EXHIBIT 99.1

Form 51-102F4

Business Acquisition Report

Item 1 Identity of Company

1.1 Name and Address of Company

Equinox Gold Corp. (“Equinox Gold”)

Suite 1501 – 700 West Pender St.

Vancouver, BC V6C 1G8

1.2 Executive Officer

For further information, please contact Susan Toews, General Counsel at 604-558-0560 ext 139.

Item 2 Details of Acquisition

2.1 Nature of Business Acquired

On March 10, 2020, Equinox Gold completed the previously announced acquisition of all of the issued and outstanding common shares (“Leagold Common Shares”) of Leagold Mining Corporation (“Leagold”), a company incorporated under the laws of British Columbia (the “Acquisition”), in accordance with a court approved plan of arrangement pursuant to the Business Corporations Act (British Columbia) (the “Arrangement”). Leagold is based in Vancouver, Canada and owns four operating gold mines in Mexico and Brazil, along with a near-term gold mine restart project in Brazil and an expansion project at the Los Filos mine complex in Mexico. Leagold was a reporting issuer in all of the provinces and territories of Canada and the Leagold Common Shares traded on the Toronto Stock Exchange under the trading symbol “LMC”.

The Arrangement was completed pursuant to the terms and conditions contained in an arrangement agreement dated December 15, 2019 between Equinox Gold and Leagold (the “Arrangement Agreement”). Pursuant to the terms of the Arrangement Agreement, Leagold became a wholly-owned subsidiary of Equinox Gold. The Arrangement was approved by Leagold’s shareholders and optionholders and by Equinox Gold’s shareholders on January 28, 2020 and by the British Columbia Supreme Court on January 30, 2020.

Further information on the Arrangement is available in the joint management information circular dated December 20, 2019 of Equinox Gold and Leagold (the “Circular”) which is available on SEDAR under Equinox Gold’s profile at www.sedar.com.

2.2 Acquisition Date

The acquisition date was March 10, 2020.

2.3 Consideration

In accordance with the terms and conditions of the Arrangement, Equinox Gold acquired beneficial ownership of 285,908,833 Leagold Common Shares, representing 100% ownership of Leagold on March 10, 2020 based on an exchange ratio of 0.331 of a common share of Equinox Gold (each, an “Equinox Gold Common Share”) for each Leagold Common Share held. Each Leagold warrant and option became exercisable for Equinox Gold Common Shares, as adjusted in accordance with the exchange ratio, and each Leagold performance share unit and deferred share unit was adjusted based on the exchange ratio.

Additionally, the Arrangement included the repayment of Leagold’s existing US$200 million term loan and US$200 million revolving credit facility (of which US$120 million was drawn as of March 10, 2020) and Equinox Gold’s US$130 million revolving credit facility (of which US$120 million was drawn as of March 10, 2020) (the “Existing Credit Facilities”).

The purchase cost of USD$764.1 million was funded from Equinox Gold’s existing cash balances and from proceeds from the following:

| (a) | a US$500 million refinancing of Existing Credit Facilities of Equinox Gold and Leagold from a syndicate of lenders, consisting of a $400 million revolving credit facility with a 48 month term and a $100 million amortizing loan with a 60 month term, |

| (b) | a private placement of Equinox Gold Common Shares, at a price of US$6.18 per Equinox Gold Common Share, for proceeds of US$40 million, and |

| (c) | a private placement of US$130 million in five-year convertible debentures bearing interest at 4.75% and convertible into Equinox Gold Common Shares at US$7.80 per Equinox Gold Common Share. |

2.4 Effect on Financial Position

The effect of the Acquisition on Equinox Gold’s financial position is outlined in the pro forma financial statements attached as Schedule “A”.

Except as described herein, Equinox Gold does not presently have plans or proposals for material changes in the business or affairs of Equinox Gold or of Leagold which may have a significant effect on the results of operations and financial position of Equinox Gold.

The information set out above is a summary only and is qualified in its entirety by the information contained in the Circular and the pro forma financial statements attached to this business acquisition report.

2.5 Prior Valuations

Not applicable.

2.6 Parties to Transaction

The Acquisition was not a transaction with an informed person, associate, or affiliate of Equinox Gold.

2.7 Date of Report

Report was completed on May 14, 2020.

Item 3 Financial Statements and Other Information

The following financial statements required by Part 8 of National Instrument 51-102 Continuous Disclosure Obligations are included in this report:

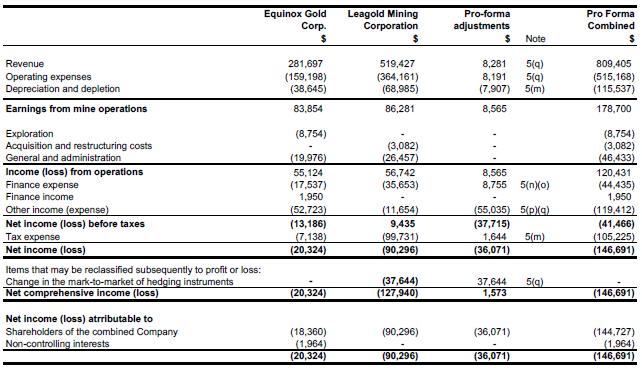

| · | Attached as Schedule “A” are the unaudited pro forma combined financial statements of Equinox Gold that give effect to the Acquisition, comprised of the unaudited pro forma combined statement of financial position as at December 31, 2019 and the unaudited pro forma combined statement of loss and comprehensive loss for the year ended December 31, 2019, together with the notes thereto. |

| · | Attached as Schedule “B” are the audited annual consolidated financial statements of Leagold for the years ended December 31, 2019 and 2018. |

Schedule “A”

Unaudited Pro Forma Combined

Financial Statements of Equinox Gold

![]()

PRO FORMA COMBINED FINANCIAL STATEMENTS

December 31, 2019

(Expressed in thousands of United States Dollars)

(Unaudited)

Pro Forma Combined Statement of Financial Position

As at December 31, 2019

(Expressed in thousands of United States dollars)

(Unaudited)

The accompanying notes form an integral part of these pro forma combined financial statements

Page | 2

Pro Forma Combined Statement of Financial Position

As at December 31, 2019

(Expressed in thousands of United States dollars)

(Unaudited)

The accompanying notes form an integral part of these pro forma combined financial statements

Page | 3

Pro Forma Combined Statement of Financial Position

As at December 31, 2019

(Expressed in thousands of United States dollars)

(Unaudited)

| 1. | Basis of Presentation |

These unaudited pro forma combined financial statements have been prepared in connection with the transaction between Equinox Gold Corp. (the “Company” or “Equinox Gold”) and Leagold Mining Corporation (“Leagold”), whereby Equinox Gold acquired all of the issued and outstanding common shares of Leagold (the “Transaction”). The Transaction closed on March 10, 2020.

These unaudited pro forma combined financial statements have been prepared from information derived from, and should be read in conjunction with, the consolidated financial statements of Equinox Gold as at and for the year ended December 31, 2019 and the consolidated financial statements of Leagold as at and for the year ended December 31, 2019. The historical financial statements of the Company and Leagold were prepared in accordance with International Financial Reporting Standards as issued by the International Accounting Standards Board (“IFRS”). These pro forma combined financial statements have been compiled from and include:

| (a) | An unaudited pro forma combined statement of financial position as at December 31, 2019 combining: |

| (i) | The consolidated statement of financial position of the Company as at December 31, 2019; |

| (ii) | The consolidated statement of financial position of Leagold as at December 31, 2019; and |

| (iii) | The adjustments described in note 5. |

| (b) | An unaudited pro forma combined statement of loss and comprehensive loss for the year ended December 31, 2019 combining: |

| (i) | The consolidated statement of loss and comprehensive loss of the Company for the year ended December 31, 2019; |

| (ii) | The consolidated statement of net (loss)/ income and comprehensive (loss)/ income of Leagold for the year ended December 31, 2019; and |

| (iii) | The adjustments described in note 5. |

The unaudited pro forma combined statement of financial position as at December 31, 2019 reflects the Transaction described in Note 3 as if it was completed on December 31, 2019. The unaudited pro forma combined statement of loss and comprehensive loss for the year ended December 31, 2019 has been prepared as if the Transaction described in Note 3 had occurred on January 1, 2019.

The unaudited pro forma combined financial statements are not intended to reflect the financial performance or the financial position of the Company which would have resulted had the Transaction been effected on the dates indicated. At the date of this Business Acquisition Report, the Company has not completed the detailed valuations necessary to conclude on the final fair value estimates of Leagold assets acquired and liabilities assumed; as a result, the final amounts recorded in relation to the Transaction will likely differ from those recorded in these unaudited pro forma combined financial statements and such differences could be material. Any potential synergies that may be realized, integration costs that may be incurred following the completion of the Transaction or other non-recurring changes have been excluded from the unaudited pro forma financial information. Further, the pro forma financial information is not necessarily indicative of the results of operations that may be obtained in the future.

Pro Forma Combined Statement of Financial Position

As at December 31, 2019

(Expressed in thousands of United States dollars)

(Unaudited)

| 2. | Significant Accounting Policies |

The accounting policies used in preparing these unaudited pro forma combined financial statements are set out in the Company’s audited consolidated financial statements for the year ended December 31, 2019. In preparing the unaudited pro forma combined financial statements a preliminary review was undertaken to identify any accounting policy differences between the accounting policies used by Leagold and those of the Company where the impact was potentially material and could be reasonably estimated. The significant accounting policies of Leagold conform, in all material respects, to those of the Company, with the exception of the derivative instruments and hedging policy included in Leagold’s consolidated financial statements for the period included herein. These unaudited pro forma combined financial statements are prepared on the basis that Equinox Gold discontinued the use of hedge accounting following the close of the Transaction as described in note 5(q). These unaudited pro forma combined financial statements also continue Leagold’s presentation of the Los Filos mine silver streaming arrangement with Wheaton Precious Metals (“WPM”) as an interest in the Los Filos Mine mineral interest held by WPM.

| 3. | Description of the Transaction |

Under the terms of the Transaction, Leagold shareholders received 0.331 of an Equinox Gold share for each Leagold share held (the "Exchange Ratio"). Outstanding Leagold options and warrants were converted into options and warrants to acquire the Company’s common shares (the “Replacement Warrants and Options”) based on the Exchange Ratio. In connection with the Transaction, Equinox Gold entered into the following financing arrangements:

| (i) | a private placement for gross proceeds of $40 million (the “Concurrent Private Placement”); |

| (ii) | a $500 million senior credit package with an interest rate of LIBOR plus 3.25% consisting of a $400 million revolving credit facility with a 48 month term and a $100 million amortizing loan with a 60 month term (the “Senior Credit Package”); and |

| (iii) | a $130 million convertible debenture, payable in 5 years, with a 4.75% fixed interest rate, which is convertible at a price of $7.80 per share (the “Convertible Debenture”). |

The funds raised from the financings have been utilized to repay Leagold’s existing $200 million term loan and $200 million revolving credit facility (of which $120 million was drawn as of December 31, 2019) and Equinox Gold’s $130 million revolving credit facility (of which $120 million was drawn as of December 31, 2019) (together the “Existing Credit Facilities”).

Prior to the Transaction, Leagold’s common shares were listed on the Toronto Stock Exchange. Following the completion of the Transaction, the shares were delisted and Leagold ceased to be a reporting issuer.

Pro Forma Combined Statement of Financial Position

As at December 31, 2019

(Expressed in thousands of United States dollars)

(Unaudited)

| 4. | Purchase Price Allocation |

The acquisition of the outstanding common shares of Leagold by the Company pursuant to the Transaction constitutes a business combination in accordance with IFRS 3 Business Combinations (“IFRS 3”), with Equinox Gold as the acquiror. Accordingly, the Company has applied the principles of IFRS 3 in the pro forma accounting for the acquisition of Leagold, which requires the Company to recognize Leagold’s identifiable assets acquired and liabilities assumed at fair value, recognize consideration transferred in the acquisition at fair value and recognize goodwill, if any, as the excess of consideration transferred over the net of the acquisition date fair value of identifiable assets acquired and liabilities assumed.

As of the date of this Business Acquisition Report, Equinox Gold has not completed the detailed valuation study necessary to arrive at the required final estimates of the fair value of the Leagold’s assets to be acquired and liabilities to be assumed. As a result, the pro forma adjustments are preliminary and are subject to change as additional analysis is performed. The preliminary pro forma adjustments have been made solely for the purpose of providing the unaudited pro forma financial information. Equinox Gold has estimated the fair value of Leagold’s assets and liabilities based on discussions with Leagold’s management, preliminary valuation information and due diligence. Any increases or decreases in the fair value of assets acquired and liabilities assumed upon completion of the final valuations will result in adjustments to the unaudited pro forma combined statement of financial position and unaudited pro forma combined statement of loss and comprehensive loss.

The final purchase price allocation may be materially different than that reflected in the pro forma purchase price allocation presented below. The purchase consideration and the preliminary fair values of assets acquired and liabilities assumed for the purposes of these unaudited pro forma combined financial statements is summarized in the tables below:

| Estimated Equinox Gold purchase consideration: | Note | $000s | |

| Shares | 5(d) | 732,042 | |

| Options(1) | 5(e) | 19,777 | |

| Warrants(1) | 5(f) | 8,543 | |

| DSUs(2) and PSUs(2) | 5(g) | 3,721 | |

| 764,083 |

Pro Forma Combined Statement of Financial Position

As at December 31, 2019

(Expressed in thousands of United States dollars)

(Unaudited)

| 4. | Purchase Price Allocation (continued) |

| Net Assets acquired: | $000s | ||

| Cash and cash equivalents | 78,320 | ||

| Accounts receivable, prepaid expenses and deposits | 44,400 | ||

| Inventory | 109,094 | ||

| Mineral properties, plant and equipment | 1,256,928 | ||

| Other non-current assets | 16,072 | ||

| Accounts payable & accrued liabilities | (101,401) | ||

| Reclamation obligations | (97,461) | ||

| Derivative liabilities | (48,345) | ||

| Other financial liabilities | (3,149) | ||

| Lease liabilities | (14,259) | ||

| Loans and borrowings | (320,000) | ||

| Other long-term liabilities | (13,577) | ||

| Deferred tax liability | (142,539) | ||

| 764,083 | |||

|

(1) Equinox Gold share options and warrants issued as part of the acquisition have been fair valued using the Black-Scholes valuation method and are fully vested at the close of the Transaction. For each outstanding Leagold share option and warrant existing immediately prior to the transaction, the number of share options and warrants and their respective exercise prices were adjusted to reflect the Exchange Ratio. The expiry date of each Leagold share option and warrant as it existed immediately prior to the transaction was used for the purpose of the Black-Scholes valuation calculation. (2) Equinox Gold DSUs and PSUs issued as part of the acquisition have been fair valued using the Leagold share price on March 9, 2020 and were adjusted to reflect the Exchange Ratio. The DSUs are fully vested at the close of the Transaction. |

|||

| 5. | Pro Forma Assumptions and Adjustments |

The unaudited pro forma combined financial statements reflect the following assumptions and adjustments to give effect to the business combination, as if the Transaction had occurred on December 31, 2019 for the pro forma combined statement of financial position and January 1, 2019 for the pro forma combined statement of loss and comprehensive loss. As of the date of this Business Acquisition Report, Equinox Gold is not aware of any additional reclassifications that would have a material impact on the unaudited pro forma financial information that are not reflected in the pro forma adjustments. Assumptions and adjustments made are as follows:

Pro forma combined statement of financial position adjustments to record:

| a) | The difference between the estimated fair value and carrying value of Leagold’s mineral properties, plant and equipment. The excess of the consideration paid over the estimated fair value of Leagold’s net assets has been allocated to mineral properties, plant and equipment for the purposes of these pro forma combined financial statements. |

Pro Forma Combined Statement of Financial Position

As at December 31, 2019

(Expressed in thousands of United States dollars)

(Unaudited)

| 5. | Pro Forma Assumptions and Adjustments (continued) |

| b) | The difference between the estimated fair value and carrying value of Leagold’s production inventory of $28.9 million and long-term debt of $9.8 million. |

| c) | The elimination of historical equity of Leagold. |

| d) | The issuance of 94,635,765 common shares to Leagold shareholders at a fair value of $7.74 (CAD$10.51) per share, based on the closing price of Equinox Gold common shares at March 9, 2020, the date immediately prior to closing date, and a CAD/USD exchange rate of 0.736. |

| e) | The issuance of 5,728,647 Equinox Gold options to Leagold option holders, for consideration of $19.8 million determined using the Black-Scholes valuation method at the closing date. |

| f) | The issuance of 16,786,949 Equinox Gold warrants to Leagold warrant holders, for consideration of $8.6 million determined using the Black-Scholes valuation method at the closing date. These warrants are considered a derivative and classified as a derivative liability as the exercise price of the warrants is expected to be fixed in Canadian dollars and therefore a variable amount of cash in the Company’s USD functional currency will be received on exercise. No adjustment has been made in the pro forma combined statement of loss and comprehensive loss for any differences in fair value arising from valuation assumptions between the warrants issued by Leagold and warrants issued by Equinox Gold. |

| g) | The issuance of 319,288 Equinox Gold DSUs and 369,919 Equinox Gold PSUs for consideration of $3.7 million to replace existing Leagold DSUs and PSUs at the closing date. |

| h) | The impact of the change in deferred tax liabilities recognized as a result of the increase in mineral properties, plant and equipment and the decrease in inventory as described in notes 5(a) and 5(b), respectively. |

| i) | The estimated additional cash transaction costs and change of control payments of $3.2 million incurred by the Company. |

| j) | The issuance of 6,472,000 common shares at a fair value of $6.18 (C$8.15) per share for net cash proceeds of $39.6 million in connection with the Concurrent Private Placement, net of estimated transaction costs of $0.4 million. |

| k) | The issuance of a Convertible Debenture with gross proceeds of $130.0 million, net of transaction costs of $2.6 million. The fair value of the debt portion of $119.1 million was estimated using a discounted cash flow model based on an expected term of 5 years and a fair value discount rate of 6.94%. The remaining proceeds of $10.9 million were allocated to equity. The transaction costs were allocated to debt and equity on a pro-rata basis. |

| l) | The net drawdown of the Senior Credit Package of $320.0 million, repayment of the Existing Credit Facilities totalling $440.0 million, a reversal of existing financing costs on Equinox Gold’s existing facility totalling $3.5 million and a net increase in deferred financing costs of $2.7 million recorded in other assets. |

Pro forma combined statement of loss and comprehensive loss adjustments to record:

| m) | Depreciation and the associated deferred tax recovery on the increase in the mineral properties, plant and equipment cost described in note 5(a). |

Pro Forma Combined Statement of Financial Position

As at December 31, 2019

(Expressed in thousands of United States dollars)

(Unaudited)

| 5. | Pro Forma Assumptions and Adjustments (continued) |

| n) | The interest and accretion on the Convertible Debenture of $6.5 million for the year ended December 31, 2019. |

| o) | The interest and accretion on the Senior Credit Package of $19.3 million for the year ended December 31, 2019 and the elimination of the interest and accretion on the Existing Credit Facilities of $34.6 million for the year ended December 31, 2019. |

| p) | The reversal of the gain on modification of Equinox Gold’s existing credit facility of $0.9 million recorded during the year ended December 31, 2019. |

| q) | The reclassification of the change in the fair value of Leagold’s gold price and currency derivatives into net loss from other comprehensive loss as the use of hedge accounting was discontinued following the close of the Transaction as described in note 2. |

| 6. | Pro Forma Share Capital |

Equinox Gold pro forma share capital as at December 31, 2019 has been determined as follows:

| Common | |||

| Shares (‘000’s) |

Amount | ||

| Issued and Outstanding, December 31, 2019 | 113,452 | $ 505,686 | |

| Shares consideration issued in connection with Leagold shares outstanding at December 31, 2019 (Note 4) | 94,636 | 732,042 | |

| Shares consideration issued in connection with the Concurrent Private Placement, net of transaction costs of $400 (Note 5(j)) | 6,472 | 39,600 | |

| Pro Forma Balance Issued and Outstanding | 214,560 | $ 1,277,328 |

| 7. | Pro Forma Loss and Comprehensive Loss per Share |

Pro forma basic loss and diluted loss per share for the year ended December 31, 2019 has been calculated based on actual weighted average number of Equinox Gold common shares outstanding for the respective period; as well as the number of shares issued in connection with the Transaction as if such shares had been outstanding since January 1, 2019:

| Year

Ended December 31, 2019 (‘000’s) |

|||

| Actual weighted average number of Equinox Gold common shares outstanding | 112,001 | ||

| Leagold weighted average number of shares outstanding | 94,299 | ||

| Number

of Equinox Gold common shares issued in relation to the Concurrent Private Placement (Note 5(j)) |

6,472 |

||

| Pro forma weighted average number of Equinox Gold common shares outstanding | 212,772 | ||

Pro forma net loss attributable to shareholders of the combined Company |

($144,727) |

||

| Pro forma net loss and diluted loss per share | ($0.68) | ||

Schedule “B”

Annual Consolidated

Financial Statements of Leagold

Consolidated Financial Statements

For the years ended December 31, 2019 and December 31, 2018

(expressed in thousands of United States dollars)

Independent Auditor’s Report

To the Board of Directors of Leagold Mining Corporation

Opinion

We have audited the consolidated financial statements of Leagold Mining Corporation (the “Company”), which comprise the consolidated statements of financial position as at December 31, 2019 and 2018, and the consolidated statements of net (loss)/ income and comprehensive (loss)/ income, changes in equity and cash flows for the years then ended, and notes to the consolidated financial statements, including a summary of significant accounting policies (collectively referred to as the “financial statements”).

In our opinion, the accompanying financial statements present fairly, in all material respects, the financial position of the Company as at December 31, 2019 and 2018, and its financial performance and its cash flows for the years then ended in accordance with International Financial Reporting Standards (“IFRS”).

Basis for Opinion

We conducted our audit in accordance with Canadian generally accepted auditing standards (“Canadian GAAS”). Our responsibilities under those standards are further described in the Auditor’s Responsibilities for the Audit of the Financial Statements section of our report. We are independent of the Company in accordance with the ethical requirements that are relevant to our audit of the financial statements in Canada, and we have fulfilled our other ethical responsibilities in accordance with these requirements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion.

Responsibilities of Management and Those Charged with Governance for the Financial Statements

Management is responsible for the preparation and fair presentation of the financial statements in accordance with IFRS, and for such internal control as management determines is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error.

In preparing the financial statements, management is responsible for assessing the Company’s ability to continue as a going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of accounting unless management either intends to liquidate the Company or to cease operations, or has no realistic alternative but to do so.

Those charged with governance are responsible for overseeing the Company’s financial reporting process.

Auditor’s Responsibilities for the Audit of the Financial Statements

Our objectives are to obtain reasonable assurance about whether the financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditor’s report that includes our opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with Canadian GAAS will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of these financial statements.

As part of an audit in accordance with Canadian GAAS, we exercise professional judgment and maintain professional skepticism throughout the audit. We also:

| · | Identify and assess the risks of material misstatement of the financial statements, whether due to fraud or error, design and perform audit procedures responsive to those risks, and obtain audit evidence that is sufficient and appropriate to provide a basis for our opinion. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control. |

| · | Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Company’s internal control. |

| · | Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and related disclosures made by management. |

| · | Conclude on the appropriateness of management’s use of the going concern basis of accounting and, based on the audit evidence obtained, whether a material uncertainty exists related to events or conditions that may cast significant doubt on the Company’s ability to continue as a going concern. If we conclude that a material uncertainty exists, we are required to draw attention in our auditor’s report to the related disclosures in the financial statements or, if such disclosures are inadequate, to modify our opinion. Our conclusions are based on the audit evidence obtained up to the date of our auditor’s report. However, future events or conditions may cause the Company to cease to continue as a going concern. |

| · | Evaluate the overall presentation, structure and content of the financial statements, including the disclosures, and whether the financial statements represent the underlying transactions and events in a manner that achieves fair presentation. |

| · | Obtain sufficient appropriate audit evidence regarding the financial information of the entities or business activities within the Company to express an opinion on the financial statements. We are responsible for the direction, supervision and performance of the group audit. We remain solely responsible for our audit opinion. |

We communicate with those charged with governance regarding, among other matters, the planned scope and timing of the audit and significant audit findings, including any significant deficiencies in internal control that we identify during our audit.

/s/ Deloitte LLP

Chartered Professional Accountants

Vancouver, British Columbia

May 8, 2020

Leagold Mining Corporation

Consolidated Statements of Financial Position

(expressed in thousands of United States dollars)

| As at December 31, 2019 | As at December 31, 2018 | |

| Assets | ||

| Cash | $ 78,320 | $ 53,021 |

| Trade and other receivables (Note 7) | 29,874 | 33,770 |

| Inventories (Note 8) | 137,438 | 111,794 |

| Prepaid expenses and other | 14,526 | 16,125 |

| 260,158 | 214,710 | |

| Mining interests (Note 9) | 809,308 | 772,759 |

| Long-term inventories (Note 8) | 525 | 1,506 |

| Deferred income tax assets (Note 21) | - | 86,681 |

| Other long-term receivables (Note 7) | 16,072 | 7,229 |

| Total assets | $ 1,086,063 | $ 1,082,885 |

| Liabilities | ||

| Trade and other payables (Note 10) | $ 101,401 | $ 101,121 |

| Deferred revenue (Note 18) | - | 23,382 |

| Reclamation and closure costs (Note 11) | 3,395 | 2,873 |

| Derivative financial instruments (Note 12) | 14,278 | 10,702 |

| Other current financial liabilities (Note 13) | 14,129 | - |

| Current portion of debt (Note 14) | - | 144,642 |

| Lease liabilities (Note 15) | 6,868 | - |

| $ 140,071 | 282,720 | |

| Reclamation and closure costs (Note 11) | 94,066 | 83,633 |

| Deferred income tax liabilities (Note 21) | 17,833 | 13,619 |

| Derivative financial instruments (Note 12) | 34,067 | - |

| Other long-term financial liabilities (Note 13) | 6,971 | 5,502 |

| Long term debt (Note 14) | 310,249 | 99,821 |

| Long-term lease liabilities (Note 15) | 7,391 | - |

| Other long-term liabilities (Note 16) | 13,577 | 13,551 |

| Total liabilities | $ 624,225 | $ 498,846 |

| Equity | ||

| Share capital (Note 17) | $ 578,880 | $ 578,351 |

| Reserves | 13,519 | 11,530 |

| Hedging reserves (Note 12) | (43,820) | (6,176) |

| Share purchase reserve (Note 17) | - | (3,221) |

| (Deficit)/retained earnings | (86,741) | 3,555 |

| Total equity | 461,838 | 584,039 |

| Total liabilities and equity | $ 1,086,063 | $ 1,082,885 |

The accompanying notes are an integral part of these consolidated financial statements

| 1 |

Leagold Mining Corporation

Consolidated Statements of Net (Loss)/Income and Comprehensive (Loss)/Income

(expressed in thousands of United States dollars, except per share and share information)

| Year ended December 31, | ||

| 2019 | 2018 | |

| Revenues (Note 18) | $ 519,427 | $ 376,511 |

| Cost of sales | ||

| Operating expenses (Note 19) | (358,141) | (267,178) |

| Depreciation and depletion (Note 9) | (68,985) | (46,862) |

| Royalties | (6,020) | (4,136) |

| Earnings from mine operations | 86,281 | 58,335 |

| Share-based payments (Note 17(b)) | (5,606) | (30) |

| Acquisition and restructuring costs (Notes 6, 28) | (3,082) | (8,038) |

| General and administration costs | (17,158) | (14,679) |

| Other expenses | (3,693) | (5,576) |

| Earnings from operations | 56,742 | 30,012 |

| Foreign exchange gain/ (loss) | 326 | (2,733) |

| Interest expense on loan facilities (Note 14) | (20,854) | (18,634) |

| Finance and accretion (expense)/income, net (Note 20) | (26,779) | 12,320 |

| Earnings before taxes | 9,434 | 20,965 |

| Current income and other tax expense (Note 21) | (8,836) | (7,797) |

| Deferred income (expense)/recovery (Note 21) | (90,895) | 2,117 |

| Net (loss)/income | (90,296) | 15,285 |

| Items that may be reclassified subsequently to profit or loss: | ||

| Change in fair value of hedging instruments (Note 12(a)) | (37,644) | (6,176) |

| Net comprehensive (loss)/income | $ (127,940) | $ 9,109 |

| Basic and diluted (loss)/earnings per share (Note 17(d)) | (0.32) | 0.07 |

| Basic and diluted earnings before taxes per share (Note 17(d)) | 0.03) | 0.09 |

| Weighted average common shares outstanding | ||

| Basic (Note 17(d)) | 284,890,609 | 232,127,862 |

| Diluted (Note 17(d)) | 284,890,609 | 232,363,478 |

The accompanying notes are an integral part of these consolidated financial statements

| 2 |

Leagold Mining Corporation

Consolidated Statements of Cash Flows

(expressed in thousands of United States dollars)

| Year ended December 31, | ||

| 2019 | 2018 | |

| Net (loss)/ income for the year | $ (90,296) | $ 15,285 |

| Adjust for: | ||

| Depreciation and depletion (Note 9) | 68,985 | 46,862 |

| Share-based payments (Note 17(b)) | 5,606 | 30 |

| Interest expense on loan facilities (Note 14) | 20,854 | 18,634 |

| Finance and accretion expense/ (income) (Note 20) | 26,779 | (12,320) |

| Current income and other tax expense (Note 21) | 8,836 | 7,797 |

| Deferred income tax expense/ (recovery) (Note 21) | 90,895 | (2,117) |

| Unrealized foreign exchange loss/(gain) | (1,555) | 2,081 |

| Inventory adjustments (Note 8) | 1,512 | 530 |

| Cash spent on reclamation (Note 23(b)) | (604) | (1,627) |

| Income taxes paid | (4,884) | (4,818) |

| Fair value adjustment on employment benefit liability | 1,212 | 58 |

| Other | 2,611 | 1,173 |

| Operating cash flows before working capital | $ 129,951 | $ 71,568 |

| Changes in working capital items: | ||

| Trade and other receivables | (1,961) | 2,774 |

| Deferred revenue (Note 18(b)) | (23,382) | 23,382 |

| Inventories | (27,131) | (28,271) |

| Prepaid expenses and other | (911) | 1,326 |

| Trade and other payables | (8,244) | (5,047) |

| Payment of acquisition-related payables assumed on Brio Acquisition (Note 6) | - | (18,105) |

| Cash provided by operating activities | $ 68,322 | $ 47,627 |

| Expenditures on mining interests (Note 23(a)) | (73,169) | (82,387) |

| Cash acquired through Brio Acquisition | - | 5,423 |

| Bridge loan issued on Brio Acquisition | - | (13,069) |

| Interest received | 321 | 399 |

| Cash used in investing activities | $ (72,848) | $ (89,634) |

| Private placement proceeds | - | 44,503 |

| Loan facility proceeds, net of issue costs (Note 14) | 309,347 | 97,546 |

| Repayment of loan facilities (Note 14) | (250,000) | (75,000) |

| Interest paid on loan facilities (Note 14) | (21,694) | (13,078) |

| Repayment of short-term loans | - | (14,501) |

| Payment of lease liabilities (Note 15(b)) | (8,313) | - |

| Cash received on sale of treasury shares (Note 17) | 2,206 | 405 |

| Proceeds from the exercise of stock options (Note 17(b)(i)) | 333 | 1,414 |

| Finance expense paid | (2,120) | - |

| Other | - | (194) |

| Cash provided by financing activities | $ 29,759 | $ 41,095 |

| Foreign exchange gain/ (loss) on cash | 66 | (106) |

| Increase/(decrease) in cash | $ 25,299 | $ (1,018) |

| Cash, beginning of year | 53,021 | 54,039 |

| Increase/(decrease) in cash | 25,299 | (1,018) |

| Cash, end of year | $ 78,320 | $ 53,021 |

The accompanying notes are an integral part of these consolidated financial statements

| 3 |

Leagold Mining Corporation

Consolidated Statements of Changes in Equity

(expressed in thousands of United States dollars, except share information)

| Share Capital | |||||||

| Common Shares | |||||||

| Number | Amount | Reserve | Hedging Reserves | Share Purchase Reserve | Deficit | Total | |

| Balance at December 31, 2017 | 151,316,959 | $ 268,777 | $ 11,312 | $ - | $ - | $ (11,730) | $ 268,359 |

| Share-based compensation (Note 17(b)) | - | - | 91 | - | - | - | 91 |

| Share issue costs (Notes 6, 17) | - | (497) | - | - | - | - | (497) |

| Shares issued pursuant to the Brio Acquisition (Note 6) | 110,876,166 | 264,052 | - | - | - | - | 264,052 |

| Share options granted during the Brio Acquisition (Note 6) | - | - | 930 | - | - | - | 930 |

| Shares issued pursuant to the private placement (Notes 6, 17) | 21,317,098 | 43,800 | - | - | - | - | 43,800 |

| Shares issued on exercise of stock options (Note 17(b)) | 1,232,152 | 2,217 | (803) | - | - | - | 1,414 |

| Warrants exercised (Note 17(b)) | 772 | 2 | - | - | - | - | 2 |

| Issuance of treasury shares (Note 17) | - | - | - | - | (3,626) | - | (3,626) |

| Sale of treasury shares (Note 17) | - | - | - | - | 405 | - | 405 |

| Change in fair value of hedging instruments (Note 12(c)) | - | - | - | (6,176) | - | - | (6,176) |

| Net income | - | - | - | - | - | 15,285 | 15,285 |

| Balance at December 31, 2018 | 284,743,147 | $ 578,351 | $ 11,530 | $ (6,176) | $ (3,221) | $ 3,555 | $ 584,039 |

| Share-based compensation (Note 17(b)) | - | - | 3,200 | - | - | - | 3,200 |

| Shares issued on exercise of stock options (Note 17(b)) | 220,437 | 529 | (196) | - | - | - | 333 |

| Sale of treasury shares (Note 17) | - | - | (1,015) | - | 3,221 | - | 2,206 |

| Change in fair value of hedging instruments (Note 12(c)) | - | - | - | (37,644) | - | (37,644) | |

| Net loss | - | - | - | - | - | (90,296) | (90,296) |

| Balance at December 31, 2019 | 284,963,584 | $ 578,880 | $ 13,519 | $ (43,820) | $ - | $ (86,741) | $ 461,838 |

The accompanying notes are an integral part of these consolidated financial statements

| 4 |

Leagold Mining Corporation

Notes to the Consolidated Financial Statements

For the years ended December 31, 2019 and 2018

(expressed in thousands of United States dollars, except as otherwise stated)

1. Nature and Continuance of Operations

Leagold Mining Corporation (Leagold) is a Canadian-based corporation and its common shares are listed on the Toronto Stock Exchange (symbol: LMC) and quoted in the United States on the OTCQX International (symbol: LMCNF). The address of the Company’s registered and records office is 2900 – 550 Burrard Street, Vancouver, British Columbia, V6C 0A3 and its executive office is 3043 - 595 Burrard Street, Vancouver, British Columbia, V7X 1J1.

Leagold is a Canadian based gold producer with four operating mines: the Los Filos mine complex in Mexico, and the RDM, Fazenda, and Pilar mines in Brazil, which were acquired from Brio Gold Inc. (Brio) on May 24, 2018. Leagold also has two near-term growth projects: the expansion of the Los Filos mine complex and the restart of the Santa Luz mine, which was also acquired on May 24, 2018. Leagold’s long-term growth strategy includes acquiring operating gold mines and projects nearing construction where the acquired assets complement its existing operations and provide further operational diversification.

On December 16, 2019, Leagold announced that it had entered into a definitive agreement with Equinox Gold Corp (Equinox Gold) to combine in an at-market merger, which results in Leagold shareholders receiving 0.331 of an Equinox Gold share for each Leagold share held (the Transaction). At closing, existing Equinox Gold and Leagold shareholders will own approximately 55% and 45% of the merged company, respectively, on an issued share basis.

As part of the Transaction, there will be a $40 million private placement subscription of Equinox Gold common shares; a new $130 million convertible debenture issued to Mubadala; a $400 million corporate revolving credit facility; and a $100 million term loan.

On January 28, 2020, both Leagold and Equinox Gold shareholders approved the Transaction.

The closing of the Transaction is subject to completion of regulatory approvals and other customary closing conditions.

| 2. | Basis of Preparation and Significant Accounting Policies |

a) Statement of compliance

These consolidated financial statements have been prepared in accordance with International Financial Reporting Standards (IFRS).

b) Basis of preparation

These consolidated financial statements have been prepared on the historical cost basis, except certain financial instruments that are measured at fair value at the end of each reporting period, as explained in the accounting policies below. The Company’s accounting policies have been applied consistently to all periods in the preparation of these consolidated financial statements.

c) Basis of consolidation

The accounts of the subsidiaries controlled by the Company are included in the consolidated financial statements from the date that control commenced until the date that control ceases. Control is achieved where the Company has the power to govern the financial and operating policies of an entity so as to obtain benefits from its activities. The subsidiaries of the Company and their geographic locations at December 31, 2019 are as follows:

| 5 |

Leagold Mining Corporation

Notes to the Consolidated Financial Statements

For the years ended December 31, 2019 and 2018

(expressed in thousands of United States dollars, except as otherwise stated)

| Direct parent company | Location | Ownership |

| Leagold (BC) Holding Corp. | Canada | 100% |

| Leagold (Barbados) Holdings Ltd. | Barbados | 100% |

| MXN Silver Corp. | Barbados | 100% |

| Leagold Netherlands B.V. | Netherlands | 100% |

| Leagold LatAM Holdings B.V. | Netherlands | 100% |

| Leagold RDM Holdings B.V. | Netherlands | 100% |

| Leagold Fazenda Holdings B.V. | Netherlands | 100% |

| Leagold Santa Luz Holdings B.V. | Netherlands | 100% |

| Leagold Pilar Holdings B.V. | Netherlands | 100% |

| Leagold Finance II B.V. | Netherlands | 100% |

| Leagold Mexico S.A.P.I. de C.V. | Mexico | 100% |

| Mina Leagold Los Filos, S.A.P.I. de C.V. | Mexico | 100% |

| Administración Los Filos, S.A.P.I. de C.V. | Mexico | 100% |

| Desarrollos Mineros San Luis S.A. de C.V. | Mexico | 100% |

| Exploradora de Yacimientos Los Filos S.A. de C.V. | Mexico | 100% |

| Minera Thesalia, S.A. de C.V. | Mexico | 100% |

| Mineracao Riacho Dos Machados Ltda | Brazil | 100% |

| Fazenda Brasileiro Desenvolvimento Mineral Ltda | Brazil | 100% |

| Santa Luz Desenvolvimento Mineral Ltda | Brazil | 100% |

| Pilar de Goias Desenvolvimento Mineral S/A | Brazil | 100% |

Intercompany balances, transactions, income and expenses arising from intercompany transactions are eliminated in full on consolidation.

d) Foreign currency translation

The presentation and functional currency of the Company is the US dollar. At each statement of financial position date, monetary assets and liabilities are translated using the period end foreign exchange rate. Non-monetary assets and liabilities in foreign currencies other than the functional currency are translated using the historical rate. All gains and losses on translation of these foreign currency transactions are included in the consolidated statements of net (loss)/income and comprehensive (loss)/income.

| e) | Derivative instruments and hedging |

On initial designation of a derivative as a hedge, the Company documents the relationship between the hedging instrument and hedged item and assesses the effectiveness of the hedging instrument in offsetting the changes in the cash flows attributable to the hedged risk and whether the forecast transaction is highly probable. Subsequent assessment will be performed on an ongoing basis to determine that the hedging instruments have been highly effective throughout the reporting periods for which they were designated. The changes in the fair value of derivatives that are designated and determined to be effective in offsetting forecasted cash flows is recognized in other comprehensive income/(loss) (OCI). The gain or loss relating to the ineffective portion is recognized immediately as a gain or loss on derivatives, net, in the consolidated statements of net (loss)/income and comprehensive (loss)/income.

| f) | Operating segments |

The Company’s senior management team performs planning, reviews operating results, assesses performance and makes resource allocation decisions based on the segment structure described in Note 22 at an operational level on a number of measures, which include mine operating earnings. Segment results that are reported to the Company's senior management team include items directly attributable to a segment as well as those that can be allocated on a reasonable basis.

| 6 |

Leagold Mining Corporation

Notes to the Consolidated Financial Statements

For the years ended December 31, 2019 and 2018

(expressed in thousands of United States dollars, except as otherwise stated)

| g) | Business combinations |

A business combination is defined as an acquisition of assets and liabilities that constitute a business. A business is an integrated set of activities and assets that is capable of being conducted and managed for the purpose of providing a return to the Company and its shareholders in the form of dividends, lower costs or other economic benefits. A business consists of inputs, including non-current assets, and processes, including operational processes, that when applied to those inputs, have the ability to create outputs that provide a return to the Company and its shareholders. A business also includes those assets and liabilities that do not necessarily have all the inputs and processes required to produce outputs, but can be integrated with the inputs and processes of the Company to create outputs. When acquiring a set of activities or assets in the exploration and development stage, which may not have outputs, the Company considers other factors to determine whether the set of activities or assets is a business.

The consideration transferred in a business combination is measured at fair value, which is calculated as the sum of the acquisition-date fair values of the assets transferred by the Company, the liabilities, including contingent consideration, incurred and payable by the Company to former owners of the acquiree and the equity interests issued by the Company. The measurement date for equity interests issued by the Company is the acquisition date, which is the date the Company obtains control over the acquiree, which is generally the date that consideration is transferred, and the Company acquires the assets and assumes the liabilities of the acquiree. The Company considers all relevant facts and circumstances in determining the acquisition date.

Acquisition-related costs, other than costs to issue debt or equity securities of the Company, are expensed as incurred. The costs to issue equity securities of the Company as consideration for the acquisition are reduced from share capital as share issue costs. The costs to issue debt to finance the acquisition are reduced from the value of the debt as debt issue costs.

It generally requires time to obtain the information necessary to complete the purchase price accounting following an acquisition. If the initial accounting for a business combination is incomplete by the end of the reporting period in which the combination occurs, the Company reports provisional amounts in its financial statements for the items for which the accounting is incomplete. During the measurement period, the Company will retrospectively adjust the provisional amounts recognized at the acquisition date to reflect new information obtained about facts and circumstances that existed as of the acquisition date and, if known, would have affected the measurement of the amounts recognized as of that date. During the measurement period, the Company will also recognize additional assets or liabilities if new information is obtained about facts and circumstances that existed as of the acquisition date and, if known, would have resulted in the recognition of those assets and liabilities as of that date. The measurement period ends as soon as the Company receives the information it was seeking about facts and circumstances that existed as of the acquisition date or learns that more information is not obtainable and shall not exceed one year from the acquisition date.

| h) | Cash |

Cash consists of cash on hand and cash balances held with banks. There were no cash equivalents at December 31, 2019 and 2018.

| i) | Inventories |

Finished goods, work-in-process, and stockpiled ore are valued at the lower of average operating expenses and net realizable value (NRV). Operating expenses include the cost of raw materials, direct labour, mine-site overhead expenses and depreciation and depletion of mining interests. Net realizable value is calculated as the estimated price at the time of sale based on prevailing metal prices less estimated future operating expenses to convert the inventories into saleable form.

Ore extracted from the mines is placed on the heap leach pads and subsequently processed into finished goods in the form of doré bars. Operating expenses are capitalized and included in work-in-process inventory based on the current mining costs incurred up to the point prior to the refining process, including applicable overhead, depreciation and depletion relating to mining interests, and removed at the average production cost per recoverable ounce of gold. Operating expenses associated with heap leach inventory which is being reprocessed are recognized in the period in which they are incurred as the costs relate directly to the current production. The average operating expenses of finished goods represent the average costs of work-in-process inventories and operating expenses of reprocessed heap leach incurred prior to the refining process, plus applicable refining costs and associated royalties. Ore on the heap leach pads is segregated between current and non-current inventories in the consolidated statement of financial position based on the period of planned usage.

| 7 |

Leagold Mining Corporation

Notes to the Consolidated Financial Statements

For the years ended December 31, 2019 and 2018

(expressed in thousands of United States dollars, except as otherwise stated)

Supplies are valued at the lower of average cost and net realizable value. Write-downs of supplies inventory are recognized in profit or loss

| j) | Mining interests |

Mining interests include interests in mining properties and related plant and equipment and are carried at cost less depreciation and depletion and any accumulated impairment.

Mineral deposits in the reserve category are classified as depletable mining properties when operating levels intended by management have been reached and are being mined. Prior to this, they are classified as non-depletable mining properties.

Resources not categorized as reserves and exploration potential are classified as non-depletable mining properties. The value associated with resources and exploration potential is often referred to as value beyond proven and probable reserves, which includes amounts assigned from costs of property acquisitions. At the end of each reporting period or when otherwise appropriate and subsequent to a review and evaluation for impairment, carrying amounts of non-depletable mining properties are reclassified to depletable mining properties as a result of the conversion into reserves that have reached operating levels intended by management.

| i. | Recognition |

Capitalized costs associated with mining properties include the following:

| · | Costs of direct acquisitions of production, development and exploration stage properties; |

| · | Costs attributed to mining properties acquired in connection with business combinations; |

| · | Expenditures related to the development of mining properties; |

| · | Expenditures related to economically recoverable exploration; |

| · | Estimates of reclamation and closure costs. |

Capitalization ceases when an asset is capable of operating in the manner intended by management.

| ii. | Acquisitions |

The cost of a property acquired as an individual asset purchase or as part of a business combination represents the property’s fair value at the date of acquisition. This cost is capitalized until the viability of the mining property is determined. When it is determined that a property is not economically viable, the amount capitalized is written off, which may include expenditures which were capitalized to the carrying amount of the property subsequent to its acquisition.

| iii. | Development expenditures |

Drilling and related costs incurred to define and delineate a mineral deposit that has not been classified as proven and probable reserves at a development stage or production stage mine are capitalized as part of the carrying amount of the related property in the period incurred, when management determines that there is sufficient evidence that the expenditure will result in a future economic benefit to the Company.

| 8 |

Leagold Mining Corporation

Notes to the Consolidated Financial Statements

For the years ended December 31, 2019 and 2018

(expressed in thousands of United States dollars, except as otherwise stated)

Drilling and related costs incurred on sites without an existing mine and on areas outside the boundary of a known mineral deposit which contains proven and probable reserves are exploration expenditures and are expensed as incurred to the date of establishing that costs incurred are economically recoverable. Further exploration expenditures, subsequent to the establishment of economic recoverability, are capitalized and included in the carrying amount of the related property.

Management uses the following criteria in its assessments of economic recoverability and probability of future economic benefit:

| · | Geology: there is sufficient geologic and economic certainty of converting a residual mineral deposit into a proven and probable reserve at a development stage or production stage mine, based on the known geology and metallurgy. There is history of conversion of resources to reserves at operating mines to support the likelihood of conversion. |

| · | Scoping: there is a scoping study or preliminary feasibility study that demonstrates the additional reserves and resources will generate a positive commercial outcome. Known metallurgy provides a basis for concluding there is a significant likelihood of being able to recoup the incremental costs of extraction and production. |

| · | Accessible facilities: the mineral deposit can be processed economically at accessible mining and processing facilities where applicable. |

| · | Life of mine plans: an overall life of mine plan and economic model to support the mine and the economic extraction of resources/reserves exists. A long-term life of mine plan, and supporting geological model identifies the drilling and related development work required to expand or further define the existing ore body. |

| · | Authorizations: operating permits and feasible environmental programs exist or are obtainable. |

| iv. | Costs incurred during production |

Mine development costs incurred to maintain current production are included in the consolidated statements of net (loss)/income and comprehensive (loss)/income. The distinction between mining expenditures incurred to develop new ore bodies and to develop mine areas in advance of current production is mainly the production timeframe of the mining area. For those areas being developed, which will be mined in future periods, the costs incurred are capitalized and depleted when the related mining area is mined, compared to current production areas where development costs are considered as costs of sales, given that the short-term nature of these expenditures matches the economic benefit of the ore being mined.

Capitalization of costs incurred ceases when an asset is capable of operating in the manner intended by management. Operating expenses incurred, and revenue earned subsequent to this point are recognized in profit or loss.

| v. | Capitalization of waste in open pit operations |

Capitalization of waste stripping requires the Company to make judgments and estimates in determining the amounts to be capitalized. In open pit mining operations, it is necessary to incur costs to remove overburden and other mine waste materials in order to access the ore body (stripping costs). During the development of a mine, stripping costs are capitalized and included in the carrying amount of the related mining property and subsequently depleted over the productive life of the mine using the unit-of-production method. During the production phase of a mine, stripping costs incurred to provide access to sources of reserves that will be produced in future periods that would not have otherwise been accessible are capitalized and included in the carrying amount of the related component of the mining property. Stripping costs incurred and capitalized during the production phase are depleted using the unit-of-production method over the reserves and a portion of resources that directly benefit from the specific stripping activity. Costs incurred for regular waste removal that do not give rise to future economic benefits are considered as costs of sales in the period incurred.

| 9 |

Leagold Mining Corporation

Notes to the Consolidated Financial Statements

For the years ended December 31, 2019 and 2018

(expressed in thousands of United States dollars, except as otherwise stated)

| vi. | Depletion |

The carrying amounts of mining properties are depleted using the unit-of-production method over the estimated recoverable ounces, when operating levels intended by management for the mining properties have been reached. Under this method, depletable costs are multiplied by the number of ounces extracted divided by the estimated total ounces to be extracted in current and future periods based on proven and probable reserves and a portion of resources.

Management reviews the estimated total recoverable ounces contained in depletable reserves and resources each financial year and when events and circumstances indicate that such a review should be made. Changes to estimated total recoverable ounces contained in depletable reserves and resources are accounted for prospectively.

| vii. | Plant and equipment |

Plant and equipment are recorded at cost less accumulated depreciation and impairment losses. Plant and equipment are depreciated using the units of production method based on ounces produced, or the straight-line method over the estimated useful lives of the related assets as follows:

| Plant | Units of production |

| Mobile equipment | 4 – 10 years |

| Computer equipment | 3 years |

| Furniture and equipment | 10 years |

Where parts (components) of an item of plant and equipment have different useful lives, they are accounted for as separate items of plant and equipment. Each asset’s estimated useful life is determined considering its physical life limitations. This physical life of each asset cannot exceed the life of the mine at which the asset is utilized. The estimated useful lives, residual values and depreciation method are reviewed at the end of each reporting period, with the effect of any changes in estimate accounted for on a prospective basis.

Amounts expended on assets under construction are capitalized until the asset becomes available for its intended use, at which time depreciation commences on the assets over its useful life. Repairs and maintenance of plant and equipment are expensed as incurred. Costs incurred to enhance the service potential of plant and equipment are capitalized and depreciated over the remaining useful life of the improved asset.

| viii. | Derecognition |

Upon disposal or abandonment, the carrying amounts of mining properties and plant and equipment and accumulated depreciation and depletion are removed from the accounts and any associated gains or losses are recorded in profit or loss.

| k) | Impairment of mining interests |

At each reporting date, the Company gives consideration whether any indicators of impairment exist. If any such indicators exist, the recoverable amount of the asset is estimated in order to determine the extent of any impairment loss, if any. When it is not possible to estimate the recoverable amount of an individual asset, the Company estimates the recoverable amount of the cash-generating unit to which the asset belongs.

Recoverable amount is the higher of fair value less costs of disposal and value in use. In assessing its recoverable amount, estimated future cash flows are discounted to their present value using a pre-tax discount rate that reflects current market assessments of the time value of money and the risks specific to the asset for which estimates of future cash flows have not been adjusted.

| 10 |

Leagold Mining Corporation

Notes to the Consolidated Financial Statements

For the years ended December 31, 2019 and 2018

(expressed in thousands of United States dollars, except as otherwise stated)

If the recoverable amount of an asset or cash-generating unit is estimated to be less than its carrying amount, the carrying amount of the asset or a cash-generating unit is reduced to its recoverable amount. An impairment loss is recognized immediately in profit or loss.

Impairment losses reverse in circumstances when indicators of the reversal of the impairment exist. When an impairment loss subsequently reverses, it is recognized immediately in profit or loss. The carrying amount of the asset or a cash-generating unit is increased to the revised estimate of its recoverable amount, but so that the increased carrying amount does not exceed the carrying amount that would have been determined had no impairment loss been recognized in prior years.

| l) | Provisions |

Provisions are recorded when a present legal or constructive obligation exists as a result of past events where it is probable that an outflow of resources embodying economic benefits will be required to settle the obligation, and a reliable estimate of the amount of the obligation can be made.

The amount recognized as a provision is the best estimate of the consideration required to settle the present obligation estimated at the end of each reporting period, taking into account the risks and uncertainties surrounding the obligation. Where a provision is measured using the cash flows estimated to settle the present obligation, its carrying amount is the present value of those cash flows. When some or all of the economic benefits required to settle a provision are expected to be recovered from a third party, the receivable is recognized as an asset if it is virtually certain that reimbursement will be received and the amount receivable can be measured reliably.

| m) | Income and deferred taxes |

The Company uses the liability method of accounting for income and mining taxes. Under the liability method, deferred tax assets and liabilities are recognized for the future tax consequences attributable to differences between the financial statement carrying amounts of existing assets and liabilities and their respective tax bases and for unused tax losses and other income tax deductions. Deferred tax assets are generally recognized for all deductible temporary differences to the extent that it is probable that taxable profits will be available against which those deductible temporary differences can be utilized. Such deferred tax assets and liabilities are not recognized if the temporary differences from the initial recognition (other than in a business combination) of assets and liabilities in a transaction that affects neither the taxable profit nor the accounting profit. In addition, deferred tax liabilities are not recognized if the temporary differences arise from the initial recognition of goodwill. Deferred tax assets and liabilities are measured using enacted or substantively enacted tax rates expected to apply if the related assets are realized or the liabilities are settled. To the extent that it is probable that taxable profit will not be available against which deductible temporary differences can be utilized a deferred tax asset may not be recognized. The effect on deferred tax assets and liabilities of a change in tax rates is recognized in earnings in the period in which the change is substantively enacted. Deferred tax assets and liabilities are considered monetary assets. Deferred tax balances denominated in other than US dollars are translated into US dollars using current exchange rates at the reporting date.

Current tax comprises the expected tax payable or receivable on the taxable income or loss for the year and any adjustment to the tax payable or receivable in respect of previous years. The amount of current tax payable or receivable is the best estimate of the tax amount expected to be paid or received that reflects uncertainty related to income taxes, if any. It is measured using tax rates enacted or substantially enacted at the reporting date.

Deferred tax assets and liabilities are offset when there is a legally enforceable right to set off current tax assets against current tax liabilities and when they relate to income taxes levied by the same taxation authority and the Company intends to settle its current tax assets and liabilities on a net basis.

| 11 |

Leagold Mining Corporation

Notes to the Consolidated Financial Statements

For the years ended December 31, 2019 and 2018

(expressed in thousands of United States dollars, except as otherwise stated)

| n) | Reclamation and closure costs |

The Company records a liability for the estimated future rehabilitation costs and decommissioning of its operating mines and development projects at the time the environmental disturbance occurs or a constructive obligation is determined. Environmental rehabilitation provisions are measured at the net present value of expected future cash flows. The unwinding of the obligation, referred to as accretion expense, is included in finance costs with a corresponding increase in the amount of the provision.

When provisions for closure and environmental rehabilitation are initially recognized, the corresponding cost is capitalized as an asset, representing part of the cost of acquiring the future economic benefits of the operation. The capitalized cost of closure and environmental rehabilitation activities is recognized in mining interests and depreciated over the expected useful life of the operation to which it relates.

Environmental rehabilitation provisions are updated annually for changes in legal or regulatory requirements, changes to the expected cash flows, and for the effect on changes in the discount rate, and the change in estimate is added or deducted from the related asset and depreciated over the expected useful life of the operation to which it relates.

Increases or decreases to the provision also arise due to changes in legal or regulatory requirements, the extent of environmental remediation required and cost estimates. The net present value of the estimated costs of these changes is recorded in the period which the change is identified and quantifiable.

| o) | Revenue recognition |

Revenue from the sale of gold in doré bar form is recognized when the Company has transferred control of the gold in doré bar form to the customer at an amount reflecting the consideration the Company expects to receive in exchange for those products. In determining whether the Company has satisfied a performance obligation, it considers the indicators of the transfer of control, which include, but are not limited to, whether: the Company has a present right to payment; the customer has legal title to the asset; the Company has transferred physical possession of the asset to the customer; and the customer has the significant risks and rewards of ownership of the asset. Revenue is gross of royalties paid to third parties.

| p) | Leases |

Subsequent to the adoption of IFRS 16, Leases (Note 3), the Company recognizes a right-of-use asset and lease liability at the lease commencement date. At this date, the right-of-use asset is measured at cost and included in mining interests. Cost includes the initial amount of the lease liability, adjusted for lease payments made before this date as well as any initial direct costs incurred. Cost also includes an estimate of costs to be incurred by the lessee in dismantling and removing the underlying asset and restoring the site on which it is located, less any lease incentives received.

The right-of-use asset is depreciated using the straight-line method from the lease commencement date to the earlier of the end of the lease term or the end of the useful life of the right-of-use asset. The estimated useful lives of right-of-use assets are determined in the same manner as those of plant and equipment. Right-of-use assets are adjusted for impairments and/or re-measurements of the lease liability.

At the lease commencement date, the lease liability is measured at the present value of the future lease payments. The lease payments are discounted using the interest rate implicit in the lease, or, if that rate cannot be readily determined, the Company’s incremental borrowing rate. Generally, the Company uses its incremental borrowing rate as the discount rate, which is the rate the Company would pay for similar assets, with similar security and value, at similar locations over a similar term.

| 12 |

Leagold Mining Corporation

Notes to the Consolidated Financial Statements

For the years ended December 31, 2019 and 2018

(expressed in thousands of United States dollars, except as otherwise stated)

| q) | Warrant derivative |

The Company uses a Black-Scholes model for valuation of the warrant derivative. The pricing models require the input of subjective assumptions including expected share price volatility, interest rate and forfeiture rate. Changes in the input assumptions can affect the fair value estimate and the Company’s net income/(loss) and warrant liability.

| r) | Financial instruments |

Financial assets and financial liabilities are recognized in the Company’s statement of financial position when the Company becomes a party to the contractual provisions of the instrument. On initial recognition, all financial assets and financial liabilities are recorded at fair value, net of attributable transaction costs, except for financial assets and liabilities classified as at fair value through profit or loss (FVTPL). The directly attributable transaction costs of financial assets and liabilities classified as at FVTPL are expensed in the period in which they are incurred. Subsequent measurement of financial assets and liabilities depends on the classification of such assets and liabilities.

| i. | Classification of financial assets |

Financial assets that meet the following conditions are measured subsequently at amortized cost:

| · | The financial asset is held within a business model whose objective is to hold financial assets in order to collect contractual cashflows, and |

| · | The contractual terms of the financial asset give rise on specific dates to cash flows that are solely payments of principal and interest on the principal amount outstanding. |

The amortized cost of a financial asset is the amount at which the financial asset is measured at initial recognition minus the principal repayments, plus the cumulative amortization using effective interest method of any difference between that initial amount and the maturity amount, adjusted for any loss allowance. Interest income is recognized using the effective interest method.

Financial assets that meet the following conditions are measured at fair value through other comprehensive income (FVTOCI):

| · | The financial asset is held within a business model who objective is achieved by both collection contractual cash flows and selling financial assets, and |

| · | The contractual terms of the financial asset give rise on specified dates to cash flows that are solely payments of principal and interest on the principal amount outstanding. |

By default, all other financial assets are measured subsequently at FVTPL.

The Company, at initial recognition, may also irrevocably designate a financial asset as measured at FVTPL if doing so eliminates or significantly reduces a measurement or recognition inconsistency that would otherwise arise from measuring assets or liabilities or recognizing the gains and losses on them on different bases.

Financial assets measured at FVTPL are measured at fair value at the end of each reporting period, with any fair value gains or losses recognized in profit or loss to the extent they are not part of a designated hedging relationship.

An equity instrument is any contract that evidences a residual interest in the assets of the Company after deducting all its liabilities. Equity instruments issued by the Company are recognized at the proceeds received, net of direct issue costs. Repurchase of the Company’s own equity instruments is recognized and deducted directly in equity. No gain or loss is recognized in profit or loss on the purchase, sale, issue or cancellation of the Company’s own equity instruments.

| 13 |

Leagold Mining Corporation

Notes to the Consolidated Financial Statements

For the years ended December 31, 2019 and 2018

(expressed in thousands of United States dollars, except as otherwise stated)

| ii. | Classification of financial liabilities |

Financial liabilities that are not contingent consideration of an acquirer in a business combination, held for trading or designated as at FVTPL, are measured at amortized cost using effective interest method.

Debt and equity instruments are classified as either financial liabilities or as equity in accordance with the substance of the contractual arrangements and the definitions of a financial liability and an equity instrument.

The Company designates certain derivatives as hedging instruments in respect of foreign currency risk and commodity price risk as cash flow hedges (Note 2(e)). Derivative instruments that do not qualify as hedging instruments are recorded at fair value with changes in fair value recognized in net (loss)/ income.

| s) | Share capital |

Common shares are classified as share capital. Incremental costs directly attributable to the issue of new share or options are shown in equity as a deduction, net of tax from the proceeds. If the Company reacquires its own equity, the cost is deducted from equity and the associated shares are cancelled or held in treasury.

| t) | Earnings per share |

Earnings per share calculations are based on the weighted average number of common and preferred shares issued and outstanding during the period. The rights of the common and preferred shares are the same and as such, common and preferred shares are treated as one class of shares for the earnings per share calculation. Diluted earnings per share are calculated using the treasury stock method, whereby the proceeds from the exercise of potentially dilutive common shares with exercise prices that are below the average market price of the underlying shares are assumed to be used in purchasing the Company’s common shares at their average market price for the period.

| u) | Share-based payment arrangements |

Cash settled share-based payments in the form of deferred share units (DSUs) and performance share units (PSUs) are measured at the fair value of the equity instruments at the grant date and revalued each reporting period. Initial recognition and the subsequent revaluation are recognized as share-based payments in consolidated statements of net (loss)/income and comprehensive (loss)/income.

Equity settled share-based payments are measured at the fair value of the equity instruments at the grant date. The fair value determined at the grant date of the equity settled share-based payments are expensed over the vesting period in accordance with the Company’s share option plan, in the consolidated statements of net (loss)/income and comprehensive (loss)/income.

3. Change in Accounting Policies and Standards