businesses representing both talent and content rights holders and distributors while our content businesses produce content, which may create a conflict of interest.

Increasingly, we must manage actual and potential internal conflicts of interest in our business due to the breadth and scale of our platform. Different parts of our business may have actual or potential conflicts of interest with each other, including our client representation, media production, events production, sponsorship, and content development businesses. Although we attempt to manage these conflicts appropriately, any failure to adequately address or manage internal conflicts of interest could adversely affect our reputation, and the willingness of clients and third parties to work with us may be affected if we fail, or appear to fail, to deal appropriately with actual or perceived internal conflicts of interest, which could have an adverse effect on our business, financial condition, and results of operations.

The markets in which we operate are highly competitive, both within the United States and internationally.

We face competition from a variety of other domestic and foreign companies. We face competition from alternative providers of the content, services, and events we and our clients offer and from other forms of entertainment and leisure activities in a rapidly changing and increasingly fragmented environment. Any increased competition, which may not be foreseeable, or our failure to adequately address any competitive factors, could result in reduced demand for our content, live events, clients, or key brands, which could have an adverse effect on our business, financial condition, and results of operations.

We depend on the continued service of the members of our executive management and other key employees, as well as management of acquired businesses, the loss or diminished performance of whom could adversely affect our business.

Our performance is substantially dependent on the performance of the members of our executive management and other key employees, as well as management of acquired businesses. We seek to acquire businesses that have strong management teams and often rely on these individuals to conduct day-to-day operations and pursue growth. Although we have entered into employment and severance protection agreements with certain members of our senior management team and we typically seek to sign employment agreements with the management of acquired businesses, we cannot be sure that any member of our senior management or management of the acquired businesses will remain with us or that they will not compete with us in the future. The loss of any member of our senior management team could impair our ability to execute our business plan and growth strategy, have a negative impact on our revenues and the effective working relationships that our executive management have developed, and cause employee morale problems and the loss of additional key employees, agents, managers, and clients.

We depend on key relationships with television and cable networks, satellite providers, digital streaming partners and other distribution partners, as well as corporate sponsors.

A key component of our success is our relationships with television and cable networks, satellite providers, digital streaming and other distribution partners, as well as corporate sponsors. We are dependent on maintaining these existing relationships and expanding upon them to ensure we have a robust network with whom we can

13

Table of Contents

work to arrange multimedia rights sales and sponsorship engagements, including distribution of our owned, operated, or represented events. Our television programming for our owned, operated, and represented events is distributed by television and cable networks, satellite providers, PPV, digital streaming, and other media. Because a portion of our revenues are generated, directly and indirectly, from this distribution, any failure to maintain or renew arrangements with distributors and platforms, the failure of distributors or platforms to continue to provide services to us, or the failure to enter into new distribution opportunities on terms favorable to us could adversely affect our business. We regularly engage in negotiations relating to substantial agreements covering the distribution of our television programming by carriers located in the United States and abroad. We have an important relationship with ESPN as they are the exclusive domestic home to all UFC events. We have agreements with multiple PPV providers globally and distribute a portion of our owned, operated, or represented events through PPV, including certain events that are sold exclusively through PPV. Any adverse change in these relationships or agreements or a deterioration in the perceived value of our clients, sponsorships, or these distribution channels could have an adverse effect on our business, financial condition and results of operations.

Owning and managing certain events for which we sell media and sponsorship rights, ticketing and hospitality exposes us to greater financial risk. If the live events that we own and manage are not financially successful, our business could be adversely affected.

We act as a principal by owning and managing certain live events for which we sell media and sponsorship rights, ticketing and hospitality, such as UFC’s events, the Miami Open, the Miss Universe competition, the Professional Bull Riders’ events, and On Location’s experiences. Organizing and operating a live event involves significant financial risk as we bear all or most event costs, including a significant amount of up-front costs. In addition, we typically book our live events many months in advance of holding the event and often agree to pay a fixed guaranteed amount prior to receiving any related revenue. Accordingly, if a planned event fails to occur or there is any disruption in our ability to live stream or otherwise distribute, whether as a result of technical difficulties or otherwise, we could lose a substantial amount of these up-front costs, fail to generate the anticipated revenue, and be forced to issue refunds for media and sponsorship rights, advertising fees, and ticket sales. If we are forced to postpone a planned event, we would incur substantial additional costs in order to stage the event on a new date, may have reduced attendance and revenue, and may have to refund fees. We could be compelled to cancel or postpone all or part of an event for many reasons, including poor weather, issues with obtaining permits or government regulation, performers failing to participate, as well as operational challenges caused by extraordinary incidents, such as terrorist or other security incidents, mass-casualty incidents, natural disasters, public health concerns including pandemics, or similar events. Such incidents have been shown to cause a nationwide disruption of commercial and leisure activities. We often have cancellation insurance policies in place to cover a portion of our losses if we are compelled to cancel an event, but our coverage may not be sufficient and is subject to deductibles. If the live events that we own and manage are not financially successful, we could suffer an adverse effect on our business, financial condition and results of operations.

Our recent acquisitions have caused us to grow rapidly, and we will need to continue to make changes to operate at our current size and scale. We may face difficulty in further integrating the operations of the businesses acquired in our recent transactions, and we may never realize the anticipated benefits and cost synergies from all of these transactions. If we are unable to manage our current operations or any future growth effectively, our business could be adversely affected.

Our recent acquisitions have caused us to grow rapidly, and we may need to continue to make changes to operate at our current size and scale. If we fail to realize the anticipated benefits and cost synergies from our recent acquisitions, or if we experience any unanticipated or unidentified effects in connection with these transactions, including write-offs of goodwill, accelerated amortization expenses of other intangible assets, or any unanticipated disruptions with important third-party relationships, our business, financial condition, and results of operations could be adversely affected. Moreover, our recent acquisitions involve risks and uncertainties including, without limitation, those associated with the integration of operations, financial reporting, technologies and personnel, and the potential loss of key employees, agents, managers, clients,

14

Table of Contents

customers, or strategic partners. Because the integration of the businesses acquired in our recent transactions have and will require significant time and resources, and we may not be able to manage the process successfully, these acquisitions may not be accretive to our earnings and they may negatively impact our results of operations. If our operations continue to grow, we will be required, among other things, to upgrade our management information systems and other processes and to obtain more space for our expanding administrative support and other headquarters personnel. Our continued growth could strain our resources and we could experience operating difficulties, including difficulties in hiring, training, and managing an increasing number of employees. These difficulties could result in the erosion of our brand image and reputation and could have an adverse effect on our business, financial condition, and operating results.

We may be unsuccessful in our strategic acquisitions, investments and commercial agreements, and we may pursue acquisitions, investments or commercial agreements for their strategic value in spite of the risk of lack of profitability.

We face significant uncertainty in connection with acquisitions, investments, and commercial agreements. To the extent we choose to pursue certain commercial, investment, or acquisition strategies, we may be unable to identify suitable targets for these deals, or to make these deals on favorable terms. If we identify suitable acquisition candidates, investments, or commercial partners, our ability to realize a return on the resources expended pursuing such deals, and to successfully implement or enter into them will depend on a variety of factors, including our ability to obtain financing on acceptable terms, requisite governmental approvals, as well as the factors discussed below. Additionally, we may decide to make or enter into acquisitions, investments, or commercial agreements with the understanding that such acquisitions, investments, or commercial agreements will not be profitable, but may be of strategic value to us. Our current and future acquisitions, investments, including existing investments accounted for under the equity method, or commercial agreements may also require that we make additional capital investments in the future, which would divert resources from other areas of our business. We cannot provide assurances that the anticipated strategic benefits of these deals will be realized in the long-term or at all.

We may fail to identify or assess the magnitude of certain liabilities, shortcomings, or other circumstances prior to acquiring a company, making an investment or entering into a commercial agreement and, as such, may not obtain sufficient warranties, indemnities, insurance, or other protections. This could result in unexpected litigation or regulatory exposure, unfavorable accounting treatment, unexpected increases in taxes, a loss of anticipated tax benefits, or other adverse effects on our business, operating results, or financial condition. Additionally, some warranties and indemnities may give rise to unexpected and significant liabilities. Future acquisitions and commercial arrangements that we may pursue could result in dilutive issuances of equity securities and the incurrence of further debt.

Our compliance with regulations may limit our operations and future acquisitions.

We are also subject to laws and regulations, including those relating to antitrust, that could significantly affect our ability to expand our business through acquisitions or joint ventures. For example, the Federal Trade Commission and the Antitrust Division of the U.S. Department of Justice with respect to our domestic acquisitions and joint ventures, and the European Commission, the antitrust regulator of the European Union (the “E.U.”), with respect to our European acquisitions and joint ventures, have the authority to challenge our acquisitions and joint ventures on antitrust grounds before or after the acquisitions or joint ventures are completed. State agencies, as well as comparable authorities in other countries, may also have standing to challenge these acquisitions and joint ventures under state or federal antitrust law. Our failure to comply with all applicable laws and regulations could result in, among other things, regulatory actions or legal proceedings against us, the imposition of fines, penalties, or judgments against us, or significant limitations on our activities. Multiple or repeated failures by us to comply with these laws and regulations could result in increased fines, actions or legal proceedings against us. Gaming authorities may levy fines against us or seize certain of our assets if we violate gaming regulations. In addition, the regulatory environment in which we operate is subject to

15

Table of Contents

change. New or revised requirements imposed by governmental regulatory authorities could have adverse effects on us, including increased costs of compliance. We also may be adversely affected by changes in the interpretation or enforcement of existing laws and regulations by these governmental authorities.

Our business and operations are subject to a variety of regulatory requirements in the United States and abroad, including, among other things, with respect to labor, tax, import and export, anti-corruption, data privacy and protection and communications monitoring and interception. Compliance with these regulatory requirements may be onerous and expensive, especially where these requirements are inconsistent from jurisdiction to jurisdiction or where the jurisdictional reach of certain requirements is not clearly defined or seeks to reach across national borders. Regulatory requirements in one jurisdiction may make it difficult or impossible to do business in another jurisdiction. We may also be unsuccessful in obtaining permits, licenses or other authorizations required to operate our business. While we have implemented policies and procedures designed to achieve compliance with these laws and regulations, we cannot be sure that we or our personnel will not violate applicable laws and regulations or our policies regarding the same.

We and certain of our affiliates, major stockholders (generally persons and entities beneficially owning a specified percentage (typically 5% or more) of our equity securities), directors, officers, and key employees are also subject to extensive background investigations and suitability standards in our businesses. Our failure, or the failure of any of our major stockholders, directors, officers, key employees, products, or technology, to obtain or retain a required license or approval in one jurisdiction could negatively impact our ability (or the ability of any of our major stockholders, directors, officers, key employees, products, or technology) to obtain or retain required licenses and approvals in other jurisdictions.

We share control in joint venture projects, other investments, and strategic alliances, which limits our ability to manage third-party risks associated with these projects.

We participate in a number of joint ventures, other non-controlling investments, and strategic alliances and may enter into additional joint ventures, investments, and strategic alliances in the future. In these joint ventures, investments, and strategic alliances, we often have shared control over the operation of the assets and businesses. As a result, such investments and strategic alliances may involve risks such as the possibility that a partner in an investment might become bankrupt, be unable to meet its capital contribution obligations, have economic or business interests or goals that are inconsistent with our business interests or goals, or take actions that are contrary to our instructions or to applicable laws and regulations. In addition, we may be unable to take action without the approval of our partners, or our partners could take binding actions without our consent. Consequently, actions by a partner or other third party could expose us to claims for damages, financial penalties, additional capital contributions, and reputational harm, any of which could have an adverse effect on our business, financial condition, and results of operations.

Preparing our financial statements requires us to have access to information regarding the results of operations, financial position, and cash flows of our joint ventures and other investments. Any deficiencies in their internal controls over financial reporting may affect our ability to report our financial results accurately or prevent or detect fraud. Such deficiencies also could result in restatements of, or other adjustments to, our previously reported or announced operating results, which could diminish investor confidence and reduce the market price for our Class A common stock. Additionally, if our joint ventures and other investments are unable to provide this information for any meaningful period or fail to meet expected deadlines, we may be unable to satisfy our financial reporting obligations or timely file our periodic reports.

Our key personnel may be adversely impacted by immigration restrictions and related factors.

Our ability to retain our key personnel is impacted, at least in part, by the fact that a portion of our key personnel in the United States is comprised of foreign nationals who are not United States citizens. In order to be legally allowed to work in the United States, these individuals generally hold immigrant visas (which may or may not be tied to their employment with us) or green cards, the latter of which makes them permanent residents in the United States.

16

Table of Contents

The ability of these foreign nationals to remain and work in the United States is impacted by a variety of laws and regulations, as well as the processing procedures of various government agencies. Changes in applicable laws, regulations, or procedures could adversely affect our ability to hire or retain these key personnel and could affect our costs of doing business and our ability to deliver services to our clients. In addition, if the laws, rules or procedures governing the ability of foreign nationals to work in the United States were to change or if the number of visas available for foreign nationals permitted to work in the United States were to be reduced, our business could be adversely affected, if, for example, we were unable to retain an employee who is a foreign national.

Corresponding issues apply with respect to our key personnel working in countries outside of the United States relating to citizenship and work authorizations. Similar changes in applicable laws, regulations or procedures in those countries could adversely affect our ability to hire or retain key personnel internationally.

The business of our agents and managers and the clients we represent is international in nature and may require them to frequently travel or live abroad. The ability of our key personnel and talent to travel internationally for their work is impacted by a variety of laws and regulations, policy considerations of foreign governments, the processing procedures of various government agencies and geopolitical actions, including war and terrorism, or natural disasters including earthquakes, hurricanes, floods, fires, as well as pandemics, such as the COVID-19 pandemic. In addition, our productions and live events internationally subject us to the numerous risks involved in foreign travel and operations and also subject us to local norms and regulations, including regulations requiring us to obtain visas for our key personnel and, in some cases, hired talent. Actions by the clients we represent that are out of our control may also result in certain countries barring them from travelling internationally, which could adversely affect our business. If our key personnel and talent were prevented from conducting their work internationally for any reason, it could have an adverse effect on our business, financial condition, and results of operations.

We rely on technology, such as our information systems, to conduct our business. Failure to protect our technology against breakdowns and security breaches could adversely affect our business.

We rely on technology, such as our information systems, content distribution systems, ticketing systems, and payment processing systems, to conduct our business. This technology is vulnerable to service interruptions and security breaches from inadvertent or intentional actions by our employees, partners, and vendors, or from attacks by malicious third parties. Such attacks are of ever-increasing levels of sophistication and are made by groups and individuals with a wide range of motives and expertise, including organized criminal groups, “hacktivists,” nation states, and others. The techniques used to breach security safeguards evolve rapidly, and they may be difficult to detect for an extended period of time, and the measures we take to safeguard our technology may not adequately prevent such incidents.

While we have taken steps to protect our confidential and personal information and that of our clients and other business relationships and have invested in information technology, there can be no assurance that our efforts will prevent service interruptions or security breaches in our systems or the unauthorized or inadvertent wrongful use or disclosure of such confidential information. Such incidents could adversely affect our business operations, reputation, and client relationships. Any such breach would require us to expend significant resources to mitigate the breach of security and to address matters related to any such breach, including the payment of fines. Although we maintain an insurance policy that covers data security, privacy liability, and cyber-attacks, our insurance may not be adequate to cover losses arising from breaches or attacks on our systems. We also may be required to notify regulators about any actual or perceived personal data breach as well as the individuals who are affected by the incident within strict time periods.

Furthermore, we have a large number of operating entities throughout the world and, therefore, operate on a largely decentralized basis. We are also in the process of integrating the technology of our acquired companies. The resulting size and diversity of our technology systems, as well as the systems of third-party vendors with

17

Table of Contents