UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

(Mark One)

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended

OR

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE TRANSITION PERIOD FROM TO |

Commission File Number

(Exact Name of Registrant as Specified in its Charter)

(State or Other Jurisdiction of Incorporation or Organization) |

(I.R.S. Employer Identification No.) |

(Address of Principal Executive Offices) |

(Zip Code) |

Registrant’s telephone number, including area code: (

Securities registered pursuant to Section 12(b) of the Act:

Title of each class |

|

Trading Symbol(s) |

|

Name of each exchange on which registered |

N/A |

|

N/A |

|

N/A |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. YES ☐

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer |

|

☐ |

|

Accelerated filer |

|

☐ |

|

|

|

|

|||

|

☐ |

|

Smaller reporting company |

|

||

|

|

|

|

|

|

|

Emerging growth company |

|

|

|

|

|

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). YES ☐ NO

As of June 30, 2023, the last business day of the registrant’s most recently completed second fiscal quarter, the aggregate market value of the voting and non-voting common stock held by non-affiliates of the registrant, based on the closing sales price of $2.25 on the OTC Pink Sheet Market, was approximately $

As of March 28, 2024, there were

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive proxy statement relating to its annual meeting of stockholders to be held in 2024 (the “2024 Annual Meeting”), to be filed with the Securities and Exchange Commission (the “SEC”) within 120 days after the end of the fiscal year to which this Annual Report on Form 10-K relates, are incorporated herein by reference where indicated. Except with respect to information specifically incorporated by reference in this Annual Report on Form 10-K, such proxy statement is not deemed to be filed as part hereof.

Table of Contents

|

|

Page |

|

|

|

Item 1. |

5 |

|

Item 1A. |

25 |

|

Item 1B. |

54 |

|

Item 1C. |

54 |

|

Item 2. |

56 |

|

Item 3. |

57 |

|

Item 4. |

57 |

|

|

|

|

|

|

|

Item 5. |

58 |

|

Item 6. |

58 |

|

Item 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

59 |

Item 7A. |

74 |

|

Item 8. |

74 |

|

Item 9. |

Changes in and Disagreements With Accountants on Accounting and Financial Disclosure |

86 |

Item 9A. |

86 |

|

Item 9B. |

87 |

|

Item 9C. |

Disclosure Regarding Foreign Jurisdictions that Prevent Inspections |

87 |

|

|

|

|

|

|

Item 10. |

88 |

|

Item 11. |

88 |

|

Item 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

88 |

Item 13. |

Certain Relationships and Related Transactions, and Director Independence |

88 |

Item 14. |

88 |

|

|

|

|

|

|

|

Item 15. |

89 |

|

Item 16. |

92 |

|

|

|

|

i

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K, including information incorporated herein by reference, contains forward-looking statements within the meaning of Section 27A of the Securities Act and Section 21E of the Exchange Act that are not historical facts. This includes, without limitation, statements regarding our financial position, business strategy and management’s plans and objectives for future operations. These statements constitute projections, forecasts and forward-looking statements, and are not guarantees of performance. Such statements can be identified by the fact that they do not relate strictly to historical or current facts. When used in this Annual Report on Form 10-K, words such as “anticipate,” “believe,” “continue,” “could,” “estimate,” “expect,” “intend,” “may,” “might,” “plan,” “possible,” “potential,” “predict,” “project,” “should,” “strive,” “would” and similar expressions may identify forward-looking statements, but the absence of these words does not mean that a statement is not forward-looking. When we discuss our strategies or plans, we are making projections, forecasts or forward-looking statements. Such statements are based on the beliefs of, as well as assumptions made by and information currently available to, our management.

All forward-looking statements are subject to risks and uncertainties that may cause actual results to differ materially from those that we expect, including:

1

The forward-looking statements contained in this Annual Report on Form 10-K and in any document incorporated by reference are based on current expectations and beliefs, which we believe to be reasonable, concerning future developments and their potential effects on us. There can be no assurance that future developments affecting us will be those that we have anticipated. These forward-looking statements involve a number of risks, uncertainties (many of which are beyond our control) or other assumptions that may cause actual results or performance to be materially different from those expressed or implied by these forward-looking statements. These risks and uncertainties include, but are not limited to, those factors described in “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and in our consolidated financial statements and the related notes thereto included elsewhere in this Annual Report on Form 10-K. Should one or more of these risks or uncertainties materialize, or should any of our assumptions prove incorrect, actual results may vary in material respects from those projected in these forward-looking statements. We undertake no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws.

In addition, statements that include phrases such as “we believe” and similar phrases reflect our beliefs and opinions on the relevant subject. These statements are based upon information available to us as of the date of this Annual Report on Form 10-K, and while we believe such information forms a reasonable basis for these statements, such information may be limited or incomplete, and our statements should not be read to indicate that we have conducted an exhaustive inquiry into, or review of, all potentially available relevant information. These statements are inherently uncertain and investors are cautioned not to unduly rely upon these statements.

2

RISK FACTOR SUMMARY

Our business is subject to numerous risks. The summary below highlights some of the risks you should consider with respect to our business. Additional risks, beyond those summarized below or discussed in “Risk Factors,” may also adversely impact our business, financial condition and results of operation. You should review and consider carefully the risks and uncertainties described in more detail in the “Risk Factors,” which includes a more complete discussion of the risks summarized here.

Privacy and Cybersecurity Risks

Risks Related to Our Business and Industry

Technology and Intellectual Property Related Risks

Other Business Risks

3

Legal and Regulatory Risks

Risks Related to our Substantial Indebtedness

Risks Related to our Common Stock

Other Miscellaneous Risks

The foregoing summary is not complete and should be read together with the more detailed discussion of these risks and uncertainties in “Risk Factors,” together with all of the other information in this Annual Report on Form 10-K, including our consolidated financial statements and the related notes thereto.

4

PART I

Item 1. Business.

In this Annual Report on Form 10-K, unless otherwise specified or where the context requires otherwise, references to “we,” “our,” “us,” “KLD” and “the Company” (i) for the periods prior to the completion of the business combination between Pivotal Acquisition Corp. and LD Topco, Inc., which closed on December 19, 2019, refer to Pivotal Acquisition Corp., the special purpose acquisition company, and (ii) for the periods after completion of the business combination, to KLDiscovery Inc., the combined company, and its consolidated subsidiaries. References to and the descriptions of the business included in this Annual Report on Form 10-K refer, prior to the business combination, to the business of LD Topco, Inc., and after the business combination, to the business of KLDiscovery Inc. This Annual Report on Form 10-K also refers to our websites, but information contained on those sites is not part of this Annual Report on Form 10-K.

Mission

We solve complex legal, regulatory and data challenges for our clients around the world by leveraging our proprietary software and innovative technology-based solutions.

Our Company

The Company was incorporated by its founder, Pivotal Acquisition Holdings LLC, or Pivotal, under the name “Pivotal Acquisition Corp.” as a blank check company on August 2, 2018 under the laws of the State of Delaware for the purpose of entering into a merger, capital stock exchange, stock purchase, reorganization or similar business combination with one or more businesses or entities. On February 4, 2019, the Company consummated its initial public offering, or the IPO, of units, with each unit consisting of one share of Class A common stock and one redeemable warrant entitling the holder to purchase one share of Class A common stock at a price of $11.50 per share, or the Public Warrants. On December 19, 2019, pursuant to an Agreement and Plan of Reorganization, dated as of May 20, 2019, as amended, the Company and LD Topco, Inc., or LD Topco, consummated a business combination transaction, or the Business Combination, pursuant to which, among other things, a merger subsidiary was merged with and into LD Topco, with LD Topco surviving the merger as a wholly owned subsidiary of the Company. The Business Combination was accounted for as a reverse merger in accordance with generally accepted accounting principles in the United States, or U.S. GAAP. Under this method of accounting, Pivotal Acquisition Corp. was treated as the “acquired” company for financial reporting purposes.

Overview

We are a leading global provider of eDiscovery, information governance and data recovery solutions to corporations, law firms, insurance companies and individuals in 17 countries around the world. With our long- standing history and transformative acquisition in 2016 of Kroll Ontrack, a storied eDiscovery platform with history dating back to 1985, we have decades of experience designing, building, and developing innovative technology solutions that evolve with the needs of our clients. Our integrated, proprietary technology solutions enable clients to efficiently and accurately collect, process, transmit, review and recover complex and large-scale enterprise data. In conjunction with our proprietary technology, we provide immediate expert consultation and 24/7/365 support worldwide, empowering us to be a “first-call” partner for mission-critical, time-sensitive, and nuanced eDiscovery and data recovery challenges. We leverage our proprietary technology solutions and extensive industry expertise to provide a more reliable, secure and seamless experience for our clients when tackling “big data” volume, velocity, and veracity challenges.

5

A key example of our purpose-built innovation is Nebula, our flagship, end-to-end AI / ML powered solution that serves as a singular platform of engagement for legal and other types of data. We also offer clients the optionality they desire—KLDiscovery-developed or externally-developed software and cloud-based or a number of different on-premise data storage options. We processed 8,041 and 8,009 Legal Technology matters for the years ended December 31, 2023 and 2022 respectively, and currently average over 32,000 data recoveries annually from all types of storage media. We believe our scale, expertise, proprietary technology and optionality, and global presence uniquely positions us to be the go-to partner for our clients and solve the world’s largest and most complicated data challenges.

Since January 1, 2020, we have provided services to a highly diverse base of more than 6,100 Legal Technology clients. Our Legal Technology clients include both law firms and corporations serving many industry sectors including finance and banking, pharmaceutical and biotechnology, technology, insurance, and real estate. Our data recovery clients include corporations and individuals that need to recover and access data. Our loyal client base includes 96% of the highest-grossing law firms in the United States as ranked by American Lawyer, known as the Am Law 100, as well as 50% of Fortune 500 companies, as of December 31, 2023. We have longstanding relationships with many of our clients. For example, the average length of our relationships with our top 25 clients based on revenue for the year ended December 31, 2023 is approximately 14 years. We actively collect and review feedback from our clients to ensure we are investing in the features and services that address their ever-evolving needs. We believe our commitment to being a “first-call” provider for our clients’ largest and most complex cases has helped drive significant revenues from larger and more complex matters, with Legal Technology matters generating over $100,000 and $500,000 in revenue representing 79% and 52%, respectively, of our Legal Technology revenue during the year ended December 31, 2023.

The legal technology industry is fragmented and bifurcated into dozens of software providers, which concentrate on technology solutions, and service providers, which license software and focus on client support to assist with managing the third-party technology. Software providers have increasingly prioritized DIY solutions and generally lack full-service support to address complex data challenges, while service providers have relied on multiple, disparate third-party tools and systems that are limited in the client use cases they can address. We bridged this gap by establishing KLDiscovery as a leading legal technology provider with scale that merges state of the art proprietary software and white-glove services. This combination allows us to manage incidents from an organization’s smallest concerns to its most complex legal reviews, as well as time and strategically sensitive legal matters.

As the first provider to license Relativity, a ubiquitous document review tool, we set a new standard in eDiscovery workflow, being the first provider to reach over one million records on the platform. Since then, we have developed KLD AI and review automation proprietary tools to augment the Relativity offering. For those clients who may choose to use third-party tools like Relativity for data hosting, we complement and enhance their experience via our proprietary toolkit to maximize the hosting platform’s functionality.

In response to an increasing number of clients seeking an end-to-end, fully integrated offering, we launched our proprietary cloud-native Nebula ecosystem in 2018. Nebula is a differentiated, comprehensive platform that addresses the full lifecycle of the Electronic Discovery Reference Model, or EDRM. Nebula is designed for enterprise adoption and can be seamlessly applied to address a multitude of use cases for the global legal and corporate communities. Clients who utilize our all-in-one platform benefit from a scalable, singular repository for their legal workflow processes, while reducing costs, and reducing data security risks inherent when processing and transferring data across multiple disparate systems and service providers. Nebula also offers clients flexibility in data delivery methods; in the public cloud, in our secure data centers, behind the client’s firewall in an enterprise server-rack and at a client’s location via Nebula Portable, optionality no other provider’s proprietary platform can offer. Regardless of data storage location, clients can seamlessly manage their data through the integrated Nebula platform. Demonstrating Nebula’s potential, we have experienced strong growth in Nebula revenues. For the year ended December 31, 2023, Nebula revenue was $46.1 million, a 62.1% increase from the prior year. 2023 revenue includes, for the first time, Nebula processing services for non-Nebula hosted engagements ($14.2 million). Our diversified and deep-rooted client relationships provide a large and loyal user base to further accelerate the adoption and growth of Nebula.

6

As Nebula’s capabilities continue to offer additional upstream use cases beyond eDiscovery, our clients are able to leverage our technology throughout their respective eDiscovery lifecycles. For example, we offer clients Nebula Archive, which captures data across numerous platforms and provides a secure, searchable copy of data under preservation, as well as Nebula Legal Hold, which allows clients to ingest and manage hold data from any source. We believe the breadth of Nebula presents an attractive entry point for us to engage with clients early and bring them onto our platform.

Additionally, we are a global leader of data recovery services, currently averaging over 26,000 data recoveries annually from all types of storage media. With our in-lab, remote, and on-site capabilities, we recover data at an over 82% success rate from almost any device, storage manufacturer, operating system, database, and back up format. We expect to continue to benefit from our deep data recovery competencies, given the increasing relevance of data privacy and cybersecurity issues at the institutional, governmental, and international levels.

Our unique combination of proprietary software and technology-enabled services, coupled with our full stack, scalable platform that covers the full EDRM life cycle, best positions us to tackle our clients’ “big data” challenges. Moreover, we believe our proprietary Nebula offering, unlike other existing solutions, offers broad flexibility in deployment methods, cost efficiency with customizable pricing models, and optimized accuracy with its underlying AI / ML technology. We see further opportunity to grow our sales among new and existing clients, scale internationally, and extend our technology leadership.

Industry background

The rule of law is integral to society—it is the foundation for systems of justice, underpins government functions, and upholds fair economic transactions and social development. From multi-national corporations and governments to local businesses and individual citizens, millions rely on legal services to navigate complex matters and uphold the law in an ever-changing world. According to Statista, legal services represents one of the largest sectors in the global economy, with worldwide spend estimated to increase to $1 trillion in 2028. As technology continues to revolutionize the legal services industry, there is a significant existing market opportunity for legal technology solutions that should continue to grow.

While the legal technology industry is vast and diverse, most organizations in the industry fall into one of four categories:

7

Despite the clear distinctions among these categories, there is often overlap between their needs. Service providers commonly license and repackage technology with their services to law firms and corporations, who typically lack the full requisite of resources and domain expertise. Additionally, each organization has specific needs and requirements relating to where data can be hosted, ranging from entirely cloud to entirely behind their firewall, or somewhere in between. While each organization’s technology and service needs are unique, software providers can nevertheless market their solutions to all of those organizations, due to the overlap in needs.

These dynamics underscore the market potential for software providers and highlight the opportunity that exists today for a solution that has broad functionality, around-the-clock client service, and optionality in delivery vehicles to meet all of a buyer’s data needs.

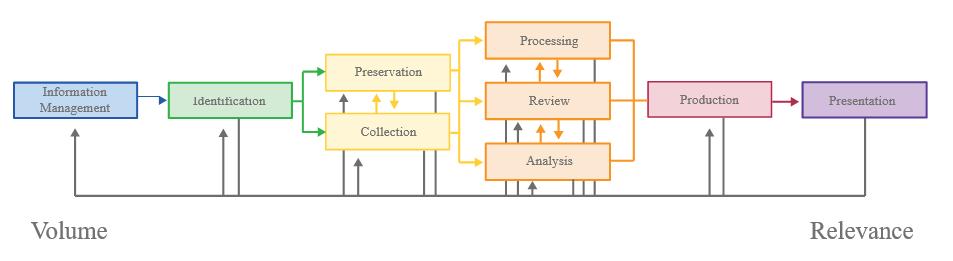

Electronic Discovery Reference Model (EDRM)

eDiscovery

eDiscovery is a critical component of the legal industry: parties preserve, collect, review, and exchange information electronically for the purpose of using it as evidence in a civil, criminal or investigative legal case or regulatory action. Electronically Stored Information or, ESI, in eDiscovery can range from simple data sources such as emails, word documents, and databases, to increasingly modern and complex data sources such as social media messages, cell phone data, and mobile applications, such as internal digital chat data, and audio / visual calls. The volume and complexity of eDiscovery varies significantly from case-to-case, ranging from small matters comprising little data to highly complex matters with vast amounts of enterprise data where support from technology and legal experts is essential. According to complexdiscovery.com, the worldwide eDiscovery software and services market is forecasted to grow from $15.1 billion in 2023 to $22.7 billion by 2028 due to the proliferation of data and legal challenges, thereby underscoring eDiscovery’s growing significance and use cases.

The eDiscovery market is highly fragmented, resulting in low penetration divided amongst many vendors. Further, within the eDiscovery industry, there is a significant disconnect between software providers and service providers. Most service providers of any scale have some proprietary technology, but very few have material portfolios and instead rely largely on licensing third party tools. These vendors lack fundamental control over the products they resell, which weakens the user experience and diminishes lifetime value.

Information governance

Information governance is a rapidly maturing discipline, the objective of which is to enable enterprises to manage their huge and growing data estates, taking into account the many demands placed upon that data. These demands include everything from ready access to data for business utility and continuity, to data protection against ransomware and other cyber-attacks, to complying with proliferating privacy and other regulatory requirements, to responding to regulatory investigations and civil litigation. Market research firm Radicati estimates the information governance market will grow to approximately $10.0 billion in 2025.

8

Vendors that offer versatile solutions can help minimize costly and duplicative workflows arising from using separate systems to address multiple needs. Information governance products also serve as attractive entry points for new eDiscovery business opportunities. We expect increases in legal and regulatory demands, and burgeoning data volumes, as well as strategic needs to protect data from cyber-attacks, to drive the growing adoption of information governance solutions.

Data recovery

Data recovery technology providers help clients, ranging from Fortune 500 companies to individual consumers, recover data that would otherwise be lost for a myriad of reasons, such as system failures, accidental deletion, physical damage, natural disasters, ransomware or user error. Data recovery companies use software tools and physical inspection to diagnose and determine the condition of the media and what data may be recovered. Then, they make an image of the data and perform a logical reconstruction of it. In the case of physical damage, large- scale facilities are required as the device may need to be disassembled in a clean room lab and spare parts used to facilitate the recovery. According to the Business Research Insights, the worldwide data protection market, which consists of data recovery, archives, and backup spending, is expected to grow to $15.3 billion in 2031.

Many of the vendors in this fragmented industry are small electronics repair shops using off-the-shelf data recovery software tools. Many smaller data recovery vendors can recover data from hard disk or external drives, while some have the capability to assist with more complex data recovery from servers, storage systems, and networks. Very few global data recovery providers support large-scale operations such as clean room labs and physical data recovery capabilities. Data recovery also complements eDiscovery and information governance by minimizing the amount of data that cannot be recovered from lost or deleted files.

Our solutions

We are a legal technology pioneer with a long-standing presence developing proprietary technology solutions. We provide an expansive suite of technology offerings including our end-to-end fully integrated solution, Nebula, which comprehensively addresses information governance, eDiscovery and data recovery needs. Our solutions have been developed in-house by capitalizing on our more than 15 years of technology expertise and legal process management experience. As the first provider to license Relativity, we have developed an entire suite of proprietary technology solutions that creates a bespoke and enhanced experience within the platform.

We introduced Nebula, our proprietary platform, in 2018 after years of learning from our many client relationships and the engagements on which we support them. Our vast experience taught us that our clients needed one comprehensive and integrated platform that can be used to complete all steps of the information governance and EDRM process, and we believe Nebula fills this critical need. Complemented by our world-class client service, Nebula empowers our clients with flexible, scalable, and innovative tools. As a result, unlike other providers who cannot update the third-party software they sell in real-time or technology companies who are unable to provide after-sale support, we fully control our proprietary technology—along with the user experience—enabling us to serve as a unified one-stop shop.

KLDiscovery value proposition

Highly differentiated combination of proprietary software and human capital

We believe our position as the differentiated legal technology provider with proprietary, state of the art, EDRM software combined with our white-glove services will help drive retention and support client growth. We have spent over 15 years investing in, delivering, and perfecting data-centric technology, including our flagship eDiscovery solution, Nebula. At the same time, we built a successful track record of solving some of the most challenging legal data problems through a combination of our proprietary technology and service-oriented culture. As the relationship between software and service providers shifts within the legal industry, we are well- positioned to disrupt the space as a singular, end-to-end and trusted provider of both software and services.

9

Full stack, scalable technology offerings covering the full spectrum of the EDRM

Through our proprietary technology offerings, we provide full stack, scalable AI-powered software solutions for corporate legal functions allowing clients to collect, process, transmit, store, analyze, and govern all of their data on a single platform in a timely and efficient manner. Nebula, our singular, end-to-end platform, allows us to provide a superior level of client service and minimize the risk of a data breach. Our solutions are designed for enterprise adoption and can be applied to a wide variety of enterprise use cases outside of litigation such as internal investigations, merger clearance, and legal holds.

Nebula is a highly differentiated and comprehensive technology platform

Our proprietary platform, Nebula, addresses virtually all potential eDiscovery and information governance use cases for the global legal and corporate communities. This end-to-end platform allows our clients to contract with a single solution provider and provides one, instantly scalable, secure repository for their legal data that avoids error-prone processes of moving data through different disparate systems. Our platform enables greater efficiency and optionality by offering our clients control over the location of their data and method of delivery. Regardless of data storage location or size, clients can seamlessly manage their data through the integrated Nebula platform with consistent user experience, performance, and features. In addition, Nebula, with its single- source platform and simple usage-based pricing model, addresses virtually all use cases, thus allowing our users to benefit from greater cost predictability and improved efficiency. With existing software solutions limited by any combination of expensive pricing models, limited features, and a lack of delivery options, we believe there is an underserved population of buyers, including eDiscovery service providers, law firms, corporations, and other organizations, that can immediately benefit from Nebula. By supporting a variety of deployment environments with increased cost-efficiency, we believe Nebula is the premier, unified solution that meets and will evolve with the needs of our clients.

State of the art AI / ML functionality

Our leading-edge AI / ML technology allows clients to review their legal data accurately and quickly. We have a strong, decades-long track record of developing award-winning workflow batching software, predictive coding, and AI / ML programs that maximize the efficiency and productivity of lawyers around the world. Developed through continuous use and refinement, our legal review technology has predictive capabilities that we believe are superior to our competitors, giving us an advantage as our clients use our solutions.

Simplified and flexible pricing to provide end-to-end optimization

Our pricing model, customized based on platform functionality and data volume, allows us to offer a wide variety of optionality for our clients. We employ different pricing structures across our large suite of offerings including usage-based subscriptions, transactional, à la carte, and alternative fee arrangements for software such as our proprietary Nebula platform and our technology-enabled services and data recovery engagements. We set transparent and attractive pricing, which allows us to deepen our relationships with our large, blue-chip client base. We believe the ease of our pricing structure and solutions, even for the largest and most complex organizations, provides critical entry points for us to onboard additional products and expand beyond traditional use cases. As the strategic value of our technology solutions continues to grow, our pricing strategy will attract both existing and new clients deeper into our ecosystem.

Our business model

We offer differentiated solutions to our clients via a flexible and scalable, usage-based business model, where, as an example, clients pay us on the basis of the amount of data processed, ingested, and/or reviewed on our platform, which drives future business opportunities. Our proprietary data and technology fuels referrals from our large global client base. As more clients begin to use our software and solutions, we have opportunities to cross- and up-sell to drive growth of our complementary features and add-ons. By continuously expanding our usage, we increase our global reach and create more value for clients and stakeholders.

10

For the years ended December 31, 2023 and 2022, revenues arising from usage-based agreements comprised 89.8% and 89.9% of revenue, respectively, while revenues arising from subscription agreements comprised 10.2% and 10.1% of revenue, respectively.

Our clients

Our Legal Technology clients include both law firms and corporations serving many industry sectors including finance and banking, pharmaceutical and biotechnology, technology, insurance, and real estate. Our data recovery clients include corporations and individuals that need to recover and access data.

Our definition of a Legal Technology client includes each primary law firm and corporation to which we provided services in a litigation matter that we billed during the past two years. Since January 1, 2020, we provided services to more than 6,100 Legal Technology clients. As of December 31, 2023, our clients include 96% of the Am Law 100 and 50% of Fortune 500 companies.

We have longstanding relationships with our clients; the average length of our client relationship with the top 25 clients for the year ended December 31, 2023 is 14 years. As of and for the year ended December 31, 2023, we did not have any single customer that represented more than five percent (5%) or more of our consolidated revenues or accounts receivable and, as of and for the year ended December 31, 2022 we had one single customer that represented approximately six percent (6%) of our consolidated revenues and one single customer that represented approximately six percent (6%) of our consolidated accounts receivable.

Our key differentiators

A trusted partner for the most complex, mission critical legal matters and data needs

Through our decades of experience, we have built a reputation of technological excellence and “first-call” expertise for the most complex legal and data challenges worldwide. Our proven ability to perform the most difficult legal data reviews (such as antitrust second requests, joint defense, and large-scale M&A matters) and help our clients through their most challenging moments (such as mitigating and navigating a ransomware event) has made us a critical partner for our clients. Our proprietary technology capabilities and ability to evolve with the needs of our clients results in better outcomes for their organizations. By building a reputation as a trusted legal solution provider, we have created a loyal client base that will allow us to drive future business opportunities and expand the reach of our offerings including Nebula. Our comprehensive offerings distinctly position us to navigate our dedicated client base through the technological transformation of the legal industry while serving as a critical partner for all their legal technology needs.

11

Comprehensive technology solutions that expand beyond traditional eDiscovery use cases

As Nebula continues to expand further upstream within the EDRM, our technology is leveraged earlier in the data lifecycle, opening an attractive entry point for engaging our clients and moving them along the eDiscovery journey within our end-to-end Nebula platform. We believe our position as a one-stop platform that offers comprehensive solutions allows clients to contract with a single provider, avoiding frictions and risks in moving data and contracting multiple providers. Additionally, we are a global leader of data recovery services, supporting both small businesses and large enterprises with business server recoveries and backup tape restorations. Our proprietary incident response solutions enable our clients to recover from the deletion or destruction of data due to malicious or accidental incidents. The rapid proliferation of ransomware episodes faced by organizations worldwide validates the value of data today and how critical it is to retrieve.

Founder led, proven and experienced management team

Chris Weiler, our Chief Executive Officer, co-founded our Company in 2005 with a mission to support clients through their most complex and stressful legal and data challenges. As one of the longest-tenured CEOs in the global eDiscovery sector, he provides extensive industry expertise and relationships. Moreover we have a deep team of seasoned executives, including Dawn Wilson (Chief Financial Officer) and Danny Zambito (Chief Operating Officer), Daniel Balthaser (EVP of Engineering), Robert Hunter (EVP of Global IT and eDiscovery Operations), Krystina Jones (Chief Revenue Officer), Anthony DeJohn (EVP of Product, Design, and Data Science), Oscar Vega (EVP of Global Sales and Marketing), Andy Southam (General Counsel), Lindsey Hammond (SVP of Global Talent), and Dan Clarkin (SVP of Global Managed Review Services) who have collectively spent over 185 years in the legal and technology industries. Furthermore, our sales and software development executives have worked together over the past 15+ years and developed a seamless feedback loop to improve our technology in response to the changing needs of our clients. Together, our experienced and passionate team is committed to delivering best-in-class solutions and a superior user experience to our clients worldwide.

Expansive global footprint

Our geographic presence spans 26 locations in 17 countries. Our broad reach provides us with the ability to act as a first responder when clients have urgent work requiring immediate attention. In addition, our familiarity with local laws and regulations allows us to effectively assist clients in navigating complex, cross-border situations.

Highly qualified and experienced sales force

Our sales management team recruits and retains highly qualified and experienced sales team members, focusing on expertise, knowledge and tenure, prioritizing the quality of team members over the quantity. Our top 15 sales team professionals by revenue average 16 plus years of experience in the eDiscovery industry and averaged more than $16.8 million in revenue per person for the year ended December 31, 2023, while our entire sales organization had a revenue per person average of over $5.3 million for the same period. We rely on a team of value-add sales professionals to act as consultants for their clients across a wide array of offerings. In 2020, we effectively integrated our data recovery and legal technology sales teams to better offer the full KLDiscovery portfolio of technology and solutions to a wider base of existing clients.

Our growth strategy

Building on the many strengths of our existing business and strategy, we are focused on continuing to enhance our proprietary solutions, expand our ecosystem, and extend our reach to capitalize on our large and growing market opportunity.

12

13

Our products and technology

We have developed an array of integrated technologies and offerings that allows us to provide exceptional value to our clients.

eDiscovery

Nebula

Nebula epitomizes the modern, cloud-native application boasting the latest in AI / ML. Our award-winning software development and data science teams have incorporated best-of-breed technologies ranging from our own patented AI / ML technology to cutting-edge public cloud machine learning suites throughout Nebula to enhance efficiencies, streamline user experiences, and drive results.

Nebula can be delivered across numerous delivery vehicles, allowing the technology to be viable for virtually any use-case.

As with all Nebula deployments, security and compliance are top requirements. Microsoft Azure supports compliance with a broad set of industry-specific laws and meets comprehensive international standards. For example, Azure has ISO 27001, ISO 27017, ISO 27018, ISO 22301, ISO 9001 certifications, PCI DSS Level 1 validation, SOC 1 Type 2 and SOC 2 Type 2 attestations, HIPAA Business Associate Agreement, and HITRUST certification. Operated and maintained globally, Microsoft Azure is regularly and independently verified for compliance with industry and international standards and provides clients the foundation to achieve compliance for their applications.

14

Nebula includes an array of tools and features including:

Nebula Archive

Nebula Archive provides a critical foundation to any information governance program. It captures data as it is created in dozens of platforms, such as Office 365, Slack, Box, and more. It provides the means to effectively

15

classify and manage that data over the course of its lifecycle, including reliably preserving data subject to legal hold. It offers excellent data assurance against loss or alteration via a separate, secure copy of critical business data. It also enhances data with the ability to search and effectively retrieve targeted results, even from petabytes of source data. Lastly, it reliably and defensibly disposes of data no longer required to be retained for any business or regulatory compliance purpose.

Nebula Archive provides an alternative and/or enhancement to traditional backup solutions, particularly in the cloud era when many SaaS productivity platforms lack effective recovery means in response to inadvertent data loss, alteration, or ransomware attacks. Nebula Archive offers a platform that is designed to satisfy strict retention and data assurance regulations, such as those of FINRA and the SEC governing broker-dealer communications. In addition, it is the foundation of a cost-effective eDiscovery strategy, permitting what we believe is unprecedented insight into data very early in a case and a highly effective means of selecting the most relevant data for quick and easy promotion within the Nebula platform.

KLD AI and review automation

To support our review platforms, we offer cutting-edge tools for our users that enhances productivity and efficiency for eDiscovery.

Nebula’s entity extraction engine is trained to recognize eight distinct categories of real-world entities, then visually cluster documents referencing the same entities. This approach, based on semantic understanding rather than simple word frequency, provides enhanced insight into the data, allowing users to isolate and retrieve relevant information or filter non-relevant material quickly. Nebula can also uncover topics that might otherwise go unnoticed, giving legal teams an advantage.

Nebula’s sentiment analysis tools analyze tone at both the document and sentence levels. At its core, sentiment analysis applies Natural Language Processing techniques and computational linguistics to derive emotional attributes from text content. By leveraging sentiment analysis, users can better understand how communications are perceived and help discern the author’s tone and intent. This

16

gives Nebula users an edge in contexts where more than just the words themselves matter, as in, for example, matters related to workplace harassment. Companies can use this feature to learn the tone of their employees to help determine if communications are positive, negative, or neutral, and help understand the behaviors and communication styles of employees and clients to identify trends and identify bad actors.

Processing

Our proprietary technology is purpose-built to address large and complex matters as easily and efficiently as it does the small and simple ones. With full integration in the Nebula ecosystem, our Processing technology allows us to address diverse needs on a massive, global scale.

We believe Nebula Processing allows us to process data with a higher degree of quality and, due to the lack of third-party licensing costs, at a lower cost point, as compared to providers relying exclusively on licensed technology. For organizations licensing Nebula for their eDiscovery needs—providers, law firms, and corporations alike—they reap the benefits of a mature processing technology that can not only be used at any scale and for any data set, but is also fully integrated and does not require any of the wrappers or clunky export/ import processes that come with licensing disparate third-party solutions.

Professional services

Leveraging our industry expertise and focus on delivering differentiated user experience, we complement our offerings with a suite of technology-enabled services.

Client Portal

The Client Portal is a secure, web-based platform offered by KLDiscovery that provides clients with access to their data and case information. It offers real-time visibility and updates on project status, as well as the ability to collaborate and share information with other stakeholders. The Client Portal is designed to streamline communication and increase efficiency throughout the discovery process. With its user-friendly interface and robust security features, the Client Portal is a valuable tool for organizations in need of a centralized platform for managing their discovery and litigation support needs.

17

Data recovery

Ontrack EasyRecovery

Developed through our partnership with one of the world’s leading data recovery software manufacturers, Ontrack EasyRecovery allows clients to perform precise file recovery of data lost through deletion, reformatting, and a number of other data loss scenarios. The product recovers data from solid-state drives and conventional hard drives, memory cards, USB hard drives, flash drives, and optical media. The product functions on both Windows and Mac operating systems and comes in several different versions, covering needs ranging from a small, one-time recovery to the most complex projects. There is a “free” version that is capable of recovering up to 1 GB of data, a “Home” version for straightforward recoveries, a “Professional” version suitable for small to medium businesses, and a “Technician” version that includes the tools needed to successfully perform data recoveries on all types of computer storage devices and rebuild broken RAID volumes.

Ontrack PowerControls

We believe Ontrack PowerControls is a market leading granular restore software product, developed from Ontrack’s expertise in data recovery. Ontrack PowerControls is used to find and export email, SharePoint items and structured query language tables for eDiscovery, litigation, investigations, compliance, selective migration, develop and test, and general restore use cases for IT.

We believe Ontrack PowerControls provides a more powerful and faster search tool than native tools, and, most importantly for legal and compliance use cases, it does not alter the metadata, making it forensically sound. Most enterprise backup platforms do not have granular restore capabilities, so they collaborate with Ontrack and integrate Ontrack PowerControls with their products.

We are currently licensing Ontrack PowerControls globally to more than 200 organizations, and to over 800 channel partners for distribution to their customers.

Ransomware recovery

Ransomware is a form of malicious software designed to block access to a computer system or certain data or publishes a victim’s data online. The attacker demands a ransom from the victim, promising—not always truthfully—to restore access to the data upon payment. When organizations are struck with ransomware, and crucial data cannot be accessed, it can be an extremely stressful time for all involved. Getting access to that critical data as quickly as possible is vital to ensure downtime is minimized and the organization can get back to normal.

The last decade has seen an increase of various ransomware Trojans surface, but the real opportunity for attackers has increased since the introduction of Bitcoin. This and other cryptocurrencies allow attackers to easily collect money from their victims without going through traditional channels.

No vertical is safe from the effects of ransomware. Unfortunately, some are more susceptible to successful attacks than others. There are various reasons for this: the technology they deploy, the security they have in place; identity governance and privilege maturity, and their overall cybersecurity protocols. And human error will always pose its own risks.

We track over 375 different types of ransomware, a population that is always evolving and growing. Ransomware changes and develops all of the time, so we want to make sure we are watching and studying the latest changes and advancements. Studying ransomware and its ever-changing forms provides additional knowledge and experience, leading to a higher probability that we will recover data that has been lost as a result of an attack.

Email extraction

We offer professional email recovery solutions for consumers and businesses alike. From individual files to entire databases, we maintain the expertise and technology to support practically any use case. The success of email recovery depends on where the email is stored. Email software, such as Microsoft Outlook, commonly stores email

18

on hardware like a laptop, desktop, mobile phone, tablet, or server. We can easily recover email from both functioning and non-functioning hardware. Additionally, our recovery engineers are experienced in recovering enterprise email no matter how it is stored on a client’s server, whether it is inside a database, a Microsoft Exchange Information Store or individual messages in separate files, such as .pst containers.

Tape Solutions

We provide a range of tape services to solve the problems associated with legacy backup tapes and regularly support our clients to solve the following challenges:

Data destruction solutions

Permanently deleting data is not as straightforward as pressing the delete button—it takes time and proper resources. Data that is not completely expunged before the media is disposed of is vulnerable to exposure. To increase the security of data, a secure, verified data destruction process is required. Based on their knowledge, our data experts seek to select and execute the most appropriate data destruction method for the client’s media. Once the data has been destroyed, we provide a certificate of destruction and disposal.

We support our clients throughout the whole data destruction process by offering data destruction solutions in our labs or onsite using Blancco Erasure Software, Ontrack Proprietary tools, or our Ontrack Degausser. For clients who want to handle the data destruction process themselves, we sell the Blancco solution and the Ontrack Degausser products to the client and advise them how to best use them.

Sales

We operate with a global sales team that was integrated in 2020 across our offerings to address the specialized needs of our client base and cultivate strategic partnerships with key clients in our industry. As of December 31, 2023, our sales organization comprised of 58 professionals and is led by our sales executives and regional managers. Our business development managers have developed “first-call” relationships with several of our largest clients while providing significant expertise in the technical nature of the services.

Our global sales structure is tailored to deliver quick responses on pricing, account ownership requests, and general assistance with client requests and training. This structure is built on our foundational values of teamwork and responsiveness. Our global sales force pursues opportunities in a wide range of geographies and is not confined by the traditional territorial structure that competitors offer. This allows us to maximize relationships and revenue.

Sales leadership encourages representatives around the world to collaborate. A global sales strategy initiative has been implemented to facilitate communication between teams on shared major accounts, which includes the coordination of regular calls and information sharing on key accounts. Most law firms have multiple buyers, and this model maximizes our ability to increase penetration.

Sales executives are encouraged to act as their own entrepreneurs, backed by the support of seasoned sales leadership and a global sales operations team. The sales operations team assists the sales team with all client requests including conflict checks, Salesforce data entry, estimate creation, and generation of client agreements and work orders. This global support team allows the sales representatives to focus on what they do best— generating new business and maintaining existing client relationships. Our global sales structure and sales operations teams

19

deliver quick responses to representatives and clients, flexible pricing models, and simplified matter initiation, giving us a competitive advantage in a fast-paced industry.

Marketing

We focus on connecting with our clients through our marketing team. Our marketing campaigns are developed internally and are focused on our mantra, the “KLD Difference. One KLD.” and our “Proprietary Powerhouse” technology. We advertise in a wide variety of trade publications and at sports and entertainment events. We also sponsor a variety of events, seminars, and conferences around the world. We operate 38 global websites, which highlight our leadership, products, services, technology, industry experience, press clippings, and our community contributions. Holding true to our values, we are heavily focused on charitable donations and community work, which are highlighted on our “KLD Community” website page. We also have several video advertising campaigns which are shared via YouTube, Twitter, and LinkedIn. Additionally, we own the “ediscovery.com” domain and believe that a continued emphasis on strategic digital marketing and search engine optimization helps KLDiscovery capture significant internet search results on eDiscovery.

Research and Development

Our research and development organization is responsible for the design, development, testing, and scaling of our proprietary technology infrastructure. We believe that our continued investment in research and development, including hiring top engineering talent, is critical for us to provide a leading and differentiated ecosystem that can tackle the industry’s most complex data problems. Additionally, our application development process is informed by the continuous feedback we receive from our own service providers, as well as long-term clients who are looking for a better and more secure solution.

Our research and development team is based across the United States and European Union, primarily in Minnesota and Poland, with an expanding presence in Greece. As of December 31, 2023, we had 178 employees in our research and development department.

Our competition

We believe the eDiscovery and information governance market is bifurcated, highly fragmented, competitive, and evolving. We encounter competition from different software and service providers with various business model and product offerings that overlap with parts of our solutions, including:

We believe the principal competitive factors in this industry include:

20

There are many small regional eDiscovery providers which may have a few captive relationships but lack the resources or scale to compete for meaningful work. Likewise, most of the global and national providers lack a comprehensive proprietary platform to complement their scale and resources. We believe we are distinctly positioned with an ideal complement of global reach, scale of resources, and proprietary technology to address almost any client need.

Additionally, we serve the data recovery market, which is highly fragmented and generally competitive. Clients choose vendors based on brand awareness and reputation, speed, price, and security. Our competitors in the data recovery market include Drivesavers, Gillware Data Recovery, Stellar Data Recovery, Disk Doctors, Digital Data Recovery DDC, and Myung Information Technologies.

We also compete in the legal hold market with companies such as Exterro, OpenText, ZApproved, and Zylab.

Intellectual property

We own a range of issued, registered and applied for intellectual property rights across the world, primarily trademarks and patents.

As of December 31, 2023, we owned 165 trademark registrations globally and had 29 trademark applications at various stages in the application process. Our material trademarks are either registered or are the subject of pending applications for registrations in the U.S. Patent and Trademark office and various non-U.S. jurisdictions (but with a focus on the European Union, the United Kingdom, Norway, Switzerland, Japan, Australia, China, Singapore and Hong Kong). We use “KLDiscovery”, “Ontrack”, and “Ibas” as our primary corporate trademarks. The trademark “KLDiscovery” has proceeded to registration in Australia, China, Brazil, the European Union, Hong Kong, Japan, India, Switzerland, and the United Kingdom. Additionally, we have applied to register “Nebula,” the brand name for our proprietary eDiscovery platform, in our key markets and, to date, applications have proceeded to registration in the United States, Japan, the European Union, United Kingdom, Hong Kong, Switzerland, and Brazil.

We previously used “Kroll Ontrack” and “KrolLDiscovery” subject to a license from Kroll, LLC. In October 2021, we executed an agreement with Kroll, LLC, which amended the existing trademark license agreement, and provided that our rights to use the Kroll Ontrack and KrolLDiscovery trade names expired in October 2023. Part of the terms of the amended trademark license was that the licensed marks be withdrawn and/or cancelled upon our instructions and Kroll, LLC be prevented from using and/or registering the same or similar marks. This agreement was a triggering event which resulted in an evaluation of impairment of our Kroll Ontrack and KrolLDiscovery tradenames capitalized as part of our 2016 Kroll Ontrack acquisition. See Note 1—Organization, business and summary of significant accounting policies to our audited consolidated financial statements.

21

We are the registered owner of 580 domain names including our key domains used to promote our activities, namely: kldiscovery.com, ontrack.com, compiled.com, and ibas.com (along with many local variants of these main domain names). We are also the registered owner of ediscovery.com, which we believe helps capture significant internet traffic. Information contained on these websites or linked therein or otherwise connected thereto does not constitute part of nor is it incorporated by reference into this Annual Report on Form 10-K, and the inclusion of these website addresses is an inactive textual reference only.

We own the copyright of many of our business software and tools as they have been created by employees in the course of their employment. These include the Nebula and EDR platforms, the PMDB Database (internal job tracking tool), Service Cloud (data recovery portal), PowerControls, and the various Relativity applications to enhance the license of standard Relativity platform services.

We have 18 patent registrations, including granted patents for our Nebula offering.

Human Capital Management

As of December 31, 2023, we had 2,687 employees. This total includes 1,382 regular employees and 1,305 temporary contingent employees who are employed on a project basis to work on active managed review matters. Our employees are not represented by a labor union, and we have not experienced any work stoppages. We believe employee relations are good.

The skills, experience, and industry knowledge of our employees significantly benefit our operations and performance. We continuously evaluate, modify, and enhance our internal processes and technologies to increase employee engagement, productivity, and efficiency.

We strive to hire employees who adhere to the following cultural values:

Annual employee training is used to reinforce these values across our global employee base. These trainings cover topics related to ethics, environment, health and safety, cyber-security, and emergency responses.

We believe that an inclusive culture where all employees feel valued and engaged makes KLDiscovery a desirable place to work, helps us to attract key talent and retain employees as they grow in their careers and fosters an environment that enhances each individual’s productivity and professional satisfaction. KLDiscovery has an Inclusion & Diversity program focused on commitment to inclusion and diversity through our Culture & Environment, Business & Technology, and Community & Partnerships. The program includes employee-led Business Resource Groups dedicated to promoting and integrating inclusion and diversity throughout the organization.

22

As of December 31, 2023, not including contingent employees who were employed temporarily to work on active managed review matters, our employees, including those employed by region, were located as follows:

Region |

Percentage |

North America |

59% |

Europe, Middle East, and Africa |

27% |

Asia Pacific |

14% |

In order to comply with local employee-related laws, we do not require our employees to disclose their race and ethnicity. As of December 31, 2023, based on self-reported information of approximately 58% of our U.S. based employees, and not including contingent employees who were employed temporarily to work on active managed review matters, our gender and ethnicity demographics were as follows:

Gender |

Employee Percentage |

Female |

34% |

Male |

66% |

|

|

Ethnicity |

Employee Percentage |

Asian |

8.5% |

Black / African American |

5.6% |

Hispanic / Latin |

7.8% |

Multiracial, Native American and Pacific Islander |

4.0% |

White |

74.1% |

Government regulation

Information on government regulation is discussed in Part I, Item 1A, “Risk Factors,” under the heading “Privacy and Cybersecurity Risks” and in Part 1, Item 1C, "Cybersecurity."

Corporate information

The mailing address of our principal executive office is 9023 Columbine Road, Eden Prairie, Minnesota 55347 and the telephone number is (703) 288-3380. Our website address is www.kldiscovery.com. Information contained on our website or linked therein or otherwise connected thereto does not constitute part of nor is it incorporated by reference into this Annual Report on Form 10-K.

Available Information

We file annual, quarterly and current reports, proxy statements and other information with the SEC. Our SEC filings are available to the public over the internet at the SEC’s website at www.sec.gov. Our SEC filings are also available free of charge on our website at www.kldiscovery.com as soon as reasonably practicable after they are filed with or furnished to the SEC. Our website and the information contained on, or that can be accessed through, our website is not incorporated into this Annual Report on Form 10-K.

Implications of being an emerging growth company and smaller reporting company

We are an “emerging growth company,” as defined under Section 2(a) of the Securities Act of 1933, as amended, or the Securities Act, as modified by the Jumpstart Our Business Startups Act of 2012, or the JOBS Act. As an emerging growth company, we are eligible to take advantage of certain exemptions from various reporting requirements that are applicable to other public companies that are not emerging growth companies. These include:

23

In addition, Section 107 of the JOBS Act provides that an emerging growth company can take advantage of an extended transition period set forth in Section 7(a)(2)(B) of the Securities Act for complying with new or revised accounting standards. We have elected to take advantage of the extended transition period and, as a result, we are not subject to the same new or revised accounting standards as other public companies that comply with new or revised standards on a non-delayed basis.

We will remain an emerging growth company until the earlier of (i) December 31, 2024 (the last day of the fiscal year following the fifth anniversary of the IPO) and (ii) the date on which we have issued more than $1.0 billion in nonconvertible debt during the prior three-year period.

We are also a “smaller reporting company” as defined in Rule 12b-2 under the Securities Exchange Act of 1934, as amended, or the Exchange Act. As a smaller reporting company, we are eligible to take advantage of certain exemptions from various reporting requirements that are applicable to other public companies that are not smaller reporting companies. These include:

We will remain a smaller reporting company until the last business day of the second fiscal quarter of a fiscal year on which either (i) the market value of our common stock held by non-affiliates is $250 million or more as of such date, or (ii) both our annual revenue was $100 million or more during the most recently completed fiscal year and the market value of our common stock held by non-affiliates is $700 million or more as of such date. However, we may continue relying on the reduced reporting requirements of smaller reporting companies through the Annual Report on Form 10-K for the fiscal year in which we no longer qualify as a smaller reporting company. Therefore, we may continue to be a smaller reporting company even after we are no longer an emerging growth company.

We have elected to take advantage of certain of these reduced disclosure obligations in this Annual Report on Form 10-K, and expect to take advantage of reduced disclosure obligations in future filings with the Securities and Exchange Commission, or SEC, while we remain an emerging growth company or smaller reporting company, as applicable. If we do, the information that we provide stockholders may be different than what you might receive from other public reporting companies in which you may have equity interests. See “Risk Factors—Risks Related to Ownership of Our Common Stock.”

24

Item 1A. Risk Factors.

RISK FACTORS

An investment in our securities carries a significant degree of risk. You should carefully consider the risks described below, together with the financial and other information contained in this Annual Report on Form 10-K, including the section titled “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and related notes, before you make an investment decision regarding our securities. Any one of these risks and uncertainties has the potential to cause material adverse effects on our business, prospects, financial condition and operating results which could cause actual results to differ materially from any forward-looking statements expressed by us and a significant decrease in the value of our securities. Additionally, macroeconomic conditions may amplify many of the risks discussed below to which we are

subject and may materially and adversely affect us in ways that are not anticipated by or known to us or that we do not currently consider to present material risk.

We may not be successful in preventing the material adverse effects that any of the following risks and uncertainties may cause. These potential risks and uncertainties may not be a complete list of the risks and uncertainties facing us. There may be additional risks and uncertainties that we are presently unaware of, or presently consider immaterial, that may become material in the future and have a material adverse effect on us. You could lose all or a significant portion of your investment due to any of these risks and uncertainties.

Privacy and Cybersecurity Risks

We collect, store, transmit, use, disclose and otherwise process personal and other regulated or confidential data, primarily on behalf of our clients, which subjects us to laws, governmental regulation and other legal and contractual obligations related to privacy and information security, and our actual or perceived failure to comply with such obligations could adversely affect our business and reputation.

In the ordinary course of business, we collect, store, transmit, use, disclose and otherwise process, which we refer to herein as “Process” or “Processing,” data that was collected from and about persons or their devices, including personal information, which is as defined broadly by relevant privacy and cybersecurity laws, and other regulated or confidential client data. In addition to terms in our contractual arrangements with clients, there are numerous federal, state, local and foreign laws, regulations and directives that govern the privacy, Processing, confidentiality, security and protection of such personal information and client data, the scope of which is continually evolving and subject to differing interpretations. We and our clients must comply with such laws, regulations and directives, which may impose significant consequences, including penalties and fines, for failure to comply.

For example, in May 2018, the GDPR replaced the Directive 95/46/EC on the protection of individuals with respect to the Processing of data and on the free movement of such data. The GDPR applies to the processing of personal information carried out by companies established in the European Union (E.U.) but also to the processing carried out by companies not established in the E.U., where such processing relates to (a) the offering of goods or services to data subjects who are in the E.U., or (b) the monitoring of the behavior of data subjects who are in the E.U.. The GDPR imposes several stringent requirements for controllers and processors of personal information (including non-E.U. processors who Process personal information on behalf of E.U. controllers), including, for example, robust internal accountability controls, an individual data rights regime, strict timelines for mandatory data breach notifications, limitations on retention and secondary use of information and additional obligations when we contract with third parties in connection with the Processing of personal information. Failure to comply with the requirements of the GDPR and the applicable national data protection laws of the E.U. member states may result in fines of up to €20 million or up to 4% of the total worldwide annual turnover of the preceding financial year, whichever is higher, and other administrative penalties. Complying with the GDPR has required us to implement additional internal processes to seek to ensure that we Process personal information in a compliant way and we have regularly re-drafted all our standard contracts to meet specific articles within the GDPR and new interpretations of

25

the GDPR. As we continue to operate under the GDPR, compliance may become onerous and adversely affect our business, financial condition, results of operations and prospects.

In addition, following Brexit (the process by which the United Kingdom left the European Union), the United Kingdom enacted the Data Protection Act 2018, which implemented legislation similar to the GDPR, referred to as the UK GDPR, which provides for fines of up to the greater of £17.5 million (sterling) or 4% of total annual worldwide turnover in the preceding financial year, whichever is higher.

Furthermore, legal developments in Europe have created complexity and compliance uncertainty regarding certain transfers of information from the E.U. to the United States. In particular, in July 2020, the E.U.-U.S. Privacy Shield Framework, which allowed for the transfer of personal information from the E.U. to the U.S., was invalidated by the Court of Justice of the European Union, or CJEU, and this was followed in September 2020 by the invalidation of the equivalent Swiss-US Privacy Shield Framework. Three of our group companies were accredited under the E.U.-U.S. Privacy Shield Framework to legitimize the transfer of personal information from the E.U. to the United States. Although the CJEU upheld the adequacy of the standard contractual clauses (a standard form of contract approved by the European Commission as an adequate personal information transfer mechanism) upon which we rely for intra group transfers of personal information (and which is the most widely used transfer mechanism by our clients), it made clear that use of the standard contractual clauses must now be assessed on a case-by-case basis taking into account the legal regime applicable in the destination country, in particular applicable surveillance laws and rights of individuals. Additionally, the European Data Protection Board (assigned by the European Commission to oversee data privacy in the E.U.) has issued guidance concerning data transfers following this CJEU decision which places a higher burden on compliance for data transfers. In June 2021, the European Union has issued a new version of the standard contractual clauses. On July 10, 2023, the European Commission adopted its adequacy decision for the new E.U.-U.S. Data Privacy Framework. This decision concludes that the U.S. ensure an adequate level of protection for personal information transferred from the E.U. to U.S. companies which have self-certified their compliance with the new E.U.-U.S. Data Privacy Framework.

The United Kingdom’s exit from the European Union has also imposed different requirements on personal information transfers with the introduction of the International Data Transfer Agreement and the Addendum to the E.U. standard contractual clauses in March 2022. Given these legal developments and the United Kingdom’s potential long-term divergence from E.U. law, the long-term validity of United Kingdom data protection measures remains uncertain, and we could be impacted by changes in law, including any future review of transfer mechanisms by the European courts or any supervisory authorities, which could require us to undertake substantial additional review of agreements on a going forward basis. On September 21, 2023 the UK Secretary of State for Science, Innovation and Technology laid regulations in the UK Parliament to give effect to the decision to establish a UK-U.S. Data Bridge. The UK-U.S. Data Bridge came into effect on 12 October 2023 and permits organizations in the UK to transfer personal information to U.S. organizations which have certified to the UK Extension to the E.U.-U.S. Data Privacy Framework. If we are unable to transfer personal information between and among countries and regions in which we operate, it could affect the manner in which we provide our solutions or could adversely affect our financial results.

In the United States, certain state laws, such as the California Consumer Protection Act of 2018 as amended by the California Privacy Rights Act of 2020, or collectively, the CCPA, have established a privacy framework, which applies to entities that conduct business in California. Among other things, the CCPA requires covered companies to provide certain disclosures to California residents and affords such residents certain rights with respect to their personal information. The CCPA includes a private right of action for certain data breaches, with potential for severe statutory damages. Similar comprehensive state privacy laws are also in effect in Virginia [and] Colorado[, Connecticut and Utah].While these laws are substantively similar to the CCPA in many respects, they also include their own unique compliance requirements. Certain aspects of the interpretation of these laws remain uncertain as regulating bodies in these jurisdictions begin to carry out enforcement for noncompliance. Comprehensive privacy laws have also been enacted and proposed in many other states and at the federal level. The effects of such laws could be significant and may require us to modify our data Processing practices and policies and incur substantial compliance-related costs and expenses. Companies like ours that operate on a national and international scale are responsible for monitoring and complying with the patchwork of federal, state and local regulations and

26

requirements in the United States as well as those in other jurisdictions worldwide, which may conflict with each other, further complicating compliance efforts.