UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

(Mark One)

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2019

OR

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from _________ to _________

Commission file no: 001-38903

POSTAL REALTY TRUST, INC.

(Exact name of registrant as specified in its charter)

| Maryland | 83-2586114 | |

| (State or other jurisdiction of | (IRS Employer | |

| incorporation or organization) | Identification No.) |

75 Columbia Avenue

Cedarhurst, NY 11516

(Address of principal executive offices) (Zip Code)

Registrant’s telephone number, including area code: (516) 295-7820

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class | Trading Symbol | Name of Each Exchange on Which Registered | ||

| Class A Common Stock, par value $0.01 per share | PSTL | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| Non-accelerated filer | ☒ | Smaller reporting company | ☒ |

| Emerging growth company | ☒ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

As of June 30, 2019, the last business day of the registrant’s most recently completed second fiscal quarter, the aggregate market value of the registrant’s Class A common stock held by non-affiliates of the registrant was approximately $70.9 million, based on the closing sales price of $15.75 per share as reported on the New York Stock Exchange.

As of March 25, 2020, the registrant had 5,392,906 shares of Class A common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s Definitive Proxy Statement for the 2020 Annual Meeting of Shareholders (to be filed with the Securities and Exchange Commission no later than 120 days after the end of the registrant’s fiscal year end) are incorporated by reference in this Annual Report on Form 10-K in response to Part II, Item 5 and Part III, Items 10, 11, 12, 13 and 14.

POSTAL

REALTY TRUST, INC.

ANNUAL REPORT ON FORM 10-K

FOR THE FISCAL YEAR ENDED DECEMBER 31, 2019

TABLE OF CONTENTS

i

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains “forward-looking statements” within the meaning of federal securities laws. These forward-looking statements are included throughout this Annual Report on Form 10-K, including in the sections entitled “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” “Business” and “Certain Relationships and Related Person Transactions,” and relate to matters such as our industry, business strategy, goals and expectations concerning our market position, future operations, margins, profitability, capital expenditures, financial condition, liquidity, capital resources, cash flows, results of operations and other financial and operating information. We have used the words “approximately,” “anticipate,” “assume,” “believe,” “budget,” “contemplate,” “continue,” “could,” “estimate,” “expect,” “future,” “intend,” “may,” “outlook,” “plan,” “potential,” “predict,” “project,” “seek,” “should,” “target,” “will” and similar terms and phrases to identify forward-looking statements in this Annual Report on Form 10-K.

In addition, important factors that could cause actual results to differ materially from such forward-looking statements include the risk factors in Item 1A. “Risk Factors” and elsewhere in this Annual Report on Form 10-K. New risks and uncertainties arise from time to time, and we cannot predict those events or how they might affect us. We assume no obligation to update any forward-looking statements after the date of this Annual Report on Form 10-K, except as required by applicable law. Given these risks and uncertainties, investors should not place undue reliance on forward-looking statements as a prediction of actual results.

When we use the terms “we,” “us,” “our,” the “Company,” “Postal” and “our company” in this Annual Report on Form 10-K, we are referring to Postal Realty Trust, Inc., a Maryland corporation, together with our consolidated subsidiaries, including Postal Realty LP, a Delaware limited partnership of which we are the sole general partner and to which we refer to as “our Operating Partnership.”

All of our forward-looking statements are subject to risks and uncertainties that may cause actual results to differ materially from those that we are expecting, including:

| ● | change in the status of the USPS as an independent agency of the executive branch of the U.S. federal government; | |

| ● | change in the demand for postal services delivered by the USPS; | |

| ● | the solvency and financial health of the USPS; | |

| ● | defaults on, early terminations of or non-renewal of leases by the USPS; | |

| ● | the competitive market in which we operate; | |

| ● | changes in the availability of acquisition opportunities; | |

| ● | our inability to successfully complete real estate acquisitions or dispositions on the terms and timing we expect, or at all; | |

| ● | our failure to successfully operate developed and acquired properties; | |

| ● | adverse economic or real estate developments, either nationally or in the markets in which our properties are located; | |

| ● | decreased rental rates or increased vacancy rates; | |

| ● | change in our business, financing or investment strategy or the markets in which we operate; | |

| ● | fluctuations in mortgage rates and increased operating costs; | |

| ● | changes in the method pursuant to which reference rates are determined and the phasing out of LIBOR after 2021; | |

| ● | general economic conditions; | |

| ● | financial market fluctuations; | |

| ● | our failure to generate sufficient cash flows to service our outstanding indebtedness; | |

| ● | our failure to obtain necessary outside financing on favorable terms or at all; | |

| ● | failure to hedge effectively against interest rate changes; | |

| ● | our reliance on key personnel whose continued service is not guaranteed; | |

| ● | the outcome of claims and litigation involving or affecting us; | |

| ● | changes in real estate, taxation, zoning laws and other legislation and government activity and changes to real property tax rates and the taxation of real estate investment trusts (“REITs”) in general; | |

| ● | operations through joint ventures and reliance on or disputes with co-venturers; | |

| ● | cybersecurity threats; | |

| ● | environmental uncertainties and risks related to adverse weather conditions and natural disasters; | |

| ● | governmental approvals, actions and initiatives, including the need for compliance with environmental requirements; | |

| ● | lack or insufficient amounts of insurance; | |

| ● | limitations imposed on our business in order to qualify and maintain our status as a REIT and our failure to qualify or maintain such status; | |

| ● | public health threats such as COVID-19; and | |

| ● | additional factors discussed under the sections captioned “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “Business.” |

ii

Overview

We are an internally managed real estate corporation that owns properties leased to the United States Postal Service (“USPS”). As of December 31, 2019, we owned a portfolio of 466 postal properties located in 44 states comprising approximately 1.4 million net leasable interior square feet, all of which is leased to the USPS other than a de-minimis non-postal tenant that shares space in a building leased to the USPS. We believe that we are one of the largest owners and manager, measured by net leasable square footage, of properties that are leased to the USPS. The majority of our leases are modified double-net leases, whereby the USPS is responsible for utilities and routine maintenance and reimburses the landlord for property taxes, while the landlord is responsible for insurance, roof and structure. We believe this structure helps insulate us from increases in certain operating expenses and provides a more predictable cash flow.

Our leadership team, led by our chief executive officer, Andrew Spodek, has extensive experience in the acquisition and management of properties leased to the USPS. Mr. Spodek has been active in the acquisition and management of USPS-leased properties for over 20 years. Jeremy Garber, our president, treasurer and secretary, has significant experience in the real estate and finance industries, including the property management of properties leased to the USPS. In addition to our executive management team, our Board of Directors has extensive experience in real estate and finance and with the USPS. Our Board of Directors is led by our Chairman, Patrick Donahoe, who completed his 39-year career with the USPS by serving as the 73rd Postmaster General of the United States from 2010 until his retirement in 2015.

Organization

The Company was organized in the state of Maryland on November 19, 2018 and commenced operations upon completion of our initial public offering (“IPO”) on May 17, 2019 and the related formation transactions (the “Formation Transactions”). We will elect to be treated as a real estate investment trust (“REIT”) for U.S. federal income tax purposes, commencing with our short tax year ended December 31, 2019, upon the filing of our tax returns for such year. We conduct our business through a traditional UPREIT structure in which our properties are owned by our Operating Partnership directly or through limited partnerships, limited liability companies or other subsidiaries. Upon completion of our IPO and the Formation Transactions, we owned and managed a portfolio of 271 postal properties located in 41 states, comprising 871,843 net leasable interior square feet and through our taxable REIT subsidiary (“TRS”), Postal Realty Management TRS, LLC (“PRM”), we provide fee-based third party property management services for an additional 403 postal properties currently leased to the USPS and owned by family members of Mr. Spodek and their partners. We are the sole general partner of our Operating Partnership through which our postal properties are directly or indirectly owned. As of December 31, 2019, we owned approximately 70.0% of the outstanding common units of limited partnership interest in our Operating Partnership (each, an “OP Unit,” and collectively, the “OP Units”) including long term incentive units of our Operating Partnership (each, an “LTIP Unit” and collectively, the “LTIP Units). Our Board oversees our business and affairs.

We closed our IPO on May 17, 2019, pursuant to which we sold 4,500,000 shares of our Class A common stock, par value $0.01 per share (our “Class A common stock”), at a public offering price of $17.00 per share. We raised $76.5 million in gross proceeds, resulting in net proceeds to us of approximately $71.1 million after deducting approximately $5.4 million in underwriting discounts and before giving effect to $6.4 million of other expenses relating to our IPO.

Our Class A common stock began trading on the New York Stock Exchange (the “NYSE”) under the symbol “PSTL” on May 15, 2019. In connection with the IPO and the Formation Transactions, we issued 1,333,112 OP Units, 637,058 shares of Class A common stock and 27,206 shares of our Class B common stock, par value $0.01 per share (our “Class B common stock” or “Voting Equivalency stock”), to Mr. Spodek and affiliates in exchange for certain properties and interests.

1

2019 Highlights

| ● | We completed our IPO on May 17, 2019 and raised $76.5 million in gross proceeds. |

| ● | From the date we completed our IPO to the end of 2019, we acquired approximately $57.5 million of postal properties leased to the USPS, which is comprised of approximately 560,000 net leasable interior square feet. |

| ● | We declared and paid an aggregate of $0.203 of dividends per share to our Class A common stockholders, Voting Equivalency stockholders, OP unitholders and LTIP unitholders. |

| ● | We entered into a credit agreement (the “Credit Agreement”) providing for a senior revolving credit facility (the “Credit Facility”) with revolving commitments in an aggregate principal amount of $100.0 million and a four-year term through September 2023. The Credit Agreement provides an accordion feature permitting expansion of the Credit Facility to $200.0 million, subject to customary conditions. Refer to Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations for a discussion of the exercise of a portion of the accordion feature in January 2020. |

Tenant Concentration

We acquire and manage postal properties and report our business as a single reportable segment. As of December 31, 2019, all of our properties were leased to a single tenant, the USPS other than a de-minimis non-postal tenant that shares space in a building leased to the USPS. See the discussions under Item 1A, “Risk Factors” under the caption “Risks Related to the USPS.”

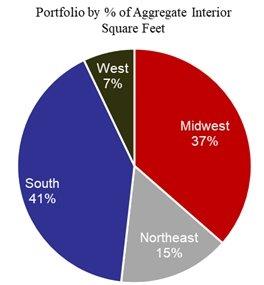

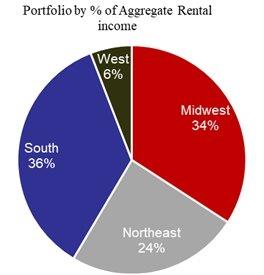

Geographic Concentration

For the year ended December 31, 2019, we owned a portfolio of 466 postal properties located in 44 states. As a percentage of our total rental revenues of $8.9 million, we had notable concentrations in the following states: Texas (10.5%), Pennsylvania (10.3%) and Massachusetts (9.7%). Such geographical concentrations could expose the Company to certain downturns in the economies of those states or other changes in such states’ respective real estate market conditions. Any material changes in the current payments programs or regulatory, economic, environmental or competitive conditions in any of these areas could have an effect on our overall business results. In the event of negative economic or other changes in any of these markets, our business, financial condition and results of operations, our ability to make distributions to our shareholders and the trading price of our common shares may be adversely affected.

Competition

We compete with other property owners in our markets that seek to acquire postal properties.

We believe that our management’s experience and relationships in, and local knowledge of, the markets in which we operate gives us a competitive advantage when seeking acquisitions. However, some of our competitors may have greater resources than we do or may have a more flexible capital structure when seeking to finance acquisitions. We believe that our intensive management services are attractive to the USPS and serve as a competitive advantage.

Environmental Matters

Under various federal, state and local laws, ordinances and regulations, as a current or former owner of real property, we may be liable for costs of the removal or remediation of certain hazardous substances, waste, or petroleum products at, on, in, under the properties that we own, including costs for investigation or remediation, natural resource damages, or third-party liability for personal injury or property damage. These laws often impose liability without regard to fault including whether the owner or operator knew of, or were responsible for, the presence or release of such materials. Some of our properties may be impacted by contamination arising from current or prior uses of the property or adjacent properties for commercial, industrial or other purposes.

Changes in laws increasing the potential liability for environmental conditions existing on properties or increasing the restrictions on discharges or other conditions may result in significant unanticipated expenditures or may otherwise adversely affect the operations of the tenants of our properties, which could materially and adversely affect us. We maintain an insurance policy for environmental liabilities at all of our properties. However, any potential or existing environmental contamination liabilities may be in excess of the coverage limits of, or not covered by, such insurance policy. As a result, we may not be aware of all potential or existing environmental contamination liabilities at the properties in our portfolio. As a result, we could potentially incur material liability for these issues.

2

In addition, some of our buildings may contain lead-based paint or asbestos containing materials or may contain or develop harmful mold or suffer from other indoor air quality issues, which could lead to liability for adverse health effects or property damage or costs for remediation. Indoor air quality issues can also stem from inadequate ventilation, chemical contamination from indoor or outdoor sources and other biological contaminants such as pollen, viruses and bacteria. Indoor exposure to lead, asbestos, or airborne toxins or irritants above certain levels can be alleged to cause a variety of adverse health effects and symptoms, including allergic or other reactions. As a result, the presence of lead, asbestos, mold or other airborne contaminants at any of our properties could require us to undertake a costly remediation program to contain or remove the mold or other airborne contaminants from the affected property or increase indoor ventilation. In addition, the presence of lead, asbestos, mold or other airborne contaminants could expose us to liability from our sole tenant, employees of our sole tenant or others if property damage or personal injury occurs. We are not presently aware of any material adverse indoor air quality issues at our properties.

Americans with Disabilities Act

Our properties must comply with Title III of the ADA to the extent that such properties are “public accommodations” as defined by the ADA. The ADA may require removal of structural barriers to access by persons with disabilities in certain public areas of our properties where such removal is readily achievable. We believe the existing properties are in substantial compliance with the ADA and that we will not be required to make substantial capital expenditures to address the requirements of the ADA. However, noncompliance with the ADA could result in imposition of fines or an award of damages to private litigants. The obligation to make readily achievable accommodations is an ongoing one, and we will continue to assess our properties and to make alterations as appropriate in this respect.

Employees

As of December 31, 2019, we had 21 full-time employees and no part time employees. We believe that our relations with our employees are satisfactory.

Availability of Reports Filed with the Securities and Exchange Commission

A copy of this Annual Report on Form 10-K, as well as our quarterly reports on Form 10-Q, current reports on Form 8-K and any amendments to such reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), are available, free of charge, on our Internet website (www.postalrealty.com). All of these reports are made available on our website as soon as reasonably practicable after they are electronically filed with or furnished to the Securities and Exchange Commission (the “SEC”). Our Governance Guidelines and Code of Business Conduct and Ethics and the charters of the Audit, Compensation, and Corporate Governance Committees of our Board of Directors are also available on our website at https://investor.postalrealtytrust.com/govdocs, and are available in print to any stockholder upon written request to Postal Realty Trust, Inc. c/o Investor Relations, 75 Columbia Avenue, Cedarhurst, New York 11516. Our telephone number is (516) 295-7820. The information on or accessible through our website is not, and shall not be deemed to be, a part of this report or incorporated into any other filing we make with the SEC.

3

The following risk factors may adversely affect our overall business, financial condition, results of operations, and cash flows; our ability to make distributions to our stockholders; our access to capital; or the market price of our Class A common stock, as further described in each risk factor below. In addition to the information set forth in this Annual Report on Form 10-K, one should carefully review and consider the information contained in our other reports and periodic filings that we make with the SEC. Those risk factors could materially affect our overall business, financial condition, results of operations, and cash flows; our ability to make distributions to our stockholders; our access to capital; or the market price of our Class A common stock. The risks that we describe in our public filings are not the only risks that we face. Additional risks and uncertainties not presently known to us, or that we currently consider immaterial, also may materially adversely affect our business, financial condition, and results of operations. Additional information regarding forward-looking statements is included in the beginning of “Part I” in this Annual Report on Form 10-K.

Risks Related to the USPS

The USPS is an independent agency of the executive branch of the U.S. federal government and any change to the USPS’s mission or purpose could have a material adverse effect on our business, financial condition and results of operations.

A change in the structure, mission, or leasing requirements of the USPS, a significant reduction in the USPS’s workforce, a relocation of personnel resources, other internal reorganization or a change in the post offices occupying our properties, would affect our lease renewal opportunities and have a material adverse effect on our business, financial condition and results of operations. In addition, any change in the federal government’s treatment of the USPS as an independent agency, including, but not limited to, the privatization of all or a portion of the USPS business operations, as has been proposed by the Trump administration, may have a material adverse effect on our business.

Our business is substantially dependent on the demand for post office space.

Any significant decrease in the demand for post office space could have an adverse effect on our business. The number of retail post office locations nationwide has decreased by approximately 1,000 post offices since 2010. Further reductions in the number of post office properties could result in entering into leases with the USPS in the future on less favorable terms than current leases, the failure of the USPS to renew leases for our properties and the reduction of the number of acquisition opportunities available to us. The level of demand for post office properties may be impacted by a variety of factors outside of our control, including changes in U.S. federal government and USPS policies or funding, changes in population density, the health and sustainability of local, regional and national economies, and the demand and use of the USPS. Moreover, technological innovations, such as autonomous delivery devices, may decrease the need for hand delivery or in-person pick up, thereby decreasing the demand for retail post offices. Recently, package delivery service providers, such as FedEx, have announced plans to implement autonomous delivery devices to assist retail companies with same-day and last-mile deliveries. The development, implementation and broad adoption of these devices may decrease the demand for postal services.

The USPS is facing legislative constraints that are hindering the USPS’s ability to maintain adequate liquidity to sustain its current operations. If the USPS’s revenues decrease due to reduced demand for postal services, then the USPS may reduce its number of post office locations.

The USPS’s inability to meet its financial obligations may render it insolvent or increase the likelihood of Congressional or regulatory reform of the USPS, which may have a material adverse effect on our business and operations.

As of December 31, 2019, the USPS had total assets of approximately $29.2 billion and total liabilities of approximately $101.5 billion. A significant portion of the USPS’s liabilities consist of unfunded fixed benefits, such as pensions and healthcare, to retired USPS workers. Although Congress regularly debates the future of the USPS, the USPS is unlikely to be able to retire its existing liabilities without regulatory or Congressional relief. If the USPS were unable to meet its financial obligations, many of our leases may be vacated by the USPS, which would have a material adverse effect on our business and operations. Any Congressional or regulatory action that decreases demand by the USPS for leased postal properties would also have a material adverse effect on our business and operations. We cannot predict whether any currently contemplated reforms will ultimately take effect and, if so, how such reforms would specifically affect us.

4

If the USPS is unable to extend its Note Purchase Agreement (as amended, the “NPA”) with the Federal Financing Bank (the “FFB”), the USPS may not be able to refinance debt with the FFB in the future at comparable terms to those currently available.

On April 1, 1999, the USPS entered into a Note Purchase Agreement with the FFB for the purpose of obtaining debt financing. Under the NPA, FFB is required to purchase notes from the USPS meeting specified conditions, up to the established maximum amounts, within five business days of delivery. The amount that the USPS borrows under the NPA varies from year to year depending upon the needs of the organization. All of the USPS’s outstanding debt as of December 31, 2019 was obtained through the NPA. The most recent extension to the NPA expired on August 31, 2019. If the USPS cannot reach acceptable terms with FFB on an extension of the NPA, the USPS would need to seek debt financing through other means, either through individual agreements with FFB (on terms that may differ from those set forth in the NPA) or from other sources. There can be no assurance that the USPS will be able to extend the term of the NPA or obtain alternative debt financing on the terms or timing that it expects, if at all.

The USPS has a substantial amount of indebtedness.

As of December 31, 2019, the USPS reported outstanding debt obligations to the FFB of $11.0 billion. As of September 30, 2019, the USPS had a total underfunded Postal Service Retiree Health Benefit Fund (“PSRHBF”) liability of $69.4 billion as reported by the United States Office of Personnel Management (“OPM”), which the USPS is required to fund in future periods. As of December 31, 2019, the USPS reported $48.4 billion as current liabilities due and payable to the PSRHBF for invoiced but unpaid contributions. As of September 30, 2019, the USPS estimated underfunded retirement benefits amortization to the Civil Service Retirement System (“CSRS”) and Federal Employees Retirement System (“FERS”) funds of $29.0 billion and $20.9 billion, respectively, as reported by OPM, which the USPS is required to fund in future periods. Of these amounts, the USPS has unpaid obligations due to OPM that total nearly $4.8 billion for CSRS amortization payments and $3.4 billion for FERS amortization payments, which the USPS reported as current liabilities. The USPS’s significant indebtedness and unpaid retirement and retiree health obligations could require the USPS to dedicate a substantial portion of its future cash flow from operations to payments on debt and retirement and retiree healthcare obligations, thus reducing the availability of cash flow to fund operating expenses, including lease payments, working capital, capital expenditures and other business activities.

The USPS is subject to congressional oversight and regulation by the PRC and other government agencies.

The USPS has a wide variety of stakeholders whose interests and needs are sometimes in conflict. The USPS operates as an independent establishment of the executive branch of the U.S. government and, as a result, is subject to a variety of regulations and other limitations applicable to federal agencies. The ability of the USPS to raise rates for its products and services is subject to the regulatory oversight and approval of the PRC. Limitations on the USPS’s ability to take action could adversely affect its operating and financial results, and as a result, reduce demand for leasing post office properties.

The business and results of operations of the USPS are significantly affected by competition from both competitors in the delivery marketplace as well as substitute products and digital communication.

Failure of the USPS to compete effectively and operate efficiently, grow marketing mail and package delivery services, and increase revenue and contribution from other sources, will adversely impact the USPS’s financial condition and this adverse impact will become more substantial over time. The USPS’s marketplace competitors include both local and national providers of package delivery services. The USPS’s competitors have different cost structures and fewer regulatory restrictions and are able to offer differing services and pricing, which may hinder the USPS’s ability to remain competitive in these service areas. In addition, most of the USPS’s competitors have access to capital markets, which allows them greater flexibility in the financing and expansion of their business. Customer usage of postal services continues to shift to substitute products and digital communication. The use of e-mail and other forms of electronic communication have reduced first class mail volume, as have electronic billing and payment. Marketing mail has recently experienced declines due to mailers’ growing use of digital advertising including digital mobile advertising. The volume of the USPS’s periodicals service continues to decline as consumers increasingly use electronic media for news and information. The growth in the USPS’s competitive service volumes over the past five years is largely attributable to the USPS’s three largest customers, UPS, FedEx and Amazon. Each of these customers is building delivery capability that could enable it to divert volume away from the USPS over time. If these customers divert significant volume away from the USPS, the growth in the USPS’s competitive service volumes may not continue, and there may be reduced demand for leasing postal properties by the USPS.

5

The USPS’s need to streamline its operations in response to declining mail volume may result in significant costs.

The USPS has considered and is considering on an ongoing basis whether to reduce its workforce and physical infrastructure to a level commensurate with declining mail volume. The USPS’s ongoing reviews of cost-savings opportunities may identify opportunities that impact mail processing operations or affect lobby hours of retail units, post offices or other facilities. Future changes in the USPS’s business strategy, operations, legislation, government regulations or economic or market conditions may result in reduced demand for leasing post offices by the USPS.

The inability of the Board of Governors of the USPS to form a quorum as due to an insufficient number of confirmed sitting Governors could adversely affect the ability of the USPS to increase postal rates, and as a result, adversely affect the USPS’s results of operations and diminish demand for the leasing of postal properties.

The Board of Governors of the USPS normally consists of nine Governors appointed by the President of the United States with the advice and consent of the Senate. The nine Governors select the Postmaster General, who becomes a member of the Board, and those ten individuals select the Deputy Postmaster General, who also serves on the Board of Governors. The Postmaster General serves at the pleasure of the Governors for an indefinite term and the Deputy Postmaster General serves at the pleasure of the Governors and the Postmaster General. The Board of Governors is required to have a quorum of six members to exercise certain powers. In the event the Board of Governors is unable to form a quorum due to an insufficient number of confirmed sitting Governors ,the USPS’s operations, including the ability of the USPS to increase postal rates and diminish demand for the leasing of postal properties, could be adversely affected.

The USPS’s potential insolvency, inability to pay rent or bankruptcy would have a material adverse effect on us, including on our financial condition, results of operations, cash flow, cash available for distribution, and our ability to service our debt obligations and could result in our inability to continue as a going concern.

Default by the USPS is likely to cause significant or complete reduction in the operating cash flow generated by our properties. There can be no assurance that the USPS will be able to avoid insolvency, make timely rental payments or avoid defaulting under its leases. If the USPS defaults, we may experience delays in enforcing our rights as landlord and may incur substantial costs in protecting our investment. Because we depend on rental payments from the USPS, the inability of the USPS to make its lease payments could adversely affect us and our ability to make distributions to you.

Although we do not believe that bankruptcy protection under the United States bankruptcy code is available to the USPS, the law is unclear. If the USPS were to file for bankruptcy, we would become a creditor, but we may not be able to collect all or any of the pre-bankruptcy amounts owed to owe us by the USPS. In addition, if the USPS were to file for bankruptcy protection, it potentially could terminate its leases with us under federal law, in which event we would have a general unsecured claim against the USPS that would likely be worth less than the full amount owed to us for the remainder of the lease term. This would have a severe adverse effect on our business, financial condition and results of operations.

Because the USPS is an independent agency of the U.S. federal government, our properties may have a higher risk of terrorist attack than similar properties leased to non-governmental tenants.

Terrorist attacks may materially adversely affect our operations, as well as directly or indirectly damage our assets, both physically and financially. Because the USPS is, and is expected to continue to be, an independent agency of the U.S. federal government, our properties are presumed to have a higher risk of terrorist attack than similar properties that are leased to non-governmental affiliated tenants. Terrorist attacks, to the extent that these properties are uninsured or underinsured, could have a material adverse effect on our business, financial condition and results of operations.

Public health threats such as COVID-19 could have a material adverse effect on the demand for post office properties and USPS operations.

The ongoing COVID-19 pandemic has resulted in a reduction in foot traffic in many public places, including post office properties. A continued reduction in the use of in-person services at post office properties may reduce the demand for post office properties by the USPS and our results of operations could decline as a result. In addition, the USPS is dependent on the efforts of its employees, many of whom come into contact with a large number of individuals on a daily basis. If USPS employees are unwilling or unable to report to work regularly because of the COVID-19 pandemic or USPS services are otherwise diminished as a result of governmental response to the pandemic, the demand for USPS services or the reputation of the USPS may suffer, leading to a reduced need for post office properties and adversely affecting our business and results of operations.

6

Risks Related to Our Business and Operations

We may be unable to identify and complete acquisitions of properties that meet our investment criteria, which may materially adversely affect our financial condition, results of operations, cash flow and growth prospects.

Our business and growth strategy involves the selective acquisition of post office properties. We may expend significant management time and other resources, including out-of-pocket costs, in pursuing these investment opportunities. Our ability to acquire properties on favorable terms, or at all, may be exposed to the following significant risks:

| ● | we may incur significant costs and divert management attention in connection with evaluating and negotiating potential acquisitions, including those that we are subsequently unable to complete; |

| ● | agreements for the acquisition of properties are subject to conditions, which we may be unable to satisfy; and |

| ● | we may be unable to obtain financing on favorable terms or at all. |

If we are unable to identify attractive investment opportunities, our financial condition, results of operations, cash flow and growth prospects could be materially adversely affected.

We may be unable to acquire and/or manage additional USPS-leased properties at competitive prices or at all.

A significant portion of our business plan is to acquire additional properties that are leased to the USPS. There are a limited number of such properties, and we will have fewer opportunities to grow our investments than REITs that purchase properties that are leased to a variety of tenants or that are not leased when they are acquired. In addition, the current ownership of properties leased to the USPS is highly fragmented with the overwhelming majority of owners holding a single property. As a result, we may need to expend resources to complete our due diligence and underwriting process on many individual properties, thereby increasing our acquisition costs and possibly reducing the amount that we are able to pay for a particular property. Accordingly, our plan to grow our business largely by acquiring additional properties that are leased to the USPS and managing properties leased to the USPS by third parties may not succeed.

There are a limited number of post office properties and competition to buy these properties may be significant.

We plan to acquire properties which are leased to the USPS whenever we are able to identify attractive opportunities and have sufficient available financing to complete such acquisitions. We may face competition for acquisition opportunities from other investors and this competition may subject us to the following risks:

| ● | we may be unable to acquire a desired property because of competition from other well capitalized real estate investors, including private investment funds and others; and |

| ● | competition from other real estate investors may significantly increase the purchase price we must pay to acquire properties. |

In addition, because of our public profile as the only publicly traded REIT dedicated to USPS properties, our IPO and operations may generate new interest in USPS-leased properties from other REITs, real estate companies and other investors with more resources than we have that did not previously focus on investment opportunities with USPS-leased properties.

We currently have a concentration of post office properties in Pennsylvania, Oklahoma, Texas, Illinois, North Carolina and Missouri and are exposed to changes in market conditions in these states.

Our business may be adversely affected by local economic conditions in the areas in which we operate, particularly in Pennsylvania, Oklahoma, Texas, Illinois, North Carolina and Missouri, where many of our post office properties are concentrated. Factors that may affect our occupancy levels, our rental revenues, our funds from operations or the value of our properties include the following, among others:

| ● | downturns in global, national, regional and local economic conditions; |

| ● | possible reduction of the USPS workforce; and |

| ● | economic conditions that could cause an increase in our operating expenses, insurance and routine maintenance. |

7

We may be unable to renew leases or sell vacated properties on favorable terms, or at all, as leases expire, which could materially adversely affect us, including our financial condition, results of operations, cash flow, cash available for distribution and our ability to service our debt obligations.

Although 100% of our properties were leased to the USPS, other than a de-minimis non-postal tenant that shares space in a building leased to the USPS as of December 31, 2019, we cannot assure you that leases will be renewed or that vacated properties will be sold on favorable terms, or at all. If rental rates for our properties decrease, our existing tenant does not renew their leases or we do not sell vacated properties on favorable terms, our financial condition, results of operations, cash flow, cash available for distributions and our ability to service our debt obligations could be materially adversely affected.

We may be required to make rent or other concessions to improve our properties in order to retain the USPS, which may materially adversely affect us.

Upon expiration of our leases to the USPS we may be required to make rent or other concessions, which would increase our costs. If we are unwilling or unable to make rent or other concessions and/or expenditures, this could result in non-renewals to the USPS upon expiration of its leases, which could have a material adverse effect on us, including our financial condition, results of operations, cash flow, cash available for distribution and our ability to service our debt obligations.

Property vacancies could result in significant capital expenditures and illiquidity.

The loss of a tenant through lease expiration may require us to spend significant amounts of capital to renovate the property before it is suitable for a new tenant. All of the properties we acquire are specifically suited to the particular business of the USPS and, as a result, if the USPS does not renew its lease, we may be required to renovate the property at substantial costs, decrease the rent we charge or provide other concessions in order to lease the property to another tenant. In the event we are required to sell the property, we may have difficulty selling it to a party other than the USPS. This potential illiquidity may limit our ability to quickly modify our portfolio in response to changes in economic or other conditions, which may materially and adversely affect us.

As of December 31, 2019, 20 of our leases were either in holdover status or expired on December 31, 2019, and if we are unable to renew these leases on equivalent terms, we might experience lower rental revenue, net operating income, cash flows and funds available for distributions.

As of December 31, 2019, 20 of our leases were either in holdover status or expired on December 31, 2019. See “Item 2. Properties— Lease Expiration Schedule”. As of March 25, 2020, 32 leases were in holdover status representing $1.1 million of annual rental revenue for the year ended December 31, 2019. We might not be successful in renewing the leases that are in holdover status or that are expiring in 2020, or obtaining positive rent renewal spreads, or even renewing the leases on terms comparable to those of the expiring leases. If we are not successful, we will likely experience reduced occupancy, traffic, rental revenue and net operating income, which could have a material adverse effect on our financial condition, results of operations and ability to make distributions to shareholders.

Our use of OP Units as consideration to acquire properties could result in stockholder dilution and/or limit our ability to sell such properties, which could have a material adverse effect on us.

We may acquire properties or portfolios of properties through tax deferred contribution transactions in exchange for OP Units, which may result in stockholder dilution. This acquisition structure may have the effect of, among other things, reducing the amount of tax depreciation we could deduct over the tax life of the acquired properties, and may require that we agree to protect the contributors’ ability to defer recognition of taxable gain through restrictions on our ability to dispose of the acquired properties and/or the allocation of partnership debt to the contributors to maintain their tax bases. These restrictions could limit our ability to sell properties at a time, or on terms, that would be favorable absent such restrictions.

8

Illiquidity of post office properties could significantly impede our ability to respond to adverse changes in the performance of our properties and harm our financial condition.

Our ability to promptly sell one or more post office properties in our portfolio in response to changing economic, financial and investment conditions may be limited. Certain types of real estate and in particular, post offices, may have limited alternative uses and thus are relatively illiquid. Return of capital and realization of gains, if any, from an investment generally will occur upon disposition or refinancing of the underlying property. We may be unable to realize our investment objectives by sale, other disposition or refinancing at attractive prices within any given period of time or may otherwise be unable to complete any exit strategy. In particular, our ability to dispose of one or more post office properties within a specific time period is subject to certain limitations imposed by our tax protection agreements, as well as weakness in or even the lack of an established market for a property, changes in the financial condition or prospects of prospective purchasers, changes in national or international economic conditions and changes in laws, regulations or fiscal policies of jurisdictions in which the property is located.

In addition, the Code imposes restrictions on a REIT’s ability to dispose of properties that are not applicable to other types of real estate companies. In particular, the tax laws applicable to REITs effectively require that we hold our properties for investment, rather than primarily for sale in the ordinary course of business, which may cause us to forego or defer sales of properties that otherwise would be in our best interests. Therefore, we may not be able to vary our portfolio in response to economic or other conditions promptly or on favorable terms.

Our business is subject to risks associated with real estate assets and the real estate industry, which could materially adversely affect our financial condition, results of operations, cash flow, cash available for distribution and our ability to service our debt obligations.

Our ability to pay expected dividends to our stockholders depends on our ability to generate revenues in excess of expenses, scheduled principal payments on debt and capital expenditure requirements. Events and conditions generally applicable to owners and operators of real property that are beyond our control may decrease cash available for distribution and the value of our properties. These events include the risks set forth here under “—Risks Related to Our Business and Operations,” as well as the following:

| ● | adverse changes in financial conditions of buyers, sellers and tenants of properties; |

| ● | vacancies or our inability to rent space on favorable terms, including possible market pressures to offer tenants rent abatements, tenant improvements, early termination rights or below-market renewal options, and the need to periodically repair, renovate and re-let space; |

| ● | increased operating costs, including insurance premiums, utilities, real estate taxes and state and local taxes; |

| ● | civil unrest, acts of war, terrorist attacks, pandemics or other health crisis, such as the recent outbreak of novel coronavirus (COVID-19) and natural disasters, including hurricanes, which may result in uninsured or underinsured losses; |

| ● | decreases in the underlying value of our real estate; and |

| ● | changing market demographics. |

In addition, periods of economic downturn or recession, rising interest rates or declining demand for real estate, or the public perception that any of these events may occur, could result in a general decline in rents or an increased incidence of defaults under existing leases, which could materially adversely affect our financial condition, results of operations, cash flow, cash available for distribution and ability to service our debt obligations.

9

The failure of properties acquired in the future to meet our financial expectations could have a material adverse effect on us, including our financial condition, results of operations, cash flow, the per share trading price of our Class A common stock and our growth prospects.

Our future acquisitions and our ability to successfully operate these properties may be exposed to the following significant risks, among others:

| ● | we may acquire properties that are not accretive to our results upon acquisition, and we may not successfully manage and lease those properties to meet our expectations; |

| ● | our cash flow may be insufficient to enable us to pay the required principal and interest payments on the debt secured by the property; |

| ● | we may spend more than budgeted amounts to make necessary improvements or renovations to acquired properties; |

| ● | we may be unable to quickly and efficiently integrate new acquisitions into our existing operations; |

| ● | market conditions may result in higher than expected vacancy rates and lower than expected rental rates; and |

| ● | we may acquire properties subject to liabilities and without any recourse, or with only limited recourse, with respect to unknown liabilities such as liabilities for clean-up of undisclosed environmental contamination, claims by tenants, vendors or other persons dealing with the former owners of the properties, liabilities incurred in the ordinary course of business and claims for indemnification by general partners, directors, officers and others indemnified by the former owners of the properties. |

If we cannot operate acquired properties to meet our financial expectations, our growth prospects could be materially adversely affected.

Many of our operating costs and expenses are fixed and will not decline if our revenues decline.

Our results of operations depend, in large part, on our level of revenues, operating costs and expenses. The expense of owning and operating a property is not necessarily reduced when circumstances such as market factors and competition cause a reduction in revenue from the property. As a result, if revenues decline, we may not be able to reduce our expenses to keep pace with the corresponding reductions in revenues. Many of the costs associated with real estate investments, such as insurance, loan payments and maintenance, generally will not be reduced if a property is not fully occupied or other circumstances cause our revenues to decrease, which could have a material adverse effect on us, including our financial condition, results of operations, cash flow, cash available for distribution and our ability to service our debt obligations.

Our real estate taxes for properties where we are not reimbursed could increase due to property tax rate changes or reassessment, which could impact our cash flows our financial condition, results of operations, cash flows, per share market price of our Class A common stock and our ability to satisfy our principal and interest obligations and to make distributions to our shareholders could be adversely affected.

Even though we intend to qualify as a REIT for U.S. federal income tax purposes, we are required to pay state and local taxes on our properties. The real property taxes on our properties may increase as property tax rates change or as our properties are assessed or reassessed by taxing authorities. Therefore, the amount of property taxes we pay in the future may increase substantially from what we have paid in the past. If the property taxes we pay increase, our financial condition, results of operations, cash flows, per share trading price of our Class A common stock and our ability to satisfy our principal and interest obligations and to make distributions to our shareholders could be adversely affected.

Increases in mortgage rates or unavailability of mortgage debt may make it difficult for us to finance or refinance our debt, which could have a material adverse effect on our financial condition, growth prospects and our ability to make distributions to stockholders.

If mortgage debt is unavailable to us at reasonable rates or at all, we may not be able to finance the purchase of additional properties or refinance existing debt when it becomes due. If interest rates are higher when we refinance our properties, our income and cash flow could be reduced, which would reduce cash available for distribution to our stockholders and may hinder our ability to raise more capital by issuing more stock or by borrowing more money. In addition, to the extent we are unable to refinance our debt when it becomes due, we will have fewer debt guarantee opportunities available to offer under our tax protection agreements, which could trigger an obligation to indemnify the protected parties under the tax protection agreements.

10

Mortgage debt obligations expose us to the possibility of foreclosure, which could result in the loss of our investment in a property or group of properties subject to mortgage debt.

Mortgage and other secured debt obligations increase our risk of property losses because defaults on indebtedness secured by properties may result in foreclosure actions initiated by lenders and ultimately our loss of the property securing any loans for which we are in default. Any foreclosure on a mortgaged property or group of properties could adversely affect the overall value of our portfolio of properties. For tax purposes, a foreclosure on any of our properties that is subject to a nonrecourse mortgage loan would be treated as a sale of the property for a purchase price equal to the outstanding balance of the debt secured by the mortgage. If the outstanding balance of the debt secured by the mortgage exceeds our tax basis in the property, we would recognize taxable income on foreclosure, but would not receive any cash proceeds, which could hinder our ability to meet the REIT distribution requirements imposed by the Code. Foreclosures could also trigger our tax indemnification obligations under the terms of our tax protection agreements with respect to the sales of certain properties.

Our future debt arrangements may involve balloon payment obligations, which may materially adversely affect us, including our cash flows, financial condition and ability to make distributions.

Our future debt arrangements may require us to make a lump-sum or “balloon” payment at maturity. Our ability to make a balloon payment at maturity is uncertain and may depend upon our ability to obtain additional financing or our ability to sell the property. At the time the balloon payment is due, we may or may not be able to refinance the existing financing on terms as favorable as the original loan or sell the property at a price sufficient to make the balloon payment. In addition, balloon payments and payments of principal and interest on our indebtedness may leave us with insufficient cash to pay the distributions that we are required to pay to qualify and maintain our qualification as a REIT.

Changes in the method pursuant to which the reference rates are determined and the phasing out of LIBOR after 2021 may affect our financial results.

The chief executive of the United Kingdom Financial Conduct Authority (“FCA”), which regulates LIBOR, has announced that the FCA intends to stop compelling banks to submit rates for the calculation of LIBOR after 2021. It is not possible to predict the effect of these changes, other reforms or the establishment of alternative reference rates in the United Kingdom or elsewhere. Furthermore, in the United States, efforts to identify a set of alternative U.S. dollar reference interest rates include proposals by the Alternative Reference Rates Committee of the Federal Reserve Board and the Federal Reserve Bank of New York. The U.S. Federal Reserve, in conjunction with the Alternative Reference Rates Committee, a steering committee comprised of large US financial institutions, is considering replacing U.S. dollar LIBOR with the Secured Overnight Financing Rate (“SOFR”), a new index calculated by short-term repurchase agreements, backed by Treasury securities. The Federal Reserve Bank of New York began publishing SOFR rates in April 2018. The market transition away from LIBOR and towards SOFR is expected to be gradual and complicated. There are significant differences between LIBOR and SOFR, such as LIBOR being an unsecured lending rate and SOFR a secured lending rate, and SOFR is an overnight rate and LIBOR reflects term rates at different maturities. These and other differences create the potential for basis risk between the two rates. The impact of any basis risk between LIBOR and SOFR may negatively affect our operating results. Any of these alternative methods may result in interest rates that are higher than if LIBOR were available in its current form, which could have a material adverse effect on results.

Any changes announced by the FCA, including the FCA Announcement, other regulators or any other successor governance or oversight body, or future changes adopted by such body, in the method pursuant to which reference rates are determined may result in a sudden or prolonged increase or decrease in the reported reference rates. If that were to occur, the level of interest payments we incur may change. In addition, although certain of our LIBOR based obligations provide for alternative methods of calculating the interest rate payable on certain of our obligations if LIBOR is not reported, which include requesting certain rates from major reference banks in London or New York, or alternatively using LIBOR for the immediately preceding interest period or using the. initial interest rate, as applicable, uncertainty as to the extent and manner of future changes may result.

Adverse economic and geopolitical conditions and dislocations in the credit markets could have a material adverse effect on us, including our financial condition, results of operations, cash flow, cash available for distribution and our ability to service our debt obligations.

Our business may be affected by market and economic challenges experienced by the U.S. economy or real estate industry as a whole, such as the dislocations in the credit markets and general global economic downturn during the recent recessionary period. These conditions, or similar conditions in the future, may materially adversely affect us as a result of the following potential consequences, among others:

| ● | decreased demand for post office space, which would cause market rental rates and property values to be negatively impacted; |

11

| ● | reduced values of our properties may limit our ability to dispose of assets at attractive prices or obtain debt financing secured by our properties and may reduce the availability of unsecured loans; |

| ● | our ability to obtain financing on terms and conditions that we find acceptable, or at all, may be limited, which could reduce our ability to pursue acquisition and development opportunities and refinance existing debt, reduce our returns from our acquisition and development activities and increase our future debt service expense; and |

| ● | lenders’ refusals to fund their financing commitment on favorable terms, or at all. |

Covenants in our debt agreements could adversely affect our financial condition.

Our Credit Agreement contains customary restrictions, requirements and other limitations on our ability to incur indebtedness. We must maintain certain ratios, including a maximum of total indebtedness to total asset value, a maximum of secured indebtedness to total asset value, a minimum of quarterly adjusted EBITDA to fixed charges, a minimum net operating income from unencumbered properties to unsecured interest expense and a maximum of unsecured indebtedness to unencumbered asset value. Our ability to borrow under our Credit Agreement is subject to compliance with our financial and other covenants.

Failure to comply with any of the covenants under our Credit Agreement or other debt instruments could result in a default under one or more of our debt instruments. In particular, we could suffer a default under a secured debt instrument that could exceed a cross-default threshold under our Credit Agreement, causing an event of default under the Credit Agreement. Under those circumstances, other sources of capital may not be available to us or be available only on unattractive terms. In addition, if we breach covenants in our debt agreements, the lenders can declare a default and, if the debt is secured, take possession of the property securing the defaulted loan.

Alternatively, even if a secured debt instrument is below the cross-default threshold for non-recourse secured debt under our Credit Agreement a default under such secured debt instrument may still cause a cross default under our Credit Agreement because such secured debt instrument may not qualify as “non-recourse” under the definition in our Credit Agreement. Another possible cross default could occur between our Credit Agreement and any senior unsecured notes that we issue. Any of the foregoing default or cross-default events could cause our lenders to accelerate the timing of payments and/or prohibit future borrowings, either of which would have a material adverse effect on our business, operations, financial condition and liquidity.

Failure to hedge effectively against interest rate changes may adversely affect our financial condition, results of operations, cash flow, cash available for distribution and our ability to service our debt obligations.

Subject to qualifying and maintaining our qualification as a REIT, we may enter into hedging transactions to protect us from the effects of interest rate fluctuations on floating rate debt. Our hedging transactions may include entering into interest rate cap agreements or interest rate swap agreements. These agreements involve risks, such as the risk that such arrangements would not be effective in reducing our exposure to interest rate changes or that a court could rule that such an agreement is not legally enforceable. In addition, interest rate hedging can be expensive, particularly during periods of rising and volatile interest rates. Hedging could increase our costs and reduce the overall returns on our investments. In addition, while hedging agreements would be intended to lessen the impact of rising interest rates on us, they could also expose us to the risk that the other parties to the agreements would not perform, we could incur significant costs associated with the settlement of the agreements or that the underlying transactions could fail to qualify as highly-effective cash flow hedges under Financial Accounting Standards Board, or FASB, Accounting Standards Codification, or ASC, Topic 815, Derivatives and Hedging.

Our success depends on key personnel whose continued service is not guaranteed, and the loss of one or more of our key personnel could adversely affect our ability to manage our business and to implement our growth strategies, or could create a negative perception of our company in the capital markets.

Our continued success and our ability to manage anticipated future growth depend, in large part, upon the efforts of key personnel, particularly Messrs. Spodek and Garber who have extensive market knowledge and relationships and exercise substantial influence over our operational and financing activity. Among the reasons that these individuals are important to our success is that each has a national or regional industry reputation that attracts business and investment opportunities and assists us in negotiations with lenders, the USPS and owners of postal properties. If we lose their services, such relationships could diminish or be adversely affected. Our employment agreements with Messrs. Spodek and Garber do not guarantee their continued employment with us.

12

Many of our other senior executives also have extensive experience and strong reputations in the real estate industry, which aid us in identifying opportunities, having opportunities brought to us and negotiating. The loss of services of one or more members of our senior management team, or our inability to attract and retain highly qualified personnel, could adversely affect our business, diminish our investment opportunities and weaken our relationships with lenders, business partners, existing and prospective tenants and industry participants, which could materially adversely affect our financial condition, results of operations, cash flow and the per share trading price of our Class A common stock.

We may be subject to on-going or future litigation, including existing claims relating to the entities that owned the properties previously and otherwise in the ordinary course of business, which could have a material adverse effect on our financial condition, results of operations, cash flow and the per share trading price of our Class A common stock.

We may be subject to litigation, including existing claims relating to the entities that owned the properties previously and otherwise in the ordinary course of business. Some of these claims may result in significant defense costs and potentially significant judgments against us, some of which are not, or cannot be, insured against. We generally intend to vigorously defend ourselves. However, we cannot be certain of the ultimate outcomes of any currently asserted claims or of those that may arise in the future. Resolution of these types of matters against us may result in our having to pay significant fines, judgments, or settlements, which, if uninsured, or if the fines, judgments, and settlements exceed insured levels, could adversely impact our earnings and cash flows, thereby having an adverse effect on our financial condition, results of operations, cash flow, cash available for distribution and our ability to service our debt obligations. Certain litigation or the resolution of certain litigation may affect the availability or cost of some of our insurance coverage, which could materially adversely affect our results of operations and cash flows, expose us to increased risks that would be uninsured and/or adversely impact our ability to attract officers and directors.

We may not be able to rebuild our existing properties to their existing specifications if we experience a substantial or comprehensive loss of such properties.

In the event that we experience a substantial or comprehensive loss of one of our properties, we may not be able to rebuild such property to its existing specifications. Further, reconstruction or improvement of such a property would likely require significant upgrades to meet zoning and building code requirements. Environmental and legal restrictions could also restrict the rebuilding of our properties.

Joint venture investments could be adversely affected by our lack of sole decision-making authority, our reliance on co-venturers’ financial condition and disputes between us and our co-venturers.

In the past, the Predecessor had, and in the future, we may, co-invest with third parties through partnerships, joint ventures or other entities, acquiring non-controlling interests in and managing the affairs of a property, partnership, joint venture or other entity. With respect to any such arrangement or any similar arrangement that we may enter into in the future, we may not be in a position to exercise sole decision-making authority regarding the development, property, partnership, joint venture or other entity. Investments in partnerships, joint ventures or other entities may, under certain circumstances, involve risks not present where a third party is not involved, including the possibility that partners or co-venturers might become bankrupt or fail to fund their share of required capital contributions. Partners or co-venturers may have economic or other business interests or goals which are inconsistent with our business interests or goals and may be in a position to take actions contrary to our policies or objectives, and they may have competing interests in our markets that could create conflicts of interest. Such investments may also have the potential risk of impasses on decisions, such as a sale or financing, because neither we nor the partner(s) or co-venturer(s) would have full control over the partnership or joint venture. In addition, a sale or transfer by us to a third party of our interests in the joint venture may be subject to consent rights or rights of first refusal, in favor of our joint venture partners, which would in each case restrict our ability to dispose of our interest in the joint venture. Where we are a limited partner or non-managing member in any partnership or limited liability company, if such entity takes or expects to take actions that could jeopardize our status as a REIT or require us to pay tax, we may be forced to dispose of our interest in such entity. We may, in certain circumstances, be liable for the actions of a partner, and the activities of a partner could adversely affect our ability to maintain our qualification as a REIT or our exclusion or exemption from registration under the Investment Company Act, even if we do not control the joint venture. Disputes between us and partners or co-venturers may result in litigation or arbitration that would increase our expenses and prevent our officers and directors from focusing their time and effort on our business. Consequently, actions by or disputes with partners or co-venturers might result in subjecting properties owned by the partnership or joint venture to additional risk. In addition, we may in certain circumstances be liable for the actions of our third-party partners or co-venturers. Our joint ventures may be subject to debt and, during periods of volatile credit markets, the refinancing of such debt may require equity capital calls.

13

We face cybersecurity risks and risks associated with security breaches which have the potential to disrupt our operations, cause material harm to our financial condition, result in misappropriation of assets, compromise confidential information and/or damage our business relationships and can provide no assurance that the steps we and our service providers take in response to these risks will be effective.

We face cybersecurity risks and risks associated with security breaches or disruptions, such as through cyber-attacks or cyber intrusions over the Internet, malware, computer viruses, attachments to emails, social engineering and phishing schemes or persons inside our organization. The risk of a security breach or disruption, particularly through cyber-attacks or cyber intrusions, including by computer hackers, nation-state affiliated actors, and cyber terrorists, has generally increased as the number, intensity and sophistication of attempted attacks and intrusions from around the world have increased. These incidents may result in disruption of our operations, material harm to our financial condition, cash flows and the market price of our common shares, misappropriation of assets, compromise or corruption of confidential information collected in the course of conducting our business, liability for stolen information or assets, increased cybersecurity protection and insurance costs, regulatory enforcement, litigation and damage to our stakeholder relationships. These risks require continuous and likely increasing attention and other resources from us to, among other actions, identify and quantify these risks, upgrade and expand our technologies, systems and processes to adequately address them and provide periodic training for our employees to assist them in detecting phishing, malware and other schemes. Such attention diverts time and other resources from other activities and there is no assurance that our efforts will be effective. Additionally, we rely on third-party service providers in our conduct of day-to-day property management, leasing and other activities at our properties and we can provide no assurance that the networks and systems that our third-party vendors have established or used will be effective.

In the normal course of business, we and our service providers (including service providers engaged in providing property management, leasing, accounting and/or payroll services) collect and retain certain personal information provided by our tenants, employees and vendors. We also rely extensively on computer systems to process transactions and manage our business. We can provide no assurance that the data security measures designed to protect confidential information on our systems established by us and our service providers will be able to prevent unauthorized access to this personal information. There can be no assurance that our efforts to maintain the security and integrity of the information we and our service providers collect and our and their computer systems will be effective or that attempted security breaches or disruptions would not be successful or damaging with the potential for disruption in our operations, material harm to our financial condition, cash flows and the market price of our common shares, increased cybersecurity protection and insurance costs, regulatory enforcement, litigation and damage to our stakeholder relationships.

Competition for skilled personnel could increase our labor costs.

We compete intensely with various other companies in attracting and retaining qualified and skilled personnel. We depend on our ability to attract and retain skilled management personnel in order to successfully manage the day-to-day operations of our company. Competitive pressures may require that we enhance our pay and benefits package to compete effectively for such personnel. We may not be able to offset such added costs by increasing the rates we charge the USPS. If there is an increase in these costs or if we fail to attract and retain qualified and skilled personnel, our business and operating results could be harmed.

Our growth depends on external sources of capital that are outside of our control and may not be available to us on commercially reasonable terms or at all, which could limit our ability to, among other things, meet our capital and operating needs or make the cash distributions to our stockholders necessary to qualify and maintain our qualification as a REIT.

In order to qualify and maintain our qualification as a REIT, we are required under the Code to, among other things, distribute annually at least 90% of our REIT taxable income, determined without regard to the dividends paid deduction and excluding any net capital gains. In addition, we will be subject to income tax at regular corporate rates to the extent that we distribute less than 100% of our REIT taxable income, including any net capital gains. Because of these distribution requirements, we may not be able to fund future capital needs, including any necessary capital expenditures, from operating cash flow. Consequently, we rely on third-party sources to fund our capital needs. We may not be able to obtain such financing on favorable terms or at all and any additional debt we incur will increase our leverage and likelihood of default. Our access to third-party sources of capital depends, in part, on:

| ● | general market conditions; |

| ● | the market’s perception of our growth potential; |

14

| ● | our current debt levels; |

| ● | our current and expected future earnings; |

| ● | our cash flow and cash distributions; and |

| ● | the market price per share of our Class A common stock. |

Historically, the capital markets have been subject to significant disruptions. If we cannot obtain capital from third-party sources, we may not be able to acquire or develop properties when strategic opportunities exist, meet the capital and operating needs of our existing properties, satisfy our debt service obligations or make the cash distributions to our stockholders necessary to qualify and maintain our qualification as a REIT.

We could incur significant costs and liabilities related to environmental matters.