Happiness Development Group Limited

No. 11, Dongjiao East Road, Shuangxi, Shunchang, Nanping City

Fujian Province, People’s Republic of China

February 8, 2023

VIA EDGAR

U.S. Securities and Exchange Commission

Division of Corporation Finance

Office of Life Sciences

100 F Street, N.E.

Washington, DC 20549

| Attn: | Daniel Crawford |

| Alan Campbell | |

| Vanessa Robertson | |

| Kevin Vaughn |

| Re: |

Happiness Development Group Limited Filed August 15, 2022 File No. 001-39098 |

Ladies and Gentlemen:

Happiness Development Group Limited (the “Company”, “HAPP,” “we”, “us” or “our”) hereby transmits its response to the letter received from the staff (the “Staff”) of the Securities and Exchange Commission (the “Commission”), dated February 2, 2023 regarding our Form 20-F for fiscal year ended March 31, 2022. For ease of reference, we have repeated the Commission’s comments in this response and numbered them accordingly.

Form 20-F for the Fiscal Year Ended March 31, 2022

Introduction, page ii

| 1. | We note that your definition of “China” or “PRC” specifically excludes Hong Kong and Macau. Please revise the definition of “China” or the “PRC” to include Hong Kong and Macau and clarify that the only time that “PRC” or “China” does not include Hong Kong or Macau is when you reference specific laws and regulations adopted by the PRC. Additionally, clarify that the “legal and operational” risks associated with operating in China also apply to operations in Hong Kong and Macau, if applicable. Lastly, discuss any commensurate laws and regulations in Hong Kong and Macau, where applicable throughout your filing, and the risks and consequences to you associated with those laws and regulations. |

Response: In response to the Staff’s comment, we propose to revise the definition of “China” or the “PRC” as follows:

| ● | “China” or the “PRC” refers to the People’s Republic of China, including Hong Kong Special Administrative Region and the Macau Special Administrative Region, unless referencing specific laws and regulations adopted by the PRC and other legal or tax matters only applicable to mainland China, and excluding, for the purposes of this annual report only, Taiwan; “PRC subsidiaries” and “PRC entities” refer to entities established in accordance with PRC laws and regulations; |

We respectfully advise the Staff that the Company has only one wholly owned subsidiary, Happiness Biology Technology Group Limited, organized under the laws of Hong Kong, which has not been engaged in any active business other than acting as holding company, and that the Company does not have any subsidiary or consolidated variable interest entity that is organized under the laws of Macau or operates in Macau. In addition, as the definition of “China” or the “PRC” will be revised to include Hong Kong and Macau, given that the Company does not have any operations in Hong Kong or Macau, we do not think it is necessary to emphasize that the legal and operational risks associated with operating in China also apply to operations in Hong Kong and Macau.

1

We propose to revise the following risk factor “Certain judgments obtained against us by our shareholders may not be enforceable” on page 21 (revisions in italic):

Certain judgments obtained against us by our shareholders may not be enforceable.

We are a Cayman Islands company and substantially all of our assets are located outside of the United States. Substantially all of our current operations are conducted in China. In addition, most of our current directors and officers are nationals and residents of countries other than the United States. Substantially all of the assets of these persons are located outside the United States. As a result, it may be difficult or impossible for you to bring an action against us or against these individuals in the United States in the event that you believe that your rights have been infringed under the U.S. federal securities laws or otherwise. Even if you are successful in bringing an action of this kind, the laws of the Cayman Islands and of China may render you unable to enforce a judgment against our assets or the assets of our directors and officers.

It may also be difficult for our shareholders to effect service of process upon us or those persons inside mainland China. As advised by our PRC legal counsel, China currently does not have treaties providing for the reciprocal recognition and enforcement of court judgments with the Cayman Islands, United States and many other countries and regions. Therefore, with respect to matters that are not subject to a binding arbitration provision, it may be difficult or impossible to recognize and enforce judgments of any of those non-PRC jurisdictions in a China court.

In addition, judgment of United States courts will not be directly enforced in Hong Kong. There are currently no treaties or other arrangements providing for reciprocal enforcement of foreign judgments between Hong Kong and the United States. There is uncertainty as to whether the courts of Hong Kong would (i) recognize or enforce judgments of United States courts obtained against us or our directors or officers predicated upon the civil liability provisions of the securities laws of the United States or any state in the United States or (ii) entertain original actions brought in Hong Kong against us or our directors or officers predicated upon the securities laws of the United States or any state in the United States. A judgment of a court in the United States predicated upon U.S. federal or state securities laws may be enforced in Hong Kong at common law by bringing an action in a Hong Kong court on that judgment for the amount due thereunder, and then seeking summary judgment on the strength of the foreign judgment, provided that the foreign judgment, among other things, is (i) for a debt or a definite sum of money (not being taxes or similar charges to a foreign government taxing authority or a fine or other penalty) and (ii) final and conclusive on the merits of the claim, but not otherwise. Such a judgment may not, in any event, be so enforced in Hong Kong if (a) it was obtained by fraud; (b) the proceedings in which the judgment was obtained were opposed to natural justice; (c) its enforcement or recognition would be contrary to the public policy of Hong Kong; (d) the court of the United States was not jurisdictionally competent; or (e) the judgment was in conflict with a prior Hong Kong judgment. Hong Kong has no arrangement for the reciprocal enforcement of judgments with the United States. As a result, there is uncertainty as to the enforceability in Hong Kong, in original actions or in actions for enforcement, of judgments of United States courts of civil liabilities predicated solely upon the federal securities laws of the United States or the securities laws of any State or territory within the United States.

| 2. | We note you state references to Happiness Development Group Limited include consolidated variable interest entities here but we did not note any such entities disclosed in this filing. Please revise or otherwise advise. |

Response: We respectfully advise the Staff that the Company does not have any consolidated variable interest entity. We propose to revise the references as set forth in our response to Comment 6 below.

2

Part I

Item 4. Information on the Company

B. Business Overview, page 27

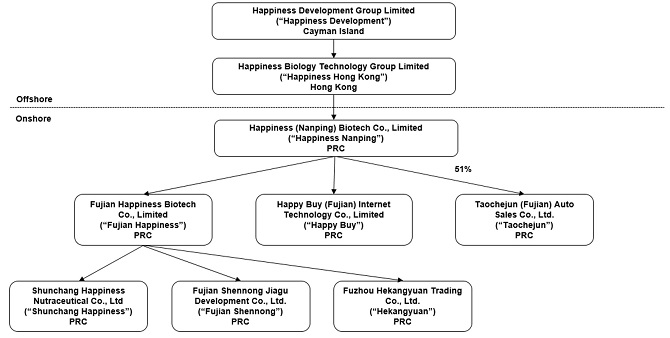

| 3. | Please revise to move the diagram of your corporate structure to the beginning of your Business Overview section. |

Response: We propose to revise the diagram of the corporate structure as follows and move it to the History and Development of the Company section:

The following chart illustrates our corporate structure, showing the Company’s principal subsidiaries as of February 7, 2023, together with the jurisdiction of incorporation of each company and the percentage of voting securities beneficially owned, controlled or directed, directly or indirectly, by the Company.

*unless otherwise indicated, the percentage of the voting power is 100% in the chart above.

In addition, we propose revise the disclosures in Item 4. Information on the Company—C. Organizational Structure as follows: See—“A. History and Development of the Company.”

| 4. | Provide prominent disclosure about the legal and operational risks associated with being based in or having the majority of the company’s operations in China. Your disclosure should make clear whether these risks could result in a material change in your operations and/or the value of your securities or could significantly limit or completely hinder your ability to offer or continue to offer securities to investors and cause the value of such securities to significantly decline or be worthless. Your disclosure should address how recent statements and regulatory actions by China’s government, such as those related to data security or anti-monopoly concerns, have or may impact the company’s ability to conduct its business, accept foreign investments, or list on a U.S. or other foreign exchange. |

Response: In response to the Staff’s comment, we propose to add the following disclosures at the onset of Item 4. Information on the Company—B. Business Overview.

Overview of our Company

We are a holding company with no material operations of our own. We conduct our operations through our subsidiaries in China.

3

We face various legal and operational risks and uncertainties related to doing business in China that could result in a material change in our operations and/or the value of our securities. Substantially all of our current business operations are conducted in China, and we are subject to complex and evolving PRC laws and regulations. The PRC government has recently issued statements and conducted regulatory actions relating to areas such as approvals, filings or other administrative requirements on offshore offerings, anti-monopoly regulatory actions, and oversight on cybersecurity and data privacy. The PRC government’s significant authority in regulating our operations and its oversight and control over offerings conducted overseas by, and foreign investment in, China-based issuers could significantly limit our and our PRC subsidiaries’ ability to conduct business and/or significantly limit or completely hinder our ability to offer or continue to offer securities to investors, accept foreign investments or list on a United States or other foreign exchange, or cause the value of our securities to significantly decline or be worthless. For more details, see “Item 3. Key Information—D. Risk Factors—Risks Related to Doing Business in China.”

For example, the recently promulgated Data Security Law and the Personal Information Protection Law in 2021 posed additional challenges to our cybersecurity and data privacy compliance. The new Cybersecurity Review Measures issued by the Cyberspace Administration of China, or the CAC and several other PRC governmental authorities in December 2021, as well as the Regulations on the Network Data Security (Draft for Comments), or the Draft Regulations, published by the CAC for public comments in November 2021, imposed potential additional restrictions on China-based overseas-listed companies like us. If future implementing rules of the new Cybersecurity Review Measures and the enacted version of the Draft Regulations mandate clearance of cybersecurity review and other specific actions to be taken by issuers like us, we face uncertainties as to whether these additional procedures can be completed by us timely, or at all, which may subject us to government enforcement actions and investigations, fines, penalties, or suspension of our non-compliant operations, and materially and adversely affect our business and results of operations and the price of our ordinary shares. For additional details, see “Item 3. Key Information—Risk Factors—Risks Related to Doing Business in China.”

In addition, on December 24, 2021, the China Securities Regulatory Commission, or the CSRC, released a draft of the Provisions of the State Council on the Administration of Overseas Securities Offering and Listing by Domestic Companies (Draft for Comments), or the Draft Provisions, and the CSRC issued a draft of Administration Measures for the Filing of Overseas Securities Offering and Listing by Domestic Companies (Draft for Comments), or the Draft Administration Measures, for public comments. According to the Draft Provisions and the Draft Administration Measures, an overseas offering and listing by a domestic company, whether directly or indirectly, shall be filed with the CSRC. As of the date of this annual report, the Draft Provisions and the Draft Administration Measures were released for public comment only. There are uncertainties as to whether the Draft Provisions and the Draft Administration Measures would be further amended, revised or updated. Substantial uncertainties exist with respect to the enactment timetable and final content of the Draft Provisions and the Draft Administration Measures. However, assuming the Draft Provisions and the Draft Administration Measures were to be adopted as-is, if we fail to obtain the relevant approval or complete other review or filing procedures for any future offshore offering or listing, the operations of our PRC subsidiaries may face sanctions by the CSRC or other PRC regulatory authorities, which may include a warning and a fine between RMB1 million to RMB10 million. In serious circumstances, our PRC subsidiaries may be ordered to suspend their businesses or suspend their businesses pending rectification, or their permits or business licenses may be revoked, each of which could have a material and adverse effect on our business, financial condition, results of operations, reputation and prospects, as well as the trading price of our ordinary shares. See “Item 3. Key Information—D. Risk Factors—Risks Related to Doing Business in China.”

Furthermore, the PRC regulators have promulgated new anti-monopoly and competition laws and regulations and strengthened the enforcement under these laws and regulations. There remain uncertainties as to how the laws, regulations and guidelines recently promulgated will be implemented and whether these laws, regulations and guidelines will have a material impact on our business, financial condition, results of operations and prospects. We cannot assure you that our business operations comply with such regulations and authorities’ requirements in all respects. If any non-compliance is raised by relevant authorities and determined against us, we may be subject to fines and other penalties.

Risks and uncertainties arising from the legal system in China, including the above-mentioned risks and uncertainties regarding the enforcement of laws and quickly evolving rules and regulations in China, could result in a material adverse change in our operations and the value of our ordinary shares. For more details, see “Item 3. Key Information—D. Risk Factors—Risks Related to Doing Business in China.”

4

Our Class A ordinary shares may be prohibited from trading on a national exchange or “over-the-counter” markets under the Holding Foreign Companies Accountable Act (the “HFCA Act”) if the Public Company Accounting Oversight Board (the “PCAOB”) is unable to inspect our auditors for three consecutive years beginning in 2021. Furthermore, on June 22, 2021, the U.S. Senate passed the Accelerating Holding Foreign Companies Accountable Act (the “AHFCAA”), which, if signed into law, would amend the HFCA Act and require the SEC to prohibit an issuer’s securities from trading on any U.S. stock exchanges if its auditor is not subject to the PCAOB inspections for two consecutive years instead of three consecutive years. Pursuant to the HFCA Act, the PCAOB issued a Determination Report on December 16, 2021 which found that the PCAOB is unable to inspect or investigate completely registered public accounting firms headquartered in: (1) mainland China of the People’s Republic of China because of a position taken by one or more authorities in mainland China; and (2) Hong Kong, a Special Administrative Region and dependency of the PRC, because of a position taken by one or more authorities in Hong Kong. In addition, the PCAOB’s report identified the specific registered public accounting firms which are subject to these determinations. On December 29, 2022, a legislation entitled “Consolidated Appropriations Act, 2023” (the “Consolidated Appropriations Act”), was signed into law by President Biden. The Consolidated Appropriations Act contained, among other things, an identical provision to AHFCAA, which reduces the number of consecutive non-inspection years required for triggering the prohibitions under the HFCA Act from three years to two. Our auditor, TPS Thayer LLC, the independent registered public accounting firm that issues the audit report included in this prospectus, as an auditor of companies that are traded publicly in the United States and a firm registered with the PCAOB, is subject to laws in the United States pursuant to which the PCAOB conducts regular inspections to assess TPS Thayer LLC’s compliance with applicable professional standards. TPS Thayer LLC is headquartered in Sugar Land, Texas with no branches or offices outside the United States and has been inspected by the PCAOB on a regular basis. Our auditor is not subject to the determinations announced by the PCAOB on December 16, 2021 relating to the PCAOB’s inability to inspect or investigate completely registered public accounting firms headquartered in mainland China of the PRC or Hong Kong because of a position taken by one or more authorities in the PRC or Hong Kong, however, recent developments with respect to audits of China-based companies create uncertainty about the ability of our PRC subsidiaries to fully cooperate with TPS Thayer LLC’s audit without the approval of the Chinese authorities. In the event it is later determined that the PCAOB is unable to inspect or investigate completely our auditor, then such lack of inspection could cause trading in our securities to be prohibited under the HFCA Act, and ultimately result in a determination by a securities exchange to delist our securities. On August 26, 2022, the PCAOB signed a Statement of Protocol (the “SOP”) Agreement with the CSRC and China’s Ministry of Finance. The SOP Agreement, together with two protocol agreements (collectively, “SOP Agreements”), governs inspections and investigations of audit firms based in mainland China and Hong Kong, taking the first step toward opening access for the PCAOB to inspect and investigate registered public accounting firms headquartered in mainland China and Hong Kong. Pursuant to the fact sheet with respect to the Protocol disclosed by the U.S. Securities and Exchange Commission (the “SEC”), the PCAOB shall have independent discretion to select any issuer audits for inspection or investigation and has the unfettered ability to transfer information to the SEC. On December 15, 2022, the PCAOB Board determined that the PCAOB was able to secure complete access to inspect and investigate registered public accounting firms headquartered in mainland China and Hong Kong and voted to vacate its previous determinations to the contrary. However, should PRC authorities obstruct or otherwise fail to facilitate the PCAOB’s access in the future, the PCAOB Board will consider the need to issue a new determination.

These risks, if materialized, could result in a material adverse change in our operations and the value of our ordinary shares, significantly limit or completely hinder our ability to continue to offer securities to investors, or cause the value of such securities to significantly decline or be worthless. For more details, see “Item 3. Key Information—D. Risk Factors—Risks Related to Doing Business in China.”

| 5. | Similar to your existing disclosure starting on page 11, please prominently disclose here whether your auditor is subject to the determinations announced by the PCAOB on December 16, 2021 and whether and how the Holding Foreign Companies Accountable Act and related regulations will affect your company. Disclose here and in your Risk Factor section that the HFCAA timeline for a potential trading prohibition was shortened from three years to two years, as part of the “Consolidated Appropriations Act, 2023,” signed into law on December 29, 2022. |

Response: In response to the Staff’s comment, we propose to add the disclosures at the onset of Item 4. Information on the Company—B. Business Overview. Please see our response to Comment 4.

5

In addition, we propose to revise the risk factor “Although the audit report included in this annual report is prepared by an auditor who are currently inspected by the Public Company Accounting Oversight Board (the “PCAOB”), there is no guarantee that future audit reports will be prepared by auditors inspected by the PCAOB and, as such, in the future investors may be deprived of the benefits of such inspection. Furthermore, trading in our securities may be prohibited under the Holding Foreign Companies Accountable Act (the “HFCA Act”) if the SEC subsequently determines our audit work is performed by auditors that the PCAOB is unable to inspect or investigate completely, and as a result, U.S. national securities exchanges, such as Nasdaq, may determine to delist our securities. Furthermore, on June 22, 2021, the U.S. Senate passed the Accelerating Holding Foreign Companies Accountable Act, which, if enacted, would amend the HFCA Act and require the SEC to prohibit an issuer’s securities from trading on any U.S. stock exchanges if its auditor is not subject to PCAOB inspections for two consecutive years instead of three” on page 11:

Although the audit report included in this annual report is prepared by an auditor who are currently inspected by the Public Company Accounting Oversight Board (the “PCAOB”), there is no guarantee that future audit reports will be prepared by auditors inspected by the PCAOB and, as such, in the future investors may be deprived of the benefits of such inspection. Furthermore, trading in our securities may be prohibited under the Holding Foreign Companies Accountable Act (the “HFCA Act”) if the SEC subsequently determines our audit work is performed by auditors that the PCAOB is unable to inspect or investigate completely, and as a result, U.S. national securities exchanges, such as Nasdaq, may determine to delist our securities. Furthermore, on December 29, 2022, the Consolidated Appropriations Act, was signed into law by President Biden. The Consolidated Appropriations Act contained, among other things, an identical provision to AHFCAA, which reduce the number of consecutive non-inspection years required for triggering the prohibitions under the HFCA Act from three years to two.

As an auditor of companies that are registered with the SEC and publicly traded in the United States and a firm registered with the PCAOB, our auditor is required under the laws of the United States to undergo regular inspections by the PCAOB to assess their compliance with the laws of the United States and professional standards.

Although we operate substantially in mainland China, a jurisdiction where the PCAOB is currently unable to conduct inspections without the approval of the Chinese government authorities, our auditor, TPS Thayer LLC, the independent registered public accounting firm that issues the audit report included elsewhere in this annual report, is subject to laws in the United States pursuant to which the PCAOB conducts regular inspections to assess our auditor’s compliance with the applicable professional standards. Inspections of other auditors conducted by the PCAOB outside mainland China have at times identified deficiencies in those auditors’ audit procedures and quality control procedures, which may be addressed as part of the inspection process to improve future audit quality. The lack of PCAOB inspections of audit work undertaken in mainland China prevents the PCAOB from regularly evaluating auditors’ audits and their quality control procedures. As a result, if there is any component of our auditor’s work papers become located in mainland China in the future, such work papers will not be subject to inspection by the PCAOB. As a result, investors would be deprived of such PCAOB inspections, which could result in limitations or restrictions to our access of the U.S. capital markets.

As part of a continued regulatory focus in the United States on access to audit and other information currently protected by national law, in particular mainland China’s, in June 2019, a bipartisan group of lawmakers introduced bills in both houses of the U.S. Congress which, if passed, would require the SEC to maintain a list of issuers for which PCAOB is not able to inspect or investigate the audit work performed by a foreign public accounting firm completely. The proposed Ensuring Quality Information and Transparency for Abroad-Based Listings on our Exchanges (“EQUITABLE”) Act prescribes increased disclosure requirements for these issuers and, beginning in 2025, the delisting from U.S. national securities exchanges such as Nasdaq of issuers included on the SEC’s list for three consecutive years. It is unclear if this proposed legislation will be enacted. Furthermore, there have been recent deliberations within the U.S. government regarding potentially limiting or restricting China-based companies from accessing U.S. capital markets. On May 20, 2020, the U.S. Senate passed the Holding Foreign Companies Accountable Act (the “HFCA Act”), which includes requirements for the SEC to identify issuers whose audit work is performed by auditors that the PCAOB is unable to inspect or investigate completely because of a restriction imposed by a non-U.S. authority in the auditor’s local jurisdiction. The U.S. House of Representatives passed the HFCA Act on December 2, 2020, and the HFCA Act was signed into law on December 18, 2020. Additionally, in July 2020, the U.S. President’s Working Group on Financial Markets issued recommendations for actions that can be taken by the executive branch, the SEC, the PCAOB or other federal agencies and department with respect to Chinese companies listed on U.S. stock exchanges and their audit firms, in an effort to protect investors in the United States. In response, on November 23, 2020, the SEC issued guidance highlighting certain risks (and their implications to U.S. investors) associated with investments in China-based issuers and summarizing enhanced disclosures the SEC recommends China-based issuers make regarding such risks. On March 24, 2021, the SEC adopted interim final rules relating to the implementation of certain disclosure and documentation requirements of the HFCA Act. We will be required to comply with these rules if the SEC identifies us as having a “non-inspection” year (as defined in the interim final rules) under a process to be subsequently established by the SEC. The SEC is assessing how to implement other requirements of the HFCA Act, including the listing and trading prohibition requirements described above. Under the HFCA Act, our securities may be prohibited from trading on Nasdaq or other U.S. stock exchanges if our auditor is not inspected by the PCAOB for three consecutive years, and this ultimately could result in our Ordinary Shares being delisted.

6

Furthermore, on June 22, 2021, the U.S. Senate passed the Accelerating Holding Foreign Companies Accountable Act (“AHFCAA”), which, if enacted, would amend the HFCA Act and require the SEC to prohibit an issuer’s securities from trading on any U.S. stock exchanges if its auditor is not subject to PCAOB inspections for two consecutive years instead of three and would reduce the time before our securities may be prohibited from trading or delisted. On September 22, 2021, the PCAOB adopted a final rule implementing the AHFCAA, which provides a framework for the PCAOB to use when determining, as contemplated under the AHFCAA, whether the Board is unable to inspect or investigate completely registered public accounting firms located in a foreign jurisdiction because of a position taken by one or more authorities in that jurisdiction. On November 5, 2021, the SEC approved the PCAOB’s Rule 6100, Board Determinations Under the HFCA Act. On December 2, 2021, the SEC issued amendments to finalize rules implementing the submission and disclosure requirements in the HFCA Act. The rules apply to registrants that the SEC identifies as having filed an annual report with an audit report issued by a registered public accounting firm that is located in a foreign jurisdiction and that PCAOB is unable to inspect or investigate completely because of a position taken by an authority in foreign jurisdictions. On December 16, 2021, the PCAOB issued a Determination Report which found that the PCAOB is unable to inspect or investigate completely registered public accounting firms headquartered in: (1) mainland China of the PRC, and (2) Hong Kong. In addition, the PCAOB’s report identified the specific registered public accounting firms which are subject to these determinations. On December 29, 2022, the Consolidated Appropriations Act, was signed into law by President Biden. The Consolidated Appropriations Act contained, among other things, an identical provision to AHFCAA, which reduce the number of consecutive non-inspection years required for triggering the prohibitions under the HFCA Act from three years to two. Our auditor, TPS Thayer LLC, is headquartered in Sugar Land, Texas, not mainland China or Hong Kong and was not identified in this report as a firm subject to the PCAOB’s determination. Therefore, our auditor is not currently subject to the determinations announced by the PCAOB on December 16, 2021, and it is currently subject to the PCAOB inspections.

While our auditor is based in the U.S. and is registered with the PCAOB and has been inspected by the PCAOB on a regular basis, in the event it is later determined that the PCAOB is unable to inspect or investigate completely our auditor because of a position taken by an authority in a foreign jurisdiction, then such lack of inspection could cause trading in the our securities to be prohibited under the HFCA Act, and ultimately result in a determination by a securities exchange to delist our securities. In addition, the recent developments would add uncertainties to the listing and trading of our Class A ordinary shares and we cannot assure you whether Nasdaq or regulatory authorities would apply additional and more stringent criteria to us after considering the effectiveness of our auditor’s audit procedures and quality control procedures, adequacy of personnel and training, or sufficiency of resources, geographic reach or experience as it relates to the audit of our financial statements. It remains unclear what the SEC’s implementation process related to the above rules will entail or what further actions the SEC, the PCAOB or Nasdaq will take to address these issues and what impact those actions will have on U.S. companies that have significant operations in the PRC and have securities listed on a U.S. stock exchange (including a national securities exchange or over-the-counter stock market). In addition, the above amendments and any additional actions, proceedings, or new rules resulting from these efforts to increase U.S. regulatory access to audit information could create some uncertainty for investors, the market price of our Ordinary Shares could be adversely affected, and we could be delisted if we and our auditor are unable to meet the PCAOB inspection requirement or being required to engage a new audit firm, which would require significant expense and management time.

On August 26, 2022, the PCAOB signed a Statement of Protocol (the “SOP”) Agreements with the CSRC and China’s Ministry of Finance. The SOP Agreement, together with two protocol agreements (collectively, “SOP Agreements”), governs inspections and investigations of audit firms based in mainland China and Hong Kong, taking the first step toward opening access for the PCAOB to inspect and investigate registered public accounting firms headquartered in mainland China and Hong Kong. Pursuant to the fact sheet with respect to the Protocol disclosed by the SEC, the PCAOB shall have independent discretion to select any issuer audits for inspection or investigation and has the unfettered ability to transfer information to the SEC. On December 15, 2022, the PCAOB Board determined that the PCAOB was able to secure complete access to inspect and investigate registered public accounting firms headquartered in mainland China and Hong Kong and voted to vacate its previous determinations to the contrary. However, should PRC authorities obstruct or otherwise fail to facilitate the PCAOB’s access in the future, the PCAOB Board will consider the need to issue a new determination. Delisting of our Class A ordinary shares would force holders of our Class A ordinary shares to sell their Class A ordinary shares. The market price of our Class A ordinary shares could be adversely affected as a result of anticipated negative impacts of these executive or legislative actions upon, as well as negative investor sentiment towards, companies with significant operations in China that are listed in the United States, regardless of whether these executive or legislative actions are implemented and regardless of our actual operating performance.

7

| 6. | Clearly disclose how you will refer to the holding company and subsidiaries when providing the disclosure throughout the document so that it is clear to investors which entity the disclosure is referencing and which subsidiaries or entities are conducting the business operations. |

Response: In response to the Staff’s comment, we respectfully propose to revise the disclosures on page ii as follows:

| ● | “HAPP,” “Happiness Development,” or “the Company” refer to Happiness Development Group Limited (formerly known as “Happiness Biotech Group Limited”), an exempted company registered in the Cayman Islands with limited liability; |

| ● | “we,” “us,” “our company” and “our” refer to Happiness Development Group Limited and its consolidated subsidiaries. We conduct operations in China through our PRC subsidiaries; |

| 7. | Provide a clear description of how cash is transferred through your organization. Disclose your intentions to distribute earnings. Quantify any cash flows and transfers of other assets by type that have occurred between the holding company and its subsidiaries, and direction of transfer. Quantify any dividends or distributions that a subsidiary have made to the holding company and which entity made such transfer, and their tax consequences. Similarly quantify dividends or distributions made to U.S. investors, the source, and their tax consequences. Your disclosure should make clear if no transfers, dividends, or distributions have been made to date. Describe any restrictions on foreign exchange and your ability to transfer cash between entities, across borders, and to U.S. investors. Describe any restrictions and limitations on your ability to distribute earnings from the company, including your subsidiaries, to the parent company and U.S. investors. |

Response: In response to the Staff’s comment, we respectfully propose to add the disclosures at the onset of Item 4. Information on the Company—B. Business Overview after the proposed disclosures in our response to Comment 4.

Cash Flows through Our Organization

The cash transfers within our organization are generally made in the following manners: (i) the Company transfers cash to its subsidiaries by way of providing loans, making capital contributions and providing operating cash, and (ii) the Company’s subsidiaries transfer cash to the Company by way of repayment of loans and repayment of operating cash due to the Company. Other than cash transfers, no transfer of other assets has occurred between the Company and its subsidiaries. The following table presents cash transfers between the Company and its subsidiaries for 2022, 2021 and 2020:

| The C ompany transfers cash to its subsidiaries by way of | FY2022 | FY2021 | FY2020 | |||||||||

| cash dividends | $ | - | $ | - | $ | - | ||||||

| providing loans | $ | - | $ | - | $ | - | ||||||

| making capital contributions | $ | 1,000,000.00 | $ | 5,199,959.00 | $ | - | ||||||

| providing operating cash | $ | 24,593,600.00 | $ | 2,746,578.00 | $ | 7,200,000.00 | ||||||

| Total | $ | 25,593,600.00 | $ | 7,946,537.00 | $ | 7,200,000.00 | ||||||

| The Company’s subsidiaries transfer cash to the Company by way of | FY2022 | FY2021 | FY2020 | |||||||||

| repayment of loans | $ | - | $ | - | $ | - | ||||||

| repayment of operating cash | $ | 6,880,000.00 | $ | - | $ | - | ||||||

| Total | $ | 6,880,000.00 | $ | - | $ | - | ||||||

8

On July 31, 2020, the Board of the Company declared a special cash dividend of $0.015 per Ordinary Shares. The dividend, equal to $375,000 in the aggregate, was fully paid on August 17, 2020. Except for the aforementioned, the Company has not made any dividend distribution to its shareholders, and the Company’s subsidiaries did not make any dividend or distribution to the Company. Pursuant to the PRC Enterprise Income Tax Law and Implementation Regulations for the Corporate Income Tax Law (the “CIT Law”), a withholding tax rate of 10% would apply to any dividends paid by a PRC “resident enterprise” to a foreign enterprise investor, unless such non-resident enterprise’s jurisdiction of incorporation has a tax treaty with China that provides for a reduced rate of withholding tax and such non-resident enterprise is the beneficial owner of the dividends. The Cayman Islands, where the holding company is incorporated, does not have such a tax treaty with China. The CIT Law provides that PRC resident enterprises are generally subject to the uniform 25% enterprise income tax rate on their worldwide income. Therefore, if we are treated as a PRC resident enterprise, we will be subject to PRC income tax on our worldwide income at the 25% uniform tax rate, which could have an impact on our effective tax rate and an adverse effect on our net income and results of operations, although we would be exempted from enterprise income tax on dividends distributed from our PRC subsidiaries to us, since such income received by PRC resident enterprise is tax exempted under the CIT Law.

In addition, we have not made any dividend or distribution to any U.S. investor as of the date of this annual report. As an offshore holding company, we may rely upon dividends paid to us by our subsidiaries in the PRC to pay dividends and to finance any debt we may incur. If our subsidiaries or any newly formed subsidiaries incur debt on their own behalf in the future, the instruments governing their debt may restrict their ability to pay dividends to us. In addition, our subsidiaries are permitted to pay dividends to us only out of their accumulated profits, if any, as determined in accordance with PRC accounting standards and regulations. Under PRC laws and regulations, each of our PRC subsidiaries are required to set aside a portion of their net profits each year to fund a statutory surplus reserve which are no less than 10% of their net profits each year until such reserve reaches 50% of its registered capital. This reserve is not distributable as dividends. As a result, our PRC subsidiaries are restricted in their ability to transfer a portion of their net assets to us in the form of dividends, loans or advances. As an offshore holding company, we are permitted under PRC laws and regulations to provide funding from the proceeds of our offshore fund-raising activities to our subsidiaries in China only through loans or capital contributions, subject to the satisfaction of the applicable government registration and approval requirements. Before providing loans to our PRC subsidiaries, we will be required to make filings about details of the loans with the State Administration of Foreign Exchange of the PRC (the “SAFE”) in accordance with relevant PRC laws and regulations. Our PRC subsidiaries that receive the loans are only allowed to use the loans for the purposes set forth in these laws and regulations. Under regulations of the SAFE, Renminbi is not convertible into foreign currencies for capital account items, such as loans, repatriation of investments and investments outside of China, unless the prior approval of the SAFE is obtained and prior registration with the SAFE is made. See “Item 4. Information on the Company—B. Business Overview—PRC Laws and Regulations Relating to Our Business” for more details.

| 8. | Disclose each permission or approval that you or your subsidiaries are required to obtain from Chinese authorities to operate your business and to offer securities to foreign investors. Similar to your Risk Factor section starting on page 13, state whether you or your subsidiaries are covered by permissions requirements from the China Securities Regulatory Commission (CSRC), Cyberspace Administration of China (CAC) or any other governmental agency that is required to approve your operations, and state affirmatively whether you have received all requisite permissions or approvals and whether any permissions or approvals have been denied. Please also describe the consequences to you and your investors if you or your subsidiaries: (i) do not receive or maintain such permissions or approvals, (ii) inadvertently conclude that such permissions or approvals are not required, or (iii) applicable laws, regulations, or interpretations change and you are required to obtain such permissions or approvals in the future. Revise where you discuss the CAC to discuss the final new measures that became effective on February 15, 2022. |

Response: In response to the Staff’s comment, we respectfully propose to add the disclosures at the onset of Item 4. Information on the Company—B. Business Overview before the proposed disclosures in our response to Comment 4, and update the disclosures to Item 4. Information on the Company—B. Business Overview—Licenses, Permits and Government Regulations—License.

We propose to add the disclosures at the onset of Item 4. Information on the Company—B. Business Overview as follows:

Permissions or Approval Required from the PRC Authorities for Our Operations and Listing

In order to operate our business activities currently conducted in China, each of our PRC subsidiaries is required to obtain a business license from the State Administration for Market Regulation (the “SAMR”). As of the date of this prospectus, our PRC subsidiaries have obtained all the permissions which are required to obtain for their operations. Each of our PRC subsidiaries has obtained a valid business license from the SAMR, and no application for any such license has been denied.

9

In addition, in China, food and nutritious supplement manufacturers are required to comply with the certain quality control, safety requirement and obtain “Food Production License” from CFDA for full compliance with the safety requirements set forth in Food Safety Law of People’s Republic of China. Besides, each nutraceutical product is required to obtain the official approval of manufacturing from CFDA, which is the commonly known as the “Blue Caps.” According to CFDA regulations, “Blue Caps” approvals granted prior to July 1, 2005 do not have any expiration date, “Blue Caps” approvals obtained after July 1, 2005 have a term of 5 years and maybe renewed. ” As of the date of this February 7, 2023, 26 of our products are approved by CFDA. Our research and development team has been closely monitoring the approval status of our products and applied for renewal before the relevant certificate expired. Failure to renew the relevant licenses and/or registrations may subject us to fines or sanctions which will have negative impact on our products. For more details, please see “Item 3. Key Information—D. Risk Factors—Risks Related to Our Business— If we fail to renew our Food Production License and registration of our nutraceutical and dietary supplements products, we may receive fines or even sanctions which may prohibit us from production” and “Item 4. Information on the Company—B. Business Overview—Licenses, Permits and Government Regulations—License.”

Furthermore, we and our PRC subsidiaries are not required to obtain permission or approval for the listing or trading of Class A ordinary shares in foreign stock exchanges from the PRC authorities including the CSRC or the CAC, or any other PRC governmental authorities. As of the date of this annual report, we or our subsidiaries have not received any inquiry, notice, warning, sanctions or regulatory objection to our listing on Nasdaq from the CSRC or other PRC governmental authorities. However, there remains significant uncertainty as to the enactment, interpretation and implementation of regulatory requirements related to overseas securities offerings and other capital markets activities.

We are aware, however, that recently the PRC government initiated a series of regulatory actions and statements to regulate business operations in China with little advance notice, including cracking down on illegal activities in the securities market, enhancing supervision over China-based companies listed overseas using a variable interest entity structure, adopting new measures to extend the scope of cybersecurity reviews, and expanding the efforts in anti-monopoly enforcement.

On December 24, 2021, the CSRC issued Provisions of the State Council on the Administration of Overseas Securities Offering and Listing by Domestic Companies (Draft for Comments) (the “Administration Provisions”), and the Administration Measures for the Filing of Overseas Securities Offering and Listing by Domestic Companies (Draft for Comments) (the “Measures”), which are now open for public comments.

The Administration Provisions and Measures for overseas listings lay out specific requirements for filing documents and include unified regulation management, strengthening regulatory coordination, and cross-border regulatory cooperation. Domestic companies seeking to list abroad must carry out relevant security screening procedures if their businesses involve such supervision. Companies endangering national security are among those off-limits for overseas listings.

10

In addition, an overseas offering and listing is prohibited under any of the following circumstances: (1) if the intended securities offering and listing is specifically prohibited by national laws and regulations and relevant provisions; (2) if the intended securities offering and listing may constitute a threat to or endangers national security as reviewed and determined by competent authorities under the State Council in accordance with law; (3) if there are material ownership disputes over the equity, major assets, and core technology, etc. of the issuer; (4) if, in the past three years, the domestic enterprise or its controlling shareholders or actual controllers have committed corruption, bribery, embezzlement, misappropriation of property, or other criminal offenses disruptive to the order of the socialist market economy, or are currently under judicial investigation for suspicion of criminal offenses, or are under investigation for suspicion of major violations; (5) if, in past three years, directors, supervisors, or senior executives have been subject to administrative punishments for severe violations, or are currently under judicial investigation for suspicion of criminal offenses, or are under investigation for suspicion of major violations; (6) other circumstances as prescribed by the State Council. The Administration Provisions and the Measures define the legal liabilities of breaches such as failure in fulfilling filing obligations or fraudulent filing conducts, imposing a fine between RMB 1 million and RMB 10 million, and in cases of severe violations, a parallel order to suspend relevant business or halt operation for rectification, revoke relevant business permits or operational license.

According to CSRC Answers, after the Administration Provisions and the Measures are implemented upon completion of public consultation and due legislative procedures, the CSRC will formulate and issue guidance for filing procedures to further specify the details of filing administration and ensure that market entities could refer to clear guidelines for filing, which means that the Administration Provisions and the Measures will not come into effect until some time. As the Administration Provisions and Measures have not yet come into effect, we are currently unaffected by these proposed regulations. However, according to CSRC Answers, new initial public offerings and refinancing by existing overseas listed Chinese companies will be required to go through the filing process; other existing overseas listed companies will be allowed a sufficient transition period to complete their filing procedure.

The Administration Provisions and the Measures, if enacted, may subject us to additional compliance requirement in the future, and we cannot assure you that we will be able to get the clearance of filing procedures under the Administration Provisions and the Measures on a timely basis, or at all. Any failure of us to fully comply with new regulatory requirements may significantly limit or completely hinder our ability to offer or continue to offer our ordinary shares, cause significant disruption to our business operations, and severely damage our reputation, which would materially and adversely affect our financial condition and results of operations and cause our ordinary shares to significantly decline in value or become worthless. As of the date of this annual report, it is uncertain when the Administration Provision and the Measures will take effect or if they will take effect as currently drafted, hence we are currently not required to complete the filing procedures and submit the relevant information to the CSRC.

Pursuant to the PRC Cybersecurity Law, which was promulgated by the SCNPC on November 7, 2016 and took effect on June 1, 2017, personal information and important data collected and generated by a critical information infrastructure operator in the course of its operations in China must be stored in China, and if a critical information infrastructure operator purchases internet products and services that affects or may affect national security, it should be subject to cybersecurity review by the CAC. Due to the lack of further interpretations, the exact scope of “critical information infrastructure operator” remains unclear. On December 28, 2021, the CAC and other relevant PRC governmental authorities jointly promulgated the Cybersecurity Review Measures (the “new Cybersecurity Review Measures”) to replace the original Cybersecurity Review Measures. The new Cybersecurity Review Measures took effect on February 15, 2022. Pursuant to the new Cybersecurity Review Measures, if critical information infrastructure operators purchase network products and services, or network platform operators conduct data processing activities that affect or may affect national security, they will be subject to cybersecurity review. A network platform operator holding more than one million users/users’ individual information also shall be subject to cybersecurity review before listing abroad. The cybersecurity review will evaluate, among others, the risk of critical information infrastructure, core data, important data, or a large amount of personal information being influenced, controlled or maliciously used by foreign governments and risk of network data security after going public overseas. As of the date of this annual report, we do not expect to be subject to cybersecurity review because: (i) we are not an operator of critical information infrastructure, and (ii) we are not an online platform operator who possesses personal information of more than one million users.

11

Since these statements and regulatory actions are new, it is highly uncertain how soon legislative or administrative regulation making bodies will respond and what existing or new laws or regulations or detailed implementations and interpretations will be modified or promulgated, if any, and the potential impact such modified or new laws and regulations will have on our daily business operation, the ability to accept foreign investments and list on a U.S. exchange. If we and our subsidiaries (i) inadvertently conclude that such permissions or approvals are not required, or (ii) applicable laws, regulations, or interpretations change, and we are required to obtain permission or approval from the PRC authorities, including the CSRC and the CAC, for the Offering of our Class A Ordinary Shares and any follow-on offering in the U.S. in the future, and if any of such permission or approval were not received maintained, or subsequently rescinded, it would likely result in a material change in our operations, including our ability to continue our existing holding company structure, carry on our current business, accept foreign investments, and offer or continue to offer securities to our investors. We may also be subject to penalties and sanctions imposed by the PRC regulatory agencies, including the CSRC, if we fail to comply with such rules and regulations. These adverse actions could cause the value of our Class A ordinary shares to significantly decline or become worthless. See “Risk Factors — Risks Related to Doing Business in China.”

We propose to update the disclosures Item 4. Information on the Company—B. Business Overview—Licenses, Permits and Government Regulations—License as follows (revisions in italic):

Dietary Supplement Production License and Official Approvals

In China, food and nutritious supplement manufacturers are required to comply with the certain quality control, safety requirement and obtain “Food Production License” from CFDA for full compliance with the safety requirements set forth in Food Safety Law of People’s Republic of China. Besides, each nutraceutical product is required to obtain the official approval of manufacturing from CFDA, which is the commonly known as the “Blue Caps”. Currently 26 of our products are approved by CFDA. The approvals of our main products are listed in the below chart.

| No. | Product Name | Code | Expiration Date | Owner | ||||

| 1 | “Happiness” Lucidum Spore Powder Capsule | No.346(1998) | not applicable | Fujian Happiness | ||||

| 2 | “Daguangrong” Cordyceps Mycelia Oral Liquid | No.220(1997) | not applicable | Shunchang Happiness | ||||

| 3 | “Happiness” Ejiao Astragalus Oral Liquid | G20040107 | not applicable | Fujian Happiness | ||||

| 4 | “Happiness” Iron and Zinc Amino Acids Oral Liquid | G20060704 | 8/13/2025 | Fujian Happiness | ||||

| 5 | “Happiness” American Ginseng Capsule | G20050572 | 7/8/2025 | Fujian Happiness | ||||

| 6 | Lishijin Qingzhi Capsule | No.0288(2003) | not applicable | Fujian Happiness | ||||

| 7 | “Happiness” Fenglingbao Capsule | No.0064(2003) | not applicable | Fujian Happiness | ||||

| 8 | “Happiness” American Ginseng Original Grain Tea bag | No.0291(2003) | not applicable | Fujian Happiness | ||||

| 9 | “Happiness” American Ginseng Oral Liquid | G20040182 | not applicable | Shunchang Happiness | ||||

| 10 | “Happiness” Taurine Zinc Oral Liquid | G20120537 | 1/6/2025 | Fujian Happiness | ||||

| 11 | “Happiness” Spirulina Tablets | G20050573 | 8/13/2025 | Fujian Happiness | ||||

| 12 | “Happiness” Sleeping Capsule | No.0198(2002) | not applicable | Fujian Happiness | ||||

| 13 | “Happiness” Tablets | G20140404 | 5/22/2026 | Fujian Happiness | ||||

| 14 | “Happiness” American Ginseng Chicken Essence Tonic | G20040889 | not applicable | Fujian Happiness | ||||

| 15 | “Happiness” Little Pigeon Oral Liquid | No.0487(1998) | not applicable | Fujian Happiness | ||||

| 16 | “Happiness” Ginseng Taurine Drink | G20140393 | 8/22/2026 | Fujian Happiness | ||||

| 17 | “Happiness” Fish Oil Vitamin E Soft Capsule | G20100155 | 9/4/2024 | Fujian Happiness | ||||

| 18 | “Happiness” Calcium Tablets | G202035000761 | not applicable | Fujian Happiness | ||||

| 19 | “Happiness” Selenium tablets | G201935001306 | not applicable | Fujian Happiness | ||||

| 20 | “Happiness” Calcium Oral Liquid | G201935000766 | not applicable | Fujian Happiness | ||||

| 21 | “Happiness” Coenzyme Q10 Capsule | G202135100829 | not applicable | Fujian Happiness | ||||

| 22 | “Happiness” American Ginseng and Antler Tablets | G20090308 | 02/10/2024 | Fujian Happiness | ||||

| 23 | “Happiness” Protein Powder | G20100744 | 09/11/2024 | Fujian Happiness | ||||

| 24 | “Gold Coast” American Ginseng Amino Acid Capsules | G20060779 | 02/17/2026 | Fujian Happiness | ||||

| 25 | “Happiness” Spirulina Chewable Tablets | G202235001630 | not applicable | Fujian Happiness | ||||

| 26 | “Happiness” Ganoderma Lucidum Spore Powder | G202235002955 | not applicable | Fujian Happiness |

12

We thank the Staff for its review of the foregoing. If you have further comments, we ask that you forward them by electronic mail to our counsel, Louis Taubman, Esq. at ltaubman@htflawyers.com or by telephone at (212) 530-2208.

| Very truly yours, | |

| /s/ Xuezhu Wang | |

| Xuezhu Wang | |

| Chief Executive Officer |

| cc: | Joan Wu, Esq. |

| Hunter Taubman Fischer & Li LLC |

13