UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

(Mark One)

þ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended March 31, 2019

or

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from_____________ to____________

Commission File Number: 333-226810

ORGANIC AGRICULTURAL COMPANY LIMITED

(Exact name of registrant as specified in its charter)

| Nevada | 82-5442097 | |

| (State or other jurisdiction of | (I.R.S. Employer | |

| incorporation or organization) | Identification Number) |

6th Floor A, Chuangxin Yilu,

No. 2305, Technology Chuangxincheng,

Gaoxin Jishu Chanye Technology Development District,

Harbin City. Heilongjiang Province.

China 150090

Office: +86 (0451) 5862-8171

(Address, including zip code, and telephone number, including area code,

of Registrant’s principal executive offices)

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class | Trading Symbol | Name of Each Exchange on Which Registered | ||

| None | None | Not Applicable |

Securities registered pursuant to Section 12(g) of the Act: None.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes þ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. þ

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| Non-accelerated filer | ☐ | Smaller reporting company | þ |

| Emerging growth company | þ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12 b-2 of the Act). Yes ☐ No ☑

APPLICABLE ONLY TO REGISTRANTS INVOLVED IN BANKRUPTCY

PROCEEDINGS DURING THE PRECEDING FIVE YEARS:

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Section 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. Yes ☐ No ☐

(APPLICABLE ONLY TO CORPORATE REGISTRANTS)

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date.

As of the date of filing of this report, there were outstanding 11,167,736 shares of the issuer’s common stock, par value $0.001 per share.

DOCUMENTS INCORPORATED BY REFERENCE

List hereunder the following documents if incorporated by reference and the Part of the Form 10-K (e.g., Part I, Part II, etc.) into which the document is incorporated: (1) Any annual report to security holders; (2) Any proxy or information statement; and (3) Any prospectus filed pursuant to Rule 424(b) or (c) under the Securities Act of 1933. The listed documents should be clearly described for identification purposes (e.g., annual report to security holders for fiscal year ended December 24, 1980).

None

TABLE OF CONTENTS

i

Cautionary Statement Regarding Forward Looking Statements

The discussion contained in this Annual Report on Form 10-K contains “forward-looking statements” within the meaning of Section 27A of the United States Securities Act of 1933, as amended, and Section 21E of the United States Securities Exchange Act of 1934, as amended. Any statements about our expectations, beliefs, plans, objectives, assumptions or future events or performance are not historical facts and may be forward-looking. These statements are often, but not always, made through the use of words or phrases like “anticipate,” “estimate,” “plans,” “projects,” “continuing,” “ongoing,” “target,” “expects,” “management believes,” “we believe,” “we intend,” “we may,” “we will,” “we should,” “we seek,” “we plan,” the negative of those terms, and similar words or phrases. We base these forward-looking statements on our expectations, assumptions, estimates and projections about our business and the industry in which we operate as of the date of this Form 10-K. These forward-looking statements are subject to a number of risks and uncertainties that cannot be predicted, quantified or controlled and that could cause actual results to differ materially from those set forth in, contemplated by, or underlying the forward-looking statements. Statements in this Form 10-K describe factors, among others, that could contribute to or cause these differences. Actual results may vary materially from those anticipated, estimated, projected or expected should one or more of these risks or uncertainties materialize, or should underlying assumptions prove incorrect. Because the factors discussed in this Form 10-K could cause actual results or outcomes to differ materially from those expressed in any forward-looking statement made by us or on our behalf, you should not place undue reliance on any such forward-looking statement. New factors emerge from time to time, and it is not possible for us to predict which will arise. In addition, we cannot assess the impact of each factor on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statement. Except as required by law, we undertake no obligation to publicly revise our forward-looking statements to reflect events or circumstances that arise after the date of this Form 10-K.

| Item 1. | Business |

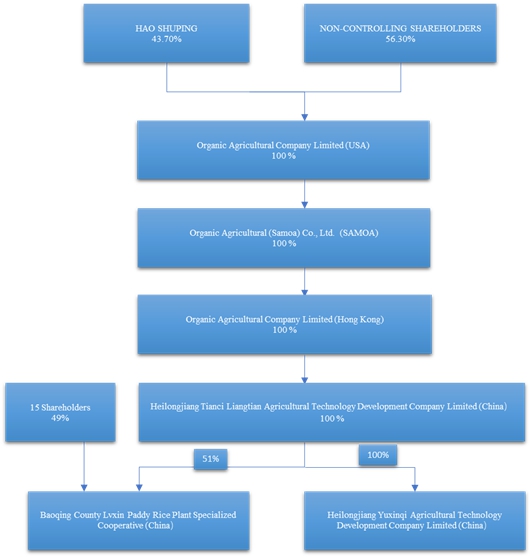

Corporate Structure

Organic Agricultural Company Limited (“Organic Agricultural”, the “Company”, “we” or “us”) was incorporated in the State of Nevada on April 17, 2018. Our website address is www.oacl.top. Our website and the information contained on, or that can be accessed through, the website is not deemed to be incorporated by reference in, and is not considered part of, this Report.

The Company, through its subsidiaries with headquarters in Harbin, China, grows and sells unmilled rice (“paddy”) and selenium-enriched paddy products, rice and other agricultural products. The Company is currently re-orienting its efforts to emphasize the sale of selenium-enriched paddy. We believe that the importance of selenium to human health and the fact of dietary selenium deficiency in large parts of China create a vast market potential for development. The Company’s subsidiaries include:

| ● | Organic Agricultural (Samoa) Co., Ltd. (“Organic Agricultural Samoa”), a wholly owned limited company registered in Samoa on December 15, 2017. Organic Agricultural Samoa owns all of the outstanding shares of capital stock of Organic Agricultural Company Limited (Hong Kong). |

| ● | Organic Agricultural Company Limited (Hong Kong) (“Organic Agricultural HK”), which was established on December 6, 2017 under the laws of Hong Kong. Organic Agricultural HK wholly owns all of the registered equity of Heilongjiang Tianci Liangtian Agricultural Technology Development Company Limited. |

| ● | Heilongjiang Tianci Liangtian Agricultural Technology Development Company Limited. (“Tianci Liangtian”), a wholly owned Limited Company registered in Heilongjiang, China on November 2, 2017. Tianci Liangtian owns: |

| ● | all of the registered equity of Heilongjiang Yuxinqi Agricultural Technology Development Company Limited (“Yuxinqi”), which was incorporated in Heilongjiang, China on February 5, 2018. Tianci Liangtian organized Yuxinqi to function as a marketing company, selling paddy and other crops to customers in PRC. Yuxingi shares offices in Harbin with Tianci Liangtian. Yuxinqi was initially engaged in marketing exclusively for Lvxin, and recorded its first sales in the quarter ended December 31, 2018. As our operations grow, Yuxinqi will undertake a broader range of marketing activities, both for paddy provided by Lvxin and for other food products. |

1

| ● | 51% of the registered equity of Baoqing County Lvxin Paddy Rice Plant Specialized Cooperative (“Lvxin”), a company registered in China on February 9, 2012. Since then, Lvxin has been engaged in the business of growing rice on leased farmland, harvesting and threshing it, then selling the paddy, primarily to the State Administration of Grain, the government entity responsible for ensuring grain supplies in the PRC. Lvxin’s office address is 1-507-1 Chaoyang Village, Chaoyang Town, Baoqing County, Shuangyashan City, Heilongjiang Province. |

Our present corporate structure is as follows:

Our Business

Selenium is one of the “essential” nutrients for humans, meaning that our bodies cannot produce it, and so we have to get it from our diet. Selenium deficiency can cause health problems including Keshan’s disease, a form of cardiomyopathy. The World Health Organization has found that between 50 and 250 micrograms of selenium constitute a healthy daily intake.

2

Scientists now know selenium is necessary in the body’s production of selenoproteins, a family of proteins that contain selenium in the form of an amino acid. So far, 25 different selenoproteins in the body have been isolated, but only half of their functions have been identified. Selenium is one of several nutrients known to have antioxidant properties, meaning selenium plays a part in chemical reactions that stop free radicals from damaging cells and DNA. Human and animal research has found selenoproteins are involved in embryo development, thyroid hormone metabolism, antioxidant defense, sperm production, muscle function and the immune system’s response to vaccinations. Antioxidant supplements, including selenium, are often touted to help prevent heart disease, cancer and vision loss.

According to the Chinese Selenium Supplements Association, selenium is purported to help people with asthma, and reduce the risk of rheumatoid arthritis and cardiovascular disease. Selenium levels drop with age, so some have claimed selenium can slow the aging process, cognitive decline and dementia. Low selenium levels are also implicated in depression, male infertility, weak immune systems and thyroid problems.

Plants grown in soil containing selenium convert it into a form that is usable to humans and animals. Soil around the world varies in its selenium concentration. The higher the concentration of selenium in soil, the higher the concentration of selenium is in crops. Soil in Nebraska, South and North Dakota, for example, is especially rich in selenium, and people living in these areas typically have the highest dietary intake of selenium in the United States. On the other hand, Seventy-two percent (72%) of the land in China is selenium-poor. In the area from the three provinces in Northeast China to the Yunnan Guizhou plateau, two-thirds of the arable land is recognized as having selenium deficiency, where the selenium content of the principal crops is less than 0.05ppm.

Because rice is a staple food in China, selenium-enriched rice obtained by bioenrichment to increase the selenium content of rice was determined to be a good selenium source for the population in selenium-deficient regions. The government of China permits rice to be labeled “selenium-enriched” if the selenium content is at least 0.04 mg/kg. Rice with a selenium concentration in excess of 0.3 mg/kg is considered dangerous and may not be sold. Lvxin’s current inventory of paddy has an average selenium content of 0.18 mg/kg. A half cup of steamed rice (an average serving) made from paddy with a selenium content of 0.18 mg/kg will contain approximately 0.015 mg (i.e. 15 micrograms) selenium.

Our subsidiary, Lvxin, has been involved in growing, threshing and selling unmilled rice since 2012, using leased farmland and the part-time labor of local farmers. Lvxin’s farming operations take place in Baoqing County of Heilongjiang Province in a region known as the Sanjiang Plain. This part of Sanjiang Plain is noteworthy for, among other things, the relatively high content of selenium in its soil. By focusing on production of selenium-enhanced rice, Lvxin hopes to develop a sustainable position in the Chinese rice market.

Our other subsidiary, Yuxinqi, was organized in February 2018, and recorded its first sales during the quarter ended December 31, 2018. Yuxinqi will devote its efforts to marketing and distribution of selenium-enriched agricultural products, initially the selenium-enriched paddy grown by Lvxin, but in time hopes to acquire and distribute a range of selenium-enriched agricultural products.

Seasonality

Our business is seasonal, as our sales are generally during the harvest season, which occurs from October to March of the following year. Our sales are typically very low from April to September, which is the planting and growing period. Accordingly, we experience significant seasonal fluctuations in our revenues and our operating costs.

In addition, adverse weather conditions and other natural disasters may affect our planting and harvesting activities and cause a reduction and loss of agricultural production or a delay in realization of revenues.

3

A major reason for our development of Yuxinqi is to offset the seasonality of our rice business with the year-round marketing efforts of Yuxinqi. We intend that Yuxinqi will market value-added products, both products based on rice and products based on other food stuffs, such as organic red beans and millet.

Operating Licenses

Our products and services are subject to regulation by governmental agencies in the PRC and Heilongjiang Province. Business and company registrations, along with the products, are certified on a regular basis and must be in compliance with the laws and regulations of the PRC and provincial and local governments and industry agencies, which are controlled and monitored through the issuance of licenses. Our licenses include:

| ● | Tianci Liangtian and Yuxinqi operating licenses enable us to undertake agricultural technology development services, primary processing of agricultural products, grain and legume cultivation, and agricultural products sales. (Legally approved projects can be launched after approval by the relevant departments). The registration numbers are 91230100MA1ATNP757 and 91230109MA1AYU4P51, respectively; and they are valid from November 2, 2017 and February 5, 2018, respectively, with no expiration date. |

| ● | Lvxin’s operating license enables us to plant rice, as well as to carry out technical exchanges and information consultation services related to paddy planting. The registration number is 93230523588124513U and it is valid from February 9, 2012 with no expiration date. |

Competition

Currently, the production of selenium-enriched paddy in China is the province of small and medium-sized enterprises, with no dominant participant in the market. The diversity of the market is primarily a function of the relatively brief period that the concept of producing selenium-enriched food stuffs has been popular. As the concept becomes more well-established, the emergence of market leaders will be likely.

We are a small company. However, with our recent focus on production of selenium-enriched paddy, we are entering a growing market. We believe that we will be able to compete effectively in this market because we have the following advantages:

| ● | Geographical advantages |

Lvxin is located in the hinterland of the Sanjiang Plain in Heilongjiang Province. The Sanjiang Plain is one of the world’s most famous areas of fertile soil and one of China’s three largest selenium-enriched belts.

| ● | Product specificity |

Our business activities are focused exclusively on the production of paddy, particularly selenium-enriched paddy. Because selenium-enriched paddy has certain differences with ordinary paddy cultivation, and the technical requirements for effective growing are relatively high, we have invited specialized technical personnel to provide guidance and realize scientific farming.

Suppliers

Over the years of operations, we have developed a solid and reliable image and reputation with the suppliers. We have established supplier relationships with several local companies.

4

Marketing

We believe that the importance of selenium to human health and the fact of selenium deficiency in large parts of China create a vast market potential for development. Selenium has been studied extensively in China. These efforts have resulted in confirming that selenium is an important element for human health and that there are areas within China that are significantly deficient in the soil and water. In the past decade, Chinese government policy has helped to enhance the importance of selenium and the potential of the selenium market.

As the market for the Company’s paddy becomes stable, and as resources become available, the Company intends to expand its product offerings to include value-added products, both products based on rice and products based on other food stuffs, such as organic red beans and millet. In this manner, the Company hopes to alleviate the seasonality of its revenues, by having products available for sale year-round.

Insurance

We do not maintain fire, theft, product liability or other insurance of any kind. We bear the economic risk with respect to loss of or damage or destruction to our property and to the interruption of our business as well as liability to third parties for damage or destruction to them or their property that may be caused by our personnel or products.

Income Taxes

United States

On December 22, 2017, the “Tax Cuts and Jobs Act” (“The Act”) was enacted. Under the provisions of the Act, the U.S. corporate tax rate decreased from 34% to 21%. Accordingly, we have remeasured our deferred tax assets on our net operating loss carryforwards in the U.S at the lower enacted tax rate of 21%. However, this remeasurement had no effect on our income tax expense as we have provided a 100% valuation allowance on our net deferred tax assets.

Samoa

Organic Agricultural (Samoa) Co., Ltd was incorporated in Samoa and, under the current laws of Samoa, is not subject to income tax.

China

Tianci Liantian and Yuxinqi are subject to a 25% standard enterprise income tax in the PRC. There was no provision for income taxes for the years ended March 31, 2019 and 2018 due to operating losses.

Lvxin product sales and services have been exempt from enterprise income tax, according to the “PRC Income Tax Law” Article 27 (1), which states that income from agricultural, forestry, animal husbandries and fisheries industries shall be exempt from business income tax.

Employees

As of March 31, 2019, we had 33 employees. None of our employees are represented by a labor union or similar collective bargaining organization.

During the growing and harvest seasons, Lvxin hires approximately 190 local farmers on a part-time basis to assist in the farming operations.

5

| Item 1A. | Risk Factors. |

An investment in our common stock involves a high degree of risk. You should carefully consider the following risk factors and other information in this 10K before deciding to invest in our Company. If any of the following risks actually occur, our business, financial condition and results of operations could be seriously harmed. As a result, the trading price of our common stock could decline and you could lose all or part of your investment.

Risks Related to Our Business

The ongoing reduction in government price support for the rice market in China may prevent us from achieving sustained profitability.

Until recently, China’s State Administration of Grain guaranteed minimum purchase prices for paddy rice grown by China’s farmers. The minimum price was generally higher than the prices quoted on world markets. As China in the past few years has allowed its Yuan to appreciate against the value of the U.S. dollar, the discrepancy between prices paid to Chinese paddy growers and world markets increased proportionately. As a result, in 2017 the State Administration of Grain reduced the minimum price. This was the principal cause of the reduction in gross revenue realized by Organic Agricultural from fiscal year 2017 to fiscal year 2018. The State Administration implemented further reductions in calendar year 2018. If the State Administration continues to withdraw its support from the market for paddy produced in China, the Company’s prospects for profitability may be adversely affected.

The amount of land available in the Sanjiang Plain for expansion of agricultural wetlands diminishes annually, which increases the cost of our leasing program and may prevent us from expanding our operations.

The Sanjiang Plain is a vast area of alluvial floodplains and low hills in northeast Heilongjiang Province, China. Over the last six decades, paddy fields on the Sanjiang Plain have experienced rapid expansion and aggregation. The Sanjiang Plain’s high-quality soils and favorable climate for grain production attracted major attention from government agricultural development programs beginning in the early 1950s. Since that time, the central government of China strongly encouraged settlement and reclamation of wetlands, and development of large-scale farming in the Sanjiang Plain. Over 5,000,000 hm2, or 47% of the land in the Sanjiang Plain, has been converted to farmland, mostly for corn, soybean, and rice production. Most of this farmland was reclaimed from various types of original wetland by massive drainage projects. While this expansion of the available agricultural acreage has made possible the development of paddy farming in the Sanjiang Plain, the forces behind it put increasing demands on the agricultural wetlands. Farmers with land leases from the government can demand increasing rentals for subleases, and the Company will find itself in competition for the better parcels of paddy lands. This demand for suitable land in the Sanjiang Plain may interfere with the Company’s efforts to expand in a cost-effective manner.

Some residents of China have recently begun to use supplements to offset selenium deficiency in their diets. We cannot predict the extent to which they may come to prefer supplements as a remedy for selenium deficiencies rather than selenium-enhanced food products.

Selenium deficiency has been a problem in eastern China for centuries, and the relationship of selenium deficiencies to Keshan Disease has long been known. Until recently, efforts to alleviate selenium deficiencies have been limited to changes in diet and the introduction of selenium-rich foods, where available. The use of selenium supplements is relatively recent. The use of selenium supplements does offer certain advantages, however, selenium supplements, if purchased from a reliable vendor, provide an assured quantity of selenium, whereas the selenium quantity in a specific item of grocery food is untested. Selenium supplements may be more cost-effective than selenium-enhanced foods, depending on the development of the market for each. For these and other reasons, the growth of the market for selenium supplements may be an obstacle to the growth of the market for selenium-enhanced foods.

Product liability claims could materially impact operating results and profitability.

Excessive ingestion of selenium can have serious harmful effects on an individual. While our technicians will use their best efforts to achieve an optimal selenium content in our products, many factors determine the selenium levels in a crop. Our technicians may be unable to determine when a crop contains an excess amount of selenium. Moreover, even if our technicians are successful in optimizing the selenium value in our crops, consumers who suffer symptoms of selenium poisoning may focus their blame on our products. In either such situation, we may be subject to lawsuits for damages. Such lawsuits could drain our financial resources, particularly as we do not presently carry any product liability insurance or business interruption insurance. Lawsuits by customers may also distract the time and attention of our management. In addition, a product liability claim, regardless of merit or eventual outcome, could result in damage to our reputation, decreased demand for our products, product recalls and loss of revenue.

6

We do not presently maintain fire, theft, product liability or any other property insurance, which leaves us with exposure in the event of loss or damage to our properties or claims filed against us.

We do not maintain fire, theft, product liability or other insurance of any kind. We bear the economic risk with respect to loss of or damage or destruction to our property and to the interruption of our business, as well as, liability to third parties for damage or destruction to them or their property that may be caused by our personnel or products. Such liability could be substantial and the occurrence of such loss or liability may have a material adverse effect on our business, financial condition and prospects.

We may not be able to effectively control and manage our planned growth.

We have limited operational, administrative and financial resources, which may be inadequate to sustain the growth we want to achieve. If our business and markets grow and develop, it will be necessary for us to finance and manage expansion accordingly. In addition, we may face challenges in managing our expanding product and service offerings, and in integrating any businesses we acquire with our own. Such growth would place increased demands on our existing management, employees and facilities. Our failure to meet these demands could interrupt or adversely affect our operations and cause administrative inefficiencies. Additionally, failure to execute our planned growth strategy could have a material adverse effect on our business, financial condition and results of operation.

As a smaller agricultural company with reporting obligations we may be at a competitive disadvantage to other agricultural companies. The agricultural industry has low barriers to entry.

Because the agricultural market is competitive, is driven in part by costs, and consists mostly of private companies that do not have public reporting obligations, our reporting obligations may put us at a competitive disadvantage. The agricultural industry has low barriers to entry. In addition, we will face additional expenses that a private agricultural company does not have, such as PCAOB auditor fees, Edgar filing fees and legal fees related to our SEC reporting obligations. Other non-public agricultural companies do not incur these costs. We are at a competitive disadvantage to our competitors because of this.

Our sales have seasonal variations and adverse weather conditions could cause a reduction and loss of agricultural production.

We will experience seasonal variations in our revenues and our operating costs due to seasonality. Normally, our current product’s selling season is in the first quarter and fourth quarter and from the second quarter through the third quarter is the planting and harvesting period. During the fiscal years ended March 31, 2019 and 2018, approximately 100% of our sales volume came during the first quarter and the fourth quarters. Further, if any natural disasters, such as snowstorms, floods, drought or earthquakes, occur, it could cause a reduction and loss of agricultural production.

7

Risks Relating to our Management

The loss of the services of any of our officers or our failure to timely identify and retain competent personnel could negatively impact our ability to develop our products and sales.

The development of our business will continue to place a significant strain on our limited personnel, management, and other resources. Our future success depends upon the continued services of our executive officers, Shen Zhenai, our President, Chairman of the Board and Director, Xun Jianjun, our Chief Executive Officer and Director, Cao Yongmei, our Chief Financial Officer, as well as the continued involvement of Hao Shuping, our Director who brought together the elements of our business. They are developing our business, which will depend on our ability to identify and retain competent employees with the skills required to execute our business objectives. The loss of the services of any of our officers or our failure to timely identify and retain competent personnel could negatively impact our ability to develop our products and sales, which could adversely affect our financial results and impair our growth.

If we are unable to hire, retain or motivate qualified personnel, consultants, independent contractors, and advisors, we may not be able to grow effectively.

Our performance will be largely dependent on the talents and efforts of highly skilled individuals. Our future success depends on our continuing ability to identify, hire, develop, motivate and retain highly qualified personnel for all areas of our organization. Competition for such qualified employees is intense. If we do not succeed in attracting competent personnel or in retaining or motivating them, we may be unable to grow effectively. In addition, our future success depends largely on our ability to retain key consultants and advisors. We cannot assure that any skilled individuals will agree to become an employee, consultant, or independent contractor of Organic Agricultural Company Limited. Our inability to retain their services could negatively impact our business and our ability to execute our business strategy.

Our internal controls over financial reporting may not be effective and our independent registered public accounting firm may not be able to certify as to their effectiveness, which could have a significant and adverse effect on our business and reputation.

As a newly public reporting company, we will be in a continuing process of developing, establishing, and maintaining internal controls and procedures that will allow our management to report on, and our independent registered public accounting firm to attest to, our internal controls over financial reporting if and when required to do so under Section 404 of the Sarbanes-Oxley Act of 2002. Although our independent registered public accounting firm is not required to attest to the effectiveness of our internal control over financial reporting pursuant to Section 404(b) of the Sarbanes-Oxley Act until the date we are no longer an emerging growth company, our management will be required to report on our internal controls over financial reporting under Section 404. If we fail to achieve and maintain the adequacy of our internal controls, we would not be able to conclude on an ongoing basis that we have effective internal controls over financial reporting in accordance with Section 404. At such time, our independent registered public accounting firm may issue a report that is adverse in the event it is not satisfied with the level at which our controls are documented, designed or operating. Moreover, our testing, or the subsequent testing by our independent registered public accounting firm, that must be performed may reveal other material weaknesses or that the material weaknesses noted have not been fully remediated. If we do not remediate the material weaknesses noted, or if other material weaknesses are identified or we are not able to comply with the requirements of Section 404 in a timely manner, our reported financial results could be materially misstated or could subsequently require restatement, we could receive an adverse opinion regarding our internal controls over financial reporting from our independent registered public accounting firm and we could be subject to investigations or sanctions by regulatory authorities, which would require additional financial and management resources.

Our lack of an independent audit committee and audit committee financial expert at this time may hinder our board of directors’ effectiveness in monitoring the Company’s compliance with its disclosure and accounting obligations. Until we establish such committee, we will be unable to obtain a listing on a national securities exchange.

Although our common stock is not listed on any national securities exchange, for purposes of independence we use the definition of independence applied by NASDAQ. Currently, we have no independent audit committee. Our full board of directors functions as our audit committee and is comprised of three directors. An independent audit committee would play a crucial role in the corporate governance process, assessing our Company’s processes relating to our risks and control environment, overseeing financial reporting, and evaluating internal and independent audit processes. The lack of an independent audit committee may deprive the Company of management’s independent judgment. We may, however, have difficulty attracting and retaining independent directors with the requisite qualifications. If we are unable to attract and retain qualified, independent directors, the management of our business could be compromised. An independent audit committee is required for listing on any national securities exchange. Therefore, until such time as we meet the audit committee independence requirements of a national securities exchange, we will be ineligible for listing on any national securities exchange.

8

Our board of directors acts as our compensation committee, which presents the risk that compensation and benefits paid to those executive officers who are board members and other officers may not be commensurate with our financial performance.

A compensation committee consisting of independent directors is a safeguard against self-dealing by company executives. Our board of directors, which has no independent members, acts as the compensation committee for the Company and determines the compensation and benefits of our executive officers, administers our employee stock and benefit plans, and reviews policies relating to the compensation and benefits of our employees. Our lack of an independent compensation committee presents the risk that an executive officer on the board may have influence over his or her personal compensation and benefits levels that may not be commensurate with our financial performance or the market place.

Limitations on director and officer liability and indemnification of our Company’s officers and directors by us may discourage stockholders from bringing a lawsuit against an officer or director.

Our Company’s certificate of incorporation and bylaws provide, with certain exceptions as required by governing state law, that a director or officer shall not be personally liable to us or our stockholders for breach of fiduciary duty as a director or officer, except for acts or omissions which involve intentional misconduct, fraud or knowing violation of law, or unlawful payments of dividends. These provisions may discourage stockholders from bringing a lawsuit against a director or officer for breach of fiduciary duty and may reduce the likelihood of derivative litigation by stockholders on the Company’s behalf against a director or officer.

Our management has limited experience managing a public company.

At the present time, none of our management has experience in managing a public company. This may hinder our ability to establish effective controls and systems and comply with all applicable requirements associated with being a public company. If compliance problems result, these problems could have a material adverse effect on our business, financial condition or results of operations. As a public company, we will incur significant legal, accounting and other expenses that we did not incur as a private company. In addition, the Sarbanes-Oxley Act of 2002, or Sarbanes-Oxley Act, and the Dodd-Frank Act of 2010, as well as rules subsequently implemented by the SEC, have imposed various new requirements on public companies, including requiring changes in corporate governance practices. Our management and other personnel will need to devote a substantial amount of time to our new compliance requirements. Moreover, these requirements will increase our legal, accounting and financial compliance costs and will make some activities more time-consuming and costly. For example, we expect it will be difficult and expensive for us to obtain director and officer liability insurance. These requirements could also make it more difficult for us to attract and retain independent and qualified persons to serve on our board of directors, our board committees or as executive officers.

We may have difficulty establishing adequate management, legal and financial controls in the PRC.

The PRC historically has not adopted a western style of management and financial reporting concepts and practices, as in modern banking, computer and other control systems. We may have difficulty in hiring and retaining a sufficient number of qualified employees to work in the PRC. As a result of these factors, we may experience difficulty in establishing management, legal and financial controls, collecting financial data and preparing financial statements, books of account and corporate records and instituting business practices that meet western standards. Therefore, we may, in turn, experience difficulties and additional costs in implementing and maintaining adequate internal controls as will be required under Section 404 of the Sarbanes Oxley Act of 2002.

Risks Related to Regulation

Our success depends upon the development of the PRC’s agricultural industry.

The PRC is currently the world’s most populous country and one of the largest producers and consumers of agricultural products. Despite the Chinese government’s emphasis on agricultural self-sufficiency, inadequate port facilities and lack of warehousing and cold storage facilities may impede the growth of the domestic agricultural trade. At the present stage, we rely on local buyers and the State Grain Reserve of China in the PRC to purchase our products. If the PRC does not develop adequate infrastructure for the distribution of agricultural products, our ability to expand our markets will be limited.

9

Changes in the policies of the PRC government could have an adverse effect on our business.

Policies of the PRC government can have significant effects on the economic conditions in the PRC. Although the PRC government has been pursuing economic reform policies and transitioning to a market-oriented economy, there is no assurance that the government will continue to pursue such policies or that such policies may not be significantly altered, especially in the event of a change in leadership, social or political disruption, or other circumstances affecting the PRC’s political, economic and social conditions. Our business could be adversely affected by changes in PRC government policies, including but not limited to changes in policies relating to taxation, currency conversion, imports and exports, and ownership of private enterprises.

PRC laws and regulations governing our current business operations are sometimes vague and subject to interpretation, and any changes in PRC laws and regulations may have a material and adverse effect on our business.

There are substantial uncertainties regarding the interpretation, application and enforcement of PRC laws and regulations, including but not limited to the laws and regulations governing our business. These laws and regulations are sometimes vague and are subject to future changes, and their official interpretation and enforcement by the various branches of the PRC government may involve substantial uncertainty. The PRC legal system is based in part on governmental policies and internal rules some of which are not published on a timely basis or at all. New laws, regulations, rules and policies that affect existing and proposed future businesses may also be applied retroactively. We cannot predict with certainty what effect existing or new PRC laws or regulations may have on our business. In addition, there is less published guidance regarding PRC laws as compared to laws in the United States, and prior rulings and interpretations of PRC laws may not necessarily carry the same precedential value as in the United States.

Governmental control of currency conversion may affect the value of your investment.

The People’s Republic of China (PRC) government imposes controls on the convertibility of Renminbi (RMB) into foreign currencies and, in certain cases, the remittance of currency out of the PRC. We receive substantially all of our revenues in RMB, which is currently not a freely convertible currency. Shortages in the availability of foreign currency may restrict our ability to remit sufficient foreign currency to pay dividends, or otherwise satisfy foreign currency dominated obligations. Under existing PRC foreign exchange regulations, payments of current account items, including profit distributions, interest payments and expenditures from the transaction, can be made in foreign currencies without prior approval from the PRC State Administration of Foreign Exchange by complying with certain procedural requirements. However, approval from appropriate governmental authorities is required where RMB is to be converted into foreign currency and remitted out of the PRC to pay capital expenses such as the repayment of bank loans denominated in foreign currencies.

The PRC government also may at its discretion restrict access in the future to foreign currencies for current account transactions. If the foreign exchange control system prevents us from obtaining sufficient foreign currency to satisfy our currency demands, we may not be able to pay certain of our expenses as they come due.

The fluctuation of RMB may materially and adversely affect your investment.

The value of the RMB against the U.S. dollar and other currencies may fluctuate and is affected by, among other things, changes in the PRC’s political and economic conditions. As we rely entirely on revenues earned in the PRC, any significant revaluation of RMB may materially and adversely affect our cash flows, revenues and financial condition. For example, to the extent that we need to convert U.S. dollars we receive from an offering of our securities into RMB for our operations, appreciation of the RMB against the U.S. dollar could have a material adverse effect on our business, financial condition and results of operations. Conversely, if we decide to convert our RMB into U.S. dollars for the purpose of making dividend payments on our common stock or for other business purposes and the U.S. dollar appreciates against the RMB, the U.S. dollar equivalent of the RMB we convert would be reduced. In addition, the depreciation of significant U.S. dollar denominated assets could result in a charge to our income statement and a reduction in the value of these assets.

Because our principal assets are located outside of the United States and because all of our directors and all our officers reside outside of the United States, it may be difficult for you to use the United States Federal securities laws to enforce your rights against us and our officers or to enforce judgments of United States courts against us or them in the PRC.

All of our present officers and directors reside outside of the United States. In addition, our operating subsidiaries, Tianci Liangtian, Yuxinqi and Lvxin, are located in the PRC and substantially all of their assets are located outside of the United States. It may therefore be difficult for investors in the United States to enforce their legal rights based on the civil liability provisions of the United States Federal securities laws against us in the courts of either the United States or the PRC and, even if civil judgments are obtained in courts of the United States, to enforce such judgments in PRC courts. Further, it is unclear if extradition treaties now in effect between the United States and the PRC would permit effective enforcement against us or our officers and directors of criminal penalties, under the United States Federal securities laws or otherwise.

10

Risks Relating to Our Common Stock

We are an emerging growth company and, as a result of the reduced disclosure and governance requirements applicable to emerging growth companies, our common stock may be less attractive to investors.

We are an emerging growth company, as defined in the JOBS Act, and we are eligible to take advantage of certain exemptions from various reporting requirements applicable to other public companies. The exemptions available to emerging growth companies include the right to present only two years of audited financial statements in our registration statements and annual reports, an exemption from the auditor attestation requirement of Section 404(b) of the Sarbanes-Oxley Act relating to internal controls, reduced disclosure about executive compensation arrangements, and no requirement to seek non-binding advisory votes on executive compensation or golden parachute arrangements. Some of these exemptions are also available to us as a smaller reporting company (i.e. a company with less than $250 million of its voting equity held by non-affiliates). We have elected to adopt these reduced disclosure requirements. We cannot predict if investors will find our common stock less attractive as a result of our taking advantage of these exemptions. If some investors find our common stock less attractive as a result of our choices, there may be a less active trading market for our common stock and our stock price may be more volatile.

Pursuant to Section 107(b) of the JOBS Act, we have elected to use the extended transition period for complying with new or revised accounting standards under Section 102(b)(2) of The JOBS Act. This election allows us to delay the adoption of new or revised accounting standards that have different effective dates for public and private companies until those standards apply to private companies. As a result, our financial statements may not be comparable to companies that comply with public company effective dates. The decision to opt out is irrevocable.

Because the worldwide market value of our common stock held by non-affiliates, or public float, was below $250 million on the last day of our second fiscal quarter, we are also a “smaller reporting company” as defined under the Exchange Act. Some of the foregoing reduced disclosure and other requirements are also available to us because we are a smaller reporting company and may continue to be available to us even after we are no longer an emerging growth company under the JOBS Act but remain a smaller reporting company under the Exchange Act. As a smaller reporting company, we are not required to:

| ● | have an auditor report on our internal control over financial reporting pursuant to Section 404(b) of the Sarbanes-Oxley Act; |

| ● | present more than two years of audited financial statements in our registration statements and annual reports on Form 10-K; or |

| ● | present any selected financial data in such registration statements and annual reports filings made by the Company. |

Because we will be subject to “penny stock” rules, the level of trading activity in our stock may be reduced.

If we are able to secure a listing for our common stock, it is likely that our common stock will be classified as a “penny stock’ when trading is initiated and for an indeterminate period thereafter. Penny stocks generally are equity securities with a price of less than $5.00 (other than securities registered on some national securities exchanges). Broker-dealer practices in connection with transactions in “penny stocks” are regulated by penny stock rules adopted by the Securities and Exchange Commission. The penny stock rules require a broker-dealer, prior to a transaction in a penny stock not otherwise exempt from the rules, to deliver a standardized risk disclosure document that provides information about penny stocks and the nature and level of risks in the penny stock market. The broker-dealer also must provide the customer with current bid and offer quotations for the penny stock, the compensation of the broker-dealer and its salesperson in the transaction, and, if the broker-dealer is the sole market maker, the broker-dealer must disclose this fact and the broker-dealer’s presumed control over the market, and monthly account statements showing the market value of each penny stock held in the customer’s account. In addition, broker-dealers who sell these securities to persons other than established customers and “accredited investors” must make a special written determination that the penny stock is a suitable investment for the purchaser and receive the purchaser’s written agreement to the transaction. Consequently, these requirements may have the effect of reducing the level of trading activity, if any, in the secondary market for a security subject to the penny stock rules. If a trading market does develop for our common stock, these regulations will likely be applicable, and investors in our common stock may find it difficult to sell their shares.

11

FINRA sales practice requirements may limit a stockholder’s ability to buy and sell our stock.

FINRA has adopted rules that require that in recommending an investment to a customer, a broker-dealer must have reasonable grounds for believing that the investment is suitable for that customer. Prior to recommending speculative low-priced securities to their non-institutional customers, broker-dealers must make reasonable efforts to obtain information about the customer’s financial status, tax status, investment objectives and other information. Under interpretations of these rules, FINRA believes that there is a high probability that speculative low-priced securities will not be suitable for at least some customers. FINRA requirements make it more difficult for broker-dealers to recommend that their customers buy our common stock, which may have the effect of reducing the level of trading activity in our common stock. As a result, fewer broker-dealers may be willing to make a market in our common stock, reducing a stockholder’s ability to resell shares of our common stock.

Shareholders do not have pre-emptive rights, which will cause them to experience dilution if we issue additional securities.

At any time or times after this offering, we may issue and sell additional shares of our authorized but previously unissued shares of common stock, preferred stock, or common stock warrants on such terms and conditions as our Board of Directors, in its sole discretion, may determine without consent of our shareholders. Our shareholders do not have pre-emptive rights to acquire additional shares should we in the future issue or sell additional securities. Thus, we are not required to offer any existing shareholder the right to purchase his or her pro rata portion of any future issuance of securities and, therefore, upon the issuance of any additional securities by us hereafter, our shareholders will not be able to maintain their then existing pro rata ownership in our outstanding shares of common stock, preferred stock, or common stock warrants without additional purchases of securities at the price then set internally by us or the market.

We are unlikely to pay cash dividends in the foreseeable future.

We currently intend to retain any future earnings for use in the operation and expansion of our business. We do not expect to pay any cash dividends in the foreseeable future but will review this policy as circumstances dictate. Should we decide in the future to do so, as a holding company, our ability to pay dividends and meet other obligations depends upon the receipt of dividends or other payments from our operating subsidiaries. Our operating subsidiaries, from time to time, may be subject to restrictions on their ability to make distributions to us, including as a result of restrictions on the conversion of local currency into U.S. dollars or other hard currency and other regulatory restrictions. The PRC government imposes controls on the convertibility of the RMB into foreign currencies and, in certain cases, the remittance of currency out of China. We and our shareholders also face uncertainties with respect to indirect transfers of equity interests in PRC resident enterprises by their non-PRC holding companies. Pursuant to a notice, or Circular 698, issued by the State Administration of Taxation, where a non-resident enterprise conducts an “indirect transfer” by transferring the equity interests of a PRC resident enterprise indirectly via disposing of the equity interests of an overseas holding company, and such overseas holding company is located in a tax jurisdiction that: (1) has an effective tax rate less than 12.5%; or (2) does not tax foreign income of its residents, the non-resident enterprise, being the transferor, shall report to the relevant tax authority of the PRC resident enterprise such indirect transfer. Using a “substance over form” principle, the PRC tax authority may disregard the existence of the overseas holding company if it lacks a reasonable commercial purpose and was established for the purpose of reducing, avoiding or deferring PRC tax. As a result, gains derived from such indirect transfer may be subject to PRC enterprise income tax, currently at a rate of 10%.

12

Our insiders own the majority of the outstanding shares of our stock, and accordingly, will have control over stockholder matters, the Company’s business and management.

As of the date of this report, the four members of our Board of Directors own, in the aggregate, common stock representing 53.6% of the outstanding shares of our common stock. While they continue to hold the majority of the voting power in our Company, these four directors will have effective control over the Company, in particular, the four directors will have the ability to:

| ● | Elect or defeat the election of our directors; |

| ● | Amend or prevent amendment of our articles of incorporation or bylaws; |

| ● | Effect or prevent a merger, sale of assets or other corporate transaction; and |

| ● | Affect the outcome of any other matter submitted to the stockholders for vote. |

Moreover, because of the significant ownership position held by our insiders, new investors will not be able to affect a change in the Company’s business or management, and therefore, shareholders would be subject to decisions made by management and the majority shareholders.

In addition, sales of significant amounts of shares held by our directors and executive officers, or the prospect of these sales, could adversely affect the market price of our common stock. Management’s stock ownership may discourage a potential acquirer from making a tender offer or otherwise attempting to obtain control of us, which in turn could reduce our stock price or prevent our stockholders from realizing a premium over our stock price.

| Item 1B. | Unresolved Staff Comments |

Not applicable.

| Item 2. | Properties. |

The Company does not own any real property. We believe the premises we now have under lease will be adequate for our operations for the foreseeable future.

Office Leases

In November 2017, Tianci Liangtian leased an office space of approximately 7,169 sqft under operating lease agreements. Tianci Liangtian paid approximately $1,592 in lease deposits and was committed to make annual lease payments of USD$43,761. The office address is the full 6th Floor A, Chuangxin Yilu, No. 2305, Technology Chuangxincheng, Gaoxin Jishu Chanye Technology Development District, Harbin City. Heilongjiang Province. China 150090. The office contains our administrative functions, sales, e-commerce operations and marketing functions. In December 2018, Yuxingqi renewed the lease agreement. Under the terms, Yuxingqi committed to make annual lease payments of CNY¥ 290,000 (approximately US$42,000) for the period from December 6, 2018 to December 5, 2019.

Effective on May 1, 2018, Lvxin leased office space of approximately 1,904 sqft for a one year period ending on April 30, 2019, with an option to extend the lease. The office lease agreement requires Lvxin to pay approximately USD$4,532 (RMB30,000) for the year’s rent, with the rent for any extended period to be based on market conditions.. The office address is the Fuyuanguandi, Pingshun Street, Baoqing County, Shuangyasha City, Heilongjiang Province. China 155600. The office contains our administrative functions, sales, e-commerce operations and marketing functions.

13

Farmland Leases

Lvxin is party to approximately 300 leases for farmland in Baoqing County, Heilongjiang Province. The area currently leased totals 1,228 acres, most of which are located in the Sanjiang Plain. We estimate that approximately four million kilograms of paddy can be grown on 1,228 acres.

Each of the 300 farmland leases was drawn on the same form. The lease permits Lvxin to conduct production operations on an identified parcel of farmland for a stated period of years, up to 22 years in some leases. There are no specific provisions for termination of the leases other than upon expiration of the stated term; accordingly, a party may terminate a lease during its term only pursuant to such provisions of law as permit termination in the event of a material irremediable breach. The leases provide for a fixed rental amount, which is paid either annually on January 1 or, in some cases, prepaid for periods from 12 to 22 years. The leases assign to Lvxin the right to receive any special subsidy that the PRC may issue from time to time. The parties agree to negotiate, should any issues arise with respect to the leasehold.

| Item 3. | Legal Proceedings. |

We are currently not involved in any litigation that we believe could have a material adverse effect on our financial condition or results of operations. There is no action, suit, proceeding, inquiry or investigation before or by any court, public board, government agency, self-regulatory organization or body pending or, to the knowledge of the executive officers of our company or any of our subsidiaries, threatened against or affecting our company, our common stock, any of our subsidiaries or of our companies or our subsidiaries’ officers or directors in their capacities as such, in which an adverse decision could have a material adverse effect.

| Item 4. | Mine Safety Disclosure |

Not applicable.

14

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities. |

Market Information

Our shares of common stock are not currently listed for trading on any exchange or quotation system and there is no active trading market for our shares of common stock.

Holders of Securities

As of the date of filing of this report,, we had 113 shareholders of record and 11,167,736 outstanding shares of common stock, par value $0.001.

There are currently effective prospectuses that will permit the public resale of 5,182,736 shares of our common stock now held by shareholders.

Dividends

We have not declared or paid any cash dividends on our common stock since our inception, and our board of directors currently intends to retain all earnings for use in the business for the foreseeable future. Any future payment of dividends will depend upon our results of operations, financial condition, cash requirements and other factors deemed relevant by our board of directors. There are currently no restrictions that limit our ability to declare cash dividends on our common stock. The PRC government imposes controls on the convertibility of the RMB into foreign currencies and, in certain cases, the remittance of currency out of China. We and our shareholders also face uncertainties with respect to indirect transfers of equity interests in PRC resident enterprises by their non-PRC holding companies. Pursuant to a notice, or Circular 698, issued by the State Administration of Taxation, where a non-resident enterprise conducts an “indirect transfer” by transferring the equity interests of a PRC resident enterprise indirectly via disposing of the equity interests of an overseas holding company, and such overseas holding company is located in a tax jurisdiction that: (1) has an effective tax rate less than 12.5%; or (2) does not tax foreign income of its residents, the non-resident enterprise, being the transferor, shall report to the relevant tax authority of the PRC resident enterprise such indirect transfer. Using a “substance over form” principle, the PRC tax authority may disregard the existence of the overseas holding company if it lacks a reasonable commercial purpose and was established for the purpose of reducing, avoiding or deferring PRC tax. As a result, gains derived from such indirect transfer may be subject to PRC enterprise income tax, currently at a rate of 10%.

Securities Authorized for Issuance Under Equity Compensation Plans

We have no equity compensation plans.

15

Sales of Unregistered Securities

The Company did not have any unregistered sales of equity securities during the fiscal quarter ended March 31, 2019.

Repurchase of Equity Securities

The Company did not repurchase any of its equity securities that were registered under Section 12 of the Securities Act during the fiscal year ended March 31, 2019.

| Item 6. | Selected Financial Data. |

Smaller reporting companies are not required to provide information under this item.

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

The following discussion and analysis of our financial condition and results of operations are based upon our consolidated financial statements and the notes thereto included elsewhere in this Annual Report on Form 10-K, which have been prepared in accordance with accounting principles generally accepted in the United States. The preparation of such financial statements requires us to make estimates and judgments that affect the reported amounts of assets, liabilities, revenues, and expenses. On an ongoing basis, we evaluate these estimates, including those related to useful lives of real estate assets, bad debts, impairment, contingencies and litigation. We base our estimates on historical experience and on various other assumptions that are believed to be reasonable under the circumstances, the results of which form the basis for making judgments about the carrying values of assets and liabilities that are not readily apparent from other sources. There can be no assurance that actual results will not differ from those estimates. The analysis set forth below is provided pursuant to applicable SEC regulations and is not intended to serve as a basis for projections of future events. See “Cautionary Statement Regarding Forward Looking Statements” above.

Application of Critical Accounting Policies

In preparing our financial statements, we are required to formulate working policies regarding valuation of our assets and liabilities and to develop estimates of those values. In our preparation of the financial statements for the year ended March 31, 2019, there was one estimate made which was (a) subject to a high degree of uncertainty and (b) material to our results:

| ● | The determination, described in Note 4 to our Consolidated Financial Statements, to record our inventories as of March 31, 2019 at their fair market value, i.e. $516,404. The cost of our inventories primarily consists of the growing costs of crops, both in the field and harvested, as well as the cost of harvesting crops that remain unsold. U.S. GAAP mandates that we record the value of our inventory at the lower of cost or net realizable value. Our determination to record the inventories at fair market value was based on our determination that the paddy in inventory, including paddy in the field, was sold for an amount below its cost in May 2019. |

16

Results of Operations for the Years Ended March 31, 2019 and 2018

The following table shows key components of the results of operations during the years ended March 31, 2019 and 2018:

| For the Years Ended March 31, | Change | |||||||||||||||

| 2019 | 2018 | $ | % | |||||||||||||

| Revenue | $ | 1,123,313 | $ | 378,899 | $ | 744,414 | 196 | % | ||||||||

| Cost of Sales | 911,092 | 225,143 | 685,949 | 305 | % | |||||||||||

| Gross Profit | 212,221 | 153,756 | 58,465 | 38 | % | |||||||||||

| Total operating costs and expenses | 1,040,221 | 138,574 | 901,647 | 651 | % | |||||||||||

| (Loss) earnings from operations before other income and income taxes | (828,000 | ) | 15,182 | (843,182 | ) | (5554 | %) | |||||||||

| Other income | 3,442 | 133 | 3,309 | 2488 | % | |||||||||||

| (Loss) income from operations before income taxes | (824,558 | ) | 15,315 | (839,873 | ) | (5484 | %) | |||||||||

| Income taxes | - | - | - | - | ||||||||||||

| Net (loss) income | (824,558 | ) | 15,315 | (839,873 | ) | (5484 | %) | |||||||||

| Less: net income attributable to non-controlling interests | 79,337 | 61,997 | 17,340 | 28 | % | |||||||||||

| Net (loss) attributable to common shareholders’ | $ | (903,895 | ) | $ | (46,682 | ) | $ | (857,213 | ) | 1836 | % | |||||

During the year ended March 31, 2019, the Company’s subsidiary, Yuxinqi, recorded its first sales of milled rice and other production. As our focus was on the rollout of that marketing operation, our revenue and cost of sales was significantly changed from prior periods:

| The Year Ended March 31, | ||||||||||||||||

| 2019 | 2018 | |||||||||||||||

| Sales | % | Sales | % | |||||||||||||

| Milled Rice and other production | $ | 245,045 | 22 | % | $ | -- | -- | |||||||||

| Paddy | 878,268 | 78 | % | 378,899 | 100 | % | ||||||||||

| $ | 1,123,313 | 100 | % | $ | 378,899 | 100 | % | |||||||||

As our results during the year ended March 31, 2018 indicate, where almost all sales for the fiscal year were recorded in the third and fourth quarters, the sale of paddy is extremely seasonal. This occurs because of the seasonal nature of paddy production, for which the period from April through September is the planting and growing season. Our development of Yuxinqi as a marketing enterprise with focus beyond paddy is largely caused by our desire to generate revenue year-round.

The costs incurred in planting and growing paddy are capitalized as additions to inventory until the harvest season, when the capitalized costs are amortized against sales. Costs of sales of $759,626 were attributable to paddy sales during the year ended March 31, 2019, resulting in gross profit of $118,642 and a gross margin of 13.5% from the sale of paddy. Costs of sales of $225,143 were attributable to paddy sales during the year ended March 31, 2018, resulting in gross profit of $153,756 and a gross margin of 40.6%. The lower market price of the paddy, and the 27.2% increase in average unit cost, caused by reduced production, are the major factors in the reduction of paddy sales gross margin compared with last year. The remainder of our cost of sales, $151,466, was attributable to the sales of milled rice and other foodstuffs, resulting in gross profit of $93,579 and a gross margin of 38.2%. The higher margin on our non-paddy lines makes our expansion in this market attractive. However, we also expect that increased advertising of the health benefits of consuming selenium-enriched rice will increase demand for our paddy products and enable greater margins. We intend to devote resources to that advertising effort as they become available.

17

During the years ended March 31, 2019 and 2018, the Company incurred $1,040,221 and $138,574, respectively, in operating expenses, the greater portion of which was attributable to the costs of our operations - i.e. salaries and office expenses. Salaries and benefits expense was increased by an estimated of $578,000 during the year ended March 31, 2019 due to increase in operation including that in June 2018 the Company granted a total of 290,000 shares to 8 employees, which resulted in $377,000 of stock compensation expense, representing the fair value of those shares on the date issued.

In addition, during the year ended March 31, 2019, we incurred advertising and promotion expenses of approximately $67,000 and an increase in traveling and related expenses of $182,000, for the purpose of promoting the Company’s expansion. We also incurred $140,056 of expenses relating to our efforts to become a reporting company in the United States, including legal and accounting fees, fees for a transfer agent and the like.

The Company’s operations produced a net loss of $824,558 and net income of $15,315 for the year ended March 31, 2019 and 2018, respectively. However, because we own only 51% of the equity in Lvxin, U.S. GAAP directs us to record all of the revenue and expenses attributable to the operations of Lvxin, but to then offset the portion of net income or net loss attributable to the noncontrolling interest. Therefore, we eliminated $79,337 and $61,997 of the net income attributable to Lvxin’ minority shareholders during the years ended March 31, 2019 and 2018. As a result, the net loss attributable to the Company’s common shareholders was $903,895 and $46,682 for the year ended March 31, 2019 and 2018, respectively.

Liquidity and Capital Resources

The Company’s operations have been financed primarily by loans from related parties. The shareholders of Lvxin financed the operations of that entity, and their loans have been repaid. Recently, Hao Shuping has been the primary source of financing for Tianci Liangtian and Yuxinqi. As a result, at March 31, 2019, the Company’s loans payable to related parties totaled $92,307 (a decrease of $479,343 from March 31, 2018), which was owed to members of the Company’s management. Working capital totaled $288,163. Working capital decreased by $51,803 during the year ended March 31, 2019, as the net loss incurred during that year eliminated most of our cash balance. The reduction in working capital was significantly less than the net loss, however, because we reclassified from other payable to equity $425,749 that had been advanced for the purchase of shares during the prior fiscal year. That balance was reclassified to shareholders’ equity when Organic Agricultural Company Limited was organized in April 2018 and the shares were issued.

The largest component of working capital is inventory, which is measured by the expenses incurred for rice in the field and in the warehouse. It is noteworthy that Lvxin and Yuxingqi had no accounts receivable at either March 31, 2019 or March 31, 2018. This occurs because the payment terms given by Lvxin and Yuxingqi to its customers are very constricted: most sales are made with COD (cash on delivery) or prepayment terms, with no customer having more than three days to complete payment.

Cash Flows

The following table summarizes our cash flows for the years ended March 31, 2019 and 2018.

For the Years Ended March 31, | Change | |||||||||||

| 2019 | 2018 | $ | ||||||||||

| Net cash (used in) provided by operating activities | $ | (472,702 | ) | $ | 172,225 | $ | (644,926 | ) | ||||

| Net cash (used in) investing activities | (238,672 | ) | - | (238,672 | ) | |||||||

| Net cash provided by financing activities | 313,773 | 262,463 | 51,310 | |||||||||

| Effect of exchange rate fluctuation on cash and cash equivalents | (48,136 | ) | 23,964 | (72,101 | ) | |||||||

| Net increase(decrease) in cash and cash equivalents | (445,737 | ) | 458,652 | (904,389 | ) | |||||||

| Cash and cash equivalents, beginning of year | 458,690 | 38 | 458,652 | |||||||||

| Cash and cash equivalents, end of year | $ | 12,953 | $ | 458,690 | $ | 445,737 | ||||||

18

During the year ended March 31, 2019, our operations used net cash of $472,702. The use of cash in operations was less than the net loss for the year primarily because the net loss included a non-cash expense of $377,000 attributable to the market value of shares issued to employees in June 2018. In addition, we preserved cash by utilizing $222,700 of inventories and adding $134,561 provided by receiving customer deposits.

The Company recorded $172,225 of cash provided by operating activities during the year ended March 31, 2018, as most cash generated by operations during that year was $178,313 of cash received from individuals who were shareholders of Lvxin at that time.

Our investing activities during the year ended March 31, 2019 used $238,672. Investing activities consisted of:

| ● | $ 10,754 used in purchases of fixed assets; |

| ● | $ 227,918 used to pay the purchase price for 51% of Lvxin. |

Our financing activities during the year ended March 31, 2019 generated $313,773. Financing activities consisted of $405,939 in proceeds from sales of common stock, offset by $104,483 used to repay loans from related parties.

Trends, Events and Uncertainties

Our business is seasonal, as our sales occur generally during the harvest season, which occurs from October to March of the following year. Our sales are typically the lowest from April to September, which is the planting and growing and harvesting period. Accordingly, we experience significant seasonal fluctuations in our revenues and our operating costs.

In addition, adverse weather conditions and other natural disasters may affect our planting and harvesting activities and cause a reduction and loss of agricultural production or a delay in realization of revenues.

As resources become available, the Company intends to expand its product offerings to include value-added products, both products based on rice and products based on other food stuffs, such as organic red beans and millet. In this manner, the Company hopes to alleviate the seasonality of its revenues, by having products available for sale year-round.

Other than the factors listed above we do not know of any trends, events or uncertainties that have had or are reasonably expected to have a material impact on our net sales or revenues or income from continuing operations.

Off-Balance Sheet Arrangements

We do not currently have any off-balance sheet arrangements that have or are reasonably likely to have a current or future effect on our financial condition or results of operations.

Recent Accounting Pronouncements

New accounting rules and disclosure requirements can significantly impact the comparability of our financial statements. Please refer to Note 2 of our consolidated financial statements included in this annual report for a discussion of the effect on our balance sheet that we anticipate occurring as we adopt in the current fiscal year the treatment of leases mandated by FASB in ASU 2018-11.

There were no other recent accounting pronouncements that we expect to have a material effect on the Company’s financial position or results of operations.

| Item 7A. | Quantitative and Qualitative Disclosures about Market Risk. |

Not applicable.

19

| Item 8. | Financial Statements and Supplementary Data. |

INDEX TO CONSOLIDATED FINANCIAL STATEMENTS

ORGANIC AGRICULTURAL COMPANY LIMITED AND SUBSIDIDARIES

F-1

To the Board of Directors and

Stockholders of Organic Agricultural Company Limited

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

Opinion on the Consolidated Financial Statements

We have audited, before the effects of the adjustments for the correction of the error described in Note 2, the balance sheet of Organic Agricultural Company Limited (the “Company”) as of March 31, 2018, and the related statement of operations and comprehensive income, changes in stockholders’ equity, and cash flows for the year then ended, and the related notes (collectively referred to as the financial statements). In our opinion, except for the error described in Note 2, the 2018 financial statements present fairly, in all material respects, the financial position of the Company as of March 31, 2018, and the results of its operations and its cash flows for the year then ended in conformity with accounting principles generally accepted in the United States of America.

We were not engaged to audit, review, or apply any procedures to the adjustments for the correction of the error described in Note 2 and, accordingly, we do not express an opinion or any other form of assurance about whether such adjustments are appropriate and have been properly applied. Those adjustments were audited by Wei, Wei & Co., LLP. (The 2018 financial statements before the effects of the adjustments discussed in Note 2 have been withdrawn and are not presented herein.)

Basis for Opinion