|

As filed with the Securities and Exchange Commission on September 23, 2020. |

Offering Circular No. 024-11290 |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_________________

FORM 1-A/A

(Amendment No. 4)

REGULATION A OFFERING CIRCULAR

UNDER THE SECURITIES ACT OF 1933

_________________

CONTACT GOLD CORP.

(Exact name of Registrant as specified in its charter)

|

Nevada |

1041 |

98-1369960 |

|

400 Burrard St., Suite 1050, |

|

(604) 449-3361 |

|

|

Registered Agent Solutions, Inc. _________________ Copy to: |

|

Preliminary Offering Circular

September 23, 2020

Subject to Completion

An Offering Statement pursuant to Regulation A relating to these securities has been filed with the United States Securities and Exchange Commission (the "SEC" or the "Commission"). Information contained in this Preliminary Offering Circular is subject to completion or amendment. These securities may not be sold nor may offers to buy be accepted before the Offering Statement filed with the Commission is qualified. This Preliminary Offering Circular shall not constitute an offer to sell or the solicitation of an offer to buy nor may there be any sales of these securities in any state in which such offer, solicitation or sale would be unlawful before registration or qualification under the laws of any such state. We may elect to satisfy our obligation to deliver a Final Offering Circular by sending you a notice within two business days after the completion of our sale to you that contains the URL where the Offering Circular was filed.

Up to 67,500,000 units

consisting of

shares of common stock

warrants

shares of common stock issuable upon exercise of warrants

This offering circular (the "Offering Circular") relates to the public offering in the United States of 67,500,000 units (the "Units") of Contact Gold Corp. (collectively, as the context requires, with its subsidiaries, "Contact Gold," the "Company," "we," "our," or "us") at a public offering price of $0.20 per Unit (the "Unit Offering Price"), in a "Tier 2 Offering" under Regulation A of the Securities Act of 1933, as amended (the "Offering"). The number of Units to be sold in this Offering is 67,500,000 for aggregate gross proceeds of $13,500,000, excluding the Over-Allotment Option (as defined herein). Unless otherwise noted herein, references to "$" are to Canadian dollars and references to "US$" are to United States dollars. This Offering is being made in Canadian dollars and you must tender the purchase price for Units in Canadian dollars.

Each Unit will consist of one share of common stock of the Company, par value US$0.001 per share (the "Common Stock" or "Shares" or "Contact Shares" and as part of the Unit, "a "Unit Share") and a purchase warrant to purchase one-half of one share of Common Stock (each whole share of Common Stock purchase warrant, a "Warrant"). Each Warrant will entitle the holder thereof to acquire, subject to adjustment in certain circumstances, one share of Common Stock (a "Warrant Share") at an exercise price of $0.27, on or before 4:30 p.m. (Vancouver time) on the date that is 24 months from the Closing Date (as defined herein). The Units will automatically separate into Unit Shares and Warrants at closing.

This Offering is being conducted by Cormark Securities Inc. (the "Lead Underwriter") together with its U.S. affiliate, Cormark Securities (USA) Limited, a registered broker-dealer and a member of the Financial Industry Regulatory Authority, Inc. ("FINRA") (each, an "Underwriter" and together with the Lead Underwriter, the "Underwriters"). The Lead Underwriter is not a U.S. registered broker-dealer or a member of FINRA and accordingly, will not, directly nor indirectly, solicit offers to purchase the Units in the United States. The Underwriters and other broker-dealers will receive compensation for sales of the securities offered hereby at a fixed commission rate consisting of: (i) a cash fee of 6% of the gross proceeds of the Offering (the "Cash Fee") and (ii) compensation warrants ("Broker Warrants"), exercisable at a price of $0.27 for a period of 24 months from the Closing Date to acquire the number of Contact Shares ("Broker Warrant Shares") equal to 6% of the Units sold during the Offering (including with respect of any exercise of the Over-Allotment Option (as defined below)), except in respect of sales to certain purchasers, including certain current shareholders of Contact Gold mutually agreed to between Contact Gold and the Underwriters (the "President's List") where 50% of the Cash Fee will be paid and 50% of the Broker Warrants will be issued in respect of any Units sold to purchasers on the President's List. It is anticipated that approximately 5,902,500 Units will be sold to persons on the President's List. See "Underwriting" in this Offering Circular.

None of the Units offered are being sold by present security holders of Contact Gold. Throughout this Offering Circular we refer to the public offering in the United States as the public offering.

In connection with the filing and qualification of the Offering Statement of Contact Gold on Form 1-A (the "Offering Statement") of which this Offering Circular is a part with the Commission, we will file a final prospectus supplement to our Canadian short form base shelf prospectus dated October 24, 2018 (the "Canadian Prospectus") with the securities regulatory authorities in each of the provinces and territories of Canada, other than Québec (the "Canadian Jurisdictions"), for the purposes of qualifying the Offering in Canada.

We expect to commence the sale of the Units as of the date on which the Offering Statement of which this Offering Circular is a part is declared qualified by the SEC.

Each subscription order is anticipated to settle on the third business day ("T+3") following the subscriber's payment of the purchase price (corresponding to a subscription accepted by the Company). The purchase price must be tendered in Canadian dollars.

|

|

Price to |

Underwriting Commissions (2)(4) |

Broker Warrants(2)(4) |

Proceeds, Before Expenses, |

|

Per Unit |

$0.20 |

$0.012 |

0.06 |

$0.188 |

|

Total(4) |

$13,500,000 |

$810,000 |

4,050,000 |

$12,690,000 |

|

(1) The offering price was determined by arm's length negotiation between Contact Gold and the Underwriters with reference to, among other things, the prevailing market price of the Common Stock. |

|

(2) This table depicts broker-dealer commissions of: (i) 6% of the gross proceeds of the Offering (including in respect of any exercise of the Over-Allotment Option (as defined below)) as the Cash Fee, other than with respect to sales to certain purchasers, including certain current shareholders, including persons on the President's List, on which 50% of the Cash Fee will be paid; and (ii) Broker Warrants equal to 6% of the Units sold during the Offering (including with respect of any exercise of the Over-Allotment Option), other than with respect to sales to certain purchasers on the President's List, where 50% of the Cash Fee will be paid and 50% of the Broker Warrants will be issued in respect of any Units sold to such purchasers. Please refer to the section entitled "Underwriting" beginning on page 132 of this Offering Circular for additional information regarding total Underwriter compensation. In addition, we have agreed to reimburse the Underwriters for their reasonable out-of-pocket expenses. |

|

(3) Does not include estimated offering expenses including, without limitation, legal, accounting, auditing, escrow agent, transfer agent, other professional, printing, advertising, travel, marketing, blue-sky compliance and other expenses of this Offering. We estimate the total expenses of this Offering, excluding the Underwriters' commissions, will be approximately $581,000, which includes reimbursement of approximately $167,500 to the Underwriters, |

|

(4) Assumes that no sales are made to persons on the President's List and excluding any exercise of the Over-Allotment Option. It is anticipated that approximately 5,902,500 Units will be sold to persons on the President's List, which would reduce the Underwriters' Fee by $35,415 to $774,585 ($896,085 if the Over-Allotment Option (defined below) is exercised in full) and the Broker Warrants by 177,075 to 3,872,925 Broker Warrants (4,480,425 Broker Warrants if the Over-Allotment Option is exercised in full) and increase the Proceeds, Before Expenses, To Company by $35,415 to $12,725,415 ($14,628,915 if the Over-Allotment Option is exercised in full). |

Contact Gold has granted the Underwriters an over-allotment option of 15% (the "Over-Allotment Option"), exercisable in whole or in part, in the sole discretion of the Underwriters, for a period of 30 days from and including the closing of the Offering, to purchase up to an additional 10,125,000 Units (the "Additional Units") and/or up to an additional 10,125,000 Unit Shares (the "Additional Unit Shares") and/or up to an additional 5,062,500 Warrants (the "Additional Warrants") to cover over-allotments, if any, and for market stabilization purposes. The Additional Units will automatically separate into Additional Unit Shares and Additional Warrants at closing of the Over-Allotment Option. The Over-Allotment Option may be exercisable by the Underwriters: (i) to acquire Additional Units at the Offering Price; and/or (ii) to acquire Additional Unit Shares at a price of $0.195 per Additional Unit Share, and/or (iii) to acquire Additional Warrants at a price of $0.01 per Additional Warrant, so long as the aggregate number of Additional Unit Shares and Additional Warrants which may be issued under the Over-Allotment Option does not exceed 10,125,000 Additional Unit Shares and 5,062,500 Additional Warrants. If the Over-Allotment Option is exercised in full solely for Additional Units, the total price for the Additional Units to the public will be $2,025,000, the total Underwriting Commission for the Additional Units will be $121,500, and the net proceeds to the Company, will be $1,903,500.

If the Over-Allotment Option is exercised in full solely for Additional Units, the total aggregate price to the public will be $15,525,000, the total aggregate Underwriters' Fee will be $931,500, and the net proceeds to the Corporation, before deducting the estimated expenses of the Offering, will be $14,593,500. A purchaser who acquires securities issuable on the exercise of the Over-Allotment Option, forming part of the Underwriters' over-allocation position, acquires such securities under this Offering Circular regardless of whether the over-allocation position is ultimately filled through the exercise of the Over-Allotment Option or secondary market purchases. The foregoing assumes that no sales will be made to persons on the President's List. See "Underwriting" and the table below:

|

Underwriters' Position |

Number of |

Exercise Period |

Exercise Price |

|

Over-Allotment Option(1)(2) |

10,125,000 Additional Units |

Up to 30 days from and including the Closing Date |

$0.20 per Additional Unit |

|

|

10,125,000 Additional Shares |

Up to 30 days from and including the Closing Date |

$0.195 per Additional Share |

|

|

5,062,500 Additional Warrants |

Up to 30 days from and including the Closing Date |

$0.01 per Additional Warrant |

|

Broker Warrants(3) |

607,500 Broker Warrants(4) |

24 months from the Closing Date |

$0.27 per Broker Warrant |

|

|

|

|

|

|

(1) This Offering Circular qualifies the grant of the Over-Allotment Option and the distribution of the Additional Units, Additional Unit Shares and/or Additional Warrants, as applicable. |

|||

|

(2) All figures in the table above assume that no sales are being made to persons on the President's List. It is anticipated that approximately 5,902,500 Units will be sold to persons on the President's List, which would reduce the Broker Warrants by 177,075 to 3,872,925 Broker Warrants (4,480,425 Broker Warrants if the Over-Allotment Option is exercised in full). (3) This Offering Circular qualifies the issuance of the Broker Warrants and Broker Warrant Shares issuable upon the exercise of Broker Warrants, as applicable, including in connection with the exercise of the Over-Allotment Option. (4) Assumes the exercise of the Over-Allotment Option in full for Units. |

|||

| Description of Security | $13.5m Offering(1) |

| Units(2) | 67,500,000 |

| Additional Units/ Additional Shares/ Additional Warrants(3) |

10,125,000/ 10,125,000/ 5,062,500 |

| Warrants/Warrant Shares(4) | 33,750,000 |

| Additional Warrant Shares(5) | 5,062,500 |

| Broker Warrants(6) | 4,657,500 |

| Broker Warrant Shares(6) | 4,657,500 |

|

(1) Based on the Offering of 67,500,000 Units for gross proceeds of $13,500,000. |

|

(2) Each Unit consists of one Unit Share and one-half of one Warrant, which are qualified under this Offering Circular. (3) The Over-Allotment Option may be exercisable by the Underwriters: (i) to acquire Additional Units (each consisting of one Additional Unit Share and one-half of one Additional Warrant) at the Offering Price; and/or (ii) to acquire Additional Unit Shares at a price of $0.195 per Additional Unit Share, and/or (iii) to acquire Additional Warrants at a price of $0.01 per Additional Warrant, so long as the aggregate number of Additional Units does not exceed 15% of the number of Units issued in the Offering; the number of Additional Unit Shares does not exceed 15% of the number of Shares issued in the Offering; and/or the number of Additional Warrants does not exceed 15% of the number of Warrants issued in the Offering, as applicable. The Additional Units, Additional Unit Shares and Additional Warrants, as applicable, are qualified under this Offering Circular. (4) Each Warrant is exercisable to acquire one Warrant Share, which is qualified under this Offering Circular. (5) Each Additional Warrant is exercisable to acquire one Additional Warrant Share, which is qualified under this Offering Circular. (6) We will issue Broker Warrants equal to 6% (3% for President's List placements) of the Units (4,050,000) and Additional Units (607,500) sold in the Offering to the Underwriters. Each Broker Warrant is exerciseable to acquire one Broker Warrant Share. Assumes the exercise of the full Over-Allotment Option and no sales are made to persons on the President's List. It is anticipated that approximately 5,902,500 Units will be sold to persons on the President's List, which would reduce the Broker Warrants by 177,075 to 3,872,925 Broker Warrants (4,480,425 Broker Warrants if the Over-Allotment Option is exercised in full). The Broker Warrants and Broker Warrant Shares are qualified under this Offering Circular. |

In addition, Contact Gold and Waterton Nevada Splitter, LLC ("Waterton Nevada"), a limited liability company of which Waterton Precious Metals Fund II Cayman, LP ("Waterton") is the sole member, holds, directly or indirectly, approximately 32.16% of the issued and outstanding Common Stock and 100% of the issued preferred stock of Contact Gold ("Preferred Stock"), on August 6, 2020 entered into a binding letter agreement (the "Waterton Letter of Intent") pursuant to which the parties agreed that if a minimum of $10,000,000 is raised in this Offering: (a) Contact Gold would use a minimum of $5,000,000 of the proceeds of this Offering to redeem a portion of the Preferred Stock at the Redemption Amount (defined per share as Face Value of US$1.00 plus all accrued and unpaid cumulative dividends, approximately US$13.842 million as of September 22, 2020); (b) Waterton Nevada would purchase Common Stock at $0.195 per share (the estimated offering price of a Unit Share) in aggregate amount equal to the Redemption Amount for the remaining issued and outstanding Preferred Stock (the "Redemption Placement"), estimated to be US$10.085 million ($13.423 million) at September 22, 2020; and (c) Contact Gold would use the proceeds of the Redemption Placement to redeem all of the remaining issued and outstanding Preferred Stock. Under the terms of the Waterton Letter of Intent and assuming a $5,000,000 redemption, Contact Gold will issue approximately 68,836,411 Shares in the Redemption Placement and Waterton Nevada will beneficially own approximately 100,188,060 Shares or approximately 42.85% of Contact Gold's issued and outstanding Shares. See, "Description of Capital Stock - Preferred Stock" and "Waterton Letter of Intent." The Offering Statement of which this Offering Circular is a part does not qualify the distribution of the Common Stock issued under the Redemption Placement.

Contact Gold's Common Stock began trading on the TSX Venture Exchange ("TSXV") under the symbol "C" on June 15, 2017. Contact Gold's Common Stock began trading on the OTCQB Venture Market ("OTCQB") under the symbol "CGOL" on May 19, 2020. The closing price of the Common Stock on September 22, 2020 was $0.215 on the TSXV and US$0.1674 on the OTCQB. The TSXV has conditionally approved the listing of the Unit Shares, the Warrant Shares, and the Broker Shares.

Contact Gold has not made application to quote or list the Warrants, Additional Warrants, or Broker Warrants on any securities exchange. Accordingly, we do not anticipate that there will be a public market for the Warrants, Additional Warrants or Broker Warrants.

These securities are speculative and involve a high degree of risk. You should purchase Units only if you can afford the complete loss of your investment. See "Risk Factors" beginning on page 9, to read about the risks you should consider before buying Units.

We are an "emerging growth company" as that term is defined in Section 2(a)(19) of the Securities Act of 1933, as amended (the "Securities Act") and used in the Jumpstart Our Business Startups Act of 2012 (the "JOBS Act"), and as such, we have elected to take advantage of certain reduced public company reporting requirements for this Offering Circular and future filings. See "Risk Factors" and "Offering Circular Summary - Implications of Being an "Emerging Growth Company." This Offering Circular follows the disclosure format of Part I of Form S-1 pursuant to the general instructions of Part II(a)(1)(ii) of Form 1-A.

No sale may be made to you in this Offering if the aggregate purchase price you pay is more than 10% of the greater of your annual income or net worth. Different rules apply to accredited investors and non-natural persons. Before making any representation that your investment does not exceed applicable thresholds, we encourage you to review Rule 251(d)(2)(i)(C) of Regulation A. For general information on investing, we encourage you to refer to www.investor.gov.

An investment in the Units is subject to certain risks and should be made only by persons or entities able to bear the risk of and to withstand the total loss of their investment. Prospective investors should carefully consider and review the RISK FACTORS beginning on page 10.

THE COMMISSION, DOES NOT PASS UPON THE MERITS OF OR GIVE ITS APPROVAL TO ANY SECURITIES OFFERED OR THE TERMS OF THE OFFERING, NOR DOES IT PASS UPON THE ACCURACY OR COMPLETENESS OF ANY OFFERING CIRCULAR OR OTHER SOLICITATION MATERIALS. THESE SECURITIES ARE OFFERED PURSUANT TO AN EXEMPTION FROM REGISTRATION WITH THE COMMISSION; HOWEVER, THE COMMISSION HAS NOT MADE AN INDEPENDENT DETERMINATION THAT THE SECURITIES OFFERED ARE EXEMPT FROM REGISTRATION.

Cormark Securities (USA) Limited

The date of this Offering Circular is __________, 2020.

TABLE OF CONTENTS

Page

Page | i

Industry and Market Data and Forecasts

The market data and certain other statistical information used throughout this Offering Circular are based on independent industry publications, government publications and other published independent sources. Although we believe these third-party sources are reliable as of their respective dates, neither we nor the Underwriters have independently verified the accuracy or completeness of this information. Some data is also based on our good faith estimates. The market data used in this Offering Circular involves a number of assumptions and limitations, and you are cautioned not to give undue weight to such estimates. Certain data is also based on our good faith estimates, which are derived from management's knowledge of the industry and independent sources. The industry in which we operate is subject to a high degree of uncertainty and risk due to a variety of factors, which could cause results to differ materially from those expressed in the estimates made by the independent parties and by us. While we are not aware of any misstatements regarding any market, industry or similar data presented herein, such data involves risks and uncertainties and is subject to change based on various factors, including those discussed under the headings "Cautionary Statement Regarding Forward-Looking Statements" and "Risk Factors" in this Offering Circular.

The annual average exchange rates for Canadian dollars in terms of the United States dollar for each of the three years in the period ended December 31, 2019, as quoted by the Bank of Canada, were as follows:

| Year ended December 31 | ||||||||

| 2019 | 2018 | 2017 | ||||||

| $ | 1.3269 | $ | 1.2957 | $ | 1.2986 | |||

On September 22, 2020, the daily rate for United States dollars in terms of the Canadian dollar, as quoted by the Bank of Canada, was US$1.00 = $1.3310.

Financial Information

The financial statements of the Company are presented in Canadian dollars and such financial statements are prepared in accordance with United States generally accepted accounting principles ("U.S. GAAP"). Unless otherwise indicated, any other financial information included or incorporated by reference in this Offering Circular has been prepared in accordance with U.S. GAAP. Financial information filed on Contact Gold's System for Electronic Document Analysis and Retrieval ("SEDAR") profile and incorporated by reference in the Canadian Prospectus prior to the fiscal year ended December 31, 2019, has been prepared in accordance with International Financial Reporting Standards ("IFRS"). U.S. GAAP differs in certain material respects from IFRS. As a result, certain financial information included or incorporated by reference in this Offering Circular may not be comparable to financial information reported by the Company at www.sedar.com and incorporated by reference in the Canadian Prospectus. This Offering Circular does not include any explanation of the principal differences or any reconciliation between IFRS and U.S. GAAP.

Technical Information

Concurrent with the filing of the Offering Statement of which this Offering Circular is a part, we filed a short form preliminary prospectus supplement dated August 6, 2020, August 10, 2020, August 31, 2020 and September 22, 2020, and a short form final prospectus supplement dated September 23, 2020, to the Canadian short form base shelf prospectus dated October 24, 2018 with the securities regulatory authorities in the Canadian Jurisdictions for the purposes of qualifying the Offering in Canada.

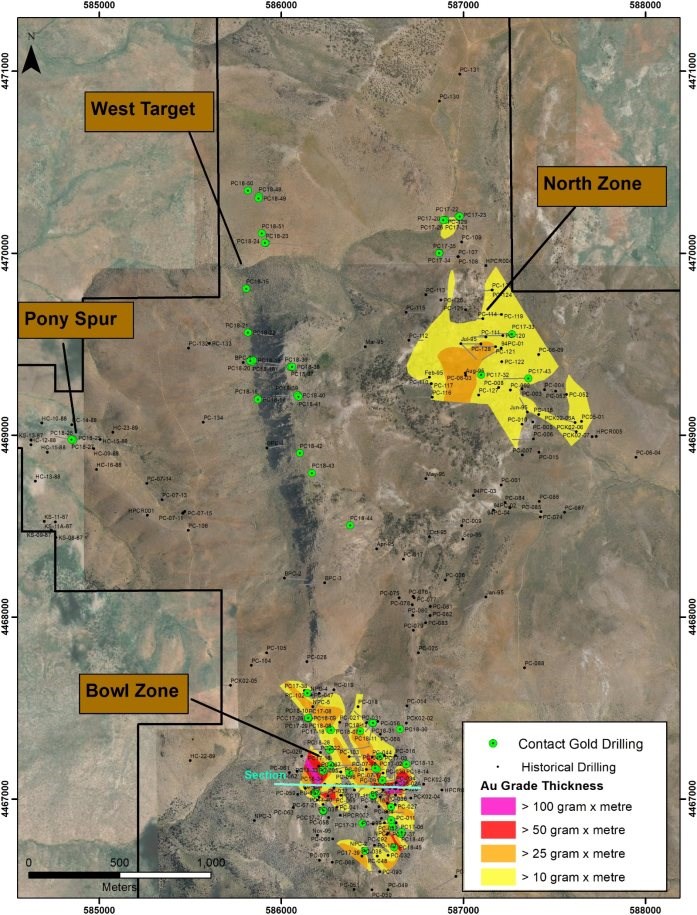

Pony Creek is an early stage exploration property and does not contain any mineral resources as defined by Canadian National Instrument 43-101-Standards of Disclosure for Mineral Projects ("NI 43-101"). There has been insufficient exploration to define a mineral resource estimate at the Pony Creek property ("Pony Creek" or the "Pony Creek Project"). Additional information about Pony Creek is contained in this Offering Circular and in the Pony Creek Technical Report (as defined below), and can be viewed under Contact Gold's issuer profile on SEDAR at www.sedar.com.

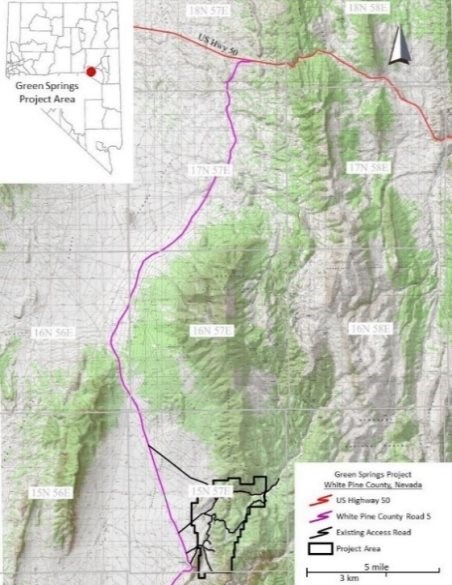

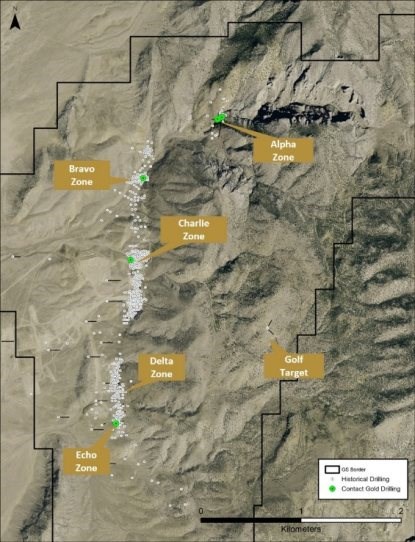

The Green Springs Project is a past operating heap leach gold mine which is an early-stage exploration project ("Green Springs" or the "Green Springs Project"). Additional information about Green Springs is contained in this Offering Circular and in the Green Springs Technical Report (as defined below), and can be viewed under Contact Gold's issuer profile on SEDAR at www.sedar.com.

There are no other recent estimates or data available to Contact Gold as at the date of this Offering Circular and a detailed exploration program is required to be conducted by Contact Gold in order to verify or treat any historical estimates contained in this Offering Circular as a current mineral resource.

Cautionary Note to U.S. Investors Regarding Reserve and Resource Estimates-The disclosure in this Offering Circular may use mineral resource classification terms that comply with reporting standards and securities laws in Canada, and mineral resource estimates that are made in accordance with NI 43-101, which differ from the requirements of United States securities laws.

The terms "mineral resource," "measured mineral resource," "indicated mineral resource" and "inferred mineral resource" are defined in and required to be disclosed by NI 43-101 and the Canadian Institute of Mining, Metallurgy and Petroleum (the "CIM") Definition Standards on Mineral Resources and Mineral Reserves, adopted by the CIM Council, as amended; however, these terms are not defined terms under SEC Industry Guide 7 under the U.S. Securities Act, as currently in effect and as set forth by the SEC ("SEC Industry Guide 7"), and are normally not permitted to be used in reports and registration statements filed with the SEC. The CIM Standards differ significantly from standards in SEC Industry Guide 7 and Subpart 1300 of Regulation S-K for mining disclosures ("SubPart 1300 Standards"). Investors are cautioned not to assume that all or any part of a mineral deposit in these categories will ever be converted into reserves. "Inferred mineral resources" have a great amount of uncertainty as to their existence, and great uncertainty as to their economic and legal feasibility. It cannot be assumed that all or any part of an inferred mineral resource will ever be upgraded to a higher category. Under Canadian securities laws and regulations, estimates of inferred mineral resources may not form the basis of feasibility or pre-feasibility studies, except in rare cases. Investors are cautioned not to assume that all or any part of an inferred mineral resource exists or is economically or legally mineable. Disclosure of "contained ounces" in a resource is permitted disclosure under Canadian regulations; however, the SEC normally only permits issuers to report mineralization that does not constitute "reserves" by SEC Industry Guide 7 standards as in place tonnage and grade without reference to unit measures. In addition, the terms "mineral reserve", "proven mineral reserve" and "probable mineral reserve" are Canadian mining terms as defined in accordance with NI 43-101 and the CIM Definition Standards on Mineral Resources and Mineral Reserves, adopted by the CIM Council, as amended. These definitions differ from the definitions in Industry Guide 7 and SubPart 1300. Under SEC Industry Guide 7 standards, as currently in effect, a "final" or "bankable" feasibility study is required to report reserves; the three-year historical average price, to the extent possible, is used in any reserve or cash flow analysis to designate reserves and the primary environmental analysis or report must be filed with the appropriate governmental authority. Consequently, information regarding mineralization contained in this Offering Circular is not comparable to similar information that would generally be disclosed by U.S. companies in accordance with the rules of the SEC, as currently in effect.

Pony Creek Technical Report Summary-The scientific and technical data about Pony Creek contained in this Offering Circular, is supported by and, has been reproduced from a technical report prepared in accordance with NI 43-101, entitled "NI 43-101 Technical Report, Pony Creek Gold Project, Elko County, Nevada, United States of America" dated October 22, 2018 (effective date: October 16, 2018) (the "Pony Creek Technical Report"). The Pony Creek Technical Report was prepared for Contact Gold, by Vance Spalding, C.P.G., Vice President of Exploration of Contact Gold, who is a "qualified person" under NI 43-101, and can be viewed under Contact Gold's issuer profile on SEDAR at www.sedar.com. The disclosure in this Offering Circular derived from the Pony Creek Technical Report has been prepared with the consent of Mr. Spalding.

Green Springs Technical Report Summary-The scientific and technical data about Green Springs contained in this Offering Circular, is supported by and, has been reproduced from a technical report prepared in accordance with NI 43-101, entitled Technical Report for the Green Spring Project, White Pine County Nevada, United States of America" dated effective June 12, 2020 (the "Green Springs Technical Report" and together with the Pony Creek Technical Report, the "Technical Reports"). The Green Springs Technical Report was prepared for Contact Gold, by John J. Read, C.P.G., who is a "qualified person" under NI 43-101 and can be viewed under Contact Gold's issuer profile on SEDAR at www.sedar.com. The disclosure in this Offering Circular derived from the Green Springs Technical Report has been prepared with the consent of Mr. Read.

The Technical Reports are subject to certain assumptions, qualifications and procedures described therein. Reference should be made to the full text of the Technical Reports, which has been filed with the applicable Canadian securities regulatory authorities pursuant to NI 43-101 and is available for review under Contact Gold's issuer profile on SEDAR at www.sedar.com. The Technical Reports are not and shall not be deemed to be incorporated by reference in this Offering Circular.

Additional Information

You should rely only on the information contained in this Offering Circular. Information filed on Contact Gold's SEDAR profile at www.sedar.com is available for informational purposes and does not constitute part of this Offering Circular. We have not authorized anyone to provide you with additional information or information different from that contained in this Offering Circular filed with the SEC. We take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. We are offering to sell, and seeking offers to buy, the Shares only in jurisdictions where offers and sales are permitted. The information contained in this Offering Circular is accurate only as of the date of this document, regardless of the time of delivery of this Offering Circular or any sale of the Units. Our business, financial condition, results of operations, and prospects may have changed since the date hereof.

OFFERING CIRCULAR SUMMARY

This summary highlights information contained elsewhere in this Offering Circular and does not contain all of the information that may be important to you. You should read this entire Offering Circular carefully, including the sections entitled "Risk Factors" and "Management's Discussion and Analysis of Financial Condition and Results of Operations" and our historical financial statements and related notes included elsewhere in this Offering Circular. In this Offering Circular, unless otherwise noted, the terms "the Company," "we," "us," and "our" refer to Contact Gold Corp. The information presented in this Offering Circular assumes (i) an public offering price of $0.20 per Unit and (ii) unless otherwise indicated, that the Underwriters do not exercise the Over-Allotment Option to purchase Additional Units, Additional Unit Shares or Additional Warrants.

Except for the statements of historical fact contained herein, the information presented in this Offering Circular constitutes "forward-looking statements" within the meaning of Canadian and United States securities and other laws, Often, but not always, forward-looking statements can be identified by the use of words such as "plans", "expects", "is expected", "budget", "scheduled", "estimates", "forecasts", "intends", "aims", "anticipates", "will", "projects", or "believes" or variations (including negative variations) of such words and phrases, or statements that certain actions, events, results or conditions "may", "could", "would", "might" or "will" be taken, occur or be achieved. By their very nature, forward-looking statements are subject to numerous risks and uncertainties, some of which are beyond the Company's control.

Forward looking statements are based on the opinions and estimates of management as of the date such statements are made and are based on various assumptions such as future business and property integrations remaining successful; the ability of the Company to continue to undertake exploration and other activities at its mineral properties during the Covid-19 coronavirus outbreak; the ability of the Company to manage Covid-19 cases at its mineral properties and maintain normal activity levels at its properties despite any such cases; that the other current or potential future effects of the Covid-19 pandemic on the Company's business, operations, and financial position, including restrictions on the movement of persons, restrictions on business activities, restrictions on the transport of goods, trade restrictions, increases in the cost of necessary inputs, reductions in the availability of necessary inputs and productivity and operational constraints, will not impact its planned exploration activities at its mineral properties; securities markets, spot and forward prices of gold, silver, base metals and certain other commodities, currency markets (such as the $ to US$ exchange rate); no materially adverse changes in national and local government, legislation, taxation, controls, regulations and political or economic developments; that various risks and hazards associated with the business of mineral exploration, development and mining (including environmental hazards, industrial accidents, unusual or unexpected formations, pressures, cave-ins and flooding) will not materialize; the ability to complete planned exploration programs; the ability to continue raising the necessary capital to finance operations; the ability to obtain adequate insurance to cover risks and hazards on favourable terms; that changes to laws and regulations will not impose greater or adverse restrictions on mineral exploration or mining activities; the continued stability of employee relations; relationships with local communities and indigenous populations; that costs associated with mining inputs and labour will not materially increase; that mineral exploration and development activities (including obtaining necessary licenses, permits and approvals from government authorities) will be successful; no disruptions due to a U.S. Government shutdown; the continued validity and ownership of title to properties; the completion and the nature of the transactions contemplated by the Waterton Letter of Intent; the satisfaction of the conditions to the completion of the transactions contemplated by the Waterton Letter of Intent, including the receipt in a timely manner of regulatory and other required approvals and clearances; and the anticipated use of proceeds of this Offering.

Although we believe that the expectations reflected in these forward-looking statements are based on reasonable assumptions, there are a number of risks and uncertainties that could cause actual results to differ materially from such forward-looking statements. These include, among others, the cautionary statements in the "Risk Factors" section and the "Management's Discussion and Analysis of Financial Condition and Results of Operations" section in this Offering Circular. See, "Cautionary Statement Regarding Forward-Looking Statements."

Business Overview

Contact Gold (formerly Winwell Ventures Inc., "Winwell") was incorporated under the Yukon Business Corporations Act on May 26, 2000 and was continued under the Business Corporations Act (British Columbia) on June 14, 2006. On June 7, 2017, upon closing of the Transactions (as defined herein), the Company completed a legal continuance into the State of Nevada (the "Continuance") and changed its name to "Contact Gold Corp." Contact Gold is domiciled in Canada and maintains a head office in Vancouver, British Columbia, Canada. Contact Gold's Common Stock began trading on the TSXV under the symbol "C" on June 15, 2017. Contact Gold's Common Stock began trading on the OTCQB under the symbol "CGOL" on May 19, 2020. Contact Gold's authorized share capital is 500,000,000 shares, par value US$0.001.

For further information about Contact Gold, see the section entitled "Business".

Organizational Structure

Contact Gold has two wholly-owned subsidiaries as set forth below:

(1) Clover Nevada II LLC ("Clover Nevada"), established under the laws of Nevada, is the only material subsidiary of Contact Gold and holds the Contact Properties.

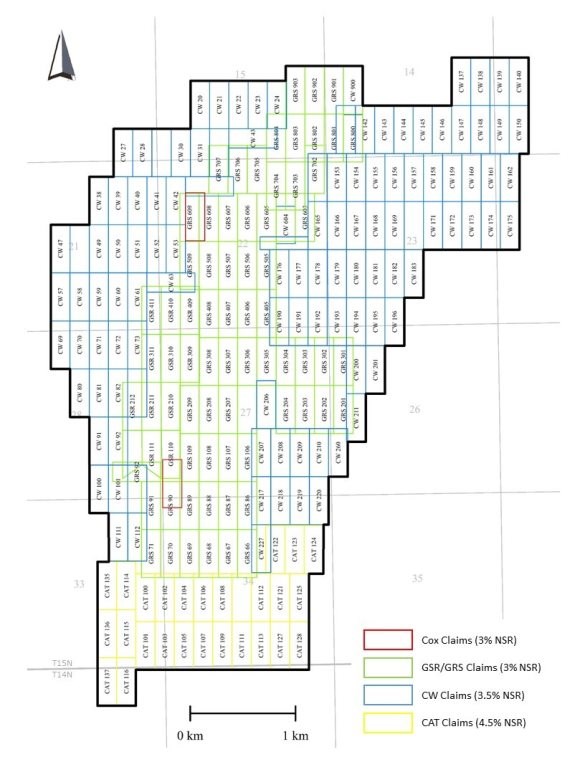

Mineral Properties

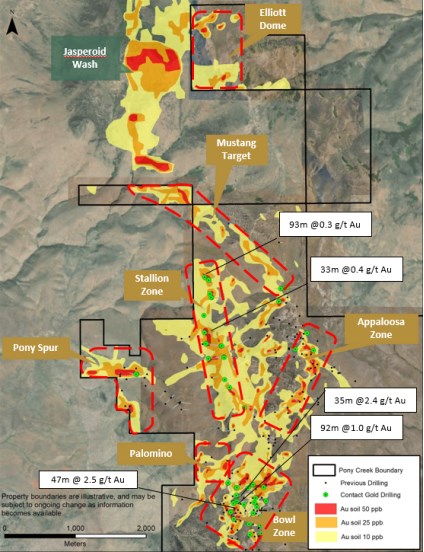

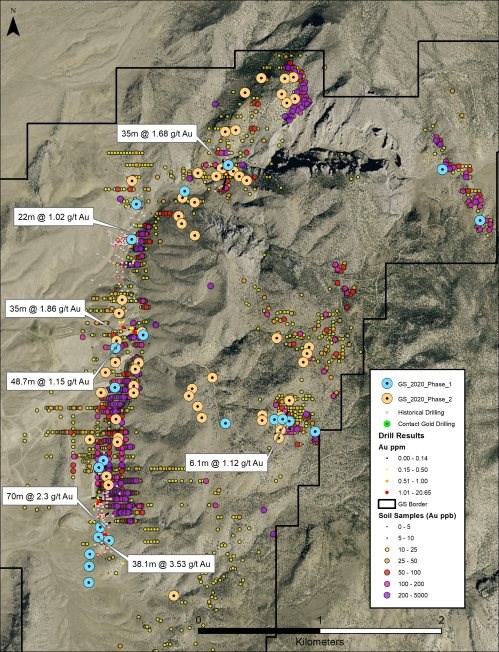

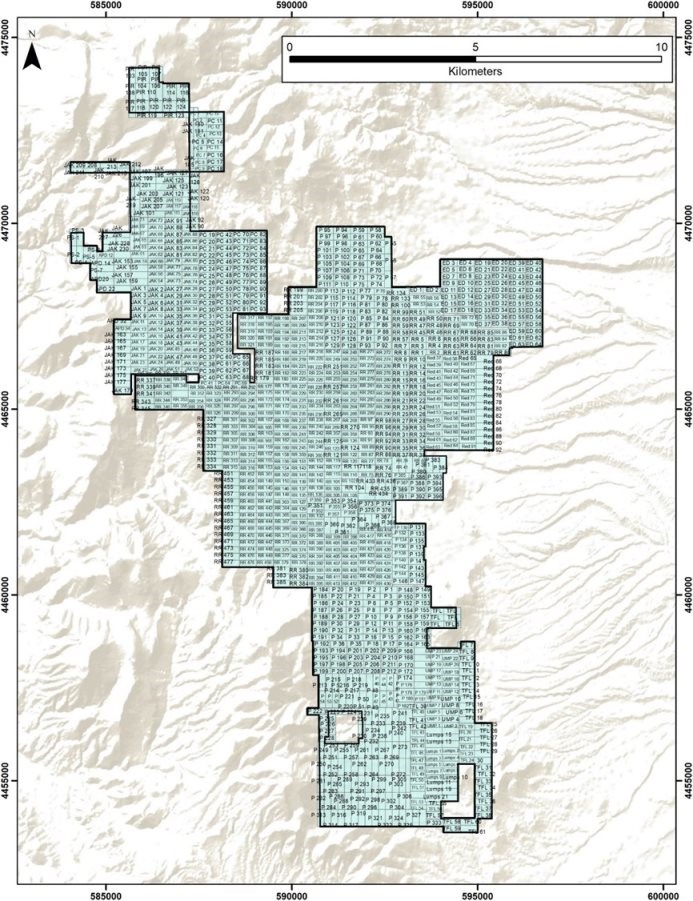

The Company's land holdings are on the Carlin, Independence, Cortez, and Northern Nevada Rift gold trends in Nevada. The Company's current properties include the Pony Creek, and the past-producing Green Springs Project, as well as a portfolio of prospective properties (together, the "Contact Properties"). As at the date hereof, the Contact Properties, including the Cobb Creek property, comprise in aggregate, approximately 140 km2 of unpatented mining claims and mineral tenure.

The Company is focused on advancing both the recently acquired Green Springs Project, and the Pony Creek Project.

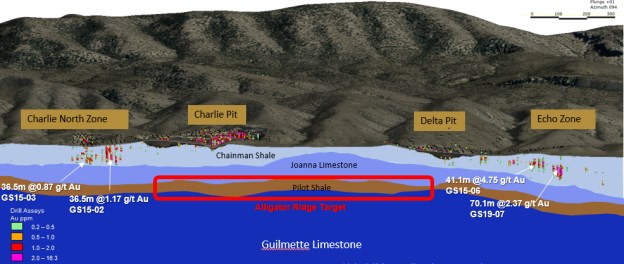

Green Springs Project

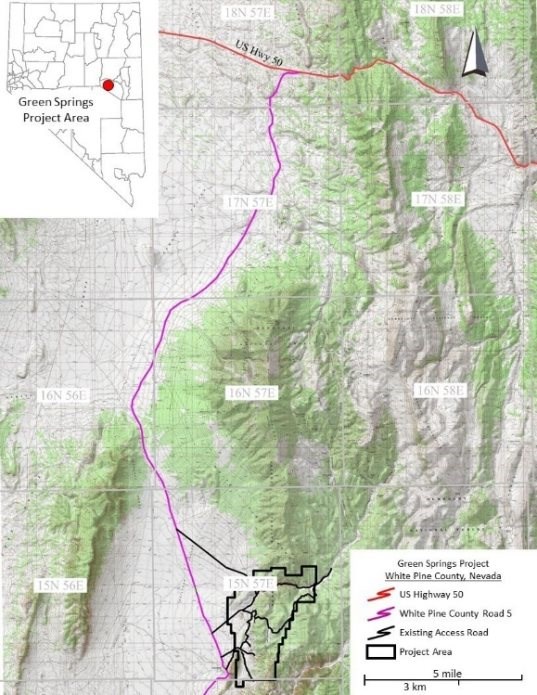

The Green Springs Project is located near the southern end of the Cortez Trend of Carlin-type gold deposits in White Pine County, Nevada approximately 360 km east of the capital city of Carson City and approximately 100 km southwest of the White Pine County seat at Ely, Nevada. The Green Springs Project comprises 220 unpatented mining claims covering approximately 16.4 km2 in parts of Sections 13-16, 21-24, 26-28, 33 & 34 of T 15 N, R 57 E and Sections 3 & 4 of T 14 N, R 57 E. The property boundaries are irregular but are situated within a rectangular area with UTM coordinates in Zone 11N, NAD27.

See under heading "Description of Mineral Property Interests" in this Offering Circular, for a discussion of the Green Springs Project.

Pony Creek Project

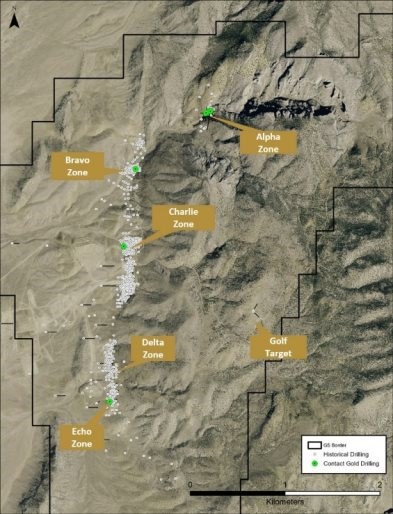

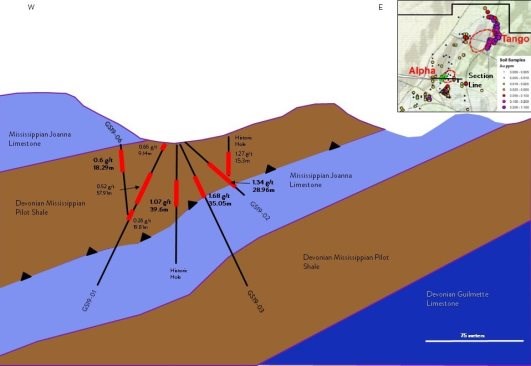

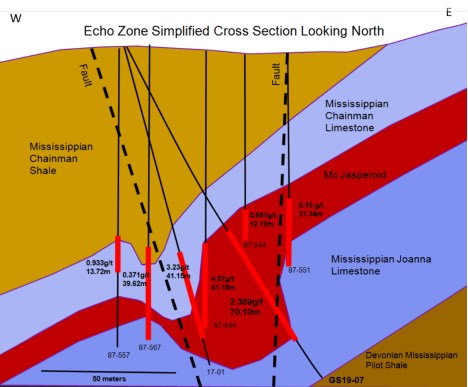

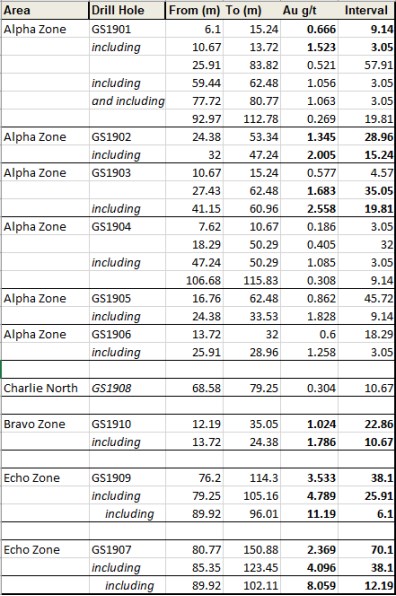

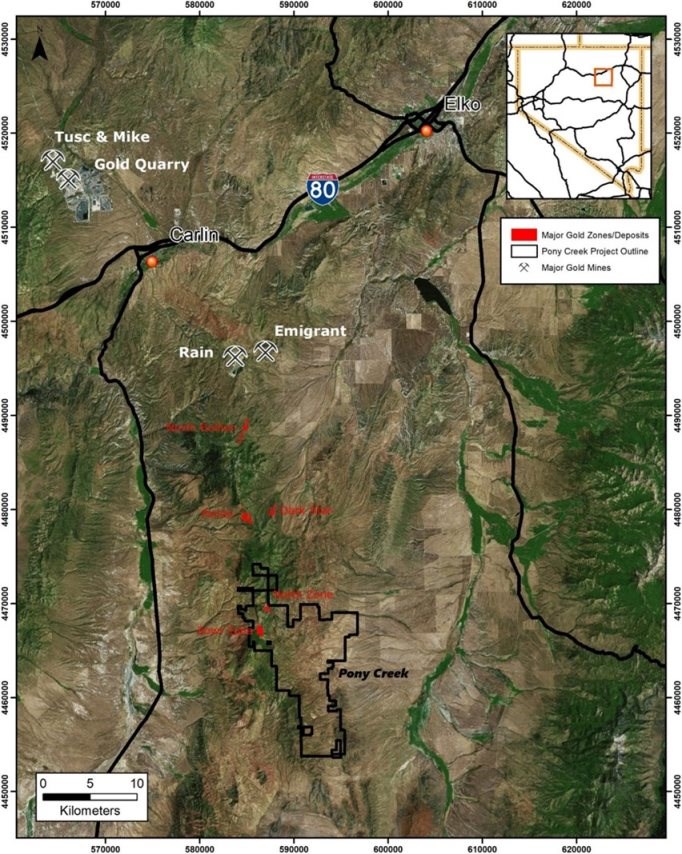

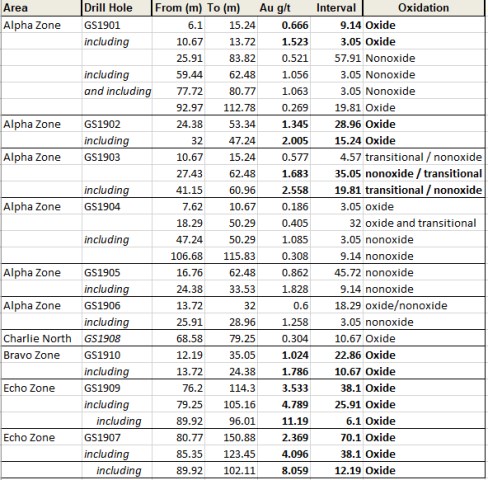

The Pony Creek Project is located in Elko County, Nevada and comprises 1,032 unpatented mining claims covering approximately 82 km2 in the southern part of the Piñon Range in Elko County, Nevada. The property is centered at approximately 40°21′10″N, 115°58′20″W, in the southern portion of the Carlin gold trend approximately 27 km south of the presently producing Emigrant gold mine operated by Nevada Gold Mines LLC ("NGM LLC") and 11 kilometers ("km") south of Gold Standard Ventures Corp.'s Pinion and Dark Star gold deposits (see Figure 1 in this Offering Circular under the heading "Description of Property"). From south to north, the claims occupy portions of T28N, R53E and R54E; T29N, R53E and R54E; and T30N, R53E, Mount Diablo Base and Meridian.

See under heading "Description of Mineral Property Interests" in this Offering Circular, for a discussion of the Pony Creek Project.

Implications of Being an "Emerging Growth Company"

As an issuer with less than US$1.07 billion in total annual gross revenues during our last fiscal year, we qualify as an "emerging growth company" under the JOBS Act. An emerging growth company may take advantage of certain reduced reporting requirements and is relieved of certain other significant requirements that are otherwise generally applicable to public companies. In particular, as an emerging growth company we:

• are not required to obtain an auditor attestation on our internal control over financial reporting pursuant to the Sarbanes- Oxley Act of 2002;

• are not required to provide a detailed narrative disclosure discussing our compensation principles, objectives and elements and analyzing how those elements fit with our principles and objectives (commonly referred to as "compensation discussion and analysis");

• are not required to obtain a non-binding advisory vote from our shareholders on executive compensation or golden parachute arrangements (commonly referred to as the "say-on-pay," "say-on-frequency" or "say-on-golden-parachute" votes);

• are exempt from certain executive compensation disclosure provisions requiring a pay-for-performance graph and CEO pay ratio disclosure;

• may present only two years of audited financial statements and only two years of related Management's Discussion & Analysis of Financial Condition and Results of Operations ("MD&A"); and

• are eligible to claim longer phase-in periods for the adoption of new or revised financial accounting standards under §107 of the JOBS Act.

We may take advantage of all of these reduced reporting requirements and exemptions, including the longer phase-in periods for the adoption of new or revised financial accounting standards under §107 of the JOBS Act. Our election to use the phase-in periods may make it difficult to compare our financial statements to those of non-emerging growth companies and other emerging growth companies that have opted out of the phase-in periods under §107 of the JOBS Act.

Certain of these reduced reporting requirements and exemptions are also available to us due to the fact that we may also qualify as a "smaller reporting company" under the SEC's rules. For instance, smaller reporting companies are not required to obtain an auditor attestation on our assessment of internal control over financial reporting; are not required to provide a compensation discussion and analysis; are not required to provide a pay-for-performance graph or CEO pay ratio disclosure; and may present only two years of audited financial statements and related MD&A disclosure.

THE OFFERING

|

Issuer: |

Contact Gold Corp. |

|

Issue: |

Units, comprised of one share of Common Stock and one-half Warrant. |

|

Offering Price: |

$0.20 |

|

Number of Units: |

67,500,000 |

|

Amount: |

$13,500,000 |

|

Common Stock outstanding after this Offering: |

164,974,914 Shares (1) (2)(3)(4) |

|

Over-allotment option |

Contact Gold has granted the Underwriters an option, exercisable at the Offering price for a period of 30 days from and including the closing of the Offering, to purchase up to 10,125,000 Additional Units, 10,125,000 Additional Unit Shares, and/or 5,062,500 Additional Warrants, as applicable, for market stabilization purposes and to cover over-allotments, if any. |

|

Waterton Letter of Intent: |

Pursuant to the Waterton Letter of Intent, if a minimum of $10,000,000 is raised in this Offering: (a) Contact Gold would use a minimum of $5,000,000 of the proceeds of this Offering to redeem a portion of the Preferred Stock at the Redemption Amount of $1.35 per share of Preferred Stock; (b) Waterton Nevada would purchase Common Stock at $0.195 per share (the estimated offering price of a Unit Share) to redeem the remaining issued and outstanding Preferred Stock at the Redemption Amount, estimated to be US$10.085 million ($13.423 million) at September 22, 2020 (the "Redemption Placement"); and (c) Contact Gold would use the proceeds of the Redemption Placement to redeem all of the remaining issued and outstanding Preferred Stock. Assuming at least $10,000,000 is raised in this Offering, Contact Gold would issue approximately 68,836,411 Shares in the Redemption Placement. See, "Description of Capital Stock - Preferred Stock" and "Waterton Letter of Intent." |

|

Use of Proceeds: (1) |

We expect to receive approximately $12,109,000 of net proceeds after deducting underwriting commissions and estimated Offering expenses payable by us. |

|

We currently intend to use up to $5,400,000 of the net proceeds from this Offering to fund exploration and development activities at the Green Springs Project, exploration and development activities at the Pony Creek Project, exploration at other projects held by Contact Gold, and for general working capital purposes. |

|

|

We currently intend to use $5,000,000 of the proceeds of this Offering to redeem a portion of the Preferred Stock at the Redemption Amount under the terms of the Waterton Letter of Intent. If the Over-Allotment Option is exercised in full, we would expect to receive approximately an additional $2,025,000 of net proceeds (assuming purchase of Additional Units), $1,903,500 after deducting underwriting discounts. We currently intend to use the proceeds from the exercise of Over-Allotment Option, if any, for general working capital purposes. See, "Use of Proceeds." |

|

|

Dividend Policy: |

Our ability to pay dividends depends on both our achievement of positive cash flow and the discretion of the board of directors of Contact Gold (the "Board") in declaring dividends. Other than Preferred Stock dividends, we do not intend to pay dividends at the current time (see "Description of Capital Stock - Preferred Stock"). |

|

President's List: |

The Underwriters have reserved for sale at the public offering price up to 10,000,000 of the Units being offered by this Offering Circular for sale to the President's List. We anticipate that approximately 5,902,500 Units will be sold to persons on the President's List, which will reduce the number of Units available to the general public. Please read "Underwriting." |

|

Listed and Trading: |

Contact Gold's Common Stock is listed on the TSXV under the symbol "C" and on the OTCQB under the symbols "CGOL". |

|

Transfer Agent and Registrar: |

Computershare Investor Services Inc. is our transfer agent and registrar with its principal office at 3rd Floor - 510 Burrard St. Vancouver, BC, Canada V6C 3B9. |

|

Risk Factors: |

You should carefully read and consider the information set forth under the heading "Risk Factors" and all other information set forth in this Offering Circular before deciding to invest in our Units. |

|

Tax Considerations: |

Please read "Material U.S. Federal Income Tax Considerations For U.S. Holders and Non-U.S. Holders." |

|

Underwriter's Commission: |

A Cash Fee equal to 6% of the gross proceeds of the Offering and Broker Warrants exercisable at a price of $0.27 for a period of 24 months from the Closing Date to acquire the number of Contact Shares equal to 6% of the Units sold during the Offering, excluding sales to President's List investors, which 50% of the Cash Fee will be paid and 50% of the Broker Warrants will be issued in respect of any Units sold to such President's List purchasers. |

|

No sale may be made to you in this Offering if the aggregate purchase price you pay is more than (i) 10% of the greater of your annual income or net worth (if you are a natural person) or (ii) 10% of the greater of your revenue or net assets (if you are not a natural person), unless you are an "accredited investor" (as defined in Rule 501(a) of Regulation D under the Securities Act). Before making any representation that your investment does not exceed applicable thresholds, we encourage you to review Rule 251(d)(2)(i)(C) of Regulation A. For general information on investing, we encourage you to refer to www.investor.gov. Each investor will be required to complete, execute and deliver a Subscription Agreement to purchase Units in this Offering, except accredited investors (satisfying one or more of the criteria set forth in Rule 501(a) of Regulation D under the Securities Act) that have a pre-existing relationship with the Underwriter (or a selling group member). See, "Underwriting." (1) As of September 22, 2020, does not include up to 8,420,000 Shares issuable upon exercise of stock options to purchase Shares ("Options") granted under the Contact Gold Omnibus Stock and Incentive Plan. The weighted average exercise price of Options awarded as September 22, 2020 is $0.33. Does not include 239,220 restricted share units ("RSUs") and 1,150,925 deferred share units ("DSUs") issued as of the date of this Offering Circular. Each RSU vests annually in thirds, vested RSUs are exercisable into Shares at the discretion of the holder prior to December 31, 2023. DSUs are held by directors and are exercisable upon cessation of his or her role as such. Does not include 12,360,000 Warrants, each of which is exercisable for one Share at a price of $0.15, subject to certain accelerated exercise provisions. There were 12,500,000 Warrants issued in three tranches and with expiry dates of April 23, 2022, May 5, 2022, and May 22, 2022. 140,000 of those Warrants were exercised on August 17, 2020. |

|

|

(2) Does not include Shares issuable upon conversion of the currently outstanding Contact Gold preferred stock ("Preferred Stock"). As of September 22, 2020, Contact Gold had 11,111,111 shares of Preferred Stock issued and outstanding, which Preferred Stock is convertible at the election of the holder at any time, into Shares (subject to a cap such that at any time following any conversion, Waterton Nevada and its affiliates shall not hold more than 49% of the aggregate issued and outstanding Common Stock). The number of Shares to be issued pursuant to such conversion right shall be equal to the sum of the face value of the Preferred Stock together with any accrued and unpaid cumulative dividends thereon to the conversion date divided by the conversion price of the Preferred Stock on the conversion date, such price being subject to adjustment from time to time. The conversion price of the Preferred Stock is $1.35 (approximately US$1.014 based on the Bank of Canada daily exchange rate on September 22, 2020), and if fully converted (based on an aggregate face value of US$13.842 million, including accrued and unpaid cumulative dividends) would convert into 13,646,740 Shares. The conversion of the Preferred Stock from time to time, at the election of the holder, will result in dilution to other existing holders of Common Stock. See, "Description of Capital Stock - Preferred Stock" and "Waterton Letter of Intent." |

|

|

|

(3) In connection with the Offering, Contact Gold is required to offer certain shareholders the right to acquire Units ("Purchase Rights") under the terms of the Waterton Governance and Investor Rights Agreement and Goldcorp Investor Rights Agreement (each as defined herein). See "Contractual Obligations" in the MD&A. The holders of Purchase Rights have elected not to participate in this Offering. (4) This figure excludes Shares sold pursuant to the Redemption Placement under the terms of the Waterton Letter of Intent, 68,836,411 Shares assuming a $5,000,000 redemption. (5) It is anticipated that approximately 5,902,500 Units will be sold to persons on the President's List, which would reduce the Underwriters' Fee by $35,415 to $774,585 ($896,085 if the Over-Allotment Option is exercised in full) and increase net proceeds, before expenses, to $11,423,415 ($13,448,415 if the Over-Allotment Option is exercised in full). |

RISK FACTORS

Investing in our Common Stock involves a high degree of risk. Prospective investors should carefully consider the risks described below, together with all of the other information included or referred to in this Offering Circular, before purchasing Units. The risks set out below are not the only risks we face. Additional risks and uncertainties not presently known to us or not presently deemed material by us might also impair our operations and performance. If any of these risks actually occurs, our business, financial condition or results of operations may be materially adversely affected. In such case, the trading price of our Common Stock, could decline and investors in our Common Stock could lose all or part of their investment.

Risks Related to our Company

Disruption caused by the Covid-19 Virus

In December 2019, a novel strain of coronavirus was reported to have surfaced in Wuhan, China, which has and is continuing to spread throughout China and other parts of the world, including Canada and the United States ("Covid-19). On January 30, 2020, the World Health Organization declared the outbreak of Covid-19 a "Public Health Emergency of International Concern." The outbreak of Covid-19 has resulted in a widespread health crisis that has adversely affected economies and financial markets worldwide. To date, the Covid-19 outbreak has not had a material impact on the Company's business. However, Contact Gold's business and development activities may be materially adversely affected by the continuing disruption caused by the Covid-19 outbreak, including as a result of supply chain delays and disruptions, governmental regulation and prevention measures, labour shortages and shutdowns. If there is an outbreak of Covid-19 cases at the Company's mineral properties or amongst the Company's employees or contractors, the Company may be required, or may voluntarily, close, curtail or otherwise limit its exploration and other business activities, which would impact the Company's business plans and timelines and could have an adverse impact on, among other things, the Company's relationship with suppliers, employees and contractors. Additionally, Covid-19 has disrupted the capital markets world-wide and commodity prices, including gold prices. Contact Gold may be unable to complete a capital raising transaction (including this Offering) if continued concerns relating to Covid-19 cause significant market disruptions, restrict travel, limit the ability to have meetings with potential investors or the market for the Common Stock does not stabilize in a timely manner. At this time, the Company cannot accurately predict the impact that Covid-19 may have on its exploration activities, business operations or financial results. The extent to which Covid-19 impacts the Company's business will depend on future developments, which are highly uncertain and cannot be predicted, including new information which may emerge concerning the severity of Covid-19 and the actions to contain Covid-19 or treat its impact, among others. If the disruptions posed by Covid-19 or other matters of global concern continue for an extensive period of time, the Company's business may be materially adversely affected. See "Risk Factors - Market Price of Securities" below.

No History of Operations

Contact Gold is an exploration company and has no history of operations, mining or refining mineral products. Contact Gold is subject to many risks common to such enterprises, including under-capitalization, cash shortages, limitations with respect to personnel, financial and other resources and lack of revenues. There is no assurance that Contact Gold will be successful in achieving a return on an investment for investors in the Common Stock and Contact Gold's likelihood of success must be considered in light of its early stage of operations.

There can be no assurance that the Contact Properties or any other property will be successfully placed into production, produce minerals in commercial quantities or otherwise generate operating earnings. Advancing projects from the exploration stage into development and commercial production requires significant capital and time and will be subject to the successful completion of further technical studies, permitting requirements and the construction of mines, processing plants, roads and related works and infrastructure. Contact Gold will continue to incur losses until mining-related operations successfully reach commercial production levels and generate sufficient revenue to fund continuing operations.

No Operating Revenues and History of Losses

Contact Gold has no operating revenues or earnings and a history of losses, and no operating revenues are anticipated until one of Contact Gold's projects comes into production, which may or may not occur. During each of the fiscal year ended December 31, 2019, and the six-month period ended June 30, 2020, the Company had negative cash flow from operating activities. As at December 31, 2019, the Company had working capital deficit of approximately $0.06 million (December 31, 2018 working capital of approximately $0.74 million) and as at June 30, 2020 had a working capital of approximately $0.26 million. As such, there is no certainty that Contact Gold will generate revenue from any source, operate profitably or provide a return on investment in the future. Contact Gold will continue to experience losses unless and until it can successfully develop and begin profitable commercial production at one of its mining properties. There can be no assurance that Contact Gold will be able to do so.

Additional Capital Requirements and Financing Risks

Contact Gold plans to focus on exploring for minerals and will use its working capital to carry out such exploration. Contact Gold has no source of operating cash flow and no assurance that acceptable additional funding will be available to it for the further exploration and development of its projects. The Company has incurred net losses in the past and may incur losses in the future and will continue to incur losses until and unless it can derive sufficient revenues from its mineral projects. These conditions, including other factors described herein, creates a material uncertainty regarding the Company's ability to continue as a going concern.

It is likely that the development and exploration of Contact Gold's Properties will require substantial additional financing. Further exploration and development of the Contact Properties and/or other properties acquired by Contact Gold may be dependent upon its ability to obtain acceptable financing through equity or debt, and there can be no assurance that it will be able to obtain adequate financing in the future or that the terms of such financing will be acceptable. Failure to obtain such additional financing could result in the delay or indefinite postponement of further exploration and development of Contact Gold's projects and Contact Gold may become unable to carry out its business objectives.

Reliance on a Limited Number of Properties

The only material property interest of Contact Gold is its interest in the Pony Creek Project located in Nevada. As a result, unless Contact Gold acquires additional property interests, any adverse developments affecting this property would have a material adverse effect upon Contact Gold and would materially and adversely affect the potential mineral resource production, profitability, financial performance and results of operations of Contact Gold. While Contact Gold may seek to acquire additional mineral properties in accordance with its business objectives, there can be no assurance that Contact Gold will be able to identify suitable additional mineral properties or, if it does identify suitable properties, that it will have sufficient financial resources to acquire such properties or that such properties will be available on terms acceptable to Contact Gold or at all and that Contact Gold will be able to successfully develop such properties and bring such properties into commercial production.

No History of Mineral Production

There is no history of mineral production on the Contact Properties. The Contact Properties are a high risk, speculative venture, and, until recently, only a minimal amount of exploration and sampling has been conducted by Contact Gold. There is no certainty that the expenditures proposed to be made by Contact Gold towards the search for and evaluation of gold or other minerals with regard to the Contact Properties or otherwise will result in discoveries of commercial quantities of gold or other minerals. Until recently, all of the drilling on the Contact Properties was completed by historical operators from 1981 through 2017.

Furthermore, there is no assurance that commercial quantities of minerals will be discovered at any properties acquired in the future by Contact Gold, nor is there any assurance that any future exploration programs of Contact Gold on the Contact Properties or any other properties will yield any positive results. Even where commercial quantities of minerals are discovered, there can be no assurance that any property of Contact Gold will ever be brought to a stage where mineral resources can be identified and mineral reserves can be profitably produced. Factors which may limit the ability of Contact Gold to produce mineral reserves from its properties include, but are not limited to, the price of mineral resources, the availability of additional capital and financing and the nature of any mineral deposits.

Early Stage Development Company

Contact Gold is a junior exploration company focused primarily on the acquisition, exploration and development of mineral properties located in Nevada. Contact Gold's properties have no established mineral reserves due to the early stage of exploration at this time. Any reference to potential quantities and/or grade is conceptual in nature, as there has been insufficient exploration to define any mineral resource and it is uncertain if further exploration will result in the determination of any mineral resource. Quantities and/or grade described in this Offering Circular should not be interpreted as assurances of a potential resource or reserve, or of potential future mine life or of the profitability of future operations.

The exploration and development of mineral deposits involves a high degree of financial risk over a significant period of time. Few properties that are explored are ultimately developed into producing mines and there is no assurance that any of Contact Gold's projects can be mined profitably. Substantial expenditures are required to establish mineral resources and reserves through drilling, to develop metallurgical processes to extract the metal from the ore and in the case of new properties, to develop the mining and processing facilities and infrastructure at any site chosen for mining. It is impossible to ensure that the current exploration and development programs of Contact Gold will result in profitable commercial mining operations. The profitability of Contact Gold's operations will be, in part, directly related to the cost and success of its exploration and development programs, which may be affected by a number of factors. Substantial expenditures are required to establish mineral resources and reserves that are sufficient to support commercial mining operations and to construct, complete and install mining and processing facilities on those properties that are actually developed.

No assurance can be given that any particular level of recovery of minerals will be realized or that any potential quantities and/or grade will ever qualify as a mineral resource or reserve, or that any such mineral resource or reserve will ever qualify as a commercially mineable (or viable) deposit which can be legally and economically exploited.

Where expenditures on a property have not led to the discovery of mineral resources or reserves, incurred expenditures will generally not be recoverable.

Exploration, Development and Operating Risks

Mining operations generally involve a high degree of risk. Contact Gold's operations are subject to all the hazards and risks normally encountered in the exploration, development and production of gold and other minerals, including unusual and unexpected geologic formations, seismic activity, rock bursts, cave-ins, flooding and other conditions involved in the drilling and removal of material, any of which could result in damage to, or destruction of, mines and other production facilities, damage to life or property, environmental damage and possible legal liability. The financing, exploration, development and mining of any of Contact Gold's properties is furthermore subject to a number of macroeconomic, legal and social factors, including commodity prices, laws and regulations, political conditions, currency fluctuations, the ability to hire and retain qualified people, the inability to obtain suitable and adequate machinery, equipment or labour and obtaining necessary services in the jurisdictions in which Contact Gold operates. Unfavourable changes to these and other factors have the potential to negatively affect Contact Gold's operations and business.

Major expenses may be required to locate and establish mineral reserves and resources, to develop metallurgical processes and to construct mining and processing facilities at a particular site. Mining, processing, development and exploration activities depend, to one degree or another, on adequate infrastructure. Reliable roads, bridges, power sources and water supply are important determinants, which affect capital and operating costs. Unusual or infrequent weather phenomena, sabotage, government or other interference in the maintenance or provision of such infrastructure could adversely affect Contact Gold's operations, financial condition and results of operations. It is impossible to ensure that the exploration or development programs planned by Contact Gold will result in a profitable commercial mining operation. Whether a gold or other precious or base metal or mineral deposit will be commercially viable depends on a number of factors, some of which are: the particular attributes of the deposit, such as the quantity and quality of mineralization and proximity to infrastructure; mineral prices, which are highly cyclical; and government regulations, including regulations relating to prices, taxes, royalties, land tenure, land use, importing and exporting minerals and environmental protection. The exact effect of these factors cannot be accurately predicted, but the combination of these factors may result in Contact Gold not receiving an adequate return on invested capital.

There is no certainty that the expenditures to be made by Contact Gold towards the exploration and evaluation of gold or other minerals will result in discoveries or production of commercial quantities of gold or other minerals. In addition, once in production, mineral reserves are finite and there can be no assurance that Contact Gold will be able to locate additional reserves as its existing reserves are depleted.

U.S. Domestic Issuer

Contact Gold is incorporated under the laws of Nevada and as such is deemed to be a "U.S. domestic issuer" (as defined in Rule 902(e) of Regulation S under the Securities Act) for U.S. securities laws purposes which creates several burdensome obligations.

Contact Gold is currently subject to continuing disclosure obligations with the SEC to submit annual reports on Form 1-K, semi-annual reports on Form 1-SA and current reports on Form 1-U. Our Common Stock will not be registered under Section 12 of the Securities Exchange Act of 1934, as amended (the "Exchange Act"), or subject to reporting obligations under Section 13 or Section 15(d) of the Exchange Act. Concurrent with the qualification of the Form 1-A, Contact Gold may voluntarily elect to register its class of Common Stock under Section 12(g) of the Exchange Act by filing a Form 8-A registration statement with the SEC. In the event that Contact Gold voluntarily elects to become registered and a reporting issuer with the SEC under the Exchange Act, Contact Gold will be subject to substantial continuous disclosure obligations including among other things, the filing of Form 10-Ks (annual reports), Form 10-Qs (quarterly reports), Form 8-Ks (current reports), Schedule 14A (proxy statements) and will be subject to applicable provisions under the Sarbanes-Oxley Act. In addition, directors, officers, and shareholders holding 10% or more of the issued and outstanding Common Stock will be subject to Section 16 reporting (Form 3, 4, and 5 filings) and the short-swing profit rules, and shareholders holding 5% or more of the issued and outstanding Common Stock will be subject to Schedule 13D/G beneficial ownership reporting obligations.

Contact Gold must prepare its financial statements in accordance with U.S. GAAP and the audit fees are typically higher due to the SEC compliance requirements. Further, Contact Gold is a Canadian reporting issuer and accordingly is also subject to the reporting and disclosure regime in Canada. All of the aforementioned requirements would significantly increase the regulatory and compliance costs of Contact Gold if Contact Gold were to become a U.S. reporting company. In addition, unless a U.S. domestic issuer is registered and reporting with the SEC, all securities issued by a U.S. domestic issuer in private placement transactions - including those that are issued outside of the United States - are "restricted securities" under Rule 144 under the Securities Act, must bear a U.S. restrictive legend and will be subject to a one (1) year hold period. The removal of the restrictive legend will also require a U.S. opinion letter to be delivered to the transfer agent. As a result, the ability for U.S. domestic issuers to raise capital is more difficult and would be expected to result in share issuances at higher discounts to the market price. Note that even if Contact Gold does become a reporting issuer under the Exchange Act or elects to submit its first and third quarter financial information on Form 1-U, all securities issued in a private placement transaction by a U.S. domestic issuer will still be subject to a six-month hold period.

Overall, the regulatory and compliance requirements and costs for U.S. domestic issuers is higher and more complex than those applicable to "foreign private issuers" and the ability to raise capital is more difficult, all of which could have a material adverse impact on Contact Gold's business and financial condition.

Land Title and Royalty Risks

General

There are uncertainties as to title matters in the mining industry. Any defects in title could cause Contact Gold to lose rights in its mineral properties and jeopardize its business operations. Contact Gold's mineral property interests currently consist of unpatented mining claims located on lands administered by the United States' Department of Interior's Bureau of Land Management (the "BLM"), Nevada State Office to which Contact Gold only has possessory title. Because title to unpatented mining claims is subject to inherent uncertainties, it is difficult to determine conclusively the ownership of such claims. These uncertainties relate to such things as sufficiency of mineral discovery, proper location and posting and marking of boundaries, proper and timely payment of annual BLM claim maintenance fees, the existence and terms of royalties, and possible conflicts with other claims not determinable from descriptions of record.

The present status of Contact Gold's unpatented mining claims located on public lands allows Contact Gold the right to mine and remove valuable minerals, such as precious and base metals, from the claims conditioned upon applicable environmental reviews and permitting programs. Contact Gold is also allowed to use the surface of the land solely for purposes related to mining and processing the mineral-bearing ores. However, legal ownership of the land remains with the United States. Contact Gold remains at risk that the mining claims may be forfeited either to the United States or to rival private claimants due to failure to comply with statutory requirements. Prior to 1993, a mining claim locator who was able to prove the discovery of valuable, locatable minerals on a mining claim, and to meet all other applicable federal and state requirements and procedures pertaining to the location and maintenance of federal unpatented mining claims, had the right to prosecute a patent application to secure fee title to the mining claim from the federal government. The right to pursue a patent, however, has been subject to a moratorium since October 1993, through federal legislation restricting the BLM from accepting any new mineral patent applications. If Contact Gold does not obtain fee title to its unpatented mining claims, there can be no assurance that it will be able to obtain compensation in connection with the forfeiture of such claims.

Pending Federal Legislation that may affect the Company's Operations

In recent years, members of the United States Congress have repeatedly introduced bills which would supplant or alter the provisions of the General Mining Act of 1872, a United States federal law that authorizes and governs prospecting and mining for economic minerals, such as gold, platinum, and silver, on federal public lands. Such bills have proposed, among other things, to either eliminate the right to a mineral patent, impose a federal royalty on production from unpatented mining claims, render certain federal lands unavailable for the location of unpatented mining claims, afford greater public involvement in the mine permitting process, provide for citizen suits, and impose new and stringent environmental operating standards and mined land reclamation requirements in addition to those already in effect. Such proposed legislation could change the cost of holding unpatented mining claims and could significantly impact Contact Gold's ability to develop mineralized material on unpatented mining claims. Currently, all of Contact Gold's mining claims are on unpatented claims. Although Contact Gold cannot predict what legislative changes might occur, the enactment of these proposed bills could adversely affect the potential for development of its mining claims, the economics of any mines that it brings into operation on federal unpatented mining claims, and as a result, adversely affect Contact Gold's financial performance.

Title to Mineral Property Interests may be Challenged

There may be challenges to title to the mineral properties in which Contact Gold holds a material interest. If there are title defects with respect to any properties, Contact Gold might be required to compensate other persons or to reduce its interest in the affected property. Furthermore, in any such case, the investigation and resolution of these issues would divert Contact Gold management's time from ongoing exploration and development programs. Title insurance generally is not available for mining claims in the U.S. and Contact Gold's ability to ensure that it has obtained secure claim to individual mineral properties may be limited. The Contact Properties may be subject to prior unregistered liens, agreements, transfers or claims, including native land claims and title may be affected by, among other things, undetected defects. In addition, Contact Gold may be unable to operate the properties as permitted or to enforce its rights with respect to its properties. The failure to comply with all applicable laws and regulations, including a failure to pay taxes or annual BLM claim maintenance fees may invalidate title to portions of the Contact Properties. Contact Gold may incur significant costs related to defending the title to its properties. A successful claim contesting title to a property may cause Contact Gold to compensate other persons, or to reduce its interest in the affected property or to lose our rights to explore and, if warranted, develop that property. This could result in Contact Gold not being compensated for its prior expenditures relating to the property. Also, in any such case, the investigation and resolution of title issues would divert management's time from ongoing exploration and, if warranted, development programs.

Mineral Properties may be Subject to Defects in Title

The ownership and validity or title of unpatented mining claims and concessions can at times be uncertain and may be contested. Contact Gold also may not have, or may not be able to obtain, all necessary surface rights to develop a property. Contact Gold has taken reasonable measures, in accordance with industry standards for properties at the same stage of exploration as that of Contact Gold, to ensure proper title to the Contact Properties. However, there is no guarantee that title to any of its properties will not be challenged or impugned.

Interpretation of Royalty Agreements; Unfulfilled Contractual Obligations

Royalty interests in Contact Properties, and any other royalty interests in respect of the properties of Contact Gold which may come into existence, may be subject to uncertainties and complexities arising from the application of contract and property laws in the jurisdictions where the mining projects are located. Operators and other parties to the agreements governing the royalty interests in Clover Nevada, or other royalty interests, may interpret their interests in a manner adverse to Contact Gold, and Contact Gold could be forced to take legal action to enforce its rights. Challenges to the terms of the royalty interests in Clover Nevada or the existence of other royalties could have a material adverse effect on the business, results of operations, cash flows and financial condition of Contact Gold. Disputes could arise with respect to, among other things:

• the existence or geographic extent of the royalty interests;

• the methods for calculating royalties;

• third party claims to the same royalty interest or to the property on which a royalty interest exists, or the existence of additional royalties on the same property;

• various rights of the operator or third parties in or to a royalty interest;

• production and other thresholds and caps applicable to payments of royalty interests;

• the obligation of an operator to make payments on royalty interests;

• various defects or ambiguities in the agreement governing a royalty interest; and

• disputes over the interpretation of buy-back rights.

Natural Resource Properties are Largely Contractual in Nature

Parties to contracts do not always honour contractual terms and contracts themselves may be subject to interpretation or technical defects. Accordingly, there may be instances where Contact Gold would be forced to take legal action to enforce its contractual rights. Such litigation may be time consuming and costly and there is no guarantee of success. Any pending proceedings or actions or any decisions determined adversely to Contact Gold, may have a material and adverse effect on Contact Gold's results of operations, financial condition and the trading price of the Common Stock.