Exhibit 99.3

IVY CRYPTO, INC.

(formerly Gryphon Digital Mining, Inc.)

CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEARS ENDED DECEMBER 31, 2023 AND 2022

Ivy Crypto, Inc.

(formerly Gryphon Digital Mining, Inc.)

For the Years Ended December 31, 2023 and 2022

Index To Financial Statements

REPORT

OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To

the Board of Directors and Stockholders

Ivy

Crypto, Inc. (formerly Gryphon Digital Mining, Inc.)

Opinion

on the Financial Statements

We have audited the accompanying consolidated

balance sheets of Ivy Crypto, Inc. (formerly Gryphon Digital Mining, Inc.) (the Company) as of December 31, 2023 and 2022, and the related

consolidated statements of operations stockholders’ equity and cash flows for each of the years in the two-year period ended December

31, 2023, and the related notes (collectively referred to as the financial statements). In our opinion, the financial statements present

fairly, in all material respects, the financial position of the Company as of December 31, 2023 and 2022, and the results of its operations

and its cash flows for each of the years in the two-year period ended December 31, 2023, in conformity with accounting principles generally

accepted in the United States of America.

The

Company’s Ability to Continue as a Going Concern

The

accompanying financial statements have been prepared assuming that the Company will continue as a going concern. As discussed in Note

1 to the accompanying financial statements, the Company has incurred a loss from operations and has an accumulated deficit that raise

substantial doubt about the company’s ability to continue as a going concern. Management's evaluation of the events and conditions

and management's plans regarding these matters are also described in Note 1. The financial statements do not include any adjustments

that might result from the outcome of this uncertainty.

Basis

for Opinion

These

consolidated financial statements are the responsibility of the Company's management. Our responsibility is to express an opinion on

the Company's financial statements based on our audits. We are a public accounting firm registered with the Public Company Accounting

Oversight Board (United States) (PCAOB) and are required to be independent with respect to the Company in accordance with the U.S. federal

securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We

conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain

reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud. The Company

is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. As part of our audits,

we are required to obtain an understanding of internal control over financial reporting, but not for the purpose of expressing an opinion

on the effectiveness of the Company's internal control over financial reporting. Accordingly, we express no such opinion.

Our

audits included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error

or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding

the amounts and disclosures in the financial statements. Our audits also included evaluating the accounting principles used and significant

estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that our audits

provide a reasonable basis for our opinion.

/s/

RBSM LLP

RBSM

LLP

April

1, 2024

We

have served as the Company’s auditor since 2020

Larkspur,

California

PCAOB

ID 587

Ivy Crypto, Inc.

(formerly Gryphon Digital Mining, Inc.)

Consolidated Balance Sheets

As of December 31,

| | |

2023 | | |

2022 | |

| | |

| | |

| |

| Assets | |

| | |

| |

| Current assets | |

| | |

| |

| Cash and cash equivalents | |

$ | 915,000 | | |

$ | 267,000 | |

| Restricted cash | |

| 8,000 | | |

| 2,000 | |

| Accounts receivable | |

| 486,000 | | |

| 470,000 | |

| Prepaid expense | |

| 581,000 | | |

| 85,000 | |

| Marketable securities | |

| 403,000 | | |

| 235,000 | |

| Digital assets held for other parties | |

| 908,000 | | |

| 41,000 | |

| Digital asset | |

| 2,097,000 | | |

| 6,746,000 | |

| Total current assets | |

| 5,398,000 | | |

| 7,846,000 | |

| | |

| | | |

| | |

| Mining equipment, net | |

| 12,916,000 | | |

| 34,368,000 | |

| Deposits | |

| 420,000 | | |

| 60,000 | |

| Intangible asset | |

| 100,000 | | |

| 100,000 | |

| Total assets | |

$ | 18,834,000 | | |

$ | 42,374,000 | |

| | |

| | | |

| | |

| Liabilities and Stockholders' Equity | |

| | | |

| | |

| Current liabilities | |

| | | |

| | |

| Accounts payable and accrued liabilities | |

$ | 3,649,000 | | |

$ | 2,993,000 | |

| Liability related to digital assets held for other parties | |

| 916,000 | | |

| 41,000 | |

| Note payable – current portion | |

| 14,868,000 | | |

| 9,126,000 | |

| Total current liabilities | |

| 19,433,000 | | |

| 12,160,000 | |

| | |

| | | |

| | |

| Note payable – long term | |

| - | | |

| 3,510,000 | |

| Total liabilities | |

| 19,433,000 | | |

| 15,670,000 | |

| | |

| | | |

| | |

| Commitments and contingencies (Note 8) | |

| - | | |

| - | |

| | |

| | | |

| | |

| Stockholders’ (deficit) equity | |

| | | |

| | |

| Preferred stock, par value $0.0001, 13,000,000 authorized and none outstanding | |

| - | | |

| - | |

| Series seed preferred stock, par value $0.0001, 6,000,000 shares authorized, and 8,845,171 shares issued and outstanding, respectively | |

| - | | |

| - | |

| Series seed II preferred stock, par value $0.0001, 1,000,000 shares authorized and 460,855 issued and outstanding, respectively | |

| - | | |

| - | |

| Common stock, $0.0001 par value, 100,000,000 shares authorized; 25,109,630 and 24,856,428 shares issued and outstanding,

respectively | |

| 2,000 | | |

| 2,000 | |

| Additional paid-in capital | |

| 46,599,000 | | |

| 45,303,000 | |

| Subscription receivable | |

| (25,000 | ) | |

| (25,000 | ) |

| Accumulated deficit | |

| (47,175,000 | ) | |

| (18,576,000 | ) |

| Total stockholders’ (deficit) equity | |

| (599,000 | ) | |

| 26,704,000 | |

| Total liabilities and stockholders’ equity | |

$ | 18,834,000 | | |

$ | 42,374,000 | |

The accompanying notes are an integral part of

these consolidated financial statements.

Ivy Crypto, Inc.

(formerly Gryphon Digital Mining, Inc.)

Consolidated Statements of Operations

For the Years Ended December 31,

| | |

2023 | | |

2022 | |

| | |

| | |

| |

| Revenues | |

| | | |

| | |

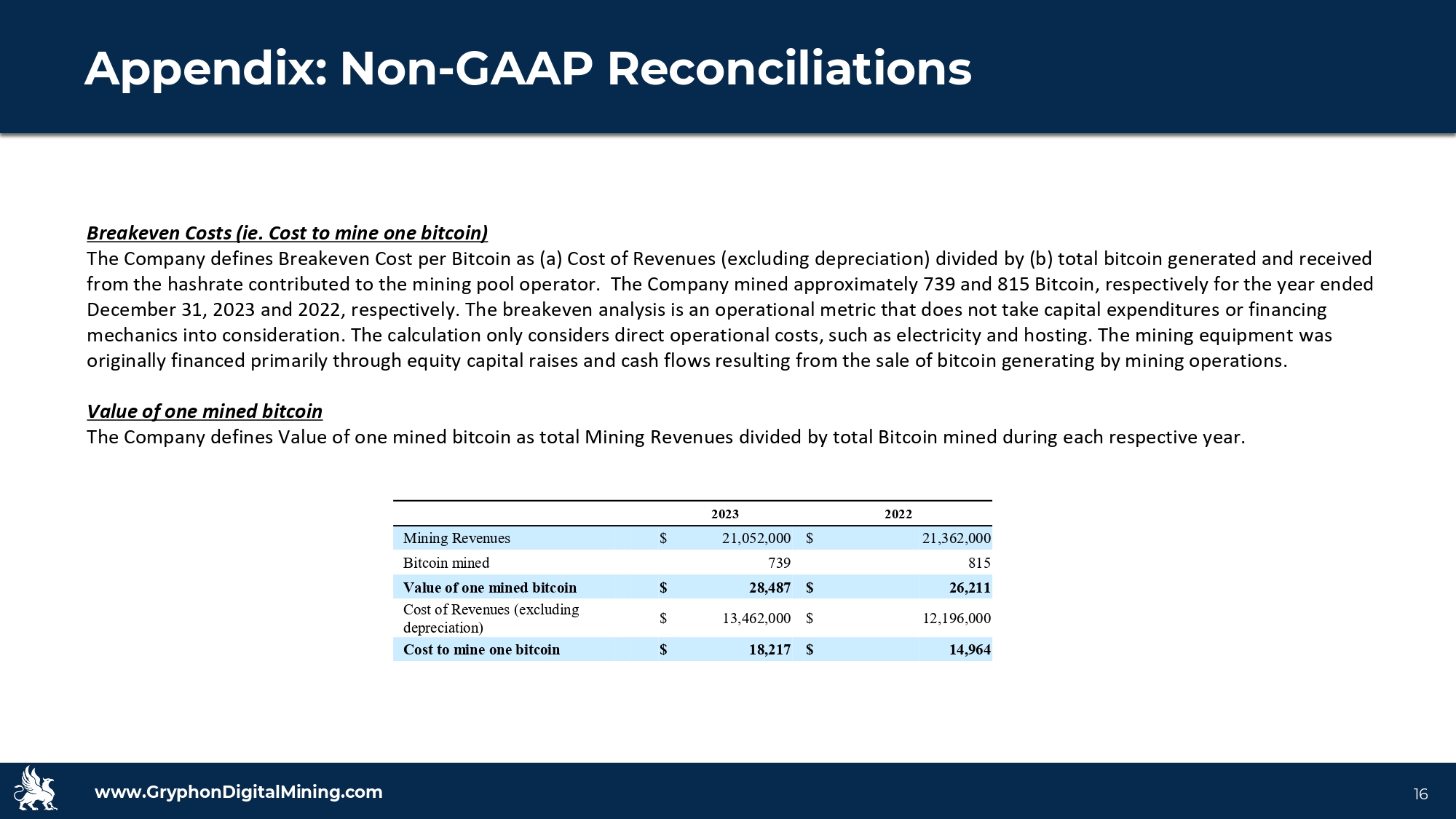

| Mining revenues | |

$ | 21,052,000 | | |

$ | 21,362,000 | |

| Management services | |

| 873,000 | | |

| 361,000 | |

| Total revenues | |

| 21,925,000 | | |

| 21,723,000 | |

| | |

| | | |

| | |

| Operating expenses | |

| | | |

| | |

| Cost of revenues (excluding depreciation) | |

| 13,462,000 | | |

| 12,196,000 | |

| General and administrative expenses | |

| 4,760,000 | | |

| 2,175,000 | |

| Stock-based compensation (income) expense | |

| (152,000 | ) | |

| 3,285,000 | |

| Impairment of digital assets | |

| 275,000 | | |

| 8,704,000 | |

| Realized gain on sale of digital assets | |

| (535,000 | ) | |

| (609,000 | ) |

| Impairment of miners | |

| 8,335,000 | | |

| - | |

| Depreciation expense | |

| 14,958,000 | | |

| 12,536,000 | |

| Total operating expenses | |

| 41,103,000 | | |

| 38,287,000 | |

| Loss from operations | |

| (19,178,000 | ) | |

| (16,564,000 | ) |

| | |

| | | |

| | |

| Other (expense) income | |

| | | |

| | |

| Unrealized income (loss) on marketable securities | |

| 168,000 | | |

| (1,499,000 | ) |

| Realized gain from use of digital assets | |

| 3,899,000 | | |

| - | |

| Loss on disposal of asset | |

| (55,000 | ) | |

| - | |

| Gain on extinguishment of debt | |

| - | | |

| 12,966,000 | |

| Loss on extinguishment of debt | |

| - | | |

| (2,746,000 | ) |

| Gain on termination of merger agreement | |

| - | | |

| 1,734,000 | |

| Change in fair value of notes payable | |

| (13,297,000 | ) | |

| 11,690,000 | |

| Other income | |

| 446,000 | | |

| 30,000 | |

| Interest expense | |

| (758,000 | ) | |

| (1,111,000 | ) |

| Amortization of debt discount | |

| - | | |

| (788,000 | ) |

| Total other (expense) income | |

| (9,597,000 | ) | |

| 20,276,000 | |

| | |

| | | |

| | |

| (Loss) income before provision for income taxes | |

| (28,775,000 | ) | |

| 3,712,000 | |

| | |

| | | |

| | |

| Provision for income taxes | |

| 176,000 | | |

| (176,000 | ) |

| Net (loss) income | |

$ | (28,599,000 | ) | |

$ | 3,536,000 | |

| | |

| | | |

| | |

| Net (loss) income per share - basic | |

$ | (1.15 | ) | |

$ | 0.14 | |

| Net (loss) income per share - diluted | |

| (1.15 | ) | |

| 0.10 | |

| Weighted average shares outstanding – basic | |

| 24,964,486 | | |

| 24,872,847 | |

| Weighted average shares outstanding – diluted | |

| 24,964,486 | | |

| 36,023,187 | |

The accompanying notes are an integral part of

these consolidated financial statements.

Ivy Crypto, Inc.

(formerly Gryphon Digital Mining, Inc.)

Consolidated Statement of Changes in Stockholders’

(Deficit) Equity

For the Years Ended December 31, 2023 and 2022

| | |

Series Seed

Preferred Stock | | |

Series Seed II

Preferred Stock | | |

Common Stock | | |

Additional

Paid-in | | |

Subscription | | |

Retained | | |

Total

Stockholders’ | |

| | |

Shares | | |

Amount | | |

Shares | | |

Amount | | |

Shares | | |

Amount | | |

Capital | | |

Receivable | | |

Earnings | | |

Equity | |

| Balance as of December 31, 2021 | |

| 8,845,171 | | |

$ | - | | |

| 460,855 | | |

$ | - | | |

| 24,494,820 | | |

$ | 2,000 | | |

$ | 41,192,000 | | |

$ | (25,000 | ) | |

$ | (22,112,000 | ) | |

$ | 19,057,000 | |

| Common stock issued for compensation | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| 1,467,000 | | |

| - | | |

| - | | |

| 1,467,000 | |

| Common stock issued for conversion of convertible debentures | |

| - | | |

| - | | |

| - | | |

| - | | |

| 75,467 | | |

| - | | |

| 277,000 | | |

| - | | |

| - | | |

| 277,000 | |

| Common stock issued for conversion of accrued interest on convertible debentures | |

| - | | |

| - | | |

| - | | |

| - | | |

| 7,239 | | |

| - | | |

| 41,000 | | |

| - | | |

| - | | |

| 41,000 | |

| Restricted common stock awards issued for compensation | |

| - | | |

| - | | |

| - | | |

| - | | |

| 235,718 | | |

| - | | |

| 2,056,000 | | |

| - | | |

| - | | |

| 2,056,000 | |

| Additional paid-in capital for services contributed by the Company’s president | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| 252,000 | | |

| - | | |

| - | | |

| 252,000 | |

| Common stock issued for Board of Director | |

| - | | |

| - | | |

| - | | |

| - | | |

| 43,184 | | |

| - | | |

| 18,000 | | |

| - | | |

| - | | |

| 18,000 | |

| Net income | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| 3,536,000 | | |

| 3,536,000 | |

| Balance as of December 31, 2022 | |

| 8,845,171 | | |

| - | | |

| 460,855 | | |

| - | | |

| 24,856,428 | | |

| 2,000 | | |

| 45,303,000 | | |

| (25,000 | ) | |

| (18,576,000 | ) | |

| 26,704,000 | |

| Common stock issued for compensation | |

| - | | |

| - | | |

| - | | |

| - | | |

| 112,510 | | |

| - | | |

| 382,000 | | |

| - | | |

| - | | |

| 382,000 | |

| Restricted common stock awards issued for compensation | |

| - | | |

| - | | |

| - | | |

| - | | |

| 71,975 | | |

| - | | |

| 620,000 | | |

| - | | |

| - | | |

| 620,000 | |

| Restricted common stock awards issued for payment of service | |

| - | | |

| - | | |

| - | | |

| - | | |

| 141,558 | | |

| - | | |

| 44,000 | | |

| - | | |

| - | | |

| 44,000 | |

| Additional paid-in capital for services contributed by the Company’s president | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| 250,000 | | |

| - | | |

| - | | |

| 250,000 | |

| Cancelled common stocks | |

| - | | |

| - | | |

| - | | |

| - | | |

| (72,842 | ) | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | |

| Net loss | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| (28,599,000 | ) | |

| (28,599,000 | ) |

| Balance as of December 31, 2023 | |

| 8,845,171 | | |

$ | - | | |

| 460,855 | | |

$ | - | | |

| 25,109,630 | | |

$ | 2,000 | | |

$ | 46,599,000 | | |

$ | (25,000 | ) | |

$ | (47,175,000 | ) | |

$ | (599,000 | ) |

The accompanying notes are an integral part of

these consolidated financial statements.

Ivy Crypto, Inc.

(formerly Gryphon Digital Mining, Inc.)

Consolidated Statements of Cash Flows

For the Years Ended December 31,

| | |

2023 | | |

2022 | |

| CASH FLOWS FROM OPERATING ACTIVITIES: | |

| | |

| |

| Net (loss) income | |

$ | (28,599,000 | ) | |

$ | 3,536,000 | |

| Adjustments to reconcile net (loss) income to cash provided by operating activities | |

| | | |

| | |

| Impairment of digital assets | |

| 275,000 | | |

| 8,704,000 | |

| Realized gain from sale of digital assets | |

| (535,000 | ) | |

| (609,000 | ) |

| Realized gain from use of digital assets | |

| (3,899,000 | ) | |

| - | |

| Impairment of miners | |

| 8,335,000 | | |

| - | |

| Amortization of debt discount | |

| - | | |

| 788,000 | |

| Depreciation expense | |

| 14,958,000 | | |

| 12,536,000 | |

| Forfeiture of restricted stock grants | |

| (1,910,000 | ) | |

| - | |

| Compensation cost related to common stock awards | |

| - | | |

| 2,873,000 | |

| Compensation cost related to restricted common stock awards | |

| 1,508,000 | | |

| 160,000 | |

| Compensation for services contributed by the Company’s President | |

| 250,000 | | |

| 252,000 | |

| Unrealized (gain) loss on marketable securities | |

| (168,000 | ) | |

| 1,499,000 | |

| Gain on termination of merger agreement | |

| - | | |

| (1,734,000 | ) |

| Gain on extinguishment of debt | |

| - | | |

| (12,966,000 | ) |

| Loss on extinguishment of debt | |

| - | | |

| 2,746,000 | |

| Loss on asset disposal | |

| 55,000 | | |

| - | |

| Change in fair value of notes payable | |

| 13,193,000 | | |

| (11,690,000 | ) |

| Interest expense | |

| 758,000 | | |

| 478,000 | |

| Digital asset revenue | |

| (21,052,000 | ) | |

| (21,362,000 | ) |

| Other | |

| 67,000 | | |

| - | |

| Changes in operating assets and liabilities | |

| | | |

| | |

| Proceeds from the sale of digital assets | |

| 18,512,000 | | |

| 30,559,000 | |

| Accounts receivable | |

| (456,000 | ) | |

| (1,089,000 | ) |

| Prepaid expense | |

| (249,000 | ) | |

| 54,000 | |

| Accounts payable and accrued liabilities | |

| 1,968,000 | | |

| (184,000 | ) |

| Net cash provided by operating activities | |

| 3,011,000 | | |

| 14,551,000 | |

| | |

| | | |

| | |

| CASH FLOWS FROM INVESTING ACTIVITIES | |

| | | |

| | |

| Deposit for purchase of bitcoin mining machines | |

| - | | |

| (8,150,000 | ) |

| Purchase of mining equipment | |

| (1,894,000 | ) | |

| (846,000 | ) |

| Refundable deposit | |

| (360,000 | ) | |

| - | |

| Net cash used in investing activities | |

| (2,254,000 | ) | |

| (8,996,000 | ) |

| | |

| | | |

| | |

| CASH FLOWS FROM FINANCING ACTIVITIES | |

| | | |

| | |

| Proceeds from the issuance of notes payable | |

| - | | |

| 2,500,000 | |

| Payment for insurance payable | |

| (109,000 | ) | |

| (37,000 | ) |

| Payment for convertible debentures | |

| - | | |

| (8,665,000 | ) |

| Net cash used in financing activities | |

| (109,000 | ) | |

| (6,202,000 | ) |

| | |

| | | |

| | |

| Net change in cash | |

| 648,000 | | |

| (647,000 | ) |

| | |

| | | |

| | |

| Cash-beginning of period | |

| 267,000 | | |

| 914,000 | |

| Cash-end of period | |

$ | 915,000 | | |

$ | 267,000 | |

| Reconciliation of cash and cash equivalents and restricted cash | |

| | | |

| | |

| Cash and cash equivalents | |

$ | 915,000 | | |

$ | 267,000 | |

| Restricted cash | |

| 8,000 | | |

| 2,000 | |

| Cash and cash equivalents and restricted cash | |

$ | 923,000 | | |

$ | 269,000 | |

| | |

| | | |

| | |

| Supplemental disclosures of cash flow information Cash paid for interest | |

$ | - | | |

$ | 839,000 | |

| Cash paid for income taxes | |

$ | 176,000 | | |

$ | - | |

| | |

| | | |

| | |

| Non-cash investing and financing activities | |

| | | |

| | |

| Digital assets used for purchase of mining equipment | |

$ | - | | |

$ | 538,000 | |

| Proceeds from loan – digital assets | |

$ | - | | |

$ | 27,592,000 | |

| Convertible debt conversion to equity | |

$ | - | | |

$ | 414,000 | |

| Interest conversion to equity | |

$ | - | | |

$ | 41,000 | |

| Accrued expense for issuance of common stock | |

$ | 845,000 | | |

$ | - | |

| Digital assets used for principal and interest payment of note payable | |

$ | 7,770,000 | | |

$ | 3,440,000 | |

The accompanying notes are an integral part of

these consolidated financial statements.

Ivy Crypto, Inc.

(formerly Gryphon Digital Mining, Inc.)

Notes to the Consolidated Financial Statements

For the Years Ended December 31, 2023 and 2022

NOTE 1 — ORGANIZATION AND SUMMARY

OF SIGNIFICANT ACCOUNTING POLICIES

Organization and Nature of Operations

Ivy Crypto, Inc. (formerly known as Gryphon Digital

Mining, Inc.) (the “Company”) was incorporated under the provisions and by the virtue of the provisions of the General Corporation

Law of the State of Delaware on October 22, 2020, with the office located in Las Vegas, Nevada. The Company will operate a digital

asset (commonly referred to as cryptocurrency) mining operation using specialized computers equipped with application-specific integrated

circuit (ASIC) chips (known as “miners”) to solve complex cryptographic algorithms in support of the Bitcoin blockchain (in

a process known as “solving a block”) in exchange for cryptocurrency rewards (primarily Bitcoin).

On April 20, 2022, the Company formed a limited

liability company named Gryphon Opco I LLC (“GOI”). GOI aims to engage in any activity for which limited liability companies

may be organized in the State of Delaware.

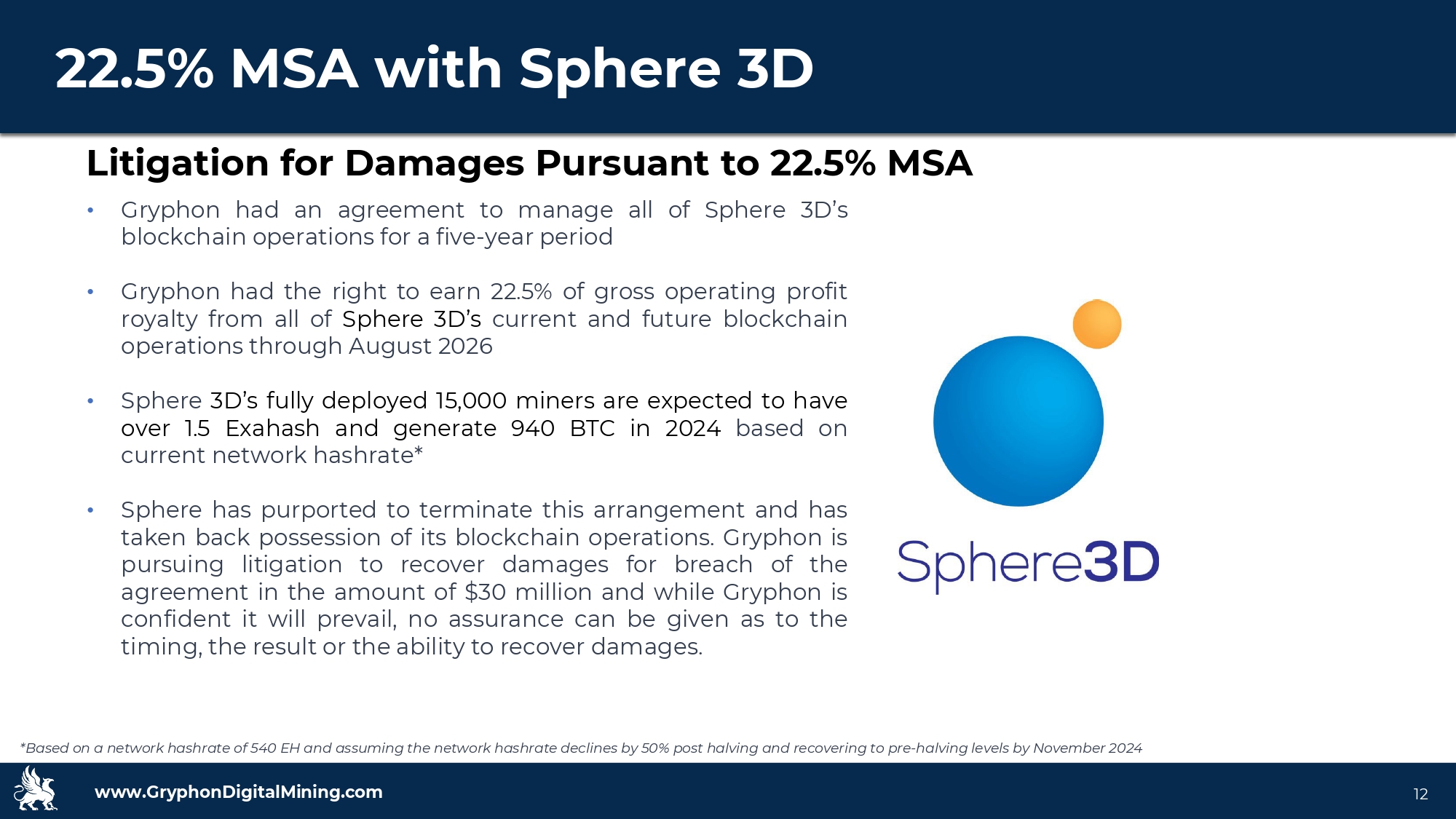

Termination of Merger — Sphere

3D Corp.

On June 3, 2021, the Company entered into

an Agreement and Plan of Merger (“Merger Agreement”) with Sphere 3D Corp. (“Sphere 3D”). Upon completion

of the merger (the “Merger”), the Sphere 3D Corp. will change its name to Gryphon Digital Mining, Inc.

As consideration for the merger transaction, Sphere

3D will issue 111,000,000 shares of its common stock to the shareholders of the Company, such that on closing, the Sphere 3D

shareholders will own approximately 23% of the consolidated company and the Company shareholders will own approximately the remaining

77% on a fully diluted basis, subject to adjustments for additional capital raises by either entity. As of the Merger Agreement, the Company

had 21,282,593 shares of common stock and share equivalents. Each share, and share equivalent, will be converted into 5.22 shares

of Sphere 3D common stock. As of the Merger Agreement, the value of a share of the Company’s common stock was approximately $8.50,

for total consideration of approximately $181,000,000.

On December 29, 2021, the Company and Sphere

3D entered into Amendment No. 1 to the Merger Agreement to give effect to the issuances by the Company of its equity securities subsequent

to June 3, 2021. The parties agreed upon an increase in the number of Sphere 3D common shares that will be issued by Sphere 3D in

the Merger from approximately 111,000,000 to approximately 122,000,000, with an effective exchange ratio of approximately 5.31. In addition,

among other matters, the parties revised the termination provisions of the Merger Agreement to allow either party to terminate the Merger

Agreement prior to March 31, 2022, upon a breach of the agreement by the other party following an opportunity to cure such breach,

and to allow either party to terminate the Merger Agreement on or after March 31, 2022, for any reason or no reason by notice to

the other party. In addition, upon termination, each party agreed to release the other party and its affiliates from any claims or

proceedings such party shall have at the time of such termination against the other party existing by reason of, based upon, or arising

out of the Merger Agreement.

On April 4, 2022, the Company and Sphere

3D mutually agreed to terminate their Merger Agreement announced on June 3, 2021, and as amended on December 29, 2021, due to

changing market conditions, the passage of time, and the relative financial positions of the companies, among other factors.

Lastly, in accordance with the Amended Merger

Agreement, the Company received 850,000 shares of Sphere 3D’s restricted common stock that were held in a third-party escrow

account, and the existing indebtedness owed by the Company to Sphere 3D in the principal amount of $12,500,000 and accrued interest of

$466,000 shall be forfeited.

Akerna Merger Agreement

On January 27, 2023, the Company, Akerna

Corp. (“Akerna”) and Akerna Merger Co. (“Merger Sub”), entered into an agreement and plan of merger (as amended,

the “Akerna Merger Agreement”).

On February 9, 2024, the Company completed the transactions contemplated

by the Akerna Merger Agreement.

Under the terms of the Akerna Merger Agreement,

Merger Sub merged with and into the Company, with the Company surviving as a wholly-owned subsidiary of Akerna (the “Merger”).

At the effective time of the Merger (the “Effective Time”), each share of the Company’s common stock, par value $0.0001

per share (the “Company Common Stock”), and the Company’s preferred stock, par value $0.0001 per share (the “Company

Preferred Stock,” collectively referred to herein with the Company Common Stock as the “Company Shares”), outstanding

immediately prior to the Effective Time was converted into the right to receive approximately 1.727 shares of common stock (“Conversion

Rate”), par value $0.001 per share (the “Akerna Stock”). All share and per-share data has been adjusted for the conversion

rate.

Following

the Merger, the former holders of the Company’s equity securities hold 92.5% of Akerna’s common stock on a fully diluted basis,

with the remaining 7.5% being held by the legacy shareholders of Akerna. The Company Common Stock outstanding of 14,536,298, as of December

31, 2023, was converted into 25,109,630 shares of Akerna common stock.

Also, the

Akerna management group resigned, and the Company’s management group was installed as the management group of Akerna. The Company’s

board of directors comprised the majority of the members of Akerna’s board.

Effective

with the merger, Akerna's operations were sold off to an independent third party, so the company's continued operations will be the Company’s

operation.

Each outstanding warrant to purchase shares of

the Company’s common stock that was issued and outstanding at the Effective Time remained issued and outstanding and was assumed

by Akerna and is exercisable for shares of Akerna’s common stock pursuant to its existing terms and conditions as adjusted to reflect

the ratio of exchange of Company Shares for shares of Akerna Stock.

Immediately after giving effect to the Merger,

Akerna had 38,733,554 shares of Akerna Stock outstanding on a fully diluted basis.

In connection with the Merger, Akerna changed

its name to “Gryphon Digital Mining, Inc.” and the Company changed its name to Ivy Crypto, Inc.

Reclassification

Certain reclassifications have been made to the

2022 consolidated financial statements in order to conform to the current period presentations. These classifications did not impact the

net income for the year ended December 31, 2022.

Principles of Consolidation

The consolidated financial statements include

the accounts of the Company and its wholly-owned subsidiary from the date of inception (April 20, 2022). All material intercompany

transactions and balances have been eliminated in consolidation.

Going Concern

The accompanying consolidated financial statements have been prepared

in conformity with accounting principles generally accepted in the United States of America (“GAAP”), which contemplate

the continuation of the Company as a going concern and the realization of assets and satisfaction of liabilities in the ordinary course

of business. The carrying amounts of assets and liabilities presented in the financial statements do not necessarily purport to represent

realizable or settlement values. The financial statements do not include any adjustment that might result from the outcome of this uncertainty.

The Company’s future results are subject to substantial risks and uncertainties.

Since the Company began revenue generation in

September 2021, management has financed the Company’s operations through equity and debt financing and the sale of the digital

assets earned through mining operations.

On December 31, 2023, the Company had cash, cash equivalents and

restricted cash totaling $923,000 and digital assets totaling $2,097,000. During the twelve months ended December 31, 2023, the Company

made payments on the loan denominated in Bitcoin of $7,900,000 for principal and interest payments.

The Company may incur additional losses from operations and negative

cash outflows from operations in the foreseeable future. In the event the Company continues to incur losses, it may need to raise debt

or equity financing to finance its operations until operations are cashflow positive. However, there can be no assurance that such financing

will be available in sufficient amounts and on acceptable terms, when and if needed, or at all. The precise amount and timing of the funding

needs cannot be determined accurately at this time and will depend on several factors, including the market price for the underlying commodity

mined by the Company and its ability to procure the required mining equipment and operate profitably. The Company’s financial statements

have been presented on a going concern basis, which contemplates the realization of assets and the satisfaction of liabilities in the

ordinary course of business.

Use of Estimates

The preparation of financial statements in accordance with GAAP requires

management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosures of contingent

assets and liabilities at the date of the financial statements, and the reported amounts of expenses during the reporting period. Actual

results could differ from those estimates. The most significant accounting estimates

inherent in the preparation of the Company’s financial statements include revenue recognition, impairment analysis of long-lived

assets, stock-based compensation, and the valuation allowance associated with the Company’s deferred tax assets.

Fair Values of Financial Instruments

The Company adopted the provisions of Accounting

Standards Codification (“ASC”) subtopic 825-10, Financial Instruments (“ASC 825-10”) which defines fair

value as the price that would be received from selling an asset or paid to transfer a liability in an orderly transaction between market

participants at the measurement date. When determining the fair value measurements for assets and liabilities required or permitted to

be recorded at fair value, the Company considers the principal or most advantageous market in which it would transact and considers assumptions

that market participants would use when pricing the asset or liability, such as inherent risk, transfer restrictions, and risk of nonperformance.

ASC 825-10 establishes a fair value

hierarchy that requires an entity to maximize the use of observable inputs and minimize the use of unobservable inputs when measuring

fair value. ASC 825-10 establishes three levels of inputs that may be used to measure fair value:

| |

|

Level 1 — |

|

Quoted prices in active markets for identical assets or liabilities. |

| |

|

Level 2 — |

|

Observable inputs other than Level 1 prices such as quoted prices for similar assets or liabilities; quoted prices in markets with insufficient volume or infrequent transactions (less active markets); or model-derived valuations in which all significant inputs are observable or can be derived principally from or corroborated by observable market data for substantially the full term of the assets or liabilities. |

| |

|

Level 3 — |

|

Unobservable inputs to the valuation methodology that are significant to the measurement of the fair value of assets or liabilities. |

Cash and Cash Equivalents

The Company considers all short-term highly liquid investments

with a remaining maturity at the date of purchase of three months or less to be cash equivalents. Cash and cash equivalents are recorded

at cost, which approximates their fair value. The Company maintains its cash and cash equivalents in banks insured by the Federal Deposit

Insurance Corporation (“FDIC”) in accounts that, at times, may be in excess of the federally insured limit of $250,000 per

bank. The Company minimizes this risk by placing its cash deposits with major financial institutions. As of December 31, 2023 and 2022,

the Company had cash and equivalents of $665,000 and $17,000, in excess of the federal insurance limit. Also, the Company holds cash for

third parties in the amounts of $8,000 and $2,000 as of December 31, 2023 and 2022, respectively. The

Company has never suffered a loss due to such excess balances.

Accounts Receivable

As of December 31, 2023, accounts receivable includes

amounts due from Sphere 3D from the revenue share agreement. The Company collected these amounts in the first quarter of 2024. See “Note

12—Subsequent Event” for more information.

As of December 31, 2022, accounts receivable pertained

to proceeds (fiat currency) not yet received for the sale of digital assets or cryptocurrencies due to the cut-off period. Management

has assessed the consideration of credit risk, and subsequent to the reporting periods where a balance existed, the Company has received

payment in full of all outstanding accounts receivable and, as such, does not believe an allowance is necessary.

Prepaid Expense

Prepaid expenses which consist of payments for

an insurance policy and are expected to be realized and consumed within twelve months after the reporting period.

Digital Assets Held for Other Parties

In accordance with the Securities and Exchange

Commission’s Staff Accounting Bulletin 121, the Company records an obligation liability and a corresponding digital asset held for

other parties’ assets based on the fair value of the cryptocurrency held for other parties at each reporting date. In accordance

with ASC 820, the Company has fair valued these digital assets and the associated liability by using the Coinbase closing price of

Bitcoin on the reporting date. This balance also includes the cash balance held for other parties.

Digital Assets

Digital assets or cryptocurrencies,

(including Bitcoin, Ethereum, DAI, and USDT) are included in current assets in the accompanying balance sheets. Cryptocurrencies purchased

are recorded at cost and cryptocurrencies obtained by the Company through its sale of common stock are accounted for based on the value

of the specific digital asset on the date received.

Pursuant to ASC Topic

210-10-20, the Company considered the operating cycle, intent and purpose and realizability of bitcoin to properly classify the asset

on its balance sheet. As the Company intends to convert its mined bitcoin rewards received into cash and use the proceeds generated within

its normal operating cycle of business (within one year of receipt), the Company may classify bitcoin as a current asset under ASC 210-10-20.

As such, the Company classified the bitcoin mined and earned as a current asset. Given the volatility of the bitcoin market, the Company

regularly reviews and reassesses the classification of bitcoin to ensure alignment with the Company’s current intent and market

conditions.

The Company accounts

for digital assets as indefinite-lived intangible assets in accordance with ASC 350, Intangibles

| — | Goodwill and Other. The Company has ownership of and control

over the cryptocurrencies and uses third-party custodial services to secure them. The digital assets are initially recorded at cost

and are subsequently remeasured on the balance sheets at cost, net of any impairment losses incurred since acquisition. |

An impairment analysis

is performed at each reporting period to identify whether events or changes in circumstances, in particular decreases in the quoted prices

on active exchanges, indicate that it is more likely than not that the digital assets held by the Company are impaired. The fair value

of digital assets is determined on a nonrecurring basis in accordance with ASC 820, Fair Value Measurement, based on quoted prices

on the active exchange(s) that the Company has determined is its principal market for cryptocurrencies (Level 1 inputs). If the carrying

value of the digital asset exceeds the fair value based on the lowest price quoted in the active exchanges during the period, an impairment

loss has occurred with respect to those digital assets in the amount equal to the difference between their carrying values and the price

determined.

Bitcoin awarded to the Company through its mining activities are accounted

for in connection with the Company’s revenue recognition policy. Bitcoin is classified on the Company’s Consolidated Balance

Sheet as a current asset due to the Company’s ability to sell it in a highly liquid marketplace and its intent to liquidate its

Bitcoin to support operations when needed.

Cryptocurrencies

awarded to the Company through its mining activities are included within operating activities in the accompanying consolidated

statements of cash flows. The cash received from the sales of cryptocurrencies earned through our mining activities is included

within operating activities in the accompanying consolidated statements of cash flows, and any realized gains or losses from such

sales are included in operating expenses in the consolidated statements of operations. The Company accounts for its gains or losses

in accordance with the specific identification (Spec ID) method of accounting. This alternative allows the Company to select the exact bitcoin to sell based on the original acquisition date.

Impairment losses are

recognized within “Operating expenses” in the statements of operations in the period in which the impairment is identified.

The impaired digital assets are written down to their fair value at the time of impairment and this new cost basis will not be adjusted

upward for any subsequent increase in fair value. Gains are not recorded until realized upon sale or disposition.

Investment in marketable equity securities

The Company measures its investments in marketable equity securities

at fair value at each balance sheet date, with unrealized holding gains and losses recorded in other income (expense), as the shares have

a readily determinable fair value since they are publicly traded.

Mining Equipment

Mining Equipment is stated at cost, including

purchase price and all shipping and customs fees, and depreciated using the straight-line method over the estimated useful lives

of the assets, generally three years for cryptocurrency mining equipment.

In accordance with ASC 360-10-35, the Company

reviews the carrying amounts of mining equipment when events or changes in circumstances indicate the assets may not be recoverable. If

any such indication exists, the recoverable amount of the asset is estimated in order to determine the extent of the impairment loss,

if any. Where it is not possible to estimate the recoverable amount of an individual asset, the Company estimates the recoverable amount

of the cash-generating unit to which the asset belongs.

The recoverable amount is the higher of fair value

less costs of disposal and value in use. In assessing value in use, the estimated future cash flows to be derived from continuing use

of the asset or cash-generating unit are discounted to their present value using a pre-tax discount rate that reflects current

market assessments of the time value of money and the risks specific to the asset. Fair value less costs of disposal is the amount obtainable

from the sale of an asset or cash-generating unit in an arm’s length transaction between knowledgeable, willing parties, less

the cost of disposal. When a binding sale agreement is not available, fair value less costs of disposal is estimated using a discounted

cash flow approach with inputs and assumptions consistent with those of a market participant. If the recoverable amount of an asset or

cash-generating unit is estimated to be less than its carrying amount, the carrying amount of the cash-generating unit is reduced

to its recoverable amount. An impairment loss is recognized immediately in net income.

At the point in time a miner becomes inoperable

and not repairable, the Company records an expense amounting to the carrying value, which is the cost basis less accumulated depreciation

at the time of write off.

LEASES

Effective July 2021,

the Company accounts for its leases under ASC 842, Leases (“ASC 842”). Under this guidance, arrangements

meeting the definition of a lease are classified as operating or financing leases and are recorded on the balance sheet as both a right-of-use asset

and a lease liability, calculated by discounting fixed lease payments over the lease term at the rate implicit in the lease or the Company’s

incremental borrowing rate. Lease liabilities are increased by interest and reduced by payments each period, and the right-of-use asset

is amortized over the lease term. For operating leases, interest on the lease liability and the amortization of the right-of-use asset

result in straight-line rent expense over the lease term.

In calculating the right-of-use asset

and the lease liability, the Company elects to combine lease and non-lease components as permitted under ASC 842. The Company

excludes short-term leases having initial terms of 12 months or less from the new guidance as an accounting policy election

and recognizes rent expense on a straight-line basis over the lease term.

Derivatives

The Company evaluates all of its financial instruments

to determine if such instruments are derivatives or contain features that qualify as embedded derivatives. For derivative financial instruments

that are accounted for as liabilities, the derivative instrument is initially recorded at its fair value and would then be re-valued at

each reporting date, with changes in the fair value reported in the condensed statements of operations. If there are stock-based derivative

financial instruments, the Company will use a probability-weighted average series Binomial lattice option pricing models to value

the derivative instruments at inception and on subsequent valuation dates.

The classification of derivative instruments,

including whether such instruments should be recorded as liabilities or as equity, is evaluated at the end of each reporting period. Derivative

instrument liabilities will be classified in the balance sheet as current or non-current based on whether or not net-cash settlement

of the derivative instrument could be required within 12 months of the balance sheet date. Derivative liability will be measured

initially and subsequently at fair value.

Revenue Recognition

The Company recognizes revenue under ASC 606,

Revenue from Contracts with Customers. The core principle of the new revenue standard is that a company should recognize revenue to depict

the transfer of promised goods or services to customers in an amount that reflects the consideration to which the company expects to be

entitled in exchange for those goods or services. The following five steps are applied to achieve that core principle:

| ● | Step 1: Identify the contract with the customer |

| ● | Step 2: Identify the performance obligations in the contract |

| ● | Step 3: Determine the transaction price |

| ● | Step 4: Allocate the transaction price to the performance

obligations in the contract |

| ● | Step 5: Recognize revenue when the Company satisfies a performance

obligation |

In order to identify the performance obligations

in a contract with a customer, a company must assess the promised goods or services in the contract and identify each promised good or

service that is distinct. A performance obligation meets ASC 606’s definition of a “distinct” good or service (or

bundle of goods or services) if both of the following criteria are met: The customer can benefit from the good or service either on its

own or together with other resources that are readily available to the customer (i.e., the good or service is capable of being distinct),

and the entity’s promise to transfer the good or service to the customer is separately identifiable from other promises in the contract

(i.e., the promise to transfer the good or service is distinct within the context of the contract).

If a good or service is not distinct, the good

or service is combined with other promised goods or services until a distinct bundle of goods or services is identified.

The transaction price is the amount of consideration

to which an entity expects to be entitled in exchange for transferring promised goods or services to a customer. The consideration promised

in a contract with a customer may include fixed amounts, variable amounts, or both. When determining the transaction price, an entity

must consider the effects of all the following:

| ● | Constraining estimates of variable consideration |

| ● | The existence of a significant financing component in the

contract |

| ● | Consideration payable to a customer |

Variable consideration is included in the transaction

price only to the extent that it is probable that a significant reversal in the amount of cumulative revenue recognized will not occur

when the uncertainty associated with the variable consideration is subsequently resolved. The transaction price is allocated to each performance

obligation on a relative standalone selling price basis. The transaction price allocated to each performance obligation is recognized

when that performance obligation is satisfied, at a point in time, or over time as appropriate.

Cryptocurrency mining:

The Company has entered

into contracts with digital asset mining pool operators to provide the service of performing hash computations for the mining pool operator.

The contracts are terminable at any time for any reason by either party without cause and without penalty and the Company’s enforceable

right to compensation only begins when the Company provides the service of performing hash computations for the mining pool operator.

The contract is for a continuous 24-hour period each day. The Company’s access and usage rights to the pool and service automatically

renew for a successive 24-hour period (00:00:00 UTC and 23:59:59 UTC) unless terminated in accordance with the terms set forth by

the terms of service. In exchange for performing hash computations for the mining pool, Gryphon is entitled to a fractional share of the

fixed cryptocurrency award the mining pool operator receives (less digital asset transaction fees to the mining pool operator which are

netted as a reduction of the transaction price). Gryphon’s fractional share is based on the proportion of hash computations Gryphon

performed for the mining pool operator to the total hash computations contributed by all mining pool participants in solving the current

algorithm during the 24-hour period. Hashrate is the measure of the computational power per second used when mining. It is measured

in units of hash per second, meaning how many calculations per second that can be performed. The consideration the Company will receive,

comprised of block rewards, transaction fees less mining pool operator fees are aggregated in a sub-balance account held by the mining

pool operator. That balance, due to the Company, is calculated by the mining pool operator based on the hashrate provided and hash computations

completed by the Company for the mining pool from midnight-to-midnight (00:00:00 UTC and 23:59:59 UTC) UTC time, and a sub-account balance

is credited one hour later at 1AM UTC time. The balance is then withdrawn to the Company’s whitelisted wallet address, once a day,

between the hours of 9am to 5pm UTC time. The rate of payment occurs once per day, as long as the minimum payout threshold of 0.01 bitcoin

has accumulated in the sub-account balance, in accordance with the mining pool operator’s terms of service. Pursuant to ASC

606-10-55-42, the Company assessed if the customer’s option to renew represented a material right that represents a separate performance

obligation and noted the renewal is not a material right. The definition of a material right is a promise in a contract to provide goods

or services to a customer at a price that is significantly lower than the stand-alone selling price of the good or service. The mining

pool operator does not provide any discounts and as such there is no economic benefit to the customer and as such a separate performance

obligation does not exist under 606-10-55-42. In addition, there are no options for renewal that are separately identifiable from other

promises in the contract such as an ability to extend the contract at a reduced price.

The performance obligation

of the Bitcoin miner under the mining contracts with Foundry Pool USA involves the service of performing hash computations to facilitate

the verification of digital asset transactions. The Company’s miners contribute computing power (i.e.. hashrate) that perform hash

calculations to the mining pool operator, engaging in the process of validating and securing transactions through the generation of cryptographic

hashes. The mining pool then utilizes a specific mining algorithm (e.g. SHA-256) to submit shares (proof of work) to the mining pool’s

server as they contribute to solving the cryptographic puzzles required to mine a block. The Company reviews and analyzes its individual

pool performance using a dashboard provided by Foundry Pool USA that includes real-time statistics on hashrate, shares submitted

and earnings. The service of performing hash computations in digital asset transaction verification services is an output of the Company’s

ordinary activities. The provision of providing these services is the only performance obligation in the Company’s contracts with

mining pool operators. The Company performs hash computations for one mining pool operator, Foundry USA. Foundry USA operates its pool

on the Full Pay Per Share (FPPS) payout method. FPPS is a variant of the Pay Per Share (PPS) method, where miners receive a fixed payout

for each valid share submitted, regardless of whether the pool finds a block.

Regardless of the pool’s

success, the Company will receive consistent rewards based on the number of valid shares it contributes. The transaction consideration

the Company receives is non-cash consideration, in the form of bitcoin. The Company measures the bitcoin at fair value on the date

earned using the average price (calculated by averaging the daily open price and the daily close price) quoted by its Principal Market

at the date the Company completed the service of performing hash computations for the mining pool operator. There are no deferred revenues

or other liability obligations recorded by the Company since there are no payments in advance of the performance. At the end of each 24

hour period (00:00:00 UTC and 23:59:59 UTC), there are no remaining performance obligations. By utilizing the average daily price of bitcoin

on the date earned, the Company eliminates any differences that may arise due to the volatility in trading price between bitcoin and fiat

currency during the period where the Company establishes and completes the contract. The consideration is all variable. There is no significant

financing component in these transactions.

If authoritative guidance

is enacted by the Financial Accounting Standards Board (“FASB”), the Company may be required to change its policies, which

could affect the Company’s financial position and results from operations.

Master service agreement:

The Company has entered into an agreement with

Sphere 3D to be an exclusive provider of management services for all blockchain and cryptocurrency-related operations including but

not limited to services relating to all mining equipment owned, purchased, leased, operated, or otherwise controlled by Sphere 3D and/or

its subsidiaries and/or its affiliates at any location. For the said services the Company will receive 22.5% of the net operating profit

of all of Sphere 3D’s blockchain and cryptocurrency-related operations. The net operating profits in defined as the value of

the digital asset mined less energy cost and profit paid to the host facility.

As Sphere 3D has the ultimate right to determine

the facility location for each machine. The Company has the responsibility for the following:

| 1) | Ensuring the machines are installed in the facility selected

by Sphere. |

| 2) | Selecting and connecting the machines to a mining pool. |

| 3) | To review the mining reports and maintain a wallet for the

coins earned for the mining operation. |

| 4) | To maintain a custodial wallet for the coins earned from

the Sphere machines. |

| 5) | To sell and/or transfer the coins at the request of Sphere. |

At the time the digital assets are mined, they

are transferred into the custodial wallet maintained by the Company. As of the receipt of the digital asset, the Company has completed

its performance obligation, the transaction price is determinable, net operating profit can be calculated so that the Company can determine

its revenue under the contract; therefore, the Company records as revenue the management fee received. See Note 8 — Commitments

and contingencies “Sphere 3D MSA” and Note 12 – Subsequent Events.

Cost of Revenues

The Company’s cost of revenue consists primarily of direct costs

of earning bitcoin related to mining operations, including electric power costs, other utilities, labor, insurance whether incurred directly

from self-mining operations or reimbursed, including any revenue sharing arrangements under co-location agreements, but excluding

depreciation and amortization, which are separately stated in the Company’s Consolidated Statements of Operations.

ASC 606-10-32-25 through

32-27 in the Financial Accounting Standards Board’s (FASB) Accounting Standards Codification (ASC) provides guidance on the

consideration of whether fees paid to a mining pool operator should be considered payments to a customer and treated as a reduction of

the transaction price or revenue. The Company’s management reviewed the standards and completed the following assessment.

Identifying the

Customer: ASC 606-10-32-25 states that an entity should determine whether the counterparty to a contract is a customer. If the

counterparty is a customer, the entity should apply the revenue recognition guidance to that contract. Under ASC 606-10-32-25, the

Company identified the mining pool operator as the customer as the Company entered into a contractual agreement with the pool

operator whereas the Company is to provide services in the form of contributing hashing power to the pool.

Mining Pool Operator

as a Customer: As the Company has determined the mining pool operator to be a customer, any fees paid to the mining

pool operator would be part of the transaction price of the contract. Any fees paid by the Company as a miner to the pool operator would

be revenue earned by the pool operator, and the pool operator is treated as the customer.

Transaction Price:

ASC 606-10-32-26 provides guidance on determining the transaction price. The Company considered the effects of variable

consideration, constraints on variable consideration, the existence of a significant financing component in the contract, and

non-cash consideration. The Company receives variable consideration given the variable nature of the amount of mining power

(hashrate) contributed on a daily basis (24-hour period per recurring contract term). The Company completes an analytical

procedure as part of its monthly close process to determine the reasonableness of consideration received. There are no significant

financing components of the transaction or delays in the timing of payments from the customer to the Company, whereas the Company

would need to adjust the transaction price for the time value of money. As the Company receives non-cash consideration, in the

form of bitcoin, ASC 606-10-32-26 specifies that the Company should measure non-cash consideration at fair value. The fair

value of the non-cash consideration would be included in the determination of the transaction price. The Company does not

receive the gross amounts of bitcoin earned prior to the transaction fees deduction by the pool operator. As such, the consideration

received is net or inclusive of the transaction fees incurred and charged by the customer (pool operator).

Variable Consideration: If

the fees paid to the mining pool operator are variable, an entity should estimate the amount of consideration to which it will be entitled.

This involves considering the likelihood and magnitude of a significant revenue reversal. ASC 606-10-32-26 emphasizes the need to

assess whether there are constraints on variable consideration. In the instance where there is uncertainty about the amount of consideration,

it is reasonable for the Company to consider a likelihood of a significant reversal of revenue. The Company reviews daily bitcoin rewards

received and reviews various factors, such as mining difficulty, the price of bitcoin and the Company’s contribution to the pool

operator. The Company estimates the amount of variable consideration the Company should receive and prepares a monthly workpaper documenting

the difference in actual bitcoin rewards received vs. estimated bitcoin earned. The Company assessed, given the pool operators payout

methodology and the revenue reasonableness test completed by management, there does not exist a likelihood of a significant reversal of

revenue.

Reduction of Transaction

Price: ASC 606-10-32-27 states that an entity should reduce the transaction price for variable consideration

only to the extent that it is probable that a significant revenue reversal will not occur when the uncertainty is subsequently resolved.

The Company assessed various factors, identifying the variable consideration, estimating the variable consideration, considered constraints

(although none existed such as performance metrics or targets), probability, documentation, regular review and monitoring of performance

with open communication with pool operators combined with dashboard usage. Due to the Company utilizing Foundry Pool’s FPPS methodology

and the previous mentioned factors, there was zero likelihood of a significant reversal of revenue as the Company receives payouts as

a pool participant on a daily basis calculated from midnight-to-midnight UTC time, regardless of if the Pool Operator receives any

block rewards.

In summary, fees paid

to the mining pool operator are considered payments to a customer and treated as a reduction of the transaction price/revenue. The Company

has carefully assessed the variable nature of these fees, considered the likelihood and magnitude of any potential adjustments, and documented

that management has applied the revenue recognition guidance accordingly.

Stock-Based Compensation

We account for our stock-based compensation

under ASC 718 “Compensation — Stock Compensation” using the fair value-based method. Under

this method, compensation cost is measured at the grant date based on the value of the award and is recognized over the service period,

which is usually the vesting period. This guidance establishes standards for the accounting of transactions in which an entity exchanges

its equity instruments for goods or services. It also addresses transactions in which an entity incurs liabilities in exchange for goods

or services that are based on the fair value of the entity’s equity instruments, or the issuance of those equity instruments may

settle that.

We use the fair value method for equity instruments

granted to non-employees and use the Black-Scholes model for measuring the fair value of options. The stock-based fair

value compensation is determined as of the date of the grant or the date at which the performance of the services is completed (measurement

date) and is recognized over the vesting periods.

Common stock awards

The Company grants common stock awards to non-employees in

exchange for services provided. The Company measures the fair value of these awards using the fair value of the services provided or the

fair value of the awards granted, whichever is more reliably measurable. The fair value measurement date of these awards is generally

the date the performance of services is complete. The fair value of the awards is recognized on a straight-line basis as services

are rendered. The share-based payments related to common stock awards for the settlement of services provided by non-employees are

recorded in accordance with ASC 718 on the statement of operations in the same manner and charged to the same account as if such

settlements had been made in cash.

Warrants

The Company has issued warrants to purchase shares

of its common stock in connection with certain financing, consulting, and collaboration arrangements. The outstanding warrants are standalone

instruments that are not puttable or mandatorily redeemable by the holder and are classified as equity awards. The Company measures the

fair value of the awards using the Black-Scholes option pricing model as of the measurement date. Warrants issued in conjunction

with the issuance of common stock are initially recorded at fair value as a reduction in additional paid-in capital of the common

stock issued. All other warrants are recorded at fair value as expense over the requisite service period or at the date of issuance if

there is not a service period.

Income Taxes

The Company accounts for income taxes under the

asset and liability method, in which deferred tax assets and liabilities are recognized for the future tax consequences attributable to

differences between the financial statement carrying amounts of existing assets and liabilities and their respective tax bases and operating

loss and tax credit carryforwards. Deferred tax assets and liabilities are measured using enacted tax rates expected to apply to taxable

income in the years in which those temporary differences are expected to be recovered or settled. The effect on deferred tax assets

and liabilities of a change in tax rates is recognized in operations in the period that includes the enactment date. A valuation allowance

is required to the extent any deferred tax assets may not be realizable.

ASC Topic 740, Income Taxes, (“ASC 740”),

also clarifies the accounting for uncertainty in income taxes recognized in an enterprise’s financial statements and prescribes

a recognition threshold and measurement process for financial statement recognition and measurement of a tax position taken or expected

to be taken in a tax return. For those benefits to be recognized, a tax position must be more likely than not to be sustained upon examination

by taxing authorities. ASC 740 also provides guidance on derecognition, classification, interest, and penalties, accounting in interim

periods, disclosure, and transition. Based on the Company’s evaluation, it has been concluded that there are no significant uncertain

tax positions requiring recognition in the Company’s financial statements. The Company believes that its income tax positions and

deductions would be sustained at the audit and does not anticipate any adjustments that would result in material changes to its financial

position.

Earnings Per Share

The Company uses ASC 260, “Earnings

Per Share” for calculating the basic and diluted earnings (loss) per share. The Company computes basic earnings (loss) per share

by dividing net income (loss) by the weighted average number of common shares outstanding. Diluted earnings (loss) per share is computed

based on the weighted average number of shares of common stock plus the effect of warrants potential common shares outstanding during

the period using the treasury stock method. Dilutive potential common shares include outstanding stock options and warrants and stock

awards. For periods with a net loss, basic and diluted loss per share is the same, in that any potential common stock equivalents would

have the effect of being anti-dilutive in the computation of net loss per share.

The following table sets forth the computation

of basic and diluted earnings (loss) per share for the years ended December 31,:

| Numerator | |

2023 | | |

2022 | |

| Net (loss) income | |

$ | (28,599,000 | ) | |

$ | 3,536,000 | |

| Effect of dilutive instruments | |

| - | | |

| - | |

| Numerator for diluted EPS | |

| (28,599,000 | ) | |

| 3,536,000 | |

| | |

| | | |

| | |

| Denominator | |

| | | |

| | |

| Denominator – for basic EPS | |

| 24,964,486 | | |

| 24,872,847 | |

| | |

| | | |

| | |

| Effect of dilutive instruments | |

| | | |

| | |

| Series Seed preferred stock | |

| - | | |

| 8,845,171 | |

| Series Seed II preferred stock | |

| - | | |

| 460,855 | |

| Warrants to purchase common stock | |

| - | | |

| 1,844,314 | |

| Dilutive potential common shares | |

| - | | |

| 11,150,340 | |

| | |

| | | |

| | |

| Denominator for diluted EPS | |

| 24,964,486 | | |

| 36,023,187 | |

Securities that could potentially dilute loss per share in the future

were not included in the computation of diluted loss per share for the year ended December 31, 2023 because their inclusion would be anti-dilutive.

Common stock equivalents amounted to 11,150,807 for the year ended December 31, 2023.

Recent Accounting Pronouncements

The Company’s management reviewed all recently

issued accounting standard updates (“ASU’s”) not yet adopted by the Company and does not believe the future adoptions

of any such ASU’s may be expected to cause a material impact on the Company’s consolidated financial condition or the results

of its operations, except for the following.

On December 13, 2023, the FASB issued ASU No. 2023-08, Intangibles

- Goodwill and Other - Crypto Assets (Topic 350-60): Accounting for and Disclosure of Crypto Assets. ASU 2023-08 requires entities to

measure crypto assets that meet specific criteria at fair value with changes recognized in net income each reporting period. Additionally,

ASU 2023-08 requires an entity to present crypto assets measured at fair value separately from other intangible assets in the balance

sheets and record changes from remeasurement of crypto assets separately from changes in the carrying amounts of other intangible assets

in the income statement. The new standard is effective for the Company for its fiscal year beginning January 1, 2025, with early adoption

permitted. The Company is currently evaluating the impact of adopting the standard.

On December 14, 2023, the Financial Accounting Standards Board (“FASB”)

issued Accounting Standards Update (“ASU”) No. 2023-09, Income Taxes (Topic 740): Improvements to Income Tax Disclosures.

ASU 2023-09 requires entities to disclose specific rate reconciliations, amount of income taxes separated by federal and individual jurisdiction,

and the amount of income (loss) from continuing operations before income tax expense (benefit) disaggregated between federal, state, and

foreign. The new standard is effective for the Company for its fiscal year beginning January 1, 2025, with early adoption permitted. The

Company is currently evaluating the impact of adopting the standard.

NOTE 2 — DIGITAL ASSETS

The following table summarizes the digital currency

(Bitcoins) transactions for:

| | |

December 31,

2023 | | |

December 31,

2022 | |

| Digital assets beginning balance | |

$ | 6,746,000 | | |

$ | 6,000 | |

| Revenue recognized from mined digital assets | |

| 21,052,000 | | |

| 21,362,000 | |

| Revenue share from Sphere 3D | |

| 321,000 | | |

| 618,000 | |

| Cost of digital assets sold for cash | |

| (17,977,000 | ) | |

| (30,270,000 | ) |

| Cost of digital assets transferred for noncash expenditures | |

| (7,770,000 | ) | |

| (3,978,000 | ) |

| Reversal of receivables from BitGo | |

| - | | |

| 120,000 | |

| Impairment loss on digital assets | |

| (275,000 | ) | |

| (8,704,000 | ) |

| Digital asset loan from Anchorage | |

| - | | |

| 27,592,000 | |

| Digital assets ending balance | |

$ | 2,097,000 | | |

$ | 6,746,000 | |

During the year then ended December 31, 2023,

the Company realized gains amounting to $535,000, related to the sale of digital assets for cash. Also, during the year then ended December

31, 2023, the Company realized gains amounting to $3,899,000 from use of digital assets.

During the year then ended December 31, 2022,

the Company realized gains amounting to $609,000, related to the disposal of its digital assets.

The table below shows the costs of the digital

assets transferred for payment of expenses for the year then ended December 31:

| | |

2023 | | |

2022 | |

| Payment for principal and interest | |

$ | 7,770,000 | | |

$ | 3,440,000 | |

| Payment for mining equipment | |

| - | | |

| 538,000 | |

NOTE 3 — MARKETABLE SECURITIES

In accordance with the Amended Merger Agreement,

the Company received 850,000 shares of Sphere 3D’s restricted common stock that are held in a third-party escrow account

upon providing written notice of the merger termination.

On April 4, 2022, the Company and Sphere

3D mutually agreed to terminate their Merger Agreement announced on June 3, 2021, and as amended on December 29, 2021, due to

changing market conditions, the passage of time, and the relative financial positions of the companies, among other factors.

According to the terms, the Company has received

850,000 shares of Sphere 3D.

On June 29, 2023, Sphere 3D had a 1:7 reverse

stock split. Shares were reduced from 850,000 to 121,428.

The shares are accounted for in accordance with

ASC 320 — Investments — Debt and Equity Securities; as such, the shares will be classified as available-for-sale securities

and will be measured at each reporting period at fair value with the unrealized gain or (loss) as a component of other income (expense).

The table below summarizes the movement in this

account for the periods:

| | |

December 31,

2023 | | |

December 31,

2022 | |

| Fair value beginning of period | |

$ | 235,000 | | |

$ | 1,734,000 | |

| Change in fair value | |

| 168,000 | | |

| (1,499,000 | ) |

| Fair value end of period | |

$ | 403,000 | | |

$ | 235,000 | |

NOTE 4 — DEPOSITS

The deposits are summarized as follows:

| | |

As of

December

31,

2023 | | |

As of

December 31,

2022 | |

| Beginning Balance | |

$ | 60,000 | | |

$ | 16,365,000 | |

| Cash deposit | |

| - | | |

| 8,150,000 | |

| Deposit paid | |

| 360,000 | | |

| - | |

| Delivered mining equipment | |

| - | | |

| (24,355,000 | ) |

| Converted carbon credit | |

| - | | |

| (100,000 | ) |

| Ending Balance | |

$ | 420,000 | | |

$ | 60,000 | |

In 2021, the Company entered into a purchase agreement

with Bitmain to acquire a total of 7,200 miners, to be shipped and delivered during 2021 and 2022. As of December 31, 2022, the Company

received 7,130 miners and the contract was deemed to be completed by the Company.

In 2022, the Company had a $60,000 refundable

deposit to Coinmint.

As of December 31, 2023, the Company had a $420,000

refundable deposit paid to Coinmint.

NOTE 5 — MINING EQUIPMENT, NET

Mining equipment consisted of 8,532, of which

229 were placed into service after December 31, 2023, and 7,410 units of bitcoin mining machines as of December 31, 2022, respectively.

The following table summarizes the carrying amount of the Company’s mining equipment:

| | |

As of

December

31,

2023 | | |

As of

December 31,

2022 | |

| Mining equipment | |

| | |

| |

| Balance, beginning of year | |

$ | 47,599,000 | | |

$ | 21,844,000 | |

| Additions | |

| 1,894,000 | | |

| 25,755,000 | |

| Disposals | |

| (105,000 | ) | |

| - | |

| Impairment | |

| (8,335,000 | ) | |

| - | |

| Revaluation from impairment | |

| (25,075,000 | ) | |

| - | |

| Ending balance | |

$ | 15,978,000 | | |

$ | 47,599,000 | |

| | |

| | | |

| | |

| Accumulated depreciation | |

| | | |

| | |

| Balance, beginning of year | |

$ | 13,231,000 | | |

$ | 695,000 | |

| Additions | |

| 14,958,000 | | |

| 12,536,000 | |

| Disposals | |

| (51,000 | ) | |

| - | |

| Revaluation from impairment | |

| (25,076,000 | ) | |

| - | |

| Ending balance | |

$ | 3,062,000 | | |

$ | 13,231,000 | |

| Net carrying amount | |

$ | 12,916,000 | | |

$ | 34,368,000 | |

During the year ended December 31, 2023, the Company

retired 18 miners of bitcoin mining machines. The cost of the fixed assets retired, and the corresponding accumulated depreciation amounted

to $105,000 and $50,000, respectively, for a loss on disposition of approximately $54,000. A total of 323 units amounting to $498,000

have been acquired but not yet received as of December 31, 2023.

Due to the significant decrease in fair values

of bitcoin mining machines as of December 31, 2023, the Company assessed the need for an impairment write-down of mining equipment (held

as fixed assets). In accordance with ASC 360-10, the Company determined that the fixed asset category had carrying values in excess of

fair value, and accordingly, the Company recognized impairment charges for mining equipment of approximately $8,335,000.

NOTE 6 — ACCOUNTS PAYABLE AND ACCRUED

EXPENSES

The following table summarizes accounts payable

and accrued expenses:

| | |

As of

December

31,

2023 | | |

As of

December 31,

2022 | |

| Accounts payable | |

$ | 2,234,000 | | |

$ | 113,000 | |

| Accrued expenses | |

| 1,415,000 | | |

| 2,880,000 | |

| Total | |

$ | 3,649,000 | | |

$ | 2,993,000 | |

NOTE 7 — NOTES PAYABLE

The following table summarizes the fair value

of the BTC Note, as of December 31,:

| | |

2023 | | |

2022 | |

| Beginning Balance | |

$ | 12,636,000 | | |

$ | - | |

| Additions | |

| - | | |

| 27,592,000 | |

| Payment | |

| (6,105,000 | ) | |

| (2,997,000 | ) |

| Amended principal payment | |

| (4,856,000 | ) | |

| | |

| Adjustment to fair value | |

| 13,193,000 | | |

| (11,690,000 | ) |

| Realized Gain (GOI) | |

| - | | |

| (269,000 | ) |

| Ending balance | |

$ | 14,868,000 | | |

$ | 12,636,000 | |

| Less – current portion | |

| 14,868,000 | | |

| 9,126,000 | |

| Ending balance – noncurrent portion | |

$ | - | | |

$ | 3,510,000 | |

On May 25, 2022, GOI (the “Borrower”)

entered into an Equipment Loan and Security Agreement (the “BTC Note”) with a lender amounting to 933.333333 Bitcoin (“BTC”)

at an annual interest rate of 5%.